Table of Contents

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

---------------------

FORM 10-Q

---------------------

x |

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2017

or

o |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to | ||

Commission File number 1-04721

---------------------

SPRINT CORPORATION

(Exact name of registrant as specified in its charter)

---------------------

Delaware | 46-1170005 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

|

|

6200 Sprint Parkway, Overland Park, Kansas | 66251 |

(Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: (855) 848-3280

---------------------

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x |

| Accelerated filer | o |

Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company | o |

|

|

| Emerging growth company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes o No x

COMMON SHARES OUTSTANDING AT OCTOBER 30, 2017 :

Sprint Corporation Common Stock | 4,000,345,604 | |

|

Table of Contents

SPRINT CORPORATION

TABLE OF CONTENTS

|

| Page Reference |

Item | PART I - FINANCIAL INFORMATION |

|

1. | Financial Statements | 1 |

| Consolidated Balance Sheets | 1 |

| Consolidated Statements of Comprehensive (Loss) Income | 2 |

| Consolidated Statements of Cash Flows | 3 |

| Consolidated Statement of Stockholders' Equity | 4 |

| Notes to the Consolidated Financial Statements | 5 |

2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 38 |

3. | Quantitative and Qualitative Disclosures About Market Risk | 60 |

4. | Controls and Procedures | 60 |

|

|

|

|

|

|

| PART II - OTHER INFORMATION |

|

1. | Legal Proceedings | 61 |

1A. | Risk Factors | 61 |

2. | Unregistered Sales of Equity Securities and Use of Proceeds | 61 |

3. | Defaults Upon Senior Securities | 61 |

4. | Mine Safety Disclosures | 61 |

5. | Other Information | 62 |

6. | Exhibits | 63 |

Signature | 65 | |

|

| |

Table of Contents

PART I - FINANCIAL INFORMATION

Item 1. | Financial Statements (Unaudited) |

SPRINT CORPORATION

CONSOLIDATED BALANCE SHEETS

| September 30, |

| March 31, | ||||

| 2017 |

| 2017 | ||||

| (in millions, except share and per share data) | ||||||

ASSETS | |||||||

Current assets: |

|

|

| ||||

Cash and cash equivalents | $ | 4,802 | |

| $ | 2,870 | |

Short-term investments | 1,610 | |

| 5,444 | | ||

Accounts and notes receivable, net of allowance for doubtful accounts and deferred interest of $350 and $354, respectively | 4,118 | |

| 4,138 | | ||

Device and accessory inventory | 751 | |

| 1,064 | | ||

Prepaid expenses and other current assets | 654 | |

| 601 | | ||

Total current assets | 11,935 | |

| 14,117 | | ||

Property, plant and equipment, net | 18,901 | |

| 19,209 | | ||

Intangible assets | | |

|

| |||

Goodwill | 6,578 | |

| 6,579 | | ||

FCC licenses and other | 41,072 | |

| 40,585 | | ||

Definite-lived intangible assets, net | 2,848 | |

| 3,320 | | ||

Other assets | 1,132 | |

| 1,313 | | ||

Total assets | $ | 82,466 | |

| $ | 85,123 | |

LIABILITIES AND STOCKHOLDERS' EQUITY | |||||||

Current liabilities: |

|

|

| ||||

Accounts payable | $ | 2,947 | |

| $ | 3,281 | |

Accrued expenses and other current liabilities | 3,808 | |

| 4,141 | | ||

Current portion of long-term debt, financing and capital lease obligations | 4,142 | |

| 5,036 | | ||

Total current liabilities | 10,897 | |

| 12,458 | | ||

Long-term debt, financing and capital lease obligations | 34,236 | |

| 35,878 | | ||

Deferred tax liabilities | 14,780 | |

| 14,416 | | ||

Other liabilities | 3,533 | |

| 3,563 | | ||

Total liabilities | 63,446 | |

| 66,315 | | ||

Commitments and contingencies | |

| | ||||

Stockholders' equity: |

|

|

| ||||

Common stock, voting, par value $0.01 per share, 9.0 billion authorized, 4.001 billion and 3.989 billion issued, respectively | 40 | |

| 40 | | ||

Paid-in capital | 27,807 | |

| 27,756 | | ||

Treasury shares, at cost | (9 | ) |

| - | | ||

Accumulated deficit | (8,426 | ) |

| (8,584 | ) | ||

Accumulated other comprehensive loss | (392 | ) |

| (404 | ) | ||

Total stockholders' equity | 19,020 | |

| 18,808 | | ||

Total liabilities and stockholders' equity | $ | 82,466 | |

| $ | 85,123 | |

See Notes to the Consolidated Financial Statements

1

Table of Contents

SPRINT CORPORATION

CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

| Three Months Ended |

| Six Months Ended | ||||||||||||

| September 30, |

| September 30, | ||||||||||||

| 2017 |

| 2016 |

| 2017 |

| 2016 | ||||||||

| (in millions, except per share amounts) | ||||||||||||||

Net operating revenues: |

|

|

|

|

|

|

| ||||||||

Service | $ | 5,967 | |

| $ | 6,413 | |

| $ | 12,038 | |

| $ | 12,929 | |

Equipment | 1,960 | |

| 1,834 | |

| 4,046 | |

| 3,330 | | ||||

| 7,927 | |

| 8,247 | |

| 16,084 | | | 16,259 | | ||||

Net operating expenses: |

|

|

|

|

|

|

| ||||||||

Cost of services (exclusive of depreciation and amortization included below) | 1,698 | |

| 2,101 | |

| 3,407 | |

| 4,200 | | ||||

Cost of products (exclusive of depreciation and amortization included below) | 1,404 | |

| 1,693 | |

| 2,949 | |

| 3,112 | | ||||

Selling, general and administrative | 2,013 | |

| 1,995 | |

| 3,951 | |

| 3,912 | | ||||

Severance and exit costs | - | |

| (5 | ) |

| - | |

| 11 | | ||||

Depreciation | 1,885 | |

| 1,710 | |

| 3,716 | |

| 3,390 | | ||||

Amortization | 209 | |

| 271 | |

| 432 | |

| 558 | | ||||

Other, net | 117 | |

| (140 | ) |

| (135 | ) |

| 93 | | ||||

| 7,326 | |

| 7,625 | |

| 14,320 | | | 15,276 | | ||||

Operating income | 601 | |

| 622 | |

| 1,764 | | | 983 | | ||||

Other (expense) income: |

|

|

|

|

|

|

| ||||||||

Interest expense | (595 | ) |

| (630 | ) |

| (1,208 | ) |

| (1,245 | ) | ||||

Other income (expense), net | 44 | |

| (15 | ) |

| (8 | ) |

| (7 | ) | ||||

| (551 | ) |

| (645 | ) |

| (1,216 | ) | | (1,252 | ) | ||||

Income (loss) before income taxes | 50 | |

| (23 | ) |

| 548 | | | (269 | ) | ||||

Income tax expense | (98 | ) |

| (119 | ) |

| (390 | ) |

| (175 | ) | ||||

Net (loss) income | $ | (48 | ) |

| $ | (142 | ) |

| $ | 158 | | | $ | (444 | ) |

|

|

|

|

|

|

|

| ||||||||

Basic net (loss) income per common share | $ | (0.01 | ) |

| $ | (0.04 | ) |

| $ | 0.04 | |

| $ | (0.11 | ) |

Diluted net (loss) income per common share | $ | (0.01 | ) |

| $ | (0.04 | ) |

| $ | 0.04 | |

| $ | (0.11 | ) |

Basic weighted average common shares outstanding | 3,998 | |

| 3,979 | |

| 3,996 | |

| 3,977 | | ||||

Diluted weighted average common shares outstanding | 3,998 | |

| 3,979 | |

| 4,080 | |

| 3,977 | | ||||

|

|

|

|

|

|

|

| ||||||||

Other comprehensive (loss) income, net of tax: |

|

|

|

|

|

|

| ||||||||

Net unrealized holding gains on securities and other | $ | 13 | |

| $ | 7 | |

| $ | 18 | |

| $ | 5 | |

Net unrealized holding gains (losses) on derivatives | 2 | |

| - | |

| (7 | ) |

| - | | ||||

Net unrecognized net periodic pension and other postretirement benefits | 1 | |

| 1 | |

| 1 | |

| 2 | | ||||

Other comprehensive gain | 16 | |

| 8 | |

| 12 | |

| 7 | | ||||

Comprehensive (loss) income | $ | (32 | ) |

| $ | (134 | ) |

| $ | 170 | |

| $ | (437 | ) |

See Notes to the Consolidated Financial Statements

2

Table of Contents

SPRINT CORPORATION

CONSOLIDATED STATEMENTS OF CASH FLOWS

| Six Months Ended | ||||||

| September 30, | ||||||

| 2017 |

| 2016 | ||||

| (in millions) | ||||||

Cash flows from operating activities: |

|

|

| ||||

Net income (loss) | $ | 158 | |

| $ | (444 | ) |

Adjustments to reconcile net income (loss) to net cash provided by operating activities: |

|

|

| ||||

Depreciation and amortization | 4,148 | |

| 3,948 | | ||

Provision for losses on accounts receivable | 199 | |

| 232 | | ||

Share-based and long-term incentive compensation expense | 87 | |

| 29 | | ||

Deferred income tax expense | 364 | |

| 157 | | ||

Gains from asset dispositions and exchanges | (479 | ) |

| (354 | ) | ||

Call premiums paid on debt redemptions | (129 | ) |

| - | | ||

Loss on early extinguishment of debt | 65 | |

| - | | ||

Amortization of long-term debt premiums, net | (90 | ) |

| (159 | ) | ||

Loss on disposal of property, plant and equipment | 410 | |

| 231 | | ||

Contract terminations | (5 | ) |

| 96 | | ||

Other changes in assets and liabilities: |

|

|

| ||||

Accounts and notes receivable | (179 | ) |

| (126 | ) | ||

Deferred purchase price from sale of receivables | - | |

| (400 | ) | ||

Inventories and other current assets | (1,459 | ) |

| (892 | ) | ||

Accounts payable and other current liabilities | (161 | ) |

| (195 | ) | ||

Non-current assets and liabilities, net | 183 | |

| (205 | ) | ||

Other, net | 127 | |

| 332 | | ||

Net cash provided by operating activities | 3,239 | |

| 2,250 | | ||

Cash flows from investing activities: |

|

|

| ||||

Capital expenditures - network and other | (1,803 | ) |

| (943 | ) | ||

Capital expenditures - leased devices | (1,105 | ) |

| (763 | ) | ||

Expenditures relating to FCC licenses | (19 | ) |

| (32 | ) | ||

Proceeds from sales and maturities of short-term investments | 5,582 | |

| 1,122 | | ||

Purchases of short-term investments | (1,748 | ) |

| (2,772 | ) | ||

Proceeds from sales of assets and FCC licenses | 218 | |

| 66 | | ||

Other, net | (1 | ) |

| (36 | ) | ||

Net cash provided by (used in) investing activities | 1,124 | |

| (3,358 | ) | ||

Cash flows from financing activities: |

|

|

| ||||

Proceeds from debt and financings | 1,860 | |

| 3,278 | | ||

Repayments of debt, financing and capital lease obligations | (4,261 | ) |

| (667 | ) | ||

Debt financing costs | (9 | ) |

| (175 | ) | ||

Other, net | (21 | ) |

| 37 | | ||

Net cash (used in) provided by financing activities | (2,431 | ) |

| 2,473 | | ||

Net increase in cash and cash equivalents | 1,932 | |

| 1,365 | | ||

Cash and cash equivalents, beginning of period | 2,870 | |

| 2,641 | | ||

Cash and cash equivalents, end of period | $ | 4,802 | |

| $ | 4,006 | |

See Notes to the Consolidated Financial Statements

3

Table of Contents

SPRINT CORPORATION

CONSOLIDATED STATEMENT OF STOCKHOLDERS' EQUITY

(in millions)

| Common Stock |

| Paid-in Capital |

| Treasury Shares |

| Accumulated Deficit |

| Accumulated Other Comprehensive Loss |

| Total | ||||||||||||||||||

| Shares |

| Amount | Shares |

| Amount | |||||||||||||||||||||||

Balance, March 31, 2017 | 3,989 | |

| $ | 40 | |

| $ | 27,756 | |

| - | |

| $ | - | |

| $ | (8,584 | ) |

| $ | (404 | ) |

| $ | 18,808 | |

Net income |

|

|

|

|

|

|

|

|

|

| 158 | |

|

|

| 158 | | ||||||||||||

Other comprehensive gain, net of tax |

|

|

|

|

|

|

|

|

|

|

|

| 12 | |

| 12 | | ||||||||||||

Issuance of common stock, net | 11 | |

|

|

| 10 | |

| 1 | |

| (9 | ) |

| |

|

|

| 1 | | |||||||||

Share-based compensation expense |

|

|

|

| 87 | |

|

|

|

|

|

|

|

|

| 87 | | ||||||||||||

Capital contribution by SoftBank |

|

|

|

| 5 | |

|

|

|

|

|

|

|

|

| 5 | | ||||||||||||

Other, net |

|

|

|

| (51 | ) |

|

|

|

|

|

|

|

|

| (51 | ) | ||||||||||||

Balance, September 30, 2017 | 4,000 | |

| $ | 40 | |

| $ | 27,807 | |

| 1 | |

| $ | (9 | ) |

| $ | (8,426 | ) |

| $ | (392 | ) |

| $ | 19,020 | |

See Notes to the Consolidated Financial Statements

4

Table of Contents

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

INDEX

|

| Page Reference |

1. | Basis of Presentation | 6 |

|

|

|

2. | New Accounting Pronouncements | 6 |

|

|

|

3. | Installment Receivables | 8 |

|

|

|

4. | Financial Instruments | 9 |

|

|

|

5. | Property, Plant and Equipment | 10 |

|

|

|

6. | Intangible Assets | 11 |

|

|

|

7. | Accounts Payable | 12 |

|

|

|

8. | Long-Term Debt, Financing and Capital Lease Obligations | 13 |

|

|

|

9. | Severance and Exit Costs | 19 |

|

|

|

10. | Income Taxes | 20 |

|

|

|

11. | Commitments and Contingencies | 21 |

|

|

|

12. | Per Share Data | 23 |

|

|

|

13. | Segments | 23 |

|

|

|

14. | Related-Party Transactions | 27 |

|

|

|

15. | Guarantor Financial Information | 29 |

|

|

|

5

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note 1. | Basis of Presentation |

The accompanying unaudited consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X for interim financial information. All normal recurring adjustments considered necessary for a fair presentation have been included. Certain disclosures normally included in annual consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States (U.S. GAAP) have been omitted. These consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes contained in our annual report on Form 10-K for the year ended March 31, 2017 . Unless the context otherwise requires, references to "Sprint," "we," "us," "our" and the "Company" mean Sprint Corporation and its consolidated subsidiaries for all periods presented, and references to "Sprint Communications" are to Sprint Communications, Inc. and its consolidated subsidiaries.

The preparation of the unaudited interim consolidated financial statements requires management of the Company to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses and the disclosure of contingent assets and liabilities at the date of the unaudited interim consolidated financial statements. These estimates are inherently subject to judgment and actual results could differ.

Certain prior period amounts have been reclassified to conform to the current period presentation.

Note 2. | New Accounting Pronouncements |

In May 2014, the Financial Accounting Standards Board (FASB) issued new authoritative literature, Revenue from Contracts with Customers, and has subsequently modified several areas of the standard in order to provide additional clarity and improvements . The issuance is part of a joint effort by the FASB and the International Accounting Standards Board (IASB) to enhance financial reporting by creating common revenue recognition guidance for U.S. GAAP and International Financial Reporting Standards and, thereby, improving the consistency of requirements, comparability of practices and usefulness of disclosures. The new standard will supersede much of the existing authoritative literature for revenue recognition. The standard and related amendments will be effective for the Company for its fiscal year beginning April 1, 2018, including interim periods within that fiscal year.

Two adoption methods are available for implementation of the standard update related to the recognition of revenue from contracts with customers. Under the full retrospective method, the guidance is applied retrospectively to contracts for each reporting period presented, subject to allowable practical expedients. Under the modified retrospective method, the guidance is applied only to the most current period presented, recognizing the cumulative effect of the change as an adjustment to the beginning balance of retained earnings, and also requires additional disclosures comparing the results to the previous guidance. We currently anticipate adopting the standard using the modified retrospective method.

The ultimate impact on revenue resulting from the application of the new standard will be subject to assessments that are dependent on many variables, including, but not limited to, the terms and mix of the contractual arrangements we have with customers. Upon adoption, we expect that the allocation of revenue between equipment and service for our wireless fixed-term service plans will result in more revenue allocated to equipment and recognized earlier as compared with current GAAP. We expect the timing of recognition of our sales commission expenses will also be impacted, as a substantial portion of these costs (which are currently expensed) will be capitalized and amortized consistent with the transfer of the related good or service. Consequently, we expect this guidance to have a material impact on our consolidated financial statements.

In July 2015, the FASB issued authoritative guidance regarding Inventory , which simplifies the subsequent measurement of certain inventories by replacing today's lower of cost or market test with a lower of cost and net realizable value test. Net realizable value is the estimated selling prices in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation. The standard is effective for the Company's fiscal year beginning April 1, 2017, including interim periods within this fiscal year, and the adoption of this guidance did not have a material impact on our consolidated financial statements.

In January 2016, the FASB issued authoritative guidance regarding Financial Instruments , which amended guidance on the classification and measurement of financial instruments. Under the new guidance, entities will be required to measure equity investments that are not consolidated or accounted for under the equity method at fair value with any changes in fair value recorded in net income, unless the entity has elected the new practicability exception. For financial liabilities

6

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

measured using the fair value option, entities will be required to separately present in other comprehensive income the portion of the changes in fair value attributable to instrument-specific credit risk. Additionally, the guidance amends certain disclosure requirements associated with the fair value of financial instruments. The standard will be effective for the Company's fiscal year beginning April 1, 2018, including interim reporting periods within that fiscal year. The Company does not expect the adoption of this guidance to have a material impact on our consolidated financial statements.

In February 2016, the FASB issued authoritative guidance regarding Leases. The new standard will supersede much of the existing authoritative literature for leases. This guidance requires lessees, among other things, to recognize right-of-use assets and liabilities on their balance sheet for all leases with lease terms longer than twelve months. The standard will be effective for the Company for its fiscal year beginning April 1, 2019, including interim periods within that fiscal year, with early application permitted. Entities are required to use modified retrospective application for leases that exist or are entered into after the beginning of the earliest comparative period in the financial statements with the option to elect certain transition reliefs. The Company is currently evaluating the guidance and assessing its overall impact. However, we expect the adoption of this guidance to have a material impact on our consolidated financial statements.

In June 2016, the FASB issued authoritative guidance regarding Financial Instruments - Credit Losses , which requires entities to use a Current Expected Credit Loss impairment model based on expected losses rather than incurred losses. Under this model, an entity would recognize an impairment allowance equal to its current estimate of all contractual cash flows that the entity does not expect to collect from financial assets measured at amortized cost. The entity's estimate would consider relevant information about past events, current conditions and reasonable and supportable forecasts, which will result in recognition of lifetime expected credit losses. The standard will be effective for the Company's fiscal year beginning April 1, 2020, including interim reporting periods within that fiscal year, although early adoption is permitted. The Company does not expect the adoption of this guidance to have a material impact on our consolidated financial statements.

In August 2016, the FASB issued authoritative guidance regarding Statement of Cash Flows: Classification of Certain Cash Receipts and Cash Payments, to address diversity in how certain cash receipts and cash payments are presented and classified in the statement of cash flows. It provides guidance on eight specific cash flow issues. The standard will be effective for the Company for its fiscal year beginning April 1, 2018, including interim periods within that fiscal year, with early adoption permitted and retrospective application required. The Company is currently evaluating the guidance and assessing the impact it will have on our consolidated financial statements.

In October 2016, the FASB issued authoritative guidance regarding Income Taxes , which amended guidance for the income tax consequences of intra-entity transfers of assets other than inventory. Under the new guidance, entities will be required to recognize the income tax consequences of an intra-entity transfer of an asset other than inventory when the transfer occurs, thereby eliminating the recognition exception within current guidance. The standard will be effective for the Company's fiscal year beginning April 1, 2018, including interim reporting periods within that fiscal year. The Company does not expect the adoption of this guidance to have a material impact on our consolidated financial statements.

In November 2016, the FASB issued authoritative guidance regarding Statement of Cash Flows: Restricted Cash, requiring that amounts generally described as restricted cash or restricted cash equivalents be included with cash and cash equivalents when reconciling the beginning-of-period and end-of-period total amounts shown on the statement of cash flows. The standard will be effective for the Company's fiscal year beginning April 1, 2018, including interim reporting periods within that fiscal year, with early adoption permitted and retrospective application required. The Company does not expect the adoption of this guidance to have a material impact on our consolidated financial statements.

In January 2017, the FASB issued authoritative guidance amending Business Combinations: Clarifying the Definition of a Business , to clarify the definition of a business with the objective of providing a more robust framework to assist management when evaluating whether transactions should be accounted for as acquisitions (or disposals) of assets or businesses. The standard will be effective for the Company for its fiscal year beginning April 1, 2018, including interim periods within that fiscal year, with early application permitted. The amendments are to be applied prospectively to business combinations that occur after the effective date.

In January 2017, the FASB issued authoritative guidance regarding Intangibles - Goodwill and Other: Simplifying the Test for Goodwill Impairment , which simplifies the goodwill impairment test by eliminating the requirement to calculate the implied fair value of goodwill to measure a goodwill impairment charge (Step 2 of the test), but rather to record an impairment charge based on the excess of the carrying value over its fair value. The standard will be effective for the

7

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Company's annual goodwill impairment test in the fiscal year beginning April 1, 2020, with early adoption permitted. The Company does not expect the adoption of this guidance to have a material impact on our consolidated financial statements.

In August 2017, the FASB issued authoritative guidance regarding Derivatives and Hedging , which provided targeted improvements and simplifications to accounting for hedging activities and applies to entities that elect to apply hedge accounting in accordance with current U.S. GAAP. The amendments will be effective for the Company's fiscal year beginning April 1, 2019, and for interim periods within that fiscal year, with early adoption permitted. The Company does not expect the adoption of this guidance to have a material impact on our consolidated financial statements.

Note 3. | Installment Receivables |

Certain subscribers have the option to pay for their devices in installments, generally up to a 24 -month period. Short-term installment receivables are recorded in "Accounts and notes receivable, net" and long-term installment receivables are recorded in "Other assets" in the consolidated balance sheets. From October 2015 to February 2017, installment receivables sold to unaffiliated third parties (the Purchasers) were treated as a sale of financial assets and we derecognized these receivables, as well as the related allowances. As a result of our Accounts Receivable Facility (Receivables Facility) being amended in February 2017, all proceeds received from the Purchasers in exchange for our installment receivables are now recorded as borrowings (see Note 8. Long-Term Debt, Financing and Capital Lease Obligations) .

The following table summarizes the installment receivables:

| September 30, |

| March 31, | ||||

| (in millions) | ||||||

Installment receivables, gross | $ | 2,017 | |

| $ | 2,270 | |

Deferred interest | (157 | ) |

| (207 | ) | ||

Installment receivables, net of deferred interest | 1,860 | |

| 2,063 | | ||

Allowance for credit losses | (277 | ) |

| (299 | ) | ||

Installment receivables, net | $ | 1,583 | |

| $ | 1,764 | |

|

|

|

| ||||

Classified on the consolidated balance sheets as: |

|

|

| ||||

Accounts and notes receivable, net | $ | 1,269 | |

| $ | 1,195 | |

Other assets | 314 | |

| 569 | | ||

Installment receivables, net | $ | 1,583 | |

| $ | 1,764 | |

The balance and aging of installment receivables on a gross basis by credit category were as follows:

| September 30, 2017 |

| March 31, 2017 | ||||||||||||||||||||

| Prime |

| Subprime |

| Total |

| Prime |

| Subprime |

| Total | ||||||||||||

| (in millions) |

| (in millions) | ||||||||||||||||||||

Unbilled | $ | 1,354 | |

| $ | 507 | |

| $ | 1,861 | |

| $ | 1,501 | |

| $ | 619 | |

| $ | 2,120 | |

Billed - current | 75 | |

| 35 | |

| 110 | |

| 74 | |

| 36 | |

| 110 | | ||||||

Billed - past due | 23 | |

| 23 | |

| 46 | |

| 20 | |

| 20 | |

| 40 | | ||||||

Installment receivables, gross | $ | 1,452 | |

| $ | 565 | |

| $ | 2,017 | |

| $ | 1,595 | |

| $ | 675 | |

| $ | 2,270 | |

8

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Activity in the deferred interest and allowance for credit losses for the installment receivables was as follows:

| Six Months Ended |

| Twelve Months Ended | ||||

| September 30, 2017 |

| March 31, 2017 | ||||

| (in millions) | ||||||

Deferred interest and allowance for credit losses, beginning of period | $ | 506 | |

| $ | - | |

Bad debt expense | 97 | |

| 61 | | ||

Write-offs, net of recoveries | (119 | ) |

| (28 | ) | ||

Change in deferred interest on short-term and long-term installment receivables | (50 | ) |

| 8 | | ||

Recognition of deferred interest and allowance for credit losses | - | |

| 465 | | ||

Deferred interest and allowance for credit losses, end of period | $ | 434 | |

| $ | 506 | |

Note 4. | Financial Instruments |

The Company carries certain assets and liabilities at fair value. Fair value is defined as an exit price, representing the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The three-tier hierarchy for inputs used in measuring fair value, which prioritizes the inputs based on the observability as of the measurement date, is as follows: quoted prices in active markets for identical assets or liabilities; observable inputs other than the quoted prices in active markets for identical assets and liabilities; and unobservable inputs for which there is little or no market data, which require the Company to develop assumptions of what market participants would use in pricing the asset or liability.

The carrying amount of cash equivalents, accounts and notes receivable, and accounts payable approximates fair value. Short-term investments are recorded at amortized cost and the respective carrying amounts approximate fair value primarily using quoted prices in active markets. Short-term investments totaled $1.6 billion and $5.4 billion and consisted of approximately $1.1 billion and $3.0 billion of time deposits and $500 million and $2.4 billion of commercial paper as of September 30, 2017 and March 31, 2017, respectively. The fair value of marketable equity securities totaling $53 million and $46 million as of September 30, 2017 and March 31, 2017 , respectively, are measured on a recurring basis using quoted prices in active markets.

Except for our financing transaction for the Handset Sale-Leaseback (Tranche 2) with Mobile Leasing Solutions, LLC (MLS) (see Note 8. Long-Term Debt, Financing and Capital Lease Obligations) , current and long-term debt and our other financings are carried at amortized cost. The Company elected to measure the financing obligation with MLS at fair value as a means to better reflect the economic substance of the arrangement. The Tranche 2 financing obligation, which amounted to $58 million as of September 30, 2017 and is reported in "Current portion of long-term debt, financing and capital lease obligations" in our consolidated balance sheets, is the only eligible financial instrument for which we have elected the fair value option.

The fair value of the financing obligation, which was determined at the outset of the arrangement using a discounted cash flow model, was derived by unobservable inputs such as customer churn rates, customer upgrade probabilities, and the likelihood that Sprint will elect the exchange option versus the termination option upon a customer upgrade. Any gains or losses resulting from changes in the fair value of the financing obligation are included in "Other income (expense), net" in the consolidated statements of comprehensive (loss) income. During the three and six-month periods ended September 30, 2017 , there was no material change in the fair value of the financing obligation. During the six-month period ended September 30, 2017 , we made principal repayments and non-cash adjustments totaling $327 million to MLS. In addition to the financing obligation with MLS, the remaining debt for which estimated fair value is determined based on unobservable inputs primarily represents borrowings under our secured equipment credit facilities, network equipment sale-leaseback, and sales of receivables under our Receivables Facility (see Note 8. Long-Term Debt, Financing and Capital Lease Obligations) . The carrying amounts associated with these borrowings approximate fair value.

The estimated fair value of the majority of our current and long-term debt, excluding our secured equipment credit facilities, sold wireless service, installment billing and future receivables, and borrowings under our network equipment sale-leaseback and Tranche 2 transactions, is determined based on quoted prices in active markets or by using other observable inputs that are derived principally from, or corroborated by, observable market data.

9

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

The following table presents carrying amounts and estimated fair values of current and long-term debt and financing obligations:

| Carrying amount at September 30, 2017 |

| Estimated Fair Value Using Input Type | ||||||||||||||||

|

| Quoted prices in active markets |

| Observable |

| Unobservable |

| Total estimated fair value | |||||||||||

| (in millions) | ||||||||||||||||||

Current and long-term debt and financing obligations | $ | 38,174 | |

| $ | 32,908 | |

| $ | 3,029 | |

| $ | 5,584 | |

| $ | 41,521 | |

| Carrying amount at March 31, 2017 |

| Estimated Fair Value Using Input Type | ||||||||||||||||

|

| Quoted prices in active markets |

| Observable |

| Unobservable |

| Total estimated fair value | |||||||||||

| (in millions) | ||||||||||||||||||

Current and long-term debt and financing obligations | $ | 40,581 | |

| $ | 33,196 | |

| $ | 4,352 | |

| $ | 5,468 | |

| $ | 43,016 | |

Note 5. | Property, Plant and Equipment |

Property, plant and equipment consists primarily of network equipment and other long-lived assets used to provide service to our subscribers. Non-cash accruals included in property, plant and equipment (excluding leased devices) totaled $360 million and $310 million as of September 30, 2017 and 2016 , respectively.

The following table presents the components of property, plant and equipment and the related accumulated depreciation:

| September 30, |

| March 31, | ||||

| (in millions) | ||||||

Land | $ | 259 | |

| $ | 260 | |

Network equipment, site costs and related software | 21,889 | |

| 21,693 | | ||

Buildings and improvements | 806 | |

| 818 | | ||

Non-network internal use software, office equipment, leased devices and other | 9,674 | |

| 8,625 | | ||

Construction in progress | 2,408 | |

| 2,316 | | ||

Less: accumulated depreciation | (16,135 | ) |

| (14,503 | ) | ||

Property, plant and equipment, net | $ | 18,901 | |

| $ | 19,209 | |

Sprint offers a leasing program to its customers whereby qualified subscribers can lease a device for a contractual period of time. At the end of the lease term, the subscriber has the option to turn in the device, continue leasing the device, or purchase the device. As of September 30, 2017 , substantially all of our device leases were classified as operating leases. Lease revenue associated with devices subject to operating leases, which is included in equipment revenue, was $966 million , $1.9 billion , $811 million and $1.6 billion for the three and six-month periods ended September 30, 2017 and 2016, respectively.

At lease inception, the devices leased through Sprint's direct channels are reclassified from inventory to property, plant and equipment. For those devices leased through indirect channels, Sprint purchases the device to be leased from the retailer at lease inception and reports these purchases as cash outflows for "Capital expenditures - leased devices" in the consolidated statements of cash flows. The devices are then depreciated using the straight-line method to their estimated residual value generally over the term of the lease.

10

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

The following table presents leased devices and the related accumulated depreciation:

| September 30, |

| March 31, | ||||

| (in millions) | ||||||

Leased devices | $ | 8,214 | |

| $ | 7,276 | |

Less: accumulated depreciation | (3,505 | ) |

| (3,114 | ) | ||

Leased devices, net | $ | 4,709 | |

| $ | 4,162 | |

During the six-month periods ended September 30, 2017 and 2016 , there were non-cash transfers to leased devices of approximately $1.9 billion and $1.2 billion , respectively, along with a corresponding decrease in "Device and accessory inventory" for devices leased through our direct channel. Non-cash accruals included in leased devices totaled $210 million and $96 million as of September 30, 2017 and 2016 , respectively, for devices purchased from indirect dealers that were leased to our subscribers. Depreciation expense incurred on all leased devices was $888 million and $1.7 billion for the three and six-month periods ended September 30, 2017 , respectively, and $724 million and $1.4 billion for the same periods in 2016 , respectively.

During the three and six-month periods ended September 30, 2017 and 2016 , we recorded $117 million , $404 million , $111 million and $231 million , respectively, of loss on disposal of property, plant and equipment, net of recoveries, which is included in "Other, net" within Operating income in our consolidated statements of comprehensive (loss) income. Net losses that resulted from the write-off of leased devices are primarily associated with lease cancellations prior to the scheduled customer lease terms where customers did not return the devices to us were $112 million , $224 million , $111 million , and $231 million for the three and six-month periods ended September 30, 2017 and 2016 , respectively. In addition, during the six-month period ended September 30, 2017 , losses totaling $180 million were related to $181 million of cell site construction costs that are no longer recoverable as a result of changes in our network plans during the three-month period ended June 30, 2017 and $5 million of hurricane-related charges during the three-month period ended September 30, 2017, offset by a $6 million gain.

Note 6. | Intangible Assets |

Indefinite-Lived Intangible Assets

Our indefinite-lived intangible assets consist of FCC licenses, which were acquired primarily through FCC auctions and business combinations, certain of our trademarks, and goodwill. At September 30, 2017 , we held 800 MHz, 1.9 GHz and 2.5 GHz FCC licenses authorizing the use of radio frequency spectrum to deploy our wireless services. As long as the Company acts within the requirements and constraints of the regulatory authorities, the renewal and extension of these licenses is reasonably certain at minimal cost. Accordingly, we have concluded that FCC licenses are indefinite-lived intangible assets. Our Sprint and Boost Mobile trademarks have also been identified as indefinite-lived intangible assets. Goodwill represents the excess of consideration paid over the estimated fair value of net tangible and identifiable intangible assets acquired in business combinations.

The following provides the activity of indefinite-lived intangible assets within the consolidated balance sheets:

| March 31, |

| Net Additions (Reductions) |

| September 30, | ||||||

| (in millions) | ||||||||||

FCC licenses | $ | 36,550 | |

| $ | 487 | | (1) | $ | 37,037 | |

Trademarks | 4,035 | |

| - | |

| 4,035 | | |||

Goodwill | 6,579 | |

| (1 | ) |

| 6,578 | | |||

| $ | 47,164 | |

| $ | 486 | |

| $ | 47,650 | |

_________________

(1) | Net additions within FCC licenses include a $479 million increase from spectrum license exchanges described below during the six-month period ended September 30, 2017 . |

11

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Spectrum License Exchanges

In the first quarter of fiscal year 2017, we exchanged certain spectrum licenses with other carriers in non-cash transactions. As a result, we recorded a non-cash gain of $479 million , which represented the difference between the fair value and the net book value of the spectrum transferred to the other carriers. The gain was recorded in "Other, net" within Operating income in the consolidated statements of comprehensive (loss) income for the six-month period ended September 30, 2017 .

Assessment of Impairment

Our annual impairment testing date for goodwill and indefinite-lived intangible assets is January 1 of each year; however, we test for impairment between our annual tests if an event occurs or circumstances change that indicate that the asset may be impaired, or in the case of goodwill, that the fair value of the reporting unit is below its carrying amount.

The determination of fair value requires considerable judgment and is highly sensitive to changes in underlying assumptions. Consequently, there can be no assurance that the estimates and assumptions made for the purposes of the goodwill, spectrum licenses, and Sprint and Boost Mobile trade names impairment tests will prove to be an accurate prediction of the future. Sustained declines in the Company's operating results, number of wireless subscribers, future forecasted cash flows, growth rates and other assumptions, as well as significant, sustained declines in the Company's stock price and related market capitalization could impact the underlying key assumptions and our estimated fair values, potentially leading to a future material impairment of goodwill or other indefinite-lived intangible assets.

Intangible Assets Subject to Amortization

Customer relationships are amortized using the sum-of-the-months' digits method, while all other definite-lived intangible assets are amortized using the straight-line method over the estimated useful lives of the respective assets. We reduce the gross carrying value and associated accumulated amortization when specified intangible assets become fully amortized. Amortization expense related to favorable spectrum and tower leases is recognized in "Cost of services" in our consolidated statements of comprehensive (loss) income.

|

|

| September 30, 2017 |

| March 31, 2017 | ||||||||||||||||||||

| Useful Lives |

| Gross |

| Accumulated |

| Net |

| Gross |

| Accumulated |

| Net | ||||||||||||

|

|

| (in millions) | ||||||||||||||||||||||

Customer relationships | 8 years |

| $ | 6,561 | |

| $ | (5,103 | ) |

| $ | 1,458 | |

| $ | 6,923 | |

| $ | (5,053 | ) |

| $ | 1,870 | |

Other intangible assets: |

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Favorable spectrum leases | 23 years |

| 861 | |

| (154 | ) |

| 707 | |

| 869 | |

| (138 | ) |

| 731 | | ||||||

Favorable tower leases | 7 years |

| 589 | |

| (414 | ) |

| 175 | |

| 589 | |

| (386 | ) |

| 203 | | ||||||

Trademarks | 34 years |

| 520 | |

| (66 | ) |

| 454 | |

| 520 | |

| (58 | ) |

| 462 | | ||||||

Other | 10 years |

| 96 | |

| (42 | ) |

| 54 | |

| 91 | |

| (37 | ) |

| 54 | | ||||||

Total other intangible assets |

| 2,066 | | | (676 | ) | | 1,390 | | | 2,069 | | | (619 | ) | | 1,450 | | |||||||

Total definite-lived intangible assets |

| $ | 8,627 | | | $ | (5,779 | ) | | $ | 2,848 | | | $ | 8,992 | | | $ | (5,672 | ) | | $ | 3,320 | | |

Note 7. | Accounts Payable |

Accounts payable at September 30, 2017 and March 31, 2017 include liabilities in the amounts of $69 million for both periods for payments issued in excess of associated bank balances but not yet presented for collection.

12

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

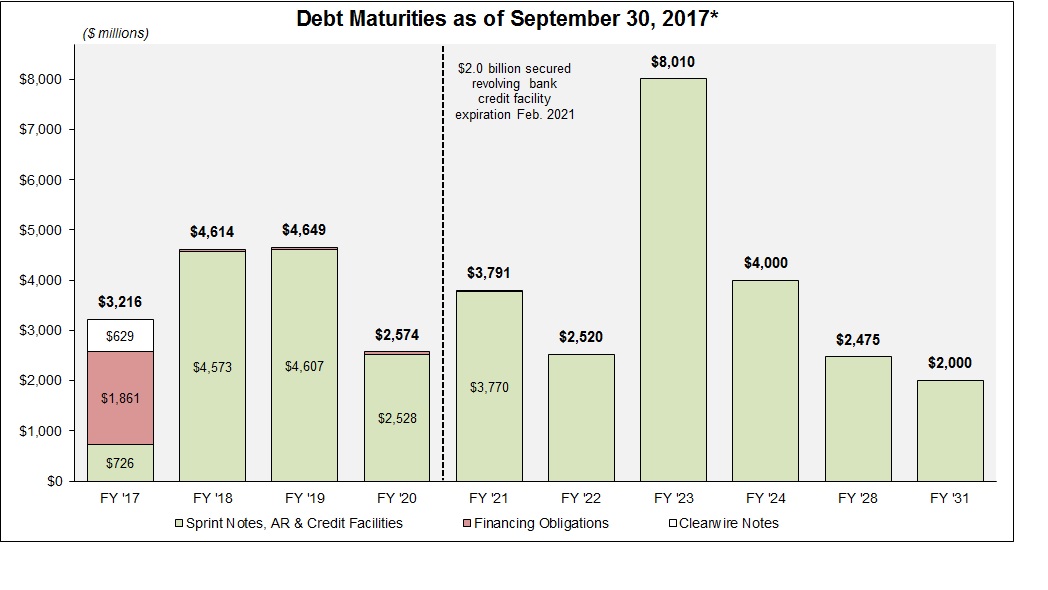

Note 8. | Long-Term Debt, Financing and Capital Lease Obligations |

| Interest Rates |

| Maturities |

| September 30, |

| March 31, | ||||||||

|

|

|

|

|

|

|

|

| (in millions) | ||||||

Notes |

|

|

|

|

|

|

|

|

|

|

| ||||

Senior notes |

|

|

|

|

|

|

|

|

|

|

| ||||

Sprint Corporation | 7.13 | - | 7.88% |

| 2021 | - | 2025 |

| $ | 10,500 | |

| $ | 10,500 | |

Sprint Communications, Inc. | 6.00 | - | 11.50% |

| 2020 | - | 2022 |

| 4,780 | |

| 6,080 | | ||

Sprint Capital Corporation | 6.88 | - | 8.75% |

| 2019 | - | 2032 |

| 6,204 | |

| 6,204 | | ||

Senior secured notes |

|

|

|

|

|

|

|

|

|

|

| ||||

Sprint Spectrum Co LLC, Sprint Spectrum Co II LLC, Sprint Spectrum Co III LLC | 3.36% |

| 2021 |

| 3,500 | |

| 3,500 | | ||||||

Sprint Communications, Inc. | 9.25% |

| 2022 |

| 200 | |

| 200 | | ||||||

Guaranteed notes |

|

|

|

|

|

|

|

|

|

|

| ||||

Sprint Communications, Inc. | 7.00 | - | 9.00% |

| 2018 | - | 2020 |

| 2,800 | |

| 4,000 | | ||

Exchangeable notes |

|

|

|

|

|

|

|

|

|

|

| ||||

Clearwire Communications LLC (1) | 8.25% |

| 2017 |

| 629 | |

| 629 | | ||||||

Credit facilities |

|

|

|

|

|

|

|

|

|

|

| ||||

Secured revolving bank credit facility | 3.75% |

| 2021 |

| - | |

| - | | ||||||

Secured term loan | 3.75% |

| 2024 |

| 3,980 | |

| 4,000 | | ||||||

Export Development Canada (EDC) | 3.74% |

| 2019 |

| 300 | |

| 300 | | ||||||

Secured equipment credit facilities | 2.58 | - | 3.38% |

| 2020 | - | 2021 |

| 552 | |

| 431 | | ||

Accounts receivable facility | 2.25 | - | 2.50% |

| 2018 |

| 2,393 | |

| 1,964 | | ||||

Financing obligations, capital lease and other obligations | 2.35 | - | 10.51% |

| 2017 | - | 2024 |

| 2,544 | |

| 3,016 | | ||

Net premiums and debt financing costs |

|

|

|

|

|

|

|

| (4 | ) |

| 90 | | ||

|

|

|

|

|

|

|

|

| 38,378 | |

| 40,914 | | ||

Less current portion |

|

|

|

|

|

|

|

| (4,142 | ) |

| (5,036 | ) | ||

Long-term debt, financing and capital lease obligations |

|

|

|

|

|

|

|

| $ | 34,236 | |

| $ | 35,878 | |

_________________

(1) | The exchangeable notes of Clearwire Communications LLC are guaranteed by certain Clearwire subsidiaries. Pursuant to notice given to holders during October 2017, and in accordance with the issuer's right of redemption, all of the exchangeable notes outstanding will, on December 1, 2017, be redeemed for 100% of their par value plus accrued interest. |

As of September 30, 2017 , Sprint Corporation, the parent corporation, had $10.5 billion in aggregate principal amount of senior notes outstanding. In addition, as of September 30, 2017 , the outstanding principal amount of the senior notes issued by Sprint Communications and Sprint Capital Corporation, the senior secured notes issued by Sprint Communications, the guaranteed notes issued by Sprint Communications, the exchangeable notes issued by Clearwire Communications LLC, Sprint Communications' secured term loan and secured revolving bank credit facility, the EDC agreement, the secured equipment credit facilities, the Receivables Facility, the Handset Sale-Leaseback Tranche 2 (subject to a cap of 20% of the aggregate cash purchase price), and certain other obligations collectively totaled $22.1 billion in principal amount of our long-term debt. Sprint Corporation fully and unconditionally guaranteed such indebtedness, which was issued by 100% owned subsidiaries. Although certain financing agreements restrict the ability of Sprint Communications and its subsidiaries to distribute cash to Sprint Corporation, the ability of the subsidiaries to distribute cash to their respective parents, including to Sprint Communications, is generally not restricted.

Cash interest payments, net of amounts capitalized of $28 million and $20 million during the six-month periods ended September 30, 2017 and 2016 , respectively, totaled $1.3 billion during each of the six-month periods ended September 30, 2017 and 2016 .

13

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Notes

As of September 30, 2017 , our outstanding notes consisted of senior notes, guaranteed notes, and exchangeable notes, all of which are unsecured, as well as senior secured notes associated with our spectrum financing transaction and senior secured notes issued by Sprint Communications. Cash interest on all of the notes is generally payable semi-annually in arrears with the exception of the spectrum financing senior secured notes, which is payable quarterly. As of September 30, 2017 , $27.8 billion aggregate principal amount of the notes was redeemable at the Company's discretion at the then-applicable redemption prices plus accrued interest.

As of September 30, 2017 , $21.6 billion aggregate principal amount of our senior notes, senior secured notes, and guaranteed notes provided holders with the right to require us to repurchase the notes if a change of control triggering event (as defined in the applicable indentures and supplemental indentures) occurs.

In October 2017, holders of the Clearwire Communications LLC exchangeable notes were notified that the issuer will redeem all of the outstanding exchangeable notes on December 1, 2017 pursuant to the terms of the exchangeable notes indenture, which provides that the notes can be tendered at the holder's option or called at our option on or after that date, in each case for 100% of the par value plus accrued interest. As a result, the entire balance of notes outstanding under this indenture has been classified as a current debt obligation.

During the three-month period ended June 30, 2017, pursuant to a cash tender offer, Sprint Communications retired $388 million principal amount of its outstanding 8.375% Notes due 2017 and $1.2 billion principal amount of its outstanding 9.000% Guaranteed Notes due 2018. We incurred costs of $129 million , which consisted of call redemption premiums and tender expenses, and removed unamortized premiums of $64 million associated with these retirements resulting in a loss on early extinguishment of debt of $65 million , which is included in "Other income (expense), net" in our consolidated statements of comprehensive (loss) income. In addition, during the three-month period ended September 30, 2017 , Sprint Communications retired the remaining $912 million principal amount of its outstanding 8.375% Notes due August 2017.

Spectrum Financing

In October 2016, Sprint transferred certain directly held and third-party leased spectrum licenses (collectively, Spectrum Portfolio) to wholly-owned bankruptcy-remote special purpose entities (collectively, Spectrum Financing SPEs). The Spectrum Portfolio, which represented approximately 14% of Sprint's total spectrum holdings on a MHz-pops basis, was used as collateral to raise an initial $3.5 billion in senior secured notes bearing interest at 3.36% per annum under a $7.0 billion program that permits Sprint to raise up to an additional $3.5 billion in senior secured notes, subject to certain conditions. The senior secured notes are repayable over a five -year term, with interest-only payments over the first four quarters and amortizing quarterly principal payments thereafter commencing December 2017 through September 2021. As of September 30, 2017 , approximately $875 million of the total principal outstanding was classified as "Current portion of long-term debt, financing and capital lease obligations" in the consolidated balance sheets.

Sprint Communications simultaneously entered into a long-term lease with the Spectrum Financing SPEs for the ongoing use of the Spectrum Portfolio. Sprint Communications is required to make monthly lease payments to the Spectrum Financing SPEs at a market rate. The lease payments, which are guaranteed by certain subsidiaries of Sprint Communications, are sufficient to service the senior secured notes and the lease also constitutes collateral for the senior secured notes. As the Spectrum Financing SPEs are wholly-owned Sprint subsidiaries, these entities are consolidated and all intercompany activity has been eliminated.

Each Spectrum Financing SPE is a separate legal entity with its own separate creditors who will be entitled, prior to and upon the liquidation of the Spectrum Financing SPE, to be satisfied out of the Spectrum Financing SPE's assets prior to any assets of the Spectrum Financing SPE becoming available to Sprint. Accordingly, the assets of the Spectrum Financing SPE are not available to satisfy the debts and other obligations owed to other creditors of Sprint until the obligations of the Spectrum Financing SPEs under the spectrum-backed senior secured notes are paid in full.

14

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Credit Facilities

Unsecured Credit Facility Commitment

During the three-month period ended September 30, 2017, Sprint Communications entered into a commitment letter with a group of banks to provide an unsecured credit facility in an aggregate principal amount up to $3.2 billion . Draws on the unsecured credit facility would bear interest at a rate equal to either the London Interbank Offered Rate (LIBOR) plus a percentage that varies depending on the days elapsed since the effective date of the facility ( 1.25% to 4.25% per annum), or base rate, as defined in the commitment letter, plus a percentage that varies depending on the days elapsed since the effective date of the facility ( 0.25% to 3.25% per annum). Commitments will be reduced by an amount equal to the proceeds from the sales of certain assets and will terminate upon certain debt issuances or sales of equity securities. Amounts borrowed and repaid cannot be redrawn and the unsecured credit facility, if executed, will terminate in March 2019. As of September 30, 2017 , the unsecured credit facility had not been executed and thus no amounts have been drawn.

Secured Term Loan and Revolving Bank Credit Facility

On February 3, 2017, we entered into a credit agreement for $6.0 billion , consisting of a $4.0 billion , seven -year secured term loan that matures in February 2024 and a $2.0 billion secured revolving bank credit facility that expires in February 2021. As of September 30, 2017 , approximately $178 million in letters of credit were outstanding under the secured revolving bank credit facility, including the letter of credit required by the Report and Order (see Note 11. Commitments and Contingencies) . As a result of the outstanding letters of credit, which directly reduce the availability of borrowings, the Company had approximately $1.8 billion of borrowing capacity available under the secured revolving bank credit facility as of September 30, 2017 . The bank credit facility requires a ratio (Leverage Ratio) of total indebtedness to trailing four quarters earnings before interest, taxes, depreciation and amortization and other non-recurring items, as defined by the bank credit facility (adjusted EBITDA), not to exceed 6.0 to 1.0 through the quarter ending December 31, 2017. After December 31, 2017, the Leverage Ratio declines on a scheduled basis until the ratio becomes fixed at 3.5 to 1.0 for the fiscal quarter ended March 31, 2020 and each fiscal quarter ending thereafter through expiration of the facility. The term loan has an interest rate equal to LIBOR plus 250 basis points and the secured revolving bank credit facility has an interest rate equal to LIBOR plus a spread that varies depending on the Leverage Ratio.

In consideration of the seven -year secured term loan, we entered into a five -year fixed-for-floating interest rate swap on a $2.0 billion notional amount that has been designated as a cash flow hedge. The effective portion of changes in fair value are recorded in "Other comprehensive (loss) income" in the consolidated statements of comprehensive (loss) income and the ineffective portion, if any, is recorded in current period earnings in the consolidated statements of comprehensive (loss) income as interest expense. The fair value of the interest rate swap was approximately $9 million as of September 30, 2017 , which was recorded as a liability in the consolidated balance sheets.

EDC Agreement

As of September 30, 2017 , the EDC agreement provided for security and covenant terms similar to our secured term loan and revolving bank credit facility. However, under the terms of the EDC agreement, repayments of outstanding amounts cannot be redrawn. As of September 30, 2017 , the total principal amount of our borrowings under the EDC facility was $300 million .

Secured Equipment Credit Facilities

Finnvera plc (Finnvera)

The Finnvera secured equipment credit facility provides for the ability to borrow up to $800 million to finance network equipment-related purchases from Nokia Solutions and Networks US LLC, USA. The facility has one tranche remaining and available for borrowing through October 2017. Such borrowings are contingent upon the amount and timing of network-related purchases made by Sprint. During the six-month period ended September 30, 2017 , we drew $92 million and made principal repayments totaling $85 million on the facility, resulting in a total principal amount of $147 million outstanding as of September 30, 2017 .

15

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

K-sure

The K-sure secured equipment credit facility provides for the ability to borrow up to $750 million to finance network equipment-related purchases from Samsung Telecommunications America, LLC. The facility can be divided in up to three consecutive tranches of varying size. In September 2017, we amended the secured equipment credit facility to extend the borrowing availability through December 2018. Such borrowings are contingent upon the amount and timing of network-related purchases made by Sprint. During the six-month period ended September 30, 2017 , we made principal repayments totaling $33 million on the facility, resulting in a total principal amount of $226 million outstanding as of September 30, 2017 .

Delcredere | Ducroire (D/D)

The D/D secured equipment credit facility provided for the ability to borrow up to $250 million to finance network equipment-related purchases from Alcatel-Lucent USA Inc. In September 2017, we amended the secured equipment credit facility to restore previously expired commitments of $150 million . During the six-month period ended September 30, 2017 , we drew $150 million and made principal repayments totaling $3 million on the facility, resulting in a total principal amount of $179 million outstanding as of September 30, 2017 .

Borrowings under the Finnvera, K-sure and D/D secured equipment credit facilities are each secured by liens on the respective network equipment purchased pursuant to each facility's credit agreement. In addition, repayments of outstanding amounts borrowed under the secured equipment credit facilities cannot be redrawn. Each of these facilities is fully and unconditionally guaranteed by both Sprint Communications and Sprint Corporation. The secured equipment credit facilities have certain key covenants similar to those in our secured term loan and revolving bank credit facility.

Accounts Receivable Facility

Transaction Overview

Our Receivables Facility provides us the opportunity to sell certain wireless service receivables, installment receivables, and future amounts due from customers who lease certain devices from us to the Purchasers. The maximum funding limit under the Receivables Facility is $4.3 billion . While we have the right to decide how much cash to receive from each sale, the maximum amount of cash available to us varies based on a number of factors and, as of September 30, 2017 , represents approximately 50% of the total amount of the eligible receivables sold to the Purchasers. As of September 30, 2017 , the total amount of borrowings under our Receivables Facility was $2.4 billion and the total amount available to be drawn was $3 million . In February 2017, the Receivables Facility was amended to extend the maturity date to November 2018. Additionally, Sprint gained effective control over the receivables transferred to the Purchasers by obtaining the right, under certain circumstances, to repurchase them. Subsequent to the February 2017 amendment, all proceeds received from the Purchasers in exchange for the transfer of our wireless service and installment receivables are recorded as borrowings and all cash inflows and outflows under the Receivables Facility are reported as financing activities in the consolidated statements of cash flows. In October 2017, the Receivables Facility was amended to, among other things, extend the maturity date to November 2019 and to reallocate the Purchasers' commitments between wireless service, installment and future lease receivables through May 2018 to 26% , 28% and 46% , respectively. After May 2018, the allocation of the Purchasers' commitments between wireless service, installment and future lease receivables will be 26% , 18% and 56% , respectively. During the six-month period ended September 30, 2017 , we drew $1.6 billion and repaid $1.1 billion to the Purchasers.

Prior to the February 2017 amendment, wireless service and installment receivables sold to the Purchasers were treated as a sale of financial assets and we derecognized these receivables, as well as the related allowances, and recognized the net proceeds received in cash provided by operating activities in the consolidated statements of cash flows. The total proceeds from the sale of these receivables were comprised of a combination of cash and a deferred purchase price (DPP). The DPP was realized by us upon either the ultimate collection of the underlying receivables sold to the Purchasers or upon Sprint's election to receive additional advances in cash from the Purchasers subject to the total availability under the Receivables Facility. The fees associated with these sales were recognized in "Selling, general and administrative" in the consolidated statements of comprehensive (loss) income through the date of the February 2017 amendment. Subsequent to the February 2017 amendment, the sale of wireless service and installment receivables are reported as financings, which is consistent with our historical treatment for the sale of future lease receivables, and the associated fees are recognized as "Interest expense" in the consolidated statements of comprehensive (loss) income.

16

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

During the six-month period ended September 30, 2016 , we remitted $185 million of funds to the Purchasers because the amount of cash proceeds received by us under the facility exceeded the maximum funding limit, which increased the total amount of the DPP due to Sprint. We also elected to receive $40 million of cash, which decreased the total amount of the DPP due to Sprint. In addition, during the six-month period ended September 30, 2016 , sales of new receivables exceeded cash collections on previously sold receivables such that the DPP increased by $255 million .

Transaction Structure

Sprint contributes certain wireless service, installment and future lease receivables, as well as the associated leased devices, to Sprint's wholly-owned consolidated bankruptcy-remote special purpose entities (SPEs). At Sprint's direction, the SPEs have sold, and will continue to sell, wireless service, installment and future lease receivables to Purchasers or to a bank agent on behalf of the Purchasers. Leased devices will remain with the SPEs, once sales are initiated, and continue to be depreciated over their estimated useful life. As of September 30, 2017 , wireless service and installment receivables contributed to the SPEs and included in "Accounts and notes receivable, net" in the consolidated balance sheets were $3.0 billion and the long-term portion of installment receivables included in "Other assets" in the consolidated balance sheets was $314 million . As of September 30, 2017 , the net book value of devices contributed to the SPEs was approximately $3.5 billion .

Each SPE is a separate legal entity with its own separate creditors who will be entitled, prior to and upon the liquidation of the SPE, to be satisfied out of the SPE's assets prior to any assets in the SPE becoming available to Sprint. Accordingly, the assets of the SPE are not available to pay creditors of Sprint or any of its affiliates (other than any other SPE), although collections from these receivables in excess of amounts required to repay the advances, yield and fees of the Purchasers and other creditors of the SPEs may be remitted to Sprint during and after the term of the Receivables Facility.

Sales of eligible receivables by the SPEs generally occur daily and are settled on a monthly basis. Sprint pays a fee for the drawn and undrawn portions of the Receivables Facility. A subsidiary of Sprint services the receivables in exchange for a monthly servicing fee, and Sprint guarantees the performance of the servicing obligations under the Receivables Facility.

Variable Interest Entity

Sprint determined that certain of the Purchasers, which are multi-seller asset-backed commercial paper conduits (Conduits) are considered variable interest entities because they lack sufficient equity to finance their activities. Sprint's interest in the receivables purchased by the Conduits is not considered a variable interest because Sprint's interest is in assets that represent less than 50% of the total activity of the Conduits.

Financing Obligations

Network Equipment Sale-Leaseback

In April 2016, Sprint sold and leased back certain network equipment to unrelated bankruptcy-remote special purpose entities (collectively, Network LeaseCo). The network equipment acquired by Network LeaseCo, which we consolidate, was used as collateral to raise approximately $2.2 billion in borrowings from external investors, including SoftBank Group Corp. (SoftBank). Principal and interest payments on the borrowings from the external investors will be repaid in staggered, unequal payments through January 2018. During the six-month period ended September 30, 2017 , we made principal repayments totaling $117 million , resulting in a total principal amount of $1.8 billion outstanding as of September 30, 2017 .

Network LeaseCo is a variable interest entity for which Sprint is the primary beneficiary. As a result, Sprint is required to consolidate Network LeaseCo and our consolidated financial statements include Network LeaseCo's debt and the related financing cash inflows. The network assets included in the transaction, which had a net book value of approximately $3.0 billion and consisted primarily of equipment located at cell towers, remain on Sprint's consolidated financial statements and continue to be depreciated over their respective estimated useful lives. As of September 30, 2017 , these network assets had a net book value of approximately $2.0 billion .

The proceeds received were reflected as cash provided by financing activities in the consolidated statements of cash flows and payments made to Network LeaseCo are reflected as principal repayments and interest expense over the

17

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

respective terms. Sprint has the option to purchase the equipment at the end of the leaseback term for a nominal amount. All intercompany transactions between Network LeaseCo and Sprint are eliminated in our consolidated financial statements.

Handset Sale-Leasebacks

Transaction Structure

Sprint sold certain iPhone ® devices being leased by our customers to MLS, a company formed by a group of equity investors, including SoftBank, and then subsequently leased the devices back. Under the agreements, Sprint generally maintains the customer leases, continues to collect and record lease revenue from the customer and remits monthly rental payments to MLS during the leaseback periods.

Under the agreements, Sprint contributed the devices and the associated customer leases to wholly-owned consolidated bankruptcy-remote special purpose entities of Sprint (SPE Lessees). The SPE Lessees then sold the devices and transferred certain specified customer lease-end rights and obligations, such as the right to receive the proceeds from customers who elect to purchase the device at the end of the customer lease term, to MLS in exchange for a combination of cash and DPP. Settlement for the DPP occurs after repayment of MLS's senior loan obligations, senior subordinated loan obligations, and a return to MLS's equity holders and can be reduced to the extent that MLS experiences a loss on the device (either not returned or sold at an amount less than the expected residual value of the device), but only to the extent of the device's DPP balance. In the event that MLS sells the devices returned from our customers at a price greater than the expected device residual value, Sprint has the potential to share some of the excess proceeds.

The SPE Lessees retain all rights to the underlying customer leases, such as the right to receive the rental payments during the device leaseback period, other than the aforementioned certain specified customer lease-end rights. Each SPE Lessee is a separate legal entity with its own separate creditors who will be entitled, prior to and upon the liquidation of the SPE Lessee, to be satisfied out of the SPE Lessee's assets prior to any assets in the SPE Lessee becoming available to Sprint. Accordingly, the assets of the SPE Lessee are not available to pay creditors of Sprint or any of its affiliates. The SPE Lessees are obligated to pay the full monthly rental payments under each device lease to MLS regardless of whether our customers make lease payments on the devices leased to them or whether the customer lease is canceled. Sprint has guaranteed to MLS (subject to a cap of 20% of the aggregate cash purchase price) the performance of the agreements and undertakings of the SPE Lessees under the transaction documents.

Handset Sale-Leasebacks Tranche 2 (Tranche 2)

In May 2016, Sprint entered into Tranche 2. We transferred devices with a net book value of approximately $1.3 billion to MLS in exchange for cash proceeds totaling $1.1 billion and a DPP of $186 million . The proceeds were accounted for as a financing. Accordingly, the devices remain in "Property, plant and equipment, net" in the consolidated balance sheets and we continue to depreciate the assets to their estimated residual values over the respective customer lease terms. At September 30, 2017 , the net book value of devices transferred to MLS was approximately $358 million . During the six-month period ended September 30, 2017 , we made principal repayments and non-cash adjustments totaling $327 million to MLS, resulting in a total principal amount of $58 million outstanding as of September 30, 2017 .

The proceeds received were reflected as cash provided by financing activities in the consolidated statements of cash flows and payments made to MLS will be reflected as principal repayments and interest expense. We have elected to account for the financing obligation at fair value. Accordingly, changes in the fair value of the financing obligation are recognized in "Other income (expense), net" in the consolidated statements of comprehensive (loss) income over the course of the arrangement.

Tranche 2 primarily includes devices from our iPhone Forever Program. The iPhone Forever Program provides our leasing customers the ability to upgrade their devices and to enter into a new lease agreement, subject to certain conditions, upon Apple's release of a next generation device. Upon a customer exercising their iPhone Forever upgrade right, Sprint has the option to terminate the existing leaseback by immediately remitting all unpaid device leaseback payments and returning the device to MLS. Alternatively, Sprint has the option to transfer the title in the new device to MLS in exchange for the title in the original device (Exchange Option). If Sprint elects the Exchange Option, we are required to continue to pay existing device leaseback rental payments related to the original device, among other requirements.

In October 2017, Sprint terminated Tranche 2 and repaid all amounts outstanding.

18

Table of Contents

Index for Notes to the Consolidated Financial Statements

SPRINT CORPORATION

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Handset Sale-Leasebacks Tranche 1 (Tranche 1)