UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTIONS 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended October 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 0-7977

NORDSON CORPORATION

(Exact name of Registrant as specified in its charter)

| Ohio | 34-0590250 | |

| (State of incorporation) | (I.R.S. Employer Identification No.) | |

28601 Clemens Road Westlake, Ohio | 44145 | |

| (Address of principal executive offices) | (Zip Code) | |

| (440) 892-1580 | ||

| (Registrant's Telephone Number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

Common Shares with no par value

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months, and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if smaller reporting company) | ||||||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of Common Shares no par value per share, held by nonaffiliates (based on the closing sale price on the Nasdaq Stock Market) as of April 29, 2011 was approximately $3,670,599,000.

There were 65,343,146 Common Shares outstanding as of November 30, 2011.

Documents incorporated by reference:

Portions of the Proxy Statement for the 2012 Annual Meeting - Part III

Table of Contents

PART I | 1 | |||||||

Item 1. | Business | 1 | ||||||

| General Description of Business | 1 | |||||||

| Corporate Purpose and Goals | 1 | |||||||

Financial Information About Operating Segments, Foreign and Domestic Operations and Export Sales | 2 | |||||||

| Principal Products and Uses | 2 | |||||||

| Manufacturing and Raw Materials | 4 | |||||||

| Intellectual Property | 4 | |||||||

| Seasonal Variation in Business | 5 | |||||||

| Working Capital Practices | 5 | |||||||

| Customers | 5 | |||||||

| Backlog | 5 | |||||||

| Government Contracts | 5 | |||||||

| Competitive Conditions | 5 | |||||||

| Research and Development | 5 | |||||||

| Environmental Compliance | 6 | |||||||

| Employees | 6 | |||||||

| Available Information | 6 | |||||||

Item 1A. | Risk Factors | 7 | ||||||

Item 1B. | Unresolved Staff Comments | 10 | ||||||

Item 2. | Properties | 11 | ||||||

Item 3. | Legal Proceedings | 12 | ||||||

Item 4. | Removed and Reserved | 12 | ||||||

| Executive Officers of the Company | 13 | |||||||

PART II | 14 | |||||||

Item 5. | Market for the Company's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 14 | ||||||

| Market Information and Dividends | 14 | |||||||

| Performance Graph | 15 | |||||||

Item 6. | Selected Financial Data | 16 | ||||||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 17 | ||||||

| Critical Accounting Policies and Estimates | 17 | |||||||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 29 | ||||||

Item 8. | Financial Statements and Supplementary Data | 31 | ||||||

| Consolidated Statements of Income | 31 | |||||||

| Consolidated Balance Sheets | 32 | |||||||

| Consolidated Statements of Shareholders' Equity | 33 | |||||||

| Consolidated Statements of Cash Flows | 34 | |||||||

| Notes to Consolidated Financial Statements | 35 | |||||||

| Management's Report on Internal Control Over Financial Reporting | 69 | |||||||

| Report of Independent Registered Public Accounting Firm | 70 | |||||||

| Report of Independent Registered Public Accounting Firm | 71 | |||||||

i

Table of Contents

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 72 | ||||||

Item 9A. | Controls and Procedures | 72 | ||||||

Item 9B. | Other Information | 72 | ||||||

PART III | 72 | |||||||

Item 10. | Directors, Executive Officers and Corporate Governance | 72 | ||||||

Item 11. | Executive Compensation | 73 | ||||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 73 | ||||||

| Equity Compensation Table | 73 | |||||||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 73 | ||||||

Item 14. | Principal Accountant Fees and Services | 73 | ||||||

PART IV | 74 | |||||||

Item 15. | Exhibits and Financial Statement Schedule | 74 | ||||||

| (a) 1. Financial Statements | 74 | |||||||

| (a) 2. Financial Statement Schedule | 74 | |||||||

| (a) 3. Exhibits | 74 | |||||||

| Signatures | 75 | |||||||

| Schedule II - Valuation and Qualifying Accounts and Reserves | 77 | |||||||

| Index to Exhibits | 78 | |||||||

| Subsidiaries of the Registrant | 81 | |||||||

| Consent of Independent Registered Public Accounting Firm | 84 | |||||||

| Certifications | 85 | |||||||

ii

PART I

NOTE REGARDING AMOUNTS AND FISCAL YEAR REFERENCES

In this annual report, all amounts related to United States dollars and foreign currency and to the number of Nordson Corporation's common shares, except for per share earnings and dividend amounts, are expressed in thousands.

Unless otherwise noted, all references to years relate to our fiscal year ending October 31.

| Item 1. | Business |

General Description of Business

Nordson engineers, manufactures and markets differentiated products and systems used for adhesive, coating, sealant and biomaterial dispensing, fluid management, testing and inspection, curing, and surface treatment, backed with application expertise and direct global sales and service. Nordson serves a wide variety of consumer non-durable, consumer durable and technology end markets including packaging, nonwovens, electronics, medical, appliances, energy, transportation, building and construction, and general product assembly and finishing.

Our strategy for long-term growth is based on a customer-driven focus and a global mindset. Headquartered in Westlake, Ohio, our products are marketed through a network of direct operations in more than 30 countries. Consistent with this global strategy, 75 percent of our revenues are generated outside the United States.

We have 4,094 employees worldwide. Principal manufacturing facilities are located in the United States in California, Colorado, Georgia, Minnesota, New Jersey, Ohio and Rhode Island, as well as in Belgium, China, Germany, India, the Netherlands and the United Kingdom.

Corporate Purpose and Goals

We strive to be a vital, self-renewing, worldwide organization that, within the framework of ethical behavior and enlightened citizenship, grows and produces wealth for our customers, employees, shareholders and communities.

We operate for the purpose of creating balanced, long-term benefits for all of our constituencies: customers, employees, shareholders and communities.

Although every quarter may not produce increased sales, earnings and earnings per share, or exceed the comparative prior year's quarter, we do expect to produce long-term gains. When short-term swings occur, we do not intend to alter our basic objectives in efforts to mitigate the impact of these natural occurrences.

Growth is achieved by seizing opportunities with existing products and markets, investing in systems to maximize productivity and pursuing growth markets. This strategy is augmented through product line additions, engineering, research and development, and acquisition of companies that can serve multinational industrial markets.

We create benefits for our customers through a Package of Values ® , which includes carefully engineered, durable products; strong service support; the backing of a well-established worldwide company with financial and technical strengths; and a corporate commitment to deliver what was promised.

We strive to provide genuine customer satisfaction; it is the foundation upon which we continue to build our business.

Complementing our business strategy is the objective to provide opportunities for employee self-fulfillment, growth, security, recognition and equitable compensation. This goal is met through Human Resources' facilitation of employee training and leadership training and the creation of on-the-job growth opportunities. The result is a highly qualified and professional management team capable of meeting corporate objectives.

1

We recognize the value of employee participation in the planning process. Strategic and operating plans are developed by all business units and divisions, resulting in a sense of ownership and commitment on the part of employees in accomplishing our objectives. In addition, employees participate in Lean and Six Sigma initiatives to continuously improve our processes.

We are an equal opportunity employer.

We are committed to contributing approximately five percent of domestic pretax earnings to human services, education and other charitable activities, particularly in communities where we have major facilities.

Financial Information About Operating Segments, Foreign and Domestic Operations and Export Sales

In accordance with accounting standards, we have reported information about our three operating segments. This information is contained in Note 16 of Notes to Consolidated Financial Statements, which can be found in Part II, Item 8 of this document.

Principal Products and Uses

We engineer, manufacture and market differentiated products and systems used for precision dispensing, testing and inspection, fluid management, surface treatment and curing. Our technology-based systems can be found in manufacturing facilities around the world producing a wide range of goods for consumer durable, consumer non-durable and technology end markets. Equipment ranges from single-use components to manual, stand-alone units for low-volume operations to microprocessor-based automated systems for high-speed, high-volume production lines.

We market our products in the United States and in more than 50 other countries, primarily through a direct sales force and also through qualified distributors and sales representatives. We have built a worldwide reputation for creativity and expertise in the design and engineering of high-technology application equipment that meets the specific needs of our customers. We create value for our customers by developing solutions that increase uptime, enable faster line speeds and reduce consumption of materials.

The following is a summary of the products and markets served by our operating segments:

| 1. | Adhesive Dispensing Systems |

This segment delivers our proprietary precision dispensing technology to diverse markets for applications that commonly reduce material consumption, increase line efficiency and enhance product strength, durability, brand and appearance.

| • | Nonwovens - Equipment for applying adhesives, lotions, liquids and fibers to disposable products. Key strategic markets include adult incontinence products, baby diapers and child-training pants, feminine hygiene products and surgical drapes, gowns, shoe covers and face masks. |

| • | Packaging - Automated adhesive dispensing systems used in the food and beverage and packaged goods industries. Key strategic markets include food packages and wrappers and drink containers. |

| • | Product Assembly - Adhesive and sealant dispensing systems for bonding or sealing plastic, metal and wood products and for use in the paper and paperboard converting industries. Key strategic markets include appliances, automotive components, building and construction materials, electronics, furniture, solar energy, and the manufacturing of bags, sacks, books, envelopes and folding cartons. |

| • | Web Coating and Extruding - Laminating and coating systems used to manufacture continuous-roll goods in the nonwovens, textile, paper and flexible packaging industries. Key strategic markets include carpet, labels, tapes, textiles, and flexible pouches and wraps. |

2

| 2. | Advanced Technology Systems |

This segment integrates our proprietary product technologies found in progressive stages of a customer's production process, such as surface preparation, precisely controlled dispensing of material onto the surface, bond testing and X-ray inspection to ensure quality. This segment primarily serves the specific needs of electronics, medical and related high-tech industries.

| • | Surface Preparation - Automated gas plasma treatment systems used to clean and condition surfaces for the semiconductor, medical and printed circuit board industries. Key strategic markets include contact lenses, electronics, medical instruments and devices, printed circuit boards and semiconductors. |

| • | Dispensing Systems - Controlled manual and automated systems for applying materials in customer processes typically requiring extreme precision and material conservation. These systems include piezoelectric and motionless two-component mixing dispensing systems. Key strategic markets include aerospace, biomaterial application, electronics (cell phones, liquid crystal displays, micro hard drives, microprocessors, printed circuit boards, micro electronic mechanical systems (MEMS), and tablets), general industrial, life sciences (dental and medical devices, including pacemakers and stents), light emitting diodes (LED) and solar energy. |

| • | Fluid Management - Precision engineered, plastic molded, single use fluid connection components used in critical medical and industrial flow control applications. Key strategic markets include anesthesia, cardiovascular and ophthalmic surgery, blood management, pneumatic control systems, water treatment, and analytical instrumentation. |

| • | Bond Testing and Inspection Systems - Bond testing and automated optical and x-ray inspection systems used in the semiconductor and printed circuit board industries. Key strategic markets include electronics (desktop, netbook and notebook computers, digital music players, mobile phones and tablets), light emitting diodes (LED), printed circuit board assemblies and semiconductor packages. |

| 3. | Industrial Coating Systems |

This segment provides both standard and highly-customized equipment used primarily for applying coatings, paint, finishes, sealants and other materials, and curing and drying of dispensed material. This segment primarily serves the consumer durables market.

| • | Automotive - Automated and manual dispensing systems used to apply materials in the automotive, heavy truck and recreational vehicle manufacturing industries. Key strategic markets include powertrain components, body assembly and final trim applications. |

| • | Container Coating - Automated and manual dispensing and curing systems used to coat and cure containers. Key strategic markets include beverage containers and food cans. |

| • | Curing and Drying Systems - Ultraviolet equipment used primarily in curing and drying operations for specialty coatings, semiconductor materials and paints. Key strategic markets include electronics, containers, and durable goods products. |

| • | Liquid Finishing - Automated and manual dispensing systems used to apply liquid paints and coatings to consumer and industrial products. Key strategic markets include automotive components, construction, metal shelving and drums. |

| • | Powder Coating - Automated and manual dispensing systems used to apply powder paints and coatings to a variety of metal, plastic and wood products. Key strategic markets include agriculture and construction equipment, appliances, automotive components, home and office furniture, lawn and garden equipment, pipe coating, and wood and metal shelving. |

3

Manufacturing and Raw Materials

Our production operations include machining and assembly. We manufacture specially designed parts and assemble components into finished equipment. Many components are made in standard modules that can be used in more than one product or in combination with other components for a variety of models. We have principal manufacturing operations in the United States in Amherst, Ohio; Norcross, Swainsboro and Dawsonville, Georgia; Carlsbad, California; Ft. Collins, Colorado; St. Paul, Minnesota; Robbinsville, New Jersey and East Providence, Rhode Island; as well as in Temse, Belgium; Shanghai and Suzhou, China; Luneburg, Germany; Bangalore, India; Maastricht, the Netherlands and in Aylesbury, United Kingdom.

Principal materials used to make our products are metals and plastics, typically in sheets, bar stock, castings, forgings, tubing and pellets. We also purchase many electrical and electronic components, fabricated metal parts, high-pressure fluid hoses, packings, seals and other items integral to our products. Suppliers are competitively selected based on cost, quality and service. All significant raw materials that we use are available through multiple sources.

Senior operating executives supervise an extensive quality control program for our equipment, machinery and systems.

Natural gas and other fuels are our primary energy sources. However, standby capacity for alternative sources is available if needed.

Intellectual Property

We maintain procedures to protect our intellectual property (including patents, trademarks and copyrights) both domestically and internationally. Risk factors associated with our intellectual property are discussed in Item 1A Risk Factors.

Our intellectual property portfolios include valuable patents, trade secrets, know-how, domain names, trademarks and trade names. As of October 31, 2011, we held 380 United States patents and 790 foreign patents and had 187 United States patent applications and 741 foreign patent applications pending, but there is no assurance that any patent application will be issued. We continue to apply for and obtain patent protection for new products on an ongoing basis.

Patents covering individual products extend for varying periods according to the date of filing or grant and legal term of patents in various countries where a patent is obtained. Our current patent portfolio has expiration dates ranging from November 2011 to December 2035. The actual protection a patent provides, which can vary from country to country, depends upon the type of patent, the scope of its coverage, and the availability of legal remedies in each country. We believe, however, that the duration of our patents generally exceeds the life cycles of the technologies disclosed and claimed in the patents.

We believe our trademarks are important assets and we aggressively manage our brands. We also own a number of trademarks in the United States and foreign countries, including registered trademarks for Nordson, Asymtek, ColorMax, Control Coat, Dage, EFD, and Saturn and various common law trademarks which are important to our business, inasmuch as they identify Nordson and our products to our customers. As of October 31, 2011, we had a total of 988 trademark registrations in the United States and in various foreign countries.

We rely upon a combination of nondisclosure and other contractual arrangements and trade secret laws to protect our proprietary rights and also enter into confidentiality and intellectual property agreements with our employees that require them to disclose any inventions created during employment, convey all rights to inventions to us, and restrict the distribution of proprietary information.

We protect and promote our intellectual property portfolio and take those actions we deem appropriate to enforce our intellectual property rights and to defend our right to sell our products. Although in aggregate our intellectual property is important to our operations, we do not believe that the loss of any one patent, trademark, or group of related patents or trademarks would have a material adverse effect on our results of operations or financial position of our overall business.

4

Seasonal Variation in Business

Generally, the highest volume of sales occurs in our fourth quarter due in large part to the timing of customers' capital spending programs. First quarter sales volume is typically the lowest of the year due to customer holiday shutdowns.

Working Capital Practices

No special or unusual practices affect our working capital. However, we generally require advance payments as deposits on customized equipment and systems and, in certain cases, require progress payments during the manufacturing of these products. We have initiated a number of new processes focused on reduction of manufacturing lead times. These initiatives have resulted in lower investment in inventory while maintaining the capability to respond promptly to customer needs.

Customers

We serve a broad customer base, both in terms of industries and geographic regions. In 2011, no single customer accounted for five percent or more of sales.

Backlog

Our backlog of open orders increased to approximately $131,000 at October 31, 2011 from approximately $128,000 at October 31, 2010. The amounts for both years were calculated based upon exchange rates in effect at October 31, 2011. The increase can be traced primarily to acquisitions completed during the year. All orders in the 2011 year-end backlog are expected to be shipped to customers in 2012.

Government Contracts

Our business neither includes nor depends upon a significant amount of governmental contracts or subcontracts. Therefore, no material part of our business is subject to renegotiation or termination at the option of the government.

Competitive Conditions

Our equipment is sold in competition with a wide variety of alternative bonding, sealing, caulking, finishing, coating, testing and inspection, and fluid management techniques . Any production process that requires surface preparation or modification, application of material to a substrate or surface, curing, testing and inspection, or fluid management is a potential use for our equipment.

Many factors influence our competitive position, including pricing, product quality and service. We enjoy a leadership position in our business segments by delivering high-quality, innovative products and technologies, as well as after-the-sale service and technical support. Working with customers to understand their processes and developing the application solutions that help them meet their production requirements also contributes to our leadership position. Our worldwide network of direct sales and technical resources also is a competitive advantage.

Research and Development

Investments in research and development are important to our long-term growth, enabling us to keep pace with changing customer and marketplace needs through the development of new products and new applications for existing products. We place strong emphasis on technology developments and improvements through internal engineering and research teams. Research and development expenses were approximately $26,997 in 2011, compared with approximately $23,835 in 2010 and $25,528 in 2009.

5

Environmental Compliance

We are subject to extensive federal, state, local and foreign environmental, safety and health laws and regulations concerning, among other things, emissions to the air, discharges to land and water and the generation, handling, treatment and disposal of hazardous waste and other materials. Under certain of these laws, we can be held strictly liable for hazardous substance contamination of any real property we have ever owned, operated or used as a disposal site or for natural resource damages associated with such contamination. We are also required to maintain various related permits and licenses, many of which require periodic modification and renewal. The operation of manufacturing plants unavoidably entails environmental, safety and health risks, and we could incur material unanticipated costs or liabilities in the future if any of these risks were realized in ways or to an extent that we did not anticipate.

We believe that we operate in compliance, in all material respects, with applicable environmental laws and regulations. Compliance with environmental laws and regulations requires continuing management effort and expenditures. We have incurred, and will continue to incur, costs and capital expenditures to comply with these laws and regulations and to obtain and maintain the necessary permits and licenses. We believe that the cost of complying with environmental laws and regulations will not have a material effect on our earnings, liquidity or competitive position but cannot assure that material compliance-related costs and expenses may not arise in the future. For example, future adoption of new or amended environmental laws, regulations or requirements or newly discovered contamination or other circumstances that could require us to incur costs and expenses that may have a material effect, but cannot be presently anticipated.

We believe that policies, practices and procedures have been properly designed to prevent unreasonable risk of material environmental damage arising from our operations. We accrue for estimated environmental liabilities with charges to expense and believe our environmental accrual is adequate to provide for our portion of the costs of all such known environmental liabilities. Compliance with federal, state and local environmental protection laws during 2011 had no material effect on our capital expenditures, earnings or competitive position. Based upon consideration of currently available information, we believe liabilities for environmental matters will not have a material adverse affect on our financial position, operating results or liquidity, but we cannot assure that material environmental liabilities may not arise in the future.

Employees

As of October 31, 2011, we had 4,094 full- and part-time employees, including 137 at our Amherst, Ohio, facility who are represented by a collective bargaining agreement that expires on November 3, 2013. No material work stoppages have been experienced at any of our facilities during any of the periods covered by this report.

Available Information

Our proxy statement, annual report to the Securities and Exchange Commission (Form 10-K), quarterly reports (Form 10-Q) and current reports (Form 8-K) and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available free of charge at http://www.nordson.com/investors as soon as reasonably practical after such material is electronically filed with, or furnished to, the SEC. Copies of these reports may also be obtained free of charge by sending written requests to Corporate Communications, Nordson Corporation, 28601 Clemens Road, Westlake, Ohio 44145.

6

| Item 1A. | Risk Factors |

In an enterprise as diverse as ours, a wide range of factors could affect future performance. We discuss in this section some of the risk factors that, if they actually occurred, could materially and adversely affect our business, financial condition, value and results of operations. You should consider these risk factors in connection with evaluating the forward-looking statements contained in this Annual Report on Form 10-K because these factors could cause our actual results and financial condition to differ materially from those projected in forward-looking statements.

The significant risk factors affecting our operations include the following:

Changes in United States or international economic conditions could adversely affect the profitability of any of our operations.

In 2011, 25 percent of our revenue was derived from domestic customers, while 75 percent was derived from international customers. Our largest markets include appliance, automotive, construction, container, electronics assembly, food and beverage, furniture, life sciences and medical, light emitting diodes (LED), metal finishing, nonwovens, packaging, paper and paperboard converting and semiconductor. A slowdown in any of these specific end markets could directly affect our revenue stream and profitability.

A portion of our product sales is attributable to industries and markets, such as the semiconductor and metal finishing industries, which historically have been cyclical and sensitive to relative changes in supply and demand and general economic conditions. The demand for our products depends, in part, on the general economic conditions of the industries or national economies of our customers. Downward economic cycles in our customers' industries or countries may reduce sales of some of our products. It is not possible to predict accurately the factors that will affect demand for our products in the future.

Any significant downturn in the health of the general economy, either globally, regionally or in the markets in which we sell products could have an adverse effect on our revenues and financial performance, resulting in impairment of assets.

Significant movements in foreign currency exchange rates or change in monetary policy may harm our financial results.

We are exposed to fluctuations in foreign currency exchange rates, particularly with respect to the euro, the yen, the pound sterling and the Chinese yuan. Any significant change in the value of the currencies of the countries in which we do business against the United States dollar could affect our ability to sell products competitively and control our cost structure, which could have a material adverse effect on our business, financial condition and results of operations. For additional detail related to this risk, see Item 7A, Quantitative and Qualitative Disclosure About Market Risk.

The majority of our consolidated revenues in 2011 were generated in currencies other than the United States dollar, which is our reporting currency. We recognize foreign currency transaction gains and losses arising from our operations in the period incurred. As a result, currency fluctuations between the United States dollar and the currencies in which we do business have caused and will continue to cause foreign currency transaction and translation gains and losses, which historically have been material and could continue to be material. We cannot predict the effects of exchange rate fluctuations upon our future operating results because of the number of currencies involved, the variability of currency exposures and the potential volatility of currency exchange rates. We take actions to manage our foreign currency exposure, such as entering into hedging transactions, where available, but we cannot assure that our strategies will adequately protect our consolidated operating results from the effects of exchange rate fluctuations.

We also face risks arising from the imposition of exchange controls and currency devaluations. Exchange controls may limit our ability to convert foreign currencies into United States dollars or to remit dividends and other payments by our foreign subsidiaries or customers located in or conducting business in a country imposing controls. Currency devaluations diminish the United States dollar value of the currency of the country instituting the devaluation and, if they occur or continue for significant periods, could adversely affect our earnings or cash flow.

7

Failure to retain our existing senior management team or the inability to attract and retain qualified personnel could hurt our business and inhibit our ability to operate and grow successfully.

Our success will continue to depend to a significant extent on the continued service of our executive management team and the ability to recruit, hire and retain other key management personnel to support our growth and operational initiatives and replace executives who retire or resign. Failure to retain our leadership team and attract and retain other important management and technical personnel could place a constraint on our global growth and operational initiatives which could lead to inefficient and ineffective management and operations, which would likely harm our revenues, operations and product development efforts and eventually result in a decrease in profitability.

The inability to continue to develop new products could limit our revenue and profitability.

Innovation is critical to our success. We believe that we must continue to enhance our existing products and to develop and manufacture new products with improved capabilities in order to continue to be a market leader. We also believe that we must continue to make improvements in our productivity in order to maintain our competitive position. Our inability to anticipate, respond to or utilize changing technologies could have a material adverse effect on our business and our consolidated results of operations.

Inability to access capital could impede growth or the repayment or refinancing of existing indebtedness.

The limits imposed on us by the restrictive covenants contained in our credit facilities could prevent us from making acquisitions or cause us to lose access to these facilities.

Our existing credit facilities contain restrictive covenants that limit our ability to, among other things:

| • | borrow money or guarantee the debts of others; |

| • | use assets as security in other transactions; |

| • | make investments or other restricted payments or distributions; |

| • | change our business or enter into new lines of business; |

| • | sell or acquire assets or merge with or into other companies. |

In addition, our credit facilities require us to meet financial ratios, including "total indebtedness" to "consolidated trailing earnings before interest taxes depreciation and amortization" (EBITDA) both as defined in the credit facility, and consolidated trailing EBITDA to consolidated trailing interest expense as defined in the credit facility.

These restrictions could limit our ability to plan for or react to market conditions or meet extraordinary capital needs and could otherwise restrict our financing activities.

Our ability to comply with the covenants and other terms of our credit facilities will depend on our future operating performance. If we fail to comply with such covenants and terms, we will be in default and the maturity of the related debt could be accelerated and become immediately due and payable. We may be required to obtain waivers from our lenders in order to maintain compliance under our credit facilities, including waivers with respect to our compliance with certain financial covenants. If we are unable to obtain necessary waivers and the debt under our credit facilities is accelerated, we would be required to obtain replacement financing at prevailing market rates.

We may need new or additional financing in the future to expand our business or refinance existing indebtedness. If we are unable to access capital on satisfactory terms and conditions, we may not be able to expand our business or meet our payment requirements under our existing credit facilities. Our ability to obtain new or additional financing will depend on a variety of factors, many of which are beyond our control. We may not be able to obtain new or additional financing because we have substantial debt or because we may not have sufficient cash flow to service or repay our existing or future debt. In addition, depending on market conditions and our financial performance, neither debt nor equity financing may be available on satisfactory terms or at all. Finally, as a consequence of worsening financial market conditions, our credit facility providers may not provide the agreed credit if they become undercapitalized.

8

Our growth strategy includes acquisitions, and we may not be able to execute on our acquisition strategy or integrate acquisitions successfully.

Our recent historical growth has depended, and our future growth is likely to continue to depend, in part on our acquisition strategy and the successful integration of acquired businesses into our existing operations. We intend to continue to seek additional acquisition opportunities both to expand into new markets and to enhance our position in existing markets throughout the world. We cannot assure, however, that we will be able to successfully identify suitable acquisition opportunities, prevail against competing potential acquirers, negotiate appropriate acquisition terms, obtain financing that may be needed to consummate such acquisitions, complete proposed acquisitions, successfully integrate acquired businesses into our existing operations or expand into new markets. In addition, we cannot assure that any acquisition, once successfully integrated, will perform as planned, be accretive to earnings, or prove to be beneficial to our operations and cash flow.

The success of our acquisition strategy is subject to other risks and uncertainties, including:

| • | our ability to realize operating efficiencies, synergies or other benefits expected from an acquisition, and possible delays in realizing the benefits of the acquired company or products; |

| • | diversion of management's time and attention from other business concerns; |

| • | difficulties in retaining key employees, customers or suppliers of the acquired business; |

| • | difficulties in maintaining uniform standards, controls, procedures and policies throughout acquired companies; |

| • | adverse effects on existing business relationships with suppliers or customers; |

| • | the risks associated with the assumption of contingent or undisclosed liabilities of acquisition targets; |

| • | the ability to generate future cash flows or the availability of financing. |

In addition, an acquisition could adversely impact our operating performance as a result of the incurrence of acquisition-related debt, acquisition expenses, the amortization of acquisition-acquired assets, or possible future impairments of goodwill or intangible assets associated with the acquisition.

We may also face liability with respect to acquired businesses for violations of environmental laws occurring prior to the date of our acquisition, and some or all of these liabilities may not be covered by environmental insurance secured to mitigate the risk or by indemnification from the sellers from which we acquired these businesses. We could also incur significant costs, including, but not limited to, remediation costs, natural resources damages, civil or criminal fines and sanctions and third-party claims, as a result of past or future violations of, or liabilities associated with environmental laws.

Our inability to protect our intellectual property rights could adversely affect product sales and financial performance.

Difficulties in acquiring and maintaining our intellectual property rights could also adversely affect our business and financial position. Our performance may depend in part on our ability to establish, protect and enforce intellectual property rights with respect to our patented technologies and proprietary rights and to defend against any claims of infringement. These activities involve complex and constantly evolving legal, scientific and factual questions and uncertainties. Our ability to compete effectively with other companies depends in part on our ability to maintain and enforce our patents and other proprietary rights, which are essential to our business. These measures afford only limited protection and may not in all cases prevent our competitors from gaining access to our intellectual property and proprietary information.

9

Litigation has been and may continue to be necessary to enforce our intellectual property rights, to protect our trade secrets and to determine the validity and scope of our proprietary rights. In addition, we may face claims of infringement that could interfere with our ability to use technology or other intellectual property rights that are material to our business operations. If litigation that we initiate is unsuccessful, we may not be able to protect the value of some of our intellectual property. If a claim of infringement against us is successful, we may be required to pay royalties or license fees to continue to use technology or other intellectual property rights that we have been using or we may be unable to obtain necessary licenses from third parties at a reasonable cost or within a reasonable time. If we are unable to timely obtain licenses on reasonable terms, we may be forced to cease selling or using any of our products that incorporate the challenged intellectual property, or to redesign or, in the case of trademark claims, rename our products to avoid infringing the intellectual property rights of third parties. This may not always be possible or, if possible, may be time consuming and expensive. Intellectual property litigation, whether successful or unsuccessful, could be expensive to us and divert some of our resources. Our intellectual property rights may not be as valuable as we believe, which could result in a competitive disadvantage or adversely affect our business and financial performance.

Political conditions in foreign countries in which we operate could adversely affect us.

We conduct our manufacturing, sales and distribution operations on a worldwide basis and are subject to risks associated with doing business outside the United States. In 2011, approximately 75 percent of our total sales were to customers outside the United States. We expect that international operations and United States export sales will continue to be important to our business for the foreseeable future. Both sales from international operations and export sales are subject in varying degrees to risks inherent in doing business outside the United States. Such risks include, but are not limited to, the following:

| • | risks of economic instability; |

| • | unanticipated or unfavorable circumstances arising from host country laws or regulations; |

| • | restrictions on the transfer of funds into or out of a country; |

| • | currency exchange rate fluctuations; |

| • | difficulties in enforcing agreements and collecting receivables through some foreign legal systems; |

| • | international customers with longer payment cycles than customers in the United States; |

| • | potential negative consequences from changes to taxation policies; |

| • | the disruption of operations from foreign labor and political disturbances; |

| • | the imposition of tariffs, import or export licensing requirements; |

| • | exchange controls or other trade restrictions including transfer pricing restrictions when products produced in one country are sold to an affiliated entity in another country. |

Any of these events could reduce the demand for our products, limit the prices at which we can sell our products, or otherwise have an adverse effect on our operating performance.

We could be adversely affected by rapid changes in interest rates.

Any period of unexpected or rapid increase in interest rates may also adversely affect our profitability. At October 31, 2011, we had $319,156 of total debt and notes payable outstanding, of which 60 percent was priced at interest rates that float with the market. A one percent increase in the interest rate on the floating rate debt in 2011 would have resulted in approximately $785 of additional interest expense. A higher level of floating rate debt would increase the exposure to changes in interest rates. For additional detail related to this risk, see Item 7A, Quantitative and Qualitative Disclosure About Market Risk.

| Item 1B. | Unresolved Staff Comments |

None.

10

| Item 2. | Properties |

The following table summarizes our principal properties as of October 31, 2011.

Location | Description of Property | Approximate Square Feet | ||||

Amherst, Ohio 1, 2, 3 | A manufacturing, laboratory and office complex | 585,000 | ||||

Norcross, Georgia 1 | A manufacturing, laboratory and office building | 150,000 | ||||

Dawsonville, Georgia 1 | A manufacturing, laboratory and office building | 134,000 | ||||

East Providence, Rhode Island 2 | A manufacturing, warehouse and office building | 116,000 | ||||

Duluth, Georgia 1 | An office and laboratory building | 110,000 | ||||

Carlsbad, California 2 | Two manufacturing and office buildings (leased) | 88,000 | ||||

Robbinsville, New Jersey 2 | A manufacturing, warehouse and office building (leased) | 88,000 | ||||

Swainsboro, Georgia 1 | A manufacturing building | 59,000 | ||||

Ft. Collins, Colorado 2 | A manufacturing, warehouse and office building (leased) | 42,000 | ||||

Vista, California 2 | A manufacturing building (leased) | 41,000 | ||||

St. Paul, Minnesota 2 | A manufacturing, warehouse and office building (leased) | 27,000 | ||||

Westlake, Ohio | Corporate headquarters | 28,000 | ||||

Luneburg, Germany 1 | A manufacturing and laboratory building | 130,000 | ||||

Shanghai, China 1, 3 | A manufacturing, warehouse and office building (leased) | 92,000 | ||||

Erkrath, Germany 1,2, 3 | An office, laboratory and warehouse building (leased) | 63,000 | ||||

Bangalore, India 1, 2, 3 | A manufacturing, warehouse and office building | 56,000 | ||||

Shanghai, China 1,2, 3 | An office and laboratory building | 54,000 | ||||

Temse, Belgium 1 | A manufacturing, warehouse and office building (leased) | 44,000 | ||||

Tokyo, Japan 1, 2, 3 | An office, laboratory and warehouse building (leased) | 42,000 | ||||

Aylesbury, U.K. 1,2 | A manufacturing, warehouse and office building (leased) | 36,000 | ||||

Mexico City, Mexico 1, 2, 3 | A warehouse and office building (leased) | 23,000 | ||||

Suzhou, China 2 | A manufacturing, warehouse and office building (leased) | 22,000 | ||||

Lagny Sur Marne, France 1, 3 | An office building (leased) | 17,000 | ||||

Segrate, Italy 1, 3 | An office, laboratory and warehouse building (leased) | 7,000 | ||||

Singapore 1, 2, 3 | A warehouse and office building (leased) | 6,000 | ||||

Business Segment - Property Identification Legend

1 - Adhesive Dispensing Systems

2 - Advanced Technology Systems

3 - Industrial Coating Systems

The facilities listed above have adequate, suitable and sufficient capacity (production and nonproduction) to meet present and foreseeable demand for our products.

Other properties at international subsidiary locations and at branch locations within the United States are leased. Lease terms do not exceed 25 years and generally contain a provision for cancellation with some penalty at an earlier date.

In addition, we lease equipment under various operating and capitalized leases. Information about leases is reported in Note 6 of Notes to Consolidated Financial Statements that can be found in Part II, Item 8 of this document.

11

| Item 3. | Legal Proceedings |

We are involved in pending or potential litigation regarding environmental, product liability, patent, contract, employee and other matters arising from the normal course of business. Including the environmental matter discussed below, it is our opinion, after consultation with legal counsel, that resolutions of these matters are not expected to result in a material effect on our financial condition, quarterly or annual operating results or cash flows.

Environmental - We have voluntarily agreed with the City of New Richmond, Wisconsin and other Potentially Responsible Parties to share costs associated with the remediation of the City of New Richmond municipal landfill (the "Site") and constructing a potable water delivery system serving the impacted area down gradient of the Site. At October 31, 2011 and 2010, our accrual for the ongoing operation, maintenance and monitoring obligation at the Site was $795 and $885, respectively.

The liability for environmental remediation represents management's best estimate of the probable and reasonably estimable undiscounted costs related to known remediation obligations. The accuracy of our estimate of environmental liability is affected by several uncertainties such as additional requirements that may be identified in connection with remedial activities, the complexity and evolution of environmental laws and regulations, and the identification of presently unknown remediation requirements. Consequently, our liability could be greater than our current estimate. However, we do not expect that the costs associated with remediation will have a material adverse effect on our financial condition or results of operations.

| Item 4. | Removed and Reserved |

12

Executive Officers of the Company

Our executive officers as of October 31, 2011, were as follows:

Name | Age | Officer Since | Position or Office with The Company and Business Experience During the Past Five (5) Year Period | |||||||

Michael F. Hilton | 57 | 2010 | President and Chief Executive Officer, 2010 Senior Vice President and General Manager-Electronics and Performance Materials Segment of Air Products and Chemicals, Inc., 2007 Vice President and General Manager-Electronics and Performance Materials Segment of Air Products and Chemicals, Inc., 2006 | |||||||

John J. Keane | 50 | 2003 | Senior Vice President, 2005 | |||||||

Peter G. Lambert | 51 | 2005 | Senior Vice President, 2010 | |||||||

| Vice President, 2005 | ||||||||||

Douglas C. Bloomfield | 52 | 2005 | Vice President, 2005 | |||||||

Gregory P. Merk | 40 | 2006 | Vice President, 2006 | |||||||

Shelly M. Peet | 46 | 2007 | Vice President, 2009 | |||||||

| Vice President, Chief Information Officer, 2007 | ||||||||||

| Director, Corporate Information Services and Chief Information Officer, 2003 | ||||||||||

Gregory A. Thaxton | 50 | 2007 | Vice President, Chief Financial Officer, 2008 | |||||||

| Vice President, Controller, 2007 | ||||||||||

| Corporate Controller and Chief Accounting Officer, 2006 | ||||||||||

Robert E. Veillette | 59 | 2007 | Vice President, General Counsel and Secretary, 2007 | |||||||

| Secretary and Assistant General Counsel, 2002 | ||||||||||

13

PART II

| Item 5. | Market for the Company's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information and Dividends

(a) Our common shares are listed on the Nasdaq Global Select Market under the symbol NDSN. As of November 30, 2011, there were 1,698 registered shareholders. The table below is a summary of dividends paid per common share and the range of closing market prices during each quarter of 2011 and 2010.

| Dividend Paid | Common Share Price | |||||||||||

Quarters | High | Low | ||||||||||

2011: | ||||||||||||

First | $ | .105 | $ | 47.58 | $ | 38.06 | ||||||

Second | .105 | 58.75 | 47.56 | |||||||||

Third | .105 | 59.01 | 48.98 | |||||||||

Fourth | .125 | 50.50 | 37.21 | |||||||||

2010: | ||||||||||||

First | $ | .095 | $ | 31.94 | $ | 26.05 | ||||||

Second | .095 | 37.96 | 27.11 | |||||||||

Third | .095 | 36.87 | 27.39 | |||||||||

Fourth | .105 | 39.88 | 31.64 | |||||||||

Source: NASDAQ OMX

| (b) | Use of Proceeds. Not applicable. |

| (c) | Issuer Purchases of Equity Securities |

| Total Number of Shares Repurchased | Average Price Paid per Share | Total Number of Shares Repurchased as Part of Publicly Announced Plans or Programs (1) | Maximum Number or Approximate Value of Shares That May Yet Be Purchased Under the Plans or Programs (1) | |||||||||||||

August 1, 2011 to August 31, 2011 | 539 | $ | 43.40 | 539 | 939 | |||||||||||

September 1, 2011 to September 30, 2011 | 1,186 | $ | 41.73 | 1,186 | $ | 89,664 | ||||||||||

October 1, 2011 to October 31, 2011 | 448 | $ | 41.84 | 448 | $ | 70,905 | ||||||||||

|

|

|

| |||||||||||||

Total | 2,173 | 2,173 | ||||||||||||||

|

|

|

| |||||||||||||

(1) In May 2011, the board of directors approved a stock repurchase program of up to 2,000 shares. This program was completed in September 2011, and the board of directors approved an additional repurchase program of up to $100,000. Uses for repurchased shares include the funding of benefit programs including stock options, nonvested stock and 401(k) matching. Shares purchased are treated as treasury shares until used for such purposes. The repurchase programs are being funded using working capital and proceeds from borrowings under our credit facilities.

14

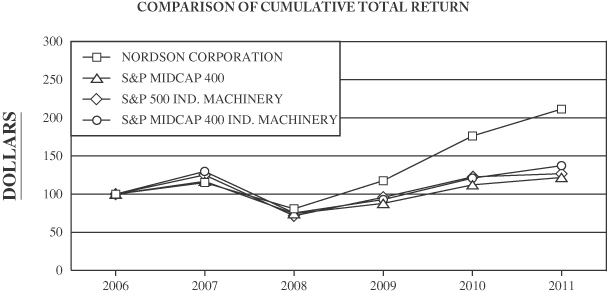

Performance Graph

The following is a graph that compares the five-year cumulative return, calculated on a dividend-reinvested basis, from investing $100 on November 1, 2006 in Nordson common shares, the S&P MidCap 400 Index, the S&P 500 Industrial Machinery Index, and the S&P MidCap 400 Industrial Machinery Index.

| Period Ending October 31 | ||||||||||||

| Company/Market/Peer Group | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | ||||||

Nordson Corporation | $100.00 | $115.32 | $80.62 | $117.69 | $176.15 | $211.33 | ||||||

S&P MidCap 400 | $100.00 | $117.02 | $74.35 | $ 87.87 | $112.15 | $121.74 | ||||||

S&P 500 Ind. Machinery | $100.00 | $125.19 | $71.65 | $ 95.87 | $122.67 | $126.92 | ||||||

S&P MidCap 400 Ind. Machinery | $100.00 | $129.99 | $75.26 | $ 93.04 | $120.92 | $137.53 | ||||||

Source: Morningstar

15

| Item 6. | Selected Financial Data |

Five-Year Summary

| 2011 | 2010 | 2009 | 2008 | 2007 | ||||||||||||||||

(In thousands except for per-share amounts) | ||||||||||||||||||||

Operating Data (a) | ||||||||||||||||||||

Sales | $ | 1,233,159 | $ | 1,041,551 | $ | 819,165 | $ | 1,124,829 | $ | 993,649 | ||||||||||

Cost of sales | 484,727 | 419,937 | 350,239 | 494,394 | 439,804 | |||||||||||||||

% of sales | 39 | 40 | 43 | 44 | 44 | |||||||||||||||

Selling and administrative expenses | 429,489 | 384,752 | 337,294 | 434,476 | 401,294 | |||||||||||||||

% of sales | 35 | 37 | 41 | 39 | 40 | |||||||||||||||

Severance and restructuring costs | 1,589 | 2,029 | 16,396 | 5,621 | 409 | |||||||||||||||

Goodwill and long-lived asset impairments | 1,811 | - | 243,043 | - | - | |||||||||||||||

Operating profit (loss) | 315,543 | 234,833 | (127,807 | ) | 190,338 | 152,142 | ||||||||||||||

% of sales | 26 | 23 | (16 | ) | 17 | 15 | ||||||||||||||

Net income (loss) | 222,364 | 168,048 | (160,055 | ) | 117,504 | 90,692 | ||||||||||||||

% of sales | 18 | 16 | (20 | ) | 10 | 9 | ||||||||||||||

Financial Data (a) | ||||||||||||||||||||

Working capital | $ | 294,796 | $ | 259,117 | $ | 190,249 | $ | 180,317 | $ | 180,010 | ||||||||||

Net property, plant and equipment and other non-current assets | 827,493 | 535,323 | 544,003 | 782,356 | 801,916 | |||||||||||||||

Total invested capital (b) | 853,071 | 567,323 | 508,989 | 847,253 | 846,911 | |||||||||||||||

Total assets | 1,304,450 | 986,354 | 890,674 | 1,166,669 | 1,211,840 | |||||||||||||||

Long-term liabilities | 550,966 | 289,368 | 364,276 | 388,561 | 450,809 | |||||||||||||||

Shareholders' equity | 571,323 | 505,072 | 369,976 | 574,112 | 531,117 | |||||||||||||||

Return on average invested capital - % (c) | 35 | 32 | 10 | (d) | 15 | 14 | ||||||||||||||

Return on average shareholders' equity - % (e) | 39 | 40 | 13 | (f) | 20 | 19 | ||||||||||||||

Per-Share Data (a)(g) | ||||||||||||||||||||

Average number of common shares | 67,616 | 67,610 | 67,129 | 67,492 | 67,094 | |||||||||||||||

Average number of common shares and common share equivalents | 68,425 | 68,442 | 67,129 | 68,613 | 68,363 | |||||||||||||||

Basic earnings (loss) per share | $ | 3.29 | $ | 2.49 | $ | (2.38 | ) | $ | 1.74 | $ | 1.35 | |||||||||

Diluted earnings (loss) per share | 3.25 | 2.46 | (2.38 | ) | 1.71 | 1.33 | ||||||||||||||

Dividends per common share | 0.44 | 0.39 | 0.36875 | 0.365 | 0.35 | |||||||||||||||

Book value per common share | 8.71 | 7.44 | 5.49 | 8.52 | 7.88 | |||||||||||||||

| (a) | See accompanying Notes to Consolidated Financial Statements. |

| (b) | Notes payable, plus current portion of long-term debt, plus long-term debt, minus cash and marketable securities, plus shareholders' equity. |

| (c) | Net income (loss), plus after-tax interest expense on borrowings as a percentage of average quarterly borrowings (net of cash) plus average quarterly shareholders' equity over five accounting periods. |

| (d) | The percentage for 2009 excludes goodwill and long-lived asset impairment charges. Including these charges, the return on average invested capital for 2009 would have been negative 21 percent. |

| (e) | Net income (loss) as a percentage of average quarterly shareholders' equity over five accounting periods. |

| (f) | The percentage for 2009 excludes goodwill and long-lived asset impairment charges. Including these charges, the return on average shareholder equity for 2009 would have been negative 28 percent. |

| (g) | Amounts adjusted for 2-for-1 stock split effective April 12, 2011. |

16

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations |

NOTE REGARDING AMOUNTS AND FISCAL YEAR REFERENCES

In this annual report, all amounts related to United States dollars and foreign currency and to the number of Nordson Corporation's common shares, except for per share earnings and dividend amounts, are expressed in thousands.

Unless otherwise noted, all references to years relate to our fiscal year ending October 31.

Critical Accounting Policies and Estimates

Our consolidated financial statements and accompanying notes have been prepared in accordance with accounting principles generally accepted in the United States. The preparation of these financial statements requires management to make estimates, judgments and assumptions that affect reported amounts of assets, liabilities, revenues and expenses. On an ongoing basis, we evaluate the accounting policies and estimates that are used to prepare financial statements. We base our estimates on historical experience and assumptions believed to be reasonable under current facts and circumstances. Actual amounts and results could differ from these estimates used by management.

Certain accounting policies that require significant management estimates and are deemed critical to our results of operations or financial position are discussed below. On a regular basis, critical accounting policies are reviewed with the Audit Committee of the board of directors.

Revenue Recognition - Most of our revenues are recognized upon shipment, provided that persuasive evidence of an arrangement exists, the sales price is fixed or determinable, collectibility is reasonably assured, and title and risk of loss have passed to the customer. In October 2009, the FASB issued an accounting standard update on multiple deliverable arrangements, which we adopted on November 1, 2010. This accounting standard update establishes a relative selling price hierarchy for determining the selling price of a deliverable based on vendor specific objective evidence (VSOE) if available, third-party evidence (TPE) if vendor-specific objective evidence is not available, or best estimated selling price (BESP) if neither vendor-specific objective evidence nor third-party evidence is available. Our multiple deliverable arrangements include installation, installation supervision, training, and spare parts, which tend to be completed in a short period of time, at an insignificant cost, and utilizing skills not unique to us, and, therefore, are typically regarded as inconsequential or perfunctory. Revenue for undelivered items is deferred and included within accrued liabilities in the accompanying balance sheet. Revenues deferred in 2011, 2010 and 2009 were not material. The requirements of this standard did not significantly change our units of accounting or how we allocate arrangement consideration to various units of accounting. The adoption of this standard had no material impact on our financial position or results of operations.

Goodwill - Goodwill is the excess of purchase price over the fair value of tangible and identifiable intangible net assets acquired in various business combinations. Goodwill is not amortized but is tested for impairment annually at the reporting unit level, or more often if indications of impairment exist. Our reporting units are the Adhesive Dispensing Systems segment, the Industrial Coating Systems segment and one level below the Advanced Technology Systems segment.

The goodwill impairment test is a two-step process. In the first step, performed in the fourth quarter of each year, we calculate a reporting unit's fair value using a discounted cash flow valuation methodology and compare the result against the reporting unit's carrying value of net assets. If the carrying value of a reporting unit exceeds its fair value, then a second step is performed to determine if goodwill is impaired. In step one, the assumptions used for discounted cash flow, revenue growth, operating margin, and working capital turnover are based on general management's strategic plans tempered by performance trends and reasonable expectations about those trends. Terminal value calculations employ a published formula known as the "Gordon Growth Model Method" that essentially captures the present value of perpetual cash flows beyond the last projected period assuming a constant Weighted Average Cost of Capital methodology (WACC) and growth rate. For each reporting unit, sensitivity calculations vary the discount and terminal growth rates in order to provide a range of assurance that our expected assumptions are fair for detecting impairment.

17

Discount rates were developed using a WACC methodology. The WACC represents the blended average required rate of return for equity and debt capital based on observed market return data and company specific risk factors. For 2011, the discount rates used ranged from 10 percent to 19 percent depending upon the reporting unit's size, end market volatility, and projection risk. The calculated internal rate of return for the step one consolidated valuation was 11.3 percent, the same as the calculated WACC for total Nordson.

To test the reasonableness of the discounted cash flow valuations, we performed the control premium test, which compares the sum of the fair values calculated for our reporting units (net of debt) to the market value of equity. The control premium was negative 11 percent as of the test date of August 1, 2011 and 0 percent as of our year-end of October 31, 2011. These comparisons indicated that the discounted cash flow valuation was reasonable. In addition, indications of value derived for each reporting unit using the market approach reconciled reasonably with the results of the discounted cash flow approach.

In 2011 and 2010, the results of our step one testing indicated no impairment; therefore, the second step of impairment testing was not necessary.

In 2009, we determined that the second step of impairment testing was necessary. In the second step, a hypothetical purchase price allocation of the reporting unit's assets and liabilities is performed using the fair value calculated in step one. The difference between the fair value of the reporting unit and the hypothetical fair value of assets and liabilities is the implied goodwill amount. Impairment is recorded if the carrying value of the reporting unit's goodwill is higher than its implied goodwill. Based upon the results of our impairment testing, we recognized an impairment charge for a reduction in the carrying value of goodwill in the amount of $232,789, relating to six reporting units as follows: Dage $166,916, Picodostec $7,530, YESTech $26,149, March Plasma Systems $16,449, UV Curing $12,129, and Industrial Coating Systems $3,616.

The excess of fair value (FV) over carrying value (CV) was compared to the carrying value for each reporting unit. Based on the results shown in the table below and based on our measurement date of August 1, 2011, our conclusion is that no indicators of impairment exist in 2011. Potential events or circumstances, such as a sustained downturn in global economies, could have a negative effect on estimated fair values.

| WACC | Excess of FV over CV | Goodwill | ||||||||||

Adhesive Dispensing | 10.0 | % | 792 | % | $ | 42,427 | ||||||

Asymtek | 13.5 | % | 2939 | % | $ | 15,151 | ||||||

EFD | 12.0 | % | 92 | % | $ | 297,632 | ||||||

Dage and YESTech | 19.0 | % | 54 | % | $ | 14,397 | ||||||

We acquired Value Plastics, Inc ("Value Plastics") on August 26, 2011, subsequent to the measurement date for impairment testing. Determination of the preliminary fair value associated with this acquisition was completed with the assistance of an independent valuation specialist on October 5, 2011. Since the date of valuation, no events or changes in circumstances have occurred that would more likely than not reduce the fair value of Value Plastics below its carrying value. For future valuation purposes, Value Plastics will be a component of EFD.

Other Long-Lived Assets - Our test for recoverability of long-lived depreciable and amortizable assets uses undiscounted cash flows. Long-lived assets are grouped at the lowest level for which there are identifiable cash flows. The total carrying value of long-lived assets for each reporting unit has been compared to the forecasted cash flows of each reporting unit's long-lived assets being tested. Cash flows have been defined as earnings before interest, taxes, depreciation, and amortization, less annual maintenance capital spending.

Estimates of future cash flows used to test the recoverability of a long-lived asset (asset group) are based on the remaining useful life of the asset. We believe that the relative value of long-lived assets within each reporting unit is a reasonable proxy for the relative importance of the assets in the production of cash flow. To get to a reasonable forecast period, the aggregate net book value of long-lived assets was divided by the current depreciation and amortization value to arrive at a blended remaining useful life. Our calculations for 2011 showed the undiscounted aggregate value of cash flows over the remaining useful life for each reporting unit was greater than the respective carrying value of the long-lived assets within each reporting unit, so no impairment charges were recognized.

18

Inventories - Inventories are valued at the lower of cost or market. Cost was determined using the last-in, first-out (LIFO) method for 26 percent of consolidated inventories at October 31, 2011, and 25 percent at October 31, 2010, with the first-in, first-out (FIFO) method used for the remaining inventory. On an ongoing basis, inventory is tested for technical obsolescence, as well as for future demand and changes in market conditions. We have historically maintained inventory reserves to reflect those conditions when the cost of inventory is not expected to be recovered. Reserves are also maintained for inventory used for demonstration purposes. The inventory reserve balance was $16,050, $16,802 and $15,740 at October 31, 2011, 2010 and 2009, respectively.

Pension Plans and Postretirement Medical Plans - The measurement of liabilities related to our pension plans and postretirement medical plans is based on management's assumptions related to future factors, including interest rates, return on pension plan assets, compensation increases, mortality and turnover assumptions, and health care cost trend rates.

The weighted-average discount rate used to determine the present value of our domestic pension plan obligations was 4.46 percent at October 31, 2011 and 5.21 percent at October 31, 2010. The discount rate for these plans, which comprised 79 percent of the worldwide pension obligations at October 31, 2011, was based on quality fixed income investments with a duration period approximately equal to the period over which pension obligations are expected to be settled. The weighted-average discount rate used to determine the present value of our various international pension plan obligations was 4.43 percent at October 31, 2011, compared to 4.17 percent at October 31, 2010. The discount rates used for the international plans were determined by using quality fixed income investments with a duration period approximately equal to the period over which pension obligations are expected to be settled.

In determining the expected return on plan assets, we consider both historical performance and an estimate of future long-term rates of return on assets similar to those in our plans. We consult with and consider the opinions of financial and actuarial experts in developing appropriate return assumptions. The expected rate of return (long-term investment rate) on domestic pension assets used to determine net benefit costs was 8.25 percent in 2011 and 8.51 percent in 2010. The average expected rate of return on international pension assets used to determine net benefit costs was 4.84 percent in 2011 and 4.85 percent in 2010.

The assumed rate of compensation increases used to determine the present value of our domestic pension plan obligations was 3.20 percent at October 31, 2011 and 3.30 percent at October 31, 2010. The assumed rate of compensation increases used to determine the present value of our international pension plan obligations was 3.16 percent at October 31, 2011, compared to 3.21 percent at October 31, 2010.

Annual expense amounts are determined based on the discount rate used at the end of the prior year. Differences between actual and assumed investment returns on pension plan assets result in actuarial gains or losses that are amortized into expense over a period of years.

Economic assumptions have a significant effect on the amounts reported. The effect of a one percent change in the discount rate, expected return on assets and compensation increase is shown in the table below. Bracketed numbers represent decreases in expense and obligation amounts.

| United States | International | |||||||||||||||

| 1% Point Increase | 1% Point Decrease | 1% Point Increase | 1% Point Decrease | |||||||||||||

Discount rate: | ||||||||||||||||

Effect on total service and interest cost components in 2011 | $ | (3,107 | ) | $ | 3,696 | $ | (324 | ) | $ | 405 | ||||||

Effect on pension obligation as of October 31, 2011 | $ | (34,776 | ) | $ | 43,229 | $ | (11,917 | ) | $ | 13,847 | ||||||

Expected return on assets: | ||||||||||||||||

Effect on total service and interest cost components in 2011 | $ | (1,889 | ) | $ | 1,888 | $ | (302 | ) | $ | 301 | ||||||

Effect on pension obligation as of October 31, 2011 | $ | - | $ | - | $ | - | $ | - | ||||||||

Compensation increase: | ||||||||||||||||

Effect on total service and interest cost components in 2011 | $ | 2,816 | $ | (2,291 | ) | $ | 462 | $ | (420 | ) | ||||||

Effect on pension obligation as of October 31, 2011 | $ | 14,649 | $ | (12,040 | ) | $ | 8,575 | $ | (7,062 | ) | ||||||

19

With respect to the domestic postretirement medical plan, the discount rate used to value the benefit obligation decreased from 5.25 percent at October 31, 2010 to 4.50 percent at October 31, 2011. The annual rate of increase in the per capita cost of covered benefits (the health care cost trend rate) is assumed to be 9.36 percent in 2012, decreasing gradually to 5.00 percent in 2016.

For the international postretirement plan, the discount rate used to value the benefit obligation was 5.85 percent at October 31, 2011 and 5.75 percent at October 31, 2010. The annual rate of increase in the per capita cost of covered benefits (the health care cost trend rate) is assumed to be 7.00 percent in 2012, decreasing gradually to 3.50 percent in 2031.

The discount rate and the health care cost trend rate assumptions have a significant effect on the amounts reported. For example, a one-percentage point change in the discount rate and assumed health care cost trend rate would have the following effects:

| United States | International | |||||||||||||||

| 1% Point Increase | 1% Point Decrease | 1% Point Increase | 1% Point Decrease | |||||||||||||

Discount rate: | ||||||||||||||||

Effect on total service and interest cost components in 2011 | $ | (628 | ) | $ | 753 | $ | (9 | ) | $ | 11 | ||||||

Effect on postretirement obligation as of October 31, 2011 | $ | (10,119 | ) | $ | 12,871 | $ | (135 | ) | $ | 181 | ||||||

Health care trend rate: | ||||||||||||||||

Effect on total service and interest cost components in 2011 | $ | 871 | $ | (688 | ) | $ | 19 | $ | (14 | ) | ||||||

Effect on postretirement obligation as of October 31, 2011 | $ | 11,804 | $ | (9,476 | ) | $ | 174 | $ | (132 | ) | ||||||

Employees hired after January 1, 2002, are not eligible to participate in the domestic postretirement medical plan.

Pension and postretirement expenses in 2012 are expected to be approximately $7,000 higher than 2011, primarily due to changes in the discount rate, expected rate of return on assets and changes in demographic assumptions.

Financial Instruments - Assets, liabilities and commitments that are to be settled in cash and are denominated in foreign currencies are sensitive to changes in currency exchange rates. We enter into foreign currency forward contracts, which are derivative financial instruments, to reduce the risk of foreign currency exposures resulting from the collection of receivables, payables and loans denominated in foreign currencies. The maturities of these contracts are usually less than 90 days. Forward contracts are not designated as hedging instruments and therefore are marked to market each accounting period, and the resulting gains or losses are included in "other-net" within other income (expense) in the Consolidated Statement of Income.

Warranties - We provide customers with a product warranty that requires us to repair or replace defective products within a specified period of time (generally one year) from the date of delivery or first use. An accrual is recorded for expected warranty costs for products shipped through the end of each accounting period. In determining the amount of the accrual, we rely primarily on historical warranty claims. Amounts charged to the warranty reserve were $7,217, $6,068 and $3,824 in 2011, 2010 and 2009, respectively. The reserve balance was $6,528, $5,242 and $4,587 at October 31, 2011, 2010 and 2009, respectively.

Long-Term Incentive Plan (LTIP) - Under the long-term incentive plan, executive officers and selected other key employees receive share awards based solely on corporate performance measures over three-year performance periods. Awards vary based on the degree to which corporate performance equals or exceeds predetermined threshold, target and maximum performance levels at the end of a performance period. No award will occur unless certain threshold performance objectives are equaled or exceeded. The amount of compensation expense is based upon current performance projections for each three-year period and the percentage of the requisite service that has been rendered. The calculations are also based upon the grant date fair value determined using the closing market price of common stock at the grant date, reduced by the implied value of dividends not to be paid. Awards are recorded as capital in excess of stated value in shareholders' equity. The amount recorded at October 31, 2011 for the plans originating in 2009, 2010 and 2011 was $6,081.

20

Compensation expense attributable to all LTIP performance periods for executive officers and selected other key employees for 2011 and 2010 was $4,067 and $3,879, respectively. There was $5,014 credited to expense in 2009 due to economic effects.

2011 and 2010