2017

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| [x] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-32395

ConocoPhillips

(Exact name of registrant as specified in its charter)

| Delaware | 01-0562944 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

600 North Dairy Ashford

Houston, TX 77079

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: 281-293-1000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |||

| Common Stock, $.01 Par Value | New York Stock Exchange | |||

| 7% Debentures due 2029 | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[x] Yes [ ] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

[ ] Yes [x] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[x] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

[x] Yes [ ] No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer [x] Accelerated filer [ ] Non-accelerated filer [ ] Smaller reporting company [ ]

Emerging growth company [ ]

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). [ ] Yes [x] No

The aggregate market value of common stock held by non-affiliates of the registrant on June 30, 2017, the last business day of the registrant's most recently completed second fiscal quarter, based on the closing price on that date of $43.96, was $54.0 billion.

The registrant had 1,174,577,506 shares of common stock outstanding at January 31, 2018.

Documents incorporated by reference:

Portions of the Proxy Statement for the Annual Meeting of Stockholders to be held on May 15, 2018 (Part III)

TABLE OF CONTENTS

Item | Page | |||||

| PART I | ||||||

1 and 2. | Business and Properties | 1 | ||||

Corporate Structure | 1 | |||||

Segment and Geographic Information | 2 | |||||

Alaska | 3 | |||||

Lower 48 | 5 | |||||

Canada | 7 | |||||

Europe and North Africa | 8 | |||||

Asia Pacific and Middle East | 11 | |||||

Other International | 15 | |||||

Competition | 18 | |||||

General | 18 | |||||

1A. | Risk Factors | 20 | ||||

1B. | Unresolved Staff Comments | 25 | ||||

3. | Legal Proceedings | 25 | ||||

4. | Mine Safety Disclosures | 25 | ||||

Executive Officers of the Registrant | 26 | |||||

PART II

| ||||||

5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 27 | ||||

6. | Selected Financial Data | 29 | ||||

7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 30 | ||||

7A. | Quantitative and Qualitative Disclosures About Market Risk | 72 | ||||

8. | Financial Statements and Supplementary Data | 75 | ||||

9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 174 | ||||

9A. | Controls and Procedures | 174 | ||||

9B. | Other Information | 174 | ||||

PART III

| ||||||

10. | Directors, Executive Officers and Corporate Governance | 175 | ||||

11. | Executive Compensation | 175 | ||||

12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 175 | ||||

13. | Certain Relationships and Related Transactions, and Director Independence | 175 | ||||

14. | Principal Accounting Fees and Services | 175 | ||||

PART IV

| ||||||

15. | Exhibits, Financial Statement Schedules | 176 | ||||

Signatures | 188 | |||||

PART I

Unless otherwise indicated, "the company," "we," "our," "us" and "ConocoPhillips" are used in this report to refer to the businesses of ConocoPhillips and its consolidated subsidiaries. Items 1 and 2-Business and Properties, contain forward-looking statements including, without limitation, statements relating to our plans, strategies, objectives, expectations and intentions that are made pursuant to the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. The words "anticipate," "estimate," "believe," "budget," "continue," "could," "intend," "may," "plan," "potential," "predict," "seek," "should," "will," "would," "expect," "objective," "projection," "forecast," "goal," "guidance," "outlook," "effort," "target" and similar expressions identify forward-looking statements. The company does not undertake to update, revise or correct any forward-looking information unless required to do so under the federal securities laws. Readers are cautioned that such forward-looking statements should be read in conjunction with the company's disclosures under the heading "CAUTIONARY STATEMENT FOR THE PURPOSES OF THE ‘SAFE HARBOR' PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995," beginning on page 70.

Items 1 and 2. BUSINESS AND PROPERTIES

CORPORATE STRUCTURE

ConocoPhillips is the world's largest independent exploration and production (E&P) company, based on proved reserves and production of liquids and natural gas. ConocoPhillips was incorporated in the state of Delaware on November 16, 2001, in connection with, and in anticipation of, the merger between Conoco Inc. and Phillips Petroleum Company. The merger between Conoco and Phillips was consummated on August 30, 2002.

In April 2012, ConocoPhillips completed the separation of the downstream business into an independent, publicly traded energy company, Phillips 66.

Headquartered in Houston, Texas, we have operations and activities in 17 countries. Our diverse portfolio includes resource-rich North American tight oil and oil sands assets; lower-risk conventional assets in North America, Europe, Asia and Australia; several liquefied natural gas (LNG) developments; and an inventory of global conventional and unconventional exploration prospects.

At December 31, 2017, ConocoPhillips employed approximately 11,400 people worldwide.

We operate in a commodity-price driven industry, subject to volatility. In line with this view, we set our operating plan for 2017, defining our cash allocation priorities which would be reinforced and partly funded by sales of noncore assets during the year. In November 2016, we announced our plan to generate $5 billion to $8 billon of proceeds over two years by optimizing our portfolio to focus on value-preserving, low cost-of-supply projects that strategically fit our development plans. In 2017, our total consideration from asset dispositions was approximately $16 billion. We disposed of assets including our 50 percent nonoperated interest in the Foster Creek Christina Lake (FCCL) Partnership, as well as the majority of our western Canada gas assets, and our interest in the San Juan Basin gas asset. Proceeds from dispositions were directed towards our cash allocation priorities and for general corporate purposes. For additional information on our cash allocation priorities and our asset sales, see the Business Environment and Executive Overview section within Management's Discussion and Analysis and Note 4-Assets Held for Sale, Sold or Acquired, in the Notes to Consolidated Financial Statements, respectively.

1

SEGMENT AND GEOGRAPHIC INFORMATION

For operating segment and geographic information, see Note 23-Segment Disclosures and Related Information, in the Notes to Consolidated Financial Statements, which is incorporated herein by reference.

We explore for, produce, transport and market crude oil, bitumen, natural gas, LNG and natural gas liquids on a worldwide basis. At December 31, 2017, our operations were producing in the United States, Norway, the United Kingdom, Canada, Australia, Timor-Leste, Indonesia, China, Malaysia, Qatar and Libya.

The information listed below appears in the "Oil and Gas Operations" disclosures following the Notes to Consolidated Financial Statements and is incorporated herein by reference:

| • | Proved worldwide crude oil, natural gas liquids, natural gas and bitumen reserves. |

| • | Net production of crude oil, natural gas liquids, natural gas and bitumen. |

| • | Average sales prices of crude oil, natural gas liquids, natural gas and bitumen. |

| • | Average production costs per barrel of oil equivalent (BOE). |

| • | Net wells completed, wells in progress and productive wells. |

| • | Developed and undeveloped acreage. |

The following table is a summary of the proved reserves information included in the "Oil and Gas Operations" disclosures following the Notes to Consolidated Financial Statements. Approximately 77 percent of our proved reserves are located in politically stable countries that belong to the Organization for Economic Cooperation and Development. Natural gas reserves are converted to BOE based on a 6:1 ratio: six thousand cubic feet (MCF) of natural gas converts to one BOE. See Management's Discussion and Analysis of Financial Condition and Results of Operations for a discussion of factors that will enhance the understanding of the following summary reserves table.

| Millions of Barrels of Oil Equivalent | ||||||||||||

Net Proved Reserves at December 31 | 2017 | 2016 | 2015 | |||||||||

|

| |||||||||||

Crude oil | ||||||||||||

Consolidated operations | 2,322 | 2,047 | 2,270 | |||||||||

Equity affiliates | 83 | 88 | 93 | |||||||||

| ||||||||||||

Total Crude Oil | 2,405 | 2,135 | 2,363 | |||||||||

| ||||||||||||

Natural gas liquids | ||||||||||||

Consolidated operations | 354 | 457 | 508 | |||||||||

Equity affiliates | 45 | 47 | 50 | |||||||||

| ||||||||||||

Total Natural Gas Liquids | 399 | 504 | 558 | |||||||||

| ||||||||||||

Natural gas | ||||||||||||

Consolidated operations | 1,267 | 1,807 | 1,988 | |||||||||

Equity affiliates | 717 | 730 | 878 | |||||||||

| ||||||||||||

Total Natural Gas | 1,984 | 2,537 | 2,866 | |||||||||

| ||||||||||||

Bitumen | ||||||||||||

Consolidated operations | 250 | 159 | 687 | |||||||||

Equity affiliates | - | 1,089 | 1,706 | |||||||||

| ||||||||||||

Total Bitumen | 250 | 1,248 | 2,393 | |||||||||

| ||||||||||||

Total consolidated operations | 4,193 | 4,470 | 5,453 | |||||||||

Total equity affiliates | 845 | 1,954 | 2,727 | |||||||||

| ||||||||||||

Total company | 5,038 | 6,424 | 8,180 | |||||||||

| ||||||||||||

2

Total production, including Libya, of 1,377 thousand barrels of oil equivalent per day (MBOED) decreased 12 percent in 2017 compared with 2016. The decrease in total average production primarily resulted from noncore asset dispositions, including our Canada and San Juan transactions in 2017 and the sale of our interest in the Block B production sharing contract (PSC) in Indonesia in 2016, and normal field decline. The decrease in production was partly offset by production from major developments, including tight oil plays in the Lower 48; Malikai and the Kebabangan gas field in Malaysia; Surmont in Canada; and APLNG in Australia. Improved drilling and well performance in Alaska, Norway and China also partly offset the decrease in production. Excluding Libya, our 2017 production was 1,356 MBOED. Adjusted for the impact of closed and planned dispositions of 191 MBOED in 2017 and 434 MBOED in 2016 and Libya, underlying production increased 32 MBOED, or 3 percent, compared with 2016.

Our worldwide annual average realized price was $39.19 per BOE in 2017, an increase of 38 percent compared with $28.35 per BOE in 2016, reflecting higher average realized prices across all commodities. Our worldwide annual average crude oil price increased 27 percent in 2017, from $40.86 per barrel in 2016 to $51.96 per barrel in 2017. Additionally, our worldwide annual average natural gas liquids prices increased 51 percent, from $16.68 per barrel in 2016 to $25.22 per barrel in 2017. Our worldwide annual average natural gas price increased 36 percent, from $3.00 per MCF in 2016 to $4.07 per MCF in 2017. Average annual bitumen prices also increased 48 percent, from $15.27 per barrel in 2016 to $22.66 per barrel in 2017.

ALASKA

The Alaska segment primarily explores for, produces, transports and markets crude oil, natural gas and natural gas liquids. We are the largest crude oil producer in Alaska and have major ownership interests in two of North America's largest oil fields located on Alaska's North Slope: Prudhoe Bay and Kuparuk. We also have a significant operating interest in the Alpine Field, located on the Western North Slope. Additionally, we are one of Alaska's largest owners of state, federal and fee exploration leases, with approximately 1 million net undeveloped acres at year-end 2017. Alaska operations contributed 22 percent of our worldwide liquids production and less than 1 percent of our natural gas production.

| 2017 | ||||||||||||||||||||

| Interest | Operator | Liquids MBD | * | Natural Gas MMCFD | ** | Total MBOED | ||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

Greater Prudhoe Area | 36.1 | % | BP | 88 | 5 | 89 | ||||||||||||||

Greater Kuparuk Area | 52.2–55.5 | ConocoPhillips | 53 | 1 | 53 | |||||||||||||||

Western North Slope | 78.0 | ConocoPhillips | 40 | 1 | 40 | |||||||||||||||

| ||||||||||||||||||||

Total Alaska | 181 | 7 | 182 | |||||||||||||||||

| ||||||||||||||||||||

*Thousands of barrels per day.

**Millions of cubic feet per day.

Greater Prudhoe Area

The Greater Prudhoe Area includes the Prudhoe Bay Field and five satellite fields, as well as the Greater Point McIntyre Area fields. Prudhoe Bay, the largest oil field on Alaska's North Slope, is the site of a large waterflood and enhanced oil recovery operation, as well as a gas plant which processes natural gas to recover natural gas liquids before reinjection into the reservoir. Prudhoe Bay's satellites are Aurora, Borealis, Polaris, Midnight Sun and Orion, while the Point McIntyre, Niakuk, Raven, Lisburne and North Prudhoe Bay State fields are part of the Greater Point McIntyre Area.

3

Greater Kuparuk Area

We operate the Greater Kuparuk Area, which consists of the Kuparuk Field and four satellite fields: Tarn, Tabasco, Meltwater and West Sak. Kuparuk is located 40 miles west of Prudhoe Bay. Field installations include three central production facilities which separate oil, natural gas and water, as well as a separate seawater treatment plant. Development drilling at Kuparuk consists of rotary-drilled wells and horizontal multi-laterals from existing well bores utilizing coiled-tubing drilling.

Drill Site 2S, in the southwestern area of the Kuparuk Field, was sanctioned in October 2014. First oil was achieved in October 2015, and completion of the first phase of the project was achieved in 2016.

The 1H Northeast West Sak (NEWS) oil development targeting the West Sak reservoir in the Kuparuk River Unit, was sanctioned in March 2015. First production was achieved in the fourth quarter of 2017.

Western North Slope

On the Western North Slope, we operate the Colville River Unit, which includes the Alpine Field and three satellite fields: Nanuq, Fiord and Qannik. Alpine is located 34 miles west of Kuparuk. In 2015, first oil was achieved at Alpine West CD5, a new drill site which extends the Alpine reservoir west into the National Petroleum Reserve-Alaska (NPR-A). During the year, we continued drilling additional wells using the available well slots on the pad.

The Greater Mooses Tooth Unit, the first unit established entirely within the NPR-A, was formed in 2008. In 2017, we began construction in the unit, which is currently planned to have two drill sites; Greater Mooses Tooth #1 and #2, with expected first oil in 2018 and 2021, respectively.

Cook Inlet Area

In January 2018, we sold our interest in the Kenai LNG Facility in the Cook Inlet Area. The facility, which consisted of a 1.6 million-tons-per-year capacity plant, as well as docking and loading facilities for LNG tankers, had no LNG export program in 2017 due to market conditions.

Point Thomson

In the first quarter of 2017, we recorded an asset impairment and assigned our 4.9 percent interest in the Point Thomson unit, located approximately 60 miles east of Prudhoe Bay, to the other owners of the field.

Alaska North Slope Gas

In 2016, we, along with affiliates of Exxon Mobil Corporation, BP p.l.c. and Alaska Gasline Development Corporation (AGDC), a state-owned corporation (collectively, the "AKLNG co-venturers"), completed preliminary front-end engineering and design (pre-FEED) technical work for a potential LNG project which would liquefy and export natural gas from Alaska's North Slope and deliver it to market. In September 2016, we, along with the affiliates of ExxonMobil and BP, indicated our intention not to progress into the next phase of the project due to changes in the economic environment. AGDC is continuing to progress the project and has recently signed several Memorandums of Understanding with various potential LNG buyers in Asia. We remain supportive of AGDC's efforts to advance the project and intend to make our equity gas available for sale to the project at mutually agreed, commercially reasonable terms.

Exploration

Appraisal of the Willow Discovery, located in the northeast portion of the National Petroleum Reserve-Alaska, continued throughout 2017 with the acquisition of 3-D seismic which is currently being processed. In 2018, we will continue appraisal of the discovery with drilling of additional wells. Further exploration of other state and federal leases is planned in 2018.

We were successful in state and federal lease sales in the North Slope in the fourth quarter of 2017, where we were the high bidder on 13 tracts for a total of approximately 78,000 net acres.

4

Acquisition

In January 2018, we entered into an agreement to acquire certain oil and gas assets in Alaska. The acquisition is subject to regulatory approval. We will have a 100 percent interest in approximately 1.2 million acres of exploration and development lands, including the Willow Discovery. For additional information, see Note 4-Assets Held for Sale, Sold or Acquired, in the Notes to Consolidated Financial Statements.

Transportation

We transport the petroleum liquids produced on the North Slope to south central Alaska through an 800-mile pipeline that is part of Trans-Alaska Pipeline System (TAPS). We have a 29.1 percent ownership interest in TAPS, and we also have ownership interests in the Alpine, Kuparuk and Oliktok pipelines on the North Slope.

Our wholly owned subsidiary, Polar Tankers, Inc., manages the marine transportation of our North Slope production, using five company-owned, double-hulled tankers, and charters third-party vessels as necessary. The tankers deliver oil from Valdez, Alaska, primarily to refineries on the west coast of the United States.

LOWER 48

The Lower 48 segment consists of operations located in the U.S. Lower 48 states and the Gulf of Mexico. The Lower 48 business is organized within three regions covering the Gulf Coast, Mid-Continent and Rockies. As a result of tight oil opportunities, we have directed our investments toward certain shorter cycle time, low cost-of-supply plays. We disposed of several noncore assets within the Lower 48 in 2017, including our interests in the San Juan Basin and the Panhandle. We hold 10.4 million net onshore and offshore acres in the Lower 48. In 2017, the Lower 48 contributed 30 percent of our worldwide liquids production and 27 percent of our natural gas production.

| 2017 | ||||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

Eagle Ford | Various | % | Various | 107 | 155 | 133 | ||||||||||||||

Gulf of Mexico | Various | Various | 15 | 13 | 17 | |||||||||||||||

Gulf Coast-Other | Various | Various | 5 | 11 | 7 | |||||||||||||||

| ||||||||||||||||||||

Total Gulf Coast | 127 | 179 | 157 | |||||||||||||||||

| ||||||||||||||||||||

Permian | Various | Various | 41 | 132 | 63 | |||||||||||||||

Barnett | Various | Various | 4 | 34 | 10 | |||||||||||||||

Anadarko Basin | Various | Various | 4 | 91 | 19 | |||||||||||||||

| ||||||||||||||||||||

Total Mid-Continent | 49 | 257 | 92 | |||||||||||||||||

| ||||||||||||||||||||

Bakken | Various | Various | 56 | 56 | 65 | |||||||||||||||

Wyoming/Uinta | Various | Various | - | 84 | 14 | |||||||||||||||

Niobrara | Various | Various | 2 | 3 | 3 | |||||||||||||||

San Juan | Various | Various | 15 | 319 | 68 | |||||||||||||||

| ||||||||||||||||||||

Total Rockies | 73 | 462 | 150 | |||||||||||||||||

| ||||||||||||||||||||

Total U.S. Lower 48 | 249 | 898 | 399 | |||||||||||||||||

| ||||||||||||||||||||

Onshore

We hold 10.4 million net acres of onshore conventional and unconventional acreage in the Lower 48, the majority of which is either held by production or owned by the company. Our unconventional holdings total approximately 1.8 million net acres in the following areas:

| • | 630,000 net acres in the Bakken, located in North Dakota and eastern Montana. |

| • | 210,000 net acres in the Eagle Ford, located in South Texas. |

| • | 134,000 net acres in the Permian, located in West Texas and southeastern New Mexico. |

5

| • | 98,000 net acres in the Niobrara, located in northeastern Colorado. |

| • | 66,000 net acres in the Barnett, located in north central Texas. |

| • | 639,000 net acres in other unconventional exploration plays. |

The majority of our 2017 onshore production originated from the Eagle Ford; San Juan, which we disposed of during the year; Bakken; and Permian. Onshore activities in 2017 were centered mostly on continued development of assets, with an emphasis on areas with low cost of supply, particularly in growing unconventional plays. The 2017 drilling activity levels increased relative to 2016 due to higher capital spending. Our major focus areas in 2017 included the following:

| • | Eagle Ford-The Eagle Ford continued full-field development in 2017. We operated six rigs on average in 2017, resulting in 133 operated wells drilled and 94 operated wells brought online. Production decreased 17 percent in 2017 compared with 2016, and reached a net peak of 164 MBOED, compared with 176 MBOED in 2016. |

| • | Bakken-We operated four rigs throughout the year in the Bakken. We continued our pad drilling with 87 operated wells drilled during the year and 64 operated wells brought online. We achieved net peak production of 75 MBOED in 2017, compared with 72 MBOED in 2016. |

| • | Permian Basin-The Permian Basin is an area where we are leveraging our conventional legacy position by utilizing new technology to improve the ultimate recovery and value from these fields. This technology should also identify new, unconventional plays across the region. We hold approximately 1 million net acres in the Permian, which includes 134,000 net unconventional acres. The Permian Basin produced 63 MBOED in 2017, staying essentially flat with 2016, including 19 MBOED of unconventional production. |

We completed the sale of our interests in the San Juan Basin on July 31, 2017, and Panhandle assets on September 29, 2017. Production from the assets sold was 74 MBOED, approximately 19 percent of total Lower 48 segment production in 2017. For additional information on our asset dispositions, see Note 4-Assets Held for Sale, Sold or Acquired, in the Notes to Consolidated Financial Statements.

Gulf of Mexico

At year-end 2017, our portfolio of producing properties in the Gulf of Mexico primarily consisted of one operated field and three fields operated by co-venturers, totaling approximately 68,000 net acres, including:

| • | 75 percent operated working interest in the Magnolia Field in Garden Banks Blocks 783 and 784. |

| • | 15.9 percent nonoperated working interest in the unitized Ursa Field located in the Mississippi Canyon Area. |

| • | 15.9 percent nonoperated working interest in the Princess Field, a northern subsalt extension of the Ursa Field. |

| • | 12.4 percent nonoperated working interest in the unitized K2 Field, comprised of seven blocks in the Green Canyon Area. |

Exploration

| • | Conventional Exploration |

At December 31, 2017, we held approximately 5,000 net acres in the deepwater Gulf of Mexico.

Our 30 percent nonoperated working interest in the Shenandoah discovery was announced in 2009. In early 2017, the sixth Shenandoah well, Shenandoah WR52-3, reached total depth and was followed by the drilling of a sidetrack well from Shenandoah WR52-3. Following the suspension of appraisal activity by the operator during the year, we recorded dry hole and leasehold impairment expense for the entire development. On December 19, 2017, we elected to withdraw from the Shenandoah leases. The withdrawal was effective February 17, 2018.

6

| • | Unconventional Exploration |

Our onshore focus areas include the Niobrara in the Denver-Julesburg Basin and the Permian in the Delaware Basin, as well as several emerging plays. We continue to assess and appraise these and other unconventional opportunities. In 2016 and 2017, we drilled a total of five operated unconventional wells in the Powder River Basin, four of which were expensed as dry holes in November 2017. The fifth Powder River Basin well was expensed as a dry hole in January 2018.

Facilities

Golden Pass LNG Terminal

We have a 12.4 percent ownership interest in the Golden Pass LNG Terminal and affiliated Golden Pass Pipeline, with a combined net book value of approximately $247 million at December 31, 2017. It is located adjacent to the Sabine-Neches Industrial Ship Channel northwest of Sabine Pass, Texas. The terminal became commercially operational in May 2011. We hold terminal and pipeline capacity for the receipt, storage and regasification of the LNG purchased from Qatar Liquefied Gas Company Limited (3) (QG3) and the transportation of regasified LNG to interconnect with major interstate natural gas pipelines. Utilization of the terminal has been and is expected to be limited, as market conditions currently favor the flow of LNG to European and Asian markets. As a result, we are evaluating opportunities to optimize the value of the terminal facilities.

Other

| • | Lost Cabin Gas Plant-We operate and own a 46 percent interest in the Lost Cabin Gas Plant, a 246 million cubic-feet-per-day capacity natural gas processing facility in Lysite, Wyoming. |

| • | Helena Condensate Processing Facility-We operate and own the Helena Condensate Processing Facility, a 110,000 barrel-per-day condensate processing plant located in Kenedy, Texas. |

| • | Sugarloaf Condensate Processing Facility-We operate and own an 87.5 percent interest in the Sugarloaf Condensate Processing Facility, a 30,000 barrel-per-day condensate processing plant located near Pawnee, Texas. |

| • | Bordovsky Condensate Processing Facility-We operate and own the Bordovsky Condensate Processing Facility, a 15,000 barrel-per-day condensate processing plant located in Kenedy, Texas. |

CANADA

Our Canadian operations mainly consist of an oil sands development in the Athabasca Region of northeastern Alberta and a liquids-rich unconventional play in western Canada. In 2017, operations in Canada contributed 16 percent of our worldwide liquids production and 6 percent of our natural gas production.

| 2017 | ||||||||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Bitumen MBD | Total MBOED | |||||||||||||||||||

|

|

|

|

|

| |||||||||||||||||||

Average Daily Net Production | ||||||||||||||||||||||||

Western Canada | Various | % | Various | 12 | 187 | - | 43 | |||||||||||||||||

Surmont | 50.0 | ConocoPhillips | - | - | 59 | 59 | ||||||||||||||||||

Foster Creek | 50.0 | Cenovus | - | - | 26 | 26 | ||||||||||||||||||

Christina Lake | 50.0 | Cenovus | - | - | 37 | 37 | ||||||||||||||||||

| ||||||||||||||||||||||||

Total Canada | 12 | 187 | 122 | 165 | ||||||||||||||||||||

| ||||||||||||||||||||||||

7

On May 17, 2017, we completed the sale of our 50 percent nonoperated interest in the FCCL Partnership, as well as the majority of our western Canada gas assets to Cenovus Energy. Production from the assets sold was 103 MBOED, approximately 62 percent of the total Canada segment production in 2017. For additional information on our asset dispositions, see Note 4-Assets Held for Sale, Sold or Acquired, in the Notes to Consolidated Financial Statements.

Oil Sands

Our bitumen resources in Canada are produced via an enhanced thermal oil recovery method called steam-assisted gravity drainage (SAGD), whereby steam is injected into the reservoir, effectively liquefying the heavy bitumen, which is recovered and pumped to the surface for further processing. We hold approximately 0.6 million net acres of land in the Athabasca Region of northeastern Alberta.

Surmont-The Surmont oil sands leases are located approximately 35 miles south of Fort McMurray, Alberta. Surmont is a 50/50 joint venture with Total S.A. The second phase of the Surmont project achieved first production in 2015, and production continued to ramp up in 2017.

Exploration

We hold exploration acreage in three areas of Canada: onshore western Canada, the Mackenzie Delta/Beaufort Sea Region and the Arctic Islands. Our primary exploration focus is on unconventional plays in western Canada.

| • | Unconventional Exploration |

We hold approximately 0.1 million net acres in the emerging Montney play in northeast British Columbia and 0.2 million net acres in Canol Northwest Territories. Our Montney activity in 2017 included completing two and bringing onstream six appraisal wells and acquiring approximately 27,000 additional net acres. Late appraisal drilling activity will continue in 2018 to further explore the area's resource potential.

| • | Conventional Exploration |

Surrender of Interest documents for our 30 percent nonoperated working interest in six exploration licenses in the Shelburne Basin, offshore Nova Scotia, were submitted on December 15, 2017, to initiate the exit process, following previously announced results of the two-well exploration drilling campaign at Cheshire and Monterey Jack.

EUROPE AND NORTH AFRICA

The Europe and North Africa segment consists of operations and exploration activities in Norway, the United Kingdom and Libya. In 2017, operations in Europe and North Africa contributed 18 percent of our worldwide liquids production and 15 percent of natural gas production.

Norway

2017 | ||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||

|

|

|

| |||||||||

Average Daily Net Production | ||||||||||||

Greater Ekofisk Area | 35.1 | % | ConocoPhillips | 57 | 50 | 65 | ||||||

Alvheim | 20.0 | Aker BP | 15 | 13 | 17 | |||||||

Heidrun | 24.0 | Statoil | 13 | 30 | 18 | |||||||

Other | Various | Statoil | 16 | 107 | 34 | |||||||

| ||||||||||||

Total Norway | 101 | 200 | 134 | |||||||||

| ||||||||||||

8

The Greater Ekofisk Area is located approximately 200 miles offshore Stavanger, Norway, in the North Sea, and comprises three producing fields: Ekofisk, Eldfisk and Embla. Crude oil is exported to Teesside, England, and the natural gas is exported to Emden, Germany. The Ekofisk and Eldfisk fields consist of several production platforms and facilities, including the Ekofisk South and Eldfisk II developments which achieved first production in 2013 and 2015, respectively. Continued development drilling in the Greater Ekofisk Area will contribute additional production over the coming years, as additional wells come online.

The Alvheim Field is located in the northern part of the North Sea near the border with the U.K. sector, and consists of a floating production, storage and offloading (FPSO) vessel and subsea installations. Produced crude oil is exported via shuttle tankers, and natural gas is transported to the Scottish Area Gas Evacuation (SAGE) terminal at St. Fergus, Scotland, through the SAGE pipeline.

The Heidrun Field is located in the Norwegian Sea. Produced crude oil is stored in a floating storage unit and exported via shuttle tankers. Part of the natural gas is currently injected into the reservoir for optimization of crude oil production, some gas is transported to Europe via gas processing terminals in Norway, while the remainder is transported for use as feedstock in a methanol plant in Norway, in which we own an 18 percent interest.

We also have varying ownership interests in five other producing fields in the Norway sector of the North Sea, as well as the Aasta Hansteen development in the Norwegian Sea. The operator is planning for first gas for Aasta Hansteen by late 2018.

Exploration

In 2017, we participated in the Korpfjell Well in the Barents Sea and the Carmen Well in the Heidrun Area of Norway, both of which made gas discoveries. The Carmen Well was considered a discovery and is currently under evaluation, while the Korpfjell Well is not considered commercial. In 2017, we were awarded four new exploration licenses including the PL865, PL888, PL890 and PL891; and two acreage additions PL053C and PL782SC. Additionally, two new licenses, PL775 and PL626, were captured through farm-in.

Transportation

We own a 35.1 percent interest in the Norpipe Oil Pipeline System, a 220-mile pipeline which carries crude oil from Ekofisk to a crude oil stabilization and natural gas liquids processing facility in Teesside, England.

United Kingdom

| 2017 | ||||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

Britannia | 58.7 | % | ConocoPhillips | 3 | 68 | 14 | ||||||||||||||

Britannia Satellites | 26.3–87.5 | * | ConocoPhillips | 13 | 84 | 27 | ||||||||||||||

J-Area | 32.5–36.5 | ConocoPhillips | 9 | 60 | 19 | |||||||||||||||

Southern North Sea | Various | ConocoPhillips | - | 46 | 8 | |||||||||||||||

East Irish Sea | 100.0 | Spirit Energy | - | 14 | 2 | |||||||||||||||

Other | Various | Various | 4 | 4 | 5 | |||||||||||||||

Total United Kingdom | 29 | 276 | 75 | |||||||||||||||||

| ||||||||||||||||||||

* Includes the Chevron-operated Alder Field, ConocoPhillips equity 26.3%.

Britannia is one of the largest natural gas and condensate fields in the North Sea. We assumed operatorship of Britannia in August 2015, following the acquisition of third-party equity in Britannia Operator Limited, which is now wholly owned by ConocoPhillips. Condensate is delivered through the Forties Pipeline to an oil stabilization and processing plant near the Grangemouth Refinery in Scotland, while natural gas is transported through Britannia's line to St. Fergus, Scotland. The Britannia satellite fields, Callanish, Brodgar, Enochdhu and Alder, produce via subsea manifolds and pipelines linked to the Britannia Platform.

9

The J-Area consists of the Judy/Joanne, Jade and Jasmine fields, located in the U.K. Central North Sea. The J-Area gas is processed on the Judy Platform and transported through the Central Area Transmission System Pipeline, while liquids are transported to Teesside through the Norpipe system. A J-Area development drilling campaign commenced in 2017, which is expected to provide additional volumes in the coming years as wells are brought online.

We have various ownership interests in several producing gas fields in the Rotliegendes and Carboniferous areas of the Southern North Sea. Decommissioning activity in the Southern North Sea is ongoing. Our interests in the East Irish Sea include the Millom, Dalton and Calder fields, which are operated on our behalf by a third party.

We own a 24 percent interest in the Clair Field, located in the Atlantic Margin. Clair Ridge is the second phase of development for the Clair Field and is comprised of a 36-slot drilling and production facility with a bridge-linked accommodation and utilities platform. The new facilities will tie into existing oil and gas export pipelines to the Shetland Islands. Initial production for Clair Ridge is expected in 2018.

Transportation

We operate the Teesside oil and Theddlethorpe gas terminals in which we have 29.3 percent and 50 percent ownership interests, respectively. We also have a 100 percent ownership interest in the Rivers Gas Terminal, operated by a third party.

Libya

| 2017 | ||||||||||||||||||||

|

| |||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

Waha Concession | 16.3 | % | Waha Oil Co. | 20 | 8 | 21 | ||||||||||||||

| ||||||||||||||||||||

Total Libya | 20 | 8 | 21 | |||||||||||||||||

| ||||||||||||||||||||

The Waha Concession consists of multiple concessions and encompasses nearly 13 million gross acres in the Sirte Basin. Our production operations in Libya and related oil exports were interrupted in mid-2013, as a result of the shutdown of the Es Sider crude oil export terminal at the end of July 2013. The Es Sider Terminal briefly reopened in the third quarter of 2014 and production and liftings resumed temporarily; however, further disruptions occurred in December 2014, and production was shut in again. Production resumed in Libya in October 2016. In 2017, we had 17 crude liftings from Es Sider. We expect a gradual, continued ramp-up in activity.

10

ASIA PACIFIC AND MIDDLE EAST

The Asia Pacific and Middle East segment has exploration and production operations in China, Indonesia, Malaysia and Australia; producing operations in Qatar and Timor-Leste; and exploration activities in Brunei. In 2017, operations in the Asia Pacific and Middle East segment contributed 14 percent of our worldwide liquids production and 52 percent of natural gas production.

Australia and Timor Sea

| 2017 | ||||||||||||||||||||

|

| |||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

Australia Pacific LNG | 37.5 | % |

| ConocoPhillips/ Origin Energy |

| - | 638 | 106 | ||||||||||||

Bayu-Undan | 56.9 | ConocoPhillips | 10 | 233 | 49 | |||||||||||||||

Athena/Perseus | 50.0 | ExxonMobil | - | 34 | 6 | |||||||||||||||

| ||||||||||||||||||||

Total Australia and Timor Sea | 10 | 905 | 161 | |||||||||||||||||

| ||||||||||||||||||||

Australia Pacific LNG

Australia Pacific LNG Pty Ltd (APLNG), our joint venture with Origin Energy Limited and China Petrochemical Corporation (Sinopec), is focused on producing coalbed methane (CBM) from the Bowen and Surat basins in Queensland, Australia, to supply the domestic gas market and convert the CBM into LNG for export. Origin operates APLNG's upstream production and pipeline system, and we operate the downstream LNG facility, located on Curtis Island near Gladstone, Queensland, as well as the LNG export sales business.

Two fully subscribed 4.5-million-metric-tonnes-per-year LNG trains have been completed. Approximately 3,900 net wells are ultimately envisioned to supply both the domestic gas market and the LNG sales contracts. The wells are supported by gathering systems, central gas processing and compression stations, water treatment facilities, and an export pipeline connecting the gas fields to the LNG facilities. The first APLNG Train 1 cargo sailed in January 2016, and LNG sales continued throughout the year. APLNG Train 2 achieved first production in the third quarter of 2016. The LNG is being sold to Sinopec under 20-year sales agreements for 7.6 million metric tonnes of LNG per year, and Japan-based Kansai Electric Power Co., Inc. under a 20-year sales agreement for approximately 1 million metric tonnes of LNG per year.

APLNG has an $8.5 billion project finance facility, which was fully drawn down and had an outstanding balance of $7.9 billion at December 31, 2017. In connection with the execution of the project financing, we provided a completion guarantee for our pro-rata share of the project finance facility until the project achieves financial completion. In October 2016, we reached financial completion for Train 1, which reduced our associated guarantee by 60 percent. In August 2017, we reached financial completion for Train 2, which removed the remaining guarantee. For additional information, see Note 2-Variable Interest Entities (VIEs), Note 5-Investments, Loans and Long-Term Receivables, and Note 11-Guarantees, in the Notes to Consolidated Financial Statements.

Bayu-Undan

The Bayu-Undan gas condensate field is located in the Timor Sea Joint Petroleum Development Area between Timor-Leste and Australia. We also operate and own a 56.9 percent interest in the associated Darwin LNG Facility, located at Wickham Point, Darwin.

The Bayu-Undan natural gas recycle facility processes wet gas; separates, stores and offloads condensate, propane and butane; and re-injects dry gas back into the reservoir. In addition, a 310-mile natural gas pipeline connects the facility to the 3.5-million-metric-tonnes-per-year capacity Darwin LNG Facility. Produced natural gas is piped to the Darwin LNG Plant, where it is converted into LNG before being transported to international markets. In 2017, we sold 150 billion gross cubic feet of LNG primarily to utility customers in Japan.

11

A continuation of the Bayu-Undan Phase Three Development has been sanctioned with internal, joint venture and regulatory approval in March 2017. The project premise consists of one subsea and two platform wells, with drilling to commence in April 2018. Production is expected to commence in the third quarter of 2018.

Athena/Perseus

The Athena production license (WA-17-L) is located offshore Western Australia and contains part of the Perseus Field, which straddles the boundary with WA-1-L, an adjoining license area. Natural gas is produced from these licenses, which are due to expire in 2019.

Greater Sunrise

We have a 30 percent interest in the Greater Sunrise natural gas and condensate field located in the Timor Sea. Timor-Leste and Australia through engagement in a conciliation process under the United Nations Convention on the Law of the Sea have reached agreement on the central elements of a maritime boundary delimitation between them in the Timor Sea. The Governments' agreement, to be formalized in a new treaty, constitutes a package that addresses boundaries, the legal status of the Greater Sunrise gas field, the establishment of a Special Regime for Greater Sunrise, a pathway to development of the resource and the sharing of resulting revenue. Discussions are ongoing between the two Governments and the Sunrise co-venturers with respect to the development concept for Greater Sunrise. Until the Governments and the Sunrise co-venturers are aligned on a development concept, activities are currently restricted to compliance and social investment, maintaining relationships and continued engagement with the Governments for a future development option.

Exploration

| • | Conventional Exploration |

We operate three exploration permits in the Browse Basin, offshore northwest Australia, in which we own a 40 percent interest in permits WA-315-P, WA-398-P and TP 28, of the Greater Poseidon Area. The TP 28 Western Australia State exploration permit was granted for five years from January 2017, with a 40 percent working interest and was excised from the existing permits as agreed between state and federal regulators. Phase I of the Browse Basin drilling campaign in 2009/2010 resulted in three discoveries in the Greater Poseidon Area: Poseidon-1, Poseidon-2 and Kronos-1. Phase II of the drilling campaign resulted in five additional discoveries: Boreas-1, Zephyros-1, Proteus-1 SD2, Poseidon-North-1 and Pharos-1. All wells have been completed, plugged and abandoned.

We operate two retention leases in the Bonaparte Basin, offshore northern Australia, where we own a 37.5 percent interest in leases NT/RL5 and NT/RL6, containing the Barossa and Caldita discoveries. A 3-D seismic survey was completed over the Barossa and Caldita fields in 2016. The drilling of the Barossa-5 and Barossa-6 appraisal wells was completed in 2017 with good quality, gas-bearing reservoir intersected at both. Additionally, the retention lease over the Barossa Discovery was renewed during the year.

Indonesia

| 2017 | ||||||||||||||||||||

|

| |||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

South Sumatra | 45.0–54.0 | % | ConocoPhillips | 2 | 308 | 53 | ||||||||||||||

| ||||||||||||||||||||

Total Indonesia | 2 | 308 | 53 | |||||||||||||||||

| ||||||||||||||||||||

12

We operate three PSCs in Indonesia: The Corridor Block and South Jambi "B," both located in South Sumatra, and Kualakurun in Central Kalimantan. Currently there is production from the Corridor Block.

South Sumatra

The Corridor PSC consists of five oil fields and seven natural gas fields in various stages of development. Natural gas is supplied from the Grissik and Suban gas processing plants to the Duri steamflood in central Sumatra and to markets in Singapore, Batam and West Java. Production from the South Jambi "B" PSC has reached depletion and field development has been suspended.

Exploration

We have a 60 percent working interest in the Kualakurun PSC, located in Central Kalimantan, which was signed in May 2015. This block has an area of approximately 2 million gross acres. During 2017, we acquired 2-D seismic data in the area.

Transportation

We are a 35 percent owner of a consortium company that has a 40 percent ownership in PT Transportasi Gas Indonesia, which owns and operates the Grissik to Duri and Grissik to Singapore natural gas pipelines.

China

| 2017 | ||||||||||||||||||||

|

| |||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

Penglai | 49.0 | % | CNOOC | 30 | - | 30 | ||||||||||||||

Panyu | 24.5 | CNOOC | 8 | - | 8 | |||||||||||||||

| ||||||||||||||||||||

Total China | 38 | - | 38 | |||||||||||||||||

| ||||||||||||||||||||

The Penglai 19-3, 19-9 and 25-6 fields are located in Bohai Bay Block 11/05. Production from the Phase 1 development of the Penglai 19-3 Field began in 2002. Phase 2 included six additional wellhead platforms and an FPSO vessel, and was fully operational by 2009.

As part of further development of the Penglai 19-9 Field, a new wellhead platform, which adds up to 62 wells, is progressing according to schedule, with 19 wells completed and brought online through December 2017.

We sanctioned the Penglai 19-3/19-9 Phase 3 Project in December 2015. This project will consist of three new wellhead platforms and a central processing platform. First oil from Phase 3 is expected in 2018.

The Panyu development, located in Block 15/34 in the South China Sea, is comprised of three oil fields: Panyu 4-2, Panyu 5-1 and Panyu 11-6. The production period for Panyu 4-2 and 5-1 will expire in 2018, and the production period for Panyu 11-6 will expire in 2022.

Exploration

In 2017, we participated in a successful appraisal well in the Penglai Field, which will support future development plans. In late 2017, we began a full-field 3-D seismic program at Penglai, covering Phase 3 and other future development opportunities. The program is expected to continue in 2018.

13

Malaysia

| 2017 | ||||||||||||||||||||

|

| |||||||||||||||||||

| Interest | Operator |

| Liquids MBD |

|

| Natural Gas MMCFD |

|

| Total MBOED |

| ||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

Siakap North-Petai | 21.0 | % | Murphy | 3 | 1 | 3 | ||||||||||||||

Gumusut | 29.0 | Shell | 29 | - | 29 | |||||||||||||||

KBB | 30.0 | KPOC | 3 | 111 | 22 | |||||||||||||||

Malikai | 35.0 | Shell | 12 | - | 12 | |||||||||||||||

| ||||||||||||||||||||

Total Malaysia | 47 | 112 | 66 | |||||||||||||||||

| ||||||||||||||||||||

We own interests in six PSCs in Malaysia. Three are located off the eastern Malaysian state of Sabah: Block G, Block J and the Kebabangan Cluster (KBBC). Three other blocks, Deepwater Block 3E, Block SK313 and Block WL4-00 are located off the eastern Malaysian state of Sarawak.

Block G

We have a 21 percent interest in the unitized Siakap North-Petai oil field, which began producing in the first quarter of 2014.

First production from the Malikai oil field was achieved in December 2016, with estimated net annual peak production of 21 MBOED expected in 2018. We own a 35 percent interest in Malikai. The Limbayong-2 appraisal well was drilled in 2013 and resulted in an oil discovery. The well was expensed in 2017.

Block J

First production from the Gumusut Field occurred from an early production system in 2012. Production from a permanent, semi-submersible floating production vessel was achieved in October 2014. Our ownership in the Gumusut Field is currently at 29 percent following the finalization of the unitization with Brunei and a redetermination of the Block J and Block K Malaysia Unit, both in 2017. Gumusut Phase 2 infill drilling is planned to start in 2018.

KBBC

We own a 30 percent interest in the KBBC PSC. Development of the KBB gas field commenced in 2011, and first production was achieved in November 2014. Development options for the Kamunsu East gas field are being evaluated.

Exploration

We own a 50 percent operated interest in Deepwater Block 3E, which encompasses approximately 480,000 gross acres offshore Sarawak. Seismic processing was completed in 2015. The Langsat-1 exploration well was drilled and expensed as a dry hole in 2017.

In the fourth quarter of 2016, we entered into a farm-in agreement to acquire a 50 percent interest in Block SK 313, a 1.4 million gross-acre exploration block, effective January 2017. Following completion of the Sadok-1 exploration well in January 2017, we assumed operatorship of the block from PETRONAS.

We were awarded Block WL4-00, which encompasses approximately 629,000 gross acres, in January 2017. We have a 50 percent operated interest in this block which includes the Salam-1 oil discovery.

We completed a 3-D seismic survey in Block SK 313 and Block WL4-00 in 2017. Further exploration drilling is expected to occur in 2018.

14

Brunei

Exploration

We have a 6.25 percent working interest in the deepwater Block CA-2 PSC. Exploration has been ongoing since September 2011, with natural gas discovered at the Kelidang NE-1 and Keratau-1 wells in 2013 and at the Keratau SW-1 Well in 2015. Evaluation of the results is ongoing.

Qatar

| 2017 | ||||||||||||||||||||

|

| |||||||||||||||||||

| Interest | Operator | Liquids MBD | Natural Gas MMCFD | Total MBOED | ||||||||||||||||

|

|

|

|

|

| |||||||||||||||

Average Daily Net Production | ||||||||||||||||||||

| Qatargas Operating | ||||||||||||||||||||

QG3 | 30.0 | % | Company Limited | 21 | 369 | 83 | ||||||||||||||

| ||||||||||||||||||||

Total Qatar | 21 | 369 | 83 | |||||||||||||||||

| ||||||||||||||||||||

QG3 is an integrated development jointly owned by Qatar Petroleum (68.5 percent), ConocoPhillips (30 percent) and Mitsui & Co., Ltd. (1.5 percent). QG3 consists of upstream natural gas production facilities, which produce approximately 1.4 billion gross cubic feet per day of natural gas from Qatar's North Field over a 25-year life, in addition to a 7.8 million gross tonnes-per-year LNG facility. LNG is shipped in leased LNG carriers destined for sale globally.

QG3 executed the development of the onshore and offshore assets as a single integrated development with Qatargas 4 (QG4), a joint venture between Qatar Petroleum and Royal Dutch Shell plc. This included the joint development of offshore facilities situated in a common offshore block in the North Field, as well as the construction of two identical LNG process trains and associated gas treating facilities for both the QG3 and QG4 joint ventures. Production from the LNG trains and associated facilities is combined and shared.

OTHER INTERNATIONAL

The Other International segment includes exploration activities in Colombia and Chile.

Colombia

Unconventional Exploration

We have an 80 percent operated interest in the Middle Magdalena Basin Block VMM-3. The block extends over approximately 67,000 net acres and contains the Picoplata-1 well, which completed drilling in 2015 and testing in 2017. Socialization and environmental permitting activities are expected to continue throughout 2018.

In July 2017, ConocoPhillips Colombia Ventures Ltd. and Canacol Energy Colombia S.A. executed an Additional Contract for the exploration and exploitation of unconventional reservoirs in an area identified as the VMM-2 Block. As a result, ConocoPhillips Colombia Ventures Ltd. and Canacol Energy Colombia S.A. also executed a joint operating agreement. We have an 80 percent operated working interest in the block which extends over approximately 58,000 net acres and is contiguous to the VMM-3 Block.

In 2017, we relinquished our 70 percent nonoperated interests in the deep rights in the Santa Isabel Block and terminated the exploration and production contract for the VMM27 Block, both in the Middle Magdalena Basin.

15

Chile

Exploration

We have a 49 percent interest in the Coiron Block located in the Magallanes Basin in southern Chile. In December 2017, two wells drilled in 2016, were expensed as dry holes.

Venezuela and Ecuador

For discussion of our contingencies in Venezuela and Ecuador, see Note 12-Contingencies and Commitments, in the Notes to Consolidated Financial Statements.

OTHER

Marketing Activities

Our Commercial organization manages our worldwide commodity portfolio, which mainly includes natural gas, crude oil, bitumen, natural gas liquids and LNG. Marketing activities are performed through offices in the United States, Canada, Europe and Asia. In marketing our production, we attempt to minimize flow disruptions, maximize realized prices and manage credit-risk exposure. Commodity sales are generally made at prevailing market prices at the time of sale. We also purchase and sell third-party volumes to better position the company to satisfy customer demand while fully utilizing transportation and storage capacity.

Natural Gas

Our natural gas production, along with third-party purchased gas, is primarily marketed in the United States, Canada, Europe and Asia. Our natural gas is sold to a diverse client portfolio which includes local distribution companies; gas and power utilities; large industrials; independent, integrated or state-owned oil and gas companies; as well as marketing companies. To reduce our market exposure and credit risk, we also transport natural gas via firm and interruptible transportation agreements to major market hubs.

Crude Oil, Bitumen and Natural Gas Liquids

Our crude oil, bitumen and natural gas liquids revenues are derived from production in the United States, Canada, Australia, Asia, Africa and Europe. These commodities are primarily sold under contracts with prices based on market indices, adjusted for location, quality and transportation.

LNG

LNG marketing efforts are focused on equity LNG production facilities located in Australia and Qatar. LNG is primarily sold under long-term contracts with prices based on market indices.

Energy Partnerships

Marine Well Containment Company (MWCC)

We are a founding member of the MWCC, a non-profit organization formed in 2010, which provides well containment equipment and technology in the deepwater U.S. Gulf of Mexico. MWCC's containment system meets the U.S. Bureau of Safety and Environmental Enforcement requirements for a subsea well containment system that can respond to a deepwater well control incident in the U.S. Gulf of Mexico. For additional information, see Note 2-Variable Interest Entities (VIEs), in the Notes to Consolidated Financial Statements.

Subsea Well Response Project (SWRP)

In 2011, we, along with several leading oil and gas companies, launched the SWRP, a non-profit organization based in Stavanger, Norway, which was created to enhance the industry's capability to respond to international subsea well control incidents. Through collaboration with Oil Spill Response Limited, a non-profit organization in the United Kingdom, subsea well intervention equipment is available for the industry to use in the event of a subsea well incident. This complements the work being undertaken in the United States by MWCC.

16

Oil Spill Response Removal Organizations (OSROs)

We maintain memberships in several OSROs across the globe as a key element of our preparedness program in addition to internal response resources. Many of the OSROs are not-for-profit cooperatives owned by the member companies wherein we may actively participate as a member of the board of directors, steering committee, work group or other supporting role. Globally, our primary OSRO is Oil Spill Response Ltd. based in the U.K., with facilities in several other countries and the ability to respond anywhere in the world. In North America, our primary OSROs include the Marine Spill Response Corporation for the continental U.S. and Alaska Clean Seas and Ship Escort/Response Vessel System for the Alaska North Slope and Prince William Sound, respectively. Internationally, we maintain memberships in various regional OSROs including the Norwegian Clean Seas Association for Operating Companies, Australian Marine Oil Spill Center and Petroleum Industry of Malaysia Mutual Aid Group.

Technology

We have several technology programs that improve our ability to develop unconventional reservoirs, produce heavy oil economically with fewer emissions, improve the efficiency of our company's exploration program, increase recoveries from our legacy fields, and implement sustainability measures.

Our Optimized Cascade ® LNG liquefaction technology business continues to be successful with the demand for new LNG plants. The technology has been licensed for use in 25 LNG trains around the world, with feasibility studies ongoing for additional trains.

17

RESERVES

We have not filed any information with any other federal authority or agency with respect to our estimated total proved reserves at December 31, 2017. No difference exists between our estimated total proved reserves for year-end 2016 and year-end 2015, which are shown in this filing, and estimates of these reserves shown in a filing with another federal agency in 2017.

DELIVERY COMMITMENTS

We sell crude oil and natural gas from our producing operations under a variety of contractual arrangements, some of which specify the delivery of a fixed and determinable quantity. Our commercial organization also enters into natural gas sales contracts where the source of the natural gas used to fulfill the contract can be the spot market or a combination of our reserves and the spot market. Worldwide, we are contractually committed to deliver approximately 1.7 trillion cubic feet of natural gas, including approximately 303 billion cubic feet related to the noncontrolling interests of consolidated subsidiaries, and 99 million barrels of crude oil in the future. These contracts have various expiration dates through the year 2029. We expect to fulfill the majority of these delivery commitments with proved developed reserves. In addition, we anticipate using proved undeveloped reserves and spot market purchases to fulfill any remaining commitments. See the disclosure on "Proved Undeveloped Reserves" in the "Oil and Gas Operations" section following the Notes to Consolidated Financial Statements, for information on the development of proved undeveloped reserves.

COMPETITION

We compete with private, public and state-owned companies in all facets of the E&P business. Some of our competitors are larger and have greater resources. Each of our segments is highly competitive, with no single competitor, or small group of competitors, dominating.

We compete with numerous other companies in the industry, including state-owned companies, to locate and obtain new sources of supply and to produce oil, bitumen, natural gas liquids and natural gas in an efficient, cost-effective manner. Based on statistics published in the September 4, 2017, issue of the Oil and Gas Journal , we were the third-largest U.S.-based oil and gas company in worldwide liquids production and reserves, and the fourth-largest U.S.-based oil and gas company in worldwide natural gas production and reserves in 2016. We deliver our production into the worldwide commodity markets. Principal methods of competing include geological, geophysical and engineering research and technology; experience and expertise; economic analysis in connection with portfolio management; and safely operating oil and gas producing properties.

GENERAL

At the end of 2017, we held a total of 734 active patents in 47 countries worldwide, including 328 active U.S. patents. During 2017, we received 32 patents in the United States and 40 foreign patents. Our products and processes generated licensing revenues of $79 million in 2017. The overall profitability of any business segment is not dependent on any single patent, trademark, license, franchise or concession.

Company-sponsored research and development activities charged against earnings were $100 million, $116 million and $222 million in 2017, 2016 and 2015, respectively.

Health, Safety and Environment

Our Health, Safety and Environment (HSE) organization provides tools and support to our business units and staff groups to help them ensure world class health, safety and environmental performance. The framework through which we safely manage our operations, the HSE Management System Standard, emphasizes process safety, risk management, emergency preparedness and environmental performance, with an intense focus on

18

process and occupational safety. In support of the goal of zero incidents, HSE milestones and criteria are established annually to drive strong safety performance. Progress toward these milestones and criteria are measured and reported. HSE audits are conducted on business functions periodically, and improvement actions are established and tracked to completion. We also have detailed processes in place to address sustainable development in our economic, environmental and social performance. Our processes, related tools and requirements focus on water, biodiversity and climate change, as well as social and stakeholder issues.

The environmental information contained in Management's Discussion and Analysis of Financial Condition and Results of Operations on pages 61 through 64 under the captions "Environmental" and "Climate Change" is incorporated herein by reference. It includes information on expensed and capitalized environmental costs for 2017 and those expected for 2018 and 2019.

Website Access to SEC Reports

Our internet website address is www.conocophillips.com . Information contained on our internet website is not part of this report on Form 10-K.

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available on our website, free of charge, as soon as reasonably practicable after such reports are filed with, or furnished to, the U.S. Securities and Exchange Commission (SEC). Alternatively, you may access these reports at the SEC's website at www.sec.gov .

19

Item 1A. RISK FACTORS

You should carefully consider the following risk factors in addition to the other information included in this Annual Report on Form 10-K. Each of these risk factors could adversely affect our business, operating results and financial condition, as well as adversely affect the value of an investment in our common stock.

Our operating results, our future rate of growth and the carrying value of our assets are exposed to the effects of changing commodity prices.

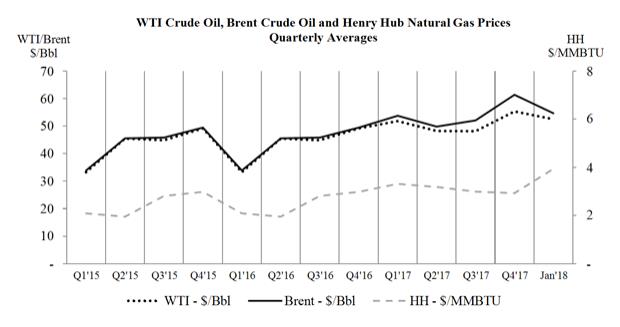

Prices for crude oil, bitumen, natural gas, natural gas liquids and LNG can fluctuate widely. Globally, prices for crude oil, bitumen, natural gas, natural gas liquids and LNG have experienced significant declines from their historic levels during 2013 and 2014, with excess of supply relative to global demand leading to global inventory builds. Total average annual prices in 2017 for Brent crude oil, WTI crude oil, Henry Hub natural gas and our realized natural gas liquids all decreased by at least 30 percent when compared with 2014 despite having improved by at least 18 percent when compared with 2016. Given volatility in commodity price drivers and the business environment, price trends may not continue or reverse themselves.

Our revenues, operating results and future rate of growth are highly dependent on the prices we receive for our crude oil, bitumen, natural gas, natural gas liquids and LNG. The factors influencing these prices are beyond our control. Lower crude oil, bitumen, natural gas, natural gas liquids and LNG prices may have a material adverse effect on our revenues, operating income, cash flows and liquidity and on the amount of dividends we elect to declare and pay on our common stock. Lower prices may also limit the amount of reserves we can produce economically, adversely affecting our reserve replacement ratio and accelerating the reduction in our existing reserve levels as we continue production from upstream fields.

Significant reductions in crude oil, bitumen, natural gas, natural gas liquids and LNG prices could also require us to reduce our capital expenditures or impair the carrying value of our assets. In the past three years, we recognized several impairments, which are described in Note 8-Impairments and the "APLNG" section of Note 5-Investments, Loans and Long-Term Receivables, in the Notes to Consolidated Financial Statements. If commodity prices remain low relative to their historic levels, and as we continue to optimize our investments and exercise capital flexibility, it is reasonably likely we will incur future impairments to long-lived assets used in operations, investments in nonconsolidated entities accounted for under the equity method and unproved properties. Although it is not reasonably practicable to quantify the impact of any future impairments at this time, our results of operations could be adversely affected as a result.

Our ability to declare and pay dividends and repurchase shares is subject to certain considerations.

Dividends are authorized and determined by our Board of Directors in its sole discretion and depend upon a number of factors, including:

| • | Cash available for distribution. |

| • | Our results of operations and anticipated future results of operations. |

| • | Our financial condition, especially in relation to the anticipated future capital needs of our properties. |

| • | The level of reserves we establish for future capital expenditures. |

| • | The level of distributions paid by comparable companies. |

| • | Our operating expenses. |

| • | Other factors our Board of Directors deems relevant. |

We expect to continue to pay quarterly distributions to our stockholders; however, we bear all expenses incurred by our operations, and our funds generated by operations, after deducting these expenses, may not be sufficient to cover desired levels of distributions to our stockholders.

20

Additionally, our share repurchase program does not obligate us to acquire any specific number of shares. Any downward revision in our distribution or share repurchase program could have a material adverse effect on the market price of our common stock.

We may need additional capital in the future, and it may not be available on acceptable terms.

We have historically relied primarily upon cash generated by our operations to fund our operations and strategy, however we have also relied from time to time on access to the debt and equity capital markets for funding. There can be no assurance that additional debt or equity financing will be available in the future on acceptable terms, or at all. In addition, although we anticipate we will be able to repay our existing indebtedness when it matures or in accordance with our stated plans, there can be no assurance we will be able to do so. Our ability to obtain additional financing, or refinance our existing indebtedness when it matures or in accordance with our stated plans, will be subject to a number of factors, including market conditions, our operating performance, investor sentiment and our ability to incur additional debt in compliance with agreements governing our then-outstanding debt. If we are unable to generate sufficient funds from operations or raise additional capital, our growth could be impeded.

In addition, we are regularly evaluated by the major rating agencies based on a number of factors, including our financial strength and conditions affecting the oil and gas industry generally. For example, due to the significant decline in prices for crude oil, bitumen, natural gas, natural gas liquids and LNG in 2015, and the expectation that these prices could remain depressed, the major ratings agencies conducted a review of the oil and gas industry and downgraded our debt ratings and those of several companies operating in the industry in 2016. Any downgrade in our credit rating, could increase the cost associated with any additional indebtedness we incur.

Our business may be adversely affected by deterioration in the credit quality of, or defaults under our contracts with, third parties with whom we do business.

The operation of our business requires us to engage in transactions with numerous counterparties operating in a variety of industries, including other companies operating in the oil and gas industry. These counterparties may default on their obligations to us as a result of operational failures or a lack of liquidity, or for other reasons, including bankruptcy. Market speculation about the credit quality of these counterparties, or their ability to continue performing on their existing obligations, may also exacerbate any operational difficulties or liquidity issues they are experiencing, particularly as it relates to other companies in the oil and gas industry as a result of the volatility in commodity prices. Any default by any of our counterparties may result in our inability to perform obligations under agreements we have made with third parties or may otherwise adversely affect our business or results of operations. In addition, our rights against any of our counterparties as a result of a default may not be adequate to compensate us for the resulting harm caused or may not be enforceable at all in some circumstances.

Unless we successfully add to our existing proved reserves, our future crude oil, bitumen, natural gas and natural gas liquids production will decline, resulting in an adverse impact to our business.

The rate of production from upstream fields generally declines as reserves are depleted. Except to the extent that we conduct successful exploration and development activities, or, through engineering studies, optimize production performance or identify additional or secondary recovery reserves, our proved reserves will decline materially as we produce crude oil, bitumen, natural gas and natural gas liquids. Accordingly, to the extent we are unsuccessful in replacing the crude oil, bitumen, natural gas and natural gas liquids we produce with good prospects for future production, our business will experience reduced cash flows and results of operations. Any cash conservation efforts we may undertake as a result of commodity price declines may further limit our ability to replace depleted reserves.

21

The exploration and production of oil and gas is a highly competitive industry.

The exploration and production of crude oil, bitumen, natural gas and natural gas liquids is a highly competitive business. We compete with private, public and state-owned companies in all facets of the exploration and production business, including to locate and obtain new sources of supply and to produce oil, bitumen, natural gas and natural gas liquids in an efficient, cost-effective manner. Some of our competitors are larger and have greater resources than we do or may be willing to incur a higher level of risk than we are willing to incur to obtain potential sources of supply. If we are not successful in our competition for new reserves, our financial condition and results of operations may be adversely affected.

Any material change in the factors and assumptions underlying our estimates of crude oil, bitumen, natural gas and natural gas liquids reserves could impair the quantity and value of those reserves.

Our proved reserve information included in this annual report has been derived from engineering estimates prepared by our personnel. Reserve estimation is a process that involves estimating volumes to be recovered from underground accumulations of crude oil, bitumen, natural gas and natural gas liquids that cannot be directly measured. As a result, different petroleum engineers, each using industry-accepted geologic and engineering practices and scientific methods, may produce different estimates of reserves and future net cash flows based on the same available data. Any significant future price changes could have a material effect on the quantity and present value of our proved reserves. Any material changes in the factors and assumptions underlying our estimates of these items could result in a material negative impact to the volume of reserves reported or could cause us to incur impairment expenses on property associated with the production of those reserves. Future reserve revisions could also result from changes in, among other things, governmental regulation. In addition to changes in the quantity and value of our proved reserves, the amount of crude oil, bitumen, natural gas and natural gas liquids that can be obtained from any proved reserve may ultimately be different from those estimated prior to extraction.

We expect to continue to incur substantial capital expenditures and operating costs as a result of our compliance with existing and future environmental laws and regulations. Likewise, future environmental laws and regulations, such as limitations on greenhouse gas emissions, may impact or limit our current business plans and reduce demand for our products.

Our businesses are subject to numerous laws and regulations relating to the protection of the environment. These laws and regulations continue to increase in both number and complexity and affect our operations with respect to, among other things:

| • | The discharge of pollutants into the environment. |