UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________

FORM 10-K

____________

(check one)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended June 26, 2010 |

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to |

Commission File No. 1-367

____________

THE L.S. STARRETT COMPANY

(Exact name of registrant as specified in its charter)

____________

MASSACHUSETTS | 04-1866480 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

121 CRESCENT STREET, ATHOL, MASSACHUSETTS | 01331 | |

(Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code 978-249-3551

____________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Class A Common - $1.00 Per Share Par Value | New York Stock Exchange | |

Class B Common - $1.00 Per Share Par Value | Not applicable |

____________

1

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one)

Large Accelerated Filer ¨ Accelerated Filer x

Non-Accelerated Filer ¨ Smaller Reporting Company ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The Registrant had 5,812,328 and 856,629 shares, respectively, of its $1.00 par value Class A and B common stock outstanding on December 27, 2009. On December 27, 2009, the last business day of the Registrant's second fiscal quarter, the aggregate market value of the common stock held by nonaffiliates was approximately $53,106,325.

There were 5,872,414 and 812,175 shares, respectively, of the Registrant's $1.00 par value Class A and Class B common stock outstanding as of August 31, 2010.

The exhibit index is located on pages 51-52.

DOCUMENTS INCORPORATED BY REFERENCE

The Registrant intends to file a definitive Proxy Statement for the Company's 2010 Annual Meeting of Stockholders within 120 days of the end of the fiscal year ended June 26, 2010. Portions of such Proxy Statement are incorporated by reference in Part III.

Portions of the Proxy Statement for October 20, 2010 Annual Meeting (Part III).

2

THE L.S. STARRETT COMPANY

FORM 10-K

FOR THE PERIOD ENDED JUNE 26, 2010

TABLE OF CONTENTS

Page Number | ||

PART I | ||

ITEM 1. | Business | 4-7 |

ITEM 1A. | Risk Factors | 7-9 |

ITEM 1B. | Unresolved Staff Comments | 9 |

ITEM 2. | Properties | 9-10 |

ITEM 3. | Legal Proceedings | 10 |

ITEM 4. | Reserved | 10 |

PART II | ||

ITEM 5. | Market for the Company's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 10-11 |

ITEM 6. | Selected Financial Data | 12 |

ITEM 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 12-19 |

ITEM 7A. | Quantitative and Qualitative Disclosures about Market Risk | 12-19 |

ITEM 8. | Financial Statements and Supplementary Data | 19-44 |

ITEM 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 44 |

ITEM 9A. | Controls and Procedures | 44-48 |

ITEM 9B. | Other Information | 49 |

PART III | ||

ITEM 10. | Directors, Executive Officers and Corporate Governance | 49-50 |

ITEM 11. | Executive Compensation | 50 |

ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 50 |

ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | 50 |

ITEM 14. | Principal Accounting Fees and Services | 51 |

PART IV | ||

ITEM 15. | Exhibits and Financial Statement Schedules | 52-53 |

EXHIBIT INDEX | 53-54 | |

SIGNATURES | 55 |

All references in this Annual Report to "Starrett", the "Company", "we", "our" and "us" means The L.S. Starrett Company and its subsidiaries.

3

PART I

Item 1 - Business

General

Founded in 1880 by Laroy S. Starrett and incorporated in 1929, the Company is engaged in the business of manufacturing over 5,000 different products for industrial, professional and consumer markets. As a global manufacturer with major subsidiaries in Brazil (1956), Scotland (1958) and China (1997), the Company offers its broad array of products to the market through multiple channels of distribution throughout the world. The Company's products include precision tools, electronic gages, gage blocks, optical and vision measuring equipment, custom engineered granite solutions, tape measures, levels, chalk products, squares, band saw blades, hole saws, hacksaw blades, jig saw blades, reciprocating saw blades, M1 ® lubricant and precision ground flat stock. The Company's financial reporting is based upon one business segment.

Starrett® is brand recognized around the world for precision, quality and innovation.

Products

The Company's tools and instruments are sold throughout North America and in over 100 foreign countries. By far the largest consumer of these products is the metalworking industry including aerospace, medical, and automotive but other important consumers are marine and farm equipment shops, do-it-yourselfers and tradesmen such as builders, carpenters, plumbers and electricians.

For 130 years the Company has been a recognized leader in providing measurement solutions consisting of hand measuring tools and precision instruments such as micrometers, vernier calipers, height gages, depth gages, electronic gages, dial indicators, steel rules, combination squares, custom and non contact gaging and many other items. Skilled personnel, superior products, manufacturing expertise, innovation and unmatched service has earned the Company its reputation as the "Best in Class" provider of measuring application solutions for industry. During fiscal 2008, the Company enhanced its wireless data collection solutions, making them more customer-friendly and more software-compatible.

The Company's saw product lines enjoy strong global brand recognition and market share. These products encompass a breadth of uses. During 2009, the Company introduced several new products including its ADVANZ carbide tipped products and its VERSATIX products with a patent pending tooth geometry designed for the cutting of structurals and small solids. This launch was further enhanced through the global introduction of new support programs and marketing collateral. These actions are aimed at positioning Starrett for global growth in wide band products for production applications as well as product range expansions for shop applications. A full line of complementary saw products, including hack, jig, reciprocating saw blades and hole saws provide cutting solutions for the building trades and are offered primarily through construction, electrical, plumbing and retail distributors. During fiscal 2008, the Company was issued a patent for its bi-metal unique® manufacturing process and products. This break-through Split Chip Advantage technology enables the Company to produce saw blades, which are up to 50% stronger and offer up to 170% more contact area than traditional electron beam (EB) products. This technology is now used on many of the Company's saw products.

Recent acquisitions have added to the Company's portfolio of custom measuring solutions that complement the Company's existing special gaging expertise. On July 17, 2007, the Company purchased all of the assets of Kinemetric Engineering. Kinemetric Engineering specializes in precision video-based metrology, specialty motion devices and custom engineered systems for measurement and inspection. Kinemetric Engineering brings a wealth of experience, engineering and manufacturing capability. This business unit also oversees the sales and support of the Company's high quality line of Starrett Optical Projectors, combining to make a very comprehensive product offering.

The Company's custom engineered granite product offering was further enhanced by the acquisition of Tru-Stone Technologies Inc. (Tru-Stone) in fiscal 2006. This strategic acquisition significantly improved the granite surface plate capabilities providing access to high-end metrology markets such as the electronics and flat panel display industry. The consolidation of the Company's granite surface plate operations with Tru-Stone provided savings in labor and operating expenses.

4

Personnel

At June 26, 2010, the Company had 1,744 employees, approximately 51% of whom were domestic. This represents a net decrease from June 27, 2009 of 24 employees. The headcount reduction was in international operations, primarily in Brazil.

None of the Company's operations are subject to collective bargaining agreements. In general, the Company considers relations with its employees to be excellent. Domestic employees hold a large share of Company stock resulting from various stock purchase plans. The Company believes that this dual role of owner-employee has strengthened employee morale over the years.

Competition

The Company is competing on the basis of its reputation as the best in class for quality, precision and innovation combined with its commitment to customer service and strong customer relationships. To that end, Starrett is increasingly focusing on providing customer centric solutions. Although the Company is generally operating in highly competitive markets, the Company's competitive position cannot be determined accurately in the aggregate or by specific market since none of its competitors offer all of the same product lines offered by the Company or serve all of the markets served by the Company.

The Company is one of the largest producers of mechanics' hand measuring tools and precision instruments. In the United States, there are three other major companies and numerous small competitors in the field, including direct foreign competitors. As a result, the industry is highly competitive. During fiscal 2010, there were no material changes in the Company's competitive position in spite of the current global economic crisis, which is accelerating the migration of American manufacturing jobs to lower cost countries. Internationally, the Company's significant investments in manufacturing and sales operations in China appear to have resulted in market share gains and enhanced brand recognition. The Company's products for the building trades, such as tape measures and levels, are under constant margin pressure due to a channel shift to large national home and hardware retailers. The Company is responding to such challenges by expanding its manufacturing operations in China. Certain large customers offer private labels ("own brand") that compete with Starrett branded products. These products are often sourced directly from low cost countries.

Saw products encounter competition from several domestic and international sources. The Company's competitive position varies by market segment and country. Continued research and development, new patented products and processes, and strong customer support have enabled the Company to compete successfully in both general and performance oriented applications.

Foreign Operations

The operations of the Company's foreign subsidiaries are consolidated in its financial statements. The subsidiaries located in Brazil, Scotland and China are actively engaged in the manufacturing and distribution of precision measuring tools, saw blades, optical and vision measuring equipment and hand tools. Subsidiaries in Canada, Argentina, Australia, New Zealand, Mexico and Germany are engaged in distribution of the Company's products. The Company expects its foreign subsidiaries to continue to play a significant role in its overall operations. A summary of the Company's foreign operations is contained in Note 15 to the Company's fiscal 2010 financial statements under the caption "OPERATING DATA" found in Item 8 of this Form 10-K.

Orders and Backlog

The Company generally fills orders from finished goods inventories on hand. Sales order backlog of the Company at any point in time is not significant. Total inventories amounted to $46.2 million at June 26, 2010 and $60.2 million at June 27, 2009. The Company uses the last-in, first-out (LIFO) method of valuing most domestic inventories (approximately 51% of all inventories). LIFO inventory amounts reported in the financial statements are approximately $25.2 million and $33.7 million, respectively, lower than if determined on a first-in, first-out (FIFO) basis at June 26, 2010 and June 27, 2009.

5

Intellectual Property

When appropriate, the Company applies for patent protection on new inventions and currently owns a number of patents. Its patents are considered important in the operation of the business, but no single patent is of material importance when viewed from the standpoint of its overall business. As noted previously, during fiscal 2008 the Company was issued a patent for its bi-metal unique® manufacturing process and products. The Company relies on its continuing product research and development efforts, with less dependence on its current patent position. It has for many years maintained engineers and supporting personnel engaged in research, product development and related activities. The expenditures for these activities during fiscal years 2010, 2009 and 2008 were approximately $0.9 million, $1.6 million and $2.4 million respectively, all of which were expensed in the Company's financial statements.

The Company uses trademarks with respect to its products and considers its trademark portfolio as one of its most valuable assets. All of the Company's important trademarks are registered and rigorously enforced.

Environmental

Compliance with federal, state, local, and foreign provisions that have been enacted or adopted regulating the discharge of materials into the environment or otherwise relating to protection of the environment is not expected to have a material effect on the capital expenditures, earnings and competitive position of the Company. Specifically, the Company has taken steps to reduce, control and treat water discharges and air emissions. The Company takes seriously its responsibility to the environment and has embraced renewable energy alternatives and expects to bring on line a new hydro – generation facility at its Athol, MA plant in 2011 to reduce its carbon foot print and energy costs, an investment in excess of $1.0 million.

Strategic Activities

Globalization has had a profound impact on product offerings and buying behaviors of industry and consumers in North America and around the world, forcing the Company to adapt to this new, highly competitive business environment. The Company continuously evaluates most aspects of its business, aiming for new world-class ideas to set itself apart from its competition.

Our strategic concentration is on global brand building and providing unique customer value propositions through technically supported application solutions for our customers. Our job is to recommend and produce the best suited standard product or design and build custom solutions. The combination of the right tool for the right job with value added service will give us a competitive advantage. The Company continues its focus on lean manufacturing, plant consolidations, global sourcing and improved logistics to optimize its value chain.

The execution of these strategic initiatives has expanded the Company's manufacturing and distribution in developing economies which has increased its international sales revenues to 52% of its consolidated sales for fiscal 2010.

On September 21, 2006, the Company sold its Alum Bank, PA level manufacturing plant and relocated the manufacturing to the Dominican Republic, where production began in fiscal 2005. The tape measure production of the Evans Rule Division facilities in Puerto Rico and Charleston, SC has been transferred to the Dominican Republic. The Company vacated and plans to sell its Evans Rule facility in North Charleston, SC. This move has achieved labor savings while satisfying the demands of its customers for lower prices.

The Tru-Stone acquisition in April 2006 represented a strategic acquisition for the Company in that it provides an enhancement of the Company's granite surface plate capabilities. Profit margins for the Company's standard plate business have improved as the Company's existing granite surface plate facility was consolidated into Tru-Stone, where average gross margins have been higher. Along the same lines, the Kinemetric Engineering acquisition in July 2007 represented another strategic acquisition in the field of precision video-based metrology which, when combined with the Company's existing optical projection line, will provide a very comprehensive product offering.

6

SEC Filings and Certifications

The Company makes its public filings with the Securities and Exchange Commission ("SEC"), including its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all exhibits and amendments to these reports, available free of charge at its website, www.starrett.com, as soon as reasonably practicable after the Company files such material with the SEC. Information contained on the Company's website is not part of this Annual Report on Form 10-K.

Item 1A – Risk Factors

SAFE HARBOR STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

This Annual Report on Form 10-K and the Company's 2010 Annual Report to Stockholders, including the President's letter, contains forward-looking statements about the Company's business, competition, sales, gross margins, expenditures, foreign operations, plans for reorganization, interest rate sensitivity, debt service, liquidity and capital resources, and other operating and capital requirements. In addition, forward-looking statements may be included in future Company documents and in oral statements by Company representatives to security analysts and investors. The Company is subject to risks that could cause actual events to vary materially from such forward-looking statements, including the following risk factors:

Risks Related to Financial Reporting: If we or our independent registered public accounting firm are unable to affirm the effectiveness of our internal control over financial reporting in future years, the market value of our common stock could be adversely affected. Our independent registered public accounting firm did audit and report on our internal controls over financial reporting as of June 26, 2010 and June 27, 2009 and identified material weaknesses in our internal controls over financial reporting. Management has implemented three of the five remediation steps outlined in our Annual Report on Form 10-K for fiscal 2009 and will complete the remaining steps before the end of the second quarter of fiscal 2011. Management has developed a plan to remediate the fiscal 2010 material weaknesses in our internal controls over financial reporting, which is outlined in Item 9a of this Annual Report on Form 10-K.

Risks Related to the Economy: The Company's results of operations are materially affected by the conditions in the global economy. As a result of the global economic recession, U.S. and foreign economies have experienced significant declines in employment, household wealth, consumer spending, and lending. Businesses, including the Company and its customers, have faced weakened demand for their products and services, difficulty obtaining access to financing, increased funding costs, and barriers to expanding operations. The Company's results of operations in fiscal 2009 and 2010 have been negatively impacted by the global economic recession; however, business activity has improved for the Company in the second half of fiscal 2010. The Company can provide no assurance that its improvement in the second half of fiscal 2010 will continue and its future results of operations will improve.

Risks Related to Reorganization: The Company continues to evaluate consolidation and reorganization of some of its manufacturing and distribution operations. There can be no assurance that the Company will be successful in these efforts or that any consolidation or reorganization will result in revenue increases or cost savings to the Company. The implementation of these reorganization measures may disrupt the Company's manufacturing and distribution activities, could adversely affect operations, and could result in asset impairment charges and other costs that will be recognized if and when reorganization or restructuring plans are implemented or obligations are incurred.

Risks Related to Technology: Although the Company's strategy includes investment in research and development of new and innovative products to meet technology advances, there can be no assurance that the Company will be successful in competing against new technologies developed by competitors.

7

Risks Related to Foreign Operations: Approximately 52% of the Company's sales and 56% of net assets related to foreign operations for fiscal 2010. Foreign operations are subject to special risks that can materially affect the sales, profits, cash flows and financial position of the Company, including taxes and other restrictions on distributions and payments, currency exchange rate fluctuations, political and economic instability, inflation, minimum capital requirements and exchange controls. The Company's Brazilian operations, which constitute over half of the Company's revenues from foreign operations, can be very volatile, changing from year to year due to the political situation, currency risk and the economy. As a result, the future performance of the Brazilian operations may be difficult to forecast.

Risks Related to Industrial Manufacturing Sector: The market for most of the Company's products is subject to economic conditions affecting the industrial manufacturing sector, including the level of capital spending by industrial companies and the general movement of manufacturing to low cost foreign countries where the Company does not have a substantial market presence. Accordingly, economic weakness in the industrial manufacturing sector may, and in some cases has, resulted in decreased demand for certain of the Company's products, which adversely affects sales and performance. Economic weakness in the consumer market will also adversely impact the Company's performance. In the event that demand for any of the Company's products declines significantly, the Company could be required to recognize certain costs as well as asset impairment charges on long-lived assets related to those products.

Risks Related to Competition: The Company's business is subject to direct and indirect competition from both domestic and foreign firms. In particular, low cost foreign sources have created severe competitive pricing pressures. Under certain circumstances, including significant changes in U.S. and foreign currency relationships, such pricing pressures tend to reduce unit sales and/or adversely affect the Company's margins.

Risks Related to Insurance Coverage: The Company carries liability, property damage, workers' compensation, medical and other insurance policies that management considers adequate for the protection of its assets and operations. There can be no assurance, however, that the coverage limits of such policies will be adequate to cover all claims and losses. Such uncovered claims and losses could have a material adverse effect on the Company. Depending on the risk, deductibles can be as high as 5% of the loss or $500,000.

Risks Related to Raw Material and Energy Costs: Steel is the principal raw material used in the manufacture of the Company's products. The price of steel has historically fluctuated on a cyclical basis and has often depended on a variety of factors over which the Company has no control. The cost of producing the Company's products is also sensitive to the price of energy. The selling prices of the Company's products have not always increased in response to raw material, energy or other cost increases, and the Company is unable to determine to what extent, if any, it will be able to pass future cost increases through to its customers. The Company's inability to pass increased costs through to its customers could materially and adversely affect its financial condition or results of operations.

Risks Related to Stock Market Performance: Currently, the Company's domestic defined benefit pension plan is underfunded. The Company is not required to provide additional funds to the domestic pension fund; however, the future return on pension assets is insufficient to cover future obligations, creating an actuarially underfunded status. This has also occurred for the Company's UK plan, which was underfunded during fiscal 2008, 2009 and 2010.

Risks Related to Acquisitions: Acquisitions, such as the Company's acquisition of Tru-Stone in fiscal 2006 and Kinemetric Engineering in fiscal 2008, involve special risks, including the potential assumption of unanticipated liabilities and contingencies, difficulty in assimilating the operations and personnel of the acquired businesses, disruption of the Company's existing business, dissipation of the Company's limited management resources, and impairment of relationships with employees and customers of the acquired business as a result of changes in ownership and management. While the Company believes that strategic acquisitions can improve its competitiveness and profitability, the failure to successfully integrate and realize the expected benefits of such acquisitions could have an adverse effect on the Company's business, financial condition and operating results.

8

Risks Related to Investor Expectations: The Company's share price remained relatively stable in fiscal 2010 after a significant decline during fiscal 2009. The Company's earnings may not continue to grow at rates similar to the growth rates achieved in recent years and may fall short of either a prior quarter or investors' expectations. If the Company fails to meet the expectations of securities analysts or investors, the Company's share price may decline.

Risks Related to the Company's Credit Facility: Under the Company's credit facility with TD Bank, N.A., the Company is required to comply with certain financial covenants. While the Company believes that it will be able to comply with the financial covenants in future periods, its failure to do so would result in defaults under the credit facility unless the covenants are amended or waived. An event of default under the credit facility, if not waived, could prevent additional borrowing and could result in the acceleration of the Company's indebtedness. This could have an impact on the Company's ability to operate its business.

Risks Related to Information Systems: The efficient operation of the Company's business is dependent on its information systems, including its ability to operate them effectively and to successfully implement new technologies, systems, controls and adequate disaster recovery systems. In addition, the Company must protect the confidentiality of data of its business, employees, customers and other third parties. The failure of the Company's information systems to perform as designed or its failure to implement and operate them effectively could disrupt the Company's business or subject it to liability and thereby harm its profitability. For those reasons, the Company implemented a new Enterprise Resource Planning (ERP) system in its principal North American locations.

Risks Related to Litigation and Changes in Laws, Regulations and Accounting Rules: Various aspects of the Company's operations are subject to federal, state, local or foreign laws, rules and regulations, any of which may change from time to time. Generally accepted accounting principles may change from time to time, as well. In addition, the Company is regularly involved in various litigation matters that arise in the ordinary course of business. Litigation, regulatory developments and changes in accounting rules and principles could adversely affect the Company's business operations and financial performance.

Item 1B – Unresolved Staff Comments

None.

Item 2 - Properties

The Company's principal plant and its corporate headquarters are located in Athol, MA on about 15 acres of Company-owned land. The plant consists of 25 buildings, mostly of brick construction of varying dates, with approximately 535,000 square feet.

The Company's Webber Gage Division in Cleveland, OH, owns and occupies two buildings totaling approximately 50,000 square feet.

The Company-owned facility in Mt. Airy, NC consists of one building totaling approximately 320,000 square feet. It is occupied by the Company's Saw Division, Ground Flat Stock Division and a distribution center. A separate 36,000 square foot building which formerly housed the distribution center was vacated in November 2008 and is currently listed for sale.

The Company's Evans Rule Division owns a 173,000 square foot building in North Charleston, SC. In fiscal 2006, manufacturing operations were moved to a new 50,000 square foot facility in the Dominican Republic from both the North Charleston site and the former Mayaguez, Puerto Rico operations. The Company now occupies a 3,400 square foot leased office in North Charleston for administrative personnel and has the North Charleston property listed for sale.

The Company's subsidiary in Itu, Brazil owns and occupies several buildings totaling 209,000 square feet. The Company's subsidiary in Jedburgh, Scotland owns and occupies a 175,000 square foot building. Two wholly owned subsidiaries in Suzhou and Shanghai (People's Republic of China) lease approximately 41,000 square feet and 5,000 square feet, respectively. The Company signed a lease in fiscal 2009 for a new 133,000 square foot building in Suzhou to accommodate our need for increased manufacturing space. We plan to close the Shanghai distribution center and sales office and consolidate all operations into the new building.

9

In addition, the Company operates warehouses and/or sales-support offices in the U.S., Canada, Australia, New Zealand, Mexico, Germany, Japan, and Argentina.

A warehouse in Glendale, AZ encompassing 35,000 square feet was closed in fiscal 2006 and the building was sold during fiscal 2008.

With the acquisition of Tru-Stone in fiscal 2006, the Company added a 90,000 square foot facility in Waite Park, MN.

With the acquisition of Kinemetric Engineering in fiscal 2008, the Company added a 9,000 square foot leased facility in Laguna Hills, CA, which was expanded to 14,000 square feet.

The Company has vacated a sales office in Kennesaw, GA and has terminated the lease.

In the Company's opinion, all of its property, plants and equipment are in good operating condition, well maintained and adequate for its needs.

Item 3 - Legal Proceedings

The Company is, in the ordinary course of business, from time to time involved in litigation that is not considered material to its financial condition or operations.

Item 4 - Reserved

PART II

Item 5 - Market for the Company's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company's Class A common stock is traded on the New York Stock Exchange. Quarterly dividend and high/low closing market price information is presented in the table below. The Company's Class B common stock is generally nontransferable, except to lineal descendants, and thus has no established trading market, but it can be converted into Class A common stock at any time. The Class B common stock was issued on October 5, 1988, and the Company has paid the same dividends thereon as have been paid on the Class A common stock since that date. On June 26, 2010, there were approximately 1,533 registered holders of Class A common stock and approximately 1,222 registered holders of Class B common stock.

Quarter Ended | Dividends | High | Low | |||||||||

September 2008 | 0.12 | 28.50 | 13.50 | |||||||||

December 2008 | 0.12 | 21.80 | 9.51 | |||||||||

March 2009 | 0.12 | 16.31 | 5.30 | |||||||||

June 2009 | 0.12 | 11.42 | 6.01 | |||||||||

September 2009 | 0.12 | 11.18 | 6.55 | |||||||||

December 2009 | 0.06 | 11.75 | 8.53 | |||||||||

March 2010 | 0.06 | 11.67 | 8.74 | |||||||||

June 2010 | 0.06 | 12.56 | 7.93 | |||||||||

The Company's dividend policy is subject to periodic review by the Board of Directors. Based upon economic conditions, the Board of Directors decided to reduce the quarterly dividend from $0.12 to $0.06 per share effective for the second quarter of fiscal 2010.

ISSUER PURCHASES OF EQUITY SECURITIES

Summary of Stock Repurchases:

10

A summary of the Company's repurchases of shares of its common stock for the fourth quarter fiscal 2010 is as follows:

Period | Shares Purchased | Average Price | Shares Purchased Under Announced Programs | Shares yet to be Purchased Under Announced Programs | ||||||||||

April 2010 | None | – | – | – | ||||||||||

May 2010 | None | – | – | – | ||||||||||

June 2010 | None | – | – | – | ||||||||||

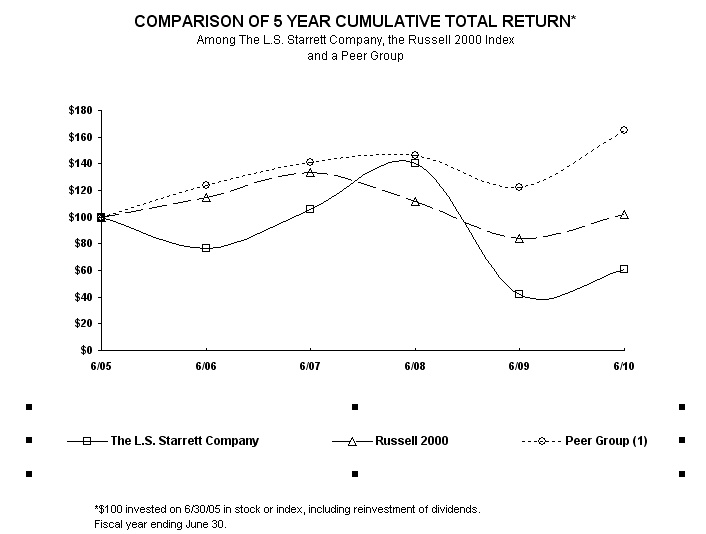

PERFORMANCE GRAPH

The following graph sets forth information comparing the cumulative total return to holders of the Company's Class A common stock over the last five fiscal years with (1) the cumulative total return of the Russell 2000 Index ("Russell 2000") and (2) a peer group index (the "Peer Group") reflecting the cumulative total returns of certain small cap manufacturing companies as described below. The peer group is comprised of the following companies: Acme United, Q.E.P. Co. Inc., Thermadyne Holdings Corp., Badger Meter, Federal Screw Works, National Presto Industries, Regal-Beloit Corp., Tecumseh Products Co., Tennant Company, The Eastern Company and WD-40.

BASE | FY2006 | FY2007 | FY2008 | FY2009 | FY2010 | |||||||||||||||||||

STARRETT | 100.00 | 76.75 | 105.59 | 140.34 | 42.07 | 60.68 | ||||||||||||||||||

RUSSELL 2000 | 100.00 | 114.58 | 133.41 | 111.80 | 83.84 | 101.85 | ||||||||||||||||||

PEER GROUP | 100.00 | 123.81 | 140.68 | 146.22 | 122.59 | 165.10 | ||||||||||||||||||

11

Item 6 - Selected Financial Data

The following selected condensed financial data has been derived from and should be read in conjunction with "Management Discussion and Analysis of Financial Condition and Results of Operations" and our Consolidated Financial Statements and notes thereto, included elsewhere in this report on Form 10K and incorporated herein by reference.

Years ended in June ($000 except per share data) | ||||||||||||||||||||

2010 | 2009 | 2008 | 2007 | 2006 | ||||||||||||||||

Net sales | $ | 203,662 | $ | 203,659 | $ | 242,371 | $ | 222,356 | $ | 200,196 | ||||||||||

Net earnings (loss) | (2,983 | ) | (3,220 | ) | 10,831 | 6,653 | (3,782 | ) | ||||||||||||

Basic earnings (loss) per share | (0.45 | ) | (0.49 | ) | 1.64 | 1.00 | (0.57 | ) | ||||||||||||

Diluted earnings (loss) per share | (0.45 | ) | (0.49 | ) | 1.64 | 1.00 | (0.57 | ) | ||||||||||||

Long-term debt (1) | 706 | 1,264 | 5,834 | 8,520 | 13,054 | |||||||||||||||

Total assets | 200,134 | 194,241 | 250,285 | 234,011 | 228,083 | |||||||||||||||

Dividends per share | 0.30 | 0.48 | 0.52 | 0.40 | 0.40 | |||||||||||||||

(1) | Note the high level of long-term debt in fiscal 2006 is related to the Tru-Stone acquisition. |

Items 7 and 7A- Management's Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosure about Market Risk

RESULTS OF OPERATIONS

Fiscal 2010 Compared to Fiscal 2009

Fiscal 2010 (12 Months North America plus 13 Months International) Compared to Fiscal 2009 (12 Months for North America and International).

As further explained in Note 2 to the consolidated financial statements, in fiscal year 2010 the Company conformed the fiscal year end of its international subsidiaries to that of the Company. Those subsidiaries previously reported on a one-month lag. In order to conform the fiscal periods, the consolidated financial statements include June 2010 results for those subsidiaries in addition to the results for their fiscal year ended May 2010. Management has concluded that the inclusion of this additional month is immaterial to the consolidated financial statements and, in the following comments, has noted those instances where Management believes identifying the impact would be useful in understanding the overall comparison of fiscal 2010 and 2009.

Overview

The Company began to experience the economic downturn in the second quarter of fiscal 2009 and significantly reduced both its manufacturing and selling, general administrative expenses in the third quarter of fiscal 2009. These cost reductions remained in place for one year until the third quarter of fiscal 2010, when an uptick in orders resulted in restoring reduced hours to normal hours for both the factory and office personnel. The economy's cycle created significant problems in managing costs and inventory levels in fiscal 2010 compared to fiscal 2009 as first half fiscal 2010 sales declined $31.0 million or 25% compared to a $31.1 million or 38% increase in the second half. We are cautiously optimistic that the second half trend will continue; however, we will make the necessary adjustments if the economic forecast begins to stagnate.

Net sales for fiscal 2010 remained level with fiscal 2009 at $203.6 million. Under the prior one month lag financial reporting policy, net sales declined $7.3 million or 3.7% from $203.6 million in fiscal 2009 to $196.3 million in fiscal 2010. Gross margins improved $1.5 million from $59.5 million or 29.2% of sales in fiscal 2009 to $61.0 million or 30.0% of sales in fiscal 2010. Selling, general and administrative expenses increased $1.6 million or 2.7% from $59.9 million in fiscal 2009 to $61.5 million in fiscal 2010. Excluding the expenses for the thirteenth month for our international subsidiaries, selling, general and administrative expenses decreased $0.7 million or 1.2%. The operating loss declined $3.4 million largely due to a net decrease of $3.5 million in goodwill and reorganization costs between fiscal 2009 and fiscal 2010.

12

Net Sales

Net sales in North America declined $5.9 million or 5.7% from $102.9 million in fiscal 2009 to $97.0 million in fiscal 2010. With the exception of Tru-Stone, all divisions posted declines as reduced volume from Sears impacting the Evans Rule division and the significant decline in customer capital expenditures adversely affected the demand for Kinemetric's products. International sales increased $5.9 million or 5.9% from $100.7 million in fiscal 2009 to $106.6 million in fiscal 2010. Foreign currency exchange rate fluctuations represented a $4.1 million of the sales gain with a stronger Brazilian Real accounting for $5.2 million and a weaker Pound Sterling posing a $1.1 million decline. Under the prior one month lag financial reporting policy, International sales declined $1.3 million or 1.3% from $100.7 million in fiscal 2009 to $99.4 million in fiscal 2010. Under the new reporting policy, a strong performance in Brazil more than offset revenue declines in Scotland and China. The Company remains cautious the favorable sales trend will continue in fiscal 2011 and is closely monitoring demand from key distributors.

Gross Margin

Gross margin in North America increased $5.3 million or 26% from $20.1 million in fiscal 2009 to $25.4 million in fiscal 2010 and also improved as a percentage of sales from 19.5% in fiscal 2009 to 26.2% in fiscal 2010. Cost reductions and reduced manufacturing hours implemented in February of 2009 coupled with increased volume, particularly in the second half, represented $1.0 million, while inventory reductions resulted in an additional net margin increase of $4.3 million, principally due to changes in the LIFO position. Excluding a $2.0 million inventory obsolescence adjustment related to the Sears' inventory (see Note 8), North American gross margins would have been $27.4 million or 28.2%. International gross margins declined $3.8 million or 9.6% from $39.4 million in fiscal 2009 to $35.6 million in fiscal 2010 and deteriorated as a percentage of sales from 39.1% in fiscal 2009 to 33.4% in fiscal 2010. Higher fixed manufacturing overhead was the prime factor influencing the gross margin decline; however, foreign exchange represented a $1.5 million improvement in gross margin in U. S. dollars resulting in a $5.3 million erosion in constant dollars. Under the prior one month lag reporting policy, gross margins declined $5.9 million to 33.3% of sales in fiscal 2010 compared to fiscal 2009.

Selling, General & Administrative Expenses

Selling, general and administrative expenses increased $1.6 million or 2.7% from $59.9 million in fiscal 2009 to $61.5 million in fiscal 2010. Under the prior one month lag financial reporting policy, selling, general and administrative expenses declined $0.7 million or 1.2%. On a twelve month basis, North American expenses increased $1.0 million or 3.2% as reduced salaries, travel and advertising costs were more than offset by higher pension expenses and the first year amortization of the new ERP system. On a thirteen month basis, International expenses increased $0.6 million or 2.0%, however, on a comparable twelve month basis, expenses declined $1.7 million or 5.9%. Higher salaries and benefits that were partially offset by lower management bonuses accounted for the majority of the $0.6 million thirteen month increase.

Operating Loss

The operating loss before goodwill impairment and reorganization costs increased $0.1 million from $0.4 million in fiscal 2009 to $0.5 million in fiscal 2010 as the increase in gross margins of $1.5 million was offset by a $1.6 million increase in selling, general and administrative expenses.

Significant Fourth Quarter Activity

As shown in Note 15, the Company recorded a $0.3 million profit in the fourth quarter of fiscal 2010. Consolidated sales of $63.9 million were an increase of $25.1 million or 65% over fiscal 2009. North America and International contributed $6.0 and $19.0 million, respectively. Under the prior one month lag financial reporting policy, sales increased $17.7 million or 46%. Operating income, excluding the Evans inventory and fixed asset and Kinemetric goodwill adjustments, improved to a $3.6 million profit compared to $2.9 million loss in fiscal 2009. The Evans inventory and fixed assets adjustments are described in Note 8 and the Kinemetric goodwill adjustment is described in Note 5.

13

Income Taxes

The effective tax rate was (40.4)% for fiscal 2010. The rate reflects a combined federal, state and foreign adjustment for permanent book/tax differences, the most significant of which relate to the Brazilian audit settlement and the losses not benefitted in China and the Dominican Republic, as described in Note 10.

The effective rate for 2009 was 42%. The change in the effective rate percentage from fiscal 2009 to fiscal 2010 reflects the impact of a lower loss compared to 2009 and higher permanent book/tax differences related to uncertain tax positions, the Brazilian audit settlement and the foreign losses not benefited which adjusted taxable income from ($0.7) million to $0.8 million.

There were no significant changes in valuation allowances relating to carryforwards for foreign NOL's, foreign tax credits and certain state NOL's other than for reversal relating to realization of NOL benefits for certain foreign subsidiaries. The Company continues to believe that it is more likely than not that it will be able to utilize its tax operating loss carryforward assets of approximately $11.5 million reflected on the Balance Sheet.

Fiscal 2009 Compared to Fiscal 2008

Overview The Company is engaged in the business of manufacturing over 5,000 different products for industrial, professional and consumer markets. As a global manufacturer with major subsidiaries in Brazil, Scotland, and China, the Company offers a broad array of products to the market through multiple channels of distribution globally. Net sales decreased 16% in fiscal 2009 compared to fiscal 2008. The Company continued to experience the severity of the global economic recession during the most recent quarter. The severe decline is due to the unprecedented slowdown in the global economy and the rapid strengthening of the U.S. dollar. This is a direct reflection of the financial market crisis, lack of liquidity and weak consumer confidence. The resultant effect has been a massive de-stocking throughout the supply chain which caused the most significant drop in Company sales in the third quarter ending March 28, 2009 in the past thirty years. Historically, the Company has lagged the economy and we expect the current harsh economic realities will be with the Company for the balance of this calendar year. For fiscal 2009, the Company incurred a net loss of $3.2 million, or $(0.49) per basic and diluted share compared to a net income of $10.8 million or $1.64 per basic and diluted share for fiscal 2008. This represents a decrease of $14.0 million comprised of a decrease in gross margin of $16.7 million, the aforementioned goodwill charge of $5.3 million, a decrease of $3.3 million in other income (expense) offset by a decrease of $2.8 million in selling, general and administrative costs and a decrease in income tax expense of $8.4 million from a $6.1 million provision in fiscal 2008 to a $2.3 million benefit in fiscal 2009. The above items are discussed below.

Net Sales Net sales for fiscal 2009 were down $38.7 million or 16% compared to fiscal 2008. North American sales decreased $27.7 million or 21%, reflecting declining U.S. demand partly caused by the widening of the recession in the manufacturing sector, decreased sales in Canada and Mexico, and lower Evans Rule sales. The declines are primarily related to unit volume declines. The impact of any price concessions and new product sales was not material. It is likely that the Company's results will continue to be impacted by the current global economic recession. Foreign sales (excluding North America) decreased 9.9% (1% increase in local currency), driven by the weakening of the Brazilian Real, British Pound, Euro, and Australian Dollar against the U.S. dollar, offset by a growth in Chinese operations ($0.4 million increase). Beyond exchange rate effects, the declines were mainly related to unit volume declines relative to the global economic collapse.

14

Earnings (loss) before taxes (benefit) The pre-tax loss for fiscal 2009 was $5.6 million, which includes $5.3 million impairment charge for goodwill, compared to pre-tax earnings of $16.9 million for fiscal 2008. This represents a decrease of pre-tax earnings of $22.4 million. This is comprised of a decrease in gross margin of $16.7 million and a decrease of $3.3 million in other income offset by a decrease in selling, general and administrative costs of $2.8 million. The decrease in gross margin is primarily attributable to the overall decline in sales from fiscal 2008 to fiscal 2009 ($10.5 million gross margin effect). The gross margin percentage decreased from 31.5% in fiscal 2008 to 29.2% in fiscal 2009. This was primarily driven by lower overhead absorption at certain domestic plants due to lower sales volumes ($4.5 million effect). Similarly, lower absorption at foreign plants due to lower sales volumes caused a $.2 million decline. This was compounded by certain material cost increases that could not be fully passed on to customers. LIFO liquidations in fiscal 2009 had an offsetting effect of $1.8 million. LIFO liquidations in fiscal 2008 were not considered material. Gross margins for fiscal 2010 could again be adversely impacted by lower absorption rates and material cost increases, which cannot be fully passed on to customers and by increased competitive pressures in various markets. As indicated above, selling, general and administrative costs decreased $2.8 million, although the percentage of sales increased from 25.9% in fiscal 2008 to 29.4% in fiscal 2009. The dollar decrease is a result of decreased sales commissions, profit sharing and bonuses ($1.9 million), decreases in marketing and advertising ($.4 million), a decrease in shipping costs ($.4 million), offset by increases in severance cost ($.7 million) and the bad debt provision ($0.3 million). The decrease in other income (expense) is comprised of a decrease in net interest income ($.7 million), decreased net exchange gains ($.4 million) and the gain on the sale of the Glendale, AZ facility ($1.7 million) in fiscal 2008. The Company currently includes the Evans North Charleston building and a building in Mount Airy, NC on the June 27, 2009 Balance Sheet as assets held for sale of $2.8 million. The Company expects to sell both buildings for a gain based on a recent appraisal.

In response to the downturn in sales volume, the Company has reduced spending on raw materials and indirect production costs. The Company has also cut salaries at certain locations by 10% and has reduced hourly labor costs through shortened work weeks, layoffs and attrition. These reductions are done with careful consideration so as not to compromise customer service levels or the retention of key employees. This is having an approximate $2.0 million impact per quarter on cost of sales and selling, general and administrative costs. In addition, layoffs instituted in April 2009 at certain domestic locations, are having an approximate $1.1 million impact per quarter on cost of sales and selling, general and administrative costs. Finally, a reduction in labor force in Brazil is expected to have a $0.2 million impact per quarter. This is in addition to temporary salary cuts in Brazil taking place over the next 6 months for a savings of $.4 million. Although the Company's recent order activity is down compared to historical levels, this decline is spread relatively proportionately across most of our customers. The Company fully expects order activity to rebound once the supply chain de-stocking abates and excess inventory levels at the Company's distributors are depleted. The Company does not anticipate any liquidity constraints given the adequacy of its working capital and its available credit line. See further discussion under Liquidity and Capital Resources.

FINANCIAL INSTRUMENT MARKET RISK

Market risk is the potential change in a financial instrument's value caused by fluctuations in interest and currency exchange rates, and equity and commodity prices. The Company's operating activities expose it to risks that are continually monitored, evaluated and managed. Proper management of these risks helps reduce the likelihood of earnings volatility.

As of June 26, 2010, the Company held $1.25 million in AAA-rated debt obligations for which there were current active quoted market prices.

The Company does not engage in tracking, market-making or other speculative activities in derivatives markets. The Company does not enter into long-term supply contracts with either fixed prices or quantities. The Company engages in a limited amount of hedging activity to minimize the impact of foreign currency fluctuations. Net foreign monetary assets are approximately $16 million as of June 26, 2010.

15

A 10% change in interest rates would not have a significant impact on the aggregate net fair value of the Company's interest rate sensitive financial instruments or the cash flows or future earnings associated with those financial instruments. A 10% change in interest rates would impact the fair value of the Company's fixed rate investments of approximately $1.3 million by an immaterial amount. See Note 12 to the Consolidated Financial Statements for details concerning the Company's long-term debt outstanding of $0.7 million.

LIQUIDITY AND CAPITAL RESOURCES

Years ended in June ($000) | ||||||||||||

2010 | 2009 | 2008 | ||||||||||

Cash provided by operations | $ | 29,458 | $ | 659 | $ | 19,012 | ||||||

Cash provided by (used in) investing activities | (8,761 | ) | 5,469 | (13,584 | ) | |||||||

Cash (used in) financing activities | (9,994 | ) | (1,298 | ) | (6,851 | ) | ||||||

The Company has a working capital ratio of 4.3 in fiscal 2010 and 4.4 in fiscal 2009. Cash, investments, accounts receivable and inventory represent 92% and 88% of current assets in fiscal 2010 and fiscal 2009, respectively. The Company had accounts receivable turnover of 6.7 in fiscal 2010 compared to 6.1 in fiscal 2009 and an inventory turnover ratio of 2.7 in fiscal 2010 compared to 2.4 in fiscal 2009.

Net cash increased $10.2 million as the Company adjusted to the economic environment by adjusting inventory to reduced sales, postponing capital expenditures and reducing debt.

Net cash provided by operations of $29.5 million was primarily the result of a $15.9 million inventory reduction program implemented in the third quarter of fiscal 2009 and $12.0 million of non-cash costs for depreciation, amortization and impairment.

The Company invested $9.3 million in fiscal 2010, principally in equipment and the new ERP system, which was partially offset by a $0.6 decrease in investments resulting in $8.8 million of net investments.

The Company reduced short–term debt by $7.5 million and distributed $2.0 million in dividends representing $9.5 million of the $10.0 million of financing activities.

Effects of translation rate changes on cash primarily result from the movement of the U.S. dollar against the British Pound, the Euro and the Brazilian Real. The Company uses a limited number of forward contracts to hedge some of this activity and a natural hedge strategy of paying for foreign purchases in local currency when economically advantageous.

Liquidity and Credit Arrangements

The Company believes it maintains sufficient liquidity and has the resources to fund its operations in the near term. In addition to its cash and investments, the Company has maintained a $23.0 million line of credit, of which, $0.975 million is reserved for letters of credit and $1.7 was outstanding as of June 26, 2010. The Company has a working capital ratio of 4.3 to one as of June 26, 2010 and 4.4 to one as of June 27, 2009.

On June 30, 2009, The L.S. Starrett Company (the "Company") and certain subsidiaries of the Company subsidiaries (the "Subsidiaries") entered into a Loan and Security Agreement (the "New Credit Facility") with TD Bank, N.A., as lender.

The New Credit Facility replaced the Company's previous Bank of America facility with a $23.0 million line of credit. On June 30, 2009, the Company utilized this line of credit to pay off the remaining balances on the Reducing Revolver and Line of Credit. The interest rate under the New Credit Facility is based upon a grid which uses the ratio of Funded Debt/EBITDA to determine the floating margin that will be added to one-month LIBOR. The initial rate is one-month LIBOR plus 1.75%. The New Credit Facility matures on April 30, 2012.

16

The obligations under the New Credit Facility are unsecured. However, in the event of certain triggering events, the obligations under the New Credit Facility will become secured by the assets of the Company and the subsidiaries party to the New Credit Facility.

Availability under the New Credit Facility is subject to a borrowing base comprised of accounts receivable and inventory. The Company believes that the borrowing base will consistently produce availability under the New Credit Facility in excess of $23.0 million. In addition, the Company anticipates that it will not need to fully utilize the amounts available to the Company and its subsidiaries under the New Credit Facility. As of August 31, 2010, the Company had borrowings of $2.6 million under the New Credit Facility.

The New Credit Facility contains financial covenants with respect to leverage, tangible net worth, and interest coverage, and also contains customary affirmative and negative covenants, including limitations on indebtedness, liens, acquisitions, asset dispositions, and fundamental corporate changes, and certain customary events of default. Upon the occurrence and continuation of an event of default, the lender may terminate the revolving credit commitment and require immediate payment of the entire unpaid principal amount of the New Credit Facility, accrued interest and all other obligations. As of June 26, 2010, the Company was in compliance with the financial covenants required for testing at that time under the New Credit Facility; however, certain procedural covenants were not in compliance. The bank has issued a waiver for the lapse in these procedural covenants, related to delays in providing accounts receivable and inventory reports impacted by the conversion to the new ERP system.

OFF-BALANCE SHEET ARRANGEMENTS

The Company does not have any material off-balance sheet arrangements as defined under the Securities and Exchange Commission rules.

CRITICAL ACCOUNTING POLICIES and ESTIMATES

The preparation of financial statements and related disclosures in conformity with accounting principles generally accepted in the United States of America requires management to make judgments, assumptions and estimates that affect the amounts reported in the consolidated financial statements and accompanying notes. The second footnote to the Company's Consolidated Financial Statements describes the significant accounting policies and methods used in the preparation of the consolidated financial statements.

Judgments, assumptions, and estimates are used for, but not limited to, the allowance for doubtful accounts receivable and returned goods; inventory allowances; income tax reserves; employee turnover, discount, and return rates used to calculate pension obligations.

Future events and their effects cannot be determined with absolute certainty. Therefore, the determination of estimates requires the exercise of judgment. Actual results inevitably will differ from those estimates, and such differences may be material to the Company's Consolidated Financial Statements. The following sections describe the Company's critical accounting policies.

Revenue recognition : Sales of merchandise and freight billed to customers are recognized when products are delivered, title and risk of loss has passed to the customer, no significant post delivery obligations remain and collection of the resulting receivable is reasonably assured. Sales are net of provisions for cash discounts, returns, customer discounts (such as volume or trade discounts), cooperative advertising and other sales related discounts. Cooperative advertising payments made to customers are included as advertising expense in selling, general and administrative in the Consolidated Statements of Operations. While the Company does allow its customers the right to return in certain circumstances, revenue is not deferred, but rather a reserve for sales returns is provided based on experience, which historically has not been significant.

The allowance for doubtful accounts of $0.6 million and $0.7 million at the end of fiscal 2010 and 2009, respectively, is based on our assessment of the collectability of specific customer accounts and the aging of our accounts receivable. While the Company believes that the allowance for doubtful accounts is adequate, if there is a deterioration of a major customer's credit worthiness, actual defaults are higher than our previous experience, or actual future returns do not reflect historical trends, the estimates of the recoverability of the amounts due the Company and sales could be adversely affected.

17

Inventory purchases and commitments are based upon future demand forecasts. If there is a sudden and significant decrease in demand for our products or there is a higher risk of inventory obsolescence because of rapidly changing technology and requirements, the Company may be required to increase the inventory reserve and, as a result, gross profit margin could be adversely affected.

The Company values property, plant and equipment (PP&E) at historical cost less accumulated depreciation. Impairment losses are recorded when indicators of impairment, such as plant closures, are present and the undiscounted cash flows estimated to be generated by those assets are less than the carrying amount. The Company continually reviews for such impairment and believes that PP&E is being carried at its appropriate value.

The Company assesses the fair value of its goodwill generally based upon a discounted cash flow methodology. The discounted cash flows are estimated utilizing various assumptions regarding future revenue and expenses, working capital, terminal value, and market discount rates. If the carrying amount of the goodwill is greater than the fair value, an impairment charge is recognized to the extent the recorded goodwill exceeds the implied fair value of goodwill.

Accounting for income taxes requires estimates of future benefits and tax liabilities. Due to temporary differences in the timing of recognition of items included in income for accounting and tax purposes, deferred tax assets or liabilities are recorded to reflect the impact arising from these differences on future tax payments. With respect to recorded tax assets, the Company assesses the likelihood that the asset will be realized. If realization is in doubt because of uncertainty regarding future profitability or enacted tax rates, the Company provides a valuation allowance related to the asset. Should any significant changes in the tax law or the estimate of the necessary valuation allowance occur, the Company would record the impact of the change, which could have a material effect on our financial position or results of operations.

Pension and postretirement medical costs and obligations are dependent on assumptions used by actuaries in calculating such amounts. These assumptions include discount rates, healthcare cost trends, inflation, salary growth, long-term return on plan assets, employee turnover rates, retirement rates, mortality and other factors. These assumptions are made based on a combination of external market factors, actual historical experience, long-term trend analysis, and an analysis of the assumptions being used by other companies with similar plans. Actual results that differ from assumptions are accumulated and amortized over future periods. Significant differences in actual experience or significant changes in assumptions would affect pension and other postretirement benefit costs and obligations. See also Employee Benefit Plans (Note 11 to the Consolidated Financial Statements).

CONTRACTUAL OBLIGATIONS

The following table summarizes future estimated payment obligations by period. The majority of the obligations represent commitments for production needs in the normal course of business.

Payments due by period (in millions) | ||||||||||||||||||||

Total | <1yr. | 1-3yrs. | 3-5yrs. | >5yrs. | ||||||||||||||||

Post-retirement benefit obligations | $ | 7.4 | $ | 0.7 | $ | 1.4 | $ | 1.4 | $ | 3.9 | ||||||||||

Long-term debt obligations | 0.7 | - | 0.7 | - | - | |||||||||||||||

Capital lease obligations | 1.6 | 0.9 | 0.3 | 0.3 | 0.1 | |||||||||||||||

Operating lease obligations | 3.7 | 1.4 | 1.7 | 0.6 | - | |||||||||||||||

Purchase obligations | 11.0 | 9.9 | 1.0 | - | 0.1 | |||||||||||||||

Investment in Supplier | 1.3 | 1.2 | 0.1 | |||||||||||||||||

Total | $ | 25.7 | $ | 14.1 | $ | 5.2 | $ | 2.3 | $ | 4.1 | ||||||||||

18

It is assumed that post-retirement benefit obligations would continue on an annual basis from 2013 to 2016. Total future payments for other obligations cannot be reasonably estimated beyond year 5.

ANNUAL NYSE CEO CERTIFICATION AND SARBANES-OXLEY SECTION 302 CERTIFICATIONS

In fiscal 2010, the Company submitted an unqualified "Annual CEO Certification" to the New York Stock Exchange as required by Section 303A.12(a) of the New York Stock Exchange Listed Company Manual. Further, the Company is filing with the Securities and Exchange Commission the certifications required by Section 302 of the Sarbanes-Oxley Act of 2002 as exhibits to the Company's Annual Report on Form 10-K.

Item 8 - Financial Statements and Supplementary Data

Contents: |

|

Page |

Report of Independent Registered Public Accounting Firm |

| 20 |

Consolidated Balance Sheets |

| 21 |

Consolidated Statements of Operations |

| 22 |

Consolidated Statements of Cash Flows |

| 23 |

Consolidated Statements of Stockholders' Equity |

| 24 |

Notes to Consolidated Financial Statements |

| 25-44 |

19

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of

The L.S. Starrett Company

We have audited the accompanying consolidated balance sheets of The L.S. Starrett Company and subsidiaries ("the Company") as of June 26, 2010 and June 27, 2009, and the related consolidated statements of operations, stockholders' equity, and cash flows for each of the three years in the period ended June 26, 2010. Our audits of the basic financial statements included the financial statement schedule listed in the index appearing under Item 15(a)(2). These consolidated financial statements and financial statement schedule are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements and financial statement schedule based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of The L.S. Starrett Company and subsidiaries as of June 26, 2010 and June 27, 2009, and the results of their operations and their cash flows for each of the three years in the period ended June 26, 2010 in conformity with accounting principles generally accepted in the United States of America. Also in our opinion, the related financial statement schedule, when considered in relation to the basic financial statements taken as a whole, presents fairly, in all material respects, the information set forth therein.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), The L.S. Starrett Company's internal control over financial reporting as of June 26, 2010, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) and our accompanying report dated September 20, 2010 expressed an adverse opinion on the effectiveness of the Company's internal control over financial reporting.

/s/ Grant Thornton LLP

Boston, Massachusetts

September 20, 2010

20

THE L.S. STARRETT COMPANY

Consolidated Balance Sheets

(in thousands except share data)

June 26, 2010 | June 27, 2009 | |||||||

ASSETS | ||||||||

Current assets: | ||||||||

Cash (Note 4) | $ | 20,478 | $ | 10,248 | ||||

Investments (Note 4) | 1,250 | 1,791 | ||||||

Accounts receivable (less allowance for doubtful accounts of $607 and $678, respectively) | 33,707 | 27,233 | ||||||

Inventories: | ||||||||

Raw materials and supplies | 14,939 | 19,672 | ||||||

Goods in process and finished parts | 16,794 | 20,265 | ||||||

Finished goods | 14,423 | 20,289 | ||||||

Total inventories | 46,156 | 60,226 | ||||||

Current deferred income tax asset (Note 10) | 3,300 | 5,170 | ||||||

Prepaid expenses and other current assets | 5,510 | 8,054 | ||||||

Total current assets | 110,401 | 112,722 | ||||||

Property, plant and equipment, net (Note 7) | 56,529 | 56,956 | ||||||

Property held for sale (Note 7) | 2,699 | 2,771 | ||||||

Intangible assets, net (Note 5) | 1,303 | 2,517 | ||||||

Goodwill (Note 5) | - | 981 | ||||||

Other assets | 280 | 275 | ||||||

Long-term taxes receivable (Note 10) | 2,807 | 2,807 | ||||||

Long-term deferred income tax asset, net (Note 10) | 26,115 | 15,212 | ||||||

Total assets | $ | 200,134 | $ | 194,241 | ||||

LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

Current liabilities: | ||||||||

Notes payable and current maturities (Note 12) | $ | 2,696 | $ | 10,136 | ||||

Accounts payable and accrued expenses | 17,740 | 10,369 | ||||||

Accrued salaries and wages | 5,037 | 5,109 | ||||||

Total current liabilities | 25,473 | 25,614 | ||||||

Long-term taxes payable (Note 10) | 9,132 | 9,140 | ||||||

Deferred income taxes (Note 10) | 2,436 | - | ||||||

Long-term debt (Note 12) | 706 | 1,264 | ||||||

Postretirement benefit and pension liability (Note 11) | 30,005 | 15,345 | ||||||

Total liabilities | 67,752 | 51,363 | ||||||

Contingencies (Note 14) | ||||||||

Stockholders' equity: | ||||||||

Class A common stock $1 par (20,000,000 shrs. auth.; 5,858,700 outstanding at June 26, 2010, 5,769,894 outstanding at June 27, 2009) | 5,859 | 5,770 | ||||||

Class B common stock $1 par (10,000,000 shrs. auth.; 821,204 outstanding at June 26, 2010, 869,426 outstanding at June 27, 2009) | 821 | 869 | ||||||

Additional paid-in capital | 50,373 | 49,984 | ||||||

Retained earnings reinvested and employed in the business | 122,724 | 127,707 | ||||||

Accumulated other comprehensive loss | (47,395 | ) | (41,452 | ) | ||||

Total stockholders' equity | 132,382 | 142,878 | ||||||

Total liabilities and stockholders' equity | $ | 200,134 | $ | 194,241 | ||||

See notes to consolidated financial statements

21

THE L.S. STARRETT COMPANY

Consolidated Statements of Operations

For the three years ended June 26, 2010

(in thousands of dollars except per share data)

6/26/10 | 6/27/09 | 6/28/08 | ||||||||||

(52 weeks) | (52 weeks) | (52 weeks) | ||||||||||

Net sales | $ | 203,662 | $ | 203,659 | $ | 242,371 | ||||||

Cost of goods sold | 142,660 | 144,115 | 166,133 | |||||||||

Gross margin | 61,002 | 59,544 | 76,238 | |||||||||

% of net sales | 30.0 | % | 29.2 | % | 31.5 | % | ||||||

Selling, general and administrative expenses | 61,525 | 59,904 | 62,707 | |||||||||

Goodwill impairment (Note 5) | 1,091 | 5,260 | - | |||||||||

Reorganization costs | 616 | - | - | |||||||||

Operating (loss)/income | (2,230 | ) | (5,620 | ) | 13,531 | |||||||

Other income (expense) | 105 | 67 | 3,340 | |||||||||

(Loss) earnings before income taxes | (2,125 | ) | (5,553 | ) | 16,871 | |||||||

Income tax expense/(benefit) | 858 | (2,333 | ) | 6,040 | ||||||||

Net (loss) earnings | $ | (2,983 | ) | $ | (3,220 | ) | $ | 10,831 | ||||

Basic and diluted (loss) earnings per share | $ | (0.45 | ) | $ | (0.49 | ) | $ | 1.64 | ||||

Average outstanding shares used in per share calculations (in thousands): | ||||||||||||

Basic | 6,667 | 6,622 | 6,596 | |||||||||

Diluted | 6,667 | 6,622 | 6,605 | |||||||||

Dividends per share | $ | 0.30 | $ | 0.48 | $ | 0.52 | ||||||

See notes to consolidated financial statements

22

THE L. S. STARRETT COMPANY

For the three years ended June 26, 2010

Consolidated Statements of Cash Flows

(in thousands of dollars)

6/26/10 | 6/27/09 | 6/28/08 | ||||||||||

(52 weeks) | (52 weeks) | (52 weeks) | ||||||||||

Cash flows from operating activities: | ||||||||||||

Net (loss) income | $ | (2,983 | ) | $ | (3,220 | ) | $ | 10,831 | ||||

Noncash operating activities: | ||||||||||||

Gain from sale of real estate | - | - | (1,703 | ) | ||||||||

Depreciation | 10,035 | 8,649 | 9,535 | |||||||||

Amortization | 1,214 | 1,247 | 1,240 | |||||||||

Impairment of fixed assets | 747 | 52 | 95 | |||||||||

Goodwill impairment | 1,091 | 5,260 | - | |||||||||

Net long-term tax payable | (215 | ) | 604 | 847 | ||||||||

Deferred taxes | (3,795 | ) | (6,145 | ) | 1,221 | |||||||

Unrealized transaction (gains)/ losses | (247 | ) | 1,077 | (990 | ) | |||||||

Retirement benefits | 2,669 | (2,088 | ) | (3,332 | ) | |||||||

Working capital changes: | ||||||||||||

Receivables | (6,883 | ) | 7,170 | 893 | ||||||||

Inventories | 15,903 | (4,233 | ) | (45 | ) | |||||||

Other current assets | 2,979 | (2,759 | ) | (157 | ) | |||||||

Other current liabilities | 7,951 | (7,313 | ) | 478 | ||||||||

Prepaid pension cost and other | 992 | 2,358 | 99 | |||||||||

Net cash provided by operating activities | 29,458 | 659 | 19,012 | |||||||||

Cash flows from investing activities: | ||||||||||||

Purchase of Kinemetric Engineering | (110 | ) | (208 | ) | (2,060 | ) | ||||||

Additions to plant and equipment | (9,266 | ) | (9,443 | ) | (8,924 | ) | ||||||

(Increase) decrease in investments | 615 | 15,120 | (5,016 | ) | ||||||||

Proceeds from sale of real estate | - | - | 2,416 | |||||||||

Net cash provided by (used in) investing activities | (8,761 | ) | 5,469 | (13,584 | ) | |||||||

Cash flows from financing activities: | ||||||||||||

Proceeds from short-term borrowings | 14,040 | 29,518 | 5,007 | |||||||||

Short-term debt repayments | (21,506 | ) | (28,603 | ) | (5,800 | ) | ||||||

Proceeds from long-term borrowings | 129 | 1,188 | - | |||||||||

Long-term debt repayments | (1,019 | ) | (552 | ) | (2,929 | ) | ||||||

Common stock issued | 362 | 596 | 620 | |||||||||

Treasury shares purchased | - | (263 | ) | (317 | ) | |||||||

Dividends | (2,000 | ) | (3,182 | ) | (3,432 | ) | ||||||

Net cash used in financing activities | (9,994 | ) | (1,298 | ) | (6,851 | ) | ||||||

Effect of translation rate changes on cash | (473 | ) | (1,097 | ) | 230 | |||||||

Net increase (decrease) in cash | 10,230 | 3,733 | (1,193 | ) | ||||||||

Cash beginning of year | 10,248 | 6,515 | 7,708 | |||||||||

Cash end of year | $ | 20,478 | $ | 10,248 | $ | 6,515 | ||||||

Supplemental cash flow information: | ||||||||||||

Interest received | $ | 964 | $ | 1,037 | $ | 1,648 | ||||||

Interest paid | 1,449 | 1,127 | 914 | |||||||||

Taxes paid, net | 1,402 | 3,663 | 3,546 | |||||||||

See notes to consolidated financial statements

23

THE L.S. STARRETT COMPANY

For the three years ended June 26, 2010

Consolidated Statements of Stockholders' Equity

Common Stock Out-standing ($1 Par) | Addi- tional Paid-in | Retained | Accumulated Other Com- | |||||||||||||||||||||

Class A | Class B | Capital | Earnings | prehensive Loss | Total | |||||||||||||||||||

Balance, June 30, 2007 | $ | 5,632 | $ | 963 | $ | 49,282 | $ | 127,023 | $ | (5,786 | ) | $ | 177,114 | |||||||||||

Comprehensive income: | ||||||||||||||||||||||||

Net income | 10,831 | 10,831 | ||||||||||||||||||||||

Unrealized net loss on investments and swap agreement | (281 | ) | (281 | ) | ||||||||||||||||||||

Minimum pension liability, net | (4,911 | ) | (4,911 | ) | ||||||||||||||||||||

Translation gain, net | 7,415 | 7,415 | ||||||||||||||||||||||

Total comprehensive income | 13,054 | |||||||||||||||||||||||

Tax adjustment for uncertain tax positions | (313 | ) | (313 | ) | ||||||||||||||||||||

Dividends ($0.52 per share) | (3,432 | ) | (3,432 | ) | ||||||||||||||||||||

Treasury shares: | ||||||||||||||||||||||||

Purchased | (20 | ) | – | (297 | ) | (317 | ) | |||||||||||||||||

Issued | 24 | – | 394 | 418 | ||||||||||||||||||||

Issuance of stock under ESPP | – | 15 | 234 | 249 | ||||||||||||||||||||

Conversion | 72 | (72 | ) | – | ||||||||||||||||||||

Balance, June 28, 2008 | $ | 5,708 | $ | 906 | $ | 49,613 | $ | 134,109 | $ | (3,563 | ) | $ | 186,773 | |||||||||||

Comprehensive loss: | ||||||||||||||||||||||||