Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

For the fiscal year ended April 30, 2013 | ||

|

|

|

o | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

|

|

For the transition period from to | ||

Commission File Number: 001-35588

JTH Holding, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | | 27-3561876 (I.R.S. Employer Identification No.) |

|

| 1716 Corporate Landing Parkway, Virginia Beach, Virginia (Address of principal executive offices) | | 23454 (Zip Code) |

|

Registrant's telephone number, including area code: (757) 493-8855

Securities registered pursuant to Section 12(b) of the Act:

| Class A Common Stock, $0.01 par value per share (Title of Class) | | The NASDAQ Stock Market LLC (Name of Exchange on which registered) |

|

Securities to be registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES o NO ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. YES o NO ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES o NO ý

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES o NO ý

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o |

| Accelerated filer o |

| Non-accelerated filer o (Do not check if a smaller reporting company) |

| Smaller reporting company ý |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES o NO ý

As of October 31, 2012, the aggregate market value of the shares of Class A common stock held by non-affiliates of the registrant was $53,212,141 based on the number of shares held by non-affiliates as of October 31, 2012 and based on the last reported sale price of the registrant's Class A common stock on the NASDAQ Global Market of $14.90 on October 31, 2012. The number of shares of the registrant's Class A common stock outstanding as of September 26, 2013 was 12,023,265.

Documents incorporated by reference: None.

Table of Contents

Table of Contents

Part I |

|

|

Item 1. | Business | 8 |

Item 1A. | Risk Factors | 22 |

Item 1B. | Unresolved Staff Comments | 37 |

Item 2. | Properties | 37 |

Item 3. | Legal Proceedings | 38 |

Item 4. | Mine Safety Disclosure s | 38 |

Part II |

|

|

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 39 |

Item 6. | Selected Financial Data | 40 |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 44 |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 62 |

Item 8. | Financial Statements and Supplementary Data | 62 |

| Report of Independent Registered Public Accounting Firm | F-1 |

| Consolidated Balance Sheets | F-2 |

| Consolidated Income Statements | F-3 |

| Consolidated Statements of Comprehensive Income | F-4 |

| Consolidated Statements of Stockholders' Equity | F-5 |

| Consolidated Statement of Cash Flows | F-8 |

| Notes to Consolidated Financial Statements | F-10 |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 62 |

Item 9A. | Controls and Procedures | 62 |

Item 9B. | Other Information | 64 |

Part III |

|

|

Item 10. | Directors, Executive Officers and Corporate Governance | 65 |

Item 11. | Executive Compensation | 69 |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 81 |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 82 |

Item 14. | Principal Accounting Fees and Services | 83 |

Part IV |

|

|

Item 15. | Exhibits, Financial Statement Schedules | 85 |

Signatures | 88 | |

3

Table of Contents

EXPLANATORY NOTE REGARDING RESTATEMENT

As previously reported, on August 1, 2013, we determined that our previously issued consolidated financial statements contained in our Annual Report on Form 10-K for the year ended April 30, 2012, and in our quarterly reports on Form 10-Q for the subsequent fiscal quarters ended July 31, 2012, October 31, 2012 and January 31, 2013, should no longer be relied upon and would be restated to reflect certain changes to our accounting policies, primarily with respect to revenue recognition and business combination accounting. These restatements of our previously issued consolidated financial statements are referred to collectively as the "Restatement," and the periods affected by the Restatement are referred to collectively as the "Restated Periods."

In this annual report, the following types of financial information and other disclosures are restated or amended, as applicable, as a result of the Restatement, as of and for the Restated Periods noted in the table below.

Type of Financial Information/Disclosure | Date or Period |

Consolidated balance sheet | As of April 30, 2012 |

Consolidated statements of income, stockholders' equity, comprehensive income and cash flows | Fiscal years ended April 30, 2012 and 2011 |

Selected financial data | Fiscal years ended and as of April 30, 2012, 2011, 2010 and 2009 |

Unaudited quarterly financial information | Each fiscal quarter in the fiscal years ended April 30, 2013 and 2012 |

Management's Discussion and Analysis of Financial Condition and Results of Operations | As of and for the years ended April 30, 2012 and 2011 |

We believe that presenting all of the financial information and other disclosures affected by the Restatement for the Restated Periods in this annual report allows investors to review all pertinent data in a single presentation. We intend to file, subsequent to the filing of this annual report, our quarterly report on Form 10-Q for the quarterly period ended July 31, 2013 and amendments to our quarterly reports on Form 10-Q for each of the quarterly periods ended July 31, 2012, October 31, 2012 and January 31, 2013, but we do not expect to file an amendment to our annual report on Form 10-K for the year ended April 30, 2012 (the "2012 Annual Report"). Accordingly, investors should rely only on the financial information and other disclosures for the Restated Periods included in this annual report, and should not rely on the 2012 Annual Report or any reports, earnings releases or similar communications relating to the Restated Periods.

As presented in more detail throughout this annual report, the Restatement reflects adjustments primarily related to the following areas:

• | We determined that our area developer, or "AD", agreements do not constitute a franchise relationship for accounting purposes. Therefore, instead of recording revenue at the inception of the AD relationship under franchise accounting, we now record these fees over the life of the AD agreement, which is typically ten years. Additionally, our consolidated financial statements now show the portion of franchise fees and royalties that the AD is entitled to receive from us in our revenue captions, with an equal amount of expense shown in a new operating expense caption as "area developer expense." These amounts were previously presented on a net basis. |

• | We changed our revenue recognition policy for franchise fees to record revenue as amounts are received from the franchisee. Previously, we generally recorded these revenues at the time of sale, net of expected note cancellations related to the amount financed. Therefore, under the new revenue recognition policy any portion of franchise fees that is financed is only reflected as revenue when the note payments are made. |

• | We also revised our methodology for the allocation of the purchase price associated with the acquisitions of businesses from franchisees. Historically, we allocated the entire purchase price to an identifiable intangible asset denominated as customer list. The new methodology allocates the purchase price to all identifiable intangible assets, which consist of reacquired rights and customer list. Any unallocated purchase price is recorded as goodwill. |

4

Table of Contents

The following table quantifies in summary format the effect of these restated items on our income before income taxes for the fiscal years ended April 30 of each year:

|

| 2009 |

| 2010 |

| 2011 |

| 2012 |

| 2013 | ||||||||||

|

| (dollars in thousands) | ||||||||||||||||||

As Reported | $ | 20,816 | |

| $ | 17,884 | |

| $ | 26,636 | |

| $ | 27,805 | |

| $ | 29,792 | | |

Adjustments related to the following areas: |

|

|

|

|

|

|

|

|

| |||||||||||

| Area developer agreements | 2,249 | |

| 5,917 | |

| 762 | |

| (1,935 | ) |

| (951 | ) | |||||

| Franchise fees | (541 | ) |

| (894 | ) |

| (2,330 | ) |

| (668 | ) |

| (26 | ) | |||||

| Business combinations | 60 | |

| 139 | |

| (256 | ) |

| 928 | |

| (18 | ) | |||||

As Restated | $ | 22,584 | |

| $ | 23,046 | |

| $ | 24,812 | |

| $ | 26,130 | |

| $ | 28,797 | | |

The following items are not affected by the Restatement:

• | The Restatement does not impact actual cash received or the reported cash balances for any of the Restated Periods. |

• | The Restatement does not impact the receipt of the total reported revenue, but instead changes the time periods over which the revenue was recognized. |

The Restatement and related matters are more fully described in Notes 18 and 19 to our Consolidated Financial Statements included in this Annual Report, as well as under the following items of this Annual Report: "Item 1A-Risk Factors," "Item 6-Selected Financial Data," "Item 7-Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Item 9A-Controls and Procedures."

5

Table of Contents

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements concerning our business, operations and financial performance and condition as well as our plans, objectives and expectations for our business operations and financial performance and condition. Any statements contained herein that are not of historical facts may be deemed to be forward-looking statements. You can identify these statements by words such as "aim," "anticipate," "assume," "believe," "could," "due," "estimate," "expect," "goal," "intend," "may," "objective," "plan," "predict," "potential," "positioned," "should," "target," "will," "would" and other similar expressions that are predictions of or indicate future events and future trends. These forward-looking statements are based on current expectations, estimates, forecasts and projections about our business and the industry in which we operate and our management's beliefs and assumptions and are not guarantees of future performance or development and involve known and unknown risks, uncertainties and other factors that are in some cases beyond our control. As a result, any or all of our forward-looking statements in this annual report may turn out to be inaccurate. Factors that may cause such differences include, but are not limited to, the risks described under "Item 1A-Risk Factors," including:

• | our possible inability to sustain growth at our historical pace; |

• | the seasonality of our business; |

• | our inability to secure reliable sources of the tax settlement products we make available to our customers; |

• | the continued service of our senior management team; |

• | government regulation and oversight, including the regulation of tax settlement products such as electronic refund checks ("ERCs") and loan settlement products; |

• | government initiatives that simplify tax return preparation, improve the timing and efficiency of processing tax returns, limit payments to tax preparers or decrease the number of tax returns filed or the size of the refunds; |

• | government initiatives to pre-populate income tax returns; |

• | increased regulation of the products and services that we offer; |

• | the possible characterization of ERCs as a form of loan or extension of credit; |

• | changes in the tax settlement products offered to our customers that make our services less attractive to customers or more costly to us; |

• | our ability to maintain relationships with our tax settlement product service providers; |

• | our ability and the ability of our franchisees to comply with regulatory requirements; |

• | changes in our franchise sale model that may reduce our revenue; |

• | the ability of our franchisees to open new territories and operate them successfully; |

• | the ability of our franchisees to generate sufficient revenue to repay their indebtedness to us; |

• | our exposure to litigation; |

• | our ability and our franchisees' ability to protect customers' personal information, including from a cyber-security incident; |

• | our ability to access the credit markets and satisfy our covenants to lenders; |

• | challenges in deploying accurate tax software in a timely way each tax season; |

• | competition in the tax preparation market; |

• | our reliance on technology systems, including the deployment of our NextGen project, and electronic communications; |

• | our ability to deploy our NextGen software in time for the 2014 tax season; |

• | potential shareholder litigation as a result of the restatement of our previously issued consolidated financial statements; |

6

Table of Contents

• | risks relating to our management's determination that there was a material weakness in our internal control over financial reporting, and as a result that our disclosure controls and procedures were not effective, as of April 30, 2013; and |

• | other factors, including the risk factors discussed in this annual report. |

Potential investors and other readers are urged to consider these factors carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on the forward-looking statements. These forward-looking statements speak only as of the date of this annual report. Unless required by law, we do not intend to publicly update or revise any forward-looking statements to reflect new information or future events or otherwise. A potential investor or other vendor should, however, review the factors and risks we describe in the reports we will file from time to time with the U.S. Securities and Exchange Commission, or "SEC", after the date of this annual report.

7

Table of Contents

PART I

Item 1. Business.

Corporate Information

We were originally incorporated in Delaware in September 2010 as JTH Holding, Inc. We are the holding company for JTH Tax, Inc. d/b/a Liberty Tax Service, which was incorporated in Delaware in October 1996. Our principal executive offices are located at 1716 Corporate Landing Parkway, Virginia Beach, Virginia 23454. Our filings with the U.S. Securities and Exchange Commission or "SEC", including annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and amendments to these reports, are accessible free of charge at our corporate website, www.libertytax.com.

We are an "emerging growth company" under applicable federal securities laws and are subject to reduced public company reporting requirements.

Definitions and Trademarks

References in this report to "years" are to our fiscal years, which end on April 30 unless otherwise noted, and all references to "tax season" refer to the period between January 1 and April 30 of the referenced year. Unless the context requires otherwise, the terms "Liberty Tax," "Liberty Tax Service," "we," "the Company," "us" and "our" refer to JTH Holding, Inc. and its consolidated subsidiaries.

This annual report includes trademarks, including "Liberty Tax," "Liberty Tax Service," "Liberty Income Tax," "Liberty Canada" and our logo, which are protected under applicable intellectual property laws and are our property and/or the property of our subsidiaries. This annual report also includes trademarks, trade names and service marks that are the property of other organizations.

Market, Industry and Other Data

Unless otherwise indicated, information contained in this annual report concerning our industry and the market in which we operate, including our general expectations and market position, market opportunity and market size, is based on information from various third-party sources, on assumptions that we have made that are based on that data and other similar sources. Some data is also based on our good faith estimates, which are derived from management's knowledge of the industry and independent sources. This data involves a number of assumptions and limitations, and a reader is cautioned not to give undue weight to such estimates. Similarly, we believe our internal research is reliable, even though such research has not been verified by any independent sources. While we believe the market position, market opportunity and market size information included in this annual report is generally reliable, such information is inherently imprecise. In addition, information relating to projections, assumptions and estimates of our future performance and the future performance of the industry in which we operate is necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in "Item 1A-Risk Factors" and elsewhere in this annual report. These and other factors could cause our results to differ materially from those expressed in the estimates made by third parties and by us.

Business Overview

We are one of the leading providers of tax preparation services in the United States and Canada. As measured by both the number of returns prepared and the number of retail offices, we are the third largest and fastest growing national retail preparer of individual tax returns in the United States and the second largest retail preparer of individual tax returns in Canada. From 2001 through 2013 , we have grown the number of U.S. tax returns prepared in our offices from approximately 137,000 to 1.8 million . These services and related financial products that we refer to as "tax settlement" products are offered primarily through franchised locations, although we operate a very limited number of company-owned offices each tax season. All of the offices are operated under the Liberty Tax Service brand. Since the 2001 tax season and through the 2013 tax season, our percentage share of the paid tax preparation market in the United States has increased from 0.2% to more than 2% .

From 2001 through 2013 , we grew our number of tax offices from 508 to 4,520 . We and our franchisees operated 4,262 of those offices in the United States during the 2013 tax season, an 8.7% increase over the 2012 tax season, when we operated 3,920 offices, which was itself a 9.2% increase over the number of offices operated in the 2011 tax season.

The following table indicates the number of offices open at any point during the tax season and the number of total tax returns filed through these offices during the fiscal year ended April 30 of each year.

8

Table of Contents

|

| 2009 |

| 2010 |

| 2011 |

| 2012 |

| 2013 | |||||

Offices - Total |

| 3,091 | |

| 3,531 | |

| 3,845 | |

| 4,183 | |

| 4,520 | |

Tax returns prepared in our offices |

| 1,632,000 | |

| 1,795,000 | |

| 1,946,000 | |

| 2,075,000 | |

| 2,116,000 | |

We provide our customers with value-added federal and state tax preparation services and related tax settlement products both in retail offices and online. Our target customers include taxpayers who for reasons of complexity, convenience or the need for prompt tax refunds desire the assistance of assisted tax preparation services. Our customer growth is driven by our ability to capture an increasing share of a continuously expanding tax preparation market.

We believe that our franchise system is the core of our highly scalable business model and the keystone of our growth. Most of the Liberty Tax offices are operated by franchisees. Because we do not own or operate a significant number of tax offices, we are able to focus on marketing, franchisee coaching and support, financial product development and other initiatives that drive our overall success. In addition, our franchise model allows us to grow our tax system with minimal capital expenditures or fixed cost investments.

Our franchise model has been recognized as an attractive investment opportunity for a variety of entrepreneurs. In May 2011, Entrepreneur Media ranked us as the best tax franchise opportunity, as well as the seventh fastest growing franchise system, based on the number of new franchise units added in the U.S. and Canada from 2009 to 2010. In February 2012, Forbes ranked us the seventh best franchise in their "Top 20 Franchises for the Buck" list, based on the estimated minimum initial investment, store survival rate, training hours offered and the total number of franchise locations. Accounting Today again honored Liberty Tax Service as a "Top Tax Firm" for 2013. We have focused on keeping the cost of establishing a Liberty Tax franchise relatively low compared to other opportunities available to potential franchisees in order to attract motivated entrepreneurs seeking to minimize their initial costs. We believe this low upfront capital requirement, combined with the potential for attractive office level profitability, provides an opportunity for a significant return on investment for our franchisees. We focus on providing best-in-class training and support to both new and existing franchisees.

Our growth is also reflected in our financial performance. Our total revenues grew to $147.6 million in 2013 from $131.2 million in 2012 and $117.9 million in 2011 , and our net income increased to $17.6 million from $16.4 million in 2012 and $14.7 million in 2011 . Our systemwide revenue, which is the base from which we derive franchise royalties, grew to $381.2 million in 2013 , from $359.1 million in 2012 and $338.6 million in 2011 . Our systemwide revenue represents the total tax preparation revenue generated by our franchised and company-owned offices.

Our Industry and Market Opportunity

We believe that Liberty Tax Service is well positioned to increase our share of the paid tax preparation market because of our strong brand, the strength of our franchise model, and our ability to take advantage of industry consolidation.

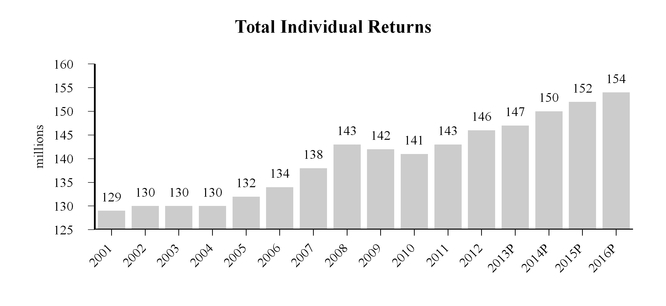

During calendar year 2013, there were estimated to have been 147.4 million tax returns filed with the Internal Revenue Service ("IRS"), of which 132.6 million tax returns were filed during the 2013 tax season. The IRS expects the number of tax returns to continue to grow, and projects a 4.5% increase in tax return filings from 2013 to 2016, as illustrated below.

9

Table of Contents

______________________________________________________________________________

Source: IRS Publication 6187 (revised 6-2013). The "P" designation for calendar years 2013 and later reflects IRS projections.

The tax return preparation market is divided into two primary distinct sectors: paid tax preparation and Do It Yourself ("DIY") preparation, which includes traditional "pen and paper" preparation as well as DIY preparation through online and software-based tax products. Although recent years have seen growth in the relative portion of the DIY sector that has been captured by online and software-based tax products, the separate paid tax preparation sector, in which we and our franchisees primarily compete, has also continued to grow. From the 2001 tax season through the 2013 tax season, the percentage of returns prepared in the DIY sector has varied from 37% to 42%, with 40% of returns in the 2013 tax season prepared in the DIY sector.

The percentage of returns filed through paid tax preparers has remained relatively stable over the past decade, with material year-to-year variations generally in years where government tax rebate programs cause a spike in filings by taxpayers who might otherwise not have filed, or where recessionary conditions, as in 2009, temporarily depress filings. The growth in the number of individual returns reflects a consistent trend over many years, and the historical data and projected IRS information indicates that both the number of individual returns prepared and those prepared by paid tax preparers have increased and we believe it will continue to increase at a relatively constant rate over the next several years. Since the 2001 tax season and through the 2013 tax season, our percentage share of the paid tax preparation market in the United States has increased from 0.2% to more than 2.0%, based on IRS data.

We believe, based on available data, that in 2013 less than 25% of the paid tax preparation market was represented by the national retail tax preparation companies: Liberty Tax and our two national competitors, H&R Block and Jackson Hewitt, each operating under a different business model. While most of our offices are operated by franchisees, H&R Block primarily operates company-owned offices and Jackson Hewitt operates a mixture of franchised and company-owned offices. The remaining paid tax preparation market is primarily comprised of tens of thousands of independent tax preparers operating at a local and regional level. We believe most of these independent preparers operate individual or a limited number of locations.

Our Business Strengths

We attribute our success in the retail tax preparation industry to a number of strengths:

We are a market leader in providing retail tax preparation services. We are presently the third largest provider of retail tax preparation services in the United States and the second largest provider of retail tax preparation services in Canada as measured by number of tax returns prepared and the number of retail offices. We currently have a network of 2,211 franchisees and had more than 4,500 offices for the 2013 tax season, the majority of which had been opened within the past five years, and many of which are in the initial stages of growth. We believe that there is no existing smaller competitor in the retail tax preparation market that could challenge our market position on a national scale due to the expense and length of time required to develop the infrastructure, systems and software necessary to create and support a nationwide network of tax preparation offices. As a result, we believe that it would be difficult for an additional national competitor to emerge in our market for the foreseeable future. Moreover, our brand identity and substantial growth have helped us cement strong repeat business in our

10

Table of Contents

offices. Our brand is reinforced by our Liberty logo and our unique advertising techniques, which include personalized and highly visible marketing strategies. We believe our model creates a powerful platform that allows our franchisees to continue to grow their scale and profitability as they become more seasoned.

A highly scalable and attractive franchise business model. Our franchise model enables us to rapidly expand while keeping capital expenditures and fixed cost investments low. Most of our offices are operated by franchisees, which allows us to focus on marketing, training and expanding our value-added services, while our franchisees focus on locating and opening new office locations and increasing the number of customers at existing locations. We believe that our time-tested and proven franchise strategy, when combined with the economics of our low-cost franchise model, enables us to grow our brand by attracting highly motivated entrepreneurs. Our standard franchise fee per territory is $40,000, which is typically lower than other franchise opportunities, and we offer our franchisees flexible structures and financing options for franchise fees and royalty payments. We believe we offer a stable franchise opportunity and have designed our franchise model to closely align our interests with those of our franchisees in an effort to promote their profitability and return on investment. Our status as a market leader is demonstrated by the fact that we continue to be highly ranked in independent national publications that rank the attractiveness of franchise opportunities and franchisee satisfaction.

Our franchisee and consumer-oriented strategy drives our success and enhances our relationships with our franchisee base. We believe that we must deliver value to both our franchisees and their customers to further drive our success. We encourage a collaborative and open culture among our franchise base and are proactive in providing ongoing training opportunities to both new and established franchisees. We actively manage our franchise base by enforcing franchisee performance standards in order to optimize systemwide revenue and the royalties we receive from our franchisees. Because of the room for growth in our franchise system, we provide our high-quality franchisees the opportunity to increase the number of offices they own and operate. Our franchise model appeals to a select group of highly motivated individuals who are attracted to a platform that requires them to be intensely focused during the relatively short tax season but also enables them to pursue other business and personal endeavors throughout the rest of the year. Because the personal success of our franchisees is directly tied to the success of their individual offices, we believe our franchisees are more focused than the operators of our primary competitors' non-franchised offices on both providing a positive customer service experience and delivering value to their customers.

The paid tax preparation business is inherently a neighborhood business, and we support our franchisees in utilizing our model in a way that allows them to maximize the success of their offices. Franchisees interact directly with existing and potential customers, which drives high customer loyalty within their market areas. In addition, we recognize that some of our customers value the wide range of tax settlement products we enable our franchisees to provide. We have consistently endeavored to provide our franchisees access to a full range of competitive products and services, including ERCs, prepaid debit cards loaded with their tax refund amounts, refund-based loans such as "Instant Cash Advances" or "ICAs," along with other electronic filing products and services. We utilize this mix of franchisee support and services to mitigate the challenges of a franchise business model, which include our lack of direct control over day-to-day operations in the tax offices and our reliance on franchisee growth and expansion to grow our business.

The evolving legal and regulatory climate surrounding some of the tax settlement products that we have made available to our franchisees and their customers has required us to adapt quickly to new limitations that made it more difficult to offer customers the same financial product choices as were available in prior tax seasons. We have adapted to these challenges by developing or obtaining alternatives for customers and by ensuring that we are a market leader in this area, and although the law and regulations may continue to change, we expect to be able to continue to give our franchisees and their customers a range of product choices that will be at least as broad as that offered by our competitors.

Our experienced management team has a proven track record. Our senior management team has significant experience in the tax preparation industry. Our founder, Chairman and CEO, John Hewitt, is a pioneer in the tax preparation industry. Prior to Liberty Tax, Mr. Hewitt began his career with H&R Block and was the founder of Jackson Hewitt. Likewise, our Chief Operating Officer, Rufe Vanderpool, has been with Liberty since 2004, and has been in the tax preparation industry since 1998, and our Chief Financial Officer, Mark Baumgartner, has been with us since 2003. Many of our other key personnel also have a long history of working in the tax preparation industry.

Our Growth Strategy

We believe we are uniquely positioned within the retail tax preparation industry to seize the available growth opportunities. Our strategy for growth includes:

We plan to grow our number of franchised office locations within the U.S. We plan to aggressively expand our number of office locations. We believe there is substantial untapped potential for us to add approximately 6,200 additional offices, after which we would be comparable to the size of our largest national competitor, H&R Block. We believe we can

11

Table of Contents

increase the average number of tax offices operated by our franchisees by continuing to offer programs and support designed to encourage franchisees to expand their business. For example, we intend to place new and existing franchisees in remaining undeveloped geographic territories. In 2008, we began to offer existing franchisees the ability to operate in additional territories for one tax season before electing to acquire those territories. We believe we can achieve this growth because we have a significant number of undeveloped territories. We also offer several innovative programs for new and existing franchisees, including a "zero franchise fee" alternative that allows franchisees to minimize their initial investment in exchange for paying higher royalties during the first five years of the franchise term. In addition, in 2012 we entered into an agreement with Walmart that allowed Liberty Tax kiosks to operate in a number of Walmart stores beginning with the 2013 tax season, when we and our franchisees operated kiosks in nearly 300 stores. We anticipate the expansion of that relationship in the 2014 tax season.

We plan to grow our number of returns. Many of our offices are relatively new, and as they continue to become more seasoned, we believe we will be able to add new customers who we expect will become repeat customers. Approximately 38% of our retail offices open during the 2013 tax season were in the first three years of operation, providing substantial room to add additional customers. Our new retail offices typically experience their most rapid growth during their first five years as they develop customer loyalty, operational experience and a referral base within their community. In addition, we believe that our unique marketing programs, customer oriented services, easy to use tax preparation software, and national presence will continue to drive the number of tax returns prepared in our franchised offices.

We are poised to take advantage of anticipated industry consolidation and strategic opportunities to increase our number of offices and returns. We expect to benefit from anticipated industry consolidation as we believe many independent tax preparers will look to exit the industry as they confront increased costs, regulatory requirements and demands to provide tax settlement products. We believe we will be a beneficiary of this consolidation because we are able to more efficiently address changing regulatory requirements due to our scale and also because we have succeeded in providing a fully competitive mix of the kinds of financial products sought by customers. In addition, our reputation in the market should continue to drive new customers to our brand, which will also enhance our position in a consolidating industry. As a result, we believe we will continue to accrete market share by virtue of our attractive platform for preparers and for new franchisees looking to capture customers from exiting independent preparers. We may also consider larger strategic transactions if those opportunities arise.

We may strategically acquire Area Developer ("AD") areas. We operate under a two-tier franchise system, which includes franchisees operating retail offices in "territories" that encompass a target population of approximately 30,000 people and ADs that operate in areas that include large clusters of territories. We use ADs to help us build out our retail franchise base by marketing available franchise territories. We initiated our AD program in 2001, at a time when we were seeking to accelerate the growth of our franchise system. We continued utilizing the AD program in recent years to focus on areas with large underdeveloped groups of territories we believed would benefit from the dedicated sales attention that an AD would bring to our franchise sales process. We presently have 132 ADs, and as of April 30, 2013 , those ADs had 4,000 unsold franchise territories located within their areas. Our arrangements with our ADs require us to pay a substantial portion of the franchise fees and royalties we receive to our ADs. Although we still expect to grow our franchise network through the limited sale of new AD areas, we will continue to seek opportunities to acquire underperforming AD areas or AD areas in more mature markets at favorable terms, offering us better future profitability from the associated franchise locations as a consequence of repurchasing the area rights of those ADs.

We will leverage our financial products leadership to attract and retain customers and to market our competitive advantage to prospective franchisees. We have expended considerable effort since 2009 to ensure that our franchisees are able to offer a complete range of tax settlement products to our customers, and to provide our customers choices in these products. With Republic's departure from refund anticipation loan ("RAL") lending after the 2012 tax season, there are no remaining banks making or facilitating loan-based tax settlement products, and in anticipation of that situation, we began to pilot an ICA refund loan product originated by a third-party lender in a limited number of states in the 2011 and 2012 tax seasons. These ICAs were offered in 27 states in the 2013 tax season, and we are exploring other alternatives to make refund-based loan tax settlement product choices available to consumers. We are also exploring product alternatives in the states where ICAs are not being offered. At the same time, we expect to continue to offer non-loan tax settlement products such as ERCs to customers in all of our offices. We believe that our innovation in offering alternatives to the traditional RAL will allow us to attract and retain customers by meeting customer demand for quicker access to funds. This competitive advantage over some of our competitors who are not offering similar ranges of products should also permit us to demonstrate to prospective new franchisees, as well as franchisees considering expansion, the potential advantages of the Liberty Tax brand.

Our Business

Our business involves the provision of retail federal and state income tax preparation services and related refund settlement products in the United States and Canada. Virtually all of our services are provided through franchised offices, and for the 2013 tax season, our services were offered in 4,520 retail offices, of which 4,262 were in the United States (with the

12

Table of Contents

remainder in Canada) and 4,028 of our retail offices in the United States, or more than 94%, were owned by franchisees. Unlike some of our primary national competitors, we have maintained a relatively simple business model. We have not attempted to diversify into banking or mortgage operations. By building on steady growth since our founding and using our available financing to fund operations between tax seasons, we have avoided excess leverage while ensuring minimal outstanding indebtedness at the end of each tax season. At April 30, 2013 and 2012 , for example, we had no outstanding balance under our revolving credit facility. Our focus since inception has been on growing the number of Liberty Tax offices, increasing the number of tax returns prepared by those offices, and enhancing profitability by offering services and products that continue to build the Liberty Tax brand.

In the 2013 tax season, we and our franchisees in the United States accounted for more than 1.8 million tax returns filed through our retail offices, and almost 160,000 additional tax returns filed through our online tax software, eSmartTax. Because some of our competitors have been unable to offer a full range of tax settlement products over the last three tax seasons, and because we believe we are positioned to maintain a competitive set of tax settlement products to offer, we believe there is a substantial opportunity to combine our retail office growth with an increase in the number of returns we and our franchisees produce on a per office basis.

A typical tax season consists of two primary filing periods: a "first peak" involving filers who file relatively quickly after receiving their Forms W-2, and late-season filers who file during the weeks leading to the usual April 15 federal tax filing deadline. In the 2013 tax season, 62% of returns filed in our retail offices were filed between January 1 and February 28, and an additional 18% were filed between April 1 and April 15. However, the "first peak" during the 2013 tax season was anomalous in that the IRS did not generally open its online filing system until January 30, 2013, almost two weeks later than in most prior years.

Liberty's Franchise Model

We rely on a franchise model for our growth. Although our larger primary competitors maintain a mix of franchise locations and company-owned offices, we have determined that we can best grow our company by increasing our franchisee base, and the number of offices operated by our existing franchisees. We have also included in our franchisee model the sale of AD areas, and under this AD model, we make large clusters of territories available to an AD who is responsible for marketing the available franchise territories within the larger AD area in order to help us fill gaps in our franchise system. As described below, when we utilize an AD to assist us in franchise sales, we receive revenue from the sale of the AD area, but sacrifice a portion of the franchise fees and the royalty stream from the franchises within the AD area.

Franchise territories. We have divided the United States into approximately 10,000 potential franchise territories We attempt to draw territory boundaries so that each territory has a target population of approximately 30,000 people. Franchisees are permitted to open more than one office in a territory, and within the territory they may also be the beneficiary of the opportunity to open offices located in a retail operation in which we have the opportunity to place a tax preparation kiosk. We presently have kiosk arrangements with certain Walmart, Kmart, Sears, Family Dollar and Ace Cash Express stores, and had 468 such kiosks open during the 2013 tax season, an increase from the 121 such kiosks opened during 2012 tax season, which was attributable almost entirely to our Walmart relationship.

As of April 30, 2013 , our largest franchisee operated 27 tax locations, and a majority of our franchisees operated two or fewer tax locations. As part of our growth strategy, we anticipate increasing substantially the average number of offices per franchisee by encouraging more of our franchisees to acquire and open additional franchise territories. We anticipate that a significant number of our franchisees may elect to remain single-office owners, but that others will be attracted to the opportunity to grow their revenue base and overall profitability by enjoying the economies of scale associated with multi-unit operations. Because we continue to have measurably fewer offices than our two largest competitors, we believe that we have a significant number of additional territories available that will allow us to implement this business model, and we are devoting a substantial amount of our sales efforts to providing opportunities to existing franchisees to acquire additional territories.

AD areas. We initiated our AD program in 2001, at a time when we were seeking to accelerate the growth of our franchise system. We presently have 132 ADs, and as of April 30, 2013 , those ADs had approximately 4,000 unsold franchise territories located within their areas. We continued utilizing the AD program in recent years to focus on areas with large underdeveloped groups of territories we believed would benefit from the dedicated sales attention that an AD would bring to our sales process. Our franchise fees for AD areas vary based on our assessment of the revenue potential of each AD area, and also depend on the performance of any existing franchisees within the AD area being sold. Our ADs generally receive 50% of both the franchise fee and royalties derived from franchises located in their AD areas and are required to provide marketing and operational support.

We strategically repurchase AD areas from existing ADs. In fiscal 2013 , we spent $5.9 million to repurchase 13 AD areas. Because AD franchise agreements generally require us to pay 50% of both the franchise fees and royalty revenue derived

13

Table of Contents

from franchises located in their AD areas to our ADs, we expect that the repurchase of those AD areas will lower our AD expense in future periods. In fiscal 2013 , our ADs in the aggregate earned $3.2 million in franchise fee revenue and $21.5 million in franchise royalties.

When we engage in repurchases of AD areas, we generally value the area by using a discounted cash flow calculation, and we purchase the area on a basis that reflects our expected return from recapturing the post-purchase royalty stream that would otherwise have been paid to the AD. By repurchasing areas at a price that provides liquidity to an AD, we are able to pay off indebtedness of that AD to us, where applicable, and secure the full benefit of franchisee royalty streams for periods after the completion of the repurchase.

Franchise sales process. We engage in an active marketing process, both directly and through our ADs, in order to sell additional franchise territories. Our sales process includes sales to new franchisees, as well as the sale of additional territories to existing franchisees willing to expand into additional territories. For new franchisees, the process includes multiple steps that culminate in a week-long training session that we call Effective Operations Training. We generally require a new franchisee to pay the entire franchise fee for the franchisee's first territory at the time of acquisition, although as described below, we often provide funding for additional territory purchases by both new and existing franchisees. In 2011, we announced a new franchise sales program pursuant to which new and existing franchisees could obtain selected unsold territories without the payment of a franchise fee. Territories acquired under this "zero franchise fee" program, as described below, require higher royalty fees during the first five years of the franchise agreement, but involve less initial financial risk to a potential franchisee. We also utilize advertising in national publications, appearances at conventions and trade shows at which we believe potential franchisees may be present, and various direct marketing techniques, in order to obtain and pursue franchisee leads.

During fiscal 2008, we began to offer two new franchise purchase programs, a "rent to own" program and a "try before you buy" program, both of which were designed to allow existing franchisees to acquire additional territories with minimal risk. In both of these programs, which are designed for the purchase of unsold territories, we allow an existing franchisee that is willing to pursue expansion to operate a territory without an obligation to pay a franchisee fee during the first tax season. If the franchisee operates the territory and elects to retain ownership of the territory, the territory becomes subject to a standard franchise agreement and the payment of the standard franchise fee.

Because of the uncertainty surrounding the availability of tax settlement products, the difficulty that many independent and smaller tax preparers are having accessing sources of these products, and an increasingly cumbersome regulatory climate, we believe that there is an opportunity to convert independent tax preparers, including smaller multi-unit operations, to Liberty Tax franchisees. We are expending significant marketing effort to encourage these conversions, and because these operations involve existing tax operations, generally offer more favorable terms to these prospective franchisees than we make available for undeveloped territories.

Our franchise agreements. Under the terms of our standard franchise agreement, each franchisee receives the right to operate a tax return preparation business under the Liberty Tax Service brand within a designated geographic area. Similarly, our agreements with ADs permit ADs to market franchise territories within a designated multi-territory area. Franchise agreements have an initial term of five years and are renewable. The agreements impose various performance requirements on franchisees, require franchisees to use our proprietary software and equipment designated by us, and obligate our franchisees to operate in their offices in accordance with standards we establish. These standards include specified in-season and out-of-season opening hours, criteria for the location of franchise offices, requirements related to tax preparers and other office employees, and minimum performance standards. Our agreements also require our franchisees to comply with applicable state and federal legal requirements. Although we do not control and are not responsible for any compliance issues that could be caused by our franchisees or their tax preparers, we provide guidance to our franchisees regarding their compliance obligations, including the provision of standard advertising templates, training materials that include detailed compliance information, and systems that alert them to unusual activity. We also use a variety of means to identify potential compliance issues and to require franchisees to address any concerns.

Each year, as part of our active management of our franchise base, we terminate a number of franchisees, and other franchisees voluntarily relinquish their territories, often in exchange for our forbearance on the remaining indebtedness owed to us in connection with the franchise territory. In fiscal 2013 and fiscal 2012 , respectively, approximately 409 and 341 retail tax locations that had been open were subject to voluntary and involuntary franchise terminations. As described below, we generally intend to resell these territories to new or existing franchisees. However, we closed some office locations, and maintained a limited number of office locations that we were not able to resell before the subsequent tax season as company-owned offices. In order to protect our competitive position, we regularly take actions to enforce the non-competition obligations and restrictions regarding customer lists and our trademarks and service marks contained in our franchise agreements.

14

Table of Contents

When a franchisee's right to operate a franchise location is terminated, voluntarily or involuntarily, we evaluate the open office in order to determine whether it will be appropriate to resell that territory, including the existing office location, to a new or existing franchisee. As indicated below, the purchase price for an existing territory differs from the purchase price for an undeveloped territory, because it is based on our assessment of the value of the existing office operation.

Company-Owned Offices. We intentionally operate relatively few company-owned offices. During the 2013 tax season, we operated 261 company-owned offices in the United States and Canada, 155 of which were tax kiosks located in Walmart stores. Tax returns prepared by our company-owned offices represented approximately 2% of the total number of tax returns prepared in the Liberty Tax system in the 2013 tax season. We focus primarily on growing through the opening of new franchise locations, and most of the company-owned offices we operate in a given tax seasons were offices that were previously owned by former franchisees who have ceased operations or did not meet our performance standards. Rather than close offices that we believe have the potential to be successful, we attempt to resell these offices, and when we fail to do so before the beginning of a tax season, we operate company-owned offices through a tax season and until we can resell them at a later time. For this reason, the number of offices that we operate as company-owned offices change substantially from season to season. The significant increase in the number of company-owned offices we operated during the 2013 tax season was attributable to our new Walmart relationship, and our commitment to open a minimum number of tax kiosks in Walmart stores. The Walmart relationship was entered into relatively late during our franchise sales season, and we therefore opened more company-owned kiosks than would be the case in a typical tax season.

Franchise fees and royalties. New franchisees (and existing franchisees acquiring additional territories) presently have several options for acquiring a new undeveloped territory:

• | For new franchisees purchasing their first territory, payment of a franchisee fee of $40,000, a portion of which might be financed (subject to credit approval) by us. |

• | For existing franchisees acquiring additional territories, payment of a franchise fee of $40,000, of which 20% must be paid as a down payment and the balance (subject to credit approval) may be financed by us. |

• | For existing franchisees willing to expand, use of our "try before you buy" or "rent to own" options, which require the same 20% down payment, but allow the franchisees to defer the payment of the down payment until they have operated the territory for most of one tax season and elect to keep the territory. |

• | Alternatively, new and existing franchisees can opt for our new "zero franchise fee" alternative, which allows a new territory to be acquired without the payment of the franchise fee, upon delivery of a minimal security deposit, subject to a franchise agreement that will impose higher royalties, as described below. |

When we resell franchises in existing territories, we generally base the fees payable by a franchisee on the revenue generated by the tax location in prior years, and in some cases may make the "rent to own" or "try before you buy" options available to prospective purchasers. The purchasing franchisee is required to pay what we consider to be a customer list purchase price, representing the value attributable to the prior operations in the franchised office.

Our franchise agreement requires franchisees to pay us:

• | A base royalty equal to 14% of the franchisee's tax preparation revenue, subject to certain specified minimums. |

• | An advertising fee of 5% of the franchisee's tax preparation revenue that we utilize to fund our collective advertising efforts. |

Franchisees acquiring territories under our new "zero franchise fee" alternative will be required to pay us franchise royalties of 25% through the first five tax seasons and thereafter 14% of their tax preparation revenue. These franchisees are also required to pay us advertising fees of 5% each tax season.

Our franchisees generally pay royalties and advertising fees to us during the month following the month in which they accrue. When a franchisee becomes past due on those payments, we have the ability to collect from our franchisees through a "fee intercept" mechanism. Because our franchisees are required to use our electronic systems to make electronic filings for customers, franchise fees and other amounts payable to us by our franchisees can be deducted from the amounts otherwise payable to the franchisee once a tax return is funded by the IRS or state taxing authority. This fee intercept mechanism minimizes our credit risk.

Franchisee loans. We provide a substantial amount of lending to our franchisees (including ADs). In addition to allowing franchisees to defer a portion of their franchise fees, which they pay over time, our franchisees utilize working capital loans to fund their operations between tax seasons, and expenditures they need to make in order to prepare for the following tax season. At April 30, 2013 , our franchisees and ADs were indebted to us in the total amount of $92.3 million , net of

15

Table of Contents

unrecognized revenue of $39.7 million , and we had recorded an allowance for doubtful accounts of $6.7 million . This indebtedness generally takes one of the following forms:

• | The unpaid portion of franchise and AD fees, which does not represent a cash advance by us to the franchisee or AD, but a loan of the franchise or AD fee, generally payable over four (territory franchise fees) to eight years (AD fees). At April 30, 2013 the unrecognized revenue related to these loans was $37.1 million. |

• | Amounts due to us in connection with the purchase price of customer lists for franchisees acquiring previously opened territories. The notes for these amounts are generally payable over five years following the acquisition. At April 30, 2013 the unrecognized revenue related to these loans was $2.6 million. |

• | Annual working capital loans made available to qualified franchisees between May 1 and January 31 each year, which are repayable to us generally by the end of February of the following year. |

• | Amounts payable in connection with promissory notes payable to us for royalty and advertising fee amounts due to us for prior periods, but not paid by a franchisee on a timely basis. |

We utilize our fee intercept mechanism in order to ensure repayment of these amounts by our franchisees, ensuring that repayment occurs from the stream of revenues our franchisees receive from tax preparation and other services. In addition, when a franchise is held by an entity, rather than an individual principal, we generally require an individual guaranty of the franchisee indebtedness.

Franchisee support. We provide substantial support to our franchisees in a variety of ways. Our franchise agreement requires our franchisees to adhere to certain minimum standards, including the use of tax preparation software we provide, the use of computers and other equipment that we select (but that we do not sell to them), training requirements and other criteria. We make substantial training opportunities available to our franchisees and their prospective employees, and we require each franchisee to send representatives to a week-long Effective Operations Training seminar before they are allowed to operate a franchise location. We also make intermediate and advanced training available to our franchisees, offer "Tax School" classes for franchisees and prospective tax preparers, and provide substantial phone and internet-based support, particularly during the tax season. During the tax season, we maintain a fully-staffed operations center, with extended hours, at our corporate headquarters in Virginia Beach, Virginia. During the peak tax season, we hold daily conference calls in which we share and allow other franchisees to share recommendations and techniques for improving office performance, and in which we emphasize the importance of implementing the marketing plan that we recommend as part of our franchisee training.

Our NextGen project is also an integral part of our determination to deliver an improved level of service to our franchisees. In addition to integrating our online and retail-based tax preparation software, we expect the NextGen project, when fully deployed, to improve the ability of our franchisees to comply with financial information protection requirements by moving most tax preparation information to a secure centralized platform, and to provide web-based support services in a way that will be both more accessible to our franchisees and their employees and less expensive for us to provide.

Marketing and Advertising

Our marketing and advertising includes both the marketing efforts we provide and those carried out by our franchisees.

We fund many of our direct marketing efforts using the 5% marketing and advertising fee paid to us by our franchisees. A portion of these fees are made available directly to franchisees to enable them to purchase from third-party vendors marketing and advertising materials that have been developed and approved by us. The remaining fees are used in connection with our provision of advertising and marketing support to our franchisees, including the maintenance of an "ad builder" program that our franchisees use to produce a variety of advertising materials. These fees are also used in connection with our national, regional and local marketing efforts, which are designed to increase brand awareness and attract both early season and late season customers. The direct advertising and marketing support that we provide often includes direct mail and yellow pages advertising (and its online equivalent). We have the capability, and provide the capability to our franchisees, to create sophisticated and demographically targeted advertising programs, and programs that target previous customers.

We embrace and expect our franchisees to adopt what we describe as "guerrilla" marketing techniques, which are intended to create awareness of our franchisee's services and products. For example, we have pioneered the use of "wavers," costumed employees, usually dressed in Lady Liberty costumes, who wave at passing cars and pedestrians and thereby remind potential customers of the availability of Liberty Tax's services. We believe that offices that deploy wavers enjoy substantially greater success than those that decline to utilize this marketing technique. We utilize our website, which includes an office locator, to direct customers to our franchise locations, but because of the significant regulation to which we and our franchisees are subject, do not permit our franchisees to operate independent websites. We also furnish franchisees with complete pre-approved advertising packages, designed to comply with the variety of federal and state regulations that govern the advertising

16

Table of Contents

of our services and products. We also encourage our franchisees to utilize discount coupons and other mechanisms to drive additional customers to their offices.

Tax Courses and Training Preparers

Our franchised and company-owned offices offer a comprehensive catalog of tax education courses. Our basic income tax courses consist of approximately 60 hours of learning and provide students with a general working knowledge of individual income taxes and tax return preparation. We also offer a series of advanced and intermediate courses of varying length to provide a more in depth level of learning to those individuals who already possess a basic understanding of income taxes and income tax return preparation. These courses develop a general interest in tax return preparation and also create public awareness of our brand. Many of the students taking these courses develop an interest in tax return preparation as a career and often become tax preparers for franchisees or our company-owned offices, or later become franchisees. We generally charge our franchisees for the cost of the manuals used to teach our tax preparation courses, and in some jurisdictions, we or our franchisees charge students taking these courses fees that are commensurate with the cost of offering the program and that are designed to ensure that the students taking the courses have a bona fide interest in tax preparation. Our operation of our tax education courses is designed by us to be effectively revenue neutral, and our tax courses are neither a source of significant revenue nor a significant cost in any fiscal year.

Tax Preparation in the Liberty System

Through our franchisees, we offer tax preparation services and related financial products to our tax customers. The services and products that our franchisees implement are designed to provide streamlined tax preparation services for taxpayers who for reasons of complexity, convenience or the need for prompt tax refunds seek assisted tax preparation services.

LibTax software. Our current proprietary tax software program, "LibTax," was first deployed for the 2007 tax season, and offers an interactive question-and-answer format that is easy for our retail office tax preparers to use, and that facilitates tax preparer training. A substantial number of changes are made each year to tax laws, regulations and forms that require us to expend substantial resources every year to develop and maintain tax preparation software, at both the federal level and for every state with income tax filing requirements, that will be ready to be deployed in every Liberty Tax office before the beginning of the tax season.

Electronic filing. The LibTax software also allows tax customers to have their federal and state income tax returns filed electronically. Electronic filing permits taxpayers to receive tax refunds substantially sooner than when a tax return is filed on paper through the mail. Based on information made available by the IRS, we believe that an electronically-filed return for which a refund is direct deposited into a bank account takes an average of 8-15 days for the refund to be made available to a taxpayer, while a refund associated with a mailed return will take 3-5 weeks if the refund is to be direct deposited and 4-6 weeks if the refund is to be mailed to the taxpayer using a government check. Although our software will permit a customer's return to be printed and filed as a paper return, substantially all of our customers utilize the electronic filing option available through our software.

Our financial products. We offer tax settlement financial products to our tax preparation customers because we believe that a substantial portion of our prospective customer base places significant value on the ability to monetize their expected income tax refund more quickly than they would be able to do if they were to file their tax return without utilizing the services of a paid tax preparer. We offer two types of tax settlement products: "refund transfer" products, which involve providing the means by which a customer may receive his or her refund more quickly and conveniently, and refund-based loans.

Refund transfer products. Many of our tax customers seek products that will enable them to obtain access to their tax refunds more quickly than they might otherwise be able to receive those funds. We believe that many of our customers are "unbanked," in that they do not have access to a traditional banking account, and therefore cannot make such an account available to the IRS and other tax authorities for the direct deposit of their tax refunds. Additional customers may have access to a traditional banking account, but for personal reasons, may prefer not to utilize that account for the deposit of their tax refunds. We call our refund transfer product an electronic refund check, or ERC. An ERC involves:

• | a direct deposit of the customer's tax refund into a newly established temporary bank account in the customer's name that we establish with one of our banking partners or other banks that have contracted with JTH Financial, LLC ("JTH Financial"), one of our subsidiaries; or |

• | delivery to the customer of a paper check or a prepaid card containing the balance of the customer's refund after the payment of tax preparation and other fees. |

When the prepaid card option is elected, the card is issued through one of our financial product partners, NetSpend, and is branded with the Liberty Tax logo. In the 2013 tax season, approximately 24,000 of our customers utilized NetSpend cards.

17

Table of Contents

When we deliver a physical refund check to a customer, we are generally able to print the check in one of our retail tax offices on check stock provided by the bank, within a matter of hours after the electronic deposit of the customer's refund has been made to the customer's temporary account. We also enter into check-cashing arrangements with a number of retail establishments, including Walmart, which facilitates the ability of our customers to monetize their check even when they do not have traditional banking relationships.

We offer ERCs in conjunction with other service providers, including providers that have contracted with JTH Financial. Consumer advocacy organizations and some government officials have asserted that non-loan tax settlement products, such as the ERCs we offer, should be treated as loan products or otherwise be more heavily regulated. That argument is also the basis for several lawsuits pending against us. We believe the ERC does not represent a loan or extension of credit, but is merely a means by which a customer's tax refund is delivered after it is received from the taxing authority, but some of these organizations and government officials have alleged that because many customers elect to pay their tax preparation fees out of their tax refunds, such as when their transaction with us is complete because we have delivered the tax refund to them, the "deferral" of the tax preparation fees should be considered a loan or extension of credit, and the fees related to the ERC should be characterized as finance charges. Moreover, as disclosed below, we are subject to a state court decision in California that will require us to disclose the fees related to the ERC as finance charges, although that decision is binding only in California. We do not believe this interpretation will be successful on a broader basis, but if it is successful, it may be more difficult for us to continue to offer ERCs to all our customers. See "Item 1A-Risk Factors-Risks Related to Regulation of Our Industry-Federal and state regulators may impose new regulations on non-loan tax settlement products that would make those products more expensive for us to offer or more difficult for our customers to obtain" and "Item 1A-Risk Factors-Risks Related to Regulation of Our Industry-We may be unsuccessful in litigation that characterizes ERCs as loans, which could subject us to damages and additional regulation, and which could adversely affect our ability to offer tax settlement products and have a material adverse effect on our operations and financial results."

Our ability to offer ERCs depends on the ability and willingness of financial institution service providers to make available the bank accounts into which our customers have their tax refunds deposited. If our financial institution service providers become unable to offer these accounts because of regulatory action, or if our service providers determine that they are unwilling to continue to offer these accounts, or cannot furnish accounts sufficient to meet the demand of our customers, we may not be able to offer ERCs to all our customers. See "Item 1A-Risk Factors-Risks Related to Regulation of Our Industry-If our financial product service providers become unable or unwilling to enable us to offer ERCs, we may be unable to offer tax settlement products to our customers."

Refund-based loans. Through the 2012 tax season, the traditional form of refund-based lending was the RAL, which is a tax refund secured loan that has traditionally been offered by tax preparers through third-party banks.

Prior to the 2010 tax season, some of the larger banks that had previously provided funding for RALs exited the RAL market, in some cases because of regulatory issues unrelated to their RAL lending. We were able to contractually secure additional lending capacity from another bank with which we previously partnered, Republic Bank. For this reason, we were able to offer RALs in all of our eligible offices in both the 2010 and 2011 tax seasons. However, in August 2010, the IRS announced it would no longer provide banks and tax preparers with access to what was known as the debt indicator, or the DI. The DI had previously been made available by the IRS, and provided an indication of whether a taxpayer had an existing lien or other claim against his or her refund that would prevent a RAL from being repaid as expected from the taxpayer's refund. In February 2011, the Federal Deposit Insurance Corporation ("FDIC") initiated an administrative proceeding against Republic Bank seeking to force Republic Bank to cease engaging in RAL lending. In December 2011, Republic Bank settled its administrative proceeding with the FDIC, and as part of that settlement, agreed to discontinue offering RALs following the completion of the 2012 tax season. Given the position taken by the FDIC against Republic Bank in that administrative proceeding, we do not believe that other federally-insured financial institutions are likely to enter the RAL business. See "Item 1A-Risk Factors-Risks Related to Regulation of Our Industry-Federal and state legislators and regulators have increasingly taken an active role in regulating tax settlement products, and because our ability to offer these products in future tax seasons may be limited, demand for our services may be reduced, we may be exposed to additional credit risk and our business may be harmed."

Since the 2011 tax season, we have partnered with non-bank counterparties to develop alternative refund-based loan and non-loan tax settlement products, including ICA loans. During the 2011 tax season, we engaged in pilot projects designed to provide loans through third-party ICAs to customers in one state, and during the 2012 tax season, ICAs were available to customers in seven states. The ICA program expanded for the 2013 tax season to 27 states. However, due largely to the condensed tax season and the issues caused by the fiscal cliff, the ICA program was only offered to our customers for 14 days during the 2013 tax season. In order to make these loans available, we contracted with a non-bank lender and developed our own proprietary system to process these transactions. We receive income from the provision of these products through the payment of fees for services by our financial product partners, but we also take additional risk because we may agree to

18

Table of Contents

repurchase loans that are not repaid or repurchased by the non-bank lender. Moreover, ICA loans cannot be offered in every state, and the program may not be significantly expanded beyond the number of states in which the program was made available during the 2013 tax season.See "Item 1A-Risk Factors-Risks Related to Our Business-The loan products made available through non-bank lenders may be limited in scope, are dependent on the availability of financing, may be more expensive and could subject us to greater risk of loss."

Notwithstanding our inability to offer RALs, and limitations on the ability to offer ICAs in all jurisdictions, we believe the continued availability of ERCs will enable us to continue to offer an adequate mix of tax settlement products to our customers. Although the number of refund-based loans obtained by our customers has declined significantly since the 2010 tax season, the "attachment rate" for tax settlement products, which we define as the rate at which our customers elect one of the financial products we offer, irrespective of whether the product is a loan-based product or an ERC, has remained relatively stable, and was 54% in the 2011 tax season, 51% in the 2012 tax season, and 54% in the 2013 tax season. The stability of this attachment rate reflects the fact that as our customers have obtained fewer refund-based loans (whether voluntarily or as a result of their reduced availability), they have generally shifted their tax settlement product choice to ERCs.

Integration of product offerings. The LibTax software makes each of our product offerings available to our customers, including loan-based products and refund transfer products. We believe that this integration of our products into our tax preparation software is essential to attracting customers to the tax preparation services offered in our retail office locations.