|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K |

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended November 1, 2015 |

|

|

o | TRANSITION REPORT PURSUANT TO SECTION 13 OF 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to . |

Commission File Number: 001-09232 |

VOLT INFORMATION SCIENCES, INC.

(Exact name of registrant as specified in its charter)

New York |

| 13-5658129 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

1133 Avenue of the Americas, New York, New York |

| 10036 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code:

(212) 704-2400

Securities Registered Pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common Stock $0.10 Par Value |

| NYSE MKT LLC |

Securities Registered Pursuant to Section 12(g) of the Act:

(Title of class)

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o |

| Accelerated filer x |

| Non-accelerated filer o |

| Smaller reporting company o |

|

|

|

| |||

|

|

|

| (Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes No x

As of May 1, 2015, there were 20,705,496 shares of common stock outstanding. The aggregate market value of the voting and non-voting common stock held by non-affiliates as of May 1, 2015 was $116,376,120, calculated by using the closing price of the common stock on such date on the NYSE MKT market of $11.86.

As of January 4, 2016 there were 20,830,457 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's Definitive Proxy Statement to be filed for its 2016 Annual Meeting of Shareholders are incorporated by reference into Part III of this report.

|

VOLT INFORMATION SCIENCES, INC.

ANNUAL REPORT ON FORM 10-K FOR THE YEAR ENDED NOVEMBER 1, 2015

TABLE OF CONTENTS

|

| Page |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | 3 | |

|

|

|

PART I |

|

|

|

|

|

ITEM 1. | Business | 4 |

ITEM 1A. | Risk Factors | 10 |

ITEM 1B. | Unresolved Staff Comments | 17 |

ITEM 2. | Properties | 18 |

ITEM 3. | Legal Proceedings | 18 |

ITEM 4. | Mine Safety Disclosures | 18 |

|

|

|

PART II |

|

|

|

|

|

ITEM 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 19 |

ITEM 6. | Selected Financial Data | 21 |

ITEM 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 22 |

ITEM 7A. | Quantitative and Qualitative Disclosures About Market Risk | 35 |

ITEM 8. | Financial Statements and Supplementary Data | 36 |

ITEM 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 36 |

ITEM 9A. | Controls and Procedures | 37 |

ITEM 9B. | Other Information | 39 |

|

|

|

PART III |

|

|

|

|

|

ITEM 10. | Directors, Executive Officers and Corporate Governance | 39 |

ITEM 11. | Executive Compensation | 39 |

ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 39 |

ITEM 13. | Certain Relationships and Related Transactions and Director Independence | 39 |

ITEM 14. | Principal Accounting Fees and Services | 39 |

|

|

|

PART IV |

|

|

|

|

|

ITEM 15. | Exhibits, Financial Statement Schedules | 40 |

|

|

|

Signatures |

| 41 |

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this report are "forward-looking" statements within the meaning of that term in Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). Forward-looking statements include statements that reflect the current views of our senior management with respect to our financial performance and future events of our business and industry in general. The terms "expect," "intend," "plan," "believe," "project," "forecast," "estimate," "may," "should," "anticipate" and similar statements of a future or forward-looking nature identify forward-looking statements. Forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements. We believe that these factors include, but are not limited to, the following:

• | competition within the staffing industry which has few barriers to entry; |

• | weak economic and uncertain business conditions; |

• | foreign currency fluctuations and other global business risks; |

• | impairment charges relating to our goodwill and long-lived assets; |

• | failure to comply with restrictive financial covenants; |

• | inability to renew our Financing Program or obtain a suitable replacement financing arrangement; |

• | fluctuations in interest rates and turmoil in the financial markets; |

• | challenges meeting contractual obligations due to delays, unanticipated costs and cancellations; |

• | contracts either provide no minimum purchase requirements, or are cancellable during the term or both; |

• | the loss of major customers; |

• | inability to attract and retain technologically qualified personnel; |

• | inability to implement new business initiatives; |

• | failure to keep pace with rapid changes in technology; |

• | failure to implement strategic information technology projects; |

• | inability to attract and maintain quality personnel; |

• | employment-related claims, client-indemnification claims and other claims from clients and third parties; |

• | inability to retain acceptable insurance coverage limits at a commercially reasonable cost and terms; |

• | unexpected changes in workers' compensation and other insurance plans; |

• | litigation costs; |

• | improper disclosure of sensitive or confidential employee or customer data; |

• | information technology systems are vulnerable to damage and interruption; |

• | inability to maintain effective internal controls over financial reporting; |

• | new and increased government regulation, employment costs and taxes; |

• | health care reform; |

• | volatility of stock price and related ability of investors to resell their shares at or above the purchase price; |

• | significant percentage of common stock owned by principal shareholders and their ability to exercise significant influence over the Company; |

• | potential proxy contest for the election of directors at our annual meeting; and |

• | New York State law and our Articles of Incorporation and By-laws contain provisions that could make the takeover of the Company more difficult. |

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this report, including under the caption "Risk Factors" in Item 1A of this report. There can be no assurance that we have correctly identified and appropriately assessed all factors affecting our business. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial also may adversely impact us. If one or more events related to these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. Readers should not place undue reliance on any forward-looking statements contained in this report, which speak only as of the date of this report. We undertake no obligation to update any forward-looking statements after the date of this report to conform such statements to actual results or to changes in our expectations.

3

PART I

ITEM 1. | BUSINESS |

Volt Information Sciences, Inc. (the "Company" or "Volt") is a global provider of staffing services (traditional time and materials-based as well as project-based), managed service programs, technology outsourcing services and information technology infrastructure services. Our staffing services consist of workforce solutions that include providing contingent workers, personnel recruitment services, and managed service programs supporting primarily professional administration, technical, information technology, light-industrial and engineering positions. Our managed service programs consist of managing the procurement and on-boarding of contingent workers from multiple providers. Our technology outsourcing services provide pre and post production development, testing, and customer support to companies in the mobile, gaming, and technology devices industries. In addition, we provide information technology infrastructure services which provide server, storage, network and desktop IT hardware maintenance, data center and network monitoring and operations. Our complementary businesses offer customized talent, technology and consulting solutions to a diverse client base. Volt services global industries including aerospace, automotive, banking and finance, consumer electronics, information technology, insurance, life sciences, manufacturing, media and entertainment, pharmaceutical, software, telecommunications, transportation, and utilities. The Company was incorporated in New York in 1957. Unless the context otherwise requires, throughout this report, the words "Volt," "the Company," "we," "us" and "our" refer to Volt Information Sciences, Inc. and its consolidated subsidiaries.

Geographic Regions and Segments:

Volt operates approximately 110 locations worldwide, with approximately 85% of our revenues generated in the United States where we have employees in all 50 states. Our principal non-U.S. markets include Canada, Europe and several Asia Pacific locations. Our global footprint enables us to deliver consistent quality to our enterprise customers that require an established international presence. For financial information concerning our domestic and international operations and segment reporting, see our Segment Disclosures Note in our Consolidated Financial Statements included in this report.

We report our activities in two reportable segments: Staffing Services and Other. Our operating segments have been determined in accordance with our internal management structure, which is based on operating activities. We evaluate business performance based upon several factors, using profitable revenue growth and segment operating income as the primary financial measures. We believe operating income provides management and investors a measure to analyze operating performance of each business segment against historical and competitors' data, although historical results, including operating income, may not be indicative of future results as operating income is highly contingent on many factors including the state of the economy, competitive conditions and customer preferences. We plan to assess potential changes to our reportable segments in fiscal 2016 based on our new management organization and the changes anticipated by implementing our new business strategies, including the initiatives to exit non-strategic and non-core operations.

We allocate all support related costs to the operating segments except for costs not directly relating to our operating activities such as corporate-wide general and administrative costs and fees related to restatement, investigations and remediation that were completed during 2014. These costs are not allocated because doing so would not enhance the understanding of segment operating performance and they are not used by management to measure segment performance.

Staffing Services

The Staffing Services segment provides workforce management expertise including technology outsourcing services and solutions. Our staffing services are provided through locations in North America, Europe and several Asia Pacific locations. We deliver a broad spectrum of contingent staffing, direct placement, staffing contracting and management, and other employment services. Our contingent workers are placed on assignment with our customers in a broad range of occupations including accounting, finance, administrative, engineering, information technology, manufacturing, assembly, warehousing and industrial. Our contingent staffing services are provided for varying periods of time to companies and other organizations (including government agencies) ranging from smaller retail accounts that may require ten or fewer contingent workers at a time to enterprise accounts that require as many as several thousand contingent workers at a time. Our enterprise accounts typically enter into longer term procurement agreements with us resulting in lower direct margins compared to our retail accounts.

Within our Staffing Services segment we refer to customers that require multi-location, coordinated account management and service delivery in multiple skill sets as enterprise customers, while our retail customers are primarily in a single location with sales and delivery handled primarily from a geographically local team and with relatively few headcount on assignment in one or two skill sets. We provide traditional staffing services for which we are paid on a time and materials basis and provide contingent staff that work under the supervision of our customers. We also provide project-based staffing services, for which we are sometimes paid on a basis other than time and materials.

4

Volt's contingent staffing services enable customers to easily scale their workforce to meet changing business conditions, complete a specific project, secure the services of a specialist on an as-needed basis, substitute for regular employees during vacation or other temporary absences, staff high turnover positions, or meet seasonal peaks in workforce needs. When requested, we also provide Volt personnel at the customer's location to coordinate and manage contingent workers. Many customers rely on Volt's staffing services as a strategic element of their overall workforce, allowing them to more efficiently meet their fluctuating staffing requirements.

Contingent staff is recruited through proprietary internet recruiting sites, independent web-based job search companies, and social networking talent communities through which we build and maintain proprietary databases of candidates from which we can fill current and future customer needs. Contingent workers become Volt employees during the period of their assignment and we are responsible for the payment of wages, payroll taxes, workers' compensation insurance, unemployment insurance and other benefits. Customers will sometimes hire Volt's contingent workers as their own employees after a period of time, for which we usually receive a fee.

We also provide recruitment and direct placement services of specialists in the information technology, engineering, technical, accounting, finance and administrative support disciplines. These services are primarily provided on a contingency basis with fees earned only if our customers ultimately hire the candidates.

Our staffing services include providing master vendor services under which we administer a customer's entire contingent workforce program. Our responsibilities for these programs usually include subcontracting procurement of contingent workers from other qualified staffing providers if we are unable to fill a position. In most cases, we are only required to pay subcontractors after we receive payment from our customer.

Our managed service programs ("MSPs") consist of managing the procurement and on-boarding of contingent workers and a broad range of specialized solutions that includes managing suppliers and providing sourcing and recruiting support, supplier performance measurement, consolidated customer billing, supplier payment, supplier optimization and analysis, and benchmarking of spend demographics and rates. The workforce placed on assignment through our MSPs is usually provided by third-party staffing providers ("associate vendors") or through our own staffing services. In most cases, we are only required to pay associate vendors after we receive payment from our customer. We also act as a subcontractor or associate vendor to other national providers in their MSPs.

Our MSPs are administered through the use of vendor management system software ("VMS") licensed from various VMS providers.

Our technology outsourcing services and solutions provide flexible and scalable customer care call centers, video and online gaming industry quality assurance testing services, project-based staffing and customer care solutions including end-user and technical, sales and retention support. Project-based staffing includes project management and provides IT infrastructure outsourcing, data center management, enterprise technology implementation and integration and corporate helpdesk services.

Other Segment

The Other segment consists of our information technology infrastructure services, telecommunication infrastructure and security services businesses, as well as our Uruguayan telephone directory publishing and printing business. We sold our telephone directory publishing and printing business during the third quarter of 2015 and we sold substantially all of the assets of our telecommunication infrastructure and security services business during the fourth quarter of 2015.

Our information technology infrastructure services business provides IT hardware maintenance services on major brands of server, storage, network and desktop products to the Fortune 1000. Other services provided include remote monitoring for corporate data centers and networks, and planning, migration and support services for clients seeking to migrate to a cloud environment. We deliver our services across the United States and in major business centers globally. We sell our services directly to corporate customers and through value-added resellers, partners and resellers. Our target markets include financial services, telecommunications and aerospace. This business has been classified as held for sale.

Our telecommunication infrastructure and security services business was an integrator of enterprise, location and metropolitan security, voice and data systems for Fortune 500 companies, critical infrastructure and telecommunications companies and government entities across the United States. We sold substantially all of the assets of this business during the fourth quarter of 2015.

Our telephone directory publishing and printing business published directories in Uruguay inclusive of telephone directories, directories for publishers in other countries, and commercial books, magazines, periodicals and advertising material. This business was sold during the third quarter of 2015.

5

Business Strategy

Fiscal 2015 was a year where Volt continued to advance our strategic plan with the disposition of several non-core assets which were very diverse with few synergies and very different business models. This challenged our organization to find collaborative opportunities and made it difficult for investors to determine the true value of our consolidated company. During the first quarter of 2015, the Company sold its Computer Systems segment which had generated operating losses in recent years and had significant upfront capital investments with extended payback periods. The results of this segment are presented as discontinued operations and have been excluded from continuing operations and from segment results for all periods presented. During the third quarter of 2015, we sold our telephone directory publishing and printing business in Uruguay as part of our continued strategy to dispose of non-core assets. During fiscal 2014, we exited our telecommunication infrastructure and security services government solutions business as reduced federal spending minimized the opportunity for growth, efficiencies and our ability to operate profitably. During the fourth quarter of 2015, we sold substantially all of the assets of this business. During the first quarter of 2016, we sold our staffing business in Uruguay. Each of these businesses had significantly different risk and return profiles than our core staffing services. These divestitures will enable the Company's management to primarily focus resources on opportunities within our core staffing services where we believe we are better positioned to add value.

Our continued strengths are our strong brand, our capabilities in sourcing a high quality contingent workforce and our longstanding relationships with our customers. Our focus continues to be expanding our revenue in more profitable vertical sectors and expanding our share of customer engagements, as well as ongoing improvements in the delivery of our staffing services. In an effort to reduce our operating costs, we are evaluating the efficiency of our current business delivery model, supply chain and back-office support functions. We expect that these activities will reduce costs of service through the consolidation and/or elimination of certain systems and processes, along with other reductions in discretionary spending. We believe that the results of these actions will ultimately drive higher revenues at improved margins. We remain committed to delivering superior client service at a reasonable cost. We believe that building upon our established brands and reinforcing our strong customer relationships will position Volt to grow both profitability and shareholder value. Key elements of our strategy include:

Provide Superior Customer Satisfaction, Interaction and Communication

In fiscal 2016, we will place increased emphasis on building end-to-end customer relationships by further enhancing our understanding of their needs and striving to anticipate and deliver the highest level of value-added service to our customers. This is a key factor that we believe will drive our top line growth and profitability.

Expand Margins and Reduce Operating Expenses

We are focused on increasing profitability through initiatives to increase revenues and expand margins, reduce operating expenses, provide superior delivery and expand profitable services. We are pursuing these initiatives along with promoting a culture of disciplined execution to further expand our operating income:

• | increase our market share in our key customers and target market sectors; |

• | provide superior delivery that will ultimately drive higher revenues at improved margins; |

• | focus on core business offerings and on market sectors where we are profitable or that have long-term growth potential, and reduce or eliminate non-core, non-strategic business; |

• | increase the percentage of our revenue represented by higher-margin business; |

• | exit or reduce business levels in sectors or with customers where profitability or business terms are unfavorable; |

• | consolidate financial and other administrative and support functions, implement process standardization, and use productivity metrics to drive more cost-effective performance; and |

• | invest in new and efficient systems, sales and marketing infrastructure. |

Volt will continue to evaluate our individual businesses and service offerings as we seek to manage the balance between profitability and top-line growth. These assessments are being conducted in the context of our broader portfolio and our targeted risk and return profile. Businesses or service offerings that do not meet our investment parameters will be discontinued or divested. We believe that these actions will continue to improve our results as well as the consistency of our returns across our portfolio of businesses.

Volt's top priority is the profitable expansion of our revenues and we believe that the actions we are taking will ultimately drive higher revenues. This will include expanding our footprint with existing customers and winning new profitable business. Also, we are taking actions to increase margins and reduce operating expenses as a percentage of margins, thus driving increased operating income.

6

Align Management Incentives with Corporate-Wide Objectives

We are changing management incentive structures corporate-wide to align with short- and long-term strategic objectives, financial goals and efficiency measures. Variable management compensation is being redesigned to tie to the achievement of our business strategy and goals emphasizing performance-based pay.

Retain, Recruit and Develop Talent Globally

We are focused on developing a workforce that has both exceptional technical capabilities and the leadership skills that are required to support future growth of the business, which will be achieved by developing new workforce capabilities and a committed, diverse executive team with the highest level of ethics and integrity.

Capital Allocation

In addition to our planned improvements in technology and overall processes which are anticipated to increase cash flows from operations over time, we have identified a number of capital allocation initiatives, which when executed, are expected to strengthen our balance sheet and increase our competitiveness in the marketplace during fiscal 2016. The timing of these initiatives is highly dependent upon attaining the cash flow and profitability objectives outlined in our plan and the cash flow resulting from the completion of our liquidity initiatives. We also see this as an opportunity to demonstrate our ongoing commitment to Volt shareholders as we continue to execute on our plan and return to sustainable profitability. Our capital allocation strategy includes the following elements:

• | Maintaining appropriate levels of working capital . Our business requires a certain level of cash resources to efficiently execute operations. Consistent with similar companies in our industry and operational capabilities, we estimate this amount to be 1.5 to 2.0 times our weekly cash disbursements on a global basis and must also accommodate seasonality and cyclical trends; |

• | Reinvesting in our business. We are executing a company-wide initiative to reinvest in our business including new information technology systems which will support our front-end recruitment and placement capabilities as well as increase efficiencies in our back-office financial suite. We are also investing in our sales and recruiting process and resources, which will enhance our ability to win in the marketplace; |

• | Deleveraging our balance sheet. By paying down our debt, we will strengthen our balance sheet, reduce interest costs and reduce risk going forward; |

• | Returning value to shareholders. Part of our capital allocation strategy in fiscal 2016 is to return value to our shareholders in connection with share buybacks through our existing share buyback program; and |

• | Acquiring value-added businesses. Identifying and acquiring companies which would be accretive to our operating income and that could leverage our scale, infrastructure and capabilities. Strategic acquisitions would strengthen us in certain industry verticals or in specific geographic locations. |

Customers

The Company serves multinational, national and local customers, providing staffing services (traditional time and materials-based as well as project-based), managed service programs, technology outsourcing services, information technology infrastructure services and telecommunication infrastructure and operations services and telephone directory publishing and printing in Uruguay through the latter part of 2015. The Company had no single customer that accounted for more than 10% of consolidated net revenue in the fiscal years 2015, 2014 and 2013. Our top 10 customers represented approximately 30%, 30% and 34% of our fiscal 2015, 2014 and 2013 revenue, respectively. The loss of one or more of these customers, unless the business is replaced, could have an adverse effect on our results of operations or cash flows.

For the fiscal years ended 2015, 2014 and 2013, 85.1%, 87.1% and 89.3% of our revenue, respectively, were from customers in the United States.

7

Competition

The markets for Volt's staffing services are highly competitive. There are few barriers to entry, so new entrants frequently appear, resulting in considerable market fragmentation. There are over 100 competitors with annual revenues over $300 million, some of whom are larger and have greater resources than we do. These large competitors collectively represent less than half of all staffing services revenues, and there are many smaller companies competing in varying degrees at local levels. Our direct staffing competitors include Adecco, Allegis, CDI Corp., Hudson Global, Inc., Insperity, Inc., Kelly Services, Inc., Manpower Group, Randstad, Recruit, Robert Half, Inc., Tempstaff and TrueBlue, Inc.

In addition, we compete with numerous smaller local companies in the various geographic markets in which we operate. Companies in our industries compete on price, service quality, new capabilities and technologies, marketing methods and speed of completing assignments.

Our IT infrastructure business competes with large system integration firms as well as software and hardware providers that are increasingly offering services to support their products. Many of our competitors are able to offer a wide range of global services and some of our competitors benefit from greater brand recognition than we have.

Intellectual Property

VOLT is the principal registered trademark for our brand in the United States. ARCTERN, A VOLT INFORMATION SCIENCES COMPANY, MAINTECH, PARTNER WITH US, COMPETE WITH ANYBODY, TEAM WITH US. COMPETE WITH ANYBODY, VOLT REACH and VOLTSOURCE are other registered trademarks in the United States. The Company also owns and uses common law trademarks and service marks.

We also own copyrights and patents and license technology from many providers. We rely on a combination of intellectual property rights in the United States and abroad to protect our brand and proprietary information.

Seasonality

Our Staffing Services segment's revenue and operating income are typically lowest in our first fiscal quarter due to the holiday season and are affected by customer facility closures during the holidays (in some cases for up to two weeks), and closures caused by severe winter weather conditions. The demand for our staffing services typically increases during our third and fourth fiscal quarters when customers increase the use of our administrative and industrial labor during the summer vacation period. The first couple of months of the calendar year typically have the lowest margins as employer payroll tax contributions restart each year in January. Margins typically increase in subsequent fiscal quarters as annual payroll tax contribution maximums are met, particularly for higher salaried employees.

Employees

As of November 1, 2015, Volt employed approximately 27,400 people, including approximately 24,700 who were on contingent staffing assignments for the Staffing Services segment. Those people on contingent staffing assignments are on our payroll for the length of their assignment.

We are focused on developing a workforce that has both exceptional technical capabilities and the leadership skills that are required to support our growth. Our strategy is to be a leader in the markets we serve, which will be achieved by developing new workforce capabilities and a committed, diverse world-class management team with the highest level of ethics and integrity.

We believe that our relations with our employees are satisfactory. While claims and legal actions related to staffing matters arise on a routine basis, we believe they are inherent in maintaining a large contingent workforce.

Regulation

Some states in the United States and certain foreign countries license and regulate contingent staffing service firms and employment agencies. Compliance with applicable present federal, state and local environmental laws and regulations has not had, and we believe that compliance with those laws and regulations in the future will not have, a material effect on our competitive position, financial condition, results of operations or cash flows.

Access to Our Information

We electronically file our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all amendments to those reports with the SEC. These and other SEC reports filed by us are available to the public free of charge at the SEC's website at www.sec.gov and in the Investors section at our website at www.volt.com, as soon as reasonably

8

practicable after filing with the SEC. You may read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, D.C. 20549.

Copies of our Code of Business Conduct and Ethics and other significant corporate documents (our Corporate Governance Guidelines, Nominating/Governance Committee Charter, Audit Committee Charter, Compensation Committee Charter, Financial Code of Ethics, Whistleblower Policy, Foreign Corrupt Practices Act Policy and Insider Trading Policy) are also available in the Investors & Governance section at our website. Copies are also available without charge upon request to Volt Information Sciences, Inc., 1133 Avenue of the Americas, New York, NY 10036, Attention: Shareholder Relations, or by calling us at (212) 704-2400.

9

ITEM 1A. | RISK FACTORS |

Risk Factors

You should carefully consider the following risks along with the other information contained in this report. The following risks could materially adversely affect our business and, as a result, our financial condition, results of operations, and the market price of our common stock. Other risks and uncertainties not known to us or that we currently do not recognize as material could also materially adversely affect our business and, as a result, our financial condition, results of operations, cash flows, and the market price of our common stock.

Risks Relating to the Economy and our Industry

The contingent staffing industry is very competitive with few significant barriers to entry

The markets for Volt's staffing services are highly competitive. There are few barriers to entry, so new entrants frequently appear resulting in considerable market fragmentation. There are over 100 competitors with annual revenues over $300 million, some of whom are larger and have greater resources than we do. These competitors may be better able than we are to attract and retain qualified personnel, to offer more favorable pricing and terms, and otherwise attract and retain the business that we seek. In addition, some of the segment's customers, generally larger companies, are mandated or otherwise motivated to utilize the services of small or minority-owned companies rather than publicly held corporations such as Volt, and have redirected substantial amounts of their staffing business to those companies. We also face the risk that certain of our current and prospective customers may decide to provide similar services internally.

There has been a significant increase in the number of customers consolidating their staffing services purchases with a single provider or a small number of providers. This trend to consolidate purchases has, in some cases, made it more difficult for us to obtain or retain customers. Additionally, pricing pressures have intensified as customers have continued to competitively bid contracts. This trend is expected to continue for the foreseeable future. As a result, we cannot assure you that we will not encounter increased competition and lower margins in the future.

In our business segments, we have experienced competition and pressure on price, margins and markups for renewals of customers' contracts. There can be no assurance that we will be able to continue to compete in our business segments without impacting revenue or margins. Additionally, our efforts to manage costs in relation to our business volumes may not be successful, and the timing of these efforts and associated earnings charges may adversely affect our business.

Certain customers continue to contract for staffing services through managed service providers who assume all payment obligations on behalf of the end-customer to service suppliers such as Volt. These managed service providers may present greater credit risks than the end-customer and some of these managed service providers have in the past, and could in the future, default on their obligations to us, adversely impacting our business.

Our business is adversely affected by weak economic and other business conditions

During periods of elevated unemployment levels demand for contingent and permanent personnel decreases, which adversely impacts our Staffing Services segment. During slower economic activity, many of our customers reduce their use of contingent workers before undertaking layoffs of their own employees, resulting in decreased demand for contingent workers. Decreased demand and higher unemployment levels result in lower levels of pay rate increases and increased pressure on our markup of staffing service rates and direct margins and higher unemployment insurance costs. Since employees are also reluctant to risk changing employers, there are fewer openings available and, therefore, reduced activity in permanent placements. In recent years, many of our customers have significantly reduced their workforce, including their use of contingent labor.

Our operational results could be negatively impacted by currency fluctuations and other global business risks

Our global operations outside of the United States subject us to risks relating to our international business activities, including global economic conditions, fluctuations in currency exchange rates and numerous legal and regulatory requirements.

Adverse global economic conditions could have a direct impact on our business, results of operations and financial position. The demand for the Company's services is highly dependent upon the state of the economy and upon the staffing needs of the Company's clients. Any variation in the economic condition or unemployment levels of any of the foreign countries in which the Company does business may severely reduce the demand for the Company's services.

Our business is exposed to fluctuation in exchange rates. Our operations outside the United States are reported in the applicable local currencies and then translated into U.S. dollars at the applicable currency exchange rates for inclusion in our

10

Consolidated Financial Statements. Exchange rates for currencies of these countries may fluctuate in relation to the U.S. dollar and these fluctuations may have an adverse or favorable effect on our operating results when translating foreign currencies into U.S. dollars.

In addition, the Company faces risks in complying with various foreign laws and technical standards and unpredictable changes in foreign regulations, including U.S. legal requirements governing U.S. companies operating in foreign countries, legal and cultural differences in the conduct of business, potential adverse tax consequences, difficulty in staffing and managing international operations.

Decline in our operating results could lead to impairment charges relating to our goodwill and long-lived assets

We regularly monitor our goodwill and long-lived assets for impairment indicators. In conducting our goodwill impairment testing, we compare the fair value of each of our reporting units with goodwill to the related net book value. The Company performs its annual impairment review of goodwill in its second fiscal quarter and when a triggering event occurs between annual impairment tests. In conducting our impairment analysis of long-lived assets, we compare the undiscounted cash flows expected to be generated from the long-lived assets to the related net book values. Changes in economic or operating conditions impacting our estimates and assumptions could result in the impairment of our goodwill or long-lived assets. In the event that we determine that our goodwill or long-lived assets are impaired, we may be required to record a significant non-cash charge to earnings that could adversely affect our results of operations.

Risks Related to our Capital Structure and Finances

Our credit facility contains financial covenants that may limit our ability to take certain actions

We remain dependent upon others for our financing needs and our current credit facility includes certain financial covenants. These covenants could constrain the execution of our business strategy and growth plans. Our ability to continue to meet these financial covenants is not assured. If we default under any of these requirements, our lenders could declare all outstanding borrowings, accrued interest and fees to be due and payable or significantly increase the cost of the facility. In these circumstances, there can be no assurance that we would have sufficient liquidity to repay or refinance this indebtedness at favorable rates or at all. If we are forced to refinance these borrowings on less favorable terms, our results of operations and financial condition could be adversely affected by increased costs and rates. During fiscal 2015, we met all of the covenant requirements.

While our recent amendment to our credit facility reduced certain financing risks (elimination of the interest coverage test and extending the maturity of the loan), it also provides for a minimum liquidity covenant test ranging from $20.0 million to $50.0 million through 2016. Sources from certain liquidity events expected to be realized by the Company may be key factors in meeting our covenant obligations during 2016. In the event we do not meet the covenant test, there could be a default of the covenant requirement if a waiver is not obtained. A default in the credit facility could lead to an acceleration of the then outstanding amount by the lender making such amount immediately due and owing.

The inability to renew our credit facility could negatively affect our operations and limit our liquidity

We rely on financing for future working capital, capital expenditures and other corporate purposes. The structure of this financing requires us to renew our arrangements periodically. There can be no assurance that replacement financing will be available to us or that we will be able to negotiate replacement financing at reasonable costs or on reasonable terms.

The volatility in credit and capital markets may create additional risks to our business in the future. We are exposed to financial market risk (including refinancing risk) resulting from, among other things, changes in interest rates and conditions in the credit and capital markets. Turmoil in the credit markets or a contraction in the availability of credit may make it more difficult for us to meet our working capital requirements and could have a material adverse effect on our business, results of operations and financial position.

Fluctuations in interest rates and turmoil in the financial markets could increase our cost of borrowing and impede access to or increase the cost of financing our operations

While we have access to global credit markets through our financing activities, credit markets may experience significant disruptions. Interest rates are highly sensitive to many factors that are beyond our control, including general economic conditions and policies of various governmental and regulatory agencies and, in particular, the Federal Reserve Board. Increases in interest rates would likely increase our borrowing costs over the medium to long-term and could negatively impact our results of operations.

11

Deterioration in global financial markets could make future financing difficult or more expensive. If a financial institution that is party to our credit facility were to declare bankruptcy or become insolvent, they may be unable to perform under their agreement with us. This could leave us with reduced borrowing capacity, which could have an adverse impact on our business, financial condition and results of operations.

Risks Related to our Particular Customers and the Projects on which we Work

Our project-related businesses are subject to delays, unanticipated costs and cancellations that may result in unforeseen costs, reductions in revenues or the payment of liquidated damages

In some of our contracts we guarantee certain results of a project, such as the substantial completion of a project by a scheduled date, performance testing levels, results and other performance requirements. Failure to meet those criteria could result in additional costs or penalties, including liquidated damages, which could exceed our projected profit. Many projects involve extended time periods, sometimes over several years. We may encounter difficulties and delays, schedule changes, delays from our customers' failure to timely obtain rights required to perform or complete a project and other factors, some of which are beyond our control, that could impact our ability to complete projects in accordance with the original delivery schedules. In addition, we often contract with subcontractors to assist us with our responsibilities, and any delay or poor performance by subcontractors may result in delays in the overall progress of projects or may cause us to incur additional costs, or both. Delays and additional costs may be substantial, we may not be able to recover any or all of these costs and our revenues and operating profits could be significantly reduced. We also may be required to invest significant working capital to fund cost overruns. Delays or cancellations also may impact our reputation or relationships with customers, adversely affecting our ability to secure new contracts.

At times, project contracts may require customers or other parties to provide the specifications, design, equipment or materials to be used on a project. In some cases, the project schedule or the design, or equipment may be deficient or delivered later than required by the project schedule. In addition, our customers may change or delay various elements of a project after commencement, resulting in additional direct or indirect costs.

Under these circumstances, we generally attempt to negotiate with the customer with respect to the amount of additional time required and the compensation to be paid to us. We may be unable to obtain, through negotiation, arbitration, mediation, litigation or otherwise, adequate amounts to compensate us for additional work or expense incurred. Litigation, arbitration or mediation of claims for compensation may be lengthy and costly, and may not ultimately result in us receiving adequate compensation for these matters, which could adversely affect our results of operations or cash flows. Delays or cancellations also may impact our reputation or relationships with customers, adversely affecting our ability to secure new contracts.

Many of our contracts either provide no minimum purchase requirements, are cancellable during the term, or both

In our Staffing Services segment most contracts are not sole source, and many of our contracts, even those with multi-year terms, provide no assurance of any minimum amount of revenue. Under many of these contracts we still must compete for each individual placement or project. In addition, many of our long-term contracts contain cancellation provisions under which the customer can cancel the contract at any time or on relatively short notice, even if we are not in default under the contract. Therefore, these contracts do not provide the assurances that typical long-term contracts often provide and are inherently uncertain with respect to the revenues and earnings we may recognize with respect to our customer contracts. Consequently, in all our business segments, if customers do not utilize our services under existing contracts or do not renew existing contracts, that could adversely affect our results of operations or cash flows.

The loss of major customers could adversely impact our business

We experience revenue concentration with large customers within certain operating units. Although we have no customer that represents over 10% of revenues, the deterioration of the financial condition or business prospects of these customers, or a change in their strategy around the use of our services, could have a material adverse effect on our business, financial condition and results of operations.

Additionally, any reductions, delays or cancellation of contracts with any of our key customers or the loss of one or more key customers could materially reduce our revenue and operating income. There is no assurance that our current customers will continue to do business with us or that contracts with existing customers will continue at current or historical levels.

We are dependent upon our ability to attract and retain technologically skilled personnel

Our operations are dependent upon our ability to attract and retain technologically skilled personnel, particularly for temporary assignments to customers of our Staffing Services segment, projects at clients for our information technology infrastructure services as well as in the areas of implementation and upgrading of internal systems. The availability of such

12

personnel is dependent upon a number of economic and demographic conditions. We may, in the future, find it difficult or more costly to hire such personnel in the face of competition from other companies.

In addition, variations in the rate of unemployment and higher wages sought by contingent workers in certain technical fields that continue to experience labor shortages could affect our ability to meet our customers' demands in these fields and adversely affect our results of operations.

Risks Related to our Internal Organization, Projects and Operations

New business initiatives may have an adverse effect on our business

As part of our business strategy, we have implemented new initiatives to exit our non-core and unprofitable businesses. This includes actions to optimize our organizational structure, technology and delivery of services and to reduce the cost of operating our business. If these initiatives are ineffective or insufficient, we may be unable to effectively implement our business strategy and there can be no assurance that we will achieve our objectives.

Our results of operations and ability to grow may be negatively affected if we are not able to keep pace with rapid changes in technology

The Company's success depends on our ability to keep pace with rapid technological changes in the development and implementation of our services and solutions. We must innovate and evolve our services and products to satisfy customer requirements and to remain competitive. There can be no assurance that in the future we will be able to foresee changes needed to identify, develop and commercialize innovative and competitive services and products in a timely and cost-effective manner to achieve customer acceptance in markets characterized by rapidly changing technology and frequent new product and service introductions.

Our information technology projects may not yield their intended results

We currently have information technology projects in process or in the planning stages, including improvements to applicant onboarding and tracking systems and ERP systems. Although the technology is intended to increase productivity and operating efficiencies, these projects may not yield their intended results. Any delays in completing, or an inability to successfully complete, these technology initiatives or an inability to achieve the anticipated efficiencies could adversely affect our operations, liquidity and financial condition.

We are dependent upon the quality of our personnel

Our operations are dependent on the continued efforts of our senior management. In addition, we are dependent on the performance and productivity of our managers and field personnel. Our ability to attract and retain business is significantly affected by customer relationships and the quality of service rendered. The loss of high quality personnel and members of management with significant experience in our industry without replacement by personnel with similar quality and experience may cause a significant disruption to our business. Moreover, the loss of key managers and field personnel could jeopardize existing customer relationships with businesses that use our services based upon relationships with those managers and field personnel.

Risks Related to Legal Compliance and Litigation

We are subject to employment–related claims, client indemnification claims and other claims and losses that could have a material adverse effect on our business

Our Staffing Services segment employs or engages individuals on a contingent basis and places them in a customer's workplace. Our ability to control the customer's workplace is limited, and we risk incurring liability to our employees for injury (which can result in increased workers' compensation costs) or other harm that they suffer at the customer's workplace. In addition we may face claims related to violations of wage and hour regulations, discrimination, harassment, the employment of undocumented or unlicensed personnel, misconduct, negligence or professional malpractice by our employees, and claims relating to the misclassification of independent contractors, among others.

Additionally, we risk liability to our customers for the actions or inactions of our employees, including those individuals employed on a contingent basis that may result in harm to our customers. Such actions may be the result of negligence or misconduct on the part of our employees, damage to customer facilities due to negligence, criminal activity and other similar claims. In some cases, we must indemnify our customers for certain acts of our employees, and certain customers have negotiated increases in the scope of such indemnification agreements. We also may incur fines, penalties and losses that are not

13

covered by insurance or negative publicity with respect to these matters. There can be no assurance that the policies and procedures we have in place will be effective or that we will not experience losses as a result of these risks.

Our ability to retain acceptable coverage limits at commercially reasonable cost and terms may adversely impact our financial results

We cannot be certain we will be able to obtain appropriate types or levels of insurance in the future, that adequate replacement policies will be available on acceptable terms, if at all, and at commercially reasonable costs, or that the companies from which we have obtained insurance will be able to pay claims we make under such policies.

Our insurance policies for various exposures including, but not limited to, general liability, auto liability, workers' compensation and employer's liability, directors' and officers' insurance, professional liability, employment practices, loss to real and personal property, business interruption, fiduciary and other management liability, are limited and the losses that we face may be not be covered, may be subject to high deductibles or may exceed the limits purchased.

Unexpected changes in workers' compensation and other insurance plans may negatively impact our financial condition

Liability for workers' compensation, automobile and general liability is insured under a retrospective experience-rated insurance program for losses exceeding specified deductible levels and the Company is self-insured for losses below the specified deductible limits.

The Company is self-insured for a portion of its medical benefit programs. The liability for the self-insured medical benefits is limited on a per-claimant basis through the purchase of stop-loss insurance. The Company's retained liability for the self-insured medical benefits is determined by utilizing actuarial estimates of expected claims based on statistical analysis of historical data.

Unexpected changes related to our workers' compensation, disability and medical benefit plans may negatively impact our financial condition. Changes in the severity and frequency of claims, in state laws regarding benefit levels and allowable claims, actuarial estimates, or medical cost inflation could result in costs that are significantly higher. If future claims-related liabilities increase due to unforeseen circumstances, or if we must make unfavorable adjustments to accruals for prior accident years, our costs could increase significantly. There can be no assurance that we will be able to increase the fees charged to our customers in a timely manner and in a sufficient amount to cover the increased costs that result from any changes in claims-related liabilities.

Costs related to litigation could adversely impact our financial condition

We are involved in pending and threatened legal proceedings from time to time, the outcome of which is inherently uncertain and difficult to predict. It is uncertain at what point any of these or new matters may affect us, and there can be no assurance that our financial resources or related insurance are sufficient to cover these matters in their entirety or any one of these matters. Therefore, there can be no assurance that these matters will not have an adverse effect on our financial condition, results of operations or cash flows.

Improper disclosure of sensitive or confidential employee or customer data, including personal data, could result in liability and harm our reputation

Our business involves the use, storage and transmission of information about our full-time and contingent employees, customers and other individuals. This information may contain sensitive or confidential employee and customer data, including personally identifiable information. Cyber attacks or other breaches of network or information technology security, as well as risks associated with compliance on data privacy, could have an adverse effect on our systems, services, reputation and financial results. Additionally, our employees may have access or exposure to customer data and systems. The misuse of information could result in legal liability. It is possible that our security controls over sensitive or confidential data and other practices we and our third-party service providers follow may not prevent the improper access to, or disclosure of, such information. Such disclosure could harm our reputation and subject us to liability under our contracts and laws that protect sensitive or personal data and confidential information in various countries and jurisdictions, resulting in increased costs or loss of revenue. Further, data privacy is subject to frequently changing rules and regulations, which sometimes conflict among jurisdictions and countries in which we provide services. Our failure to adhere to or successfully implement processes in response to changing regulatory requirements in this area could result in legal liability or impairment to our reputation in the marketplace.

14

The possession and use of personal information and data in conducting our business subjects us to legislative and regulatory burdens. We may be required to incur significant expenses to secure our systems and comply with mandatory privacy and security standards and protocols imposed by laws, regulation, industry standards or contractual obligations.

We rely extensively on our information technology systems which are vulnerable to damage and interruption

We rely on information technology networks and systems, including the Internet, to process, transmit and store electronic and financial information, to manage a variety of business processes and activities, and to comply with regulatory, legal and tax requirements. We depend on our information technology infrastructure for digital marketing activities, collection and retention of customer data, employee information and for electronic communications among our locations, personnel, customers and suppliers around the world. These information technology systems may be susceptible to damage, disruptions or shutdowns due to failures during the process of upgrading or replacing software, databases or components thereof, power outages, hardware failures, computer viruses, attacks by computer hackers, telecommunication failures, user errors or catastrophic events. Our sales, financial condition and results of operations may be materially and adversely affected, and we could experience delays in reporting our financial results, if our information technology systems suffer severe damage, disruption or shutdown and our business continuity plans do not effectively resolve the issues in a timely manner.

Failure to maintain adequate financial and management processes and internal controls could lead to errors in our financial reporting

The accuracy of our financial reporting is dependent on the effectiveness of our internal control. If our management is unable to certify the effectiveness of our internal controls or if our independent registered public accounting firm can not render an opinion on the effectiveness of our internal controls over financial reporting, or if material weaknesses in our internal controls are identified, we could be subject to regulatory scrutiny and a loss of public confidence. In addition, if we do not maintain adequate financial and management personnel, processes and controls, we may not be able to accurately report our financial performance on a timely basis, which could lead to significant decreases in the trading price of our shares, or the delisting of our shares from the NYSE MKT, which would harm our shareholders.

New and increased government regulation, employment costs or taxes could have a material adverse effect on our business, especially for our contingent staffing business

Certain of our businesses are subject to licensing and regulation in some states and most foreign jurisdictions. There can be no assurance that we will continue to be able to comply with these requirements, or that the cost of compliance will not become material. Additionally, the jurisdictions in which we do or intend to do business may:

• | create new or additional regulations that prohibit or restrict the types of services that we currently provide; |

• | impose new or additional employment costs that we may not be able to pass on to customers or that could cause customers to reduce their use of our services, especially in our Staffing Services segment, which could adversely impact our business; |

• | require us to obtain additional licenses; or |

• | increase taxes (especially payroll and other employment-related taxes) or enact new or different taxes payable by the providers or users of services such as those offered by us, thereby increasing our costs, some of which we may not be able to pass on to customers or that could cause customers to reduce their use of our services especially in our Staffing Services segment, which could adversely impact our results of operations or cash flows. |

In some of our foreign markets, new and proposed regulatory activity may impose additional requirements and costs, and could cause changes in customers' attitudes regarding the use of outsourcing and contingent workers in general, which could have an adverse effect on our contingent staffing business.

15

Health care reform could increase the costs of the Company's staffing business

In March 2010, the Patient Protection and Affordable Care Act ("the Act") was signed into U.S. law. The Act represents comprehensive U.S. health care reform legislation that, in addition to other provisions, subject us to potential penalties unless we offer our employees minimum essential health care coverage that is affordable and provides minimum value. In order to comply with the employer mandate provision of the Act, we have begun offering health care coverage to all employees eligible for coverage under the Act. Designating employees as eligible is complex, and is subject to challenge by employees and the Internal Revenue Service. While we believe we have properly identified eligible employees, a later determination that we failed to offer the required health coverage to eligible employees could result in penalties that may harm our business. We cannot be certain that compliant insurance coverage will remain available to us on reasonable terms, and we could face additional risks arising from future changes to the Act or changed interpretations of our obligations under the Act. There can be no assurance that we will be able to recover all related costs through increased pricing to our customers or that they will be recovered in the period in which costs are incurred, and the net financial impact on our results of operations could be significant.

Risks Related to Our Common Stock

Our stock price could be volatile and, as a result, investors may not be able to resell their shares at or above the price they paid for them

Our stock price has in the past, and could in the future, fluctuate as a result of a variety of factors, including:

• | our failure to meet the expectations of the investment community or our estimates of our future results of operations; |

• | industry trends and the business success of our customers; |

• | loss of one or more key customers; |

• | strategic moves by our competitors, such as product or service announcements or acquisitions; |

• | regulatory developments; |

• | litigation; |

• | general economic conditions; |

• | other domestic and international macroeconomic factors unrelated to our performance; and |

• | any of the other previously noted risk factors. |

The stock market has experienced, and is likely to in the future experience, volatility that has often been unrelated to the operating performance of particular companies. These broad market fluctuations may also adversely affect the market price of our common stock.

Our principal shareholders, whose interests may differ from those of other shareholders, own a significant percentage of our common stock and will be able to exercise significant influence over Volt

As of December 31, 2015, a significant amount of our outstanding common stock was controlled by related family members. Although there can be no assurance as to how these shareholders will vote, if they vote in the same manner, these shareholders might be able to control the composition of our board of directors and many other matters requiring shareholder approval and would continue to have significant influence over our affairs. The interests of our principal shareholders may not align with those of our other shareholders.

Furthermore, the provisions of the New York Business Corporation Law, to which we are subject, require the affirmative vote of the holders of two-thirds of all of our outstanding shares entitled to vote in order to adopt a plan of merger or consolidation between us and another entity and to approve a sale, lease, exchange or other disposition of all or substantially all of our assets not made in our usual and regular course of business. Accordingly, our principal shareholders, acting together, could prevent the approval of such transactions even if such transactions are in the best interests of our other shareholders.

Our business could be negatively affected as a result of a potential proxy contest for the election of directors at our annual meeting, and such proxy contest could cause us to incur significant expense, hinder execution of our business strategy and impact the trading value of the Company's securities

In 2014 and 2015, the Company was subjected to a threatened proxy contest, which resulted in the negotiation of significant changes to the Board of Directors and substantial costs were incurred.

A proxy contest would require us to incur significant legal fees and proxy solicitation expenses and require significant time and attention by management and the Board of Directors. The potential of a proxy contest could interfere with our ability to execute our strategic plan, give rise to perceived uncertainties as to our future direction, adversely affect our relationships with key business partners, result in the loss of potential business opportunities and make it more difficult to attract and retain qualified personnel, any of which could materially and adversely affect our business and operating results.

16

The market price of our common stock could be subject to significant fluctuation or otherwise be adversely affected by the events, risks and uncertainties related to stockholder activism.

New York State law and our Articles of Incorporation and By-laws contain provisions that could make the takeover of Volt more difficult

Certain provisions of New York State law and our articles of incorporation and by-laws could have the effect of delaying or preventing a third party from acquiring Volt, even if a change in control would be beneficial to our shareholders. These provisions of our articles of incorporation and by-laws include:

• | permitting removal of directors only for cause; |

• | providing that vacancies on the board of directors will be filled by the remaining directors then in office, other than as set forth in the March 30, 2015 agreement between the Company and Glacier Peak Capital LLC and certain of its affiliates; and |

• | requiring advance notice for shareholder proposals and director nominees. |

In addition to the voting power of our principal shareholders discussed above, our board of directors could choose not to negotiate with a potential acquirer that it did not believe was in our strategic interests. If an acquirer is discouraged from offering to acquire Volt or prevented from successfully completing an acquisition by these or other measures, our shareholders could lose the opportunity to sell their shares at a more favorable price.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

17

ITEM 2. PROPERTIES

As of December 2015, our corporate headquarters is located in approximately 15,000 square feet at 1133 Avenue of the Americas, New York, New York. A summary of our principal owned and leased properties (those exceeding 20,000 square feet) that are currently in use is set forth below:

United States

Location |

| Business Segment/Purpose |

| Own/Lease |

| Lease Expiration |

| Approximate Square Feet | ||

Orange County, California |

| Staffing Services and General and Administrative Offices |

| Own (1) |

| - | |

| 200,000 | |

San Antonio, Texas |

| Staffing Services |

| Lease |

| 2019 | |

| 71,000 | |

Redmond, Washington |

| Staffing Services |

| Lease |

| 2020 | |

| 66,000 | |

Montreal, Quebec |

| Staffing Services |

| Lease |

| 2020 | |

| 35,000 | |

Wallington, New Jersey |

| Other |

| Lease |

| 2018 | |

| 32,000 | |

(1) | See our Note on Debt in our Consolidated Financial Statements for information regarding a term loan secured by a deed of trust on this property. We lease approximately 39,000 square feet of these premises to an unaffiliated third party with a term through October 31, 2020, with the tenant having two additional 60-month lease renewal options and certain rights of early termination. We have undertaken a process for a sale leaseback transaction of our Orange, CA facility. The transaction is expected to take place within the first or second fiscal quarter of 2016. |

We lease space in approximately 100 other facilities worldwide, excluding month-to-month leases, each of which consists of less than 20,000 square feet. The Company's leases expire at various times from 2016 until 2025.

At times we lease space to others in the buildings that we own or lease if we do not require the space for our own business. We believe that our facilities are adequate for our presently anticipated uses, and we are not dependent upon any individual leased premises.

For additional information pertaining to lease commitments, see our Note on Commitments and Contingencies in our Consolidated Financial Statements.

ITEM 3. | LEGAL PROCEEDINGS |

From time to time, the Company is subject to claims in legal proceedings arising in the ordinary course of its business, including payroll-related and various employment-related matters. All litigation currently pending against the Company relates to matters that have arisen in the ordinary course of business and the Company believes that such matters will not have a material adverse effect on its consolidated financial condition, results of operations or cash flows.

ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

18

PART II

ITEM 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Until August 25, 2014, our common stock was listed on the over-the-counter market under the symbol "VISI". Since then it has traded on the NYSE MKT under the symbol "VISI". The following table sets forth, for the periods indicated, the high and low sales prices or the high and low bid quotations for our common stock for the years ended November 1, 2015 and November 2, 2014. The over-the-counter market bid quotations reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not necessarily represent actual transactions.

Fiscal Period |

|

| First Quarter |

| Second Quarter |

| Third Quarter |

| Fourth Quarter | ||||||||

2015 | High |

| $ | 12.73 | |

| $ | 12.85 | |

| $ | 11.96 | |

| $ | 9.98 | |

| Low |

| $ | 8.28 | |

| $ | 10.28 | |

| $ | 8.95 | |

| $ | 7.97 | |

2014 | High |

| $ | 10.05 | |

| $ | 10.15 | |

| $ | 9.50 | |

| $ | 9.50 | |

| Low |

| $ | 8.30 | |

| $ | 7.94 | |

| $ | 7.45 | |

| $ | 7.77 | |

On January 5, 2016 there were 261 holders of record of our common stock, exclusive of shareholders whose shares were held by brokerage firms, depositories and other institutional firms in "street name" for their customers.

Issuer Purchases of Equity Securities

On January 14, 2015, the Board of Directors approved a new 36-month share repurchase program of up to 1,500,000 shares of the Company's common stock to begin on January 19, 2015, replacing a prior program. Such repurchases can be made through open market or private transactions. Share repurchases under the program will be subject to specified parameters and certain price and volume restraints and any repurchased shares will be held in treasury. The exact number and timing of share repurchases will depend upon market conditions and other factors. There were no shares purchased in the fourth quarter of fiscal 2015.

19

Performance Information

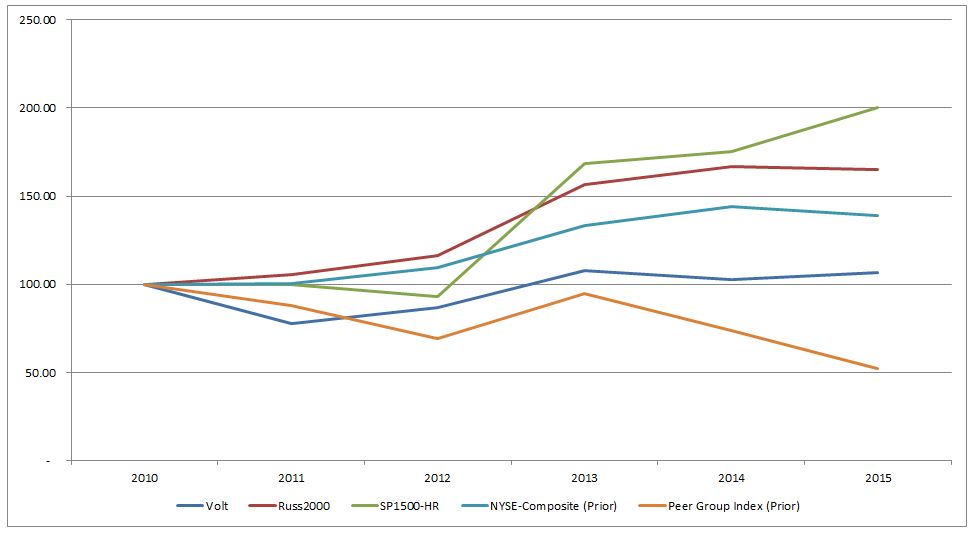

Shareholder Return Performance Graph

The Company has changed its indexes for fiscal 2015, removing both the NYSE Composite and a custom peer group of companies having market capitalizations that are within 5% of the market capitalization of the Company's common stock as of the year-end of fiscal period. This peer group was previously selected because of its operations in diverse business segments. However, as a result of our exit of non-core businesses, the Company has selected the S&P 1500 Human Resources and Employment Services Index to more appropriately reflect our performance relative to our peers. The Company has also been included in the Russell 2000 index since June 2015 and consequently, this index will replace the NYSE Composite.

The graph includes two indexes from fiscal year 2014 - NYSE Composite (Prior) and Peer Group Index (Prior).

* $100 invested on 11/1/10 in stock or index, including reinvestment of dividends.

20

ITEM 6. | SELECTED FINANCIAL DATA |