UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2015

Commission file number 1-5153

Marathon Oil Corporation

(Exact name of registrant as specified in its charter)

Delaware |

| 25-0996816 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

5555 San Felipe Street, Houston, TX 77056-2723

(Address of principal executive offices)

(713) 629-6600

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common Stock, par value $1.00 |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes R No £

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes £ No R

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months and (2) has been subject to such filing requirements for the past 90 days. Yes R No £

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer R Accelerated filer £ Non-accelerated filer £ Smaller reporting company £

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes £ No R

The aggregate market value of Common Stock held by non-affiliates as of June 30, 2015 : $17,916 million . This amount is based on the closing price of the registrant's Common Stock on the New York Stock Exchange on that date. Shares of Common Stock held by executive officers and directors of the registrant are not included in the computation. The registrant, solely for the purpose of this required presentation, has deemed its directors and executive officers to be affiliates.

There were 676,886,641 shares of Marathon Oil Corporation Common Stock outstanding as of February 15, 2016 .

Documents Incorporated By Reference:

Portions of the registrant's proxy statement relating to its 2016 Annual Meeting of Stockholders, to be filed with the Securities and Exchange Commission pursuant to Regulation 14A under the Securities Exchange Act of 1934, are incorporated by reference to the extent set forth in Part III, Items 10-14 of this report.

MARATHON OIL CORPORATION

Unless the context otherwise indicates, references to "Marathon Oil," "we," "our" or "us" in this Annual Report on Form 10-K are references to Marathon Oil Corporation, including its wholly-owned and majority-owned subsidiaries, and its ownership interests in equity method investees (corporate entities, partnerships, limited liability companies and other ventures over which Marathon Oil exerts significant influence by virtue of its ownership interest).

Table of Contents

PART I |

|

|

|

|

|

|

|

| Item 1. | Business | 5 |

|

|

|

|

| Item 1A. | Risk Factors | 25 |

|

|

|

|

| Item 1B. | Unresolved Staff Comments | 34 |

|

|

|

|

| Item 2. | Properties | 34 |

|

|

|

|

| Item 3. | Legal Proceedings | 34 |

|

|

|

|

| Item 4. | Mine Safety Disclosures | 34 |

PART II |

|

|

|

|

|

|

|

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 35 |

|

|

|

|

| Item 6. | Selected Financial Data | 36 |

|

|

|

|

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 37 |

|

|

|

|

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 60 |

|

|

|

|

| Item 8. | Financial Statements and Supplementary Data | 63 |

|

|

|

|

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 118 |

|

|

|

|

| Item 9A. | Controls and Procedures | 118 |

|

|

|

|

| Item 9B. | Other Information | 118 |

|

|

|

|

PART III |

|

|

|

|

|

|

|

| Item 10. | Directors, Executive Officers and Corporate Governance | 119 |

|

|

|

|

| Item 11. | Executive Compensation | 119 |

|

|

|

|

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 119 |

|

|

|

|

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 120 |

|

|

|

|

| Item 14. | Principal Accountant Fees and Services | 120 |

|

|

|

|

PART IV |

|

|

|

|

|

|

|

| Item 15. | Exhibits, Financial Statement Schedules | 121 |

|

|

|

|

|

| SIGNATURES | 122 |

Definitions

Throughout this report, the following company or industry specific terms and abbreviations are used.

AMPCO – Atlantic Methanol Production Company LLC, a company located in Equatorial Guinea in which we own a 45% equity interest.

AOSP – Athabasca Oil Sands Project, an oil sands mining, transportation and upgrading joint venture located in Alberta, Canada, in which we hold a 20% non-operated working interest.

bbl – One stock tank barrel, which is 42 United States gallons liquid volume.

bcf – Billion cubic feet.

boe – Barrels of oil equivalent.

btu – British thermal unit, an energy equivalence measure.

Capital Program – Includes capital expenditures, cash investments in equity method investees and other investments, exploration costs that are expensed as incurred rather than capitalized, such as geological and geophysical costs and certain staff costs, and other miscellaneous investment expenditures.

DD&A – Depreciation, depletion and amortization.

Development well – A well drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive.

Downstream business – The refining, marketing and transportation ("RM&T") operations, spun-off on June 30, 2011 and treated as discontinued operations.

Dry well – A well found to be incapable of producing either oil or natural gas in sufficient quantities to justify completion.

E.G. – Equatorial Guinea.

EGHoldings – Equatorial Guinea LNG Holdings Limited, a liquefied natural gas production company located in E.G. in which we own a 60% equity interest.

EIA – United States Energy Information Agency.

EPA – United States Environmental Protection Agency.

Exploratory well – A well drilled to find oil or natural gas in an unproved area or find a new reservoir in a field previously found to be productive in another reservoir.

FASB – Financial Accounting Standards Board.

FPSO - Floating production, storage and offloading vessel.

Henry Hub price - a natural gas benchmark price quoted at settlement date average.

IRS – United States Internal Revenue Service.

LNG – Liquefied natural gas.

LPG – Liquefied petroleum gas.

Liquid hydrocarbons or liquids – Collectively, crude oil, synthetic crude oil, condensate and natural gas liquids.

LLS – Louisiana Light Sweet crude oil, an oil index benchmark price as per Bloomberg Finance LLP: LLS St. James.

Marathon Oil – Marathon Oil Corporation and its consolidated subsidiaries: the company as it exists following the June 30, 2011 spin-off of the downstream business.

mbbld – Thousand barrels per day.

mboed – Thousand barrels of oil equivalent per day.

mcf – Thousand cubic feet.

mmbbl – Million barrels.

mmboe – Million barrels of oil equivalent.

mmbtu – Million British thermal units.

1

mmcfd – Million cubic feet per day.

mmta – Million metric tonnes per annum.

MPC - Marathon Petroleum Corporation – The separate independent company which now owns and operates the downstream business.

mtd – Thousand metric tonnes per day.

Net acres or Net wells – The sum of the fractional working interests owned by us in gross acres or gross wells.

NGL or NGLs – Natural gas liquid or natural gas liquids, which are naturally occurring substances found in natural gas, including ethane, butane, isobutane, propane and natural gasoline, that can be collectively removed from produced natural gas, separated into these substances and sold.

NYMEX - New York Mercantile Exchange.

OECD – Organization for Economic Cooperation and Development.

OPEC – Organization of Petroleum Exporting Countries.

Operational availability – A term used to measure the ability of an asset to produce to its maximum capacity over a specified period of time, after consideration of internal losses.

Productive well – A well that is not a dry well. Productive wells include producing wells and wells that are mechanically capable of production.

Proved developed reserves – Proved reserves that can be expected to be recovered through existing wells with existing equipment and operating methods or for which the cost of the required equipment is relatively minor compared to the cost of a new well and through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by means not involving a well.

Proved reserves – Proved crude oil and condensate, NGLs, natural gas and synthetic crude oil reserves are those quantities of crude oil and condensate, NGLs, natural gas and synthetic crude oil, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible from a given date forward, from known reservoirs, and under existing economic conditions, operating methods, and government regulations-prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time.

Proved undeveloped reserves – Proved reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for recompletion or through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by means not involving a well. Reserves on undrilled acreage shall be limited to those directly offsetting development spacing areas that are reasonably certain of production when drilled, unless evidence using reliable technology exists that establishes reasonable certainty of economic producibility at greater distances.

PSC – Production sharing contract.

Quest CCS – Quest Carbon Capture and Storage project at the AOSP in Alberta, Canada.

Reserve replacement ratio – A ratio which measures the amount of proved reserves added to our reserve base during the year relative to the amount of liquid hydrocarbons and natural gas produced.

Royalty interest – An interest in an oil or natural gas property entitling the owner to a share of oil or natural gas production free of costs of production.

SAGE – United Kingdom Scottish Area Gas Evacuation system composed of a pipeline and processing terminal.

SAR or SARs – Stock appreciation right or stock appreciation rights.

SCOOP – South Central Oklahoma Oil Province.

SEC – United States Securities and Exchange Commission.

Seismic – An exploration method of sending energy waves or sound waves into the earth and recording the wave reflections to indicate the type, size, shape and depth of subsurface rock formation (3-D seismic provides three-dimensional pictures and 4-D factors in changes that occurred over time).

STACK – Sooner Trend, Anadarko (basin), Canadian (and) Kingfisher (counties).

2

TD - Total depth or the bottom of a drilled hole.

Total proved reserves – The summation of proved developed reserves and proved undeveloped reserves.

U.K. – United Kingdom.

U.S. – United States of America.

U.S. GAAP – Accounting principles generally accepted in the U.S.

WCS – Western Canadian Select, an oil index benchmark price with monthly pricing based upon average WTI adjusted for differentials unique to western Canada.

Working interest – The interest in a mineral property which gives the owner that share of production from the property. A working interest owner bears that share of the costs of exploration, development and production in return for a share of production. Working interests are sometimes burdened by overriding royalty interest or other interests.

WTI – West Texas Intermediate crude oil, an oil index benchmark price as quoted by NYMEX.

3

Disclosures Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These are statements, other than statements of historical fact, that give current expectations or forecasts of future events, including without limitation: our operational, financial and growth strategies, including drilling plans and projects, planned wells, rig count, inventory, seismic, exploration plans, maintenance activities, drilling and completion improvements, workforce reductions and expected savings, cost reductions, non-core asset sales, and financial flexibility; our ability to successfully effect those strategies and the expected timing and results thereof; our 2016 Capital Program and the planned allocation thereof; planned capital expenditures and the impact thereof; expectations regarding future economic and market conditions and their effects on us; our ability and strategies to manage through the lower commodity price cycle; our financial and operational outlook, and ability to fulfill that outlook; our financial position, balance sheet, liquidity and capital resources, and the benefits thereof; resource and asset potential; reserve estimates; growth expectations; and future production and sales expectations, and the drivers thereof. In addition, many forward-looking statements may be identified by the use of forward-looking terminology such as "anticipates," "believes," "estimates," "expects," "targets," "plans," "projects," "could," "may," "should," "would" or similar words indicating that future outcomes are uncertain. While we believe that our assumptions concerning future events are reasonable, we can give no assurance that these expectations will prove to be correct. A number of factors could cause results to differ materially from those indicated by such forward-looking statements including, but not limited to:

• | conditions in the oil and gas industry, including pricing and supply/demand levels for crude oil and condensate, NGLs, natural gas and synthetic crude oil; |

• | changes in expected reserve or production levels; |

• | changes in political or economic conditions in key operating markets, including international markets; |

• | capital available for exploration and development; |

• | well production timing; |

• | availability of drilling rigs, materials and labor; |

• | difficulty in obtaining necessary approvals and permits; |

• | non-performance by third parties of their contractual obligations; |

• | unforeseen hazards such as weather conditions, acts of war or terrorist acts and the governmental or military response thereto; |

• | cyber-attacks; |

• | changes in safety, health, environmental and other regulations; |

• | other geological, operating and economic considerations; and |

• | other factors discussed in Item 1. Business, Item 1A. Risk Factors, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations, Item 7A. Quantitative and Qualitative Disclosures About Market Risk, and elsewhere in this report. |

All forward-looking statements included in this report are based on information available to us on the date of this report. Except as required by law, we assume no duty to revise or update any forward-looking statements whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained throughout this report.

4

PART I

Item 1. Business

General

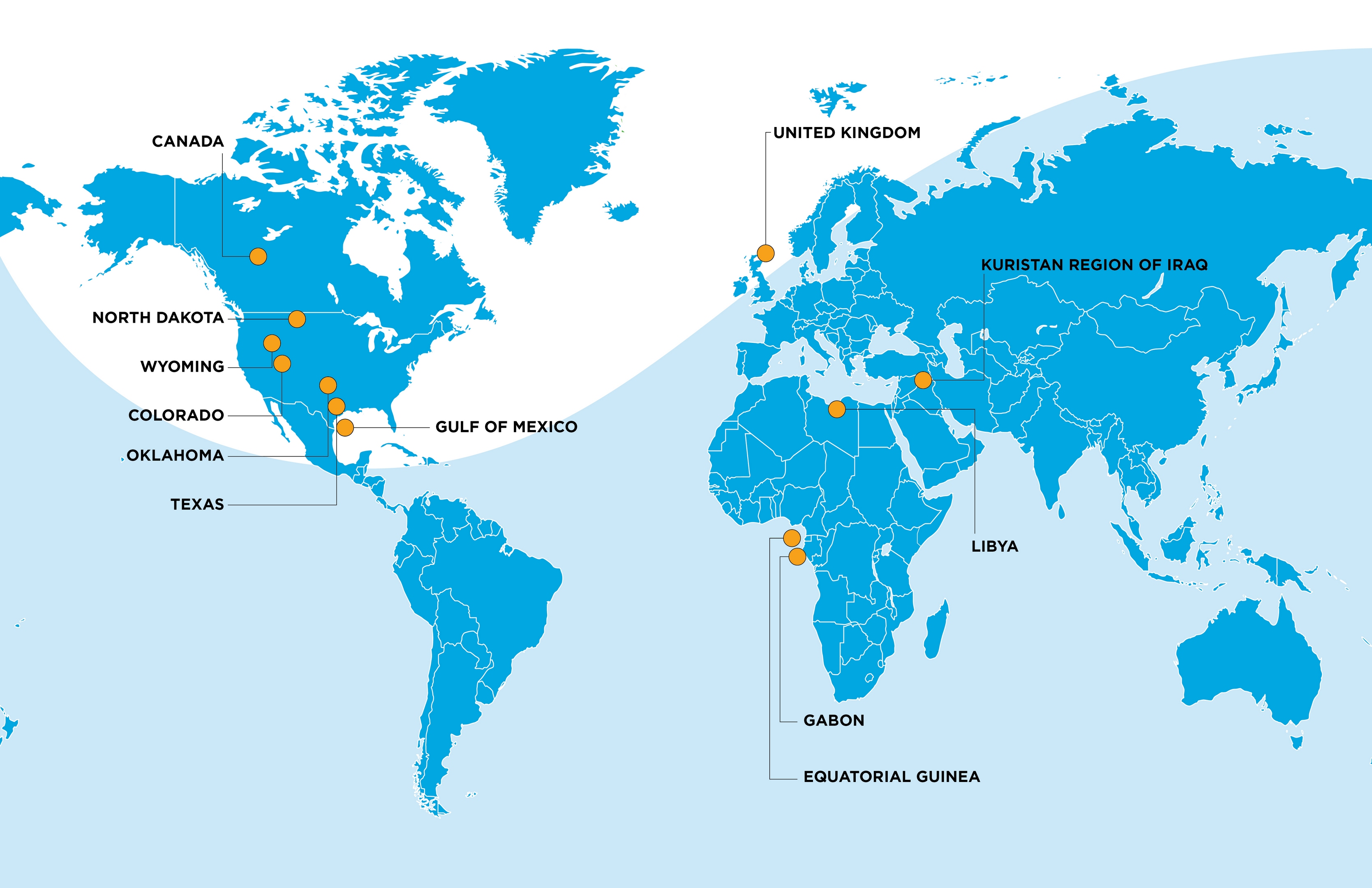

Marathon Oil Corporation is an independent global exploration and production company based in Houston, Texas, with operations in North America, Europe and Africa. Our corporate headquarters are located at 5555 San Felipe Street, Houston, Texas 77056-2723 and our telephone number is (713) 629-6600. Each of our three reportable operating segments is organized based upon both geographic location and the nature of the products and services it offers.

• | North America E&P – explores for, produces and markets crude oil and condensate, NGLs and natural gas in North America; |

• | International E&P – explores for, produces and markets crude oil and condensate, NGLs and natural gas outside of North America and produces and markets products manufactured from natural gas, such as LNG and methanol, in E.G.; and |

• | Oil Sands Mining – mines, extracts and transports bitumen from oil sands deposits in Alberta, Canada, and upgrades the bitumen to produce and market synthetic crude oil and vacuum gas oil. |

We were incorporated in 2001. On June 30, 2011, we completed the spin-off of our downstream business, creating two independent energy companies: Marathon Oil and MPC.

Strategy and Results Summary

Marathon Oil's strategy is to safely and sustainably deliver value by investing in low cost, liquids-rich projects with a focus on risk-adjusted rates of return. We are focused in the high quality core of three premier unconventional resource plays in the U.S.: the Eagle Ford, Bakken and Oklahoma Resource Basins. Our strategy for our operated conventional producing assets in E.G., the U.K. and the U.S. is to maximize value and cash flow to provide flexibility to invest in the shorter cycle opportunities in the U.S. resource plays. Our conventional exploration program is currently limited to existing commitments in the Gulf of Mexico and Gabon. Our strategy is guided by the following seven strategic imperatives ("SI 7 "):

1. Living Our Values

2. | Investing in Our People |

3. | Continuous Improvement in Operational and Capital Efficiency |

4. | Driving Profitable and Sustainable Growth |

5. | Rigorous Portfolio Management |

6. | Quality and Material Resource Capture |

7. | Delivering Long-Term Shareholder Value |

Commodity prices are the most significant factor impacting our revenues, profitability, operating cash flows and the amount of capital available to reinvest into our business. The low pricing environment has presented several challenges for us and our industry. We responded to the lower commodity prices in a number of ways:

• | Reduced our 2015 Capital Program by approximately 50% from the prior year, down to $3 billion |

• | Established our 2016 Capital Program at $1.4 billion |

• | Exercised cost discipline, significantly reducing drilling and completion, production and general and administrative costs |

• | Drove sustainable operational efficiency gains in the U.S. unconventional resource plays |

• | Scaled back our conventional exploration program to focus on our U.S. unconventional resources plays |

• | Increased our target for non-core asset sales, now $750 million to $1 billion, up from our previous goal of $500 million |

◦ | Closed over $300 million of non-core asset sales (excluding closing adjustments) |

• | Protected our liquidity and capital structure: |

◦ | Issued $2 billion aggregate principal amount of unsecured senior notes ($1 billion of which was used to repay the 0.90% senior notes that matured in November 2015) |

◦ | Increased the capacity of the revolving credit facility from $2.5 billion to $3.0 billion while also extending the maturity date an additional year to May 2020 |

◦ | Decreased our quarterly dividend from $0.21 to $0.05 per share, saving approximately $425 million of cash on an annualized basis |

5

In 2015, we continued to focus on the U.S. unconventional resource plays. We progressed co-development in the Eagle Ford, further delineated Austin Chalk in the Eagle Ford along with SCOOP/STACK in the Oklahoma Resource Basins and improved overall competitiveness in the Bakken with cost reductions and enhanced completions. Our U.S. operations added 73 mmboe proved reserves in 2015, excluding acquisitions, dispositions and production, amounting to an increase of 107% over the prior year's ending balance.

Net sales volumes from continuing operations increased by 6% to 438 mboed in 2015 from 415 mboed in 2014. Volumes from our three U.S. resource plays totaled 218 mboed, an increase of 20% from 181 mboed in 2014. For the total company, we ended 2015 with proved reserves of approximately 2,163 mmboe as compared to 2,198 mmboe at the end of 2014 .

See Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations - Outlook, for a more detailed discussion of our operating results, cash flows and outlook, including the 2016 Capital Program.

The map below shows the locations of our worldwide operations.

Segment and Geographic Information

For operating segment and geographic financial information, see Item 8. Financial Statements and Supplementary Data – Note 7 to the consolidated financial statements.

In the following discussion regarding our North America E&P, International E&P and Oil Sands Mining segments, references to net wells, acres, sales or investment indicate our ownership interest or share, as the context requires.

North America E&P Segment

We are engaged in oil and gas exploration, development and/or production activities in the U.S. and Canada. Our primary focus in the North America E&P segment is concentrated within our unconventional resource plays. The following tables provide additional detail regarding net sales volumes, sales mix and operated drilling activity:

6

Net Sales Volumes | 2015 |

| Increase |

| 2014 |

| Increase |

| 2013 | |||||

Equivalent Barrels ( mboed ) |

|

|

|

|

|

|

|

|

| |||||

Eagle Ford | 134 | |

| 20 | % |

| 112 | |

| 38 | % |

| 81 | |

Oklahoma Resource Basins | 25 | |

| 39 | % |

| 18 | |

| 29 | % |

| 14 | |

Bakken | 59 | |

| 16 | % |

| 51 | |

| 31 | % |

| 39 | |

Other North America (a) | 51 | |

| (11 | )% |

| 57 | |

| (15 | )% |

| 67 | |

Total North America E&P ( mboed ) | 269 | |

| 13 | % |

| 238 | |

| 18 | % |

| 201 | |

Sales Mix - U.S. Resource Plays - 2015 | Eagle Ford |

| Oklahoma Resource Basins |

| Bakken | |||

Crude oil and condensate | 60 | % |

| 19 | % |

| 87 | % |

Natural gas liquids | 19 | % |

| 28 | % |

| 7 | % |

Natural gas | 21 | % |

| 53 | % |

| 6 | % |

Drilling Activity - U.S. Resource Plays | 2015 |

| 2014 |

| 2013 | |||

Gross Operated |

|

|

|

|

| |||

Eagle Ford: |

|

|

|

|

| |||

Wells drilled to total depth | 251 | |

| 360 | |

| 299 | |

Wells brought to sales | 276 | |

| 310 | |

| 307 | |

Oklahoma Resource Basins: |

|

|

|

|

| |||

Wells drilled to total depth | 20 | |

| 19 | |

| 10 | |

Wells brought to sales | 21 | |

| 18 | |

| 9 | |

Bakken: |

|

|

|

|

| |||

Wells drilled to total depth | 35 | |

| 83 | |

| 76 | |

Wells brought to sales | 56 | |

| 69 | |

| 77 | |

Eagle Ford - As of December 31, 2015 , we had approximately 153,000 net acres in the Eagle Ford in south Texas and 1,236 gross (911 net) operated producing wells, where we have been operating since 2011.

Of the 276 gross wells brought to sales in 2015, 56 were in the Austin Chalk, 28 were in the Upper Eagle Ford and 192 were in the Lower Eagle Ford. Of the 310 gross wells brought to sales in 2014, 22 were in the Austin Chalk and four were in the Upper Eagle Ford. Our 2015 average spud-to-TD time was 11 days compared to 13 days in 2014 . Our high-density pad drilling continues to average approximately four wells per pad in 2015 . The continued focus on stimulation design has contributed to incremental improvements in well performance across our area of activity.

During 2015, we continued evaluation of the Austin Chalk formation and began delineation of Upper Eagle Ford across our acreage position in south Texas, with a total of 22,000 Austin Chalk acres and 16,500 Upper Eagle Ford acres now delineated. The mix of crude oil and condensate, NGLs and natural gas from the Austin Chalk wells is similar to Eagle Ford condensate wells. Co-development of the Austin Chalk, Upper and Lower Eagle Ford horizons will leverage the infrastructure investments we have made to support production growth across the Eagle Ford operating area.

We operate approximately 800 miles of gathering pipeline in the Eagle Ford area. We now have 32 central gathering and treating facilities, with aggregate capacity of more than 475 mboed. We also own and operate the Sugarloaf gathering system, a 42-mile natural gas pipeline through the heart of our acreage in Karnes, Atascosa and Bee Counties of south Texas.

In late 2015 , we connected to a newly constructed third-party liquids pipeline, which allowed us to increase the amount of our Eagle Ford production transported by pipeline to 90% at year-end, up from an average of 70% during 2014. The ability to transport more barrels by pipeline enables us to improve/optimize price realizations, reduce costs, improve reliability and lessen our environmental footprint.

Approximately 42% of our 2016 Capital Program, $600 million, is allocated to the Eagle Ford. We expect drilling activity to average five rigs in 2016. Our drilling plans for 2016 include drilling 91 - 96 net wells (150 - 160 gross, of which we will operate 134 - 141). We anticipate bringing 124 - 132 gross operated wells to sales during 2016.

Oklahoma Resource Basins – Our primary focus in 2016 will be in the SCOOP and STACK areas. In the SCOOP and STACK areas we hold approximately 265,000 net acres with rights to the Woodford, Springer, Meramec, Granite Wash and

7

other Pennsylvanian and Mississippian plays. This includes 8,000 net acres added in the Oklahoma Resource Basins, primarily in the STACK Meramec play during 2015.

Approximately 90% of our SCOOP acreage is held by production. In the SCOOP Woodford, we delineated over 70% of our acreage. We estimate the SCOOP Springer has a high oil yield that is about 85% liquids. We believe about 80% of our acreage in STACK has the potential for co-development of multiple horizons. About 67,000 STACK Woodford acres are delineated while approximately 42,000 acres of STACK Meramec acreage is delineated.

Approximately 14% of our 2016 Capital Program, $204 million, is allocated to the Oklahoma Resource Basins, which will support two rigs and lease retention in the STACK and delineation of the SCOOP Springer and Meramec. Our drilling plans for the Oklahoma Resource Basins in 2016 call for drilling and completing 23 - 28 net wells (65 - 75 gross, of which 24 - 27 are company operated wells). We anticipate bringing 20 - 22 gross operated wells to sales during 2016.

Bakken – We hold approximately 277,000 net acres in the Bakken shale oil play in North Dakota and eastern Montana, where we have been operating since 2006. We continue to see improvement in efficiency and well performance through optimizing completion techniques. We successfully completed a 55-well enhanced completion trial program that began in late 2014 and continued through 2015. We will continue executing and evaluating enhanced completion designs, including increased stage counts, high proppant volumes and fluid types as opportunities arise in 2016. Our large scale water gathering system is currently handling over 50% of our produced water. With a second phase expected to be fully operational in the second half of 2016, we anticipate this system will manage 80% of produced water by year end.

Our time to drill a well averaged 15 days spud-to-TD in 2015 compared to 17 days in 2014 . We recompleted 11 wells during 2015. In efforts to optimize price realizations, we sell our production in local North Dakota markets and to select purchasers who may elect to transport outside the state.

Approximately 13% of our 2016 Capital Program, $193 million, is allocated to the Bakken, which will support one rig in 2016. Our 2016 Bakken program includes plans to drill 10 - 12 net wells (45 - 55 gross, of which we will operate 8 - 10). We anticipate bringing 13 - 15 gross operated wells to sales during 2016.

Other North America

During 2015, we further emphasized our focus on the U.S. unconventional resource plays, continued to maximize cash generation from our conventional assets and continued to dispose of non-core assets. In August 2015, we closed the sale of our East Texas, North Louisiana and Wilburton, Oklahoma natural gas assets. In December 2015, we closed the sale of our operated producing properties in the greater Ewing Bank area and non-operated producing interests in the Petronius field in the Gulf of Mexico. In February 2016, we closed the sale of our non-operated producing interests in the Neptune field in the Gulf of Mexico. These assets collectively produced approximately 14 mboed in 2015.

Other North America consists primarily of onshore production operations in Wyoming and development activities in the Gulf of Mexico. In the Gulf, development work continues in the Gunflint field located on Mississippi Canyon Blocks 948, 949, 992 (N/2) and 993 (N/2). The development wells were completed in 2015. First oil is expected in mid-2016 after the completion of work at the third-party Gulfstar 1 host facility. We hold an 18% non-operated working interest in the Gunflint field.

A deepwater oil discovery on the Shenandoah prospect, located on Walker Ridge Block 51, was drilled in 2009. We own a 10% non-operated working interest in this prospect. The first appraisal well on the Shenandoah prospect reached total depth in 2013 and was successful. The operator drilled a second appraisal well in 2014, which was unsuccessful. A third appraisal well was spud in 2015, and was successfully sidetracked, logged and cored, finding more than 620 feet of net oil pay. A fourth appraisal well is expected to be spud in the first quarter of 2016.

Wyoming - We have ongoing waterflood and enhanced oil recovery projects in the mature Big Horn and Wind River Basins. Marathon is the third largest oil producer in the state of Wyoming. We also have conventional natural gas operations in the Greater Green River Basin.

Our Wyoming net sales averaged 17 mbbld of liquid hydrocarbons and 4 mmcfd of natural gas, or 17 mboed, during 2015 compared to 18 mboed in 2014. In addition, Marathon owns the 420-mile Red Butte Pipeline which connects oil fields in the Big Horn Basin to both the Silvertip Station on the Montana/Wyoming state line and to alternate outlets in Casper, Wyoming.

8

North America E&P--Exploration

In September 2015, we announced our intention to scale back our conventional exploration program. Our 2016 Capital Program includes $15 million for conventional exploration. No conventional exploration wells are planned in 2016. Our Capital Program is limited to existing commitments in the Gulf of Mexico. We continue to evaluate options for utilization of our remaining commitments on the Maersk Valiant drillship. The rig is currently being operated by our rig share partner, and we anticipate the rig to be available for our use in early 2017.

The Solomon exploration prospect located on Walker Ridge Block 225 was spud during the second quarter of 2015 and reached total depth in the fourth quarter. The well did encounter the lower tertiary target interval. The well was plugged and abandoned, with well costs charged to dry well expense, and the rig was released with no further activity planned on the block. We hold a 58% operated working interest in this prospect.

We hold interests in both operated and non-operated exploration stage oil sand leases in Alberta, Canada, which could be developed using in-situ methods of extraction. These leases cover approximately 142,000 gross ( 54,000 net) acres in four project areas: Namur, in which we hold a 70% operated interest; Birchwood, in which we hold a 100% operated interest; Ells River, in which we hold a 20% non-operated interest; and Saleski in which we hold a 33% non-operated interest. During 2015, in connection with our decision to scale back our conventional exploration program, and also after further evaluation of the estimated recoverable resources and our development plans at Birchwood, Ells River and Namur, we impaired the remaining net book values of these in-situ properties.

International E&P Segment

We are engaged in oil and gas exploration, development and/or production activities in E.G., Gabon, the Kurdistan Region of Iraq, Libya and the U.K. We include the results of our natural gas liquefaction operations and methanol production operations in E.G. in our International E&P segment. The following table provides net sales volumes for our significant operational areas within this segment:

Net Sales Volumes | 2015 |

| Increase |

| 2014 |

| Increase |

| 2013 | |||||

Equivalent Barrels ( mboed ) |

|

|

|

|

|

|

|

|

| |||||

Equatorial Guinea | 97 | |

| (7 | )% |

| 104 | |

| (3 | )% |

| 107 | |

United Kingdom (a) | 19 | |

| 19 | % |

| 16 | |

| (20 | )% |

| 20 | |

Libya | - | |

| (100 | )% |

| 7 | |

| (75 | )% |

| 28 | |

Total International E&P ( mboed ) | 116 | |

| (9 | )% |

| 127 | |

| (18 | )% |

| 155 | |

Net Sales Volumes of Equity Method Investees |

|

|

|

|

|

|

|

|

| |||||

LNG ( mtd ) | 5,884 | |

| (10 | )% |

| 6,535 | |

| - | % |

| 6,548 | |

Methanol ( mtd ) | 937 | |

| (14 | )% |

| 1,092 | |

| (13 | )% |

| 1,249 | |

Africa

Equatorial Guinea – Production – We own a 63% operated working interest under a PSC in the Alba field which is offshore E.G. Operational availability from our company-operated facilities averaged approximately 97% in 2015 . In the third quarter of 2015, production was increased as the Alba C21 development well came online with higher than expected liquid yields, in combination with a successful well intervention program on five existing Alba wells. In January 2016, we completed the installation of an offshore compression platform which is expected to start up mid-2016 following completion of hookup and commissioning activities. The compression project was designed to maintain the production plateau two additional years and extend field life up to eight years.

Equatorial Guinea – Gas Processing – We own a 52% interest in Alba Plant LLC, an equity method investee, that operates an onshore LPG processing plant located on Bioko Island. Alba field natural gas is processed by the LPG plant. Under a long-term contract at a fixed price per btu, the LPG plant extracts secondary condensate and LPG from the natural gas stream and uses some of the remaining dry natural gas in its operations.

We also own 60% of EGHoldings and 45% of AMPCO, both of which are accounted for as equity method investments. EGHoldings operates an LNG production facility and AMPCO operates a methanol plant, both located on Bioko Island. These facilities allow us to monetize natural gas reserves from the Alba field.

EGHoldings' 3.7 mmta LNG production facility sells LNG under a 3.4 mmta, or 460 mmcfd, sales and purchase agreement through 2023. The purchaser under the agreement takes delivery of the LNG on Bioko Island, with pricing linked principally to the Henry Hub index. Gross sales of LNG from this production facility totaled 3.6 mmta in 2015 .

9

AMPCO had gross sales totaling 760 mt in 2015 . Production from the plant is used to supply customers in Europe and the U.S.

Libya – We hold a 16% non-operated working interest in the Waha concessions, which encompass almost 13 million gross acres located in the Sirte Basin of eastern Libya, where civil and political unrest continues to interrupt our production operations. Operations were interrupted in mid-2013 as a result of the shutdown of the Es Sider crude oil terminal, and although temporarily re-opened during the second half of 2014, production remains shut-in through early 2016. Considerable uncertainty remains around the timing of future production and sales levels. We and our partners in the Waha concessions continue to assess the situation and the condition of our assets in Libya. See Item 8. Financial Statements and Supplementary Data – Note 12 to the consolidated financial statements for additional information about our Libya operations.

Other International

United Kingdom – Our largest asset in the U.K. sector of the North Sea is the Brae area complex where we are the operator and have a 42% working interest in the South, Central, North and West Brae fields and a 39% working interest in the East Brae field. The Brae Alpha platform and facilities host the South, Central and West Brae fields. The North Brae and East Brae fields are natural gas condensate fields which are produced via the Brae Bravo and the East Brae platforms, respectively. The East Brae platform also hosts the nearby Braemar field in which we have a 28% working interest. During the second quarter of 2015, we completed the final three wells of a five-well Brae infill drilling program that began in 2014.

The strategic location of the Brae platforms, along with pipeline and onshore infrastructure, has generated third-party processing and transportation business since 1986. Currently, the operators of 31 third-party fields are contracted to use the Brae system and 72 mboed are being processed or transported through the Brae infrastructure. In addition to generating processing and pipeline tariff revenue, this third-party business optimizes infrastructure usage.

The working interest owners of the Brae area producing assets collectively own a 50% non-operated interest in the SAGE system. The SAGE pipeline transports natural gas from the Brae area, and the third-party Beryl area, and has a total wet natural gas capacity of 1.1 bcf per day. The SAGE terminal at St. Fergus in northeast Scotland processes natural gas from the SAGE pipeline as well as approximately 0.3 bcf per day of third-party natural gas.

We own non-operated working interests in the Foinaven area complex, consisting of a 28% working interest in the main Foinaven field, a 47% working interest in East Foinaven and a 20% working interest in the T35 and T25 fields. The export of Foinaven liquid hydrocarbons is via shuttle tanker from an FPSO to market. All natural gas sales are to the non-operated Magnus platform for use as injection gas.

Kurdistan Region of Iraq – In aggregate, we have approximately 109,000 net acres in the Kurdistan Region of Iraq. We have a 45% operated working interest in the Harir block located northeast of Erbil. We also have non-operated interests in two blocks located north-northwest of Erbil: Atrush with 15% working interest and Sarsang with 20% working interest.

On the non-operated Atrush block, following the successful appraisal program and a declaration of commerciality, the Kurdistan Ministry of Natural Resources approved a plan for field development in September 2013. The development project consists of drilling four production wells and constructing a central processing facility in Phase 1 which provides for a 25-year production period. We expect first production in late 2016 with estimated initial gross production of approximately 30 mbbld of oil. Subject to further drilling and testing results, and partner and government approvals, a potential Phase 2 development could add an additional gross 30 mbbld facility.

On the non-operated Sarsang block, the Swara Tika discovery was declared commercial in May 2014 and a field development plan was filed in June 2014. The plan was approved by the Kurdistan Ministry of Natural Resources in the fourth quarter of 2015. The first producing well came online in 2014 and the second producing well came online in December 2015. In 2016, an additional well is planned to come on-line. As the development plan progresses, we expect to increase production after 2016.

International E&P Exploration

In September 2015, we announced our intention to scale back our conventional exploration program. Our 2016 Capital Program includes $16 million for conventional exploration. No conventional exploration wells are planned in 2016. Our Capital Program is limited to existing commitments in Gabon.

Equatorial Guinea – Exploration – We hold a 63% operated working interest in the Deep Luba discovery on the Alba Block and an 80% operated working interest in the Corona well on Block D. We plan to develop Block D through a unitization with the Alba field. Negotiations have been substantially completed and approval is expected in 2016. We also have an 80% operated working interest in exploratory Block A-12 offshore Bioko Island, located immediately west of our operated Alba Field.

10

Gabon – Exploration – We hold a 21.25% non-operated working interest in the Diaba License G4-223 and its related permit offshore Gabon, which covers approximately 2.2 million gross (477,000 net) acres. Multiple additional pre-salt prospects have been identified on this License.

In August 2014, we signed an exploration and production sharing contract for Gabon offshore Block G13, which was subsequently re-named Tchicuate. The block, which is located in the pre-salt play offshore Gabon, encompasses 277,000 acres. The seismic program was completed during 2015 and processing will occur through 2016. We hold a 100% participating interest and operatorship in the block. In the event of development, the Republic of Gabon will assume a 20% financed interest in the contract upon commencement of production. The State holds additional rights to participate in the block in the future as a co-investor.

Kurdistan Region of Iraq – During 2015, in connection with our decision to scale back our conventional exploration program, we impaired our investment in the operated Harir block.

International E&P Disposition

In the third quarter of 2015, we entered into an agreement to sell our East Africa exploration acreage in Ethiopia and Kenya. The Kenya transaction closed in February 2016 and the Ethiopia transaction is expected to close during the first quarter of 2016. See Item 8. Financial Statements and Supplementary Data - Note 5 to the consolidated financial statements for additional information about this disposition.

Oil Sands Mining Segment

We hold a 20% non-operated interest in the AOSP, an oil sands mining and upgrading joint venture located in Alberta, Canada. Other JV partners include Shell Canada Limited with a 60% ownership interest and Chevron Canada Limited with a 20% ownership interest. Shell Canada Limited operates the joint venture, which produces bitumen from oil sands deposits in the Athabasca region utilizing mining techniques and upgrades the bitumen into synthetic crude oils and vacuum gas oil.

The AOSP's mining and extraction assets are located near Fort McMurray, Alberta, and include the Muskeg River and the Jackpine mines. Gross design capacity of the combined mines is 255,000 (51,000 net) barrels of bitumen per day. The AOSP operations use established processes to mine oil sands deposits from an open-pit mine, extract the bitumen and upgrade it into synthetic crude oils. Ore is mined using traditional truck and shovel mining techniques. The mined ore passes through a series of primary crushers and rotary breakers for particle size reduction. The particles are combined with hot water to create slurry. The slurry is hydro-transported to a primary separation vessel where it separates into sand, clay and bitumen-rich froth. A solvent is added to the bitumen froth to separate out the remaining solids, water and heavy asphaltenes. The solvent washes the sand and produces clean bitumen that is required for the upgrader to run efficiently. The process yields a mixture of solvent and bitumen which is then transported from the mine to the Scotford upgrader via the approximately 300-mile Corridor Pipeline.

The AOSP's Scotford upgrader is located at Fort Saskatchewan, northeast of Edmonton, Alberta. The bitumen is upgraded at Scotford using both hydrotreating and hydroconversion processes to remove sulfur and break the heavy bitumen molecules into lighter products. Blendstocks acquired from outside sources are utilized in the production of our saleable products. The upgrader produces synthetic crude oils and vacuum gas oil. The vacuum gas oil is sold to an affiliate of the operator under a long-term contract at market-related prices and the other products are sold in the marketplace.

As of December 31, 2015 , we own or have rights to participate in developed and undeveloped surface mineable leases totaling approximately 159,000 gross (32,000 net) acres. The underlying developed leases are held for the duration of the project, with royalties payable to the province of Alberta. Synthetic crude oil sales volumes for 2015 averaged 53 mbbld and net-of-royalty production was 45 mbbld.

The operating cost structure of our Oil Sands Mining operations is predominantly fixed and therefore many of the costs incurred in times of full operation continue during production downtime. Per-unit costs are sensitive to production rates. As average price realizations are typically at a discount to WTI, the fixed operating cost structure for Oil Sands Mining will not fully track the price realization. Significant cost improvement efforts were employed in 2015 resulting in a material reduction to the production cost structure. See Item 7. Consolidated Results of Operations: 2015 compared to 2014 for additional detail on production expenses.

The governments of Alberta and Canada agreed to partially fund Quest CCS. Construction began in 2012 and was completed in February 2015. Government funding commenced in 2012 and continued as milestones were achieved during the development, construction and operating phases of the project. Quest CCS was successfully completed and commissioned in the fourth quarter of 2015.

11

Productive and Drilling Wells

For our North America E&P and International E&P segments, the following table sets forth gross and net productive wells and service wells as of December 31, 2015 , 2014 and 2013 and drilling wells as of December 31, 2015 .

| Productive Wells (a) |

|

|

|

|

|

|

|

| ||||||||||||||

| Oil |

| Natural Gas |

| Service Wells |

| Drilling Wells | ||||||||||||||||

| Gross |

| Net |

| Gross |

| Net |

| Gross |

| Net |

| Gross |

| Net | ||||||||

2015 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

U.S. | 7,198 | |

| 2,878 | |

| 1,796 | |

| 750 | |

| 2,727 | |

| 747 | |

| 29 | |

| 12 | |

E.G. | - | |

| - | |

| 17 | |

| 11 | |

| 2 | |

| 1 | |

| - | |

| - | |

Other Africa | 1,071 | |

| 175 | |

| 7 | |

| 1 | |

| 94 | |

| 16 | |

| 4 | |

| 1 | |

Total Africa | 1,071 | |

| 175 | |

| 24 | |

| 12 | |

| 96 | |

| 17 | |

| 4 | |

| 1 | |

Other International | 59 | |

| 21 | |

| 39 | |

| 16 | |

| 24 | |

| 8 | |

| 1 | |

| - | |

Total | 8,328 | |

| 3,074 | |

| 1,859 | |

| 778 | |

| 2,847 | |

| 772 | |

| 34 | |

| 13 | |

2014 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

U.S. | 7,058 | |

| 2,919 | |

| 2,246 | |

| 1,023 | |

| 2,638 | |

| 760 | |

|

|

|

| ||

E.G. | - | |

| - | |

| 16 | |

| 11 | |

| 2 | |

| 1 | |

|

|

|

| ||

Other Africa | 1,071 | |

| 175 | |

| 7 | |

| 1 | |

| 94 | |

| 16 | |

|

|

|

| ||

Total Africa | 1,071 | |

| 175 | |

| 23 | |

| 12 | |

| 96 | |

| 17 | |

|

|

|

| ||

Other International | 55 | |

| 20 | |

| 39 | |

| 16 | |

| 24 | |

| 8 | |

|

|

|

| ||

Total | 8,184 | |

| 3,114 | |

| 2,308 | |

| 1,051 | |

| 2,758 | |

| 785 | |

|

|

|

| ||

2013 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

U.S. | 6,632 | |

| 2,568 | |

| 2,763 | |

| 1,482 | |

| 2,349 | |

| 744 | |

|

|

|

| ||

E.G. | - | |

| - | |

| 16 | |

| 11 | |

| 2 | |

| 1 | |

|

|

|

| ||

Other Africa | 1,064 | |

| 174 | |

| 7 | |

| 1 | |

| 94 | |

| 16 | |

|

|

|

| ||

Total Africa | 1,064 | |

| 174 | |

| 23 | |

| 12 | |

| 96 | |

| 17 | |

|

|

|

| ||

Other International | 56 | |

| 21 | |

| 40 | |

| 16 | |

| 25 | |

| 9 | |

|

|

|

| ||

Total | 7,752 | |

| 2,763 | |

| 2,826 | |

| 1,510 | |

| 2,470 | |

| 770 | |

|

|

|

| ||

(a) | Of the gross productive wells, wells with multiple completions operated by us totaled 12 , 31 and 31 as of December 31, 2015 , 2014 and 2013 . Information on wells with multiple completions operated by others is unavailable to us. |

12

Drilling Activity

For our North America E&P and International E&P segments, the following table sets forth, by geographic area, the number of net productive and dry development and exploratory wells completed in each of the last three years.

| Development |

| Exploratory |

|

| |||||||||||||||||||||

| Oil |

| Natural Gas |

| Dry |

| Total |

| Oil |

| Natural Gas |

| Dry |

| Total |

| Total | |||||||||

Year Ended December 31, 2015 |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

U.S. | 135 | |

| 36 | |

| 11 | |

| 182 | |

| 49 | |

| 48 | |

| 1 | |

| 98 | |

| 280 | |

E.G. | - | |

| 1 | |

| - | |

| 1 | |

| - | |

| - | |

| 1 | |

| 1 | |

| 2 | |

Other Africa | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

Total Africa | - | |

| 1 | |

| - | |

| 1 | |

| - | |

| - | |

| 1 | |

| 1 | |

| 2 | |

Other International | 1 | |

| - | |

| - | |

| 1 | |

| - | |

| - | |

| - | |

| - | |

| 1 | |

Total | 136 | |

| 37 | |

| 11 | |

| 184 | |

| 49 | |

| 48 | |

| 2 | |

| 99 | |

| 283 | |

Year Ended December 31, 2014 |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

U.S. | 253 | |

| 43 | |

| 1 | |

| 297 | |

| 49 | |

| 19 | |

| 4 | |

| 72 | |

| 369 | |

E.G. | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| 1 | |

| 1 | |

| 1 | |

Other Africa | 1 | |

| - | |

| - | |

| 1 | |

| - | |

| - | |

| - | |

| - | |

| 1 | |

Total Africa | 1 | |

| - | |

| - | |

| 1 | |

| - | |

| - | |

| 1 | |

| 1 | |

| 2 | |

Other International | 1 | |

| - | |

| - | |

| 1 | |

| - | |

| - | |

| - | |

| - | |

| 1 | |

Total | 255 | |

| 43 | |

| 1 | |

| 299 | |

| 49 | |

| 19 | |

| 5 | |

| 73 | |

| 372 | |

Year Ended December 31, 2013 |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

U.S. | 237 | |

| 20 | |

| - | |

| 257 | |

| 73 | |

| 13 | |

| 3 | |

| 89 | |

| 346 | |

E.G. | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

Other Africa | 4 | |

| - | |

| - | |

| 4 | |

| 1 | |

| - | |

| 2 | |

| 3 | |

| 7 | |

Total Africa | 4 | |

| - | |

| - | |

| 4 | |

| 1 | |

| - | |

| 2 | |

| 3 | |

| 7 | |

Other International | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| 3 | |

| 3 | |

| 3 | |

Total | 241 | |

| 20 | |

| - | |

| 261 | |

| 74 | |

| 13 | |

| 8 | |

| 95 | |

| 356 | |

Acreage

We believe we have satisfactory title to our North America E&P and International E&P properties in accordance with standards generally accepted in the industry; nevertheless, we can be involved in title disputes from time to time which may result in litigation. In the case of undeveloped properties, an investigation of record title is made at the time of acquisition. Drilling title opinions are usually prepared before commencement of drilling operations. Our title to properties may be subject to burdens such as royalty, overriding royalty, carried, net profits, working and other similar interests and contractual arrangements customary in the industry. In addition, our interests may be subject to obligations or duties under applicable laws or burdens such as net profits interests, liens related to operating agreements, development obligations or capital commitments under international PSCs or exploration licenses.

The following table sets forth, by geographic area, the gross and net developed and undeveloped acreage held in our North America E&P and International E&P segments as of December 31, 2015 .

| Developed |

| Undeveloped |

| Developed and Undeveloped | ||||||||||||

(In thousands) | Gross |

| Net |

| Gross |

| Net |

| Gross |

| Net | ||||||

U.S. | 1,323 | |

| 1,035 | |

| 801 | |

| 638 | |

| 2,124 | |

| 1,673 | |

Canada | - | |

| - | |

| 142 | |

| 54 | |

| 142 | |

| 54 | |

Total North America | 1,323 | |

| 1,035 | |

| 943 | |

| 692 | |

| 2,266 | |

| 1,727 | |

E.G. | 45 | |

| 29 | |

| 183 | |

| 164 | |

| 228 | |

| 193 | |

Other Africa | 12,909 | |

| 2,108 | |

| 26,145 | |

| 9,612 | |

| 39,054 | |

| 11,720 | |

Total Africa | 12,954 | |

| 2,137 | |

| 26,328 | |

| 9,776 | |

| 39,282 | |

| 11,913 | |

Other International | 90 | |

| 32 | |

| 345 | |

| 110 | |

| 435 | |

| 142 | |

Total | 14,367 | |

| 3,204 | |

| 27,616 | |

| 10,578 | |

| 41,983 | |

| 13,782 | |

13

In the ordinary course of business, based on our evaluations of certain geologic trends and prospective economics, we have allowed certain lease acreage to expire and may allow additional acreage to expire in the future. If production is not established or we take no other action to extend the terms of the leases, licenses or concessions, undeveloped acreage listed in the table below will expire over the next three years. We plan to continue the terms of certain of these licenses and concession areas or retain leases through operational or administrative actions; however, the majority of the undeveloped acres associated with Other Africa as listed in the table below pertains to our licenses in Ethiopia and Kenya, for which we executed agreements in 2015 to sell. The Kenya transaction closed in February 2016 and the Ethiopia transaction is expected to close in the first quarter of 2016. See Item 8. Financial Statements and Supplementary Data - Note 5 to the consolidated financial statements for additional information about this disposition.

| Net Undeveloped Acres Expiring | |||||||

| Year Ended December 31, | |||||||

(In thousands) | 2016 |

| 2017 |

| 2018 | |||

U.S. | 68 | |

| 89 | |

| 128 | |

E.G. | - | |

| 92 | |

| 36 | |

Other Africa | 189 | |

| 4,352 | |

| 854 | |

Total Africa | 189 | |

| 4,444 | |

| 890 | |

Other International | - | |

| - | |

| - | |

Total | 257 | |

| 4,533 | |

| 1,018 | |

14

Reserves

Estimated Reserve Quantities

Reserves are disclosed by continent and by country if the proved reserves related to any geographic area, on an oil equivalent barrel basis, represent 15% or more of our total proved reserves. A geographic area can be an individual country, group of countries within a continent or a continent. Other International ("Other Int'l"), includes the U.K. and the Kurdistan Region of Iraq. We closed the sale of our East Texas/North Louisiana/Wilburton assets in the third quarter of 2015 and part of our Gulf of Mexico business in the fourth quarter of 2015. Additionally, we closed the sale of our Angola assets and our Norway business in 2014, and both are represented as discontinued operations ("Disc Ops") for periods presented. Approximately 77% of our proved reserves are located in OECD countries.

Our December 31, 2015 proved reserves were calculated using the unweighted average of closing prices nearest to the first day of each month within the 12-month period ("SEC pricing"). The table below provides the 2015 SEC pricing of benchmark prices as well as the unweighted average for the first two months of 2016:

| SEC Pricing 2015 | 2-month Average 2016 | ||||

WTI Crude oil | $ | 50.28 | | $ | 34.19 | |

Henry Hub natural gas | $ | 2.59 | | $ | 2.28 | |

Brent crude oil | $ | 54.25 | | $ | 34.86 | |

Natural gas liquids | $ | 17.32 | | $ | 12.87 | |

When determining the December 31, 2015 proved reserves for each property, the 2015 SEC prices listed above were adjusted using price differentials that account for property-specific quality and location differences.

Beginning in the second half of 2014, the crude oil and natural gas benchmarks began to decline and these declines continued through 2015 and into 2016. Commodity prices are likely to remain volatile based on global supply and demand and could decline further. Sustained reduced commodity prices could have a material effect on the quantity and future cash flows of our proved reserves.

Estimates of future cash flows associated with proved reserves are based on actual costs of developing and producing the reserves as of the end of the year. The decline in commodity prices prompted a concerted effort to reduce the costs of developing and producing reserves. Therefore, the impact of sustained reduced commodity prices on future cash flows will be partially offset by the resulting lower costs to develop and produce reserves.

A sustained period of lower commodity prices could also result in additional decreases to our near term capital program and deferrals of investment until prices improve. A shifting of capital expenditures into future periods beyond five years from the initial proved reserve booking could potentially lead to a reduction in proved undeveloped reserves. See Item 1A. Risk Factors for a further discussion of how a substantial extended decline in commodity prices could impact us.

As of December 31, 2015, total proved reserves declined 35 mmboe, primarily due to negative revisions in the U.S. totaling 173 mmboe largely a result of reductions to our capital development program which deferred proved undeveloped reserves beyond the 5-year plan, as well as routine production. This decline was partially offset by increased reserves from the drilling programs in our U.S. unconventional shale plays totaling 246 mmboe as well as a positive revision of 67 mmboe in OSM. The OSM revision was a consequence of technical reevaluation and lower royalty percentages due to lower realized prices. Royalties paid in Canada are on a sliding scale; as the sales price of our synthetic crude oil decreases, our royalty rate decreases. See Item 8. Financial Statements and Supplementary Data - Supplementary Information on Oil and Gas Producing Activities for more information.

15

The following tables set forth estimated quantities of our proved crude oil and condensate, NGLs, natural gas and synthetic crude oil reserves based upon an SEC pricing for periods ended December 31, 2015, 2014 and 2013.

| North America |

| Africa |

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2015 | U.S. |

| Canada |

| Total |

| E.G. |

| Other |

| Total |

| Other Int'l |

| Cont Ops |

| Disc Ops |

| Total | ||||||||||

Proved Developed Reserves |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Crude oil and condensate (mmbbl) | 327 | |

| - | |

| 327 | |

| 25 | |

| 173 | |

| 198 | |

| 16 | |

| 541 | |

| - | |

| 541 | |

Natural gas liquids (mmbbl) | 92 | |

| - | |

| 92 | |

| 12 | |

| - | |

| 12 | |

| - | |

| 104 | |

| - | |

| 104 | |

Natural gas (bcf) | 640 | |

| - | |

| 640 | |

| 552 | |

| 94 | |

| 646 | |

| 11 | |

| 1,297 | |

| - | |

| 1,297 | |

Synthetic crude oil (mmbbl) | - | |

| 698 | |

| 698 | |

| - | |

| - | |

| - | |

| - | |

| 698 | |

| - | |

| 698 | |

Total proved developed reserves (mmboe) | 526 | |

| 698 | |

| 1,224 | |

| 129 | |

| 189 | |

| 318 | | | 18 | |

| 1,560 | |

| - | | | 1,560 | |

Proved Undeveloped Reserves |

|

|

|

|

|

|

|

|

|

|

|

| |

| |

|

|

| | ||||||||||

Crude oil and condensate ( mmbbl ) | 253 | |

| - | |

| 253 | |

| 27 | |

| 28 | |

| 55 | |

| 6 | |

| 314 | |

| - | |

| 314 | |

Natural gas liquids ( mmbbl ) | 80 | |

| - | |

| 80 | |

| 16 | |

| - | |

| 16 | |

| - | |

| 96 | |

| - | |

| 96 | |

Natural gas ( bcf ) | 511 | |

| - | |

| 511 | |

| 538 | |

| 112 | |

| 650 | |

| 4 | |

| 1,165 | |

| - | |

| 1,165 | |

Synthetic crude oil (mmbbl) | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| - | |

Total proved undeveloped reserves ( mmboe ) | 418 | |

| - | |

| 418 | |

| 132 | |

| 46 | |

| 178 | |

| 7 | |

| 603 | |

| - | |

| 603 | |

Total Proved Reserves |

|

|

|

|

|

|

|

|

|

|

|

| |

| |

|

|

| | ||||||||||

Crude oil and condensate ( mmbbl ) | 580 | |

| - | |

| 580 | |

| 52 | |

| 201 | |

| 253 | |

| 22 | |

| 855 | |

| - | |

| 855 | |

Natural gas liquids ( mmbbl ) | 172 | |

| - | |

| 172 | |

| 28 | |

| - | |

| 28 | |

| - | |

| 200 | |

| - | |

| 200 | |

Natural gas ( bcf ) | 1,151 | |

| - | |

| 1,151 | |

| 1,090 | |

| 206 | |

| 1,296 | |

| 15 | |

| 2,462 | |

| - | |

| 2,462 | |

Synthetic crude oil ( mmbbl ) | - | |

| 698 | |

| 698 | |

| - | |

| - | |

| - | |

| - | |

| 698 | |

| - | |

| 698 | |

Total proved reserves ( mmboe ) | 944 | |

| 698 | |

| 1,642 | |

| 261 | |

| 235 | |

| 496 | |

| 25 | |

| 2,163 | |

| - | |

| 2,163 | |

| North America |

| Africa |

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2014 | U.S. |

| Canada |

| Total |

| E.G. |

| Other |

| Total |

| Other Int'l |

| Cont Ops |

| Disc Ops |

| Total | ||||||||||

Proved Developed Reserves |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Crude oil and condensate (mmbbl) | 294 | |

| - | |

| 294 | |

| 30 | |

| 175 | |

| 205 | |

| 19 | |

| 518 | |

| - | |

| 518 | |

Natural gas liquids (mmbbl) | 68 | |

| - | |

| 68 | |

| 15 | |

| - | |

| 15 | |

| - | |

| 83 | |

| - | |

| 83 | |

Natural gas (bcf) | 575 | |

| - | |

| 575 | |

| 664 | |

| 94 | |

| 758 | |

| 17 | |

| 1,350 | |

| - | |

| 1,350 | |

Synthetic crude oil (mmbbl) | - | |

| 644 | |

| 644 | |

| - | |

| - | |

| - | |

| - | |

| 644 | |

| - | |

| 644 | |

Total proved developed reserves (mmboe) | 458 | |

| 644 | |

| 1,102 | |

| 155 | |

| 191 | |

| 346 | |

| 22 | |

| 1,470 | |

| - | |

| 1,470 | |

Proved Undeveloped Reserves |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Crude oil and condensate (mmbbl) | 340 | |

| - | |

| 340 | |

| 27 | |

| 33 | |

| 60 | |

| 10 | |

| 410 | |

| - | |

| 410 | |

Natural gas liquids (mmbbl) | 93 | |

| - | |

| 93 | |

| 15 | |

| - | |

| 15 | |

| 1 | |

| 109 | |

| - | |

| 109 | |

Natural gas (bcf) | 569 | |

| - | |

| 569 | |

| 541 | |

| 115 | |

| 656 | |

| 5 | |

| 1,230 | |

| - | |

| 1,230 | |

Synthetic crude oil (mmbbl) | - | |

| 4 | |

| 4 | |

| - | |

| - | |

| - | |

| - | |

| 4 | |

| - | |

| 4 | |

Total proved undeveloped reserves (mmboe) | 528 | |

| 4 | |

| 532 | |

| 133 | |

| 52 | |

| 185 | |

| 11 | |

| 728 | |

| - | |

| 728 | |

Total Proved Reserves |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

Crude oil and condensate (mmbbl) | 634 | |

| - | |

| 634 | |

| 57 | |

| 208 | |

| 265 | |

| 29 | |

| 928 | |

| - | |

| 928 | |

Natural gas liquids (mmbbl) | 161 | |

| - | |

| 161 | |

| 30 | |

| - | |

| 30 | |

| 1 | |

| 192 | |

| - | |

| 192 | |

Natural gas (bcf) | 1,144 | |

| - | |

| 1,144 | |

| 1,205 | |

| 209 | |

| 1,414 | |

| 22 | |

| 2,580 | |

| - | |

| 2,580 | |

Synthetic crude oil (mmbbl) | - | | | 648 | |

| 648 | | | - | |

| - | |

| - | | | - | |

| 648 | |

| - | | | 648 | |

Total proved reserves (mmboe) | 986 | |

| 648 | |

| 1,634 | |

| 288 | |

| 243 | |

| 531 | |

| 33 | |

| 2,198 | |

| - | |

| 2,198 | |

16

| North America |

| Africa |

|

|

|

|

|

|

|

| ||||||||||||||||||

December 31, 2013 | U.S. |

| Canada |

| Total |

| E.G. |

| Other |

| Total |

| Other Int'l |

| Cont Ops |

| Disc Ops |

| Total | ||||||||||

Proved Developed Reserves |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Crude oil and condensate (mmbbl) | 241 | |

| - | |

| 241 | |

| 37 | |

| 176 | |

| 213 | |

| 19 | |

| 473 | |

| 77 | |

| 550 | |

Natural gas liquids (mmbbl) | 51 | |

| - | |

| 51 | |

| 18 | |

| - | |

| 18 | |

| 1 | |

| 70 | |

| - | |

| 70 | |

Natural gas (bcf) | 540 | |

| - | |

| 540 | |

| 823 | |

| 95 | |

| 918 | |

| 21 | |

| 1,479 | |

| 20 | |

| 1,499 | |

Synthetic crude oil (mmbbl) | - | |

| 674 | |

| 674 | |

| - | |

| - | |

| - | |

| - | |

| 674 | |

| - | |

| 674 | |

Total proved developed reserves (mmboe) | 382 | |

| 674 | |

| 1,056 | |

| 193 | |

| 192 | |

| 385 | |

| 23 | |

| 1,464 | |

| 80 | |

| 1,544 | |

Proved Undeveloped Reserves |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||

Crude oil and condensate (mmbbl) | 256 | |

| - | |

| 256 | |

| 27 | |

| 39 | |

| 66 | |

| 6 | |

| 328 | |

| 14 | |

| 342 | |

Natural gas liquids (mmbbl) | 68 | |

| - | |

| 68 | |

| 16 | |

| - | |

| 16 | |

| - | |

| 84 | |

| - | |

| 84 | |

Natural gas (bcf) | 485 | |

| - | |

| 485 | |

| 497 | |

| 110 | |

| 607 | |

| 7 | |

| 1,099 | |

| 73 | |

| 1,172 | |

Synthetic crude oil (mmbbl) | - | |

| 6 | |

| 6 | |

| - | |

| - | |

| - | |

| - | |

| 6 | |

| - | |

| 6 | |

Total proved undeveloped reserves (mmboe) | 405 | |

| 6 | |

| 411 | |

| 125 | |

| 57 | |

| 182 | |

| 8 | |

| 601 | |

| 26 | |

| 627 | |

Total Proved Reserves |

|

|

|

|

| | |

|

|

|

|

|

|

| | | |||||||||||||

Crude oil and condensate (mmbbl) | 497 | |

| - | |

| 497 | |

| 64 | |

| 215 | |

| 279 | |

| 25 | |

| 801 | |

| 91 | |

| 892 | |

Natural gas liquids (mmbbl) | 119 | |

| - | |

| 119 | |

| 34 | |

| - | |

| 34 | |

| 1 | |

| 154 | |

| - | |

| 154 | |

Natural gas (bcf) | 1,025 | |

| - | |

| 1,025 | |

| 1,320 | |

| 205 | |

| 1,525 | |

| 28 | |

| 2,578 | |

| 93 | |

| 2,671 | |

Synthetic crude oil (mmbbl) | - | |

| 680 | |

| 680 | |

| - | |

| - | |

| - | |

| - | |

| 680 | |

| - | |

| 680 | |

Total proved reserves (mmboe) | 787 | |

| 680 | |

| 1,467 | |

| 318 | |

| 249 | |

| 567 | |

| 31 | |

| 2,065 | |

| 106 | |

| 2,171 | |

Preparation of Reserve Estimates

All estimates of reserves are made in compliance with SEC Rule 4-10 of Regulation S-X. Crude oil and condensate, NGLs, natural gas and synthetic crude oil reserve estimates are reviewed and approved by our Corporate Reserves Group, which includes our Director of Corporate Reserves and his staff of Reserve Coordinators. Crude oil and condensate, NGLs and natural gas reserve estimates are developed or reviewed by Qualified Reserves Estimators ("QREs"). QREs are engineers or geoscientists who hold at least a Bachelor of Science degree in the appropriate technical field, have a minimum of three years of industry experience with at least one year in reserve estimation and have completed Marathon Oil's QRE training course. All QREs must complete a QRE refresher course at least once every three years. Our Corporate Reserves group screens all fields with net proved reserves of 20 mmboe or greater, every year, to determine if a field review is required. Any change to proved reserve estimates in excess of 1 mmboe on a total field basis, within a single month, must be approved by a Reserve Coordinator.

Our Director of Corporate Reserves, who reports to our Vice President, Technology and Innovation, has a Bachelor of Science degree in petroleum engineering and is a registered Professional Engineer in the State of Texas. In his 28 years with Marathon Oil, he has held numerous engineering and management positions, including managing our OSM segment. He is a member of the Society of Petroleum Engineers ("SPE") and a former member of the Petroleum Engineering Advisory Council for the University of Texas at Austin.

Estimates of synthetic crude oil reserves are prepared by GLJ Petroleum Consultants ("GLJ") of Calgary, Alberta, Canada, third-party consultants. Their reports for all years are filed as exhibits to this Annual Report on Form 10-K. The individual responsible for the estimates of our synthetic crude oil reserves has 15 years of experience in petroleum engineering, has conducted surface mineable oil sands evaluations since 2009 and is a registered Practicing Professional Engineer in the Province of Alberta.

Audits of Estimates

We engage third-party consultants to provide, at a minimum, independent estimates for fields that comprise 80% of our total proved reserves over a rolling four-year period. We exceeded this percentage for the four-year period ended December 31, 2015 , with 82% of our total proved reserves independently audited. We have established a tolerance level of +/- 10% such that initial estimates by the third-party consultants for each field are accepted if they are within 10% of our internal estimates. Should the third-party consultants' initial analysis fail to reach our tolerance level, both parties re-examine the information provided, request additional data and refine their analysis, if appropriate. In the very limited instances where differences outside the 10% tolerance cannot be resolved by year end, a plan to resolve the difference is developed and executive management consent is obtained. The audit process did not result in any significant changes to our reserve estimates for 2015 , 2014 or 2013 .

17