UNITED STATES SECURITIES AND EXCHANGE COMMISSION |

Washington, D.C. 20549 |

|

Form 10-K |

(Mark one)

[x] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended June 30, 2014

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File No. 1-434

THE PROCTER & GAMBLE COMPANY |

One Procter & Gamble Plaza, Cincinnati, Ohio 45202 |

Telephone (513) 983-1100 |

IRS Employer Identification No. 31-0411980 |

State of Incorporation: Ohio |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common Stock, without Par Value |

| New York Stock Exchange, NYSE Euronext-Paris |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company (as defined in Rule 12b-2 of the Exchange Act).

Large accelerated filer ☑ Accelerated filer o Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ☑

The aggregate market value of the voting stock held by non-affiliates amounted to $221 billion on December 31, 2013 .

There were 2,707,652,337 shares of Common Stock outstanding as of July 31, 2014 .

Documents Incorporated by Reference

Portions of the Proxy Statement for the 2014 Annual Meeting of Shareholders which will be filed within one hundred and twenty days of the fiscal year ended June 30, 2014 ( 2014 Proxy Statement) are incorporated by reference into Part III of this report to the extent described herein.

The Procter & Gamble Company 11

PART I

Item 1. Business .

Additional information required by this item is incorporated herein by reference to Management's Discussion and Analysis (MD&A); Note 1 to our Consolidated Financial Statements and Note 12 to our Consolidated Financial Statements. Unless the context indicates otherwise, the terms the "Company," "P&G," "we," "our" or "us" as used herein refer to The Procter & Gamble Company (the registrant) and its subsidiaries.

The Procter & Gamble Company is focused on providing branded consumer packaged goods of superior quality and value to improve the lives of the world's consumers. The Company was incorporated in Ohio in 1905, having been built from a business founded in 1837 by William Procter and James Gamble. Today, we sell our products in more than 180 countries and territories.

Throughout this Form 10-K, we incorporate by reference information from other documents filed with the Securities and Exchange Commission (SEC).

The Company's annual report on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, and amendments thereto, are filed electronically with the SEC. The SEC maintains an internet site that contains these reports at: www.sec.gov. You can also access these reports through links from our website at: www.pg.com/investors.

Copies of these reports are also available, without charge, by contacting Computershare Inc., 250 Royall Street, Canton, MA 02021.

Financial Information about Segments

As of June 30, 2014, the Company has five reportable segments under U.S. GAAP: Beauty; Grooming; Health Care; Fabric Care and Home Care; and Baby, Feminine and Family Care. Many of the factors necessary for understanding these businesses are similar. Operating margins of the individual businesses vary due to the nature of materials and processes used to manufacture the products, the capital intensity of the businesses and differences in selling, general and administrative expenses as a percentage of net sales. Net sales growth by business is also expected to vary slightly due to the underlying growth of the markets and product categories in which they operate. While none of our reportable segments are highly seasonal, components within certain reportable segments, such as Batteries (Fabric Care and Home Care), Appliances (Grooming) and Prestige Fragrances (Beauty) are seasonal. In addition, anticipation or occurrence of natural disasters, such as hurricanes, can drive unusually high demand for batteries.

Additional information about our reportable segments can be found in MD&A and Note 12 to our Consolidated Financial Statements.

Narrative Description of Business

Business Model . Our business model relies on the continued growth and success of existing brands and products, as well as the creation of new products. The markets and industry segments in which we offer our products are highly competitive. Our products are sold in more than 180 countries and territories around the world primarily through mass merchandisers, grocery stores, membership club stores, drug stores, department stores, salons, e-commerce and high-frequency stores. We utilize our superior marketing and online presence to win with consumers at the "zero moment of truth" - when they are searching for information about a brand or product. We work collaboratively with our customers to improve the in-store presence of our products and win the "first moment of truth" - when a consumer is shopping in the store. We must also win the "second moment of truth" - when a consumer uses the product, evaluates how well it met his or her expectations and decides whether it was a good value. We believe we must continue to provide new, innovative products and branding to the consumer in order to grow our business. Research and product development activities, designed to enable sustained organic growth, continued to carry a high priority during the past fiscal year. While many of the benefits from these efforts will not be realized until future years, we believe these activities demonstrate our commitment to future growth.

Key Product Categories . Information on key product categories can be found in Note 12 to our Consolidated Financial Statements.

Key Customers . Our customers include mass merchandisers, grocery stores, membership club stores, drug stores, department stores, salons, distributors, e-commerce and high-frequency stores. Sales to Wal-Mart Stores, Inc. and its affiliates represent approximately 14% of our total revenue in 2014, 2013 and 2012. No other customer represents more than 10% of our net sales. Our top ten customers account for approximately 30% of our total unit volume in 2014 and 2013 and 31% of our total unit volume in 2012. The nature of our business results in no material backlog orders or contracts with the government. We believe our practices related to working capital items for customers and suppliers are consistent with the industry segments in which we compete.

Sources and Availability of Materials . Almost all of the raw and packaging materials used by the Company are purchased from others, some of which are single-source suppliers. We produce certain raw materials, primarily chemicals, for further use in the manufacturing process. In addition, fuel, natural gas and derivative products are important commodities consumed in our manufacturing process and in the distribution of input materials and finished

12 The Procter & Gamble Company

product to customers. The prices we pay for materials and other commodities are subject to fluctuation. When prices for these items change, we may or may not pass the change to our customers. The Company purchases a substantial variety of other raw and packaging materials, none of which is material to our business taken as a whole.

Trademarks and Patents . We own or have licenses under patents and registered trademarks which are used in connection with our activity in all businesses. Some of these patents or licenses cover significant product formulation and processes used to manufacture our products. The trademarks are important to the overall marketing and branding of our products. All major products and trademarks in each business are registered. In part, our success can be attributed to the existence and continued protection of these trademarks, patents and licenses.

Competitive Condition . The markets in which our products are sold are highly competitive. Our products compete against similar products of many large and small companies, including well-known global competitors. In many of the markets and industry segments in which we sell our products, we compete against other branded products as well as retailers' private-label brands. We are well positioned in the industry segments and markets in which we operate, often holding a leadership or significant market share position. We support our products with advertising, promotions and other marketing vehicles to build awareness and trial of our brands and products in conjunction with an extensive sales force. We believe this combination provides the most efficient method of marketing for these types of products. Product quality, performance, value and packaging are also important differentiating factors.

Research and Development Expenditures . Research and development expenditures enable us to develop technologies and obtain patents across all categories in order to meet the needs and improve the lives of our consumers. Total research and development expenses were $2.0 billion in 2014, 2013 and 2012.

Expenditures for Environmental Compliance . Expenditures for compliance with federal, state and local environmental laws and regulations are fairly consistent from year to year and are not material to the Company. No material change is expected in fiscal year 2015.

Employees . Total number of employees is an estimate of total Company employees excluding interns, co-ops and employees of joint ventures. The number of employees includes manufacturing and non-manufacturing employees. A discussion of progress on non-manufacturing enrollment objectives is included in Note 3 to our Consolidated Financial Statements. Historical numbers include employees of discontinued operations.

| Total Number of Employees |

2014 | 118,000 |

2013 | 121,000 |

2012 | 126,000 |

2011 | 129,000 |

2010 | 127,000 |

2009 | 132,000 |

Financial Information about Foreign and Domestic Operations

Net sales in the U.S. account for approximately 35% of total net sales. No other individual country exceeds 10% of total net sales. Operations outside the U.S. are generally characterized by the same conditions discussed in the description of the business above and may be affected by additional factors including changing currency values, different rates of inflation, economic growth and political and economic uncertainties and disruptions. Our sales by geography for the fiscal years ended June 30 were as follows:

| 2014 |

| 2013 |

| 2012 |

North America (1) | 39% |

| 39% |

| 39% |

Western Europe | 18% |

| 18% |

| 19% |

Asia | 18% |

| 18% |

| 18% |

CEEMEA (2) | 15% |

| 15% |

| 14% |

Latin America | 10% |

| 10% |

| 10% |

(1) | North America includes results for the United States and Canada only. |

(2) | CEEMEA includes Central and Eastern Europe, Middle East and Africa. |

Net sales and total assets in the United States and internationally were as follows (in billions):

| United States | International |

Net Sales (for the years ended June 30) | ||

2014 | $29.4 | $53.7 |

2013 | $29.2 | $53.4 |

2012 | $28.4 | $53.6 |

|

|

|

Total Assets (June 30) | ||

2014 | $68.8 | $75.5 |

2013 | $68.3 | $71.0 |

2012 | $68.0 | $64.2 |

Item 1A. Risk Factors.

We discuss our expectations regarding future performance, events and outcomes, such as our business outlook and objectives in this Form 10-K, quarterly reports, press releases and other written and oral communications. All statements, except for historical and present factual information, are "forward-looking statements" and are based on financial data and business plans available only as of the

The Procter & Gamble Company 13

time the statements are made, which may become outdated or incomplete. We assume no obligation to update any forward-looking statements as a result of new information, future events, or other factors. Forward-looking statements are inherently uncertain and investors must recognize that events could significantly differ from our expectations.

The following discussion of "risk factors" identifies the most significant factors that may adversely affect our business, operations, financial position or future financial performance. This information should be read in conjunction with MD&A and the Consolidated Financial Statements and related Notes incorporated in this report. The following discussion of risks is not all inclusive, but is designed to highlight what we believe are important factors to consider when evaluating our expectations. These factors could cause our future results to differ from those in the forward-looking statements and from historical trends.

A change in consumer demand for our products and/or lack of market growth could have a significant impact on our business.

We are a consumer products company and rely on continued global demand for our brands and products. To achieve business goals, we must develop and sell products that appeal to consumers. This is dependent on a number of factors, including our ability to develop effective sales, advertising and marketing programs. We expect to achieve our financial targets, in part, by focusing on the most profitable businesses, biggest innovations and most important emerging markets. We also expect to achieve our financial targets, in part, by achieving disproportionate growth in developing regions. If demand for our products and/or market growth rates, in either developed or developing markets, falls substantially below expected levels or our market share declines significantly in these businesses, our volume, and consequently our results, could be negatively impacted. This could occur due to, among other things, unforeseen negative economic or political events, unexpected changes in consumer trends and habits or negative consumer responses to pricing actions.

The ability to achieve our business objectives is dependent on how well we can compete with our local and global competitors in new and existing markets and channels.

The consumer products industry is highly competitive. Across all of our categories, we compete against a wide variety of global and local competitors. As a result, there are ongoing competitive pressures in the environments in which we operate, as well as challenges in maintaining profit margins. This includes, among other things, increasing competition from mid- and lower-tier value products in both developed and developing markets. To address these challenges, we must be able to successfully respond to competitive factors, including pricing, promotional incentives and trade terms. In addition, the emergence of new sales channels may affect customer and consumer preferences, as well as market dynamics. Failure to

effectively compete in these new channels could negatively impact results.

Our ability to meet our growth targets depends on successful product, marketing and operations innovation and our ability to successfully respond to competitive innovation .

Achieving our business results depends, in part, on the successful development, introduction and marketing of new products and improvements to our equipment and manufacturing processes. Successful innovation depends on our ability to correctly anticipate customer and consumer acceptance, to obtain and maintain necessary intellectual property protections and to avoid infringing the intellectual property rights of others. We must also be able to successfully respond to technological advances made by competitors and intellectual property rights granted to competitors. Failure to do so could compromise our competitive position and impact our results.

Our businesses face cost fluctuations and pressures that could affect our business results.

Our costs are subject to fluctuations, particularly due to changes in commodity prices, raw materials, labor costs, energy costs, pension and healthcare costs and foreign exchange and interest rates. Therefore, our success is dependent, in part, on our continued ability to manage these fluctuations through pricing actions, cost saving projects and sourcing decisions, while maintaining and improving margins and market share. In addition, our financial projections include cost savings described in our announced productivity plan. Failure to deliver these savings could adversely impact our results.

We face risks that are inherent in global manufacturing that could negatively impact our business results.

We need to maintain key manufacturing and supply arrangements, including any key sole supplier and sole manufacturing plant arrangements, to achieve our cost targets. While we have business continuity and contingency plans for key manufacturing sites and the supply of raw materials, it may be impracticable to have a sufficient alternative source, particularly when the input materials are in limited supply. In addition, our strategy for global growth includes increased presence in emerging markets. Some emerging markets have greater political volatility and greater vulnerability to infrastructure and labor disruptions than established markets. Any significant disruption of manufacturing, such as labor disputes, loss or impairment of key manufacturing sites, natural disasters, acts of war or terrorism and other external factors over which we have no control, could interrupt product supply and, if not remedied, have an adverse impact on our business.

14 The Procter & Gamble Company

We rely on third parties in many aspect our business, which creates additional risk.

Due to the scale and scope of our business, we must rely on relationships with third parties for certain functions, such as our suppliers, distributors, contractors, joint venture partners or external business partners. While we have policies and procedures for managing these relationships, they inherently involve a lesser degree of control over business operations, governance and compliance, thereby potentially increasing our financial, legal, reputational and/or operational risk.

We face risks associated with having significant international operations.

We are a global company, with manufacturing operations in more than 40 countries and a significant portion of our revenue outside the U.S. Our international operations are subject to a number of risks, including, but not limited to:

• | compliance with U.S. laws affecting operations outside of the United States, such as the Foreign Corrupt Practices Act; |

• | compliance with a variety of local regulations and laws; |

• | changes in tax laws and the interpretation of those laws; |

• | changes in exchange controls and other limits on our ability to repatriate earnings from overseas; |

• | discriminatory or conflicting fiscal policies; |

• | difficulties enforcing intellectual property and contractual rights in certain jurisdictions; |

• | risk of uncollectible accounts and longer collection cycles; |

• | effective and immediate implementation of control environment processes across our diverse operations and employee base; and |

• | imposition of increased or new tariffs, quotas, trade barriers or similar restrictions on our sales outside the U.S. |

We have sizable businesses and maintain local currency cash balances in a number of foreign countries with exchange, import authorization or pricing controls, including, but not limited to, Venezuela, Argentina, China, India and Egypt. Our results of operations and/or financial condition could be adversely impacted if we are unable to successfully manage these and other risks of international operations in an increasingly volatile environment.

Fluctuations in exchange rates may have an adverse impact on our business results or financial condition.

We hold assets and incur liabilities, earn revenues and pay expenses in a variety of currencies other than the U.S. dollar. Because our consolidated financial statements are presented in U.S. dollars, the financial statements of our subsidiaries outside the U.S. are translated into U.S. dollars. Our operations outside of the U.S. generate a significant portion of our net revenue. Fluctuations in exchange rates may therefore adversely impact our business results or financial condition. See also the Results of Operations and Cash Flow, Financial Condition and Liquidity sections of the

MD&A and Note 5 to our Consolidated Financial Statements.

We face risks related to changes in the global and political economic environment, including the global capital and credit markets.

Our business is impacted by global economic conditions, which continue to be volatile. Our products are sold in more than 180 countries and territories around the world. If the global economy experiences significant disruptions, our business could be negatively impacted by reduced demand for our products related to: a slow-down in the general economy; supplier, vendor or customer disruptions resulting from tighter credit markets; and/or temporary interruptions in our ability to conduct day-to-day transactions through our financial intermediaries involving the payment to or collection of funds from our customers, vendors and suppliers.

Our objective is to maintain credit ratings that provide us with ready access to global capital and credit markets. Any downgrade of our current credit ratings by a credit rating agency could increase our future borrowing costs and impair our ability to access capital and credit markets on terms commercially acceptable to us.

We could also be negatively impacted by political issues or crises in individual countries or regions, including sovereign risk related to a default by or deterioration in the credit worthiness of local governments. For example, we could be adversely impacted by instability in the banking and governmental sectors of certain countries in the European Union or the dynamics associated with the federal and state debt and budget challenges in the U.S.

Consequently, our success will depend, in part, on our ability to manage continued global and/or economic uncertainty, especially in our significant geographies, as well as any political or economic disruption. These risks could negatively impact our overall liquidity and financing costs, as well as our ability to collect receipts due from governments, including refunds of value added taxes, and/or create significant credit risks relative to our local customers and depository institutions.

If the reputation of the Company or one or more of our brands erodes significantly, it could have a material impact on our financial results.

The Company's reputation is the foundation of our relationships with key stakeholders and other constituencies, such as customers and suppliers. In addition, many of our brands have worldwide recognition. This recognition is the result of the large investments we have made in our products over many years. The quality and safety of our products is critical to our business. Our Company also devotes significant time and resources to programs that are consistent with our corporate values and are designed to protect and preserve our reputation, such as social responsibility and environmental sustainability. If we are unable to effectively

The Procter & Gamble Company 15

manage real or perceived issues, including concerns about safety, quality, efficacy or similar matters, sentiments toward the Company or our products could be negatively impacted; our ability to operate freely could be impaired and our financial results could suffer. Our financial success is directly dependent on the success of our brands and the success of these brands can suffer if our marketing plans or product initiatives do not have the desired impact on a brand's image or its ability to attract consumers. Our results could also be negatively impacted if one of our brands suffers a substantial impediment to its reputation due to a significant product recall, product-related litigation, allegations of product tampering or the distribution and sale of counterfeit products. Widespread use of social media and networking sites by consumers has greatly increased the speed and accessibility of information dissemination. Negative or inaccurate postings or comments about the Company could generate adverse publicity that could damage the reputation of our brands. In addition, given the association of our individual products with the Company, an issue with one of our products could negatively affect the reputation of our other products, or the Company as a whole, thereby potentially hurting results.

Our ability to successfully manage ongoing organizational change could impact our business results.

Our financial targets assume a consistent level of productivity improvement. If we are unable to deliver expected productivity improvements, while continuing to invest in business growth, our financial results could be adversely impacted. We continue to execute a number of significant business and organizational changes, including acquisitions, divestitures and workforce optimization projects to support our growth strategies. We expect these types of changes, which may include many staffing adjustments as well as employee departures, to continue for the foreseeable future. Successfully managing these changes, including retention of particularly key employees, is critical to our business success. We are generally a build-from-within company and our success is dependent on identifying, developing and retaining key employees to provide uninterrupted leadership and direction for our business. This includes developing and retaining organizational capabilities in key growth markets where the depth of skilled or experienced employees may be limited and competition for these resources is intense.

Our ability to successfully manage ongoing acquisition, joint venture and divestiture activities could impact our business results.

As a company that manages a portfolio of consumer brands, our ongoing business model involves a certain level of acquisition, joint venture and divestiture activities. We must be able to successfully manage the impacts of these activities, while at the same time delivering against our business objectives. Specifically, our financial results could be adversely impacted if: 1) changes in the cash flows or other market-based assumptions cause the value of acquired

assets to fall below book value, 2) we are unable to offset the dilutive impacts from the loss of revenue associated with divested brands, or 3) we are not able to deliver the expected cost and growth synergies associated with our acquisitions and joint ventures, which could also have an impact on goodwill and intangible assets.

Our business is subject to changes in legislation, regulation and enforcement, and our ability to manage and resolve pending legal matters in the U.S. and abroad.

Changes in laws, regulations and related interpretations, including changes in accounting standards, taxation requirements and increased enforcement actions and penalties may alter the environment in which we do business. The increasingly complex and rapidly changing legal and regulatory environment creates additional challenges for our ethics and compliance programs. Our ability to continue to meet these challenges could have an impact on our legal, reputational and business risk.

As a U.S.-based multinational company, we are subject to tax regulations in the U.S. and multiple foreign jurisdictions, some of which are interdependent. For example, certain income that is earned and taxed in countries outside the U.S. is not taxed in the U.S., provided those earnings are indefinitely reinvested outside the U.S. If these or other tax regulations should change, our financial results could be impacted. For example, there are increasing calls in the U.S. from members of leadership in both major U.S. political parties for "comprehensive tax reform" which may significantly change the income tax rules that are applicable to U.S. domiciled corporations, such as P&G. It is very difficult to assess whether the overall effect of such potential legislation would be cumulatively positive or negative for our earnings and cash flows, but such changes could significantly impact our financial results.

Our ability to manage regulatory, environmental, tax (including, but not limited to, any audits or other investigations) and legal matters (including, but not limited to, product liability, patent and other intellectual property matters) and to resolve pending legal matters without significant liability may materially impact our results of operations and financial position. Furthermore, if pending legal matters, including the competition law and antitrust investigations described in Note 11 to our Consolidated Financial Statements, result in fines or costs in excess of the amounts accrued to date, that could materially impact our results of operations and financial position.

A significant change in customer relationships or in customer demand for our products could have a significant impact on our business.

We sell most of our products via retail customers, which consist of mass merchandisers, grocery stores, membership club stores, drug stores, department stores, salons, distributors, e-commerce and high-frequency stores. Our success is dependent on our ability to successfully manage relationships with our retail trade customers. This includes

16 The Procter & Gamble Company

our ability to offer trade terms that are acceptable to our customers and are aligned with our pricing and profitability targets. Our business could suffer if we cannot reach agreement with a key customer based on our trade terms and principles. Our business would be negatively impacted if a key customer were to significantly reduce the inventory level of our products or experience a significant business disruption.

Consolidation among our retail customers could also create significant cost and margin pressure and lead to more complexity across broader geographic boundaries for both us and our key retailers. This would be particularly challenging if major customers are addressing local trade pressures, local law and regulation changes or financial distress.

A breach of information security, including a cybersecurity breach or failure of one or more key information technology systems, networks, processes, associated sites or service providers could have a material adverse impact on our business or reputation.

We rely extensively on information technology (IT) systems, networks and services, including internet sites, data hosting and processing facilities and tools and other hardware, software and technical applications and platforms, some of which are managed, hosted, provided and/or used by third-parties or their vendors, to assist in conducting our business. The various uses of these IT systems, networks and services include, but are not limited to:

• | ordering and managing materials from suppliers; |

• | converting materials to finished products; |

• | shipping products to customers; |

• | marketing and selling products to consumers; |

• | collecting and storing customer, consumer, employee, investor and other stakeholder information and personal data; |

• | processing transactions; |

• | summarizing and reporting results of operations; |

• | hosting, processing and sharing confidential and proprietary research, business plans and financial information; |

• | complying with regulatory, legal or tax requirements; |

• | providing data security; and |

• | handling other processes necessary to manage our business. |

Numerous and evolving cybersecurity threats, including advanced persistent threats, pose a potential risk to the security of our IT systems, networks and services, as well as the confidentiality, availability and integrity of our data. The Company has made investments seeking to address these threats, including monitoring of networks and systems,

employee training and security policies for the Company and its third-party providers. However, because the techniques used in these attacks change frequently and may be difficult to detect for periods of time, we may face difficulties in anticipating and implementing adequate preventative measures. If the IT systems, networks or service providers we rely upon fail to function properly, or if we or one of our third-party providers suffer a loss or disclosure of our business or stakeholder information, due to any number of causes, ranging from catastrophic events or power outages to improper data handling or security breaches, and our business continuity plans do not effectively address these failures on a timely basis, we may be exposed to reputational, competitive and business harm as well as litigation and regulatory action. The costs and operational consequences of responding to breaches and implementing remediation measures could be significant.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

In the U.S., we own and operate 32 manufacturing sites located in 22 different states or territories. In addition, we own and operate 105 manufacturing sites in 40 other countries. Many of the domestic and international sites manufacture products for multiple businesses. Beauty products are manufactured at 42 of these locations; Grooming products at 16; Fabric Care and Home Care products at 53; Baby, Feminine and Family Care products at 48; and Health Care products at 21. Management believes that the Company's production facilities are adequate to support the business and that the properties and equipment have been well maintained.

Item 3. Legal Proceedings.

The Company is subject, from time to time, to certain legal proceedings and claims arising out of our business, which cover a wide range of matters, including antitrust and trade regulation, product liability, advertising, contracts, environmental issues, patent and trademark matters, labor and employment matters and tax. See Note 11 to our Consolidated Financial Statements for information on certain legal proceedings for which there are contingencies.

This item should be read in conjunction with the Company's Risk Factors in Part I, Item 1A for additional information.

Item 4. Mine Safety Disclosure.

Not Applicable.

The Procter & Gamble Company 17

Executive Officers of the Registrant

The names, ages and positions held by the Executive Officers of the Company on August 8, 2014 , are:

Name |

| Position |

| Age |

| First Elected to Officer Position | |

A. G. Lafley |

| Chairman of the Board, President and Chief Executive Officer |

| 67 | |

| 2013 |

|

| Director since May 23, 2013 |

|

|

|

| |

|

|

|

| ||||

Jon Moeller |

| Chief Financial Officer |

| 50 | |

| 2009 |

|

|

|

|

|

|

| |

Giovanni Ciserani |

| Group President - Global Fabric and Home Care |

| 52 | |

| 2013 |

|

|

|

| ||||

Mary Lynn Ferguson-McHugh |

| Group President - Europe |

| 54 | |

| 2014 |

|

|

|

|

|

|

| |

Melanie Healey |

| Group President - North America |

| 53 | |

| 2013 |

|

|

|

| ||||

Deborah A. Henretta |

| Group President - Global Beauty |

| 53 | |

| 2013 |

|

|

|

| ||||

Martin Riant |

| Group President - Global Baby, Feminine and Family Care |

| 55 | |

| 2013 |

|

|

|

|

|

|

| |

David Taylor |

| Group President - Global Health and Grooming |

| 56 | |

| 2013 |

|

|

|

|

|

|

| |

Filippo Passerini |

| Group President - Global Business Services and Chief Information Officer |

| 57 | |

| 2003 |

|

|

|

|

|

|

| |

Mark Biegger |

| Chief Human Resources Officer |

| 52 | |

| 2012 |

|

|

|

|

|

|

| |

Linda Clement-Holmes |

| Global Information & Decision Solutions Officer |

| 52 | |

| 2014 |

|

|

|

|

|

|

| |

Tarek Farahat |

| President - Latin America |

| 50 | |

| 2014 |

|

|

|

|

|

|

| |

Kathleen B. Fish |

| Chief Technology Officer |

| 57 | |

| 2014 |

|

|

|

| ||||

Hatsunori Kiriyama |

| President - Asia |

| 51 | |

| 2014 |

|

|

|

| ||||

Deborah P. Majoras |

| Chief Legal Officer and Secretary |

| 50 | |

| 2010 |

|

|

|

| ||||

Marc S. Pritchard |

| Global Brand Building Officer |

| 54 | |

| 2008 |

|

|

|

| ||||

Mohamed Samir |

| President - India, Middle East and Africa |

| 47 | |

| 2014 |

|

|

|

|

|

|

| |

Valarie Sheppard |

| Senior Vice President, Comptroller & Treasurer |

| 50 | |

| 2005 |

|

|

|

|

|

|

| |

Yannis Skoufalos |

| Global Product Supply Officer |

| 57 | |

| 2011 |

|

|

|

|

|

|

| |

Shannan Stevenson |

| President - Greater China |

| 49 | |

| 2014 |

|

|

|

|

|

|

| |

Carolyn M. Tastad |

| Global Customer Business Development Officer |

| 53 | |

| 2014 |

18 The Procter & Gamble Company

All the Executive Officers named above, excluding Mr. Lafley, have been employed by the Company for more than the past five years. Mr. Lafley is Chairman of the Board, President and Chief Executive Officer of the Company and was reappointed to this position on May 23, 2013. Mr. Lafley originally joined the Company in 1977 and held positions of increasing responsibility, in the U.S. and internationally, until he was elected President and Chief Executive Officer in 2000, a position he held until June 30, 2009. On July 1, 2002, Mr. Lafley was elected Chairman of the Board, a position he held until January 2010, at which time he retired from the Company. During the past five years, in addition to his roles as a Company employee, Mr. Lafley served as a consultant to the Company and as a member of the boards of directors of public companies Dell, Inc. and General Electric Company. He no longer serves on these boards. After his initial retirement from the Company in 2010, he served as a Senior Advisor at Clayton, Dubilier & Rice, LLC, a private equity partnership, and was appointed by President Obama to serve on The President's Council on Jobs and Competitiveness. Mr. Lafley consulted with a number of Fortune 50 companies on business and innovation strategy. He also advised on CEO succession and executive leadership development, and coached experienced, new and potential CEOs. He currently serves on the board of directors of Legendary Pictures, LLC (a film production company).

The Procter & Gamble Company 19

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

ISSUER PURCHASES OF EQUITY SECURITIES

Period |

| Total Number of Shares Purchased (1 ) |

| Average Price Paid per Share (2) |

| Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs (3) |

| Approximate Dollar Value of Shares That May Yet be Purchased Under our Share Repurchase Program (3) |

4/1/2014 - 4/30/2014 |

| 6,180,000 |

| $80.90 |

| 6,180,000 |

| (3) |

5/1/2014 - 5/31/2014 |

| - |

| - |

| - |

| (3) |

6/1/2014 - 6/30/2014 |

| - |

| - |

| - |

| (3) |

(1 | ) | The total number of shares purchased was 6,180,000 for the quarter. All transactions were made in the open market with large financial institutions. This table excludes shares withheld from employees to satisfy minimum tax withholding requirements on option exercises and other equity-based transactions. The Company administers cashless exercises through an independent third party and does not repurchase stock in connection with cashless exercises. |

(2 | ) | Average price paid per share is calculated on a settlement basis and excludes commission. |

(3 | ) | On April 23, 2014, the Company stated that fiscal year 2014 share repurchases to reduce Company shares outstanding were estimated to be approximately $6 billion. This does not include any purchases under the Company's compensation and benefit plans. The share repurchases were authorized pursuant to a resolution issued by the Company's Board of Directors and were financed through a combination of operating cash flows and issuance of long-term and short-term debt. The total dollar value of shares purchased under the share repurchase plan was $6.0 billion. The share repurchase plan ended on June 30, 2014. |

Additional information required by this item can be found in Part III, Item 12 of this Form 10-K.

Shareholder Return Performance Graphs

Market and Dividend Information

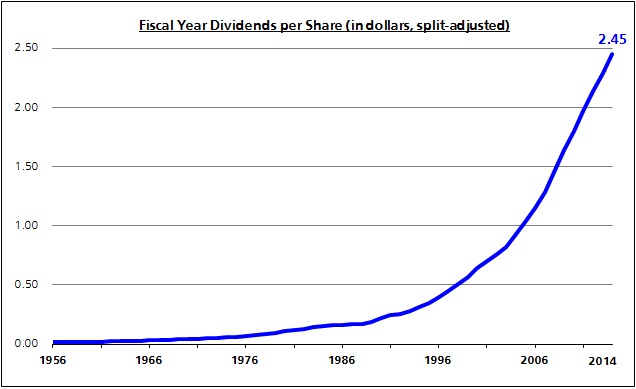

P&G has been paying a dividend for 124 consecutive years since its incorporation in 1890 and has increased its dividend for 58 consecutive years at an annual compound average rate of over 9%.

(in dollars; split-adjusted) | 1956 | 1966 | 1976 | 1986 | 1996 | 2006 | 2014 | |||||||

Dividends per Share | $ | 0.01 | $ | 0.03 | $ | 0.06 | $ | 0.16 | $ | 0.40 | $ | 1.15 | $ | 2.45 |

20 The Procter & Gamble Company

QUARTERLY DIVIDENDS

Quarter Ended | 2013-2014 | |

| 2012-2013 | | ||

September 30 | $ | 0.6015 | |

| $ | 0.5620 | |

December 31 | 0.6015 | |

| 0.5620 | | ||

March 31 | 0.6015 | |

| 0.5620 | | ||

June 30 | 0.6436 | |

| 0.6015 | | ||

COMMON STOCK PRICE RANGE

| 2013-2014 |

| 2012 - 2013 | ||||||||||||

Quarter Ended | High |

| Low |

| High |

| Low | ||||||||

September 30 | $ | 82.40 | |

| $ | 73.61 | |

| $ | 69.97 | |

| $ | 60.78 | |

December 31 | 85.82 | |

| 75.20 | |

| 70.99 | |

| 65.84 | | ||||

March 31 | 81.70 | |

| 75.26 | |

| 77.82 | |

| 68.35 | | ||||

June 30 | 82.98 | |

| 78.43 | |

| 82.54 | |

| 75.10 | | ||||

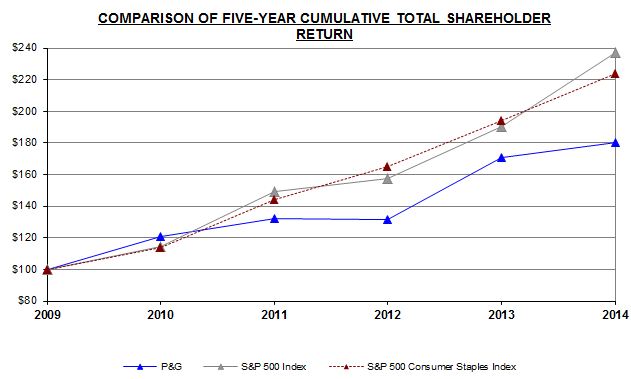

SHAREHOLDER RETURN

The following graph compares the cumulative total return of P&G's common stock for the 5-year period ending June 30, 2014, against the cumulative total return of the S&P 500 Stock Index (broad market comparison) and the S&P 500 Consumer Staples Index (line of business comparison). The graph and table assume $100 was invested on June 30, 2009, and that all dividends were reinvested.

| Cumulative Value of $100 Investment, through June 30 | |||||||||||||||||

Company Name/Index | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | ||||||||||||

P&G | $ | 100 | | $ | 121 | | $ | 132 | | $ | 132 | | $ | 171 | | $ | 180 | |

S&P 500 Index | 100 | | 114 | | 150 | | 158 | | 190 | | 237 | | ||||||

S&P 500 Consumer Staples Index | 100 | | 114 | | 144 | | 165 | | 194 | | 224 | | ||||||

The Procter & Gamble Company 21

Item 6. Selected Financial Data.

The information required by this item is incorporated by reference to Note 1 and Note 12 to our Consolidated Financial Statements.

Financial Summary (Unaudited)

Amounts in millions, except per share amounts | 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 |

| 2009 | ||||||||||||

Net sales | $ | 83,062 | |

| $ | 82,581 | |

| $ | 82,006 | |

| $ | 79,385 | |

| $ | 75,785 | |

| $ | 73,565 | |

Gross profit | 40,602 | |

| 41,190 | |

| 40,595 | |

| 40,551 | |

| 39,663 | |

| 36,882 | | ||||||

Operating income | 15,288 | |

| 14,330 | |

| 13,035 | |

| 15,233 | |

| 15,306 | |

| 14,819 | | ||||||

Net earnings from continuing operations | 11,707 | |

| 11,301 | |

| 9,150 | |

| 11,523 | |

| 10,573 | |

| 10,414 | | ||||||

Net earnings from discontinued operations | 78 | |

| 101 | |

| 1,754 | |

| 404 | |

| 2,273 | |

| 3,108 | | ||||||

Net earnings attributable to Procter & Gamble | 11,643 | |

| 11,312 | |

| 10,756 | |

| 11,797 | |

| 12,736 | |

| 13,436 | | ||||||

Net Earnings margin from continuing operations | 14.1 | % |

| 13.7 | % |

| 11.2 | % |

| 14.5 | % |

| 14.0 | % |

| 14.2 | % | ||||||

Basic net earnings per common share (1) : |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Earnings from continuing operations | $ | 4.16 | |

| $ | 4.00 | |

| $ | 3.18 | |

| $ | 3.98 | |

| $ | 3.53 | |

| $ | 3.44 | |

Earnings from discontinued operations | 0.03 | |

| 0.04 | |

| 0.64 | |

| 0.14 | |

| 0.79 | |

| 1.05 | | ||||||

Basic net earnings per common share | 4.19 | |

| 4.04 | |

| 3.82 | |

| 4.12 | |

| 4.32 | |

| 4.49 | | ||||||

Diluted net earnings per common share (1) : |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Earnings from continuing operations | $ | 3.98 | |

| $ | 3.83 | |

| $ | 3.06 | |

| $ | 3.80 | |

| $ | 3.38 | |

| $ | 3.27 | |

Earnings from discontinued operations | 0.03 | |

| 0.03 | |

| 0.60 | |

| 0.13 | |

| 0.73 | |

| 0.99 | | ||||||

Diluted net earnings per common share | 4.01 | |

| 3.86 | |

| 3.66 | |

| 3.93 | |

| 4.11 | |

| 4.26 | | ||||||

Dividends per common share | $ | 2.45 | |

| $ | 2.29 | |

| $ | 2.14 | |

| $ | 1.97 | |

| $ | 1.80 | |

| $ | 1.64 | |

Research and development expense | $ | 2,023 | |

| $ | 1,980 | |

| $ | 1,987 | |

| $ | 1,940 | |

| $ | 1,888 | |

| $ | 1,802 | |

Advertising expense | 9,236 | |

| 9,612 | |

| 9,222 | |

| 9,086 | |

| 8,338 | |

| 7,338 | | ||||||

Total assets | 144,266 | |

| 139,263 | |

| 132,244 | |

| 138,354 | |

| 128,172 | |

| 134,833 | | ||||||

Capital expenditures | 3,848 | |

| 4,008 | |

| 3,964 | |

| 3,306 | |

| 3,067 | |

| 3,238 | | ||||||

Long-term debt | 19,811 | |

| 19,111 | |

| 21,080 | |

| 22,033 | |

| 21,360 | |

| 20,652 | | ||||||

Shareholders' equity | 69,976 | |

| 68,709 | |

| 64,035 | |

| 68,001 | |

| 61,439 | |

| 63,382 | | ||||||

(1) Basic net earnings per common share and diluted net earnings per common share are calculated based on net earnings attributable to Procter & Gamble.

22 The Procter & Gamble Company

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Management's Discussion and Analysis

Forward-Looking Statements

Certain statements in this report, other than historical and present factual information, including estimates, projections, statements relating to our business plans, objectives and expected operating results and the assumptions upon which those statements are based, are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements may appear throughout this report, including, without limitation, in the following sections: "Management's Discussion and Analysis" and "Risk Factors." These forward-looking statements generally are identified by the words "believe," "project," "expect," "anticipate," "estimate," "intend," "strategy," "future," "opportunity," "plan," "may," "should," "will," "would," "will be," "will continue," "will likely result" and similar expressions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties which may cause actual results to differ materially from the forward-looking statements. A detailed discussion of risks and uncertainties that could cause actual results and events to differ materially from such forward-looking statements is included in the section titled "Economic Conditions, Challenges and Risks" and the section titled "Risk Factors" (Item 1A of this Form 10-K). Forward-looking statements are made as of the date of this report and we undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events or otherwise.

The following Management's Discussion and Analysis (MD&A) is intended to provide the reader with an understanding of P&G's financial condition, results of operations and cash flows by focusing on changes in certain key measures from year to year. MD&A is provided as a supplement to, and should be read in conjunction with, our Consolidated Financial Statements and accompanying Notes. MD&A is organized in the following sections:

• | Overview |

• | Summary of 2014 Results |

• | Economic Conditions, Challenges and Risks |

• | Results of Operations |

• | Segment Results |

• | Cash Flow, Financial Condition and Liquidity |

• | Significant Accounting Policies and Estimates |

• | Other Information |

Throughout MD&A, we refer to measures used by management to evaluate performance, including unit volume growth, net sales and net earnings. We also refer to a

number of financial measures that are not defined under accounting principles generally accepted in the United States of America (U.S. GAAP), including organic sales growth, core earnings per share (Core EPS), free cash flow and free cash flow productivity. Organic sales growth is net sales growth excluding the impacts of foreign exchange, acquisitions and divestitures. Core EPS is diluted net earnings per share from continuing operations excluding certain specified charges and gains. Free cash flow is operating cash flow less capital spending. Free cash flow productivity is the ratio of free cash flow to net earnings. We believe these measures provide our investors with additional information about our underlying results and trends, as well as insight to some of the metrics used to evaluate management. The explanation at the end of MD&A provides more details on the use and derivation of these measures.

Management also uses certain market share and market consumption estimates to evaluate performance relative to competition despite some limitations on the availability and comparability of share and consumption information. References to market share and market consumption in MD&A are based on a combination of vendor-reported consumption and market size data, as well as internal estimates. All market share references represent the percentage of sales in dollar terms on a constant currency basis of our products, relative to all product sales in the category and are measured on an annual basis versus the prior 12 month period. References to competitive activity include promotional and product initiatives from our competitors.

OVERVIEW

P&G is a global leader in fast moving consumer goods focused on providing branded consumer packaged goods of superior quality and value to our consumers around the world. Our products are sold in more than 180 countries and territories primarily through mass merchandisers, grocery stores, membership club stores, drug stores, department stores, salons, distributors, e-commerce and high-frequency stores. We continue to expand our presence in other channels, including perfumeries and pharmacies. We have on-the-ground operations in approximately 70 countries.

Our market environment is highly competitive with global, regional and local competitors. In many of the markets and industry segments in which we sell our products, we compete against other branded products as well as retailers' private-label brands. Additionally, many of the product segments in which we compete are differentiated by price tiers (referred to as super-premium, premium, mid-tier and value-tier products). We are well positioned in the industry segments and markets in which we operate, often holding a leadership or significant market share position.

The Procter & Gamble Company 23

ORGANIZATIONAL STRUCTURE

Our organizational structure is comprised of Global Business Units (GBUs), Global Operations, Global Business Services (GBS) and Corporate Functions (CF).

Global Business Units

Under U.S. GAAP, the GBUs are aggregated into five reportable segments: Beauty; Grooming; Health Care; Fabric Care and Home Care; and Baby, Feminine and Family Care. The GBUs are responsible for developing overall brand strategy, new product upgrades and innovations and marketing plans. The following provides additional detail on our reportable segments and the key product categories and brand composition within each segment.

Reportable Segment | % of Net Sales* | % of Net Earnings* | GBUs (Categories) | Billion Dollar Brands |

Beauty | 24% | 23% | Beauty Care (Antiperspirant and Deodorant, Cosmetics, Personal Cleansing, Skin Care); Hair Care and Color; Prestige; Salon Professional | Head & Shoulders, Olay, Pantene, SK-II, Wella |

Grooming | 10% | 17% | Shave Care (Electronic Hair Removal, Female Blades & Razors, Male Blades & Razors, Pre- and Post-Shave Products, Other Shave Care) | Fusion, Gillette, Mach3, Prestobarba |

Health Care | 9% | 9% | Personal Health Care (Gastrointestinal, Rapid Diagnostics, Respiratory, Vitamins/Minerals/Supplements, Other Personal Health Care); Oral Care (Toothbrush, Toothpaste, Other Oral Care) | Crest, Oral-B, Vicks |

Fabric Care and Home Care | 32% | 26% | Fabric Care (Laundry Additives, Fabric Enhancers, Laundry Detergents); Home Care (Air Care, Dish Care, P&G Professional, Surface Care); Personal Power (Batteries) | Ariel, Dawn, Downy, Duracell, Febreze, Gain, Tide |

Baby, Feminine and Family Care | 25% | 25% | Baby Care (Baby Wipes, Diapers and Pants); Feminine Care (Adult Incontinence, Feminine Care); Family Care (Paper Towels, Tissues, Toilet Paper) | Always, Bounty, Charmin, Pampers |

* Percent of net sales and net earnings from continuing operations for the year ended June 30, 2014 (excluding results held in Corporate).

Recent Developments: On July 31, 2014 the Company completed the divestiture of its pet care operations in North America, Latin America, and other selected countries to Mars, Incorporated (Mars) for $2.9 billion in an all-cash transaction. The gain or loss related to this transaction is not expected to be material and will be included in fiscal 2015 results. The European Union countries are not included in the agreement with Mars. The Company is pursuing alternate plans to sell its Pet Care business in these markets. In accordance with the applicable accounting guidance for the disposal of long-lived assets, the results of our Pet Care business are presented as discontinued operations and, as such, have been excluded from continuing operations and from segment results for all periods presented.

Beauty: We are a global market leader in the beauty category. Most of the beauty markets in which we compete are highly fragmented with a large number of global and local competitors. We compete in beauty care, hair care and color and prestige. In beauty care, we offer a wide variety of products, ranging from deodorants to cosmetics to skin care, such as our Olay brand, which is the top facial skin care brand in the world with over 8% global market share. In hair care and color, we compete in both the retail and salon professional channels. We are the global market leader in the retail hair care and color market with over 20% global market share primarily behind our Pantene and Head &

Shoulders brands. In the prestige channel, we compete primarily with our prestige fragrances behind Dolce & Gabbana, Gucci and Hugo Boss fragrance brands and the SK-II brand.

Grooming: We are the global market leader in the blades and razors market globally. Our global blades and razors market share is approximately 70%, primarily behind the Gillette franchise including Fusion, Mach3, Prestobarba and Venus. Our electronic hair removal devices, such as electric razors and epilators, are sold under the Braun brand in a number of markets around the world where we compete against both global and regional competitors. We hold over 20% of the male shavers market and over 40% of the female epilators market.

Health Care: We compete in oral care and personal health care. In oral care, there are several global competitors in the market and we have the number two market share position with approximately 20% global market share. In personal health care, we are a top ten competitor in a large, highly fragmented industry behind respiratory treatments (Vicks brand) and nonprescription heartburn medications (Prilosec OTC brand). Nearly all of our sales outside the U.S in personal health are generated through the PGT Healthcare partnership with Teva Pharmaceuticals Ltd.

24 The Procter & Gamble Company

Fabric Care and Home Care: This segment is comprised of a variety of fabric care products, including: laundry detergents, additives and fabric enhancers; home care products, including dishwashing liquids and detergents, surface cleaners and air fresheners; and batteries. In fabric care, we generally have the number one or number two share position in the markets in which we compete and are the global market leader, with over 25% global market share, primarily behind our Tide, Ariel and Downy brands. Our global home care market share is approximately 20% across the categories in which we compete. In batteries, we have over 25% global battery market share, behind our Duracell brand.

Baby, Feminine and Family Care: In baby care, we compete mainly in diapers, pants and baby wipes, with over 30% global market share. We are the number one or number two baby care competitor in most of the key markets in which we compete, primarily behind Pampers, the Company's largest brand, with annual net sales of more than $10 billion. We are the global market leader in the feminine care category with over 30% global market share, primarily behind Always. Our family care business is predominantly a North American business comprised largely of the Bounty paper towel and Charmin toilet paper brands. U.S. market shares are approximately 45% for Bounty and over 25% for Charmin.

Global Operations

Global Operations is comprised of our Sales and Market Operations (SMO), which is responsible for developing and executing go-to-market plans at the local level. The SMO includes dedicated retail customer, trade channel and country-specific teams. Through June 30, 2014, it was organized along five geographic regions: North America, Western Europe, Central & Eastern Europe/Middle East/Africa (CEEMEA), Latin America and Asia, which is comprised of Japan, Greater China and ASEAN/Australia/India/Korea (AAIK). Throughout MD&A, we reference business results in developing markets, which we define as the aggregate of CEEMEA, Latin America, AAIK and Greater China, and developed markets, which are comprised of North America, Western Europe and Japan. Effective July 1, 2014, our SMO reorganized under five revised regions, comprised of North America, Europe, Latin America, Asia, and India/Middle East/Africa (IMEA).

Global Business Services

GBS provides technology, processes and standard data tools to enable the GBUs and the SMO to better understand the business and better serve consumers and customers. The GBS organization is responsible for providing world-class solutions at a low cost and with minimal capital investment.

Corporate Functions

CF provides Company-level strategy and portfolio analysis, corporate accounting, treasury, tax, external relations,

governance, human resources and legal, as well as other centralized functional support.

STRATEGIC FOCUS

We are focused on strategies that we believe are right for the long-term health of the Company with the objective of delivering total shareholder return in the top one-third of our peer group.

We are focusing our resources on our leading, most profitable categories and markets:

• | Strengthening core categories, such as baby care and fabric care, and core markets, such as the U.S., to grow these businesses. |

• | Investing in developing markets on the categories and countries with the largest size of prize and highest likelihood of winning. |

• | Narrowing and refocusing the Company's portfolio to compete in categories and brands that are structurally attractive and that play to P&G strengths and looking at alternatives to partner, divest or discontinue the balance. This will enable us to allocate resources to leading brands - marketed in the right set of countries, channels, and customers - where the size of the prize and probability of winning is highest. |

Innovation has always been - and continues to be - P&G's lifeblood. To consistently win with consumers around the world across price tiers and preferences and to consistently win versus our best competitors, each P&G product category needs a full portfolio of innovation, including a mix of commercial programs, product improvements and game-changing innovations.

Productivity is a core strength for P&G, which creates flexibility to fund our growth efforts and deliver our financial commitments. We have taken significant steps to accelerate productivity and savings across all elements of costs, including cost of goods sold, marketing expense and non-manufacturing overhead.

Finally, we are focused on improving execution and operating discipline in everything we do. Operating discipline and execution have always been - and must continue to be - core capabilities and competitive advantages for P&G.

At current market growth rates, the Company expects the consistent delivery of the following annual financial targets will result in total shareholder returns in the top third of the competitive peer group:

• | Organic sales growth modestly above market growth rates in the categories and geographies in which we compete; |

• | Core EPS growth of high single digits; and |

• | Free cash flow productivity of 90% or greater. |

The Procter & Gamble Company 25

SUMMARY OF 2014 RESULTS

Amounts in millions, except per share amounts | 2014 |

| Change vs. Prior Year |

| 2013 |

| Change vs. Prior Year |

| 2012 | ||||||

Net sales | $ | 83,062 | |

| 1% |

| $ | 82,581 | |

| 1% |

| $ | 82,006 | |

Operating income | 15,288 | |

| 7% |

| 14,330 | |

| 10% |

| 13,035 | | |||

Net earnings from continuing operations | 11,707 | |

| 4% |

| 11,301 | |

| 24% |

| 9,150 | | |||

Net earnings from discontinued operations | 78 | |

| (23)% |

| 101 | |

| (94)% |

| 1,754 | | |||

Net earnings attributable to Procter & Gamble | 11,643 | |

| 3% |

| 11,312 | |

| 5% |

| 10,756 | | |||

Diluted net earnings per common share | 4.01 | |

| 4% |

| 3.86 | |

| 5% |

| 3.66 | | |||

Diluted net earnings per share from continuing operations | 3.98 | |

| 4% |

| 3.83 | |

| 25% |

| 3.06 | | |||

Core earnings per common share | 4.22 | |

| 5% |

| 4.02 | |

| 6% |

| 3.79 | | |||

• | Net sales increased 1% to $83.1 billion including a negative 2% impact from foreign exchange. |

◦ | Organic sales increased 3%. |

◦ | Unit volume increased 3%. Volume grew mid-single digits for Fabric Care and Home Care and Baby, Feminine and Family Care. Volume increased low single digits for Grooming and Health Care. Volume was unchanged for Beauty. |

• | Net earnings attributable to Procter & Gamble were $11.6 billion, an increase of $331 million or 3% versus the prior year period. |

◦ | Net earnings from continuing operations increased $406 million or 4% largely due to net sales growth and net earnings margin expansion behind reduced selling, general and administrative costs (SG&A), partially offset by gross margin contraction. Foreign exchange impacts negatively impacted net earnings by approximately 9%. |

◦ | Net earnings from discontinued operations decreased $23 million due to reduced earnings in Pet Care from ongoing impacts of prior year product recalls. |

• | Diluted net earnings per share increased 4% to $4.01. |

◦ | Diluted net earnings per share from continuing operations increased 4% to $3.98 |

◦ | Core EPS increased 5% to $4.22. |

• | Cash flow from operating activities was $14.0 billion. |

◦ | Free cash flow was $10.1 billion. |

◦ | Free cash flow productivity was 86%. |

ECONOMIC CONDITIONS, CHALLENGES AND RISKS

We discuss expectations regarding future performance, events and outcomes, such as our business outlook and objectives, in annual and quarterly reports, press releases and other written and oral communications. All such statements, except for historical and present factual information, are "forward-looking statements" and are based on financial data and our business plans available only as of the time the statements are made, which may become out-of-date or incomplete. We assume no obligation to update any

forward-looking statements as a result of new information, future events or other factors. Forward-looking statements are inherently uncertain and investors must recognize that events could be significantly different from our expectations. For more information on risks that could impact our results, refer to Item 1A Risk Factors in this 10-K.

Ability to Achieve Business Plans . We are a consumer products company and rely on continued demand for our brands and products. To achieve business goals, we must develop and sell products that appeal to consumers and retail trade customers. Our continued success is dependent on innovation with respect to both products and operations and on the continued positive reputations of our brands. This means we must be able to obtain and maintain patents and trademarks and respond to technological advances and patents granted to competition. Our success is also dependent on effective sales, advertising and marketing programs in a more fast-paced and rapidly changing environment. Our ability to innovate and execute in these areas will determine the extent to which we are able to grow existing net sales and volume profitably, especially with respect to the product categories and geographic markets (including developing markets) in which we have chosen to focus. There are high levels of competitive activity in the markets in which we operate. To address these challenges, we must respond to competitive factors, including pricing, promotional incentives, trade terms and product initiatives. We must manage each of these factors, as well as maintain mutually beneficial relationships with our key customers, in order to effectively compete and achieve our business plans.

As a company that manages a portfolio of consumer brands, our ongoing business model involves a certain level of ongoing acquisition, divestiture and joint venture activities. We must be able to successfully manage the impacts of these activities, while at the same time delivering against base business objectives.

Daily conduct of our business also depends on our ability to maintain key information technology systems, including systems operated by third-party suppliers and to maintain security over our data.

26 The Procter & Gamble Company

Cost Pressures . Our costs are subject to fluctuations, particularly due to changes in commodity prices, raw materials, labor costs, foreign exchange and interest rates. Therefore, our success is dependent, in part, on our continued ability to manage these fluctuations through pricing actions, cost savings projects, sourcing decisions and certain hedging transactions, as well as ongoing productivity improvements. We also must manage our debt and currency exposure, especially in certain countries with currency exchange controls, such as Venezuela, China, India, Egypt and Argentina. We need to maintain key manufacturing and supply arrangements, including sole supplier and manufacturing plant arrangements, and successfully manage any disruptions at Company manufacturing sites. We must implement, achieve and sustain cost improvement plans, including our established outsourcing relationships and those related to general overhead and workforce optimization. Successfully managing these changes, including identifying, developing and retaining key employees, is critical to our success.

Global Economic Conditions . Demand for our products has a correlation to global macroeconomic factors. The current macroeconomic factors remain dynamic. Economic changes, terrorist activity, political unrest and natural disasters may result in business interruption, inflation, deflation or decreased demand for our products. Our success will depend, in part, on our ability to manage continued global political and/or economic uncertainty, especially in our significant geographic markets, due to terrorist and other hostile activities or natural disasters. We could also be negatively impacted by a global, regional or national economic crisis, including sovereign risk in the event of a deterioration in the credit worthiness of, or a default by local governments, resulting in a disruption of credit markets. Such events could negatively impact our ability to collect receipts due from governments, including refunds of value added taxes, create significant credit risks relative to our local customers and depository institutions and/or negatively impact our overall liquidity. Additionally, changes in exchange controls and other limits could impact our ability to repatriate earnings from overseas.

Regulatory Environment . Changes in laws, regulations and the related interpretations may alter the environment in which we do business. This includes changes in environmental, competitive and product-related laws, as well as changes in accounting standards and tax laws or the enforcement thereof. Our ability to manage regulatory, tax and legal matters (including, but not limited to, product liability, patent and other intellectual property matters) and to resolve pending legal matters within current estimates may impact our results.

RESULTS OF OPERATIONS

The key metrics included in our discussion of our consolidated results of operations include net sales, gross margin, selling, general and administrative expenses (SG&A), other non-operating items and income taxes. The

primary factors driving year-over-year changes in net sales include overall market growth in the categories in which we compete, product initiatives, the level of initiatives and other activities by competitors, geographic expansion and acquisition and divestiture activity, all of which drive changes in our underlying unit volume, as well as pricing actions (which can also indirectly impact volume), changes in product and geographic mix and foreign currency impacts on sales outside the U.S.

Most of our cost of products sold and SG&A are to some extent variable in nature. Accordingly, our discussion of these operating costs focuses primarily on relative margins rather than the absolute year-over-year changes in total costs. The primary drivers of changes in gross margin are input costs (energy and other commodities), pricing impacts, geographic mix (for example, gross margins in developed markets are generally higher than in developing markets for similar products), product mix (for example, the Beauty segment has higher gross margins than the Company average), foreign exchange rate fluctuations (in situations where certain input costs may be tied to a different functional currency than the underlying sales), the impacts of manufacturing savings projects and to a lesser extent scale impacts (for costs that are fixed or less variable in nature). The primary drivers of SG&A are marketing-related costs and overhead costs. Marketing-related costs are primarily variable in nature, although we do achieve some level of scale benefit over time due to overall growth and other marketing efficiencies. Overhead costs are also variable in nature, but on a relative basis, less so than marketing costs due to our ability to leverage our organization and systems infrastructures to support business growth. Accordingly, we generally experience more scale-related impacts for these costs.

The Company is in the midst of a productivity and cost savings plan to reduce costs in the areas of supply chain, research and development, marketing and overhead expenses. The plan is designed to accelerate cost reductions by streamlining management decision making, manufacturing and other work processes to fund the Company's growth strategy. The Company expects to incur in excess of $4.5 billion in before-tax restructuring costs over a five-year period (fiscal 2012 through fiscal 2016) as part of this plan. Overall, the costs and other non-manufacturing enrollment reductions are expected to deliver in excess of $ 2.8 billion in annual gross before-tax savings (see Note 3 to our Consolidated Financial Statements).

Net Sales

Fiscal year 2014 compared with fiscal year 2013

Net sales increased 1% to $83.1 billion in 2014 on a 3% increase in unit volume versus the prior year period. Fabric Care and Home Care along with Baby, Feminine and Family Care volume grew mid-single digits. Grooming and Health Care volume grew low single digits. Beauty volume was unchanged. Volume increased low single digits in developed regions and grew mid-single digits in developing regions.

The Procter & Gamble Company 27

Unfavorable foreign exchange reduced net sales by 2%. Organic sales grew 3% driven by the unit volume increase. A 1% favorable impact from higher pricing was offset by a 1% impact from unfavorable geographic and product mix due to higher relative growth of developing regions, which have lower than average selling prices, and of lower priced product categories such as Fabric Care and Baby Care.

Fiscal year 2013 compared with fiscal year 2012

Net sales increased 1% to $82.6 billion in 2013 on a 2% increase in unit volume. Volume in Health Care and Baby, Feminine and Family Care grew mid-single digits. Volume in Fabric Care and Home Care grew low single digits.

Beauty volume was in line with the prior year. Grooming volume decreased low single digits. Volume grew low single digits in both developed and developing regions. The impact of overall global market growth was partially offset by market share declines in certain categories. Price increases added 1% to net sales, driven by price increases across all business segments, primarily executed in prior periods to offset cost increases and devaluing developing market currencies. Foreign exchange reduced net sales by 2%. Organic sales growth was 3% driven by both volume and price increases.

Operating Costs

Comparisons as a percentage of net sales; Years ended June 30 | 2014 |

| Basis Point Change |

| 2013 |

| Basis Point Change |

| 2012 | |||||

Gross margin | 48.9 | % |

| (100 | ) |

| 49.9 | % |

| 40 | |

| 49.5 | % |

Selling, general and administrative expense | 30.5 | % |

| (170 | ) |

| 32.2 | % |

| 50 | |

| 31.7 | % |

Goodwill and indefinite-lived intangible asset impairment charges | - | % |

| (40 | ) |

| 0.4 | % |

| (150 | ) |

| 1.9 | % |

Operating margin | 18.4 | % |

| 100 | |

| 17.4 | % |

| 150 | |

| 15.9 | % |

Earnings from continuing operations before income taxes | 17.9 | % |

| 10 | |

| 17.8 | % |

| 250 | |

| 15.3 | % |

Net earnings from continuing operations | 14.1 | % |

| 40 | |

| 13.7 | % |

| 250 | |

| 11.2 | % |

Net earnings attributable to Procter & Gamble | 14.0 | % |

| 30 | |

| 13.7 | % |

| 60 | |

| 13.1 | % |

Fiscal year 2014 compared with fiscal year 2013