Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

|

FORM 10-K | |

|

|

x | Annual report pursuant to section

13 or 15(d) of the Securities Exchange Act of 1934. |

|

|

o | Transition report pursuant to Section

13 or 15(d) of the Securities Exchange Act of 1934. |

Commission File No. 1-7707

|

|

|

Medtronic, Inc. |

(Exact name of registrant as specified in charter) |

|

|

|

Minnesota |

| 41-0793183 |

(State of incorporation) |

| (I.R.S. Employer Identification No.) |

710 Medtronic Parkway

Minneapolis, Minnesota 55432

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: (763) 514-4000

Securities registered pursuant to Section 12(b) of the Act:

|

|

Title of each class | Name of each exchange on which registered |

Common stock, par value $0.10 per share | New York Stock Exchange, Inc. |

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer o Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Aggregate market value of voting stock of Medtronic, Inc. held by nonaffiliates of the registrant as of October 28, 2011, based on the closing price of $35.48, as reported on the New York Stock Exchange: approximately $37.5 billion. Shares of Common Stock outstanding on June 22, 2012: 1,025,044,679

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Registrant's Proxy Statement for its 2012 Annual Meeting are incorporated by reference into Part III hereto.

TABLE OF CONTENTS

|

|

|

|

|

|

|

Item |

|

| Description |

|

| Page |

|

|

|

|

| ||

|

| PART I |

|

| ||

1. |

| Business |

| 1 | ||

1A. |

| Risk Factors |

| 17 | ||

1B. |

| Unresolved Staff Comments |

| 26 | ||

2. |

| Properties |

| 26 | ||

3. |

| Legal Proceedings |

| 26 | ||

4. |

| Mine Safety Disclosures |

| 26 | ||

|

| PART II |

|

| ||

5. |

| Market for Medtronic's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities |

| 26 | ||

6. |

| Selected Financial Data |

| 28 | ||

7. |

| Management's Discussion and Analysis of Financial Condition and Results of Operations |

| 29 | ||

7A. |

| Quantitative and Qualitative Disclosures About Market Risk |

| 56 | ||

8. |

| Financial Statements and Supplementary Data |

| 58 | ||

9. |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

| 122 | ||

9A. |

| Controls and Procedures |

| 122 | ||

9B. |

| Other Information |

| 122 | ||

|

| PART III |

|

| ||

10. |

| Directors, Executive Officers, and Corporate Governance |

| 123 | ||

11. |

| Executive Compensation |

| 123 | ||

12. |

| Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters |

| 123 | ||

13. |

| Certain Relationships and Related Transactions, and Director Independence |

| 123 | ||

14. |

| Principal Accounting Fees and Services |

| 123 | ||

|

| PART IV |

|

| ||

15. |

| Exhibits and Financial Statement Schedules |

| 124 | ||

Table of Contents

Investor Information

Annual Meeting and Record Dates

Medtronic, Inc.'s (Medtronic or the Company) Annual Meeting of Shareholders will be held on Thursday, August 23, 2012 at 10:30 a.m., Central Daylight Time at the Company's World Headquarters, 710 Medtronic Parkway, Minneapolis (Fridley), Minnesota. The record date for the Annual Meeting is June 25, 2012 and all shareholders of record at the close of business on that day will be entitled to vote at the Annual Meeting.

Medtronic Website

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 are available through our website ( www.medtronic.com under the "Investors" caption and "Financial Information - SEC Filings" subcaption) free of charge as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (SEC).

Information relating to corporate governance at Medtronic, including our Principles of Corporate Governance, Code of Conduct (including our Code of Ethics for Senior Financial Officers), Code of Business Conduct and Ethics for Members of the Board of Directors and information concerning our executive officers, directors and Board committees (including committee charters) and transactions in Medtronic securities by directors and officers, is available on or through our website at www.medtronic.com under the "Investors" caption and the "Corporate Governance" subcaption.

The information listed above may also be obtained upon request from the Medtronic Investor Relations Department, 710 Medtronic Parkway, Minneapolis (Fridley), Minnesota 55432, USA.

We are not including the information on our website as a part of, or incorporating it by reference into, our Form 10-K.

Available Information

The SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers, including the Company, that file electronically with the SEC. The public can obtain any documents that the Company files with the SEC at http://www.sec.gov . The Company files annual reports, quarterly reports, proxy statements, and other documents with the SEC under the Securities Exchange Act of 1934, as amended (Exchange Act). The public may read and copy any materials that the Company files with the SEC at the SEC's Public Reference Room at 100 F Street, N.E., Room 1580, Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

Stock Transfer Agent and Registrar

Wells Fargo Shareowner Services SM acts as transfer agent and registrar, dividend paying agent, and direct stock purchase plan agent for Medtronic and maintains all shareholder records for the Company. If you are a registered shareholder, you may access your account information online at www.shareowneronline.com . If you have questions regarding the Medtronic stock you own, stock transfers, address or name changes, direct deposit of dividends, lost dividend checks, lost stock certificates, or duplicate mailings, please contact Wells Fargo Shareowner Services SM by writing or calling: Wells Fargo Shareowner Services SM , 1110 Centre Pointe Curve, Suite 101, Mendota Heights, MN 55120 USA, Telephone: 888-648-8154 or 651-450-4064, Fax: 651-450-4033, www.wellsfargo.com/shareownerservices .

Direct Stock Purchase Plan

Medtronic's transfer agent, Wells Fargo Shareowner Services SM , administers the direct stock purchase plan, which is called the Shareowner Service Plus Plan SM . Features of this plan include direct stock purchase and reinvestment of dividends to purchase whole or fractional shares of Medtronic stock. All registered shareholders and potential investors may participate.

Table of Contents

To request information on the Shareowner Service Plus Plan SM , or to enroll in the plan, contact Wells Fargo Shareowner Services SM at 888-648-8154 or 651-450-4064. You may also enroll via the Internet by visiting www.shareowneronline.com and selecting "Direct Purchase Plan."

Trademarks

The following are registered and unregistered trademarks of Medtronic, Inc. and its affiliated companies: Activa® PC and RC, Adapta™, AdaptiveStim™, Advisa®, Advisa® DR MRI™, Advisa MRI™ SureScan®, Arctic Front®, Attain Ability®, CD HORIZON® LEGACY™ (CD HORIZON), CGMS®, Carelink®, Carelink Express™, Conexus®, Consulta®, CoreValve®, DBS Therapies™, Endeavor®, Endurant® Abdominal Stent Graft System, Enlite™, HeartRescueSM, INFUSE® Bone Graft, InterStim® Therapy, MAST®, MasterGraft®, Melody® Transcatheter Pulmonary Valve, MiniMed® Paradigm® Veo™ System (VEO), MiniMed® Revel™ Systems (Revel), NIM® 3.0 Nerve Monitoring System, O-arm® 3.1.2, O-arm® Imaging Systems, OptiVol®, Paradigm®, Pillar® Palatal Implant System, Progenix®, Protecta™, Resolute™, Resolute™ Integrity®, Resting Heart® System, RestoreSensor®™, Reveal®, Revo MRI™ SureScan®, Secura®, SmartShock™ Technology, Solera™, Sprint Fidelis™, StealthStation® S7®, Symplicity® Catheter System, Synergy® Spine 2.0, Talent® Abdominal Aortic Aneurysm, Vision 3D™.

Table of Contents

P ART I

I tem 1. Business

Overview

Medtronic is the global leader in medical technology - alleviating pain, restoring health, and extending life for millions of people around the world. Medtronic was founded in 1949, incorporated as a Minnesota corporation in 1957, and today serves hospitals, physicians, clinicians, and patients in more than 120 countries worldwide. We remain committed to a mission written by our founder more than 50 years ago that directs us "to contribute to human welfare by the application of biomedical engineering in the research, design, manufacture, and sale of products to alleviate pain, restore health, and extend life."

We currently function in two operating segments that manufacture and sell device-based medical therapies. Our operating segments are as follows:

|

|

|

|

| • | Cardiac and Vascular Group | |

|

|

| |

|

| Cardiac Rhythm Disease Management (CRDM) | |

|

|

| |

|

| CardioVascular | |

|

|

| |

| • | Restorative Therapies Group | |

|

|

| |

|

| Spinal | |

|

|

| |

|

| Neuromodulation | |

|

|

| |

|

| Diabetes | |

|

|

| |

|

| Surgical Technologies |

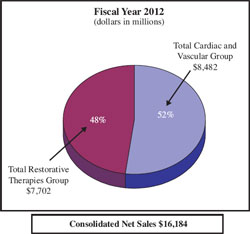

The chart above shows the net sales and percentage of total net sales contributed by each of our operating segments for the fiscal year ended April 27, 2012 (fiscal year 2012). For more information please see Note 19 to the consolidated financial statements in "Item 8. Financial Statements and Supplementary Data" in this Annual Report on Form 10-K.

The results of operations, assets, and liabilities of the Physio-Control business, which were previously presented as a component of the Cardiac and Vascular Group operating segment, are classified as discontinued operations. All information, including the chart above, in this "Item 1. Business" includes only results from continuing operations (excluding Physio-Control) for all periods presented, unless otherwise noted. For further information regarding discontinued operations, see Note 3 to the consolidated financial statements in "Item 8. Financial Statements and Supplementary Data" in this Annual Report on Form 10-K.

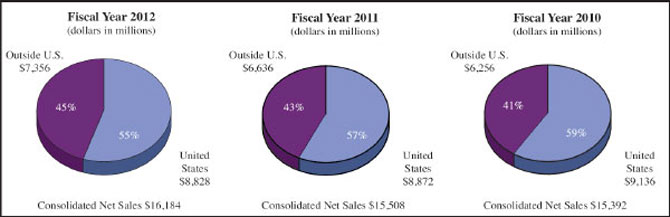

With innovation and market leadership, we have pioneered advances in medical technology in all of our businesses. Over the last five years, our net sales on a compounded annual growth basis have increased more than 5 percent, from $13.186 billion in fiscal year 2008 to $16.184 billion in fiscal year 2012. Our commitment to developing and acquiring new products to treat an expanding array of medical conditions is driven by the following key imperatives:

|

|

|

| • | Providing economic value |

|

|

|

| • | Accelerating globalization |

Our primary customers include hospitals, clinics, third-party health care providers, distributors, and other institutions, including governmental health care programs and group purchasing organizations.

1

Table of Contents

CARDIAC AND VASCULAR GROUP

Cardiac Rhythm Disease Management

CRDM develops, manufactures, and markets products for the diagnosis, treatment, and management of heart rhythm disorders and heart failure, including implantable devices, leads and delivery systems, products for the treatment of atrial fibrillation (AF), and information systems for the management of patients with CRDM devices.

The following are the principal products offered by our CRDM business:

Implantable Cardiac Pacemakers (Pacemakers). A pacemaker is a battery-powered device implanted in the chest that delivers electrical impulses to treat bradycardia, a condition of abnormally slow heart rhythms, usually less than 60 beats per minute, or unsteady heart rhythms that cause symptoms such as dizziness, fainting, fatigue, and shortness of breath. Our latest generation of pacemaker systems is compatible with certain magnetic resonance imaging (MRI) machines. This includes the Revo MRI SureScan with United States (U.S.) Food and Drug Administration (U.S. FDA) approval and the Advisa and Ensura MRI SureScan models with Conformite Europeene (CE) Mark approval. Medtronic also continues to market the Adapta product family, which includes the Adapta, Versa, Sensia, and Relia models.

Implantable Cardioverter Defibrillators (ICDs). An ICD continually monitors the heart and delivers therapy when an abnormal heart rhythm, such as tachyarrhythmia, or rapid heart rhythm, occurs and leads to sudden cardiac arrest. The latest generation of Medtronic ICDs is the Protecta family with SmartShock technology, including the Lead Integrity Alert, an exclusive technology designed to improve the detection of lead fractures. Devices in the ICD family are the Protecta XT, Protecta, Cardia, and Egida models. Medtronic also continues to market the Secura and Maximo II devices. Medtronic ICDs are designed to work with the Sprint Quattro defibrillation leads.

Implantable Cardiac Resynchronization Therapy Devices (CRT-Ds and CRT-Ps). Implantable cardiac resynchronization therapy devices are combined with defibrillation (CRT-D) or are pacing-only (CRT-P). These devices treat heart failure patients by altering the abnormal electrical sequence of cardiac contractions by sending tiny electrical impulses to the lower chambers of the heart to help them beat in a more synchronized fashion. The latest generation of Medtronic CRT-Ds is the Protecta family with SmartShock technology, including Protecta XT and Protecta, and the latest CRT-P devices are Consulta and Syncra. Medtronic also continues to market the Consulta, Cardia, Egida, and Maximo II CRT-D devices. In addition to these devices, Medtronic has a unique offering of left heart leads and delivery catheters with its Attain family of products.

AF Products. AF is a condition in which the atrium quivers instead of pumping blood effectively. Our portfolio of AF products includes the Arctic Front Cardiac CryoAblation Catheter designed specifically to treat paroxysmal AF by performing pulmonary vein isolation. Additionally, we have a CE Mark approved portfolio of anatomically-shaped ablation catheters that use a duty cycled, phased radio frequency energy system for the treatment of permanent and persistent AF. These products are currently being evaluated by the U.S. FDA. We also offer the Reveal XT Insertable Cardiac Monitor, which is designed to identify and quantify episodes of AF.

Diagnostics and Monitoring Devices. The Reveal DX and Reveal XT Insertable Cardiac Monitors are small, memory-stick sized devices that are placed under the skin and can continuously monitor the heart. The devices are used to record the heart's electrical activity before, during, and after transient symptoms such as syncope (i.e., fainting) and palpitations to help provide a diagnosis. The latest generation product, Reveal XT, adds the capability to detect AF and provides long-term trending information to help inform the ongoing management of AF.

Patient Management Tools. We have a number of patient management tools, such as CareLink, Paceart, and CardioSight Service. CareLink enables patients to transmit data from their pacemaker, ICD, CRT-D, or Insertable Cardiac Monitors using a portable monitor that is connected to a standard telephone line or cellular network using the Medtronic M-Link accessory. Paceart organizes and archives data for cardiac devices from major device manufacturers, serving as the central hub for patients' device data. CardioSight Service is an in-clinic data access tool available to physicians treating heart failure patients who have one of several types of Medtronic CRT-Ds or ICDs.

2

Table of Contents

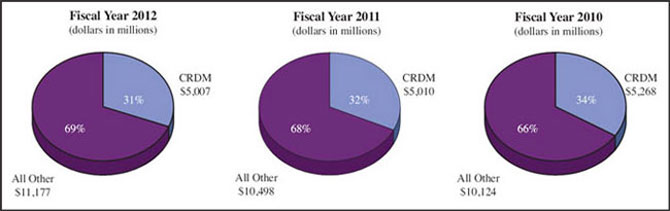

The charts below set forth net sales of our CRDM products as a percentage of our total net sales for each of the last three fiscal years:

Customers and Competitors

The primary medical specialists who use our CRDM products include electrophysiologists, implanting cardiologists, heart failure specialists, and cardiovascular surgeons. Our primary competitors in the CRDM business are St. Jude Medical, Inc. (St. Jude), Boston Scientific Corporation (Boston Scientific), Biotronik, Inc., and Sorin Group.

CardioVascular

CardioVascular is composed of the following three businesses: Coronary, Endovascular and Peripheral, and Structural Heart.

The Coronary business includes therapies to treat coronary artery disease (CAD) and hypertension. The products contained within this business include coronary stents and related delivery systems, along with a broad line of balloon angioplasty catheters, guide catheters, guidewires, diagnostic catheters, and accessories. The following are the principal products offered by our Coronary business:

Percutaneous Coronary Intervention (PCI). PCI encompasses a variety of procedures used to treat patients with CAD. CAD is commonly treated with balloon angioplasty, which is performed to open narrowed heart vessels by inserting a balloon catheter into the vessel and advancing it to the site of the blockage where it is inflated to widen the obstructed vessel. Balloon angioplasty can be followed up with a coronary stent, a support device which works as scaffolding to keep the vessel open following the intervention. Our PCI stent products include our Integrity, Driver, and Micro-Driver bare metal stent systems as well as our Resolute, Resolute Integrity, and Endeavor drug-eluting coronary stent systems.

Renal Denervation. The Symplicity Catheter System is designed to treat chronic uncontrolled hypertension by delivering radio frequency energy through the renal artery walls to denervate the renal nerves, or ablate the nerves lining the renal arteries. This technology has received CE Mark approval and is available in select markets. The Company is currently conducting a U.S. IDE study (HTN-3) for U.S. approval.

The Endovascular and Peripheral business is comprised of a comprehensive line of products and therapies to treat abdominal and thoracic aortic aneurysms and peripheral vascular disease (PVD). Our products include endovascular stent graft systems, embolic protection systems, and stent systems for the treatment of narrowed iliac arteries. The following are the principal products offered by our Endovascular and Peripheral business:

Endovascular Stent Grafts. An endovascular stent graft is a minimally invasive device to repair an aortic aneurysm, which is a weakened and bulging area in the aorta, the major blood vessel that feeds blood to the body. Our products are designed to treat aortic aneurysms in either the abdomen (AAA) or thoracic (TAA) regions of the aorta. Our product line includes a range of endovascular stent grafts including the market-leading Endurant, Talent and AneuRx abdominal stent grafts for minimally invasive AAA and the Talent, Talent Captivia, Valiant and Valiant Captivia (available in select markets outside the U.S.) stent grafts for minimally invasive TAA repair.

3

Table of Contents

Peripheral Vascular Intervention (PVI). PVI encompasses a variety of procedures to treat patients with PVD, a narrowing or blockage of vessels outside the heart which impedes blood supply to the brain, kidneys, legs, and other vital organs. Similar to CAD, PVD is commonly treated with balloon angioplasty which can be followed up with a peripheral stent. Our PVI products include the Complete SE stent, Assurant Cobalt Iliac Stent, Pioneer Plus lumen re-entry device, percutaneous angioplasty balloons, drug-eluting balloons for coronary and lower-extremity vessels, as well as embolic protection devices and stents for the treatment of carotid artery disease.

The Structural Heart business offers a comprehensive line of products and therapies to treat a variety of heart valve disorders. Our products include products for the repair and replacement of heart valves, perfusion systems, positioning and stabilization systems for beating heart revascularization surgery, and surgical ablation products. The following are our principal products offered by our Structural Heart business:

Heart Valves. We offer a complete line of surgical valve replacement and repair products for damaged or diseased heart valves. Our replacement products include both tissue and mechanical valves. Our replacement tissue valve product offerings include the Mosaic bioprosthetic stented, Freestyle stentless, Hancock II stented valves, and 3f Biological tissue valve. Our mechanical valves include the Open Pivot valve. Our valve repair products include the Duran Flexible and CG Future Band, the CG Composite Annuloplasty Systems, the Profile 3D Annuloplasty Ring, the Simulus Ring portfolio, and the Tri-Ad Annuloplasty Ring.

Transcatheter Heart Valves. Transcatheter valve (TCV) technology represents a less invasive means to treat heart valve disease and is designed to allow physicians to deliver replacement valves via a catheter through the body's cardiovascular system, eliminating the need to open the chest. Our TCVs include the Melody pulmonary valve and the CoreValve aortic valve. The Melody has received CE Mark approval as well as U.S. FDA approval under a Humanitarian Device Exemption (HDE). CoreValve has received CE Mark approval and is currently being clinically studied in the U.S. for approval.

Arrested Heart Surgery. In conventional coronary artery bypass graft procedures and heart valve surgery, the patient's heart is temporarily stopped, or arrested. The patient is placed on a circulatory support system that temporarily functions as the patient's heart and lungs and provides blood flow to the body. We offer a complete line of blood-handling products that form this circulatory support system and maintain and monitor blood circulation and coagulation status, oxygen supply, and body temperature during arrested heart surgery.

Beating Heart Surgery. To assist physicians performing beating heart surgery, we offer positioning and stabilization technologies. These technologies include our Starfish 2 and Urchin heart positioners, which are designed to work in concert with our family of Octopus tissue stabilizers.

Surgical Ablation. Our Cardioblate surgical ablation system, which includes the Cardioblate LP surgical ablation system, the Cardioblate navigator tissue dissector, and the Cardioblate Cryoflex system, allows cardiac surgeons to create ablation lines during cardiac surgery.

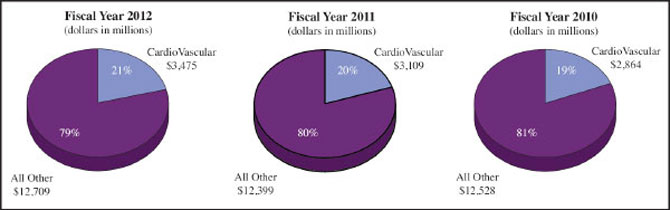

The charts below set forth net sales of our CardioVascular products as a percentage of our total net sales for each of the last three fiscal years:

4

Table of Contents

Customers and Competitors

The primary medical specialists who use our Coronary products are interventional cardiologists, while products in our Endovascular and Peripheral business may be used by interventional radiologists, vascular surgeons, cardiac surgeons, and interventional cardiologists. The principal medical specialists who use our Structural Heart products are cardiac surgeons and interventional cardiologists. Our primary competitors in the Coronary business are Abbott Laboratories (Abbott), Boston Scientific, and Johnson & Johnson. Our primary competitors in the Endovascular and Peripheral business are Cook, Inc., W. L. Gore & Associates, Inc. (Gore), Endologix, Inc., C.R. Bard, Inc., and Johnson & Johnson. Our primary competitors in the Structural Heart business are Edwards LifeSciences Corporation, St. Jude, Terumo Medical Corporation, and Sorin Group.

RESTORATIVE THERAPIES GROUP

Spinal

Our Spinal business develops, manufactures, and markets a comprehensive line of medical devices and implants used in the treatment of the spine and musculoskeletal system. Our products and therapies treat a variety of conditions affecting the spine, including degenerative disc disease, spinal deformity, spinal tumors, fractures of the spine, and stenosis. Our Spinal business also provides biologic solutions for the dental and orthopedic markets.

We offer some of the industry's broadest lines of devices, including a wide range of sophisticated internal spinal stabilization devices, instruments, and biomaterials used in the treatment of spinal conditions. Our Spinal products are used in spinal fusion of both the thoracolumbar region, referring to the mid to lower vertebrae, as well as of the cervical region, or upper spine and neck vertebrae. Products used to treat spinal conditions include rods, pedicle screws, hooks, plates, and interbody devices, as well as biologics products, primarily bone growth substitutes including bone graft extenders and structural allografts such as dowels and wedges. In concert with our Surgical Technologies business, we offer unique and highly differentiated navigation, neuromonitoring, and power technologies designed for spine procedures.

The following are the principal products offered by our Spinal business:

Thoracolumbar Products. Products used to treat conditions in this region of the spine include the CD HORIZON SOLERA and LEGACY Systems, the TSRH 3Dx System, and the T2 Altitude System. In addition, Medtronic offers a number of products that facilitate less invasive thoracolumbar surgeries, including the CD HORIZON SOLERA SEXTANT and LONGITUDE Percutaneous Fixation Systems, the Direct Lateral Access System and corresponding CLYDESDALE Interbody Implant, Xpander II Balloon Kyphoplasty product for vertebral compression fractures, the METRx System, and the NIM-ECLIPSE Spinal System.

Cervical Products. Products used to treat conditions in this region of the spine include the ATLANTIS VISION ELITE Anterior Cervical Plate System, the VERTEX SELECT Reconstruction System, and the PRESTIGE and BRYAN Cervical Discs.

Biologics Products. Products in our Biologics platform include INFUSE Bone Graft (InductOs in the European Union (EU)), which contains a recombinant human bone morphogenetic protein, rhBMP-2, for spinal, trauma, and oral maxillofacial applications, Demineralized Bone Matrix (DBM) products, including MagniFuse, Grafton/Grafton Plus, and PROGENIX, and the MASTERGRAFT family of synthetic bone graft products – Matrix, Putty, and Granules.

5

Table of Contents

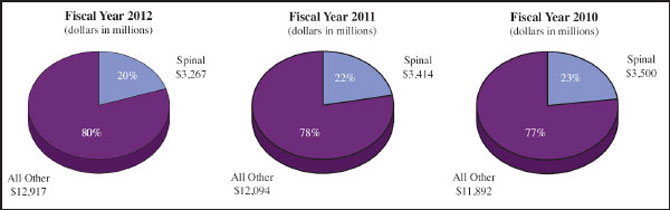

The charts below set forth net sales of our Spinal products as a percentage of our total net sales for each of the last three fiscal years:

Customers and Competitors

The primary medical specialists who use our Spinal products are spinal surgeons, orthopedic surgeons, neurosurgeons, and interventional radiologists. Competitors in this business include DePuy Spine, Inc., Synthes, Inc., Stryker Corporation, NuVasive, Inc., Globus Medical, Inc., Zimmer, Inc., Alphatec Spine, Inc., Orthofix International N.V., Biomet, Inc., and over 200 smaller competitors and physician-owned companies. Johnson & Johnson, the parent company for DePuy Spine, Inc., acquired Synthes, Inc. in June 2012.

Neuromodulation

Our Neuromodulation business develops, manufactures, and markets medical devices for the treatment of chronic pain, movement disorders, psychological disorders, and urological, fecal, and gastroenterological disorders.

The following are the principal products offered by our Neuromodulation business:

Neurostimulators for Chronic Pain. Spinal cord stimulation uses a surgically implanted medical device, similar to a cardiac pacemaker, to deliver mild electrical signals to the epidural space. We have the largest portfolio of neurostimulation systems in the industry, including rechargeable and non-rechargeable devices and a large selection of leads used to treat chronic back and leg pain. Our portfolio of products includes the RestoreSensor (rechargeable), with our proprietary AdaptiveStim technology, as well as the RestoreULTRA (rechargeable), RestoreADVANCED (rechargeable), and PrimeADVANCED (non-rechargeable) neurostimulation systems.

Implantable Drug Delivery Systems. The SynchroMed II Programmable Infusion System delivers small quantities of drug directly into the intrathecal space surrounding the spinal cord. These devices are used to treat chronic, intractable pain and severe spasticity associated with cerebral palsy, multiple sclerosis, spinal cord and traumatic brain injuries, and stroke.

Deep Brain Stimulation (DBS) Systems. DBS uses a surgically implanted medical device, similar to a cardiac pacemaker, to deliver carefully controlled electrical stimulation to precisely targeted areas in the brain. It works by electrically stimulating specific structures that control movement and muscle function. DBS is used to treat the symptoms of movement disorders such as Parkinson's disease, epilepsy (certain countries outside the U.S. only), essential tremor, and dystonia, as well as psychiatric disorders such as obsessive-compulsive disorder. Our family of Activa Neurostimulators for DBS includes Activa SC (single-channel primary cell), Activa PC (dual channel primary cell), and Activa RC (dual channel rechargeable).

Urology, Fecal, & Gastroenterology Devices. Sacral nerve stimulation uses a surgically implanted medical device, similar to a cardiac pacemaker, to offer long-term control of urinary control and bowel control symptoms through modulation of the nerve activity by focusing on the nerves that control the pelvic floor and lower urinary tract. Our therapeutic portfolio for urology and gastroenterology includes the InterStim Therapy System, which treats the symptoms of overactive bladder, urinary retention, and chronic fecal incontinence, and the Enterra Therapy System for the treatment of chronic nausea and vomiting caused by gastroparesis of diabetic or idiopathic origin for drug refractory patients.

6

Table of Contents

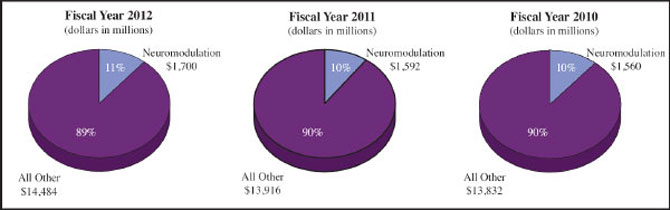

The charts below set forth net sales of our Neuromodulation products as a percentage of our total net sales for each of the last three fiscal years:

Customers and Competitors

The primary medical specialists who use our pain management and movement disorder products are neurosurgeons, neurologists, pain management specialists, anesthesiologists, physiatrists, and orthopedic spine surgeons. Our primary competitors in this business are Boston Scientific and St. Jude.

The primary medical specialists who use our gastroenterology and urology products are urologists, urogynecologists, gastroenterologists, and colorectal surgeons. Our primary competitors in this business are Urologix, Inc. and Allergan.

Diabetes

Our Diabetes business develops, manufactures, and markets advanced, integrated diabetes management solutions that include insulin pump therapy, continuous glucose monitoring systems, and therapy management software.

The following are the principal products offered by our Diabetes business:

Integrated Diabetes Management Solutions. We have the only integrated insulin pump and continuous glucose monitoring (CGM) system in the U.S. Outside the U.S., we offer our Paradigm Veo System, an integrated system that includes a Low Glucose Suspend feature that automatically suspends insulin delivery when glucose levels become too low. In the U.S., we offer the Paradigm Revel System, which incorporates new CGM features including predictive alerts that can give early warning to people with diabetes so they can take action to prevent dangerous high or low glucose events.

Professional CGM. Medtronic offers physicians a Professional CGM product called the iPro CGM and iPro2 Professional CGM. Physicians send patients home wearing the iPro recorder to capture glucose data, which is later uploaded in a physician's office to reveal glucose patterns and potential problems, including hyperglycemic and hypoglycemic episodes, which can lead to more informed treatment decisions.

CareLink Therapy Management Software. We offer web-based therapy management software solutions, including CareLink Personal software for patients and CareLink Pro software, to help patients and their health care providers control their diabetes.

7

Table of Contents

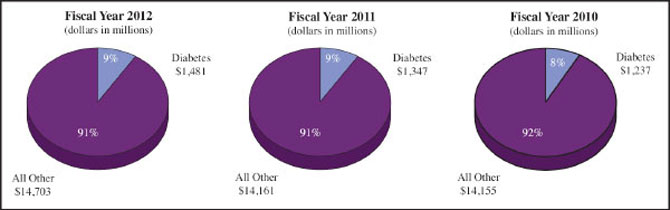

The charts below set forth net sales of our Diabetes products as a percentage of our total net sales for each of the last three fiscal years:

Customers and Competitors

The primary medical specialists who use and/or prescribe our Diabetes products are endocrinologists, diabetologists, and internists. Our primary competitors for diabetes products are DexCom, Inc., Insulet Corporation, Johnson & Johnson, and Roche Ltd.

Surgical Technologies

Our Surgical Technologies business develops, manufactures, and markets products and therapies to treat diseases and conditions of the ear, nose, and throat (ENT) and certain neurological disorders. In addition, the business develops, manufactures, and markets image-guided surgery and intra-operative imaging systems that facilitate surgical planning during precision cranial, spinal, sinus, and orthopedic surgeries. In August 2011, we completed the acquisition of two privately-held companies, PEAK Surgical, Inc. (PEAK) and Salient Surgical Technologies, Inc. (Salient), that are focused on advanced energy devices. PEAK is a recognized leader in the emerging field of advanced energy surgical incision technology, and Salient is a leader in the advanced energy category for haemostatic sealing of soft tissue and bone.

The following are the principal products offered by our Surgical Technologies business:

ENT. The following products treat ENT diseases and conditions: NIM Nerve Monitoring Systems, Fusion ENT Navigation System, Hydrodebrider Endoscopic Sinus Irrigation System, Meniett Device for Meniere's Disease, Pillar Procedure for Snoring and Sleep Apnea, and Repose System for Obstructive Sleep Apnea.

Neurological Technologies. The following products treat certain neurological disorders and conditions: Midas Rex Spine Shaver, the Midas Rex MR7 Pneumatic Platform, the Midas Rex Legend EHS High Speed Surgical Drill, the Strata Family of Adjustable Valves for the treatment of Hydrocephalus, Duet External Drainage & Monitoring System, the IPC System, and the Subdural Evacuating Port System.

Navigation. The following products are used in cranial, spinal, sinus, and orthopedic surgeries: the StealthStation S7 Navigation and i7 Integrated Navigation Systems, the O-Arm 2D/3D Surgical Imaging System, and the PoleStar Surgical MRI System.

Advanced Energy. The following products make up the Advanced Energy business: PEAK Surgery System, a tissue dissection system that consists of the PEAK PlasmaBlade and the PULSAR Generator and is cleared for use in a variety of settings, including ENT, plastic reconstructive and general surgery; and the Aquamantys System, which uses patented Transcollation technology to provide haemostatic sealing of soft tissue and bone and is cleared for use in a variety of surgical procedures, including orthopedic surgery, spine, solid organ resection and thoracic procedures.

8

Table of Contents

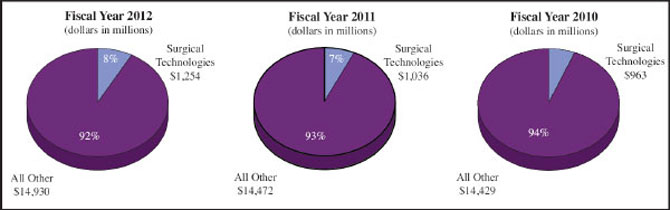

The charts below set forth net sales of our Surgical Technologies products as a percentage of our total net sales for each of the last three fiscal years:

Customers and Competitors

The primary customers for our products relating to ENT diseases and conditions are ENT surgeons and the hospitals and clinics where they perform surgery. Competitors in this part of our Surgical Technologies business include Gyrus ACMI (a group company of Olympus Corporation), Stryker Corporation, and Johnson & Johnson.

The primary customers for our neurosurgical products are neurosurgeons, spinal surgeons, and the hospitals and clinics where they perform surgery. Competitors include Johnson & Johnson, Stryker Corporation, and Integra LifeSciences Holdings Corporation.

The primary customers for our image-guided surgery and intra-operative imaging systems are hospitals and clinics. Competitors include BrainLAB, Inc., Stryker Corporation, GE Healthcare, Siemens Medical Solutions USA, Inc., and Philips Medical Systems.

The primary customers for our advanced energy products are orthopedic surgeons, spinal surgeons, neurosurgeons, and the hospitals and clinics where they perform surgery. Competitors include Covidien, Johnson & Johnson, and ArthroCare Corporation.

Research and Development

The markets in which we participate are subject to rapid technological advances. Constant improvement of products and introduction of new products is necessary to maintain market leadership. Our research and development (R&D) efforts are directed toward maintaining or achieving technological leadership in each of the markets we serve in order to help ensure that patients using our devices and therapies receive the most advanced and effective treatment possible. We are committed to developing technological enhancements and new indications for existing products, as well as less invasive and new technologies to address unmet patient needs and to help reduce patient care costs and length of hospital stays. We have not engaged in significant customer or government-sponsored research.

During fiscal years 2012, 2011, and 2010, we spent $1.490 billion (9.2 percent of net sales), $1.472 billion (9.5 percent of net sales), and $1.424 billion (9.3 percent of net sales) on R&D, respectively. Our R&D activities include improving existing products and therapies, expanding their indications and applications for use, and developing new products. During fiscal year 2012, we have focused on optimizing innovation, including improving our R&D productivity. We have made efforts to reallocate resources into driving growth in emerging markets and in evidence generation for our growth platforms, and are assessing our R&D programs based on their ability to deliver economic value to the customer.

Acquisitions and Investments

Our strategy to provide a broad range of therapies to restore patients to fuller, healthier lives requires a wide variety of technologies, products, and capabilities. The rapid pace of technological development in the medical industry and the specialized expertise required in different areas of medicine make it difficult for one company alone to develop a broad portfolio of technological solutions. In addition to internally generated growth through our R&D efforts, historically we have relied, and expect to continue to rely, upon acquisitions, investments, and alliances to provide access to new technologies both in areas served by our existing businesses as well as in new areas and markets.

9

Table of Contents

We expect to make future investments or acquisitions where we believe that we can stimulate the development of, or acquire new technologies and products to further our strategic objectives and strengthen our existing businesses. Mergers and acquisitions of medical technology companies are inherently risky and no assurance can be given that any of our previous or future acquisitions will be successful or will not materially adversely affect our consolidated results of operations, financial condition, and/or cash flows.

Fiscal Year 2012

On August 31, 2011, we acquired Salient. Salient develops and markets devices for haemostatic sealing of soft tissue and bone incorporating advanced energy technology. Salient's devices are used in a variety of surgical procedures including orthopedic surgery, spine, open abdominal, and thoracic procedures. Total consideration for the transaction was approximately $497 million. We had previously invested in Salient and held an 8.9 percent ownership position in the company. In connection with the acquisition of Salient, we recognized a gain on our previously-held investment of $32 million, which was recorded within acquisition-related items in the consolidated statement of earnings in the second quarter of fiscal year 2012. Net of this ownership position, the transaction value was approximately $452 million.

On August 31, 2011, we acquired PEAK. PEAK develops and markets tissue dissection devices incorporating advanced energy technology. Total consideration for the transaction was approximately $113 million. We had previously invested in PEAK and held an 18.9 percent ownership position in the company. In connection with the acquisition of PEAK, we recognized a gain on our previously-held investment of $6 million, which was recorded within acquisition-related items in the consolidated statement of earnings in the second quarter of fiscal year 2012. Net of this ownership position, the transaction value was approximately $96 million.

Fiscal Year 2011

On January 13, 2011, we acquired privately-held Ardian, Inc. (Ardian). We had previously invested in Ardian and held an 11.3 percent ownership position. Ardian develops catheter-based therapies to treat uncontrolled hypertension and related conditions. Total consideration for the transaction was $1.020 billion which includes the estimated fair value of revenue-based contingent consideration of $212 million. The terms of the transaction included an upfront cash payment of $717 million, excluding our pro-rata share in Ardian, plus potential future commercial milestone payments equal to the annual revenue growth beginning in fiscal year 2012 through the end of our fiscal year 2015. We recognized a gain of $85 million on our previously-held investment, which was recorded within acquisition-related items in the consolidated statement of earnings in the third quarter of fiscal year 2011.

On November 16, 2010, we acquired Osteotech, Inc. (Osteotech). Osteotech develops innovative biologic products for regenerative medicine. Under the terms of the agreement, we paid shareholders $6.50 per share in cash for each share of Osteotech common stock that they owned. Total consideration for the transaction was approximately $123 million.

On August 12, 2010, we acquired ATS Medical, Inc. (ATS Medical). ATS Medical is a leading developer, manufacturer, and marketer of products and services focused on cardiac surgery, including heart valves and surgical cryoablation technology. Under the terms of the agreement, ATS Medical shareholders received $4.00 per share in cash for each share of ATS Medical common stock that they owned. Total consideration for the transaction was approximately $394 million which included the assumption of existing ATS Medical debt and acquired contingent consideration.

On June 2, 2010, we acquired substantially all of the assets of Axon Systems, Inc. (Axon), a privately-held company. Prior to the acquisition, we distributed a large portion of Axon's products. This acquisition has helped us bring to market the next generation of surgeon-directed and professionally supported spinal and cranial neuromonitoring technologies and expand the availability of these technologies. Total consideration for the transaction, net of cash acquired, was $62 million, which included the settlement of existing Axon debt.

10

Table of Contents

Fiscal Year 2010

On April 21, 2010, we acquired Invatec S.p.A. (Invatec), a developer of innovative medical technologies for the interventional treatment of cardiovascular disease. Under the terms of the agreement, the transaction included an initial up-front payment of $350 million, which included the assumption and settlement of existing Invatec debt. The agreement also included potential additional payments of up to $150 million contingent upon achievement of certain revenue and product development milestones. During fiscal year 2012, we paid an aggregate of $141 million upon achievement of these milestones.

Patents and Licenses

We rely on a combination of patents, trademarks, copyrights, trade secrets, and nondisclosure and non-competition agreements to establish and protect our proprietary technology. We have filed and obtained numerous patents in the U.S. and abroad, and regularly file patent applications worldwide in our continuing effort to establish and protect our proprietary technology. U.S. patents typically have a 20-year term from the application date while patent protection outside the U.S. varies from country to country. In addition, we have entered into exclusive and non-exclusive licenses relating to a wide array of third-party technologies. We have also obtained certain trademarks and tradenames for our products to distinguish our genuine products from our competitors' products, and we maintain certain details about our processes, products, and strategies as trade secrets. Our efforts to protect our intellectual property and avoid disputes over proprietary rights have included ongoing review of third-party patents and patent applications. For additional information see "Item 1A. Risk Factors" and Note 17 to the consolidated financial statements in "Item 8. Financial Statements and Supplementary Data" in this Annual Report on Form 10-K.

Markets and Distribution Methods

We sell most of our medical devices through direct sales representatives in the U.S. and a combination of direct sales representatives and independent distributors in markets outside the U.S. The three largest markets for our medical devices are the U.S., Western Europe, and Japan. Emerging markets are an area of increasing focus and opportunity as we believe they remain underpenetrated.

Our marketing and sales strategy is focused on rapid, cost-effective delivery of high-quality products to a diverse group of customers worldwide - including physicians, hospitals, other medical institutions, and group purchasing organizations. To achieve this objective, we organize our marketing and sales teams around physician specialties. This focus enables us to develop highly knowledgeable and dedicated sales representatives who are able to foster strong relationships with physicians and other customers and enhance our ability to cross-sell complementary products. We believe that we maintain excellent working relationships with physicians and others in the medical industry that enable us to gain a detailed understanding of therapeutic and diagnostic developments, trends, and emerging opportunities and respond quickly to the changing needs of physicians and patients. We attempt to enhance our presence in the medical community through active participation in medical meetings and by conducting comprehensive training and educational activities. We believe that these activities contribute to physician expertise.

In keeping with the increased emphasis on cost-effectiveness in health care delivery, the current trend among hospitals and other customers of medical device manufacturers is to consolidate into larger purchasing groups to enhance purchasing power. As a result, transactions with customers have become increasingly significant and more complex. This enhanced purchasing power may also lead to pressure on pricing and increased use of preferred vendors. Our customer base continues to evolve to reflect such economic changes across the geographic markets we serve. We are not dependent on any single customer for more than 10 percent of our total net sales.

Competition and Industry

We compete in both the therapeutic and diagnostic medical markets in more than 120 countries throughout the world. These markets are characterized by rapid change resulting from technological advances and scientific discoveries. In the product lines in which we compete, we face a mixture of competitors ranging from large manufacturers with multiple business lines to small manufacturers that offer a limited selection of products. In addition, we face competition from providers of alternative medical therapies such as pharmaceutical companies.

11

Table of Contents

Major shifts in industry market share have occurred in connection with product problems, physician advisories, and safety alerts, reflecting the importance of product quality in the medical device industry. In addition, in the current environment of managed care, economically motivated customers, consolidation among health care providers, increased competition and declining reimbursement rates, we have been increasingly required to compete on the basis of price. In order to continue to compete effectively, we must continue to create or acquire advanced technology, incorporate this technology into proprietary products, obtain regulatory approvals in a timely manner, maintain high-quality manufacturing processes, and successfully market these products.

Worldwide Operations

For financial reporting purposes, net sales and long-lived assets attributable to significant geographic areas are presented in Note 19 to the consolidated financial statements in "Item 8. Financial Statements and Supplementary Data" in this Annual Report on Form 10-K.

Impact of Business Outside of the U.S.

Our operations in countries outside the U.S. are accompanied by certain financial and other risks. Relationships with customers and effective terms of sale vary by country, often with longer-term receivables than are typical in the U.S. Inventory management is an important business concern due to the potential for obsolescence and long lead times from sole source providers. Foreign currency exchange rate fluctuations can affect revenues, net of expenses, and cash flows from operations outside the U.S. We use operational and economic hedges, as well as currency exchange rate derivative contracts to manage the impact of currency exchange rate changes on earnings and cash flow. See "Item 7A. Quantitative and Qualitative Disclosures About Market Risk" and Note 10 to the consolidated financial statements in "Item 8. Financial Statements and Supplementary Data" in this Annual Report on Form 10-K. In addition, the repatriation of certain earnings of subsidiaries outside the U.S. may result in substantial U.S. tax cost.

Production and Availability of Raw Materials

We manufacture most of our products at 38 manufacturing facilities located in various countries throughout the world. The largest of these manufacturing facilities are located in Arizona, California, Colorado, Connecticut, Florida, Indiana, Massachusetts, Minnesota, New Jersey, Texas, Puerto Rico, Canada, France, Germany, Ireland, Italy, Mexico, The Netherlands, Singapore, and Switzerland. We purchase many of the components and raw materials used in manufacturing these products from numerous suppliers in various countries. For reasons of quality assurance, sole source availability, or cost effectiveness, certain components and raw materials are available only from a sole supplier. We work closely with our suppliers to help ensure continuity of supply while maintaining high quality and reliability. Due to the U.S. FDA's requirements regarding manufacturing of our products, we may not be able to quickly establish additional or replacement sources for certain components or materials. Generally, we have been able to obtain adequate supplies of such raw materials and components. However, the reduction or interruption in supply, and an inability to develop alternative sources for such supply, could adversely affect our operations.

Working Capital Practices

Our goal is to carry sufficient levels of inventory to ensure adequate supply of raw materials from suppliers and meet the product delivery needs of our customers. We also provide payment terms to customers in the normal course of business and rights to return product under warranty to meet the operational demands of our customers.

12

Table of Contents

Employees

On April 27, 2012, we employed approximately 45,000 employees (including full-time equivalent employees). Our employees are vital to our success. We believe we have been successful in attracting and retaining qualified personnel in a highly competitive labor market due to our competitive compensation and benefits, and our rewarding work environment.

Seasonality

Worldwide sales, including U.S. sales, do not reflect any significant degree of seasonality.

Government Regulation and Other Considerations

Our medical devices are subject to regulation by numerous government agencies, including the U.S. FDA and comparable agencies outside the U.S. To varying degrees, each of these agencies requires us to comply with laws and regulations governing the development, testing, manufacturing, labeling, marketing, and distribution of our medical devices.

Authorization to commercially distribute a new medical device in the U.S. is generally received in one of two ways. The first, known as pre-market notification or the 510(k) process, requires us to demonstrate that our new medical device is substantially equivalent to a legally marketed medical device. In this process, we must submit data that supports our equivalence claim. If human clinical data is required, it must be gathered in compliance with U.S. FDA investigational device exemption regulations. We must receive an order from the U.S. FDA finding substantial equivalence to another legally marketed medical device before we can commercially distribute the new medical device. Modifications to cleared medical devices can be made without using the 510(k) process if the changes do not significantly affect safety or effectiveness. A very small number of our devices are exempt from pre-market review.

The second, more rigorous process, known as pre-market approval (PMA), requires us to independently demonstrate that the new medical device is safe and effective. We do this by collecting data regarding design, materials, bench and animal testing, and human clinical data for the medical device. The U.S. FDA will authorize commercial distribution if it determines there is reasonable assurance that the medical device is safe and effective. This determination is based on the benefit outweighing the risk for the population intended to be treated with the device. This process is much more detailed, time-consuming, and expensive than the 510(k) process. A third, seldom used, process for approval exists for products intended for orphan populations, which is less than 4,000 patients per year in the U.S. This exemption is similar to the PMA process; however, a full showing of product effectiveness from large clinical trials is not required. The threshold for approving these products is probable benefit and safety.

Both before and after a product is commercially released, we have ongoing responsibilities under U.S. FDA regulations. The U.S. FDA reviews design and manufacturing practices, labeling and record keeping, and manufacturers' required reports of adverse experiences and other information to identify potential problems with marketed medical devices. We are also subject to periodic inspection by the U.S. FDA for compliance with the U.S. FDA's quality system regulations, which govern the methods used in, and the facilities and controls used for, the design, manufacture, packaging, and servicing of all finished medical devices intended for human use. In addition, the U.S. FDA and other U.S. regulatory bodies (including the Federal Trade Commission, the Office of the Inspector General of the Department of Health and Human Services, the Department of Justice (DOJ), and various state Attorneys General) monitor the manner in which we promote and advertise our products. Although surgeons are permitted to use their medical judgment to employ medical devices for indications other than those cleared or approved by the U.S. FDA, we are prohibited from promoting products for such "off-label" uses, and can only market our products for cleared or approved uses. If the U.S. FDA were to conclude that we are not in compliance with applicable laws or regulations, or that any of our medical devices are ineffective or pose an unreasonable health risk, the U.S. FDA could require us to notify health professionals and others that the devices present unreasonable risks of substantial harm to the public health, order a recall, repair, replacement, or refund of such devices, detain or seize adulterated or misbranded medical devices, or ban such medical devices. The U.S. FDA may also impose operating restrictions, enjoin and/or restrain certain conduct resulting in violations of applicable law pertaining to medical devices, and assess civil or criminal penalties against our officers, employees, or us. The U.S. FDA may also recommend prosecution to the DOJ. Conduct giving rise to civil or criminal penalties may also form the basis for private civil litigation by third-party payers or other persons allegedly harmed by our conduct.

13

Table of Contents

The U.S. FDA, in cooperation with U.S. Customs and Border Protection (CBP), administers controls over the import of medical devices into the U.S. The CBP imposes its own regulatory requirements on the import of our products, including inspection and possible sanctions for noncompliance. Medtronic is also subject to foreign trade controls administered by several U.S. government agencies, including the Bureau of Industry and Security within the Commerce Department and the Office of Foreign Assets Control within the Treasury Department.

The U.S. FDA also administers certain controls over the export of medical devices from the U.S. International sales of our medical devices that have not received U.S. FDA approval are subject to U.S. FDA export requirements. Many countries outside the U.S. to which we export medical devices also subject such medical devices to their own regulatory requirements. Frequently, we obtain regulatory approval for medical devices in countries outside the U.S. first because their regulatory approval is faster than that of the U.S. FDA. However, as a general matter, non-U.S. regulatory requirements are becoming increasingly common and more stringent.

In the EU, a single regulatory approval process exists, and conformity with the legal requirements is represented by the CE Mark. To obtain a CE Mark, defined products must meet minimum standards of performance, safety, and quality (i.e., the essential requirements), and then, according to their classification, comply with one or more of a selection of conformity assessment routes. A notified body assesses the quality management systems of the manufacturer and the product conformity to the essential and other requirements within the medical device directive. Medtronic is subject to inspection by notified bodies for compliance. The competent authorities of the EU countries, generally in the form of their ministries or departments of health, oversee the clinical research for medical devices and are responsible for market surveillance of products once they are placed on the market. We are required to report device failures and injuries potentially related to product use to these authorities in a timely manner. Various penalties exist for non-compliance with the laws transcribing the medical device directives.

To be sold in Japan, most medical devices must undergo thorough safety examinations and demonstrate medical efficacy before they are granted approval, or "shonin." The Japanese government, through the Ministry of Health, Labour, and Welfare (MHLW), regulates medical devices under the Pharmaceutical Affairs Law (PAL). Oversight for medical devices is conducted with participation by the Pharmaceutical and Medical Devices Agency (PMDA), a quasi-government organization performing many of the review functions for MHLW. Penalties for a company's noncompliance with PAL could be severe, including revocation or suspension of a company's business license and criminal sanctions. MHLW and PMDA also assess the quality management systems of the manufacturer and the product conformity to the requirements of the PAL. Medtronic is subject to inspection for compliance by these agencies.

The process of obtaining approval to distribute medical products is costly and time-consuming in virtually all of the major markets where we sell medical devices. We cannot assure that any new medical devices we develop will be approved in a timely or cost-effective manner or approved at all.

Federal and state laws protect the confidentiality of certain patient health information, including patient medical records, and restrict the use and disclosure of patient health information by health care providers. In particular, in April 2003, the U.S. Department of Health and Human Services (HHS) published patient privacy rules under the Health Insurance Portability and Accountability Act of 1996 (HIPAA) and, in April 2005, published security rules for protected health information. The HIPAA privacy and security rules govern the use, disclosure, and security of protected health information by "Covered Entities," which are health care providers that submit electronic claims, health plans, and health care clearinghouses. In 2009, Congress passed the HITECH Act, which modified certain provisions of the HIPAA privacy and security rules for Covered Entities and their Business Associates (which is anyone that performs a service on behalf of a Covered Entity involving the use or disclosure of protected health information and is not a member of the Covered Entity's workforce). These included directing HHS to publish more specific security standards, and increasing breach notification requirements, as well as tightening certain aspects of the privacy rules. HHS has proposed, but not finalized, these new rules. In addition, the HITECH Act provided that Business Associates will now be subject to the same security requirements as Covered Entities, and that with regard to both the security and privacy rule, Business Associates will be subject to direct enforcement by HHS, including civil and criminal liability, just as Covered Entities are. In the past, HIPAA has generally affected us indirectly. Medtronic is generally not a Covered Entity, except for a few units such as our Diabetes business and our health insurance plans. Medtronic only operates as a Business Associate to Covered Entities in a limited number of instances. In those cases, the patient data that we receive and analyze may include protected health information. We are committed to maintaining the security and privacy of patients' health information and believe that we meet the expectations of the HIPAA rules. Some modifications to our systems and policies may be necessary, but the framework is already in place. However, the potential for enforcement action against us is now greater, as HHS can take action directly against Business Associates. Thus, while we believe we are and will be in substantial compliance with HIPAA standards, there is no guarantee that the government will not disagree. Enforcement actions can be costly and interrupt regular operations of our business. Nonetheless, these requirements affect a limited subset of our business. We believe the ongoing costs and impacts of assuring compliance with the HIPAA privacy and security rules are not material to our business. We are also impacted by the privacy requirements of countries outside the U.S. Privacy standards in Europe and Asia are becoming increasingly strict. Enforcement action and financial penalties related to privacy in the EU are growing, and new laws and restrictions are being passed. The management of cross border transfers of information among and outside of EU member countries is becoming more complex, which may complicate our clinical research activities, as well as product offerings that involve transmission or use of clinical data. We will continue our efforts to comply with those requirements and to adapt our business processes to the standards.

14

Table of Contents

Government and private sector initiatives to limit the growth of health care costs, including price regulation, competitive pricing, coverage and payment policies, comparative effectiveness of therapies, technology assessments, and managed-care arrangements, are continuing in many countries where we do business, including the U.S. These changes are causing the marketplace to put increased emphasis on the delivery of more cost-effective medical devices and therapies. Government programs, including Medicare and Medicaid, private health care insurance, and managed-care plans have attempted to control costs by limiting the amount of reimbursement they will pay for particular procedures or treatments, tying reimbursement to outcomes, and other mechanisms designed to constrain utilization and contain costs. Hospitals, which purchase implants, are also seeking to reduce costs through a variety of mechanisms, including, for example, gainsharing, where a hospital agrees with physicians to share any realized cost savings resulting from the physicians' collective change in practice patterns such as standardization of devices where medically appropriate. This has created an increasing level of price sensitivity among customers for our products. Some third-party payers must also approve coverage for new or innovative devices or therapies before they will reimburse health care providers who use the medical devices or therapies. Even though a new medical device may have been cleared for commercial distribution, we may find limited demand for the device until reimbursement approval has been obtained from governmental and private third-party payers. In addition, some private third-party payers require that certain procedures or that the use of certain products be authorized in advance as a condition of reimbursement. As a result of our manufacturing efficiencies and cost controls, we believe we are well-positioned to respond to changes resulting from the worldwide trend toward cost-containment; however, uncertainty remains as to the nature of any future legislation, making it difficult for us to predict the potential impact of cost-containment trends on future operating results.

The delivery of our devices is subject to regulation by HHS and comparable state and non-U.S. agencies responsible for reimbursement and regulation of health care items and services. U.S. laws and regulations are imposed primarily in connection with the Medicare and Medicaid programs, as well as the government's interest in regulating the quality and cost of health care. Foreign governments also impose regulations in connection with their health care reimbursement programs and the delivery of health care items and services.

Federal health care laws apply when we or customers submit claims for items or services that are reimbursed under Medicare, Medicaid, or other federally-funded health care programs. The principal federal laws include: (1) the False Claims Act which prohibits the submission of false or otherwise improper claims for payment to a federally-funded health care program; (2) the Anti-Kickback Statute which prohibits offers to pay or receive remuneration of any kind for the purpose of inducing or rewarding referrals of items or services reimbursable by a Federal health care program; (3) the Stark law which prohibits physicians from referring Medicare or Medicaid patients to a provider that bills these programs for the provision of certain designated health services if the physician (or a member of the physician's immediate family) has a financial relationship with that provider; and (4) health care fraud statutes that prohibit false statements and improper claims to any third-party payer. There are often similar state false claims, anti-kickback, and anti-self referral and insurance laws that apply to state-funded Medicaid and other health care programs and private third-party payers. In addition, the U.S. Foreign Corrupt Practices Act can be used to prosecute companies in the U.S. for arrangements with physicians, or other parties outside the U.S. if the physician or party is a government official of another country and the arrangement violates the law of that country.

15

Table of Contents

The laws applicable to us are subject to change, and subject to evolving interpretations. If a governmental authority were to conclude that we are not in compliance with applicable laws and regulations, Medtronic and its officers and employees could be subject to severe criminal and civil penalties including substantial fines and damages, and exclusion from participation as a supplier of product to beneficiaries covered by Medicare or Medicaid.

We operate in an industry characterized by extensive patent litigation. Patent litigation can result in significant damage awards and injunctions that could prevent the manufacture and sale of affected products or result in significant royalty payments in order to continue selling the products. At any given time, we are involved as both a plaintiff and a defendant in a number of patent infringement actions. While it is not possible to predict the outcome of patent litigation incidents to our business, we believe the costs associated with this type of litigation could have a material adverse impact on our consolidated results of operations, financial position, or cash flows. For additional information, see Note 17 to the consolidated financial statements in "Item 8. Financial Statements and Supplementary Data" in this Annual Report on Form 10-K.

We operate in an industry susceptible to significant product liability claims. These claims may be brought by individuals seeking relief on their own behalf or purporting to represent a class. In addition, product liability claims may be asserted against us in the future based on events we are not aware of at the present time.

We are also subject to various environmental laws and regulations both within and outside the U.S. Like other medical device companies, our operations involve the use of substances regulated under environmental laws, primarily those used in manufacturing and sterilization processes. To the best of our knowledge at this time, we do not expect that compliance with environmental protection laws will have a material impact on our consolidated results of operations, financial position, or cash flows.

We have elected to self-insure most of our insurable risks, including medical and dental costs, physical loss to property, business interruptions, workers' compensation, comprehensive general, director and officer, and product liability. Decisions to self-insure are based on comparisons between the price, availability, and value of insurance coverage. We continue to monitor the insurance marketplace to evaluate the value to the Company of obtaining insurance coverage in the future. Based on historical loss trends, we believe that our self-insurance program accruals will be adequate to cover future losses. Historical trends, however, may not be indicative of future losses. These losses could have a material adverse impact on our consolidated results of operations, financial position, or cash flows.

Executive Officers of Medtronic

Set forth below are the names and ages of current Section 16(b) executive officers of Medtronic, Inc., as well as information regarding their positions with Medtronic, their periods of service in these capacities, and their business experiences. There are no family relationships among any of the officers named, nor is there any arrangement or understanding pursuant to which any person was selected as an officer.

Omar Ishrak , age 56, has been Chairman and Chief Executive Officer of Medtronic since June 2011. Prior to joining Medtronic, Mr. Ishrak served as President and Chief Executive Officer of GE Healthcare Systems, a division of GE Healthcare, from 2009 to 2011. He was President and Chief Executive Officer of GE Healthcare Clinical Systems from 2005 to 2008, Vice President and General Manager of GE Healthcare Ultrasound and BMD from 2000 to 2004, and General Manager, Global Ultrasound from 1995 to 2000.

Michael J. Coyle, age 49, has been Executive Vice President and Group President, Cardiac and Vascular Group since December 2009. Prior to that, he served as President of the Cardiac Rhythm Management division at St. Jude from 2001 to 2007, and prior positions included serving St. Jude as President of the company's Daig Catheter division and numerous leadership positions at Eli Lilly & Company. Mr. Coyle is a member of the board of directors of Volcano Corporation.

16

Table of Contents

H. James Dallas, age 53, has been Senior Vice President, Quality and Operations since April 2008. Prior to that, he was Senior Vice President and Chief Information Officer of Medtronic from April 2006 to April 2008. He was Vice President and Chief Information Officer of Georgia Pacific Corporation from December 2002 to December 2005; General Manager of the Transportation Division and President of the Lumber Division of Georgia Pacific Corporation from October 2001 to December 2002; and Vice President, Building Products Distribution Sales and Logistics, Georgia Pacific Corporation from October 2000 to October 2001. Mr. Dallas is a member of the board of directors of KeyCorp.

Gary L. Ellis, age 55, has been Senior Vice President and Chief Financial Officer since May 2005. Prior to that, he was Vice President, Corporate Controller and Treasurer since October 1999 and Vice President and Corporate Controller from August 1994 to October 1999. Mr. Ellis joined Medtronic in 1989 as Assistant Corporate Controller and was promoted to Vice President of Finance for Medtronic Europe in 1992, until being named as Corporate Controller in 1994. Mr. Ellis is a member of the board of directors of The Toro Company and past chairman of the American Heart Association.

D. Cameron Findlay, age 52, has been Senior Vice President, General Counsel and Corporate Secretary since August 2009. Prior to that, Mr. Findlay was Executive Vice President and General Counsel of Aon Corporation from August 2003 to June 2009. Prior to joining Aon, Mr. Findlay served as the U.S. Deputy Secretary of Labor. Before joining the Labor Department in June 2001, Mr. Findlay was a partner at the law firm now known as Sidley Austin LLP. Before that, he served in the White House as an aide to U.S. President George H. W. Bush.

Richard Kuntz, M.D., age 55, has been Senior Vice President and Chief Scientific, Clinical and Regulatory Officer since August 2009. Prior to that, he was Senior Vice President and President, Neuromodulation from October 2005 to August 2009; and prior to that, he was an interventional cardiologist and Chief of the Division of Clinical Biometrics at Brigham and Women's Hospital and Associate Professor of Medicine and Chief Scientific Officer of the Harvard Clinical Research Institute. Mr. Kuntz is a member of the board of directors of Tengion, Inc.

Christopher J. O'Connell, age 45, has been Executive Vice President and Group President, Restorative Therapies Group since August 2009. Prior to that, he was Senior Vice President and President, Diabetes from October 2006 to August 2009, President of Medtronic's Emergency Response Systems division from May 2005 to October 2006, and Vice President of Sales and Marketing of Medtronic's Cardiac Rhythm Disease Management division from November 2001 to May 2005. Mr. O'Connell has served in various management positions since joining the Company in 1994.

Caroline Stockdale, age 48, has been Senior Vice President and Chief Human Resources Officer since April 2010. Prior to that, she served as Vice President of Revenue Cycle Operations at Accretive Health from January 2009 to May 2010. From 2005 to 2009, she served as Executive Vice President of Global Human Resources at Warner Music Group; from 2002 to 2005, she was Senior Vice President, Human Resources, at American Express Financial Advisors (Ameriprise); and from 1997 to 2002, she was Executive Vice President and Global HR Leader at GE Capital.

Item 1A. Risk Factors

Investing in Medtronic involves a variety of risks and uncertainties, known and unknown, including, among others, those discussed below.

The medical device industry is highly competitive and we may be unable to compete effectively.