UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

FORM 10-K

(Mark One) |

|

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 1, 2014 | |

OR | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | |

Commission file number 1-6049

|

TARGET CORPORATION

(Exact name of registrant as specified in its charter)

|

|

|

Minnesota (State or other jurisdiction of incorporation or organization) |

| 41-0215170 (I.R.S. Employer Identification No.) |

1000 Nicollet Mall, Minneapolis, Minnesota (Address of principal executive offices) |

| 55403 (Zip Code) |

Registrant's telephone number, including area code: 612/304-6073

Securities Registered Pursuant To Section 12(B) Of The Act:

|

|

|

Title of Each Class |

| Name of Each Exchange on Which Registered |

Common Stock, par value $0.0833 per share |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by checkmark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files. Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Rule 12b-2 of the Act).

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

Aggregate market value of the voting stock held by non-affiliates of the registrant on August 3, 2013 was 45,036,171,526 , based on the closing price of $71.50 per share of Common Stock as reported on the New York Stock Exchange Composite Index.

Indicate the number of shares outstanding of each of registrant's classes of Common Stock, as of the latest practicable date. Total shares of Common Stock, par value $0.0833, outstanding at March 10, 2014 were 633,174,692.

DOCUMENTS INCORPORATED BY REFERENCE

1. Portions of Target's Proxy Statement to be filed on or about April 28, 2014 are incorporated into Part III.

TABLE OF CONTENTS

PART I |

| | ||

Item 1 |

| Business | 2 | |

Item 1A |

| Risk Factors | 5 | |

Item 1B |

| Unresolved Staff Comments | 10 | |

Item 2 |

| Properties | 11 | |

Item 3 |

| Legal Proceedings | 12 | |

Item 4 |

| Mine Safety Disclosures | 12 | |

Item 4A |

| Executive Officers | 12 | |

PART II |

| |||

Item 5 |

| Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 14 | |

Item 6 |

| Selected Financial Data | 16 | |

Item 7 |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 16 | |

Item 7A |

| Quantitative and Qualitative Disclosures About Market Risk | 31 | |

Item 8 |

| Financial Statements and Supplementary Data | 33 | |

Item 9 |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 65 | |

Item 9A |

| Controls and Procedures | 65 | |

Item 9B |

| Other Information | 65 | |

PART III |

| |||

Item 10 |

| Directors, Executive Officers and Corporate Governance | 65 | |

Item 11 |

| Executive Compensation | 66 | |

Item 12 |

| Security Ownership of Certain Beneficial Owners and Management and | 66 | |

Item 13 |

| Certain Relationships and Related Transactions, and Director Independence | 66 | |

Item 14 |

| Principal Accountant Fees and Services | 66 | |

PART IV |

| |||

Item 15 |

| Exhibits and Financial Statement Schedules | 67 | |

Signatures | 71 | | ||

Exhibit Index | 72 | | ||

Exhibit 12 – Computations of Ratios of Earnings to Fixed Charges for each of the Five Years in the Period Ended February 1, 2014 | 74 | | ||

1

PART I

Item 1. Business

General

Target Corporation (Target, the Corporation or the Company) was incorporated in Minnesota in 1902. We offer our customers, referred to as "guests," both everyday essentials and fashionable, differentiated merchandise at discounted prices. Our ability to deliver a preferred shopping experience to our guests is supported by our strong supply chain and technology infrastructure, a devotion to innovation that is ingrained in our organization and culture, and our disciplined approach to managing our business and investing in future growth.

We operate as two reportable segments: U.S. and Canadian. Our U.S. Segment includes all of our U.S. retail operations, which are designed to enable guests to purchase products seamlessly in stores, online or through mobile devices. The U.S. Segment also includes our credit card servicing activities and certain centralized operating and corporate activities not allocated to our Canadian Segment. Our Canadian Segment includes all of our Canadian retail operations, including 124 stores opened during 2013. We currently do not have a digital sales channel within our Canadian Segment.

Prior to the first quarter of 2013, we operated a U.S. Credit Card Segment that offered credit to qualified guests through our branded credit cards: the Target Credit Card and the Target Visa Credit Card. In the first quarter of 2013, we sold our U.S. consumer credit card portfolio, and TD Bank Group (TD) now underwrites, funds and owns Target Credit Card and Target Visa consumer receivables in the U.S. We perform account servicing and primary marketing functions and earn a substantial portion of the profits generated by the portfolio. Following the sale of our U.S. consumer credit card portfolio to TD, we combined our historical U.S. Retail Segment and U.S. Credit Card Segment into one U.S. Segment. Refer to Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, and Note 6 of the Consolidated Financial Statements included in Item 8, Financial Statements and Supplementary Data, for more information on the credit card receivables transaction and segment change.

Data Breach

During the fourth quarter of 2013, we experienced a data breach in which an intruder stole certain payment card and other guest information from our network (the Data Breach). For further information about the Data Breach, see Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations.

Financial Highlights

For information about our fiscal years, see Item 8, Financial Statements and Supplemental Data - Note 1, Summary of Accounting Policies, of this Annual Report on Form 10-K.

For information on key financial highlights and segment financial information, see the items referenced in Item 6, Selected Financial Data, Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations and Item 8, Financial Statements and Supplemental Data - Note 28, Segment Reporting, of this Annual Report on Form 10-K.

Seasonality

A larger share of annual revenues and earnings traditionally occurs in the fourth quarter because it includes the peak sales period from Thanksgiving to the end of December.

Merchandise

We sell a wide assortment of general merchandise and food. Our general merchandise and CityTarget stores offer an edited food assortment, including perishables, dry grocery, dairy and frozen items, while our SuperTarget stores offer a full line of food items comparable to traditional supermarkets. Our digital channels include a wide assortment of general merchandise, including many items found in our stores and a complementary assortment, such as extended sizes and colors, that are only sold online.

2

A significant portion of our sales is from national brand merchandise. Approximately one-third of 2013 sales related to our owned and exclusive brands, including but not limited to the following:

Owned Brands |

|

|

Archer Farms® | Gilligan & O'Malley® | Sutton & Dodge® |

Simply Balanced™ | Market Pantry® | Threshold™ |

Boots & Barkley® | Merona® | up & up® |

CHEFS® | Room Essentials® | Wine Cube® |

Circo® | Smith & Hawken® | Xhilaration® |

Embark® | Spritz™ |

|

|

|

|

Exclusive Brands |

|

|

Assets® by Sarah Blakely | Genuine Kids from OshKosh® | Nate Berkus for Target® |

C9 by Champion® | Giada De Laurentiis™ for Target® | Nick & Nora® |

Carlton® | Harajuku Mini for Target® | Shaun White |

Chefmate® | Just One You made by Carter's | Simply Shabby Chic® |

Cherokee® | Kid Made Modern® | Sonia Kashuk® |

Converse® One Star® | Kitchen Essentials® from Calphalon® | Thomas O'Brien® |

dENiZEN™ from Levi's® | Liz Lange® for Target |

|

Fieldcrest® | Mossimo Supply Company® |

|

We also sell merchandise through periodic exclusive design and creative partnerships, and also generate revenue from in-store amenities such as Target Café, Target Clinic, Target Pharmacy and Target Photo, and leased or licensed departments such as Target Optical, Pizza Hut, Portrait Studio and Starbucks.

Distribution

The vast majority of merchandise is distributed to our stores through our network of 40 distribution centers, 37 in the United States and 3 in Canada. General merchandise is shipped to and from our distribution centers by common carriers. Certain food items and other merchandise is shipped directly to our stores in the U.S. and Canada by vendors or third party distributors.

Employees

At February 1, 2014 , we employed approximately 366,000 full-time, part-time and seasonal employees, referred to as "team members." During our peak sales period from Thanksgiving to the end of December, our employment levels peaked at approximately 416,000 team members. We offer a broad range of company-paid benefits to our team members. Eligibility for, and the level of, these benefits varies, depending on team members' full-time or part-time status, compensation level, date of hire and/or length of service. These company-paid benefits include a pension plan,

401(k) plan, medical and dental plans, a retiree medical plan, disability insurance, paid vacation, tuition reimbursement, various team member assistance programs, life insurance and merchandise discounts. We believe our team member relations are good.

Working Capital

Our working capital needs are greater in the months leading up to our peak sales period from Thanksgiving to the end of December, which we typically finance with cash flow provided by operations and short-term borrowings. Additional details are provided in the Liquidity and Capital Resources section in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations.

Effective inventory management is key to our ongoing success. We use various techniques including demand forecasting and planning and various forms of replenishment management. We achieve effective inventory management by being in-stock in core product offerings, maintaining positive vendor relationships, and carefully planning inventory levels for seasonal and apparel items to minimize markdowns.

3

Competition

We compete with traditional and off-price general merchandise retailers, apparel retailers, internet retailers, wholesale clubs, category specific retailers, drug stores, supermarkets and other forms of retail commerce. Our ability to positively differentiate ourselves from other retailers and provide a compelling value proposition largely determine our competitive position within the retail industry.

Intellectual Property

Our brand image is a critical element of our business strategy. Our principal trademarks, including Target, SuperTarget and our "Bullseye Design," have been registered with the U.S. Patent and Trademark Office. We also seek to obtain and preserve intellectual property protection for our owned brands.

Geographic Information

The vast majority of our revenues are generated within the United States. During 2013, a modest percentage of our revenues were generated in Canada. The vast majority of our long-lived assets are located within the United States and Canada.

Available Information

Our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act are available free of charge at www.Target.com/Investors as soon as reasonably practicable after we file such material with, or furnish it to, the U.S. Securities and Exchange Commission (SEC). Our Corporate Governance Guidelines, Business Conduct Guide, Corporate Responsibility Report and the position descriptions for our Board of Directors and Board committees are also available free of charge in print upon request or at www.Target.com/Investors.

4

Item 1A. Risk Factors

Our business is subject to many risks. Set forth below are the most significant risks that we face.

If we are unable to positively differentiate ourselves from other retailers, our results of operations could be adversely affected.

The retail business is highly competitive. In the past we have been able to compete successfully by differentiating our guests' shopping experience by creating an attractive value proposition through a careful combination of price, merchandise assortment, convenience, guest service, loyalty programs and marketing efforts. Our ability to create a personalized guest experience through the collection and use of guest data is increasingly important to our ability to differentiate from other retailers. Guest perceptions regarding the cleanliness and safety of our stores, the functionality and reliability of our digital channels, our in-stock levels and other factors also affect our ability to compete. No single competitive factor is dominant, and actions by our competitors on any of these factors could have an adverse effect on our sales, gross margins and expenses.

We sell many products under our owned and exclusive brands. These brands are an important part of our business because they differentiate us from other retailers, generally carry higher margins than equivalent national brand products and represent a significant portion of our overall sales. If one or more of these brands experiences a loss of consumer acceptance or confidence, our sales and gross margins could be adversely affected.

The continuing migration and evolution of retailing to online and mobile channels has increased our challenges in differentiating ourselves from other retailers. In particular, consumers are able to quickly and conveniently comparison shop with digital tools, which can lead to decisions based solely on price. We work with our vendors to offer unique and distinctive merchandise, and encourage our guests to shop with confidence with our price match policy. Failure to effectively execute in these efforts, actions by our competitors in response to these efforts or failures of our vendors to manage their own channels and content could hurt our ability to differentiate ourselves from other retailers and, as a result, have an adverse effect on sales, gross margins and expenses.

Our continued success is substantially dependent on positive perceptions of Target which, if eroded, could adversely affect our business and our relationships with our guests and team members.

We believe that one of the reasons our guests prefer to shop at Target and our team members choose Target as a place of employment is the reputation we have built over many years for serving our four primary constituencies: guests, team members, the communities in which we operate, and shareholders. To be successful in the future, we must continue to preserve, grow and leverage the value of Target's reputation. Reputational value is based in large part on perceptions. While reputations may take decades to build, any negative incidents can quickly erode trust and confidence, particularly if they result in adverse mainstream and social media publicity, governmental investigations or litigation. Those types of incidents could have an adverse impact on perceptions and lead to tangible adverse effects on our business, including consumer boycotts, lost sales, loss of new store development opportunities, or team member retention and recruiting difficulties. For example, we experienced weaker than expected U.S. Segment sales following the announcement of the Data Breach and are unable to determine whether there will be a long-term impact to our relationship with our guests and whether we will need to engage in significant promotional or other activities to regain their trust .

If we are unable to successfully develop and maintain a relevant and reliable multichannel experience for our guests, our sales, results of operations and reputation could be adversely affected.

Our business has evolved from an in-store experience to interaction with guests across multiple channels (in-store, online, mobile and social media, among others). Our guests are using computers, tablets, mobile phones and other devices to shop in our stores and online and provide feedback and public commentary about all aspects of our business. We currently provide full and mobile versions of our website (Target.com), applications for mobile phones and tablets and interact with our guests through social media. Multichannel retailing is rapidly evolving and we must keep pace with changing guest expectations and new developments and technology investments by our competitors. If we are unable to attract and retain team members or contract with third parties having the specialized skills needed to support our multichannel efforts, implement improvements to our guest‑facing technology in a timely manner, or provide a convenient and consistent experience for our guests regardless of the ultimate sales channel, our ability to compete and our results of operations could be adversely affected. In addition, if Target.com and our other guest‑facing technology systems do not appeal to our guests or reliably function as designed, we may experience a loss of guest

5

confidence, lost sales or be exposed to fraudulent purchases, which, if significant, could adversely affect our reputation and results of operations.

If we fail to anticipate and respond quickly to changing consumer preferences, our sales, gross margins and profitability could suffer.

A substantial part of our business is dependent on our ability to make trend‑right decisions and effectively manage our inventory in a broad range of merchandise categories, including apparel, home décor, seasonal offerings, food and other merchandise. Failure to accurately predict constantly changing consumer tastes, preferences, spending patterns and other lifestyle decisions, and personalize our offerings to our guests may result in lost sales, spoilage and increased inventory markdowns, which would lead to a deterioration in our results of operations by hurting our sales, gross margins and profitability.

Our earnings are highly susceptible to the state of macroeconomic conditions and consumer confidence in the United States.

Most of our stores and all of our digital sales are in the United States, making our results highly dependent on U.S. consumer confidence and the health of the U.S. economy. In addition, a significant portion of our total sales is derived from stores located in five states: California, Texas, Florida, Minnesota and Illinois, resulting in further dependence on local economic conditions in these states. Deterioration in macroeconomic conditions or consumer confidence could negatively affect our business in many ways, including slowing sales growth or reduction in overall sales, and reducing gross margins. These same considerations impact the success of our credit card program. Even though we no longer own a consumer credit card receivables portfolio, we share in the economic performance of the credit card program with TD. Deterioration in macroeconomic conditions could adversely affect the volume of new credit accounts, the amount of credit card program balances and the ability of credit card holders to pay their balances. These conditions could result in us receiving lower profit‑sharing payments.

We rely on a large, global and changing workforce of Target team members, contractors and temporary staffing. If we do not effectively manage our workforce and the concentration of work in certain global locations, our labor costs and results of operations could be adversely affected.

With approximately 366,000 team members, our workforce costs represent our largest operating expense, and our business is dependent on our ability to attract, train and retain the appropriate mix of qualified team members, contractors and temporary staffing. Many team members are in entry-level or part-time positions with historically high turnover rates. Our ability to meet our labor needs while controlling our costs is subject to external factors such as unemployment levels, prevailing wage rates, collective bargaining efforts, health care and other benefit costs and changing demographics. If we are unable to attract and retain adequate numbers and an appropriate mix of qualified team members, contractors and temporary staffing, our operations, guest service levels and support functions could suffer. Those factors, together with increasing wage and benefit costs, could adversely affect our results of operations. As of March 14, 2014, none of our team members were working under collective bargaining agreements. We are periodically subject to labor organizing efforts. If we become subject to one or more collective bargaining agreements in the future, it could adversely affect our labor costs and how we operate our business.

We have a concentration of support functions located in India where there has been greater political, financial, environmental and health instability than the United States. An extended disruption of our operations in India could adversely affect certain operations supporting stability and maintenance of our digital channels and information technology development.

If our capital investments in technology, new stores and remodeling existing stores do not achieve appropriate returns, our competitive position, financial condition and results of operations may be adversely affected.

Our business is becoming increasingly reliant on technology investments and the returns on these investments are less predictable than building new stores and remodeling existing stores. We are currently making, and will continue to make, significant technology investments to support our multichannel efforts, implement improvements to our guest‑facing technology and transform our information processes and computer systems to more efficiently run our business and remain competitive and relevant to our guests. These technology initiatives might not provide the anticipated benefits or may provide them on a delayed schedule or at a higher cost. We must monitor and choose the right investments and implement them at the right pace. Targeting the wrong opportunities, failing to make the best

6

investments, or making an investment commitment significantly above or below our needs could result in the loss of our competitive position and adversely impact our financial condition or results of operations.

In addition, our growth also depends, in part, on our ability to build new stores and remodel existing stores in a manner that achieves appropriate returns on our capital investment. We compete with other retailers and businesses for suitable locations for our stores. Many of our expected new store sites are located in fully developed markets, which are generally more time-consuming and expensive undertakings than expansion into undeveloped suburban and ex-urban markets.

Interruptions in our supply chain or increased commodity prices and supply chain costs could adversely affect our gross margins, expenses and results of operations.

We are dependent on our vendors to supply merchandise in a timely and efficient manner. If a vendor fails to deliver on its commitments, whether due to financial difficulties or other reasons, we could experience merchandise out-of-stocks that could lead to lost sales. In addition, a large portion of our merchandise is sourced, directly or indirectly, from outside the United States, with China as our single largest source. Political or financial instability, trade restrictions, the outbreak of pandemics, labor unrest, transport capacity and costs, port security, weather conditions, natural disasters or other events that could slow port activities and affect foreign trade are beyond our control and could disrupt our supply of merchandise and/or adversely affect our results of operations. In addition, changes in the costs of procuring commodities used in our merchandise or the costs related to our supply chain, including vendor costs, labor, fuel, tariffs, currency exchange rates and supply chain transparency initiatives, could have an adverse effect on gross margins, expenses and results of operations.

Failure to address product safety concerns could adversely affect our sales and results of operations.

If our merchandise offerings, including food, drug and children's products, do not meet applicable safety standards or our guests' expectations regarding safety, we could experience lost sales and increased costs and be exposed to legal and reputational risk. All of our vendors must comply with applicable product safety laws, and we are dependent on them to ensure that the products we buy comply with all safety standards. Events that give rise to actual, potential or perceived product safety concerns, including food or drug contamination, could expose us to government enforcement action or private litigation and result in costly product recalls and other liabilities. In addition, negative guest perceptions regarding the safety of the products we sell could cause our guests to seek alternative sources for their needs, resulting in lost sales. In those circumstances, it may be difficult and costly for us to regain the confidence of our guests.

The data breach we experienced in 2013 has resulted in government inquiries and private litigation, and if our efforts to protect the security of information about our guests and team members are unsuccessful, future issues may result in additional costly government enforcement actions and private litigation and our sales and reputation could suffer.

The nature of our business involves the receipt and storage of information about our guests and team members. We have a program in place to detect and respond to data security incidents. However, because the techniques used to obtain unauthorized access, disable or degrade service, or sabotage systems change frequently and may be difficult to detect for long periods of time, we may be unable to anticipate these techniques or implement adequate preventive measures. In addition, hardware, software or applications we develop or procure from third parties may contain defects in design or manufacture or other problems that could unexpectedly compromise information security. Unauthorized parties may also attempt to gain access to our systems or facilities through fraud, trickery or other forms of deceiving our team members, contractors and temporary staff. Until the fourth quarter of 2013, all incidents we experienced were insignificant. The Data Breach we experienced was significant and went undetected for several weeks. We experienced weaker than expected U.S. Segment sales immediately following the announcement of the Data Breach, and we are currently facing more than 80 civil lawsuits filed on behalf of guests, payment card issuing banks and shareholders. In addition, state and federal agencies, including State Attorneys General, the Federal Trade Commission and the SEC, are investigating events related to the Data Breach, including how it occurred, its consequences and our responses. Those claims and investigations may have an adverse effect on how we operate our business and our results of operations.

If we experience additional significant data security breaches or fail to detect and appropriately respond to significant data security breaches, we could be exposed to additional government enforcement actions and private litigation. In addition, our guests could further lose confidence in our ability to protect their information, which could cause them to discontinue using our REDcards or pharmacy services, or stop shopping with us altogether.

7

Our failure to comply with federal, state, local and international laws, or changes in these laws could increase our costs, reduce our margins and lower our sales.

Our business is subject to a wide array of laws and regulations in the United States, Canada and other countries in which we operate. Significant workforce-related legislative changes could increase our expenses and adversely affect our operations. Examples of possible workforce-related legislative changes include changes to an employer's obligation to recognize collective bargaining units, the process by which collective bargaining agreements are negotiated or imposed, minimum wage requirements, and health care mandates. In addition, changes in the regulatory environment affecting Medicare reimbursements, privacy and information security, product safety, supply chain transparency, or environmental protection, among others, could cause our expenses to increase without an ability to pass through any increased expenses through higher prices. For example, we are currently facing government inquiries related to the Data Breach that may result in the imposition of fines or other penalties. In addition, any legislative or regulatory changes adopted in reaction to the recent retail-industry data breaches could increase or accelerate our compliance costs. Also, our pharmacy and clinic operations are governed by various regulations, and a significant change in, or our noncompliance with, these regulations could have a material adverse effect on our compliance costs and results of operations. In addition, if we fail to comply with other applicable laws and regulations, including wage and hour laws, the Foreign Corrupt Practices Act and local anti-bribery laws, we could be subject to legal risk, including government enforcement action and class action civil litigation, which could adversely affect our results of operations by increasing our costs, reducing our margins and lowering our sales.

Weather conditions where our stores are located may impact consumer shopping patterns, which alone or together with natural disasters, particularly in areas where our sales are concentrated, could adversely affect our results of operations.

Uncharacteristic or significant weather conditions can affect consumer shopping patterns, particularly in apparel and seasonal items, which could lead to lost sales or greater than expected markdowns and adversely affect our short-term results of operations. In addition, our three largest states by total sales are California, Texas and Florida, areas where natural disasters are more prevalent. Natural disasters in those states or in other areas where our sales are concentrated could result in significant physical damage to or closure of one or more of our stores or distribution centers, and cause delays in the distribution of merchandise from our vendors to our distribution centers and stores, which could adversely affect our results of operations by increasing our costs and lowering our sales.

Changes in our effective income tax rate could adversely affect our net income.

A number of factors influence our effective income tax rate, including changes in tax law, tax treaties, interpretation of existing laws, and our ability to sustain our reporting positions on examination. Changes in any of those factors could change our effective tax rate, which could adversely affect our net income. In addition, our operations outside of the United States may cause greater volatility in our effective tax rate.

If we are unable to access the capital markets or obtain bank credit, our financial position, liquidity and results of operations could suffer.

We are dependent on a stable, liquid and well-functioning financial system to fund our operations and capital investments. In particular, we have historically relied on the public debt markets to fund portions of our capital investments and the commercial paper market and bank credit facilities to fund seasonal needs for working capital. Our continued access to these markets depends on multiple factors including the condition of debt capital markets, our operating performance and maintaining strong debt ratings. If rating agencies lower our credit ratings, it could adversely impact our ability to access the debt markets, our cost of funds and other terms for new debt issuances. Each of the credit rating agencies reviews its rating periodically, and there is no guarantee our current credit rating will remain the same. In addition, we use a variety of derivative products to manage our exposure to market risk, principally interest rate and equity price fluctuations. Disruptions or turmoil in the financial markets could reduce our ability to meet our capital requirements or fund our working capital needs, and lead to losses on derivative positions resulting from counterparty failures, which could adversely affect our financial position and results of operations.

A significant disruption in our computer systems and our inability to adequately maintain and update those systems could adversely affect our operations and our ability to maintain guest confidence.

We rely extensively on our computer systems to manage inventory, process guest transactions, manage guest data, communicate with our vendors and other third parties, service REDcard accounts and summarize and analyze results, and on continued and unimpeded access to the internet to use our computer systems. Our systems are subject to

8

damage or interruption from power outages, telecommunications failures, computer viruses and malicious attacks, security breaches and catastrophic events. If our systems are damaged or fail to function properly, we may incur substantial repair or replacement costs, experience data loss and impediments to our ability to manage inventories or process guest transactions, and encounter lost guest confidence, which could adversely affect our results of operations. The Data Breach we experienced negatively impacted our ability to timely handle customer inquiries, and we experienced weaker than expected U.S. Segment sales following the announcement of the Data Breach.

We continually make significant technology investments that will help maintain and update our existing computer systems. Implementing significant system changes increases the risk of computer system disruption. Additionally, the potential problems and interruptions associated with implementing technology initiatives could disrupt or reduce our operational efficiency, and could impact the guest experience and guest confidence.

If we do not positively differentiate the Target experience and appeal to our new Canadian guests, our financial results could be adversely affected.

In fiscal 2013 we opened 124 Target stores in Canada, which was our first retail store expansion outside of the United States. Our initial sales and operating results in Canada have not met our initial expectations. Improving our sales in Canada is contingent on our ability to deploy new marketing programs that positively differentiate us from other retailers in Canada, and achieve market acceptance by Canadian guests. In addition, our sales and operating results in Canada are dependent on our ability to manage our inventory to offer the expected assortment of merchandise to our Canadian guests while avoiding overstock situations, and general macroeconomic conditions in Canada. If we do not effectively execute our marketing program and manage our inventory in Canada, our financial results could be adversely affected.

A disruption in relationships with third parties who provide us services in connection with certain aspects of our business could adversely affect our operations.

We rely on third parties to support a variety of business functions, including our Canadian supply chain, portions of our technology development and systems, our multichannel platforms and distribution network operations, credit and debit card transaction processing, and extensions of credit for our 5% REDcard Rewards loyalty program. If we are unable to contract with third parties having the specialized skills needed to support those strategies or integrate their products and services with our business, or if those third parties fail to meet our performance standards and expectations, including with respect to data security, our reputation, sales and results of operations could be adversely affected. In addition, we could face increased costs associated with finding replacement providers or hiring new team members to provide these services in-house.

We experienced a significant data security breach in the fourth quarter of fiscal 2013 and are not yet able to determine the full extent of its impact and the impact of government investigations and private litigation on our results of operations, which could be material.

The Data Breach we experienced involved the theft of certain payment card and guest information through unauthorized access to our network. Our investigation of the matter is ongoing, and it is possible that we will identify additional information that was accessed or stolen, which could materially worsen the losses and reputational damage we have experienced. For example, when the intrusion was initially identified, we thought the information stolen was limited to payment card information, but later discovered that other guest information was also stolen.

We are currently subject to a number of governmental investigations and private litigation and other claims relating to the Data Breach, and in the future we may be subject to additional investigations and claims of this sort. These investigations and claims could have a material adverse impact on our results of operations or profitability. Our financial liability arising from such investigations and claims will depend on many factors, one of which is whether, at the time of the Data Breach, the portion of our network that handles payment card data was in compliance with applicable payment card industry standards. While that portion of our network was determined to be compliant by an independent third-party assessor in the fall of 2013, we expect the forensic investigator working on behalf of the payment card networks to claim that we were not in compliance. Another factor is whether, and if so to what extent, any fraud losses or other expenses experienced by cardholders, card issuers and/or the payment card networks on or with respect to the payment card accounts affected by the Data Breach can be properly attributed to the Data Breach and whether, and if so to what extent, it would in any event be our legal responsibility. In addition, the governmental agencies investigating the Data Breach may seek to impose on us fines and/or other monetary relief and/or injunctive relief that could materially increase our data security costs, adversely impact how we operate our network and collect and use guest information, and put us at a competitive disadvantage with other retailers.

9

Finally, we believe that the greatest risk to our business arising out of the Data Breach is the negative impact on our reputation and loss of confidence of our guests, as well as the possibility of decreased participation in our REDcards Rewards loyalty program which our internal analysis has indicated drives meaningful incremental sales. We experienced weaker than expected U.S. Segment sales after the announcement of the Data Breach, but are unable to determine whether there will be a long-term impact to our relationship with our guests or whether we will need to engage in significant promotional or other activities to regain their trust, which could have a material adverse impact on our results of operations or profitability.

Item 1B. Unresolved Staff Comments

Not applicable.

10

Item 2. Properties

U.S. Stores at February 1, 2014 | Stores | | Retail Sq. Ft. (in thousands) | |

|

| Stores | | Retail Sq. Ft. (in thousands) | |

Alabama | 22 | | 3,150 | |

| Montana | 7 | | 780 | |

Alaska | 3 | | 504 | |

| Nebraska | 14 | | 2,006 | |

Arizona | 47 | | 6,264 | |

| Nevada | 19 | | 2,461 | |

Arkansas | 9 | | 1,165 | |

| New Hampshire | 9 | | 1,148 | |

California | 262 | | 34,718 | |

| New Jersey | 43 | | 5,701 | |

Colorado | 41 | | 6,215 | |

| New Mexico | 10 | | 1,185 | |

Connecticut | 20 | | 2,672 | |

| New York | 69 | | 9,437 | |

Delaware | 3 | | 440 | |

| North Carolina | 48 | | 6,360 | |

District of Columbia | 1 | | 179 | |

| North Dakota | 4 | | 554 | |

Florida | 123 | | 17,345 | |

| Ohio | 64 | | 8,002 | |

Georgia | 54 | | 7,398 | |

| Oklahoma | 16 | | 2,285 | |

Hawaii | 4 | | 695 | |

| Oregon | 19 | | 2,280 | |

Idaho | 6 | | 664 | |

| Pennsylvania | 64 | | 8,384 | |

Illinois | 91 | | 12,514 | |

| Rhode Island | 4 | | 517 | |

Indiana | 33 | | 4,377 | |

| South Carolina | 19 | | 2,359 | |

Iowa | 22 | | 3,015 | |

| South Dakota | 5 | | 580 | |

Kansas | 19 | | 2,577 | |

| Tennessee | 32 | | 4,114 | |

Kentucky | 14 | | 1,660 | |

| Texas | 149 | | 20,976 | |

Louisiana | 16 | | 2,246 | |

| Utah | 13 | | 1,953 | |

Maine | 5 | | 630 | |

| Vermont | - | | - | |

Maryland | 38 | | 4,938 | |

| Virginia | 57 | | 7,650 | |

Massachusetts | 36 | | 4,734 | |

| Washington | 36 | | 4,194 | |

Michigan | 59 | | 7,057 | |

| West Virginia | 6 | | 755 | |

Minnesota | 75 | | 10,777 | |

| Wisconsin | 39 | | 4,773 | |

Mississippi | 6 | | 743 | |

| Wyoming | 2 | | 187 | |

Missouri | 36 | | 4,736 | |

|

|

| |

| |

|

| |

| |

| Total | 1,793 | | 240,054 | |

Canadian Stores at February 1, 2014 | Stores | | Retail Sq. Ft. | |

|

| Stores | | Retail Sq. Ft. | |

Alberta | 14 | | 1,633 | |

| Nunavut | - | | - | |

British Columbia | 18 | | 2,047 | |

| Ontario | 50 | | 5,772 | |

Manitoba | 4 | | 457 | |

| Prince Edward Island | 1 | | 106 | |

New Brunswick | 3 | | 320 | |

| Quebec | 25 | | 2,876 | |

Newfoundland and Labrador | 2 | | 216 | |

| Saskatchewan | 3 | | 319 | |

Northwest Territories | - | | - | |

| Yukon | - | | - | |

Nova Scotia | 4 | | 443 | |

|

|

|

| ||

|

| |

| |

| Total | 124 | | 14,189 | |

11

U.S. Stores and Distribution Centers at February 1, 2014 | Stores | | Distribution Centers (a) | |

Owned | 1,535 | | 31 | |

Leased | 91 | | 6 | |

Owned buildings on leased land | 167 | | - | |

Total | 1,793 | | 37 | |

(a) | The 37 distribution centers have a total of 50,111 thousand square feet. |

Canadian Stores and Distribution Centers at February 1, 2014 | Stores | | Distribution Centers (a) | |

Owned | - | | 3 | |

Leased | 124 | | - | |

Total | 124 | | 3 | |

(a) | The 3 distribution centers have a total of 3,963 thousand square feet. |

We own our corporate headquarters buildings located in and around Minneapolis, Minnesota, and we lease and own additional office space in Minneapolis and elsewhere in the United States. We lease our Canadian headquarters in Mississauga, Ontario. Our international sourcing operations include 22 office locations in 14 countries, all of which are leased. We also lease office space in Bangalore, India, where we operate various support functions. Our properties are in good condition, well maintained, and suitable to carry on our business.

For additional information on our properties, see the Capital Expenditures section in Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations and Notes 12 and 20 of the Notes to Consolidated Financial Statements included in Item 8, Financial Statements and Supplementary Data.

Item 3. Legal Proceedings

No response is required under Item 103 of Regulation S-K, which requires disclosure of legal proceedings that are material, based on an analysis of the probability and magnitude of the outcome. For a description of other legal proceedings, including a discussion of litigation and government inquiries related to the Data Breach we experienced in the fourth quarter of fiscal 2013 in which certain payment card and guest information was stolen through unauthorized access to our network, see Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations and Note 17 of the Notes to Consolidated Financial Statements included in Item 8, Financial Statements and Supplementary Data.

Item 4. Mine Safety Disclosures

Not applicable.

Item 4A. Executive Officers

Executive officers are elected by, and serve at the pleasure of, the Board of Directors. There is neither a family relationship between any of the officers named and any other executive officer or member of the Board of Directors, nor any arrangement or understanding pursuant to which any person was selected as an officer.

12

Name | Title and Business Experience | Age | |

Timothy R. Baer | Executive Vice President, General Counsel and Corporate Secretary since March 2007. | 53 | |

Anthony S. Fisher | President, Target Canada since January 2011. Vice President, Merchandise Operations from February 2010 to January 2011. Divisional Merchandise Manager, Toys and Sporting Goods, from June 2008 to January 2010. | 39 | |

John D. Griffith | Executive Vice President, Property Development since February 2005. | 52 | |

Jeffrey J. Jones II | Executive Vice President and Chief Marketing Officer since April 2012. Partner and President of McKinney Ventures LLC from March 2006 to March 2012. | 46 | |

Jodeen A. Kozlak | Executive Vice President, Human Resources since March 2007. | 50 | |

John J. Mulligan | Executive Vice President and Chief Financial Officer since April 2012. Senior Vice President, Treasury, Accounting and Operations from February 2010 to April 2012. Vice President, Pay and Benefits from February 2007 to February 2010. | 48 | |

Tina M. Schiel | Executive Vice President, Stores since January 2011. Senior Vice President, New Business Development from February 2010 to January 2011. Senior Vice President, Stores from February 2001 to February 2010. | 48 | |

Gregg W. Steinhafel | Chairman of the Board, President and Chief Executive Officer since February 2009. President and Chief Executive Officer since May 2008. Director since January 2007. President since August 1999. | 59 | |

Kathryn A. Tesija | Executive Vice President, Merchandising and Supply Chain since October 2012. Executive Vice President, Merchandising from May 2008 to September 2012. | 51 | |

Laysha L. Ward | President, Community Relations and Target Foundation since July 2008. | 46 | |

13

PART II

Item 5. Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Our common stock is listed on the New York Stock Exchange under the symbol "TGT." We are authorized to issue up to 6,000,000,000 shares of common stock, par value $0.0833, and up to 5,000,000 shares of preferred stock, par value $0.01. At March 10, 2014 , there were 15,875 shareholders of record. Dividends declared per share and the high and low closing common stock price for each fiscal quarter during 2013 and 2012 are disclosed in Note 29 of the Notes to Consolidated Financial Statements included in Item 8, Financial Statements and Supplementary Data.

In January 2012, our Board of Directors authorized the repurchase of $5 billion of our common stock, with no stated expiration for the share repurchase program. We have repurchased 49.1 million shares of our common stock under this program for a total cash investment of $3.1 billion ( $62.99 average price per share).

The table below presents Target common stock purchases made during the three months ended February 1, 2014 by Target, as defined in Rule 10b-18(a)(3) under the Exchange Act.

Period | Total Number of Shares Purchased (a)(b) | | Average Price Paid per Share (a)(b) | | Total Number of Shares Purchased as Part of the Current Program (a) | | Dollar Value of Shares that May Yet Be Purchased Under the Program | | ||

November 3, 2013 through November 30, 2013 | 2,406 | | $ | - | | 49,148,329 | | $ | 1,904,324,394 | |

December 1, 2013 through January 4, 2014 | 18,310 | | - | | 49,148,329 | | 1,904,324,394 | | ||

January 5, 2014 through February 1, 2014 | 147,537 | | - | | 49,148,329 | | 1,904,324,394 | | ||

| 168,253 | | $ | - | | 49,148,329 | | $ | 1,904,324,394 | |

(a) | The table above includes shares reacquired upon settlement of prepaid forward contracts. At February 1, 2014 , we held asset positions in prepaid forward contracts for 1 million shares of our common stock, for a total cash investment of $63 million, or an average per share price of $48.83. No shares were reacquired under such contracts during the fourth quarter. Refer to Notes 23 and 25 of the Notes to Consolidated Financial Statements included in Item 8, Financial Statements and Supplementary Data for further details of these contracts. |

(b) | The number of shares above includes shares of common stock reacquired from team members who tendered owned shares to satisfy the tax withholding on equity awards as part of our long-term incentive plans or to satisfy the exercise price on stock option exercises. For the three months ended February 1, 2014 ,168,253 shares were reacquired at an weighted average per share price of $61.91 pursuant to our long-term incentive plan. |

14

Comparison of Cumulative Five Year Total Return

| Fiscal Years Ended | |||||||||||||||||

| January 31, | | January 30, | | January 29, | | January 28, | | February 2, | | February 1, | | ||||||

Target | $ | 100.00 | | $ | 167.08 | | $ | 179.93 | | $ | 169.27 | | $ | 211.54 | | $ | 200.64 | |

S&P 500 Index | 100.00 | | 133.14 | | 161.44 | | 170.04 | | 199.98 | | 240.58 | | ||||||

Previous Peer Group | 100.00 | | 128.10 | | 146.82 | | 163.21 | | 205.64 | | 247.92 | | ||||||

Current Peer Group | 100.00 | | 128.46 | | 147.71 | | 164.25 | | 207.23 | | 249.77 | | ||||||

The graph above compares the cumulative total shareholder return on our common stock for the last five fiscal years with (i) the cumulative total return on the S&P 500 Index, (ii) the peer group used in previous filings consisting of 15 online, general merchandise, department store, food and specialty retailers, which are large and meaningful competitors (Amazon.com, Best Buy, Costco, CVS Caremark, Home Depot, J. C. Penney, Kohl's, Kroger, Lowe's, Macy's, Safeway, Sears, Supervalu, Walgreens and Walmart) (Previous Peer Group), and (iii) a new peer group consisting of the companies in the Previous Peer Group excluding Supervalu. The change in peer groups was made to be consistent with the retail peer group used for our definitive Proxy Statement to be filed on or about April 28, 2014.

Both peer groups are weighted by the market capitalization of each component company. The graph assumes the investment of $100 in Target common stock, the S&P 500 Index, the Previous Peer Group and the Current Peer Group on January 31, 2009, and reinvestment of all dividends.

15

Item 6. Selected Financial Data

| As of or for the Year Ended | |||||||||||||||||

(millions, except per share data) | 2013 | | 2012 (a) | | 2011 | | 2010 | | 2009 | | 2008 | | ||||||

Financial Results: |

|

|

|

|

|

| ||||||||||||

Total revenues (b) | $ | 72,596 | | $ | 73,301 | | $ | 69,865 | | $ | 67,390 | | $ | 65,357 | | $ | 64,948 | |

Net earnings | 1,971 | | 2,999 | | 2,929 | | 2,920 | | 2,488 | | 2,214 | | ||||||

Per Share: |

|

|

|

|

|

| ||||||||||||

Basic earnings per share | 3.10 | | 4.57 | | 4.31 | | 4.03 | | 3.31 | | 2.87 | | ||||||

Diluted earnings per share | 3.07 | | 4.52 | | 4.28 | | 4.00 | | 3.30 | | 2.86 | | ||||||

Cash dividends declared per share | 1.65 | | 1.38 | | 1.15 | | 0.92 | | 0.67 | | 0.62 | | ||||||

Financial Position: |

|

|

|

|

|

| ||||||||||||

Total assets | 44,553 | | 48,163 | | 46,630 | | 43,705 | | 44,533 | | 44,106 | | ||||||

Long-term debt, including current portion | 13,782 | | 17,648 | | 17,483 | | 15,726 | | 16,814 | | 18,752 | | ||||||

Note: This information should be read in conjunction with Management's Discussion and Analysis of Financial Condition and Results of Operations, included in Item 7 of this Report, and our consolidated financial statements and notes thereto, included in Item 8 of this Report.

(a) | Consisted of 53 weeks. |

(b) | For 2013, total revenues include sales generated by our U.S. and Canadian retail operations. For 2012 and prior, total revenues include sales generated by our U.S. retail operations and credit card revenues. |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Executive Summary

Fiscal 2013 included the following notable items:

• | GAAP earnings per share were $3.07 , including dilution of $1.13 related to the Canadian Segment. |

• | Adjusted earnings per share were $4.38 on a comparable sales decrease of 0.4 percent. |

• | We paid dividends of $1,006 million and repurchased 21.9 million of our shares for $1,474 million . |

• | We opened 124 stores in Canada, marking the biggest single-year store opening cycle in the Company's history and first year of international retail operations. |

• | We completed the sale of our U.S. consumer credit card portfolio to TD in March 2013 and recognized a gain of $391 million. |

• | We used $1.4 billion of the net proceeds received from the sale of our U.S. consumer credit card portfolio to repurchase, at market value, $970 million of debt. |

Sales were $72,596 million for 2013 , an increase of $636 million or 0.9 percent from the prior year. Consolidated earnings before interest expense and income taxes for 2013 decreased by $1,142 million or 21.3 percent from 2012 to $4,229 million . Cash flow provided by operations was $6,520 million , $5,325 million and $5,434 million for 2013 , 2012 and 2011 , respectively. In connection with the sale of our U.S. credit card receivables, we received cash of $5.7 billion. Of this amount, $2.7 billion is included in cash flow provided by operations and $3.0 billion is included in cash flow provided by investing activities.

Earnings Per Share |

|

|

| Percent Change | |||||||||

| 2013 | | 2012 (a) | | 2011 | | 2013/2012 | | 2012/2011 | | |||

GAAP diluted earnings per share | $ | 3.07 | | $ | 4.52 | | $ | 4.28 | | (32.1 | )% | 5.6 | % |

Adjustments | 1.31 | | 0.24 | | 0.13 | |

| |

| | |||

Adjusted diluted earnings per share | $ | 4.38 | | $ | 4.76 | | $ | 4.41 | | (8.0 | )% | 7.9 | % |

(a) | Consisted of 53 weeks. |

16

Data Breach

Description of Event

As previously disclosed, we experienced a data breach in which an intruder stole certain payment card and other guest information from our network (the Data Breach). Based on our investigation to date, we believe that the intruder accessed and stole payment card data from approximately 40 million credit and debit card accounts of guests who shopped at our U.S. stores between November 27 and December 15, 2013, through malware installed on our point-of-sale system in our U.S. stores. On December 15, we removed the malware from virtually all registers in our U.S. stores. Payment card data used in transactions made by 56 additional guests in the period between December 16 and December 17 was stolen prior to our disabling malware on one additional register that was disconnected from our system when we completed the initial malware removal on December 15. In addition, the intruder stole certain guest information, including names, mailing addresses, phone numbers or email addresses, for up to 70 million individuals. Our investigation of the matter is ongoing, and we are supporting law enforcement efforts to identify the responsible parties.

Expenses Incurred and Amounts Accrued

In the fourth quarter of 2013, we recorded $61 million of pretax Data Breach-related expenses, and expected insurance proceeds of $44 million, for net expenses of $17 million ($11 million after tax), or $0.02 per diluted share. These expenses were included in our Consolidated Statements of Operations as Selling, General and Administrative Expenses (SG&A), but were not part of our segment results. Expenses include costs to investigate the Data Breach, provide credit-monitoring services to our guests, increase staffing in our call centers, and procure legal and other professional services.

The $61 million of fourth quarter expenses also includes an accrual related to the expected payment card networks' claims by reason of the Data Breach. The ultimate amount of these claims will likely include amounts for incremental counterfeit fraud losses and non-ordinary course operating expenses (such as card reissuance costs) that the payment card networks believe they or their issuing banks have incurred. In order for us to have liability for such claims, we believe that a court would have to find among other things that (1) at the time of the Data Breach the portion of our network that handles payment card data was noncompliant with applicable data security standards in a manner that contributed to the Data Breach, and (2) the network operating rules around reimbursement of operating costs and counterfeit fraud losses are enforceable. While an independent third-party assessor found the portion of our network that handles payment card data to be compliant with applicable data security standards in the fall of 2013, we expect the forensic investigator working on behalf of the payment card networks nonetheless to claim that we were not in compliance with those standards at the time of the Data Breach. We base that expectation on our understanding that, in cases like ours where prior to a data breach the entity suffering the breach had been found by an independent third-party assessor to be fully compliant with those standards, the network-approved forensic investigator nonetheless regularly claims that the breached entity was not in fact compliant with those standards. As a result, we believe it is probable that the payment card networks will make claims against us. We expect to dispute the payment card networks' anticipated claims, and we think it is likely that our disputes would lead to settlement negotiations consistent with the experience of other entities that have suffered similar payment card breaches. We believe such negotiations would effect a combined settlement of both the payment card networks' counterfeit fraud loss allegations and their non-ordinary course operating expense allegations. We based our year-end accrual on the expectation of reaching negotiated settlements of the payment card networks' anticipated claims and not on any determination that it is probable we would be found liable on these claims were they to be litigated. Currently, we can only reasonably estimate a loss associated with settlements of the networks' expected claims for non-ordinary course operating expenses. The year-end accrual does not include any amounts associated with the networks' expected claims for alleged incremental counterfeit fraud losses because the loss associated with settling such claims, while probable in our judgment, is not reasonably estimable, in part because we have not yet received third-party fraud reporting from the payment card networks. We are not able to reasonably estimate a range of possible losses in excess of the year-end accrual related to the expected settlement of the payment card networks' claims because the investigation into the matter is ongoing and there are significant factual and legal issues to be resolved. We believe that the ultimate amount paid on payment card network claims could be material to our results of operations in future periods.

17

Litigation and Governmental Investigations

In addition, more than 80 actions have been filed in courts in many states and other claims have been or may be asserted against us on behalf of guests, payment card issuing banks, shareholders or others seeking damages or other related relief, allegedly arising out of the Data Breach. State and federal agencies, including the State Attorneys General, the Federal Trade Commission and the SEC are investigating events related to the Data Breach, including how it occurred, its consequences and our responses. Although we are cooperating in these investigations, we may be subject to fines or other obligations, which may have an adverse effect on how we operate our business and our results of operations. While a loss from these matters is reasonably possible, we cannot reasonably estimate a range of possible losses because our investigation into the matter is ongoing, the proceedings remain in the early stages, alleged damages have not been specified, there is uncertainty as to the likelihood of a class or classes being certified or the ultimate size of any class if certified, and there are significant factual and legal issues to be resolved. Further, we do not believe that a loss from these matters is probable; therefore, we have not recorded a loss contingency liability for litigation, claims and governmental investigations in the fourth quarter. See Note 17 of the Notes to Consolidated Financial Statements included in Item 8, Financial Statements and Supplementary Data.

Future Costs

We expect to incur significant investigation, legal and professional services expenses associated with the Data Breach in future periods. We will recognize these expenses as services are received. We also expect to incur additional expenses associated with incremental fraud and reissuance costs on Target REDcards.

Insurance Coverage

To limit our exposure to Data Breach losses, we maintain $100 million of network-security insurance coverage, above a $10 million deductible. This coverage and certain other insurance coverage may reduce our exposure. We will pursue recoveries to the maximum extent available under the policies. As of February 1, 2014, we have recorded a $44 million receivable for costs we believe are reimbursable and probable of recovery under our insurance coverage, which partially offsets the $61 million of expense relating to the Data Breach.

Future Capital Investments

We plan to accelerate a previously planned investment of approximately $100 million to equip our proprietary REDcards and all of our U.S. store card readers with chip-enabled smart-card technology by the first quarter of 2015.

In addition, we may accelerate or make additional investments in our information technology systems, but we are unable to estimate such investments because the nature and scope has not yet been determined. We do not expect such amounts to be material to any fiscal period.

Effect on Sales and Guest Loyalty

We believe the Data Breach adversely affected our fourth quarter U.S. Segment sales. Prior to our December 19, 2013 announcement of the Data Breach, our U.S. Segment fourth quarter comparable sales were positive, followed by meaningfully negative comparable sales results following the announcement. Comparable sales began to recover in January 2014. The collective interaction of year-over-year changes in the retail calendar ( e.g. , the number of days between Thanksgiving and Christmas), combined with the broad array of competitive, consumer behavioral and weather factors makes any quantification of the precise impact of the Data Breach on sales infeasible.

Fourth quarter sales penetration on our REDcards was 20.9 percent, up 5.4 percentage points from 2012. While the rate of increase slowed following the Data Breach, year-over-year penetration continued to grow.

We know our guests' confidence in Target and the broader U.S. payment system has been shaken. We are committed to, and actively engaged in, activities to restore their confidence. We cannot predict the length or extent of any ongoing impact to sales.

Credit Card Receivables Transaction

In March 2013, we sold our entire U.S. consumer credit card portfolio to TD and recognized a gain of $391 million. This transaction was accounted for as a sale, and the receivables are no longer reported in our Consolidated Statements of Financial Position. Consideration received included cash of $5.7 billion, equal to the gross (par) value of the

18

outstanding receivables at the time of closing, and a $225 million beneficial interest asset. The beneficial interest asset effectively represents a receivable for the present value of future profit-sharing we expect to receive on the receivables sold. Based on historical payment patterns, we estimate that the beneficial interest asset will be reduced over a four-year period following the sale, with larger reductions in the early years. As of February 1, 2014, a $127 million beneficial interest asset remained. Concurrent with the sale of the portfolio, we repaid the nonrecourse debt collateralized by credit card receivables (2006/2007 Series Variable Funding Certificate) at par of $1.5 billion, resulting in net cash proceeds of $4.2 billion.

TD now underwrites, funds and owns Target Credit Card and Target Visa consumer receivables in the U.S. TD controls risk management policies and oversees regulatory compliance, and we perform account servicing and primary marketing functions. We earn a substantial portion of the profits generated by the Target Credit Card and Target Visa portfolios. Income from the TD profit-sharing arrangement and our related account servicing expenses are classified within SG&A expenses in the U.S. Segment.

Beginning with the first quarter of 2013, we no longer report a U.S. Credit Card Segment.

Analysis of Results of Operations

U.S. Segment

U.S. Segment Results |

|

|

| Percent Change | |||||||||

(dollars in millions) | 2013 | | 2012 (a) | | 2011 | | 2013/2012 | | 2012/2011 | | |||

Sales | $ | 71,279 | | $ | 71,960 | | $ | 68,466 | | (0.9 | )% | 5.1 | % |

Cost of sales | 50,039 | | 50,568 | | 47,860 | | (1.0 | ) | 5.7 | | |||

Gross margin | 21,240 | | 21,392 | | 20,606 | | (0.7 | ) | 3.8 | | |||

SG&A expenses (b) | 14,285 | | 13,759 | | 13,079 | | 3.8 | | 5.2 | | |||

EBITDA | 6,955 | | 7,633 | | 7,527 | | (8.9 | ) | 1.4 | | |||

Depreciation and amortization | 1,996 | | 2,044 | | 2,084 | | (2.4 | ) | (1.9 | ) | |||

EBIT | $ | 4,959 | | $ | 5,589 | | $ | 5,443 | | (11.3 | )% | 2.7 | % |

Note: See Note 28 to our Consolidated Financial Statements for a reconciliation of our segment results to earnings before income taxes.

(a) | Consisted of 53 weeks. |

(b) | SG&A includes credit card revenues and expenses for all periods presented prior to the March 2013 sale of our U.S. consumer credit card portfolio to TD. For 2013, SG&A also includes $653 million of profit-sharing income from the arrangement with TD. |

U.S. Segment Rate Analysis |

| Twelve Months Ended February 2, 2013 |

| 2013 U.S. Segment Change vs. 2012 | ||||||||||||

| Twelve Months Ended February 1, 2014 | |

| U.S. Segment, as revised | |

| Impact of Historical U.S. Credit Card Segment (a) | |

| Historical U.S. Retail Segment | |

| U.S. Segment, as revised | |

| Historical U.S. Retail Segment |

Gross margin rate | 29.8 | % |

| 29.7 | % |

| - | | pp | 29.7 | % |

| 0.1pp | |

| 0.1pp |

SG&A expense rate | 20.0 | |

| 19.1 | |

| (0.8 | ) |

| 19.9 | |

| 0.9 | |

| 0.1 |

EBITDA margin rate | 9.8 | |

| 10.6 | |

| 0.8 | |

| 9.8 | |

| (0.8 | ) |

| - |

Depreciation and amortization expense rate | 2.8 | |

| 2.8 | |

| - | |

| 2.8 | |

| - | |

| - |

EBIT margin rate | 7.0 | |

| 7.8 | |

| 0.8 | |

| 7.0 | |

| (0.8 | ) |

| - |

19

U.S. Segment Rate Analysis |

| Twelve Months Ended January 28, 2012 |

| 2012 U.S. Segment Change vs. 2011 | |||||||||||||

| Twelve Months Ended February 2, 2013 | |

| U.S. Segment, as revised | |

| Impact of Historical U.S. Credit Card Segment (a) | |

| Historical U.S. Retail Segment | |

| U.S. Segment, as revised | |

| Historical U.S. Retail Segment | |

Gross margin rate | 29.7 | % |

| 30.1 | % |

| - | | pp | 30.1 | % |

| (0.4)pp | |

| (0.4)pp | |

SG&A expense rate | 19.1 | |

| 19.1 | |

| (1.0 | ) |

| 20.1 | |

| - | |

| (1.0 | ) |

EBITDA margin rate | 10.6 | |

| 11.0 | |

| 1.0 | |

| 10.0 | |

| (0.4 | ) |

| 0.6 | |

Depreciation and amortization expense rate | 2.8 | |

| 3.0 | |

| - | |

| 3.0 | |

| (0.2 | ) |

| (0.2 | ) |

EBIT margin rate | 7.8 | |

| 8.0 | |

| 1.0 | |

| 7.0 | |

| (0.2 | ) |

| 0.8 | |

Rate analysis metrics are computed by dividing the applicable amount by sales.

(a) | Represents the impact of combining the historical U.S. Credit Card Segment and the U.S. Retail Segment into one U.S. Segment. Compared with the historical U.S. Retail Segment results for the same period, segment results, as revised, reflect lower SG&A rates and increased EBIT and EBITDA margin rates resulting from the inclusion of credit card profits, net of expenses, within SG&A compared with historical U.S. Segment results for the same period. |

Sales

Sales include merchandise sales, net of expected returns, and gift card breakage. Refer to Note 2 of the Notes to Consolidated Financial Statements for a definition of gift card breakage. The decrease in sales in 2013 reflects the impact of an additional week in 2012 and a decline in comparable sales, partially offset by the contribution from new stores. Sales growth in 2012 resulted from higher comparable sales, the contribution from new stores and a 1.7 percentage point benefit from an additional week in the fiscal year. Inflation did not materially affect sales in any period presented.

Comparable sales is a measure that highlights the performance of our existing stores and digital sales by measuring the change in sales for a period over the comparable, prior-year period of equivalent length. The method of calculating comparable sales varies across the retail industry. As a result, our comparable sales calculation is not necessarily comparable to similarly titled measures reported by other companies. Comparable sales include all sales, except sales from stores open less than thirteen months.

Comparable Sales | 2013 | | 2012 | | 2011 | |

Comparable sales change | (0.4 | )% | 2.7 | % | 3.0 | % |

Drivers of change in comparable sales: |

|

|

| |||

Number of transactions | (2.7 | )% | 0.5 | % | 0.4 | % |

Average transaction amount | 2.3 | % | 2.3 | % | 2.6 | % |

Selling price per unit | 1.6 | % | 1.3 | % | 0.3 | % |

Units per transaction | 0.7 | % | 1.0 | % | 2.3 | % |

U.S. Sales by Product Category | Percentage of Sales | |||||

| 2013 | | 2012 | | 2011 | |

Household essentials (a) | 25 | % | 25 | % | 25 | % |

Hardlines (b) | 18 | | 18 | | 19 | |

Apparel and accessories (c) | 19 | | 19 | | 19 | |

Food and pet supplies (d) | 21 | | 20 | | 19 | |

Home furnishings and décor (e) | 17 | | 18 | | 18 | |

Total | 100 | % | 100 | % | 100 | % |

(a) | Includes pharmacy, beauty, personal care, baby care, cleaning and paper products. |

(b) | Includes electronics (including video game hardware and software), music, movies, books, computer software, sporting goods and toys. |

20

(c) | Includes apparel for women, men, boys, girls, toddlers, infants and newborns, as well as intimate apparel, jewelry, accessories and shoes. |

(d) | Includes dry grocery, dairy, frozen food, beverages, candy, snacks, deli, bakery, meat, produce and pet supplies. |

(e) | Includes furniture, lighting, kitchenware, small appliances, home décor, bed and bath, home improvement, automotive and seasonal merchandise such as patio furniture and holiday décor. |

The collective interaction of a broad array of macroeconomic, competitive and consumer behavioral factors, as well as sales mix, and transfer of sales to new stores makes further analysis of sales metrics infeasible.

Credit is offered by TD to qualified guests through Target-branded credit cards: the Target Credit Card and the Target Visa Credit Card (Target Credit Cards). Additionally, we offer a branded proprietary Target Debit Card. Collectively, we refer to these products as REDcards ® . Guests receive a 5 percent discount on virtually all purchases when they use a REDcard at Target. We monitor the percentage of sales that are paid for using REDcards (REDcard Penetration) because our internal analysis has indicated that a meaningful portion of incremental purchases on our REDcards are also incremental sales for Target.

REDcard Penetration | 2013 | | 2012 | | 2011 | |

Target Credit Cards | 9.3 | % | 7.9 | % | 6.8 | % |

Target Debit Card | 9.9 | | 5.7 | | 2.5 | |

Total store REDcard Penetration | 19.3 | % | 13.6 | % | 9.3 | % |

Note: The sum of Target Credit Cards and Target Debit Card penetration may not equal Total store REDcard Penetration due to rounding.

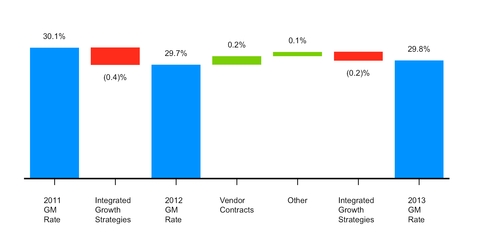

Gross Margin Rate

Our gross margin rate was 29.8 percent in 2013 , 29.7 percent in 2012 and 30.1 percent in 2011 . The 2013 increase is primarily the result of a change in vendor contracts regarding payments received in support of marketing programs. Increases to the rate were offset by our integrated growth strategies of our 5 percent REDcard Rewards loyalty program and our store remodel program.

The 2013 change to certain merchandise vendor contracts resulted in more vendor consideration being recognized as a reduction of our cost of sales rather than a reduction of SG&A. This change increased our gross margin rate for 2013, with an equal and offsetting increase in our SG&A rate, and has no impact on EBITDA or EBIT margin rates.

21

Selling, General and Administrative Expense Rate

(a) Represents revised U.S. Segment results.

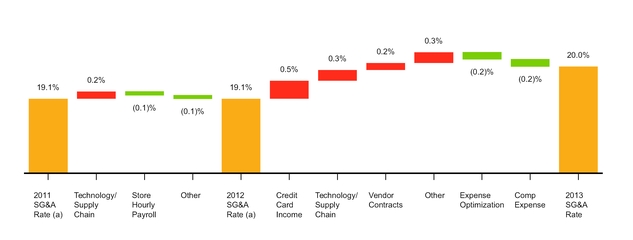

Our SG&A expense rate was 20.0 percent in 2013 , and 19.1 percent in both 2012 and 2011 . The increase in 2013 resulted from a smaller contribution from our credit card portfolio, investments in technology and supply chain in support of multichannel initiatives, changes in merchandise vendor contracts described on the previous page, and other increases. Increases were partially offset by the benefit from our company-wide expense optimization efforts and favorable incentive compensation and store hourly payroll. During 2012, investments in technology and supply chain were offset by improvements in store hourly payroll and disciplined expense management across the Company.

Store Data

Change in Number of Stores | 2013 | | 2012 | |

Beginning store count | 1,778 | | 1,763 | |

Opened | 19 | | 23 | |

Closed | (4 | ) | (5 | ) |

Relocated | - | | (3 | ) |

Ending store count | 1,793 | | 1,778 | |

Number of stores remodeled during the year | 100 | | 252 | |

Number of Stores and | Number of Stores |

| Retail Square Feet (a) | ||||||

February 1, 2014 | | February 2, 2013 | |

| February 1, 2014 | | February 2, 2013 | | |

Target general merchandise stores | 289 | | 391 | |

| 33,843 | | 46,584 | |

Expanded food assortment stores | 1,245 | | 1,131 | |

| 160,891 | | 146,249 | |

SuperTarget stores | 251 | | 251 | |

| 44,500 | | 44,500 | |

CityTarget stores | 8 | | 5 | |

| 820 | | 514 | |

Total | 1,793 | | 1,778 | |

| 240,054 | | 237,847 | |

(a) | In thousands, reflects total square feet less office, distribution center and vacant space. |

22