UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017 |

|

OR |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________________ to ________________ |

Commission file number: 1-35335

Groupon, Inc.

(Exact name of registrant as specified in its charter)

Delaware |

| 27-0903295 |

(State or other jurisdiction of |

| (I.R.S. Employer |

incorporation or organization) |

| Identification No.) |

|

|

|

600 West Chicago Avenue, Suite 400 Chicago, Illinois |

| 60654 |

(Address of principal executive offices) |

| (Zip Code) |

312-334-1579

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common Stock, par value $0.0001 |

| Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x | No ¨ |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨

Non-accelerated filer (Do not check if a smaller reporting company) ¨ Smaller reporting company ¨

Emerging growth company ¨

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ¨ No x

As of June 30, 2017, the aggregate market value of shares held by non-affiliates of the registrant was $1,597,986,820 based on the number of shares of common stock held by non-affiliates as of June 30, 2017 and based on the last reported sale price of the registrant's common stock on June 30, 2017.

As of February 12, 2018, there were 561,532,375 shares of the registrant's common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Report, to the extent not set forth herein, is incorporated herein by reference from the registrant's definitive proxy statement relating to the Annual Meeting of Stockholders to be held in 2018 , which definitive proxy statement shall be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Report relates.

1

TABLE OF CONTENTS

PART I | Page |

Forward-Looking Statements | 3 |

Item 1. Business | 3 |

Item 1A. Risk Factors | 10 |

Item 1B. Unresolved Staff Comments | 28 |

Item 2. Properties | 28 |

Item 3. Legal Proceedings | 28 |

Item 4. Mine Safety Disclosures | 28 |

PART II |

|

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 29 |

Item 6. Selected Financial Data | 32 |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations | 34 |

Item 7A. Quantitative and Qualitative Disclosure about Market Risk | 70 |

Item 8. Financial Statements and Supplementary Data | 71 |

Item 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 172 |

Item 9A. Controls and Procedures | 172 |

Item 9B. Other Information | 174 |

PART III |

|

Item 10. Directors, Executive Officers and Corporate Governance | 175 |

Item 11. Executive Compensation | 175 |

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 175 |

Item 13. Certain Relationships and related Transactions, and Director Independence | 175 |

Item 14. Principal Accountant Fees and Services | 175 |

Part IV |

|

Item 15. Exhibits and Financial Statement Schedule | 176 |

______________________________________________________

2

PART I

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including statements regarding our future results of operations and financial position, business strategy and plans and our objectives for future operations. The words "may," "will," "should," "could," "expect," "anticipate," "believe," "estimate," "intend," "continue" and other similar expressions are intended to identify forward-looking statements. We have based these forward looking statements largely on current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives, and financial needs. These forward-looking statements involve risks and uncertainties that could cause our actual results to differ materially from those expressed or implied in our forward-looking statements. Such risks and uncertainties include, but are not limited to, risk related to volatility in our operating results; execution of our business and marketing strategies; retaining existing customers and adding new customers; challenges arising from our international operations, including fluctuations in currency exchange rates, legal and regulatory developments and any potential adverse impact from the United Kingdom's likely exit from the European Union; retaining and adding high quality merchants; our voucherless offerings; cybersecurity breaches; competing successfully in our industry; changes to merchant payment terms; providing a strong mobile experience for our customers; maintaining our information technology infrastructure; delivery and routing of our emails; claims related to product and service offerings; managing inventory and order fulfillment risks; litigation; managing refund risks; retaining and attracting members of our executive team; completing and realizing the anticipated benefits from acquisitions, dispositions, joint ventures and strategic investments; lack of control over minority investments; tax liabilities; tax legislation; compliance with domestic and foreign laws and regulations, including the CARD Act, GDPR and regulation of the Internet and e-commerce; classification of our independent contractors; protecting our intellectual property; maintaining a strong brand; customer and merchant fraud; payment-related risks; our ability to raise capital if necessary and our outstanding indebtedness; global economic uncertainty; our common stock, including volatility in our stock price; our senior convertible notes; our ability to realize the anticipated benefits from the hedge and warrant transactions; and those risks and other factors discussed in Item 1A. Risk Factors of this Annual Report on Form 10-K, as well as in our consolidated financial statements, related notes, and the other financial information appearing elsewhere in this report and our other filings with the Securities and Exchange Commission, or the SEC. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. We do not intend, and undertake no obligation, to update any of our forward-looking statements after the date of this report to reflect actual results or future events or circumstances. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

As used herein, "Groupon," "we," "our," and similar terms include Groupon, Inc. and its subsidiaries, unless the context indicates otherwise.

ITEM 1: BUSINESS

Overview

Groupon is a global leader in local commerce, making it easy for people around the world to search and discover great businesses and merchandise. Our vision is to connect local commerce, increasing consumer buying power while driving more business to merchants through price and discovery. We want Groupon to be the destination that consumers check first when they are out and about; the place they start when they are looking to buy just about anything, anywhere, anytime. We provide consumers with savings and help them discover what to do, eat, see, buy and where to travel. By bringing the brick and mortar world of local commerce onto the Internet, Groupon is helping local merchants to attract customers and sell goods and services.

Groupon operates online local commerce marketplaces throughout the world that connect merchants to consumers by offering goods and services, generally at a discount. Consumers access those marketplaces through our websites, primarily localized groupon.com sites in many countries, and our mobile applications. More than two-thirds of the transactions on our platform are completed on mobile devices.

Our operations are organized into two segments: North America and International. We offer goods and services through our marketplaces in three primary categories: Local Deals ("Local"), Groupon Goods ("Goods") and Groupon Getaways ("Travel").

3

We act as a marketing agent primarily by selling vouchers ("Groupons") that can be redeemed for products or services with third-party merchants. We also sell merchandise inventory directly to customers.

Our results from 2017 were impacted by the strategic initiatives discussed in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations . Those results include the following:

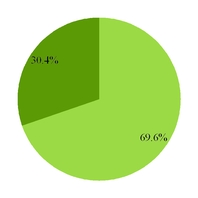

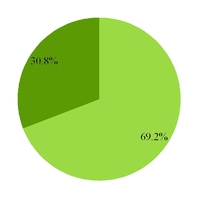

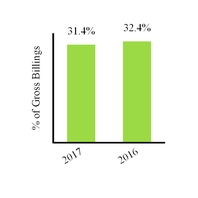

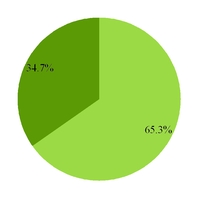

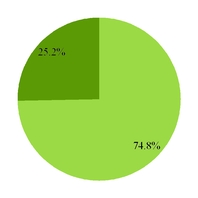

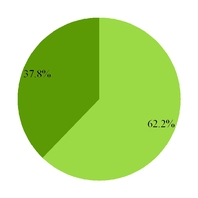

• | Gross billings decreased to $5.6 billion in 2017 , as compared to $5.7 billion in 2016 . In 2017 , 69.6% and 30.4% of our gross billings were generated in North America and International, respectively, as compared to 69.2% and 30.8% in 2016 . Gross billings represent the total dollar value of customer purchases of goods and services. Gross billings differs from our revenue, which is presented net of the merchant's share of the transaction price for transactions in which we act as a third-party marketing agent. Gross billings and revenue are the same for transactions in which we sell merchandise inventory directly to customers. |

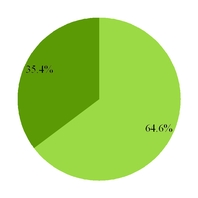

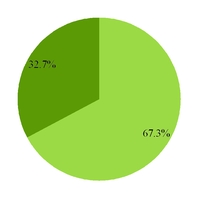

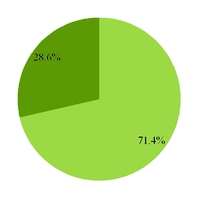

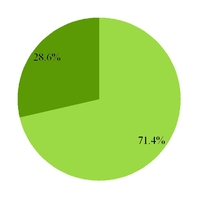

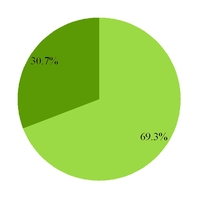

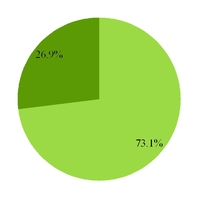

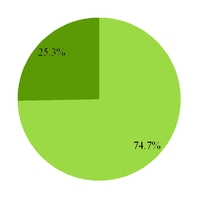

• | Revenue decreased to $2.8 billion in 2017 , as compared to $3.0 billion in 2016 . In 2017 , 67.3% and 32.7% of our revenue was generated in North America and International, respectively, as compared to 71.4% and 28.6% in 2016 . |

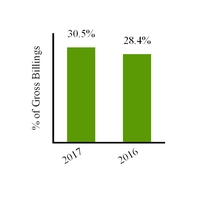

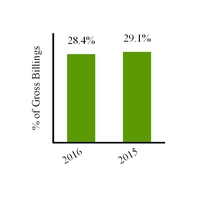

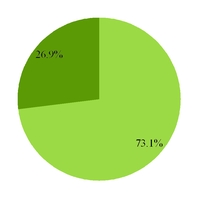

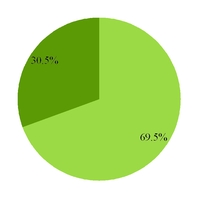

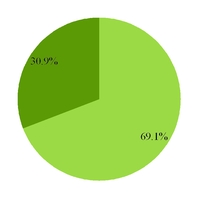

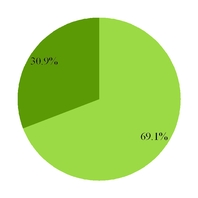

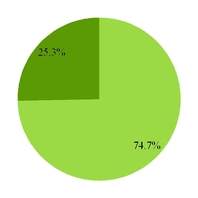

• | Gross profit of $1.3 billion in 2017 was consistent with the prior year. In 2017 , 69.5% and 30.5% of our gross profit was generated in North America and International, respectively, as compared to 69.1% and 30.9% in 2016 . |

• | Income from operations was $29.4 million in 2017 , as compared to a loss from operations of $100.2 million in 2016 . |

• | The number of active customers, which is defined as unique user accounts that have made a purchase within the last 12 months either through one of our online marketplaces or directly with a merchant for which we earned a commission, increased to 49.5 million as o f December 31, 2017 from 47.9 million as of December 31, 2016 . |

We are a Delaware corporation, incorporated on January 15, 2008 under the name "ThePoint.com, Inc." We started Groupon in October 2008 and officially changed our name to Groupon, Inc. by filing an amended certificate of incorporation on June 16, 2009. Our principal executive offices are located at 600 West Chicago Avenue, Suite 400, Chicago, Illinois 60654, and our telephone number at this address is (312) 334-1579. Our investor relations department can be reached through our investor relations hotline, which is (312) 999-3098. Our website is www.groupon.com . Information contained on our website is not a part of this Annual Report on Form 10-K. We completed our initial public offering in November 2011 and our common stock is listed on the Nasdaq Global Select Market under the symbol "GRPN."

GROUPON, the GROUPON logo and other GROUPON-formative marks are trademarks of Groupon, Inc. in the United States or other countries. This Annual Report on Form 10-K also includes other trademarks of Groupon and trademarks of other persons.

Our Strategy

Our goal is to continue to build marketplaces that our customers rely on to discover and save on amazing things to do, eat, see, buy and where to travel. Key elements of our strategy for 2018 include the following:

Grow long-term customer value. Our activities to grow long-term customer value are primarily focused on initiatives to improve the customer experience and marketing activities. We intend to improve the customer experience by continuing to invest in new products and technologies that will create a frictionless experience for our customers and merchants. As we continue to build out our marketplaces, we want our customers to have a superior, frictionless experience when they use our product whether finding, booking, buying or redeeming an offer. For merchants, this includes providing capabilities to manage demand for their goods and services and improving their ability to acquire customers. For consumers, this includes easily finding offers and accessing features that augment the overall experience, as well as seamlessly purchasing and redeeming offers. We are currently investing in initiatives to improve the purchase and redemption experience, such as enhancing our mobile applications, testing offerings with voucherless redemption resulting in cash back directly to customers' credit cards, which we refer to as Groupon+, and adding direct booking tools, including for health and beauty offerings. We believe that those initiatives may ultimately increase customer purchase frequency and drive growth in our business. Our marketing activities are critical to our ability to increase our global active customer base and improve gross profit per customer. We significantly increased our global marketing spend throughout 2016 and 2017 in order to drive customer growth and we expect that trend to continue. Our online marketing campaigns are primarily focused on customer acquisition, customer retention and driving repeat purchase behavior. We are focusing our offline

4

advertising activities on developing our brand strength and increasing awareness of our product and service offerings. We also use order discounts and other promotional initiatives to drive customer acquisition, activation and purchasing activity.

Building out a more extensive local commerce marketplace platform. We ultimately want Groupon to become a daily habit for our customers. In order to achieve that long-term aspiration, we believe that we need to significantly increase the offerings available through our online local commerce marketplaces to ensure that our customers can consistently find what they are looking for. Our initiatives to grow our inventory of deal offerings include entering into commercial agreements with third parties that enable us to feature additional merchant offerings through our marketplaces, identifying new distribution channels through which to sell our marketplace offerings and launching an internal initiative to optimize the activities performed by our sales teams. Additionally, we believe that our efforts to increase our active customer base and improve gross profit per customer may improve the health of our marketplaces, making our marketing and promotional services more effective for the merchants who feature offerings on our platform.

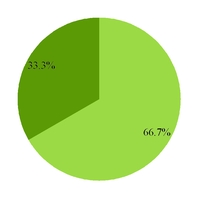

Unlocking the potential of our international markets. From 2015 to 2017, we reduced our global operating footprint from 47 countries to the 15 core countries that we believe have the greatest potential to favorably impact our results of operations. The gross profit generated by our International segment represented only 30.5% of our consolidated gross profit in 2017, and we are maintaining a long-term focus on driving International to ultimately achieve gross profit that is more comparable to North America. Our initiatives to grow International gross profit include increasing our international marketing spending, investing in more technology resources in order to expand and advance its product and service offerings, growing our inventory of deal offerings by entering into commercial agreements with third parties that enable us to feature additional merchant offerings through our marketplaces and other initiatives.

Our Business

We earn revenue from transactions in which we provide marketing services primarily by selling vouchers through our online local marketplaces that can be redeemed for goods or services with third-party merchants. Our third-party revenue from those transactions is reported on a net basis as the purchase price received from the customer for the voucher less an agreed upon portion of the purchase price paid to the merchant. We also earn revenue by selling merchandise inventory directly to customers through our online marketplaces. Our direct revenue from those transactions is the purchase price received from the customer.

Our business model has evolved in recent years from primarily an email-based "push" model with a limited number of deals offered at any given time to more extensive online "pull" marketplaces, where customers can come to Groupon's websites and mobile applications to search and browse for deals on goods and services. We also publish ratings and helpful tips from customers to highlight the unique aspects of local merchants, including merchants that have featured offerings through our marketplaces.

We offer goods and services through our online local marketplaces in three primary categories: Local, Goods and Travel. Collectively, Local and Travel comprise our "Services" offerings and Goods reflects our product offerings.

Local. Our Local category includes offerings from local and national merchants, as well as local events. Local also includes other revenue sources such as commission revenue and advertising revenue, as these revenue sources are primarily generated through our relationships with local and national merchants. Our local offerings comprise multiple subcategories, including events and activities, beauty and spa, health and fitness, food and drink, home and garden and automotive. National merchants also have used our marketplaces as an alternative to traditional marketing and brand advertising. Although our business today is weighted toward offerings from local merchants, we continue to feature offerings from national merchants to build our brand awareness, acquire new customers and generate additional revenue. In addition to local and national deals, we give consumers the ability to access digital coupons from thousands of retailers through our Coupons offering. We also offer deals on concerts, sports, theater and other live entertainment events. We are increasingly featuring offerings on our site from other online marketplaces to further expand local offerings.

Goods. In our Goods category, we earn direct revenue from transactions in which we sell merchandise inventory directly to customers, as well as third-party revenue from transactions in which third-party merchants sell products to customers through our marketplaces. Our Goods category offers customers the ability to find discounted merchandise across multiple product lines, including electronics, sporting goods, jewelry, toys, household items and apparel. We expect that we will continue to add new brands to our platform in order to expand our offerings.

Travel . Through our Travel category, we feature travel offers at both discounted and market rates, including hotels, airfare and package deals covering both domestic and international travel. For many of our travel offerings, the customer must contact

5

the merchant directly to make a travel reservation after purchasing a travel voucher from us. However, for some of our hotel offerings, customers make room reservations directly through our websites.

Distribution

Our customers access our online local commerce marketplaces through our mobile applications and our websites, which primarily consist of localized groupon.com sites in countries throughout the world . We use a variety of marketing channels to direct customers to the deal offerings available through these marketplaces, as described in the Marketing section below.

Consumers predominately access our offerings through our mobile applications and, to a lesser extent, through mobile web browsers. Our applications and mobile websites enable consumers to browse, purchase, manage and redeem deals on their mobile devices. In addition, the mobile experience leverages location in several ways, enabling consumers to filter by distance, discover deals near them and visualize the assortment of Groupon offers through a maps view. In the fourth quarter of 2017 , over 69% of our global transactions were completed on mobile devices.

Marketing

We primarily use marketing to acquire customers and promote awareness of our marketplaces and the services and product offerings available through those marketplaces. Consequently, marketing is an important part of our growth strategy and remains a key element of our business operations. We increased our global marketing spend by $48.7 million , or 13.8% , for the year ended December 31, 2017 as compared to the prior period. We expect to continue to invest in marketing in future periods in connection with our efforts to increase active customers and customer purchase frequency.

We use a variety of marketing channels to make customers aware of the deal offerings on our mobile and web platforms, including search engines, email and push notifications, affiliate channels, social and display advertising and offline marketing, which increased significantly during 2017 .

Search engines. Customers can access our deal offerings indirectly through third-party search engines. We use search engine optimization ("SEO") and marketing ("SEM") to increase the visibility of our offerings in web search results.

Email and push notifications. In North America and most of our international markets, we use targeting technology to determine which deal offerings to communicate to our subscribers based on their locations and personal preferences. A subscriber who clicks on a deal offering within an email or push notification is directed to our website or mobile application to learn more about the deal and be able to make a purchase.

Affiliate channels. We have an affiliate program that utilizes third parties to promote our deal offerings online. Affiliates earn commissions when customers access our deal offerings through links on their websites and make purchases on our platform. We expect to continue to leverage affiliate relationships to extend the distribution of our deals to a broad base of potential customers.

Social and display. We publish deals through various social networks and adapt our notifications to the particular format of each of these social networking platforms. Our websites and mobile application interfaces enable consumers to share deal offerings with their personal social networks. We also promote our deal offerings using display advertising on websites.

Television and other offline. In 2017 , we significantly increased the extent to which we use offline marketing such as television advertising, and to a lesser extent, print and radio advertising.

Our marketing activities also include elements that are not presented as Marketing on our consolidated statements of operations, such as order discounts and free shipping on qualifying merchandise sales.

6

Sales and Operations

Our sales force consists of approximately 2,400 merchant sales representatives and sales support staff, who build merchant relationships and provide local expertise. Our North American merchant sales representatives and support staff are primarily based in our offices in Chicago and Phoenix, and our international merchant sales representatives and support staff are based in their respective local offices. Our global sales and sales support headcount by segment as of December 31, 2017 was as follows:

North America | 872 | |

International | 1,535 | |

Total | 2,407 | |

Other key operational functions include deal managers, editorial, merchant services, customer service, technology, merchandising and logistics. Deal managers work with sales teams to optimize deal structure and pricing, as well as manage the category, discount and geographic mix of deals in their respective markets. Our editorial department is responsible for creating the written and visual content on the deals we offer. Merchant services representatives work with merchants to plan for increased customer traffic before an offering is active and serve as an ongoing point of contact for the merchant over the term of a deal. Our customer service department is responsible for answering questions received via phone, email and on public discussion boards regarding purchases, shipping status, returns and other areas of customer inquiry. Our technology team is focused on the design and development of new features and products, maintenance of our websites and development and maintenance of our internal systems. Merchandising and logistics personnel are responsible for managing inventory and the flow of products from suppliers to our customers.

Our websites are hosted at two U.S. data centers in California and at an international data center in Ireland. Our data centers host our public-facing websites and applications, as well as our back-end business intelligence systems. We employ security practices to protect and maintain the systems located at our data centers. We have invested in intrusion and anomaly detection tools to try to recognize intrusions to our websites. We engage independent third-party Internet security firms to regularly test the security of our websites and identify vulnerabilities. In financial transactions with customers conducted on our websites and mobile applications, we use data encryption protocols to secure information while in transit. See Risk Factors for additional information relating to cyber threats.

Competition

Our business is rapidly evolving and we face competition from a variety of sources. Some of our competitors offer deals as an add-on to their core business, and others have adopted a business model similar to ours. We also compete against companies that offer other types of advertising and promotional services to local businesses. In addition to such competitors, we expect to increasingly compete against other large Internet and technology-based businesses that have launched initiatives that are directly competitive to our core business. Such competitors may be much larger companies who have more resources and significantly greater scale. We also expect to compete against other Internet sites that are focused on specific communities or interests and offer coupons or discount arrangements related to such communities or interests. Further, as our business continues to evolve, we anticipate facing new competition. We believe the principal competitive factors in our markets include the following:

• | quality and performance of our merchants; |

• | size and composition of our customer base; |

• | mobile penetration; |

• | understanding of local business trends; |

• | ability to structure deal offerings to generate a positive return on investment for merchants; |

• | ability to generate large volumes of sales; and |

• | reputation, strength and recognition of brand. |

7

Although we believe that we compete favorably on the factors described above and benefit from scale, we anticipate that larger, more established companies may directly compete with us over time. Many of our current and potential competitors have longer operating histories, significantly greater financial, technical, marketing and other resources and larger customer bases than we do. These factors may allow our competitors to benefit from their existing customer base with lower acquisition costs or to respond more quickly than we can to new or emerging technologies and changes in customer requirements. These competitors may engage in more extensive research and development efforts, undertake more far-reaching marketing campaigns and adopt more aggressive pricing policies, which may allow them to build a larger subscriber base or to monetize that subscriber base more effectively than we do. Our competitors may develop products or services that are similar to our products and services or that achieve greater market acceptance than our products and services.

Seasonality

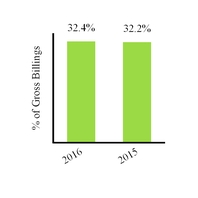

Some of our offerings experience seasonal buying patterns mirroring that of the larger consumer retail and e-commerce markets, where demand declines during customary summer vacation periods and increases during the fourth quarter holiday season. We believe that this seasonality pattern has affected, and will continue to affect, our business and quarterly sequential revenue growth rates. We recognized 30.7% , 30.0% and 29.7% of our annual revenue during the fourth quarter of 2017 , 2016 and 2015 , respectively.

Regulation

We are subject to a number of foreign and domestic laws and regulations that affect companies conducting business on the Internet. Additionally, those laws and regulations may be interpreted differently across domestic and foreign jurisdictions. As a company in a relatively new and rapidly innovating industry, we are exposed to the risk that many of those laws may evolve or be interpreted by regulators or in the courts in ways that could materially affect our business. Those laws and regulations may involve taxation, unclaimed property, intellectual property, product liability, travel, distribution, electronic contracts and other communications, competition, consumer protection, the provision of various online payment services, employee, merchant and customer privacy and data security or other areas.

The Credit Card Accountability Responsibility and Disclosure Act of 2009 (the "CARD Act"), as well as the laws of most states, contain provisions governing gift cards, gift certificates, stored value or pre-paid cards or coupons ("gift cards"). Groupon vouchers may be included within the definition of "gift cards" under many laws. In addition, certain foreign jurisdictions have laws that govern disclosure and certain product terms and conditions, including restrictions on expiration dates and fees, that may apply to Groupon vouchers. There are also a number of legislative proposals pending before the U.S. Congress, various state legislative bodies and foreign governments that could affect us, and our global operations may be constrained by regulatory regimes and laws in Europe and other jurisdictions outside the United States that may be more restrictive and adversely impact our business.

Various U.S. laws and regulations, such as the Bank Secrecy Act of 1970 (the "Bank Secrecy Act"), the Dodd-Frank Wall Street Reform and Consumer Protection Act, the USA PATRIOT Act and the CARD Act impose certain anti-money laundering requirements on companies that are financial institutions or that provide financial products and services. Those laws and regulations broadly define financial institutions to include money services businesses such as money transmitters, check cashers and sellers or issuers of stored value. Requirements imposed on financial institutions under those laws include customer identification and verification programs, record retention policies and procedures and transaction reporting. We do not believe that we are a financial institution subject to those laws and regulations.

We are subject to a variety of federal, state and international laws and regulations governing consumer data. The General Data Protection Regulation ("GDPR"), which was recently adopted by the European Union and will become effective in May 2018, requires companies to satisfy new requirements regarding the handling of personal and sensitive data, including its collection, use, protection and the ability of persons whose data is stored to correct or delete such data about themselves. Complying with the GDPR is expected to cause us to update certain business practices and systems. Non-compliance with GDPR could result in proceedings against us by governmental entities or others and fines up to the greater of €20 million or 4% of annual global revenues.

Intellectual Property

We protect our intellectual property rights by relying on federal, state and common law rights, as well as contractual restrictions. We control access to our proprietary technology by entering into confidentiality and invention assignment agreements with our employees and contractors, and confidentiality agreements with third parties.

In addition to those contractual arrangements, we also rely on a combination of trade secrets, copyrights, trademarks, service marks, trade dress, domain names and patents to protect our intellectual property. Groupon and its related entities own a

8

number of trademarks and service marks registered or pending in the United States and internationally. In addition, we own a number of issued patents and pending patent applications in the United States and internationally and own and have applied for copyright registrations.

Circumstances outside our control could pose a threat to our intellectual property rights and the efforts we have taken to protect our proprietary rights may not be sufficient or effective or deter independent development of equivalent or superior intellectual property rights by others. Any significant impairment of our intellectual property rights could harm our business or our ability to compete. Also, protecting our intellectual property rights is costly and time-consuming. Any unauthorized disclosure or use of our intellectual property could make it more expensive to do business and harm our operating results.

Companies in the Internet, technology and other industries as well as non-practicing entities may own large numbers of patents, copyrights and trademarks or other intellectual property rights and may request license agreements, threaten litigation or file suit against us based on allegations of infringement or other violations of intellectual property rights. We are currently subject to, and expect to face in the future, lawsuits and allegations that we have infringed the intellectual property rights of third parties. As our business grows, we will likely face more claims of infringement, and may experience an adverse result which could impact our business and/or our operating results.

We have received in the past, and we anticipate we will receive in the future, communications alleging that items offered or sold through our website infringe third-party copyrights, trademarks, patents and trade names or other intellectual property rights or that we have otherwise infringed third parties' past, current or future intellectual property rights. We may be unable to prevent third parties from offering and selling unlawful or infringing goods or goods of disputed authenticity, and we may be subject to allegations of civil or criminal liability for unlawful activities carried out by third parties through our website. We may implement measures in an effort to protect against these potential liabilities that could require us to spend substantial resources and/or to reduce revenues by discontinuing certain service offerings. Any costs incurred as a result of liability or asserted liability relating to the sale of unlawful goods or the unlawful sale of goods could harm our business.

Employees

As of December 31, 2017 , there were 2,639 employees in our North America segment, consisting of 872 sales representatives and 1,767 corporate, operational and customer service representatives, and 4,033 employees in our International segment, consisting of 1,535 sales representatives and 2,498 corporate, operational and customer service representatives.

Executive Officers

The following table sets forth information about our executive officers:

Name |

| Age | Position | ||||||||||

|

|

| |||||||||||

Rich Williams | 43 | Chief Executive Officer and Director | |||||||||||

Michael Randolfi | 45 | Chief Financial Officer | |||||||||||

Steve Krenzer | 59 | Chief Operating Officer | |||||||||||

Dane Drobny | 50 | General Counsel and Corporate Secretary | |||||||||||

Brian Stevens | 43 | Chief Accounting Officer and Treasurer | |||||||||||

Rich Williams has served as our Chief Executive Officer and a member of our Board of Directors since November 2015. Prior to this role, Mr. Williams served as our Chief Operating Officer since June 2015 and President of North America since October 2014. He joined the Company in June 2011 as Senior Vice President of Marketing. Prior to joining Groupon, Mr. Williams served in a variety of marketing leadership roles at Amazon.com, Inc. (NASDAQ: AMZN) from January 2008 to June 2011, most recently as the Director, Paid Traffic leading global advertising. Prior to joining Amazon, he spent nearly seven years in sales and marketing leadership roles at Experian plc (LSE: EXPN), a global information services company.

Michael Randolfi has served as our Chief Financial Officer since April 2016. Prior to joining Groupon, Mr. Randolfi served as the Chief Financial Officer of Orbitz Worldwide, Inc. (NYSE: OWW) from March 2013 until November 2015 (when he departed following its acquisition by Expedia, Inc.). Prior to joining Orbitz, Mr. Randolfi served as Vice President and then as Senior Vice President and Controller at Delta Air Lines (NYSE: DAL) from February 2008 to February 2013. From June 1999 to February 2008, he held various executive positions at Delta Air Lines in financial planning and analysis, controllership and treasury.

9

Prior to his 14-year career at Delta, Mr. Randolfi held positions with Continental Airlines (NYSE: UAL) and Raymond James and Associates (NYSE: RJF). Mr. Randolfi is a CPA and a certified management accountant.

Steve Krenzer has served as our Chief Operating Officer since November 2017. Prior to joining Groupon, Mr. Krenzer was the Chief Executive Officer of Core Digital Media, Inc. from October 2012 to November 2017. From November 1996 to October 2012, Mr. Krenzer held a variety of senior executive positions at Experian (LSE: EXPN), ultimately serving as President of Interactive Media.

Dane Drobny has served as our General Counsel and Corporate Secretary since July 2014. Prior to joining Groupon, Mr. Drobny was Senior Vice President, General Counsel and Corporate Secretary at Sears Holdings Corporation (NASDAQ: SHLD) from May 2010 to June 2014. Prior to joining Sears Holdings, he spent 17 years at the international law firm of Winston & Strawn LLP, most recently as a partner.

Brian Stevens has served as our Chief Accounting Officer and Treasurer since May 2016 and as our Chief Accounting Officer since September 2012. Prior to joining Groupon, Mr. Stevens spent 16 years with KPMG LLP, most recently as a partner. Mr. Stevens spent five years in KPMG's Department of Professional Practice and was a practice fellow at the Financial Accounting Standards Board from 2006 to 2008. Mr. Stevens is a member of the American Institute of Certified Public Accountants and served on its Financial Reporting Executive Committee (FinREC) from November 2013 to January 2018.

Available Information

The Company electronically files reports with the SEC. The public may read and copy any materials the Company has filed with the SEC at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site (www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. Copies of the Company's Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are also available free of charge through the Company's website (www.groupon.com), as soon as reasonably practicable after electronically filing with or otherwise furnishing such information to the SEC, and are available in print to any stockholder who requests them. The Company's Code of Conduct, Corporate Governance Guidelines and committee charters are also posted on the site. The Company uses its Investor Relations website (investor.groupon.com) and its blog (www.groupon.com/blog) as a means of disclosing material non-public information and for complying with its disclosure obligations under Regulation FD. Information contained on our website and blog is not a part of this Annual Report on Form 10-K.

ITEM 1A: RISK FACTORS

Our business, prospects, financial condition, operating results and the trading price of our common stock could be materially adversely affected by the risks described below. In assessing those risks, you should also refer to the other information contained in this Annual Report on Form 10-K, including Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A) and the consolidated financial statements and the related notes in Part II, Item 8. Financial Statements and Supplementary Data of this Annual Report on Form 10-K.

Risks Related to Our Business

Our operating results may vary significantly from quarter to quarter.

Our operating results may vary significantly from quarter to quarter due to seasonality and other reasons such as the rapidly evolving nature of our business. We believe that our ability to achieve and maintain profitability will depend, among other factors, on our ability to:

• | acquire new customers and retain existing customers; |

• | attract and retain quality merchants; |

• | effectively address and respond to challenges in international markets; |

10

• | expand the number, variety and relevance of products and deals we offer, including through third party business partners and technology integrations, as we attempt to build a more complete local marketplace; |

• | achieve additional mobile adoption to capitalize on customers' continued shift toward mobile device usage; |

• | increase the awareness of our brand; |

• | successfully achieve the anticipated benefits of business combinations or acquisitions, strategic investments, divestitures and restructuring activities; |

• | provide a superior customer service experience for our customers; |

• | avoid interruptions to our services, including as a result of attempted or successful cybersecurity attacks or breaches; |

• | respond to continuous changes in consumer and merchant use of technology; |

• | react to challenges from existing and new competitors; |

• | respond to seasonal changes in supply and demand; and |

• | address challenges from existing and new laws and regulations. |

In addition, our margins and profitability may depend on our product sales mix, our geographic revenue mix and merchant pricing terms. In recent periods, we have shifted the focus of our offerings to our Local category, which tend to have a higher margin and more differentiation than our Goods category. We believe that this shift should provide us with a greater opportunity for long-term gross profit growth. If we are not successful in achieving this objective, our business, financial position and results of operations could be harmed. Further, sales in our Goods category may constitute a greater percentage of our sales in certain periods relative to other categories, which may result in lower margins and profitability during those periods. Accordingly, our profitability may vary significantly from quarter to quarter.

Our strategy to grow our business may not be successful and may expose us to additional risks.

Our strategy to grow our business focuses on several key priorities including increasing customer value, building out a more extensive local commerce marketplace platform, improving the customer experience and unlocking the potential of our international markets. We have undertaken several initiatives as we execute this strategy. For example, we have continued to invest in growth by increasing our marketing investment as we attempt to increase our active customer base, increase customer purchase frequency, improve brand awareness and introduce new products.

In addition, as we focus on building out a more extensive local commerce marketplace platform, we have also devoted significant resources to attracting new merchants, retaining merchants who are willing to run deals on a continuous basis with us and engaging with third-party business partners via technology integrations in order to build a significant inventory for our customers. We have accepted, and expect to continue to accept, a lower portion of the gross billings from some of our merchants and business partners as we expand our marketplaces and introduce new products. In addition, we are continuously refining our process for presenting the most relevant deals to our customers based on their personal preferences and location. We are also continuing our efforts to optimize the mix of products that we offer. If we are not successful in achieving these objectives, our business, financial position and results of operations could be harmed. Further, we have implemented technology integrations with a number of third party business partners that we rely on to support various products (such as Groupon+ and other voucherless offerings) and augment inventory across all categories of our business. Significant disruption in these services, or breakdown of these relationships, could negatively impact our ability to grow.

We also have prioritized building a great product and customer experience. To this end, we have continued to invest in improving the customer experience, from search to purchase to redemption, in removing friction from our websites and mobile applications and in product development. For example, Groupon+, our voucherless card-linked offer product, is a new frictionless offering that we believe will improve the customer experience. Additionally, we have continued to expand our direct booking offerings that allow for seamless mobile redemption. There are no assurances that Groupon+, our booking features, third party offerings and other new products and deal structures will be successful in improving the customer experience, increasing our customer and merchant base, or improving customer purchase frequency in the short term or at all. If we are unable to realize expected outcomes from Groupon+ and other new offerings and deal structures, our business and operating results may be harmed.

11

With respect to our international markets, following the completion of our restructuring plan in 2017, we expect to continue to focus on improving our products and customer experience and applying our North American playbook to our International business. If we are unable to successfully execute these initiatives and unlock the potential of our international markets, our business and operating results may be harmed.

Our efforts to execute our strategy may prove more difficult than we currently anticipate, and we may not succeed in realizing the benefits of these efforts, including increasing gross profit, unit growth or gross profit per customer, in a short time frame or at all.

Our financial results may be adversely affected if we are unable to execute on our marketing strategy.

Our marketing strategy is focused on customer acquisition, activation and conversion, purchase frequency and mobile application downloads, as well as increasing awareness of our brand and online marketplaces and introducing consumers and merchants to new products. In furtherance of this strategy, we increased our marketing expense to $400.9 million during 2017 as compared to $352.2 million during 2016, and we expect our marketing spend to increase in 2018. We also expect to continue to focus on maintaining a payback period on our global marketing spend of approximately 12 to 18 months; however, there are no assurances that we will be able to achieve this result. If any of our assumptions regarding our marketing activities and strategies prove incorrect, including with respect to payback periods and the efficiency of our marketing spend, our ability to generate gross profit from our investments may be less than we anticipated. In such case, we may need to increase marketing expenditures or otherwise alter our strategy and our results of operations could be negatively impacted.

If we fail to retain our existing customers or acquire new customers, our operating results and business will be harmed.

We must continue to retain and acquire customers who make purchases on our platform in order to increase profitability. Further, as our customer base evolves, the composition of our customers may change in a manner that makes it more difficult to generate revenue to offset the loss of existing customers and the costs associated with acquiring and retaining customers and to maintain or increase our customers' purchase frequency. If customers do not perceive our offerings to be attractive or if we fail to introduce new and more relevant deals or increase awareness and understanding of the offerings on our marketplace platform, we may not be able to retain or acquire customers at levels necessary to grow our business and profitability. Further, the organic traffic to our websites and mobile applications, including traffic from consumers responding to our emails, has declined in recent years, such that an increasing proportion of our traffic is generated from paid marketing channels, such as search engine marketing. If we are unable to acquire new customers in numbers sufficient to grow our business and offset the number of existing active customers that have ceased to make purchases, or if new customers do not make purchases at expected levels, our profitability may decrease and our operating results may be adversely affected.

Our international operations are subject to varied and evolving commercial and regulatory challenges, and our inability to adapt to the diverse and changing landscapes of our international markets may adversely affect our business.

Our international operations require management attention and resources and also require us to localize our services to conform to a wide variety of local cultures, business practices, laws and policies. Our international operations are subject to numerous risks, including the following:

• | our ability to maintain merchant and customer satisfaction such that our marketplace will continue to attract high quality merchants; |

• | our ability to successfully respond to macroeconomic challenges, including by optimizing our deal mix to take into account consumer preferences at a particular point in time; |

• | political, economic and civil instability and uncertainty (including acts of terrorism, civil unrest, labor unrest, violence and outbreaks of war); |

• | risks associated with the withdrawal of the United Kingdom from the European Union ("Brexit"), including volatility in worldwide and European financial markets, potential restrictions on the free movement of goods and labor between the United Kingdom and the European Union and other potential impediments to our ability to transact within and between each of the United Kingdom and the European Union; |

• | currency exchange rate fluctuations; |

12

• | strong local competitors, who may better understand the local market and/or have greater resources in the local market; |

• | different regulatory or other legal requirements, including regulation of gift cards and coupon terms, Internet services, professional selling, distance selling, bulk emailing, privacy and data protection (including GDPR, which will become effective in May 2018), cybersecurity, business licenses and certifications, taxation (including the European Union's voucher directive and similar regulations), consumer protection laws including those restricting the types of services we may offer (e.g., medical-related services), banking and money transmitting, that may limit or prevent the offering of our services in some jurisdictions, cause unanticipated compliance expenses or limit our ability to enforce contractual obligations; |

• | our ability to use a common technology platform in our North America and International segments to operate our business without significant business interruptions or delays; |

• | difficulties in integrating with local payment providers, including banks, credit and debit card networks and electronic funds transfer systems; |

• | different employee/employer relationships and the existence and actions of workers' councils and labor unions; |

• | difficulty in staffing, developing and managing foreign operations as a result of distance, language barriers and cultural differences; |

• | shorter payment cycles and greater problems in collecting accounts receivable; |

• | higher Internet service provider costs; |

• | seasonal reductions in business activity; |

• | expenses associated with localizing our products; and |

• | differing intellectual property laws. |

We are subject to complex foreign and U.S. laws and regulations that apply to our international operations, such as data privacy and protection requirements, including GDPR, the Foreign Corrupt Practices Act, the UK Anti-Bribery Act and similar local laws prohibiting certain payments to government officials, banking and payment processing regulations and anti-competition regulations, among others. The cost of complying with these various, and sometimes conflicting, laws and regulations is substantial. We have implemented and continue to implement policies and procedures to ensure compliance with these laws and regulations, however, we cannot ensure that our employees, contractors, or agents will not violate our policies. Changing laws, regulations and enforcement actions in the United States and throughout the world could harm our business. If commercial and regulatory constraints in our international markets restrict our ability to conduct our operations or execute our strategic plan, our business may be adversely affected.

Our future success depends upon our ability to attract and retain high quality merchants.

We must continue to attract and retain high quality merchants in order to increase profitability. We depend on our ability to attract and retain merchants that are prepared to offer products or services on compelling terms through our marketplaces and provide our customers with a good experience. We do not have long-term arrangements to guarantee the availability of deals that offer attractive quality, value and variety to customers or favorable payment terms to us. If merchants decide that utilizing our services no longer provides an effective means of attracting new customers or selling their goods and services, they may stop working with us or negotiate to pay us lower margins or fees. In addition, current or future competitors may accept lower margins, or negative margins, to secure merchants offers that attract attention and acquire new customers. If competitors engage in group buying initiatives in which merchants receive a higher portion of the purchase price than we currently offer, or if we target merchants who will only agree to run deals if they receive a higher portion of the proceeds, we may receive a lower portion of the gross billings on deals offered through our marketplaces. In addition, we may experience attrition in our merchants due to shifts in our business model and the way we pay merchants, or in the ordinary course of business resulting from several factors, including losses to competitors and merchant closures or merchant bankruptcies. If we are unable to attract and retain high quality merchants in numbers sufficient to grow our business, or if merchants are unwilling to offer products or services with compelling terms through our marketplaces or offer favorable payment terms to us, our operating results may be adversely affected.

13

Our business is exposed to risks associated with our voucherless offerings.

We are developing and scaling voucherless offerings, including offers that are linked to customer credit cards, through our Groupon+ product and direct booking deals in our Health, Beauty & Wellness and Things To Do categories. Although we believe that voucherless offerings have the potential to increase customer purchase frequency and generate gross profit growth over the long term, there are no assurances that we will be able to scale our voucherless products or that our voucherless products will be successful in increasing customer purchase frequency or gross profit growth, if and when scaled. If we are unable to grow the number of voucherless products in our marketplaces, our results of operations may be adversely affected. In addition, as we scale our Groupon+ product, including investment in efforts to increase customer awareness of Groupon+ offerings, we may experience a short term negative impact to our financial performance.

Further, we currently depend on third party business partners and technology integrations for many of our voucherless offerings. Specifically, our ability to offer Groupon+ currently depends on our arrangements with card brand networks. In the event any card brand network no longer supports our Groupon+ offerings or significantly changes their fee requirements in connection with this service, Groupon+ may not grow or may fail, and our results of operations and financial condition could be adversely affected.

Further, Groupon+ deals, which offer cash back to customers' payment card statements based on qualifying purchases at participating merchants, involve the Company collecting fees from the merchant, rather than collecting payment from the customer and then remitting a portion of the proceeds to the merchant (as with the sale of vouchers). Accordingly, our gross billings are expected to be reduced if and when Groupon+ offerings (or similarly structured products) become a larger portion of our overall product mix.

We may be subject to breaches of our information technology systems, which could harm our relationships with our customers and merchants, subject us to negative publicity and litigation, and cause substantial harm to our business.

In operating a global online business, we and our third-party service providers maintain significant proprietary information and manage large amounts of personal data and confidential information about our employees, customers and merchants. We and such service providers are at constant risk of cyber-attacks or cyber intrusions via the Internet, computer viruses, break-ins, malware, phishing attacks, hacking, denial-of-service attacks or other attacks and similar disruptions from the unauthorized use of or access to computer systems (including from internal and external sources). These types of incidents have become more prevalent and pervasive across industries, including in our industry, and such attacks on our systems are expected to occur in the future. Further, we believe that we are a compelling target for such attacks as a result of the high profile of our brand and the amount and type of information we maintain relating to our customers and merchants. Any such incident could lead to interruptions, delays or website outages, causing loss of critical data or the unauthorized disclosure or use of personally identifiable or other confidential information.

Any failure to prevent or mitigate cybersecurity breaches or other improper access to, or disclosure of, our data or confidential information, including non-public financial information, could result in the loss or misuse of such data or information, negatively impacting customers' and merchants' confidence in the security of our services and potentially resulting in significant customer or merchant attrition, a decline in customer purchase frequency, litigation and/or regulatory investigations, and/or damage to our brand and reputation.

Our risk and exposure to these matters remains heightened because of, among other things, the evolving nature of these threats, our prominent size and scale, the large number of transactions that we process, our geographic footprint and international presence, our use of open source software, the complexity of our systems, the maturity of our systems, processes and risk management framework, our number of employees, the location of our businesses and data storage facilities, the jurisdictions in which we operate and the various and evolving laws and regulatory schemes governing data and data protection applicable to us, the extent to which our current systems, controls, processes and practices permit us to detect, log and monitor security events, our use of cloud based technologies and the outsourcing of some of our business operations.

Although cybersecurity and the continued development and enhancement of our controls, processes and practices designed to protect our systems, computers, software, data and networks from attack, damage or unauthorized access are a high priority for us, our activities and investment may not be deployed quickly enough or successfully protect our systems against all vulnerabilities, including technologies developed to bypass our security measures or zero day vulnerabilities. In addition, outside parties may attempt to fraudulently induce employees, merchants or customers to disclose access credentials or other sensitive information in order to gain access to our secure systems and networks. We also may be subject to additional vulnerabilities as we integrate the systems, computers, software and data of acquired businesses into our networks and separate the systems, computers, software and data of disposed businesses from our networks.

14

We regularly evaluate and assess our systems and the controls, processes and practices to protect those systems and also conduct penetration testing against our own system. The evaluations, assessments and testing identify areas of potential weakness in, and suggested improvements to, the maturity of our systems, processes, and risk management framework as well as vulnerabilities in those systems, processes, and risk management framework that could be attacked and exploited to access and acquire proprietary and confidential information, including information about our customers and merchants. There are no assurances that our actions and investments to improve the maturity of our systems, processes and risk management framework or remediate vulnerabilities will be sufficient or completed quickly enough to prevent or limit the impact of any cyber intrusion. In addition, in the future we may be required to expend significant additional resources to modify or enhance our protective measures, controls and systems or to improve the maturity of our systems, processes and risk management framework, or investigate or remediate any information security vulnerabilities. These improvements, modifications and enhancements may take significant time to implement. Further, the sophistication of potential attacks or the capabilities of our systems and processes may not permit us to detect the occurrence of cyber incidents until significant data loss has occurred. Moreover, because the techniques used to gain access to or sabotage systems often are not recognized until launched against a target, we may be unable to anticipate the methods necessary to defend against these types of attacks and we cannot predict the extent, frequency or impact these problems may have on us. Any actual breach, the perceived threat of a breach or a perceived breach, could cause our customers, merchants, card brands and payment card processors to cease doing business with us or do business with us less frequently, subject us to lawsuits, investigations, regulatory fines or other action or liability or damage to our brand and reputation, which would harm our business, financial condition and results of operations.

We operate in a highly competitive industry with relatively low barriers to entry and must compete successfully in order to grow our business.

Competition in our industry may increase in future periods. A number of e-commerce sites that attempt to replicate our business model operate around the world. We also compete against companies that offer other types of advertising and promotional services to local businesses. In addition to such competitors, we may experience increased competition from other large businesses who offer deals similar to ours as an add-on to their core business. We also compete with other companies that offer digital coupons and/or card-linking services through their websites or mobile applications. Further, we compete against other e-commerce companies that serve niche markets and interests. In some of our categories, such as Goods and Travel, we compete against much larger companies who have more resources and significantly greater scale. In addition, we compete with traditional offline coupon and discount services, as well as newspapers, magazines and other traditional media companies who provide coupons and discounts on products and services.

We believe that our ability to compete successfully depends upon many factors both within and beyond our control, including the following:

• | the size, composition and retention of our customer base and the number of merchants we feature; |

• | mobile penetration; |

• | understanding local business trends; |

• | ability to structure deals to generate positive return on investment for merchants; |

• | the timing and market acceptance of deals we offer, including the developments and enhancements to those deals offered by us or our competitors; |

• | customer and merchant service and support efforts; |

• | selling and marketing efforts; |

• | ease of use, performance, price and reliability of services offered either by us or our competitors; |

• | our ability to improve customer purchase frequency; |

• | our ability to drive organic traffic to our marketplaces; |

• | the number, quality and reliability of the digital coupons that can be accessed through our platform; |

• | the quality and performance of our merchants; |

15

• | our ability to cost-effectively manage our operations; and |

• | our reputation and brand strength relative to our competitors. |

Many of our current and potential competitors have longer operating histories, greater financial, marketing and other resources and larger customer bases than we do. These factors may allow our competitors to benefit from their existing customer base with lower customer acquisition costs or to respond more quickly than we can to new or emerging technologies and changes in consumer habits. In addition, our competitors may engage in more extensive research and development efforts, undertake more far-reaching marketing campaigns and adopt more aggressive pricing policies, which may allow them to build larger customer and/or merchant bases or generate revenue from their customer bases more effectively than we do. Our competitors may offer deals that are similar to the deals we offer or that achieve greater market acceptance than the deals we offer. This could attract customers away from our websites and mobile applications, reduce our market share and adversely impact our gross profit. In addition, we are dependent on some of our existing or potential competitors for display advertisements and other marketing initiatives to acquire new customers. Our ability to utilize their platforms to acquire new customers may be adversely affected if they choose to compete more directly with us or prevent us from using their services.

Our operating cash flow could be adversely impacted if we change our merchant payment terms.

Our merchant payment terms and revenue growth have historically provided us with operating cash flow to fund our working capital needs. Our merchant arrangements are generally structured such that we collect cash up front when our customers purchase vouchers or products on our website or mobile application and we make payments to merchants or suppliers at a subsequent date, either on a fixed schedule or upon redemption by customers. For Groupon+ deals, we offer cash back on customers' credit card statements based on qualifying purchases with participating merchants. For those offerings, we remit payment to a card brand network at the time of the qualifying purchase for the customer's cash back incentive and then we collect from the merchant both our commission and reimbursement for the customer's cash back incentive, generally on a bi-weekly basis. The working capital impact of Groupon+ offerings is less favorable to us than voucher transactions, for which we collect payment from customers at the time of sale and remit payment to merchants at a later date. We have used the operating cash flow provided by our merchant payment terms and revenue growth to fund our working capital needs. If we offer merchants more favorable or accelerated payment terms and/or scale our Groupon+ offerings, our operating cash flow could be adversely impacted and we may have to seek alternative financing to fund our working capital needs.

Our success is dependent upon our ability to provide a superior mobile experience for our customers and our customers' continued ability to access our offerings through mobile devices.

In the fourth quarter of 2017, over 69% of our global transactions were completed on mobile devices. Additionally, over 170.8 million people have downloaded our mobile applications worldwide as of December 31, 2017. In order to continue to grow our mobile transactions, it is critical that our applications are compatible with a range of mobile technologies, systems, networks and standards. As part of our growth strategy, we have been developing and testing a number of product enhancements that are intended to make our offerings easier to use for both customers and merchants, including voucherless offerings that are linked to customer credit cards. Our business may be adversely affected if our customers choose not to access our offerings on their mobile devices or use mobile devices that do not offer access to our mobile applications or if we fail to develop applications and produce enhancements with adequate functionality on a wide range of mobile devices.

Our business depends on our ability to maintain and improve the technology infrastructure necessary to send our emails and operate our websites, mobile applications and transaction processing systems, and any significant disruption in service on our email network infrastructure, websites, mobile applications or transaction processing systems could result in a loss of customers or merchants.

Customers access our marketplaces through our websites and mobile applications, as well as via emails that are often targeted by location, purchase history and personal preferences. Customers can also access our deal offerings indirectly through third-party search engines. Our reputation and ability to acquire, retain and serve our current and potential customers are dependent upon the reliable performance of our websites, mobile applications, email delivery and transaction processing systems and the underlying network infrastructure. Our systems may not be adequately designed with the necessary reliability and redundancy to avoid performance delays or outages that could be prolonged and harmful to our business. If our websites or mobile applications are unavailable when users attempt to access them, or if they do not load as quickly as expected, users may not return as often in the future, or at all. As our customer base and the amount of information shared on our websites and mobile applications continue to grow, we will need an increasing amount of network capacity and computing power. We have spent and expect to continue to spend substantial amounts on data centers and equipment and related network infrastructure and services to handle the traffic on our websites and mobile applications and to help shorten the time of or prevent system interruptions. The operation of these systems

16

is expensive and complex and could result in operational failures. While resiliency and redundancy are considerations in the design and operation of Groupon's systems, interruptions, delays or failures in these systems, whether due to earthquakes, adverse weather conditions, other natural disasters, power loss, computer viruses, cybersecurity attacks, physical break-ins, terrorism, errors in our software or otherwise, could be prolonged and could affect the security or availability of our websites and applications, and prevent our customers from accessing our services. If we do not maintain or expand our network infrastructure successfully or if we experience operational failures or prolonged disruptions or delays in the availability of our systems or a significant search engine, we could lose current and potential customers and merchants, which could harm our operating results and financial condition.

In addition, a portion of our network infrastructure is hosted by third-party providers. We also rely on a variety of tools and third-party commercial partners to provide certain services and offerings (e.g., booking tools and food delivery offers). Any disruption or failure of these providers, tools and/or other third parties to handle existing or increased traffic and transactions could significantly harm our business. Any financial or other difficulties these providers face may adversely affect our business, and we exercise little control over these providers, which increases our vulnerability to problems with the services they provide.

If our emails are not delivered and accepted, or are routed by email providers less favorably than other emails, or our sites or mobile applications are not accessible, or are treated disadvantageously by Internet service providers, our business may be substantially harmed.

If email providers or Internet service providers ("ISPs") implement new or more restrictive email or content delivery or accessibility policies, including with respect to net neutrality, it may become more difficult to deliver emails to our customers or for customers to access our site and services. For example, certain email providers, including Google, categorize our emails as "promotional," and these emails are directed to an alternate, and less readily accessible, section of a customer's inbox. If email providers materially limit or halt the delivery of our emails, or if we fail to deliver emails to customers in a manner compatible with email providers' email handling or authentication technologies, our ability to contact customers through email could be significantly restricted. In addition, if we are placed on "spam" lists or lists of entities that have been involved in sending unwanted, unsolicited emails, our operating results and financial condition could be substantially harmed. Further, if ISPs prioritize or provide superior access to our competitors' content, our business and results of operations may be negatively impacted.

We purchase and sell some products from indirect suppliers and allow third parties to sell products via our site and services, which increase our risk of litigation and other losses.