UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2017

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

Commission File Number 1-11758

(Exact Name of Registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 1585 Broadway New York, NY 10036 (Address of principal executive offices, including zip code) | 36-3145972 (I.R.S. Employer Identification No.) | (212) 761-4000 (Registrant's telephone number, including area code) |

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer ☒ | Accelerated Filer ☐ | |

Non-Accelerated Filer ☐ | Smaller reporting company ☐ | |

(Do not check if a smaller reporting company) | Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of October 31, 2017, there were 1,807,899,161 shares of the Registrant's Common Stock, par value $0.01 per share, outstanding.

QUARTERLY REPORT ON FORM 10-Q

For the quarter ended September 30, 2017

| Table of Contents | Part | Item | Page | |||||

Financial Information | I | 1 | ||||||

Management's Discussion and Analysis of Financial Condition and Results of Operations | 2 | 1 | ||||||

Introduction | 1 | |||||||

Executive Summary | 2 | |||||||

Business Segments | 7 | |||||||

Supplemental Financial Information and Disclosures | 18 | |||||||

Accounting Development Updates | 18 | |||||||

Critical Accounting Policies | 19 | |||||||

Liquidity and Capital Resources | 19 | |||||||

Quantitative and Qualitative Disclosures about Market Risk | 3 | 32 | ||||||

Controls and Procedures | 4 | 42 | ||||||

Report of Independent Registered Public Accounting Firm | 43 | |||||||

Financial Statements | 1 | 44 | ||||||

Consolidated Financial Statements and Notes | 44 | |||||||

Consolidated Income Statements (Unaudited) | 44 | |||||||

Consolidated Comprehensive Income Statements (Unaudited) | 45 | |||||||

Consolidated Balance Sheets (Unaudited at September 30, 2017) | 46 | |||||||

Consolidated Statements of Changes in Total Equity (Unaudited) | 47 | |||||||

Consolidated Cash Flow Statements (Unaudited) | 48 | |||||||

Notes to Consolidated Financial Statements (Unaudited) | 49 | |||||||

1. Introduction and Basis of Presentation | 49 | |||||||

2. Significant Accounting Policies | 50 | |||||||

3. Fair Values | 51 | |||||||

4. Derivative Instruments and Hedging Activities | 63 | |||||||

5. Investment Securities | 67 | |||||||

6. Collateralized Transactions | 70 | |||||||

7. Loans and Allowance for Credit Losses | 72 | |||||||

8. Equity Method Investments | 75 | |||||||

9. Deposits | 75 | |||||||

10. Long-Term Borrowings and Other Secured Financings | 75 | |||||||

11. Commitments, Guarantees and Contingencies | 76 | |||||||

12. Variable Interest Entities and Securitization Activities | 80 | |||||||

13. Regulatory Requirements | 83 | |||||||

14. Total Equity | 86 | |||||||

15. Earnings per Common Share | 88 | |||||||

16. Interest Income and Interest Expense | 88 | |||||||

17. Employee Benefit Plans | 89 | |||||||

18. Income Taxes | 89 | |||||||

19. Segment and Geographic Information | 89 | |||||||

20. Subsequent Events | 91 | |||||||

Financial Data Supplement (Unaudited) | 92 | |||||||

Other Information | II | 95 | ||||||

Legal Proceedings | 1 | 95 | ||||||

Unregistered Sales of Equity Securities and Use of Proceeds | 2 | 96 | ||||||

Exhibits | 6 | 96 | ||||||

Exhibit Index | E-1 | |||||||

Signatures |

|

S-1 |

| |||||

i

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the U.S. Securities and Exchange Commission (the "SEC"). You may read and copy any document we file with the SEC at the SEC's public reference room at 100 F Street, NE, Washington, DC 20549. Please call the SEC at 1-800-SEC-0330 for information on the public reference room. The SEC maintains an internet site, www.sec.gov , that contains annual, quarterly and current reports, proxy and information statements and other information that issuers file electronically with the SEC. Our electronic SEC filings are available to the public at the SEC's internet site.

Our internet site is www.morganstanley.com . You can access our Investor Relations webpage at www.morganstanley.com/about-us-ir . We make available free of charge, on or through our Investor Relations webpage, our Proxy Statements, Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to the Securities Exchange Act of 1934, as amended (the "Exchange Act"), as soon as reasonably practicable after such material is electronically filed with, or furnished to, the SEC. We also make available, through our Investor Relations webpage, via a link to the SEC's internet site, statements of beneficial ownership of our equity securities filed by our directors, officers, 10% or greater shareholders and others under Section 16 of the Exchange Act.

You can access information about our corporate governance at www.morganstanley.com/about-us-governance. Our Corporate Governance webpage includes:

| • | Amended and Restated Certificate of Incorporation; |

| • | Amended and Restated Bylaws; |

| • | Charters for our Audit Committee, Compensation, Management Development and Succession Committee, Nominating and Governance Committee, Operations and Technology Committee, and Risk Committee; |

| • | Corporate Governance Policies; |

| • | Policy Regarding Corporate Political Activities; |

| • | Policy Regarding Shareholder Rights Plan; |

| • | Equity Ownership Commitment; |

| • | Code of Ethics and Business Conduct; |

| • | Code of Conduct; |

| • | Integrity Hotline Information; and |

| • | Environmental and Social Policies. |

Our Code of Ethics and Business Conduct applies to all directors, officers and employees, including our Chief Executive Officer, Chief Financial Officer and Deputy Chief Financial Officer. We will post any amendments to the Code of Ethics and Business Conduct and any waivers that are required to be disclosed by the rules of either the SEC or the New York Stock Exchange LLC ("NYSE") on our internet site. You can request a copy of these documents, excluding exhibits, at no cost, by contacting Investor Relations, 1585 Broadway, New York, NY 10036 (212-761-4000). The information on our internet site is not incorporated by reference into this report.

ii

|

Financial Information

Management's Discussion and Analysis of Financial Condition and Results of Operations

Introduction

Morgan Stanley, a financial holding company, is a global financial services firm that maintains significant market positions in each of its business segments-Institutional Securities, Wealth Management and Investment Management. Morgan Stanley, through its subsidiaries and affiliates, provides a wide variety of products and services to a large and diversified group of clients and customers, including corporations, governments, financial institutions and individuals. Unless the context otherwise requires, the terms "Morgan Stanley," "Firm," "us," "we," or "our" mean Morgan Stanley (the "Parent Company") together with its consolidated subsidiaries.

A description of the clients and principal products and services of each of our business segments is as follows:

Institutional Securities provides investment banking, sales and trading, lending and other services to corporations, governments, financial institutions, and high to ultra-high net worth clients. Investment banking services consist of capital raising and financial advisory services, including services relating to the underwriting of debt, equity and other securities, as well as advice on mergers and acquisitions, restructurings, real estate and project finance. Sales and trading services include sales, financing and market-making activities in equity and fixed income products, including prime brokerage services, global macro, credit and commodities products. Lending services include originating and/or purchasing corporate loans, commercial and residential mortgage lending, asset-backed lending, and financing extended to equities and commodities customers and municipalities. Other services include investment and research activities.

Wealth Management provides a comprehensive array of financial services and solutions to individual investors and

small to medium-sized businesses/institutions covering brokerage and investment advisory services, financial and wealth planning services, annuity and insurance products, credit and other lending products, banking and retirement plan services.

Investment Management provides a broad range of investment strategies and products that span geographies, asset classes, and public and private markets to a diverse group of clients across institutional and intermediary channels. Strategies and products include equity, fixed income, liquidity and alternative/other products. Institutional clients include defined benefit/defined contribution plans, foundations, endowments, government entities, sovereign wealth funds, insurance companies, third-party fund sponsors and corporations. Individual clients are serviced through intermediaries, including affiliated and non-affiliated distributors.

The results of operations in the past have been, and in the future may continue to be, materially affected by competition; risk factors; and legislative, legal and regulatory developments; as well as other factors. These factors also may have an adverse impact on our ability to achieve our strategic objectives. Additionally, the discussion of our results of operations herein may contain forward-looking statements. These statements, which reflect management's beliefs and expectations, are subject to risks and uncertainties that may cause actual results to differ materially. For a discussion of the risks and uncertainties that may affect our future results, see "Forward-Looking Statements" immediately preceding Part I, Item 1, "Business-Competition" and "Business-Supervision and Regulation" in Part I, Item 1, "Risk Factors" in Part I, Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2016 (the "2016 Form 10-K") and "Liquidity and Capital Resources-Regulatory Requirements" herein.

| 1 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

Executive Summary

Overview of Financial Results

Consolidated Results

Net Revenues

($ in millions)

Net Income Applicable to Morgan Stanley

($ in millions)

Earnings per Common Share 1

| 1. | For the calculation of basic and diluted earnings per common share, see Note 15 to the financial statements. |

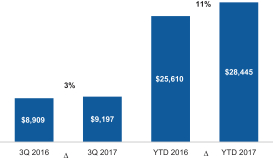

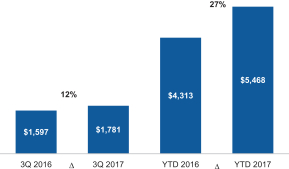

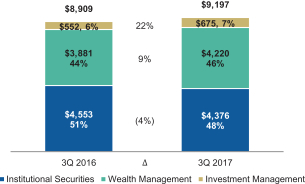

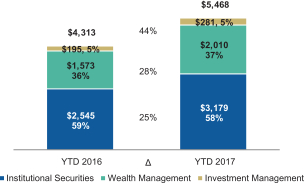

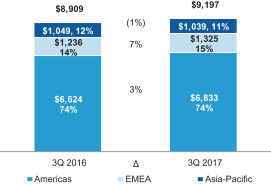

| • | We reported net revenues of $9,197 million in the three months ended September 30, 2017 ("current quarter," or "3Q 2017"), compared with $8,909 million in the three months ended September 30, 2016 ("prior year quarter," or "3Q 2016"). For the current quarter, net income applicable to Morgan Stanley was $1,781 million, or $0.93 per diluted common share, compared with $1,597 million, or $0.81 per diluted common share, in the prior year quarter. |

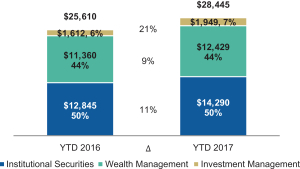

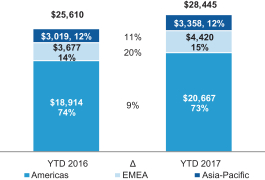

| • | We reported net revenues of $28,445 million in the nine months ended September 30, 2017 ("current year period," or "YTD 2017"), compared with $25,610 million in the nine months ended September 30, 2016 ("prior year period," or "YTD 2016"). For the current year period, net income applicable to Morgan Stanley was $5,468 million, or $2.79 per diluted common share, compared with $4,313 million, or $2.11 per diluted common share in the prior year period. |

Non-interest Expenses

($ in millions)

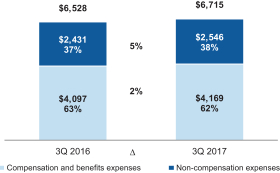

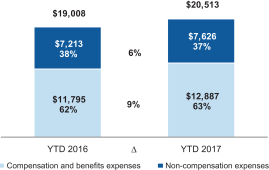

| • | Compensation and benefits expenses of $4,169 million in the current quarter and $12,887 million in the current year period increased 2% and 9%, respectively, from $4,097 million in the prior year quarter and $11,795 million in the prior year period. The current quarter results primarily reflected increases in the formulaic payout to Wealth Management representatives linked to higher revenues and deferred compensation associated with carried interest in the Investment Management business segment, partially offset by a decrease in discretionary incentive compensation mainly driven by lower revenues in the Institutional Securities business segment. The current year period results primarily reflected increases in the fair value of investments to which certain deferred compensation plans are referenced, discretionary incentive compensation mainly driven by higher revenues, the formulaic payout to |

| September 2017 Form 10-Q | 2 |

| Management's Discussion and Analysis | |

Wealth Management representatives linked to higher revenues, and deferred compensation associated with carried interest. |

| • | Non-compensation expenses were $2,546 million in the current quarter and $7,626 million in the current year period compared with $2,431 million in the prior year quarter and $7,213 million in the prior year period, representing a 5% and a 6% increase, respectively. These increases were primarily as a result of higher volume-driven expenses. In addition, non-compensation expenses increased in the current year period due to a provision related to a United Kingdom ("U.K.") indirect tax (i.e. value-added tax or "VAT") matter and higher litigation costs. For further discussion of the U.K. VAT matter, see "Institutional Securities-Investments, Other Revenues, Non-interest Expenses and Other Items-Other Items" herein. |

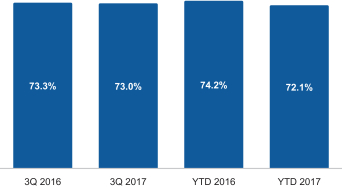

Expense Efficiency Ratio

| • | The expense efficiency ratio was 73.0% in the current quarter and 72.1% in the current year period. The expense efficiency ratio was 73.3% in the prior year quarter and 74.2% in the prior year period (see "Selected Non-Generally Accepted Accounting Principles ("Non-GAAP") Financial Information" herein). |

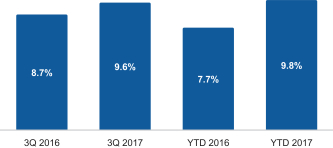

Return on Average Common Equity

| • | The annualized return on average common equity ("ROE") was 9.6% in the current quarter and 9.8% in the current year period. The annualized ROE was 8.7% in the prior year quarter and 7.7% in the prior year period (see "Selected Non-Generally Accepted Accounting Principles ("Non-GAAP") Financial Information" herein). |

Business Segment Results

Net Revenues by Segment 1, 2

($ in millions)

| 3 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

Net Income Applicable to Morgan Stanley by Segment 1, 3

($ in millions)

| 1. | The percentages in the charts represent the contribution of each business segment to the total. Amounts do not necessarily total to 100% due to intersegment eliminations, where applicable. |

| 2. | The total amount of Net Revenues by Segment also includes intersegment eliminations of $(74) million and $(77) million in the current quarter and prior year quarter, respectively, and $(223) million and $(207) million in the current year period and prior year period, respectively. |

| 3. | The total amount of Net Income Applicable to Morgan Stanley by Segment also includes intersegment eliminations of $(4) million in the current quarter and $(2) million in the current year period. |

| • | Institutional Securities net revenues of $4,376 million in the current quarter and $14,290 million in the current year period decreased 4% from the prior year quarter and increased 11% from the prior year period. The current quarter results primarily reflected lower revenues from fixed income sales and trading, partially offset by higher underwriting and advisory revenues. The current year period results primarily reflected higher revenues from underwriting and fixed income sales and trading. |

| • | Wealth Management net revenues of $4,220 million in the current quarter and $12,429 million in the current year period increased 9% both from the prior year quarter and the prior year period. The current quarter and the current year period results reflected growth in asset management fee revenues and Net interest income. |

| • | Investment Management net revenues of $675 million in the current quarter and $1,949 million in the current year period increased 22% from the prior year quarter and increased 21% from the prior year period. The current quarter and the current year period results primarily reflected higher carried interest and investment gains and growth in asset management fee revenues. |

Net Revenues by Region 1

($ in millions)

EMEA-Europe, Middle East and Africa

| 1. | For a discussion of how the geographic breakdown for net revenues is determined, see Note 21 to the consolidated financial statements in the 2016 Form 10-K. |

| September 2017 Form 10-Q | 4 |

| Management's Discussion and Analysis | |

Selected Financial Information and Other Statistical Data

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| $ in millions | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Income from continuing operations applicable to Morgan Stanley | $ | 1,775 | $ | 1,589 | $ | 5,489 | $ | 4,312 | ||||||||

Income (loss) from discontinued operations applicable to Morgan Stanley | 6 | 8 | (21 | ) | 1 | |||||||||||

Net income applicable to Morgan Stanley | 1,781 | 1,597 | 5,468 | 4,313 | ||||||||||||

Preferred stock dividends and other | 93 | 79 | 353 | 314 | ||||||||||||

Earnings applicable to Morgan Stanley common shareholders | $ | 1,688 | $ | 1,518 | $ | 5,115 | $ | 3,999 | ||||||||

Effective income tax rate from continuing operations | 28.1% | 31.5% | 29.7% | 32.7% | ||||||||||||

| At September 30, 2017 | At December 31, 2016 | |||||||

Capital ratios |

| |||||||

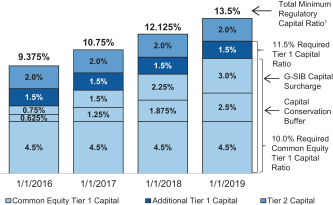

Common Equity Tier 1 capital ratio 1 | 16.9% | 16.9% | ||||||

Tier 1 capital ratio 1 | 19.3% | 19.0% | ||||||

Total capital ratio 1 | 22.2% | 22.0% | ||||||

Tier 1 leverage ratio | 8.4% | 8.4% | ||||||

| 1. | At September 30, 2017, our capital ratios are based on the Standardized Approach transitional rules. At December 31, 2016, our capital ratios were based on the Advanced Approach transitional rules. For a discussion of our regulatory capital ratios, see "Liquidity and Capital Resources-Regulatory Requirements" herein. |

| in millions, except per share and employee data | At September 30, 2017 | At December 31, 2016 | ||||||

Loans 1 | $ | 104,431 | $ | 94,248 | ||||

Total assets | $ | 853,693 | $ | 814,949 | ||||

Global Liquidity Reserve 2 | $ | 189,966 | $ | 202,297 | ||||

Deposits | $ | 154,639 | $ | 155,863 | ||||

Long-term borrowings | $ | 191,677 | $ | 164,775 | ||||

Common shareholders' equity | $ | 70,458 | $ | 68,530 | ||||

Common shares outstanding | 1,812 | 1,852 | ||||||

Book value per common share 3 | $ | 38.87 | $ | 36.99 | ||||

Worldwide employees | 57,702 | 55,311 | ||||||

| 1. | Amounts include loans held for investment (net of allowance) and loans held for sale but exclude loans at fair value, which are included in Trading assets in the balance sheets (see Note 7 to the financial statements). |

| 2. | For a discussion of Global Liquidity Reserve, see "Management's Discussion and Analysis of Financial Condition and Results of Operations-Liquidity and Capital Resources-Liquidity Risk Management Framework-Global Liquidity Reserve" in Part II, Item 7 of the 2016 Form 10-K. |

| 3. | Book value per common share equals common shareholders' equity divided by common shares outstanding. |

Selected Non-Generally Accepted Accounting Principles ("Non-GAAP") Financial Information

We prepare our financial statements using accounting principles generally accepted in the United States of America ("U.S. GAAP"). From time to time, we may disclose certain "non-GAAP financial measures" in this document, or in the course of our earnings releases, earnings and other conference calls, financial presentations, Definitive Proxy Statement and otherwise. A "non-GAAP financial measure" excludes, or includes, amounts from the most directly comparable measure calculated and presented in accordance with U.S. GAAP. We consider the non-GAAP financial measures we disclose to be useful to us, investors and analysts by providing further transparency about, or an alternate means of assessing, our financial condition, operating results, prospective regulatory capital requirements, or capital adequacy. These measures are not in accordance with, or a substitute for, U.S. GAAP and may be different from or inconsistent with non-GAAP financial measures used by other companies. Whenever we refer to a non-GAAP financial measure, we will also generally define it or present the most directly comparable financial measure calculated and presented in accordance with U.S. GAAP, along with a reconciliation of the differences between the U.S. GAAP financial measure and the non-GAAP financial measure.

The principal non-GAAP financial measures presented in this document are set forth below.

Reconciliations from U.S. GAAP to Non-GAAP Consolidated Financial Measures

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| $ in millions, except per share data | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Net income applicable to Morgan Stanley |

| |||||||||||||||

U.S. GAAP | $ | 1,781 | $ | 1,597 | $ | 5,468 | $ | 4,313 | ||||||||

Impact of discrete tax provision 1 | (83 | ) | - | (65 | ) | - | ||||||||||

Net income applicable to Morgan Stanley, excluding discrete tax provision-non-GAAP | $ | 1,698 | $ | 1,597 | $ | 5,403 | $ | 4,313 | ||||||||

Earnings per diluted common share |

| |||||||||||||||

U.S. GAAP | $ | 0.93 | $ | 0.81 | $ | 2.79 | $ | 2.11 | ||||||||

Impact of discrete tax provision 1 | (0.05 | ) | - | (0.03 | ) | - | ||||||||||

Earnings per diluted common share, excluding discrete tax provision-non-GAAP | $ | 0.88 | $ | 0.81 | $ | 2.76 | $ | 2.11 | ||||||||

Effective income tax rate | ||||||||||||||||

U.S. GAAP | 28.1% | 31.5% | 29.7% | 32.7% | ||||||||||||

Impact of discrete tax provision 1 | 3.3% | - | 0.8% | - | ||||||||||||

Effective income tax rate from continuing operations, excluding discrete tax provision-non-GAAP | 31.4% | 31.5% | 30.5% | 32.7% | ||||||||||||

| 5 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

Tangible Equity

| Monthly Average Balance | ||||||||||||||||||||||||

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||||||||||

| $ in millions | At September 30, | At December 31, 2016 | 2017 | 2016 | 2017 | 2016 | ||||||||||||||||||

U.S. GAAP | ||||||||||||||||||||||||

Common equity | $ | 70,458 | $ | 68,530 | $ | 70,487 | $ | 69,531 | $ | 69,786 | $ | 68,859 | ||||||||||||

Preferred equity | 8,520 | 7,520 | 8,520 | 7,520 | 8,420 | 7,520 | ||||||||||||||||||

Morgan Stanley shareholders' equity | 78,978 | 76,050 | 79,007 | 77,051 | 78,206 | 76,379 | ||||||||||||||||||

Junior subordinated debentures issued to capital trusts | - | - | - | 1,427 | - | 2,278 | ||||||||||||||||||

Less: Goodwill and net intangible assets | (9,079 | ) | (9,296) | (9,120 | ) | (9,368 | ) | (9,192 | ) | (9,447 | ) | |||||||||||||

Morgan Stanley tangible shareholders' equity-non-GAAP | $ | 69,899 | $ | 66,754 | $ | 69,887 | $ | 69,110 | $ | 69,014 | $ | 69,210 | ||||||||||||

U.S. GAAP | ||||||||||||||||||||||||

Common equity | $ | 70,458 | $ | 68,530 | $ | 70,487 | $ | 69,531 | $ | 69,786 | $ | 68,859 | ||||||||||||

Less: Goodwill and net intangible assets | (9,079 | ) | (9,296) | (9,120 | ) | (9,368 | ) | (9,192 | ) | (9,447 | ) | |||||||||||||

Tangible common equity-non-GAAP | $ | 61,379 | $ | 59,234 | $ | 61,367 | $ | 60,163 | $ | 60,594 | $ | 59,412 | ||||||||||||

Consolidated Non-GAAP Financial Measures

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| $ in billions | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Average common equity 1, 2 |

| |||||||||||||||

Unadjusted | $ | 70.5 | $ | 69.5 | $ | 69.8 | $ | 68.9 | ||||||||

Excluding DVA | 71.3 | 69.6 | 70.4 | 69.0 | ||||||||||||

Excluding DVA and discrete tax provision (benefit) | 71.2 | 69.6 | 70.4 | 69.0 | ||||||||||||

Return on average common equity 1, 3, 4 |

| |||||||||||||||

Unadjusted | 9.6% | 8.7% | 9.8% | 7.7% | ||||||||||||

Excluding DVA | 9.5% | 8.7% | 9.7% | 7.7% | ||||||||||||

Excluding DVA and discrete tax provision (benefit) | 9.0% | 8.7% | 9.6% | 7.7% | ||||||||||||

Average tangible common equity 1, 2, 5 |

| |||||||||||||||

Unadjusted | $ | 61.4 | $ | 60.2 | $ | 60.6 | $ | 59.4 | ||||||||

Excluding DVA | 62.1 | 60.2 | 61.2 | 59.5 | ||||||||||||

Excluding DVA and discrete tax provision (benefit) | 62.1 | 60.2 | 61.3 | 59.5 | ||||||||||||

Return on average tangible common equity 1, 4 |

| |||||||||||||||

Unadjusted | 11.0% | 10.1% | 11.3% | 9.0% | ||||||||||||

Excluding DVA | 10.9% | 10.1% | 11.1% | 9.0% | ||||||||||||

Excluding DVA and discrete tax provision (benefit) | 10.3% | 10.1% | 11.0% | 9.0% | ||||||||||||

Expense efficiency ratio 6 | 73.0% | 73.3% | 72.1% | 74.2% | ||||||||||||

| At September 30, 2017 | At December 31, 2016 | |||||||

| Tangible book value per common share 5 | $ | 33.86 | $ | 31.98 | ||||

Non-GAAP Financial Measures by Business Segment

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| $ in billions | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Pre-tax profit margin 7 | ||||||||||||||||

Institutional Securities | 28% | 30% | 31% | 30% | ||||||||||||

Wealth Management | 27% | 23% | 25% | 22% | ||||||||||||

Investment Management | 19% | 18% | 19% | 16% | ||||||||||||

Consolidated | 27% | 27% | 28% | 26% | ||||||||||||

Average common equity 8 |

| |||||||||||||||

Institutional Securities | $ | 40.2 | $ | 43.2 | $ | 40.2 | $ | 43.2 | ||||||||

Wealth Management | 17.2 | 15.3 | 17.2 | 15.3 | ||||||||||||

Investment Management | 2.4 | 2.8 | 2.4 | 2.8 | ||||||||||||

Parent Company | 10.7 | 8.2 | 10.0 | 7.6 | ||||||||||||

Consolidated average common equity | $ | 70.5 | $ | 69.5 | $ | 69.8 | $ | 68.9 | ||||||||

Return on average common equity 4 |

| |||||||||||||||

Institutional Securities | 8.9% | 8.3% | 9.6% | 7.1% | ||||||||||||

Wealth Management | 15.8% | 14.5% | 15.0% | 13.3% | ||||||||||||

Investment Management | 18.8% | 9.3% | 15.4% | 9.0% | ||||||||||||

Consolidated | 9.6% | 8.7% | 9.8% | 7.7% | ||||||||||||

DVA-Debt valuation adjustment represents the change in the fair value resulting from fluctuations in our credit spreads and other credit factors related to liabilities carried at fair value under the fair value option, primarily certain Long-term and Short-term borrowings.

| 1. | Beginning in 2017, with the adoption of the accounting update Improvements to Employee Share-Based Payment Accounting , the income tax consequences related to share-based payments are required to be recognized in Provision for income taxes in the income statements upon the conversion of employee share-based awards, which primarily occur in the first quarter of each year. The impact of the income tax consequences upon conversion of the awards may be either a benefit or a provision and is treated as a discrete item. When excluding discrete tax provision (benefit) above only discrete tax provisions (benefits) other than income tax consequences arising from conversion activity are excluded as we anticipate conversion activity each quarter. See Note 2 to the financial statements for information on the adoption of the accounting update Improvements to Employee Share-Based Payment Accounting . For further information on the discrete tax provision, see "Supplemental Financial Information and Disclosures-Income Tax Matters" herein. |

| 2. | The impact of DVA on average common equity and average tangible common equity was approximately $(775) million and $(62) million in the current quarter and prior year quarter, respectively, and approximately $(652) million and $(118) million in the current year period and prior year period, respectively. |

| 3. | The calculation used in determining the Firm's "ROE Target" is return on average common equity excluding DVA and discrete tax items as set forth above. |

| 4. | Return on average common equity and return on average tangible common equity equal annualized net income applicable to Morgan Stanley less preferred dividends as a percentage of average common equity and average tangible common equity, respectively, on a consolidated or business segment basis as indicated. When excluding DVA, it is only excluded from the denominator. When excluding the discrete tax provision (benefit), both the numerator and denominator are adjusted. |

| 5. | Tangible book value per common share equals tangible common equity divided by common shares outstanding. |

| 6. | The expense efficiency ratio represents total non-interest expenses as a percentage of net revenues. |

| 7. | Pre-tax profit margin represents income from continuing operations before income taxes as a percentage of net revenues. |

| September 2017 Form 10-Q | 6 |

| Management's Discussion and Analysis | |

| 8. | Average common equity for each business segment is determined at the beginning of each year using our Required Capital framework, an internal capital adequacy measure (see "Liquidity and Capital Resources-Regulatory Requirements-Attribution of Average Common Equity According to the Required Capital Framework" herein) and remains fixed throughout the year until the next annual reset. |

Return on Equity Target

We have an ROE Target of 9% to 11% to be achieved by 2017. Our ROE Target and the related strategies and goals are forward-looking statements that may be materially affected by many factors, including, among other things: macroeconomic and market conditions; legislative and regulatory developments; industry trading and investment banking volumes; equity market levels; interest rate environment; legal expenses and the ability to reduce expenses in general; capital levels; and discrete tax items. For further information on our ROE Target and related assumptions, see "Management's Discussion and Analysis of Financial Condition and Results of Operations-Executive Summary-Return on Equity Target" in Part II, Item 7 of the 2016 Form 10-K.

Business Segments

Substantially all of our operating revenues and operating expenses are directly attributable to the business segments.

Certain revenues and expenses have been allocated to each business segment, generally in proportion to its respective net revenues, non-interest expenses or other relevant measures.

As a result of treating certain intersegment transactions as transactions with external parties, we include an Intersegment Eliminations category to reconcile the business segment results to our consolidated results.

Net Revenues, Compensation Expense and Income Taxes

For discussions of our net revenues, see "Management's Discussion and Analysis of Financial Condition and Results of Operations-Business Segments-Net Revenues" and "Management's Discussion and Analysis of Financial Condition and Results of Operations-Business Segments-Net Revenues by Segment" in Part II, Item 7 of the 2016 Form 10-K. For a discussion of our compensation expense, see "Management's Discussion and Analysis of Financial Condition and Results of Operations-Business Segments-Compensation Expense" in Part II, Item 7 of the 2016 Form 10-K. For a discussion of income taxes, see "Management's Discussion and Analysis of Financial Condition and Results of Operations-Business Segments-Income Taxes" in Part II, Item 7 of the 2016 Form 10-K.

| 7 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

Institutional Securities

Income Statement Information

| Three Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Revenues | ||||||||||||

Investment banking | $ | 1,270 | $ | 1,104 | 15% | |||||||

Trading | 2,504 | 2,393 | 5% | |||||||||

Investments | 52 | 36 | 44% | |||||||||

Commissions and fees | 561 | 592 | (5)% | |||||||||

Asset management, distribution and administration fees | 88 | 68 | 29% | |||||||||

Other | 143 | 243 | (41)% | |||||||||

Total non-interest revenues | 4,618 | 4,436 | 4% | |||||||||

Interest income | 1,421 | 980 | 45% | |||||||||

Interest expense | 1,663 | 863 | 93% | |||||||||

Net interest | (242) | 117 | N/M | |||||||||

Net revenues | 4,376 | 4,553 | (4)% | |||||||||

Compensation and benefits | 1,532 | 1,657 | (8)% | |||||||||

Non-compensation expenses | 1,608 | 1,513 | 6% | |||||||||

Total non-interest expenses | 3,140 | 3,170 | (1)% | |||||||||

Income from continuing operations before income taxes | 1,236 | 1,383 | (11)% | |||||||||

Provision for income taxes | 260 | 381 | (32)% | |||||||||

Income from continuing operations | 976 | 1,002 | (3)% | |||||||||

Income (loss) from discontinued operations, net of income taxes | 6 | 8 | (25)% | |||||||||

Net income | 982 | 1,010 | (3)% | |||||||||

Net income applicable to noncontrolling interests | 9 | 44 | (80)% | |||||||||

Net income applicable to | $ | 973 | $ | 966 | 1% | |||||||

Nine Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Revenues | ||||||||||||

Investment banking | $ | 4,100 | $ | 3,202 | 28% | |||||||

Trading | 8,241 | 6,782 | 22% | |||||||||

Investments | 155 | 144 | 8% | |||||||||

Commissions and fees | 1,811 | 1,854 | (2)% | |||||||||

Asset management, distribution and administration fees | 268 | 210 | 28% | |||||||||

Other | 442 | 385 | 15% | |||||||||

Total non-interest revenues | 15,017 | 12,577 | 19% | |||||||||

Interest income | 3,788 | 2,999 | 26% | |||||||||

Interest expense | 4,515 | 2,731 | 65% | |||||||||

Net interest | (727) | 268 | N/M | |||||||||

Net revenues | 14,290 | 12,845 | 11% | |||||||||

Compensation and benefits | 5,069 | 4,664 | 9% | |||||||||

Non-compensation expenses | 4,812 | 4,384 | 10% | |||||||||

Total non-interest expenses | 9,881 | 9,048 | 9% | |||||||||

Income from continuing operations before income taxes | 4,409 | 3,797 | 16% | |||||||||

Provision for income taxes | 1,132 | 1,109 | 2% | |||||||||

Income from continuing operations | 3,277 | 2,688 | 22% | |||||||||

Income (loss) from discontinued operations, net of income taxes | (21) | 1 | N/M | |||||||||

Net income | 3,256 | 2,689 | 21% | |||||||||

Net income applicable to noncontrolling interests | 77 | 144 | (47)% | |||||||||

Net income applicable to | $ | 3,179 | $ | 2,545 | 25% | |||||||

N/M-Not Meaningful

| September 2017 Form 10-Q | 8 |

| Management's Discussion and Analysis | |

Investment Banking

Investment Banking Revenues

| ||||||

| Three Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Advisory | $ | 555 | $ | 504 | 10% | |||||||

Underwriting: | ||||||||||||

Equity | 273 | 236 | 16% | |||||||||

Fixed income | 442 | 364 | 21% | |||||||||

Total underwriting | 715 | 600 | 19% | |||||||||

Total investment banking | $ | 1,270 | $ | 1,104 | 15% | |||||||

| Nine Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Advisory | $ | 1,555 | $ | 1,592 | (2)% | |||||||

Underwriting: | ||||||||||||

Equity | 1,068 | 662 | 61% | |||||||||

Fixed income | 1,477 | 948 | 56% | |||||||||

Total underwriting | 2,545 | 1,610 | 58% | |||||||||

Total investment banking | $ | 4,100 | $ | 3,202 | 28% | |||||||

Investment Banking Volumes

| ||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| $ in billions | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Completed mergers and acquisitions 1 | $ | 229 | $ | 190 | $ | 585 | $ | 728 | ||||||||

Equity and equity- related offerings 2, 3 | 16 | 13 | 46 | 34 | ||||||||||||

Fixed income offerings 2, 4 | 60 | 72 | 201 | 185 | ||||||||||||

Source: Thomson Reuters, data at October 2, 2017. Transaction volumes may not be indicative of net revenues in a given period. In addition, transaction volumes for prior periods may vary from amounts previously reported due to the subsequent withdrawal or change in the value of a transaction.

| 1. | Amounts include transactions of $100 million or more. Completed mergers and acquisitions volumes are based on full credit to each of the advisors in a transaction. |

| 2. | Equity and equity-related offerings and fixed income offerings are based on full credit for single book managers and equal credit for joint book managers. |

| 3. | Amounts include Rule 144A issuances and registered public offerings of common stock and convertible securities and rights offerings. |

| 4. | Amounts include non-convertible preferred stock, mortgage-backed and asset-backed securities, and taxable municipal debt. Amounts include publicly registered and Rule 144A issuances. Amounts exclude leveraged loans and self-led issuances. |

Investment banking revenues are composed of fees from advisory services and revenues from the underwriting of securities offerings and syndication of loans, net of syndication expenses.

Investment banking revenues of $1,270 million in the current quarter and $4,100 million in the current year period increased 15% and 28% from the comparable prior year periods. The increase in the current quarter reflected both higher underwriting and advisory revenues. The increase in the current year period was due to higher underwriting revenues.

| • | Advisory revenues increased in the current quarter reflecting the higher volumes of completed merger, acquisition and restructuring transactions ("M&A") (see Investment Banking Volumes table). Advisory revenues decreased in the current year period reflecting the lower volumes of completed M&A, partially offset by the positive impact of higher fee realizations. |

| • | Equity underwriting revenues increased in the current quarter and current year period as a result of higher global market volumes in both follow-on and initial public offerings (see Investment Banking Volumes table). In the current year period, equity underwriting revenues also increased as a result of higher levels of deal activity. Fixed income underwriting revenues increased in the current quarter primarily due to higher non-investment grade bond fees and loan fees. Fixed income underwriting revenues increased in the current year period primarily due to higher bond fees and non-investment grade loan fees. |

Sales and Trading Net Revenues

By Income Statement Line Item

| Three Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Trading | $ | 2,504 | $ | 2,393 | 5% | |||||||

Commissions and fees | 561 | 592 | (5)% | |||||||||

Asset management, distribution and administration fees | 88 | 68 | 29% | |||||||||

Net interest | (242) | 117 | N/M | |||||||||

Total | $ | 2,911 | $ | 3,170 | (8)% | |||||||

| Nine Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Trading | $ | 8,241 | $ | 6,782 | 22% | |||||||

Commissions and fees | 1,811 | 1,854 | (2)% | |||||||||

Asset management, distribution and administration fees | 268 | 210 | 28% | |||||||||

Net interest | (727) | 268 | N/M | |||||||||

Total | $ | 9,593 | $ | 9,114 | 5% | |||||||

N/M-Not Meaningful

| 9 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

By Business

| Three Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Equity | $ | 1,891 | $ | 1,883 | -% | |||||||

Fixed income | 1,167 | 1,479 | (21)% | |||||||||

Other | (147) | (192) | 23% | |||||||||

Total | $ | 2,911 | $ | 3,170 | (8)% | |||||||

| Nine Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Equity | $ | 6,062 | $ | 6,084 | -% | |||||||

Fixed income | 4,120 | 3,649 | 13% | |||||||||

Other | (589) | (619) | 5% | |||||||||

Total | $ | 9,593 | $ | 9,114 | 5% | |||||||

Sales and Trading Activities-Equity and Fixed Income

Following is a description of the sales and trading activities within our equities and fixed income businesses as well as how their results impact the income statement line items, followed by a presentation and explanation of results.

Equities-Financing. We provide financing and prime brokerage services to our clients active in the equity markets through a variety of products including margin lending, securities lending and swaps. Results from this business are largely driven by the difference between financing income earned and financing costs incurred, which are reflected in Net interest for securities and equity lending products and in Trading revenues for derivative products.

Equities-Execution services. We make markets for our clients in equity-related securities and derivative products, including providing liquidity and hedging products. A significant portion of the results for this business is generated by commissions and fees from executing and clearing client transactions on major stock and derivative exchanges as well as from over-the-counter ("OTC") transactions. Market-making also generates gains and losses on inventory, which are reflected in Trading revenues.

Fixed income- Within fixed income we make markets in order to facilitate client activity as part of the following products and services.

| • | Global macro products. We make markets for our clients in interest rate, foreign exchange and emerging market products, including exchange-traded and OTC securities, loans and derivative instruments. The results of this market-making activity are primarily driven by gains and losses from buying and selling positions to stand ready for and satisfy client demand, and are recorded in Trading revenues. |

| • | Credit products. We make markets in credit-sensitive products, such as corporate bonds and mortgage securities and |

other securitized products, and related derivative instruments. The values of positions in this business are sensitive to changes in credit spreads and interest rates, which result in gains and losses reflected in Trading revenues. Due to the amount and type of the interest-bearing securities and loans making up this business, a significant portion of the results is also reflected in Net interest revenues. |

| • | Commodities products and Other. We make markets in various commodity products related primarily to electricity, natural gas, oil, and precious metals, with the results primarily reflected in Trading revenues. Other activities include the results from the centralized management of our fixed income derivative counterparty exposures, which are primarily recorded in Trading revenues. |

Sales and Trading Net Revenues-Equity and Fixed Income

Three Months Ended September 30, 2017 | ||||||||||||||||

| $ in millions | Trading | Fees 1 | Net Interest 2 | Total | ||||||||||||

Financing | $ | 1,029 | $ | 92 | $ | (206 | ) | $ | 915 | |||||||

Execution services | 540 | 495 | (59 | ) | 976 | |||||||||||

Total Equity | $ | 1,569 | $ | 587 | $ | (265 | ) | $ | 1,891 | |||||||

Total Fixed income | $ | 1,073 | $ | 65 | $ | 29 | $ | 1,167 | ||||||||

Three Months Ended September 30, 2016 | ||||||||||||||||

| $ in millions | Trading | Fees 1 | Net Interest 2 | Total | ||||||||||||

Financing | $ | 872 | $ | 83 | $ | (110 | ) | $ | 845 | |||||||

Execution services | 536 | 541 | (39 | ) | 1,038 | |||||||||||

Total Equity | $ | 1,408 | $ | 624 | $ | (149 | ) | $ | 1,883 | |||||||

Total Fixed income | $ | 1,209 | $ | 38 | $ | 232 | $ | 1,479 | ||||||||

Nine Months Ended September 30, 2017 | ||||||||||||||||

| $ in millions | Trading | Fees 1 | Net Interest 2 | Total | ||||||||||||

Financing | $ | 3,126 | $ | 269 | $ | (621 | ) | $ | 2,774 | |||||||

Execution services | 1,805 | 1,643 | (160 | ) | 3,288 | |||||||||||

Total Equity | $ | 4,931 | $ | 1,912 | $ | (781 | ) | $ | 6,062 | |||||||

Total Fixed income | $ | 3,785 | $ | 167 | $ | 168 | $ | 4,120 | ||||||||

Nine Months Ended September 30, 2016 | ||||||||||||||||

| $ in millions | Trading | Fees 1 | Net Interest 2 | Total | ||||||||||||

Financing | $ | 2,797 | $ | 259 | $ | (152 | ) | $ | 2,904 | |||||||

Execution services | 1,621 | 1,690 | (131 | ) | 3,180 | |||||||||||

Total Equity | $ | 4,418 | $ | 1,949 | $ | (283 | ) | $ | 6,084 | |||||||

Total Fixed income | $ | 2,782 | $ | 115 | $ | 752 | $ | 3,649 | ||||||||

| 1. | Includes Commissions and fees and Asset management, distribution and administration fees. |

| 2. | Funding costs are allocated to the businesses based on funding usage and are included in Net interest. |

| September 2017 Form 10-Q | 10 |

| Management's Discussion and Analysis | |

We manage each of the sales and trading businesses based on its aggregate net revenues, which are comprised of the income statement line items quantified in the previous table. Trading revenues are affected by a variety of market dynamics, including volumes, bid-offer spreads, and inventory prices, as well as impacts from hedging activity, which are interrelated. We provide qualitative commentary in the discussion of results that follow on the key drivers of period over period variances, as the quantitative impact of the various market dynamics typically cannot be disaggregated.

For additional information on total Trading revenues, see the table "Trading Revenues by Product Type" in Note 4 to the financial statements.

Sales and Trading Net Revenues during the Current Quarter

Equity

Equity sales and trading net revenues of $1,891 million in the current quarter were relatively unchanged from the prior year quarter, reflecting higher results in our financing business, offset by lower results in execution services.

| • | Financing revenues increased 8% from the prior year quarter due to higher client activity in equity swaps reflected in Trading revenues, partially offset by lower Net interest revenues due to a shift in the mix of financing transactions. |

| • | Execution services decreased 6% from the prior year quarter as reduced market volumes in the United States resulted in lower commissions and fees, while reduced Trading revenues from derivative products were offset by increased Trading revenues from cash equity products. |

Fixed Income

Fixed income net revenues of $1,167 million in the current quarter were 21% lower than the prior year quarter, primarily driven by lower results in credit and global macro products.

| • | Credit products decreased due to tighter corporate credit spreads and lower volatility compared with the prior year quarter, which impacted Trading revenues. In addition, Net interest revenues decreased due to a lower level of interest realized in securitized products in the current quarter. |

| • | Global macro products decreased due to lower market and interest rate volatility, which reduced Trading revenues. In addition, Net interest revenues decreased due to the effect of interest rate products inventory management. |

| • | Commodities products and Other remained relatively unchanged from the prior year quarter. |

Sales and Trading Net Revenues during the Current Year Period

Equity

Equity sales and trading net revenues of $6,062 million in the current year period were relatively unchanged from the prior year period, reflecting lower results in our financing business, offset by higher results in execution services.

| • | Financing revenues decreased 4% from the prior year period as Net interest revenues declined from higher net interest costs, reflecting increased liquidity requirements and a shift in the mix of financing transactions, partially offset by higher client activity in equity swaps reflected in Trading revenues. |

| • | Execution services increased 3% from the prior year period primarily due to improved results in cash equity inventory management reflected in Trading revenues, partially offset by lower commissions and fees driven by reduced market volumes in the United States. |

Fixed Income

Fixed income net revenues of $4,120 million in the current year period were 13% higher than the prior year period, driven by higher results across all three product areas.

| • | Credit products increased due to the absence of inventory losses driven by a widening spread environment in the prior year period, which increased Trading revenues. This was partially offset by a lower level of interest realized in securitized products in the current year period, which reduced Net interest revenues. |

| • | Global macro products increased due to increased Trading revenues in foreign exchange driven by market volatility, and structured interest rate products driven by higher client activity. This was partially offset by higher interest costs impacting Net interest revenues in the current year period which resulted from interest rate products inventory management. |

| • | Commodities products and Other increased due to improved metals trading, commodities lending results and the absence of losses from counterparty risk management incurred in the prior year period. |

Investments, Other Revenues, Non-interest Expenses and Other Items

Investments

| • | Net investment gains of $52 million in the current quarter increased from the prior year quarter primarily as a result of higher gains on real estate investments, partially offset by lower gains on equities business related investments. |

| 11 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

| • | Net investment gains of $155 million in the current year period increased from the prior year period primarily reflecting gains on investments associated with our compensation plans in the current year period compared with losses in the prior year period and higher gains on real estate investments, partially offset by lower gains on equities business related investments. |

Other

| • | Other revenues of $143 million in the current quarter decreased from the prior year quarter primarily reflecting lower mark-to-market gains on loans held for sale. Other revenues of $442 million in the current year period increased from the prior year period primarily reflecting a decrease in the provision on loans held for investment. |

Non-interest Expenses

Non-interest expenses of $3,140 million in the current quarter were relatively unchanged from the prior year quarter primarily reflecting an 8% decrease in Compensation and benefits expenses and a 6% increase in Non-compensation expenses. Non-interest expenses of $9,881 million in the current year period increased from the prior year period reflecting a 9% increase in Compensation and benefits expenses and a 10% increase in Non-compensation expenses.

| • | Compensation and benefits expenses decreased in the current quarter primarily due to decreases in discretionary incentive compensation driven mainly by lower revenues, |

and lower amortization of deferred cash and equity awards. Compensation and benefits expenses increased in the current year period primarily due to increases in discretionary incentive compensation driven mainly by higher revenues and the fair value of investments to which certain deferred compensation plans are referenced. |

| • | Non-compensation expenses increased in the current quarter and current year period primarily due to higher volume-driven expenses and litigation costs. In addition to higher volume-driven expenses and litigation costs, non-compensation expenses increased in the current year period due to a provision related to the U.K. VAT matter (see Other Items below). |

Other Items

During the second quarter, the Firm self-identified an issue regarding VAT on intercompany services provided by certain overseas affiliates to our U.K. group. The Firm is reviewing the reporting of U.K. VAT as the focus and nature of services shifted among geographic locations. In the current year period, we have recorded a provision of $86 million that incorporates potential additional VAT, interest and penalties for this exposure. We are actively working with Her Majesty's Revenue and Customs to resolve this matter. The provision reflected is based on currently available information and analyses, and our review of this matter is continuing.

| September 2017 Form 10-Q | 12 |

| Management's Discussion and Analysis | |

Wealth Management

Income Statement Information

| Three Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Revenues | ||||||||||||

Investment banking | $ | 125 | $ | 129 | (3)% | |||||||

Trading | 212 | 229 | (7)% | |||||||||

Investments | 1 | - | N/M | |||||||||

Commissions and fees | 402 | 433 | (7)% | |||||||||

Asset management, distribution and administration fees | 2,393 | 2,133 | 12% | |||||||||

Other | 62 | 72 | (14)% | |||||||||

Total non-interest revenues | 3,195 | 2,996 | 7% | |||||||||

Interest income | 1,155 | 979 | 18% | |||||||||

Interest expense | 130 | 94 | 38% | |||||||||

Net interest | 1,025 | 885 | 16% | |||||||||

Net revenues | 4,220 | 3,881 | 9% | |||||||||

Compensation and benefits | 2,326 | 2,203 | 6% | |||||||||

Non-compensation expenses | 775 | 777 | -% | |||||||||

Total non-interest expenses | 3,101 | 2,980 | 4% | |||||||||

Income from continuing operations before income taxes | 1,119 | 901 | 24% | |||||||||

Provision for income taxes | 421 | 337 | 25% | |||||||||

Net income applicable to | $ | 698 | $ | 564 | 24% | |||||||

| Nine Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 1 | % Change | |||||||||

Revenues | ||||||||||||

Investment banking | $ | 405 | $ | 373 | 9% | |||||||

Trading | 657 | 675 | (3)% | |||||||||

Investments | 3 | (2 | ) | N/M | ||||||||

Commissions and fees | 1,266 | 1,268 | -% | |||||||||

Asset management, distribution and administration fees | 6,879 | 6,269 | 10% | |||||||||

Other | 191 | 232 | (18)% | |||||||||

Total non-interest revenues | 9,401 | 8,815 | 7% | |||||||||

Interest income | 3,348 | 2,813 | 19% | |||||||||

Interest expense | 320 | 268 | 19% | |||||||||

Net interest | 3,028 | 2,545 | 19% | |||||||||

Net revenues | 12,429 | 11,360 | 9% | |||||||||

Compensation and benefits | 6,940 | 6,443 | 8% | |||||||||

Non-compensation expenses | 2,340 | 2,371 | (1)% | |||||||||

Total non-interest expenses | 9,280 | 8,814 | 5% | |||||||||

Income from continuing operations before income taxes | 3,149 | 2,546 | 24% | |||||||||

Provision for income taxes | 1,139 | 973 | 17% | |||||||||

Net income applicable to | $ | 2,010 | $ | 1,573 | 28% | |||||||

N/M – Not Meaningful

| 1. | Effective July 1, 2016, the Institutional Securities and Wealth Management business segments entered into an agreement, whereby Institutional Securities assumed management of Wealth Management's fixed income client-driven trading activities and employees. Institutional Securities now pays fees to Wealth Management based on distribution activity (collectively, the "Fixed Income Integration"). Prior periods have not been recast for this new intersegment agreement due to immateriality. |

Financial Information and Statistical Data

| $ in billions | At September 30, 2017 | At December 31, 2016 | ||||||

Client assets | $ | 2,307 | $ | 2,103 | ||||

Fee-based client assets 1 | $ | 1,003 | $ | 877 | ||||

Fee-based client assets as a percentage of total client assets | 43% | 42% | ||||||

Client liabilities 2 | $ | 78 | $ | 73 | ||||

Investment securities portfolio | $ | 60.6 | $ | 63.9 | ||||

Loans and lending commitments | $ | 76.2 | $ | 68.7 | ||||

Wealth Management representatives | 15,759 | 15,763 | ||||||

| Three Months Ended September 30, | ||||||||

| 2017 | 2016 | |||||||

Annualized revenues per representative (dollars in thousands) 3 | $ | 1,071 | $ | 977 | ||||

Client assets per representative (dollars in millions) 4 | $ | 146 | $ | 132 | ||||

Fee-based asset flows 5 (dollars in billions) | $ | 15.8 | $ | 13.5 | ||||

| Nine Months Ended September 30, | ||||||||

| 2017 | 2016 | |||||||

Annualized revenues per representative (dollars in thousands) 3 | $ | 1,051 | $ | 953 | ||||

Client assets per representative (dollars in millions) 4 | $ | 146 | $ | 132 | ||||

Fee-based asset flows 5 (dollars in billions) | $ | 54.5 | $ | 31.4 | ||||

| 1. | Fee-based client assets represent the amount of assets in client accounts where the basis of payment for services is a fee calculated on those assets. |

| 2. | Client liabilities include securities-based and tailored lending, residential real estate loans and margin lending. |

| 3. | Annualized revenues per representative equal Wealth Management's annualized revenues divided by the average representative headcount. |

| 4. | Client assets per representative equal total period-end client assets divided by period-end representative headcount. |

| 5. | Fee-based asset flows include net new fee-based assets, net account transfers, dividends, interest and client fees and exclude institutional cash management-related activity. |

| 13 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

Net Revenues

Transactional Revenues

| Three Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Investment banking | $ | 125 | $ | 129 | (3)% | |||||||

Trading | 212 | 229 | (7)% | |||||||||

Commissions and fees | 402 | 433 | (7)% | |||||||||

Total | $ | 739 | $ | 791 | (7)% | |||||||

| Nine Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Investment banking | $ | 405 | $ | 373 | 9% | |||||||

Trading | 657 | 675 | (3)% | |||||||||

Commissions and fees | 1,266 | 1,268 | -% | |||||||||

Total | $ | 2,328 | $ | 2,316 | 1% | |||||||

Transactional revenues of $739 million in the current quarter decreased 7% from the prior year quarter primarily reflecting lower Commissions and fees and Trading revenues.

Transactional revenues of $2,328 million in the current year period increased 1% from the prior year period primarily reflecting higher revenues in Investment banking revenues, partially offset by decreased Trading revenues.

| • | Investment banking revenues were relatively unchanged in the current quarter. The increase in the current year period was due to higher revenues from structured products and equity syndicate activities, partially offset by lower preferred stock syndicate activity. |

| • | Trading revenues decreased in the current quarter primarily due to lower client activity in fixed income products. In addition to lower client activity, Trading revenues decreased in the current year period due to lower revenues related to the Fixed Income Integration, partially offset by gains related to investments associated with certain employee deferred compensation plans. |

| • | Commissions and fees decreased in the current quarter primarily due to decreased activity in equities, mutual funds and annuities. Commissions and fees were relatively unchanged in the current year period, with decreased activity in annuities and mutual funds essentially offset by the impact of the Fixed Income Integration. |

Asset Management

| • | Asset management, distribution and administration fees of $2,393 million in the current quarter and $6,879 million in the current year period increased 12% and 10%, respectively. The increase in both periods is primarily due to market appreciation and net positive flows. See "Fee-Based Client Assets" herein. |

Net Interest

| • | Net interest of $1,025 million in the current quarter and $3,028 million in the current year period increased 16% and 19%, respectively, primarily due to higher loan balances and higher interest rates, partially offset by higher interest paid on deposits. |

Other

| • | Other revenues of $62 million in the current quarter and $191 million in the current year period decreased 14% and 18%, respectively, due to lower realized gains from the available for sale ("AFS") securities portfolio. |

Non-interest Expenses

Non-interest expenses of $3,101 million in the current quarter and $9,280 million in the current year period increased 4% and 5%, respectively, as a result of the increase in Compensation and benefits expenses.

| • | Compensation and benefits expenses increased in the current quarter primarily due to the formulaic payout to Wealth Management representatives linked to higher revenues. In addition to the higher formulaic payout, Compensation and benefits expenses increased in the current year period due to increases in the fair value of investments to which certain deferred compensation plans are referenced. |

| • | Non-compensation expenses were relatively unchanged in the current quarter. Non-compensation expenses decreased in the current year period primarily due to lower litigation and information processing costs, partially offset by higher deposit insurance expense and higher consulting fees related to strategic initiatives. |

Fee-Based Client Assets

For a description of fee-based client assets, including descriptions for the fee based client asset types and rollforward items in the following tables, see "Management's Discussion and Analysis of Financial Condition and Results of Operations-Business Segments-Wealth Management-Fee-Based Client Assets Activity and Average Fee Rate by Account Type" in Part II, Item 7 of the 2016 Form 10-K.

| September 2017 Form 10-Q | 14 |

| Management's Discussion and Analysis | |

Fee-Based Client Assets Rollforward

| $ in billions | At June 30, 2017 | Inflows | Outflows | Market Impact | At September 30, 2017 | |||||||||||||||

Separately managed accounts 1, 2 | $ | 237 | $ | 8 | $ | (5 | ) | $ | 3 | $ | 243 | |||||||||

Unified managed accounts 2 | 228 | 11 | (7 | ) | 7 | 239 | ||||||||||||||

Mutual fund advisory | 21 | 1 | (1 | ) | - | 21 | ||||||||||||||

Representative as advisor | 138 | 9 | (7 | ) | 4 | 144 | ||||||||||||||

Representative as portfolio manager | 321 | 18 | (11 | ) | 10 | 338 | ||||||||||||||

Subtotal | $ | 945 | $ | 47 | $ | (31 | ) | $ | 24 | $ | 985 | |||||||||

Cash management | 17 | 3 | (2 | ) | - | 18 | ||||||||||||||

Total fee-based | $ | 962 | $ | 50 | $ | (33 | ) | $ | 24 | $ | 1,003 | |||||||||

| $ in billions | At June 30, 2016 | Inflows | Outflows | Market Impact | At September 30, 2016 | |||||||||||||||

Separately managed accounts 1 | $ | 279 | $ | 8 | $ | (15 | ) | $ | 7 | $ | 279 | |||||||||

Unified managed accounts | 120 | 17 | (5 | ) | 4 | 136 | ||||||||||||||

Mutual fund advisory | 23 | - | (1 | ) | 1 | 23 | ||||||||||||||

Representative as advisor | 117 | 10 | (7 | ) | 3 | 123 | ||||||||||||||

Representative as portfolio manager | 265 | 19 | (12 | ) | 6 | 278 | ||||||||||||||

Subtotal | $ | 804 | $ | 54 | $ | (40 | ) | $ | 21 | $ | 839 | |||||||||

Cash management | 16 | 2 | (2 | ) | - | 16 | ||||||||||||||

Total fee-based | $ | 820 | $ | 56 | $ | (42 | ) | $ | 21 | $ | 855 | |||||||||

| $ in billions | At December 31, 2016 | Inflows | Outflows | Market Impact | At September 30, | |||||||||||||||

Separately managed accounts 1, 2 | $ | 222 | $ | 24 | $ | (16 | ) | $ | 13 | $ | 243 | |||||||||

Unified managed accounts 2 | 204 | 36 | (22 | ) | 21 | 239 | ||||||||||||||

Mutual fund advisory | 21 | 1 | (3 | ) | 2 | 21 | ||||||||||||||

Representative as advisor | 125 | 27 | (20 | ) | 12 | 144 | ||||||||||||||

Representative as portfolio manager | 285 | 57 | (29 | ) | 25 | 338 | ||||||||||||||

Subtotal | $ | 857 | $ | 145 | $ | (90 | ) | $ | 73 | $ | 985 | |||||||||

Cash management | 20 | 9 | (11 | ) | - | 18 | ||||||||||||||

Total fee-based client assets | $ | 877 | $ | 154 | $ | (101 | ) | $ | 73 | $ | 1,003 | |||||||||

| $ in billions | At December 31, 2015 | Inflows | Outflows | Market Impact | At September 30, 2016 | |||||||||||||||

Separately managed accounts 1 | $ | 283 | $ | 24 | $ | (31 | ) | $ | 3 | $ | 279 | |||||||||

Unified managed accounts | 105 | 37 | (13 | ) | 7 | 136 | ||||||||||||||

Mutual fund advisory | 25 | 1 | (5 | ) | 2 | 23 | ||||||||||||||

Representative as advisor | 115 | 22 | (20 | ) | 6 | 123 | ||||||||||||||

Representative as portfolio manager | 252 | 48 | (32 | ) | 10 | 278 | ||||||||||||||

Subtotal | $ | 780 | $ | 132 | $ | (101 | ) | $ | 28 | $ | 839 | |||||||||

Cash management | 15 | 8 | (7 | ) | - | 16 | ||||||||||||||

Total fee-based client assets | $ | 795 | $ | 140 | $ | (108 | ) | $ | 28 | $ | 855 | |||||||||

Average Fee Rates 3

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| Fee Rate in bps | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Separately managed accounts 2 | 17 | 35 | 16 | 36 | ||||||||||||

Unified managed accounts 2 | 97 | 104 | 98 | 106 | ||||||||||||

Mutual fund advisory | 118 | 119 | 118 | 119 | ||||||||||||

Representative as advisor | 84 | 85 | 84 | 85 | ||||||||||||

Representative as portfolio manager | 94 | 98 | 96 | 99 | ||||||||||||

Subtotal | 76 | 76 | 76 | 77 | ||||||||||||

Cash management | 6 | 6 | 6 | 6 | ||||||||||||

Total fee-based client assets | 75 | 75 | 75 | 76 | ||||||||||||

bps-Basis points

| 1. | Includes non-custody account values reflecting prior quarter-end balances due to a lag in the reporting of asset values by third-party custodians. |

| 2. | A shift in client assets of approximately $66 billion in the fourth quarter of 2016 from separately managed accounts to unified managed accounts resulted in a lower average fee rate for those platforms but did not impact the average fee rate for total fee-based client assets. |

| 3. | Certain data enhancements made in the first quarter of 2017 resulted in a modification to the "Fee Rate" calculations. Prior periods have been restated to reflect the revised calculations. |

| 15 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

Investment Management

Income Statement Information

Three Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Revenues | ||||||||||||

Investment banking | $ | - | $ | (2 | ) | N/M | ||||||

Trading | (7 | ) | (3 | ) | (133)% | |||||||

Investments | 114 | 51 | 124% | |||||||||

Asset management, distribution and administration fees | 568 | 508 | 12% | |||||||||

Other | 1 | (3 | ) | 133% | ||||||||

Total non-interest revenues | 676 | 551 | 23% | |||||||||

Interest income | 1 | 1 | -% | |||||||||

Interest expense | 2 | - | N/M | |||||||||

Net interest | (1 | ) | 1 | (200)% | ||||||||

Net revenues | 675 | 552 | 22% | |||||||||

Compensation and benefits | 311 | 237 | 31% | |||||||||

Non-compensation expenses | 233 | 218 | 7% | |||||||||

Total non-interest expenses | 544 | 455 | 20% | |||||||||

Income from continuing operations before income taxes | 131 | 97 | 35% | |||||||||

Provision for income taxes | 16 | 31 | (48)% | |||||||||

Net income | 115 | 66 | 74% | |||||||||

Net income (loss) applicable to noncontrolling interests | 1 | (1 | ) | 200% | ||||||||

Net income applicable to | $ | 114 | $ | 67 | 70% | |||||||

Nine Months Ended September 30, | ||||||||||||

| $ in millions | 2017 | 2016 | % Change | |||||||||

Revenues | ||||||||||||

Investment banking | $ | - | $ | (1 | ) | N/M | ||||||

Trading | (21 | ) | (8 | ) | (163)% | |||||||

Investments | 337 | 37 | N/M | |||||||||

Commissions and fees | - | 3 | N/M | |||||||||

Asset management, distribution and administration fees | 1,624 | 1,551 | 5% | |||||||||

Other | 9 | 28 | (68)% | |||||||||

Total non-interest revenues | 1,949 | 1,610 | 21% | |||||||||

Interest income | 3 | 5 | (40)% | |||||||||

Interest expense | 3 | 3 | -% | |||||||||

Net interest | - | 2 | N/M | |||||||||

Net revenues | 1,949 | 1,612 | 21% | |||||||||

Compensation and benefits | 878 | 688 | 28% | |||||||||

Non-compensation expenses | 695 | 665 | 5% | |||||||||

Total non-interest expenses | 1,573 | 1,353 | 16% | |||||||||

Income from continuing operations before income taxes | 376 | 259 | 45% | |||||||||

Provision for income taxes | 87 | 78 | 12% | |||||||||

Net income | 289 | 181 | 60% | |||||||||

Net income (loss) applicable to noncontrolling interests | 8 | (14 | ) | 157% | ||||||||

Net income applicable to | $ | 281 | $ | 195 | 44% | |||||||

N/M – Not Meaningful

Net Revenues

Investments

| • | Investments gains of $114 million in the current quarter compared with $51 million in the prior year quarter reflected higher carried interest principally in Infrastructure investments, partially offset by weaker investment performance which resulted in the reversal of previously accrued carried interest in Private Equity. |

| • | Investments gains of $337 million in the current year period compared with $37 million in the prior year period reflected higher carried interest and performance gains in all asset classes. |

Asset Management, Distribution and Administration Fees

| • | Asset management, distribution and administration fees of $568 million increased 12% in the current quarter compared to the prior year quarter as a result of higher average assets under management or supervision ("AUM") across all asset classes and higher performance fees. |

| • | Asset management, distribution and administration fees of $1,624 million increased 5% in the current year period compared to the prior year period primarily as a result of higher average AUM. |

See "Assets Under Management or Supervision" herein.

Non-interest Expenses

Non-interest expenses of $544 million in the current quarter and $1,573 million in the current year period increased 20% and 16% from the comparable prior periods primarily due to higher Compensation and benefits expenses.

| • | Compensation and benefits expenses increased in the current quarter and current year period due to higher discretionary incentive compensation and an increase in deferred compensation associated with carried interest. |

| • | Non-compensation expenses increased in the current quarter and current year period primarily due to higher brokerage, clearing and exchange fees. |

Assets Under Management or Supervision

For a description of the asset classes and rollforward items in the following tables, see "Management's Discussion and Analysis of Financial Condition and Results of Operations-Business Segments-Investment Management-Assets Under Management or Supervision" in Part II, Item 7 of the 2016 Form 10-K.

| September 2017 Form 10-Q | 16 |

| Management's Discussion and Analysis | |

AUM Rollforwards

| $ in billions | At June 30, 2017 | Inflows | Outflows | Market Impact | Other 1 | At September 30, | ||||||||||||||||||

Equity | $ | 94 | $ | 5 | $ | (6 | ) | $ | 4 | $ | - | $ | 97 | |||||||||||

Fixed income | 66 | 7 | (5 | ) | 1 | - | 69 | |||||||||||||||||

Liquidity | 154 | 279 | (277 | ) | 1 | (1 | ) | 156 | ||||||||||||||||

Alternative / Other products | 121 | 5 | (3 | ) | 1 | 1 | 125 | |||||||||||||||||

Total AUM | $ | 435 | $ | 296 | $ | (291 | ) | $ | 7 | $ | - | $ | 447 | |||||||||||

Shares of minority stake assets | 8 | 7 | ||||||||||||||||||||||

| $ in billions | At June 30, 2016 | Inflows | Outflows | Market Impact | Other 1 | At September 30, 2016 | ||||||||||||||||||

Equity | $ | 81 | $ | 4 | $ | (6 | ) | $ | 4 | $ | - | $ | 83 | |||||||||||

Fixed income | 61 | 6 | (5 | ) | 1 | - | 63 | |||||||||||||||||

Liquidity | 149 | 358 | (352 | ) | (1 | ) | - | 154 | ||||||||||||||||

Alternative / Other products | 115 | 4 | (4 | ) | 2 | - | 117 | |||||||||||||||||

Total AUM | $ | 406 | $ | 372 | $ | (367 | ) | $ | 6 | $ | - | $ | 417 | |||||||||||

Shares of minority stake assets | 8 | 7 | ||||||||||||||||||||||

| $ in billions | At December 31, 2016 | Inflows | Outflows | Market Impact | Other 1 | At September 30, | ||||||||||||||||||

Equity | $ | 79 | $ | 16 | $ | (16 | ) | $ | 17 | $ | 1 | $ | 97 | |||||||||||

Fixed income | 60 | 20 | (16 | ) | 3 | 2 | 69 | |||||||||||||||||

Liquidity | 163 | 915 | (923 | ) | 1 | - | 156 | |||||||||||||||||

Alternative / Other products | 115 | 18 | (13 | ) | 5 | - | 125 | |||||||||||||||||

Total AUM | $ | 417 | $ | 969 | $ | (968 | ) | $ | 26 | $ | 3 | $ | 447 | |||||||||||

Shares of minority stake assets | 8 | 7 | ||||||||||||||||||||||

| $ in billions | At December 31, 2015 | Inflows | Outflows | Market Impact | Other 1 | At September 30, 2016 | ||||||||||||||||||

Equity | $ | 83 | $ | 14 | $ | (18 | ) | $ | 4 | $ | - | $ | 83 | |||||||||||

Fixed income | 60 | 18 | (19 | ) | 3 | 1 | 63 | |||||||||||||||||

Liquidity | 149 | 985 | (979 | ) | (1 | ) | - | 154 | ||||||||||||||||

Alternative / Other products | 114 | 18 | (18 | ) | 3 | - | 117 | |||||||||||||||||

Total AUM | $ | 406 | $ | 1,035 | $ | (1,034 | ) | $ | 9 | $ | 1 | $ | 417 | |||||||||||

Shares of minority stake assets | 8 | 7 | ||||||||||||||||||||||

Average AUM

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| $ in billions | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Equity | $ | 96 | $ | 83 | $ | 90 | $ | 81 | ||||||||

Fixed income | 68 | 62 | 65 | 61 | ||||||||||||

Liquidity | 156 | 151 | 155 | 149 | ||||||||||||

Alternative / Other products | 123 | 116 | 120 | 115 | ||||||||||||

Total AUM | $ | 443 | $ | 412 | $ | 430 | $ | 406 | ||||||||

Shares of minority stake assets | 7 | 7 | 7 | 8 | ||||||||||||

Average Fee Rate

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| Fee Rate in bps | 2017 | 2016 | 2017 | 2016 | ||||||||||||

Equity | 75 | 74 | 74 | 72 | ||||||||||||

Fixed income | 34 | 32 | 33 | 32 | ||||||||||||

Liquidity | 18 | 18 | 18 | 18 | ||||||||||||

Alternative / Other products | 68 | 73 | 69 | 76 | ||||||||||||

Total AUM | 47 | 47 | 46 | 48 | ||||||||||||

AUM-Assets under management or supervision

bps-Basis points

| 1. | Includes distributions and foreign currency impact. |

| 17 | September 2017 Form 10-Q |

| Management's Discussion and Analysis | |

Supplemental Financial Information and Disclosures

U.S. Bank Subsidiaries