UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

| FOR THE FISCAL YEAR ENDED JANUARY 31, 2016 | COMMISSION FILE NO. 001-09097 |

REX AMERICAN RESOURCES CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 31-1095548 (I.R.S. Employer Identification No.) | |

| 7720 Paragon Road, Dayton, Ohio (Address of principal executive offices) | 45459 (Zip Code) |

Registrant's telephone number, including area code (937) 276-3931

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

| Common Stock, $.01 par value | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act . Yes o No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (check one):

| Large accelerated filer o | Accelerated filer ☑ | Non-accelerated filer o | Smaller reporting company o |

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes o No ☑

At the close of business on July 31, 2015 the aggregate market value of the registrant's outstanding Common Stock held by non-affiliates of the registrant (for purposes of this calculation, 963,902 shares beneficially owned by directors and executive officers of the registrant were treated as being held by affiliates of the registrant), was $318,852,936.

There were 6,560,527 shares of the registrant's Common Stock outstanding as of March 24, 2016.

Documents Incorporated by Reference

Portions of REX American Resources Corporation's definitive Proxy Statement for its Annual Meeting of Shareholders on June 7, 2016 are incorporated by reference into Part III of this Form 10-K.

Forward-Looking Statements

This Form 10-K contains or may contain forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. Such statements can be identified by use of forward-looking terminology such as "may," "expect," "believe," "estimate," "anticipate" or "continue" or the negative thereof or other variations thereon or comparable terminology. Readers are cautioned that there are risks and uncertainties that could cause actual events or results to differ materially from those referred to in such forward-looking statements. These risks and uncertainties include the risk factors set forth from time to time in the Company's filings with the Securities and Exchange Commission and include among other things: the impact of legislative changes, the price volatility and availability of corn, distillers grains, ethanol, non-food grade corn oil, gasoline, natural gas, ethanol plants operating efficiently and according to forecasts and projections, changes in the international, national or regional economies, weather and the effects of terrorism or acts of war. The Company does not intend to update publicly any forward-looking statements except as required by law. Other factors that could cause actual results to differ materially from those in the forward-looking statements are set forth in Item 1A.

Available Information

REX makes available free of charge on its Internet website its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. REX's Internet website address is www.rexamerican.com. The contents of the Company's website are not a part of this report.

PART I

| Item 1. | Business |

References to "we", "us", "our", "REX" or "the Company" refer to REX American Resources Corporation and its majority owned subsidiaries.

Overview

REX was incorporated in Delaware in 1984 as a holding company. Our principal offices are located at 7720 Paragon Road, Dayton, Ohio 45459. Our telephone number is (937) 276-3931. We have been an investor in various alternative energy entities beginning with synthetic fuel partnerships in 1998 and later ethanol production facilities beginning in 2006. Historically, we were a specialty retailer in the consumer electronics and appliance industry serving small to medium-sized towns and communities. Recognizing the change in our business, we changed our corporate name from REX Stores Corporation to REX American Resources Corporation in 2010 as we completed the transition out of the retail business into the ethanol business.

We are currently invested in three ethanol production entities, two of which we have a majority ownership interest in. We may make additional investments in the energy industry in the future.

Our ethanol operations are highly dependent on commodity prices, especially prices for corn, ethanol, distillers grains, non-food grade corn oil and natural gas. As a result of price volatility for these commodities, our operating results can fluctuate substantially. The price and availability of corn is subject to significant fluctuations depending upon a number of factors that affect commodity prices in general, including crop conditions, weather, federal policy and foreign trade. Because the market price of ethanol is not always directly related to corn prices (for example, crude and other energy prices can impact ethanol prices), at times ethanol prices may lag movements in corn prices and, in an environment of higher corn

| 2 |

prices or lower ethanol prices, reduce the overall margin structure at the plants. As a result, at times, we may operate our plants at negative or marginally positive operating margins.

We expect our ethanol plants to produce approximately 2.8 gallons of denatured ethanol for each bushel of grain processed in the production cycle. We refer to the difference between the price per gallon of ethanol and the price per bushel of grain (divided by 2.8) as the "crush spread." Should the crush spread decline, it is possible that our ethanol plants will generate operating results that do not provide adequate cash flows for sustained periods of time. In such cases, production at the ethanol plants may be reduced or stopped altogether in order to minimize variable costs at individual plants.

We attempt to manage the risk related to the volatility of grain and ethanol prices by utilizing forward grain purchase and forward ethanol, distillers grains and non-food grade corn oil sale contracts. We attempt to match quantities of these sales contracts with an appropriate quantity of grain purchase contracts over a given period of time when we can obtain an adequate gross margin resulting from the crush spread inherent in the contracts we have executed. However, the market for future ethanol sales contracts is not a mature market. Consequently, we generally execute fixed price contracts for no more than two months into the future at any given time and we may lock in our corn or ethanol price without having a corresponding locked in ethanol or corn price for short durations of time. As a result of the relatively short period of time our fixed price contracts cover, we generally cannot predict the future movements in the crush spread for more than two months; thus, we are unable to predict the likelihood or amounts of future income or loss from the operations of our ethanol facilities. We utilize derivative financial instruments, primarily exchange traded commodity future contracts, in conjunction with certain of our grain procurement activities.

The crush spread realized in fiscal year 2015 was subject to significant volatility. For fiscal year 2015, the average Chicago Board of Trade ("CBOT") near-month corn price ranged from a low of approximately $3.48 per bushel in June 2015 to a high of approximately $4.41 per bushel in July 2015. Corn prices benefitted throughout the year from the three strongest corn harvests in U. S. history in 2013, 2014 and 2015 (in order of strength of harvest production). Ethanol prices had significant fluctuations ranging from approximately $1.31 per gallon in January 2016 to a high of approximately $1.69 per gallon in May 2015. Ethanol prices were influenced by many factors throughout the year including low energy prices, particularly late in fiscal year 2015 and over-production of ethanol. The CBOT crush spread during fiscal year 2015 ranged from approximately $0.02 in February 2015 to approximately $0.37 in May 2015.

Income from continuing operations, net of tax was approximately $31.4 million in fiscal year 2015 compared to approximately $86.8 million in fiscal year 2014. The decrease in profitability primarily resulted from lower crush spreads (compared to the prior year) experienced in the ethanol industry for a majority of fiscal year 2015 as lower energy prices and over supply of ethanol reduced ethanol pricing during fiscal year 2015. We expect that future operating results, from our consolidated plants, will be based upon combined annual production of between 215 and 240 million gallons of ethanol, which assumes that our consolidated ethanol plants will operate at or above nameplate capacity. However, due to the inherent volatility of the crush spread, we cannot predict the likelihood of future operating results being similar to the fiscal year 2015 results.

We plan to seek and evaluate various investment opportunities including energy related, agricultural or other ventures we believe fit our investment criteria. We can make no assurances that we will be successful in our efforts to find such opportunities.

Through a wholly owned subsidiary REX I.P., LLC, we have entered into a joint venture with Hytken HPGP LLC ("Hytken") to file and defend patents for eSteam technology relating to heavy oil and oil sands production methods, and to attempt to commercially exploit the technology to generate license fees, royalty income and development opportunities. The patented technology is an enhanced method of heavy oil

| 3 |

recovery involving zero emissions downhole steam generation. To date, we have paid approximately $1.6 million for our ownership interest, patent and other expenses, but have not successfully demonstrated that the technology is commercially feasible. We own 60% and Hytken owns 40% of the entity named Future Energy, LLC ("Future Energy"), an Ohio limited liability company. Future Energy is managed by a board of three managers, two appointed by us and one by Hytken.

Fiscal Year

All references in this report to a particular fiscal year are to REX's fiscal year ended January 31. For example, "fiscal year 2015" means the period February 1, 2015 to January 31, 2016. We refer to our fiscal year by reference to the year immediately preceding the January 31 fiscal year end date.

Alternative Energy Overview

We began investing in the ethanol industry during fiscal year 2006. We seek to identify quality ethanol plant opportunities located near adequate feedstock supply with good transportation capabilities or other economically beneficial attributes, and that utilize leading ethanol production technology.

The form and structure of our investments is tailored to the specific needs and goals of each project and the local farmer group or investor with whom we are partnering. We generally participate in the management of our projects through our membership on the board of managers of the limited liability companies that own the plants.

Ethanol Investments

We have equity investments in three entities as of January 31, 2016. The following table is a summary of our ethanol investments at January 31, 2016 (gallons in millions):

| Entity | Trailing 12 Months Ethanol Gallons Shipped | REX's Current Ownership Interest | Current Effective Ownership of Trailing 12 Months Ethanol Gallons Shipped | |||||||||

| One Earth Energy, LLC | 113.5 | 74.7 | % | 84.8 | ||||||||

| NuGen Energy, LLC | 118.5 | 99.5 | % | 117.9 | ||||||||

| Big River Resources W Burlington, LLC | 106.2 | 9.7 | % | 10.3 | ||||||||

| Big River Resources Galva, LLC | 118.1 | 9.7 | % | 11.5 | ||||||||

| Big River United Energy, LLC | 123.5 | 5.4 | % | 6.7 | ||||||||

| Big River Resources Boyceville, LLC | 57.7 | 9.7 | % | 5.6 | ||||||||

| Total | 637.5 | 236.8 | ||||||||||

One Earth Energy, LLC

We own 74.7% of the outstanding membership units of One Earth Energy, LLC, or One Earth. We consolidate One Earth with our financial results. One Earth commenced operations in the second quarter of fiscal year 2009 of its ethanol production facility in Gibson City, Illinois.

| 4 |

NuGen Energy, LLC

We own 99.5% of the outstanding membership units of NuGen Energy, LLC, or NuGen. We consolidate NuGen, which operates an ethanol producing facility in Marion, South Dakota, with our financial results.

Big River Resources, LLC

We own 9.7% of the outstanding membership units of Big River Resources, LLC, or Big River. Big River is a holding company for several entities including Big River Resources West Burlington, LLC which operates an ethanol plant in West Burlington, Iowa. Big River completed construction in the second quarter of fiscal year 2009 of its second plant which is located in Galva, Illinois. In August 2009, Big River acquired a 50.5% interest in Big River United Energy, LLC, which operates an ethanol production facility located in Dyersville, Iowa. Reflecting REX's 9.7% ownership interest in Big River, we have an effective 5.4% ownership interest in this entity. In December 2011, Big River acquired a 100% interest in an ethanol production facility which is located in Boyceville, Wisconsin. Big River also operates six agricultural elevators with a storage capacity of 15 million bushels. During fiscal year 2015, Big River completed construction of a zein protein plant, which is expected to begin production in the first quarter of fiscal year 2016.

Ethanol Industry

Ethanol is a renewable fuel source produced by processing corn and other biomass through a fermentation process that creates combustible alcohol that can be used as an additive or replacement to fossil fuel based gasoline. The majority of ethanol produced in the United States is made from corn because of its wide availability and ease of convertibility from large amounts of carbohydrates into glucose, the key ingredient in producing alcohol that is used in the fermentation process. Ethanol production can also use feedstocks such as grain sorghum, switchgrass, wheat, barley, potatoes and sugarcane as carbohydrate sources. Most ethanol plants have been located near large corn production areas, such as Illinois, Indiana, Iowa, Minnesota, Nebraska, Ohio and South Dakota. Railway access and interstate access are vital for ethanol facilities due to the large amount of raw materials and finished goods required to be shipped to and from the ethanol plant facilities.

According to the Renewable Fuels Association, or RFA, the United States ethanol industry produced an estimated 14.8 billion gallons of ethanol in 2015. Approximately 13.7 billion gallons were blended domestically and approximately 0.8 billion gallons were exported in 2015. According to the RFA, as of January 2016, the United States ethanol industry has grown to 214 plants (199 operating) in 29 states with an annual nameplate capacity of approximately 15.6 billion gallons (approximately 15.1 billion gallons at operating plants) of ethanol production.

On December 19, 2007, the Energy Independence and Security Act of 2007 (the "Energy Act of 2007") was enacted. The Energy Act of 2007 established new levels of renewable fuel mandates, including two different categories of renewable fuels: conventional biofuels and advanced biofuels. Corn-based ethanol is considered conventional biofuels which was subject to a renewable fuel standard ("RFS") of at least 14.4 billion gallons in 2014 and 15.0 billion gallons thereafter through 2022. The Environmental Protection Agency ("EPA") has the authority to waive the mandates in whole or in part if one of two conditions is met: 1) there is inadequate domestic renewable fuel supply, or 2) implementation of the mandate requirement severely harms the economy or environment of a state, region or the United States.

In November 2013, the EPA released its Notice of Proposed Rulemaking for the 2014 RFS, seeking comment on a range of total renewable fuel volumes and proposing a level of 15.2 billion gallons, including approximately 13.0 billion gallons of conventional corn-derived renewable fuel. The proposal included a

| 5 |

variety of approaches for setting the 2014 standard and a number of production and consumption ranges of biofuels covered by Renewable Fuel Standard II ("RFS II") to address two constraints of RFS II: (1) the volume limitations of ethanol given the practical constraints of vehicles that can use higher ethanol blends, and (2) the industry's ability to produce sufficient volumes of qualifying renewable fuel. In November 2014, the EPA rescinded its 2013 proposal. Furthermore, the EPA did not finalize the 2014 standard under the RFS program before the end of that year.

On June 10, 2015, the EPA proposed volume targets for conventional ethanol of 13.25 billion gallons, 13.40 billion gallons and 14.00 billion gallons for 2014, 2015 and 2016, respectively. On November 30, 2015, the EPA announced final volume requirements for conventional ethanol that were higher than levels proposed in June 2015 of 13.61 billion gallons, 14.05 billion gallons and 14.50 billion gallons for 2014, 2015 and 2016, respectively. The EPA has not yet announced its proposed volume requirements for subsequent years.

Ethanol Production

The plants we have invested in are designed to use the dry milling method of producing ethanol. In the dry milling process, the entire corn kernel is first ground into flour, which is referred to as "meal," and processed without separating out the various component parts of the grain. The meal is processed with enzymes, chemicals and water, and then placed in a high-temperature cooker. It is then transferred to fermenters where yeast is added and the conversion of sugar to ethanol begins. After fermentation, the resulting liquid is transferred to distillation columns where the ethanol is separated from the remaining "stillage" for fuel uses. The anhydrous ethanol is then blended with denaturant, such as natural gasoline, to render it undrinkable and thus not subject to beverage alcohol tax. With the starch elements of the corn consumed in the above described process, the principal co-product produced by the dry milling process is dry distillers grains with solubles, or DDGS. DDGS is sold as a protein used in animal feed and recovers a portion of the corn cost not absorbed in ethanol production. During fiscal year 2012, we began generating revenues from the sale of non-food grade corn oil at our One Earth and NuGen facilities. Non-food grade corn oil is sold to the animal feed market, as well as biodiesel and other chemical markets.

The Primary Uses of Ethanol

Blend component. Today, much of the ethanol blending in the U.S. is done to meet the RFS. Currently, ethanol is blended into approximately 97% of the gasoline sold in the United States, the majority as E-10 (a blend of 10% ethanol and 90% gasoline), according to the RFA. Going forward, the industry is attempting to expand the E-85 market, as well as to raise the federal cap on ethanol blend above the current 10% for most vehicles in use. The U.S. Environmental Protection Agency approved the use of 15% ethanol in gasoline for cars, SUV's and light duty trucks made in 2001 and later. Despite this, it will take time for this measure to be implemented and is still being met with great resistance.

Clean air additive. Ethanol is employed by the refining industry as a fuel oxygenate, which when blended with gasoline, allows engines to combust fuel more completely and reduce emissions from motor vehicles. Ethanol contains 35% oxygen, which results in more complete combustion of the fuel in the engine cylinder. Oxygenated gasoline is used to help meet certain federal and air emission standards.

Octane enhancer. Ethanol increases the octane rating of gasoline with which it is blended. As such, ethanol is used by gasoline suppliers as an octane enhancer both for producing regular grade gasoline from lower octane blending stocks and for upgrading regular gasoline to premium grades.

| 6 |

Legislation

The United States ethanol industry is highly dependent upon federal and state legislation. See Item 1A. Risk Factors for a discussion of legislation affecting the U.S. ethanol industry.

Facilities

At January 31, 2016, our consolidated ethanol entities own a combined 477 acres of land and two facilities that shipped a combined quantity of approximately 232 million gallons of ethanol in fiscal year 2015. In addition, we own three former retail store properties that are leased to outside, unrelated parties, and one vacant former retail store property that we are attempting to either lease or sell. We also own the office building (approximately 7,500 square feet) our corporate headquarters is located in.

Employees

At January 31, 2016, we had 116 employees at our two consolidated ethanol plants and at our corporate headquarters. None of our employees are represented by a labor union. We expect this employment level to remain relatively stable. We consider our relationship with our employees to be good.

Service Marks

We have registered the service marks "REX", and "Farmers Energy", with the United States Patent and Trademark Office. We are not aware of any adverse claims concerning our service marks.

| Item 1A. | Risk Factors |

We encourage you to carefully consider the risks described below and other information contained in this report when considering an investment decision in REX common stock. Any of the events discussed in the risk factors below may occur. If one or more of these events do occur, our results of operations, financial condition or cash flows could be materially adversely affected. In this instance, the trading price of REX stock could decline, and investors might lose all or part of their investment.

We have concentrations of cash deposits at financial institutions that exceed federal insurance limits.

We generally have cash deposits that exceed federal insurance limits. Should the financial institutions we deposit our cash at experience insolvency or other financial difficulty, our access to cash deposits could be limited. In extreme cases, we could lose our cash deposits entirely. This would negatively impact our liquidity and results of operations.

The current interest rate environment has resulted in lower yields on our excess cash.

We have experienced lower yields on our excess cash compared to historical yields. Should the present economic conditions result in a sustained period of historically low interest rates, our interest income would be negatively impacted.

Risks Related to our Alternative Energy Business

The ethanol industry is changing rapidly which could result in unexpected developments that could negatively impact our operations.

| 7 |

According to the RFA, the ethanol industry has grown from approximately 1.5 billion gallons of domestic annual ethanol production in 1999 to approximately 14.8 billion gallons in 2015. Thus, there have been significant changes in the supply and demand of ethanol over a relatively short period of time which could lead to difficulty in maintaining profitable operations at our ethanol plants.

We operate in a capital intensive industry. Limitations to external financing could adversely affect our financial performance.

We may need to incur additional financing to fund growth of our business or in times of increasing liquidity requirements (such as increases in raw material costs). Bankruptcy filings by several ethanol companies over the past several years and capital market volatility has reduced available capital for the ethanol industry. Any delays in obtaining additional financing, or our inability to do so, could have a material adverse impact on our financial results.

The financial returns on our ethanol investments are highly dependent on commodity prices, which are subject to significant volatility and uncertainty, and the availability of supplies, so our results could fluctuate substantially.

The financial returns on our ethanol investments are highly dependent on commodity prices, especially prices for corn, natural gas, ethanol, dried distillers grains, non-food grade corn oil and unleaded gasoline. As a result of the volatility of the prices for these items, the returns may fluctuate substantially and our investments could experience periods of declining prices for their products and increasing costs for their raw materials, which could result in operating losses at our ethanol plants.

Our returns on ethanol investments are highly sensitive to grain prices. Corn is the principal raw material our ethanol plants use to produce ethanol and co-products. As a result, changes in the price of corn can significantly affect our businesses. Rising corn prices result in higher costs of ethanol and co-products. Because ethanol competes with non-corn-based fuels, our ethanol plants may not be able to pass along increased grain costs to our customers. At certain levels, grain prices may make ethanol uneconomical to produce.

The price of corn is influenced by weather conditions and other factors affecting crop yields, transportation costs, farmer planting decisions, exports, the value of the U.S. dollar and general economic, market and regulatory factors. These factors include government policies and subsidies with respect to agriculture and international trade and global and local demand and supply. The significance and relative effect of these factors on the price of corn is difficult to predict. Any event that tends to negatively affect the supply of corn, such as adverse weather or crop disease, could increase corn prices and potentially harm the business of our ethanol plants. Increasing domestic ethanol capacity could boost the demand for corn and result in increased corn prices. Much of the Midwestern United States experienced drought conditions during 2012 which led to a smaller harvest of corn and increased corn prices. Our ethanol plants may also have difficulty, from time to time, in physically sourcing corn on economical terms due to supply shortages. Such a shortage could require our ethanol plants to suspend operations which would have a material adverse effect on our consolidated results of operations.

The spread between ethanol and corn prices can vary significantly. The gross margin at our ethanol plants depends principally on the spread between ethanol and corn prices. Fluctuations in the spread are likely to continue to occur. A sustained narrow or negative spread, whether as a result of sustained high or increased corn prices or sustained low or decreased ethanol prices, would adversely affect the results of operations at our ethanol plants.

| 8 |

Our risk management strategies may be ineffective and may expose us to decreased profitability and liquidity. In an attempt to partially offset the impact of volatility of commodity prices, we enter into forward contracts to sell a portion of our ethanol and distillers grains production and to purchase a portion of our corn and natural gas requirements. The financial impact of these risk management activities is dependent upon, among other items, the prices involved and our ability to receive or deliver the commodities involved. Risk management activities can result in financial loss when positions are purchased in a declining market or when positions are sold in an increasing market. In addition, we may not be able to match the appropriate quantity of corn contracts with quantities of ethanol, distillers grains and non-food grade corn oil contracts. We vary the amount of risk management techniques we utilize, and we may choose not to engage in any risk management activities. Should we fail to properly manage the inherent volatility of commodities prices, our results of operations and financial condition may be adversely affected.

The market for natural gas is subject to market conditions that create uncertainty in the price and availability of the natural gas that our ethanol plants use in their manufacturing process. Our ethanol plants rely upon third parties for their supply of natural gas, which is consumed as fuel in the production of ethanol. The prices for and availability of natural gas are subject to volatile market conditions. These market conditions often are affected by factors beyond the ethanol plants' control, such as weather conditions, overall economic conditions and foreign and domestic governmental regulation and relations. Significant disruptions in the supply of natural gas could impair or completely prevent the ethanol plants' ability to economically manufacture ethanol for their customers. Furthermore, increases in natural gas prices or changes in our natural gas costs relative to natural gas costs paid by competitors may adversely affect results of operations and financial position at our ethanol plants.

Fluctuations in the selling price of commodities may reduce profit margins at our ethanol plants. Ethanol is marketed as a fuel additive to reduce vehicle emissions from gasoline, as an octane enhancer to improve the octane rating of gasoline with which it is blended and, to a lesser extent, as a gasoline substitute. As a result, ethanol prices are influenced by the supply and demand for gasoline and our ethanol plants' results of operations and financial position may be materially adversely affected if gasoline demand or prices decrease.

Distillers grains compete with other protein based animal feed products. The price of distillers grains may decrease when the prices of competing feed products decrease. The prices of competing animal feed products are based in part on the prices of the commodities from which their products are made. Historically, sales prices for distillers grains have tracked along with the price of corn. However, there have been instances when the price increase for distillers grains has lagged price increases in corn prices.

The production of distillers grains has increased as a result of increases in dry mill ethanol production in the United States. This could lead to price declines in what we can sell our distillers grains for in the future. Such declines could have an adverse material effect on our results of operations.

Increased ethanol production or decreases in demand for ethanol may result in excess production capacity in the ethanol industry, which may cause the price of ethanol, distillers grains and non-food grade corn oil to decrease.

According to the RFA, domestic ethanol production nameplate capacity is approximately 15.6 billion gallons per year at January 2016. The RFA estimates that, as of January 2016, approximately 162 million gallons per year of additional production capacity is under construction or expansion. In addition, certain operating plants have qualified as efficient ethanol producers through the EPA pathway assessment, and are expanding, or planning to expand their capacity. The EPA set the RFS requirement to be satisfied by corn derived ethanol at 14.5 billion gallons for 2016. Excess capacity in the ethanol industry could have an adverse effect on the results of our operations. In a manufacturing industry with excess capacity, producers

| 9 |

have an incentive to manufacture additional products for so long as the price exceeds the marginal cost of production (i.e., the cost of producing only the next unit, without regard for interest, overhead or fixed costs). This incentive could result in the reduction of the market price of ethanol to a level that is inadequate to generate sufficient cash flow to cover costs.

Excess capacity may also result from decreases in the demand for ethanol, which could result from a number of factors, including, but not limited to, regulatory developments and reduced U.S. gasoline consumption. Reduced gasoline consumption could occur as a result of increased prices for gasoline or crude oil, which could cause businesses and consumers to reduce driving or acquire vehicles with more favorable gasoline mileage or acquire hybrid vehicles.

In addition, because ethanol production produces distillers grains and non-food grade corn oil as co-products, increased ethanol production will also lead to increased supplies of distillers grains and non-food grade corn oil. An increase in the supply of distillers grains and non-food grade corn oil, without corresponding increases in demand, could lead to lower prices or an inability to sell our ethanol plants' distillers grains and non-food grade corn oil production. A decline in the price of distillers grains or non-food grade corn oil could have a material adverse effect on the results of our ethanol operations.

Trade restrictions on ethanol exports and unfavorable foreign currency exchange rates could reduce the demand for ethanol.

The United States exported approximately 844 million gallons of ethanol in 2015. If producers and exporters of ethanol are subject to trade restrictions, or additional duties are imposed on exports, it may make it uneconomical to export ethanol. Furthermore, unfavorable changes in foreign currency exchange rates could reduce the demand for United States ethanol exports. This could result in an oversupply of ethanol in the United States which could have a material adverse effect on the results of our ethanol operations.

We depend on our partners to operate certain of our ethanol investments .

Our investments currently represent both majority and minority equity positions. Day-to-day operating control of minority owned plants generally remains with the local farmers' cooperative or investor group that has promoted the plant. We do not have the ability to directly modify the operations of these plants in response to changes in the business environment or in response to any deficiencies in local operations of the plants. In addition, local plant operators, who also represent the primary suppliers of corn and other crops to the plants, may have interests, such as the price and sourcing of corn and other crops, that may differ from our interest, which is based solely on the operating profit of the plant. The limitations on our ability to control day-to-day plant operations could adversely affect plant results of operations.

We may not successfully acquire or develop additional ethanol investments.

The growth of our ethanol business depends on our ability to identify and develop new ethanol investments. Our ethanol development strategy depends on referrals, and introductions, to new investment opportunities from industry participants, such as ethanol plant builders, financial institutions, marketing agents and others. We must continue to maintain favorable relationships with these industry participants, and a material disruption in these sources of referrals would adversely affect our ability to expand our ethanol investments.

Any expansion strategy will depend on prevailing market conditions for the price of ethanol and the costs of corn and natural gas and the expectations of future market conditions. There is increasing competition for suitable sites for ethanol plants. Even if suitable sites or opportunities are identified, we may not be able to secure the services and products from contractors, engineering firms, construction firms and equipment

| 10 |

suppliers necessary to build or expand ethanol plants on a timely basis or on acceptable economic terms. Construction costs associated with expansion may increase to levels that would make a new plant too expensive to complete or unprofitable to operate. Additional financing may also be necessary to implement any expansion strategy, which may not be accessible or available on acceptable terms. New and more stringent environmental regulations could increase the operating costs and risks of new plants, which, in turn could discourage us from further expansion.

Our ethanol plants may be adversely affected by technological advances and efforts to anticipate and employ such technological advances may prove unsuccessful.

The development and implementation of new technologies may result in a significant reduction in the costs of ethanol production. For instance, any technological advances in the efficiency or cost to produce ethanol from inexpensive, cellulosic sources such as corn stalk, wheat, oat or barley straw could have an adverse effect on our ethanol plants, because those facilities are designed to produce ethanol from corn, which is, by comparison, a raw material with other high value uses. We cannot predict when new technologies may become available, the rate of acceptance of new technologies by competitors or the costs associated with new technologies. In addition, advances in the development of alternatives to ethanol could significantly reduce demand for or eliminate the need for ethanol.

Any advances in technology which require significant unanticipated capital expenditures to remain competitive or which reduce demand or prices for ethanol would have a material adverse effect on the results of our ethanol operations.

In addition, alternative fuels, additives and oxygenates are continually under development. Alternative fuel additives that can replace ethanol may be developed, which may decrease the demand for ethanol. It is also possible that technological advances in engine and exhaust system design and performance could reduce the use of oxygenates, which would lower the demand for ethanol, and the results of our ethanol operations may be materially adversely affected.

The U.S. ethanol industry is highly dependent upon a myriad of federal and state legislation and regulation and any changes in legislation or regulation could materially and adversely affect our results of operations and financial position.

The Energy Independence and Security Act of 2007 (EISA) established RFS II, which modified the renewable fuel standard from prior legislation. EISA increased the amount of renewable fuel required to be blended into gasoline and required a minimum usage of corn derived renewable fuels of 12.0 billion gallons in 2010, increasing annually by 600 million gallons to 15.0 billion gallons in 2015. The EPA has the authority to assign the mandated amounts of renewable fuels to be blended into transportation fuel to individual fuel blenders. RFS II has been a primary factor in the growth of ethanol usage. On April 10, 2013, the Renewable Fuel Standard Elimination Act was introduced as H.R. 1461 to target the repeal of RFS II. Also introduced on April 10, 2013 was the RFS Reform Bill, H.R. 1462, which would prohibit more than ten percent ethanol in gasoline and reduce the RFS II required volume of renewable fuel. On May 14, 2013, the Domestic Alternatives Fuels Act of 2013 was introduced in the United States House of Representatives as H.R. 1959 to permit ethanol produced from natural gas to be used to meet the RFS II mandate. These bills failed to make it out of congressional committees and were not finalized into law. H.R. 21 was introduced on January 6, 2015 to provide for a comprehensive assessment of the scientific and technical research on the implication of the use of mid-level ethanol blends. This bill seeks to eliminate the waiver granted by the EPA to allow E15 fuel in 2001 and newer model cars and trucks. H.R. 434 was introduced on January 21, 2015 which seeks to modify the Clean Air Act by limiting or removing the authority of the EPA to grant waivers for higher blends of ethanol in domestic gasoline supply. This bill also repeals existing waivers

| 11 |

already granted by the EPA regarding E15 fuel. H.R. 704 was introduced February 4, 2015 and it is similar to H.R. 21 as it proposes limiting ethanol blends higher than 10% in domestic fuel supply and seeks to repeal the RFS.

Under EISA, the EPA has the authority to waive or modify the mandated RFS II requirements in whole or in part. In order to grant a waiver, the EPA administrator must determine in consultation with the Secretaries of Agriculture and Energy, that one of the following two conditions has been met: i) there is inadequate domestic renewable fuel supply or ii) implementation of the requirement would severely harm the economy or environment of a state, region or the country. During fiscal year 2012, several waiver requests were submitted to the EPA based on drought conditions, which were subsequently denied by the EPA.

The RFS II mandate increased to 14.4 billion gallons of corn derived renewable fuel for 2014 and 15.0 billion gallons in 2015 and was to remain at that level until 2022, subsequent to which time, no specific amount was established. In November of 2013, the EPA released a proposal that included several approaches for establishing the 2014 standards. The proposal was for approximately 15.2 billion gallons, including approximately 13.0 billion gallons of corn derived renewable fuel. The proposal addresses two constraints of RFS II: i) limitations in the volume of ethanol that can be consumed in gasoline given the practical constraints on the supply of higher ethanol blends to the vehicles that can use them and ii) limitations in the ability of the industry to produce sufficient volumes of qualifying renewable fuel. In November 2014, the EPA rescinded its 2013 proposal. Furthermore, the EPA did not finalize the 2014 standard under the RFS program before the end of that year.

On June 10, 2015, the EPA proposed volume targets for conventional ethanol of 13.25 billion gallons, 13.40 billion gallons and 14.00 billion gallons for 2014, 2015 and 2016, respectively. On November 30, 2015, the EPA announced final volume requirements for conventional ethanol that were higher than levels proposed in June of 13.61 billion gallons, 14.05 billion gallons and 14.50 billion gallons for 2014, 2015 and 2016, respectively. The EPA has not announced its proposed volume requirements for subsequent years.

To document compliance with RFS II, renewable identification numbers ("RINs"), are generated and attached to renewable fuels, and detached when the renewable fuel is blended into the transportation fuel supply. Detached RINs may be retired by obligated parties to demonstrate compliance with RFS II or may be separately traded in the market. The market price of detached RINs may affect the price of ethanol in certain U.S. markets as obligated parties may factor these costs into their purchasing decisions. Moreover, at certain price levels for various types of RINs, it becomes more economical to import foreign sugar cane ethanol. If changes to RFS II result in significant changes in the price of various types of RINs, it could negatively affect the price of ethanol and our ethanol business.

Changes in corporate average fuel economy standards could adversely impact ethanol prices. Flexible fuel vehicles receive preferential treatment in meeting federally mandated corporate average fuel economy ("CAFE") standards for automobiles manufactured by car makers. High blend ethanol fuels such as E-85 result in lower fuel efficiencies. Absent the CAFE preferences, car makers would not likely build flexible-fuel vehicles. Any change in CAFE preferences could reduce the growth of E-85 markets and result in lower ethanol prices.

Various studies have criticized the efficiency of ethanol, in general, and corn-based ethanol in particular, which could lead to the reduction or repeal of incentives and tariffs that promote the use and domestic production of ethanol or otherwise negatively impact public perception and acceptance of ethanol as an alternative fuel.

| 12 |

Although many trade groups, academics and governmental agencies have supported ethanol as a fuel additive that promotes a cleaner environment, others have criticized ethanol production as consuming considerably more energy and emitting more greenhouse gases than other biofuels and as potentially depleting water resources. Other studies have suggested that corn-based ethanol is less efficient than ethanol produced from switchgrass or wheat grain and that it negatively impacts consumers by causing prices for dairy, meat and other foodstuffs from livestock that consume corn to increase. If these views gain acceptance, support for existing measures promoting use and domestic production of corn-based ethanol could decline, leading to reduction or repeal of these measures. These views could also negatively impact public perception of the ethanol industry and acceptance of ethanol as an alternative fuel.

Federal support of cellulosic ethanol may result in reduced incentives to corn-derived ethanol producers.

The American Recovery and Reinvestment Act of 2009 and EISA provide funding opportunities in support of cellulosic ethanol obtained from biomass sources such as switchgrass and poplar trees. The amended RFS mandates an increasing level of production of non-corn derived biofuels. These federal policies may suggest a long-term political preference for cellulosic processes using alternative feedstocks such as switchgrass, silage or wood chips. Cellulosic ethanol has a smaller carbon footprint and is unlikely to divert foodstuff from the market. Several cellulosic ethanol plants are under development and there is a risk that cellulosic ethanol could displace corn ethanol. Our plants are designed as single-feedstock facilities, located in corn production areas with limited alternative feedstock nearby, and would require significant additional investment to convert to the production of cellulosic ethanol. The adoption of cellulosic ethanol as the preferred form of ethanol could have a significant adverse effect on our ethanol business.

Our ethanol business is affected by environmental and other regulations which could impede or prohibit our ability to successfully operate our plants.

Our ethanol production facilities are subject to extensive air, water and other environmental regulations. We have had to obtain numerous permits to construct and operate our plants. Regulatory agencies could impose conditions or other restrictions in the permits that are detrimental or which increase our costs. More stringent federal or state environmental regulations could be adopted which could significantly increase our operating costs or require us to expend considerable resources.

Our ethanol plants emit various airborne pollutants as by-products of the ethanol production process, including carbon dioxide. In 2007, the U.S. Supreme Court classified carbon dioxide as an air pollutant under the Clean Air Act in a case seeking to require the EPA to regulate carbon dioxide in vehicle emissions. In February 2010, the EPA released its final regulations on the Renewable Fuel Standard program. We believe our plants are grandfathered at their current operating capacity, but plant expansion will need to meet a 20% threshold reduction in greenhouse gas (GHG) emissions from a 2005 baseline measurement to produce ethanol eligible for the RFS II mandate. To expand our plant capacity, we may be required to obtain additional permits, install advanced technology equipment, or reduce drying of certain amounts of distillers grains. We may also be required to install carbon dioxide mitigation equipment or take other steps in order to comply with future laws or regulations. Compliance with future laws or regulations of carbon dioxide, or if we choose to expand capacity at certain of our plants, compliance with then-current regulations of carbon dioxide, could be costly and may prevent us from operating our plants as profitably, which may have a negative impact on our financial performance. We also face the risk of ethanol production above our grandfathered capacity not qualifying for RINS if the plants do not meet certain emission requirements.

The California Air Resources Board ("CARB") has adopted a Low Carbon Fuel Standard ("LCFS") requiring a 10% reduction in GHG emissions from transportation fuels by 2020. An Indirect Land Use

| 13 |

Charge is included in this lifecycle GHG emission calculation. After a series of rulings that temporarily prevented CARB from enforcing these regulations, the State of California Office of Administrative Law approved the LCFS on November 26, 2012 and revised LCFS regulations took effect in January 2013. This standard could have an adverse impact on the market for corn-based ethanol in California if corn-based ethanol fails to achieve lifecycle GHG emission reductions. This could have a negative impact on our financial performance.

Our ethanol business may become subject to various environmental and health and safety and property damage claims and liabilities.

Operations of our ethanol business will expose the business to the risk of environmental and health and safety claims and property damage claims, such as failure to comply with environmental regulations. These types of claims could also be made against our ethanol business based upon the acts or omissions of other persons. Serious claims could have a material negative impact on our results of operations, financial position and future cash flows.

Our business is not significantly diversified.

Our financial results depend heavily on our ability to operate our ethanol plants profitably. We do not have other lines of business or other sources of revenue to depend upon if we are unable to operate our ethanol plants profitably. Such lack of significant diversification could have a material negative impact on our results of operations, financial position and future cash flows should our ethanol plants operate unprofitably.

Our revenue from the sale of distillers grains depends upon its continued market acceptance as an animal feed.

Distillers grains is a co-product from the fermentation of corn to produce ethanol. Antibiotics may be used during the fermentation process to control bacterial contamination; therefore antibiotics may be present in small quantities in distillers grains marketed as animal feed. The U. S. Food and Drug Administration's, or FDA's, Center for Veterinary Medicine has expressed concern about potential animal and human health hazards from the use of distillers grains as an animal feed due to the possibility of antibiotic residues. If the public became concerned about the impact of distillers grains in the food supply or as an acceptable animal feed, the market for distillers grains could be negatively impacted, which would have a negative impact on our results of operations. We may not be able to obtain a suitable replacement for antibiotics, should this be required, which would also negatively impact the market for distillers grains.

Exports of distillers grains produced in the United States have been increasing in recent years. The price of distillers grains has benefitted from the increased exports of the product, with China being the largest importer. In 2013, China rejected certain shipments of distillers grains due to the presence of unapproved genetically modified organisms. If shipments to China or other countries are rejected or delayed, the market price for distillers grains would be negatively impacted, which would have a negative impact on our ethanol results of operations.

At certain of our plants, we extract and sell non-food grade corn oil immediately prior to the production of distillers grains. Several studies are trying to determine how non-food grade corn oil extraction may impact the nutritional value of the resulting distillers grains. If it is determined that non-food grade corn oil extraction adversely impacts the nutritional energy content of distillers grains, the value of the distillers grains we sell may be negatively impacted, which would have a negative impact on our results of operations.

| 14 |

The price of distillers grains may decline as a result of restrictions or duties on distillers grains exports from the United States or from unfavorable changes in foreign currency exchange rates.

Exports of distillers grains produced in the United States have been increasing in recent years. However, the export market may be jeopardized if foreign governments impose trade barriers or other measures to protect the foreign local markets. In January 2016, the China' Ministry of Commerce announced it has initiated anti-dumping and countervailing duty investigations of U.S. dried distillers grains exports to China. If producers and exporters of distillers grains are subjected to trade barriers when selling distillers grains to foreign customers, there may be a reduction in the price of distillers grains in the United States. In addition, foreign currency exchange rate fluctuations could reduce the demand for United States exports of distillers grains. Declines in the price we receive for our distillers grains could lead to decreased revenues and may result in our inability to operate our ethanol plants profitably.

We face significant competition in the ethanol industry.

We face significant competition for new ethanol investment opportunities. There are varied enterprises seeking to participate in the ethanol industry. Some enterprises provide financial and management support similar to our business model. Other enterprises seek to acquire or develop plants which they will directly own and operate. Many of our competitors are larger and have greater financial resources and name recognition than we do. We must compete for investment opportunities based on our strategy of supporting and enhancing local development of ethanol plant opportunities. We may not be successful in competing for investment opportunities based on our strategy.

The ethanol industry is primarily comprised of entities that engage exclusively in ethanol production and large integrated grain companies that produce ethanol along with their base grain business. Several large oil companies have entered the ethanol production market. If these companies increase their ethanol plant ownership or other oil companies seek to engage in direct ethanol production, there would be less of a need to purchase ethanol from independent producers like our ethanol plants.

Plants sold as part of a bankruptcy proceeding may have significantly lower fixed costs than our ethanol plants. Absent significant growth and diversification, our ethanol plants may not be able to operate profitably in a more competitive environment. No assurance can be given that our ethanol plants will be able to compete successfully or that competition from larger companies with greater financial resources will not have a materially adverse impact on the results of our ethanol operations.

We may face competition from foreign companies.

There is a risk of foreign competition in the ethanol industry. Brazil is presently the second largest producer of ethanol in the world. Brazil's ethanol production is sugarcane based, and, depending on feedstock prices, may be cheaper to produce. Under the RFS, certain parties were obligated to meet an advanced biofuel standard. In recent years, sugarcane based ethanol imported from Brazil has been one of the most economical means for obligated parties to comply with this standard.

If significant additional foreign ethanol production capacity is created, such facilities could create excess supplies of ethanol, which may result in lower prices of ethanol. In addition, foreign ethanol producers may be able to produce ethanol at costs lower than ours. These risks could have significant adverse effects on our financial performance.

In addition, the tariff that protected the U.S. ethanol industry expired at the end of 2011. The expiration of the tariff could lead to increases in the import of ethanol produced outside of the U.S.

| 15 |

We are exposed to credit risk from our sales of ethanol and distillers grains to customers.

The inability of a customer to make payments to us for our accounts receivable may cause us to experience losses and may adversely impact our liquidity and our ability to make our payments when due.

We may not be able to hire and retain qualified personnel to operate our ethanol plants.

Our ability to attract and retain competent personnel has a significant impact on operating efficiencies and plant profitability. Competition for key plant employees in the ethanol industry can be intense, and we may not be able to attract and retain qualified employees. Failure to do so could have a negative impact on our financial results at individual plants.

Our plants depend on an uninterrupted supply of energy and water to operate. Unforeseen plant shutdowns could harm our business.

Our plants require a significant and uninterrupted supply of natural gas, electricity and water to operate. We generally rely on third parties to provide these resources. If there is an interruption in the supply of energy or water for any reason, such as supply, delivery or mechanical problems and we are unable to secure an adequate alternative supply to sustain plant operations, we may be required to stop production. A production halt for an extended period of time could result in material losses.

Potential business disruption from factors outside our control, including natural disasters, severe weather conditions, accidents, strikes, unexpected equipment failures and unforeseen plant shutdowns, could adversely affect our cash flow and operating results.

The debt agreements for certain of the ethanol plants limit, or otherwise restrict the amount of dividends and other payments the ethanol subsidiaries can transfer to their members.

We are dependent on dividends from our ethanol subsidiaries to generate cash flow. Presently our unconsolidated ethanol subsidiary has debt agreements that limit payments to members. Therefore, this company cannot distribute all of the cash it generates to their members. Furthermore, we may not be able to use the excess cash flow from one subsidiary to fund corporate needs or needs of another operating ethanol subsidiary.

We rely on information technology in our operations and financial reporting and any material failure, inadequacy, interruption or security breach of that technology could harm our ability to efficiently operate our business and report our financial results accurately and timely.

We rely heavily on information technology systems across our operations, including for management of inventory, purchase orders, production, invoices, shipping, accounting and various other processes and transactions. Our ability to effectively manage our business, coordinate the production, distribution and sale of our products and ensure the timely and accurate recording and disclosure of financial information depends significantly on the reliability and capacity of these systems. The failure of these systems to operate effectively, problems with transitioning to upgraded or replacement systems, or a breach in security of these systems through a cyber-attack or otherwise could cause delays in product sales, reduced efficiency of our operations and delays in reporting our financial results. Significant capital investments could be required to remediate any such problem. Security breaches of employee information or other confidential or proprietary data could also adversely impact our reputation, and could result in litigation against us or the imposition of penalties.

| 16 |

We are exposed to potential business disruption from factors outside our control, including natural disasters, severe weather conditions, accidents, and unforeseen operational failures any of which could negatively affect our transportation operations and could adversely affect our cash flows and operating results.

Potential business disruption in available transportation due to natural disasters, significant track damage resulting from a train derailment, strikes or other interruptions by our transportation providers could result in delays in procuring and supplying raw materials to our ethanol facilities, or transporting ethanol and distillers grains to our customers. Such business disruptions may result in our inability to meet customer demand or contract delivery requirements, as well as the potential loss of customers.

Rail cars used to transport ethanol may need to be modified or replaced to meet proposed rail safety regulations.

The leased rail cars we use to transport ethanol to market will need to be retrofitted or replaced as the Enhanced Tank Car Standards and Operation Controls for High-Hazard Flammable Trains adopted by the U.S. Department of Transportation ("DOT") calls for an enhanced tank car standard known as the DOT specification 117 and establishes a schedule to retrofit or replace older tank cars that carry crude oil and ethanol. The rule also establishes braking standards intended to reduce the severity of accidents and new operational protocols. This could lead to increased rail car lease costs and delays in transportation of ethanol if rail cars are out of service for extended periods of time.

Risks Related to our eSteam investments and operations.

eSteam may not be commercially viable technology.

During fiscal year 2013, we invested in eSteam, a new technology utilizing steam to extract deep heavy oil. Cumulatively, we have spent approximately $1.6 million on this patented but unproven technology. Low energy and crude oil prices may make eSteam technology less attractive to potential users. If we cannot demonstrate that the technology is commercially feasible, we may incur additional losses.

Our eSteam technology may be subject to patent challenges.

We could be required to spend considerable time and resources defending our technology from patent challenges.

Operations utilizing our eSteam technology may be subject to stringent environmental regulations.

These operations will require significant amounts of water and energy. If we are unable to obtain the proper permits and sources of water and energy, then we may not be able to operate the new technologies, and thus, generate any revenue.

Operations utilizing our eSteam technology may cause environmental damage.

When operating the eSteam technology, we may cause environmental damage, as we would be injecting water into the ground in order to extract oil. We could be subject to significant penalties and fines if we were to cause environmental damage.

| Item 1B. | Unresolved Staff Comments |

None.

| 17 |

| Item 2. | Properties |

The information required by this Item 2 is set forth in Item 1 of this report under "Ethanol Investments" and "Facilities" and is incorporated herein by reference.

| Item 3. | Legal Proceedings |

We are involved in various legal proceedings incidental to the conduct of our business from time to time. We believe that the current proceedings will not have a material adverse effect on our financial condition or results of operations.

Executive Officers of the Company

Set forth below is certain information about each of our executive officers.

| Name | Age | Position | ||

| Stuart Rose | 61 | Executive Chairman of the Board* | ||

| Zafar Rizvi | 66 | Chief Executive Officer and President* | ||

| Douglas Bruggeman | 55 | Vice President-Finance, Chief Financial Officer and Treasurer | ||

| Edward Kress | 66 | Secretary* |

*Also serves as a director.

Stuart Rose was elected our Executive Chairman of the Board in 2015. Mr. Rose had served as our Chairman of the Board and Chief Executive Officer since our incorporation in 1984 as a holding company. Prior to 1984, Mr. Rose was Chairman of the Board and Chief Executive Officer of Rex Radio and Television, Inc., which he founded in 1980 to acquire the stock of a corporation which operated four retail stores.

Zafar Rizvi was elected Chief Executive Officer in 2015. Mr. Rizvi has been our President and Chief Operating Officer since 2010, was Vice President from 2006 to 2010 and has been President of Farmers Energy Incorporated, our alternative energy investment subsidiary, since 2006. From 1991 to 2006, Mr. Rizvi was our Vice President – Loss Prevention.

Douglas Bruggeman has been our Vice President–Finance and Treasurer since 1989 and was elected Chief Financial Officer in 2003. From 1987 to 1989, Mr. Bruggeman was our Manager of Corporate Accounting. Mr. Bruggeman was employed with the accounting firm of Ernst & Young prior to joining us in 1986.

Edward Kress has been our Secretary since 1984. Mr. Kress has been a partner of the law firm of Dinsmore & Shohl LLP (formerly Chernesky, Heyman & Kress P.L.L.), our legal counsel, since 1988. Mr. Kress has practiced law in Dayton, Ohio since 1974.

| Item 4. | Mine Safety Disclosures |

Not Applicable

| 18 |

PART II

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

SHAREHOLDER INFORMATION

Common Share Information and Quarterly Share Prices

Our common stock is traded on the New York Stock Exchange under the symbol REX.

| Fiscal Quarter Ended | High | Low | |||||||

| April 30, 2014 | $ | 68.41 | $ | 37.33 | |||||

| July 31, 2014 | 90.69 | 56.59 | |||||||

| October 31, 2014 | 110.65 | 55.46 | |||||||

| January 31, 2015 | 76.29 | 51.63 | |||||||

| April 30, 2015 | $ | 65.99 | $ | 53.65 | |||||

| July 31, 2015 | 67.99 | 51.59 | |||||||

| October 31, 2015 | 58.99 | 43.50 | |||||||

| January 31, 2016 | 64.40 | 44.48 | |||||||

As of March 23, 2016, there were 88 holders of record of our common stock, including shares held in nominee or street name by brokers.

Dividend Policy

We did not pay dividends in the current or prior years. We (including our consolidated subsidiaries) currently have no restrictions on the payment of dividends. Our minority owned ethanol subsidiary has restrictions on its ability to pay dividends to members (including REX). One Earth paid dividends to REX of approximately $11.4 million, $13.2 million and $4.4 million during fiscal years 2015, 2014 and 2013, respectively. NuGen paid no dividends to REX during fiscal year 2015, and paid dividends to REX of approximately $34.8 million and $5.0 million during fiscal years 2014 and 2013, respectively.

Issuer Purchases of Equity Securities

| Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (1) | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs (1) | |||||||||||||

| November 1-30, 2015 | - | $ | - | - | 452,809 | ||||||||||||

| December 1-31, 2015 | 27,426 | $ | 49.46 | 27,426 | 425,383 | ||||||||||||

| January 1-31, 2016 | 182,145 | $ | 47.96 | 182,145 | 243,238 | ||||||||||||

| Total | 209,571 | $ | 48.16 | 209,571 | 243,238 | ||||||||||||

| 19 |

| (1) | On August 26, 2015, our Board of Directors increased our share repurchase authorization by an additional 500,000 shares. At January 31, 2016, a total of 243,238 shares remained available to purchase under this authorization. |

Equity Compensation Plans

Refer to Item 12 – Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters for information regarding shares authorized for issuance under equity compensation plans.

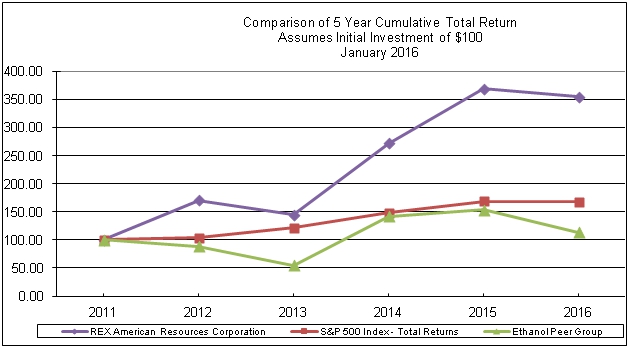

Performance Graph

The following graph compares the yearly percentage change in the cumulative total shareholder return on our Common Stock against the cumulative total return of the S&P 500 Stock Index and a peer group comprised of selected publicly traded ethanol producers (*) for the period commencing January 31, 2011 and ended January 31, 2016. The graph assumes an investment of $100 in our Common Stock and each index on January 31, 2011 and reinvestment of all dividends.

* The peer group is comprised of Pacific Ethanol, Inc. and Green Plains, Inc.

| Item 6. | Selected Financial Data |

The following statements of operations and balance sheet data have been derived from our consolidated financial statements and should be read in conjunction with Management's Discussion and Analysis of Financial Condition and Results of Operations and the Consolidated Financial Statements and related Notes. See Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations for a discussion of net sales and revenue and gross profit, income from ethanol investments, derivative financial

| 20 |

instruments, and long-term debt. These items have fluctuated significantly in recent years and may affect comparability of years.

| 21 |

Five Year Financial Summary

(In Thousands, Except Per Share Amounts)

| Years Ended January 31, | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||

| Net sales and revenue | $ | 436,488 | $ | 572,230 | $ | 666,045 | $ | 656,589 | $ | 408,856 | ||||||||||

| Cost of sales | 385,654 | 430,291 | 601,757 | 642,787 | 373,912 | |||||||||||||||

| Gross profit | 50,834 | 141,939 | 64,288 | 13,802 | 34,944 | |||||||||||||||

| Selling, general and administrative expenses | (19,813 | ) | (19,422 | ) | (17,846 | ) | (12,546 | ) | (10,376 | ) | ||||||||||

| Equity in income of unconsolidated ethanol affiliates | 8,984 | 32,229 | 17,175 | 627 | 21,532 | |||||||||||||||

| Interest expense | - | (2,074 | ) | (3,898 | ) | (4,828 | ) | (3,374 | ) | |||||||||||

| Net income (loss) attributable to REX common shareholders | 31,436 | 87,337 | 35,073 | (2,295 | ) | 28,270 | ||||||||||||||

| Diluted net income (loss) per share attributable to REX common shareholders | $ | 4.30 | $ | 10.76 | $ | 4.29 | $ | (0.28 | ) | $ | 3.08 | |||||||||

| January 31, | 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 135,765 | $ | 137,697 | $ | 105,149 | $ | 69,073 | $ | 75,013 | ||||||||||

| Current assets | 179,360 | 175,745 | 148,810 | 114,927 | 127,039 | |||||||||||||||

| Property and equipment – net | 189,976 | 194,447 | 202,258 | 223,180 | 240,084 | |||||||||||||||

| Equity method investments | 38,707 | 80,389 | 71,189 | 59,959 | 61,679 | |||||||||||||||

| Long term debt | - | - | 63,500 | 91,306 | 108,527 | |||||||||||||||

| Total REX shareholders' equity | 311,263 | 349,971 | 279,281 | 246,352 | 252,511 | |||||||||||||||

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations |

Overview

We have been an investor in various alternative energy entities beginning with synthetic fuel partnerships in 1998 and later ethanol production facilities beginning in 2006. We currently have equity investments in three ethanol production entities, two of which we have a majority ownership interest. We may make additional alternative energy investments in the future.

Our ethanol operations are highly dependent on commodity prices, especially prices for corn, ethanol, distillers grains, non-food grade corn oil and natural gas. As a result of price volatility for these commodities, our operating results can fluctuate substantially. The price and availability of corn is subject to significant fluctuations depending upon a number of factors that affect commodity prices in general, including crop conditions, weather, federal policy and foreign trade. Because the market price of ethanol is not always directly related to corn prices, at times ethanol prices may not follow movements in corn prices and, in an environment of higher corn prices or lower ethanol prices, reduce the overall margin structure at the plants. As a result, at times, we may operate our plants at negative or marginally positive operating margins.

We expect our ethanol plants to produce approximately 2.8 gallons of denatured ethanol for each bushel of grain processed in the production cycle. We refer to the difference between the price per gallon of ethanol

| 22 |

and the price per bushel of grain (divided by 2.8) as the "crush spread." Should the crush spread decline, our ethanol plants are likely to generate operating results that do not provide adequate cash flows for sustained periods of time. In such cases, production at the ethanol plants may be reduced or stopped altogether in order to minimize variable costs at individual plants.

We attempt to manage the risk related to the volatility of grain and ethanol prices by utilizing forward grain purchase and forward ethanol, distillers grains and non-food grade corn oil sale contracts. We attempt to match quantities of these sale contracts with an appropriate quantity of grain purchase contracts over a given period of time when we can obtain an adequate gross margin resulting from the crush spread inherent in the contracts we have executed. However, the market for future ethanol sales contracts is not a mature market. Consequently, we generally execute fixed price contracts for no more than two months into the future at any given time and we may lock in our corn or ethanol price without having a corresponding locked in ethanol or corn price for short durations of time. As a result of the relatively short period of time our fixed price contracts cover, we generally cannot predict the future movements in the crush spread for more than two months; thus, we are unable to predict the likelihood or amounts of future income or loss from the operations of our ethanol facilities.

The crush spread realized in fiscal year 2015 was subject to significant volatility. For fiscal year 2015, the average Chicago Board of Trade ("CBOT") near-month corn price ranged from a low of approximately $3.48 per bushel in June 2015 to a high of approximately $4.41 per bushel in July 2015. Corn prices were favorably impacted throughout the year from the three strongest corn harvests in U. S. history in 2013, 2014 and 2015 (in order of strength of harvest production). Ethanol prices had significant fluctuations ranging from approximately $1.31 per gallon in January 2016 to a high of approximately $1.69 per gallon in May 2015. Ethanol prices were influenced by many factors throughout the year including low energy prices, particularly late in fiscal year 2015 and over-production of ethanol. The CBOT crush spread during fiscal year 2015 ranged from approximately $0.02 in February 2015 to approximately $0.37 in May 2015.

Income from continuing operations, net of tax was approximately $31.4 million in fiscal year 2015 compared to approximately $86.8 million in fiscal year 2014. We sold our interest in Patriot Holdings, LLC ("Patriot") effective June 1, 2015 for an after tax gain of approximately $6.6 million. The gain and resulting loss of income from Patriot using the equity method of accounting affects comparability between years. The decrease in profitability primarily resulted from lower crush spreads (compared to the prior year) experienced in the ethanol industry for a majority of fiscal year 2015 as lower energy prices and over supply of ethanol reduced ethanol pricing during fiscal year 2015. We expect that future operating results, from our consolidated plants, will be based upon combined annual production of between 215 and 240 million gallons of ethanol, which assumes that our consolidated ethanol plants will operate at or above nameplate capacity. However, due to the inherent volatility of the crush spread, we cannot predict the likelihood of future operating results being similar to the fiscal year 2015 results. We utilize derivative financial instruments, primarily exchange traded commodity future contracts, in conjunction with certain of our grain procurement activities.

The crush spread in the first quarter of fiscal year 2016 has continued to be negatively impacted by lower energy pricing and over supply of ethanol. Likewise, distillers grains pricing has also trailed the prior year which we believe is largely being impacted by lower corn prices and over supply. Distillers grains pricing may also be negatively impacted by the Chinese government initiating an anti-dumping and countervailing duty investigation in January 2016.

The EPA has reduced the RFS required volume from conventional biofuels for 2014, 2015 and 2016 from its originally mandated levels of 14.4 billion, 15.0 billion and 15.0 billion gallons to 13.6 billion, 14.1 billion and 14.5 billion gallons, respectively. The uncertainty regarding the required RFS volumes for future years could negatively impact ethanol pricing. The U.S. ethanol industry produced approximately 14.8 billion

| 23 |

gallons of conventional biofuel in 2015. The U.S. exported approximately 844 million gallons in 2015. If the export market is not maintained or increased, ethanol pricing may be negatively impacted.