(Exact name of Registrant

as specified in its charter)

(Exact name of Registrant

as specified in its charter) | Delaware (State or other jurisdiction of incorporation�or�organization) | 1585 Broadway New�York,�NY�10036 (Address�of�principal�executive�offices, including zip code) | 36-3145972 (I.R.S.�Employer�Identification�No.) | (212) 761-4000 (Registrant�s�telephone�number, including area code) |

| Securities registered pursuant to Section�12(b) of the Act: | ||||

| Title of each class | Name�of�exchange�on which registered | |||

| Common Stock, $0.01 par value | New�York�Stock�Exchange | |||

| Depositary Shares, each representing 1/1,000th interest in a share of Floating Rate Non-Cumulative Preferred Stock, Series�A, $0.01�par value | New York Stock Exchange | |||

| Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series�E, $0.01�par value | New York Stock Exchange | |||

| Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series�F, $0.01�par value | New York Stock Exchange | |||

| Depositary Shares, each representing 1/1,000th interest in a share of 6.625% Non-Cumulative Preferred Stock, Series�G, $0.01�par value | New York Stock Exchange | |||

| Depositary Shares, each representing 1/1,000th interest in a share of Fixed-to-Floating Rate Non-Cumulative Preferred Stock, Series�I, $0.01�par value | New York Stock Exchange | |||

| 6 1 / 4 % Capital Securities of Morgan Stanley Capital Trust III (and Registrant�s guarantee with respect thereto) | New York Stock Exchange | |||

| 6 1 / 4 % Capital Securities of Morgan Stanley Capital Trust IV (and Registrant�s guarantee with respect thereto) | New York Stock Exchange | |||

| 5 3 / 4 % Capital Securities of Morgan Stanley Capital Trust V (and Registrant�s guarantee with respect thereto) | New York Stock Exchange | |||

| 6.45% Capital Securities of Morgan Stanley Capital Trust VIII (and Registrant�s guarantee with respect thereto) | New York Stock Exchange | |||

| Global Medium-Term Notes, Series A, Fixed Rate Step-Up Senior Notes Due 2026 of Morgan Stanley Finance LLC (and Registrant�s guarantee with respect thereto) | New York Stock Exchange | |||

| Market Vectors ETNs due March�31, 2020 (2 issuances); Market Vectors ETNs due April�30, 2020 (2 issuances) | NYSE Arca, Inc. | |||

| Morgan Stanley Cushing � MLP High Income Index ETNs due March�21, 2031 | NYSE Arca, Inc. | |||

| Large Accelerated Filer x Non-Accelerated�Filer � (Do not check if a smaller reporting company) | Accelerated�Filer � Smaller reporting company � |

ANNUAL REPORT ON FORM

10-K for the year ended December�31, 2015 | Table�of�Contents | Page | |||||

| Part I | ||||||

| Item�1. | Business | 1 | ||||

| Overview | 1 | |||||

| Business Segments | 1 | |||||

| Competition | 1 | |||||

| Supervision and Regulation | 2 | |||||

| Executive Officers of Morgan Stanley | 11 | |||||

| Item�1A. | Risk Factors | 13 | ||||

| Item�1B. | Unresolved Staff Comments | 23 | ||||

| Item�2. | Properties | 23 | ||||

| Item�3. | Legal Proceedings | 24 | ||||

| Item�4. | Mine Safety Disclosures | 32 | ||||

| Part�II | ||||||

| Item 5. | Market for Registrant�s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 33 | ||||

| Item 6. | Selected Financial Data | 36 | ||||

| Item 7. | Management�s Discussion and Analysis of Financial Condition and Results of Operations | 38 | ||||

| Introduction | 38 | |||||

| Executive Summary | 39 | |||||

| Business Segments | 46 | |||||

| Supplemental Financial Information and Disclosures | 67 | |||||

| Accounting Developments Updates | 70 | |||||

| Critical Accounting Policies | 71 | |||||

| Liquidity and Capital Resources | 75 | |||||

| Item�7A. | Quantitative and Qualitative Disclosures about Market Risk | 98 | ||||

| Item 8. | Financial Statements and Supplementary Data | 121 | ||||

| Report of Independent Registered Public Accounting Firm | 121 | |||||

| Consolidated Statements of Income | 122 | |||||

| Consolidated Statements of Comprehensive Income | 123 | |||||

| Consolidated Statements of Financial Condition | 124 | |||||

| Consolidated Statements of Changes in Total Equity | 125 | |||||

| Consolidated Statements of Cash Flows | 126 | |||||

| Notes to Consolidated Financial Statements | 127 | |||||

| 1. Introduction and Basis of Presentation | 127 | |||||

| 2. Significant Accounting Policies | 129 | |||||

| 3. Fair Values | 141 | |||||

| 4. Derivative Instruments and Hedging Activities | 167 | |||||

| 5. Investment Securities | 176 | |||||

| 6. Collateralized Transactions | 181 | |||||

| 7. Loans and Allowance for Credit Losses | 185 | |||||

| 8. Equity Method Investments | 191 | |||||

| 9. Goodwill and Net Intangible Assets | 191 | |||||

| 10. Deposits | 193 | |||||

| 11. Borrowings and Other Secured Financings | 194 | |||||

| i |  |

| Table�of�Contents | Page | |||||

| 12. Commitments, Guarantees and Contingencies | 197 | |||||

| 13. Variable Interest Entities and Securitization Activities | 205 | |||||

| 14. Regulatory Requirements | 214 | |||||

| 15. Total Equity | 218 | |||||

| 16. Earnings per Common Share | 222 | |||||

| 17. Interest Income and Interest Expense | 223 | |||||

| 18. Deferred Compensation Plans | 223 | |||||

| 19. Employee Benefit Plans | 228 | |||||

| 20. Income Taxes | 237 | |||||

| 21. Segment and Geographic Information | 241 | |||||

| 22. Parent Company | 245 | |||||

| 23. Quarterly Results (Unaudited) | 249 | |||||

| 24. Subsequent Events | 250 | |||||

| Financial Data Supplement (Unaudited) | 251 | |||||

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 259 | ||||

| Item�9A. | Controls and Procedures | 259 | ||||

| Item�9B. | Other Information | 261 | ||||

| Part III | ||||||

| Item 10. | Directors, Executive Officers and Corporate Governance | 262 | ||||

| Item 11. | Executive Compensation | 262 | ||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 262 | ||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 262 | ||||

| Item 14. | Principal Accounting Fees and Services | 262 | ||||

| Part IV | ||||||

| Item�15. | Exhibits, Financial Statement Schedules | 263 | ||||

| Signatures | S-1 | |||||

| Exhibit Index | E-1 | |||||

| | ii |

| � | the effect of economic and political conditions and geopolitical events; |

| � | sovereign risk; |

| � | the effect of market conditions, particularly in the global equity, fixed income, currency, credit and commodities markets, including corporate and mortgage (commercial and residential) lending and commercial real estate markets and energy markets; |

| � | the impact of current, pending and future legislation (including the Dodd-Frank Wall Street Reform and Consumer Protection Act (the �Dodd-Frank�Act�)), regulation (including capital, leverage, funding and liquidity requirements), policies (including fiscal and monetary), and legal and regulatory actions in the United States of America (�U.S.�) and worldwide; |

| � | the level and volatility of equity, fixed income and commodity prices (including oil prices), interest rates, currency values and other market indices; |

| � | the availability and cost of both credit and capital as well as the credit ratings assigned to our unsecured short-term and long-term debt; |

| � | investor, consumer and business sentiment and confidence in the financial markets; |

| � | the performance and results of our acquisitions, divestitures, joint ventures, strategic alliances or other strategic arrangements; |

| � | our reputation and the general perception of the financial services industry; |

| � | inflation, natural disasters, pandemics and acts of war or terrorism; |

| � | the actions and initiatives of current and potential competitors as well as governments, regulators and self-regulatory organizations; |

| � | the effectiveness of our risk management policies; |

| � | technological changes instituted by us, our competitors or counterparties and technological risks, including cybersecurity, business continuity and related operational risks; |

| � | our ability to provide innovative products and services and execute our strategic objectives; and |

| � | other risks and uncertainties detailed under �Business�Competition� and �Business�Supervision and Regulation� in Part I, Item�1, �Risk Factors� in Part I, Item�1A and elsewhere throughout this report. |

| iii | |

| � | Amended and Restated Certificate of Incorporation; |

| � | Amended and Restated Bylaws; |

| � | Charters for its Audit Committee, Compensation, Management Development and Succession Committee, Nominating and Governance Committee, Operations and Technology Committee, and Risk Committee; |

| � | Corporate Governance Policies; |

| � | Policy Regarding Communication with the Board of Directors; |

| � | Policy Regarding Director Candidates Recommended by Shareholders; |

| � | Policy Regarding Corporate Political Activities; |

| � | Policy Regarding Shareholder Rights Plan; |

| � | Equity Ownership Commitment; |

| � | Code of Ethics and Business Conduct; |

| � | Code of Conduct; and |

| � | Integrity Hotline information. |

| | iv |

| Item�1. | Business. |

| 1 | |

| | 2 |

| � | A minimum Common Equity Tier 1 capital ratio of 4.5%; Tier 1 capital ratio of 6.0%; Total capital ratio of 8.0%; and Tier 1 leverage ratio of 4.0%; |

| � | A supplementary leverage ratio of at least 5.0%, which includes a Tier 1 supplementary leverage capital buffer of at least 2.0% in addition to the 3.0% minimum supplementary leverage ratio; |

| 3 | |

| � | A greater than 2.5% Common Equity Tier 1 capital conservation buffer; |

| � | Up to a 2.5% Common Equity Tier 1 countercyclical buffer, if deployed by banking regulators; and |

| � | A global systemically important bank capital surcharge, which the Federal Reserve calculated at 3% for the Company in July 2015. |

| | 4 |

| 5 | |

| | 6 |

| 7 | |

| | 8 |

| 9 | |

| | 10 |

| 11 | |

| | 12 |

| Item�1A. | Risk Factors. |

| 13 | |

| | 14 |

| 15 | |

| | 16 |

| 17 | |

| | 18 |

| 19 | |

| | 20 |

| 21 | |

| | 22 |

| Item�1B. | Unresolved Staff Comments. |

| Item�2. | Properties. |

| Location | Owned/ Leased | Lease Expiration | Approximate�Square�Footage as of December�31, 2015(1) | |||||||

| U.S. Locations | ||||||||||

| 1585 Broadway New York, New York (Global Headquarters and Institutional Securities Headquarters) | Owned | N/A | 1,332,700�square�feet | |||||||

| 2000 Westchester Avenue Purchase, New York (Wealth Management Headquarters) | Owned | N/A | 597,400 square feet | |||||||

| 522 Fifth Avenue New York, New York (Investment Management Headquarters) | Owned | N/A | 571,800 square feet | |||||||

| International Locations | ||||||||||

| 20 Bank Street London (London Headquarters) | Leased | 2038 | 546,500 square feet | |||||||

| 1 Austin Road West Kowloon (Hong Kong Headquarters) | Leased | 2019 | 499,900 square feet | |||||||

| Otemachi Financial City South Tower Otemachi, Chiyoda-ku (Tokyo Headquarters) | Leased | 2028 | 245,600 square feet | |||||||

| (1) | The indicated total aggregate square footage leased does not include space leased by Morgan Stanley branch offices. |

| 23 | |

| Item�3. | Legal Proceedings. |

| | 24 |

| 25 | |

| | 26 |

| 27 | |

| | 28 |

| 29 | |

| | 30 |

| 31 | |

| Item�4. | Mine Safety Disclosures. |

| | 32 |

| Item�5. | Market for Registrant�s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

| Low Sale�Price | High Sale�Price | Dividends Declared�per Common�Share | ||||||||||

| 2015: | ||||||||||||

| Fourth Quarter | $ | 30.15 | $ | 35.74 | $ | 0.15 | ||||||

| Third Quarter | $ | 30.40 | $ | 41.04 | $ | 0.15 | ||||||

| Second Quarter | $ | 35.36 | $ | 40.26 | $ | 0.15 | ||||||

| First Quarter | $ | 33.72 | $ | 39.15 | $ | 0.10 | ||||||

| 2014: | ||||||||||||

| Fourth Quarter | $ | 31.35 | $ | 39.19 | $ | 0.10 | ||||||

| Third Quarter | $ | 31.12 | $ | 36.44 | $ | 0.10 | ||||||

| Second Quarter | $ | 28.31 | $ | 32.82 | $ | 0.10 | ||||||

| First Quarter | $ | 28.78 | $ | 33.52 | $ | 0.05 | ||||||

| 33 | |

| Period | Total Number�of Shares Purchased | Average�Price Paid� per Share | Total�Number�of Shares�Purchased as�Part� of�Publicly Announced Plans or Programs(1) | Approximate�Dollar Value of Shares That May Yet Be Purchased under the Plans or Programs | ||||||||||||

| Month #1 (October 1, 2015-October 31, 2015) | ||||||||||||||||

| Share Repurchase Program(2) | 2,448,000 | $ | 32.17 | 2,448,000 | $ | 1,796 | ||||||||||

| Employee transactions(3) | 83,738 | $ | 32.06 | � | � | |||||||||||

| Month #2 (November 1, 2015-November 30, 2015) | ||||||||||||||||

| Share Repurchase Program(2) | 7,985,128 | $ | 33.99 | 7,985,128 | $ | 1,525 | ||||||||||

| Employee transactions(3) | 243,334 | $ | 34.58 | � | � | |||||||||||

| Month #3 (December 1, 2015-December 31, 2015) | ||||||||||||||||

| Share Repurchase Program(2) | 8,210,166 | $ | 33.47 | 8,210,166 | $ | 1,250 | ||||||||||

| Employee transactions(3) | 72,712 | $ | 33.87 | � | � | |||||||||||

| Quarter ended at December�31, 2015 | ||||||||||||||||

| Share Repurchase Program(2) | 18,643,294 | $ | 33.52 | 18,643,294 | $ | 1,250 | ||||||||||

| Employee transactions(3) | 399,784 | $ | 33.92 | � | � | |||||||||||

| (1) | Share purchases under publicly announced programs are made pursuant to open-market purchases, Rule 10b5-1 plans or privately negotiated transactions (including with employee benefit plans) as market conditions warrant and at prices the Company deems appropriate and may be suspended at any time. |

| (2) | The Company�s Board of Directors has authorized the repurchase of the Company�s outstanding stock under a share repurchase program (the �Share Repurchase Program�). The Share Repurchase Program is a program for capital management purposes that considers, among other things, business segment capital needs, as well as stock-based compensation and benefit plan requirements. The Share Repurchase Program has no set expiration or termination date. Share repurchases by the Company are subject to regulatory approval. In March 2015, the Company received no objection from the Federal Reserve to repurchase up to $3.1 billion of the Company�s outstanding common stock during the period that began April�1, 2015 through June�30, 2016 under the Company�s 2015 capital plan. During the quarter ended December�31, 2015, the Company repurchased approximately $625 million of the Company�s outstanding common stock as part of its Share Repurchase Program. For further information, see �Liquidity and Capital Resources�Capital Management� in Part II, Item�7. |

| (3) | Includes shares acquired by the Company in satisfaction of the tax withholding obligations on stock-based awards and the exercise price of stock options granted under the Company�s stock-based compensation plans. |

| | 34 |

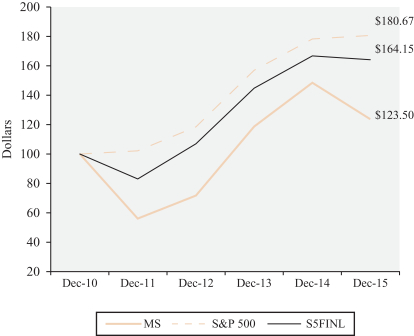

| MS | S&P�500 | S5FINL | ||||||||||

| 12/31/2010 | $ | 100.00 | $ | 100.00 | $ | 100.00 | ||||||

| 12/31/2011 | $ | 56.07 | $ | 102.10 | $ | 82.94 | ||||||

| 12/31/2012 | $ | 71.73 | $ | 118.44 | $ | 106.78 | ||||||

| 12/31/2013 | $ | 118.60 | $ | 156.78 | $ | 144.79 | ||||||

| 12/31/2014 | $ | 148.35 | $ | 178.22 | $ | 166.76 | ||||||

| 12/31/2015 | $ | 123.50 | $ | 180.67 | $ | 164.15 | ||||||

| 35 | |

| Item�6. | Selected Financial Data. |

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| Income Statement Data: | ||||||||||||||||||||

| Revenues: | ||||||||||||||||||||

| Total non-interest revenues | $ | 32,062 | $ | 32,540 | $ | 31,715 | $ | 26,383 | $ | 31,953 | ||||||||||

| Interest income | 5,835 | 5,413 | 5,209 | 5,692 | 7,234 | |||||||||||||||

| Interest expense | 2,742 | 3,678 | 4,431 | 5,897 | 6,883 | |||||||||||||||

| Net interest | 3,093 | 1,735 | 778 | (205 | ) | 351 | ||||||||||||||

| Net revenues | 35,155 | 34,275 | 32,493 | 26,178 | 32,304 | |||||||||||||||

| Non-interest expenses: | ||||||||||||||||||||

| Compensation and benefits | 16,016 | 17,824 | 16,277 | 15,615 | 16,325 | |||||||||||||||

| Other | 10,644 | 12,860 | 11,658 | 9,967 | 9,792 | |||||||||||||||

| Total non-interest expenses | 26,660 | 30,684 | 27,935 | 25,582 | 26,117 | |||||||||||||||

| Income from continuing operations before income taxes | 8,495 | 3,591 | 4,558 | 596 | 6,187 | |||||||||||||||

| Provision for (benefit from) income taxes | 2,200 | (90 | ) | 902 | (161 | ) | 1,491 | |||||||||||||

| Income from continuing operations | 6,295 | 3,681 | 3,656 | 757 | 4,696 | |||||||||||||||

| Discontinued operations: | ||||||||||||||||||||

| Income (loss) from discontinued operations before income taxes | (23 | ) | (19 | ) | (72 | ) | (48 | ) | (170 | ) | ||||||||||

| Provision for (benefit from) income taxes | (7 | ) | (5 | ) | (29 | ) | (7 | ) | (119 | ) | ||||||||||

| Income (loss) from discontinued operations | (16 | ) | (14 | ) | (43 | ) | (41 | ) | (51 | ) | ||||||||||

| Net income | 6,279 | 3,667 | 3,613 | 716 | 4,645 | |||||||||||||||

| Net income applicable to redeemable noncontrolling interests(1) | � | � | 222 | 124 | � | |||||||||||||||

| Net income applicable to nonredeemable noncontrolling interests(1) | 152 | 200 | 459 | 524 | 535 | |||||||||||||||

| Net income applicable to Morgan Stanley | $ | 6,127 | $ | 3,467 | $ | 2,932 | $ | 68 | $ | 4,110 | ||||||||||

| Preferred stock dividends and other | 456 | 315 | 277 | 98 | 2,043 | |||||||||||||||

| Earnings (loss) applicable to Morgan Stanley common shareholders(2) | $ | 5,671 | $ | 3,152 | $ | 2,655 | $ | (30 | ) | $ | 2,067 | |||||||||

| Amounts applicable to Morgan Stanley: | ||||||||||||||||||||

| Income from continuing operations | $ | 6,143 | $ | 3,481 | $ | 2,975 | $ | 138 | $ | 4,168 | ||||||||||

| Income (loss) from discontinued operations | (16 | ) | (14 | ) | (43 | ) | (70 | ) | (58 | ) | ||||||||||

| Net income applicable to Morgan Stanley | $ | 6,127 | $ | 3,467 | $ | 2,932 | $ | 68 | $ | 4,110 | ||||||||||

| | 36 |

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||

| Per Share Data: | ||||||||||||||||||||

| Earnings (loss) per basic common share(3): | ||||||||||||||||||||

| Income from continuing operations | $ | 2.98 | $ | 1.65 | $ | 1.42 | $ | 0.02 | $ | 1.28 | ||||||||||

| Income (loss) from discontinued operations | (0.01 | ) | (0.01 | ) | (0.03 | ) | (0.04 | ) | (0.03 | ) | ||||||||||

| Earnings (loss) per basic common share | $ | 2.97 | $ | 1.64 | $ | 1.39 | $ | (0.02 | ) | $ | 1.25 | |||||||||

| Earnings (loss) per diluted common share(3): | ||||||||||||||||||||

| Income from continuing operations | $ | 2.91 | $ | 1.61 | $ | 1.38 | $ | 0.02 | $ | 1.27 | ||||||||||

| Income (loss) from discontinued operations | (0.01 | ) | (0.01 | ) | (0.02 | ) | (0.04 | ) | (0.04 | ) | ||||||||||

| Earnings (loss) per diluted common share | $ | 2.90 | $ | 1.60 | $ | 1.36 | $ | (0.02 | ) | $ | 1.23 | |||||||||

| Book value per common share(4) | $ | 35.24 | $ | 33.25 | $ | 32.24 | $ | 30.70 | $ | 31.42 | ||||||||||

| Dividends declared per common share | 0.55 | 0.35 | 0.20 | 0.20 | 0.20 | |||||||||||||||

| Average common shares outstanding(2): | ||||||||||||||||||||

| Basic | 1,909,116,527 | 1,923,805,397 | 1,905,823,882 | 1,885,774,276 | 1,654,708,640 | |||||||||||||||

| Diluted | 1,952,815,453 | 1,970,535,560 | 1,956,519,738 | 1,918,811,270 | 1,675,271,669 | |||||||||||||||

| Balance Sheet and Other Operating Data: | ||||||||||||||||||||

| Trading assets | $ | 228,280 | $ | 256,801 | $ | 280,744 | $ | 267,603 | $ | 275,353 | ||||||||||

| Loans(5) | 85,759 | 66,577 | 42,874 | 29,046 | 15,369 | |||||||||||||||

| Total assets | 787,465 | 801,510 | 832,702 | 780,960 | 749,898 | |||||||||||||||

| Total deposits | 156,034 | 133,544 | 112,379 | 83,266 | 65,662 | |||||||||||||||

| Long-term borrowings | 153,768 | 152,772 | 153,575 | 169,571 | 184,234 | |||||||||||||||

| Morgan Stanley shareholders� equity | 75,182 | 70,900 | 65,921 | 62,109 | 62,049 | |||||||||||||||

| Return on average common equity(6) | 8.5% | 4.8% | 4.3% | N/M | 3.8% | |||||||||||||||

| (1) | Reflects 51% ownership of the retail securities joint venture between the Company and Citigroup Inc. up to September�17, 2012, 65% up to June�28, 2013 and 100% thereafter (see Note 15 to the consolidated financial statements in Part II, Item�8). |

| (2) | Amounts shown are used to calculate earnings (loss) per basic and diluted common share. |

| (3) | For the calculation of basic and diluted earnings (loss) per common share, see Note 16 to the consolidated financial statements in Part II, Item�8. |

| (4) | Book value per common share equals common shareholders� equity of $67,662 million at December�31, 2015, $64,880 million at December�31, 2014, $62,701 million at December�31, 2013, $60,601 million at December�31, 2012 and $60,541 million at December�31, 2011, divided by common shares outstanding of 1,920�million at December�31, 2015, 1,951�million at December�31, 2014, 1,945�million at December�31, 2013, 1,974�million at December�31, 2012 and 1,927�million at December�31, 2011. |

| (5) | Amounts include loans held for investment and loans held for sale but exclude loans at fair value, which are included in Trading assets in the consolidated statements of financial condition (see Note 7 to the consolidated financial statements in Part II, Item�8). |

| (6) | The calculation of return on average common equity equals net income applicable to Morgan Stanley less preferred dividends as a percentage of average common equity. The return on average common equity is a non-generally accepted accounting principle (�non-GAAP�) financial measure that the Company considers to be a useful measure to the Company and its investors to assess operating performance. |

| 37 | |

| Item�7. | Management�s Discussion and Analysis of Financial Condition and Results of Operations. |

| | 38 |

| � | The Company reported net revenues of $35,155 million in 2015, a 3% increase from net revenues of $34,275 million in 2014. The impact of debt valuation adjustment (�DVA�) included in net revenues was positive $618 million and $651 million in 2015 and 2014, respectively. |

| � | Net income applicable to Morgan Stanley for the current year was $6,127 million, or $2.90 per diluted common share, compared with $3,467 million, or $1.60 per diluted common share, a year ago. The current year included net discrete tax benefits of $564 million, or $0.29 per diluted common share, compared with $2,226 million, or $1.13 per diluted common share, in the prior year. For a further discussion of these net discrete tax benefits, see �Supplemental Financial Information and Disclosures�Income Tax Matters� herein. The prior year also included litigation costs related to residential mortgage-backed securities and credit crisis matters of $3,083 million, or a loss of $1.47 per diluted common share, 2014 compensation actions of approximately $1,137 million (see also �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein), or a loss of $0.39 per diluted common share, and a funding valuation adjustment (�FVA�) implementation charge of $468 million, or a loss of $0.17 per diluted common share. |

| � | Excluding DVA, net revenues were $34,537 million in 2015 compared with $33,624 million in 2014, and net income applicable to Morgan Stanley was $5,728 million, or $2.70 per diluted common share, in 2015 compared with $3,049 million, or $1.39 per diluted common share, in 2014. Excluding both DVA and the net discrete tax benefits, net income applicable to Morgan Stanley was $5,164 million, or $2.41 per diluted common share, in 2015 compared with $823 million, or $0.26 per diluted common share, in 2014. |

| � | Institutional Securities net revenues of $17,953 million in 2015 increased 6% compared with $16,871 million in 2014, primarily as a result of higher Sales and trading net revenues, partially offset by lower Other revenues and lower revenues in Investment banking. |

| � | Wealth Management net revenues of $15,100 million in 2015 increased 1% from $14,888 million in 2014, primarily as a result of higher net interest income and asset management revenues, partially offset by lower transactional revenues. |

| � | Investment Management net revenues of $2,315 million in 2015 decreased 15% from $2,712 million in 2014, primarily reflecting the reversal of previously accrued carried interest, reduction in revenues attributable to non-controlling interests and markdowns on principal investments. |

| � | Compensation and benefits expenses of $16,016 million in 2015 were down 10% from $17,824 million in 2014, primarily due to the 2014 compensation actions, a decrease in 2015 in the fair value of deferred compensation plan referenced investments and carried interest, and a decrease in the level of discretionary incentive compensation in 2015 (see also �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein). |

| � | Non-compensation expenses were $10,644 million in 2015 compared with $12,860 million in 2014, representing a 17% decrease, primarily as a result of lower legal expenses in the Institutional Securities business segment associated with residential mortgage-backed securities and credit crisis-related matters. |

| 39 | |

| � | The return on average common equity was 8.5% in 2015, or 7.8% excluding DVA, and 7.0% excluding DVA and the net discrete tax benefits. For 2014, the return on average common equity was 4.8%, or 4.1% excluding DVA, and 0.8% excluding DVA and the net discrete tax benefits. |

| � | The Company reported net revenues of $34,275 million in 2014, a 5% increase compared with $32,493 million in 2013. Net revenues in 2014 included positive revenues due to the impact of DVA of $651 million compared with negative revenues of $681 million in 2013. In addition, net revenues in 2014 included a charge of approximately $468 million related to the implementation of FVA (see �Critical Accounting Policies� herein and Note 2 to the consolidated financial statements in Item�8), which was recorded in the Institutional Securities business segment. |

| � | For 2014, net income applicable to Morgan Stanley was $3,467 million, or $1.60 per diluted common share, compared with $2,932 million, or $1.36 per diluted common share, in 2013. 2014 included net discrete tax benefits of $2,226 million, or $1.13 per diluted common share, compared with $407 million, or $0.21 per diluted common share, in 2013. For a further discussion of these net discrete tax benefits, see �Supplemental Financial Information and Disclosures�Income Tax Matters� herein. |

| � | Excluding DVA, net revenues were $33,624 million in 2014 compared with $33,174 million in 2013, and net income applicable to Morgan Stanley was $3,049 million, or $1.39 per diluted common share, in 2014 compared with $3,384 million, or $1.59 per diluted common share, in 2013. Excluding both DVA and the net discrete tax benefits, net income applicable to Morgan Stanley was $823 million, or $0.26 per diluted common share, in 2014 compared with $2,977 million, or $1.38 per diluted common share, in 2013. |

| � | Institutional Securities net revenues of $16,871 million in 2014 increased 9% compared with $15,519 million in 2013, primarily as a result of an increase in Sales and trading net revenues and Investment banking revenues, partially offset by lower net investment gains. |

| � | Wealth Management net revenues of $14,888 million in 2014 increased 5% from $14,143 million in 2013, primarily as a result of higher Asset management, distribution and administration fees and an increase in net interest income, partially offset by lower transactional revenues. |

| � | Investment Management net revenues of $2,712 million in 2014 decreased 11% from $3,059 million in 2013. The decrease in net revenues was primarily related to lower net investment gains, including from investments in the Company�s employee deferred compensation and co-investment plans, and lower carried interest, partially offset by higher management and administration revenues. |

| � | Compensation and benefits expenses of $17,824 million in 2014 increased 10% from $16,277 million in 2013, primarily due to the 2014 compensation actions of approximately $1,137 million (see �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein). |

| � | Non-compensation expenses were $12,860 million in 2014 compared with $11,658 million in 2013, representing a 10% increase, primarily due to higher legal expenses. |

| � | The return on average common equity was 4.8% in 2014, or 4.1% excluding DVA, and 0.8% excluding DVA and the net discrete tax benefits. Return on average common equity in 2013 was 4.3%, or 4.9% excluding DVA, and 4.3% excluding DVA and the net discrete tax benefits. |

| | 40 |

| 2015 | 2014 | 2013 | ||||||||||

| (dollars in millions, except where noted) | ||||||||||||

| Net revenues: | ||||||||||||

| Institutional Securities | $ | 17,953 | $ | 16,871 | $ | 15,519 | ||||||

| Wealth Management | 15,100 | 14,888 | 14,143 | |||||||||

| Investment Management | 2,315 | 2,712 | 3,059 | |||||||||

| Intersegment Eliminations | (213 | ) | (196 | ) | (228 | ) | ||||||

| Consolidated net revenues | $ | 35,155 | $ | 34,275 | $ | 32,493 | ||||||

| Income (loss) from continuing operations applicable to Morgan Stanley(1): | ||||||||||||

| Institutional Securities | $ | 3,713 | $ | (77 | ) | $ | 983 | |||||

| Wealth Management | 2,085 | 3,192 | 1,473 | |||||||||

| Investment Management | 345 | 366 | 519 | |||||||||

| Income from continuing operations applicable to Morgan Stanley | $ | 6,143 | $ | 3,481 | $ | 2,975 | ||||||

| Pre-tax profit margin(2): | ||||||||||||

| Institutional Securities | 26% | N/M | 6% | |||||||||

| Wealth Management | 22% | 20% | 18% | |||||||||

| Investment Management | 21% | 24% | 33% | |||||||||

| Consolidated | 24% | 10% | 14% | |||||||||

| Average common equity (dollars in billions)(3)(4): | ||||||||||||

| Institutional Securities | $ | 34.6 | $ | 32.2 | $ | 37.9 | ||||||

| Wealth Management | 11.2 | 11.2 | 13.2 | |||||||||

| Investment Management | 2.2 | 2.9 | 2.8 | |||||||||

| Parent capital | 18.9 | 19.0 | 8.0 | |||||||||

| Consolidated average common equity | $ | 66.9 | $ | 65.3 | $ | 61.9 | ||||||

| Return on average common equity(3)(4): | ||||||||||||

| Institutional Securities | 10.0% | N/M | 2.3% | |||||||||

| Wealth Management | 16.9% | 27.5% | 9.9% | |||||||||

| Investment Management | 15.8% | 12.8% | 18.1% | |||||||||

| Consolidated | 8.5% | 4.8% | 4.3% | |||||||||

| Regional net revenues(5): | ||||||||||||

| Americas | $ | 25,080 | $ | 25,140 | $ | 23,358 | ||||||

| EMEA | 5,353 | 4,772 | 4,542 | |||||||||

| Asia-Pacific | 4,722 | 4,363 | 4,593 | |||||||||

| Net revenues | $ | 35,155 | $ | 34,275 | $ | 32,493 | ||||||

| Effective income tax rate from continuing operations | 25.9% | (2.5)% | 19.8% | |||||||||

| 41 | |

| At December�31, 2015 | At December�31, 2014 | |||||||

| (dollars in millions, except where noted) | ||||||||

| Global Liquidity Reserve managed by bank and non-bank legal entities(6): | ||||||||

| Bank legal entities | $ | 94,328 | $ | 87,944 | ||||

| Non-bank legal entities | 108,936 | 105,225 | ||||||

| Total | $ | 203,264 | $ | 193,169 | ||||

| Maturities of long-term borrowings outstanding (next 12 months) | $ | 22,396 | $ | 20,740 | ||||

| Capital ratios (Transitional)(7): | ||||||||

| Common Equity Tier 1 capital ratio | 15.5% | 12.6% | ||||||

| Tier 1 capital ratio | 17.4% | 14.1% | ||||||

| Total capital ratio | 20.7% | 16.4% | ||||||

| Tier 1 leverage ratio(8) | 8.3% | 7.9% | ||||||

| Assets under management or supervision (dollars in billions)(9): | ||||||||

| Wealth Management | $ | 784 | $ | 778 | ||||

| Investment Management | 406 | 403 | ||||||

| Total | $ | 1,190 | $ | 1,181 | ||||

| Worldwide employees | 56,218 | 55,802 | ||||||

| | 42 |

| 2015 | 2014 | 2013 | ||||||||||

| (dollars in millions, except per share amounts) | ||||||||||||

| Net revenues | ||||||||||||

| Net revenues�non-GAAP | $ | 34,537 | $ | 33,624 | $ | 33,174 | ||||||

| Impact of DVA | 618 | 651 | (681 | ) | ||||||||

| Net revenues�U.S. GAAP | $ | 35,155 | $ | 34,275 | $ | 32,493 | ||||||

| Net income applicable to Morgan Stanley | ||||||||||||

| Net income applicable to Morgan Stanley, excluding DVA and net discrete tax benefits�non-GAAP | $ | 5,164 | $ | 823 | $ | 2,977 | ||||||

| Impact of net discrete tax benefits(10) | 564 | 2,226 | 407 | |||||||||

| Net income applicable to Morgan Stanley, excluding DVA�non-GAAP | $ | 5,728 | $ | 3,049 | $ | 3,384 | ||||||

| Impact of DVA | 399 | 418 | (452 | ) | ||||||||

| Net income applicable to Morgan Stanley�U.S. GAAP | $ | 6,127 | $ | 3,467 | $ | 2,932 | ||||||

| Earnings per diluted common share | ||||||||||||

| Earnings per diluted common share, excluding DVA and net discrete tax benefits�non-GAAP | $ | 2.41 | $ | 0.26 | $ | 1.38 | ||||||

| Impact of net discrete tax benefits(10) | 0.29 | 1.13 | 0.21 | |||||||||

| Earnings per diluted common share, excluding DVA�non-GAAP | $ | 2.70 | $ | 1.39 | $ | 1.59 | ||||||

| Impact of DVA | 0.20 | 0.21 | (0.23 | ) | ||||||||

| Earnings per diluted common share�U.S. GAAP | $ | 2.90 | $ | 1.60 | $ | 1.36 | ||||||

| Effective income tax rate | ||||||||||||

| Effective income tax rate from continuing operations�non-GAAP | 32.5% | 59.5% | 28.7% | |||||||||

| Impact of net discrete tax benefits(10) | (6.6)% | (62.0)% | (8.9)% | |||||||||

| Effective income tax rate from continuing operations�U.S. GAAP | 25.9% | (2.5)% | 19.8% | |||||||||

| 2015 | 2014 | 2013 | ||||||||||

| (dollars in millions) | ||||||||||||

| Average common equity(4)(11) | ||||||||||||

| Average common equity, excluding DVA and net discrete tax benefits | $ | 67,139 | $ | 65,679 | $ | 62,805 | ||||||

| Average common equity, excluding DVA | $ | 67,573 | $ | 66,392 | $ | 62,952 | ||||||

| Average common equity | $ | 66,936 | $ | 65,284 | $ | 61,895 | ||||||

| Return on average common equity(4)(12) | ||||||||||||

| Return on average common equity, excluding DVA and net discrete tax benefits | 7.0% | 0.8% | 4.3% | |||||||||

| Return on average common equity, excluding DVA | 7.8% | 4.1% | 4.9% | |||||||||

| Return on average common equity | 8.5% | 4.8% | 4.3% | |||||||||

| Average tangible common equity(11) | ||||||||||||

| Average tangible common equity, excluding DVA and net discrete tax benefits | $ | 57,478 | $ | 55,943 | $ | 53,906 | ||||||

| Average tangible common equity, excluding DVA | $ | 57,912 | $ | 56,656 | $ | 54,052 | ||||||

| Average tangible common equity | $ | 57,275 | $ | 55,548 | $ | 52,995 | ||||||

| Return on average tangible common equity(13) | ||||||||||||

| Return on average tangible common equity, excluding DVA and net discrete tax benefits | 8.2 | % | 0.9 | % | 5.0 | % | ||||||

| Return on average tangible common equity, excluding DVA | 9.1% | 4.8% | 5.8% | |||||||||

| Return on average tangible common equity | 9.9% | 5.7% | 5.0% | |||||||||

| 43 | |

| At December�31,� 2015 | At December�31,� 2014 | |||||||

| Tangible book value per common share(14) | $ | 30.26 | $ | 28.26 | ||||

| (1) | The Institutional Securities business segment�s net income applicable to noncontrolling interests was $133 million, $109 million and $278 million in 2015, 2014 and 2013, respectively. The Wealth Management business segment�s net income applicable to noncontrolling interests was $221 million in 2013. The Investment Management business segment�s net income applicable to noncontrolling interests was $19 million, $91 million and $182 million in 2015, 2014 and 2013, respectively. See Note 15 to the consolidated financial statements in Item�8 for further information. |

| (2) | Pre-tax profit margin is a non-GAAP financial measure that the Company considers to be a useful measure to the Company and investors to assess operating performance. Percentages represent income from continuing operations before income taxes as a percentage of net revenues. |

| (3) | The computation of average common equity for each business segment is determined using the Company�s Required Capital framework, an internal capital adequacy measure (see �Liquidity and Capital Resources�Regulatory Requirements�Required Capital� herein). The calculation of each business segment�s return on average common equity equals net income applicable to Morgan Stanley less preferred dividends as a percentage of each business segment�s average common equity. The effective tax rates used in the computation of each business segment�s return on average common equity were determined on a separate legal entity basis. Average common equity and the return on average common equity for each business segment are non-GAAP financial measures that the Company considers to be useful measures to the Company and investors to assess capital adequacy and to allow better comparability of period-to-period operating performance, respectively. |

| (4) | The calculation of return on average common equity equals consolidated net income applicable to Morgan Stanley less preferred dividends as a percentage of average common equity. To determine the return on average common equity, excluding DVA, and excluding DVA and net discrete tax benefits, both the numerator and denominator were adjusted to exclude those items. Average common equity, the return on average common equity, and average common equity and the return on average common equity, both excluding DVA, and excluding DVA and net discrete tax benefits, are non-GAAP financial measures that the Company considers useful for investors to assess capital adequacy and to allow better comparability of period-to-period operating performance. |

| (5) | For a discussion regarding the geographic methodology for net revenues, see Note 21 to the consolidated financial statements in Item�8. |

| (6) | For a discussion of Global Liquidity Reserve, see �Liquidity and Capital Resources�Liquidity Risk Management Framework�Global Liquidity Reserve� herein. |

| (7) | For a discussion of the Company�s methods for calculating its risk-based capital ratios, see �Liquidity and Capital Resources�Regulatory Requirements� herein. |

| (8) | See Note 14 to the consolidated financial statements in Item�8 for information on the Tier 1 leverage ratio. |

| (9) | Amounts exclude the Investment Management business segment�s proportionate share of assets managed by entities in which it owns a minority stake and assets for which fees are not generated. For 2015, amounts include $4.6 billion of inflows related to the transfer of certain portfolio managers and their portfolios from the Wealth Management business segment to the Investment Management business segment. |

| (10) | For a discussion of the Company�s net discrete tax benefits, see �Supplemental Financial Information and Disclosures�Income Tax Matters� herein. |

| (11) | The impact of DVA on average common equity and average tangible common equity was $(637) million, $(1,108) million and $(1,057) million in 2015, 2014 and 2013, respectively. The impact of net discrete tax benefits on average common equity and average tangible common equity was approximately $434 million, $713 million and $146 million in 2015, 2014 and 2013, respectively. |

| (12) | The impact of DVA on return on average common equity was 0.7%, 0.7% and (0.6)% in 2015, 2014 and 2013, respectively. The impact of net discrete tax benefits on return on average common equity was 0.8%, 3.3% and 0.6% in 2015, 2014 and 2013, respectively. |

| | 44 |

| (13) | The calculation of return on average tangible common equity equals net income applicable to Morgan Stanley less preferred dividends as a percentage of average tangible common equity. To determine the return on average tangible common equity, excluding DVA, and excluding DVA and net discrete tax benefits, both the numerator and the denominator were adjusted to exclude the impact of DVA and the impact of net discrete tax benefits. The impact of DVA was 0.8%, 0.9% and (0.8)% in 2015, 2014 and 2013, respectively. The impact of net discrete tax benefits was 0.9%, 3.9% and 0.8% in 2015, 2014 and 2013, respectively. |

| (14) | Tangible book value per common share equals tangible common equity of $58,098 million at December�31, 2015 and $55,138 million at December�31, 2014 divided by common shares outstanding of 1,920�million at December�31, 2015 and 1,951�million at December�31, 2014. |

| � | Revenue and profitability growth: |

| � | Wealth Management pre-tax margin improvement to approximately 23% to 25% through net interest income growth via continued high quality lending, expense efficiency and business growth; |

| � | Continued strength in Investment Banking and Equity Sales and Trading results; |

| � | Steady performance in Investment Management; |

| � | Expense efficiency: |

| � | Achieve an expense efficiency target ratio excluding DVA of 74%, assuming a flat revenue environment (not including any outsized litigation expense or penalties); |

| � | Sufficient capital: |

| � | Continuing to right-size the Fixed Income and Commodities Sales and Trading business from an operational and capital standpoint; and |

| � | Increasing capital returns to shareholders, subject to regulatory approval. |

| 45 | |

| | 46 |

| 47 | |

| | 48 |

| % Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Revenues: | ||||||||||||||||||||

| Investment banking | $ | 5,008 | $ | 5,203 | $ | 4,377 | (4)% | 19% | ||||||||||||

| Trading | 9,400 | 8,445 | 8,147 | 11% | 4% | |||||||||||||||

| Investments | 274 | 240 | 707 | 14% | (66)% | |||||||||||||||

| Commissions and fees | 2,616 | 2,610 | 2,425 | � | 8% | |||||||||||||||

| Asset management, distribution and administration fees | 281 | 281 | 280 | � | � | |||||||||||||||

| Other | 221 | 684 | 684 | (68)% | � | |||||||||||||||

| Total non-interest revenues | 17,800 | 17,463 | 16,620 | 2% | 5% | |||||||||||||||

| Interest income | 3,190 | 3,389 | 3,572 | (6)% | (5)% | |||||||||||||||

| Interest expense | 3,037 | 3,981 | 4,673 | (24)% | (15)% | |||||||||||||||

| Net interest | 153 | (592 | ) | (1,101 | ) | N/M | 46% | |||||||||||||

| Net revenues | 17,953 | 16,871 | 15,519 | 6% | 9% | |||||||||||||||

| Compensation and benefits | 6,467 | 7,786 | 6,823 | (17)% | 14% | |||||||||||||||

| Non-compensation expenses | 6,815 | 9,143 | 7,750 | (25)% | 18% | |||||||||||||||

| Total non-interest expenses | 13,282 | 16,929 | 14,573 | (22)% | 16% | |||||||||||||||

| Income (loss) from continuing operations before income taxes | 4,671 | (58 | ) | 946 | N/M | N/M | ||||||||||||||

| Provision for (benefit from) income taxes | 825 | (90 | ) | (315 | ) | N/M | 71% | |||||||||||||

| Income from continuing operations | 3,846 | 32 | 1,261 | N/M | (97)% | |||||||||||||||

| Discontinued operations: | ||||||||||||||||||||

| Income (loss) from discontinued operations before income taxes | (24 | ) | (26 | ) | (81 | ) | 8% | 68% | ||||||||||||

| Provision for (benefit from) income taxes | (7 | ) | (7 | ) | (29 | ) | � | 76% | ||||||||||||

| Income (losses) from discontinued operations | (17 | ) | (19 | ) | (52 | ) | 11% | 63% | ||||||||||||

| Net income | 3,829 | 13 | 1,209 | N/M | (99)% | |||||||||||||||

| Net income applicable to redeemable noncontrolling interests | � | � | 1 | N/M | (100)% | |||||||||||||||

| Net income applicable to nonredeemable noncontrolling interests | 133 | 109 | 277 | 22% | (61)% | |||||||||||||||

| Net income (loss) applicable to Morgan Stanley | $ | 3,696 | $ | (96 | ) | $ | 931 | N/M | N/M | |||||||||||

| Amounts applicable to Morgan Stanley: | ||||||||||||||||||||

| Income (loss) from continuing operations | $ | 3,713 | $ | (77 | ) | $ | 983 | N/M | N/M | |||||||||||

| Income (loss) from discontinued operations | (17 | ) | (19 | ) | (52 | ) | 11% | 63% | ||||||||||||

| Net income (loss) applicable to Morgan Stanley | $ | 3,696 | $ | (96 | ) | $ | 931 | N/M | N/M | |||||||||||

| 49 | |

| %

Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Advisory revenues | $ | 1,967 | $ | 1,634 | $ | 1,310 | 20% | 25% | ||||||||||||

| Underwriting revenues: | ||||||||||||||||||||

| Equity underwriting revenues | 1,398 | 1,613 | 1,262 | (13)% | 28% | |||||||||||||||

| Fixed income underwriting revenues | 1,643 | 1,956 | 1,805 | (16)% | 8% | |||||||||||||||

| Total underwriting revenues | 3,041 | 3,569 | 3,067 | (15)% | 16% | |||||||||||||||

| Total investment banking revenues | $ | 5,008 | $ | 5,203 | $ | 4,377 | (4)% | 19% | ||||||||||||

| 2015(1) | 2014(1) | 2013(1) | ||||||||||

| (dollars in billions) | ||||||||||||

| Announced mergers and acquisitions(2) | $ | 1,550 | $ | 657 | $ | 497 | ||||||

| Completed mergers and acquisitions(2) | 636 | 624 | 526 | |||||||||

| Equity and equity-related offerings(3) | 67 | 72 | 61 | |||||||||

| Fixed income offerings(4) | 256 | 286 | 291 | |||||||||

| (1) | Source: Thomson Reuters, data at January�15, 2016. Announced and completed mergers and acquisitions volumes are based on full credit to each of the advisors in a transaction. Equity and equity-related offerings and fixed income offerings are based on full credit for single book managers and equal credit for joint book managers. Transaction volumes may not be indicative of net revenues in a given period. In addition, transaction volumes for prior periods may vary from amounts previously reported due to the subsequent withdrawal or change in the value of a transaction. |

| (2) | Amounts include transactions of $100 million or more. Announced mergers and acquisitions exclude terminated transactions. |

| (3) | Amounts include Rule 144A issuances and registered public offerings of common stock and convertible securities and rights offerings. |

| (4) | Amounts include non-convertible preferred stock, mortgage-backed and asset-backed securities, and taxable municipal debt. Amounts include publicly registered and Rule 144A issues. Amounts exclude leveraged loans and self-led issuances. |

| � | Advisory revenues increased led primarily by merger, acquisition and restructuring transactions (�M&A�) in the Americas. Global industry-wide announced M&A volume activity for 2015 increased significantly compared with 2014. |

| � | Equity underwriting revenues decreased driven by decreases in initial public offering volumes. Fixed income underwriting revenues decreased primarily driven by lower non-investment grade bond and loan fees. |

| � | Advisory revenues from M&A increased due to increased deal activity in the Americas and Asia-Pacific regions. Industry-wide announced M&A volume activity for 2014 increased across all regions compared with 2013, primarily driven by cross-border activity. |

| � | Equity underwriting revenues increased driven by increased activity with clients across all regions. Fixed income underwriting revenues increased driven by increased investment grade volumes. |

| | 50 |

| %

Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014(1) | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Trading | $ | 9,400 | $ | 8,445 | $ | 8,147 | 11% | 4% | ||||||||||||

| Commissions and fees | 2,616 | 2,610 | 2,425 | � | 8% | |||||||||||||||

| Asset management, distribution and administration fees | 281 | 281 | 280 | � | � | |||||||||||||||

| Net interest | 153 | (592 | ) | (1,101 | ) | N/M | 46% | |||||||||||||

| Total sales and trading net revenues | $ | 12,450 | $ | 10,744 | $ | 9,751 | 16% | 10% | ||||||||||||

| %

Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014(1) | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Equity | $ | 8,288 | $ | 7,135 | $ | 6,529 | 16% | 9% | ||||||||||||

| Fixed income and commodities | 4,758 | 4,214 | 3,594 | 13% | 17% | |||||||||||||||

| Other | (596 | ) | (605 | ) | (372 | ) | 1% | (63)% | ||||||||||||

| Total sales and trading net revenues | $ | 12,450 | $ | 10,744 | $ | 9,751 | 16% | 10% | ||||||||||||

| (1) | Results in 2014 included a charge of $468 million related to the implementation of FVA (Equity: $2 million; Fixed income and commodities: $466 million). |

| %

Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Total sales and trading net revenues�non-GAAP | $ | 11,832 | $ | 10,561 | $ | 10,432 | 12% | 1% | ||||||||||||

| Impact of DVA | 618 | 651 | (681 | ) | (5)% | N/M | ||||||||||||||

| Impact of FVA | � | (468 | ) | � | 100% | N/M | ||||||||||||||

| Total sales and trading net revenues | $ | 12,450 | $ | 10,744 | $ | 9,751 | 16% | 10% | ||||||||||||

| Equity sales and trading net revenues�non-GAAP | $ | 8,125 | $ | 6,905 | $ | 6,607 | 18% | 5% | ||||||||||||

| Impact of DVA | 163 | 232 | (78 | ) | (30)% | N/M | ||||||||||||||

| Impact of FVA | � | (2 | ) | � | 100% | N/M | ||||||||||||||

| Equity sales and trading net revenues | $ | 8,288 | $ | 7,135 | $ | 6,529 | 16% | 9% | ||||||||||||

| Fixed income and commodities sales and trading net revenues�non-GAAP | $ | 4,303 | $ | 4,261 | $ | 4,197 | 1% | 2% | ||||||||||||

| Impact of DVA | 455 | 419 | (603 | ) | 9% | N/M | ||||||||||||||

| Impact of FVA | � | (466 | ) | � | 100% | N/M | ||||||||||||||

| Fixed income and commodities sales and trading net revenues | $ | 4,758 | $ | 4,214 | $ | 3,594 | 13% | 17% | ||||||||||||

| 51 | |

| � | Equity sales and trading net revenues, excluding the impact of DVA and the implementation of FVA, increased driven by strong results in prime brokerage and derivatives products. Higher client balances primarily drove the increase in prime brokerage results, while the improved results in derivatives reflected increased client activity and gains on inventory. |

| � | Excluding the impact of DVA and the implementation of FVA, fixed income and commodities sales and trading net revenues increased as higher commodity net revenues were partially offset by lower fixed income product results. |

| � | Fixed income product net revenues, excluding the impact of DVA and the implementation of FVA, decreased due to lower results in credit and securitized products from wider credit spread environment which were partially offset by higher revenues in interest rates and foreign exchange products from higher client activity. |

| � | Commodity net revenues, excluding the impact of DVA and the implementation of FVA, increased primarily reflecting higher revenues from the global oil merchanting business, which was sold on November�1, 2015 (see �Investments, Other Revenues, Non-interest Expenses, Income Tax Items, Dispositions and Other Items�2015 Compared with 2014�Dispositions� herein). The increase was partially offset by credit driven losses and the absence of revenues from TransMontaigne Inc., which was sold on July�1, 2014 (see �Investments, Other Revenues, Non-interest Expenses, Income Tax Items, Dispositions and Other Items�2014 Compared with 2013�Dispositions� herein). |

| � | Equity sales and trading net revenues, excluding the impact of DVA and the implementation of FVA of $2 million, increased primarily due to higher revenues in the prime brokerage business driven by higher client balances partially offset by a decrease in derivatives revenues, reflecting unfavorable volatility movement. |

| � | Fixed income and commodities sales and trading net revenues in 2014 included a charge of $466 million related to the implementation of FVA. Excluding the impact of DVA and the implementation of FVA, fixed income and commodities sales and trading net revenues increased as higher commodity net revenues were partially offset by lower fixed income product results. |

| � | Fixed income product net revenues, excluding the impact of DVA and the implementation of FVA, decreased as higher results in interest rate products were offset by declines in credit products, which reflected an unfavorable market environment. |

| � | Commodity net revenues, excluding the impact of DVA and the implementation of FVA, increased reflecting higher levels of client demand for structured transactions and volatility in natural gas and power partly offset by lower revenues in the oil related businesses in part attributable to TransMontaigne Inc., which was sold on July�1, 2014 |

| | 52 |

| (see �Investments, Other Revenues, Non-interest Expenses, Income Tax Items, Dispositions and Other Items�2014 Compared with 2013�Dispositions� herein). |

| � | Net investment gains of $274 million in 2015 increased 14% from the prior year driven by gains on business related investments. |

| � | Other revenues of $221 million in 2015 decreased 68% from the prior year primarily due to the absence of gains realized on certain assets sold in 2014 (see Note 1 to the consolidated financial statements in Item�8) and markdowns and provisions on loans held for sale and held for investment, respectively. |

| � | Compensation and benefits expenses decreased primarily due to the 2014 compensation actions, a decrease in the fair value of deferred compensation plan referenced investments, and a decrease in the level of discretionary incentive compensation in 2015 (see also �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein). |

| � | Non-compensation expenses decreased primarily due to lower litigation expenses. |

| � | Net investment gains of $240 million in 2014 decreased 66% from the prior year reflecting a gain recorded in 2013 related to the disposition of an investment in an insurance broker, and lower gains on principal investments and investments associated with the deferred compensation and co-investment plans in 2014. |

| � | Other revenues of $684 million remained unchanged. The results in 2014 included lower income from the Company�s 40% stake in Mitsubishi UFJ Morgan Stanley Securities Co., Ltd. (�MUMSS�) compared with 2013 (see �Other Items�Japanese Securities Joint Venture� herein and Note 8 to the consolidated financial statements in |

| 53 | |

| Item�8). In 2014, Other revenues also included gains realized on certain assets sold (see Note 1 to the consolidated financial statements in Item�8). |

| � | Compensation and benefits expenses increased primarily due to the 2014 compensation actions and an increase in base salaries and fixed allowances partially offset by a decrease in the fair value of deferred compensation plan referenced investments (see also �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein). |

| � | Non-compensation expenses increased primarily due to higher legal expenses related to certain legacy residential mortgage-backed securities and credit crisis-related matters (see �Supplemental Financial Information and Disclosures�Legal� herein and �Contingencies�Legal� in Note 12 to the consolidated financial statements in Item�8). |

| | 54 |

| 55 | |

| % Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Revenues: | ||||||||||||||||||||

| Investment banking | $ | 623 | $ | 791 | $ | 923 | (21)% | (14)% | ||||||||||||

| Trading | 731 | 957 | 1,161 | (24)% | (18)% | |||||||||||||||

| Investments | 18 | 9 | 14 | 100% | (36)% | |||||||||||||||

| Commissions and fees | 1,981 | 2,127 | 2,209 | (7)% | (4)% | |||||||||||||||

| Asset management, distribution and administration fees | 8,536 | 8,345 | 7,571 | 2% | 10% | |||||||||||||||

| Other | 255 | 320 | 390 | (20)% | (18)% | |||||||||||||||

| Total non-interest revenues | 12,144 | 12,549 | 12,268 | (3)% | 2% | |||||||||||||||

| Interest income | 3,105 | 2,516 | 2,100 | 23% | 20% | |||||||||||||||

| Interest expense | 149 | 177 | 225 | (16)% | (21)% | |||||||||||||||

| Net interest | 2,956 | 2,339 | 1,875 | 26% | 25% | |||||||||||||||

| Net revenues | 15,100 | 14,888 | 14,143 | 1% | 5% | |||||||||||||||

| Compensation and benefits | 8,595 | 8,825 | 8,265 | (3)% | 7% | |||||||||||||||

| Non-compensation expenses | 3,173 | 3,078 | 3,274 | 3% | (6)% | |||||||||||||||

| Total non-interest expenses | 11,768 | 11,903 | 11,539 | (1)% | 3% | |||||||||||||||

| Income from continuing operations before income taxes | 3,332 | 2,985 | 2,604 | 12% | 15% | |||||||||||||||

| Provision for (benefit from) income taxes | 1,247 | (207 | ) | 910 | N/M | N/M | ||||||||||||||

| Income from continuing operations | 2,085 | 3,192 | 1,694 | (35)% | 88% | |||||||||||||||

| Discontinued operations: | ||||||||||||||||||||

| Income (loss) from discontinued operations before income taxes | � | � | (1 | ) | N/M | (100)% | ||||||||||||||

| Provision for (benefit from) income taxes | � | � | � | N/M | N/M | |||||||||||||||

| Income (loss) from discontinued operations | � | � | (1 | ) | N/M | (100)% | ||||||||||||||

| Net income | 2,085 | 3,192 | 1,693 | (35)% | 89% | |||||||||||||||

| Net income applicable to redeemable noncontrolling interests | � | � | 221 | N/M | (100)% | |||||||||||||||

| Net income applicable to Morgan Stanley | $ | 2,085 | $ | 3,192 | $ | 1,472 | (35)% | N/M | ||||||||||||

| Amounts applicable to Morgan Stanley: | ||||||||||||||||||||

| Income from continuing operations | $ | 2,085 | $ | 3,192 | $ | 1,473 | (35)% | N/M | ||||||||||||

| Income (loss) from discontinued operations | � | � | (1 | ) | N/M | (100)% | ||||||||||||||

| Net income applicable to Morgan Stanley | $ | 2,085 | $ | 3,192 | $ | 1,472 | (35)% | N/M | ||||||||||||

| | 56 |

| % Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Investment banking | $ | 623 | $ | 791 | $ | 923 | (21)% | (14)% | ||||||||||||

| Trading | 731 | 957 | 1,161 | (24)% | (18)% | |||||||||||||||

| Commissions and fees | 1,981 | 2,127 | 2,209 | (7)% | (4)% | |||||||||||||||

| Transactional revenues | $ | 3,335 | $ | 3,875 | $ | 4,293 | (14)% | (10)% | ||||||||||||

| � | Investment banking revenues decreased primarily due to lower revenues from the distribution of underwritten offerings. |

| � | Trading revenues decreased primarily due to losses related to investments associated with certain employee deferred compensation plans and lower revenues from fixed income products. |

| � | Commissions and fees decreased primarily due to lower revenues from equity, mutual fund and annuity products partially offset by higher revenues from alternatives asset classes. |

| � | Investment banking revenues decreased primarily due to lower levels of underwriting activity in closed-end funds partially offset by higher revenues from structured products. |

| � | Trading revenues decreased primarily as a result of lower gains related to investments associated with certain employee deferred compensation plans and lower revenues from fixed income products. |

| � | Commissions and fees revenues decreased primarily due to lower equity, insurance and mutual fund activity. |

| � | Asset management, distribution and administration fees of $8,536 million in 2015 increased 2% from the prior year primarily due to higher fee-based revenues that resulted from positive flows and higher average market values over 2015 as compared with the average market values during 2014 (see �Statistical Data� herein). The increase in fee-based revenues was partially offset by lower referral fees from the bank deposit program, reflecting the completion of the transfer of the deposits from Citigroup Inc. (�Citi�) to the Company (see Note 10 to the consolidated financial statements in Item�8). |

| � | Net interest of $2,956 million in 2015 increased 26% from the prior year primarily due to higher balances in the bank deposit program and growth in loans and lending commitments. |

| 57 | |

| � | Other revenues of $255 million in 2015 decreased 20% from the prior year primarily due to a $40 million gain on sale of a retail property space in the prior year and an increase in the allowance for credit losses in 2015. |

| � | Compensation and benefits expenses decreased primarily due to the 2014 compensation actions, a decrease in the fair value of deferred compensation plan referenced investments and a decrease in the level of discretionary incentive compensation in 2015 (see also �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein). |

| � | Non-compensation expenses increased primarily due to an increase in Professional services, resulting from increased consulting and legal fees partially offset by a provision related to a rescission offer in the prior year. Other expenses in 2014 included $50 million related to a rescission offer to Wealth Management clients who may not have received a prospectus for certain securities transactions, for which delivery of a prospectus was required. |

| � | Asset management, distribution and administration fees of $8,345 million in 2014 increased 10% from the prior year primarily due to higher fee-based revenues partially offset by lower revenues from referral fees from the bank deposit program. The referral fees for deposits placed with Citi-affiliated depository institutions declined to $81 million in 2014 from $240 million in 2013, reflecting the transfer of deposits to the Company from Citi. |

| � | Net interest of $2,339 million in 2014 increased 25% from the prior year primarily due to higher lending balances and growth in loans and lending commitments in Portfolio Loan Account (�PLA�) securities-based lending products. |

| � | Other revenues of $320 million in 2014 decreased 18% from the prior year primarily as a result of a gain on sale of the U.K. operation of the Global Stock Plan Services business in 2013 and lower account fees. The results for Other revenues in 2014 included a $40 million gain on sale of a retail property space. |

| � | Compensation and benefits expenses increased primarily due to a higher formulaic payout to Wealth Management representatives linked to higher net revenues and an increase in base salaries. |

| � | Non-compensation expenses decreased in 2014 primarily driven by technology write-offs and an impairment expense related to certain intangible assets (management contracts) associated with alternative investments funds in 2013, lower intangible amortization and a lower Federal Deposit Insurance Corporation (�FDIC�) assessment on deposits partially offset by a provision in 2014 related to a rescission offer to Wealth Management clients. |

| 58 |

| At December� 31, 2015 | At December� 31, 2014 | |||||||||||

| Client assets | $ | 1,985 | $ | 2,025 | ||||||||

| Fee-based client assets(1) | $ | 795 | $ | 785 | ||||||||

| Fee-based client assets as a percentage of total client assets | 40% | 39% | ||||||||||

| Client liabilities(2) | $ | 64 | $ | 51 | ||||||||

| Bank deposit program(3) | $ | 149 | $ | 137 | ||||||||

| Investment securities portfolio | $ | 57.9 | $ | 57.3 | ||||||||

| Loans and lending commitments | $ | 55.3 | $ | 42.7 | ||||||||

| Wealth Management representatives | 15,889 | 16,076 | ||||||||||

| Retail locations | 608 | 622 | ||||||||||

| 2015 | 2014 | 2013 | ||||||||||

| Annual revenues per representative (dollars in thousands)(4) | $ | 950 | $ | 914 | $ | 863 | ||||||

| Client assets per representative (dollars in millions)(5) | $ | 125 | $ | 126 | $ | 116 | ||||||

| Fee-based asset flows(6) | $ | 46.3 | $ | 58.8 | $ | 51.9 | ||||||

| (1) | Fee-based client assets represent the amount of assets in client accounts where the basis of payment for services is a fee calculated on those assets. |

| (2) | Client liabilities include securities-based and tailored lending, home loans and margin lending. |

| (3) | Balances in the bank deposit program included deposits held by Morgan Stanley Bank, N.A. (�MSBNA�) and Morgan Stanley Private Bank, National Association (�MSPBNA�) (collectively, �U.S. Bank Subsidiaries�) of $149 billion and $128 billion at December�31, 2015 and December�31, 2014, respectively, with the remainder at December�31, 2014 held at Citi-affiliated FDIC insured depositories. At June�30, 2015, the transfer of deposits from Citi to the Company was completed. See Note 10 to the consolidated financial statements in Item�8 for further discussion of the Company�s customer deposits previously held by Citi. |

| (4) | Annual revenues per representative equal the Wealth Management business segment�s annual revenues divided by the average representative headcount. |

| (5) | Client assets per representative equal total period-end client assets divided by period-end representative headcount. |

| (6) | Fee-based asset flows include net new fee-based assets, net account transfers, dividends, interest and client fees and exclude cash management-related activity. |

| 59 | |

| At December�31, 2014 | Inflows | Outflows | Market Impact | At December�31, 2015 | Average�for�the Year Ended December�31, 2015 | |||||||||||||||||

| Fee�Rate(1) | ||||||||||||||||||||||

| (dollars in billions) | (in bps) | |||||||||||||||||||||

| Separately managed accounts(2) | $ | 285 | $ | 42 | $ | (32 | ) | $ | (12 | ) | $ | 283 | 34 | |||||||||

| Unified managed accounts | 93 | 29 | (14 | ) | (3 | ) | 105 | 113 | ||||||||||||||

| Mutual fund advisory | 31 | 3 | (6 | ) | (3 | ) | 25 | 121 | ||||||||||||||

| Representative as advisor | 119 | 29 | (25 | ) | (8 | ) | 115 | 89 | ||||||||||||||

| Representative as portfolio manager | 241 | 58 | (38 | ) | (9 | ) | 252 | 104 | ||||||||||||||

| Subtotal | $ | 769 | $ | 161 | $ | (115 | ) | $ | (35 | ) | $ | 780 | 76 | |||||||||

| Cash management | 16 | 9 | (10 | ) | � | 15 | 6 | |||||||||||||||

| Total fee-based client assets | $ | 785 | $ | 170 | $ | (125 | ) | $ | (35 | ) | $ | 795 | 74 | |||||||||

| At December�31, 2013 | Inflows | Outflows | Market Impact | At December�31, 2014 | Average�for�the Year Ended December�31, 2014 | |||||||||||||||||

| Fee�Rate(1) | ||||||||||||||||||||||

| (dollars in billions) | (in bps) | |||||||||||||||||||||

| Separately managed accounts(2) | $ | 260 | $ | 41 | $ | (31 | ) | $ | 15 | $ | 285 | 35 | ||||||||||

| Unified managed accounts | 78 | 24 | (11 | ) | 2 | 93 | 116 | |||||||||||||||

| Mutual fund advisory | 34 | 5 | (8 | ) | � | 31 | 121 | |||||||||||||||

| Representative as advisor | 111 | 30 | (23 | ) | 1 | 119 | 90 | |||||||||||||||

| Representative as portfolio manager | 201 | 60 | (28 | ) | 8 | 241 | 106 | |||||||||||||||

| Subtotal | $ | 684 | $ | 160 | $ | (101 | ) | $ | 26 | $ | 769 | 77 | ||||||||||

| Cash management | 13 | 12 | (9 | ) | � | 16 | 6 | |||||||||||||||

| Total fee-based client assets | $ | 697 | $ | 172 | $ | (110 | ) | $ | 26 | $ | 785 | 75 | ||||||||||

| At December�31, 2012 | Inflows | Outflows | Market Impact/ Other (3) | At December�31, 2013 | Average�for�the Year Ended December�31, 2013 | |||||||||||||||||

| Fee�Rate(1) | ||||||||||||||||||||||

| (dollars in billions) | (in bps) | |||||||||||||||||||||

| Separately managed accounts(2) | $ | 195 | $ | 43 | $ | (32 | ) | $ | 54 | $ | 260 | 37 | ||||||||||

| Unified managed accounts | 61 | 19 | (10 | ) | 8 | 78 | 120 | |||||||||||||||

| Mutual fund advisory | 31 | 5 | (6 | ) | 4 | 34 | 121 | |||||||||||||||

| Representative as advisor | 94 | 28 | (21 | ) | 10 | 111 | 91 | |||||||||||||||

| Representative as portfolio manager | 160 | 51 | (25 | ) | 15 | 201 | 109 | |||||||||||||||

| Subtotal | $ | 541 | $ | 146 | $ | (94 | ) | $ | 91 | $ | 684 | 78 | ||||||||||

| Cash management | 13 | 6 | (6 | ) | � | 13 | 6 | |||||||||||||||

| Total fee-based client assets | $ | 554 | $ | 152 | $ | (100 | ) | $ | 91 | $ | 697 | 77 | ||||||||||

| (1) | Average fee rate is for the year ended December�31, 2015,�December�31, 2014 and December�31, 2013, respectively. |

| (2) | Includes non-custody account values reflecting prior quarter-end balances due to a lag in the reporting of asset values by third-party custodians. |

| (3) | Effective in 2013, client assets include certain additional non-custodied assets as a result of the completion of the platform conversion between the Company and Citi. |

| � | Inflows �include new accounts, account transfers, deposits, dividends and interest. |

| � | Outflows �include closed or terminated accounts, account transfers, withdrawals and client fees. |

| � | Market impact �includes realized and unrealized gains and losses on portfolio investments. |

| | 60 |

| � | Separately managed accounts �Accounts by which third-party asset managers are engaged to manage clients� assets with investment decisions made by the asset manager. One third-party asset manager strategy can be held per account. |

| � | Unified managed accounts �Accounts that provide the client with the ability to combine separately managed accounts, mutual funds and exchange traded funds all in one aggregate account. Unified managed accounts can be client-directed, financial advisor-directed or Company-directed (with �directed� referring to the investment direction or decision/discretion/power of attorney). |

| � | Mutual fund advisory �Accounts that give the client the ability to systematically allocate assets across a wide range of mutual funds. Investment decisions are made by the client. |

| � | Representative as advisor �Accounts where the investment decisions must be approved by the client and the financial advisor must obtain approval each time a change is made to the account or its investments. |

| � | Representative as portfolio manager �Accounts where a financial advisor has discretion (contractually approved by the client) to make ongoing investment decisions without the client�s approval for each individual change. |

| � | Cash management �Accounts where the financial advisor provides discretionary cash management services to institutional clients whereby securities or proceeds are invested and reinvested in accordance with the client�s investment criteria. Generally, the portfolio will be invested in short-term fixed income and cash equivalent investments. |

| 61 | |

| % Change from�Prior�Year: | ||||||||||||||||||||

| 2015 | 2014 | 2013 | 2015 | 2014 | ||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||

| Revenues: | ||||||||||||||||||||

| Investment banking | $ | 1 | $ | 5 | $ | 11 | (80)% | (55)% | ||||||||||||

| Trading | (1 | ) | (19 | ) | 41 | 95% | N/M | |||||||||||||

| Investments | 249 | 587 | 1,056 | (58)% | (44)% | |||||||||||||||

| Commissions and fees | 1 | � | � | N/M | N/M | |||||||||||||||

| Asset management, distribution and administration fees | 2,049 | 2,049 | 1,920 | � | 7% | |||||||||||||||

| Other | 32 | 106 | 32 | (70)% | N/M | |||||||||||||||

| Total non-interest revenues | 2,331 | 2,728 | 3,060 | (15)% | (11)% | |||||||||||||||

| Interest income | 2 | 2 | 9 | � | (78)% | |||||||||||||||

| Interest expense | 18 | 18 | 10 | � | 80% | |||||||||||||||

| Net interest | (16 | ) | (16 | ) | (1 | ) | � | N/M | ||||||||||||

| Net revenues | 2,315 | 2,712 | 3,059 | (15)% | (11)% | |||||||||||||||

| Compensation and benefits | 954 | 1,213 | 1,189 | (21)% | 2% | |||||||||||||||

| Non-compensation expenses | 869 | 835 | 862 | 4% | (3)% | |||||||||||||||

| Total non-interest expenses | 1,823 | 2,048 | 2,051 | (11)% | � | |||||||||||||||

| Income from continuing operations before income taxes | 492 | 664 | 1,008 | (26)% | (34)% | |||||||||||||||

| Provision for income taxes | 128 | 207 | 307 | (38)% | (33)% | |||||||||||||||

| Income from continuing operations | 364 | 457 | 701 | (20)% | (35)% | |||||||||||||||

| Discontinued operations: | ||||||||||||||||||||

| Income from discontinued operations before income taxes | 1 | 7 | 9 | (86)% | (22)% | |||||||||||||||

| Provision for (benefit from) income taxes | � | 2 | � | (100)% | N/M | |||||||||||||||

| Income from discontinued operations | 1 | 5 | 9 | (80)% | (44)% | |||||||||||||||

| Net income | 365 | 462 | 710 | (21)% | (35)% | |||||||||||||||

| Net income applicable to nonredeemable noncontrolling interests | 19 | 91 | 182 | (79)% | (50)% | |||||||||||||||

| Net income applicable to Morgan Stanley | $ | 346 | $ | 371 | $ | 528 | (7)% | (30)% | ||||||||||||

| Amounts applicable to Morgan Stanley: | ||||||||||||||||||||

| Income from continuing operations | $ | 345 | $ | 366 | $ | 519 | (6)% | (29)% | ||||||||||||

| Income from discontinued operations | 1 | 5 | 9 | (80)% | (44)% | |||||||||||||||

| Net income applicable to Morgan Stanley | $ | 346 | $ | 371 | $ | 528 | (7)% | (30)% | ||||||||||||

| | 62 |

| � | Investments of $249 million in 2015 decreased 58% from the prior year reflecting the reversal of previously accrued carried interest associated with Asia Private Equity and additional net markdowns on principal investments. |

| � | Asset management, distribution and administration fees were unchanged from the prior year as the impact of positive net flows was offset by a shift in the asset class mix from equity and fixed income products to liquidity products, (see �Statistical Data� herein). |

| � | Other revenues of $32 million in 2015 decreased 70% from the prior year due to lower revenues associated with the Company�s minority investment in certain third-party investment managers. |

| � | Compensation and benefits expenses decreased primarily due to the 2014 compensation actions, a decrease in deferred compensation associated with carried interest and a decrease in the level of incentive compensation in 2015 (see also �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein). |

| � | Non-compensation expenses increased primarily due to higher Brokerage and clearing, Professional services, resulting from higher consulting and legal fees and Information processing and communications expenses. |

| � | Trading losses of $19 million in 2014 compared with gains of $41�million in 2013 primarily reflected losses related to certain consolidated real estate funds sponsored by the Company. |

| � | Investments of $587 million in 2014 decreased 44% from the prior year primarily related to lower net investment gains, lower carried interest in the Merchant Banking and Real Estate Investing businesses and lower gains from investments in the Company�s employee deferred compensation and co-investment plans. 2014 results were also negatively impacted by the deconsolidation in the second quarter of 2014 of certain legal entities associated with a real estate fund sponsored by the Company. |

| � | Asset management, distribution and administration fees of $2,049 million in 2014 increased 7% from the prior year primarily reflected higher management and administration revenues as a result of higher average assets under management (�AUM�), (see �Statistical Data� herein). |

| � | Other revenues of $106 million in 2014 increased from $32 million in 2013 primarily due to higher revenues associated with the Company�s minority investment in certain third-party investment managers and a $17 million gain on sale of a retail property space. |

| 63 | |

| � | Compensation and benefits expenses increased due to the 2014 compensation actions and increases in salaries partially offset by a decrease in the fair value of deferred compensation plan referenced investments (see also �Supplemental Financial Information and Disclosures�Discretionary Incentive Compensation� herein). |

| � | Non-compensation expenses decreased primarily due to an impairment expense related to certain intangible assets (management contracts) associated with alternative investments funds in 2013 and the result of lower consumption taxes in the European Union. |