UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

[ X ] | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

[__] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For Fiscal Year Ended May 30, 2015 | Commission File No. 001-15141 |

Herman Miller, Inc.

(Exact name of registrant as specified in its charter)

| Michigan |

| 38-0837640 |

|

| (State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

|

|

|

| 855 East Main Avenue |

|

|

|

| PO Box 302 |

|

|

|

| Zeeland, Michigan |

| 49464-0302 |

|

| (Address of principal executive offices) |

| (Zip Code) |

|

Registrant's telephone number, including area code: (616) 654 3000 |

|

Securities registered pursuant to Section 12(b) of the Act: None |

|

Securities registered pursuant to Section 12(g) of the Act: | Common Stock, $.20 Par Value (Title of Class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | |

| Yes [ X ] No [__] |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. | |

| Yes [__] No [ X ] |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | |

| Yes [ X ] No [__] |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | |

| Yes [ X ] No [__] |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ X ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of "accelerated filer," "large accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ X ] Accelerated filer [__] Non-accelerated filer [__] Smaller reporting company [__]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). | |

| Yes [__] No [ X ] |

The aggregate market value of the voting stock held by "nonaffiliates" of the registrant (for this purpose only, the affiliates of the registrant have been assumed to be the executive officers and directors of the registrant and their associates) as of November 29, 2014 , was $ 1,790,393,512 (based on $30.39 per share which was the closing sale price as reported by NASDAQ).

The number of shares outstanding of the registrant's common stock, as of July 23, 2015 : Common stock, $.20 par value - 59,838,458 shares outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the Registrant's Proxy Statement for the Annual Meeting of Stockholders to be held on October 12, 2015, are incorporated into Part III of this report.

This page intentionally left blank.

TABLE OF CONTENTS

| Page No. |

Part I |

|

Item 1 Business | 3 |

Item 1A Risk Factors | 6 |

Item 1B Unresolved Staff Comments | 9 |

Item 2 Properties | 10 |

Item 3 Legal Proceedings | 11 |

Additional Item: Executive Officers of the Registrant | 11 |

Item 4 Mine Safety Disclosures | 12 |

Part II |

|

Item 5 Market for the Registrant's Common Equity, Related Stockholder Matters, and |

|

Issuer Purchases of Equity Securities | 13 |

Item 6 Selected Financial Data | 15 |

Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations | 17 |

Item 7A Quantitative and Qualitative Disclosures about Market Risk | 41 |

Item 8 Financial Statements and Supplementary Data | 43 |

Item 9 Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | 82 |

Item 9A Controls and Procedures | 82 |

Item 9B Other Information | 82 |

Part III |

|

Item 10 Directors, Executive Officers, and Corporate Governance | 83 |

Item 11 Executive Compensation | 83 |

Item 12 Security Ownership of Certain Beneficial Owners and Management and Related |

|

Stockholder Matters | 83 |

Item 13 Certain Relationships and Related Transactions, and Director Independence | 83 |

Item 14 Principal Accountant Fees and Services | 83 |

Part IV |

|

Item 15 Exhibits and Financial Statement Schedule | 84 |

Signatures | 85 |

Report of Independent Registered Public Accounting Firm on Financial Statement Schedule | 86 |

Schedule II Valuation and Qualifying Accounts | 87 |

Exhibit Index | 88 |

PART I

Item 1 BUSINESS

General Development of Business

Herman Miller's mission statement is, Inspiring Designs to Help People Do Great Things . To this end, the company researches, designs, manufactures, and distributes interior furnishings for use in various environments including office, healthcare, educational, and residential settings, and provides related services that support organizations and individuals all over the world. Through research, the company seeks to define and clarify customer needs and problems existing in its markets and to design, through innovation where appropriate and feasible, products, systems, and services that serve as compelling solutions to such problems. The company's products are sold primarily through the following channels: Owned and independent contract furniture dealers, direct customer sales, owned and independent retailers, direct-mail catalog program, and the company's online stores.

In July 2014, Herman Miller acquired Design Within Reach, Inc. (DWR) and formed a new consumer-focused business unit comprised of DWR and the company's existing eCommerce and retail wholesale business. This acquisition represents an important step in the company's strategy to extend the reach of its brand into the consumer and design trade markets. It also represents a step toward enhancing the awareness and connection of the Herman Miller brand to the users and specifiers of products sold within the company's core contract furniture business (an ambition the company refers to as shifting from an "Industry" to "Industry+Consumer" focus). DWR brings with it a powerful multi-channel distribution structure that integrates brick and mortar retail studios (33 locations as of May 30, 2015), a successful direct-mail catalog program, an eCommerce platform, and a focused business-to-business selling model aimed at serving contract customers in work and hospitality environments.

Herman Miller, Inc. was incorporated in Michigan in 1905. One of the company's major plants and its corporate offices are located at 855 East Main Avenue, PO Box 302, Zeeland, Michigan, 49464-0302, and its telephone number is (616) 654-3000. Unless otherwise noted or indicated by the context, the term "company" includes Herman Miller, Inc., its predecessors, and majority-owned subsidiaries. Further information relating to principles of consolidation is provided in Note 1 to the Consolidated Financial Statements included in Item 8 of this report.

Financial Information about Segments

Information relating to segments is provided in Note 14 to t he Consolidated Financial Statements included in Item 8 of this report.

Narrative Description of Business

The company's principal business consists of the research, design, manufacture, selling, and distribution of office furniture systems, seating products, other freestanding furniture elements, textiles, and related services. Most of these systems and products are designed to be used together.

The company's ingenuity and design excellence creates award-winning products and services, which has made us a leader in design and development of furniture, furniture systems, and textiles. This leadership is exemplified by the innovative concepts introduced by the company in its modular systems (including Canvas Office Landscape™, Locale®, Metaform Portfolio™, Public Office Landscape™, Layout Studio®, Action Office®, Ethospace®, Arras®, and Resolve®). The company also offers a broad array of seating (including Embody®, Aeron®, Mirra2™, Setu®, Sayl®, Celle®, Equa®, and Ergon® office chairs), storage (including Meridian® and Tu™ products), wooden casegoods (including Geiger® products), freestanding furniture products (including Abak®, Intent®, Sense™ and Envelop®), healthcare products (including Palisade™, Compass®, Nala®, and other Nemschoff® products) the Thrive portfolio of ergonomic solutions, and the textiles of Maharam Fabric Corporation (Maharam).

The company's products are marketed worldwide by its own sales staff, independent dealers and retailers, its owned dealer network, and via its e-commerce website. Salespeople work with dealers, the architecture and design community, and directly with end-users. Independent dealerships concentrate on the sale of Herman Miller products and some complementary product lines of other manufacturers. It is estimated that approximately 74 percent of the company's sales in the fiscal year ended May 30, 2015 , were made to or through independent dealers. The remaining sales were made directly to end-users, including federal, state, and local governments, and several major corporations, by the company's own sales staff, its owned dealer network, DWR retail studios or independent retailers.

The company is a recognized leader within its industry for the use, development, and integration of customer-centered technologies that enhance the reliability, speed, and efficiency of our customers' operations. This includes proprietary sales tools, interior design and product specification software; order entry and manufacturing scheduling and production systems; and direct connectivity to the company's suppliers.

The company's furniture systems, seating, freestanding furniture, storage, casegood and textile products, and related services are used in (1) institutional environments including offices and related conference, lobby, and lounge areas, and general public areas including transportation

- 3 -

terminals; (2) health/science environments including hospitals, clinics, and other healthcare facilities; (3) industrial and educational settings; and (4) residential and other environments.

Raw Materials

The company's manufacturing materials are available from a significant number of sources within the United States, Canada, Europe, and Asia. To date, the company has not experienced any difficulties in obtaining its raw materials. The costs of certain direct materials used in the company's manufacturing and assembly operations are sensitive to shifts in commodity market prices. In particular, the costs of steel, plastic, aluminum components, and particleboard are sensitive to the market prices of commodities such as raw steel, aluminum, crude oil, lumber, and resins. Increases in the market prices for these commodities can have an adverse impact on the company's profitability. Further information regarding the impact of direct material costs on the company's financial results is provided in Management's Discussion and Analysis in Item 7 of this report.

Patents, Trademarks, Licenses, Etc.

The company has 138 active United States utility patents on various components used in its products and 54 active United States design patents. Many of the inventions covered by the United States patents also have been patented in a number of foreign countries. Various trademarks, including the name and stylized "Herman Miller" and the "Herman Miller Circled Symbolic M" trademark are registered in the United States and many foreign countries. The company does not believe that any material part of its business depends on the continued availability of any one or all of its patents or trademarks, or that its business would be materially adversely affected by the loss of any thereof, except for Herman Miller®, Herman Miller Circled Symbolic M®, Maharam®, Geiger®, Design Within Reach®, DWR®, Nemschoff®, Action Office®, Ethospace®, Aeron®, Mirra®, Embody®, Setu®, Sayl®, Eames®, PostureFit®, Meridian®, and Canvas Office Landscape®. It is estimated that the average remaining life of such patents and trademarks is approximately 5 years and 6 years, respectively.

Working Capital Practices

Information concerning the company's inventory levels relative to its sales volume can be found under the Executive Overview section in Item 7 of this report. Beyond this discussion, the company does not believe that it or the industry in general, has any special practices or special conditions affecting working capital items that are significant for understanding the company's business.

Customer Base

It is estimated that no single dealer accounted for more t han 5 percent of the company's net sales in the fiscal year ended May 30, 2015 . It is also estimated that the largest single end-user customer, the U.S. federal government, accounted for $97 million , $102 million , and $114 million of the company's net sales in fiscal 2015 , 2014 , and 2013 , respectively. This represents approximately 5 percent , 5 percent and 6 percent of the company's net sales in fiscal 2015 , 2014 , and 2013 , respectively. The 10 largest customers accounted for approximately 20 percent , 23 percent , and 23 percent of net sales in fiscal 2015 , 2014 , and 2013 , respectively.

Backlog of Unfilled Orders

As of May 30, 2015 , the company's backlog of unfilled orders was $322.2 million . At May 31, 2014 , the company's backlog totaled $306.4 million . It is expected that substantially all the orders forming the backlog at May 30, 2015 , will be filled during the next fiscal year. Many orders received by the company are reflected in the backlog for only a short period while other orders specify delayed shipments and are carried in the backlog for up to one year. Accordingly, the amount of the backlog at any particular time does not necessarily indicate the level of net sales for a particular succeeding period.

Government Contracts

Other than standard provisions contained in contracts with the United States Government, the company does not believe that any significant portion of its business is subject to material renegotiation of profits or termination of contracts or subcontracts at the election of various government entities. The company sells to the U.S. Government both through a General Services Administration ("GSA") Multiple Award Schedule Contract and through competitive bids. The GSA Multiple Award Schedule Contract pricing is principally based upon the company's commercial price list in effect when the contract is initiated, rather than being determined on a cost-plus-basis. The company is required to receive GSA approval to apply list price increases during the term of the Multiple Award Schedule Contract period.

Competition

All aspects of the company's business are highly competitive. From an office furniture perspective, the company competes largely on design, product and service quality, speed of delivery, and product pricing. Although the company is one of the largest office furniture manufacturers in the world, it competes with manufacturers that have significant resources and sales as well as many smaller companies. In the United States, the company's most significant competitors are Haworth, HNI Corporation, Kimball International, Knoll, and Steelcase.

The company also competes in the home furnishings industry, primarily against regional and national independent home furnishings retailers who market high-craft furniture to the interior design community. Similar to our office furniture product offerings, the company competes primarily on design, product and service quality, speed of delivery, and product pricing in the consumer space.

- 4 -

Research, Design, and Development

The company draws great competitive strength from its research, design, and development programs. Accordingly, the company believes that its research and design activities are of significant importance. Through research, the company seeks to define and clarify customers and the problems which they are trying to solve. The company designs innovative products and services that address customer needs and solve their problems. The company uses both internal and independent research resources and independent design resources. Exclusive of royalty payments, the company spent approximately $56.7 million , $53.9 million , and $48.3 million on research and development activities in fiscal 2015 , 2014 , and 2013 , respectively. Generally, royalties are paid to designers of the company's products as the products are sold and are not included in research and development costs since they are variable based on product sales.

Environmental Matters

For over 50 years, respecting the environment has been more than good business practice for us-it is the right thing to do. Our 10-year sustainability strategy - Earthright - begins with three principles: positive transparency, products as living things, and becoming greener together. Our goals are focused around the smart use of resources, eco-inspired design, and becoming community driven. Based on current facts known to management, the company does not believe that existing environmental laws and regulations have had or will have any material effect upon the capital expenditures, earnings, or competitive position of the company. However, there can be no assurance that environmental legislation and technology in this area will not result in or require material capital expenditures or additional costs to our manufacturing process.

Human Resources

The company considers its employees to be another of its major competitive strengths. The company stresses individual employee participation and incentives, believing that this emphasis has helped attract and retain a competent and motivated workforce. The company's human resources group provides employee recruitment, education and development, as well as compensation planning and counseling. Additionally, there have been no work stoppages or labor disputes in the company's history. Approximately 14.1 percent of the company's employees are covered by collective bargaining agreements, most of whom are employees of its Nemschoff, Herman Miller Ningbo, and Herman Miller Dongguan subsidiaries.

As of May 30, 2015 , the company had 7,510 employees, representing a 4.7 percent increase as compared with May 31, 2014 . The increase in employees was driven principally by our acquisition of DWR during fiscal 2015. Refer to Note 2 of the Consolidated Financial Statements for further information regarding this acquisition. In addition to its employee work force, the company uses temporary labor to meet uneven demand in its manufacturing operations.

Information about International Operations

The company's sales in international markets are made primarily to office/institutional customers. Foreign sales consist mostly of office furniture products such as Abak®, Aeron®, Mirra®, Celle®, Sayl®, Layout Studio®, Arras™, and other seating and storage products (including POSH products). The company conducts business in the following major international markets: Europe, Canada, the Middle East, Latin America, South America, and the Asia/Pacific region.

The company's products currently sold in international markets are manufactured by wholly owned subsidiaries in the United States, the United Kingdom, and China. Sales are made through wholly owned subsidiaries or branches in Canada, France, Germany, Italy, Japan, Mexico, Australia, Singapore, China (including Hong Kong), India, and the Netherlands. The company's products are offered in the Middle East, Europe, South America, Africa, and Asia through dealers.

Additional information with respect to operations by geographic area appears i n Note 14 of the Consolidated Financial Statements included in Item 8 of this report. Fluctuating exchange rates and factors beyond the control of the company, such as tariff and foreign economic policies, may affect future results of international operations. Refer to Item 7A, Quantitative and Qualitative Disclosures about Market Risk , for further discussion regarding the company's foreign exchange risk.

Available Information

The company's annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports are made available free of charge through the "Investors" section of the company's internet website at www.hermanmiller.com , as soon as practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission (SEC). The company's filings with the SEC are also available for the public to read and copy in person at the SEC's Public Reference Room at 100 F Street NE, Washington, DC 20549, by phone at 1-800-SEC-0330, or via their internet website at www.sec.gov .

- 5 -

Item 1A RISK FACTORS

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones we face; others, either unforeseen or currently deemed less significant, may also have a negative impact on our company. If any of the following actually occurs, our business, operating results, cash flows, and financial condition could be materially adversely affected.

Sustained downturn in the economy could adversely impact our access to capital.

The recent disruptions in the global economic and financial markets adversely impacted the broader financial and credit markets, at times reducing the availability of debt and equity capital for the market as a whole. Conditions such as these could re-emerge in the future. Accordingly, our ability to access the capital markets could be restricted at a time when we would like, or need, to access those markets, which could have an impact on our flexibility to react to changing economic and business conditions. The resulting lack of available credit, increased volatility in the financial markets and reduced business activity could materially and adversely affect our business, financial condition, results of operations, our ability to take advantage of market opportunities and our ability to obtain and manage our liquidity. In addition, the cost of debt financing and the proceeds of equity financing may be materially and adversely impacted by these market conditions. The extent of any impact would depend on several factors, including our operating cash flows, the duration of tight credit conditions and volatile equity markets, our credit capacity, the cost of financing, and other general economic and business conditions. Our credit agreements contain performance covenants, such as a limit on the ratio of debt to earnings before interest, taxes, depreciation and amortization, and limits on subsidiary debt and incurrence of liens. Although we believe none of these covenants are presently restrictive to our operations, our ability to meet the financial covenants can be affected by events beyond our control.

We may not be successful in implementing and managing our growth strategy.

We have established a growth strategy for the business based on a changing and evolving world. Through this strategy we are positioning the company to take advantage of existing markets, explore growth opportunities in new markets with supportive demographics, increase demand by addressing unmet needs, and expanding into areas that yield higher prospects for margins and profitability.

We ultimately aspire to create a lifestyle brand, and we intend to grow in certain targeted ways. First, we will invest in areas that increase our addressable markets across focused customer segments (such as healthcare, education, small and medium business, textiles, and consumer). Second, we will expand into emerging geographic markets that offer growth potential based upon their supportive demographics. Third, we will continue to invest in innovative products, which has been a hallmark of our success for many years. And finally, we will grow through targeted acquisitions.

While we have confidence that our strategic plan reflects opportunities that are appropriate and achievable and that we have anticipated and will manage the associated risks, there is the possibility that the strategy may not deliver the projected results due to inadequate execution, incorrect assumptions, sub-optimal resource allocation, or changing customer requirements.

There is no assurance that our current product and service offering will allow us to meet these goals. Accordingly, we believe we will be required to continually invest in the research, design, and development of new products and services. There is no assurance that such investments will have commercially successful results.

Certain growth opportunities may require us to invest in acquisitions, alliances, and the startup of new business ventures. These investments may not perform according to plan and may involve the assumption of business, operational, or other risks that are new to our business.

Future efforts to expand our business within developing economies, particularly within China and India, may expose us to the effects of political and economic instability. Such instability may impact our ability to compete for business. It may also put the availability and/or value of our capital investments within these regions at risk. These expansion efforts expose us to operating environments with complex, changing, and in some cases, inconsistently applied legal and regulatory requirements. Developing knowledge and understanding of these requirements poses a significant challenge and failure to remain compliant with them could limit our ability to continue doing business in these locations.

Pursuing our strategic plan in new and adjacent markets, as well as within developing economies, will require us to find effective new channels of distribution. There is no assurance that we can develop or otherwise identify these channels of distribution.

The markets in which we operate are highly competitive and we may not be successful in winning new business.

We are one of several companies competing for new business within the furniture industry. Many of our competitors offer similar categories of products, including office seating, systems and freestanding office furniture, casegoods, storage, and residential and healthcare furniture solutions. We believe that our innovative product design, functionality, quality, depth of knowledge, and strong network of distribution partners differentiates us in the marketplace. However, increased market pricing pressure could make it difficult for us to win new business with certain customers and within certain market segments at acceptable profit margins.

- 6 -

The retail furnishings market is highly competitive. We compete with national and regional furniture retailers and department stores. In addition, we compete with mail order catalogs and online retailers focused on home furnishings. We compete with these and other retailers for customers, suitable retail locations, vendors, qualified employees, and management personnel. Some of our competitors have significantly greater financial, marketing and other resources than we possess. This may result in our competitors being quicker at the following: adapting to changes, devoting greater resources to the marketing and sale of their products, generating greater national brand recognition, or adopting more aggressive pricing policies. In addition, increased catalog mailings by our competitors may adversely affect response rates to our own catalog mailings. As a result, increased competition may adversely affect our future financial performance.

Adverse economic and industry conditions could have a negative impact on our business, results of operations, and financial condition.

Customer demand within the contract office furniture industry is affected by various macro-economic factors; general corporate profitability, white-collar employment levels, new office construction rates, and existing office vacancy rates are among the most influential factors. History has shown that declines in these measures can have an adverse effect on overall office furniture demand. Additionally, factors and changes specific to our industry, such as developments in technology, governmental standards and regulations, and health and safety issues can influence demand. There are current and future economic and industry conditions, which could adversely affect our business, operating results, or financial condition.

Other macroeconomic developments, such as the recent recessions in Europe, the debt crisis in certain countries in the European Union, and the economic slow down in Asia could negatively affect the company's ability to conduct business in those geographies. The continuing debt crisis in certain European countries could cause the value of the Euro to deteriorate, reducing the purchasing power of the company's European customers and potentially undermining the financial health of the company's suppliers and customers in other parts of the world. Financial difficulties experienced by the company's suppliers and customers, including distributors, could result in product delays and inventory issues; risks to accounts receivable could result in delays in collection and greater bad debt expense.

Our business presence outside the United States exposes us to certain risks that could negatively affect our results of operations and financial condition.

We have significant manufacturing and sales operations in the United Kingdom, which represents our largest marketplace outside the United States. We also have manufacturing operations in China. Additionally, our products are sold internationally through wholly-owned subsidiaries or branches in various countries including Canada, Mexico, Brazil, France, Germany, Italy, Netherlands, Japan, Australia, Singapore, China, Hong Kong, and India. In certain other regions of the world, our products are offered primarily through independent dealerships.

Doing business internationally exposes us to certain risks, many of which are beyond our control and could potentially impact our ability to design, develop, manufacture, or sell products in certain countries. These factors could include, but would not necessarily be limited to:

• | Political, social, and economic conditions |

• | Legal and regulatory requirements |

• | Labor and employment practices |

• | Cultural practices and norms |

• | Natural disasters |

• | Security and health concerns |

• | Protection of intellectual property |

• | Changes in foreign currency exchange rates |

In some countries, the currencies in which we import and export products can differ. Fluctuations in the rate of exchange between these currencies could negatively impact our business. Additionally, tariff and import regulations, international tax policies and rates, and changes in U.S. and international monetary policies may have an adverse impact on results of operations and financial condition.

Risks and Costs Associated with Protecting the Integrity and Security of Our Systems and Confidential Information

We collect certain customer-specific data, including credit card information, in connection with orders placed through our e-commerce websites, direct-mail catalog marketing program, and DWR retail studios. In order for these sales channels to function and develop successfully, we and other parties involved in processing customer transactions must be able to transmit confidential information, including credit card information and other personal information on our customers, securely over public and private networks. Third parties may have or develop the technology or knowledge to breach, disable, disrupt or interfere with our systems or processes or those of our vendors. Although we take the security of our systems and the privacy of our customers' confidential information seriously and we believe we take reasonable steps to protect the security and confidentiality of the information we collect, we cannot guarantee that our security measures will effectively prevent others from obtaining unauthorized access to our information and our customers' information. The techniques used to obtain unauthorized access to systems change frequently and are not often recognized until after they have been launched.

Any person who circumvents our security measures could destroy or steal valuable information or disrupt our operations. Any security breach could cause consumers to lose confidence in the security of our information systems, including our e-commerce websites or stores and choose not to purchase from us. Any security breach could also expose us to risks of data loss, litigation, regulatory investigations, and other significant

- 7 -

liabilities. Such a breach could also seriously disrupt, slow or hinder our operations and harm our reputation and customer relationships, any of which could harm our business.

A security breach includes a third party wrongfully gaining unauthorized access to our systems for the purpose of misappropriating assets or sensitive information, loading corrupting data, or causing operational disruption. These actions may lead to a significant disruption of the Company's IT systems and/or cause the loss of business and business information resulting in an adverse business impact, including: (1) future financial results due to theft, destruction, loss misappropriation, or release of confidential data or intellectual property; (2) operational or business delays resulting from the disruption of IT systems, and subsequent clean-up and mitigation activities; and (3) negative publicity resulting in reputation or brand damage with customers, partners or industry peers.

In addition, states and the federal government are increasingly enacting laws and regulations to protect consumers against identity theft. Also, as our business expands globally, we are subject to data privacy and other similar laws in various foreign jurisdictions. If we are the target of a cybersecurity attack resulting in unauthorized disclosure of our customer data, we may be required to undertake costly notification procedures. Compliance with these laws will likely increase the costs of doing business. If we fail to implement appropriate safeguards or to detect and provide prompt notice of unauthorized access as required by some of these laws, we could be subject to potential claims for damages and other remedies, which could harm our business.

Disruptions in the supply of raw and component materials could adversely affect our manufacturing and assembly operations.

We rely on outside suppliers to provide on-time shipments of the various raw materials and component parts used in our manufacturing and assembly processes. The timeliness of these deliveries is critical to our ability to meet customer demand. Any disruptions in this flow of delivery could have a negative impact on our business, results of operations, and financial condition.

Increases in the market prices of manufacturing materials may negatively affect our profitability.

The costs of certain manufacturing materials used in our operations are sensitive to shifts in commodity market prices. In particular, the costs of steel, plastic, aluminum components, and particleboard are sensitive to the market prices of commodities such as raw steel, aluminum, crude oil, lumber, and resins. Increases in the market prices of these commodities may have an adverse impact on our profitability if we are unable to offset them with strategic sourcing, continuous improvement initiatives or increased prices to our customers.

Disruptions within our dealer network could adversely affect our business.

Our ability to manage existing relationships within our network of independent dealers is crucial to our ongoing success. Although the loss of any single dealer would not have a material adverse effect on the overall business, our business within a given market could be negatively affected by disruptions in our dealer network caused by the termination of commercial working relationships, ownership transitions, or dealer financial difficulties.

If dealers go out of business or restructure, we may suffer losses because they may not be able to pay for products already delivered to them. Also, dealers may experience financial difficulties, creating the need for outside financial support, which may not be easily obtained. In the past, we have, on occasion, agreed to provide direct financial assistance through term loans, lines of credit, and/or loan guarantees to certain dealers.

We are unable to control many of the factors affecting consumer spending, and declines in consumer spending on furnishings could reduce demand for our products.

The operations of our Consumer segment are sensitive to a number of factors that influence consumer spending, including general economic conditions, consumer disposable income, unemployment, inclement weather, availability of consumer credit, consumer debt levels, conditions in the housing market, interest rates, sales tax rates and rate increases, inflation, and consumer confidence in future economic conditions. Adverse changes in these factors may reduce consumer demand for our products, resulting in reduced sales and profitability.

A number of factors that affect our ability to successfully implement our retail studio strategy, including opening new locations and closing existing studios, are beyond our control. These factors may harm our ability to increase the sales and profitability of our retail operations.

Approximately 60% of the sales within our Consumer segment are generated by our DWR retail studios. Our ability to open additional studios or close existing studios successfully will depend upon a number of factors beyond our control, including:

• | General economic conditions |

• | Identification and availability of suitable studio locations |

• | Success in negotiating new leases and amending or terminating existing leases on acceptable terms |

• | The success of other retailers in and around our retail locations |

• | Ability to secure required governmental permits and approvals |

• | Hiring and training skilled studio operating personnel |

• | Landlord financial stability |

- 8 -

Increasing competition for highly skilled and talented workers could adversely affect our business.

The successful implementation of our business strategy depends, in part, on our ability to attract and retain a skilled workforce. The increasing competition for highly skilled and talented employees could result in higher compensation costs, difficulties in maintaining a capable workforce, and leadership succession planning challenges.

Costs related to product defects could adversely affect our profitability.

We incur various expenses related to product defects, including product warranty costs, product recall and retrofit costs, and product liability costs. These expenses relative to product sales vary and could increase. We maintain reserves for product defect-related costs based on estimates and our knowledge of circumstances that indicate the need for such reserves. We cannot, however, be certain that these reserves will be adequate to cover actual product defect-related claims in the future. Any significant increase in the rate of our product defect expenses could have a material adverse effect on operations.

We are subject to risks associated with self-insurance related to health benefits.

We are self-insured for our health benefits and maintain per employee stop loss coverage; however, we retain the insurable risk at an aggregate level. Therefore unforeseen or catastrophic losses in excess of our insured limits could have a material adverse effect on the company's financial condition and operating results. See Note 1 of the Consolidated Financial Statements for information regarding the company's retention level.

Government and other regulations could adversely affect our business.

Government and other regulations apply to the manufacture and sale of many of our products. Failure to comply with these regulations or failure to obtain approval of products from certifying agencies could adversely affect the sales of these products and have a material negative impact on operating results.

Item 1B UNRESOLVED STAFF COMMENTS

None

- 9 -

Item 2 PROPERTIES

The company owns or leases facilities located throughout the United States and several foreign countries. The location, square footage, and use of the most significant facilities at May 30, 2015 were as follows:

Owned Locations | Square Footage | |

| Use |

Holland, Michigan | 917,400 | |

| Manufacturing, Distribution, Warehouse, Design, Office |

Zeeland, Michigan | 750,800 | |

| Manufacturing, Warehouse, Office |

Spring Lake, Michigan | 582,700 | |

| Manufacturing, Warehouse, Office |

Dongguan, China | 224,019 | |

| Manufacturing, Distribution, Warehouse, Office |

Sheboygan, Wisconsin | 207,700 | |

| Manufacturing, Warehouse, Office |

Melksham, United Kingdom (1) | 170,000 | |

| Manufacturing, Warehouse, Office |

Hildebran, North Carolina | 93,000 | |

| Manufacturing, Office |

Bath, United Kingdom | 85,000 | |

| Manufacturing, Office |

(1) The company is currently completing the construction of a consolidated manufacturing and distribution facility in Melksham, United Kingdom. Once completed in late summer 2015, this will replace two existing United Kingdom facilities in Bath and Chippenham. | ||||

|

|

|

| |

Leased Locations | Square Footage | |

| Use |

Hebron, Kentucky | 316,800 | |

| Warehouse |

Atlanta, Georgia | 176,700 | |

| Manufacturing, Warehouse, Office |

Hong Kong, China | 104,402 | |

| Warehouse, Office |

Chippenham, United Kingdom | 100,800 | |

| Manufacturing, Warehouse, Office |

Ningbo, China | 94,700 | |

| Manufacturing, Warehouse, Office |

Yaphank, New York | 92,000 | |

| Warehouse, Office |

Bangalore, India | 61,300 | |

| Manufacturing, Warehouse, Office |

Brooklyn, New York | 39,440 | |

| Warehouse, Retail |

Secaucus, New Jersey | 36,400 | |

| Warehouse, Retail |

The company also maintains showrooms, sales offices and retail studios near many major metropolitan areas throughout North America, Europe, Asia/Pacific, and Latin America. The company considers its existing facilities to be in good condition and adequate for its design, production, distribution, and selling requirements.

- 10 -

Item 3 LEGAL PROCEEDINGS

The company is involved in legal proceedings and litigation arising in the ordinary course of business. In the opinion of management, the outcome of such proceedings and litigation currently pending will not materially affect the company's consolidated operations, cash flows and financial condition.

ADDITIONAL ITEM: EXECUTIVE OFFICERS OF THE REGISTRANT

Certain information relating to Executive Officers of the company is as follows.

Name | Age | Year Elected an Executive Officer | Position with the Company |

Brian C. Walker | 53 | 1996 | President and Chief Executive Officer |

Andrew J. Lock | 61 | 2003 | Executive Vice President, President, International |

Donald D. Goeman | 58 | 2005 | Executive Vice President, Research, Design & Development |

Gregory J. Bylsma | 50 | 2009 | Executive Vice President, Chief Operating Officer Herman Miller North America (Work and Learning) |

Steven C. Gane | 60 | 2009 | Senior Vice President, President, Geiger & Specialty/Consumer |

Jeffrey M. Stutz | 44 | 2009 | Executive Vice President, Chief Financial Officer |

B. Ben Watson | 50 | 2010 | Executive Creative Director |

Michael F. Ramirez | 50 | 2011 | Senior Vice President, People, Places and Administration |

Louise McDonald | 60 | 2013 | Executive Vice President, President, Healthcare |

H. Timothy Lopez | 44 | 2014 | Senior Vice President, Legal Services and Secretary |

Jeffrey L. Kurburski | 49 | 2014 | Vice President, Information Technology |

John Edelman | 48 | 2015 | Executive Vice President and Chief Executive Officer, Design Within Reach, Inc. |

John McPhee | 52 | 2015 | Executive Vice President and President, Design Within Reach, Inc. |

Kevin Veltman | 40 | 2015 | Vice President, Investor Relations and Treasurer |

Malisa Bryant | 48 | 2015 | Senior Vice President of Sales and Distribution, Herman Miller North America (Work and Learning) |

Except as discussed below, each of the named officers has served the company in an executive capacity for more than five years.

Ms. Bryant joined the Company in 2013 as Vice President and General Manager of Focused Market Segments and most recently served as Vice President of North America Sales. Prior to joining the Company, she held several leadership roles within the industry, including the Vice President of Customer Support, Vice President and General Manager of Strategic Accounts, and Vice President of Sales for Allsteel, in each case at HNI.

Mr. Edelman joined Herman Miller, Inc. in 2015 subsequent to the company's acquisition of DWR. Prior to joining DWR as President and Chief Executive Office in 2010 he served as President and CEO of Edelman Leather and Sam & Libby, Inc., where he was responsible for its U.S. business.

Mr. McPhee joined Herman Miller, Inc. in 2015 subsequent to the company's acquisition of DWR. Prior to that he served in various roles at DWR including Chief Operating Officer and President. Mr. McPhee previously held senior management positions with Edelman Leather, Candie's, Inc. and Sam & Libby, Inc.

Mr. Veltman joined Herman Miller in 2014 and serves as Vice President - Investor Relations and Treasurer. Previously he worked for BISSELL, Inc, most recently as Vice President – Finance, for 8 years and Ernst & Young, LLP for 10 years.

Mr. Kurburski joined Herman Miller in 1990. He served as Director of IT, Herman Miller Casegoods from 1998 to 2003, Director of IT Infrastructure from 2003 to 2007, and has served in his current capacity of Vice President of Information Technology since 2007.

Mr. Lopez joined Herman Miller in 2012 and serves as Senior Vice President of Legal Services, General Counsel and Secretary. Prior to this he was an Associate General Counsel with A. O. Smith Corporation from 2008 to 2012 and Senior Staff Attorney to Kohler Co. from 2002 to 2008.

- 11 -

Ms. McDonald joined Herman Miller in 2013 as President of Healthcare, and prior to this she worked for Welch Allyn for 31 years serving mostly as an Executive Vice President.

Mr. Ramirez joined Herman Miller in 1998 and served as Director of Purchasing from 1998 to 2005, Vice President of Inclusiveness and Diversity from 2005 to 2009, and Vice President of Sales Operations from 2009 to 2011.

There are no family relationships between or among the above-named executive officers. There are no arrangements or understandings between any of the above-named officers pursuant to which any of them was named an officer.

Item 4 MINE SAFETY DISCLOSURES - Not applicable

- 12 -

PART II

Item 5 MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES

Share Price, Earnings, and Dividends Summary

Herman Miller, Inc., common stock is traded on the NASDAQ-Global Select Market System (Symbol: MLHR). As of July 23, 2015, there were approximately 20,000 record holders, including individual participants in security position listings, of the company's common stock.

Per Share and Unaudited

| Market Price High (at close) | |

| Market Price Low (at close) | |

| Market Price Close | |

| Earnings (loss) Per Share- Diluted (1) | |

| Dividends Declared Per Share | | |||||

Year ended May 30, 2015: |

|

|

|

|

|

|

|

|

| ||||||||||

First quarter | $ | 32.26 | |

| $ | 28.69 | |

| $ | 29.72 | |

| $ | 0.42 | |

| $ | 0.140 | |

Second quarter | 32.12 | |

| 28.44 | |

| 30.39 | |

| 0.46 | |

| 0.140 | | |||||

Third quarter | 31.89 | |

| 27.69 | |

| 30.97 | |

| 0.35 | |

| 0.140 | | |||||

Fourth quarter | 31.20 | |

| 27.12 | |

| 27.70 | |

| 0.39 | |

| 0.140 | | |||||

Year | $ | 32.26 | |

| $ | 27.12 | |

| $ | 27.70 | |

| $ | 1.62 | |

| $ | 0.560 | |

Year ended May 31, 2014: |

|

|

|

|

|

|

|

|

| ||||||||||

First quarter | $ | 29.13 | |

| $ | 25.47 | |

| $ | 25.47 | |

| $ | 0.38 | |

| $ | 0.125 | |

Second quarter | 31.91 | |

| 25.56 | |

| 31.91 | |

| (1.37 | ) |

| 0.125 | | |||||

Third quarter | 30.95 | |

| 26.47 | |

| 28.18 | |

| 0.33 | |

| 0.140 | | |||||

Fourth quarter | 32.43 | |

| 27.83 | |

| 31.27 | |

| 0.28 | |

| 0.140 | | |||||

Year | $ | 32.43 | |

| $ | 25.47 | |

| $ | 31.27 | |

| $ | (0.37 | ) |

| $ | 0.530 | |

(1) The sum of the quarters may not equal the annual balance due to rounding associated with the calculation of earnings per share on an individual quarter basis

Dividends were declared and paid quarterly during fiscal 2015 and 2014 as approved by the Board of Directors. While it is anticipated that the company will continue to pay quarterly cash dividends, the amount and timing of such dividends is subject to the discretion of the Board depending on the company's future results of operations, financial condition, capital requirements, and other relevant factors.

Issuer Purchases of Equity Securities

The following is a summary of share repurchase activity during the fourth quarter ended May 30, 2015 .

Period | (a) Total Number of Shares (or Units) Purchased | |

| (b) Average Price Paid per Share or Unit | |

| (c) Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | |

| (d) Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet be Purchased Under the Plans or Programs (1) | | |

3/1/15-3/28/15 | 850 | |

| 28.06 | |

| 850 | |

| $ | 146,949,608 | |

3/29/15-4/25/15 | 1,478 | |

| 28.50 | |

| 1,478 | |

| $ | 146,907,485 | |

4/26/15-5/30/15 | 12,467 | |

| 28.11 | |

| 12,467 | |

| $ | 146,557,022 | |

Total | 14,795 | |

| | |

| 14,795 | |

|

| ||

(1) Amounts are as of the end of the period indicated

- 13 -

The company has a share repurchase plan authorized by the Board of Directors on September 28, 2007, which provided share repurchase authorization of $300,000,000 with no specified expiration date.

No repurchase plans expired or were terminated during the fourth quarter of fiscal 2015 .

During the period covered by this report, the company did not sell any of its equity shares that were not registered under the Securities Act of 1933.

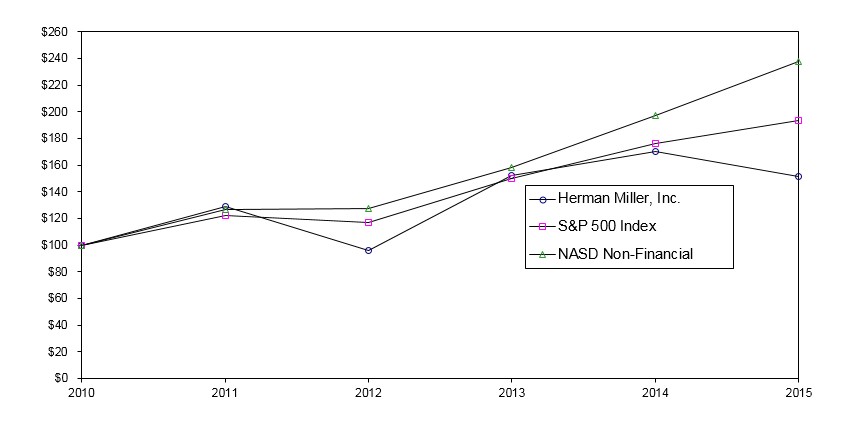

Stockholder Return Performance Graph

Set forth below is a line graph comparing the yearly percentage change in the cumulative total stockholder return on the company's common stock with that of the cumulative total return of the Standard & Poor's 500 Stock Index and the NASD Non-Financial Index for the five-year period ended May 30, 2015 . The graph assumes an investment of $100 on May 29, 2010 in the company's common stock, the Standard & Poor's 500 Stock Index and the NASD Non-Financial Index, with dividends reinvested.

| 2010 |

| 2011 |

| 2012 |

| 2013 |

| 2014 |

| 2015 | ||||||||||||

Herman Miller, Inc. | $ | 100 | |

| $ | 129 | |

| $ | 96 | |

| $ | 152 | |

| $ | 170 | |

| $ | 151 | |

S&P 500 Index | $ | 100 | |

| $ | 122 | |

| $ | 117 | |

| $ | 150 | |

| $ | 177 | |

| $ | 193 | |

NASD Non-Financial | $ | 100 | |

| $ | 127 | |

| $ | 128 | |

| $ | 158 | |

| $ | 197 | |

| $ | 238 | |

Information required by this item is also contained in Item 12 of this report.

- 14 -

Item 6 SELECTED FINANCIAL DATA

Review of Operations |

|

|

|

|

|

|

|

|

| ||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||

(In millions, except key ratios and per share data) | 2015 |

| 2014 | 2013 |

| 2012 |

| 2011 |

| ||||||||||

Operating Results |

|

|

|

|

|

|

|

|

| ||||||||||

Net sales | $ | 2,142.2 | |

| $ | 1,882.0 | | $ | 1,774.9 | |

| $ | 1,724.1 | |

| $ | 1,649.2 | |

|

Gross margin | 791.4 | |

| 631.0 | | 605.2 | |

| 590.6 | |

| 538.1 | |

| |||||

Selling, general, and administrative (8) | 556.6 | |

| 590.8 | | 430.4 | |

| 400.3 | |

| 369.0 | |

| |||||

Design and research | 71.4 | |

| 65.9 | | 59.9 | |

| 52.7 | |

| 45.8 | |

| |||||

Operating earnings (loss) | 163.4 | |

| (25.7 | ) | 114.9 | |

| 137.6 | |

| 123.3 | |

| |||||

Earnings (loss) before income taxes | 145.2 | |

| (43.4 | ) | 97.2 | |

| 119.5 | |

| 102.5 | |

| |||||

Net earnings (loss) | 98.1 | |

| (22.1 | ) | 68.2 | |

| 75.2 | |

| 70.8 | |

| |||||

Cash flow from operating activities | 167.7 | |

| 90.1 | | 136.5 | |

| 90.1 | |

| 89.0 | |

| |||||

Cash flow used in investing activities | (213.6 | ) |

| (48.2 | ) | (209.7 | ) |

| (58.4 | ) |

| (31.4 | ) |

| |||||

Cash flow used in financing activities | 6.8 | |

| (22.4 | ) | (16.0 | ) |

| (1.6 | ) |

| (50.2 | ) |

| |||||

Depreciation and amortization | 49.8 | |

| 42.4 | | 37.5 | |

| 37.2 | |

| 39.1 | |

| |||||

Capital expenditures | 63.6 | |

| 40.8 | | 50.2 | |

| 28.5 | |

| 30.5 | |

| |||||

Common stock repurchased plus cash dividends paid | 37.1 | |

| 43.0 | | 22.7 | |

| 7.9 | |

| 6.0 | |

| |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Key Ratios |

|

|

|

|

|

|

|

|

| ||||||||||

Sales growth | 13.8 | % |

| 6.0 | % | 2.9 | % |

| 4.5 | % |

| 25.1 | % |

| |||||

Gross margin (1) | 36.9 | |

| 33.5 | | 34.1 | |

| 34.3 | |

| 32.6 | |

| |||||

Selling, general, and administrative (1) (8) | 26.0 | |

| 31.4 | | 24.3 | |

| 23.2 | |

| 22.4 | |

| |||||

Design and research (1) | 3.3 | |

| 3.5 | | 3.4 | |

| 3.1 | |

| 2.8 | |

| |||||

Operating earnings (1) | 7.6 | |

| (1.4 | ) | 6.5 | |

| 8.0 | |

| 7.5 | |

| |||||

Net earnings growth (decline) | 543.9 | |

| (132.4 | ) | (9.3 | ) |

| 6.2 | |

| 150.2 | |

| |||||

After-tax return on net sales (4) | 4.6 | |

| (1.2 | ) | 3.8 | |

| 4.4 | |

| 4.3 | |

| |||||

After-tax return on average assets (5) | 9.0 | |

| (2.3 | ) | 7.6 | |

| 9.1 | |

| 9.0 | |

| |||||

After-tax return on average equity (6) | 24.5 | % |

| (6.4 | )% | 24.0 | % |

| 33.2 | % |

| 49.7 | % |

| |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Share and Per Share Data |

|

|

|

|

|

|

|

|

| ||||||||||

Earnings (loss) per share-diluted | $ | 1.62 | |

| $ | (0.37 | ) | $ | 1.16 | |

| $ | 1.29 | |

| $ | 1.06 | |

|

Cash dividends declared per share | 0.56 | |

| 0.53 | | 0.43 | |

| 0.09 | |

| 0.09 | |

| |||||

Book value per share at year end | 7.18 | |

| 6.27 | | 5.44 | |

| 4.25 | |

| 3.53 | |

| |||||

Market price per share at year end | 27.70 | |

| 31.27 | | 28.11 | |

| 17.87 | |

| 24.56 | |

| |||||

Weighted average shares outstanding-diluted | 60.1 | |

| 59.0 | | 58.8 | |

| 58.5 | |

| 57.7 | |

| |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Financial Condition |

|

|

|

|

|

|

|

|

| ||||||||||

Total assets | $ | 1,188.2 | |

| $ | 990.9 | | $ | 946.5 | |

| $ | 839.1 | |

| $ | 808.0 | |

|

Working capital (3) | 112.6 | |

| 145.7 | | 109.3 | |

| 201.6 | |

| 205.9 | |

| |||||

Current ratio (2) | 1.3 | |

| 1.3 | | 1.4 | |

| 1.8 | |

| 1.8 | |

| |||||

Interest-bearing debt and related swap agreements | 290.0 | |

| 250.0 | | 250.0 | |

| 250.0 | |

| 250.0 | |

| |||||

Stockholders' equity | 428.1 | |

| 372.1 | | 319.5 | |

| 248.3 | |

| 205.0 | |

| |||||

Total capital (7) | 718.1 | |

| 622.1 | | 569.5 | |

| 498.3 | |

| 455.0 | |

| |||||

(1) Shown as a percent of net sales.

(2) Calculated using current assets divided by current liabilities.

(3) Calculated using current assets less non-interest bearing current liabilities.

(4) Calculated as net earnings (loss) divided by net sales.

(5) Calculated as net earnings (loss) divided by average assets.

(6) Calculated as net earnings (loss) divided by average equity.

(7) Calculated as interest-bearing debt plus stockholders' equity.

(8) Selling, general, and administrative expenses includes restructuring and impairment expenses in years that are applicable.

- 15 -

Review of Operations |

|

|

|

|

|

|

|

|

| ||||||||||

|

|

|

|

|

|

|

|

|

| ||||||||||

(In millions, except key ratios and per share data) | 2010 | 2009 |

| 2008 |

| 2007 |

| 2006 |

| ||||||||||

Operating Results |

|

|

|

|

|

|

|

|

| ||||||||||

Net sales | $ | 1,318.8 | | $ | 1,630.0 | |

| $ | 2,012.1 | |

| $ | 1,918.9 | |

| $ | 1,737.2 | |

|

Gross margin | 428.5 | | 527.7 | |

| 698.7 | |

| 645.9 | |

| 574.8 | |

| |||||

Selling, general, and administrative (8) | 334.4 | | 359.2 | |

| 400.9 | |

| 395.8 | |

| 371.7 | |

| |||||

Design and research | 40.5 | | 45.7 | |

| 51.2 | |

| 52.0 | |

| 45.4 | |

| |||||

Operating earnings | 53.6 | | 122.8 | |

| 246.6 | |

| 198.1 | |

| 157.7 | |

| |||||

Earnings before income taxes | 34.8 | | 98.9 | |

| 230.4 | |

| 187.0 | |

| 147.6 | |

| |||||

Net earnings | 28.3 | | 68.0 | |

| 152.3 | |

| 129.1 | |

| 99.2 | |

| |||||

Cash flow from operating activities | 98.7 | | 91.7 | |

| 213.6 | |

| 137.7 | |

| 150.4 | |

| |||||

Cash flow used in investing activities | (77.6 | ) | (29.5 | ) |

| (51.0 | ) |

| (37.4 | ) |

| (47.6 | ) |

| |||||

Cash flow used in financing activities | (78.9 | ) | (16.5 | ) |

| (86.5 | ) |

| (131.5 | ) |

| (151.4 | ) |

| |||||

Depreciation and amortization | 42.6 | | 41.7 | |

| 43.2 | |

| 41.2 | |

| 41.6 | |

| |||||

Capital expenditures | 22.3 | | 25.3 | |

| 40.5 | |

| 41.3 | |

| 50.8 | |

| |||||

Common stock repurchased plus cash dividends paid | 5.7 | | 19.5 | |

| 287.9 | |

| 185.6 | |

| 175.4 | |

| |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Key Ratios |

|

|

|

|

|

|

|

|

| ||||||||||

Sales growth (decline) | (19.1 | )% | (19.0 | )% |

| 4.9 | % |

| 10.5 | % |

| 14.6 | % |

| |||||

Gross margin (1) | 32.5 | | 32.4 | |

| 34.7 | |

| 33.7 | |

| 33.1 | |

| |||||

Selling, general, and administrative (1) (8) | 25.4 | | 22.0 | |

| 19.9 | |

| 20.6 | |

| 21.4 | |

| |||||

Design and research (1) | 3.1 | | 2.8 | |

| 2.5 | |

| 2.7 | |

| 2.6 | |

| |||||

Operating earnings (1) | 4.1 | | 7.5 | |

| 12.3 | |

| 10.3 | |

| 9.1 | |

| |||||

Net earnings growth (decline) | (58.4 | ) | (55.4 | ) |

| 18.0 | |

| 30.1 | |

| 45.9 | |

| |||||

After-tax return on net sales (4) | 2.1 | | 4.2 | |

| 7.6 | |

| 6.7 | |

| 5.7 | |

| |||||

After-tax return on average assets (5) | 3.7 | | 8.8 | |

| 21.0 | |

| 19.4 | |

| 14.4 | |

| |||||

After-tax return on average equity (6) | 64.2 | % | 433.1 | % |

| 170.5 | % |

| 87.9 | % |

| 64.2 | % |

| |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Share and Per Share Data |

|

|

|

|

|

|

|

|

| ||||||||||

Earnings per share-diluted | $ | 0.43 | | $ | 1.25 | |

| $ | 2.56 | |

| $ | 1.98 | |

| $ | 1.45 | |

|

Cash dividends declared per share | 0.09 | | 0.29 | |

| 0.35 | |

| 0.33 | |

| 0.31 | |

| |||||

Book value per share at year end | 1.41 | | 0.15 | |

| 0.42 | |

| 2.47 | |

| 2.10 | |

| |||||

Market price per share at year end | 19.23 | | 14.23 | |

| 24.80 | |

| 36.53 | |

| 30.34 | |

| |||||

Weighted average shares outstanding-diluted | 57.5 | | 54.5 | |

| 59.6 | |

| 65.1 | |

| 68.5 | |

| |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Financial Condition |

|

|

|

|

|

|

|

|

| ||||||||||

Total assets | $ | 770.6 | | $ | 767.3 | |

| $ | 783.2 | |

| $ | 666.2 | |

| $ | 668.0 | |

|

Working capital (3) | 182.9 | | 243.7 | |

| 182.7 | |

| 103.2 | |

| 93.8 | |

| |||||

Current ratio (2) | 1.3 | | 1.6 | |

| 1.6 | |

| 1.4 | |

| 1.3 | |

| |||||

Interest-bearing debt and related swap agreements | 301.2 | | 377.4 | |

| 375.5 | |

| 176.2 | |

| 178.8 | |

| |||||

Stockholders' equity | 80.1 | | 8.0 | |

| 23.4 | |

| 155.3 | |

| 138.4 | |

| |||||

Total capital (7) | 381.3 | | 385.4 | |

| 398.9 | |

| 331.5 | |

| 317.2 | |

| |||||

- 16 -

Item 7 MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Management's Discussion and Analysis

You should read the issues discussed in Management's Discussion and Analysis in conjunction with the company's Consolidated Financial Statements and the Notes to the Consolidated Financial Statements included in this Form 10-K.

Executive Overview

Herman Miller's mission statement is, Inspiring Designs to Help People Do Great Things. At present, most of our customers come to us for interior environments in corporate office and healthcare settings. We also have a growing presence in educational and consumer markets. Our primary products include furniture systems, seating, storage, freestanding furniture, healthcare environment products, casegoods and textiles.

More than 100 years of innovative business practices and a commitment to social responsibility have established Herman Miller as a recognized global company. A past recipient of the Smithsonian Institution's Cooper Hewitt National Design Award, Herman Miller designs can be found in the permanent collections of museums worldwide. Innovative business practices and a commitment to social responsibility have also helped establish Herman Miller as a recognized global leader. Herman Miller maintains the Human Rights Campaign Foundation's top rating in its annual Corporate Equality Index and was named among the 50 Best U.S. Manufacturers by Industry Week in 2014. Herman Miller is included in the Dow Jones Sustainability World Index and trades on the NASDAQ Global Select Market under the symbol MLHR.

Herman Miller's products are sold internationally through wholly-owned subsidiaries or branches in various countries including the United Kingdom, Canada, France, Germany, Italy, Japan, Mexico, Australia, Singapore, China, Hong Kong, India, and the Netherlands. The company's products are offered elsewhere in the world primarily through independent dealerships or joint ventures with customers in over 100 countries.

The company is globally positioned in terms of manufacturing operations. In the United States, the manufacturing operations are located in Michigan, Georgia, Wisconsin and North Carolina. In Europe, the manufacturing presence is located within the United Kingdom. The manufacturing operations in Asia include facilities located in Dongguan and Ningbo, China. The company manufactures products using a system of lean manufacturing techniques collectively referred to as the Herman Miller Performance System (HMPS). Herman Miller strives to maintain efficiencies and cost savings by minimizing the amount of inventory on hand. Accordingly, production is order-driven with direct materials and components purchased as needed to meet demand. The standard lead time for the majority of our products is 10 to 20 days. These factors result in a high rate of inventory turns and typically cause our inventory levels to appear relatively low compared to sales volume.

A key element of the company's manufacturing strategy is to limit fixed production costs by sourcing component parts from strategic suppliers. This strategy has allowed the company to increase the variable nature of our cost structure while retaining proprietary control over those production processes that we believe provide us a competitive advantage. As a result of this strategy, our manufacturing operations are largely assembly-based.

The business is comprised of various operating segments as defined by generally accepted accounting principles in the United States (U.S. GAAP). The operating segments are determined on the basis of how the company internally reports and evaluates financial information used to make operating decisions. For external reporting purposes, the company has identified the following reportable segments:

• | North American Furniture Solutions - Includes the operations associated with the design, manufacture, and sale of furniture products for work-related settings, including office, education, and healthcare environments, throughout the United States and Canada. The North American Furniture Solutions reportable segment is the aggregation of two operating segments. In addition, the company has determined that both operating segments within the North American Furniture Solutions reportable segment represent reporting units. |

• | ELA Furniture Solution s - ELA Furniture Solutions includes the operations associated with the design, manufacture, and sale of furniture products, primarily for work-related settings, in the EMEA, Latin America, and Asia-Pacific geographic regions. |

• | Specialty - Includes the operations associated with design, manufacture, and sale of high-craft furniture products and textiles including Geiger wood products, Maharam textiles, and Herman Miller Collection products. |

• | Consumer - Includes the operations associated with the sale of modern design furnishings and accessories to third party retail distributors, as well as direct to consumer sales through eCommerce, direct mailing catalogs, and DWR studios. |

The company also reports a corporate category consisting primarily of unallocated corporate expenses including restructuring, impairment, acquisition-related costs, and other unallocated corporate costs.

- 17 -

Core Strengths

The company relies on the following core strengths in delivering workplace solutions to customers.

• | Brands - The Herman Miller brand is recognized by customers as a pioneer in design and sustainability, and as an advocate that supports their needs and interests. Within the industries the company operates, Herman Miller, DWR, Geiger, Maharam, POSH, Nemschoff and Colbrook Bosson Saunders (CBS) are acknowledged as leading brands that inspire architects and designers to create their best design solutions. Leveraging the company's brand equity across the lines of business to extend the company's reach to customers and consumers is an important element of the company's business strategy. |

• | Problem-Solving Design and Innovation - The company is committed to developing research-based functionality and aesthetically innovative new products and has a history of doing so, in collaboration with a global network of leading independent designers. The company believes its skills and experience in matching problem-solving design with the workplace needs of customers provides the company with a competitive advantage in the marketplace. An important component of the company's business strategy is to actively pursue a program of new product research, design, and development. The company accomplishes this through the use of an internal research and engineering staff that engages with third party design resources generally compensated on a royalty basis. |

• | Operational Excellence - The company was among the first in our industry to embrace the concepts of lean manufacturing. HMPS provides the foundation for all of our manufacturing operations. The company is committed to continuously improving both product quality and production and operational efficiency. The company has extended this lean process work to its non-manufacturing processes as well as externally to our manufacturing supply chain and distribution channel. The company believes these concepts hold significant promise for further gains in reliability, quality and efficiency. |

• | Building and Leading Networks - The company values relationships in all areas of the business. The company considers its network of innovative designers, owned and independent dealers, and suppliers to be among the most important competitive factors and vital to the long-term success of the business. |

Channels of Distribution

The company's products and services are offered to most of its customers under standard trade credit terms between 30 and 45 days and are sold through the following distribution channels.

• | Independent and Owned Contract Furniture Dealers - Most of the company's product sales are made to a network of independently owned and operated contract furniture dealerships doing business in many countries around the world. These dealers purchase the company's products and distribute them to end customers. The company recognizes revenue on product sales through this channel once products are shipped and title passes to the dealer. Many of these dealers also offer furniture-related services, including product installation. |

At May 30, 2015 , the company owned three contract furniture dealerships, some of which have operations in multiple locations. The financial results of these owned dealers are included in our Consolidated Financial Statements. Product sales to these dealerships are eliminated as inter-company transactions from our consolidated financial results. The company recognizes revenue on these sales once products are shipped to the end customer and installation is substantially complete. The company believes independent ownership of contract furniture dealers is generally the best model for a financially strong distribution network. With this in mind, the company's strategy is to continue to pursue opportunities to transition the remaining owned dealerships to independent owners. Where possible, the goal is to involve local managers in these ownership transitions.

• | Direct Customer Sales - The company also sells products and services directly to end customers without an intermediary (e.g. sales to the U.S. federal government). In most of these instances, the company contracts separately with a dealership or third-party installation company to provide sales-related services. The company recognizes revenue on these sales once products are shipped and installation is substantially complete. |

• | DWR Retail Studios - At the end of fiscal 2015 DWR had 33 retail studio and two outlet locations located in metropolitan cities throughout the United States. Revenue on sales from these studios is recognized upon delivery to the end customer. |

• | E-Commerce - The company sells products through its online stores, in which products are available for sale via the company's website, hermanmiller.com as well as through the DWR online store, dwr.com. These sites complement our existing methods of distribution and extend the company's brand to new customers. The company recognizes revenue on these sales either upon shipment of the product, or for sales through the DWR online store, upon product delivery to the end customer. |

- 18 -

• | DWR Direct-Mail Catalogs - The company's consumer business unit utilizes a direct-mail catalog program through its DWR subsidiary. A regular schedule of catalog mailings is maintained throughout the fiscal year and these serve as a key driver of sales across each of DWR's channels, including retail studios and eCommerce websites. Revenue on sales transacted through this catalog program is recognized upon product delivery to the end customer. |

• | Independent Retailers - Certain products are sold to end customers through independent retail operations. Revenue is recognized on these sales once products are shipped and title passes to the independent retailer. |

Challenges Ahead

Like all businesses, the company is faced with a host of challenges and risks. The company believes its core strengths and values, which provide the foundation for its strategic direction, have us well prepared to respond to the inevitable challenges the company will face in the future. While the company is confident in its direction, the company acknowledges the risks specific to the business and industry. Refer to Item 1A for discussion of certain of these risk factors.

Future Avenues of Growth

In spite of the risks and challenges it faces, the company believes it's well positioned to successfully pursue its mission of inspiring designs to help people do great things. To find opportunities for growth, we are always examining the ways in which the world is changing and evolving. This helps us better meet the needs of our customers and ultimately, to exceed their expectations. We have identified 3 areas of fundamental social and technological change that are informing our business strategy.

• | Globalization & Demographics - Demographic shifts in the global workforce are significantly changing how and where value creation happens. Not only has the millennial generation overtaken the majority representation of the workforce, but economies that once relied on industrial production are increasingly becoming driven by knowledge work. |

• | Inherently Global & Seamlessly Digital - The ubiquity of technology allows people to connect with other people, content, work, businesses, and ideas wherever and whenever they want. This means the way people work is changing, where people work is changing, and how people work with each other is changing. |

• | The Era of Ideas - With the ongoing optimization of industrial production and information sharing, the demand for more innovative business solutions increases. The global focus of work is shifting to the successful generation and deployment of new ideas. As creativity and idea generation drive greater value - people, not process, provide the distinguishing capability. In this shift, workplaces are fundamentally changing from standardized and process-driven designs to diverse places that harness human capability, creativity, and relationships. |

We have developed a strategy to grow our business by shifting our focus in four fundamental ares in response to these changes. Through these shifts we are positioning the company to take advantage of existing markets, explore growth opportunities in new markets with supportive demographics, increase demand by addressing unmet needs, and expanding into areas that yield higher prospects for margins and profitability. The four fundamental shifts are described below:

• | From Product Centric to Solutions - The first strategic shift is to move from a product centric focus to one based upon delivering broader solutions to our customers. Herman Miller is retooling its core business to speak to customers with fresh insights, to spur new demand, and to change the game with unique solutions and services. |