Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 26, 2015

Commission file number 1-1183

PepsiCo, Inc.

(Exact Name of Registrant as Specified in Its Charter)

North Carolina (State or Other Jurisdiction of Incorporation or Organization) |

| 13-1584302 (I.R.S. Employer Identification No.) |

700 Anderson Hill Road, Purchase, New York (Address of Principal Executive Offices) |

| 10577 (Zip Code) |

Registrant's telephone number, including area code: 914-253-2000

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

Title of each class |

| Name of each exchange on which registered |

Common Stock, par value 1-2/3 cents per share |

| New York and Chicago Stock Exchanges |

2.500% Senior Notes Due 2022 |

| New York Stock Exchange |

1.750% Senior Notes Due 2021 |

| New York Stock Exchange |

2.625% Senior Notes Due 2026 |

| New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x | Accelerated filer ¨ |

Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of PepsiCo, Inc. Common Stock held by nonaffiliates of PepsiCo, Inc. (assuming for these purposes, but without conceding, that all executive officers and directors of PepsiCo, Inc. are affiliates of PepsiCo, Inc.) as of June 12, 2015 , the last day of business of our most recently completed second fiscal quarter, was $137.9 billion (based on the closing sale price of PepsiCo, Inc.'s Common Stock on that date as reported on the New York Stock Exchange).

The number of shares of PepsiCo, Inc. Common Stock outstanding as of February 4, 2016 was 1,445,412,743 .

Documents Incorporated by Reference

Portions of the Proxy Statement relating to PepsiCo, Inc.'s 2016 Annual Meeting of Shareholders are incorporated by reference into Part III of this Form 10-K.

Table of Contents

PepsiCo, Inc.

Form 10-K Annual Report

For the Fiscal Year Ended

December 26, 2015

Table of Contents

PART I |

|

|

Item 1. | Business | 2 |

Item 1A. | Risk Factors | 11 |

Item 1B. | Unresolved Staff Comments | 25 |

Item 2. | Properties | 26 |

Item 3. | Legal Proceedings | 27 |

Item 4. | Mine Safety Disclosures | 27 |

|

|

|

PART II |

|

|

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 31 |

Item 6. | Selected Financial Data | 34 |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 38 |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 127 |

Item 8. | Financial Statements and Supplementary Data | 127 |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 127 |

Item 9A. | Controls and Procedures | 127 |

Item 9B. | Other Information | 128 |

|

|

|

PART III |

|

|

Item 10. | Directors, Executive Officers and Corporate Governance | 128 |

Item 11. | Executive Compensation | 128 |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 128 |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 129 |

Item 14. | Principal Accounting Fees and Services | 129 |

|

|

|

PART IV |

|

|

Item 15. | Exhibits and Financial Statement Schedules | 130 |

1

Table of Contents

Forward-Looking Statements

This Annual Report on Form 10-K contains statements reflecting our views about our future performance that constitute "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995 (Reform Act). Statements that constitute forward-looking statements within the meaning of the Reform Act are generally identified through the inclusion of words such as "aim," "anticipate," "believe," "drive," "estimate," "expect," "expressed confidence," "forecast," "future," "goal," "guidance," "intend," "may," "objective," "outlook," "plan," "position," "potential," "project," "seek," "should," "strategy," "target," "will" or similar statements or variations of such words and other similar expressions. All statements addressing our future operating performance, and statements addressing events and developments that we expect or anticipate will occur in the future, are forward-looking statements within the meaning of the Reform Act. These forward-looking statements are based on currently available information, operating plans and projections about future events and trends. They inherently involve risks and uncertainties that could cause actual results to differ materially from those predicted in any such forward-looking statement. These risks and uncertainties include, but are not limited to, those described in "Item 1A. Risk Factors" and "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations – Our Business – Our Business Risks." Investors are cautioned not to place undue reliance on any such forward-looking statements, which speak only as of the date they are made. We undertake no obligation to update any forward-looking statement, whether as a result of new information, future events or otherwise. The discussion of risks below and elsewhere in this report is by no means all-inclusive but is designed to highlight what we believe are important factors to consider when evaluating our future performance.

PART I

Item 1. Business.

When used in this report, the terms "we," "us," "our," "PepsiCo" and the "Company" mean PepsiCo, Inc. and its consolidated subsidiaries, collectively. Certain terms used in this Annual Report on Form 10-K are defined in the Glossary included in Item 7. of this report.

Company Overview

We were incorporated in Delaware in 1919 and reincorporated in North Carolina in 1986. We are a leading global food and beverage company with a complementary portfolio of enjoyable brands, including Frito-Lay, Gatorade, Pepsi-Cola, Quaker and Tropicana. Through our operations, authorized bottlers, contract manufacturers and other third parties, we make, market, distribute and sell a wide variety of convenient and enjoyable beverages, foods and snacks, serving customers and consumers in more than 200 countries and territories.

Our Operations

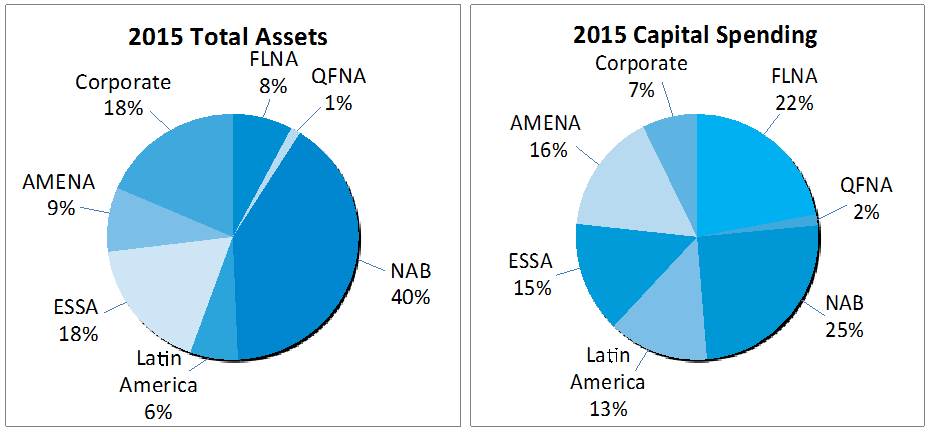

We are organized into six reportable segments (also referred to as divisions), as follows:

1) | Frito-Lay North America (FLNA); |

2) | Quaker Foods North America (QFNA); |

3) | North America Beverages (NAB); |

4) | Latin America, which includes all of our beverage, food and snack businesses in Latin America; |

5) | Europe Sub-Saharan Africa (ESSA), which includes all of our beverage, food and snack businesses in Europe and Sub-Saharan Africa; and |

6) | Asia, Middle East and North Africa (AMENA), which includes all of our beverage, food and snack businesses in Asia, Middle East and North Africa. |

2

Table of Contents

See Note 1 to our consolidated financial statements for financial information about our divisions and geographic areas. North America includes the United States and Canada. See also "Item 1A. Risk Factors" below for a discussion of certain risks associated with our operations, including outside the United States.

Frito-Lay North America

Either independently or in conjunction with third parties, FLNA makes, markets, distributes and sells branded snack foods. These foods include Lay's potato chips, Doritos tortilla chips, Cheetos cheese-flavored snacks, Tostitos tortilla chips, branded dips, Fritos corn chips, Ruffles potato chips and Santitas tortilla chips. FLNA's branded products are sold to independent distributors and retailers. In addition, FLNA's joint venture with Strauss Group makes, markets, distributes and sells Sabra refrigerated dips and spreads. FLNA's net revenue was $14.8 billion , $14.5 billion and $14.1 billion in 2015 , 2014 and 2013 , respectively, and approximated 23% of our total net revenue in 2015 , 22% of our total net revenue in 2014 and 21% of our total net revenue in 2013 .

Quaker Foods North America

Either independently or in conjunction with third parties, QFNA makes, markets, distributes and sells cereals, rice, pasta and other branded products. QFNA's products include Quaker oatmeal, Aunt Jemima mixes and syrups, Quaker Chewy granola bars, Cap'n Crunch cereal, Quaker grits, Life cereal, Rice-A-Roni side dishes, Quaker rice cakes, Quaker natural granola and Quaker oat squares. These branded products are sold to independent distributors and retailers. QFNA's net revenue was $2.5 billion in 2015 and $2.6 billion in both 2014 and 2013 , and approximated 4% of our total net revenue in each of 2015 , 2014 and 2013 .

North America Beverages

Either independently or in conjunction with third parties, NAB makes, markets, distributes and sells beverage concentrates, fountain syrups and finished goods under various beverage brands including Pepsi, Gatorade, Mountain Dew, Diet Pepsi, Aquafina, Diet Mountain Dew, Tropicana Pure Premium, Sierra Mist and Mug. NAB also, either independently or in conjunction with third parties, makes, markets and sells ready-to-drink tea and coffee products through joint ventures with Unilever (under the Lipton brand name) and Starbucks, respectively. Further, NAB manufactures and distributes certain brands licensed from Dr Pepper Snapple Group, Inc. (DPSG), including Dr Pepper, Crush and Schweppes, and certain juice brands licensed from Dole Food Company, Inc. (Dole) and Ocean Spray Cranberries, Inc. (Ocean Spray). NAB operates its own bottling plants and distribution facilities and sells branded finished goods directly to independent distributors and retailers. NAB also sells concentrate and finished goods for our brands to authorized and independent bottlers, who in turn sell our branded finished goods to independent distributors and retailers in certain markets. NAB's net revenue was $20.6 billion , $20.2 billion and $20.1 billion in 2015 , 2014 and 2013 , respectively, and approximated 33% of our total net revenue in 2015 and 30% of our total net revenue in both 2014 and 2013 .

Latin America

Either independently or in conjunction with third parties, Latin America makes, markets, distributes and sells a number of snack food brands including Doritos, Cheetos, Marias Gamesa, Ruffles, Emperador, Saladitas, Sabritas, Lay's, Rosquinhas Mabel and Tostitos, as well as many Quaker-branded cereals and snacks. Latin America also, either independently or in conjunction with third parties, makes, markets, distributes and sells beverage concentrates, fountain syrups and finished goods under various beverage brands including Pepsi, 7UP, Gatorade, Mirinda, Diet 7UP, Manzanita Sol and Diet Pepsi. These branded products are sold to authorized bottlers, independent distributors and retailers. Latin America also, either independently or in conjunction with third parties, makes, markets and sells ready-to-drink tea through an international joint venture with Unilever (under the Lipton brand name). Latin America's net revenue was $8.2 billion , $9.4

3

Table of Contents

billion and $9.3 billion in 2015 , 2014 and 2013 , respectively, and approximated 13% of our total net revenue in 2015 and 14% of our total net revenue in both 2014 and 2013 .

See Note 1 to our consolidated financial statements for information about the deconsolidation of our Venezuelan subsidiaries, which was effective as of the end of the third quarter of 2015.

Europe Sub-Saharan Africa

Either independently or in conjunction with third parties, ESSA makes, markets, distributes and sells a number of leading snack food brands including Lay's, Walkers, Doritos, Cheetos and Ruffles, as well as many Quaker-branded cereals and snacks, through consolidated businesses as well as through noncontrolled affiliates. ESSA also, either independently or in conjunction with third parties, makes, markets, distributes and sells beverage concentrates, fountain syrups and finished goods under various beverage brands including Pepsi, 7UP, Pepsi Max, Mirinda, Diet Pepsi and Tropicana. These branded products are sold to authorized bottlers, independent distributors and retailers. In certain markets, however, ESSA operates its own bottling plants and distribution facilities. ESSA also, either independently or in conjunction with third parties, makes, markets and sells ready-to-drink tea products through an international joint venture with Unilever (under the Lipton brand name). In addition, ESSA makes, markets, sells and distributes a number of leading dairy products including Chudo, Agusha and Domik v Derevne. ESSA's net revenue was $10.5 billion , $13.4 billion and $13.8 billion in 2015 , 2014 and 2013 , respectively, and approximated 17% of our total net revenue in 2015 , 20% of our total net revenue in 2014 and 21% of our total net revenue in 2013 .

Asia, Middle East and North Africa

Either independently or in conjunction with third parties, AMENA makes, markets, distributes and sells a number of leading snack food brands including Lay's, Kurkure, Chipsy, Doritos, Cheetos and Crunchy through consolidated businesses, as well as through noncontrolled affiliates. Further, either independently or in conjunction with third parties, AMENA makes, markets, distributes and sells many Quaker-branded cereals and snacks. AMENA also makes, markets, distributes and sells beverage concentrates, fountain syrups and finished goods under various beverage brands including Pepsi, Mirinda, 7UP, Mountain Dew, Aquafina and Tropicana. These branded products are sold to authorized bottlers, independent distributors and retailers. In certain markets, however, AMENA operates its own bottling plants and distribution facilities. AMENA also, either independently or in conjunction with third parties, makes, markets, distributes and sells ready-to-drink tea products through an international joint venture with Unilever (under the Lipton brand name). Further, we license the Tropicana brand for use in China on co-branded juice products in connection with a strategic alliance with Tingyi (Cayman Islands) Holding Corp. (Tingyi). AMENA's net revenue was $6.4 billion , $6.6 billion and $6.4 billion in 2015 , 2014 and 2013 , respectively, and approximated 10% of our total net revenue in each of 2015, 2014 and 2013 .

Our Distribution Network

Our products are brought to market through direct-store-delivery (DSD), customer warehouse and distributor networks. The distribution system used depends on customer needs, product characteristics and local trade practices.

Direct-Store-Delivery

We, our independent bottlers and our distributors operate DSD systems that deliver beverages, foods and snacks directly to retail stores where the products are merchandised by our employees or our independent bottlers. DSD enables us to merchandise with maximum visibility and appeal. DSD is especially well-suited to products that are restocked often and respond to in-store promotion and merchandising.

4

Table of Contents

Customer Warehouse

Some of our products are delivered from our manufacturing plants and warehouses to customer warehouses. These less costly systems generally work best for products that are less fragile and perishable, and have lower turnover.

Distributor Networks

We distribute many of our products through third-party distributors. Third-party distributors are particularly effective when greater distribution reach can be achieved by including a wide range of products on the delivery vehicles. For example, our foodservice and vending business distributes beverages, foods and snacks to restaurants, businesses, schools and stadiums through third-party foodservice and vending distributors and operators.

Ingredients and Other Supplies

The principal ingredients we use in our beverage, food and snack products are apple, orange and pineapple juice and other juice concentrates, aspartame, corn, corn sweeteners, flavorings, flour, grapefruit and other fruits, oats, oranges, potatoes, raw milk, rice, seasonings, sucralose, sugar, vegetable and essential oils, and wheat. We also use water in the manufacturing of our products. Our key packaging materials include plastic resins, including polyethylene terephthalate (PET) and polypropylene resins used for plastic beverage bottles and film packaging used for snack foods, aluminum used for cans, glass bottles, closures, cardboard and paperboard cartons. Fuel and natural gas are also important commodities for us due to their use in our facilities and the vehicles delivering our products. We employ specialists to secure adequate supplies of many of these items and have not experienced any significant continuous shortages that would prevent us from meeting our requirements. Many of these ingredients, raw materials and commodities are purchased in the open market. The prices we pay for such items are subject to fluctuation, and we manage this risk through the use of fixed-price contracts and purchase orders, pricing agreements and derivative instruments, including swaps and futures. In addition, risk to our supply of certain raw materials is mitigated through purchases from multiple geographies and suppliers. When prices increase, we may or may not pass on such increases to our customers. In addition, we continue to make investments to improve the sustainability and resources of our agricultural supply chain, including by developing our initiative to advance sustainable farming practices by our suppliers and expanding it globally. See Note 10 to our consolidated financial statements for additional information on how we manage our exposure to commodity costs.

Our Brands and Intellectual Property Rights

We own numerous valuable trademarks which are essential to our worldwide businesses, including Agusha, Amp Energy, Aquafina, Aquafina Flavorsplash, Aunt Jemima, Cap'n Crunch, Cheetos, Chester's, Chipsy, Chudo, Cracker Jack, Crunchy, Diet Mountain Dew, Diet Mug, Diet Pepsi, Diet 7UP (outside the United States), Diet Sierra Mist, Domik v Derevne, Doritos, Duyvis, Elma Chips, Emperador, Frito-Lay, Fritos, Fruktovy Sad, Frustyle, G Series, G2, Gatorade, Grandma's, Imunele, Izze, Kas, Kurkure, Lay's, Life, Lifewater, Lubimy, Manzanita Sol, Marias Gamesa, Matutano, Mirinda, Miss Vickie's, Mother's, Mountain Dew, Mountain Dew Code Red, Mountain Dew Kickstart, Mug, Munchies, Naked, Near East, O.N.E., Paso de los Toros, Pasta Roni, Pepsi, Pepsi Max, Pepsi Next, Propel, Quaker, Quaker Chewy, Rice-A-Roni, Rold Gold, Rosquinhas Mabel, Ruffles, Sabritas, Sakata, Saladitas, Sandora, Santitas, 7UP (outside the United States) and 7UP Free (outside the United States), Sierra Mist, Simba, Smartfood, Smith's, Snack a Jacks, SoBe, SoBe Lifewater, SoBe V Water, Sonric's, Stacy's, Sting, SunChips, Tonus, Tostitos, Trop 50, Tropicana, Tropicana Farmstand, Tropicana Pure Premium, Tropicana Twister, Vesely Molochnik, Walkers and Ya. We also hold long-term licenses to use valuable trademarks in connection with our products in certain markets, including Dole and Ocean Spray. We also distribute Rockstar Energy drinks, Muscle Milk protein shakes and various DPSG brands, including Dr Pepper in certain markets, Crush and Schweppes. Joint ventures in which we have an ownership interest either own or have the right to use certain trademarks, such as Lipton,

5

Table of Contents

Sabra and Starbucks. Trademarks remain valid so long as they are used properly for identification purposes, and we emphasize correct use of our trademarks. We have authorized, through licensing arrangements, the use of many of our trademarks in such contexts as snack food joint ventures and beverage bottling appointments. In addition, we license the use of our trademarks on merchandise that is sold at retail, which enhances brand awareness.

We either own or have licenses to use a number of patents which relate to certain of our products, their packaging, the processes for their production and the design and operation of various equipment used in our businesses. Some of these patents are licensed to others.

Seasonality

Our businesses are affected by seasonal variations. For instance, our beverage sales are higher during the warmer months and certain food and dairy sales are higher in the cooler months. Weekly beverage and snack sales are generally highest in the third quarter due to seasonal and holiday-related patterns, and generally lowest in the first quarter. However, taken as a whole, seasonality has not had a material impact on our consolidated financial results.

Our Customers

Our customers include wholesale and other distributors, foodservice customers, grocery stores, drug stores, convenience stores, discount/dollar stores, mass merchandisers, membership stores, e-commerce retailers and authorized independent bottlers, among others. We normally grant our independent bottlers exclusive contracts to sell and manufacture certain beverage products bearing our trademarks within a specific geographic area. These arrangements provide us with the right to charge our independent bottlers for concentrate, finished goods and Aquafina royalties and specify the manufacturing process required for product quality. We also grant distribution rights to our independent bottlers for certain beverage products bearing our trademarks for specified geographic areas.

We rely on and provide financial incentives to our customers to assist in the distribution and promotion of our products to the consumer. For our independent distributors and retailers, these incentives include volume-based rebates, product placement fees, promotions and displays. For our independent bottlers, these incentives are referred to as bottler funding and are negotiated annually with each bottler to support a variety of trade and consumer programs, such as consumer incentives, advertising support, new product support, and vending and cooler equipment placement. Consumer incentives include coupons, pricing discounts and promotions, and other promotional offers. Advertising support is directed at advertising programs and supporting independent bottler media. New product support includes targeted consumer and retailer incentives and direct marketplace support, such as point-of-purchase materials, product placement fees, media and advertising. Vending and cooler equipment placement programs support the acquisition and placement of vending machines and cooler equipment. The nature and type of programs vary annually.

Changes to the retail landscape, including increased consolidation of retail ownership, and the current economic environment continue to increase the importance of major customers. In 2015 , sales to Wal-Mart Stores, Inc. (Wal-Mart), including Sam's Club (Sam's), represented approximately 13% of our total net revenue. Our top five retail customers represented approximately 32% of our 2015 net revenue in North America, with Wal-Mart (including Sam's) representing approximately 18% . These percentages include concentrate sales to our independent bottlers, which were used in finished goods sold by them to these retailers.

See Note 8 to our consolidated financial statements for more information on our customers, including our independent bottlers.

6

Table of Contents

Our Competition

Our beverage, food and snack products are in highly competitive categories and markets and compete against products of international beverage, food and snack companies that, like us, operate in multiple geographies, as well as regional, local and private label manufacturers and other competitors. In many countries in which our products are sold, including the United States, The Coca-Cola Company is our primary beverage competitor. Other beverage, food and snack competitors include, but are not limited to, DPSG, Kellogg Company, The Kraft Heinz Company, Mondelēz International, Inc., Monster Beverage Corporation, Nestlé S.A., Red Bull GmbH and Snyder's-Lance, Inc.

Many of our food and snack products hold significant leadership positions in the food and snack industry in the United States and worldwide. In 2015, we and The Coca-Cola Company represented approximately 24% and 20%, respectively, of the U.S. liquid refreshment beverage category by estimated retail sales in measured channels, according to Information Resources, Inc. However, The Coca-Cola Company has significant carbonated soft drink (CSD) share advantage in many markets outside the United States.

Our beverage, food and snack products compete primarily on the basis of brand recognition, taste, price, quality, product variety, innovation, distribution, advertising, marketing and promotional activity, packaging, convenience, service and the ability to anticipate and effectively respond to consumer preferences and trends, including increased consumer focus on health and wellness. Success in this competitive environment is dependent on effective promotion of existing products, effective introduction of new products and the effectiveness of our advertising campaigns, marketing programs, product packaging, pricing, increased efficiency in production techniques, new vending and dispensing equipment and brand and trademark development and protection. We believe that the strength of our brands, innovation and marketing, coupled with the quality of our products and flexibility of our distribution network, allows us to compete effectively.

Research and Development

We engage in a variety of research and development activities and continue to invest to accelerate growth and to drive innovation globally. These activities principally involve: development of new ingredients and products; reformulation and improvement in the quality and appeal of existing products; improvement and modernization of manufacturing processes; improvements in product quality, safety and integrity; development of, and improvements in, dispensing equipment, packaging technology, package design and portion sizes; and efforts focused on identifying opportunities to transform, grow and broaden our product portfolio, including by developing products with improved nutrition profiles that reduce sodium, saturated fat or added sugars, including through the use of sweetener alternatives and flavor modifiers and innovation in existing sweeteners, and by offering more options with whole grains, fruits and vegetables. Our research centers are located around the world, including in Brazil, China, Germany, India, Mexico, Russia, the United Arab Emirates, the United Kingdom and the United States, and leverage nutrition science, food science, engineering and consumer insights to meet our strategy to continue to develop nutritious, convenient beverages, foods and snacks.

In 2015 , we continued to refine our beverage, food and snack portfolio to meet changing consumer demands by developing a broader portfolio of product choices, including: launching beverage options that contain no high fructose corn syrup and are made with natural flavors; building on our important nutrition platforms and brands – Quaker (grains), Tropicana (fruits and vegetables), Gatorade (sports nutrition for athletes) and Naked Juice (juices and smoothies); expanding our whole grain products globally; and expanding our portfolio of nutritious products in growing categories, such as dairy, hummus and other refrigerated dips, and baked grain snacks. We also continued to develop and implement new technologies to enhance the quality and value of our current and future products. In addition, we continued to make investments to reduce our impact on the environment, including: efforts to conserve raw materials and energy, such as by working to achieve reductions in greenhouse gas emissions across our global businesses, by helping to protect and conserve

7

Table of Contents

global water supplies especially in water-stressed areas (including conserving water within our operations and promoting the reduction of water use in our agricultural supply chain), and by incorporating into our operations improvements in the sustainability and resources of our agricultural supply chain; efforts to reduce waste generated by our operations and disposed of in landfills; efforts to recycle containers; efforts to use renewable resources; and efforts to optimize package technology and design to make our packaging increasingly sustainable with lower environmental impact.

Research and development costs were $ 754 million , $718 million and $ 665 million in 2015 , 2014 and 2013 , respectively, and are reported within selling, general and administrative expenses. Consumer research is excluded from such research and development costs and included in other marketing costs.

Regulatory Environment and Environmental Compliance

The conduct of our businesses, including the production, storage, distribution, sale, display, advertising, marketing, labeling, content, quality and safety of our products, occupational health and safety practices, transportation and use of many of our products, are subject to various laws and regulations administered by federal, state and local governmental agencies in the United States, as well as to laws and regulations administered by government entities and agencies outside the United States in markets in which our products are made, manufactured, distributed or sold. It is our policy to abide by the laws and regulations around the world that apply to our businesses.

We are required to comply with a variety of U.S. laws and regulations, including but not limited to: the Federal Food, Drug and Cosmetic Act and various state laws governing food safety; the Food Safety Modernization Act; the Occupational Safety and Health Act; the Clean Air Act; the Clean Water Act; the Resource Conservation and Recovery Act; the Comprehensive Environmental Response, Compensation and Liability Act; the Federal Motor Carrier Safety Act; the Lanham Act; various federal and state laws and regulations governing competition and trade practices; various federal and state laws and regulations governing our employment practices, including those related to equal employment opportunity, such as the Equal Employment Opportunity Act and the National Labor Relations Act; customs and foreign trade laws and regulations; and laws regulating the sale of certain of our products in schools. In our business dealings, we are also required to comply with the Foreign Corrupt Practices Act, the U.K. Bribery Act and the Trade Sanctions Reform and Export Enhancement Act. We are also subject to various state and local statutes and regulations, including state consumer protection laws such as Proposition 65 in California, which requires that, unless a safe harbor level exists and has been met, a specific warning appear on any product that contains a substance listed by the State of California as having been found to cause cancer or birth defects.

We are also subject to numerous similar and other laws and regulations outside the United States, including but not limited to laws and regulations governing food safety, occupational health and safety, competition, anti-corruption and data privacy. In many jurisdictions, compliance with competition laws is of special importance to us due to our competitive position in those jurisdictions, as is compliance with anti-corruption laws. We rely on legal and operational compliance programs, as well as in-house and outside counsel, to guide our businesses in complying with the laws and regulations around the world that apply to our businesses.

Certain jurisdictions in which our products are sold have either imposed, or are considering imposing, taxes, labeling requirements or other limitations on, or regulations pertaining to, the sale of certain of our products, ingredients or substances contained in, or attributes of, our products or commodities used in the production of our products, including certain of our products that contain added sugars, sodium or saturated fat, exceed a specified caloric content, or include specified ingredients such as caffeine. For example, taxes on sugar-sweetened beverages were imposed in Mexico and Berkeley, California; the U.S. Food and Drug Administration is considering requiring nutrition labels to include information about added sugars; and Brazil and Vermont have enacted legislation requiring labeling of products that contain genetically modified

8

Table of Contents

ingredients. In addition, a number of other jurisdictions in the United States and outside the United States are considering similar measures. Regulators may also restrict the use of benefit programs, such as the Supplemental Nutrition Assistance Program, to purchase certain beverages and foods. In addition, legislation has been enacted in certain U.S. states and in certain other countries where our products are sold that requires collection and recycling of containers or that prohibits the sale of our beverages in certain non-refillable containers, unless a deposit or other fee is charged. It is possible that similar or more restrictive legal requirements may be proposed or enacted in the future. In addition, as our products are made, manufactured, distributed and sold in more than 200 countries and territories, we are subject to tax laws and regulations in the United States and numerous foreign jurisdictions. Economic and political conditions may result in changes in tax rates, and existing laws on how U.S. multinational corporations are taxed on foreign earnings are subject to changes in interpretation and enforcement, which could affect our financial performance. The cost of compliance with such U.S. and foreign laws has not had a material financial impact on our consolidated results of operations.

We are also subject to national and local environmental laws in the United States and in foreign countries in which we do business, including laws related to water consumption and treatment, wastewater discharge and air emissions. In the United States, our facilities must comply with the Clean Air Act, the Clean Water Act, the Comprehensive Environmental Response, Compensation and Liability Act, the Resource Conservation and Recovery Act and other federal and state laws regarding handling, storage, release and disposal of wastes generated on-site and sent to third-party owned and operated off-site licensed facilities and our facilities outside the United States must comply with similar laws and regulations. Our policy is to abide by all applicable environmental compliance requirements, and we have internal programs in place to enhance our global environmental compliance. We have made, and plan to continue making, necessary expenditures for compliance with applicable laws. While these expenditures have not had a material impact on our business, financial condition or results of operations, changes in environmental compliance requirements, and any expenditures necessary to comply with such requirements, could affect our financial performance. In addition, we and our subsidiaries are subject to environmental remediation obligations arising in the normal course of business, as well as remediation and related indemnification obligations in connection with certain historical activities and contractual obligations, including those of businesses acquired by us or our subsidiaries. While these environmental and indemnification obligations cannot be predicted with certainty, environmental compliance costs have not had, and are not expected to have, a material impact on our capital expenditures, earnings or competitive position.

In addition to the discussion in this section, see under "Item 1A. Risk Factors" below "Changes in, or failure to comply with, laws and regulations applicable to our products or our business operations could adversely affect our business, financial condition or results of operations.", "Imposition of new taxes, disagreements with tax authorities or additional tax liabilities could adversely affect our business, financial condition or results of operations.", "Our business, financial condition or results of operations could be adversely affected if we are unable to grow our business in developing and emerging markets or as a result of unstable political conditions, civil unrest or other developments and risks in the markets where our products are made, manufactured, distributed or sold" and "Climate change or water scarcity, or legal, regulatory or market measures to address climate change or water scarcity, may negatively affect our business and operations or damage our reputation."

The Iran Threat Reduction and Syria Human Rights Act of 2012 (ITRA) requires disclosure of certain activities relating to Iran by PepsiCo or its affiliates that occurred during our 2015 fiscal year. As previously disclosed, one of our foreign subsidiaries historically maintained a small office in Iran, which provided sales support to independent bottlers in Iran in connection with in-country sales of foreign-owned beverage brands, and which was not in contravention of any applicable U.S. sanctions laws. The office ceased all commercial activity since the enactment of ITRA. During our 2015 fiscal year, our foreign subsidiary received a license

9

Table of Contents

from the U.S. Treasury Department's Office of Foreign Assets Control authorizing it to engage in activities related to the winding down of the office in Iran and completed the process of winding down its office. The foreign subsidiary did not engage in any activities in Iran other than wind-down activities in 2015 , or have any revenues or profits attributable to activities in Iran during 2015 .

Employees

As of December 26, 2015 , we and our consolidated subsidiaries employed approximately 263,000 people worldwide, including approximately 110,000 people within the United States. In certain countries, our employment levels are subject to seasonal variations. We or our subsidiaries are a party to numerous collective bargaining agreements. We expect that we will be able to renegotiate these collective bargaining agreements on satisfactory terms when they expire. We believe that relations with our employees are generally good.

Available Information

We are required to file annual, quarterly and current reports, proxy statements and other information with the U.S. Securities and Exchange Commission (SEC). The public may read and copy any materials that we file with the SEC at the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov .

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements and amendments to those documents filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (Exchange Act), are also available free of charge on our Internet site at http://www.pepsico.com as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC.

Investors should note that we currently announce material information to our investors and others using filings with the SEC, press releases, public conference calls or webcasts. In addition, we have used, and intend to continue to use, these channels or our corporate website ( www.pepsico.com ) to communicate important information, including news and announcements regarding our financial performance, key personnel, our brands and our business strategy. Information that we post on our corporate website could be deemed material to investors. We encourage investors, the media, our customers, consumers, business partners and others interested in us to review the information we post on our corporate website from time to time. We may from time to time update the list of channels we will use to communicate information that could be deemed material and will post information about any such change on www.pepsico.com . The information on our website is not, and shall not be deemed to be, a part hereof or incorporated into this or any of our other filings with the SEC.

10

Table of Contents

Item 1A. Risk Factors.

In addition to the other information set forth in this Annual Report on Form 10-K, you should carefully consider the following factors that could have a material adverse effect on our business, financial condition, results of operations or the price of our common stock. The following information should be read together and in conjunction with "Forward-Looking Statements," "Item 1. Business," "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations," our consolidated financial statements and the accompanying notes thereto. The risks below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also adversely affect our business, financial condition, results of operations or the price of our common stock.

Demand for our products may be adversely affected by changes in consumer preferences or any inability on our part to innovate or market our products effectively, and any significant reduction in demand could adversely affect our business, financial condition or results of operations.

We are a global food and beverage company operating in highly competitive categories and markets and we rely on continued demand for our products. To generate revenues and profits, we must sell products that appeal to our customers and to consumers. Any significant changes in consumer preferences or any inability on our part to anticipate or react to such changes could result in reduced demand for our products and erosion of our competitive and financial position and could adversely affect our business, financial condition or results of operations. Our success depends in part on our ability to anticipate and effectively respond to shifts in consumer trends and preferences, including increased demand for products that meet the needs of consumers who are concerned with: health and wellness (including products that have less sodium, added sugars and saturated fat); convenience (including responding to changes in in-home and on-the-go consumption patterns); or the location of origin or source of the ingredients and products. Our success also depends on: product quality; our ability to extend our portfolio of products in growing markets and categories; our ability to respond to cultural differences and regional consumer preferences; our ability to monitor and adjust our use of ingredients to respond to applicable local regulations; our ability to develop or acquire new products that are responsive to certain consumer preferences; our ability to develop a broader portfolio of product choices and continue to increase non-carbonated beverage offerings and other alternatives to traditional carbonated beverage offerings; our ability to develop sweetener alternatives and innovation; our ability to improve the production and packaging of our products; and our ability to respond to competitive product and pricing pressures. For example, our growth rate may be adversely affected if we are unable to maintain or grow our current share of the liquid refreshment beverage market or snacks market, or if demand for our products does not grow in developing and emerging markets.

In general, changes in consumption in our product categories or consumer demographics could result in reduced demand for our products. Consumer preferences have been evolving, and are expected to continue to evolve, due to a variety of factors, including: the aging of the general population; consumer concerns or perceptions regarding the nutrition profile of certain of our products, including their caloric content, or perceptions (whether or not valid) regarding the health effects of ingredients or substances present in certain of our products, such as 4-MeI, acrylamide, artificial flavors and colors, artificial sweeteners, aspartame, caffeine, high-fructose corn syrup, saturated fat, sodium, sugar, trans fats or other product ingredients, substances or attributes, including genetically engineered ingredients; taxes or other restrictions imposed on our products; consumer concerns or perceptions regarding packaging materials, such as with respect to the environmental sustainability or chemical makeup thereof; changes in package or portion size; changes in social trends that impact travel, vacation or leisure activity patterns; changes in weather patterns or seasonal consumption cycles; negative publicity (whether or not valid) resulting from regulatory action, litigation against us or other companies in our industry or negative or inaccurate posts or comments in the media, including social media, about us, our products or advertising campaigns and marketing programs; consumer

11

Table of Contents

perception of social media posts or other information disseminated by us or our employees, agents, customers, suppliers, bottlers, distributors, joint venture partners or other third parties; consumer perception of our employees, agents, customers, suppliers, bottlers, distributors, joint venture partners or other third parties or the business practices of such parties; or a downturn in economic conditions. Any of these changes may reduce consumers' willingness to purchase our products.

Our continued success is also dependent on our product and marketing innovation, including: maintaining a robust pipeline of new products; improving the quality of existing products; and the effectiveness of our product packaging and distribution, advertising campaigns and marketing programs, including our ability to successfully adapt to a rapidly changing media environment, including through use of social media and online advertising campaigns and marketing programs.

Although we devote significant resources to the items mentioned above, there can be no assurance as to our continued ability to develop, launch and maintain successful new products or variants of existing products in a timely manner or our ability to correctly anticipate or effectively react to changes in consumer preference or develop and effectively execute advertising and marketing campaigns that appeal to customers and consumers. Our failure to make the right strategic investments to drive innovation or successfully launch new products or variants of existing products could decrease demand for our existing products by negatively affecting consumer perception of existing brands and may result in inventory write-offs and other costs that could adversely affect our business, financial condition or results of operations.

Changes in, or failure to comply with, laws and regulations applicable to our products or our business operations could adversely affect our business, financial condition or results of operations.

Our businesses are subject to various laws and regulations administered by federal, state and local governmental agencies in the United States, as well as government entities and agencies outside the United States, including laws and regulations relating to the production, content, quality, safety, storage, distribution, sale, display, advertising, marketing, labeling, transportation and use of products, as well as our occupational health and safety practices. Many of these laws and regulations have differing or conflicting legal standards across the various markets where our products are made, manufactured, distributed or sold and, in certain markets, such as developing and emerging markets, may be less developed or certain. In addition, these laws and regulations and related interpretations may change, sometimes dramatically, as a result of a variety of factors, including political, economic or social events. Such changes may include changes in: food and drug laws; laws related to product labeling, advertising and marketing practices; laws regarding the import or export of our products or ingredients used in our products; laws and programs restricting the sale and advertising of certain of our products; laws and programs aimed at reducing, restricting or eliminating ingredients or substances in, or attributes of, certain of our products; laws and programs aimed at discouraging the consumption or altering the package or portion size of certain of our products, including laws imposing restrictions on the use of government funds or programs, such as the Supplemental Nutrition Assistance Program, to purchase certain of our products; increased regulatory scrutiny of, and increased litigation involving product claims and concerns (whether or not valid) regarding the effects on health of ingredients or substances in, or attributes of, certain of our products, including without limitation those found in energy drinks; state consumer protection laws; taxation requirements, including the imposition or proposed imposition of new or increased taxes or other limitations on the sale of our products; accounting rules and interpretations; competition laws; anti-corruption laws; employment laws; privacy laws; laws regulating the price we may charge for our products; laws regulating water rights and access to and use of water or utilities; and environmental laws, including laws relating to the regulation of water treatment and discharge of wastewater and air emissions.

12

Table of Contents

The imposition by any jurisdiction in the United States or outside the United States of new laws, regulations or governmental policy and their related interpretations, or changes in any of the foregoing, including taxes, labeling, product or production requirements or other limitations on, or pertaining to, the sale or advertisement of certain of our products, ingredients or substances contained in, or attributes of, our products or commodities used in the production of our products, may alter the environment in which we do business and, therefore, may increase our costs or liabilities or reduce demand for our products, which could adversely affect our business, financial condition or results of operations. For example, taxes on sugar-sweetened beverages were imposed in Mexico and Berkeley, California; the U.S. Food and Drug Administration is considering requiring nutrition labels to include information about added sugars; and Brazil and Vermont have enacted legislation requiring labeling of products that contain genetically modified ingredients. In addition, a number of other jurisdictions in the United States and outside the United States are considering similar measures. If one jurisdiction imposes or proposes to impose new requirements or restrictions, other jurisdictions may follow and the requirements or restrictions, or proposed requirements or restrictions, may result in adverse publicity (whether or not valid). For example, if one jurisdiction imposes a specific labeling requirement or requires a specific warning on any product that contains certain ingredients or substances, other jurisdictions may react and impose restrictions on products containing the same ingredients or substances, which may result in adverse publicity or increased concerns about the health implications of consumption of such ingredients or substances in our products (whether or not valid). Changes in regulatory requirements, and competing regulations and standards, where our products are made, manufactured, distributed or sold, may result in higher compliance costs, capital expenditures and higher production costs, which could adversely affect our business, financial condition or results of operations.

In addition, studies are underway by third parties to assess the health implications of consumption of certain ingredients or substances present in certain of our products, such as 4-MeI, acrylamide, caffeine, added sugars and sodium. If consumer concerns (whether or not valid) about the health implications of consumption of such ingredients or substances present in certain of our products increase as a result of these studies, new scientific evidence, new labeling, product or production requirements or other restrictions, or for any other reason, including adverse publicity (whether or not valid) as a result of any of the foregoing, or if we are required to add warning labels to any of our products or place warnings in locations where our products are sold, demand for our products could decline, or we could be subject to lawsuits or new regulations that could affect sales of our products, any of which could adversely affect our business, financial condition or results of operations.

In many jurisdictions, compliance with competition laws is of special importance to the conduct of our businesses due to our competitive position in those jurisdictions, as is compliance with anti-corruption laws. In addition, regulatory authorities under whose laws we operate may have enforcement powers that can subject us to actions such as product recall, seizure of products or assets or other sanctions, which could have an adverse effect on the sales of products in our portfolio or could lead to damage to our reputation. Although we have policies and procedures in place that are designed to promote legal and regulatory compliance, our employees, suppliers, or other third parties with whom we do business could take actions, intentional or not, that violate these policies and procedures or applicable laws or regulations. Violations of these laws or regulations could subject us to criminal or civil enforcement actions, including fines, penalties, disgorgement of profits or activity restrictions, any of which could result in adverse publicity or affect our business, financial condition or results of operations.

In addition, we and our subsidiaries are party to a variety of legal and environmental remediation obligations arising in the normal course of business, as well as environmental remediation, product liability, toxic tort and related indemnification proceedings in connection with certain historical activities and contractual obligations, including those of businesses acquired by us or our subsidiaries. Due to regulatory complexities, uncertainties inherent in litigation and the risk of unidentified contaminants on current and former properties

13

Table of Contents

of ours and our subsidiaries, the potential exists for remediation, liability and indemnification costs to differ materially from the costs we have estimated. We cannot guarantee that our costs in relation to these matters will not exceed our established liabilities or otherwise have an adverse effect on our business, financial condition or results of operations.

Imposition of new taxes, disagreements with tax authorities or additional tax liabilities could adversely affect our business, financial condition or results of operations.

Our products are made, manufactured, distributed or sold in more than 200 countries and territories. As such, we are subject to tax laws and regulations of various federal, state and local governments in the United States as well as to tax laws and regulations outside the United States. The imposition or proposed imposition of new or increased taxes or other limitations on the sale of our products, ingredients or substances contained in, or attributes of, our products or commodities used in the production of our products, could increase the cost of our products, reduce overall consumption of our products, lead to negative publicity (whether or not valid) or leave consumers with the perception that our products do not meet their health and wellness needs, which could adversely affect our business, financial condition or results of operations. If one jurisdiction imposes new or increased taxes or limitations, other jurisdictions may follow, which may result in adverse publicity or increased concerns about the health implications of consumption of our products (whether or not valid).

In addition, we are subject to regular reviews, examinations and audits by the Internal Revenue Service (IRS) and other taxing authorities with respect to income and non-income based taxes both within and outside the United States. Economic and political pressures to increase tax revenues in jurisdictions in which we operate, or the adoption of new or reformed tax legislation or regulation, may make resolving tax disputes more difficult and the final resolution of tax audits and any related litigation could differ from our historical provisions and accruals, resulting in an adverse impact on our business, financial condition or results of operations.

Our operations outside the United States generate a significant portion of our income and income tax associated with repatriation of foreign earnings to the United States could adversely affect our business, financial condition or results of operations. In addition, many of the countries in which our products are made, manufactured, distributed or sold, including countries in which we have significant operations, are actively considering changes to existing tax laws. Changes in how U.S. multinational corporations are taxed on foreign earnings, including changes in how existing tax laws are interpreted or enforced, could adversely affect our business, financial condition or results of operations.

Our business, financial condition or results of operations could suffer if we are unable to compete effectively.

Our beverage, food and snack products are in highly competitive categories and markets and compete against products of international beverage, food and snack companies that, like us, operate in multiple geographic areas, as well as regional, local and private label manufacturers and other competitors. In many countries in which our products are sold, including the United States, our primary beverage competitor is The Coca-Cola Company. We also compete with other large companies in each of the beverage, food and snack categories, including DPSG, Kellogg Company, The Kraft Heinz Company, Mondelēz International, Inc., Monster Beverage Corporation, Nestlé S.A., Red Bull GmbH and Snyder's-Lance, Inc.

Our beverage, food and snack products compete primarily on the basis of brand recognition, taste, price, quality, product variety, innovation, distribution, advertising, marketing and promotional activity, packaging, convenience, service and the ability to anticipate and effectively respond to consumer preferences and trends, including increased consumer focus on health and wellness. If we are unable to effectively promote our

14

Table of Contents

existing products or introduce new products, if our advertising or marketing campaigns are not effective or if we are otherwise unable to compete effectively, we may be unable to grow or maintain sales, gross margins or category share in the global market or in various local markets or we may need to increase capital, marketing or other expenditures, which may adversely affect our business, financial condition or results of operations.

Our business, financial condition or results of operations could be adversely affected if we are unable to grow our business in developing and emerging markets or as a result of unstable political conditions, civil unrest or other developments and risks in the markets where our products are made, manufactured, distributed or sold.

Our operations outside of the United States, particularly in Mexico, Russia, Canada, the United Kingdom and Brazil, contribute significantly to our revenue and profitability, and we believe that these countries and other developing and emerging markets, including China and India, present important future growth opportunities for us. However, there can be no assurance that our existing products, variants of our existing products or new products that we make, manufacture, distribute or sell will be accepted or be successful in any particular developing or emerging market, due to local or global competition, product price, cultural differences, consumer preferences or otherwise. The following factors could reduce demand for our products in such developing and emerging markets: unstable economic, political or social conditions, acts of war, terrorist acts, and civil unrest in certain of these markets where our products are made, manufactured, distributed or sold, including Russia, Ukraine, Brazil and the Middle East; increased competition; volatility in the economic growth of certain of these markets and the related impact on developed countries who export to these markets; our inability to acquire businesses, form strategic business alliances or to make necessary infrastructure investments; our inability to complete divestitures or refranchisings; imposition of new or increased labeling, product or production requirements, or other restrictions; imposition of new or increased sanctions against, or other regulations restricting contact with, certain countries in these markets in which our products are made, manufactured, distributed or sold, such as Russia, or imposition of new or increased sanctions against U.S. multinational corporations operating in these markets; foreign ownership restrictions; nationalization of our assets or the assets of our suppliers, bottlers, distributors, joint venture partners or other third parties; government-mandated closure, or threatened closure, of our operations or the operations of our suppliers, bottlers, distributors, joint venture partners or other third parties; restrictions on the import or export of our products or ingredients or substances used in our products; regulations on the repatriation of funds currently held in foreign jurisdictions to the United States; highly inflationary currency, devaluation or fluctuation, such as the devaluation of the Russian ruble, Venezuelan bolivar, Mexican peso, euro, Brazilian real and the Canadian dollar; regulations on the transfer of funds to and from foreign countries, currency controls or other currency exchange restrictions, which result in significant cash balances in foreign countries, from time to time, or could significantly affect our ability to effectively manage our operations in certain of these markets and could result in the deconsolidation of such businesses, such as the deconsolidation of our Venezuelan businesses effective as of the end of the third quarter of 2015; the lack of well-established or reliable legal systems; increased costs of doing business due to compliance with complex foreign and United States laws and regulations that apply to our international operations, including the Foreign Corrupt Practices Act, the U.K. Bribery Act and the Trade Sanctions Reform and Export Enhancement Act; and adverse consequences, such as the assessment of fines or penalties, for any failure to comply with these laws and regulations. If we are unable to expand our businesses in developing and emerging markets, effectively operate, or manage the risks associated with operating, in these markets, or achieve the return on capital we expect from our investments in these markets, our business, financial condition or results of operations could be adversely affected.

15

Table of Contents

Unfavorable economic conditions may have an adverse impact on our business, financial condition or results of operations.

Many of the countries in which we operate have experienced and continue to experience unfavorable economic conditions. Our business or financial results may be adversely impacted by these unfavorable economic conditions, including: adverse changes in interest rates, tax laws or tax rates; volatile commodity markets, including speculative influences; highly inflationary currency, devaluation or fluctuation; contraction in the availability of credit in the marketplace due to legislation or economic conditions; the effects of government initiatives, including austerity or stimulus measures, to manage economic conditions and any changes to or cessation of such initiatives; the effects of any default by or deterioration in the credit worthiness of the countries in which our products are sold or of countries that may then impact countries in which our products are sold; reduced demand for our products resulting from volatility in general global economic conditions or a shift in consumer preferences for economic reasons or otherwise to regional, local or private label products or other lower-cost products, or to less profitable channels; or a decrease in the fair value of pension or post-retirement assets that could increase future employee benefit costs and/or funding requirements of our pension or post-retirement plans. In addition, we cannot predict how current or future economic conditions will affect our customers, consumers, suppliers, bottlers, distributors, joint venture partners or other third parties and any negative impact on any of the foregoing may also have an adverse impact on our business, financial condition or results of operations.

In addition, some of the major financial institutions with which we execute transactions, including U.S. and non-U.S. commercial banks, insurance companies, investment banks and other financial institutions, may be exposed to a ratings downgrade, bankruptcy, liquidity, default or similar risks as a result of unfavorable economic conditions, changing regulatory requirements or other factors beyond our control. A ratings downgrade, bankruptcy, receivership, default or similar event involving a major financial institution, or changes in the regulatory environment, may limit the ability or willingness of financial institutions to enter into financial transactions with us, including to provide banking or related cash management services, or to extend credit on terms commercially acceptable to us or at all; may leave us with reduced borrowing capacity or exposed to certain currencies or price risk associated with forecasted purchases of raw materials; or may result in a decline in the market value of our investments in debt securities, which could have an adverse impact on our business, financial condition or results of operations.

Our business, financial condition or results of operations may be adversely affected by increased costs, disruption of supply or shortages of raw materials and other supplies.

We and our business partners use various raw materials and other supplies in our business. The principal ingredients we use in our beverage, food and snack products are apple, orange and pineapple juice and other juice concentrates, aspartame, corn, corn sweeteners, flavorings, flour, grapefruit and other fruits, oats, oranges, potatoes, raw milk, rice, seasonings, sucralose, sugar, vegetable and essential oils, and wheat. We also use water in the manufacturing of our products. Our key packaging materials include plastic resins, including PET and polypropylene resins used for plastic beverage bottles and film packaging used for snack foods, aluminum used for cans, glass bottles, closures, cardboard and paperboard cartons. Fuel and natural gas are also important commodities for our businesses due to their use in our facilities and the vehicles delivering our products.

Some of these raw materials and supplies are sourced from countries experiencing civil unrest, political instability or unfavorable economic conditions, and some are available from a limited number of suppliers or are in short supply when seasonal demand is at its peak. The raw materials and energy, including fuel, that we use for the manufacturing, production and distribution of our products are largely commodities that are subject to price volatility and fluctuations in availability caused by many factors, including changes in global

16

Table of Contents

supply and demand, weather conditions, disease or pests, agricultural uncertainty, health epidemics or pandemics, governmental incentives and controls, political uncertainties, governmental instability or currency exchange rates. Shortage of some of these raw materials and other supplies, sustained interruption in their supply or an increase in their costs could adversely affect our business, financial condition or results of operations. Many of our ingredients, raw materials and commodities are purchased in the open market. The prices we pay for such items are subject to fluctuation, and we manage this risk through the use of fixed-price contracts and purchase orders, pricing agreements and derivatives. If commodity price changes result in unexpected or significant increases in raw materials and energy costs, we may not be able to increase our product prices or effectively hedge against commodity price increases to offset these increased costs without suffering reduced volume, revenue, margins and operating results. In addition, certain of the derivatives used to hedge price risk do not qualify for hedge accounting treatment and, therefore, can result in increased volatility in our net earnings in any given period due to changes in the spot prices of the underlying commodities.

Water is also a limited resource in many parts of the world. The lack of available water of acceptable quality and increasing pressure to conserve water in areas of scarcity and stress may lead to: supply chain disruption, adverse effects on our operations, higher compliance costs, capital expenditures (including additional investments in the development of technologies to enhance water efficiency and reduce water consumption), higher production costs, the cessation of operations at, or relocation of, our facilities or the facilities of our suppliers, bottlers, distributors, joint venture partners or other third parties, or damage to our reputation, any of which could adversely affect our business, financial condition or results of operations.

Failure to realize anticipated benefits from our productivity initiatives or global operating model could have an adverse impact on our business, financial condition or results of operations.

Our future success and earnings growth depend in part on our ability to continue to reduce costs and improve efficiencies. Our productivity initiatives help support our growth initiatives and contribute to our results of operations. We continue to implement strategic plans that we believe will position our business for future success and long-term sustainable growth by allowing us to achieve a lower cost structure and operate more efficiently in the highly competitive beverage, food and snack categories and markets. We are also continuing to implement our global operating model to improve efficiency, decision making, innovation and brand management across the global PepsiCo organization to enable us to compete effectively. Further, in order to capitalize on our cost reduction efforts and our global operating model, it will be necessary to make certain investments in our business, which may be limited due to capital constraints. Some of these measures could yield unintended consequences, such as business disruptions, distraction of management and employees, reduced employee morale and productivity, and unexpected additional employee attrition, including the inability to attract or retain key personnel. It is critical that we have the appropriate personnel in place to continue to lead and execute our plans, including to effectively manage personnel adjustments and transitions resulting from these initiatives and increased competition for employees with the skills necessary to implement our plans. If we are unable to successfully implement our productivity initiatives and global operating model as planned, fail to implement these initiatives as timely as we anticipate, do not achieve expected savings as a result of these initiatives or incur higher than expected or unanticipated costs in implementing these initiatives, or fail to identify and implement additional productivity opportunities in the future, or fail to successfully manage business disruptions or unexpected employee consequences on our workforce, morale or productivity, we may not realize all or any of the anticipated benefits, which could adversely affect our business, financial condition or results of operations.

17

Table of Contents

Business disruptions could have an adverse impact on our business, financial condition or results of operations.

Our ability, and that of our suppliers and other third parties, including our independent bottlers, contract manufacturers, joint venture partners, independent distributors and customers, to make, manufacture, transport, distribute and sell products in our portfolio is critical to our success. Damage or disruption to our or their operations due to any of the following factors could impair the ability to make, manufacture, transport, distribute or sell products in our portfolio: adverse weather conditions or natural disaster, such as a hurricane, earthquake or flooding; government action; economic or political uncertainties or instability in countries in which such products are made, manufactured, distributed or sold, which may also affect our ability to protect the security of our assets and employees; fire; terrorism; outbreak or escalation of armed hostilities; food safety warnings or recalls, whether related to products in our portfolio or otherwise; health epidemics or pandemics; unplanned delays or unexpected problems associated with repairs or enhancements of facilities in which such products are made, manufactured, distributed or sold; cyber incidents; industrial accidents or other occupational health and safety issues; telecommunications failures; power or water shortages; strikes and other labor disputes; or other reasons beyond our control or the control of our suppliers and other third parties. Failure to take adequate steps to mitigate the likelihood or potential impact of such events, or to effectively manage such events if they occur, could adversely affect our business, financial condition or results of operations, as well as require additional resources to restore our operations.

Product contamination or tampering or issues or concerns with respect to product quality, safety and integrity could adversely affect our business, financial condition or results of operations.

Product contamination or tampering, the failure to maintain high standards for product quality, safety and integrity, including with respect to raw materials and ingredients obtained from suppliers, or allegations (whether or not valid) of product quality issues, mislabeling, misbranding, spoilage, allergens or contamination may reduce demand for products in our portfolio, cause production and delivery disruptions or increase costs, which could adversely affect our business, financial condition or results of operations. If any of the products in our portfolio are mislabeled or become unfit for consumption or cause injury, illness or death, or if appropriate resources are not devoted to product quality and safety (particularly as we expand our portfolio into new categories) or to comply with changing food safety requirements, products in our portfolio may be subject to a product recall and/or be subject to liability or government action, which could result in payment of damages or fines, cause certain products in our portfolio to be unavailable for a period of time or result in adverse publicity, which could reduce consumer demand and brand equity. Our business could also be adversely affected if consumers lose confidence in product quality, safety and integrity generally, even if such loss of confidence is unrelated to products in our portfolio. Any of the foregoing could adversely affect our business, financial condition or results of operations. In addition, if we do not have adequate insurance, if we do not have contractual indemnification from suppliers, bottlers, distributors, joint venture partners or other third parties or if indemnification is not available, the liability relating to such product claims or disruption as a result of recall efforts could materially adversely affect our business, financial condition or results of operations.

Any damage to our reputation or brand image could adversely affect our business, financial condition or results of operations.