UNITED STATES

SECURITIES AND EXCHANGE

COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13

OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2011

Commission file number 1-9924

Citigroup

Inc.

(Exact name of registrant as

specified in its charter)

| Delaware | 52-1568099 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

| 399 Park Avenue, New York, NY | 10022 |

| (Address of principal executive offices) | (Zip code) |

Registrant's telephone number, including area code: (212) 559-1000

Securities registered pursuant to Section 12(b) of the Act: See Exhibit 99.01

Securities registered pursuant to Section 12(g) of the Act: none

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o Yes X No

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes X No

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. X Yes o No

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). X Yes o No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| X Large accelerated filer | o Accelerated filer | o Non-accelerated filer | o Smaller reporting company |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes X No

The aggregate market value of Citigroup Inc. common stock held by non-affiliates of Citigroup Inc. on June 30, 2011 was approximately $121.3 billion.

Number of shares of common stock outstanding on January 31, 2012: 2,928,662,136

Documents Incorporated by Reference: Portions of the Registrant's Proxy Statement for the annual meeting of stockholders scheduled to be held on April 17, 2012, are incorporated by reference in this Form 10-K in response to Items 10, 11, 12, 13 and 14 of Part III.

10-K CROSS-REFERENCE INDEX

This Annual Report on Form 10-K incorporates the requirements of the accounting profession and the Securities and Exchange Commission.

| FORM 10-K | ||||

| Item Number | Page | |||

| Part I | ||||

| 1. | Business | 4–36, 40, 116–121, | ||

| 124–125, 156, 287–289 | ||||

| 1A. | Risk Factors | 55–65 | ||

| 1B. | Unresolved Staff Comments | Not Applicable | ||

| 2. | Properties | 289 | ||

| 3. | Legal Proceedings | 267–275 | ||

| 4. | Mine Safety Disclosures | Not Applicable | ||

| Part II | ||||

| 5. | Market for Registrant's | |||

| Common Equity, | ||||

| Related Stockholder Matters, and Issuer Purchases of | ||||

| Equity Securities | 43, 163, 285, | |||

| 290–291, 293 | ||||

| 6. | Selected Financial Data | 10–11 | ||

| 7. | Management's Discussion | |||

| and Analysis of Financial | ||||

| Condition and Results of Operations | 6–54, 66–115 | |||

| 7A. | Quantitative and Qualitative | |||

| Disclosures About Market Risk | 66–115, 157–158, | |||

| 181–212, 215–259 | ||||

| 8. | Financial Statements and | |||

| Supplementary Data | 131–286 | |||

| 9. | Changes in and Disagreements | |||

| with Accountants on | ||||

| Accounting and Financial | ||||

| Disclosure | Not Applicable | |||

| 9A. | Controls and Procedures | 122–123 | ||

| 9B. | Other Information | Not Applicable | ||

| Part III | ||||

| 10. | Directors, Executive Officers and | |||

| Corporate Governance | 292–293, 295* | |||

| 11. | Executive Compensation | ** | ||

| 12. | Security Ownership of Certain | |||

| Beneficial Owners and Management | ||||

| and Related Stockholder Matters | *** | |||

| 13. | Certain Relationships and Related | |||

| Transactions, and Director | ||||

| Independence | **** | |||

| 14. | Principal Accounting Fees and | |||

| Services | ***** | |||

| Part IV | ||||

| 15. | Exhibits and Financial Statement | |||

| Schedules | ||||

| * | For additional information regarding Citigroup's Directors, see "Corporate Governance," "Proposal 1: Election of Directors" and "Section 16(a) Beneficial Ownership Reporting Compliance" in the definitive Proxy Statement for Citigroup's Annual Meeting of Stockholders scheduled to be held on April 17, 2012, to be filed with the SEC (the Proxy Statement), incorporated herein by reference. | |

| ** | See "Executive Compensation-The Personnel and Compensation Committee Report," "-Compensation Discussion and Analysis" and "-2011 Summary Compensation Table" and in the Proxy Statement, incorporated herein by reference. | |

| *** | See "About the Annual Meeting," "Stock Ownership" and "Proposal 3: Approval of Amendment to the Citigroup 2009 Stock Incentive Plan" in the Proxy Statement, incorporated herein by reference. | |

| **** | See "Corporate Governance-Director Independence," "-Certain Transactions and Relationships, Compensation Committee Interlocks and Insider Participation," "-Indebtedness," "Proposal 1: Election of Directors" and "Executive Compensation" in the Proxy Statement, incorporated herein by reference. | |

| ***** | See "Proposal 2: Ratification of Selection of Independent Registered Public Accounting Firm" in the Proxy Statement, incorporated herein by reference. |

2

CITIGROUP'S 2011 ANNUAL REPORT ON FORM 10-K

| OVERVIEW | 4 | |

| CITIGROUP SEGMENTS AND REGIONS | 5 | |

| MANAGEMENT'S DISCUSSION AND ANALYSIS | ||

| OF FINANCIAL CONDITION AND RESULTS | ||

| OF OPERATIONS | 6 | |

| Executive Summary | 6 | |

| RESULTS OF OPERATIONS | 10 | |

| Five-Year Summary of Selected | ||

| Financial Data | 10 | |

| SEGMENT AND BUSINESS-INCOME (LOSS) | ||

| AND REVENUES | 12 | |

| CITICORP | 14 | |

| Global Consumer Banking | 15 | |

| North America Regional Consumer Banking | 16 | |

| EMEA Regional Consumer Banking | 18 | |

| Latin America Regional Consumer Banking | 20 | |

| Asia Regional Consumer Banking | 22 | |

| Institutional Clients Group | 24 | |

| Securities and Banking | 26 | |

| Transaction Services | 28 | |

| CITI HOLDINGS | 30 | |

| Brokerage and Asset Management | 31 | |

| Local Consumer Lending | 32 | |

| Special Asset Pool | 35 | |

| CORPORATE/OTHER | 36 | |

| BALANCE SHEET REVIEW | 37 | |

| Segment Balance Sheet at December 31, 2011 | 40 | |

| CAPITAL RESOURCES AND LIQUIDITY | 41 | |

| Capital Resources | 41 | |

| Funding and Liquidity | 47 | |

| Off-Balance-Sheet Arrangements | 53 | |

| CONTRACTUAL OBLIGATIONS | 54 | |

| RISK FACTORS | 55 | |

| MANAGING GLOBAL RISK | 66 | |

| Risk Management-Overview | 66 | |

| Risk Aggregation and Stress Testing | 67 | |

| Risk Capital | 67 | |

| Credit Risk | 67 | |

| Loans Outstanding | 68 | |

| Details of Credit Loss Experience | 69 | |

| Non-Accrual Loans and Assets, and | ||

| Renegotiated Loans | 71 | |

| North America Consumer Mortgage Lending | 75 | |

| North America Cards | 82 | |

| Consumer Loan Details | 84 | |

| Consumer Loan Modification Programs | 86 |

| Consumer Mortgage-Representations and | ||

| Warranties | 88 | |

| Securities and Banking-Sponsored Legacy Private-Label | ||

| Residential Mortgage Securitizations- | ||

| Representations and Warranties | 91 | |

| Corporate Loan Details | 92 | |

| Exposure to Commercial Real Estate | 94 | |

| Market Risk | 95 | |

| Operational Risk | 106 | |

| Country and Cross-Border Risk | 107 | |

| FAIR VALUE ADJUSTMENTS FOR | ||

| DERIVATIVES AND STRUCTURED DEBT | 113 | |

| CREDIT DERIVATIVES | 114 | |

| SIGNIFICANT ACCOUNTING POLICIES AND | ||

| SIGNIFICANT ESTIMATES | 116 | |

| DISCLOSURE CONTROLS AND PROCEDURES | 122 | |

| MANAGEMENT'S ANNUAL REPORT ON | ||

| INTERNAL CONTROL OVER FINANCIAL | ||

| REPORTING | 123 | |

| FORWARD-LOOKING STATEMENTS | 124 | |

| REPORT OF INDEPENDENT REGISTERED | ||

| PUBLIC ACCOUNTING FIRM-INTERNAL | ||

| CONTROL OVER FINANCIAL REPORTING | 126 | |

| REPORT OF INDEPENDENT REGISTERED | ||

| PUBLIC ACCOUNTING FIRM- | ||

| CONSOLIDATED FINANCIAL STATEMENTS | 127 | |

| FINANCIAL STATEMENTS AND NOTES TABLE | ||

| OF CONTENTS | 129 | |

| CONSOLIDATED FINANCIAL STATEMENTS | 131 | |

| NOTES TO CONSOLIDATED FINANCIAL | ||

| STATEMENTS | 137 | |

| FINANCIAL DATA SUPPLEMENT (Unaudited) | 286 | |

| Ratios | 286 | |

| Average Deposit Liabilities in Offices Outside the U.S. | 286 | |

| Maturity Profile of Time Deposits ($100,000 or more) | ||

| in U.S. Offices | 286 | |

| SUPERVISION AND REGULATION | 287 | |

| Customers | 288 | |

| Competition | 288 | |

| Properties | 289 | |

| Legal Proceedings | 289 | |

| Unregistered Sales of Equity; | ||

| Purchases of Equity Securities; Dividends | 290 | |

| Performance Graph | 291 | |

| CORPORATE INFORMATION | 292 | |

| Citigroup Executive Officers | 292 | |

| CITIGROUP BOARD OF DIRECTORS | 295 |

3

OVERVIEW

Citigroup's history dates back

to the founding of Citibank in 1812. Citigroup's original corporate predecessor

was incorporated in 1988 under the laws of the State of Delaware. Following a

series of transactions over a number of years, Citigroup Inc. was formed in 1998

upon the merger of Citicorp and Travelers Group

Inc.

Citigroup is a global diversified financial services holding company

whose businesses provide consumers, corporations, governments and institutions

with a broad range of financial products and services. Citi has approximately

200 million customer accounts and does business in more than 160 countries and

jurisdictions.

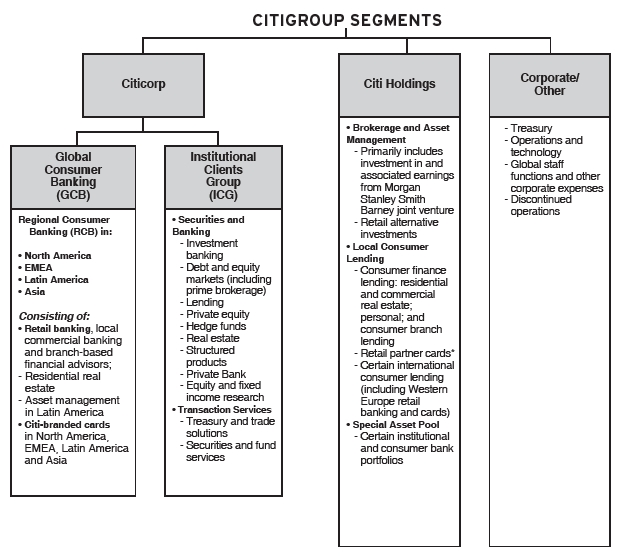

Citigroup currently operates, for management reporting purposes, via two

primary business segments: Citicorp, consisting of Citi's Global Consumer Banking businesses and Institutional Clients Group ; and Citi Holdings, consisting of Brokerage and Asset Management, Local Consumer

Lending and Special Asset Pool . For a further description of the business

segments and the products and services they provide, see "Citigroup Segments"

below, "Management's Discussion and Analysis of Financial Condition and Results

of Operations" and Note 4 to the Consolidated Financial Statements.

Throughout this report, "Citigroup," "Citi" and

"the Company" refer to Citigroup Inc. and its consolidated

subsidiaries.

Additional information about Citigroup is available on Citi's Web site at www.citigroup.com . Citigroup's recent annual reports on Form 10-K,

quarterly reports on Form 10-Q, proxy statements, as well as other filings with

the SEC, are available free of charge through the Citi's Web site by clicking on

the "Investors" page and selecting "All SEC Filings." The SEC's Web site also

contains current reports, information statements, and other information

regarding Citi at www.sec.gov .

Within this Form 10-K, please refer to the tables of contents on pages 3

and 129 for page references to Management's Discussion and Analysis of Financial

Condition and Results of Operations and Notes to Consolidated Financial

Statements, respectively.

At December 31, 2011, Citi had approximately 266,000 full-time employees

compared to approximately 260,000 full-time employees at December 31,

2010.

Please see "Risk Factors" below for a discussion of

certain

risks and uncertainties that could materially impact

Citigroup's financial

condition and results of operations.

Certain reclassifications have been made to the prior periods' financial statements to conform to the current period's presentation.

4

As described above, Citigroup is managed pursuant to the following segments:

* Effective in the first quarter of 2012, Citi will transfer the substantial majority of the retail partner cards business (approximately $45 billion of assets, including approximately $41 billion of loans) from Citi Holdings – Local Consumer Lending to Citicorp- North America RCB .

The following are the four regions in which Citigroup operates. The regional results are fully reflected in the segment results above.

(1) North America includes the U.S., Canada and Puerto Rico, Latin America includes Mexico, and Asia includes Japan.

5

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

EXECUTIVE SUMMARY

Market and Economic

Environment

During 2011,

Citigroup remained focused on executing its strategy of growth through

increasing the returns on and investments in its core businesses of

Citicorp- Global Consumer

Banking and Institutional Clients Group -while continuing to reduce the assets and

businesses within Citi Holdings in an economically rational manner. While Citi

continued to make progress in these areas during the year, its 2011 operating

results were impacted by the ongoing challenging operating environment,

particularly in the second half of the year, as macroeconomic concerns,

including in the U.S. and the Eurozone, weighed heavily on investor and

corporate confidence. Market activity was down globally, with a particular

impact on capital markets-related activities in the fourth quarter of 2011. This

affected Citigroup's results of operations in many businesses, including not

only Securities and

Banking , but also the Securities

and Fund Services business in Transaction Services and

investment sales in Global

Consumer Banking . Citi believes

that the European sovereign debt crisis and its potential impact on the global

markets and growth will likely continue to create macro uncertainty and remain

an issue until the market, investors and Citi's clients and customers believe

that a comprehensive resolution to the crisis is structured, and achievable.

Such uncertainty could have a continued negative impact on investor activity,

and thus on Citi's activity levels and results of operations, in

2012.

Compounding this continuing macroeconomic uncertainty is the ongoing

uncertainty facing Citigroup and its businesses as a result of the numerous

regulatory initiatives underway, both in the U.S. and internationally. As of

December 31, 2011, regulatory changes in significant areas, such as Citi's

future capital requirements and prudential standards, the proposed

implementation of the "Volcker Rule" and the proposed regulation of the

derivatives markets, were incomplete and significant rulemaking and

interpretation remained. See "Risk Factors-Regulatory Risks" below. The

continued uncertainty, including the potential costs, associated with the actual

implementation of these changes will continue to require significant attention

by Citi's management. In addition, it is also not clear what the cumulative

impact of regulatory reform will be.

Citigroup

Citigroup reported net income of $11.1 billion and diluted EPS of $3.63

per share in 2011, compared to $10.6 billion and $3.54 per share, respectively,

in 2010. In 2011, results included a net positive impact of $1.8 billion from

credit valuation adjustments (CVA) on derivatives (excluding monolines), net of

hedges, and debt valuation adjustments (DVA) on Citigroup's fair value option

debt, compared to a net negative impact of $(469) million in 2010. In addition,

Citi has adjusted its 2011 results of operations that were previously announced

on January 17, 2012 for an additional $209 million (after tax) charge. This

charge relates to the agreement in principle with the United States and state attorneys general announced on February 9, 2012 regarding

the settlement of a number of investigations into residential loan servicing and

origination litigation, as well as the resolution of related mortgage litigation

(see Notes 29, 30 and 32 to the Consolidated Financial Statements). Excluding

CVA/DVA, Citi's net income declined $952 million, or 9%, to $9.9 billion in

2011, reflecting lower revenues and higher operating expenses as compared to

2010, partially offset by a significant decline in credit

costs.

Citi's revenues of $78.4 billion were down $8.2 billion, or 10%, compared

to 2010. Excluding CVA/DVA, revenues of $76.5 billion were down $10.5 billion,

or 12%, as lower revenues in Citi Holdings and Securities and Banking more than offset growth in Global Consumer Banking and Transaction Services . Net

interest revenues decreased by $5.7 billion, or 11%, to $48.4 billion in 2011 as

compared to 2010, primarily due to continued declining loan balances and lower

interest-earning assets in Citi Holdings. Non-interest revenues, excluding

CVA/DVA, declined by $4.8 billion, or 15%, to $28.1 billion in 2011 as compared

to 2010, driven by lower revenues in Citi Holdings and Securities and Banking .

Because of Citi's extensive global operations,

foreign exchange translation also impacts Citi's results of operations as Citi

translates revenues, expenses, loan balances and other metrics from foreign

currencies to U.S. dollars in preparing its financial statements. During 2011,

the U.S. dollar generally depreciated versus local currencies in which Citi

operates. As a result, the impact of foreign exchange translation (as used

throughout this Form 10-K, FX translation) accounted for an approximately 1%

growth in Citi's revenues and 2% growth in expenses, while contributing less

than 1% to Citi's pretax net income for the year.

6

Expenses

Citigroup expenses were $50.9 billion in 2011, up

$3.6 billion, or 8%, compared to 2010. Over two-thirds of this increase resulted

from higher legal and related costs (approximately $1.5 billion) and higher

repositioning charges (approximately $200 million, including severance) as

compared to 2010, as well as the impact of FX translation (approximately $800

million). Excluding these items, expenses were up $1.0 billion, or 2%, compared

to the prior year.

Investment spending was $3.9 billion higher in

2011, of which roughly half was funded with efficiency savings, primarily in

operations and technology, labor reengineering and business support functions

(e.g., call centers and collections) of $1.9 billion. The $3.9 billion increase

in investment spending in 2011 included higher investments in Global Consumer Banking ($1.6 billion, including incremental cards

marketing campaigns and new branch openings), Securities and Banking (approximately $800 million, including new hires

and technology investments) and Transaction Services (approximately $600 million, including new mandates and platform enhancements),

as well as additional firm-wide initiatives and investments to comply with

regulatory requirements. All other expense increases, including higher

volume-related costs in Citicorp, were more than offset by a decline in Citi

Holdings expenses. While Citi will continue some level of incremental investment

spending in its businesses going forward, Citi currently believes these

increases in investments will be self-funded through ongoing reengineering and

efficiency savings. Accordingly, Citi believes that the increased level of

investment spending incurred during the latter part of 2010 and 2011 was

largely completed by year end 2011.

Citicorp expenses were $39.6 billion in 2011, up $3.5 billion, or 10%,

compared to 2010. Over one-third of this increase resulted from higher legal and

related costs and higher repositioning charges (including severance) as compared

to 2010, as well as the impact of FX translation. The remainder of the increase

was primarily driven by investment spending (as described above), partially

offset by ongoing productivity savings and other expense reductions.

Citi Holdings expenses were $8.8 billion in 2011,

down $824 million, or 9%, principally due to the continued decline in assets,

partially offset by higher legal and related costs.

Credit

Costs

Credit trends for

Citigroup continued to improve in 2011, particularly for Citi's North America Citi-branded and retail partner cards businesses,

as well as its North

America mortgage portfolios in

Citi Holdings, although the pace of improvement in these businesses slowed.

Citi's total provisions for credit losses and for benefits and claims of $12.8

billion declined $13.2 billion, or 51%, from 2010. Net credit losses of $20.0

billion in 2011 were down $10.8 billion, or 35%, reflecting improvement in both

Consumer and Corporate credit trends. Consumer net credit losses declined $10.0

billion, or 35%, to $18.4 billion, driven by continued improvement in credit in North America Citi-branded cards and retail partner cards and North America real estate lending in Citi Holdings. Corporate

net credit losses decreased $810 million, or 33%, to $1.6 billion, as credit

quality continued to improve in the Corporate

portfolio.

The net release of allowance for loan losses and unfunded lending

commitments was $8.2 billion in 2011, compared to a net release of $5.8 billion

in 2010. Of the $8.2 billion net reserve release in 2011, $5.9 billion related

to Consumer and was mainly driven by North America Citi-branded

cards and retail partner cards. The $2.3 billion net Corporate reserve release

reflected continued improvement in Corporate credit trends, partially offset by

loan growth.

More than half of the net credit reserve release in 2011, or $4.8

billion, was attributable to Citi Holdings. The $3.5 billion net credit release

in Citicorp increased from $2.2 billion in the prior year, as a higher net

release in Citi-branded cards in North America was

partially offset by lower net releases in international Regional Consumer Banking and the Corporate portfolio, each driven by loan

growth.

7

Capital and Loan Loss

Reserve Positions

Citigroup's capital and loan loss reserve positions remained strong at

year end 2011. Citigroup's Tier 1 Capital ratio was 13.6% and the Tier 1 Common

ratio was 11.8%.

Citigroup's total allowance for loan

losses was $30.1 billion at year end 2011, or 4.7% of total loans, down from

$40.7 billion, or 6.3% of total loans, at the end of the prior year. The decline

in the total allowance for loan losses reflected asset sales, lower non-accrual

loans, and overall continued improvement in the credit quality of Citi's loan

portfolios. The Consumer allowance for loan losses was $27.2 billion, or 6.45%,

of total Consumer loans at year end 2011, compared to $35.4 billion, or 7.80%,

of total Consumer loans at year end 2010. See details of "Credit Loss

Experience-Allowance for Loan Losses" below for additional information on Citi's

loan loss coverage ratios as of December 31,

2011.

Citigroup's non-accrual loans of $11.2 billion at year end 2011 declined

42% from the prior year, and the allowance for loan losses represented 268% of

non-accrual loans.

Citicorp

Citicorp

net income of $14.4 billion in 2011 decreased by $269 million, or 2%, from the

prior year. Excluding CVA/DVA, Citicorp's net income declined $1.6

billion, or 10.6%, to $13.4 billion in 2011, reflecting lower revenues and

higher operating expenses, partially offset by the significantly lower credit

costs. Asia and Latin America contributed

roughly half of Citicorp's net income for the year.

Citicorp revenues were $64.6 billion, down $989

million, or 2%, from 2010. Excluding CVA/DVA, revenues of $62.8 billion were

down $3.1 billion, or 5%, as compared to 2010. Net interest revenues decreased

by $450 million, or 1%, to $38.1 billion, as lower revenues in North America Regional Consumer

Banking and Securities and Banking more than offset growth in Latin America and Asia Regional Consumer Banking and Transaction

Services . Non-interest revenues,

excluding CVA/DVA, declined by $2.7 billion, or 10%, to $24.7 billion in 2011 as

compared to 2010, driven by lower revenues in Securities and Banking .

Global Consumer Banking revenues of $32.6 billion were up $211 million

year-over-year, as continued growth in Asia and Latin America Regional Consumer

Banking was partially offset by

lower revenues in North America

Regional Consumer Banking . The

2011 results in Global Consumer

Banking included continued

momentum in Citi's international regions, as well as early signs of growth in

its North America business:

Securities and

Banking revenues of $21.4

billion decreased 7% year-over-year. Excluding CVA/DVA (for details on Securities and

Banking CVA/DVA amounts, see

" Institutional Clients

Group-Securities and Banking "

below), revenues were $19.7 billion, down 16% from the prior year, due primarily

to the continued challenging macroeconomic environment, which resulted in lower

revenues across fixed income and equity markets as well as investment

banking.

Fixed income markets revenues, which

constituted over 50% of Securities and

Banking revenues in 2011, of $10.9

billion, excluding CVA/DVA, decreased 24% in 2011 as compared to 2010, driven

primarily by a decline in credit-related and securitized products and, to a

lesser extent, a decline in rates and currencies. Equity markets revenues of

$2.4 billion, excluding CVA/DVA, were down 35% year-over-year, mainly driven by

weak trading performance in equity derivatives as well as losses in equity

proprietary trading resulting from the wind down of this business, which was

complete as of December 31, 2011. Investment banking revenues of $3.3 billion

were down 14% in 2011 as compared to 2010, driven by lower market activity

levels across all products. Lending revenues of $1.8 billion were up $840

million, from $962 million in 2010, primarily due to net hedging gains of $73

million in 2011, as compared to net hedging losses of $711 million in 2010,

driven by spread tightening in Citi's lending portfolio.

Transaction Services revenues were $10.6 billion in 2011, up 5% from

the prior year, driven by growth in Treasury and Trade Solutions as well as

Securities and Fund Services. Revenues grew in 2011 in all international regions

as strong growth in business volumes was partially offset by continued spread

compression. Average deposits and other customer liabilities grew 9% in 2011,

while assets under custody remained relatively flat year over year.

Citicorp end of period loans increased 14% in 2011

to $465.4 billion, with 7% growth in Consumer loans and 24% growth in Corporate

loans.

8

Citi

Holdings

Citi Holdings'

net loss of $(2.6) billion in 2011 improved by $1.6 billion as compared to the

net loss in 2010. The improvement in 2011 reflected a significant decline in

credit costs and lower operating expenses, given the continued decline in

assets, partially offset by lower revenues.

While Citi Holdings' impact on Citi has been declining, it will likely

continue to present a headwind for Citi's overall performance due to, among

other factors, the lower percentage of interest-earning assets remaining in Citi

Holdings, the slower pace of asset reductions and the transfer of the

substantial majority of retail partner cards out of Citi Holdings into

Citicorp- North America Regional

Consumer Banking in the first

quarter of 2012. During the first quarter of 2012, Citi will republish its

historical segment reporting for Citicorp and Citi Holdings to reflect this

transfer in prior periods. The adjusted net loss in Citi Holdings for these

historical periods will be higher than previously reported, as the retail

partner cards business in Local

Consumer Lending was the primary

source of profitability in Citi Holdings.

Citi

Holdings' revenues declined 33% to $12.9 billion from the prior year. Net

interest revenues decreased by $4.5 billion, or 30%, to $10.3 billion, primarily

due to the decline in assets, including lower interest-earning assets in the Special Asset Pool . Non-interest revenues declined by $1.9 billion,

or 42%, to $2.6 billion in 2011, driven by lower gains on asset sales and other

revenue marks as compared to 2010, as well as divestitures.

Citi Holdings' assets declined $90 billion, or 25%, to $269 billion at

the end of 2011, although Citi believes the pace of asset wind-down in Citi

Holdings will decrease going forward. The decline during 2011 reflected nearly

$49 billion in asset sales and business dispositions, $35 billion in net run-off

and amortization and approximately $6 billion in net cost of credit and net

asset marks. As of December 31, 2011, Local Consumer Lending continued to represent the largest segment within Citi Holdings, with $201

billion of assets. Over half of Local Consumer Lending assets, or approximately $109 billion, were related to North America real estate lending. As of December 31, 2011,

there were approximately $10 billion of loan loss reserves allocated to North America real estate lending in Citi Holdings,

representing roughly 31 months of coincident net credit loss coverage.

At the end of 2011, Citi Holdings assets comprised

approximately 14% of total Citigroup GAAP assets and 25% of its risk-weighted

assets. The first quarter of 2012 transfer of the substantial majority of the

retail partner cards business (approximately $45 billion of assets, including

approximately $41 billion of loans) will result in Citi Holdings comprising

approximately 12% of total Citigroup GAAP assets and 21% of risk-weighted

assets.

9

RESULTS OF OPERATIONS

| FIVE-YEAR SUMMARY OF SELECTED FINANCIAL DATA-PAGE 1 | Citigroup Inc. and Consolidated Subsidiaries | ||||||||||||||

| In millions of dollars, except per-share amounts, ratios and direct staff | 2011 | (1) | 2010 | (2)(3) | 2009 | (3) | 2008 | (3) | 2007 | (3) | |||||

| Net interest revenue | $ | 48,447 | $ | 54,186 | $ | 48,496 | $ | 53,366 | $ | 45,300 | |||||

| Non-interest revenue | 29,906 | 32,415 | 31,789 | (1,767 | ) | 32,000 | |||||||||

| Revenues, net of interest expense | $ | 78,353 | $ | 86,601 | $ | 80,285 | $ | 51,599 | $ | 77,300 | |||||

| Operating expenses | 50,933 | 47,375 | 47,822 | 69,240 | 58,737 | ||||||||||

| Provisions for credit losses and for benefits and claims | 12,796 | 26,042 | 40,262 | 34,714 | 17,917 | ||||||||||

| Income (loss) from continuing operations before income taxes | $ | 14,624 | $ | 13,184 | $ | (7,799 | ) | $ | (52,355 | ) | $ | 646 | |||

| Income taxes (benefits) | 3,521 | 2,233 | (6,733 | ) | (20,326 | ) | (2,546 | ) | |||||||

| Income (loss) from continuing operations | $ | 11,103 | $ | 10,951 | $ | (1,066 | ) | $ | (32,029 | ) | $ | 3,192 | |||

| Income (loss) from discontinued operations, net of taxes (4) | 112 | (68 | ) | (445 | ) | 4,002 | 708 | ||||||||

| Net income (loss) before attribution of noncontrolling interests | $ | 11,215 | $ | 10,883 | $ | (1,511 | ) | $ | (28,027 | ) | $ | 3,900 | |||

| Net income (loss) attributable to noncontrolling interests | 148 | 281 | 95 | (343 | ) | 283 | |||||||||

| Citigroup's net income (loss) | $ | 11,067 | $ | 10,602 | $ | (1,606 | ) | $ | (27,684 | ) | $ | 3,617 | |||

| Less: | |||||||||||||||

| Preferred dividends-Basic | $ | 26 | $ | 9 | $ | 2,988 | $ | 1,695 | $ | 36 | |||||

| Impact of the conversion price reset related to the $12.5 billion | |||||||||||||||

| convertible preferred stock private issuance-Basic | - | - | 1,285 | - | - | ||||||||||

| Preferred stock Series H discount accretion-Basic | - | - | 123 | 37 | - | ||||||||||

| Impact of the public and private preferred stock exchange offer | - | - | 3,242 | - | - | ||||||||||

| Dividends and undistributed earnings allocated to employee restricted | |||||||||||||||

| and deferred shares that contain nonforfeitable rights to dividends, | |||||||||||||||

| applicable to Basic EPS | 186 | 90 | 2 | 221 | 261 | ||||||||||

| Income (loss) allocated to unrestricted common shareholders for Basic EPS | $ | 10,855 | $ | 10,503 | $ | (9,246 | ) | $ | (29,637 | ) | $ | 3,320 | |||

| Less: Convertible preferred stock dividends (5) | - | - | (540 | ) | (877 | ) | - | ||||||||

| Add: Interest expense, net of tax, on convertible securities and | |||||||||||||||

| adjustment of undistributed earnings allocated to employee | |||||||||||||||

| restricted and deferred shares that contain nonforfeitable rights to | |||||||||||||||

| dividends, applicable to diluted EPS | 17 | 2 | - | - | - | ||||||||||

| Income (loss) allocated to unrestricted common shareholders for diluted EPS (5) | $ | 10,872 | $ | 10,505 | $ | (8,706 | ) | $ | (28,760 | ) | $ | 3,320 | |||

| Earnings per share (6) | |||||||||||||||

| Basic | |||||||||||||||

| Income (loss) from continuing operations | 3.69 | 3.66 | (7.61 | ) | (63.89 | ) | 5.32 | ||||||||

| Net income (loss) | 3.73 | 3.65 | (7.99 | ) | (56.29 | ) | 6.77 | ||||||||

| Diluted (5) | |||||||||||||||

| Income (loss) from continuing operations | $ | 3.59 | $ | 3.55 | $ | (7.61 | ) | $ | (63.89 | ) | $ | 5.30 | |||

| Net income (loss) | 3.63 | 3.54 | (7.99 | ) | (56.29 | ) | 6.74 | ||||||||

| Dividends declared per common share | 0.03 | 0.00 | 0.10 | 11.20 | 21.60 | ||||||||||

Statement continues on the next page, including notes to the table.

10

| FIVE-YEAR SUMMARY OF SELECTED FINANCIAL DATA-PAGE 2 | Citigroup Inc. and Consolidated Subsidiaries | |||||||||||||||

| In millions of dollars, except per-share amounts, ratios and direct staff | 2011 | (1) | 2010 | (2) | 2009 | (3) | 2008 | (3) | 2007 | (3) | ||||||

| At December 31 | ||||||||||||||||

| Total assets | $ | 1,873,878 | $ | 1,913,902 | $ | 1,856,646 | $ | 1,938,470 | $ | 2,187,480 | ||||||

| Total deposits | 865,936 | 844,968 | 835,903 | 774,185 | 826,230 | |||||||||||

| Long - term debt | 323,505 | 381,183 | 364,019 | 359,593 | 427,112 | |||||||||||

| Mandatorily redeemable securities of subsidiary trusts (included in long-term debt) | 16,057 | 18,131 | 19,345 | 24,060 | 23,756 | |||||||||||

| Common stockholders' equity | 177,494 | 163,156 | 152,388 | 70,966 | 113,447 | |||||||||||

| Total Citigroup stockholders' equity | 177,806 | 163,468 | 152,700 | 141,630 | 113,447 | |||||||||||

| Direct staff (in thousands) | 266 | 260 | 265 | 323 | 375 | |||||||||||

| Ratios | ||||||||||||||||

| Return on average common stockholders' equity (7) | 6.3 | % | 6.8 | % | (9.4 | )% | (28.8 | )% | 2.9 | % | ||||||

| Return on average total stockholders' equity (7) | 6.3 | 6.8 | (1.1 | ) | (20.9 | ) | 3.0 | |||||||||

| Tier 1 Common (8) | 11.80 | % | 10.75 | % | 9.60 | % | 2.30 | % | 5.02 | % | ||||||

| Tier 1 Capital | 13.55 | 12.91 | 11.67 | 11.92 | 7.12 | |||||||||||

| Total Capital | 16.99 | 16.59 | 15.25 | 15.70 | 10.70 | |||||||||||

| Leverage (9) | 7.19 | 6.60 | 6.87 | 6.08 | 4.03 | |||||||||||

| Common stockholders' equity to assets | 9.47 | % | 8.52 | % | 8.21 | % | 3.66 | % | 5.19 | % | ||||||

| Total Citigroup stockholders' equity to assets | 9.49 | 8.54 | 8.22 | 7.31 | 5.19 | |||||||||||

| Dividend payout ratio (10) | 0.8 | NM | NM | NM | 320.5 | |||||||||||

| Book value per common share (6) | $ | 60.70 | $ | 56.15 | $ | 53.50 | $ | 130.21 | $ | 227.12 | ||||||

| Ratio of earnings to fixed charges and preferred stock dividends | 1.59 | x | 1.51 | x | NM | NM | 1.01 | x | ||||||||

| (1) | As noted in the "Executive Summary" above, Citi has adjusted its 2011 results of operations that were previously announced on January 17, 2012 for an additional $209 million (after tax) charge. This charge relates to the agreement in principle with the United States and state attorneys general announced on February 9, 2012 regarding the settlement of a number of investigations into residential loan servicing and origination litigation, as well as the resolution of related mortgage litigation. The impact of these adjustments was a $275 million (pretax) increase in Other operating expenses , a $209 million (after-tax) reduction in Net income and a $0.06 (after-tax) reduction in Diluted earnings per share , for the full year of 2011. See Notes 29, 30 and 32 to the Consolidated Financial Statements. | |

| (2) | On January 1, 2010, Citigroup adopted SFAS 166/167. Prior periods have not been restated as the standards were adopted prospectively. See Note 1 to the Consolidated Financial Statements. | |

| (3) | On January 1, 2009, Citigroup adopted SFAS No. 160, Noncontrolling Interests in Consolidated Financial Statements (now ASC 810-10-45-15, Consolidation: Noncontrolling Interest in a Subsidiary ), and FSP EITF 03-6-1, "Determining Whether Instruments Granted in Share-Based Payment Transactions Are Participating Securities" (now ASC 260-10-45-59A, Earnings Per Share: Participating Securities and the Two-Class Method ). All prior periods have been restated to conform to the current period's presentation. | |

| (4) | Discontinued operations for 2007 to 2009 reflect the sale of Nikko Cordial Securities to Sumitomo Mitsui Banking Corporation, the sale of Citigroup's German retail banking operations to Crédit Mutuel, and the sale of CitiCapital's equipment finance unit to General Electric. Discontinued operations for 2007 to 2010 also include the operations and associated gain on sale of Citigroup's Travelers Life & Annuity, substantially all of Citigroup's international insurance business, and Citigroup's Argentine pension business sold to MetLife Inc. Discontinued operations for the second half of 2010 also reflect the sale of The Student Loan Corporation and, for 2011, primarily reflect the sale of the Egg Banking PLC credit card business. See Note 3 to the Consolidated Financial Statements. | |

| (5) | The diluted EPS calculation for 2009 and 2008 utilizes basic shares and income allocated to unrestricted common stockholders (Basic) due to the negative income allocated to unrestricted common stockholders. Using diluted shares and income allocated to unrestricted common stockholders (Diluted) would result in anti-dilution. | |

| (6) | All per share amounts and Citigroup shares outstanding for all periods reflect Citigroup's 1-for-10 reverse stock split, which was effective May 6, 2011. | |

| (7) | The return on average common stockholders' equity is calculated using net income less preferred stock dividends divided by average common stockholders' equity. The return on average total Citigroup stockholders' equity is calculated using net income divided by average Citigroup stockholders' equity. | |

| (8) | As defined by the banking regulators, the Tier 1 Common ratio represents Tier 1 Capital less qualifying perpetual preferred stock, qualifying noncontrolling interests in subsidiaries and qualifying mandatorily redeemable securities of subsidiary trusts divided by risk-weighted assets. | |

| (9) | The Leverage ratio represents Tier 1 Capital divided by adjusted average total assets. | |

| (10) | Dividends declared per common share as a percentage of net income per diluted share. | |

| NM | Not meaningful |

11

SEGMENT AND BUSINESS - INCOME (LOSS) AND REVENUES

The following tables show the

income (loss) and revenues for Citigroup on a segment and business

view:

CITIGROUP INCOME (LOSS)

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| Income (loss) from continuing operations | ||||||||||||||

| CITICORP | ||||||||||||||

| Global Consumer Banking | ||||||||||||||

| North America | $ | 2,589 | $ | 650 | $ | 789 | NM | (18 | )% | |||||

| EMEA | 79 | 91 | (220 | ) | (13 | )% | NM | |||||||

| Latin America | 1,601 | 1,789 | 429 | (11 | ) | NM | ||||||||

| Asia | 1,927 | 2,131 | 1,391 | (10 | ) | 53 | ||||||||

| Total | $ | 6,196 | $ | 4,661 | $ | 2,389 | 33 | % | 95 | % | ||||

| Securities and Banking | ||||||||||||||

| North America | $ | 1,011 | $ | 2,465 | $ | 2,369 | (59 | )% | 4 | % | ||||

| EMEA | 2,008 | 1,805 | 3,414 | 11 | (47 | ) | ||||||||

| Latin America | 978 | 1,091 | 1,558 | (10 | ) | (30 | ) | |||||||

| Asia | 898 | 1,138 | 1,854 | (21 | ) | (39 | ) | |||||||

| Total | $ | 4,895 | $ | 6,499 | $ | 9,195 | (25 | )% | (29 | )% | ||||

| Transaction Services | ||||||||||||||

| North America | $ | 447 | $ | 529 | $ | 609 | (16 | )% | (13 | )% | ||||

| EMEA | 1,142 | 1,225 | 1,299 | (7 | ) | (6 | ) | |||||||

| Latin America | 645 | 664 | 616 | (3 | ) | 8 | ||||||||

| Asia | 1,173 | 1,255 | 1,254 | (7 | ) | - | ||||||||

| Total | $ | 3,407 | $ | 3,673 | $ | 3,778 | (7 | )% | (3 | )% | ||||

| Institutional Clients Group | $ | 8,302 | $ | 10,172 | $ | 12,973 | (18 | )% | (22 | )% | ||||

| Total Citicorp | $ | 14,498 | $ | 14,833 | $ | 15,362 | (2 | )% | (3 | )% | ||||

| CITI HOLDINGS | ||||||||||||||

| Brokerage and Asset Management | $ | (286 | ) | $ | (226 | ) | $ | 6,850 | (27 | )% | NM | |||

| Local Consumer Lending | (2,834 | ) | (4,988 | ) | (10,484 | ) | 43 | 52 | % | |||||

| Special Asset Pool | 596 | 1,158 | (5,425 | ) | (49 | ) | NM | |||||||

| Total Citi Holdings | $ | (2,524 | ) | $ | (4,056 | ) | $ | (9,059 | ) | 38 | % | 55 | % | |

| Corporate/Other | $ | (871 | ) | $ | 174 | $ | (7,369 | ) | NM | NM | ||||

| Income (loss) from continuing operations | $ | 11,103 | $ | 10,951 | $ | (1,066 | ) | 1 | % | NM | ||||

| Discontinued operations | $ | 112 | $ | (68 | ) | $ | (445 | ) | ||||||

| Net income attributable to noncontrolling interests | 148 | 281 | 95 | (47 | )% | NM | ||||||||

| Citigroup's net income (loss) | $ | 11,067 | $ | 10,602 | $ | (1,606 | ) | 4 | % | NM | ||||

NM Not meaningful

12

CITIGROUP REVENUES

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| CITICORP | ||||||||||||||

| Global Consumer Banking | ||||||||||||||

| North America | $ | 13,614 | $ | 14,790 | $ | 8,575 | (8 | )% | 72 | % | ||||

| EMEA | 1,479 | 1,503 | 1,550 | (2 | ) | (3 | ) | |||||||

| Latin America | 9,483 | 8,685 | 7,883 | 9 | 10 | |||||||||

| Asia | 8,009 | 7,396 | 6,746 | 8 | 10 | |||||||||

| Total | $ | 32,585 | $ | 32,374 | $ | 24,754 | 1 | % | 31 | % | ||||

| Securities and Banking | ||||||||||||||

| North America | $ | 7,558 | $ | 9,393 | $ | 8,836 | (20 | )% | 6 | % | ||||

| EMEA | 7,221 | 6,849 | 10,056 | 5 | (32 | ) | ||||||||

| Latin America | 2,364 | 2,547 | 3,435 | (7 | ) | (26 | ) | |||||||

| Asia | 4,274 | 4,326 | 4,813 | (1 | ) | (10 | ) | |||||||

| Total | $ | 21,417 | $ | 23,115 | $ | 27,140 | (7 | )% | (15 | )% | ||||

| Transaction Services | ||||||||||||||

| North America | $ | 2,442 | $ | 2,485 | $ | 2,525 | (2 | )% | (2 | )% | ||||

| EMEA | 3,486 | 3,356 | 3,389 | 4 | (1 | ) | ||||||||

| Latin America | 1,705 | 1,516 | 1,391 | 12 | 9 | |||||||||

| Asia | 2,936 | 2,714 | 2,513 | 8 | 8 | |||||||||

| Total | $ | 10,569 | $ | 10,071 | $ | 9,818 | 5 | % | 3 | % | ||||

| Institutional Clients Group | $ | 31,986 | $ | 33,186 | $ | 36,958 | (4 | )% | (10 | )% | ||||

| Total Citicorp | $ | 64,571 | $ | 65,560 | $ | 61,712 | (2 | )% | 6 | % | ||||

| CITI HOLDINGS | ||||||||||||||

| Brokerage and Asset Management | $ | 282 | $ | 609 | $ | 14,623 | (54 | )% | (96 | )% | ||||

| Local Consumer Lending | 12,067 | 15,826 | 17,765 | (24 | ) | (11 | ) | |||||||

| Special Asset Pool | 547 | 2,852 | (3,260 | ) | (81 | ) | NM | |||||||

| Total Citi Holdings | $ | 12,896 | $ | 19,287 | $ | 29,128 | (33 | )% | (34 | )% | ||||

| Corporate/Other | $ | 886 | $ | 1,754 | $ | (10,555 | ) | (49 | )% | NM | ||||

| Total net revenues | $ | 78,353 | $ | 86,601 | $ | 80,285 | (10 | )% | 8 | % | ||||

NM Not meaningful

13

CITICORP

Citicorp is Citigroup's global bank for consumers and businesses

and represents Citi's core franchises. Citicorp is focused on providing best-in-class products and services to customers

and leveraging Citigroup's unparalleled global network. Citicorp is physically present in approximately 100 countries, many

for over 100 years, and offers services in over 160 countries and jurisdictions. Citi believes this global network provides a

strong foundation for servicing the broad financial services needs of large multinational clients and for meeting the needs of

retail, private banking, commercial, public sector and institutional clients around the world. Citigroup's global footprint

provides coverage of the world's emerging economies, which Citi continues to believe represent a strong area of growth. At

December 31, 2011, Citicorp had approximately $1.3 trillion of assets and $797 billion of deposits, representing approximately

70% of Citi's total assets and approximately 92% of its deposits.

At

December 31, 2011, Citicorp consisted of the following businesses: Global Consumer Banking (which included retail banking

and Citi-branded cards in four regions- North America, EMEA, Latin America and Asia ) and Institutional Clients

Group (which included Securities and Banking and Transaction Services ).

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| Net interest revenue | $ | 38,135 | $ | 38,585 | $ | 34,197 | (1 | )% | 13 | % | ||||

| Non-interest revenue | 26,436 | 26,975 | 27,515 | (2 | ) | (2 | ) | |||||||

| Total revenues, net of interest expense | $ | 64,571 | $ | 65,560 | $ | 61,712 | (2 | )% | 6 | % | ||||

| Provisions for credit losses and for benefits and claims | ||||||||||||||

| Net credit losses | $ | 8,307 | $ | 11,789 | $ | 6,155 | (30 | )% | 92 | % | ||||

| Credit reserve build (release) | (3,544 | ) | (2,167 | ) | 2,715 | (64 | ) | NM | ||||||

| Provision for loan losses | $ | 4,763 | $ | 9,622 | $ | 8,870 | (50 | )% | 8 | % | ||||

| Provision for benefits and claims | 152 | 151 | 164 | 1 | (8 | ) | ||||||||

| Provision for unfunded lending commitments | 92 | (32 | ) | 138 | NM | NM | ||||||||

| Total provisions for credit losses and for benefits and claims | $ | 5,007 | $ | 9,741 | $ | 9,172 | (49 | )% | 6 | % | ||||

| Total operating expenses | $ | 39,620 | $ | 36,144 | $ | 32,698 | 10 | % | 11 | % | ||||

| Income from continuing operations before taxes | $ | 19,944 | $ | 19,675 | $ | 19,842 | 1 | % | (1 | )% | ||||

| Provisions for income taxes | 5,446 | 4,842 | 4,480 | 12 | 8 | % | ||||||||

| Income from continuing operations | $ | 14,498 | $ | 14,833 | $ | 15,362 | (2 | )% | (3 | )% | ||||

| Net income attributable to noncontrolling interests | 56 | 122 | 68 | (54 | ) | 79 | ||||||||

| Citicorp's net income | $ | 14,442 | $ | 14,711 | $ | 15,294 | (2 | )% | (4 | )% | ||||

| Balance sheet data (in billions of dollars) | ||||||||||||||

| Total EOP assets | $ | 1,319 | $ | 1,284 | $ | 1,138 | 3 | % | 13 | % | ||||

| Average assets | $ | 1,358 | $ | 1,257 | $ | 1,088 | 8 | % | 16 | % | ||||

| Total EOP deposits | 797 | 760 | 734 | 5 | 4 | |||||||||

NM Not meaningful

14

GLOBAL CONSUMER

BANKING

Global Consumer

Banking (GCB) consists of

Citigroup's four geographical Regional Consumer Banking (RCB) businesses that provide traditional banking services to retail

customers. As of December 31, 2011, GCB also contained Citigroup's branded cards

and local commercial banking businesses and, effective in the first quarter of

2012, will also include its retail partner cards business. GCB is a globally

diversified business with nearly 4,200 branches in 39 countries around the

world. At December 31, 2011, GCB had $340 billion of assets and $313 billion of

deposits.

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| Net interest revenue | $ | 23,090 | $ | 23,184 | $ | 16,353 | - | 42 | % | |||||

| Non-interest revenue | 9,495 | 9,190 | 8,401 | 3 | % | 9 | ||||||||

| Total revenues, net of interest expense | $ | 32,585 | $ | 32,374 | $ | 24,754 | 1 | % | 31 | % | ||||

| Total operating expenses | $ | 18,933 | $ | 16,547 | $ | 15,125 | 14 | % | 9 | % | ||||

| Net credit losses | $ | 7,688 | $ | 11,216 | $ | 5,395 | (31 | )% | NM | |||||

| Credit reserve build (release) | (2,988 | ) | (1,541 | ) | 1,823 | (94 | ) | NM | ||||||

| Provisions for unfunded lending commitments | 3 | (3 | ) | - | NM | - | ||||||||

| Provision for benefits and claims | 152 | 151 | 164 | 1 | (8 | )% | ||||||||

| Provisions for credit losses and for benefits and claims | $ | 4,855 | $ | 9,823 | $ | 7,382 | (51 | )% | 33 | % | ||||

| Income (loss) from continuing operations before taxes | $ | 8,797 | $ | 6,004 | $ | 2,247 | 47 | % | NM | |||||

| Income taxes (benefits) | 2,601 | 1,343 | (142 | ) | 94 | NM | ||||||||

| Income (loss) from continuing operations | $ | 6,196 | $ | 4,661 | $ | 2,389 | 33 | % | 95 | % | ||||

| Net income (loss) attributable to noncontrolling interests | - | (9 | ) | - | 100 | - | ||||||||

| Net income (loss) | $ | 6,196 | $ | 4,670 | $ | 2,389 | 33 | % | 95 | % | ||||

| Average assets (in billions of dollars) | $ | 335 | $ | 309 | $ | 242 | 8 | % | 28 | % | ||||

| Return on assets | 1.85 | % | 1.51 | % | 0.99 | % | ||||||||

| Total EOP assets | $ | 340 | $ | 328 | $ | 255 | 4 | 29 | ||||||

| Average deposits (in billions of dollars) | 311 | 295 | 275 | 5 | 7 | |||||||||

| Net credit losses as a percentage of average loans | 3.25 | % | 5.11 | % | 3.62 | % | ||||||||

| Revenue by business | ||||||||||||||

| Retail banking | $ | 16,229 | $ | 15,767 | $ | 14,782 | 3 | % | 7 | % | ||||

| Citi-branded cards | 16,356 | 16,607 | 9,972 | (2 | ) | 67 | ||||||||

| Total | $ | 32,585 | $ | 32,374 | $ | 24,754 | 1 | % | 31 | % | ||||

| Income (loss) from continuing operations by business | ||||||||||||||

| Retail banking | $ | 2,529 | $ | 3,082 | $ | 2,387 | (18 | )% | 29 | % | ||||

| Citi-branded cards | 3,667 | 1,579 | 2 | NM | NM | |||||||||

| Total | $ | 6,196 | $ | 4,661 | $ | 2,389 | 33 | % | 95 | % | ||||

NM Not meaningful

15

NORTH AMERICA REGIONAL CONSUMER

BANKING

North America

Regional Consumer Banking (NA RCB) provides traditional banking and Citi-branded card services to retail

customers and small to mid-size businesses in the U.S. Effective in the first

quarter of 2012, NA RCB will also include the substantial majority

of Citi's retail partner cards business, which will add approximately $45

billion of assets, including $41 billion of loans, to NA RCB . NA RCB's 1,016 retail bank branches and 12.7 million

customer accounts, as of December 31, 2011, are largely concentrated in the

greater metropolitan areas of New York, Los Angeles, San Francisco, Chicago,

Miami, Washington, D.C., Boston, Philadelphia and certain larger cities in

Texas. At December 31, 2011, NA

RCB had $38.9 billion of retail

banking loans and $148.8 billion of deposits. In addition, NA RCB had 22.0 million Citi-branded credit card accounts, with $75.9 billion in

outstanding card loan balances.

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| Net interest revenue | $ | 10,367 | $ | 11,216 | $ | 5,206 | (8 | )% | NM | |||||

| Non-interest revenue | 3,247 | 3,574 | 3,369 | (9 | ) | 6 | % | |||||||

| Total revenues, net of interest expense | $ | 13,614 | $ | 14,790 | $ | 8,575 | (8 | )% | 72 | % | ||||

| Total operating expenses | $ | 7,329 | $ | 6,163 | $ | 5,890 | 19 | % | 5 | % | ||||

| Net credit losses | $ | 4,949 | $ | 8,019 | $ | 1,152 | (38 | )% | NM | |||||

| Credit reserve build (release) | (2,740 | ) | (312 | ) | 527 | NM | NM | |||||||

| Provisions for benefits and claims | 22 | 24 | 50 | (8 | ) | (52 | )% | |||||||

| Provisions for loan losses and for benefits and claims | $ | 2,231 | $ | 7,731 | $ | 1,729 | (71 | )% | NM | |||||

| Income from continuing operations before taxes | $ | 4,054 | $ | 896 | 956 | NM | (6 | )% | ||||||

| Income taxes | 1,465 | 246 | 167 | NM | 47 | |||||||||

| Income from continuing operations | $ | 2,589 | $ | 650 | $ | 789 | NM | (18 | )% | |||||

| Net income attributable to noncontrolling interests | - | - | - | - | - | |||||||||

| Net income | $ | 2,589 | $ | 650 | $ | 789 | NM | (18 | )% | |||||

| Average assets (in billions of dollars) | $ | 123 | $ | 119 | $ | 73 | 3 | % | 63 | % | ||||

| Average deposits (in billions of dollars) | 145 | 145 | 141 | - | 3 | |||||||||

| Net credit losses as a percentage of average loans | 4.60 | % | 7.48 | % | 2.43 | % | ||||||||

| Revenue by business | ||||||||||||||

| Retail banking | $ | 5,111 | $ | 5,325 | $ | 5,236 | (4 | )% | 2 | % | ||||

| Citi-branded cards | 8,503 | 9,465 | 3,339 | (10 | ) | NM | ||||||||

| Total | $ | 13,614 | $ | 14,790 | $ | 8,575 | (8 | )% | 72 | % | ||||

| Income (loss) from continuing operations by business | ||||||||||||||

| Retail banking | $ | 488 | $ | 762 | $ | 751 | (36 | )% | 1 | % | ||||

| Citi-branded cards | 2,101 | (112 | ) | 38 | NM | NM | ||||||||

| Total | $ | 2,589 | $ | 650 | $ | 789 | NM | (18 | )% | |||||

| Total GAAP revenues | $ | 13,614 | $ | 14,790 | $ | 8,575 | (8 | )% | 72 | % | ||||

| Net impact of credit card securitizations activity (1) | - | - | 6,672 | |||||||||||

| Total managed revenues | $ | 13,614 | $ | 14,790 | $ | 15,247 | (3 | )% | ||||||

| Total GAAP net credit losses | $ | 4,949 | $ | 8,019 | $ | 1,152 | (38 | )% | NM | |||||

| Impact of credit card securitizations activity (1) | - | - | 6,931 | |||||||||||

| Total managed net credit losses | $ | 4,949 | $ | 8,019 | $ | 8,083 | (1 | )% | ||||||

| (1) | See Note 1 to the Consolidated Financial Statements for a discussion of the impact of SFAS 166/167. | |

| NM | Not meaningful |

2011 vs. 2010

Net income increased $1.9 billion as compared to the prior year, driven by higher

loan loss reserve releases and an improvement in net credit losses, partly

offset by lower revenues and higher expenses. Citi does not expect the same

level of loan loss reserve releases in NA RCB in 2012 as it

believes credit costs in the business have generally

stabilized.

Revenues decreased 8% mainly due to lower net interest margin and loan balances in the Citi-branded cards business as well as lower mortgage-related revenues, primarily relating to lower refinancing activity and lower margins as compared to the prior year.

16

Net interest revenue decreased 8%, driven primarily by lower cards net interest margin which

was negatively impacted by the look-back provision of The Credit Card

Accountability Responsibility and Disclosure Act (CARD Act). As previously

disclosed, the look-back provision of the CARD Act generally requires a review

to be done once every six months for card accounts where the annual percentage

rate (APR) has been increased since January 1, 2009 to assess whether changes in

credit risk, market conditions or other factors merit a future decline in the

APR. In addition, net interest margin for cards was negatively impacted by

higher promotional balances and lower total average loans. As a result, cards

net interest revenue as a percentage of average loans decreased to 9.48% from

10.28% in the prior year. Citi expects margin growth to remain under pressure

into 2012 given the continued investment spending in the business during 2012,

which largely began in the second half of 2011.

Non-interest revenue decreased 9%, primarily due to

lower gains from the sale of mortgage loans as Citi held more loans on-balance

sheet. In addition, the decline in non-interest revenue reflected lower banking

fee income.

Expenses increased 19%, primarily driven

by the higher investment spending in the business during the second half of

2011, particularly in cards marketing and technology, and increases in

litigation accruals related to the interchange litigation (see Note 29 to the

Consolidated Financial Statements).

Provisions decreased

$5.5 billion, or 71%, primarily due to a loan loss reserve release of $2.7

billion in 2011, compared to a loan loss reserve release of $0.3 billion in

2010, and lower net credit losses in the Citi-branded cards portfolio. Cards net

credit losses were down $3.0 billion, or 39%, from 2010, and the net credit loss

ratio decreased 366 basis points to 6.36% for 2011. The decline in credit costs

was driven by improving credit conditions as well as continued stricter

underwriting criteria, which lowered the cards risk profile. As referenced

above, Citi believes the improvements in, and Citi's resulting benefit from,

declining credit costs in NA RCB will likely slow into 2012.

2010 vs. 2009

Net income declined by $139 million, or 18%, as compared to

the prior year, driven by higher credit costs due to Citi's adoption of SFAS

166/167, partially offset by higher revenues.

Revenues increased

72% from the prior year, primarily due to the consolidation of securitized

credit card receivables pursuant to the adoption of SFAS 166/167 effective

January 1, 2010. On a comparable basis, revenues declined 3% from the prior

year, mainly due to lower volumes in Citi-branded cards as well as the net

impact of the CARD Act on cards revenues. This decrease was partially offset by

better mortgage-related revenues driven by higher refinancing

activity.

Net interest

revenue was down 6% on a

comparable basis driven primarily by lower volumes in cards, with average

managed loans down 7% from the prior year, and in retail banking, where average

loans declined 11%. The decline in cards was driven by the stricter underwriting

criteria referenced above as well as the impact of CARD Act. The increase in

deposit volumes, up 3% from the prior year, was offset by lower spreads due to

the then-current interest rate environment.

Non-interest revenue increased 6% on a comparable basis from the prior year mainly driven by

better servicing hedge results and higher gains on sale from the sale of

mortgage loans.

Expenses increased 5% from the prior year, driven by the

impact of higher litigation accruals, primarily in the first quarter of 2010,

and higher marketing costs.

Provisions increased $6.0 billion,

primarily due to the consolidation of securitized credit card receivables

pursuant to the adoption of SFAS 166/167. On a comparable basis, provisions

decreased $0.9 billion, or 11%, primarily due to a net loan loss reserve release

of $0.3 billion in 2010 compared to a $0.5 billion loan loss reserve build in

the prior year coupled with lower net credit losses in the cards portfolio. Also

on a comparable basis, the cards net credit loss ratio increased 61 basis points

to 10.02%, driven by lower average loans.

17

EMEA REGIONAL CONSUMER

BANKING

EMEA Regional

Consumer Banking (EMEA RCB) provides traditional banking and Citi-branded card services to retail

customers and small to mid-size businesses, primarily in Central and Eastern

Europe, the Middle East and Africa (remaining retail banking and cards

activities in Western Europe are included in Citi Holdings). The countries in

which EMEA RCB has the largest presence are Poland, Turkey,

Russia and the United Arab Emirates. At December 31, 2011, EMEA RCB had 292 retail bank branches with 3.7 million customer accounts, $4.2

billion in retail banking loans and $9.5 billion in deposits. In addition, the

business had 2.6 million Citi-branded card accounts with $2.7 billion in

outstanding card loan balances.

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| Net interest revenue | $ | 893 | $ | 923 | $ | 974 | (3 | )% | (5 | )% | ||||

| Non-interest revenue | 586 | 580 | 576 | 1 | 1 | |||||||||

| Total revenues, net of interest expense | $ | 1,479 | $ | 1,503 | $ | 1,550 | (2 | )% | (3 | )% | ||||

| Total operating expenses | $ | 1,287 | $ | 1,179 | $ | 1,120 | 9 | % | 5 | % | ||||

| Net credit losses | $ | 172 | $ | 316 | $ | 472 | (46 | )% | (33 | )% | ||||

| Provision for unfunded lending commitments | 3 | (4 | ) | - | NM | - | ||||||||

| Credit reserve build (release) | (118 | ) | (118 | ) | 310 | - | NM | |||||||

| Provisions for loan losses | $ | 57 | $ | 194 | $ | 782 | (71 | )% | (75 | )% | ||||

| Income (loss) from continuing operations before taxes | $ | 135 | $ | 130 | $ | (352 | ) | 4 | % | NM | ||||

| Income taxes (benefits) | 56 | 39 | (132 | ) | 44 | NM | ||||||||

| Income (loss) from continuing operations | $ | 79 | $ | 91 | $ | (220 | ) | (13 | )% | NM | ||||

| Net income (loss) attributable to noncontrolling interests | - | (1 | ) | - | 100 | - | ||||||||

| Net income (loss) | $ | 79 | $ | 92 | $ | (220 | ) | (14 | )% | NM | ||||

| Average assets (in billions of dollars) | $ | 10 | $ | 10 | $ | 11 | - | (9 | )% | |||||

| Return on assets | 0.79 | % | 0.92 | % | (2.01 | )% | ||||||||

| Average deposits (in billions of dollars) | $ | 10 | $ | 9 | $ | 9 | 11 | - | ||||||

| Net credit losses as a percentage of average loans | 2.38 | % | 4.45 | % | 5.64 | % | ||||||||

| Revenue by business | ||||||||||||||

| Retail banking | $ | 811 | $ | 822 | $ | 884 | (1 | )% | (7 | )% | ||||

| Citi-branded cards | 668 | 681 | 666 | (2 | ) | 2 | ||||||||

| Total | $ | 1,479 | $ | 1,503 | $ | 1,550 | (2 | )% | (3 | )% | ||||

| Income (loss) from continuing operations by business | ||||||||||||||

| Retail banking | $ | (56 | ) | $ | (54 | ) | $ | (188 | ) | (4 | )% | 71 | % | |

| Citi-branded cards | 135 | 145 | (32 | ) | (7 | ) | NM | |||||||

| Total | $ | 79 | $ | 91 | $ | (220 | ) | (13 | )% | NM | ||||

NM Not meaningful

2011 vs. 2010

Net income declined 14% as compared to the prior year as an improvement in net

credit losses was partially offset by lower revenues and higher expenses from

increased investment spending. During 2011, the U.S. dollar generally

depreciated versus local currencies. As a result, the impact of FX translation

accounted for an approximately 1% growth in revenues and expenses,

respectively.

Revenues declined 2%

driven by the continued liquidation of higher yielding non-strategic customer

portfolios and a lower contribution from Akbank, Citi's equity investment in

Turkey. The revenue decline was partly offset by the impact of FX translation

and improved underlying trends in the core lending portfolio, discussed

below.

Net interest revenue declined 3% due to the continued

decline in the higher yielding non-strategic retail banking portfolio and spread

compression in the Citi-branded cards portfolio. Interest rate caps on credit

cards, particularly in Turkey and Poland, contributed to the lower spreads in

the cards portfolio.

Non-interest revenue increased 1%, reflecting higher investment sales and cards fees, partly offset

by the lower contribution from Akbank. Underlying drivers continued to show

growth as investment sales grew 28% from the prior year and cards purchase sales

grew 14%.

Expenses increased 9%, due to the impact of FX

translation, investment spending and higher transactional expenses, partly

offset by continued savings initiatives. Expenses could remain at elevated

levels in 2012 given continued investment spending.

Provisions were 71% lower than the prior year driven by a reduction in net credit

losses. Net credit losses decreased 46%, reflecting the continued credit quality

improvement during the year, stricter underwriting criteria and the move to

lower risk products. Loan loss reserve releases were flat. Assuming the

underlying core portfolio continues to grow and season in 2012, Citi expects

credit costs to rise.

18

2010 vs. 2009

Net income improved by $313 million, driven by the reduction in credit costs,

partly offset by lower revenues and higher expenses. During 2010, the U.S.

dollar generally appreciated versus local currencies. As a result, the impact of

FX translation accounted for an approximately 1% decline in revenues and

expenses, respectively.

Revenues declined 3% driven by FX translation and the continued liquidation of

non-strategic customer portfolios. Net interest revenue was

5% lower due to the continued decline in the higher yielding non-strategic

retail banking portfolio. In 2010, Citi focused its lending strategy around

higher credit quality customers who tend to revolve less, meaning they have

lower average balances than customers previously had. While this led to lower credit

costs, it also negatively impacted Net interest revenue as customers

paid off their loans more quickly. Non-interest revenue increased 1%, reflecting higher investment sales and a higher

contribution from Citi's equity investment in Akbank.

Expenses increased 5%, due to account acquisition-focused investment spending and

volumes. As the average customer credit quality improved, Citi focused on volume

growth to compensate for the lower revenue. The expansion of the sales force in

2010 drove some of the expense increase as compared to 2009.

Provisions decreased 75% from the prior year driven by reduction in net credit

losses and higher loan loss reserve releases. Net credit losses decreased 33%,

reflecting continued credit quality improvement and the move to lower risk

products.

19

LATIN AMERICA REGIONAL CONSUMER

BANKING

Latin America

Regional Consumer Banking (LATAM RCB) provides traditional banking and branded card services to retail

customers and small to mid-size businesses, with the largest presence in Mexico

and Brazil. LATAM

RCB includes branch networks

throughout Latin

America as well as Banco Nacional

de Mexico, or Banamex, Mexico's second-largest bank, with over 1,700 branches.

At December 31, 2011, LATAM

RCB overall had 2,221 retail

branches, with 29.2 million customer accounts, $24.0 billion in retail banking

loans and $44.8 billion in deposits. In addition, the business had 12.9 million

Citi-branded card accounts with $13.7 billion in outstanding loan

balances.

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| Net interest revenue | $ | 6,465 | $ | 5,968 | $ | 5,365 | 8 | % | 11 | % | ||||

| Non-interest revenue | 3,018 | 2,717 | 2,518 | 11 | 8 | |||||||||

| Total revenues, net of interest expense | $ | 9,483 | $ | 8,685 | $ | 7,883 | 9 | % | 10 | % | ||||

| Total operating expenses | $ | 5,734 | $ | 5,159 | $ | 4,550 | 11 | % | 13 | % | ||||

| Net credit losses | $ | 1,684 | $ | 1,868 | $ | 2,432 | (10 | )% | (23 | )% | ||||

| Credit reserve build (release) | (67 | ) | (823 | ) | 463 | 92 | NM | |||||||

| Provision for benefits and claims | 130 | 127 | 114 | 2 | 11 | |||||||||

| Provisions for loan losses and for benefits and claims | $ | 1,747 | $ | 1,172 | $ | 3,009 | 49 | % | (61 | )% | ||||

| Income (loss) from continuing operations before taxes | $ | 2,002 | $ | 2,354 | $ | 324 | (15 | )% | NM | |||||

| Income taxes (benefits) | 401 | 565 | (105 | ) | (29 | ) | NM | |||||||

| Income (loss) from continuing operations | $ | 1,601 | $ | 1,789 | $ | 429 | (11 | )% | NM | |||||

| Net (loss) attributable to noncontrolling interests | - | (8 | ) | - | 100 | - | ||||||||

| Net income (loss) | $ | 1,601 | $ | 1,797 | $ | 429 | (11 | )% | NM | |||||

| Average assets (in billions of dollars) | $ | 80 | $ | 73 | $ | 66 | 10 | % | 11 | % | ||||

| Return on assets | 2.00 | % | 2.45 | % | 0.65 | % | ||||||||

| Average deposits (in billions of dollars) | $ | 46 | $ | 41 | $ | 36 | 12 | % | 14 | % | ||||

| Net credit losses as a percentage of average loans | 4.64 | % | 6.05 | % | 8.52 | % | ||||||||

| Revenue by business | ||||||||||||||

| Retail banking | $ | 5,482 | $ | 5,034 | $ | 4,401 | 9 | % | 14 | % | ||||

| Citi-branded cards | 4,001 | 3,651 | 3,482 | 10 | 5 | |||||||||

| Total | $ | 9,483 | $ | 8,685 | $ | 7,883 | 9 | % | 10 | % | ||||

| Income (loss) from continuing operations by business | ||||||||||||||

| Retail banking | $ | 923 | $ | 938 | $ | 657 | (2 | )% | 43 | % | ||||

| Citi-branded cards | 678 | 851 | (228 | ) | (20 | ) | NM | |||||||

| Total | $ | 1,601 | $ | 1,789 | $ | 429 | (11 | )% | NM | |||||

NM Not meaningful

2011 vs. 2010

Net income declined 11% as lower loan loss reserve releases more than offset

increased operating margin. During 2011, the U.S. dollar generally depreciated

versus local currencies. As a result, FX translation contributed approximately

2% to the growth in each of revenues and

expenses.

Revenues increased 9%

primarily due to higher volumes as well as the impact of FX translation. Net interest revenue increased 8% driven by the

continued growth in lending and deposit volumes, partially offset by continued

spread compression. The declining rate environment negatively impacted Net interest

revenue as interest revenue

declined at a faster pace than interest expense. Spread compression was also

driven by the continued move towards customers with a lower risk profile and

stricter underwriting criteria, especially in the branded cards portfolio. Non-interest

revenue increased 11%,

predominantly driven by an increase in banking fee income from credit card

purchase sales, which grew 22%.

Expenses increased 11% due

to higher volumes and investment spending, including increased marketing and

customer acquisition costs as well as new branches. These increased expenses

were partially offset by continued savings initiatives. The increase in the

level of investment spending in the business was largely completed at the end of

2011.

Provisions increased 49% reflecting lower loan loss reserve

releases in 2011 as compared to 2010. Towards the end of 2011, there was a build

in the loan loss reserves, primarily driven by increased volumes, particularly

in the personal loan portfolio in Mexico. Net credit losses declined 10%, driven

primarily by improvements in the Mexico cards portfolio. The cards net credit

loss ratio declined from 11.7% in 2010 to 8.8% in 2011, driven in part by the

continued move towards customers with a lower risk profile and stricter

underwriting criteria. Citi currently expects the Citi-branded cards net credit

loss ratio to stabilize in 2012 as new loans continue to season. Credit costs

will likely increase in line with portfolio growth.

20

2010 vs. 2009

Net income increased $1.4 billion driven by lower credit costs as Citi released

reserves in 2010 as compared to reserve builds in 2009. During 2010, the U.S.

dollar generally appreciated versus local currencies. As a result, FX

translation contributed approximately 5% to the decline in both revenues and

expenses.

Revenues increased 10%. Net interest

revenue increased 11% as higher

loan volumes, particularly in the retail bank, offset the effect of spread

compression. Spread compression was driven by the lower interest rates and move

towards the above referenced lower risk customer base. Non-interest revenue increased 8% due to higher banking fee income from

increased purchase sale activity and FX translation.

Expenses increased 13% due to FX translation as well as higher volumes and

transaction-related expenses as economic conditions improved. The increase in

expenses was also due to increased investment spending, including new cards

acquisitions and new branches.

Provisions decreased 61% primarily reflecting loan loss reserve releases of $823

million compared to a build of $463 million in the prior year as well as a $564

million improvement in net credit losses. The increase in loan loss reserve

releases and decrease in net credit losses primarily resulted from improved

credit conditions and portfolio quality in the Citi-branded cards portfolio,

primarily in Mexico, as well as the move to customers with a lower risk profile

and stricter underwriting criteria referenced above.

21

ASIA REGIONAL CONSUMER

BANKING

Asia Regional

Consumer Banking (Asia RCB) provides traditional banking and Citi-branded card services to retail

customers and small- to mid-size businesses, with the largest Citi presence in

South Korea, Japan, Taiwan, Singapore, Australia, Hong Kong, India and

Indonesia. Citi's Japan Consumer Finance business, which Citi has been exiting

since 2008, is included in Citi Holdings (see "Citi Holdings- Local Consumer Lending " below). At December 31, 2011, Asia RCB had 671 retail branches, 16.3 million customer accounts, $66.2 billion in

retail banking loans and $109.7 billion in deposits. In addition, the business

had 15.9 million Citi-branded card accounts with $21.0 billion in outstanding

loan balances.

| % Change | % Change | |||||||||||||

| In millions of dollars | 2011 | 2010 | 2009 | 2011 vs. 2010 | 2010 vs. 2009 | |||||||||

| Net interest revenue | $ | 5,365 | $ | 5,077 | $ | 4,808 | 6 | % | 6 | % | ||||

| Non-interest revenue | 2,644 | 2,319 | 1,938 | 14 | 20 | |||||||||

| Total revenues, net of interest expense | $ | 8,009 | $ | 7,396 | $ | 6,746 | 8 | % | 10 | % | ||||

| Total operating expenses | $ | 4,583 | $ | 4,046 | $ | 3,565 | 13 | % | 13 | % | ||||

| Net credit losses | $ | 883 | $ | 1,013 | $ | 1,339 | (13 | )% | (24 | )% | ||||

| Credit reserve build (release) | (63 | ) | (287 | ) | 523 | 78 | NM | |||||||

| Provisions for loan losses and for benefits and claims | $ | 820 | $ | 726 | $ | 1,862 | 13 | % | (61 | )% | ||||

| Income from continuing operations before taxes | $ | 2,606 | $ | 2,624 | $ | 1,319 | (1 | )% | 99 | % | ||||

| Income taxes (benefits) | 679 | 493 | (72 | ) | 38 | NM | ||||||||

| Income from continuing operations | $ | 1,927 | $ | 2,131 | $ | 1,391 | (10 | )% | 53 | % | ||||

| Net income attributable to noncontrolling interests | - | - | - | - | - | |||||||||

| Net income | $ | 1,927 | $ | 2,131 | $ | 1,391 | (10 | )% | 53 | % | ||||

| Average assets (in billions of dollars) | $ | 122 | $ | 108 | $ | 93 | 13 | % | 16 | % | ||||

| Return on assets | 1.58 | % | 1.97 | % | 1.50 | % | ||||||||

| Average deposits (in billions of dollars) | $ | 110 | $ | 100 | $ | 89 | 10 | % | 12 | % | ||||