UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2013

Commission File Number 1-13783

Integrated Electrical Services, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 76-0542208 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

5433 Westheimer Road, Suite 500, Houston, Texas, 77056

(Address of principal executive offices and ZIP code)

Registrant's telephone number, including area code: (713) 860-1500

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

| Common Stock, par value $0.01 per share | NASDAQ |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting stock of the Registrant on March 29, 2013 held by non-affiliates was approximately $31.9 million. On December 16, 2013, there were 17,841,640 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information contained in the Proxy Statement for the 2014 Annual Meeting of Stockholders of the Registrant to be held on February 4, 2014 is incorporated by reference into Part III of this Form 10-K.

FORM 10-K

INTEGRATED ELECTRICAL SERVICES, INC.

Table of Contents

| Page | ||||||

| PART I | ||||||

DEFINITIONS | 1 | |||||

DISCLOSURE REGARDING FORWARD LOOKING STATEMENTS | 1 | |||||

Item 1 | BUSINESS | 3 | ||||

Item 1A | RISK FACTORS | 11 | ||||

Item 1B | UNRESOLVED STAFF COMMENTS | 15 | ||||

Item 2 | PROPERTIES | 15 | ||||

Item 3 | LEGAL PROCEEDINGS | 15 | ||||

Item 4 | MINE SAFETY DISCLOSURES | 16 | ||||

| PART II | ||||||

Item 5 | MARKET FOR REGISTRANT'S COMMON EQUITY; RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 16 | ||||

Item 6 | SELECTED FINANCIAL DATA | 18 | ||||

Item 7 | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 19 | ||||

Item 7A | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 34 | ||||

Item 8 | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 35 | ||||

Item 9 | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 75 | ||||

Item 9A | CONTROLS AND PROCEDURES | 75 | ||||

Item 9B | OTHER INFORMATION | 75 | ||||

PART III | ||||||

Item 10 | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 76 | ||||

Item 11 | EXECUTIVE COMPENSATION | 76 | ||||

Item 12 | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 76 | ||||

Item 13 | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE | 77 | ||||

Item 14 | PRINCIPAL ACCOUNTANT FEES AND SERVICES | 77 | ||||

PART IV | ||||||

Item 15 | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 77 | ||||

SIGNATURES | 81 | |||||

EX-21.1 | ||||||

EX-23.1 | ||||||

EX-31.1 | ||||||

EX-31.2 | ||||||

EX-32.1 | ||||||

EX-32.2 | ||||||

PART I

DEFINITIONS

In this Annual Report on Form 10-K, the words "IES", the "Company", the "Registrant", "we", "our", "ours" and "us" refer to Integrated Electrical Services, Inc. and, except as otherwise specified herein, to our subsidiaries.

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K includes certain statements that may be deemed "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, all of which are based upon various estimates and assumptions that the Company believes to be reasonable as of the date hereof. In some cases, you can identify forward-looking statements by terminology such as "may," "will," "could," "should," "expect," "plan," "project," "intend," "anticipate," "believe," "seek," "estimate," "predict," "potential," "pursue," "target," "continue," the negative of such terms or other comparable terminology. These statements involve risks and uncertainties that could cause the Company's actual future outcomes to differ materially from those set forth in such statements. Such risks and uncertainties include, but are not limited to:

| • | the ability of our controlling shareholder to take action not aligned with other shareholders; |

| • | the sale or disposition of the shares of our common stock held by our majority shareholder, which, under certain circumstances, would trigger change of control provisions in our severance plan or financing and surety arrangements; |

| • | the possibility that certain tax benefits of our net operating losses may be restricted or reduced in a change in ownership; |

| • | limitations on the availability of sufficient credit or cash flow to fund our working capital needs and capital expenditures and debt service; |

| • | difficulty in fulfilling the covenant terms of our credit facilities; |

| • | competition in our respective industries, both from third parties and former employees, which could result in the loss of one or more customers or lead to lower margins on new projects; |

| • | the inability to achieve, or difficulties and delays in achieving, potential benefits of the acquisition of MISCOR Group, Ltd; |

| • | challenges integrating other new businesses into the Company or new types of work, products or processes into our segments; |

| • | fluctuations in operating activity due to downturns in levels of construction, seasonality and differing regional economic conditions; |

| • | a general reduction in the demand for our services; |

| • | a change in the mix of our customers, contracts and business; |

| • | our ability to successfully manage projects; |

| • | possibility of errors when estimating revenue and progress to date on percentage-of-completion contracts; |

| • | additional closures or sales of facilities could result in significant future charges and a significant disruption of our operations; |

| • | inaccurate estimates used when entering into fixed-priced contracts; |

| • | the cost and availability of qualified labor; |

| • | increased cost of surety bonds affecting margins on work and the potential for our surety providers to refuse bonding or require additional collateral at their discretion; |

| • | increases in bad debt expense and days sales outstanding due to liquidity problems faced by our customers; |

1

| • | the recognition of potential goodwill, long-lived assets and other investment impairments; |

| • | credit and capital market conditions, including changes in interest rates that affect the cost of construction financing and mortgages, and the inability for some of our customers to retain sufficient financing which could lead to project delays or cancellations; |

| • | accidents resulting from the physical hazards associated with our work and the potential for accidents; |

| • | our ability to pass along increases in the cost of commodities used in our business, in particular, copper, aluminum, steel, fuel and certain plastics; |

| • | potential supply chain disruptions due to credit or liquidity problems faced by our suppliers; |

| • | loss of key personnel and effective transition of new management; |

| • | success in transferring, renewing and obtaining electrical and construction licenses; |

| • | uncertainties inherent in estimating future operating results, including revenues, operating income or cash flow; |

| • | disagreements with taxing authorities with regard to tax positions we have adopted; |

| • | the recognition of tax benefits related to uncertain tax positions; |

| • | complications associated with the incorporation of new accounting, control and operating procedures; |

| • | the financial impact of new or proposed accounting regulations; |

| • | the effect of litigation, claims and contingencies, including warranty losses, damages or other latent defect claims in excess of our existing reserves and accruals; |

| • | warranty losses or other unexpected liabilities stemming from former segments which we have sold or closed; |

| • | growth in latent defect litigation in states where we provide residential electrical work for home builders not otherwise covered by insurance; |

| • | changes in the assumptions made regarding future events used to value our stock options and performance-based stock awards; |

| • | the ability of IES to enter into, and the terms of, future contracts; |

| • | the inability to carry out plans and strategies as expected; |

| • | future capital expenditures and refurbishment, repair and upgrade costs; and delays in and costs of refurbishment, repair and upgrade projects; and |

| • | liabilities under laws and regulations protecting the environment. |

You should understand that the foregoing, as well as other risk factors discussed in this document, including those listed in Part I, Item 1A of this report under the heading " Risk Factors ", could cause future outcomes to differ materially from those experienced previously or those expressed in such forward-looking statements. We undertake no obligation to publicly update or revise any information, including information concerning our controlling shareholder, net operating losses, borrowing availability, cash position, or any forward-looking statements to reflect events or circumstances that may arise after the date of this report. Forward-looking statements are provided in this Form 10-K pursuant to the safe harbor established under the Private Securities Litigation Reform Act of 1995 and should be evaluated in the context of the estimates, assumptions, uncertainties and risks described herein.

2

| Item 1. | Business |

OVERVIEW OF OUR SERVICES

Integrated Electrical Services, Inc. is a holding company that owns and manages subsidiaries' operating across a variety of end markets. Our operations are currently organized into four principal business segments, based upon the nature of our current products and services:

| • | Communications – Nationwide provider of products and services for mission critical infrastructure, such as data centers, of large corporations. |

| • | Residential – Regional provider of electrical installation services for single-family housing and multi-family apartment complexes. |

| • | Commercial & Industrial – Provider of electrical design, construction, and maintenance services to the commercial and industrial markets in various regional markets and nationwide in certain areas of expertise, such as the power infrastructure market. |

| • | Infrastructure Solutions – Provider of industrial and rail services, and electrical and mechanical solutions to domestic and international customers. This segment was created in connection with the acquisition of MISCOR Group, Ltd. in September 2013, as described further below under Corporate Strategy. |

Our businesses are managed in a decentralized manner. While sharing common goals and values, each of the Company's segments manages its own day-to-day operations. Our corporate office is focused on significant capital allocation decisions, investment activities and selection of segment leadership, as well as strategic and operational improvement initiatives and the establishment and monitoring of risk management practices within our segment.

CORPORATE STRATEGY

We seek to create shareholder value through positive returns on capital and generation of free cash flow. In addition, we seek to acquire or invest in similar stand-alone platform companies based in North America or acquire businesses that strategically fit within our existing business segments. In evaluating potential acquisition candidates, we seek to invest in businesses with, among other characteristics:

| • | Significant market share in niche industries and low technological and/or product obsolescence risk; |

| • | Proven management with a willingness to continue post acquisition; |

| • | Established market position and sustainable advantage; |

| • | High returns on invested capital; and |

| • | Strong cash flow characteristics. |

We believe that acquisitions provide an opportunity to expand into new end markets and diversify our revenue and profit streams. Further, by acquiring businesses with strong cash flow characteristics we expect to maximize the value of our significant net operating loss carry forwards ("NOLs"). While we may use acquisitions to build our presence in the electrical infrastructure industry, we will also consider potential acquisitions in other industries, which could result in changes in our operations from those historically conducted by us.

Integrated Electrical Services, Inc. is a Delaware corporation established in 1997 and headquartered in Houston, Texas, with its executive office in Greenwich, Connecticut.

A majority of our outstanding common stock is owned by Tontine Capital Partners, L.P. and its affiliates (collectively, "Tontine"). On September 13, 2013, Tontine filed an amended Schedule 13D indicating its ownership level of 58%. As a result, Tontine can control most of our affairs, including any action requiring the approval of shareholders, such as the approval of any potential merger or sale of all or substantially all assets, segments, or the Company itself. While Tontine is subject to restrictions under federal securities laws on sales of its shares as an affiliate, Tontine is party to a Registration Rights Agreement with the Company under which it has the ability, subject to certain restrictions, to demand registration of its shares in order to permit unrestricted sales of those shares. On February 20, 2013, pursuant to the Registration Rights Agreement, Tontine delivered a request to the Company for registration of all of its shares of IES common stock, and on February 21, 2013, the Company filed a shelf registration statement (as amended, the "Shelf Registration Statement") to register Tontine's shares. The Shelf Registration Statement was declared effective by the U.S. Securities and Exchange Commission ("SEC") on June 18, 2013. As long as the Shelf Registration Statement remains effective, Tontine has the ability to resell any or all of its shares from time to time in one or more offerings, as described in the Shelf Registration Statement and in any prospectus supplement filed in connection with an offering pursuant to the Shelf Registration Statement. Additionally, a

3

change in control would trigger the change of control provisions in a number of our material agreements, including our credit facility, bonding agreements with our sureties and our executive severance plan. For more information see Note 3, "Controlling Shareholder" in the notes to our Consolidated Financial Statements.

Net Operating Loss Carry Forward

The Company and certain of its subsidiaries have a federal NOL of approximately $466 million at September 30, 2013, including approximately $141 million resulting from the additional amortization of personal goodwill. A change in ownership, as defined by Internal Revenue Code Section 382, could reduce the availability of net operating losses for federal and state income tax purposes. Should Tontine sell or otherwise dispose of all or a portion of its position in IES, a change in ownership could occur. In addition a change in ownership could result from the purchase of common stock by an existing or a new 5% shareholder as defined by Internal Revenue Code Section 382. Should a change in ownership occur, all net operating losses incurred prior to the change in ownership would be subject to limitation imposed by Internal Revenue Code Section 382, which would substantially reduce the amount of NOL currently available to offset taxable income. For more information see Item 8, " Financial Statements and Supplementary Data " of this Form 10-K.

On January 28, 2013, the Company implemented a tax benefit protection plan (the "NOL Rights Plan") that was designed to deter an acquisition of the Company's stock in excess of a threshold amount that could trigger a change of control within the meaning of Internal Revenue Code Section 382. The NOL Rights Plan was filed as an Exhibit to our Current Report on Form 8-K filed with the SEC on January 28, 2013 and any description thereof is qualified in its entirety by the terms of the NOL Rights Plan.

MISCOR Acquisition

On September 13, 2013, the Company completed its acquisition of MISCOR Group, Ltd. ("the Merger"). MISCOR Group, Ltd. ("MISCOR") is a provider of electrical and mechanical solutions to domestic and international customers. The acquisition of MISCOR is part of IES' strategic plan to invest in companies that meet our strategic and financial criteria and allow us to accelerate the utilization of our NOLs.

In connection with to the Merger, IES issued approximately 2.8 million shares of common stock and paid approximately $4.1 million in cash to MISCOR shareholders. The shares of IES common stock issued to MISCOR shareholders in connection with the Merger represent approximately 15.6% of the shares of IES common stock issued and outstanding immediately after the Merger.

Tontine owned approximately 49.9% of MISCOR prior to the Merger and elected to receive stock consideration in exchange for 100% of its shares of MISCOR common stock tendered in connection with the Merger, such that, according to its amended Schedule 13D filed on September 13, 2013, its ownership of IES increased from approximately 56.7% immediately prior to the Merger to approximately 58.0% immediately following the Merger.

In connection with the Merger, the Company entered into an amendment to the existing term loan with Wells Fargo Bank, National Association, in the amount of $13.1 million, the proceeds of which were used to pay the cash component of the merger consideration, to repay outstanding MISCOR debt and to pay certain transaction expenses associated with the Merger. For more information on the Merger and the acquisition term loan, see Note 20, "Business Combination" , in the notes to our Consolidated Financial Statements. The Agreement and Plan of Merger, First Amendment to Agreement and Plan of Merger, and Second Amendment to Credit and Security Agreement, dated September 13, 2013, by and among the Company, each of the other Borrowers and Guarantors named therein and Wells Fargo Bank, National Association, are filed as Exhibits to this Form 10-K.

The MISCOR business will be reported as a new operating segment, Infrastructure Solutions, as shown below.

OPERATING SEGMENTS

The Company's reportable segments consist of the consolidated operating units identified above, which offer different products and services and are managed separately. The table below describes the percentage of our total revenues attributable to each of our four segments over each of the last three years:

| Years Ended September 30, | ||||||||||||||||||||||||

| 2013 | 2012 | 2011 | ||||||||||||||||||||||

| $ | % | $ | % | $ | % | |||||||||||||||||||

| (Dollars in thousands, Percentage of revenues) | ||||||||||||||||||||||||

Communications | $ | 126,348 | 25.5 | % | $ | 121,492 | 26.6 | % | $ | 83,615 | 20.6 | % | ||||||||||||

Residential | 162,611 | 32.9 | % | 129,974 | 28.5 | % | 114,732 | 28.2 | % | |||||||||||||||

Commercial & Industrial | 203,481 | 41.1 | % | 204,649 | 44.9 | % | 207,794 | 51.2 | % | |||||||||||||||

Infrastructure Solutions (1) | 2,153 | 0.5 | % | - | - | - | - | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total Consolidated | $ | 494,593 | 100.0 | % | $ | 456,115 | 100.0 | % | $ | 406,141 | 100.0 | % | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| (1) | Includes revenues from MISCOR subsequent to acquisition on September 13, 2013. |

4

For additional financial information by segment, see Note 11, "Operating Segments" in the notes to our Consolidated Financial Statements. The residential, industrial, mission critical infrastructure and commercial industries in which we operate are exposed to many regional and national trends such as the demand for single and multi-family housing, the need for mission critical facilities as a result of technology-driven advancements, and changes in commercial, industrial, institutional, public infrastructure and electric utility spending. For a further discussion of the industries in which we operate, please see the discussion below of each of our segments.

Communications

Business Description

Originally established in 1984, our Communications segment is a leading provider of network infrastructure products and services for data centers and other mission critical environments. Services offered include the design, installation and maintenance of network infrastructure for the financial, medical, hospitality, government, high-tech manufacturing, educational and information technology industries. We also provide the design and installation of audio/visual, telephone, fire, wireless and intrusion alarm systems as well as design/build, service and maintenance of data network systems. A significant portion of our Communications revenue is generated from long-term, repeat customers, some of whom use IES as a preferred provider for major projects. We perform services across the United States from our ten offices, which includes our Communications headquarters located in Tempe, Arizona, allowing dedicated onsite maintenance teams at our customers' sites.

Industry Overview

Our Communications segment is driven by demand increases for computing and storage resources as a result of technology advancements and changes in data consumption patterns. We believe this trend towards increased data storage and retrieval on the "cloud" will continue to grow the data center segment of this industry. Additionally, devices continue to require greater bandwidth and interconnectivity. Nevertheless, due to economic, technological and other factors, there can be no assurance that construction and demand will continue to increase.

Sales and Marketing

We primarily specialize in installations of communication systems, and site and national account support for the mission critical infrastructure of Fortune 500 corporations. Our sales strategy relies on a concentrated business development effort, with centralized corporate marketing programs and direct end-customer communications and relationships. Due to the mission critical nature of the facilities we service, our end-customers significantly rely upon our past performance record, technical expertise and specialized knowledge. Our long-term strategy is to improve our position as a preferred mission critical solutions and services provider to large national corporations and strategic local companies. Key elements of our long-term strategy include continued investment in our employees' technical expertise and expansion of our onsite maintenance and recurring revenue model.

Competition

Our competition consists of both small, privately owned contractors who have limited access to capital and large public companies. We compete on quality of service and/or price, and seek to emphasize our long history of delivering high quality solutions to our customers.

Seasonality and Quarterly Fluctuations

The effects of seasonality on our Communications business are insignificant, as work generally is performed inside structures protected from the weather. Our service and maintenance business is also generally not affected by seasonality. In addition, the construction industry has historically been highly cyclical. Our volume of business may be adversely affected by declines in construction projects resulting from adverse regional or national economic conditions. Quarterly results may also be materially affected by the timing of new construction projects. Accordingly, operating results for any fiscal period are not necessarily indicative of results that may be achieved for any subsequent fiscal period.

Residential

Business Description

Residential provides electrical installation services for single-family housing and multi-family apartment complexes and CATV cabling installations for residential and light commercial applications. In addition to our core electrical construction work, the

5

Residential segment also provides services for the installation of residential solar power, smart meters, and electric car charging stations, both for new construction and existing residences. The Residential segment is made up of 24 total locations, which includes the headquarters in Houston. These locations geographically cover Texas, the Sun-Belt, and the Western and Mid-Atlantic regions of the United States, including Hawaii.

Industry Overview

Our Residential business is closely correlated to the single and multi-family housing market in the United States and our installation capabilities have the ability to effectively scale according to the housing cycle. Demand for both single-family and multi-family housing has increased with the economic recovery. Nevertheless, due to economic, technological or other factors there can be no assurance that construction and demand will continue to increase in the future.

Sales and Marketing

Demand for our Residential services is highly dependent on the number of single-family and multi-family home starts in the markets we serve. Although we operate in multiple states throughout the Sun-Belt, Mid-Atlantic and western regions of the United States, the majority of our segment revenues are derived from services provided in the state of Texas. Our sales efforts include a variety of strategies, including a concentrated focus on national homebuilders and multi-family developers and a local sales strategy for single and multi-family housing projects. Our cable, solar and electric car charging station revenues are typically generated through industry-specific third parties to which we act as a preferred provider of installation services.

Our long-term strategy is to continue to be the leading national provider of electrical services to the residential market. Although the key elements of our long-term strategy include a continued focus on maintaining a low and variable cost structure and cash generation, during the housing downturn we modified our strategy by expanding into markets less exposed to national building cycles, such as solar panel and electric car charging installations.

Competition

Our competition primarily consists of small, privately owned contractors who have limited access to capital. We believe that we have a competitive advantage over these smaller competitors due to our key employees' long-standing customer relationships, our financial capabilities, and our local market knowledge and competitive pricing. There are few barriers to entry for our electrical contracting services in the residential markets.

Seasonality and Quarterly Fluctuations

Results of operations from our Residential segment can be seasonal, depending on weather trends, with typically higher revenues generated during spring and summer and lower revenues during fall and winter. Our service and maintenance business is generally not affected by seasonality. In addition, the construction industry has historically been highly cyclical. Our volume of business may be adversely affected by declines in construction projects resulting from adverse regional or national economic conditions. Quarterly results may also be materially affected by the timing of new construction projects. Accordingly, operating results for any fiscal period are not necessarily indicative of results that may be achieved for any subsequent fiscal period.

Commercial & Industrial

Business Description

This segment offers a broad range of electrical design, construction, renovation, engineering and maintenance services to the commercial and industrial markets. The Commercial & Industrial segment consists of 18 total locations, which includes the segment headquarters in Houston, Texas. These locations geographically cover Texas, Nebraska, Colorado, Oregon and the Mid-Atlantic region.

Services include the design of electrical systems within a building or complex and procurement and installation of wiring and connection to power sources, end-use equipment and fixtures, as well as contract maintenance. We focus on projects that require special expertise, such as design-and-build projects that utilize the capabilities of our in-house experts, or projects which require specific market expertise, such as transmission and distribution projects. We also focus on service, maintenance and certain renovation and upgrade work, which tends to be either recurring or have lower sensitivity to economic cycles, or both. We provide services for a variety of projects, including: office buildings, manufacturing facilities, data centers, chemical plants, refineries, wind farms, solar facilities and municipal infrastructure and health care facilities. Our utility services consist of overhead and underground installation and maintenance of electrical and other utilities transmission and distribution networks, installation and splicing of high-voltage transmission and distribution lines, substation construction and substation and right-of-way maintenance. Our maintenance services generally provide recurring revenues that are typically less affected by levels of construction activity. Service and maintenance revenues are derived from service calls and routine maintenance contracts, which tend to be recurring and less sensitive to short-term economic fluctuations.

Industry Overview

Given the diverse end markets of our Commercial & Industrial customers, which include both commercial buildings, such as offices, healthcare facilities and schools, and industrial projects, such as power, chemical, refinery and heavy manufacturing facilities, we are subject to many trends within the construction industry. In general, demand for our Commercial & Industrial services is driven by construction and renovation activity levels, economic growth, and availability of bank lending. Due to economic, technological or other factors there can be no assurance that construction and demand will increase.

6

Sales and Marketing

Demand for our Commercial & Industrial services is driven by construction and renovation activity levels, economic growth, and availability of bank lending. Certain of our industrial projects have longer cycle times than our typical Commercial & Industrial services and may follow the economic trends with a lag. Our sales focus varies by location, but is primarily based upon regional and local relationships and a demonstrated expertise in certain industries, such as transmission and distribution.

Our long-term strategy has been modified over the past two years due to the downturn in the construction industry. Our long-term strategy is to be the preferred provider of electrical services in the markets where we have demonstrated expertise or are a local market leader. Key elements of our long-term strategy include leveraging our expertise in certain niche markets, expansion of our service and maintenance business and maintaining our focus on our returns on risk adjusted capital.

Competition

The electrical infrastructure services industry is generally highly competitive and includes a number of regional or small privately-held local firms. There are few barriers to entry for our electrical contracting services in the commercial and industrial markets, which limits our advantages when competing for projects. Industry expertise, project size, location and past performance will determine our bidding strategy, the level of involvement from competitors and our level of success in winning awards. Our primary advantages vary by location and market, but mostly are based upon local individual relationships with key employees or a demonstrated industry expertise. Additionally, due to the size of many of our projects, our financial resources help us compete effectively against local competitors.

Seasonality and Quarterly Fluctuations

The effects of seasonality on our Commercial & Industrial business are insignificant, as work generally is performed inside structures protected from the weather. Our service and maintenance business is also generally not affected by seasonality. In addition, the construction industry has historically been highly cyclical. Our volume of business may be adversely affected by declines in construction projects resulting from adverse regional or national economic conditions. Quarterly results may also be materially affected by the timing of new construction projects. Accordingly, operating results for any fiscal period are not necessarily indicative of results that may be achieved for any subsequent fiscal period.

Infrastructure Solutions

Business Description

Our Infrastructure Solutions segment provides maintenance and repair services to several industries, including electric motor repair and rebuilding for the steel, railroad, marine, petrochemical, pulp and paper, wind energy, mining, automotive and power generation industries. Infrastructure Solutions repairs and manufactures industrial lifting magnets for the steel and scrap industries, provides locomotive maintenance, remanufacturing, and repair services to the rail industry, and manufactures and rebuilds power assemblies, engine parts, and other components for large diesel engines. For more information see Note 20, " Business Combination " in the notes to our Consolidated Financial Statements.

Industry Overview

Given the diverse end-markets of Infrastructure Solutions' customers, we are subject to many economic trends. In general, demand for our products and services has been driven by in-house maintenance departments continuing to outsource maintenance and repair work, output levels and equipment utilization at heavy industrial facilities, railroad companies' capital investment in locomotives, and an overall improvement in the economy. Further, given our strategic locations in Ohio, Indiana, and West Virginia, we believe that we are well-positioned to capture spending on unconventional oil and gas exploration and production.

Sales and Marketing

Demand for Infrastructure Solutions' products and services is largely driven by the degree to which industrial and mechanical services are outsourced by our customers, production rates at steel, power generation and other heavy industrial facilities, the need for electrical infrastructure improvements, and spending on unconventional oil and gas exploration and production. Our sales effort is largely driven by personnel based at our nine locations and independent sales representatives. Given that the majority of our customers lie within a 200 mile radius of our facilities, we believe that this structure allows us to rapidly address and respond to the needs of our customers. Our long term strategy is to be the preferred provider of outsourced electro-mechanical and power assembly services, repairs, and manufacturing to our select markets.

Competition

Our competition is comprised mainly of small, specialized manufacturing and repair shops, a limited number of other multi-location providers of electric motor repair, engineering and maintenance services, and various original equipment manufacturers. Participants in this industry compete primarily on the basis of capabilities, service, quality, timeliness and, to a lesser extent, price. We believe that we have a competitive advantage over most small service providers due to our breadth of capabilities, focus on quality, technical support and customer service.

7

Raw Materials

The principal raw materials used in Infrastructure Solutions are copper, raw steel, and various flexible materials. Certain raw materials are obtained from a number of commercial sources at prevailing prices, and we do not depend on any single supplier for any substantial portion of raw materials. We obtain copper and raw steel from across the country through multiple sources. The cost to deliver copper and raw steel can limit the geographic areas from which we can obtain this material. Infrastructure Solutions attempts to minimize this risk by stocking adequate levels of key components. However, we may encounter problems from time to time in obtaining the raw materials necessary to conduct our Infrastructure Solutions business.

Seasonality and Quarterly Fluctuations

Infrastructure Solutions' revenues from industrial services may be affected by the timing of scheduled outages at its industrial customers' facilities and by weather conditions with respect to projects conducted outdoors, but the effects of seasonality on revenues in its industrial services business are insignificant. The effects of seasonality on revenues for rail services are also insignificant. Accordingly, Infrastructure Solutions' quarterly results may fluctuate and the results of one fiscal quarter may not be representative of the results of any other quarter or of the full fiscal year.

DISCONTINUED OPERATIONS

During the economic downturn we focused on return on capital and cash flow to maximize long-term shareholder value. As a result, beginning in 2011, we increased our focus on a number of initiatives to return the Company to profitability (the "2011 Restructuring Plan"). Included in these initiatives was the closure or sale of a number of facilities within our Commercial & Industrial segment and one location in our Communications segment. During 2011, we initiated the sale or closure of all or portions of our Commercial facilities in Arizona, Florida, Iowa, Maryland, Massachusetts, Nevada and Texas, our Industrial facility in Louisiana, and our Communications facility in Maryland. We have substantially concluded the closure of these facilities as of September 30, 2013. Results from operations of these facilities for the years ended September 30, 2013, 2012, and 2011 are presented in our Consolidated Statements of Comprehensive Income as discontinued operations. For further discussion of discontinued operations, please refer to Note 21, "Discontinued Operations" in the notes to our Consolidated Financial Statements. The 2011 Restructuring Plan is more fully described in Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations – The 2011 Restructuring Plan" of this Form 10-K.

RISK MANAGEMENT

The primary risks in our existing operations include project bidding and management, bodily injury, property and environmental damage, and construction defects. We monitor project bidding and management practices at various levels within our company. We maintain automobile, general liability and construction defect insurance for third party health, bodily injury and property damage, pollution coverage and workers' compensation coverage, which we consider appropriate to insure against these risks. Our third-party insurance is subject to deductibles for which we establish reserves. In light of these risks, we are also committed to a strong safety and environmental compliance culture. We employ full-time and part-time regional safety managers, under the supervision of our full-time Vice President of Safety, and seek to maintain standardized safety and environmental policies, programs, procedures and personal protection equipment relative to each segment, including programs to train new employees, which apply to employees new to the industry and those new to the Company. To further emphasize our commitment to safety, we have also tied management incentives to specific safety performance results.

In the electrical contracting industry, our ability to post surety bonds provides us with an advantage over competitors that are smaller or have fewer financial resources. We believe that the strength of our balance sheet, as well as a good relationship with our bonding providers, enhances our ability to obtain adequate financing and surety bonds. For a further discussion of our risks, please refer to Item 1A. "Risk Factors" of this Form 10-K.

CUSTOMERS

We have a diverse customer base. During the twelve-month periods ended September 30, 2013, 2012 and 2011, no single customer accounted for more than 10% of our revenues. We will continue to emphasize developing and maintaining relationships with our customers by providing superior, high-quality service. Management at each of our segments is responsible for determining sales strategy and sales activities.

BACKLOG

Backlog is a measure of revenue that we expect to recognize from work that has yet to be performed on uncompleted contracts, and from work that has been contracted but has not started. Backlog is not a guarantee of future revenues, as contractual commitments may change. As of September 30, 2013, our backlog was approximately $204 million compared to $234 million as of September 30, 2012. There were multiple large projects included in the 2012 backlog that were not replicated in 2013, consistent with our operating principle of focusing on higher quality projects and margins rather than high project volume.

8

REGULATIONS

Our operations are subject to various federal, state and local laws and regulations, including:

| • | licensing requirements applicable to electricians; |

| • | building and electrical codes; |

| • | regulations relating to worker safety and protection of the environment; |

| • | regulations relating to consumer protection, including those governing residential service agreements; and |

| • | qualifications of our business legal structure in the jurisdictions where we do business. |

Many state and local regulations governing electricians require permits and licenses to be held by individuals. In some cases, a required permit or license held by a single individual may be sufficient to authorize specified activities for all our electricians who work in the state or county that issued the permit or license. It is our policy to ensure that, where possible, any permits or licenses that may be material to our operations in a particular geographic area are held by multiple employees within that area.

We believe we have all licenses required to conduct our operations and are in compliance with applicable regulatory requirements. Failure to comply with applicable regulations could result in substantial fines or revocation of our operating licenses or an inability to perform government work.

CAPITAL FACILITIES

During fiscal year 2013, the Company maintained a credit facility, as described in Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations-Credit Facilities" of this Form 10-K. For a discussion of the Company's capital resources, see Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations-Capital Resources" of this Form 10-K.

FINANCIAL INFORMATION

For information on the Company's financial information by segment, see Note 11, "Operating Segments" in the notes to our Consolidated Financial Statements.

EMPLOYEES

At September 30, 2013, we had 2,740 employees. We are party to two collective bargaining agreements within our Infrastructure Solutions segment. We believe that our relationship with our employees is strong.

LOCATIONS

We have 61 domestic locations serving the United States. In addition to our executive and corporate offices, we have ten locations within our Communications business, 24 locations within our Residential business, 18 locations within our Commercial & Industrial business and nine locations within our Infrastructure Solutions business. This diversity helps to reduce our exposure to unfavorable economic developments in any given region.

9

EXECUTIVE OFFICERS OF THE REGISTRANT

Certain information with respect to each executive officer is as follows:

James M. Lindstrom, 41, has served as President and Chief Executive Officer of the Company since October 3, 2011. He previously served as Interim President and Chief Executive Officer of the Company since June 30, 2011. Mr. Lindstrom was an employee at Tontine Associates, LLC, a private investment fund and an affiliate of our controlling shareholder Tontine from 2006 to October 3, 2011. From 2003 to 2006, Mr. Lindstrom was Chief Financial Officer of Centrue Financial Corporation, a regional financial services company, and had prior experience in private equity and investment banking. Mr. Lindstrom served as a director of Broadwind Energy, Inc. from October 2007 to May 2010 and has served as a board observer on multiple public and private boards.

Robert W. Lewey , 51, has served as Senior Vice President and Chief Financial Officer since January 20, 2012. From 2001 to 2006 and since 2007, Mr. Lewey served as Director of Tax, Vice President, Tax and Treasurer for IES. From 2006 to 2007, he served as Vice President, Tax for Sulzer US Holdings, Inc. From 1995 to 2001, Mr. Lewey served as Vice President, Tax for Metamor Worldwide, Inc., a leading provider of information technology solutions. Mr. Lewey began his career with Deloitte.

Gail D. Makode , 38, has served as Senior Vice President, General Counsel and Corporate Secretary since October 15, 2012. Ms. Makode was previously General Counsel and Member of the Board at MBIA Insurance Corporation and Chief Compliance Officer of MBIA Inc. Prior to MBIA, Ms. Makode served as vice president and counsel for Deutsche Bank AG, and before that, was an associate at Cleary, Gottlieb, Steen & Hamilton, where she specialized in public and private securities offerings and mergers and acquisitions.

We have adopted a Code of Ethics for Financial Executives that applies to our Chief Executive Officer, Chief Financial Officer and Chief Accounting Officer. The Code of Ethics may be found on our website at www.ies-corporate.com . If we make any substantive amendments to the Code of Ethics or grant any waiver, including any implicit waiver, from a provision of the code to our Chief Executive Officer, Chief Financial Officer or Chief Accounting Officer, we will disclose the nature of such amendment or waiver on that website or in a report on Form 8-K. Paper copies of these documents are also available free of charge upon written request to us.

AVAILABLE INFORMATION

General information about us can be found on our website at www.ies-corporate.com under "Investors." We file our interim and annual financial reports, as well as other reports required by the Securities Exchange Act of 1934, as amended (the "Exchange Act"), with the United States Securities and Exchange Commission (the "SEC").

Our annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, as well as any amendments and exhibits to those reports are available free of charge through our website as soon as it is reasonably practicable after we file them with, or furnish them to, the SEC. You may also contact our Investor Relations department and they will provide you with a copy of these reports. The materials that we file with the SEC are also available free of charge through the SEC website at www.sec.gov . You may also read and copy these materials at the SEC's Public Reference Room at 100 F Street, NE., Washington, D.C. 20549. Information on the operation of the Public Reference Room is available by calling the SEC at 1–800–SEC–0330.

In addition to the Code of Ethics for Financial Executives, we have adopted a Code of Business Conduct and Ethics for directors, officers and employees (the Legal Compliance and Corporate Policy Manual), and established Corporate Governance Guidelines and adopted charters outlining the duties of our Audit, Human Resources and Compensation and Nominating/Governance Committees, copies of which may be found on our website. Paper copies of these documents are also available free of charge upon written request to us. We have designated an "audit committee financial expert" as that term is defined by the SEC. Further information about this designee may be found in the Proxy Statement for the 2014 Annual Meeting of Stockholders of the Company.

10

Item 1A. Risk Factors

You should consider carefully the risks described below, as well as the other information included in this document before making an investment decision. Our business, results of operations or financial condition could be materially and adversely affected by any of these risks, and the value of your investment may decrease due to any of these risks.

Existence of a controlling shareholder.

A majority of our outstanding common stock is owned by Tontine Capital Partners, L.P. and its affiliates (collectively, "Tontine"). On September 13, 2013, Tontine filed an amended Schedule 13D indicating its ownership level of 58%. As a result, Tontine can control most of our affairs, including the election of our directors, who in turn appoint executive management, and can control any action requiring the approval of shareholders, including the adoption of amendments to our corporate charter and approval of any potential merger or sale of all or substantially all assets, segments, or the Company itself. This control also gives Tontine the ability to bring matters to a shareholder vote that may not be in the best interest of our other shareholders lenders, surety and customers. Additionally, Tontine is in the business of investing in companies and may, from time to time, acquire and hold interests in businesses that compete directly or indirectly with us or act as suppliers or customers of the Company.

Availability of net operating losses may be reduced by a change in ownership.

A change in ownership, as defined by Internal Revenue Code Section 382, could reduce the availability of net operating losses, ("NOLs"), for federal and state income tax purposes. Should Tontine sell or otherwise dispose of all or a portion of its position in IES, a change in ownership could occur. A change in ownership could also result from the purchase of common stock by an existing or a new 5% shareholder as defined by Internal Revenue Code Section 382. Currently, we have approximately $315 million of federal NOLs that are available to use to offset taxable income, exclusive of NOLs from the amortization of additional tax goodwill. Should a change in ownership occur, all NOLs incurred prior to the change in ownership would be subject to limitation imposed by Internal Revenue Code Section 382, which would substantially reduce the amount of NOL currently available to offset taxable income.

On January 28, 2013, we implemented the NOL Rights Plan, which was designed to deter an acquisition of the Company's stock in excess of a threshold amount that could trigger a change of control within the meaning of Internal Revenue Code Section 382. We can make no assurances the NOL Rights Plan will be effective in deterring a change in control or protecting or realizing NOLs.

To service our indebtedness and to fund working capital, we will require a significant amount of cash. Our ability to generate cash depends on many factors that are beyond our control.

Our ability to make payments on and to refinance our indebtedness and to fund working capital requirements will depend on our ability to generate cash in the future. This is subject to our operational performance, as well as general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control.

We cannot provide assurance that our business will generate sufficient cash flow from operations or asset sales or that future borrowings will be available to us under our credit facility in an amount sufficient to enable us to pay our indebtedness or to fund our other liquidity needs. We may need to refinance all or a portion of our indebtedness, on or before maturity. We cannot provide assurance that we will be able to refinance any of our indebtedness on commercially reasonable terms, or at all. Our inability to refinance our debt on commercially reasonable terms could have a material adverse effect on our business.

We have restrictions and covenants under our credit facility.

We may not be able to remain in compliance with the covenants in our credit facility. A failure to fulfill the terms and requirements of our credit facility may result in a default under one or more of our material agreements, which could have a material adverse effect on our ability to conduct our operations and our financial condition.

The highly competitive nature of our industries could affect our profitability by reducing our profit margins.

With respect to electrical contracting services, the industries in which we compete are highly fragmented and are served by many small, owner-operated private companies. There are also several large private regional companies and a small number of large public companies from which we face competition in these industries. In the future, we could also face competition from new competitors entering these markets because certain segments, such as our electrical contracting services, have a relatively low barrier for entry while other segments, such as our services for mission critical infrastructure, have attractive dynamics. Some of our competitors offer a greater range of services, including mechanical construction, facilities management, plumbing and heating, ventilation and air conditioning services. Competition in our markets depends on a number of factors, including price. Some of our competitors may have lower overhead cost structures and may, therefore, be able to provide services comparable to ours at lower rates than we do. If we are unable to offer our services at competitive prices or if we have to reduce our prices to remain competitive, our profitability would be impaired.

11

The markets in which Infrastructure Solutions does business are highly competitive, and we do not expect the level of competition that we face to decrease in the future. An increase in competitive pressures in these markets or our failure to compete effectively may result in pricing reductions, reduced gross margins, and loss of market share. Many of the competitors of the acquired MISCOR business have longer operating histories, greater name recognition, more customers, and significantly greater financial, marketing, technical, and other competitive resources than we have. While the combined corporation presents the opportunity to leverage MISCOR's resources to improve financial results, our competitors may still be able to adapt more quickly to new technologies and changes in customer needs or devote greater resources to the development, promotion, and sale of their products and services. While we believe Infrastructure Solutions' overall product and service offerings distinguish it from its competitors, these competitors could develop new products or services that could directly compete with Infrastructure Solutions' products and services.

We may experience difficulties in integrating MISCOR's business and could fail to realize potential benefits of the merger.

Achieving the anticipated benefits of the merger will depend in part upon whether we are able to integrate MISCOR's business in an efficient and effective manner. We may not be able to complete this integration process smoothly or successfully. The difficulties of integrating MISCOR's business potentially will include, among other things:

| • | geographically separated organizations and possible differences in corporate cultures and management philosophies; |

| • | significant demands on management resources, which may distract management's attention from day-to-day business; |

| • | differences in the disclosure systems, compliance requirements, accounting systems, and accounting controls and procedures of the two companies, which may interfere with our ability to make timely and accurate public disclosure; and |

| • | the demands of managing new locations, new personnel and new lines of business acquired in the Merger. |

Any inability to realize the potential benefits of the Merger, as well as any delays in integration, could have an adverse effect upon our revenues, level of expenses and operating results, which may adversely affect the value of our common stock.

We may be unsuccessful at integrating other companies that we may acquire, or new types of work, products or processes into our segments.

We may engage in acquisitions and dispositions of operations, assets and investments, or develop new types of work, processes or products from time to time in the future. If we are unable to successfully integrate newly acquired assets or operations or if we make untimely or unfavorable dispositions of operations or investments, it could negatively impact the market value of our common stock. Additionally, any future acquisition or disposition may result in significant changes in the composition of our assets and liabilities, and as a result, our financial condition, results of operations and the market value of our common stock following any such acquisition or disposition may be affected by factors different from those currently affecting our financial condition, results of operations and market value of our common stock.

The current changing economic environment poses significant challenges for us.

Although general economic conditions have improved, the current economic environment continues to present challenges for our customers and us. While we have limited direct exposure to problems in Europe and the financial markets, we are nevertheless affected by general economic trends. Many of our customers depend on the availability of credit to purchase our services or electrical and mechanical products. Continued uncertainties or the return of constrained credit market conditions could have adverse effects on our customers, which would adversely affect our financial condition and results of operations. This continued uncertainty in economic conditions coupled with the on-going weak national economic recovery could have an adverse effect on our revenue and profits.

Changes in operating factors that are beyond our control could hurt our operating results.

Our operating results may fluctuate significantly in the future as a result of a variety of factors, many of which are beyond management's control. These factors include the costs of new technology; the relative speed and success with which Infrastructure Solutions can acquire customers for its products and services; capital expenditures for equipment; sales, marketing, and promotional activities expenses; changes in its pricing policies, suppliers, and competitors; changes in operating expenses; increased competition in the markets we serve; and other general economic and seasonal factors. Adverse changes in one or more of these factors could hurt our operating results.

Backlog may not be realized or may not result in profits.

Customers often have no obligation under our contracts to assign or release work to us, and many contracts may be terminated on short notice. Reductions in backlog due to cancellation of one or more contracts by a customer or for other reasons could significantly reduce the revenue and profit we actually receive from contracts included in backlog. In the event of a project cancellation, we may be reimbursed for certain costs but typically have no contractual right to the total revenues reflected in our backlog.

12

Our use of percentage-of-completion accounting could result in a reduction or elimination of previously reported profits.

As discussed in Item 7, " Management's Discussion and Analysis of Financial Condition and Results of Operations - Critical Accounting Policies" and in the notes to our Consolidated Financial Statements included in Item 8, " Financial Statements and Supplementary Data" of this Form 10-K, a significant portion of our revenues are recognized using the percentage-of-completion method of accounting, utilizing the cost-to-cost method. This method is used because management considers costs incurred to be the best available measure of progress on these contracts. We recognize costs for materials upon installation. The percentage-of-completion accounting practice we use results in our recognizing contract revenues and earnings ratably over the contract term in proportion to our incurrence of contract costs. The earnings or losses recognized on individual contracts are based on estimates of contract revenues, costs and profitability. Contract losses are recognized in full when determined to be probable and reasonably estimable and contract profit estimates are adjusted based on ongoing reviews of contract profitability. Further, a portion of our contracts contain various cost and performance incentives. Penalties are recorded when known or finalized, which generally occurs during the latter stages of the contract. In addition, we record cost recovery claims when we believe recovery is probable and the amounts can be reasonably estimated. Actual collection of claims could differ from estimated amounts and could result in a reduction or elimination of previously recognized earnings. In certain circumstances, it is possible that such adjustments could be significant.

We may incur significant charges or be adversely impacted by the closure or sale of additional facilities.

While, historically, we have incurred significant costs associated with the closure or disposition of facilities, we will continue to evaluate the need for facility closures or dispositions from time to time in the future. If we were to elect to dispose of a substantial portion of any of our segments, the realized values of such actions could be substantially less than current book values, which would likely result in a material adverse impact on our financial results.

The availability and cost of surety bonds affect our ability to enter into new contracts and our margins on those engagements.

Many of our customers require us to post performance and payment bonds issued by a surety. Those bonds guarantee the customer that we will perform under the terms of a contract and that we will pay subcontractors and vendors. We obtain surety bonds from two primary surety providers; however, there is no commitment from these providers to guarantee our ability to issue bonds for projects as they are required. Our ability to access this bonding capacity is at the sole discretion of our surety providers.

Due to seasonality and differing regional economic conditions, our results may fluctuate from period to period.

Our business is subject to seasonal variations in operations and demand that affect the construction business, particularly in the Residential and Commercial & Industrial segments, as well as seasonal variations in the industrial and rail industries in which Infrastructure Solutions participates. Untimely weather delay from rain, heat, ice, cold or snow can not only delay our work but can negatively impact our schedules and profitability by delaying the work of other trades on a construction site. Our quarterly results may also be affected by regional economic conditions that affect the construction market. Infrastructure Solutions' revenues from industrial services may be affected by the timing of scheduled outages at its industrial customers' facilities and by weather conditions with respect to projects conducted outdoors. Accordingly, our performance in any particular quarter may not be indicative of the results that can be expected for any other quarter or for the entire year.

The estimates we use in placing bids could be materially incorrect. The use of incorrect estimates could result in losses on a fixed price contract. These losses could be material to our business.

We currently generate, and expect to continue to generate, a significant portion of our revenues under fixed price contracts. The cost of fuel, labor and materials, including copper wire, may vary significantly from the costs we originally estimate. Variations from estimated contract costs along with other risks inherent in performing fixed price contracts may result in actual revenue and gross profits for a project differing from those we originally estimated, and could result in losses on projects. Depending upon the size of a particular project, variations from estimated contract costs can have a significant impact on our operating results.

Commodity and labor costs may fluctuate materially, and we may not be able to pass on all cost increases during the term of a contract, which could have an adverse effect on our ability to maintain our profitability.

We enter into many contracts at fixed prices, and if the costs associated with labor; and commodities such as copper, aluminum, steel, fuel and certain plastics increase, losses may be incurred. Some of these materials have been and may continue to be subject to sudden and significant price increases. Depending on competitive pressures and customer resistance, we may not be able to pass on these cost increases to our customers, which would reduce our gross profit margins and, in turn, make it more difficult for us to maintain our profitability.

We may experience difficulties in managing our billings and collections.

Our billings under fixed price contracts in our electrical contracting business are generally based upon achieving certain milestones and will be accepted by the customer once we demonstrate those milestones have been met. If we are unable to demonstrate compliance with billing requests, or if we fail to issue a project billing, our likelihood of collection could be delayed or impaired, which, if experienced across several large projects, could have a materially adverse effect on our results of operations.

13

Our reported operating results could be adversely affected as a result of goodwill impairment write-offs.

When we acquire a business, we record an asset called "goodwill" if the amount we pay for the business, including liabilities assumed, is in excess of the fair value of the assets of the business we acquire. Accounting principles generally accepted in the United States of America ("GAAP") requires that goodwill attributable to each of our reporting units be tested at least annually. The testing includes comparing the fair value of each reporting unit with its carrying value. Fair value is determined using discounted cash flows, market multiples and market capitalization. Significant estimates used in the methodologies include estimates of future cash flows, future short-term and long-term growth rates, weighted average cost of capital and estimates of market multiples for each of the reporting units. On an ongoing basis, we expect to perform impairment tests at least annually as of September 30. Impairment adjustments, if any, are required to be recognized as operating expenses. We cannot assure that we will not have future impairment adjustments to our recorded goodwill.

The vendors who make up our supply chain may be adversely affected by the current operating environment and credit market conditions.

We are dependent upon the vendors within our supply chain to maintain a steady supply of inventory, parts and materials. Many of our segments are dependent upon a limited number of suppliers, and significant supply disruptions could adversely affect our operations. Under recent market conditions, including both the construction slowdown and the tightening credit market, it is possible that one or more of our suppliers will be unable to meet the terms of our operating agreements due to financial hardships, liquidity issues or other reasons related to the prolonged market recovery.

Our operations are subject to numerous physical hazards. If an accident occurs, it could result in an adverse effect on our business.

Hazards related to our industry include, but are not limited to, electrocutions, fires, machinery-caused injuries, mechanical failures and transportation accidents. These hazards can cause personal injury and loss of life, severe damage to or destruction of property and equipment, and may result in suspension of operations. Our insurance does not cover all types or amounts of liabilities. Our third-party insurance is subject to deductibles for which we establish reserves. No assurance can be given that our insurance or our provisions for incurred claims and incurred but not reported claims will be adequate to cover all losses or liabilities we may incur in our operations; nor can we provide assurance that we will be able to maintain adequate insurance at reasonable rates.

Our internal controls over financial reporting and our disclosure controls and procedures may not prevent all possible errors that could occur. Internal controls over financial reporting and disclosure controls and procedures, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control system's objective will be met.

On a quarterly basis we evaluate our internal controls over financial reporting and our disclosure controls and procedures, which include a review of the objectives, design, implementation and effectiveness of the controls and the information generated for use in our periodic reports. In the course of our controls evaluation, we sought (and seek) to identify data errors, control problems and to confirm that appropriate corrective actions, including process improvements, are being undertaken. This type of evaluation is conducted on a quarterly basis so that the conclusions concerning the effectiveness of our controls can be reported in our periodic reports.

A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control system's objectives will be satisfied. Internal controls over financial reporting and disclosure controls and procedures are designed to give reasonable assurance that they are effective and achieve their objectives. We cannot provide absolute assurance that all possible future control issues have been detected. These inherent limitations include the possibility that our judgments can be faulty, and that isolated breakdowns can occur because of human error or mistake. The design of our system of controls is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed absolutely in achieving our stated goals under all potential future or unforeseeable conditions. Because of the inherent limitations in a cost-effect control system, misstatements due to error could occur without being detected.

We have adopted tax positions that a taxing authority may view differently. If a taxing authority differs with our tax positions, our results may be adversely affected.

Our effective tax rate and cash paid for taxes are impacted by the tax positions that we have adopted. Taxing authorities may not always agree with the positions we have taken. We have established reserves for tax positions that we have determined to be less likely than not to be sustained by taxing authorities. However, there can be no assurance that our results of operations will not be adversely affected in the event that disagreement over our tax positions does arise.

14

Litigation and claims can cause unexpected losses.

In the construction business there are frequently claims and litigation. There are also inherent claims and litigation risks associated with the number of people that work on construction sites and the fleet of vehicles on the road every day. In all of our businesses, we are subject to potential claims and litigation. Claims are sometimes made and lawsuits filed for amounts in excess of their value or in excess of the amounts for which they are eventually resolved. Claims and litigation normally follow a predictable course of time to resolution. However, there may be periods of time in which a disproportionate amount of our claims and litigation are concluded in the same quarter or year. If multiple matters are resolved during a given period, then the cumulative effect of these matters may be higher than the ordinary level in any one reporting period.

Latent defect claims could expand.

Latent defect litigation is normal for residential home builders in some parts of the country; however, such litigation is increasing in certain states where we perform work. Also, in recent years, latent defect litigation has expanded to aspects of the commercial market. Should we experience similar increases in our latent defect claims and litigation, additional pressure may be placed on the profitability of the Residential and Commercial & Industrial segments of our business.

We may be required to conduct environmental remediation activities, which could be expensive and inhibit the growth of our business and our ability to maintain profitability, particularly in our Infrastructure Solutions business.

We are subject to a number of environmental laws and regulations, including those concerning the handling, treatment, storage, and disposal of hazardous materials. These laws predominately affect our Infrastructure Solutions business but may impact our other businesses. These environmental laws generally impose liability on present and former owners and operators, transporters and generators of hazardous materials for remediation of contaminated properties. We believe that our business is operating in compliance in all material respects with applicable environmental laws, many of which provide for substantial penalties for violations. There can be no assurance that future changes in such laws, interpretations of existing regulations or the discovery of currently unknown problems or conditions will not require substantial additional expenditures. In addition, if we do not comply with these laws and regulations, we could be subject to material administrative, civil or criminal penalties, or other liabilities. We may also be required to incur substantial costs to comply with current or future environmental and safety laws and regulations. Any such additional expenditures or costs that we may incur could hurt our operating results.

The loss of a group or several key personnel, either at the corporate or operating level, could adversely affect our business.

The loss of key personnel or the inability to hire and retain qualified employees could have an adverse effect on our business, financial condition and results of operations. Our operations depend on the continued efforts of our executive officers, senior management and management personnel at our segments. We cannot guarantee that any member of management at the corporate or subsidiary level will continue in their capacity for any particular period of time. We have a severance plan in place that covers certain of our senior leaders; however, this plan can neither guarantee that we will not lose key employees, nor prevent them from competing against us, which is often dependent on state and local employment laws. If we lose a group of key personnel or even one key person at a segment, we may not be able to recruit suitable replacements at comparable salaries or at all, which could adversely affect our operations. Additionally, we do not maintain key man life insurance for members of our management.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Facilities

At September 30, 2013, we maintained branch offices, warehouses, sales facilities and administrative offices at 61 locations. Substantially all of our facilities are leased. We lease our executive office located in Greenwich, Connecticut and our corporate office located in Houston, Texas. We believe that our properties are adequate for our present needs, and that suitable additional or replacement space will be available as required.

Item 3. Legal Proceedings

For further information regarding legal proceedings, see Note 17, "Commitments and Contingencies - Legal Matters " in the notes to our Consolidated Financial Statements.

15

Item 4. Mine Safety Disclosures

None.

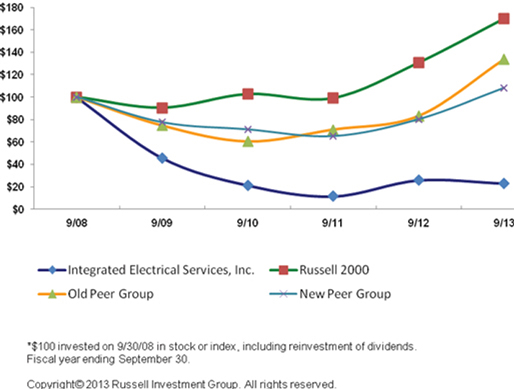

Item 5. Market for Registrant's Common Equity; Related Stockholder Matters and Issuer Purchases of Equity Securities