|

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________________________________

FORM 10-K | ||||

_______________________________________________________________________

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

December 31, 2014

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

______________________________________________________________________ _

STRYKER CORPORATION

(Exact name of registrant as specified in its charter)

_______________________________________________________________________

Michigan |

| 38-1239739 |

(State of incorporation) |

| (I.R.S. Employer Identification No.) |

2825 Airview Boulevard, Kalamazoo, Michigan |

| 49002 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code: (269) 385-2600

_______________________________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common Stock, $.10 par value |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ý NO o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES o NO ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities and Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ý NO o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ý NO o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of large "accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ý |

| Accelerated filer o |

Non-accelerated filer o |

| Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES o NO ý

Based on the closing sales price of June 30, 2014 , the aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $29,425,287,926 . The number of shares outstanding of the registrant's common stock, $.10 par value, was 378,749,951 at January 31, 2015 .

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement to be filed with the U.S. Securities and Exchange Commission relating to the 2015 Annual Meeting of Shareholders (the 2015 proxy statement) are incorporated by reference into Part III.

|

STRYKER CORPORATION 2014 Form 10-K

TABLE OF CONTENTS

|

|

| |

PART I |

| ||

Item 1. | Business | 1 | |

Item 1A. | Risk Factors | 4 | |

Item 1B. | Unresolved Staff Comments | 6 | |

Item 2. | Properties | 6 | |

Item 3. | Legal Proceedings | 7 | |

Item 4. | Mine Safety Disclosures | 7 | |

|

| ||

PART II |

| ||

Item 5. | Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 7 | |

Item 6. | Selected Financial Data | 8 | |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 9 | |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 16 | |

Item 8. | Financial Statements and Supplementary Data | 17 | |

| Report of Independent Registered Public Accounting Firm on Consolidated Financial Statements | 17 | |

| Consolidated Statements of Earnings | 18 | |

| Consolidated Statements of Comprehensive Income | 18 | |

| Consolidated Balance Sheets | 19 | |

| Consolidated Statements of Shareholders' Equity | 20 | |

| Consolidated Statements of Cash Flows | 21 | |

| Notes to Consolidated Financial Statements | 22 | |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 34 | |

Item 9A. | Controls and Procedures | 34 | |

Item 9B. | Other Information | 35 | |

|

| ||

PART III |

| ||

Item 10. | Directors, Executive Officers and Corporate Governance | 35 | |

Item 11. | Executive Compensation | 35 | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 35 | |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 35 | |

Item 14. | Principal Accounting Fees and Services | 35 | |

|

| ||

PART IV |

| ||

Item 15. | Exhibits, Financial Statement Schedules | 36 | |

STRYKER CORPORATION 2014 Form 10-K

PART I |

ITEM 1. | BUSINESS. |

General

Stryker Corporation is one of the world's leading medical technology companies, with 2014 revenues of $9,675 and net earnings of $515 . Stryker's products include implants used in joint replacement and trauma surgeries; surgical equipment and surgical navigation systems; endoscopic and communications systems; patient handling and emergency medical equipment; neurosurgical, neurovascular and spinal devices; as well as other medical device products used in a variety of medical specialties.

Stryker was incorporated in Michigan in 1946 as the successor company to a business founded in 1941 by Dr. Homer H. Stryker, a prominent orthopaedic surgeon and the inventor of several orthopaedic products. In the United States, most of our products are marketed directly to doctors, hospitals and other healthcare facilities. Internationally, our products are sold in over 100 countries through company-owned sales subsidiaries and branches as well as third-party dealers and distributors.

As used herein, and except where the context otherwise requires, "Stryker," "we," "us," and "our" refer to Stryker Corporation and its consolidated subsidiaries.

Business Segments and Geographic Information

In December 2014 we changed the name of our Reconstructive business segment to Orthopaedics. This change did not change the composition of any of our business segments and had no financial impact.

We segregate our reporting into three reportable business segments: Orthopaedics, MedSurg, and Neurotechnology and Spine. Financial information regarding our reportable business segments and certain geographic information is included under "Results of Operations" in Item 7 of this report and Note 12 to the Consolidated Financial Statements in Item 8 of this report.

Net sales by reportable segment over the last three years were:

| 2014 |

| 2013 |

| 2012 | ||||||||||||

Orthopaedics | $ | 4,153 | | 43 | % |

| $ | 3,949 | | 44 | % |

| $ | 3,823 | | 44 | % |

MedSurg | 3,781 | | 39 | % |

| 3,414 | | 38 | % |

| 3,265 | | 38 | % | |||

Neurotechnology and Spine | 1,741 | | 18 | % |

| 1,658 | | 18 | % |

| 1,569 | | 18 | % | |||

Total | $ | 9,675 | | 100 | % |

| $ | 9,021 | | 100 | % |

| $ | 8,657 | | 100 | % |

Orthopaedics

Orthopaedics products consist primarily of implants used in hip and knee joint replacements and trauma and extremities surgeries. We bring patients and physicians advanced implant designs and specialized instrumentation that make orthopaedic surgery and recovery simpler, faster and more effective. We support surgeons with the technology and services they need as they develop new surgical techniques.

Stryker is one of five leading competitors globally for joint replacement and trauma products; the other four are Zimmer Holdings, Inc. (Zimmer), DePuy Synthes Company, a subsidiary of Johnson & Johnson, Biomet, Inc. and Smith & Nephew plc (Smith & Nephew).

The composition of net sales of Orthopaedics products over the last three years was:

| 2014 |

| 2013 |

| 2012 | ||||||||||||

Knees | $ | 1,396 | | 34 | % |

| $ | 1,371 | | 35 | % |

| $ | 1,356 | | 35 | % |

Hips | 1,291 | | 31 | % |

| 1,272 | | 32 | % |

| 1,233 | | 32 | % | |||

Trauma and Extremities | 1,230 | | 30 | % |

| 1,116 | | 28 | % |

| 989 | | 26 | % | |||

Other | 236 | | 5 | % |

| 190 | | 5 | % |

| 245 | | 7 | % | |||

Total | $ | 4,153 | | 100 | % |

| $ | 3,949 | | 100 | % |

| $ | 3,823 | | 100 | % |

In September 2014 we acquired certain assets of Small Bone Innovations, Inc. (SBi) for an aggregate purchase price of approximately $ 358 . SBi products are designed and promoted for upper and lower extremity small bone indications, with a focus on small joint replacement.

In December 2013 we acquired MAKO Surgical Corp. (MAKO). The acquisition of MAKO, combined with our strong history in joint reconstruction, capital equipment (operating room integration and surgical navigation) and surgical instruments, will help further advance the growth of robotic arm assisted surgery. Our combined expertise offers the potential to simplify joint reconstruction procedures, reduce variability and enhance the surgeon and patient experience.

In March 2013 we acquired Trauson Holdings Company Limited (Trauson). The acquisition of Trauson enhances our product offerings, primarily within our Orthopaedics segment, broadens our presence in China and enables us to expand into the fast growing value segment of the emerging markets.

In 2013 we launched the Tritanium Cementless Baseplate for our Triathlon Knee Arthroscopy (TKA) system, which combines biologic fixation with Triathlon's kinematics to provide surgeons with a superior option for cementless TKA. We also launched the Secur-Fit Advanced Femoral Hip Stem, which facilitates the accurate restoration of biomechanics when used with our new and unique Stryker Orthopaedics Modeling and Analytics system.

In 2012 we voluntarily recalled our Rejuvenate and ABG II Modular-Neck hip stems and terminated global distribution of these hip products. We notified healthcare professionals and regulatory bodies of this recall, which was taken due to potential risks associated with fretting and/or corrosion that may lead to adverse local tissue reactions. In November 2014 we entered into a Settlement Agreement (the "Settlement Agreement") to compensate eligible United States patients who had surgery to replace their Rejuvenate and ABG II modular-neck hip stems, known as a "revision surgery", prior to November 3, 2014. To date we have recorded charges to earnings totaling $1,534 ($1,713 before $179 of third party insurance recoveries) representing the actuarially determined low end of the range of probable loss to resolve this entire matter globally. It is expected that a majority of the payments under the Settlement Agreement will be made by the end of 2015. See Note 7 to the Consolidated Financial Statements in Item 8 of this report for further information.

In 2012 we launched Accolade II, the first hip stem with a Morphometric Wedge design, an evolution of the tapered wedge stem.

MedSurg

MedSurg products include surgical equipment and surgical navigation systems (Instruments); endoscopic and communications systems (Endoscopy); patient handling and emergency medical equipment (Medical); and reprocessed and remanufactured medical devices (Sustainability) as well as other medical device products used in a variety of medical specialties.

1 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

Stryker is one of four market leaders in Instruments, competing principally with Zimmer, Medtronic plc. and ConMed Linvatec, Inc., a subsidiary of CONMED Corporation (ConMed Linvatec) globally. In Endoscopy, we compete with Smith & Nephew Endoscopy, ConMed Linvatec, Inc., Arthrex, Inc., Karl Storz GmbH & Co. and Olympus Optical Co. Ltd. Our primary competitor in Medical is Hill-Rom Holdings, Inc.

The composition of net sales of MedSurg products over the last three years was:

| 2014 |

| 2013 |

| 2012 | ||||||||||||

Instruments | $ | 1,424 | | 38 | % |

| $ | 1,269 | | 37 | % |

| $ | 1,261 | | 39 | % |

Endoscopy | 1,382 | | 37 | % |

| 1,222 | | 36 | % |

| 1,111 | | 34 | % | |||

Medical | 766 | | 20 | % |

| 710 | | 21 | % |

| 691 | | 21 | % | |||

Sustainability | 209 | | 5 | % |

| 213 | | 6 | % |

| 202 | | 6 | % | |||

Total | $ | 3,781 | | 100 | % |

| $ | 3,414 | | 100 | % |

| $ | 3,265 | | 100 | % |

In January 2015 we announced the asset acquisition of privately-held CHG Hospital Beds, Inc. ("CHG") in an all cash transaction. CHG, headquartered in London, Ontario, Canada, manufactures and markets low-height hospital beds and related accessories across Canada, and in the United States and the United Kingdom.

In April 2014 we acquired Berchtold Holding, AG (Berchtold), a privately-held business with operations in Germany and the United States, for an aggregate purchase price of approximately $184. Berchtold sells surgical tables, equipment booms and surgical lighting systems. In March 2014 we acquired Patient Safety Technologies, Inc. (PST), for an aggregate purchase price of $120. PST conducts its business through its wholly owned subsidiary, SurgiCount Medical, Inc. PST's proprietary Safety-Sponge ® System and SurgiCount 360™ compliance software help prevent Retained Foreign Objects in the operating room. Other business acquisitions in 2014 include the acquisition of Pivot Medical, Inc. (Pivot), which develops and sells innovative products for hip arthroscopy.

In March 2013 we received a warning letter from the United States Food and Drug Administration (FDA) concerning quality system observations made during an inspection and citing us for failing to notify the FDA of a product recall and for marketing devices, including certain of our Neptune Waste Management Systems, without a required 510(k) clearance. We were notified in January 2014 that the actions taken to address issues raised in the warning letter were sufficient and no further corrective actions related to the warning letter were required.

In December 2013 we received 510(k) clearance to market a modified Neptune 2 Waste Management System. The Neptune 2 Waste Management System mitigates risks to healthcare workers by eliminating harmful exposure to fluids and smoke in the operating room. This constantly closed system collects surgical waste and disposes of it without exposing the operator to contact with infectious fluids and surgical plumes.

In 2012 we launched System 7, the next generation of heavy duty surgical power tools. These tools are used in total joint procedures, such as hip and knee replacements, and offer the latest in advanced cutting technology. We also launched the 1488 HD 3-Chip Endoscopic Camera System, which utilizes advanced CMOS technology and premium optics to provide a clear bright image designed to enhance patient outcomes. In addition, we launched Power-LOAD TM , our cot fastener system that lifts and lowers the cot into and out of ambulances, thereby reducing spinal loads and the risk of cumulative trauma injuries to emergency responders.

Neurotechnology and Spine

Our Neurotechnology and Spine products include both neurosurgical and neurovascular devices. Our neurotechnology offering includes products used for minimally invasive endovascular techniques; a comprehensive line of products for traditional brain and open skull base surgical procedures; orthobiologic and biosurgery products, including synthetic bone grafts and vertebral augmentation products; and minimally invasive products for the treatment of acute ischemic and hemorrhagic stroke. We also develop, manufacture and market spinal implant products including cervical, thoracolumbar and interbody systems used in spinal injury, deformity and degenerative therapies.

Our primary competitors in Neurotechnology are Medtronic, including Covidien, which was recently acquired by Medtronic, and Johnson & Johnson. We are one of five market leaders in Spine, along with Medtronic Sofamor Danek, Inc. (a subsidiary of Medtronic), DePuy Synthes (a subsidiary of Johnson & Johnson), Nuvasive, Inc. and Globus Medical, Inc.

The composition of net sales of Neurotechnology and Spine products over the last three years was:

| 2014 |

| 2013 |

| 2012 | ||||||||||||

Neurotechnology | $ | 1,001 | | 57 | % |

| $ | 915 | | 55 | % |

| $ | 842 | | 54 | % |

Spine | 740 | | 43 | % |

| 743 | | 45 | % |

| 727 | | 46 | % | |||

Total | $ | 1,741 | | 100 | % |

| $ | 1,658 | | 100 | % |

| $ | 1,569 | | 100 | % |

In 2012 we received 510(k) clearance to market the Trevo ® Pro Retriever, our next generation clot removal technology that utilizes proprietary Stentriever ® Technology for optimized clot integration and retrieval in patients experiencing acute ischemic stroke. In addition, we received 510(k) clearance to market our Trevo ® ProVEU TM Retriever, the first clot removal device fully visible during the procedure for precise positioning within the clot and optimized clot retrieval in patients experiencing acute ischemic stroke.

Geographic Areas

In 2014 approximately 68.0% of our revenues were generated from customers in the United States. Additional geographic information is included under "Results of Operations" in Item 7 of this report and Note 12 to the Consolidated Financial Statements in Item 8 of this report.

Raw Materials and Inventory

Raw materials essential to our business are generally readily available from multiple sources. Substantially all products we manufacture are stocked in inventory, while certain MedSurg products are assembled to order. The dollar amount of backlog orders at any given time is not considered material to an understanding of our business taken as a whole.

Patents and Trademarks

Patents and trademarks are significant to our business to the extent that a product or an attribute of a product represents a unique design or process. Patent protection of such products restricts competitors from duplicating these unique designs and features. We seek to obtain patent protection on our products whenever appropriate for protecting our competitive advantage. As of December 31, 2014 we owned approximately 1,900 United States patents and approximately 3,400 international patents.

Seasonality

Our business is generally not seasonal in nature; however, the number of Orthopaedics implant surgeries is generally lower during the summer months and sales of capital equipment are generally higher in the fourth quarter.

2 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

Competition

In all of our product lines we compete with local and global companies located throughout the world. Competition exists in all product lines without regard to the number and size of the competing companies involved. The development of new and innovative products is important to our success in all areas of our business and competition in research, involving the development and the improvement of new and existing products and processes, is particularly significant. The competitive environment requires substantial investments in continuing research and in maintaining sales forces.

The principal factors that we believe differentiate us in the highly competitive product categories in which we operate and enable us to compete effectively include our commitment to innovation and quality, service and reputation. We believe that our competitive position in the future will depend to a large degree on our ability to develop new products and make improvements to existing products.

Product Development

Most of our products and product improvements have been developed internally at research facilities in the United States, Ireland, Puerto Rico, Germany, Switzerland, India and France. We also invest through acquisitions in technologies developed by third parties that have the potential to expand the markets in which we operate. We maintain close working relationships with physicians and medical personnel in hospitals and universities who assist us in product development efforts. The total costs of research, development and engineering activities were $614, $536, and $471 in 2014, 2013 and 2012, respectively.

Regulation

Our businesses are subject to varying degrees of governmental regulation in the countries in which we operate, and the general trend is toward increasingly stringent regulation.

In the United States, the Medical Device Amendments of 1976 to the Federal Food, Drug and Cosmetic Act and its subsequent amendments, and the regulations issued and proposed thereunder, provide for regulation by the FDA of the design, manufacture and marketing of medical devices, including most of our products. Many of our new products fall into FDA classifications that require notification submitted as a 510(k) and review by the FDA before we begin marketing them. Certain of our products require extensive clinical testing, consisting of safety and efficacy studies, followed by pre-market approval (PMA) applications for specific surgical indications.

The FDA's Quality System regulations set forth standards for our product design and manufacturing processes, require the maintenance of certain records and provide for inspections of our facilities by the FDA. There are also certain requirements of state and local and foreign governments that must be complied with in the manufacture and marketing of our products.

The member states of the European Union (EU) have adopted the European Medical Device Directives that form a single set of medical device regulations for all EU member countries. These regulations require companies that wish to manufacture and distribute medical devices in EU member countries to meet certain quality system requirements and obtain CE marking for their products. We have authorization to apply the CE marking to substantially all of our products. In addition, we comply with the unique regulatory requirements of each of the countries in Europe and other countries in which we market our products.

Initiatives sponsored by government agencies, legislative bodies and the private sector to limit the growth of healthcare expenses

generally and hospital costs in particular, including price regulation and competitive pricing, are ongoing in markets where we do business. It is not possible to predict at this time the long-term impact of such cost containment measures on our future business. In addition, business practices in the healthcare industry have come under increased scrutiny, particularly in the United States, by government agencies and state attorneys general, and resulting investigations and prosecutions carry the risk of significant civil and criminal penalties.

Employees

At December 31, 2014 , we had approximately 26,000 employees worldwide. Certain international employees are covered by collective bargaining agreements. We believe that we maintain positive relationships with our employees worldwide.

Executive Officers of the Registrant

The names and ages of our executive officers as of January 31, 2015 and certain information about them are:

Name | Age |

| First Became an Executive Officer |

Kevin A. Lobo | 49 | Chairman, President and Chief Executive Officer | 2011 |

Steven P. Benscoter | 47 | Vice President, Human Resources | 2012 |

William E. Berry Jr. | 49 | Vice President, Corporate Controller and Principal Accounting Officer | 2014 |

Lonny J. Carpenter | 53 | Group President, Global Quality and Operations | 2008 |

David K. Floyd | 54 | Group President, Orthopaedics | 2012 |

Michael D. Hutchinson | 44 | General Counsel | 2014 |

William R. Jellison | 57 | Vice President and Chief Financial Officer | 2013 |

Katherine A. Owen | 44 | Vice President, Strategy and Investor Relations | 2007 |

Bijoy S.N. Sagar | 46 | Vice President, Chief Information Officer | 2014 |

Timothy J. Scannell | 50 | Group President, MedSurg and Neurotechnology | 2008 |

Ramesh Subrahmanian | 53 | Group President, International | 2011 |

Each of our executive officers was elected by our Board of Directors to serve in the office indicated until the first meeting of the Board of Directors following the annual meeting of shareholders in 2015 or until a successor is chosen and qualified or until his or her resignation or removal. Each of our executive officers has held the position above or has served Stryker in various executive or administrative capacities for at least five years, except for Mr. Lobo, Mr. Berry, Mr. Jellison, Mr. Sagar, Mr. Subrahmanian and Mr. Floyd. Prior to joining Stryker in April 2011, Mr. Lobo held a variety of senior level leadership roles for the previous nine years at Johnson & Johnson, most recently as Worldwide President of Ethicon Endo-Surgery. Prior to joining Stryker in August 2011, Mr. Berry served for two years as Assistant Corporate Controller for Whirlpool Corporation, the world's leading manufacturer and marketer of major home appliances, and before that held a variety of senior finance roles at Delphi Automotive and Federal Mogul Corporation, both global automotive parts manufacturers. Prior to joining Stryker in April 2013, Mr. Jellison was Senior Vice President and Chief Financial Officer at Dentsply International, the world's largest manufacturer of professional dental products, and before that held a variety of senior level leadership roles over a 15-year period at Dentsply. Prior to joining Stryker in May 2014, Mr. Sagar served

3 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

as the Chief Information officer for Merck Millipore, and before that as Global Head of Information Systems and a member of the divisional board for the chemicals division of Merck KGaA. Prior to joining Stryker in September 2011, Mr. Subrahmanian was the Senior Vice President & President, Asia Pacific Human Health with Merck & Co. Inc. Prior to joining Stryker in November 2012, Mr. Floyd was the Chief Executive Officer for OrthoWorx and held a variety of senior level leadership roles with DePuy (a division of Johnson & Johnson), Abbott Spine, AxioMed Spine, and Centerpulse Orthopaedics.

Available Information

Our main corporate website address is www.stryker.com. Copies of our Quarterly Reports on Form 10-Q, Annual Reports on Form 10-K and Current Reports on Form 8-K filed or furnished to the United States Securities and Exchange Commission (SEC) will be provided without charge to any shareholder submitting a written request to our Corporate Secretary at our principal executive offices. All of our SEC filings are also available free of charge on our website within the "For Investors - SEC Filings & Ownership Reports" link as soon as reasonably practicable after having been electronically filed or furnished to the SEC. All SEC filings are also available at the SEC's website at www.sec.gov .

ITEM 1A. | RISK FACTORS. |

This report contains statements referring to us that are not historical facts and are considered "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. These statements, which are intended to take advantage of the "safe harbor" provisions of the Reform Act, are based on current projections about operations, industry conditions, financial condition and liquidity. Words that identify forward-looking statements include words such as "may," "could," "will," "should," "possible," "plan," "predict," "forecast," "potential," "anticipate," "estimate," "expect," "project," "intend," "believe," "may impact," "on track," and words and terms of similar substance used in connection with any discussion of future operating or financial performance, an acquisition or our businesses. In addition, any statements that refer to expectations, projections or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Those statements are not guarantees and are subject to risks, uncertainties and assumptions that are difficult to predict. Therefore, actual results could differ materially and adversely from these forward-looking statements. Some important factors that could cause our actual results to differ from our expectations in any forward-looking statements include the risks discussed below.

Our operations and financial results are subject to various risks and uncertainties that could adversely affect our business, cash flows, financial condition and results of operations. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, cash flows, financial condition or results of operations.

LEGAL AND REGULATORY RISKS

The impact of United States healthcare reform legislation on our business remains uncertain. In 2010 federal legislation to reform the United States healthcare system was enacted into law. The legislation is far-reaching and is intended to expand access to health insurance coverage and improve the quality and reduce the costs of healthcare over time. Its provisions become effective at various dates and there are many programs and requirements for which the details have not been determined. We expect the law will have a significant impact upon various aspects of our business operations. Among other things, the law imposed a 2.3 percent

excise tax on Class I, II and III medical devices that applies to United States sales of a majority of our medical device products. Other provisions of this legislation, including Medicare provisions aimed at improving quality and decreasing costs, comparative effectiveness research, an independent payment advisory board, and pilot programs to evaluate alternative payment methodologies, could meaningfully change the way healthcare is developed and delivered. Further, we cannot predict what other healthcare programs and regulations will be ultimately implemented at the federal or state level or the effect of any future legislation or regulation in the United States on our business and results of operations

We may be adversely affected by product liability claims, unfavorable court decisions or legal settlements. Our business exposes us to potential product liability risks that are inherent in the design, manufacture and marketing of medical devices, many of which are intended to be implanted in the human body for long periods of time or indefinitely. We are currently defendants in a number of product liability matters, including those relating to our Rejuvenate and ABGII Modular-Neck hip stems discussed in Note 7 to the Consolidated Financial Statements in Item 8 of this report. These matters are subject to many uncertainties and outcomes are not predictable. In addition, we may incur significant legal expenses regardless of whether we are found to be liable. We are currently self-insured for product liability-related claims and expenses. The ultimate cost to us with respect to product liability claims could be materially different than the amount of the current estimates and accruals and could have a material adverse effect on our financial position, results of operations and cash flows.

Intellectual property litigation and infringement claims could cause us to incur significant expenses or prevent us from selling certain of our products. The medical device industry is characterized by extensive intellectual property litigation and, from time to time, we are the subject of claims by third parties of potential infringement or misappropriation. Regardless of outcome, such claims are expensive to defend and divert the time and effort of management and operating personnel from other business issues. A successful claim or claims of patent or other intellectual property infringement against us could result in our payment of significant monetary damages and/or royalty payments or negatively impact our ability to sell current or future products in the affected category.

Dependence on patent and other proprietary rights and failing to protect such rights or to be successful in litigation related to such rights may impact offerings in our product portfolios. Our long-term success largely depends on our ability to market technologically competitive products. If we fail to obtain or maintain adequate intellectual property protection, such a failure could allow others to sell products that compete with offerings in our product portfolio. Also, our issued patents are subject to claims concerning priority, scope and other issues, and currently pending or future patent applications may not result in issued patents.

We are subject to extensive governmental regulations relating to the manufacturing, labeling and marketing of our products. Substantially all of our products are subject to regulation by the FDA and other governmental authorities in the United States and internationally. The process of obtaining regulatory approvals to market a medical device can be costly and time consuming and approvals might not be granted for future products on a timely basis, if at all. We have ongoing responsibilities under FDA regulations with respect to our products and facilities and are subject to periodic inspections by the FDA to determine compliance with the quality system and medical device reporting regulations and other requirements. If we fail to fully comply with applicable regulatory requirements, we may be subject to a range of sanctions, including

4 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

warning letters, product recalls, the suspension of product manufacturing, monetary fines and criminal prosecution.

We are subject to federal, state and foreign healthcare regulations, including fraud and abuse laws, as well as anti-bribery laws, and could face substantial penalties if we fail to fully comply with such regulations and laws. Our relationship with healthcare professionals, such as physicians, hospitals and those that may market our products, are subject to scrutiny under various state and federal laws often referred to collectively as healthcare fraud and abuse laws. In addition, the United States and foreign government regulators have increased the enforcement of the Foreign Corrupt Practices Act and other anti-bribery laws. These laws are broad in scope and are subject to evolving interpretation, which could require us to incur substantial costs to monitor compliance or to alter our practices if we are found not to be in compliance. We also must comply with a variety of other laws which protect the privacy of individually identifiable healthcare information and impose extensive tracking and reporting related to all transfers of value provided to certain healthcare professionals. Violations of these laws may be punishable by criminal or civil sanctions, including substantial fines, imprisonment and exclusion from participation in governmental healthcare programs.

MARKET RISKS

Macroeconomic developments could negatively affect our ability to conduct business in affected regions. Financial difficulties experienced by our customers, including distributors, and suppliers could result in product delays and inventory issues; risks to accounts receivable could also include delays in collection and greater bad debt expense.

Exposure to exchange rate fluctuations on cross border transactions and translation of local currency results into United States dollars. We report our financial results in United States Dollars and approximately one-third of our revenues are denominated in foreign currencies, including the Euro, the British Pound, and the Japanese Yen. Cross border transactions, both with external parties and intercompany relationships, result in increased exposure to foreign exchange effects. Our results of operations and, in some cases, cash flows, have been and may in the future be adversely affected by movements in foreign exchange rates. While we implement currency hedges to partially reduce our exposure to changes in foreign currency exchange rates; our hedging strategies may not be successful, and our unhedged exposures continue to be subject to currency fluctuations. In addition, the weakening or strengthening of the United States dollar results in favorable or unfavorable translation effects when the results of our foreign locations are translated into United States dollars for inclusion in our consolidated financial statements and results.

BUSINESS AND OPERATIONAL RISKS

Cost containment measures in the United States and other countries resulting in pricing pressures could have a negative impact on our future operating results. Initiatives sponsored by government agencies, legislative bodies and the private sector to limit the growth of healthcare costs, including price regulation and competitive pricing, are ongoing in markets where we do business. Pricing pressure has also increased in our markets due to continued consolidation among healthcare providers, trends toward managed care, the shift towards governments becoming the primary payers of healthcare expenses, and government laws and regulations relating to sales and promotion, reimbursement and pricing generally. Reductions in reimbursement levels or coverage for our products or other cost containment measures, including any that reduce medical procedure volumes, could unfavorably affect our future operating results.

We may be unable to effectively develop and market products against the products of our competitors in a highly competitive industry. Our present or future products could be rendered obsolete or uneconomical by technological advances by our competitors. Competitive factors include price, customer service, technology, innovation, quality, reputation and reliability. Our competition may respond more quickly to new or emerging technologies, undertake more extensive marketing campaigns, have greater financial, marketing and other resources or be more successful in attracting potential customers, employees and strategic partners. Given these factors, we cannot guarantee that we will be able to continue our level of success in the industry.

Competition in the development and improvement of new and existing products is particularly significant and results from time to time in product obsolescence. The markets in which we operate are highly competitive, and new products and surgical procedures are introduced on an ongoing basis. Such marketplace changes may cause some of our products to become obsolete. If actual product life cycles, product demand or acceptance of new product introductions are less favorable than projected by management, a higher level of inventory write downs may result.

We may be unable to maintain adequate working relationships with healthcare professionals. We seek to maintain close working relationships with respected physicians and medical personnel in hospitals and universities who assist in product research and development. We rely on these professionals to assist us in the development of proprietary products and product improvements to complement and expand our existing product lines. If we are unable to maintain these relationships, our ability to develop, market and sell new and improved products could decrease.

We are subject to additional risks associated with our extensive international operations. We develop, manufacture and distribute our products throughout the world. Our international operations are subject to a number of additional risks and potential costs, including changes in foreign medical reimbursement policies and programs, unexpected changes in foreign regulatory requirements, differing local product preferences and product requirements, diminished protection of intellectual property in some countries, trade protection measures and import or export licensing requirements, difficulty in staffing and managing foreign operations, political and economic instability. Our results of operations and/or financial condition could be adversely impacted if we are unable to successfully manage these and other risks of international operations in an increasingly volatile environment.

We may be unable to capitalize on previous or future acquisitions. In addition to internally developed products, we rely upon investment in new technologies through acquisitions. Investments in medical technology are inherently risky, and we cannot guarantee that any acquisition will be successful or will not have a material unfavorable impact on us. These risks include the activities required to integrate new businesses, which may result in the need to allocate more resources to integration and product development activities than originally anticipated, diversion of management time, which could adversely affect management's ability to focus on other projects, the inability to realize the expected benefits, savings or synergies from the acquisition, the loss of key personnel of the acquired company, and exposure to unexpected liabilities of the acquired company. In addition, we cannot be certain that the businesses we acquire will become profitable or remain so, which may result in unexpected impairment charges.

5 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

We may record future goodwill impairment charges related to one or more of our business units, which could materially adversely impact our results of operations. We perform our annual impairment test for goodwill in the fourth quarter of each year, or more frequently if indicators are present or changes in circumstances suggest that impairment may exist. In evaluating the potential for impairment we make assumptions regarding revenue projections, growth rates, cash flows, tax rates, and discount rates. These assumptions are uncertain and by nature may vary from actual results. A significant reduction in the estimated fair values could result in impairment charges that could materially affect our results of operations.

Our results of operations could be negatively impacted by future changes in the allocation of income to each of the income tax jurisdictions in which we operate. We operate in multiple income tax jurisdictions both in the United States and internationally. Accordingly, our management must determine the appropriate allocation of income to each jurisdiction based on current interpretations of complex income tax regulations. Income tax authorities regularly perform audits of our income tax filings. Income tax audits associated with the allocation of income and other complex issues, including inventory transfer pricing and cost sharing, product royalty and foreign branch arrangements, may require an extended period of time to resolve and may result in significant income tax adjustments. If changes to the income allocation are required between jurisdictions with different income tax rates, the related adjustments could have a material unfavorable impact on our results of operations.

Failure of a key information technology system, process or site could have a material adverse impact on our business. We rely extensively on information technology systems to conduct business. These systems include, but are not limited to, ordering and managing materials from suppliers, converting materials to finished products, shipping products to customers, processing transactions, summarizing and reporting results of operations, complying with regulatory, legal or tax requirements, providing data security and other processes necessary to manage our business. If our systems are damaged or cease to function properly due to any number of causes, ranging from catastrophic events to power outages to security breaches, and our business continuity plans do not effectively compensate on a timely basis, we may suffer interruptions in our operations.

A breach of information security, including a cybersecurity breach or failure of one or more key information technology systems, networks, processes, associated sites or service providers could have a material adverse impact on our business or reputation. We rely extensively on information technology (IT) systems, networks and services, including internet sites, data hosting and processing facilities and tools and other hardware, software and technical applications and platforms, some of which are managed, hosted, provided and/or used by third-parties or their vendors, to assist in conducting our business. Numerous and evolving cybersecurity threats, including advanced persistent threats, pose a potential risk to the security of our IT systems, networks and services, as well as the confidentiality, availability, integrity of our data and our responsibilities to governments. We have made investments seeking to address these threats, including monitoring of networks and systems, hiring of experts, employee training and security policies for employees and third-party providers. However, because the techniques used in these attacks change frequently and may be difficult to detect for periods of time, we may face difficulties in anticipating and implementing adequate preventative measures. If the IT systems, networks or service providers we rely upon fail to function properly, or if we or one of

our third-party providers suffer a loss or disclosure of our business or stakeholder information, due to any number of causes, ranging from catastrophic events or power outages to improper data handling or security breaches, and our business continuity plans do not effectively address these failures on a timely basis, we may be exposed to reputational, competitive and business harm as well as litigation and regulatory action. The costs and operational consequences of responding to breaches and implementing remediation measures could be significant.

We may be unable to attract and retain key employees. Our sales, technical and other key personnel play an integral role in the development, marketing and selling of new and existing products. If we are unable to recruit, hire, develop and retain a talented, competitive work force, we may not be able to meet our strategic business objectives.

ITEM 1B. | UNRESOLVED STAFF COMMENTS. |

None.

ITEM 2. | PROPERTIES. |

The following are our principal manufacturing locations as of December 31, 2014 :

Location |

| Segment |

| Approximate Square Feet |

| Owned/ Leased | |

Portage, Michigan |

| M |

| 1,027,000 | |

| Owned |

Changzhou, China |

| O, NS |

| 625,000 | |

| Owned |

Mahwah, New Jersey |

| O |

| 531,000 | |

| Owned |

Arroyo, Puerto Rico |

| M |

| 220,000 | |

| Leased |

San Jose, California |

| M |

| 185,000 | |

| Leased |

Kiel, Germany |

| O |

| 173,000 | |

| Owned |

Suzhou, China |

| O, NS |

| 160,000 | |

| Owned |

Carrigtwohill, Ireland |

| M, O |

| 154,000 | |

| Owned |

Lakeland, Florida |

| M |

| 153,000 | |

| Leased |

Selzach, Switzerland |

| O |

| 137,000 | |

| Owned |

Limerick, Ireland |

| O |

| 130,000 | |

| Owned |

Freiburg, Germany |

| O |

| 123,000 | |

| Owned |

Flower Mound, Texas |

| M |

| 114,000 | |

| Leased |

Carrigtwohill, Ireland |

| NS |

| 110,000 | |

| Leased |

Phoenix, Arizona |

| M |

| 100,000 | |

| Leased |

Cestas, France |

| NS |

| 91,000 | |

| Owned |

Neuchatel, Switzerland |

| NS |

| 88,000 | |

| Owned |

Limerick, Ireland |

| O |

| 78,000 | |

| Leased |

Ft. Lauderdale, Florida |

| O, NS |

| 78,000 | |

| Leased |

Malvern, Pennsylvania |

| O |

| 65,000 | |

| Leased |

Mountain View, California |

| M, NS |

| 62,000 | |

| Leased |

Fremont, California |

| M, NS |

| 50,000 | |

| Leased |

Guayama Puerto Rico |

| M |

| 46,000 | |

| Leased |

Cestas, France |

| NS |

| 35,000 | |

| Leased |

Freiburg, Germany |

| M, O |

| 34,000 | |

| Leased |

Stetten, Germany |

| O |

| 33,000 | |

| Owned |

Rennes, France |

| O |

| 31,000 | |

| Leased |

West Valley, Utah |

| O, NS |

| 29,000 | |

| Leased |

Tokyo, Japan |

| M |

| 11,000 | |

| Leased |

|

|

|

|

|

|

| |

O = Orthopaedics M = MedSurg NS = Neurotechnology and Spine | |||||||

Our corporate headquarters is located in Kalamazoo, Michigan, in a 75,000 square foot owned facility. In addition, we maintain administrative and sales offices and warehousing and distribution facilities in multiple countries. We believe that our properties are suitable and adequate for the manufacture and distribution of our products.

6 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

ITEM 3. | LEGAL PROCEEDINGS. |

We are involved in various proceedings, legal actions and claims arising in the normal course of business, including proceedings related to product, labor and intellectual property, and other matters that are more fully described in Note 7 to the Consolidated Financial Statements in Item 8 of this report; this information is incorporated herein by reference.

ITEM 4. | MINE SAFETY DISCLOSURES. |

Not applicable.

PART II |

ITEM 5. | MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Our common stock is traded on the New York Stock Exchange under the symbol SYK. Quarterly stock price and dividend information for the years ended December 31, 2014 and 2013 were as follows:

2014 Quarter Ended |

| Mar 31 |

| Jun 30 |

| Sep 30 |

| Dec 31 | ||||||||

Dividends declared per share of common stock |

| $ | 0.305 | |

| $ | 0.305 | |

| $ | 0.305 | |

| $ | 0.345 | |

Market price of common stock: |

|

|

|

|

|

| ||||||||||

High |

| 83.86 | |

| 86.93 | |

| 85.91 | |

| 98.24 | | ||||

Low |

| 74.02 | |

| 75.78 | |

| 78.91 | |

| 77.87 | | ||||

2013 Quarter Ended |

| Mar 31 |

| Jun 30 |

| Sep 30 |

| Dec 31 | ||||||||

Dividends declared per share of common stock |

| $ | 0.265 | |

| $ | 0.265 | |

| $ | 0.265 | |

| $ | 0.305 | |

Market price of common stock: |

|

|

|

|

|

| ||||||||||

High |

| 66.92 | |

| 70.00 | |

| 71.94 | |

| 75.55 | | ||||

Low |

| 55.24 | |

| 63.35 | |

| 63.71 | |

| 66.93 | | ||||

Our Board of Directors considers payment of cash dividends at each of its quarterly meetings. On January 31, 2015 , there were 3,285 shareholders of record of our common stock.

In December of 2012 and 2011, we announced that our Board of Directors had authorized us to purchase up to $405 and $500, respectively, of our common stock (the 2012 and 2011 Repurchase Programs, respectively). The manner, timing and amount of purchases is determined by management based on an evaluation of market conditions, stock price and other factors and is subject to regulatory considerations. Purchases are to be made from time to time in the open market, in privately negotiated transactions or otherwise.

Shares repurchased under the share repurchase programs are available for general corporate purposes, including offsetting dilution associated with stock option and other equity-based employee benefit plans. During the year ended December 31, 2014 we repurchased 1.3 million shares at a cost of $100 under the 2011 Repurchase Program. As of December 31, 2014 , the maximum dollar value of shares that may yet be purchased under the 2011 Repurchase Program was $178. We have not made any repurchases pursuant to the 2012 Repurchase Program in 2014.

The activity pursuant to the 2011 Repurchase Program for the three months ended December 31, 2014 is summarized as follows:

Period | Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plan | Maximum Dollar Value of Shares that may yet be Purchased Under the Plan | ||||||

10/1/2014-10/31/2014 | - | | $ | - | | - | | $ | 178 | |

11/1/2014-11/30/2014 | - | | - | | - | | 178 | | ||

12/1/2014-12/31/2014 | - | | - | | - | | 178 | | ||

Total | - | | $ | - | | - | |

| ||

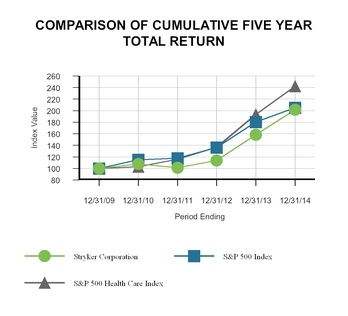

The following graph compares our total returns (including reinvestments of dividends) against the Standard & Poor's (S&P) 500 Index and the S&P 500 Health Care Index. The graph assumes $100 (not in millions) invested on December 31, 2009 in our Common Stock and each of the indices.

Company / Index | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 |

Stryker Corporation | 100.00 | 107.89 | 101.29 | 113.54 | 158.16 | 201.50 |

S&P 500 Index | 100.00 | 115.06 | 117.49 | 136.30 | 180.44 | 205.14 |

S&P 500 Health Care Index | 100.00 | 102.90 | 116.00 | 136.75 | 193.45 | 242.46 |

7 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

ITEM 6. | SELECTED FINANCIAL DATA. |

Selected financial data for each of the five years ended December 31, 2014 is as follows:

CONSOLIDATED OPERATIONS |

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 | ||||||||||

Net sales |

| $ | 9,675 | |

| $ | 9,021 | |

| $ | 8,657 | |

| $ | 8,307 | |

| $ | 7,320 | |

Cost of sales |

| 3,291 | |

| 2,977 | |

| 2,781 | |

| 2,811 | |

| 2,286 | | |||||

Gross profit |

| 6,384 | |

| 6,044 | |

| 5,876 | |

| 5,496 | |

| 5,034 | | |||||

Research, development and engineering expenses |

| 614 | |

| 536 | |

| 471 | |

| 462 | |

| 394 | | |||||

Selling, general and administrative expenses |

| 3,575 | |

| 3,492 | |

| 3,367 | |

| 3,226 | |

| 2,831 | | |||||

Recall charges, net of insurance recoveries |

| 761 | |

| 622 | |

| 174 | |

| - | |

| - | | |||||

Intangibles amortization |

| 188 | |

| 138 | |

| 123 | |

| 122 | |

| 58 | | |||||

|

| 5,138 | |

| 4,788 | |

| 4,135 | |

| 3,810 | |

| 3,283 | | |||||

Operating income |

| 1,246 | |

| 1,256 | |

| 1,741 | |

| 1,686 | |

| 1,751 | | |||||

Other income (expense) |

| (86 | ) |

| (44 | ) |

| (36 | ) |

| - | |

| (22 | ) | |||||

Earnings before income taxes |

| 1,160 | |

| 1,212 | |

| 1,705 | |

| 1,686 | |

| 1,729 | | |||||

Income taxes |

| 645 | |

| 206 | |

| 407 | |

| 341 | |

| 456 | | |||||

Net earnings |

| $ | 515 | |

| $ | 1,006 | |

| $ | 1,298 | |

| $ | 1,345 | |

| $ | 1,273 | |

|

|

|

|

|

|

|

|

|

|

| ||||||||||

PER SHARE DATA |

|

|

|

|

|

|

|

|

|

| ||||||||||

Net earnings per share of common stock: |

|

|

|

|

|

|

|

|

|

| ||||||||||

Basic |

| $ | 1.36 | |

| $ | 2.66 | |

| $ | 3.41 | |

| $ | 3.48 | |

| $ | 3.21 | |

Diluted |

| $ | 1.34 | |

| $ | 2.63 | |

| $ | 3.39 | |

| $ | 3.45 | |

| $ | 3.19 | |

Dividends per share of common stock: |

|

|

|

|

|

|

|

|

|

| ||||||||||

Declared |

| $ | 1.26 | |

| $ | 1.10 | |

| $ | 0.90 | |

| $ | 0.75 | |

| $ | 0.63 | |

Paid |

| $ | 1.22 | |

| $ | 1.06 | |

| $ | 0.85 | |

| $ | 0.72 | |

| $ | 0.60 | |

Average number of shares outstanding-in millions: |

|

|

|

|

|

|

|

|

|

| ||||||||||

Basic |

| 378.5 | |

| 378.6 | |

| 380.6 | |

| 386.5 | |

| 396.4 | | |||||

Diluted |

| 382.8 | |

| 382.1 | |

| 383.0 | |

| 389.5 | |

| 399.5 | | |||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||

CONSOLIDATED FINANCIAL POSITION |

|

|

|

|

|

|

|

|

|

| ||||||||||

Cash, cash equivalents and current marketable securities |

| $ | 5,000 | |

| $ | 3,980 | |

| $ | 4,285 | |

| $ | 3,418 | |

| $ | 4,380 | |

Accounts receivable-net |

| 1,572 | |

| 1,518 | |

| 1,430 | |

| 1,417 | |

| 1,252 | | |||||

Inventory-net |

| 1,588 | |

| 1,422 | |

| 1,265 | |

| 1,283 | |

| 1,057 | | |||||

Property, plant and equipment-net |

| 1,098 | |

| 1,081 | |

| 948 | |

| 888 | |

| 798 | | |||||

Capital expenditures |

| 233 | |

| 195 | |

| 210 | |

| 226 | |

| 182 | | |||||

Depreciation and amortization |

| 586 | |

| 511 | |

| 486 | |

| 481 | |

| 410 | | |||||

Total assets |

| 17,713 | |

| 15,743 | |

| 13,206 | |

| 12,146 | |

| 10,895 | | |||||

Accounts payable |

| 329 | |

| 314 | |

| 288 | |

| 345 | |

| 292 | | |||||

Total debt |

| 3,973 | |

| 2,764 | |

| 1,762 | |

| 1,768 | |

| 1,021 | | |||||

Shareholders' equity |

| 8,595 | |

| 9,047 | |

| 8,597 | |

| 7,683 | |

| 7,174 | | |||||

Net cash provided by operating activities |

| 1,782 | |

| 1,886 | |

| 1,657 | |

| 1,434 | |

| 1,547 | | |||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||

OTHER DATA |

|

|

|

|

|

|

|

|

|

| ||||||||||

Number of shareholders of record |

| 3,305 | |

| 3,612 | |

| 4,258 | |

| 4,508 | |

| 4,586 | | |||||

Approximate number of employees |

| 26,000 | |

| 25,000 | |

| 22,000 | |

| 21,000 | |

| 20,000 | | |||||

8 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

ABOUT STRYKER

Stryker is one of the world's leading medical technology companies, with 2014 revenues of $9,675 and net earnings of $515 . We offer a diverse array of innovative medical technologies, including reconstructive, medical and surgical, and neurotechnology and spine products to help people lead more active and more satisfying lives.

In the United States, most of our products are marketed directly to doctors, hospitals and other healthcare facilities. In general, we maintain separate dedicated sales forces for each of our principal product lines to provide focus and a high level of expertise to each medical specialty served. Internationally our products are sold in over 100 countries through company-owned sales subsidiaries and branches as well as third-party dealers and distributors. Our business is generally not seasonal in nature; however, the number of Orthopaedics implant surgeries is generally lower during the summer months and sales of capital equipment are generally higher in the fourth quarter.

At the heart of what we do and believe is making healthcare better. We do this by collaborating with our customers to develop innovative products and services that ultimately improve the lives of our patients. We express this through our mission statement:

"Together with our customers,

we are driven to make healthcare better."

We believe our success in the highly competitive product categories in which we operate depends to a large degree on our ability to develop new products and make improvements to existing products. We are committed to internal innovation to develop products and services that improve outcomes and deliver greater cost savings and efficiencies and to augment our efforts with focused acquisitions. Our success further depends on the ability of our people to execute effectively, every day.

Our goal is to drive sales growth at the high-end of the MedTech industry and maintain our capital allocation strategy that prioritizes:

1. | Acquisitions |

2. | Dividends |

3. | Share repurchases |

Overview of 2014

In 2014 we achieved sales growth of 7.3% in line with our ongoing goal to grow organic sales at the high-end of the MedTech industry. Excluding the impact of acquisitions, sales grew 5.8% in constant currency. We converted our sales growth into a 5.3% growth in adjusted net earnings per diluted share (See page 12 for a reconciliation of reported net earnings per diluted share to adjusted net earnings per diluted share) . We continued our capital allocation strategy by investing $916 in acquisitions, paying $462 in dividends to our shareholders and using $100 for share repurchases.

In November 2014 we entered into a Settlement Agreement to compensate eligible United States patients who had "revision surgery" to replace their Rejuvenate Modular-Neck hip stem and/or ABG II Modular-Neck hip stem.

In September 2014 we acquired the assets of Small Bone Innovations, Inc. (SBi) for an aggregate purchase price of approximately $358 . SBi products are designed and promoted for upper and lower extremity small bone indications, with a focus on small joint replacement.

In July 2014 we established a European regional headquarters in the Netherlands. We believe that this increased presence will strengthen our brand in Europe, support the growth of our global business, provide operational efficiencies and simplify our customers' experience.

In April 2014 we acquired Berchtold Holding, AG (Berchtold), a privately-held business with operations in Germany and the United States, for an aggregate purchase price of approximately $184 . Berchtold sells surgical tables, equipment booms and surgical lighting systems.

In March 2014 we acquired Patient Safety Technologies, Inc. (PST), for an aggregate purchase price of $120 . PST conducts its business through its wholly owned subsidiary, SurgiCount Medical, Inc. PST's proprietary Safety-Sponge ® System and SurgiCount 360™ compliance software help prevent retained foreign objects in the operating room. Other business acquisitions in 2014 include the acquisition of Pivot Medical, Inc, which develops and sells innovative products for hip arthroscopy.

Consolidated results of operations: | Years Ended December 31, |

| Percentage Change | ||||||

| 2014 | 2013 | 2012 |

| 2014/2013 | 2013/2012 | |||

Net Sales | $9,675 | $9,021 | $8,657 |

| 7.3 | | 4.2 | | |

Gross Profit | 6,384 | 6,044 | 5,876 |

| 5.6 | | 2.9 | | |

Research, development and engineering expenses | 614 | 536 | 471 |

| 14.6 | | 13.8 | | |

Selling, general and administrative expenses | 4,336 | 4,114 | 3,541 |

| 5.4 | | 16.2 | | |

Intangibles amortization | 188 | 138 | 123 |

| 36.2 | | 12.2 | | |

Other income (expense) | (86) | (44) | (36 | ) |

| 95.5 | | 22.2 | |

Income taxes | 645 | 206 | 407 |

| 213.1 | | (49.4 | ) | |

Net Earnings | $515 | $1,006 | $1,298 |

| (48.8 | ) | (22.5 | ) | |

Diluted Net Earnings per share | $1.34 | $2.63 | $3.39 |

| (49.0 | ) | (22.4 | ) | |

Adjusted Net Earnings per share (1) | $4.73 | $4.49 | $4.30 |

| 5.3 | | 4.4 | | |

9 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

Geographic and segment net sales: |

|

|

| Percentage Change | ||||||||||||||||

|

|

|

| 2014/2013 |

| 2013/2012 | ||||||||||||||

|

| Years Ended December 31, |

|

|

| Constant |

|

|

| Constant | ||||||||||

|

| 2014 |

| 2013 |

| 2012 |

| Reported |

|

| Reported |

| ||||||||

Geographic sales: |

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

United States |

| $ | 6,558 | |

| $ | 5,984 | |

| $ | 5,658 | |

| 9.6 |

| 9.6 |

| 5.8 |

| 5.8 |

International |

| 3,117 | |

| 3,037 | |

| 2,999 | |

| 2.6 |

| 5.7 |

| 1.3 |

| 6.0 | |||

Total net sales |

| $ | 9,675 | |

| $ | 9,021 | |

| $ | 8,657 | |

| 7.3 |

| 8.3 |

| 4.2 |

| 5.9 |

Segment sales: |

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Orthopaedics |

| $ | 4,153 | |

| $ | 3,949 | |

| $ | 3,823 | |

| 5.2 |

| 6.3 |

| 3.3 |

| 5.4 |

MedSurg |

| 3,781 | |

| 3,414 | |

| 3,265 | |

| 10.8 |

| 11.7 |

| 4.6 |

| 5.5 | |||

Neurotechnology and Spine |

| 1,741 | |

| 1,658 | |

| 1,569 | |

| 5.0 |

| 6.2 |

| 5.6 |

| 7.7 | |||

Total net sales |

| $ | 9,675 | |

| $ | 9,021 | |

| $ | 8,657 | |

| 7.3 |

| 8.3 |

| 4.2 |

| 5.9 |

Net sales increased 7.3% in 2014. In 2014 net sales grew by 7.8% as a result of increased unit volume and changes in product mix and 2.5% due to acquisitions and were negatively impacted by 2.0% due to changes in price and 1.0% due to the unfavorable impact of foreign currency exchange rates. Excluding the impact of acquisitions, net sales increased 5.8% in constant currency. Net sales increased primarily due to higher shipments of instruments products, trauma and extremities products, endoscopy products, neurotechnology products, medical products, and the impact of acquisitions.

Net sales increased 4.2% in 2013. In 2013 net sales grew by 6.5% as a result of unit volume and changes in product mix and 0.8%

due to acquisitions and were negatively impacted by 1.4% due to changes in price and 1.6% due to the unfavorable impact of foreign currency exchange rates. Excluding the impact of acquisitions, 2013 net sales increased 5.1% in constant currency. Net sales increased primarily due to higher shipments of trauma and extremities products, neurotechnology products, hips and endoscopy products.

In the United States net sales increased 9.6% in 2014 after increasing 5.8% in 2013. In constant currency, International sales increased 5.7% in 2014 after increasing 6.0% in 2013.

|

|

| Percentage Change |

|

|

| Percentage Change | ||||||||||||||||||||||

| Years Ended December 31, |

|

| U.S. | International |

| Years Ended December 31, |

|

| U.S. | International | ||||||||||||||||||

| 2014 | 2013 | As Reported | Constant Currency | As Reported | As Reported | Constant Currency |

| 2013 | 2012 | As Reported | Constant Currency | As Reported | As Reported | Constant Currency | ||||||||||||||

Orthopaedics |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Knees | 1,396 | | 1,371 | | 1.8 | % | 2.7 | % | 4.3 | % | (3.5 | )% | (0.7 | )% |

| 1,371 | | 1,356 | | 1.1 | % | 2.6 | % | 3.4 | % | (3.3 | )% | 1.1 | % |

Hips | 1,291 | | 1,272 | | 1.5 | % | 2.7 | % | 6.1 | % | (4.2 | )% | (1.4 | )% |

| 1,272 | | 1,233 | | 3.2 | % | 6.0 | % | 7.2 | % | (1.4 | )% | 4.5 | % |

Trauma and Extremities | 1,230 | | 1,116 | | 10.2 | % | 11.4 | % | 14.8 | % | 5.1 | % | 7.7 | % |

| 1,116 | | 989 | | 12.8 | % | 15.1 | % | 18.4 | % | 7.2 | % | 11.8 | % |

Other | 236 | | 190 | | 24.0 | % | 25.2 | % | 37.4 | % | (7.6 | )% | (3.7 | )% |

| 190 | | 245 | | (22.5 | )% | (20.9 | )% | (19.7 | )% | (28.3 | )% | (23.4 | )% |

ORTHOPAEDICS | 4,153 | | 3,949 | | 5.2 | % | 6.3 | % | 9.4 | % | (1.1 | )% | 1.7 | % |

| 3,949 | | 3,823 | | 3.3 | % | 5.4 | % | 6.2 | % | (0.6 | )% | 4.4 | % |

MedSurg |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Instruments | 1,424 | | 1,269 | | 12.2 | % | 13.1 | % | 14.8 | % | 5.7 | % | 8.8 | % |

| 1,269 | | 1,261 | | 0.6 | % | 1.9 | % | 0.7 | % | 0.6 | % | 5.1 | % |

Endoscopy | 1,382 | | 1,222 | | 13.1 | % | 14.2 | % | 13.3 | % | 12.6 | % | 16.2 | % |

| 1,222 | | 1,111 | | 10.0 | % | 11.0 | % | 11.4 | % | 6.5 | % | 9.9 | % |

Medical | 766 | | 710 | | 7.9 | % | 8.8 | % | 9.3 | % | 2.2 | % | 6.7 | % |

| 710 | | 691 | | 2.8 | % | 3.1 | % | 3.4 | % | 0.3 | % | 2.0 | % |

Sustainability | 209 | | 213 | | (1.9 | )% | (1.9 | )% | (1.8 | )% | nm | | nm | |

| 213 | | 202 | | 5.6 | % | 5.6 | % | 5.8 | % | nm | | nm | |

MEDSURG | 3,781 | | 3,414 | | 10.8 | % | 11.7 | % | 11.7 | % | 7.9 | % | 11.5 | % |

| 3,414 | | 3,265 | | 4.6 | % | 5.5 | % | 5.2 | % | 2.9 | % | 6.4 | % |

Neurotechnology and Spine |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

Neurotechnology | 1,001 | | 915 | | 9.4 | % | 10.9 | % | 11.2 | % | 6.7 | % | 10.4 | % |

| 915 | | 842 | | 8.7 | % | 11.4 | % | 11.2 | % | 5.1 | % | 11.8 | % |

Spine | 740 | | 743 | | (0.4 | )% | 0.3 | % | (1.6 | )% | 2.5 | % | 5.2 | % |

| 743 | | 727 | | 2.1 | % | 3.4 | % | 1.8 | % | 2.9 | % | 7.2 | % |

NEUROTECHNOLOGY AND SPINE | 1,741 | | 1,658 | | 5.0 | % | 6.2 | % | 5.0 | % | 5.1 | % | 8.5 | % |

| 1,658 | | 1,569 | | 5.6 | % | 7.7 | % | 6.4 | % | 4.3 | % | 10.0 | % |

nm = not meaningful

Orthopaedics Net Sales

Orthopaedics net sales in 2014 increased 5.2%, primarily due to a 6.2% increase in unit volume and changes in product mix and 3.0% due to acquisitions. Net sales were negatively impacted by 2.9% due to changes in price and 1.1% due to the unfavorable impact of foreign currency exchange rates. In constant currency, net sales increased by 6.3% in 2014 , primarily due to increases in trauma and extremities products and the impact of acquisitions. Net sales in 2013 increased 3.3%, primarily due to a 7.9% increase in unit

volume and changes in product mix and 1.4% due to acquisitions. Net sales were negatively impacted by 2.4% due to changes in price and 2.1% due to the unfavorable impact of foreign currency exchange rates. Excluding the impact of acquisitions, net sales increased by 5.4% in constant currency in 2013 , primarily due to increases in trauma and extremities products and hips.

10 |

| Dollar amounts in millions except per share amounts or as otherwise specified. |

STRYKER CORPORATION 2014 Form 10-K

MedSurg Net Sales

MedSurg net sales in 2014 increased 10.8%, primarily due to a 9.5% increase in unit volume and changes in product mix and 3.0% due to acquisitions, and were negatively impacted by 0.8% due to changes in price and 0.9% due to the unfavorable impact of foreign currency exchange rates. In constant currency, net sales in 2014 increased 11.7%, led by higher shipments of instruments products and medical products and the impact of acquisitions; these higher shipments were partially offset by lower shipments of sustainability products. Net sales in 2013 increased 4.6%, primarily due to a 3.8% increase in unit volume and changes in product mix and were negatively impacted by 0.9% due to the unfavorable impact of foreign currency exchange rates. The effect of pricing was not significant. In constant currency, net sales in 2013 increased 5.5%, led by higher shipments of endoscopy products.

Neurotechnology and Spine Net Sales

Neurotechnology and Spine net sales in 2014 increased 5.0%, primarily due to an 8.1% increase in unit volume and changes in product mix and 0.5% due to acquisitions, and were negatively impacted by 2.4% due to changes in price and 1.2% due to the unfavorable impact of foreign currency exchange rates. In constant currency net sales in 2014 increased 6.2% led by higher shipments of neurotechnology products. Net sales in 2013 increased 5.6%, primarily due to an 8.8% increase in unit volume and changes in product mix and 0.9% due to acquisitions, and were negatively impacted by 2.0% due to changes in price and 2.1% due to the unfavorable impact of foreign currency exchange rates. Excluding the impact of acquisitions, net sales in 2013 increased 6.8% in constant currency, due to higher shipments of neurotechnology products.

Consolidated Cost of Sales

Cost of sales increased 10.5% in 2014 to 34.0% of sales compared to 33.0% in 2013 . Cost of sales as a percentage of sales was adversely impacted by changes in selling prices for our products, unfavorable product mix and by the unfavorable effect of foreign currency exchange rates. Our product mix was unfavorable due to the impact of recent acquisitions and strong MedSurg sales. Cost of sales in 2014 and 2013 includes an additional cost of $27 and $28, respectively, related to inventory that was "stepped up" to fair value following acquisitions; $1 and $11, respectively in restructuring related charges; and $7 in 2013 for disgorgement of profits associated with a legal settlement. Cost of sales increased 7.0% in 2013 to 33.0% of sales compared to 32.1% in 2012 . Cost of sales in 2012 includes an additional cost of $18 related to inventory that was "stepped up" to fair value following acquisitions and $5 in restructuring related costs.

Research, Development and Engineering Expenses

Research, development and engineering expenses represented 6.3% of sales in 2014 compared to 5.9% in 2013 and 5.4% in 2012 . The increased spending levels in 2014 and 2013 were driven by the impact of acquisitions and by the timing of projects and our continued investment in new technologies.

Selling, General and Administrative Expenses

Selling, general and administrative expenses increased 5.4% in 2014 and represented 44.9% of sales compared to 45.6% in 2013 and 40.9% in 2012 , driven by strong sales growth and cost improvement efforts. These expenses included $75 and $70 in 2014 and 2013 , respectively, of acquisition and integration related charges; $116 and $52, respectively, of restructuring related charges, $761 and $622, respectively, related to the Rejuvenate, ABG II and Neptune recalls; $62 in 2013 related to regulatory and legal matters; $25 in 2013 representing a donation to an educational

institution. Excluding the impact of these charges, selling, general and administrative expenses were 35.0% of sales in 2014 compared to 36.4% in 2013 .

Other Income (Expense)

Other expense increased by $42 in 2014 after increasing by $8 in 2013 . Net expense in 2014 increased primarily due to higher interest expense from the $1,000 senior unsecured notes issued in May 2014, partially offset by lower interest expense due to favorable tax audit resolutions. Net expense in 2013 increased due to lower income from interest and marketable securities, offset by hedge gains and lower interest expense. The decrease in interest expense was due to favorable tax audit resolutions in multiple jurisdictions, partially offset by higher interest expense on borrowings.

Income Taxes

Our effective income tax rate on earnings was 55.6%, 17.0% and 23.9% in 2014, 2013 and 2012, respectively. The effective income tax rate for 2014 includes the tax impacts of the establishment of a European regional headquarters and a cash repatriation to the United States planned for 2015. The effective income tax rate for 2013 includes income tax benefits relating to favorable audit resolutions in multiple jurisdictions. The effective income tax rate for 2012 includes the net impact of effective settlement of all tax matters through 2004 relating to two German subsidiaries, and adjustment of the estimate of foreign tax credits to the amount shown on the tax return as filed.