UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017 | Commission file number 1-9700 |

THE CHARLES SCHWAB CORPORATION

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 94-3025021 (I.R.S. Employer Identification No.) |

211 Main Street, San Francisco, CA 94105

(Address of principal executive offices and zip code)

Registrant's telephone number, including area code: (415) 667-7000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock – $.01 par value per share | New York Stock Exchange |

Depositary Shares, each representing a 1/40 th ownership interest in a |

|

share of 6.00% Non-Cumulative Preferred Stock, Series C | New York Stock Exchange |

Depositary Shares, each representing a 1/40 th ownership interest in a |

|

share of 5.95% Non-Cumulative Preferred Stock, Series D | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10‑K. ☒

Large accelerated filer ☒ | Accelerated filer ☐ |

Non-accelerated filer ☐ (Do not check if a smaller reporting company) | Smaller reporting company ☐ |

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2017 , the aggregate market value of the voting stock held by non-affiliates of the registrant was $51.2 billion. For purposes of this information, the outstanding shares of Common Stock owned by directors and executive officers of the registrant were deemed to be shares of the voting stock held by affiliates.

The number of shares of Common Stock outstanding as of January 31, 2018, was 1,346,473,499.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Form 10-K incorporates certain information contained in the registrant's definitive proxy statement for its annual meeting of stockholders, to be held May 15, 2018 , by reference to that document.

THE CHARLES SCHWAB CORPORATION

Annual Report On Form 10-K

For Fiscal Year Ended December 31, 2017

Part I |

|

| |

|

|

| |

Item 1. | Business | 1 | |

| General Corporate Overview | 1 | |

| Business Strategy and Competitive Environment | 1 | |

| Sources of Net Revenues | 2 | |

| Products and Services | 2 | |

| Regulation | 5 | |

| Available Information | 8 | |

Item 1A. | Risk Factors | 9 | |

Item 1B. | Unresolved Securities and Exchange Commission Staff Comments | 15 | |

Item 2. | Properties | 15 | |

Item 3. | Legal Proceedings | 15 | |

Item 4. | Mine Safety Disclosures | 15 | |

|

|

| |

Part II |

|

| |

|

|

| |

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters, and Issuer Purchases of |

| |

| Equity Securities | 16 | |

Item 6. | Selected Financial Data | 18 | |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 19 | |

| Forward-Looking Statements | 19 | |

| Glossary of Terms | 21 | |

| Overview | 24 | |

| Current Regulatory Environment and Other Developments | 26 | |

| Results of Operations | 27 | |

| Risk Management | 35 | |

| Capital Management | 42 | |

| Fair Value of Financial Instruments | 45 | |

| Critical Accounting Estimates | 45 | |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 47 | |

Item 8. | Financial Statements and Supplementary Data | 48 | |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 102 | |

Item 9A. | Controls and Procedures | 102 | |

Item 9B. | Other Information | 102 | |

|

|

| |

Part III |

|

| |

|

|

| |

Item 10. | Directors, Executive Officers, and Corporate Governance | 102 | |

Item 11. | Executive Compensation | 102 | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 103 | |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 103 | |

Item 14. | Principal Accountant Fees and Services | 103 | |

|

|

| |

Part IV |

|

| |

|

|

| |

Item 15. | Exhibits, Financial Statement Schedules | 104 | |

| Exhibit Index | 105 | |

| Signatures | 110 | |

| Statistical Disclosure by Bank Holding Companies | F-1 | |

THE CHARLES SCHWAB CORPORATION

PART I

Item 1. | Business |

General Corporate Overview

The Charles Schwab Corporation (CSC) is a savings and loan holding company, headquartered in San Francisco, California. CSC was incorporated in 1986 and engages, through its subsidiaries (collectively referred to as Schwab or the Company), in wealth management, securities brokerage, banking, asset management, custody, and financial advisory services. At December 31, 2017 , Schwab had $3.36 trillion in client assets, 10.8 million active brokerage accounts, 1.6 million corporate retirement plan participants, and 1.2 million banking accounts.

Significant business subsidiaries of CSC include the following:

• | Charles Schwab & Co., Inc. (CS&Co), incorporated in 1971, a securities broker-dealer with over 345 domestic branch offices in 46 states, as well as a branch in the Commonwealth of Puerto Rico. In addition, Schwab serves clients in England, Hong Kong, Singapore, and Australia through various subsidiaries; |

• | Charles Schwab Bank (Schwab Bank), a federal savings bank; and |

• | Charles Schwab Investment Management, Inc. (CSIM), the investment advisor for Schwab's proprietary mutual funds (Schwab Funds ® ) and Schwab's exchange-traded funds (Schwab ETFs™). |

Schwab provides financial services to individuals and institutional clients through two segments – Investor Services and Advisor Services. The Investor Services segment provides retail brokerage and banking services to individual investors and retirement plan services, as well as other corporate brokerage services, to businesses and their employees. The Advisor Services segment provides custodial, trading, banking, and support services, as well as retirement business services, to independent registered investment advisors (RIAs), independent retirement advisors, and recordkeepers. These services are further described in the segment discussion below.

As of December 31, 2017 , Schwab had full-time, part-time, temporary employees, and persons employed on a contract basis that represented the equivalent of approximately 17,600 full-time employees.

Unless otherwise indicated, the terms "Schwab," "the Company," "we," "us," or "our" mean CSC together with its consolidated subsidiaries.

Business Strategy and Competitive Environment

Schwab was founded on the belief that all Americans deserve access to a better investing experience. Although much has changed in the intervening years, our purpose remains clear – to champion every client's goals with passion and integrity. Guided by this purpose and the aspiration of creating the most trusted leader in investment services, management has adopted a strategy described as "Through Clients' Eyes."

Under this approach, our strategic goals are focused on putting clients' perspectives, needs, and desires at the forefront. Because investing plays a fundamental role in building financial security, we strive to deliver a better investing experience for our clients – individual investors and the people and institutions who serve them – by disrupting longstanding industry practices on their behalf and providing superior service. We aim to offer a broad range of products and solutions to meet client needs with a focus on transparency and value. In addition, management works to couple Schwab's scale and resources with ongoing expense discipline to keep costs low and ensure that products and solutions are affordable as well as responsive to client needs. Finally, we seek to maximize our market valuation and stockholder returns over time.

Management estimates that investable wealth in the U.S. currently exceeds $30 trillion, which means the Company's $3.36 trillion in client assets leaves substantial opportunity for growth. Our strategy is based on the principle that developing trusted relationships will translate into more assets from both new and existing clients, ultimately driving more revenue and, along with expense discipline, generate earnings growth and build long-term stockholder value.

- 1 -

THE CHARLES SCHWAB CORPORATION

Within Investor Services, our competition in serving individual investors includes a wide range of brokerage, wealth management, and asset management firms, as well as banks and trust companies. In the Advisor Services arena, we compete with institutional custodians, traditional and discount brokers, banks and investment advisory firms, and trust companies.

Across both segments, our key competitive advantages are:

• | Scale and Size of the Business – As one of the largest investment services firms in the United States (U.S.), we are able to spread operating costs, amortize new investments over a large base of clients, and have the resources to evolve capabilities to meet client needs. |

• | Operating Efficiency – Coupled with scale, our operating efficiency and sharing of infrastructure across different businesses creates a cost advantage that enables us to competitively price products and services while profitably serving many different client channels. |

• | Operating Structure – Adding bank and asset management capabilities to the broker-dealers helps serve a wider array of client needs, thereby deepening client relationships, enhancing the stability of client assets, and enabling diversified revenue streams. |

• | Brand and Corporate Reputation – In an industry dependent on trust, Schwab's reputation and brand across multiple constituents enables us to attract clients and employees while credibly introducing new products to the market. |

• | Service Culture – Delivering a great client experience earns the trust and loyalty of clients and increases the likelihood that those clients will refer others. |

• | Willingness to Disrupt – Management's willingness to challenge the status quo to benefit clients fosters innovation and continuous improvement, which helps to attract more clients and assets. |

Sources of Net Revenues

Our major sources of net revenues are net interest revenue, asset management and administration fees, and trading revenue. These revenue streams are supported by the combination of bank, broker-dealer, and asset management operating subsidiaries, each of which brings specific capabilities that enable us to provide clients with the products and services they are looking for.

Net interest revenue is the difference between interest generated on interest-earning assets and interest paid on funding sources, the majority of which is derived from client cash balances held by Schwab as part of the clients' overall relationship with the Company. While certain client cash balances are held on CS&Co's balance sheet or swept to our money market funds, a substantial amount of existing cash balances and most new client cash inflows are swept to a banking subsidiary. Over time, as supporting capital has been available, we have been directing a growing proportion of client cash sweep balances to a banking subsidiary relative to those going to the broker-dealer or money market funds. This shift has been effected through changes to default sweep options and the periodic bulk transfer of larger balances. Bank sweep balances have access to Federal Deposit Insurance Corporation (FDIC) insurance protection, as allowed, and provide us with greater flexibility in terms of options for investing the cash and administering the interest rate paid.

The majority of asset management and administration fees are earned from proprietary money market mutual funds, proprietary and third-party mutual funds and exchange-traded funds (ETFs), and fee-based advisory solutions.

Trading revenue includes commissions earned for executing trades for clients in individual equities, options, futures, fixed income securities, and certain third-party mutual funds and ETFs, as well as principal transaction revenue earned primarily from actions to support client trading in fixed income securities.

Products and Services

We offer a broad range of products to address our clients' varying investment and financial needs. Examples of these product offerings include the following:

• | Brokerage – an array of full-feature brokerage accounts with margin lending, options trading, and cash management capabilities including third-party certificates of deposit; |

• | Mutual funds – third-party mutual funds through the Mutual Fund Marketplace ® , including no-transaction fee mutual funds through the Mutual Fund OneSource ® service, which also includes proprietary mutual funds, plus mutual fund trading and clearing services to broker-dealers; |

- 2 -

THE CHARLES SCHWAB CORPORATION

• | Exchange-traded funds – an extensive offering of ETFs, including many proprietary and third-party ETFs available without a commission through Schwab ETF OneSource™; |

• | Advice solutions – managed portfolios of both proprietary and third-party mutual funds and ETFs, separately managed accounts, customized personal advice for tailored portfolios, specialized planning, and full-time portfolio management; |

• | Banking – checking and savings accounts, first lien residential real estate mortgage loans (First Mortgages), home equity lines of credit (HELOCs), and pledged asset lines (PALs); and |

• | Trust – trust custody services, personal trust reporting services, and administrative trustee services. |

This full array of investing services is made available through two business segments – Investor Services and Advisor Services. Schwab's major sources of revenues are generated by both of the reportable segments. Revenue is attributable to a reportable segment based on which segment has the primary responsibility for serving the client. The accounting policies of the reportable segments are the same as those described in "Item 8 – Financial Statements and Supplementary Data – Notes to Consolidated Financial Statements" (Item 8) – Note 2. For financial information related to the Company's reportable segments, see "Item 7 – Management's Discussion and Analysis of Financial Condition and Results of Operations – Results of Operations" (Item 7) and Item 8 – Note 22.

Investor Services

Charles Schwab initially founded the Company over 40 years ago to provide individual investors with access to the financial markets at a reasonable cost. The Company has been expanding offerings over time in response to client needs, aiming to provide a compelling and often disruptive solution in the marketplace. As products and services have evolved over the years, the Investor Services segment has expanded and now includes the Retail Investor, Retirement Plan Services, Mutual Fund Clearing Services, and Off-Platform Sales business units.

Through the Retail Investor business unit, we offer individual investors a multi-channel service delivery model, which includes online, mobile, telephone, and branch capabilities. We provide personalized service at competitive prices while giving clients the choice of where, when, and how they do business with us. Financial Consultants (FCs) in Schwab's branches and regional telephone service centers focus on building and sustaining client relationships. We have the ability to meet client investing needs through a single ongoing point of contact, even as those needs change over time. We believe that this ability to give those clients seeking help, guidance, or advice with an individually tailored solution – ranging from occasional consultations to an ongoing relationship with a Schwab FC or an independent RIA in the Schwab Advisor Network ® – is a competitive strength compared to the more fragmented or limited offerings of other firms.

Our service delivery model provides quick and efficient access to an extensive array of information, research, tools, trade execution, and administrative services, which clients can access according to their needs. For example, clients that trade more actively can use these channels to access highly competitive pricing, expert tools, and extensive service capabilities – including experienced, knowledgeable teams of trading specialists, and integrated product offerings. Management also believes the Company is able to compete with the wide variety of financial services firms striving to attract individual client relationships by complementing these capabilities with a range of investment and banking products.

Schwab strives to educate and assist clients in reaching their financial goals. Educational tools include workshops, webcasts, interactive courses, and online information about investing, from which Schwab does not earn revenue. Additionally, we provide various online research and analysis tools that are designed to help clients achieve better investment outcomes. As an example of such tools, Schwab Equity Ratings ® is a quantitative model-based stock rating system that provides all clients with ratings on approximately 3,000 stocks, assigning each equity a single grade: A, B, C, D, or F. Schwab Equity Ratings International ® , an international ranking methodology, covers stocks of approximately 4,000 foreign companies.

Clients may seek specific investment recommendations, either from time to time or on an ongoing basis. Schwab provides clients seeking advice with personalized solutions. Our approach to advice is based on long-term investment strategies and guidance on portfolio diversification and asset allocation. This approach is designed to be offered consistently across all of Schwab's delivery channels.

Schwab Private Client features a personal advice relationship with a designated Portfolio Consultant, supported by a team of investment professionals who provide individualized service, a customized investment strategy developed in collaboration with the client, and ongoing guidance and execution.

- 3 -

THE CHARLES SCHWAB CORPORATION

For clients seeking a relationship in which investment decisions are fully delegated to a financial professional, Schwab offers several alternatives. We provide investors access to professional investment management in a diversified account that is invested exclusively in either mutual funds or ETFs through the Schwab Managed Portfolios and Windhaven Investment Management, Inc. (Windhaven ® ), or equity securities and ETFs through ThomasPartners ® programs. We also refer investors who want to utilize a specific third-party money manager to direct a portion of their investment assets to the Schwab Managed Account program. Schwab Intelligent Portfolios ® , available since 2015, are for clients who are looking to have their assets professionally managed via a fully automated online investment advisory service. In late 2016, we introduced Schwab Intelligent Advisory ® to offer our clients a hybrid advisory service which combines live credentialed professionals and algorithm-driven technology to make financial and investment planning more accessible to investors. Finally, clients who want the assistance of an independent professional in managing their financial affairs may be referred to RIAs in the Schwab Advisor Network. These RIAs provide personalized portfolio management, financial planning, and wealth management solutions.

To meet the specific needs of clients who actively trade, Schwab offers integrated web- and software-based trading platforms, which incorporate intelligent order routing technology, real-time market data, options trading, premium stock and futures research, and multi-channel access, as well as sophisticated account and trade management features, risk management and decision support tools, and dedicated personal support.

For U.S. clients wishing to invest in foreign equities, we offer a suite of global investing capabilities, including online access to certain foreign equity markets with the ability to trade in their local currencies. In addition, Schwab serves both foreign investors and non-English-speaking U.S. clients who wish to trade or invest in U.S. dollar-based securities. In the U.S., Schwab serves Mandarin-, Cantonese-, Spanish-, and Vietnamese-speaking clients through a combination of its branch offices, web-based and telephonic services.

We also offer equity compensation plan sponsors full-service recordkeeping for stock plans, stock options, restricted stock, performance shares, and stock appreciation rights. Specialized services for executive transactions and reporting, grant acceptance tracking, and other services are offered to employers to meet the needs of administering the reporting and compliance aspects of an equity compensation plan. In addition, we provide software and services for compliance departments of regulated companies and firms with special requirements to monitor employee personal trading, including trade surveillance technology.

Our Retirement Plan Services business unit offers a bundled 401(k) retirement plan product that provides retirement plan sponsors a wide array of investment options, trustee or custodial services, and participant-level recordkeeping. Retirement plan design features, which increase plan efficiency and achieve employer goals, are also offered, such as automatic enrollment, automatic fund mapping at conversion, and automatic contribution increases. In addition to an open architecture investment platform, we offer access to low cost index mutual funds and ETFs. Individuals investing for retirement through 401(k) plans can take advantage of bundled offerings of multiple investment choices, education, and third-party advice. This third-party advice service is delivered online, by phone, or in person, including recommendations based on the core investment fund choices in their retirement plan and specific recommended savings rates. Services also include support for Roth 401(k) accounts, profit sharing, and defined benefit plans.

Lastly, the Mutual Fund Clearing Services business unit provides custody, recordkeeping, and trading services to banks, brokerage firms, and trust companies, and the Off-Platform Sales business unit offers proprietary mutual funds, ETFs, and collective trust funds outside the Company. They are included within the Investor Services segment given their leveraging of the products and services offered to individual investors.

Advisor Services

More than twenty-five years ago, Schwab supported a small group of entrepreneurial advisors who challenged the industry by creating independent firms. Through the Advisor Services segment, Schwab has become the largest provider of custodial, trading, banking, and support services to RIAs and their clients. We also provide retirement business services to independent retirement advisors and recordkeepers. Management believes that we can maintain our market leadership position primarily through the efforts of our sales, support, and business consulting service teams, which are dedicated to helping RIAs grow, compete, and succeed in serving their clients. In addition to focusing on superior service, we utilize technology to provide RIAs with a highly-developed, scalable platform for administering their clients' assets easily and efficiently. Advisor Services sponsors a variety of national, regional, and local events designed to help RIAs identify and implement better ways to expand and efficiently manage their practices.

- 4 -

THE CHARLES SCHWAB CORPORATION

RIAs who custody client accounts at Schwab may use proprietary software that provides them with up-to-date client account information as well as trading capabilities. The Advisor Services website is the core platform for RIAs to conduct daily business activities online with Schwab, including viewing and managing client account information and accessing news and market information. The website provides account servicing capabilities for RIAs, including account opening, money movement, transfer of assets, trading, checking status, and communicating with our service team. The site provides multi-year archiving of statements, trade confirms, and tax reports, along with document search capabilities.

To help RIAs grow and manage their practices, we offer a variety of services, including business management and technology and operations consulting on a variety of topics critical to an RIA's success including strategic business planning, client segmentation, growth strategies, technological strategies, and succession planning. The Advisor Services website provides interactive tools, educational content, and research reports to assist advisors thinking about establishing and managing their own independent practices.

We also offer an array of services to help advisors establish their own independent practices through the Business Start-up Solutions package. These services include access to dedicated service teams and outsourcing of back-office operations, as well as third-party firms who provide assistance with real estate, errors and omissions insurance, and company benefits.

We provide a variety of educational materials, programs, and events to RIAs seeking to expand their knowledge of industry issues and trends, as well as sharpen their individual expertise and practice management skills. We update and share market research on an ongoing basis, and hold a series of events and conferences every year to discuss topics of interest to RIAs, including business strategies and best practices. Schwab sponsors the annual IMPACT ® conference, which provides a national forum for the Company, RIAs, and other industry participants to gather and share information and insights, as well as a multitude of smaller events across the country each year.

RIAs and their clients have access to a broad range of our products and services, including individual securities, mutual funds, ETFs, managed accounts, cash products, and bank lending. By functioning as the custodian, Schwab earns revenue associated with the underlying client assets invested in our products and utilization of the services we provide. In this capacity, we do not charge an explicit custodial fee.

The Advisor Services segment also includes the Retirement Business Services and Corporate Brokerage Retirement Services business units. Retirement Business Services provides trust, custody, and retirement business services to independent retirement plan advisors and independent recordkeepers. Retirement plan assets are held at the Business Trust division of Schwab Bank. The Company and independent retirement plan providers work together to serve plan sponsors; combining the consulting and administrative expertise of the administrator with our investment, technology, trust, and custodial services. Retirement Business Services also offers the Schwab Personal Choice Retirement Account ® , a self-directed brokerage offering for retirement plans.

Corporate Brokerage Retirement Services serves plan sponsors, advisors, and independent recordkeepers seeking a brokerage-based account to hold retirement plan assets. Retirement plans held at Schwab are either self-trusteed or trusteed by a separate, independent trustee. Corporate Brokerage Retirement Services also offers the Schwab Personal Choice Retirement Account ® , and the Company Retirement Account, both of which are self-directed brokerage-based solutions designed to hold the assets of company-sponsored retirement plans.

Regulation

As a participant in the securities, banking and financial services industries, Schwab is subject to extensive regulation under both federal and state laws by governmental agencies, supervisory authorities, and self-regulatory organizations (SROs). We are also subject to oversight by regulatory bodies in other countries in which we operate. These regulations affect our business operations and impose capital, client protection, and market conduct requirements.

As a result of the enactment of the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010 (Dodd-Frank), the adoption of implementing regulations by the federal regulatory agencies, and other recent regulatory reforms, we have experienced significant changes in the laws and regulations that apply to us, how we are regulated, and regulatory expectations in the areas of compliance, risk management, corporate governance, operations, capital, and liquidity.

- 5 -

THE CHARLES SCHWAB CORPORATION

Holding Company and Bank Regulation

CSC is a savings and loan holding company and is regulated, supervised, and examined by the Board of Governors of the Federal Reserve System (Federal Reserve). CSC's principal depository institution subsidiary, Schwab Bank, is a federal savings bank and is regulated, supervised, and examined by the Office of the Comptroller of the Currency (OCC), the Consumer Financial Protection Bureau (CFPB), and the FDIC. CSC and Schwab Bank are also subject to regulation and various requirements and restrictions under state and other federal laws.

This regulatory framework is designed to protect depositors and consumers, the safety and soundness of depository institutions and their holding companies, and the stability of the banking system as a whole. This framework affects the activities and investments of CSC and its subsidiaries and gives the regulatory authorities broad discretion in connection with their supervisory, examination and enforcement activities and policies.

Financial Regulatory Reform

Following the enactment of Dodd-Frank, the federal banking agencies have adopted a number of implementing regulations and other regulatory reforms that are significant for CSC and its banking subsidiaries. These regulations are highlighted below.

Basel III Capital and Liquidity Framework

Banking organizations are subject to the regulatory capital rules issued by the Federal Reserve and other U.S. banking regulators, including the OCC and the FDIC. In addition to minimum risk-based capital requirements, banking organizations must hold additional capital, referred to as a capital conservation buffer, to avoid being subject to limits on capital distributions and discretionary bonus payments to executive officers.

The regulatory capital rules provide for a "standardized approach" framework for the calculation of a banking organization's regulatory capital and risk-weighted assets. Depository institutions and their holding companies with consolidated total assets of $250 billion or more, or total on-balance-sheet foreign exposure of $10 billion or more, are also required to calculate their regulatory capital and risk-weighted assets using an "advanced approaches" framework and must satisfy the minimum capital requirements under both approaches. Such companies must also maintain a minimum supplementary leverage ratio of at least 3.0%, must include accumulated other comprehensive income (AOCI) in their calculation of their capital ratios, and are subject to certain other enhanced provisions, including additional reporting requirements. CSC and its banking subsidiaries are currently only subject to the "standardized approach" framework but will become subject to the "advanced approaches" framework upon exceeding either of the thresholds.

The liquidity coverage ratio (LCR) rule requires banking organizations with consolidated total assets of $250 billion or more, or total on-balance-sheet foreign exposure of $10 billion or more and their depository institution subsidiaries with $10 billion or more in total consolidated assets to hold high quality liquid assets (HQLA) in an amount equal to at least 100% of their projected net cash outflows over the 30-day period, calculated on each business day. Other bank and savings and loan holding companies with total consolidated assets of $50 billion or more are subject to a modified LCR rule requiring them to hold HQLA in an amount equal to at least 70% of their projected net cash outflows over the 30-day period, calculated as of the last business day of the month.

Capital Stress Testing

Savings and loan holding companies and federal savings bank with total consolidated assets of more than $10 billion are required to conduct annual company-run stress tests. Under the Dodd-Frank Act Stress Test (DFAST) rules, CSC (for the first time in 2017) and Schwab Bank must conduct annual stress tests using certain scenarios and prescribed stress-testing methodologies, report the results to the Federal Reserve and, for Schwab Bank, the OCC, and publish summaries of the results of their stress tests.

As a savings and loan holding company, CSC is not subject to the annual Comprehensive Capital Analysis and Review (CCAR) process, which requires certain financial institutions to submit annual capital plans to the Federal Reserve. CSC continues to enhance its stress testing policies, procedures, systems, and governance structures to be consistent with regulatory expectations for a firm of its size and complexity.

- 6 -

THE CHARLES SCHWAB CORPORATION

Insured Depository Institution Resolution Plans

The FDIC requires insured depository institutions with total consolidated assets of $50 billion or more to submit to the FDIC periodic plans providing for their resolution by the FDIC in the event of failure (resolution plans or so-called "living wills") under the receivership and liquidation provisions of the Federal Deposit Insurance Act. Schwab Bank is required to file with the FDIC an annual resolution plan demonstrating how the bank could be resolved in an orderly and timely manner in the event of receivership such that the FDIC would be able to: ensure that the bank's depositors receive access to their deposits within one business day; maximize the net present value of the bank's assets when disposed of; and minimize losses incurred by the bank's creditors.

Consumer Financial Protection

The CFPB has broad rulemaking, supervisory and enforcement authority for a wide range of federal consumer protection laws relating to financial products. The CFPB has examination and primary enforcement authority over depository institutions with $10 billion or more in consolidated total assets.

Deposit Insurance Assessments

The FDIC's Deposit Insurance Fund (DIF) provides insurance coverage for certain deposits, generally up to $250,000 per depositor per account ownership type, and is funded by quarterly assessments on insured depository institutions. The FDIC uses a risk-based deposit premium assessment system that, for large insured depository institutions with at least $10 billion in total consolidated assets, uses a scorecard method based on a number of factors, including the institution's regulatory ratings, asset quality and brokered deposits. The deposit insurance assessment base is calculated as average consolidated total assets minus average tangible equity.

The Dodd-Frank Act (i) raised the minimum reserve ratio for the DIF to 1.35% (from the former minimum of 1.15%) and (ii) required that the DIF's reserve ratio reach 1.35% by September 30, 2020.

In July 2016, the FDIC imposed a flat-rate quarterly surcharge on insured depository institutions with total assets of $10 billion or more and certain of their bank affiliates to pay for the increase. The surcharge took effect at the same time as a scheduled reduction in the regular FDIC insurance. As a result, Schwab's banking subsidiaries are now subject to a 3 basis point regular assessment on their respective assessment bases (down from 5 basis points) and a new 4.5 basis point surcharge on the amount of their aggregate assessment base in excess of $10 billion that will remain in effect until the earlier of the DIF reaching 1.35% or December 31, 2018. If DIF has not reached 1.35% by such date, the FDIC will impose a shortfall assessment.

Community Reinvestment Act

The Community Reinvestment Act of 1977 (CRA) requires the primary federal bank regulatory agency for each of Schwab's depository institution subsidiaries to assess the subsidiary's record in meeting the credit needs of the communities served by the bank, including low- and moderate-income neighborhoods and persons. Institutions are assigned one of four ratings ("outstanding," "satisfactory," "needs to improve," or "substantial noncompliance"). The failure of an institution to receive at least a "satisfactory" rating could inhibit the institution or its holding company from undertaking certain activities, including acquisitions or opening branch offices.

Source of Strength

The Dodd-Frank Act codified the Federal Reserve's long-held position that a depository institution holding company must serve as a source of financial strength for its subsidiary depository institutions, the so-called "source of strength doctrine." In effect, the holding company may be compelled to commit resources to support the subsidiary in the event the subsidiary is in financial distress.

- 7 -

THE CHARLES SCHWAB CORPORATION

Broker-Dealer and Investment Advisor Regulation

Schwab's principal broker-dealer is CS&Co. CS&Co is registered as a broker-dealer with the United States Securities and Exchange Commission (SEC), the fifty states, the District of Columbia and Puerto Rico. CS&Co and CSIM are registered as investment advisors with the SEC. Additionally, CS&Co is regulated by the Commodities Futures Trading Commission (CFTC) with respect to the commodity futures and trading activities it conducts as an introducing broker.

Much of the regulation of broker-dealers has been delegated to SROs. CS&Co is a member of the Financial Industry Regulatory Authority, Inc. (FINRA), the Municipal Securities Rulemaking Board (MSRB), NYSE Arca, and the Chicago Board Options Exchange (CBOE). In addition to the SEC, the primary regulators of CS&Co are FINRA and, for municipal securities, the MSRB. The National Futures Association (NFA) is CS&Co's primary regulator for futures and commodities trading activities.

The principal purpose of regulating broker-dealers and investment advisors is the protection of clients and securities markets. The regulations cover all aspects of the securities business, including, among other things, sales and trading practices, publication of research, margin lending, uses and safekeeping of clients' funds and securities, capital adequacy, recordkeeping and reporting, fee arrangements, disclosure to clients, fiduciary duties owed to advisory clients, and the conduct of directors, officers, and employees.

CS&Co is subject to Rule 15c3-1 under the Securities Exchange Act of 1934 (the Uniform Net Capital Rule) and related SRO requirements. The CFTC and NFA also impose net capital requirements. The Uniform Net Capital Rule specifies minimum capital requirements intended to ensure the general financial soundness and liquidity of broker-dealers. CSC itself is not a registered broker-dealer and it is not subject to the Uniform Net Capital Rule. If CS&Co fails to maintain specified levels of net capital, such failure could constitute a default by CSC of certain debt covenants under its credit agreement.

The Uniform Net Capital Rule prohibits CS&Co from paying cash dividends, making unsecured advances or loans or repaying subordinated loans if such payment would result in a net capital amount of less than 5% of aggregate debit balances or less than 120% of its minimum dollar requirement of $250,000.

In addition to net capital requirements, as a self-clearing broker-dealer, CS&Co is subject to cash deposit and collateral requirements with clearing houses, such as the Depository Trust & Clearing Corporation and Options Clearing Corporation, which may fluctuate significantly from time to time based upon the nature and size of clients' trading activity and market volatility.

Financial Service Regulation

Bank Secrecy Act of 1970 and USA PATRIOT Act of 2001

CSC and its subsidiaries that conduct financial services activities are subject to the Bank Secrecy Act of 1970 (BSA), as amended by the USA PATRIOT Act of 2001, which requires financial institutions to develop and implement programs reasonably designed to achieve compliance with these regulations. The BSA and USA PATRIOT Act include a variety of monitoring, recordkeeping and reporting requirements (such as currency transaction reporting and suspicious activity reporting), as well as identity verification and client due diligence requirements which are intended to detect, report and/or prevent money laundering, and the financing of terrorism. In addition, CSC and various subsidiaries of the Company are subject to U.S. sanctions programs administered by the Office of Foreign Assets Control.

Available Information

Schwab files annual, quarterly, and current reports, proxy statements, and other information with the SEC. The SEC filings are available to the public over the Internet on the SEC's website at https://www.sec.gov . You may read and copy any document that the Company files with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

On Schwab's website, https://www.aboutschwab.com , the following filings are posted after they are electronically filed with or furnished to the SEC: annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934.

- 8 -

THE CHARLES SCHWAB CORPORATION

In addition, the website also includes the Dodd-Frank stress test results and our regulatory capital disclosures based on Basel III.

All such filings are available free of charge either on our website or by request via email ( [email protected] ), telephone (415-667-7000), or mail (Charles Schwab Investor Relations at 211 Main Street, San Francisco, CA 94105).

Item 1A. | Risk Factors |

We face a variety of risks that may affect our operations, financial results, or stock price and many of those risks are driven by factors that we cannot control or predict. The following discussion addresses those risks that management believes are the most significant, although there may be other risks that could arise, or may prove to be more significant than expected, that may affect our operations or financial results.

For a discussion of our risk management, including operational risk, compliance risk, credit risk, market risk, and liquidity risk, see Risk Management and Capital Management in Part II, Item 7.

Developments in the business, economic, and geopolitical environment could negatively impact our business.

Our business can be adversely affected by the general environment – economic, corporate, securities market, regulatory, and geopolitical developments all play a role in client asset valuations, trading activity, interest rates, and overall investor engagement, and are outside of our control. Deterioration in the housing and credit markets, reduction in short-term interest rates, and decreases in securities valuations negatively impact our results of operations and capital resources.

Extensive regulation of our businesses may subject us to significant penalties or limitations on business activities.

As a participant in the securities, banking, and financial services industries, we are subject to extensive regulation under federal, state, and foreign laws by governmental agencies, supervisory authorities and SROs. The costs and uncertainty related to complying with such regulations continue to increase. These regulations affect our business operations and impose capital, client protection, and market conduct requirements on us.

In addition to specific banking laws and regulations, our banking regulators have broad discretion in connection with their supervisory and enforcement activities and examination policies and could require CSC and/or our banking subsidiaries to hold more capital, increase liquidity, or limit their ability to pay dividends or CSC's ability to repurchase or redeem shares. The banking regulators could also limit our ability to grow, including adding assets, launching new products, making acquisitions, and undertaking strategic investments, could limit our banking subsidiaries' ability to accept deposits swept from client brokerage accounts and brokered deposits and could prevent us from pursuing our business strategy.

Despite our efforts to comply with applicable legal requirements, there are a number of risks, particularly in areas where applicable laws or regulations may be unclear or where regulators could revise their previous guidance. Any enforcement actions or other proceedings brought by our regulators against us or our affiliates, officers or employees could result in fines, penalties, cease and desist orders, enforcement actions, suspension, disqualification or expulsion, or other disciplinary sanctions, including limitations on our business activities, any of which could harm our reputation and adversely affect our results of operations and financial condition.

While we maintain systems and procedures designed to ensure that we comply with applicable laws and regulations, violations could occur. In addition, some legal/regulatory frameworks provide for the imposition of fines or penalties for noncompliance even though the noncompliance was inadvertent or unintentional and even though systems and procedures reasonably designed to prevent violations were in place at the time. There may be other negative consequences resulting from a finding of noncompliance, including restrictions on certain activities. Such a finding may also damage our reputation and our relationships with our regulators and could restrict the ability of institutional investment managers to invest in our securities.

- 9 -

THE CHARLES SCHWAB CORPORATION

Legislation or changes in rules and regulations could negatively affect our business and financial results.

New legislation, rules, regulations and guidance, or changes in the interpretation or enforcement of existing federal, state, foreign and SRO rules, regulations and guidance, including changes relating to mutual funds, broker-dealer fiduciary duties and regulatory treatment of deposit accounts, may directly affect the operation and profitability of Schwab or its specific business lines. Our profitability could also be affected by rules and regulations that impact the business and financial communities generally, including changes to the laws governing taxation, electronic commerce, client privacy and security of client data. In addition, the rules and regulations could result in limitations on the lines of business we conduct, modifications to our business practices, more stringent capital and liquidity requirements, increased deposit insurance assessments or additional costs. These changes may also require us to invest significant management attention and resources to evaluate and make necessary changes to our compliance, risk management, treasury and operations functions.

Failure to meet capital adequacy and liquidity guidelines could affect our financial condition.

CSC, together with its banking and broker-dealer subsidiaries, must meet certain capital and liquidity standards, subject to qualitative judgments by regulators about the adequacy of Schwab's capital and Schwab's internal assessment of its capital needs. The Uniform Net Capital Rule limits CS&Co's ability to transfer capital to CSC and other affiliates. New regulatory capital, liquidity, and stress testing requirements may limit or otherwise restrict how we utilize our capital, including paying dividends, stock repurchases, and redemptions, and may require us to increase our capital and/or liquidity or to limit our growth. Failure by either CSC or its banking subsidiaries to meet minimum capital requirements could result in certain mandatory and additional discretionary actions by regulators that, if undertaken, could have a negative impact on us. In addition, failure by CSC or our banking subsidiaries to maintain a sufficient amount of capital to satisfy their capital conservation buffer requirements (as phased in) would result in restrictions on our ability to make capital distributions and discretionary cash bonus payments to executive officers. Any requirement that we increase our regulatory capital, replace certain capital instruments which presently qualify as Tier 1 capital, or increase regulatory capital ratios or liquidity, could require us to liquidate assets, deleverage or otherwise change our business and/or investment plans, which may adversely affect our financial results. Issuing additional common stock would dilute the ownership of existing stockholders.

With $243.3 billion in consolidated total assets at December 31, 2017 , we are currently only subject to the "standardized approach" capital framework of Basel III and modified liquidity requirements. When our consolidated total assets equal or exceed $250 billion, we will become subject to the "advanced approaches" framework, including being subject to a supplementary leverage ratio, the inclusion of AOCI in regulatory capital, the unmodified LCR, enhanced Basel III disclosures, and a more complex calculation of risk weighted assets that includes an assessment of the impact of operational risk. In addition, federal banking agencies have broad discretion and could require CSC or its banking subsidiaries to hold higher levels of capital or increase liquidity above the applicable regulatory requirements.

Significant interest rate changes could affect our profitability.

The direction and level of interest rates are important factors in our earnings. A decline in interest rates may have a negative impact on our net interest revenue. A low interest rate environment may also have a negative impact on our asset management and administration fee revenues if we have to waive a portion of our management fees for certain Schwab-sponsored money market mutual funds in order to continue providing a positive return to clients.

Overall, we are positioned to benefit from a rising interest rate environment. A rise in interest rates may cause our funding costs to increase if market conditions or the competitive environment forces us to raise our interest rates to avoid losing deposits. Higher funding costs without offsetting increases in yields on interest-earning assets can reduce our net interest revenue.

The manner in which interest rates are calculated could also impact our net interest revenue. For example, certain securities in Schwab's investment portfolios have floating interest rates based on benchmarks like the one-month LIBOR, which has been the subject of recent regulatory guidance and proposals for reform. These reforms may cause LIBOR to perform differently than in the past, or be replaced as a benchmark, and could result in lower interest payments and a reduction in the value of the securities.

- 10 -

THE CHARLES SCHWAB CORPORATION

A significant change in client cash allocations could negatively impact our net interest revenue.

We rely heavily on bank deposits as a low cost source of funding to extend loans to clients and purchase investment securities. Our bank deposits are primarily driven by our bank sweep feature: uninvested cash balances in our client brokerage accounts are swept to our banking subsidiaries. A significant reduction in our clients' allocation to cash, a change in the allocation of that cash, or a transfer of cash away from the Company, could reduce net interest revenue.

Security breaches of our systems, or those of our clients or third parties, may subject us to significant liability and damage Schwab's reputation.

Our business involves the secure processing, storage, and transmission of confidential information about our clients and us. Information security risks for financial institutions are increasing, in part because of the use of the internet and mobile technologies to conduct financial transactions, and the increased sophistication and activities of organized crime, activists, hackers and other external parties, including foreign state actors. Our systems and those of other financial institutions have been and are likely to continue to be the target of cyber attacks, malicious code, computer viruses and denial of service attacks that could result in unauthorized access, misuse, loss or destruction of data (including confidential client information), account takeovers, unavailability of service or other events. Despite our efforts to ensure the integrity of our systems, we may not be able to anticipate or to implement effective preventive measures against all security breaches of these types, especially because the techniques used change frequently or are not recognized until launched, and because security attacks can originate from a wide variety of sources. Data security breaches may also result from non-technical means, for example, employee misconduct.

Given the high volume of transactions that we process, the large number of clients, counterparties and third-party service providers with which we do business and the increasing sophistication of cyber attacks, a cyber attack could occur and persist for an extended period of time before being detected. The extent of a particular cyber attack and the steps we may need to take to investigate the attack may not be immediately clear, and it may take a significant amount of time before an investigation is completed and full and reliable information about the attack is known. During such time we would not necessarily know the extent of the harm or how best to remediate it, and certain errors or actions could be repeated or compounded before they are discovered and remediated, all or any of which would further increase the costs and consequences of a cyber attack.

Security breaches, including breaches of our security measures or those of our third-party service providers or clients, could result in a violation of applicable privacy and other laws and could subject us to significant liability or loss that may not be covered by insurance, actions by our regulators, damage to Schwab's reputation, or a loss of confidence in our security measures which could harm our business. We may be required to expend significant additional resources to modify our protective measures or to investigate and remediate vulnerabilities or other exposures.

We also face risk related to external fraud involving the misappropriation and use of clients' user names, passwords or other personal information to gain access to clients' financial accounts at Schwab. This could occur from the compromise of clients' personal electronic devices or as a result of a data security breach at an unrelated company where clients' personal information is taken and then made available to fraudsters. Such risk has grown in recent years due to the increased sophistication and activities of organized crime and other external parties, including foreign state-sponsored parties. Losses reimbursed to clients under our guarantee against unauthorized account activity could have a negative impact on our business, financial condition and results of operations.

Technology and operational failures or errors could subject us to losses, litigation, regulatory actions, and reputational damage.

We must process, record and monitor a large number of transactions and our operations are highly dependent on the integrity of our technology systems and our ability to make timely enhancements and additions to our systems. System interruptions, errors or downtime can result from a variety of causes, including changes in client use patterns, technological failure, changes to our systems, linkages with third-party systems and power failures and can have a significant impact on our business and operations. Our systems are vulnerable to disruptions from human error, execution errors, errors in models such as those used for asset management, capital planning and management, risk management, stress testing and compliance, employee misconduct, unauthorized trading, external fraud, computer viruses, distributed denial of service attacks, cyber attacks, terrorist attacks, natural disaster, power outage, capacity constraints, software flaws, events impacting key business partners and vendors, and similar events. For example, Schwab and other financial institutions have been the

- 11 -

THE CHARLES SCHWAB CORPORATION

target of various denial of service attacks that have, in certain circumstances, made websites, mobile applications and email unavailable for periods of time. It could take an extended period of time to restore full functionality to our technology or other operating systems in the event of an unforeseen occurrence, which could affect our ability to process and settle client transactions. Moreover, instances of fraud or other misconduct might also negatively impact Schwab's reputation and client confidence in the Company, in addition to any direct losses that might result from such instances. Despite our efforts to identify areas of risk, oversee operational areas involving risk, and implement policies and procedures designed to manage these risks, there can be no assurance that we will not suffer unexpected losses, reputational damage or regulatory action due to technology or other operational failures or errors, including those of our vendors or other third parties.

While we devote substantial attention and resources to the reliability, capacity and scalability of our systems, extraordinary trading volumes could cause our computer systems to operate at unacceptably slow speeds or even fail, affecting our ability to process client transactions and potentially resulting in some clients' orders being executed at prices they did not anticipate. Disruptions in service and slower system response times could result in substantial losses and decreased client satisfaction. We are also dependent on the integrity and performance of securities exchanges, clearing houses and other intermediaries to which client orders are routed for execution and settlement. System failures and constraints and transaction errors at such intermediaries could result in delays and erroneous or unanticipated execution prices, cause substantial losses for us and for our clients, and subject us to claims from our clients for damages.

A significant decrease in our liquidity could negatively affect our business and financial management as well as reduce client confidence in Schwab.

Maintaining adequate liquidity is crucial to our business operations, including margin lending, mortgage lending, and transaction settlement, among other liquidity needs. We meet our liquidity needs primarily through cash generated by client activity and operating earnings, as well as cash provided by external financing. Fluctuations in client cash or deposit balances, as well as changes in regulatory treatment of client deposits or market conditions, may affect our ability to meet our liquidity needs. A reduction in our liquidity position could reduce client confidence in Schwab, which could result in the loss of client accounts, or could cause us to fail to satisfy our liquidity requirements, including the modified LCR. In addition, if our broker-dealer or depository institution subsidiaries fail to meet regulatory capital guidelines, regulators could limit the subsidiaries' operations or their ability to upstream funds to CSC, which could reduce CSC's liquidity and adversely affect its ability to repay debt and pay cash dividends. In addition, CSC may need to provide additional funding to such subsidiaries.

Factors which may adversely affect our liquidity position include CS&Co having temporary liquidity demands due to timing differences between brokerage transaction settlements and the availability of segregated cash balances, unanticipated outflows of company cash, fluctuations in cash held in banking or brokerage client accounts, a dramatic increase in our client lending activities (including margin, mortgage-related, and personal lending), increased capital requirements, changes in regulatory guidance or interpretations, other regulatory changes, or a loss of market or client confidence in Schwab.

When cash generated by client activity and operating earnings is not sufficient for our liquidity needs, we may seek external financing. During periods of disruptions in the credit and capital markets, potential sources of external financing could be reduced, and borrowing costs could increase. Although CSC and CS&Co maintain committed and uncommitted, unsecured bank credit lines and CSC has a commercial paper issuance program, as well as a universal shelf registration statement filed with the SEC which can be used to sell securities, financing may not be available on acceptable terms or at all due to market conditions or disruptions in the credit markets. In addition, a significant downgrade in the Company's credit ratings could increase its borrowing costs and limit its access to the capital markets.

We may suffer significant losses from our credit exposures.

Our businesses are subject to the risk that a client, counterparty or issuer will fail to perform its contractual obligations, or that the value of collateral held to secure obligations will prove to be inadequate. While we have policies and procedures designed to manage this risk, the policies and procedures may not be fully effective. Our exposure mainly results from margin lending, clients' options trading, futures activities, securities lending, mortgage lending, pledged asset lending, our role as a counterparty in financial contracts and investing activities, and indirectly from the investing activities of certain of the proprietary funds we sponsor.

When clients purchase securities on margin, borrow on lines of credit collateralized by securities, or trade options or futures, we are subject to the risk that clients may default on their obligations when the value of the securities and cash in their

- 12 -

THE CHARLES SCHWAB CORPORATION

accounts falls below the amount of clients' indebtedness. Abrupt changes in securities valuations and the failure of clients to meet margin calls could result in substantial losses.

We have exposure to credit risk associated with our investments. Those investments are subject to price fluctuations as a result of changes in the financial market's assessment of credit quality. Loss of value of securities can negatively affect earnings if management determines that such securities are other than temporarily impaired. The evaluation of whether other-than-temporary impairment (OTTI) exists is a matter of judgment, which includes the assessment of several factors. If management determines that a security is OTTI, the cost basis of the security may be adjusted and a corresponding loss may be recognized in current earnings. Deterioration in the performance of available for sale (AFS) and held to maturity (HTM) securities could result in the recognition of future impairment charges. Even if a security is not considered OTTI, if we were ever forced to sell the security sooner than intended prior to maturity due to liquidity needs, we would have to recognize any unrealized losses at that time.

Our bank loans primarily consist of First Mortgages, HELOCs, and PALs. Increases in delinquency and default rates, housing and stock price declines, increases in the unemployment rate, and other economic factors can result in charges for loan loss reserves and write downs on such loans.

Heightened credit exposures to specific counterparties or instruments can increase our risk of loss. Examples include:

• | Large positions in financial instruments collateralized by assets with similar economic characteristics or in securities of a single issuer or industry; |

• | Mortgage loans and HELOCs to banking clients which are secured by properties in the same geographic region; and |

• | Client margins, options or futures, pledged assets, and securities lending activities collateralized by or linked to securities of a single issuer, index, or industry. |

We sponsor a number of proprietary money market mutual funds and other proprietary funds. Although we have no obligation to do so, we may decide for competitive or other reasons to provide credit, liquidity or other support to our funds in the event of significant declines in valuation of fund holdings or significant redemption activity that exceeds available liquidity. Such support could cause us to take significant charges, could reduce our liquidity and, in certain situations, could, with respect to proprietary funds other than money market mutual funds, result in us having to consolidate a supported fund in our financial statements. If we chose not to provide credit, liquidity or other support in such a situation, Schwab could suffer reputational damage and its business could be adversely affected.

We are subject to litigation and regulatory investigations and proceedings and may not be successful in defending against claims or proceedings.

The financial services industry faces significant litigation and regulatory risks. We are subject to claims and lawsuits in the ordinary course of business, including arbitrations, class actions and other litigation, some of which include claims for substantial or unspecified damages. We are also the subject of inquiries, investigations, and proceedings by regulatory and other governmental agencies.

Litigation and arbitration claims include those brought by our clients and the clients of third party advisors whose assets are custodied at Schwab. Claims from clients of third party advisors may allege losses due to investment decisions made by the third party advisors or the advisors' misconduct. Litigation claims also include claims from third parties alleging infringement of their intellectual property rights (e.g., patents). Such litigation can require the expenditure of significant company resources. If we were found to have infringed on a third-party patent, or other intellectual property rights, we could incur substantial damages, and in some circumstances could be enjoined from using certain technology, or providing certain products or services.

Actions brought against us may result in settlements, awards, injunctions, fines, penalties or other results adverse to us, including reputational harm. Even if we are successful in defending against these actions, the defense of such matters may result in us incurring significant expenses. A substantial judgment, settlement, fine, or penalty could be material to our operating results or cash flows for a particular future period, depending on our results for that period. In market downturns, the volume of legal claims and amount of damages sought in litigation and regulatory proceedings against financial services companies have historically increased.

- 13 -

THE CHARLES SCHWAB CORPORATION

We rely on outsourced service providers to perform key functions.

We rely on external service providers to perform certain key technology, processing, servicing, and support functions. These service providers face technology, operating, business, and economic risks, and any significant failures by them, including the improper use or disclosure of our confidential client, employee, or company information, could cause us to incur losses and could harm Schwab's reputation. An interruption in or the cessation of service by any external service provider as a result of systems failures, capacity constraints, financial difficulties or for any other reason, and our inability to make alternative arrangements in a timely manner could disrupt our operations, impact our ability to offer certain products and services, and result in financial losses to us. Switching to an alternative service provider may require a transition period and result in less efficient operations.

Potential strategic transactions could have a negative impact on our financial position.

We evaluate potential strategic transactions, including business combinations, acquisitions, and dispositions. Any such transaction could have a material impact on our financial position, results of operations, or cash flows. The process of evaluating, negotiating, and effecting any such strategic transaction may divert management's attention from other business concerns, and might cause the loss of key clients, employees, and business partners. Moreover, integrating businesses and systems may result in unforeseen expenditures as well as numerous risks and uncertainties, including the need to integrate operational, financial, and management information systems and management controls, integrate relationships with clients and business partners, and manage facilities and employees in different geographic areas. In addition, an acquisition may cause us to assume liabilities or become subject to litigation or regulatory proceedings. Further, we may not realize the anticipated benefits from an acquisition, and any future acquisition could be dilutive to our current stockholders' percentage ownership or to earnings per common share (EPS).

Our acquisitions and dispositions are typically subject to closing conditions, including regulatory approvals and the absence of material adverse changes in the business, operations or financial condition of the entity being acquired or sold. To the extent we enter into an agreement to buy or sell an entity, there can be no guarantee that the transaction will close when expected, or at all. If a material transaction does not close, our stock price could decline.

Our industry is characterized by aggressive price competition.

We continually monitor our pricing in relation to competitors and periodically adjust trade commission rates, interest rates on deposits and loans, fees for advisory services, expense ratios on mutual funds and ETFs, and other pricing to enhance our competitive position. Increased price competition from other financial services firms, such as reduced commissions to attract trading volume, higher deposit rates to attract client cash balances or reduced expense ratios to attract mutual fund or ETF investments, could impact our results of operations and financial condition.

We face competition in hiring and retaining qualified employees.

The market for qualified personnel in our business is highly competitive. At various times, different functions and roles are in especially high demand in the market, compelling us to pay more to attract talent. Our ability to continue to compete effectively will depend upon our ability to attract new employees and retain existing employees while managing compensation costs.

Our stock price has fluctuated historically, and may continue to fluctuate.

Our stock price can be volatile. Among the factors that may affect the volatility of our stock price are the following:

• | Our exposure to changes in interest rates; |

• | Speculation in the investment community or the press about, or actual changes in, our competitive position, organizational structure, executive team, operations, financial condition, financial reporting and results, expense discipline, or strategic transactions; |

• | The announcement of new products, services, acquisitions, or dispositions by us or our competitors; and |

• | Increases or decreases in revenue or earnings, changes in earnings estimates by the investment community, and variations between estimated financial results and actual financial results. |

- 14 -

THE CHARLES SCHWAB CORPORATION

Changes in the stock market generally, or as it concerns our industry, as well as geopolitical, corporate, regulatory, business, and economic factors may also affect our stock price.

Future sales of CSC's equity securities may adversely affect the market price of CSC's common stock and result in dilution.

CSC's certificate of incorporation authorizes CSC's Board of Directors, among other things, to issue additional shares of common or preferred stock or securities convertible or exchangeable into equity securities, without stockholder approval.

CSC may issue additional equity or convertible securities to raise additional capital or for other purposes. The issuance of any additional equity or convertible securities could be substantially dilutive to holders of CSC's common stock and may adversely affect the market price of CSC's common stock.

Item 1B. Unresolved Securities and Exchange Commission Staff Comments

None.

Item 2. Properties

A summary of Schwab's significant locations is presented in the following table. Locations are leased or owned as noted below. The square footage amounts are presented net of space that has been subleased to third parties.

December 31, 2017 | Square Footage | |

(amounts in thousands) | Leased | Owned |

Location |

|

|

Corporate headquarters: |

|

|

San Francisco, CA | 569 | - |

Service and other office space: |

|

|

Phoenix, AZ | 28 | 720 |

Denver, CO | - | 731 |

Austin, TX | 219 | 191 |

Dallas, TX | 188 | - |

Indianapolis, IN | - | 161 |

Orlando, FL | 148 | - |

Richfield, OH | - | 117 |

El Paso, TX | - | 105 |

Chicago, IL | 104 | - |

Substantially all of our branch offices are located in leased premises. The corporate headquarters, data centers, offices, and service centers support both of our segments.

Item 3. | Legal Proceedings |

For a discussion of legal proceedings, see Item 8 – Note 13.

Item 4. | Mine Safety Disclosures |

Not applicable.

- 15 -

THE CHARLES SCHWAB CORPORATION

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters,

and Issuer Purchases of Equity Securities

CSC's common stock is listed on The New York Stock Exchange under the ticker symbol SCHW. The number of common stockholders of record as of January 31, 2018 , was 6,055 . The closing market price per share on that date was $53.34 .

The quarterly high and low sales prices for CSC's common stock and the other information required to be furnished pursuant to this item are included in Item 8 – Note 18 and Note 24.

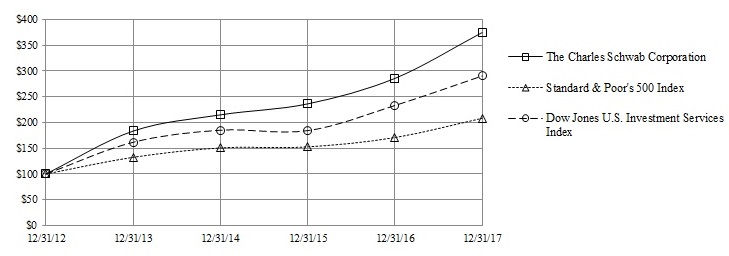

The following graph shows a five-year comparison of cumulative total returns for CSC's common stock, the Dow Jones U.S. Investment Services Index, and the Standard & Poor's 500 Index, each of which assumes an initial investment of $100 and reinvestment of dividends.

December 31, | 2012 | |

| 2013 | |

| 2014 | |

| 2015 | |

| 2016 | |

| 2017 | | ||||||

The Charles Schwab Corporation | $ | 100 | |

| $ | 183 | |

| $ | 215 | |

| $ | 236 | |

| $ | 286 | |

| $ | 375 | |

Standard & Poor's 500 Index | $ | 100 | |

| $ | 132 | |

| $ | 151 | |

| $ | 153 | |

| $ | 171 | |

| $ | 208 | |

Dow Jones U.S. Investment Services Index | $ | 100 | |

| $ | 162 | |

| $ | 185 | |

| $ | 184 | |

| $ | 233 | |

| $ | 290 | |

- 16 -

THE CHARLES SCHWAB CORPORATION

Issuer Purchases of Equity Securities

At December 31, 2017 , approximately $596 million of future share repurchases are authorized under the Share Repurchase Program. There were no share repurchases during the fourth quarter. There were two authorizations under this program by CSC's Board of Directors, each covering up to $500 million of common stock that were publicly announced by CSC on April 25, 2007, and March 13, 2008. The remaining authorizations do not have an expiration date.

The following table summarizes purchases made by or on behalf of CSC of its common stock for each calendar month in the fourth quarter of 2017 :

Month | Total Number of Shares Purchased |

| Average | |||

October: |

|

|

| |||

Employee transactions (1) | 4 | |

| $ | 44.12 | |

November: |

|

|

| |||

Employee transactions (1) | 779 | |

| $ | 44.70 | |

December: |

|

|

| |||

Employee transactions (1) | 2 | |

| $ | 48.97 | |

Total: |

|

|

| |||

Employee transactions (1) | 785 | |

| $ | 44.71 | |