UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

January 31, 2011

Commission File No. 0-18370

MFRI, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 36-3922969 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

7720 N. Lehigh Avenue, Niles, Illinois | 60714 |

(Address of principal executive offices) | (Zip Code) |

(847) 966-1000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered |

Common Stock, $.01 per share | The NASDAQ Stock Market, LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this FORM 10-K or any amendment to this FORM 10-K. Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one): Large accelerated filer o Accelerated filer o Non-accelerated filer o Smaller reporting company x

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of The Exchange Act) Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant (the exclusion of the market value of the shares owned by any person shall not be deemed an admission by the registrant that such person is an affiliate of the registrant) was $34,981,103 based on the closing sale price of $6.30 per share as reported on the NASDAQ Global Market on July 31, 2010.

The number of shares of the registrant's common stock outstanding at March 31, 2011 was 6,854,646 .

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement for the 2010 Annual Meeting of Stockholders are incorporated by reference in Part III.

MFRI, Inc.

FORM 10-K

For the fiscal period ended

January 31, 2011

TABLE OF CONTENTS

Item |

| Page | |

Part I |

|

| |

1. | Business | 1 |

|

| Piping Systems Business | 2 |

|

| Filtration Products Business

| 3 |

|

| Industrial Process Cooling Equipment Business | 5 |

|

| Employees

| 6 |

|

| International

| 6 |

|

| Executive Officers of the Registrant

| 7 |

|

1A. | Risk Factors

| 8 |

|

1B. | Unresolved Staff Comments

| 10 |

|

2. | Properties | 10 |

|

3. | Legal Proceedings

| 11 |

|

4. | RESERVED

| 11 |

|

|

|

| |

Part II |

|

| |

5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 11 |

|

6. | Selected Financial Data | 13 |

|

7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 13 |

|

7A. | Quantitative and Qualitative Disclosures About Market Risk | 23 |

|

8. | Financial Statements and Supplementary Data | 24 |

|

9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 24 |

|

9A. | Controls and Procedures | 24 |

|

9B. | Other Information | 24 |

|

|

|

| |

Part III |

|

| |

10. | Directors, Executive Officers and Corporate Governance | 25 |

|

11. | Executive Compensation | 25 |

|

12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 25 |

|

13. | Certain Relationships and Related Transactions, and Director Independence | 25 |

|

14. | Principal Accountant Fees and Services | 25 |

|

|

|

| |

Part IV |

|

| |

15. | Exhibits and Financial Statement Schedules | 25 |

|

|

|

| |

Report of Independent Registered Public Accounting Firm | 26 |

| |

Signatures | 54 |

| |

PART I

Forward Looking Statements

Statements in this Form 10-K that are not historical facts, so-called "forward-looking statements," are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Investors are cautioned that all forward-looking statements involve risks and uncertainties, including those detailed in MFRI's filings with the Securities and Exchange Commission ("SEC"). See "Risk Factors" in Item 1A.

Item 1. BUSINESS

MFRI, Inc., collectively with its subsidiaries ("MFRI", the "Company" or the "Registrant"), is engaged in the manufacture and sale of products in three distinct business segments: piping systems, filtration products and industrial process cooling equipment. Corporate and other includes the installation of heating, ventilation and air conditioning ("HVAC") systems. This activity is not sufficiently large to constitute a reportable segment. The Company's fiscal year ends on January 31. Years and balances described as 2010 and 2009 are the fiscal years ended January 31, 2011 and 2010 , respectively. In the year ended January 31, 2011 , no customer accounted for 10% or more of the Company's net sales.

Information with respect to the Company's business segments is included in the following discussions of the separate business segments and in the financial statements and related notes thereto.

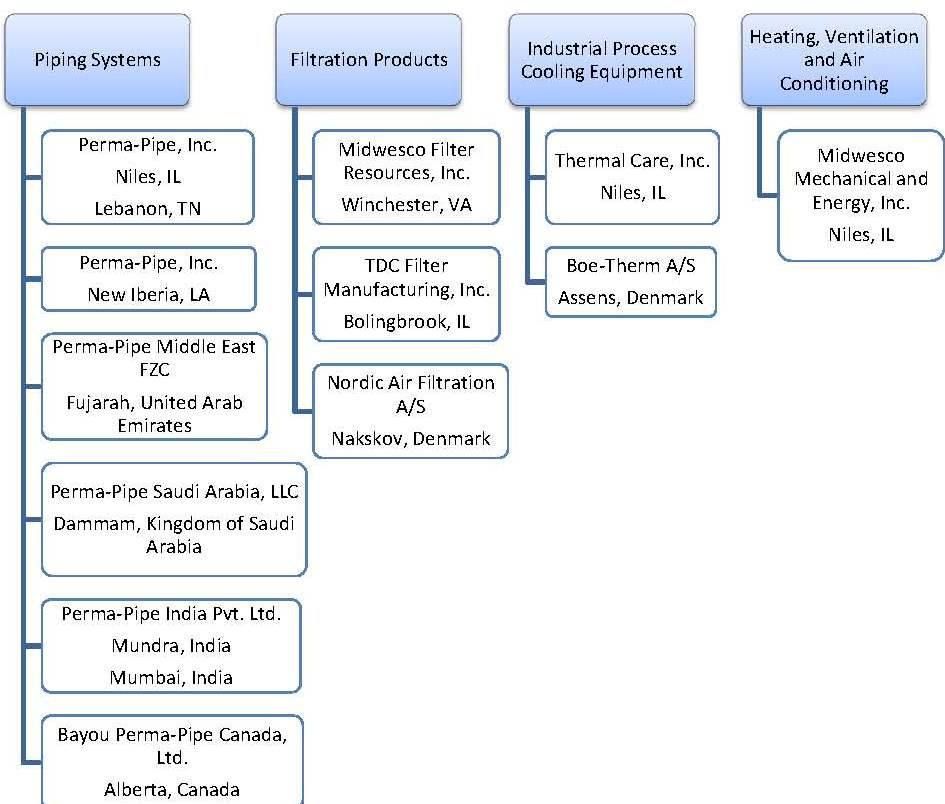

MFRI, Inc.'s Operating Units

All subsidiaries shown are, directly or indirectly, wholly owned by MFRI except Bayou Perma-Pipe Canada, Ltd., which is owned 49% by MFRI and 51% by an unrelated party.

1

Available Information

The Company files with, and furnishes to the SEC, reports including annual meeting materials, annual reports on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, as well as amendments thereto. The Company maintains a website www.mfri.com , where these reports and related materials are available free of charge as soon as reasonably practicable after the Company electronically delivers such material to the SEC. The information on the Company's website is not part of this annual report on Form 10-K, and is not incorporated into this or any other filings by the Company with the SEC.

Piping Systems

Products and Services. The Company engineers, designs, manufactures and sells specialty piping leak detection and location systems. Piping systems include (i) industrial and secondary containment piping systems for transporting chemicals, hazardous fluids and petroleum products, (ii) insulated and jacketed district heating and cooling ("DHC") piping systems for efficient energy distribution to multiple locations from central energy plants, and (iii) oil and gas gathering flow and long lines for oil and mineral transportation. The Company's leak detection and location systems are sold with many of its piping systems, and on a stand-alone basis to monitor areas where fluid intrusion may contaminate the environment, endanger personal safety, cause a fire hazard, impair essential services or damage equipment or property.

The Company's piping systems are frequently custom fabricated to job site dimensions and/or to incorporate provisions for thermal expansion due to varying temperatures. This custom fabrication helps to minimize the amount of field labor required by the installation contractor. Most of the Company's piping systems are produced for underground installations and, therefore, require trenching, which is done by unaffiliated installation contractors.

The Company's piping systems business is seasonal. See "Management's Discussion and Analysis of Financial Condition and Results of Operations - Piping Systems Business."

Marketing. The customer base is industrially and geographically diverse. In the United States of America ("U.S."), the Company employs national and regional sales managers who use and assist a network of independent manufacturers' representatives, none of whom sells products that are competitive with the Company's piping systems. Globally, the Company employs a direct sales force as well as an exclusive agent network for several countries in the Middle and Far East to market and sell products and services.

Recent Development. An additional insulated pipe manufacturing plant is being established in Dammam, Saudi Arabia to better serve the Gulf Cooperation Council ("GCC"), and nearby countries. This new state-of-the-art manufacturing facility will serve the special requirements of the oil and gas industry as well as the rapidly growing market for district cooling networks. Perma-Pipe Saudi Arabia, ("PPSA"), will feature Perma-Pipe's Xtru-Therm automated spray polyurethane insulation and several jacketing systems including polyethylene, metal and fiber reinforced plastic offering a comprehensive product range. PPSA will also be equipped to custom manufacture pipe spools and a complete range of pre-insulated fittings. The Company has received an industrial license and the required commercial registration and expects the plant to be fully operational in 2011.

Patents and Trademarks. The Company owns several patents covering its piping and electronic leak detection systems. The patents are not material either individually or in the aggregate to the overall business because the Company believes sales in the business would not be materially reduced if patent protection were not available. The Company owns numerous trademarks connected with its piping and leak detection systems business including the following: Perma-Pipe®, Chil-Gard®, Double Quik®, Escon-A®, FluidWatch®, Galva-Gard®, Polytherm®, Pal-AT®, Stereo-Heat®, LiquidWatch®, PalCom®, Xtru-therm®, Auto-Therm®, Pex-Gard®, Multi-Therm®, and Ultra-Therm®. The Company also owns a Canadian trademarks for Ric-Wil®, Perma-Pipe™, and Pal-at™, a Denmark trademark for Ric-Wil®, France trademark for Perma-Pipe®, German trademark for Perma-Pipe®, Oman trademarks for Perma-Pipe®, Pal-At® and Xtru-therm®, Kuwait trademarks for Perma-Pipe®, Pal-At® and Xtru-therm®, Saudi Arabia trademarks for Perma-Pipe® and Xtru-therm®, Singapore trademarks for Perma-Pipe®, Pal-At® and Xtru-therm®, India trademarks for Perma-Pipe™, Pal-At™ and Xtru-therm™, Australia trademark for

2

Ric-Wil® and Pal-at™, and United Kingdom trademarks for Polytherm®, Perma-Pipe® and Ric-Wil®, Hong Kong trademarks for Perma-Pipe®, Pal-At®, Xtru-therm® and Ric-Wil®.

Backlog. As of January 31, 2011 , the backlog (uncompleted firm orders) was $46.5 million, substantially all of which is expected to be completed in 2011. As of January 31, 2010 , the backlog was $48.8 million.

Raw Materials. The basic raw materials used in production are pipes and tubes made of carbon steel, alloy, copper, ductile iron, plastics and various chemicals such as polyols, isocyanate, urethane resin, polyethylene and fiberglass, mostly purchased in bulk quantities. The Company believes there are currently adequate supplies or sources of availability of these needed raw materials.

The sensor cables used in the leak detection and location systems are manufactured to the Company's specifications by companies regularly engaged in the business of manufacturing such cables. The Company owns patents for some of the features of its sensor cables. The Company assembles the monitoring component of the leak detection and location system from standard components purchased from many sources.

Competition. The piping systems business is highly competitive. The Company believes its principal competition in this segment consists of between ten and twenty major competitors and more small competitors. The Company believes quality, service, a comprehensive product line and price are the key competitive factors. The Company also believes it has a more comprehensive line for DHC than any of its competitors. Some competitors of the Company have greater financial resources and some have cost advantages as a result of manufacturing a limited range of products.

Government Regulation. The demand for the Company's leak detection and location systems and secondary containment piping systems, a small percentage of the total annual piping sales, is driven by federal and state environmental regulation with respect to hazardous waste. The Federal Resource Conservation and Recovery Act requires, in some cases, that the storage, handling and transportation of fluids through underground pipelines feature secondary containment and leak detection. The National Emission Standard for hydrocarbon airborne particulates requires reduction of airborne volatile organic compounds and fugitive emissions. Under this regulation, many major refineries are required to recover fugitive vapors and dispose of the recovered material in a process sewer system, which then becomes a hazardous secondary waste system that must be contained. Although there can be no assurances as to the ultimate effects of these governmental regulations, the Company believes it may increase the demand for its piping systems products.

Filtration Products

Products and Services. The Company manufactures and sells a wide variety of filter elements for cartridge collectors and baghouse air filtration and particulate collection systems. The principle types of industrial air filtration and particulate collection systems in use are baghouses, cartridge collectors, electrostatic precipitators, scrubbers and mechanical collectors. This equipment is used to eliminate particulate from the air by passing particulate laden gases through fabric filters (filter bags) or pleated media filter elements, in the case of baghouses or cartridge collectors, between electrically charged collector plates, in the case of electrostatic precipitators and contact with liquid reagents (scrubbers). The Company manufactures filter elements in standard industry sizes, shapes and filtration media and to custom specifications, maintaining manufacturing standards for more than 10,000 styles of filter elements to suit substantially all industrial applications. Filter elements are manufactured from industrial yarn, fabric and paper purchased in bulk. Most filter elements are produced from cellulose, acrylic, fiberglass, polyester, aramid, laminated membranes, or polypropylene fibers. The Company also manufactures filter elements from more specialized materials, sometimes using special finishes.

The Company markets numerous filter related products and accessories used during the installation, operation and maintenance of cartridge collectors and baghouses, including wire cages used to support filter bags, spring assemblies for proper tensioning of filter bags and clamps and hanger assemblies for attaching filter elements. In addition, the Company markets other hardware items used in the operation and maintenance of cartridge collectors and baghouses. The Company also provides maintenance services, consisting primarily of air filtration system

3

inspection and filter element replacement, using a network of independent contractors.

Over the past three years, the Company's filtration products business has supplied filter elements to more than 4,000 user locations. The Company has particular expertise in supplying filter bags for use with electric arc furnaces in the steel industry. The Company believes its production capacity and quality control procedures make it a leading supplier of filter bags to large users in the electric power industry. Orders from the electric power industry tend to be substantial in size, but are usually at lower margins than from other industries.

Marketing. The customer base is industrially and geographically diverse. These products and services are used primarily by operators of utility and industrial coal-fired boilers, incinerators and cogeneration plants and by producers of metals, cement, chemicals and other industrial products.

The Company has an integrated sales program for its filtration products business, which consists of field-based sales personnel, manufacturers' representatives, a telemarketing operation and computer-based customer information systems. The Company believes the computer-based information systems are instrumental in increasing sales of filter-related products and accessories and maintenance services, as well as sales of filter elements. The Company's filtration products are marketed domestically under the names, Midwesco Filter and TDC Filter Manufacturing.

The Company markets its U.S. manufactured filtration products internationally using domestically based sales resources to target major users in foreign countries. The Denmark filtration facility markets pleated filter elements throughout Europe and Asia, primarily to original equipment manufacturers.

Trademarks. The Company owns the following trademarks covering its filtration products: Seamless Tube®, Leak Seeker®, Prekote®, We Take the Dust Out of Industry®, Pleatkeeper®, Pleat Plus® and EFC®.

Backlog. As of January 31, 2011 , the backlog was $19.9 million, substantially all of which is expected to be completed in 2011. As of January 31, 2010 , the backlog was $21.4 million. Customers had until recently been delaying their purchase decisions in response to the economic climate; however, new infrastructure project spending continues to be at reduced levels.

Raw Materials. The basic raw materials used are industrial fibers and media supplied by leading producers of such materials. The majority of raw materials purchased are woven fiberglass fabric, yarns for manufacturing Seamless Tube® products and other woven, felted, spun bond, laminated membranes, and cellulose media. Only a limited number of suppliers are available for some of these materials. The Company believes supplies of all materials are adequate to meet current demand.

Competition. The filtration products industry is highly competitive. In addition, new installations of cartridge collectors and baghouses are subject to competition from alternative technologies including electrostatic precipitators, scrubbers, and mechanical collectors described above under Products and Services. The Company believes, based on domestic sales, that its principle competitors in this segment consist of approximately five major competitors and at least 50 smaller competitors, most of which are doing business on a regional or local basis. In Europe, several companies supply filtration products, and the Company is a relatively small participant in that market. Some of the Company's competitors have greater financial resources than the Company.

The Company believes quality, service, and price are the most important competitive factors in its filtration products business. Often, a manufacturer has a competitive advantage when its products have performed successfully for a particular customer in the past. Additional effort is required by a competitor to market products to such a customer. In certain applications, the Company's proprietary Seamless Tube® product and customer support provide the Company with a competitive advantage. Some competitors may have a competitive advantage with respect to their own proprietary products and processes, such as specialized fabrics and fabric finishes. In addition, some competitors may have cost advantages with respect to products as a result of lower wage rates and/or greater vertical integration.

4

Government Regulation . The Company's filtration products business is dependent upon governmental regulation of air pollution at the federal and state levels. Federal clean air legislation requires compliance with national primary and secondary ambient air quality standards for specific pollutants, including particulate. The states are primarily responsible for implementing these standards and, in some cases, have adopted more stringent standards than those issued by the U.S. Environmental Protection Agency ("EPA") under the Clean Air Act Amendments of 1990 ("Clean Air Act"). In addition, the EPA issued its own fine particle pollution standards in 1997 and 2006.

Industrial Process Cooling Equipment

Products and Services. The Company engineers, designs, manufactures and sells cooling and temperature control equipment for industrial applications. The Company believes it manufactures the most complete line of chillers available in its primary markets. Products include: chillers (portable and central); cooling towers; plant circulating assemblies; hot water, hot oil, and negative pressure temperature controllers; water treatment equipment; specialty cooling devices for printing presses and ink management; and replacement parts and various accessories relating to the foregoing products. The Company's products are used to optimize manufacturing productivity by quickly removing heat from manufacturing processes and providing accurate temperature control. The Company combines chillers and/or cooling towers with plant circulating systems to create plant wide systems that account for a large portion of its business. The Company specializes in customizing cooling systems and computerized controls according to customer specifications.

The principle markets for the Company's cooling and temperature control products are thermoplastics processing and the printing industries. The Company also sells its products to original equipment manufacturers, to other cooling manufacturers on a private branded basis and to manufacturers in the laser, metallizing, machine tool, and various other industries.

Marketing. The Company sells its products in the global thermoplastics and printing markets as well as to other industrial applications that require specialized heat transfer equipment. Domestic thermoplastics processors are the largest market served by the Company, representing the core of its business. The Company's cooling products are sold through independent manufacturers' representatives on an exclusive territory basis. Temperature control products are sold through a network of independent dealers/distributors in major industrial markets.

The Company believes the total annual U.S. market for water cooling equipment in the plastics industry was more than $100 million on a pre-recession basis, and the Company is one of the three largest suppliers of such equipment to the plastics industry. The Company believes the plastics industry is a mature industry with growth consistent with that of the national economy. The Company has increased sales to non-plastics industries that require specialized heat transfer equipment, usually sold to end users as a package by the supplier of the primary equipment, particularly in the laser, metalizing, and machine tool industries. The Company believes the size of this market was more than $200 million annually prior to the current recession. The original equipment manufacturer distributes products to the end user in these markets.

Trademarks. The Company has registered the trademarks Thermal Care®, AWS® and Applied Web Systems®.

Backlog. As of January 31, 2011 , the backlog was $4.3 million, substantially all of which is expected to be completed in 2011. As of January 31, 2010 , the backlog was $2.4 million.

Raw Materials. The Company uses prefabricated sheet metal and subassemblies manufactured by both Thermal Care and outside vendors for chillers and temperature control fabrication. Cooling towers are manufactured using fiberglass and hardware components purchased from several sources. The Company believes its access to sheet metal, subassemblies, fiberglass and hardware components is adequate to meet demands.

Competition. The Company believes there are about 15 competitors selling cooling equipment in the domestic plastics market. The Company further believes three manufacturers, including the Company, account for approximately 50% of the domestic plastics cooling equipment market. Many international customers, with relatively small cooling needs, are able to purchase small refrigeration units (portable chillers), which are

5

manufactured in their respective local markets at prices below that which the Company can offer due to issues such as freight cost and customs duties. However, such local manufacturers often lack the technology and products needed for plant wide cooling systems. The Company believes its reputation for producing quality plant wide cooling products results in a significant portion of the Company's business in the cooling product area. Temperature control units, which are sold globally, compete with both local and European manufacturers. The quality, reliability, features and range of temperature control applications addressed by the Company's products provide a competitive advantage.

The Company believes quality, service, a comprehensive product line and price are the key competitive factors in its industrial process cooling equipment business. The Company believes it has a more comprehensive line of cooling products than any of its competitors. Certain competitors of the Company have cost advantages as a result of manufacturing in non-union shops and offering a limited range of products. Some of the Company's competitors may have greater financial resources than the Company.

Government Regulation. The Company does not expect compliance with federal, state and local provisions regulating the discharge of materials into the environment or otherwise relating to the protection of the environment to have a material effect on capital expenditures, earnings or the Company's competitive position. Management is not aware of the need for any material capital expenditures for environmental control facilities for the foreseeable future. Regulations, promulgated under the Clean Air Act, prohibit the manufacture and sale of certain refrigerants. The Company does not use those refrigerants in its products. The Company expects that suitable refrigerants conforming to federal, state and local laws and regulations will continue to be available to the Company, although no assurances can be given as to the ultimate effect of the Clean Air Act and related laws on the Company.

Employees

As of February 28, 2011 , the Company had 1,123 full-time employees, of whom 38.1% worked outside the U.S.

International

The Company's international operations as of January 31, 2011 include subsidiaries and a joint venture in five foreign countries on three continents. The Company's international operations contributed approximately 27.6% of revenue in 2010 , 29.0% of revenue in 2009 , and 30.7% of revenue in 2008.

Refer to the Business Segment descriptions on pages 1 through 5 above and Note 1 - Business and Segment Information in the Notes to Consolidated Financial Statements for additional information on international activities. International operations are subject to risks inherent in conducting business in foreign countries, including price controls, exchange controls, limitations on participation in local enterprises, nationalization, expropriation and other governmental action, and changes in currency exchange rates.

6

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table set forth information regarding the executive officers of the Company as of March 15, 2011:

Name | Offices and Positions, if any, held with the Company; Age | Executive Officer of the Company or its Predecessor since |

David Unger | Director, Chairman of the Board, and Chief Executive Officer of the Company; Age 76 | 1972 |

|

|

|

Bradley E. Mautner | Director, President and Chief Operating Officer of the Company; Age 55 | 1994 |

|

|

|

Michael D. Bennett | Vice President, Chief Financial Officer, Secretary and Treasurer; Age 66 | 1989 |

|

|

|

Timothy P. Murphy | Vice President; Age 61 | 2008 |

|

|

|

Fati A. Elgendy | President, Perma-Pipe; Age 62 | 1990 |

|

|

|

Robert A. Maffei | Vice President, Perma-Pipe; Age 63 | 1987 |

|

|

|

John Mark Foster | President, Midwesco Filter; Age 49 | 2008 |

|

|

|

Stephen C. Buck | President, Thermal Care; Age 62 | 2007 |

|

|

|

Edward A. Crylen | President, Midwesco Mechanical and Energy; Age 59 | 2006 |

All of the executive officers serve at the discretion of the Board of Directors.

David Unger

, Chairman of the Board and Chief Executive Officer since 1989; President from 1994 until 2004.

Bradley E. Mautner,

President and Chief Operating Officer since December 2004; Executive Vice President from December 2002 to December 2004;Vice President from December 1996 through December 2002; Director since 1994. Bradley E. Mautner is the son of Henry M. Mautner, a director.

Michael D. Bennett,

Chief Financial Officer and Vice President since August 1989.

Timothy P. Murphy,

Vice President of Human Resources ("HR") since May 2008. Prior to joining the Company, Mr. Murphy spent 28 years as a business consultant in roles including Principal Partner of Murphy & Hill Consulting, Managing Director of the Bay Area office of RHR, International and Consultant with YSC, Ltd. Mr. Murphy previously consulted to the Company from 1985 to 2008.

Fati A. Elgendy

, President and Chief Operating Officer of Perma-Pipe since March 1995.

Robert A. Maffei

, Vice President, Director of Sales and Marketing of Perma-Pipe since August 1996.

John Mark Foster,

President of Midwesco Filter since August, 2008. Mr. Foster previously worked at Saint-Gobain (PAR: SGO) in the areas of industrial/project engineering and plant management, followed by positions in market management, human resources and a series of North American and European general management assignments.

7

Stephen C. Buck,

Presidentof Thermal Care since October, 2007. Mr. Buck joined Thermal Care after a 22 year career most recently as President - Safety Products Group with Federal Signal Corporation (NYSE: FSS), which manufactures and markets products to industrial and municipal customers worldwide. Prior to his employment with Federal Signal Corporation, Mr. Buck held various positions in marketing and management for companies in computer hardware/software, oil field services and telecommunications.

Edward A. Crylen,

President and Chief Operating Officer of Midwesco Mechanical and Energy, since its formation in December 2006. From 1989 to December 2006, he was President of the Midwesco Mechanical and Energy, division of Midwesco, Inc. (affiliate) that was primarily owned by two principal stockholders who were also members of management.

Item 1A. RISK FACTORS

The Company's business, financial condition, results of operations and cash flows are subject to various risks, including, but not limited to those set forth below, which could cause actual results to vary materially from recent results or from anticipated future results. These risk factors should be considered together with information included elsewhere in this Annual Report on Form 10-K.

Economic Factors . All of the Company's businesses, directly or indirectly, serve markets that continue to be adversely impacted by the continuing global economic climate. Although the economy appears to be improving, the timing of economic recovery in the markets we serve remains uncertain. A further downturn in one or more of our significant markets could have a material adverse effect on the Company's business, results of operations or financial condition. Because economic and market conditions vary within the Company's business segments, the Company's future performance by business segment will also vary. In addition, the Company is exposed to fluctuations in currency exchange rates and commodity prices. Failure to successfully manage any of these risks could have an adverse impact on the Company's financial position, results of operations and cash flows.

Customer Access to Capital Funds. Uncertainty about current economic market conditions in the U.S. and globally poses risks that the Company's customers may postpone spending for capital improvement and maintenance projects in response to tighter credit markets or negative financial news, which could have a material negative effect on the demand for the Company's products. The adverse effect of the credit availability experienced by the Emirate of Dubai has significantly decelerated construction activity both in the United Arab Emirates ("U.A.E.") and across other GCC countries, negatively impacting sales volume at the U.A.E. facility.

International rapid growth. Potential international future rapid growth could place a significant strain on management, operations and financial systems as well as on the Company's ability to attract and retain competent employees. Future operating results depend on the Company's ability to continue to implement and improve operating and financial controls and management information systems. Failure to effectively manage growth could materially adversely impact the business, financial conditions and results of operations.

Changes in Government Policies and Laws, Worldwide Economic Conditions . International sales represent a significant portion of the Company's total sales and continued growth and profitability may involve further international expansion. The Company's financial results could be affected by changes in trade, monetary and fiscal policies, laws and regulations, or other activities of U.S. and non U.S. governments, agencies and similar organizations. These conditions include, but are not limited, to changes in a country's or region's economic or political conditions, trade regulations affecting production, pricing and marketing of products, local labor conditions and regulations, reduced protection of intellectual property rights in some countries, changes in the regulatory or legal environment, restrictions on currency exchange activities, burdensome taxes and tariffs and other trade barriers. International risks and uncertainties, including changing social and economic conditions as well as terrorism, political hostilities and war, could lead to reduced international sales and reduced profitability associated with such sales.

Government regulation. Demand for the Company's leak detection and location and secondary containment piping systems is driven primarily by government regulation with respect to hazardous waste. Laws such as the Federal

8

Resource Conservation and Recovery Act and standards such as the National Emission Standard for Hydrocarbon Airborne Particulates have increased the demand for the Company's leak detection and location and secondary containment piping systems. The Company's filtration products business, to a large extent, is dependent on governmental regulation of air pollution at the federal and state levels. The Company believes that continuing growth in the sale of filtration products and services will be materially dependent on continuing enforcement of environmental laws such as the Clean Air Act. Although changes in such environmental regulations could significantly alter the demand for the Company's products and services, the Company does not believe such a change is likely to decrease demand in the foreseeable future.

Financing. If there were an event of default under the Company's current revolving credit facility, the holders of the defaulted debt could cause all amounts outstanding with respect to that debt to be due and payable immediately. The Company cannot assure that the assets or cash flow would be sufficient to fully repay amounts due under any of the financing arrangements, if accelerated upon an event of default, or, that the Company would be able to repay, refinance or restructure the payments under any such arrangements. Complying with the covenants under the Company's revolving credit facility may limit management's discretion by restricting options such as:

· incurring additional debt;

· entering into transactions with affiliates;

· making investments or other restricted payments;

· paying dividends or make other distributions; and

· creating liens.

Any additional financing the Company may obtain could contain similar or more restrictive covenants. The Company's ability to comply with any covenants may be adversely affected by general economic conditions, political decisions, industry conditions and other events beyond management's control.

Competition. The businesses in which the Company is engaged are highly competitive. Many of the competitors are larger and have more resources than the Company. Additionally, many of the Company's products are also subject to competition from alternative technologies and alternative products. To the extent the Company relies upon a single source for key components of several of its products, the Company believes there are alternate sources available for such components; however, there can be no assurance that the interruption of supplies of such components would not have an adverse effect on the financial condition of the Company, and that the Company, if required to do so, would be able to negotiate agreements with alternative sources on acceptable terms.

Backlog. The Company defines backlog as the revenue value in dollars attributed to confirmed customer purchase orders that have not yet been recognized as revenues. However, by industry practice, orders may be canceled or modified at any time. When a customer cancels an order, the customer is responsible for all finished goods, all direct and indirect costs incurred, and also for a reasonable allowance for anticipated profits. No assurance can be given that these amounts will be recovered after cancellation. Any cancellation or delay in orders may result in lower than expected revenues.

Percentage-of-completion method of accounting. The Company measures and recognizes a portion of revenue and profits under the percentage-of-completion accounting methodology. This methodology allows revenue and profits to be recognized proportionally over the life of a contract by comparing the amount of the cost incurred to date against the total amount of cost expected to be incurred. The effect of revisions to revenue and total estimated cost is recorded when the amounts are known and can be reasonably estimated. These revisions can occur at any time and could be material. On a historical basis, management believes that reasonably reliable estimates of the progress towards completion on long-term contracts have been made. However, given the uncertainties associated with these types of contracts, it is possible for actual cost to vary from estimates previously made, which may result in reductions or reversals of previously recorded revenue and profits.

Regulatory and legal requirements . As a public company, the Company is required to comply with the reporting obligations of the Securities Exchange Act of 1934. Keeping informed of, and in compliance with, changing laws,

9

regulations and standards relating to corporate governance, public disclosure and accounting standards, including the Sarbanes-Oxley Act, Dodd-Frank Act, as well as new and proposed SEC regulations and accounting standards, has required an increased amount of management attention and external resources. Compliance with such requirements may result in increased general and administrative expenses and an increased allocation of management time and attention to compliance activities.

Item 1B. UNRESOLVED STAFF COMMENTS

None

Item 2. PROPERTIES

Piping Systems Business

Illinois | Owned production facilities and office space | 16,800 square feet |

Louisiana | Owned production facilities and leased land | 18,900 square feet |

Tennessee | Owned production facilities and office space | 131,800 square feet on approximately 23.5 acres |

Canada | Joint venture owned production facilities and office space | 87,160 square feet on approximately 128 acres |

India | Leased production facilities, office space and land | 227,390 square feet |

United Arab Emirates | Leased office space and land for production facilities | 117,900 square feet on 16 acres |

Saudi Arabia | Planned production facilities on leased land | 88,960 square feet |

Filtration Products Business

Illinois | Bolingbrook - owned production facilities and office space | 101,500 square feet on 5.5 acres |

| Cicero - owned former production facilities and office space currently idle | 130,700 square feet on 2.8 acres |

Virginia | Owned production facilities | 97,500 square feet on 5.0 acres |

| Leased production and office space | 67,000 square feet |

Denmark | Owned production facilities and office space | 69,800 square feet on 3.5 acres |

Industrial Process Cooling Equipment Business

Illinois | Owned production facilities and office space | 87,600 square feet on 8.1 acres |

Denmark | Owned production facilities and office space | 16,500 square feet |

The Company's principal executive offices, which occupy approximately 23,400 square feet of space in Niles, Illinois, are owned by the Company. The Company believes its properties and equipment are well maintained and in good operating condition and, that productive capacities will be adequate for present and currently anticipated needs.

The Company has four significant lease agreements as follows:

• | Planned production facilities and land of approximately 88,960 square feet in the Kingdom of Saudi Arabia is leased through 2030. |

10

• | Office Space and land for production facilities of approximately 117,900 square feet in the U.A.E. leased until June 30, 2012. |

• | Production facilities, office space and land of approximately 227,390 square feet in India are leased through October, 2012 and December, 2012, respectively. |

• | Production facilities and office space of approximately 67,000 square feet in Virginia are leased through July 31, 2012 and July 31, 2013, respectively. |

For further information, see Note 6 - Lease Information, in the Notes to Consolidated Financial Statements.

Item 3. LEGAL PROCEEDINGS

The Company had no pending litigation material to its business.

Item 4. RESERVED

PART II

Item 5.

MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

The Company's fiscal year ends on January 31. Years and balances described as 2010, 2009, 2008, 2007, and 2006 are the fiscal years ended January 31, 2011, 2010, 2009, 2008, and 2007, respectively.

The Company's Common Stock is traded on the Nasdaq Global Market under the symbol "MFRI". The following table sets forth, for the periods indicated, the high and low Common Stock sale prices as reported by the Nasdaq Global Market for 2010 and for 2009.

| High |

| Low |

|

2010 |

|

| ||

First Quarter | $7.21 | $6.16 | ||

Second Quarter | 6.95 |

| 5.86 |

|

Third Quarter | 8.76 |

| 6.25 |

|

Fourth Quarter | 11.00 |

| 7.68 |

|

2009 |

|

| ||

First Quarter | 6.43 |

| 4.85 |

|

Second Quarter | 8.04 |

| 5.45 |

|

Third Quarter | 7.43 |

| 6.00 |

|

Fourth Quarter | 7.32 |

| 6.38 |

|

As of March 15, 2011, there were 73 stockholders of record.

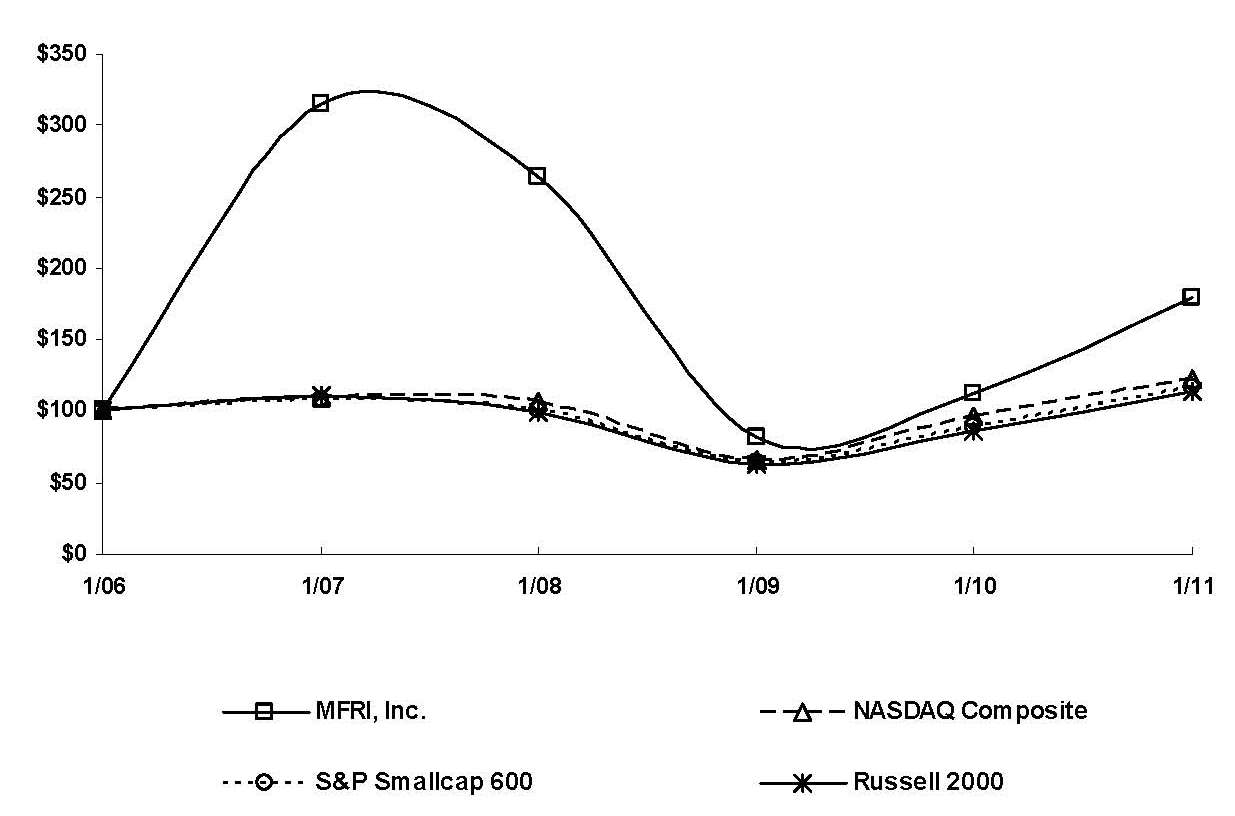

STOCK PRICE PERFORMANCE GRAPH

The Stock Price Performance Graph compares the yearly dollar change in the Company's cumulative total stockholder return on its Common Stock with the cumulative total returns of the Nasdaq Composite Index (the "Nasdaq Index"), the Russell 2000 Index and the S&P Smallcap 600 Index. The Company has selected these indices because they include companies with similar market capitalizations to the Company, as the most appropriate comparisons because the Company has three distinctly different business segments and no industry "peer" group is comparable to the Company. The comparison assumes $100.00 investments on January 31, 2006 in the Company's

11

Common Stock, the Nasdaq Index, the Russell 2000 Index, and the S&P Smallcap 600 Index and further assumes reinvestment of dividends.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among MFRI, Inc., the NASDAQ Composite Index,

the S&P Smallcap 600 Index and the Russell 2000 Index

*$100 invested on 1/31/06 in stock or index, including reinvestment of dividends.

Copyright© 2011 S&P, a division of the McGraw-Hill Companies Inc. All rights reserved.

Fiscal year ending January 31, | 2006 |

| 2007 |

| 2008 |

| 2009 |

| 2010 |

| 2011 |

|

MFRI, Inc. | $100.00 | $315.70 | $264.13 | $81.82 | $112.73 | $180.08 | ||||||

NASDAQ Composite | 100.00 |

| 109.00 |

| 107.06 |

| 66.17 |

| 96.82 |

| 122.57 |

|

S&P Smallcap 600 | 100.00 |

| 108.41 |

| 100.73 |

| 63.73 |

| 88.56 |

| 115.95 |

|

Russell 2000 | 100.00 |

| 110.44 |

| 99.63 |

| 62.92 |

| 86.72 |

| 113.92 |

|

The Company has never declared or paid a cash dividend and does not anticipate paying cash dividends on its Common Stock in the foreseeable future. Management presently intends to retain all available funds for the development of the business and for use as working capital. Future dividend policy will depend upon the Company's earnings, capital requirements, financial condition and other relevant factors. The Company's line of credit agreement does not permit the payment of dividends. For further information, see Note 5 - Debt in the Notes to Consolidated Financial Statements.

Neither the Company nor any "affiliated purchaser" as defined in Rule 10b-18 purchased any shares of the Company's Common Stock during the period covered by this report. The Company has not made any sale of unregistered securities during the preceding three years.

The Transfer Agent and Registrar for the Common Shares is Continental Stock Transfer & Trust Company, 17 Battery Place, New York, New York 10004, (212) 509-4000.

12

Equity Compensation Plan Information

The following table provides information regarding the number of shares of Common Stock to be issued upon exercise of outstanding options, warrants and rights under the Company's equity compensation plans and the weighted average exercise price and number of shares of Common Stock remaining available for issuance under those plans as of January 31, 2011 .

Plan Category | Number of shares to be | Weighted-average exercise | Number of shares | ||

Equity compensation plans approved by stockholders | 777,441 |

| $11.88 | 479,157 |

|

Item 6. SELECTED FINANCIAL DATA

The following selected financial data for the Company for the years 2010, 2009, 2008, 2007, and 2006 are derived from the financial statements of the Company. The information set forth below should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" included herein in response to Item 7 and the consolidated financial statements and related notes included herein in response to Item 8.

Referenced as | 2010 |

| 2009 |

| 2008 |

| 2007 |

| 2006 |

|

|

|

| January 31, |

|

| |||||

(In thousands, except per share data) | 2011 |

| 2010 |

| 2009 |

| 2008 |

| 2007 |

|

Statements of Operations Data |

|

|

|

|

| |||||

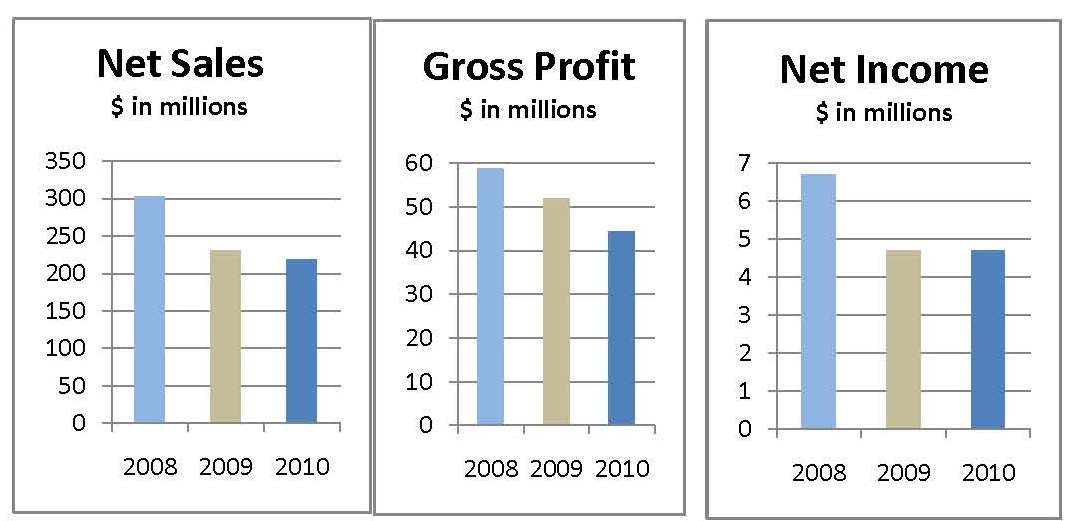

Net sales | $218,598 | $230,381 | $303,066 | $239,487 | $213,471 | |||||

Income from operations | 2,898 |

| 7,197 |

| 10,792 |

| 2,896 |

| 8,942 |

|

Net income (loss) | 4,510 |

| 4,671 |

| 6,689 |

| (298 | ) | 4,593 |

|

Net income (loss) per share - basic | 0.66 | 0.68 |

| 0.98 |

| (0.04 | ) | 0.86 |

| |

Net income (loss) per share - diluted | 0.66 | 0.68 |

| 0.98 |

| (0.04 | ) | 0.82 |

| |

|

|

|

|

|

| |||||

Balance Sheet Data |

|

|

|

|

| |||||

Total assets | $163,275 | $150,547 | $181,148 | $140,412 | $121,440 | |||||

Long-term debt (excluding capital | 36,009 |

| 33,877 |

| 41,763 |

| 19,556 |

| 29,606 |

|

Capital leases, less current portion | 183 |

| 195 |

| 327 |

| 152 |

| 238 |

|

Item 7.

MANAGEMENT'S DISCUSSION AND ANALYSIS ("MD&A") OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The statements contained under the caption "Management's Discussion and Analysis of Financial Condition and Results of Operations" and other information contained elsewhere in this annual report, which can be identified by the use of forward-looking terminology such as "may," "will," "expect," "continue," "remains," "intend," "aim," "should," "prospects," "could," "future," "potential," "believes," "plans," "likely" and "probable" or the negative thereof or other variations thereon or comparable terminology, constitute "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and are subject to the safe harbors created thereby. These statements should be considered as subject to the many risks and uncertainties that exist in the Company's operations and business environment. Such risks and uncertainties could cause actual results to differ materially from those projected as a result of many factors, including but not limited to those under the heading Item 1A. Risk Factors.

13

CONSOLIDATED RESULTS OF OPERATIONS

Consolidated Backlog(In thousands ): | 1/31/2011 |

| 1/31/2010 |

|

Piping Systems | $46,452 | $48,770 | ||

Filtration Products | 19,935 |

| 21,400 |

|

Industrial Process Cooling Equipment | 4,332 |

| 2,380 |

|

Corporate and Other | 9,751 |

| 790 |

|

Total | $80,470 | $73,340 | ||

MFRI, Inc. is engaged in the manufacture and sale of products in three reportable business segments: piping systems, filtration products, and industrial process cooling equipment. Piping systems' domestic sales and earnings are seasonal, typically lower during the fourth and first quarters due to unfavorable weather for construction over much of North America, and are correspondingly higher during the second and third quarters. The Company website address is www.mfri.com .

The analysis presented below and discussed in more detail throughout the MD&A was organized to provide instructive information for understanding the business going forward. However, this discussion should be read in conjunction with the consolidated financial statements in Item 8 of this report, including the notes thereto. An overview of the segment results is provided in Note 1 - Business and Segment Information to the consolidated financial statements in Item 8 of this report.

Critical Accounting Policies and Estimates

MD&A discusses the audited consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period.

Management believes that judgments and estimates related to the following critical accounting policies could materially affect the consolidated financial statements:

• | Revenue recognition |

• | Percentage of completion revenue recognition |

• | Inventory |

• | Income taxes |

• | Equity-based compensation |

• | Fair value of financial instruments |

In the fourth quarter of 2010, there were no changes in the above critical accounting policies.

14

All of the Company's businesses directly or indirectly serve markets that were adversely impacted by recent global economic conditions. Although improvement is expected, the timing of economic recovery in the markets we serve remains uncertain. A further downturn in one or more of our significant markets could have a material adverse effect on the Company's business, results of operations or financial condition. Because economic and market conditions vary within the Company's business segments, the Company's future performance by business segment will also vary. Should the current credit crisis and general economic recession continue, the Company could continue to experience a period of declining net sales, which could adversely impact the Company's results of operations. The adverse effect of the credit crisis experienced by the Emirate of Dubai has significantly decelerated construction activity both in the U.A.E. and across other GCC countries, negatively impacting sales volume at the U.A.E. facility.

2010 Compared to 2009

Net sales were $218.6 million in 2010 , a decrease of 5.1% from $230.4 million in 2009 . Year-to-date sales increased in the industrial process cooling and filtration products businesses while decreasing in the piping systems business. HVAC activity decreased in the current year; however, the backlog in 2010 increased to $9.8 million.

Gross profit of $44.5 million in 2010 decreased 14.4% from $51.9 million in 2009 . Gross margin was 20.3% compared to 22.5% in 2009 . Virtually the entire gross profit decline occurred in the piping systems, which decreased to $27.3 million in 2010 from $38.0 million in 2009 . The decrease in gross profit was attributed primarily to lower volume of the piping systems business in the U.A.E and a significant decrease in sales associated with the completion of the India pipeline project. The filtration products and industrial process cooling businesses each experienced an increase in their gross profits for the period, primarily due to increased sales volume, margin improvements and benefits from previous expense reduction initiatives.

General and administrative expenses decreased 12.0% to $27.9 million from $31.7 million. The reduction was mainly due to lower profit-based management incentive compensation expense, lower legal expenses, and reduced foreign exchange loss in the current year partially offset by an increase in deferred compensation expense.

Selling expenses increased 4.6% to $13.6 million from $13.0 million. Commission expense increased in the filtration products and industrial process cooling businesses, and trade show activity was higher in the piping systems business.

The Company's worldwide effective income tax rates for 2010 and 2009 were (72.1)% and 12.0% , respectively. For additional information, see the Income Tax section of the MD&A and see Note 7 - Income Taxes in the Notes to the Financial Statements.

Net income was level at $4.5 million. The fourth quarter produced a net loss of $1.5 million significantly better than the net loss of $5.8 million in the comparable prior-year's quarter. The filtration products and industrial process cooling businesses and the piping systems joint venture drove this improvement. Another factor was the look-through rules of Subpart F passive income which expired December 31, 2009, and then were retroactively extended in December 2010. In the second quarter, the Company had recorded $0.3 million in tax expense related to passive income that was reversed in the fourth quarter.

2009 Compared to 2008

Net sales were $230.4 million in 2009 , a decrease of 24.0% from $303.1 million in 2008, with decreased sales in the piping systems business, the filtration products business and the industrial process cooling business. This decrease was most pronounced in the fourth quarter. The 2009 fourth quarter compared to prior-year's quarter decreased 40.6%, with all segments and geographies down. In the piping systems business, district heating and cooling as well as oil and gas products experienced softer market conditions. Other contributing factors were the completion of the India pipeline project in the third quarter 2009 and the dramatically weaker market conditions in Dubai. The HVAC business also showed decreased sales as construction decisions for new projects have been deferred.

15

Gross profit of $51.9 million decreased 11.9% from $58.9 million. Gross margin rose to 22.5% from 19.5%.

General and administrative expenses increased 2.9% to $31.7 million from $30.8 million. The increase was mainly due to increased legal fees associated with collection activities in the U.A.E., foreign exchange loss, increased deferred compensation expense and increased stock compensation expense.

Selling expenses decreased 10.5% to $13.0 million from $14.6 million. This decrease was primarily driven by the industrial process cooling equipment business and the filtration product business, which had decreased commission expense from lower sales and a decline in compensation and related expenses due to staff reductions.

The Company's worldwide effective income tax rates for 2009 and 2008 were 12.0% and 17.0% , respectively.

Net income was $4.7 million in 2009, down from net income of $6.7 million in 2008 primarily due to decreased sales, the reasons summarized above and those discussed in more detail below. The fourth quarter produced a net loss of $5.8 million compared to a net loss of $0.8 million in the prior-year's quarter. The net loss in the fourth quarter of 2009 was higher than the same period in 2008 due to lower sales in all segments and compressed margins due to competitive factors.

Piping Systems

Piping systems' domestic sales and earnings are seasonal, typically lower during the fourth and first quarters due to unfavorable weather for construction over much of North America, and are correspondingly higher during the second and third quarters.

|

|

|

| % (Decrease) Increase | ||||||

(In thousands) | 2010 |

| 2009 |

| 2008 |

| 2010 |

| 2009 |

|

Net sales | $104,559 | $111,665 | $151,792 | (6.4 | )% | (26.4 | )% | |||

|

|

|

|

|

| |||||

Gross profit | 27,303 | 37,974 | 37,871 | (28.1 | )% | 0.3 | % | |||

Percentage of net sales | 26.1 | % | 34.0 | % | 24.9 | % |

|

| ||

|

|

|

|

|

| |||||

Income from operations | 13,831 | 22,399 | 24,037 | (38.3 | )% | (6.8 | )% | |||

Percentage of net sales | 13.2 | % | 20.1 | % | 15.8 | % |

|

| ||

2010 Compared to 2009

Despite significant sales drops in the Middle East and India, net sales of $104.6 million decreased only 6.4% from $111.7 million, in the prior-year, attributed primarily to a rise in sales in both domestic heating and cooling, and oil and gas products. The insulation of pipe for a crude oil pipeline project in India began full production in the third quarter 2008 and contributed to the increase in sales of $11.3 million in 2009 when the Company had successfully completed the production on the India pipeline project. Significantly smaller India pipeline sales followed in 2010.

Gross margin decreased to 26.1% of net sales from 34.0% of net sales in the prior-year attributed primarily to

the reduced volume in the U.A.E. and the significantly lower sales associated with the India pipeline project in the current year.

General and administrative expense decreased to $10.3 million or 9.9% of net sales in 2010 from $12.8 million or 11.4% of net sales in 2009. This decrease was primarily due to less profit-based management incentive expense, lower legal fees, and staff reductions in the U.A.E.

Selling expense increased to $3.1 million or 3.0% of net sales in 2010 from $2.8 million or 2.5% of net sales in

16

2009. The increase was mainly due to advertising and trade show activities, partially offset by a decrease in commission expense.

2009 Compared to 2008

Net sales of $111.7 million decreased 26.4% from $151.8 million, attributed primarily to a drop in sales in both international and domestic heating and cooling, as well as oil and gas products due to the economic slowdown both in the U.S. and in the U.A.E. The insulation of pipe for a crude oil pipeline project in India began full production in the third quarter 2008 and contributed to sales in 2009. As of October 31, 2009, the Company had completed the India pipeline project, and has received additional orders for at least 150 kilometers (93 miles), which began in May of 2010.

The adverse effect of the credit crisis experienced by the Emirate of Dubai has significantly decelerated construction activity both in the U.A.E. and across other GCC countries, negatively impacting sales volume at the U.A.E. facility.

Gross margin as a percent of net sales increased to 34.0% in 2009 from 24.9% in 2008, primarily due to production efficiencies in the international operations and the favorable adjustment of cost estimates associated with the completion of the India pipeline project. Gross profit in the U.A.E. also improved due to decreased raw material costs.

General and administrative expense increased to $12.8 million or 11.4% of net sales in 2009 from $11.0 million or 7.2% of net sales in 2008. The increase in general and administrative expenses was primarily due to increased legal fees associated with collection activities in the U.A.E., increased profit-based management incentive expense and foreign exchange loss.

Selling expense remained level at $2.8 million in 2009. As a percentage of sale, selling expenses decreased to 2.5% of net sales in 2009 from 1.9% of net sales in 2008.

Filtration Products

The timing of large orders can have a material effect on net sales and gross profit from period to period. Pricing on large orders was extremely competitive and therefore resulted in relatively low gross margins in all periods.

The Company's filtration products business is dependent on government regulation of air quality at the federal and state levels. The Company believes that growth in the sale of its filtration products and services will be materially dependent on continued enforcement of environmental laws such as the Clean Air Act. Although there can be no assurance what the ultimate effect of the Clean Air Act will be on the Company's filtration products business, the Company believes the Clean Air Act is likely to have a positive long-term effect on demand for the Company's filtration products and services.

|

|

|

| % Increase (Decrease) | ||||||

(In thousands) | 2010 |

| 2009 |

| 2008 |

| 2010 |

| 2009 |

|

Net sales | $85,133 | $80,819 | $105,390 | 5.3 | % | (23.3 | )% | |||

|

|

|

|

|

| |||||

Gross profit | 10,394 | 6,733 | 11,424 | 54.4 | % | (41.1 | )% | |||

Percentage of net sales | 12.2 | % | 8.3 | % | 10.8 | % |

|

| ||

|

|

|

|

|

| |||||

Loss from operations | (1,335) | (5,290) | (2,936) | 74.8 | % | (80.2 | )% | |||

Percentage of net sales | (1.6 | )% | (6.5 | )% | (2.8 | )% |

|

| ||

17

2010 Compared to 2009

Net sales increased 5.3% to $85.1 million in 2010 from $80.8 million in 2009. Improving business conditions in filtration markets led to increased sales.

Gross margin increased to 12.2% of net sales from 8.3% of net sales in 2009 primarily due to cost containment efforts, improved product mix and the benefit of higher volume leveraged against reduced fixed costs.

In July 2010, the Company announced that the facility in South Africa would close in the third quarter. Expenses

related to the closing were approximately $577 thousand. These expenses are included in cost of goods sold, general and administrative and selling expenses.

General and administrative expenses decreased to $4.8 million or 5.6% of net sales from $5.2 million or 6.4% of net sales in 2009. The decrease is mainly driven by lower foreign exchange loss in 2010 and lower professional expenses partially offset by closing costs related to the facility in South Africa.

Selling expenses increased to $7.0 million from $6.8 million in 2009 primarily as a result of higher commissions for external agents and additional advertising costs. Selling expenses as a percentage of net sales decreased to 8.2% in 2010 from 8.5% of net sales in 2009.

2009 Compared to 2008

Net sales decreased 23.3% to $80.8 million in 2009 from $105.4 million in 2008. Sales declines were the result of lower market demand across all filtration products. Customers delayed their purchases and curtailing infrastructure projects in response to the economic climate.

Gross margin as a percent of net sales decreased to 8.3% in 2009 from 10.8% in 2008, primarily due to the lower pricing driven by excess capacity in the filter bag markets.

General and administrative expenses increased to $5.2 million or 6.4% of net sales from $5.1 million or 4.8% of net sales in 2008. The increase was primarily due to additional professional costs, higher bank fees, and foreign currency exchange loss. These factors were partially offset by personnel reductions.

Selling expense decreased to $6.8 million in 2009 from $7.6 million in 2008. The dollar decrease in selling expense was primarily due to fewer selling personnel, decreased commission expense related to lower sales and decreased advertising expense. Selling expenses as a percentage of net sales increased to 8.5% from 7.2% in the prior-year due to the effect of lower sales.

Industrial Process Cooling Equipment

|

|

|

| % Increase (Decrease) | ||||||

(In thousands) | 2010 |

| 2009 |

| 2008 |

| 2010 |

| 2009 |

|

Net sales | $26,220 | $21,818 | $31,738 | 20.2 | % | (31.3 | )% | |||

|

|

|

|

|

| |||||

Gross profit | 7,044 | 4,977 | 7,919 | 41.5 | % | (37.2 | )% | |||

Percentage of net sales | 26.9 | % | 22.8 | % | 25.0 | % |

|

| ||

|

|

|

|

|

| |||||

Income (loss) from operations | 295 | (1,935) | (1,765) | 115.2 | % | (9.6 | )% | |||

Percentage of net sales | 1.1 | % | (8.9 | )% | (5.6 | )% |

|

| ||

2010 Compared to 2009

Net sales of $26.2 million increased 20.2% from $21.8 million in 2009 due to improving business conditions in the

18

plastic and industrial market sectors.

Gross margin increased to 26.9% of net sales in 2010 from 22.8% of net sales in 2009 primarily due to product mix, lower warranty costs and higher sales volume to spread fixed overhead expenses.

General and administrative expenses decreased to $3.2 million or 12.3% of net sales from $3.5 million or 16.2%

of net sales in 2009. The change in spending was a result of lower compensation expenses and fewer professional expenses partially offset by increased incentive compensation expense.

Selling expenses increased to $3.5 million in 2010 from $3.4 million in 2009. This was primarily driven by higher commission expense due to the increase in net sales partially offset by salary reductions and staff reductions. Selling expense as a percentage of net sales decreased to 13.5% from 15.5% of net sales in 2009.

2009 Compared to 2008

Net sales decreased 31.3% to $21.8 million in 2009 from $31.7 million in 2008. The decrease was primarily due to lower demand for products in all market sectors.

Gross margin decreased to 22.8% in 2009 from 25.0% in 2008, primarily due to lower sales volume and an unfavorable product mix.

General and administrative expense decreased to $3.5 million in 2009 from $4.4 million in 2008. The change in spending was the result of reduced outside product development services and lower compensation and related expenses due to workforce reductions. General and administrative expenses as a percentage of net sales increased to 16.2% from 14.0% in the prior-year due to the effect of lower sales.

Selling expense decreased to $3.4 million in 2009 from $4.1 million in 2009. This was primarily driven by decreased commission expense from lower sales, and a decline in compensation and related expenses due to workforce reductions. Selling expense as a percentage of net sales increased to 15.5% from 13.0% in the prior-year due to the effect of lower sales.

Corporate and Other

2010 Compared to 2009

Net sales of $2.7 million in 2010 decreased from $16.1 million in 2009 due to decreased construction activity. During 2009, the Company worked off existing backlog. New construction has been adversely affected by the current economy. In 2010, the Company obtained new orders for approximately $11.3 million.

General and administrative expenses decreased 5.9% to $9.6 million from $10.2 million in 2009. The decrease was due mainly to lower profit-based management incentive compensation expense, lower SOX404 compliance expense and decreased stock compensation expense partially offset by increased deferred compensation expense. General and administrative expenses as a percentage of consolidated net sales remained the same in 2009 and 2010.

Interest expense decreased to $1.9 million from $2.1 million in 2009 primarily due to lower borrowings and interest rates. Interest income increased to $0.7 million from $0.2 million due to interest earned overseas in the piping systems business.

2009 Compared to 2008

Net sales increased to $16.1 million in 2009 from $14.1 million in 2008 related to the HVAC systems business.

General and administrative expense decreased 0.4% to $10.2 million in 2009 from $10.3 million in 2008, but increased as a percentage of consolidated net sales to 4.4% in 2009 from 3.4% in 2008. The dollar decrease was

19

due mainly to lower profit-based management incentive expense and lower expenses incurred to comply with SOX404, partially offset by increased deferred compensation expense, increased stock compensation expense, and hiring.

Interest expense decreased 32.5% to $1.9 million in 2009 from $2.8 million, net of capitalized interest, in 2008 primarily due to decreased borrowings and lower interest rates.

INCOME TAXES

The Company's worldwide effective income tax rates were (72.2)% , 12.0% , and 17.0% in 2010, 2009, and 2008 , respectively. The effective tax rate in the periods presented was the result of the mix of income earned in multiple tax jurisdictions with various income tax rates. Income earned in the U.A.E. is not subject to any local country income tax. The effective tax rates in 2010 and 2009 were less than the statutory U.S. federal income tax rate, mainly due to the large portion of income earned in the U.A.E.

Several valuation allowances impacted the effective tax rates. In 2010, the Company closed its operations in South Africa and released intercompany liabilities. Related income was offset by existing NOLs for which a prior valuation allowance had been previously provided. This release of liabilities increased the federal NOL. During 2009, the Company established a partial valuation allowance of $0.8 million for the $1.3 million research and development credits, as the Company no longer believed that it was more likely than not that a portion of the research and development credits would be utilized within the next five years.

During 2010, the Company reevaluated the need for a valuation allowance against deferred tax assets and determined that no additional reserve was needed. As of January 31, 2010 and January 31, 2011 , no valuation allowance was deemed necessary on the federal NOL. For additional information, see Note 7 - Income Taxes in the Notes to the Financial Statements.

As of January 31, 2011 , the Company had undistributed earnings of foreign subsidiaries for which deferred taxes have not been provided. The Company intends and has the ability to reinvest these earnings for the foreseeable future outside the U.S. If these amounts were distributed to the U.S., in the form of dividends or otherwise, the Company would be subject to additional U.S. income taxes. Determination of the amount of unrecognized deferred income tax liabilities on these earnings is not practicable because such liability, if any, is dependent on circumstances existing if and when remittance occurs.

A reconciliation of the effective income tax rate to the U.S. Statutory tax rate is as follows:

| 2010 |

| 2009 |

|

Statutory tax rate | 34.0 | % | 34.0 | % |

Differences in foreign tax rate | (60.7 | )% | (54.9 | )% |

Valuation allowance for foreign and state NOLs | (20.8 | )% | 5.4 | % |

State taxes, net of federal benefit | (16.6 | )% | 1.7 | % |

Nontaxable income from the Canadian joint venture | (12.8 | )% | (0.9 | )% |

Cash Surrender Value of deferred compensation plan | (4.9 | )% | (0.3 | )% |

All other, net expense | 9.6 | % | 12.9 | % |

Research tax credit, net of valuation allowance | - | % | 14.1 | % |

Effective tax rate | (72.2 | )% | 12.0 | % |

For further information, see Note 7 - Income Taxes in the Notes to Consolidated Financial Statements.

LIQUIDITY AND CAPITAL RESOURCES

Cash and cash equivalents as of January 31, 2011 were $16.7 million as compared to $8.1 million at January 31, 2010 . The Company's working capital was $58.8 million at January 31, 2011 compared to $53.3 million at

20

January 31, 2010 . Cash provided by operations in 2010 was $8.7 million compared to $34.6 million at January 31, 2010 . Compared to January 31, 2010 trade accounts payable increased $4.8 million, primarily due to the purchase of inventory for production in the filtration business.

Net cash used in investing activities in 2010 included $3.9 million for capital expenditures, primarily for machinery and equipment in the piping systems business. The Company estimates that capital expenditures for 2011 will be approximately $13.9 million, of which the Company may finance capital expenditures through real estate mortgages, equipment financing loans, internally generated funds and its revolving line of credit. The majority of such expenditures relates to foreign growth within the piping systems business.

Debt totaled $39.3 million at January 31, 2011 , an increase of $2.1 million since January 31, 2010 . Net cash provided by financing activities was $3.4 million. Other long-term liabilities of $3.3 million were composed primarily of deferred compensation and accrued pension cost.

The following table summarizes the Company's estimated contractual obligations at January 31, 2011 .

(In thousands) |

| January 31, |

| |||||||||||

Contractual Obligations | Total |

| 2012 |

| 2013 |

| 2014 |

| 2015 |

| 2016 |

| Thereafter |

|

Revolving line domestic (1) | $18,252 | $0 | $0 | $18,252 | $0 | $0 | $0 | |||||||

Mortgages (2) | 19,266 |

| 1,458 |

| 1,160 |

| 932 |

| 935 |

| 934 | 13,847 |

| |

Revolving line foreign | 2,412 |

| 710 |

| 1,312 |

| 15 |

| 15 |

| 15 | 345 |

| |

Term loans (3) | 7,365 |

| 1,723 |

| 1,493 |

| 1,787 |

| 184 |

| 89 | 2,089 |

| |

Subtotal | 47,295 |

| 3,891 |

| 3,965 |

| 20,986 |

| 1,134 |

| 1,038 |

| 16,281 |

|

Capitalized lease obligations | 460 |

| 254 |

| 102 |

| 45 |

| 31 |

| 28 |

| - |

|

Operating lease obligations (4) | 6,500 |

| 1,534 |

| 1,119 |

| 555 |

| 366 |

| 247 | 2,679 |

| |

Projected pension contributions (5) | 3,855 |

| 590 |

| 318 |

| 328 |

| 347 |

| 361 | 1,911 |

| |

Deferred compensation (6) | 5,138 |

| 109 |

| 531 |

| 99 |

| 99 |

| 99 |

| 4,201 |

|

Employment agreements (7) | 101 |

| - |

| - |

| - |

| - |

| - |

| 101 |

|

Uncertain tax position obligations (8) | 1,016 |

| - |

| - |

| - |

| - |

| - |

| 1,016 |

|

Total | $64,365 | $6,378 | $6,035 | $22,013 | $1,977 | $1,773 | $26,189 | |||||||

Notes to Contractual Obligations Table

(1) Interest obligations exclude floating rate interest on debt payable under the domestic revolving line of credit. Based on the amount of such debt at January 31, 2011 , and the weighted average interest rates of 3.16% on that debt at that date, such interest was being incurred at an annual rate of approximately $0.6 million.

(2) Scheduled maturities, including interest.