UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

FOR ANNUAL AND TRANSITION REPORTS

PURSUANT TO SECTIONS 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

(Mark One)

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-15451

United Parcel Service, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 58-2480149 | |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

| 55 Glenlake Parkway, N.E. Atlanta, Georgia | 30328 | |

| (Address of Principal Executive Offices) | (Zip Code) |

(404) 828-6000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

| Class B common stock, par value $.01 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

Class A common stock, par value $.01 per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No ☑

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of "accelerated filer", "large accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. Check one:

Large accelerated filer ☑ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ☑

The aggregate market value of the class B common stock held by non-affiliates of the registrant was $53,668,942,247 as of June 30, 2011. The registrant's class A common stock is not listed on a national securities exchange or traded in an organized over-the-counter market, but each share of the registrant's class A common stock is convertible into one share of the registrant's class B common stock.

As of February 10, 2012, there were 236,015,165 outstanding shares of class A common stock and 722,705,229 outstanding shares of class B common stock.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement for its annual meeting of shareowners scheduled for May 3, 2012 are incorporated by reference into Part III of this report.

UNITED PARCEL SERVICE, INC.

ANNUAL REPORT ON FORM 10-K FOR THE YEAR ENDED DECEMBER 31, 2011

TABLE OF CONTENTS

| PART I | ||||||

Item 1. | Business | 1 | ||||

Overview | 1 | |||||

Business Strategy | 2 | |||||

Technology | 3 | |||||

Reporting Segments and Products & Services | 4 | |||||

Sustainability | 8 | |||||

Community | 9 | |||||

Reputation | 9 | |||||

Employees | 9 | |||||

Safety | 10 | |||||

Competition | 10 | |||||

Competitive Strengths | 10 | |||||

Government Regulation | 11 | |||||

Where You Can Find More Information | 13 | |||||

Item 1A. | Risk Factors | 14 | ||||

Item 1B. | Unresolved Staff Comments | 18 | ||||

Item 2. | Properties | 18 | ||||

Operating Facilities | 18 | |||||

Fleet | 20 | |||||

Item 3. | Legal Proceedings | 20 | ||||

Item 4. | Mine Safety Disclosures | 20 | ||||

| PART II | ||||||

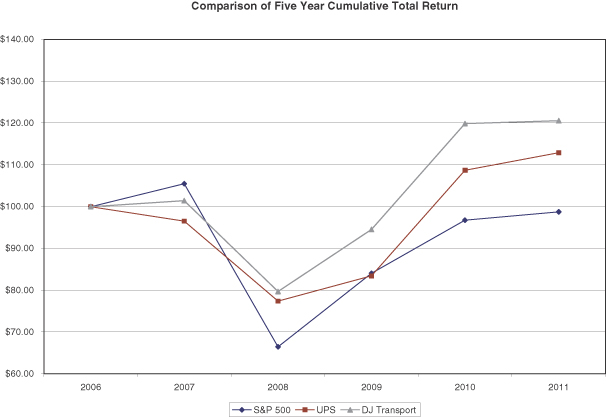

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 21 | ||||

Shareowner Return Performance Graph | 22 | |||||

Item 6. | Selected Financial Data | 23 | ||||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 24 | ||||

Overview | 24 | |||||

Items Affecting Comparability | 25 | |||||

U.S. Domestic Package Operations | 27 | |||||

International Package Operations | 30 | |||||

Supply Chain & Freight Operations | 34 | |||||

Operating Expenses | 37 | |||||

Investment Income and Interest Expense | 40 | |||||

Income Tax Expense | 41 | |||||

Liquidity and Capital Resources | 42 | |||||

New Accounting Pronouncements | 51 | |||||

Critical Accounting Policies and Estimates | 51 | |||||

Item 7A. | Quantitative and Qualitative Disclosures about Market Risk | 56 | ||||

Item 8. | Financial Statements and Supplementary Data | 59 | ||||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 123 | ||||

Item 9A. | Controls and Procedures | 123 | ||||

Item 9B. | Other Information | 123 | ||||

| PART III | ||||||

Item 10. | Directors, Executive Officers and Corporate Governance | 124 | ||||

Item 11. | Executive Compensation | 125 | ||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 125 | ||||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 125 | ||||

Item 14. | Principal Accounting Fees and Services | 126 | ||||

| PART IV | ||||||

Item 15. | Exhibits and Financial Statement Schedules | 127 | ||||

PART I

Cautionary Statement About Forward-Looking Statements

This report includes certain "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Statements in the future tense, and all statements accompanied by terms such as "believe," "project," "expect," "estimate," "assume," "intend," "anticipate," "target," "plan," and variations thereof and similar terms are intended to be forward-looking statements. We intend that all forward-looking statements we make will be subject to safe harbor protection of the federal securities laws pursuant to Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934.

Our disclosure and analysis in this report, in our Annual Report to Shareholders and in our other filings with the Securities and Exchange Commission ("SEC") contain forward-looking statements regarding our intent, belief and current expectations about our strategic direction, prospects and future results. From time to time, we also provide forward-looking statements in other materials we release as well as oral forward-looking statements. Such statements give our current expectations or forecasts of future events; they do not relate strictly to historical or current facts. Management believes that these forward-looking statements are reasonable as and when made. However, caution should be taken not to place undue reliance on any such forward-looking statements because such statements speak only as of the date when made.

Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our historical experience and our present expectations or anticipated results. These risks and uncertainties are described in Part I, "Item 1A. Risk Factors" and may also be described from time to time in our future reports filed with the SEC. You should consider the limitations on, and risks associated with, forward-looking statements and not unduly rely on the accuracy of predictions contained in such forward-looking statements. We do not undertake any obligation to update forward-looking statements to reflect events, circumstances, changes in expectations, or the occurrence of unanticipated events after the date of those statements.

| Item 1. | Business |

Overview

United Parcel Service, Inc. ("UPS") was founded in 1907 as a private messenger and delivery service in Seattle, Washington. Today, UPS is the world's largest package delivery company, a leader in the U.S. less-than-truckload industry and the premier provider of global supply chain management solutions. We deliver packages each business day for 1.1 million shipping customers to 7.7 million consignees in over 220 countries and territories. In 2011, we delivered an average of 15.8 million pieces per day worldwide, or a total of 4.01 billion packages. Total revenue in 2011 was $53.1 billion.

We are a global leader in logistics, and we create value for our customers through solutions that lower costs, improve service and provide highly customizable supply chain control and visibility. Customers are attracted to our broad set of services that are delivered as promised through our integrated ground, air and ocean global network.

Our services and integrated network allow shippers to simplify their supply chains by using fewer carriers and to adapt their transportation requirements and spend as their businesses evolve. Across our service portfolio, we also provide control and visibility of customers' inventories and supply chains via our UPS technology platform. The information flow from UPS technology drives improvements for our customers, as well as for UPS, in reliability, flexibility, productivity and efficiency.

Particularly over the last decade, UPS has significantly expanded the scope of our capabilities to include more than package delivery. Our logistics and distribution capabilities give companies the power to easily expand their businesses to new markets around the world. By leveraging our international infrastructure, UPS

1

enables our customers to bridge time zones, cultures, distances and languages to keep the entire supply chain moving smoothly. We operate approximately 800 logistics facilities, in more than 120 countries, offering warehouse space of 35 million square feet.

We serve the global market for logistics services, which include transportation, distribution, forwarding, ground, ocean and air freight, brokerage and financing. Our technology seamlessly binds our service portfolio. We have three reportable segments: U.S. Domestic Package, International Package and Supply Chain & Freight, all of which are described below. For financial information concerning our reportable segments and geographic regions, refer to note 12 of our consolidated financial statements.

Business Strategy

Customers leverage our broad array of services; balanced global presence in North America, Europe, Asia and Latin America; reliability; and industry leading technology for competitive advantage in markets where they choose to compete. We prudently invest to expand our integrated network and our service portfolio. Technology investments create user-friendly shipping, e-commerce, logistics management and visibility tools for our customers, while supporting UPS's ongoing efforts to increase operational efficiencies.

Our service portfolio and investments are rewarded with among the best returns on invested capital and operating margins in the industry. We have a long history of sound financial management. Our balance sheet reflects financial strength that few companies can match. As of December 31, 2011, we had a balance of cash and marketable securities of approximately $4.275 billion and shareowners' equity of $7.108 billion. Our Moody's and Standard & Poor's short-term credit ratings are P-1 and A-1+, respectively, and our Moody's and Standard & Poor's long-term credit ratings are Aa3 and AA-, respectively. We have a stable outlook from both of these credit rating agencies. Cash generation is a significant strength of UPS. This gives us strong capacity to service our obligations and allows for distributions to shareowners, reinvestment in our businesses and the pursuit of growth opportunities.

We enable and are the beneficiaries of the following trends:

Expansion of Global Trade

Trade across borders is predicted to grow at rates that are at least double the growth rates of U.S. and global domestic production for the foreseeable future. As a result, U.S. and international economies are becoming more inter-connected and dependent on foreign trade.

UPS plays an important role in global trade and is uniquely positioned to take advantage of trade growth, wherever it emerges. Our balanced global presence and productivity enhancing technologies allow customers to effortlessly expand to new markets. We advocate the expansion of free trade, including the passage of regional trade pacts and the removal of trade barriers. Free trade is a catalyst for job creation, economic growth and improved living standards; additionally, it propels our growth.

Emerging Market Growth

As our current and prospective customers seek growth outside of developed markets, they look to emerging markets for expansion. We make long-term, measured investments in markets where our customers choose to grow. Our investments are scaled to the local opportunity. We typically follow a pattern of entering a market through importing and exporting, expanding domestically with a partner or alliance, and then ultimately acquiring domestic operations where we see value and return. China is a prime example of this strategy as we continue to clear hurdles that will enable us to realize this vision. Our two key air hubs in Shanghai and Shenzhen support market expansion through increased cargo capacity and faster intra-Asia transit times, while enabling our customers to ship later in the day. We link Asia to Europe with overnight flights from Hong Kong through our air hub in Cologne, Germany.

Taken together, these two trends (expanding global trade and emerging market growth) underscore why our international business is a catalyst for UPS's growth.

2

Increasing need for vertical expertise in the integrated carrier space

We provide repeatable, scalable sector solutions for our customers. We invest in global capabilities and create value propositions for certain industries where there is a fit between our customers' needs and our offerings. Segments where we bring unique value propositions include health care, high-tech, automotive & industrial manufacturing, retail, government and professional services.

The health care industry faces complex challenges, including the continuing expiration of drug patents and the shifting landscape of regulatory requirements and drug pricing controls that differ by country. To counter these threats, many pharmaceutical companies have embarked on global expansion strategies that require infrastructure. UPS has aligned our resources to serve these needs through a well-developed supply chain management capability that is designed to satisfy regulatory and compliance requirements. We have built 33 dedicated health care facilities with over 5 million square feet of distribution space. These facilities allow us to provide reliable, secure, cost-effective warehousing and distribution for pharmaceutical firms' supply chains, which, in turn, allow them to easily navigate across and within borders.

We will continue to expand our vertical offerings, growing not only our physical and market footprint, but also our expertise and technology to support industry specific needs. Our growth strategy is to increase the number of customers benefitting from these vertical solutions and gain their associated small package and freight transportation.

Outsourcing

Outsourcing supply chain management is becoming more prevalent, as customers increasingly view professional management and operation of their supply chains as a strategic advantage. This trend enables companies to focus on what they do best. We can meet our customers' needs for outsourced logistics with our global capabilities in customized forwarding, warehousing, distribution, delivery and post-sales services. As we move deeper into customers' supply chains, we do so with a shared vision on how to best serve those who rely on our customers. We integrate our technology for efficiencies, visibility and control to ensure that we execute as promised.

Retail e-Commerce Growth

Throughout much of the world, e-commerce growth continues to outpace traditional lines of business. We continue to create new services, supported by UPS technology, that complement the traditional UPS premium home delivery service to address the needs of e-commerce shippers and receivers ("consignees"). Our offerings span a broad spectrum from cost-sensitive solutions such as SurePost, for shipments where economy takes precedence over speed, up to feature-rich solutions, including our new UPS My Choice service that provides consignees with revolutionary visibility and control of their inbound shipments.

With UPS My Choice, consignees direct the timing and location of their deliveries before a delivery attempt is made. Premium features include online delivery planners, detailed driver instructions, alternate delivery locations and a two-hour delivery window. Delivery alerts come via the channel chosen by the consignee-email, SMS text, etc. We strive to give our customers that ship using UPS My Choice the best delivery experience in the industry-delivery on the first attempt, where and when their customers want it.

Technology

Technology powers logistics. We bring industry leading UPS technology to our customers who, in turn, realize increased productivity, greater control of their supply chains and improved customer experience when they integrate with our technology. Customers benefit through offerings such as:

| • | UPS Quantum View which can speed up the revenue cycle (i.e. faster transit times, coupled with confirmation of delivery, allow shippers to collect accounts receivable more quickly), allow for inbound volume planning, manage third party shipping costs, automatically notify customers of incoming shipments, and of course, track shipments and let the customer react if a specific shipment status changes. |

3

| • | Flex Global View which provides customs alerts, supplier key performance indicators and inventory monitoring. |

| • | UPS Paperless Invoice which enables customers to submit a commercial invoice electronically when shipping internationally. This eliminates redundant data entry and errors, while reducing customs holds and paper waste. |

| • | UPS Import Control which gives our customers the ability to initiate their import shipments, define billing terms and assign accounts to charge, and remove commercial invoices prior to delivery to a third-party. |

| • | UPS Mobile apps, which allow our customers to track, ship and find UPS locations from mobile devices, are among the top downloaded applications for businesses. |

| • | UPS My Choice which focuses on the consignee and transforms the residential delivery experience. Receivers direct the timing and circumstances of their deliveries. This innovative service, which is unmatched in our industry, is powered by the complex integration of real-time route optimization and other technologies with our delivery network. We believe that UPS My Choice gives us a substantial lead over the competition. |

Technology, coupled with high-quality UPS employees, forms the foundation of our reliability and allows us to take customer experience to a higher level. Technology delivers value to our customers and returns to our shareholders. Recent advancements that evidence further gains in UPS's operational efficiency, flexibility, reliability and customer experience include:

| • | Continuing to rollout telematics to our delivery and tractor-trailer fleet. Telematics helps UPS determine a truck's performance and condition by capturing data on more than 200 elements, including speed, RPM, oil pressure, seat belt use, number of times the truck is placed in reverse and idling time. Together, improved data and driver coaching help reduce fuel consumption, emissions and maintenance costs, while improving driver safety. Moreover, customers experience more consistent pickup times and more reliable deliveries, thereby enhancing their profitability and competitiveness. |

| • | Implementing our On Road Integrated Optimization and Navigation ("ORION") system, which employs advanced algorithms to determine the optimal route for each delivery while meeting service commitments. |

| • | Converting our package cars to keyless entry, where drivers will be able to remotely turn the engine off with a button that will unlock the bulkhead door at the same time. |

| • | Ramping up installations of our Next Generation Small Sort ("NGSS") technology, which reduces the amount of memorization required to sort a package, thereby improving productivity and quality. Employees sort packages to bins tagged with flashing lights, rather than memorizing addresses, allowing us to dramatically reduce training time. |

Reporting Segments and Products & Services

As a global leader in logistics, UPS offers a broad range of domestic and export delivery services; the facilitation of international trade; and the deployment of advanced technology to more efficiently manage the world of business. We seek to streamline our customers' shipment processing and integrate critical transportation information into their own business processes, helping them to create supply chain efficiencies, better serve their customers and improve their cash flows.

4

Global Small Package

UPS's global small package operations provide time-definite delivery services for express letters, documents and small packages via air and ground services. We provide domestic delivery services within 56 countries and export services to more than 220 countries and territories around the world. We handle packages that weigh up to 150 pounds and are up to 165 inches in combined length and girth. All of our package services are supported by numerous shipping, visibility and billing technologies.

UPS handles all levels of service (air, ground, domestic, international, commercial, residential) through one global integrated pickup and delivery network. All packages are commingled throughout their journey in our network, except when necessary to meet their specific service commitments. This enables one UPS driver to pick up our customers' shipments, for any of our services, at the same scheduled time, day after day. Compared to companies with single service network designs, our integrated network uniquely provides operational and capital efficiencies while being easier on the environment.

Upon request, we offer same-day pickup of air and ground packages. Based on their needs, customers can schedule pickups for one to five days a week. Additionally, we provide our customers with easy access to UPS, with over 150,000 domestic and international entry points including: 40,000 drop boxes, 1,000 customer centers, 4,700 independently owned and operated locations of The UPS Store worldwide, 13,000 authorized shipping outlets and commercial counters, 6,300 alliance locations and 86,300 UPS drivers who can accept packages provided to them.

With the growth of online shopping, our customers' needs for efficient and reliable returns have increased. To this end, we have developed a robust selection of returns services that are available in over 100 countries. Options vary based on customer needs and country, and range from cost-effective solutions such as UPS Returns, which simply enables shippers to provide their customers with a return shipping label, to services as specialized as UPS Returns Exchange. In this new service, the UPS driver simplifies product exchanges by delivering a replacement item and picking up a return item in the same stop, and assisting with the re-packaging process.

We operate a global ground fleet of approximately 101,000 vehicles, of which our U.S. ground fleet serves all business and residential zip codes in the contiguous U.S. We operate a global air fleet of 523 aircraft, and we are one of the largest airlines in the world. Our global air network is centered at our Worldport hub in Louisville, Kentucky. Worldport sort capacity, currently at 416,000 packages per hour, has expanded over the years due to volume growth and a centralization effort. This facility is supplemented by our regional U.S. air hubs in Hartford, Connecticut; Ontario, California; Philadelphia, Pennsylvania; and Rockford, Illinois. This network design allows for cost-effective package processing in our most technology-enabled facility while enabling us to use fewer, larger and more fuel-efficient aircraft. Our largest international air hub is in Cologne, Germany, with other regional international hubs in Miami, Florida; Canada; Hong Kong; Singapore; Taiwan; and China.

U.S. Domestic Package Reporting Segment

UPS is a leader in time-definite, money-back guaranteed, small package delivery services. We offer a full spectrum of U.S. domestic guaranteed ground and air package transportation services. Depending on the delivery speed needed, customers can select from a range of guaranteed time and day definite delivery options.

| • | Customers can select from same day, next day, two day and three day delivery alternatives. Many of these services offer options that enable customers to specify a time of day cut-off for their delivery (e.g. by 8:30, 10:30, noon, end of day, etc.) |

| • | Customers can also leverage our extensive ground network to ship using our day-definite guaranteed ground service that serves every U.S. business and residential address. UPS delivers more ground packages than any other carrier, with over 11 million ground packages delivered on time every day in the U.S., most within one to three business days. |

5

| • | UPS also offers UPS SurePost, an economy residential ground service for customers with non-urgent, light weight residential shipments. UPS SurePost is a contractual residential ground service that combines the consistency and reliability of the UPS Ground network with final delivery provided by the U.S. Postal Service. |

International Package Reporting Segment

Our International Package reporting segment includes the small package operations in Europe, Asia, Canada and Latin America. UPS offers a wide selection of guaranteed, day and time-definite international shipping services.

| • | We offer three guaranteed time-definite express options (Express Plus, Express and Express Saver) to more locations than any other carrier. |

| • | For international shipments that do not require express services, UPS Worldwide Expedited offers a reliable, deferred, guaranteed day-definite service option. |

| • | For cross-border ground package delivery, we offer UPS Transborder Standard delivery services within Europe, between the U.S. and Canada and between the U.S. and Mexico. |

Europe, our largest region outside of the U.S., accounts for roughly half of international revenue and is one of our growth engines. Factors contributing to this are the highly fragmented nature of the market and the fact that exports make up a significant part of Europe's GDP. Given our well-known, trusted brand and distinctive integrated network, we believe there is continued strong potential for growth in small package exports in Germany, the U.K., France, Italy, Spain and the Netherlands. Due to our strong growth, we are expanding our main European air hub in Cologne by 70% to a capacity of 190,000 packages per hour. Expansion will come in stages; the first stage was completed in the fourth quarter of 2011 with the final stage targeted for 2013.

Asia is another growth engine due to attractive growth rates in intra-Asian trade and the dynamic Chinese economy. We are bringing faster time-in-transit to customers focused on intra-Asian trade, reducing transit days from Asia to Europe, and continuing to build our China presence. Our recent China investments include:

| • | Material outlays to add capabilities, facilities and quality employees. We are building awareness and relevance while demonstrating superior UPS performance. |

| • | Opened an air hub in Shenzhen in mid-2010. |

| • | Added intra-Asia and around-the-world flight frequencies allowing customers to reach more of Europe the next day, guaranteed, than any other express carrier. |

We serve more than 40 Asia-Pacific countries and territories through more than two dozen alliances with local delivery companies that supplement company-owned operations. In Vietnam, our volume has doubled since entering into an alliance with a local partner in 2010.

Additional International highlights include the following:

| • | Since our 2009 acquisition of Unsped Paket Servisi San ve Ticaret A.S. in Turkey, we have seen double-digit export and domestic growth in that country. |

| • | In South and Central America, we benefit from the strong regional economy. Our offerings include express package delivery in major cities as well as distribution and forwarding. |

| • | We continue to grow our business organically in Mexico. We are well positioned with freight, domestic, international and distribution services. |

| • | In February 2012 we broadened our European business-to-consumer service portfolio by acquiring Kiala S.A., a Belgium-based developer of a platform that enables e-commerce retailers to offer consumers the option of having goods delivered to a convenient retail location. |

6

Supply Chain & Freight Reporting Segment

The Supply Chain & Freight segment consists of our forwarding and logistics services, our UPS Freight business, and our financial offerings through UPS Capital. We manage supply chains in over 195 countries and territories, with approximately 35 million square feet of distribution space worldwide. Supply chain complexity creates demand for a global service offering that incorporates transportation, distribution and international trade and brokerage services, with financial and information services. We meet this demand by offering a broad array of services, which are described below.

The 2011 acquisition of Italy-based Pieffe Group ("Pieffe") supports our global health care strategy, which has seen us make investments to better serve our growing customer base in the pharmaceutical, biotech and medical device industries. Previously family-owned, Pieffe is a pharmaceutical logistics business with more than 35 years of experience offering high-quality storage, distribution and cold chain solutions to some of the world's leading pharmaceutical brands.

Freight Forwarding

UPS is the second largest U.S. domestic air freight carrier and among the top six international air freight forwarders globally. UPS offers a portfolio of guaranteed and non-guaranteed global air freight services. Additionally, as one of the world's leading non-vessel operating common carriers, UPS also provides ocean freight full-container load and less-than container load shipments between most major ports around the world.

Customs Brokerage

UPS is among the world's largest customs brokers by both the number of shipments processed annually and by the number of dedicated brokerage employees worldwide. With decades of customs brokerage experience, we provide our customers with customs clearance, trade management and international trade consulting services.

Logistics and Distribution

UPS Logistics offers the following:

| • | Distribution Services: UPS's comprehensive distribution services are provided through a global network of distribution centers that manage the flow of goods from receiving to storage and order processing to shipment, allowing companies to save time and money by minimizing their capital investment and positioning products closer to their customers. |

| • | Post Sales: Post Sales services support goods after they have been delivered or installed in the field. The four core service offerings within Post Sales include: 1) Critical Parts Fulfillment; 2) Reverse Logistics; 3) Test, Repair, and Refurbish; and 4) Network and Parts Planning. We leverage our global distribution network of 600+ field stocking locations to ensure that the right type and quantity of our customers' stock is in the right locations to meet the needs of their end-customers. Our customers are able to minimize spend and maximize service. |

| • | UPS Mail Innovations: UPS Mail Innovations offers an efficient, cost-effective method for sending lightweight parcels and flat mail to global addresses from the U.S. We pick up customers' domestic and international mail, sort, post, manifest and then expedite the secured mail containers to the destination postal service for last-mile delivery. |

7

UPS Freight

UPS Freight offers regional, inter-regional and long-haul less-than-truckload ("LTL") services, as well as full truckload services, in all 50 states, Canada, Puerto Rico, Guam, the U.S. Virgin Islands and Mexico. UPS Freight provides reliable LTL service backed by a day-definite, on-time guarantee at no additional cost. Additionally, many user-friendly small package technology offerings are also available for freight. Applications such as UPS WorldShip, Billing Center, and Quantum View allow customers to process and track LTL shipments, create electronic bills of lading and reconcile billing.

UPS Capital

UPS Capital offers a range of services, including export and import financing to help improve cash flow, risk mitigation offerings to protect goods, as well as payment solutions that help speed the conversion cycle of payments.

Sustainability

UPS's business and corporate responsibility strategies pursue a common interest to increase the vitality and environmental sustainability of the global economy by aggregating the shipping activity of millions of businesses and individuals worldwide into a single, highly efficient logistics network. This provides benefits to:

| • | UPS, by ensuring strong demand for our services. |

| • | The economy, by making global supply chains more efficient and less expensive. |

| • | The environment, by enabling our global customers to leverage UPS's carbon efficiency and thereby reduce the carbon intensity of their supply chains. |

We pursue sustainable business practices worldwide through operational efficiency, fleet advances, facility engineering projects and conservation enabling technology and service offerings. We help our customers to do the same.

Sustainability highlights in 2011 include:

| • | Rated 1 st in Social Responsibility in Fortune Magazine's 2011 "World's Most Admired" for the Delivery Industry. |

| • | One of Corporate Responsibility's "100 Best Corporate Citizens" and one of "The Best Corporate Citizens in Government Contracting". |

| • | Recognized by Ethisphere Institute as one of the "World's Most Ethical Companies". |

| • | Named to Interbrands "Best Global Brands" for the 7th consecutive year. We ranked in the Top 100 in brand value around the world (#27) and were the only company in the transportation sector to make the list in 2011. |

| • | Recognized as a constituent of the Dow Jones Sustainability Index for the 10th consecutive year. |

| • | One of America's Top Organizations for Multicultural Business Opportunities by DiversityBusiness.com. |

| • | Achieved a score of 99% in response to the Carbon Disclosure Project. Our Carbon Disclosure Leadership Index score is the highest in the U.S. and ties with only three other companies globally. |

| • | Recognized by ClimateCounts.org as best company in the consumer shipping sector for the 3rd consecutive year. |

More information is available on the UPS Sustainability website.

8

Community

We believe that strong communities are vital to the success of our company. By combining our philanthropy with the volunteer time and talents of our employees, UPS helps drive positive change for organizations and communities in need across the globe. The highlights of our corporate citizenship efforts in 2011 include:

| • | Local non-profits around the world received more than 1.6 million hours of volunteer service from UPS employees participating in our Neighbor-to-Neighbor program. |

| • | The UPS Foundation, our charitable organization, oversaw $97 million in donations of cash and in-kind services to global causes primarily in four focus areas-community safety, environmental sustainability, diversity and volunteerism. |

| • | UPS led all U.S. companies in United Way donations last year with more than $55 million, and surpassed $1 billion in cumulative donations to United Way. |

| • | UPS continued to help save lives through our UPS Humanitarian Relief program by providing our logistics expertise and resources to aid the famine-stricken Horn of Africa and areas impacted by the Japan earthquake. |

| • | Thousands of teenagers and novice drivers in the U.S., Canada, the U.K., and Germany participated in UPS Road Code. This safety program for new drivers features UPS employees as instructors – a role where they get to share driving knowledge and safety tips amassed over our 104-year history of safe driving. |

Reputation

Many of our customers trust UPS to extend their brand. We were pleased that UPS earned the top rating in our industry on the American Customer Satisfaction Index in 2011. As noted in Millward Brown's and Interbrand's top brand rankings, we have one of the most valuable brands in the world. UPS also has been named to industry leading positions in Fortune Magazine's Most Admired and Harris Interactive's Reputation Quotient surveys.

Employees

The strength of our company is our people, working together with a common purpose. We had approximately 398,000 employees as of December 31, 2011, of which 323,000 are in the U.S. and 75,000 are located internationally. Our global workforce includes approximately 71,000 management employees (36% of whom are part-time) and 327,000 hourly employees (46% of whom are part-time).

As of December 31, 2011, we had approximately 245,000 employees employed under a national master agreement and various supplemental agreements with local unions affiliated with the International Brotherhood of Teamsters ("Teamsters"). These agreements run through July 31, 2013.

We have approximately 2,700 pilots who are employed under a collective bargaining agreement with the Independent Pilots Association ("IPA"), which became amendable at the end of 2011.

Our airline mechanics are covered by a collective bargaining agreement with Teamsters Local 2727, which runs through November 1, 2013. In addition, approximately 3,200 of our ground mechanics who are not employed under agreements with the Teamsters are employed under collective bargaining agreements with the International Association of Machinists and Aerospace Workers ("IAM"). Our agreement with the IAM runs through July 31, 2014.

The experience of our management team continues to be an organizational strength. Nearly 40% of our full-time managers have more than 20 years of service with UPS.

9

We believe that our relations with our employees are good. We periodically survey all our employees to determine their level of job satisfaction. Areas of concern receive management attention as we strive to keep UPS the employer of choice among our employees. We consistently receive numerous awards and wide recognition as an employer-of-choice, resulting in part from our emphasis on diversity and corporate citizenship.

Safety

We promote safety throughout our operations. Our Automotive Fleet Safety Program is built with the following components:

| • | Selection. Five out of every six drivers come from our part-time ranks. Therefore, many of our new drivers are familiar with our philosophies, policies, practices and training programs. |

| • | Training. Training is the cornerstone of our Fleet Safety Program. Our approach starts with training the trainer. All trainers are certified to ensure that they have the skills and motivation to effectively train novice drivers. A new driver's employment includes extensive classroom and online training as well as on-road training, followed by three safety training rides integrated into his or her training cycle. |

| • | Responsibility. Our operations managers are responsible for their drivers' safety records. We investigate every accident. If we determine that an accident could have been prevented, we retrain the driver. |

| • | Preventive Maintenance. An integral part of our Fleet Safety Program is a comprehensive Preventive Maintenance Program. Our fleet is tracked electronically to ensure that each vehicle is serviced before a breakdown or accident is likely to occur. |

| • | Honor Plan. A well-defined safe driver honor plan recognizes and rewards our drivers when they achieve success. We have over 4,000 drivers who have driven for 25 years or more without an avoidable accident. |

Our workplace safety program is built upon a comprehensive health and safety process. The foundation of this process is our employee-management health and safety committees. The workplace safety process focuses on employee conditioning and safety-related habits. Our employee co-chaired health and safety committees complete comprehensive facility audits and injury analyses, and recommend facility and work process changes.

Competition

We are the largest package delivery company in the world, in terms of both revenue and volume. We offer a broad array of services in the package and freight delivery industry and, therefore, compete with many different local, regional, national and international companies. Our competitors include worldwide postal services, various motor carriers, express companies, freight forwarders, air couriers and others. Through our supply chain service offerings, we compete with a number of participants in the supply chain, financial services and information technology industries.

Competitive Strengths

Our competitive strengths include:

Integrated Global Network. We believe that our integrated global ground and air network is the most extensive in the industry. We handle all levels of service (air, ground, domestic, international, commercial, residential) through a single pickup and delivery service network.

Our sophisticated engineering systems allow us to optimize our network efficiency and asset utilization on a daily basis. This unique, integrated global business model creates consistent and superior returns.

10

We believe we have the most comprehensive integrated delivery and information services portfolio of any carrier in Europe. In other regions of the world, we rely on both our own and local service providers' capabilities to meet our service commitments.

Global Presence. UPS serves more than 220 countries and territories around the world. We have a presence in all of the world's major economies.

Leading-edge Technology. We are a global leader in developing technology that helps our customers optimize their shipping and logistics business processes to lower costs, improve service and increase efficiency.

Technology powers virtually every service we offer and every operation we perform. Our technology offerings are initiated by our customers' needs. We offer a variety of on-line service options that enable our customers to integrate UPS functionality into their own businesses not only to conveniently send, manage and track their shipments, but also to provide their customers with better information services. We provide the infrastructure for an Internet presence that extends to tens of thousands of customers who have integrated UPS tools directly into their own web sites.

Broad Portfolio of Services. Our portfolio of services enables customers to choose the delivery option that is most appropriate for their requirements. Increasingly, our customers benefit from business solutions that integrate many UPS services in addition to package delivery. For example, our supply chain services-such as freight forwarding, customs brokerage, order fulfillment, and returns management-help improve the efficiency of the supply chain management process.

Customer Relationships. We focus on building and maintaining long-term customer relationships. We serve 1.1 million pick-up customers and 7.7 million delivery customers daily. Cross-selling small package, supply chain and freight services across our customer base is an important growth mechanism for UPS.

Brand Equity. We have built a leading and trusted brand that stands for quality service, reliability and product innovation. The distinctive appearance of our vehicles and the friendliness and helpfulness of our drivers are major contributors to our brand equity.

Distinctive Culture. We believe that the dedication of our employees results in large part from our distinctive "employee-owner" concept. Our employee stock ownership tradition dates from 1927, when our founders, who believed that employee stock ownership was a vital foundation for successful business, first offered stock to employees. To facilitate employee stock ownership, we maintain several stock-based compensation programs.

Our long-standing policy of "promotion from within" complements our tradition of employee ownership, and this policy reduces the need for us to hire managers and executive officers from outside UPS. The majority of our management team began their careers as full-time or part-time hourly UPS employees, and have spent their entire careers with us. Many of our executive officers have more than 30 years of service with UPS and have accumulated a meaningful ownership stake in our company. Therefore, our executive officers have a strong incentive to effectively manage UPS, which benefits all our shareowners.

Financial Strength. Our balance sheet reflects financial strength that few companies can match. Our financial strength gives us the resources to achieve global scale; to invest in employee development, technology, transportation equipment and buildings; to pursue strategic opportunities that facilitate our growth; to service our obligations; and to return value to our shareowners in the form of dividends and share repurchases.

Government Regulation

Air Operations

The U.S. Department of Transportation ("DOT"), the Federal Aviation Administration ("FAA"), and the U.S. Department of Homeland Security, through the Transportation Security Administration ("TSA"), have

11

regulatory authority over United Parcel Service Co.'s ("UPS Airlines'") air transportation services. The Federal Aviation Act of 1958, as amended, is the statutory basis for DOT and FAA authority and the Aviation and Transportation Security Act of 2001, as amended, is the basis for TSA aviation security authority.

The DOT's authority primarily relates to economic aspects of air transportation, such as discriminatory pricing, non-competitive practices, interlocking relations and cooperative agreements. The DOT also regulates, subject to the authority of the President of the United States, international routes, fares, rates and practices, and is authorized to investigate and take action against discriminatory treatment of U.S. air carriers abroad. International operating rights for U.S. airlines are usually subject to bilateral agreement between the U.S. and foreign governments. UPS Airlines has international route operating rights granted by the DOT and we may apply for additional authorities when those operating rights are available and are required for the efficient operation of our international network. The efficiency and flexibility of our international air transportation network is dependent on DOT and foreign government regulations and operating restrictions.

The FAA's authority primarily relates to safety aspects of air transportation, including aircraft operating procedures, transportation of hazardous materials, record keeping standards and maintenance activities, personnel and ground facilities. In 1988, the FAA granted us an operating certificate, which remains in effect so long as we meet the safety and operational requirements of the applicable FAA regulations. In addition, we are subject to non-U.S. government regulation of aviation rights involving non-U.S. jurisdictions, and non-U.S. customs regulation.

FAA regulations mandate an aircraft corrosion control program, along with aircraft inspection and repair at periodic intervals specified by approved programs and procedures, for all aircraft. Our total expenditures under these programs for 2011 were not material. The future cost of repairs pursuant to these programs may fluctuate according to aircraft condition, age and the enactment of additional FAA regulatory requirements.

The TSA regulates various security aspects of air cargo transportation in a manner consistent with the TSA mission statement to "protect the Nation's transportation systems to ensure freedom of movement for people and commerce." UPS Airlines, and specified airport and off airport locations, are regulated under TSA regulations applicable to the transportation of cargo in an air network. In addition, personnel, facilities and procedures involved in air cargo transportation must comply with TSA regulations.

UPS Airlines, along with a number of other domestic airlines, participates in the Civil Reserve Air Fleet ("CRAF") program. Our participation in the CRAF program allows the U.S. Department of Defense ("DOD") to requisition specified UPS Airlines wide-body aircraft for military use during a national defense emergency. The DOD compensates us for the use of aircraft under the CRAF program. In addition, participation in CRAF entitles UPS Airlines to bid for military cargo charter operations.

Ground Operations

Our ground transportation of packages in the U.S. is subject to the DOT's jurisdiction with respect to the regulation of routes and to both the DOT's and the states' jurisdiction with respect to the regulation of safety, insurance and hazardous materials. We are subject to similar regulation in many non-U.S. jurisdictions.

The Postal Reorganization Act of 1970 created the U.S. Postal Service as an independent establishment of the executive branch of the federal government, and created the Postal Rate Commission, an independent agency, to recommend postal rates. The Postal Accountability and Enhancement Act of 2006 amended the 1970 Act to give the re-named Postal Regulatory Commission revised oversight authority over many aspects of the Postal Service, including postal rates, product offerings and service standards. We sometimes participate in the proceedings before the Postal Regulatory Commission in an attempt to secure fair postal rates for competitive services.

12

Customs

We are subject to the customs laws in the countries in which we operate, regarding the import and export of shipments, including those related to the filing of documents on behalf of client importers and exporters.

Environmental

We are subject to federal, state and local environmental laws and regulations across all of our business units. These laws and regulations cover a variety of processes, including, but not limited to: proper storage, handling, and disposal of hazardous and other waste; managing wastewater and stormwater; monitoring and maintaining the integrity of underground storage tanks; complying with laws regarding clean air, including those governing emissions; protecting against and appropriately responding to spills and releases; and communicating the presence of reportable quantities of hazardous materials to local responders. UPS has established site- and activity-specific environmental compliance and pollution prevention programs to address our environmental responsibilities and remain compliant. In addition, UPS has created numerous programs which seek to minimize waste and prevent pollution within our operations.

Other Regulations

We are subject to numerous other U.S. federal and state laws and regulations, in addition to applicable foreign laws, in connection with our package and non-package businesses in the countries in which we operate. These laws and regulations include those enforced by U.S. Customs and Border Protection and other agencies of the U.S. Department of Homeland Security, the U.S. Department of Treasury, the Federal Maritime Commission, the U.S. Drug Enforcement Administration, the U.S. Food and Drug Administration and the U.S. Department of Agriculture.

Where You Can Find More Information

UPS maintains a website at www.ups.com . Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) of the Securities Exchange Act of 1934 are made available through our website www.investors.ups.com as soon as reasonably practical after we electronically file or furnish the reports to the SEC. Also available on the Corporation's website are the Company's Corporate Governance Guidelines and Committee Charters. Information on these websites, however, is not incorporated by reference into this report or any other report filed with or furnished to the SEC.

We have adopted a written Code of Business Conduct that applies to all of our directors, officers and employees, including our principal executive officer and senior financial officers. It is available in the governance section of the investor relations website, located at www.investors.ups.com . In the event that we make changes in, or provide waivers from, the provisions of the Code of Business Conduct that the SEC requires us to disclose, we intend to disclose these events in the governance section of our investor relations website.

Our Corporate Governance Guidelines and the charters for our Audit Committee, Compensation Committee and Nominating and Corporate Governance Committee are also available in the governance section of the investor relations website.

Our sustainability report, which describes our activities that support our commitment to acting responsibly and contributing to society, is available at www.sustainability.ups.com . We provide the addresses to our internet sites solely for the information of investors. We do not intend any addresses to be active links or to otherwise incorporate the contents of any website into this report.

13

| Item 1A. | Risk Factors |

You should carefully consider the following factors, which could materially affect our business, financial condition or results of operations. You should read these Risk Factors in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Item 7 and our Consolidated Financial Statements and related notes in Item 8.

General economic conditions, both in the U.S. and internationally, may adversely affect our results of operations.

We conduct operations in over 220 countries and territories. Our U.S. and international operations are subject to normal cycles affecting the economy in general, as well as the local economic environments in which we operate. The factors that create cyclical changes to the economy and to our business are beyond our control, and it may be difficult for us to adjust our business model to mitigate the impact of these factors. In particular, our business is affected by levels of industrial production, consumer spending and retail activity, and our business, financial position and results of operations could be materially affected by adverse developments in these aspects of the economy.

We face significant competition which could adversely affect our business, financial position and results of operations.

We face significant competition on a local, regional, national and international basis. Our competitors include the postal services of the U.S. and other nations, various motor carriers, express companies, freight forwarders, air couriers and others. Competition may also come from other sources in the future. Some of our competitors have cost and organizational structures that differ from ours and may offer services and pricing terms that we may not be willing or able to offer. If we are unable to timely and appropriately respond to competitive pressures, our business, financial position and results of operations could be adversely affected.

The transportation industry continues to consolidate and competition remains strong. As a result of consolidation, our competitors may increase their market share and improve their financial capacity, and may strengthen their competitive positions. Business combinations could also result in competitors providing a wider variety of services and products at competitive prices, which could adversely affect our financial performance.

Our business is subject to complex and stringent regulation in the U.S. and internationally.

We are subject to complex and stringent aviation, transportation, environmental, security, labor, employment and other governmental laws and regulations, both in the U.S. and in the other countries in which we operate. In addition, our business is impacted by laws and regulations that affect global trade, including tariff and trade policies, export requirements, taxes and other restrictions and charges. Changes in laws, regulations and the related interpretations may alter the landscape in which we do business and may affect our costs of doing business. The impact of new laws and regulations cannot be predicted. Compliance with new laws and regulations may increase our operating costs or require significant capital expenditures. Any failure to comply with applicable laws or regulations in the U.S. or in any of the countries in which we operate could result in substantial fines or possible revocation of our authority to conduct our operations, which could adversely affect our financial performance.

Increased security requirements could impose substantial costs on us and we could be the target of an attack or have a security breach.

As a result of concerns about global terrorism and homeland security, governments around the world have adopted or may adopt stricter security requirements that will result in increased operating costs for businesses in

14

the transportation industry. These requirements may change periodically as a result of regulatory and legislative requirements and in response to evolving threats. We cannot determine the effect that these new requirements will have on our cost structure or our operating results, and these rules or other future security requirements may increase our costs of operations and reduce operating efficiencies. Regardless of our compliance with security requirements or the steps we take to secure our facilities or fleet, we could be the target of an attack or security breaches could occur, which could adversely affect our operations or our reputation.

We may be affected by global climate change or by legal, regulatory or market responses to such potential change.

Concern over climate change, including the impact of global warming, has led to significant federal, state and international legislative and regulatory efforts to limit greenhouse gas ("GHG") emissions. For example, in the past several years, the U.S. Congress has considered various bills that would regulate GHG emissions. While these bills have not yet received sufficient Congressional support for enactment, some form of federal climate change legislation is possible in the future. Even in the absence of such legislation, the Environmental Protection Agency, spurred by judicial interpretation of the Clean Air Act, may regulate GHG emissions, especially aircraft or diesel engine emissions, and this could impose substantial costs on us. These costs include an increase in the cost of the fuel and other energy we purchase and capital costs associated with updating or replacing our aircraft or vehicles prematurely. Until the timing, scope and extent of any future regulation becomes known, we cannot predict its effect on our cost structure or our operating results. It is reasonably possible that such legislation or regulation could impose material costs on us. Moreover, even without such legislation or regulation, increased awareness and any adverse publicity in the global marketplace about the GHGs emitted by companies in the airline and transportation industries could harm our reputation and reduce customer demand for our services, especially our air services.

Strikes, work stoppages and slowdowns by our employees could adversely affect our business, financial position and results of operations.

A significant number of our employees are employed under a national master agreement and various supplemental agreements with local unions affiliated with the Teamsters and our airline pilots, airline mechanics, ground mechanics and certain other employees are employed under other collective bargaining agreements. Strikes, work stoppages and slowdowns by our employees could adversely affect our ability to meet our customers' needs, and customers may do more business with competitors if they believe that such actions or threatened actions may adversely affect our ability to provide services. We may face permanent loss of customers if we are unable to provide uninterrupted service, and this could adversely affect our business, financial position and results of operations. The terms of future collective bargaining agreements also may affect our competitive position and results of operations.

We are exposed to the effects of changing prices of energy, including gasoline, diesel and jet fuel, and interruptions in supplies of these commodities.

Changing fuel and energy costs may have a significant impact on our operations. We require significant quantities of fuel for our aircraft and delivery vehicles and are exposed to the risk associated with variations in the market price for petroleum products, including gasoline, diesel and jet fuel. We mitigate our exposure to changing fuel prices through our indexed fuel surcharges and we may also enter into hedging transactions from time to time. If we are unable to maintain or increase our fuel surcharges, higher fuel costs could adversely impact our operating results. Even if we are able to offset the cost of fuel with our surcharges, high fuel surcharges may result in a mix shift from our higher yielding air products to lower yielding ground products or an overall reduction in volume. If fuel prices rise sharply, even if we are successful in increasing our fuel surcharge, we could experience a lag time in implementing the surcharge, which could adversely affect our short-term operating results. There can be no assurance that our hedging transactions will be effective to protect us

15

from changes in fuel prices. Moreover, we could experience a disruption in energy supplies, including our supply of gasoline, diesel and jet fuel, as a result of war, actions by producers, or other factors which are beyond our control, which could have an adverse effect on our business.

Changes in exchange rates or interest rates may have an adverse effect on our results.

We conduct business across the globe with a significant portion of our revenue derived from operations outside the United States. Our operations in international markets are affected by changes in the exchange rates for local currencies, and in particular the Euro, British Pound Sterling and Canadian Dollar.

We are exposed to changes in interest rates, primarily on our short-term debt and that portion of our long-term debt that carries floating interest rates. The impact of a 100-basis-point change in interest rates affecting our debt is discussed in the "Quantitative and Qualitative Disclosures about Market Risk" section of this report.

We monitor and manage our exposures to changes in currency exchange rates and interest rates, and make limited use of currency exchange contracts, over the counter option contracts, commodity forwards, swaps and futures contracts to mitigate the impact of changes in currency values, but changes in exchange rates and interest rates cannot always be predicted or hedged.

If we are unable to maintain our brand image and corporate reputation, our business may suffer.

Our success depends in part on our ability to maintain the image of the UPS brand and our reputation for providing excellent service to our customers. Service quality issues, actual or perceived, even when false or unfounded, could tarnish the image of our brand and may cause customers to use other companies. Also, adverse publicity surrounding labor relations, environmental concerns, security matters, political activities and the like, or attempts to connect our company to these sorts of issues, either in the United States or other countries in which we operate, could negatively affect our overall reputation and acceptance of our services by customers. Damage to our reputation and loss of brand equity could reduce demand for our services and thus have an adverse effect on our business, financial position and results of operations, and could require additional resources to rebuild our reputation and restore the value of our brand.

A significant privacy breach or IT system disruption could adversely affect our business and we may be required to increase our spending on data and system security.

We rely on information technology networks and systems, including the Internet, to process, transmit and store electronic information, and to manage or support a variety of business processes and activities. In addition, the provision of service to our customers and the operation of our network involve the storage and transmission of proprietary information and sensitive or confidential data, including personal information of customers, employees and others. Our information technology systems, some of which are managed by third-parties, may be susceptible to damage, disruptions or shutdowns due to failures during the process of upgrading or replacing software, databases or components thereof, power outages, hardware failures, computer viruses, attacks by computer hackers, telecommunication failures, user errors or catastrophic events. Groups of hackers may also act in a coordinated manner to launch distributed denial of service attacks or other coordinated attacks that may cause service outages or other interruptions. In addition, breaches in security could expose us, our customers or the individuals affected to a risk of loss or misuse of proprietary information and sensitive or confidential data. Any of these occurrences could result in disruptions in our operations, the loss of existing or potential customers, damage to our brand and reputation, and litigation and potential liability for the company. In addition, the cost and operational consequences of implementing further data or system protection measures could be significant.

Severe weather or other natural or manmade disasters could adversely affect our business.

Severe weather conditions and other natural or manmade disasters, including storms, floods, fires and earthquakes, may result in decreased revenues, as our customers reduce their shipments, or increased costs to

16

operate our business, which could have an adverse effect on our results of operations for a quarter or year. Any such event affecting one of our major facilities could result in a significant interruption in or disruption of our business.

We make significant capital investments in our business of which a significant portion is tied to projected volume levels.

We require significant capital investments in our business consisting of aircraft, vehicles, technology, facilities and sorting and other types of equipment to support both our existing business and anticipated growth. Forecasting projected volume involves many factors which are subject to uncertainty, such as general economic trends, changes in governmental regulation and competition. If we do not accurately forecast our future capital investment needs, we could have excess capacity or insufficient capacity, either of which would negatively affect our revenues and profitability. In addition to forecasting our capital investment requirements, we adjust other elements of our operations and cost structure in response to adverse economic conditions; however, these adjustments may not be sufficient to allow us to maintain our operating margins in an adverse economy.

We derive a significant portion of our revenues from our international operations and are subject to the risks of doing business in emerging markets.

We have significant international operations and while the geographical diversity of our international operations helps ensure that we are not overly reliant on a single region or country, we are continually exposed to changing economic, political and social developments beyond our control. Emerging markets are typically more volatile than those in the developed world, and any broad-based downturn in these markets could reduce our revenues and adversely affect our business, financial position and results of operations.

We are subject to changes in markets and our business plans that have resulted, and may in the future result, in substantial write-downs of the carrying value of our assets, thereby reducing our net income.

Our regular review of the carrying value of our assets has resulted, from time to time, in significant impairments, and we may in the future be required to recognize additional impairment charges. Changes in business strategy, government regulations, or economic or market conditions have resulted and may result in further substantial impairments of our intangible or other assets at any time in the future. In addition, we have been and may be required in the future to recognize increased depreciation and amortization charges if we determine that the useful lives of our fixed assets are shorter than we originally estimated. Such changes could reduce our net income.

Employee health and retiree health and pension benefit costs represent a significant expense to us.

With approximately 398,000 employees, including approximately 323,000 in the U.S., our expenses relating to employee health and retiree health and pension benefits are significant. In recent years, we have experienced significant increases in certain of these costs, largely as a result of economic factors beyond our control, including, in particular, ongoing increases in health care costs well in excess of the rate of inflation. Continued increasing health care costs, volatility in investment returns and discount rates, as well as changes in laws, regulations and assumptions used to calculate retiree health and pension benefit expenses, may adversely affect our business, financial position, results of operations or require significant contributions to our pension plans.

We participate in a number of trustee-managed multiemployer pension and health and welfare plans for employees covered under collective bargaining agreements. Several factors could cause us to make significantly higher future contributions to these plans, including unfavorable investment performance, increases in health care costs, changes in demographics and increased benefits to participants. At this time, we are unable to determine the amount of additional future contributions, if any, or whether any material adverse effect on our financial condition, results of operations or liquidity could result from our participation in these plans.

17

We may be subject to various claims and lawsuits that could result in significant expenditures.

The nature of our business exposes us to the potential for various claims and litigation related to labor and employment, personal injury, property damage, business practices, environmental liability and other matters. Any material litigation or a catastrophic accident or series of accidents could have a material adverse effect on our business, financial position and results of operations.

We may not realize the anticipated benefits of acquisitions, joint ventures or strategic alliances.

As part of our business strategy, we may acquire businesses and form joint ventures or strategic alliances. Whether we realize the anticipated benefits from these transactions depends, in part, upon the successful integration between the businesses involved, the performance of the underlying operation, capabilities or technologies and the management of the transacted operations. Accordingly, our financial results could be adversely affected by our failure to effectively integrate the acquired operations, unanticipated performance issues, transaction-related charges or charges for impairment of long-term assets that we acquire.

Insurance and claims expenses could have a material adverse effect on our business, financial condition and results of operations.

We have a combination of both self-insurance and high-deductible insurance programs for the risks arising out of the services we provide and the nature of our global operations, including claims exposure resulting from cargo loss, personal injury, property damage, aircraft and related liabilities, business interruption and workers' compensation. Workers' compensation, automobile and general liabilities are determined using actuarial estimates of the aggregate liability for claims incurred and an estimate of incurred but not reported claims, on an undiscounted basis. Our accruals for insurance reserves reflect certain actuarial assumptions and management judgments, which are subject to a high degree of variability. If the number or severity of claims for which we are retaining risk increases, our financial condition and results of operations could be adversely affected. If we lose our ability to self-insure these risks, our insurance costs could materially increase and we may find it difficult to obtain adequate levels of insurance coverage.

| Item 1B. | Unresolved Staff Comments |

Not applicable.

| Item 2. | Properties |

Operating Facilities

We own our headquarters, which are located in Atlanta, Georgia and consist of about 735,000 square feet of office space on an office campus, and our UPS Supply Chain Solutions group's headquarters, which are located in Alpharetta, Georgia, and consist of about 310,000 square feet of office space.

We also own our 27 principal U.S. package operating facilities, which have floor spaces that range from approximately 310,000 to 693,000 square feet. In addition, we have a 1.9 million square foot operating facility near Chicago, Illinois, which is designed to streamline shipments between East Coast and West Coast destinations, and we own or lease over 1,000 additional smaller package operating facilities in the U.S. The smaller of these facilities have vehicles and drivers stationed for the pickup of packages and facilities for the sorting, transfer and delivery of packages. The larger of these facilities also service our vehicles and equipment and employ specialized mechanical installations for the sorting and handling of packages.

We own or lease almost 800 facilities that support our international package operations and an additional 800 facilities that support our freight forwarding and logistics operations. Our freight forwarding and logistics operations maintain facilities with approximately 35 million square feet of floor space. We own and operate a logistics campus consisting of approximately 3.1 million square feet in Louisville, Kentucky.

18

UPS Freight operates 196 service centers with a total of 5.9 million square feet of floor space. UPS Freight owns 148 of these service centers, while the remainder are occupied under operating lease agreements. The main offices of UPS Freight are located in Richmond, Virginia and consist of about 240,000 square feet of office space.

Our aircraft are operated in a hub and spokes pattern in the U.S. Our principal air hub in the U.S., known as Worldport, is located in Louisville, Kentucky. The Worldport facility consists of over 5.2 million square feet and the site includes approximately 596 acres. Between 2009 and 2010, we completed an expansion of our Worldport facility, which increased the sorting capacity to approximately 416,000 packages per hour. The expansion, which cost over $1 billion, involved the addition of two aircraft load / unload wings to the hub building, followed by the installation of high-speed conveyor and computer control systems.

We also have regional air hubs in Hartford, Connecticut; Ontario, California; Philadelphia, Pennsylvania; and Rockford, Illinois. These hubs house facilities for the sorting, transfer and delivery of packages. Our European air hub is located in Cologne, Germany, and we maintain Asia-Pacific air hubs in Shanghai, China; Shenzhen, China; Taipei, Taiwan; Hong Kong; and Singapore. Our regional air hub in Canada is located in Hamilton, Ontario, and our regional air hub for Latin America and the Caribbean is in Miami, Florida.