Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended February 2, 2013

or

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________ to___________

Commission file number 001-15059

NORDSTROM, INC.

(Exact name of registrant as specified in its charter)

Washington |

| 91-0515058 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

| |

1617 Sixth Avenue, Seattle, Washington |

| 98101 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code 206-628-2111

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common stock, without par value |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☑ NO ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☑ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☑ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Large accelerated filer ☑ | Accelerated filer ¨ |

Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ¨ NO ☑

As of July 27, 2012 the aggregate market value of the Registrant's voting and non-voting stock held by non-affiliates of the Registrant was approximately $9.0 billion using the closing sales price on that day of $54.40 . On March 12, 2013 , 195,891,451 shares of common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 2013 Annual Meeting of Shareholders scheduled to be held on May 14, 2013 are incorporated into Part III.

Nordstrom, Inc. and subsidiaries 1

[This page intentionally left blank.]

Table of Contents

TABLE OF CONTENTS |

| |

|

| Page |

PART I |

| |

Item 1. | Business. | 4 |

Item 1A. | Risk Factors. | 6 |

Item 1B. | Unresolved Staff Comments. | 9 |

Item 2. | Properties. | 10 |

Item 3. | Legal Proceedings. | 12 |

Item 4. | Mine Safety Disclosures. | 12 |

|

| |

PART II |

| |

Item 5. | Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities. | 13 |

Item 6. | Selected Financial Data. | 15 |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. | 16 |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk. | 34 |

Item 8. | Financial Statements and Supplementary Data. | 35 |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure. | 62 |

Item 9A. | Controls and Procedures. | 62 |

Item 9B. | Other Information. | 64 |

|

| |

PART III |

| |

Item 10. | Directors, Executive Officers and Corporate Governance. | 64 |

Item 11. | Executive Compensation. | 64 |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters. | 64 |

Item 13. | Certain Relationships and Related Transactions, and Director Independence. | 64 |

Item 14. | Principal Accounting Fees and Services. | 64 |

|

| |

PART IV |

| |

Item 15. | Exhibits and Financial Statement Schedules. | 65 |

|

| |

Signatures | 66 | |

Consent of Independent Registered Public Accounting Firm | 67 | |

Exhibit Index | 68 | |

Nordstrom, Inc. and subsidiaries 3

Table of Contents

PART I

Item 1. Business.

DESCRIPTION OF BUSINESS

Founded in 1901 as a retail shoe business in Seattle, Nordstrom later incorporated in the state of Washington in 1946 and went on to become one of the leading fashion specialty retailers based in the U.S. We operate 242 U.S. stores located in 31 states as of March 18, 2013 , as well as a robust e-commerce business through nordstrom.com. The west and east coasts of the United States are the areas in which we have the largest presence. We have two reportable segments: Retail and Credit.

As of March 18, 2013 , the Retail segment includes our 117 'Nordstrom' branded full-line stores and our online store at www.nordstrom.com, our 121 off-price 'Nordstrom Rack' stores, one clearance store that operates under the name 'Last Chance' and our other retail channels including our online private sale subsidiary 'HauteLook,' our two 'Jeffrey' boutiques and one philanthropic 'treasure&bond' store. Through these multiple retail channels, we try to deliver the best customer experience possible. We offer a wide selection of high-quality brand name and private label merchandise focused on apparel, shoes, cosmetics and accessories. Our integrated Nordstrom full-line stores and online store allow us to provide our customers with a seamless shopping experience. Purchases within our stores are primarily fulfilled from that store's inventory, but may also be shipped to our customers from our fulfillment center in Cedar Rapids, Iowa, or from other Nordstrom full-line stores for inventory unavailable at the original store. Online purchases are primarily shipped to our customers from our Cedar Rapids fulfillment center, but may also be shipped from our Nordstrom full-line stores. Our customers also have the option to pick up online orders in our Nordstrom full-line stores if inventory is available at that location. These capabilities allow us to better serve customers across various channels and improve sales. The Nordstrom Rack stores purchase high-quality name brand merchandise directly from vendors and also serve as outlets for clearance merchandise from our Nordstrom stores. Our online private sale retailer, HauteLook, offers limited time sale events on fashion and lifestyle brands.

Our Credit segment includes our wholly owned federal savings bank, Nordstrom fsb, through which we provide a private label credit card, two Nordstrom VISA credit cards and a debit card. The credit and debit cards feature a shopping-based loyalty program designed to increase customer visits and spending. Although the primary purpose of our Credit business is to strengthen and build customer relationships, foster greater customer loyalty and drive more sales, we also generate revenues through finance charges and other fees on these cards and save on interchange fees that would be incurred by the Retail segment if our customers used third-party cards.

For more information about our business and our reportable segments, see Item 7: Management's Discussion and Analysis of Financial Condition and Results of Operations and Note 16: Segment Reporting in Item 8: Financial Statements and Supplementary Data.

FISCAL YEAR

We operate on a 52/53-week fiscal year ending on the Saturday closest to January 31st. References to 2012 relate to the 53-week fiscal year ended February 2, 2013 . References to any other years included within this document are based on a 52-week fiscal year.

TRADEMARKS

We have 139 trademarks, each of which is the subject of one or more trademark registrations and/or trademark applications. Our most notable trademarks include Nordstrom, Nordstrom Rack, HauteLook, Halogen, Caslon, and BP. Each of our trademarks is renewable indefinitely, provided that it is still used in commerce at the time of the renewal.

RETURN POLICY

We have a liberal approach to returns at Nordstrom. We do not have a formal return policy at our Nordstrom full-line stores or online at www.nordstrom.com. If a customer is not satisfied with something they purchased, we evaluate the situation on a case-by-case basis with the ultimate objective of taking care of the customer. We also try to make returns and exchanges easy for our customers, whether in our stores or online, where we offer free shipping and free returns. Our Nordstrom Rack stores generally accept returns up to 30 days from the date of purchase with the original price tag and sales receipt. HauteLook generally accepts returns of apparel, footwear and accessories within 21 days from the date of shipment.

SEASONALITY

Due to our Anniversary Sale in July, the holidays in December and the half-yearly sales that occur in the second and fourth quarters, our sales are typically higher in the second and fourth quarters of the fiscal year than in the first and third quarters. In 2012 , our Anniversary Sale shifted to the last week of July and the first week of August to align with the historical timing of our sale event. This moved one week of event sales to the third quarter.

4

Table of Contents

INVENTORY

We plan our merchandise purchases and receipts to coincide with expected sales trends. For instance, our merchandise purchases and receipts increase prior to our Anniversary Sale, which has historically extended over the last two weeks of July. As discussed above, in 2012 this shifted to the last week of July and the first week of August. We also purchase and receive a larger amount of merchandise in the fall as we prepare for the holiday shopping season (from late November through December). In 2012, we increased our investment in pack and hold inventory at Nordstrom Rack, which involves the acquisition of merchandise from some of our top brands in advance of the upcoming selling seasons in order to take advantage of strategic buying opportunities. This inventory is typically held for six months on average and has contributed to the growth in our Rack business. We pay for our merchandise purchases under the terms established with our vendors.

In order to offer merchandise that our customers want, we purchase merchandise from a wide variety of high-quality suppliers, including domestic and foreign businesses. We also have arrangements with agents and contract manufacturers to produce our private label merchandise. We expect our suppliers to meet our "Nordstrom Partnership Guidelines," which address our corporate social responsibility standards for matters such as legal and regulatory compliance, labor, health and safety and the environment, and are available on our website at www.nordstrom.com.

COMPETITIVE CONDITIONS

We operate in a highly competitive business environment. We compete with other national, regional and local retailers that may carry similar lines of merchandise, including department stores, specialty stores, off-price stores, boutiques and Internet businesses. Our specific competitors vary from market to market. We believe the keys to competing in our industry are customer service and creating a great customer experience in store and online, which includes compelling price and value, fashion newness, quality of products, selection, convenience, technology, product fulfillment, service and stores in top locations.

EMPLOYEES

During 2012 , we employed approximately 61,000 employees on a full- or part-time basis. Due to the seasonal nature of our business, employment increased to approximately 63,500 employees in July 2012 and 64,500 in December 2012 . Substantially all of our employees are non-union. We believe our relationship with our employees is good.

CAUTIONARY STATEMENT

Certain statements in this Annual Report on Form 10-K contain or may suggest "forward-looking" information (as defined in the Private Securities Litigation Reform Act of 1995) that involve risks and uncertainties, including, but not limited to, anticipated financial outlook for the fiscal year ending February 1, 2014, anticipated annual same-store sales rate, anticipated Return on Invested Capital and trends in our operations. Such statements are based upon the current beliefs and expectations of the company's management and are subject to significant risks and uncertainties. Actual future results may differ materially from historical results or current expectations depending upon factors including, but not limited to:

• | successful execution of our growth strategy, including expansion into new markets, technological investments and acquisitions, our ability to realize the anticipated benefits from such growth initiatives, and the timely completion of construction associated with newly planned stores, relocations and remodels, all of which may be impacted by the financial health of third parties, |

• | our ability to manage the transformation of our business/financial model as we increase our investments in growth opportunities, including our online business and our ability to manage related organizational changes, |

• | our ability to maintain relationships with our employees and to effectively attract, develop and retain our future leaders, |

• | effective inventory management, disruptions in our supply chain and our ability to control costs, |

• | the impact of any systems failures, cybersecurity and/or security breaches, including any security breach that results in the theft, transfer or unauthorized disclosure of customer, employee or company information or our compliance with information security and privacy laws and regulations in the event of such an incident, |

• | successful execution of our information technology strategy, |

• | efficient and proper allocation of our capital resources, |

• | our ability to safeguard our reputation and maintain our vendor relationships, |

• | the impact of economic and market conditions and the resultant impact on consumer spending patterns, |

• | our ability to respond to the business environment, fashion trends and consumer preferences, including changing expectations of service and experience in stores and online, |

• | the effectiveness of planned advertising, marketing and promotional campaigns in the highly competitive retail industry, |

• | weather conditions, natural disasters, health hazards, national security or other market disruptions, or the prospects of these events and the impact on consumer spending patterns, |

• | our compliance with applicable banking related laws and regulations impacting our ability to extend credit to our customers, employment laws and regulations, certain international laws and regulations, other laws and regulations applicable to us, including the outcome of claims and litigation and resolution of tax matters, and ethical standards, |

• | impact of the current regulatory environment and financial system and health care reforms, |

Nordstrom, Inc. and subsidiaries 5

Table of Contents

• | compliance with debt covenants, availability and cost of credit, changes in interest rates, and trends in personal bankruptcies and bad debt write-offs, and |

• | the timing and amounts of share repurchases by the company, if any, or any share issuances by the company, including issuances associated with option exercises or other matters. |

These and other factors could affect our financial results and cause actual results to differ materially from any forward-looking information we may provide. We undertake no obligation to update or revise any forward-looking statements to reflect subsequent events, new information or future circumstances.

SEC FILINGS

We file annual, quarterly and current reports, proxy statements and other documents with the Securities and Exchange Commission ("SEC"). All material we file with the SEC is publicly available at the SEC's Public Reference Room at 100 F Street NE, Washington, DC 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains a website at www.sec.gov that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

WEBSITE ACCESS

Our website address is www.nordstrom.com. We make available free of charge on or through our website our annual and quarterly reports on Form 10-K and 10-Q (including related filings in eXtensible Business Reporting Language ("XBRL") format), current reports on Form 8-K, proxy statements, statements of changes in beneficial ownership of securities on Form 4 and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file the report with or furnish it to the SEC. Interested parties may also access a webcast of quarterly earnings conference calls and other financial events through our website.

CORPORATE GOVERNANCE

We have a long-standing commitment to upholding a high level of ethical standards. In addition, as required by the listing standards of the New York Stock Exchange ("NYSE") and the rules of the SEC, we have adopted Codes of Business Conduct and Ethics for our employees, officers and directors ("Codes of Ethics") and Corporate Governance Guidelines. We have posted on our website our Codes of Ethics, our Corporate Governance Guidelines and our Committee Charters for the Audit, Compensation, Corporate Governance and Nominating and Finance Committees. Any amendments and waivers to these will also be available on our website.

For printed versions of these items or any other inquiries, please use the following contact information:

Nordstrom Investor Relations

PO Box 2737

Seattle, Washington 98111

(206) 233-6564

Item 1A. Risk Factors.

Our business faces many risks. We believe the risks described below outline the items of most concern to us.

RISKS DUE TO STRATEGIC AND OPERATIONAL FACTORS

Our strategic growth plans focus on both our stores and on e-commerce and failure to successfully execute our plans could negatively impact our current business and future profitability.

We plan to accelerate the number of new Nordstrom Rack store openings. New store openings both at the Rack and in our full-line stores involve certain risks, including the availability of suitable locations, constructing, furnishing and supplying a store in a timely and cost-effective manner and accurately assessing the demographic or retail environment for a particular location. In addition, sales at new, relocated or remodeled stores may not meet our projections, which could adversely affect our return on investment. We also intend to open stores in new and international markets, such as Canada, Puerto Rico and Manhattan, and expansion will require additional management attention and resources and may distract us from executing our core operations. In addition, competition from strong local competitors, compliance with foreign and local laws and regulatory requirements and potentially unfavorable tax consequences may cause our business to be adversely impacted.

6

Table of Contents

We are also enhancing our customer shopping experience in our stores, online, and in mobile and social channels by pursuing a heightened focus on technology and e-commerce to fuel our growth. In addition, other growth opportunities may include acquisitions of, or investments in, other businesses, as well as new technologies or other investments to improve and integrate these experiences. If we target the wrong opportunities, fail to make the best investments or make an investment commitment significantly above or below our needs, it may result in the loss of our competitive position. If these technologies and investments do not perform as expected or are not seamlessly integrated, our profitability and growth could be adversely affected. In addition, if we do not maintain our current systems, we may see interruptions to our business and increased costs in order to bring our systems up to date.

As we execute our plans and continue to evolve and transform our strategy, we may not adequately manage the related organizational changes or appropriately monitor, report or communicate the changes in an effective manner, adversely impacting our current business and future profitability.

Improvements to our merchandise buying processes and systems could adversely affect our business if not successfully executed.

We are making investments to improve our merchandise planning, procurement and allocation capabilities through changes in personnel, processes and technology over a period of several years. If we encounter challenges associated with change management, the ability to hire and retain key personnel involved in these efforts, implementation of associated information technology or adoption of new processes, our ability to continue to successfully execute our strategy could be adversely affected. As a result, we may not derive the expected benefits to our sales and profitability, or we may incur increased costs relative to our current expectations.

If we do not effectively implement our strategic and business planning processes to attract, retain, train and develop future leaders, our business may suffer .

We rely on the experience of our senior management, who have specific knowledge relating to us and our industry that is difficult to replace. If unexpected leadership turnover occurs without adequate succession plans, the loss of the services of any of these individuals, or any negative perceptions of our business as a result, could damage our reputation and our business.

We could expose our customers and our business to risk if we fail to take the appropriate measures to safeguard our information security and privacy environment from security breaches.

Our operations involve the collection, storage and transmission of customers' personal information, consumer preferences and credit card information, in addition to employee information and company financial and strategic data. Any measures we implement to prevent a security or cybersecurity threat may not be totally effective and may have the potential to harm relations with our customers or decrease activity on our websites by making them more difficult to use. In addition, the regulatory environment surrounding information security, cybersecurity and privacy is increasingly demanding, with new and constantly changing requirements. Security breaches and cyber incidents and their remediation, whether at our company, our third-party providers or our peer retailers, could expose us to a risk of loss or misappropriation of this information, litigation, potential liability, reputation damage and loss of customers' trust and business.

If we fail to appropriately manage our capital, we may negatively impact our operations and shareholder return.

We utilize capital to finance our operations, make capital expenditures and acquisitions, manage our debt levels and return value to our shareholders through dividends and share repurchases. If our access to capital is restricted or our cost of capital increases, our operations and financial condition could be adversely impacted. Further, if we do not properly allocate our capital to maximize returns, our operations, cash flows and returns to shareholders could be adversely affected.

Our customer and employee relationships could be negatively affected if we fail to maintain our corporate culture and reputation.

We have a well-recognized culture and reputation that consumers may associate with a high level of integrity, customer service and quality merchandise, and it is one of the reasons employees choose Nordstrom as a place of employment. Any significant damage to our reputation could negatively impact sales, diminish customer trust, reduce employee morale and productivity and lead to difficulties in recruiting and retaining qualified employees.

RISKS DUE TO ECONOMIC AND EXTERNAL MARKET FACTORS

A downturn in economic conditions could have a significant adverse effect on our business.

During economic downturns, fewer customers may shop for the high-quality items in our stores and on our website as they may be seen as discretionary and those who do shop may limit the amount of their purchases. This reduced demand may lead to lower sales, higher markdowns and increased marketing and promotional spending. Deterioration of economic conditions and consumer confidence may also adversely affect our credit customers' payment patterns and delinquency rates, increasing our bad debt expense.

Nordstrom, Inc. and subsidiaries 7

Table of Contents

Our business could suffer if we do not appropriately assess and react to competitive market forces.

We compete with other national, regional, local and online retailers that may carry similar lines of merchandise, including department stores, specialty stores, off-price stores, boutiques and Internet businesses. Online retail shopping is rapidly evolving and we expect competition in the e-commerce market to intensify in the future as the Internet facilitates competitive entry and comparison shopping. We may lose market share to our competitors and our sales and profitability could suffer if we are unable to remain competitive in the key areas of price and value, fashion newness, quality of products, depth of selection, convenience, fulfillment, service and the shopping experience, including the online and store environment and location.

Our Credit segment faces competition from other retailers who also offer credit card products with associated loyalty programs, large banks and other credit card companies, some of which have substantial financial resources. If we do not effectively anticipate or respond to the competitive banking and credit card environment, we could lose market share to our competitors.

Our sales and customer relationships may be negatively impacted if we do not anticipate and respond to consumer preferences and fashion trends appropriately.

Our ability to predict or respond to constantly changing fashion trends, consumer preferences and spending patterns significantly impacts our sales and operating results. If we do not identify and respond to emerging trends in consumer spending and preferences quickly enough, we may harm our ability to retain our existing customers or attract new customers. If we purchase too much inventory, we may be forced to sell our merchandise at lower average margins, which could harm our business. Conversely, if we fail to purchase enough merchandise, we may lose opportunities for additional sales and damage our relationships with our customers.

The results of our Credit operations could be adversely affected by changes in market conditions.

Our credit card revenues and profitability are subject in large part to economic and market conditions that are beyond our control, including, but not limited to, interest rates, consumer credit availability, consumer debt levels, unemployment trends, laws and regulations and other factors. These economic and market conditions could impair our ability to assess the creditworthiness of our customers if the criteria and/or models we use to underwrite and manage our customers become less predictive of future losses. This could cause our losses to rise and have a negative impact on our results of operations.

Our business and operations could be materially and adversely affected by supply chain disruptions, severe weather patterns, natural disasters, widespread pandemics and other natural or man-made disruptions.

We derive a significant amount of our total sales from stores located on the west and east coasts of the United States, particularly in California, which increases our exposure to conditions in these regions. These disruptions could cause, among other things, a decrease in consumer spending that would negatively impact our sales; staffing shortages in our stores, distribution centers or corporate offices; interruptions in the flow of merchandise to our stores; disruptions in the operations of our merchandise vendors or property developers; increased costs; and a negative impact on our reputation and long-term growth plans.

RISKS DUE TO LEGAL AND REGULATORY FACTORS

We are subject to certain laws, litigation, regulatory matters and ethical standards, and our failure to comply with or adequately address developments as they arise could adversely affect our reputation and operations.

Our policies, procedures and practices and the technology we implement are designed to comply with federal, state, local and foreign laws, rules and regulations, including those imposed by the SEC and other regulatory agencies, the marketplace, the banking industry and foreign countries, as well as responsible business, social and environmental practices, all of which may change from time to time. Significant legislative changes, including those that relate to employment matters and health care reform, could impact our relationship with our workforce, which could increase our expenses and adversely affect our operations. In addition, if we fail to comply with applicable laws and regulations or implement responsible business, social and environmental practices, we could be subject to damage to our reputation, class action lawsuits, legal and settlement costs, civil and criminal liability, increased cost of regulatory compliance, restatements of our financial statements, disruption of our business and loss of customers. Any required changes to our employment practices could result in the loss of employees, reduced sales, increased employment costs, low employee morale and harm to our business and results of operations. In addition, political and economic factors could lead to unfavorable changes in federal and state tax laws, which may increase our tax liabilities. An increase in our tax liabilities could adversely affect our results of operations. We are also regularly involved in various litigation matters that arise in the ordinary course of business. Litigation or regulatory developments could adversely affect our business and financial condition.

8

Table of Contents

Our business faces uncertainties as we implement newly enacted financial system reforms that could have an adverse affect on our operations.

The recession resulted in increased legislative and regulatory changes affecting the financial industry. The Credit Card Accountability Responsibility and Disclosure Act of 2009 included new rules and restrictions on credit card pricing, finance charges and fees, customer billing practices and payment application, which required us to make changes to our credit card practices and systems. We expect more regulations and interpretations of the new rules to emerge and, depending on the nature and extent of the full impact from these rules, the revenues and profitability of our Credit segment could be adversely affected.

In addition, the Dodd-Frank Wall Street Reform and Consumer Protection Act was enacted in July 2010. It significantly restructures regulatory oversight and other aspects of the financial industry, creates a new federal agency to supervise and enforce consumer lending laws and regulations and expands state authority over consumer lending. Numerous regulations will be issued in the near future to implement the requirements of this Act, which remain uncertain at this time. Depending on the nature and extent of these regulations, and the enforcement approach of regulators under the new law, there could be an adverse impact to our Credit segment.

Item 1B. Unresolved Staff Comments.

None.

Nordstrom, Inc. and subsidiaries 9

Table of Contents

Item 2. Properties.

| Number of stores |

| % of total store square footage | |

Leased stores on leased land | 143 |

| 34 | % |

Owned stores on leased land | 61 |

| 43 | % |

Owned stores on owned land | 35 |

| 22 | % |

Partly owned and partly leased store | 1 |

| 1 | % |

Total | 240 |

| 100 | % |

Fiscal year | 2012 | | | 2011 | | | 2010 | |

Number of stores, beginning of year | 225 | |

| 204 | |

| 184 | |

Stores opened | 16 | |

| 22 | |

| 20 | |

Stores closed | (1 | ) |

| (1 | ) |

| - | |

Number of stores, end of year | 240 | |

| 225 | |

| 204 | |

|

|

|

|

|

| |||

Nordstrom | 117 | |

| 117 | |

| 115 | |

Nordstrom Rack and Other | 123 | |

| 108 | |

| 89 | |

In 2012 , we opened one Nordstrom full-line store (Salt Lake City, Utah), opened 15 Nordstrom Rack stores (Orange, California; Boise, Idaho; Alpharetta, Georgia; Farmington, Connecticut; Temecula, California; Willow Grove, Pennsylvania; Manchester, Missouri; Vienna, Virginia; San Diego, California; Huntington Beach, California; Phoenix, Arizona; San Antonio, Texas; Huntington, New York; Warwick, Rhode Island; and Seattle, Washington) and relocated three Nordstrom Rack stores (Seattle, Washington; Long Island, New York; and White Plains, New York).

To date in 2013 , we have opened two Nordstrom Rack stores (Boston, Massachusetts and Upland, California). During the remainder of 2013 , we have announced the opening of 14 additional Nordstrom Rack stores (Ann Arbor, Michigan; Auburn Hills, Michigan; Birmingham, Alabama; Columbia, Maryland; Portland, Maine; Washington, D.C.; Atlanta, Georgia; Cleveland, Ohio; Columbus, Ohio; Concord, California; El Paso, Texas; Eugene, Oregon; Jacksonville, Florida; and Naples, Florida), the relocation of one Nordstrom full-line store (Glendale, California) and the relocation of two Nordstrom Rack stores (Culver City, California and Honolulu, Hawaii).

We also own six merchandise distribution centers (Portland, Oregon; Dubuque, Iowa; Ontario, California; Newark, California; Upper Marlboro, Maryland; and Gainesville, Florida) and we own one fulfillment center on leased land (Cedar Rapids, Iowa), all of which are utilized by our Retail segment. HauteLook, which is also included in our Retail segment, leases two administrative offices (in Los Angeles, California and New York, New York) and one fulfillment center (in Fontana, California). We lease an office building in Centennial, Colorado and one in Scottsdale, Arizona, both for use by our Credit segment. Our administrative offices in Seattle, Washington are a combination of leased and owned space. We also lease a data center in Centennial, Colorado.

10

Table of Contents

The following table lists our retail store count and facility square footage by state as of February 2, 2013 :

Retail stores by channel |

| Nordstrom Full-Line Stores |

| Nordstrom Rack and Other 1 |

| Total | |||||||||

State |

| Count | | Square Footage (000's) | |

| Count | | Square Footage (000's) | |

| Count | | Square Footage (000's) | |

Alaska |

| 1 | | 97 | |

| - | | - | |

| 1 | | 97 | |

Arizona |

| 2 | | 384 | |

| 6 | | 228 | |

| 8 | | 612 | |

California 2 |

| 32 | | 5,481 | |

| 33 | | 1,300 | |

| 65 | | 6,781 | |

Colorado |

| 3 | | 559 | |

| 4 | | 148 | |

| 7 | | 707 | |

Connecticut |

| 1 | | 189 | |

| 1 | | 36 | |

| 2 | | 225 | |

Delaware |

| 1 | | 127 | |

| - | | - | |

| 1 | | 127 | |

Florida 2 |

| 9 | | 1,431 | |

| 7 | | 247 | |

| 16 | | 1,678 | |

Georgia |

| 3 | | 555 | |

| 4 | | 130 | |

| 7 | | 685 | |

Hawaii |

| 1 | | 211 | |

| 1 | | 34 | |

| 2 | | 245 | |

Idaho |

| - | | - | |

| 1 | | 37 | |

| 1 | | 37 | |

Illinois |

| 4 | | 947 | |

| 7 | | 280 | |

| 11 | | 1,227 | |

Indiana |

| 1 | | 134 | |

| 1 | | 35 | |

| 2 | | 169 | |

Kansas |

| 1 | | 219 | |

| 1 | | 35 | |

| 2 | | 254 | |

Maryland |

| 4 | | 765 | |

| 3 | | 115 | |

| 7 | | 880 | |

Massachusetts |

| 4 | | 595 | |

| 3 | | 121 | |

| 7 | | 716 | |

Michigan |

| 3 | | 552 | |

| 2 | | 80 | |

| 5 | | 632 | |

Minnesota |

| 1 | | 240 | |

| 2 | | 75 | |

| 3 | | 315 | |

Missouri |

| 2 | | 342 | |

| 2 | | 69 | |

| 4 | | 411 | |

Nevada |

| 1 | | 207 | |

| 1 | | 35 | |

| 2 | | 242 | |

New Jersey |

| 5 | | 991 | |

| 2 | | 70 | |

| 7 | | 1,061 | |

New York |

| 2 | | 460 | |

| 6 | | 162 | |

| 8 | | 622 | |

North Carolina |

| 2 | | 300 | |

| 2 | | 74 | |

| 4 | | 374 | |

Ohio |

| 3 | | 549 | |

| 2 | | 75 | |

| 5 | | 624 | |

Oregon |

| 5 | | 705 | |

| 4 | | 158 | |

| 9 | | 863 | |

Pennsylvania |

| 2 | | 381 | |

| 2 | | 85 | |

| 4 | | 466 | |

Rhode Island |

| 1 | | 206 | |

| 1 | | 38 | |

| 2 | | 244 | |

Tennessee |

| 1 | | 145 | |

| - | | - | |

| 1 | | 145 | |

Texas |

| 7 | | 1,284 | |

| 10 | | 348 | |

| 17 | | 1,632 | |

Utah |

| 2 | | 277 | |

| 2 | | 66 | |

| 4 | | 343 | |

Virginia |

| 5 | | 894 | |

| 5 | | 201 | |

| 10 | | 1,095 | |

Washington 2 |

| 8 | | 1,463 | |

| 7 | | 277 | |

| 15 | | 1,740 | |

Washington D.C. |

| - | | - | |

| 1 | | 41 | |

| 1 | | 41 | |

Total (31 states) |

| 117 | | 20,690 | |

| 123 | | 4,600 | |

| 240 | | 25,290 | |

1 Other includes one Last Chance clearance store, two Jeffrey boutiques and one philanthropic treasure&bond store.

2 California, Washington and Florida had the highest square footage, with a combined 10,199 square feet, representing 40% of the total company square footage.

Nordstrom, Inc. and subsidiaries 11

Table of Contents

Item 3. Legal Proceedings.

We are subject from time to time to various claims and lawsuits arising in the ordinary course of business including lawsuits alleging violations of state and/or federal wage and hour and other employment laws, privacy and other consumer-based claims. Some of these lawsuits purport or may be determined to be class or collective actions and seek substantial damages or injunctive relief, or both, and some may remain unresolved for several years. We believe the recorded reserves in our consolidated financial statements are adequate in light of the probable and estimable liabilities. As of the date of this report, we do not believe any currently identified claim, proceeding or litigation, either alone or in the aggregate, will have a material impact on our results of operations, financial position or cash flows. Since these matters are subject to inherent uncertainties, our view of them may change in the future.

Item 4. Mine Safety Disclosures.

None.

12

Table of Contents

PART II

Item 5. Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities.

MARKET, SHAREHOLDER AND DIVIDEND INFORMATION

Our common stock, without par value, is traded on the New York Stock Exchange under the symbol "JWN." The approximate number of holders of common stock as of March 12, 2013 was 150,000 , based upon the number of registered and beneficial shareholders, as well as the number of employee shareholders in the Nordstrom 401(k) Plan and Profit Sharing Plan. On this date we had 195,891,451 shares of common stock outstanding.

| Common Stock Price |

|

|

|

| ||||||

| 2012 |

| 2011 |

| Dividends per Share | ||||||

| High |

| Low |

| High |

| Low |

| 2012 |

| 2011 |

1st Quarter | $56.75 |

| $48.00 |

| $48.70 |

| $40.03 |

| $0.27 |

| $0.23 |

2nd Quarter | $57.75 |

| $46.27 |

| $52.15 |

| $41.88 |

| $0.27 |

| $0.23 |

3rd Quarter | $58.44 |

| $51.50 |

| $53.35 |

| $37.28 |

| $0.27 |

| $0.23 |

4th Quarter | $58.40 |

| $50.94 |

| $51.75 |

| $44.22 |

| $0.27 |

| $0.23 |

Full Year | $58.44 |

| $46.27 |

| $53.35 |

| $37.28 |

| $1.08 |

| $0.92 |

SHARE REPURCHASES

Dollar and share amounts in millions, except per share amounts

| Total Number of Shares (or Units) Purchased | |

| Average Price Paid Per Share (or Unit) | |

| Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | |

| Maximum Number (or Approximate Dollar Value) of Shares (or Units) that May Yet Be Purchased Under the Plans or Programs 1 | | ||

November 2012 | 0.6 | |

| | $54.99 | |

| 0.6 | |

| | $583 | |

December 2012 | 2.3 | |

| | $52.58 | |

| 2.3 | |

| | $463 | |

January 2013 | 1.3 | |

| | $54.69 | |

| 1.3 | |

| | $393 | |

Total | 4.2 | |

| | $53.55 | |

| 4.2 | |

|

| ||

1 In 2012 , we completed the $750 repurchase program authorized by our Board of Directors in May 2011 . In February 2012 , our Board of Directors authorized a program (the "2012 Program" ), which allows for the repurchase of up to $800 of our common stock through February 1, 2014 . As of February 2, 2013 , there was $393 in remaining share repurchase capacity under the 2012 Program. During 2012 , we repurchased 14.0 shares for an aggregate purchase price of $ 717 in accordance with the 2012 Program. Subsequent to year-end, in February 2013, our Board of Directors authorized a new program to repurchase up to $800 of our outstanding common stock, through March 1, 2015, in addition to the remaining amount available for repurchase under the 2012 program. The actual number and timing of future share repurchases, if any, will be subject to market and economic conditions and applicable Securities and Exchange Commission rules.

Nordstrom, Inc. and subsidiaries 13

Table of Contents

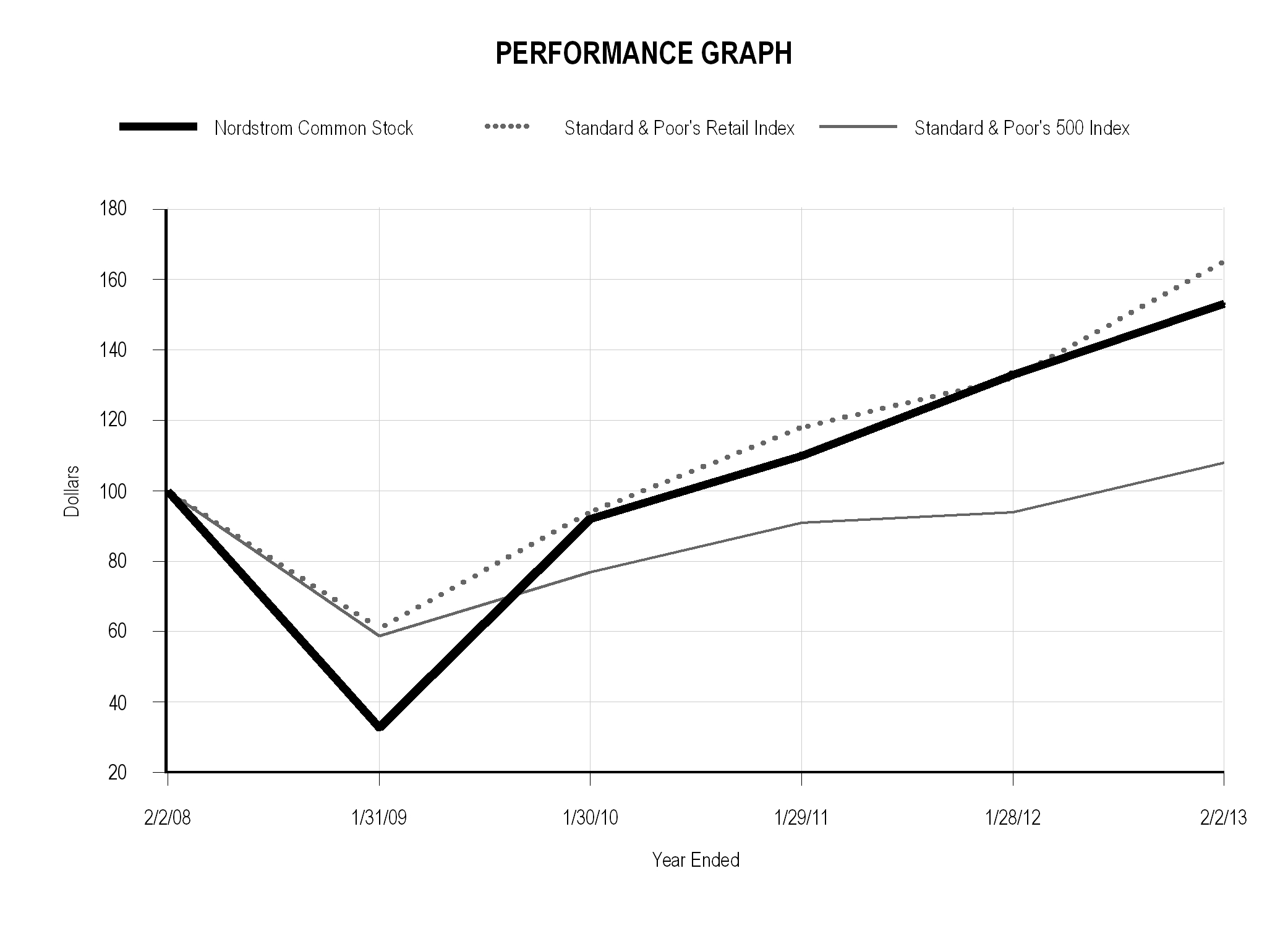

STOCK PRICE PERFORMANCE

The following graph compares for each of the last five fiscal years, ending February 2, 2013 , the cumulative total return of Nordstrom common stock, Standard & Poor's Retail Index and Standard & Poor's 500 Index. The Retail Index is comprised of 33 retail companies, including Nordstrom, representing an industry group of the Standard & Poor's 500 Index. The cumulative total return of Nordstrom common stock assumes $100 invested on February 2, 2008 in Nordstrom common stock and assumes reinvestment of dividends.

End of fiscal year | 2007 | |

| 2008 | |

| 2009 | |

| 2010 | |

| 2011 | |

| 2012 | |

Nordstrom common stock | 100 | |

| 33 | |

| 92 | |

| 110 | |

| 133 | |

| 153 | |

Standard & Poor's Retail Index | 100 | |

| 61 | |

| 94 | |

| 118 | |

| 132 | |

| 165 | |

Standard & Poor's 500 Index | 100 | |

| 59 | |

| 77 | |

| 91 | |

| 94 | |

| 108 | |

14

Table of Contents

Item 6. Selected Financial Data.

Dollars in millions except per square foot and per share amounts

Fiscal year | 2012 | |

| 2011 | |

| 2010 | |

| 2009 | |

| 2008 | | |||||

Earnings Results |

|

|

|

|

|

|

|

|

| ||||||||||

Net sales | | $11,762 | | | | $10,497 | | | | $9,310 | |

| | $8,258 | |

| | $8,272 | |

Credit card revenues | 386 | | | 380 | | | 390 | |

| 369 | |

| 301 | | |||||

Gross profit 1 | 4,330 | | | 3,905 | | | 3,413 | |

| 2,930 | |

| 2,855 | | |||||

Selling, general and administrative ("SG&A") expenses: |

|

|

|

|

|

|

|

|

| ||||||||||

Retail | (3,166 | ) | | (2,807 | ) | | (2,412 | ) |

| (2,109 | ) |

| (2,103 | ) | |||||

Credit | (205 | ) | | (229 | ) | | (273 | ) |

| (356 | ) |

| (274 | ) | |||||

Earnings before interest and income taxes ("EBIT") | 1,345 | | | 1,249 | | | 1,118 | |

| 834 | |

| 779 | | |||||

Net earnings | 735 | | | 683 | | | 613 | |

| 441 | |

| 401 | | |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Balance Sheet and Cash Flow Data |

|

|

|

|

|

|

|

|

| ||||||||||

Cash and cash equivalents | | $1,285 | |

| | $1,877 | |

| | $1,506 | |

| | $795 | |

| | $72 | |

Accounts receivable, net | 2,129 | | | 2,033 | |

| 2,026 | |

| 2,035 | |

| 1,942 | | |||||

Merchandise inventories | 1,360 | | | 1,148 | |

| 977 | |

| 898 | |

| 900 | | |||||

Current assets | 5,081 | | | 5,560 | |

| 4,824 | |

| 4,054 | |

| 3,217 | | |||||

Land, buildings and equipment, net | 2,579 | | | 2,469 | |

| 2,318 | |

| 2,242 | |

| 2,221 | | |||||

Total assets | 8,089 | | | 8,491 | |

| 7,462 | |

| 6,579 | |

| 5,661 | | |||||

Current liabilities | 2,226 | | | 2,575 | |

| 1,879 | |

| 2,014 | |

| 1,601 | | |||||

Long-term debt, including current portion | 3,131 | | | 3,647 | |

| 2,781 | |

| 2,613 | |

| 2,238 | | |||||

Shareholders' equity | 1,913 | | | 1,956 | |

| 2,021 | |

| 1,572 | |

| 1,210 | | |||||

Cash flow from operations | 1,110 | | | 1,177 | |

| 1,177 | |

| 1,251 | |

| 848 | | |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Performance Metrics |

|

|

|

|

|

|

|

|

| ||||||||||

Same-store sales percentage change 2 | 7.3 | % |

| 7.2 | % |

| 8.1 | % |

| (4.2 | %) |

| (9.0 | %) | |||||

Gross profit % of net sales | 36.8 | % |

| 37.2 | % |

| 36.7 | % |

| 35.5 | % |

| 34.5 | % | |||||

Retail SG&A % of net sales | 26.9 | % |

| 26.7 | % |

| 25.9 | % |

| 25.5 | % |

| 25.4 | % | |||||

Total SG&A % of net sales | 28.7 | % |

| 28.9 | % |

| 28.8 | % |

| 29.8 | % |

| 28.7 | % | |||||

EBIT % of net sales | 11.4 | % |

| 11.9 | % |

| 12.0 | % |

| 10.1 | % |

| 9.4 | % | |||||

Return on shareholders' equity | 38.0 | % |

| 34.3 | % |

| 34.1 | % |

| 31.7 | % |

| 34.5 | % | |||||

Return on assets | 8.9 | % | | 8.7 | % | | 8.6 | % | | 7.1 | % | | 7.0 | % | |||||

Return on invested capital ("ROIC") 3 | 13.9 | % | | 13.3 | % | | 13.6 | % | | 12.1 | % | | 11.6 | % | |||||

Sales per square foot 4 | | $470 | |

| | $431 | |

| | $397 | |

| | $368 | |

| | $388 | |

Ending inventory per square foot | | $53.77 | |

| | $46.41 | |

| | $40.96 | |

| | $39.44 | |

| | $41.14 | |

Inventory turnover rate 5 | 5.37 | |

| 5.56 | |

| 5.56 | |

| 5.41 | |

| 5.20 | | |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Per Share Information |

|

|

|

|

|

|

|

|

| ||||||||||

Earnings per diluted share | | $3.56 | | | | $3.14 | | | | $2.75 | |

| | $2.01 | |

| | $1.83 | |

Dividends declared per share | 1.08 | |

| 0.92 | |

| 0.76 | |

| 0.64 | |

| 0.64 | | |||||

Book value per share | 9.71 | |

| 9.42 | |

| 9.27 | |

| 7.22 | |

| 5.62 | | |||||

|

|

|

|

|

|

|

|

|

| ||||||||||

Store Information (at year-end) |

|

|

|

|

|

|

|

|

| ||||||||||

Nordstrom full-line stores | 117 | |

| 117 | |

| 115 | |

| 112 | |

| 109 | | |||||

Nordstrom Rack and other stores | 123 | |

| 108 | |

| 89 | |

| 72 | |

| 60 | | |||||

Total square footage | 25,290,000 | |

| 24,745,000 | |

| 23,838,000 | |

| 22,773,000 | |

| 21,876,000 | | |||||

1 | Gross profit is calculated as net sales less cost of sales and related buying and occupancy costs (for all segments). |

2 | Same-store sales include sales from stores that have been open at least one full year at the beginning of the year. Fiscal year 2012 includes an extra week (the 53 rd week) as a result of our 4-5-4 retail reporting calendar. The 53 rd week is not included in same-store sales calculations. We also include sales from our Nordstrom online store in same-store sales because of the integration of our Nordstrom full-line stores and online store. |

3 | See Return on Invested Capital ("ROIC") (Non-GAAP financial measure) on page 26 for additional information and reconciliation to the most directly comparable GAAP financial measure. |

4 | Sales per square foot is calculated as net sales divided by weighted-average square footage. Weighted-average square footage includes a percentage of year-end square footage for new stores equal to the percentage of the year during which they were open. |

5 | Inventory turnover rate is calculated as annual cost of sales and related buying and occupancy costs (for all segments) divided by 4-quarter average inventory. |

Nordstrom, Inc. and subsidiaries 15

Table of Contents

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Dollar, share and square footage amounts in millions except percentages, per share and per square foot amounts

OVERVIEW

Nordstrom is a leading fashion specialty retailer offering high-quality apparel, shoes, cosmetics and accessories for women, men and children. We offer a wide selection of brand name and private label merchandise through our various channels: 'Nordstrom' branded full-line stores and online at www.nordstrom.com, 'Nordstrom Rack' off-price stores, 'Last Chance' clearance store, 'HauteLook' online private sale subsidiary, 'Jeffrey' boutiques and our 'treasure&bond' philanthropic store. Our stores are located in 31 states throughout the United States. In addition, we offer our customers a loyalty program along with a variety of payment products and services, including credit and debit cards.

Our 2012 results reflected the ongoing, consistent strength of our business. For the third consecutive year, we achieved double-digit growth in net sales and earnings per diluted share, added over one billion dollars in net sales and delivered same-store sales growth of over 7%. These accomplishments reflect the high level of execution across all channels and our ongoing investments in improving the customer experience as we seek to enhance the merchandise offering, increase relevance with existing and new customers, and aggressively grow our online capabilities.

E-commerce is our fastest-growing business. We continued to make investments to improve the experience online by expanding our merchandise selection, enhancing the website and mobile experience with improvements to search, navigation and checkout, and increasing the speed of fulfillment and delivery. These investments helped drive same-store sales growth of 37% in our Direct channel on top of last year's 29% growth.

We also continue to grow through new opportunities to increase our market share. We announced plans for our initial entry into Canada, beginning with four full-line stores and with the potential for a total of eight to 10 full-line stores and 15 to 20 Rack stores. In addition, we are again increasing the pace of expansion of our Rack stores with plans to grow to over 230 stores by the end of 2016. We also announced plans to open our first full-line store in Manhattan, which will increase our exposure within a premiere retail market.

Our strong financial position enables us to invest in our stores through expansion, remodels and other initiatives to improve the customer experience. During 2012, we opened one Nordstrom full-line store, 15 Nordstrom Rack stores and relocated three Nordstrom Rack stores. Increasingly, we are using technology as an enabler of service. As an example, we now have mobile point-of-sale devices at all of our full-line and Rack stores to increase the speed at checkout and drive incremental volume. Additionally, mobile devices in our full-line stores have virtually the same functionality as our cash registers, and we continue to make progress in creating a fully mobile store environment.

Our credit business also plays an important role in reaching new customers and strengthening existing customer relationships through our Fashion Rewards program, payment products and our ability to serve customers directly through our wholly owned credit services. The Fashion Rewards program contributes to our overall results, with members shopping more frequently and spending more on average than non-members. In 2012, net sales from our members increased 23% over the prior year. With the launch of our enhanced program in early 2012, we opened over one million new accounts, and ended the year with 3.3 million active members, a 27% increase over last year. Our overall credit card portfolio also remains healthy, with delinquency and write-off trends at pre-recession levels.

Our ongoing focus on the customer drives the investments we are making to take advantage of multiple growth opportunities. The opportunities include Canada, Rack, e-commerce, Manhattan and other new full-line stores and provide a platform to deliver sustainable, profitable growth. As our business and operating model evolves with our growth, we remain focused on our overall financial goals of achieving high single-digit total sales growth and mid-teens Return on Invested Capital ("ROIC"), as these measures correlate strongly with shareholder return.

RESULTS OF OPERATIONS

Our reportable segments are Retail and Credit. Our Retail segment includes our Nordstrom branded full-line stores and website, our Nordstrom Rack stores, our Last Chance clearance store and our other retail channels including HauteLook, our Jeffrey stores and our treasure&bond store. For purposes of discussion and analysis of our results of operations, we combine our Retail segment results with revenues and expenses in the "Corporate/Other" column of our segment reporting footnote (collectively, the "Retail Business"). We analyze our results of operations through earnings before interest and income taxes for our Retail Business and earnings before income taxes for Credit, while interest expense and income taxes are discussed on a total company basis.

Similar to many other retailers, Nordstrom follows the retail 4-5-4 reporting calendar, which included an extra week in the fourth quarter of 2012 (the "53rd week"). The analysis of our results of operations, liquidity and capital resources compares the 53 weeks in 2012 to the 52 weeks in 2011. However, the 53rd week is not included in same-store sales calculations. In 2012, the 53rd week contributed approximately $0.04 to earnings per diluted share.

16

Table of Contents

Retail Business

Summary

Fiscal year |

| 2012 |

| 2011 |

| 2010 | |||||||||||||||

|

| Amount | |

| % of net sales | |

| Amount | |

| % of net sales | |

| Amount | |

| % of net sales | | |||

Net sales |

| | $11,762 | |

| 100.0 | % |

| | $10,497 | |

| 100.0 | % |

| | $9,310 | |

| 100.0 | % |

Cost of sales and related buying and occupancy costs |

| (7,318 | ) |

| (62.2 | %) |

| (6,517 | ) |

| (62.1 | %) |

| (5,831 | ) |

| (62.6 | %) | |||

Gross profit |

| 4,444 | |

| 37.8 | % |

| 3,980 | |

| 37.9 | % |

| 3,479 | |

| 37.4 | % | |||

Selling, general and administrative expenses |

| (3,166 | ) |

| (26.9 | %) |

| (2,807 | ) |

| (26.7 | %) |

| (2,412 | ) |

| (25.9 | %) | |||

Earnings before interest and income taxes |

| | $1,278 | |

| 10.9 | % |

| | $1,173 | |

| 11.2 | % |

| | $1,067 | |

| 11.5 | % |

Fiscal year | 2012 | |

| 2011 | |

| 2010 | | |||

Net sales by channel: |

|

|

|

|

| ||||||

Nordstrom full-line stores | | $7,964 | |

| | $7,513 | | | | $6,995 | |

Direct | 1,269 | |

| 913 | | | 705 | | |||

Nordstrom | 9,233 | |

| 8,426 | |

| 7,700 | | |||

Nordstrom Rack | 2,445 | |

| 2,045 | |

| 1,691 | | |||

Other retail 1 | 271 | |

| 185 | |

| 29 | | |||

Total Retail segment | 11,949 | |

| 10,656 | |

| 9,420 | | |||

Corporate/Other | (187 | ) |

| (159 | ) |

| (110 | ) | |||

Total net sales | | $11,762 | |

| | $10,497 | |

| | $9,310 | |

|

|

|

|

|

| ||||||

Net sales increase | 12.1 | % |

| 12.7 | % |

| 12.7 | % | |||

|

|

|

|

|

| ||||||

Same-store sales increase by channel: |

|

|

|

|

| ||||||

Nordstrom full-line stores | 3.9 | % |

| 6.0 | % |

| 7.9 | % | |||

Direct | 37.1 | % |

| 29.5 | % |

| 25.1 | % | |||

Nordstrom | 7.5 | % |

| 8.2 | % |

| 9.3 | % | |||

Nordstrom Rack | 7.4 | % |

| 3.7 | % |

| 0.7 | % | |||

Total | 7.3 | % |

| 7.2 | % |

| 8.1 | % | |||

|

|

|

|

|

| ||||||

Sales per square foot | | $470 | |

| | $431 | |

| | $397 | |

4-wall sales per square foot 2 | | $417 | |

| | $394 | |

| | $372 | |

|

|

|

|

|

| ||||||

Percentage of net sales by merchandise category: |

|

|

|

|

| ||||||

Women's apparel | 31 | % |

| 33 | % |

| 34 | % | |||

Shoes | 23 | % |

| 23 | % |

| 23 | % | |||

Men's apparel | 16 | % |

| 15 | % |

| 15 | % | |||

Women's accessories | 13 | % |

| 12 | % |

| 12 | % | |||

Cosmetics | 11 | % |

| 11 | % |

| 10 | % | |||

Kids' apparel | 3 | % |

| 3 | % |

| 3 | % | |||

Other | 3 | % |

| 3 | % |

| 3 | % | |||

Total | 100 | % |

| 100 | % |

| 100 | % | |||

1 Other retail includes our HauteLook online private sale subsidiary, our Jeffrey stores and our treasure&bond store.

2 4-wall sales per square foot is calculated as sales for Nordstrom full-line, Nordstrom Rack, Jeffrey and treasure&bond stores divided by their weighted-average square footage. Weighted-average square footage includes a percentage of period-end square footage for new stores equal to the percentage of the period during which they were open.

Nordstrom, Inc. and subsidiaries 17

Table of Contents

NET SALES – 2012 VS 2011

Our total net sales increase of 12.1% for 2012 was driven by the same-store sales increase of 7.3% and strong performances across all channels. Our sales productivity continued to improve, reaching a high of $470 in sales per square foot in 2012 from increases in both our stores and online. During the year, we opened one Nordstrom full-line store, 15 Nordstrom Rack stores and relocated three Nordstrom Rack stores. These additions represented 1.5% of our total net sales for 2012 , and increased our square footage by 2.2% . The 53rd week contributed approximately $162 in additional net sales.

Nordstrom net sales for 2012 were $9,233 , an increase of 9.6% compared with 2011 , with same-store sales up 7.5% . Our sales growth was due in large part to the ongoing, consistent strength of our business both in store and online. We enhanced our Fashion Rewards loyalty program and expanded our relationship with our customers. At the same time, we made investments to improve the in-store, online and mobile experience. Both the number of items sold and the average selling price increased in 2012 compared with 2011 . Category highlights included Handbags , Men's Shoes , Men's Apparel and Cosmetics . We also saw improvements in our Women's Apparel business in the second half of the year.

Full-line net sales for 2012 were $7,964 , an increase of 6.0% compared with 2011 , with same-store sales up 3.9% . The top-performing geographic regions for full-line stores for 2012 were the South and Midwest . The Direct channel continued to show strong sales growth with net sales of $1,269 , an increase of 39% compared with 2011 , with same-store sales up 37% on a comparable 52-week basis. These increases significantly outpaced our overall performance and are reflective of how customers are responding to our ongoing e-commerce initiatives.

Nordstrom Rack net sales were $2,445 , an increase of 20% compared with 2011 , while same-store sales increased 7.4% for the year. Men's Apparel , Shoes and Women's Apparel were the strongest performing categories for the year. Both the number of items sold and the average selling price increased in 2012 compared with 2011 .

NET SALES – 2011 VS 2010

Net sales for 2011 increased 12.7% compared with 2010 , while same-store sales increased 7.2% . During 2011 , we opened three Nordstrom full-line stores, 18 Nordstrom Rack stores and one treasure&bond store, relocated two Nordstrom Rack stores and acquired HauteLook. These additions represented 4.0% of our total net sales for 2011 , and increased our square footage by 3.8% .

Nordstrom net sales for 2011 were $8,426 , up 9.4% compared with 2010 , with same-store sales up 8.2% . Our sales growth was driven by our merchandising, inventory management and multi-channel initiatives as well as our efforts to build stronger relationships with customers and to improve the shopping experience across all channels. Both the average selling price and the number of items sold increased in 2011 compared with 2010 . Category highlights included Designer , Handbags and Shoes .

Full-line net sales for 2011 were $7,513 , an increase of 7.4% compared with 2010 , with same-store sales up 6.0% . The top-performing geographic regions for full-line stores for 2011 were the South and Midwest . The Direct channel continued to show strong sales growth with net sales of $913 , an increase of 30% in 2011 compared with 2010 .

Nordstrom Rack net sales were $2,045 , up 21% compared with 2010 , while same-store sales increased 3.7% for the year. Shoes , Dresses and Accessories were the strongest performing categories for the year. Both the average selling price and the number of items sold increased in 2011 compared with 2010 .

18

Table of Contents

Fiscal year | 2012 | |

| 2011 | |

| 2010 | | |||

Gross profit 1 | | $4,444 | |

| | $3,980 | | | | $3,479 | |

Gross profit rate | 37.8 | % |

| 37.9 | % | | 37.4 | % | |||

Ending inventory per square foot | | $53.77 | |

| | $46.41 | |

| | $40.96 | |

Inventory turnover rate 2 | 5.37 | |

| 5.56 | |

| 5.56 | | |||

1 | Retailers do not uniformly record the costs of buying and occupancy and supply chain operations (freight, purchasing, receiving, distribution, etc.) between gross profit and selling, general and administrative expense. As such, our gross profit and selling, general and administrative expenses and rates may not be comparable to other retailers' expenses and rates. |

2 | Inventory turnover rate is calculated as annual cost of sales and related buying and occupancy costs (for all segments) divided by 4-quarter average inventory. |

GROSS PROFIT – 2012 VS 2011

Retail gross profit increased $464 in 2012 compared with 2011 due to our strong sales performance, partially offset by an increase in occupancy costs for our investments in new stores and remodeling of existing stores. Our gross profit rate decreased 13 basis points compared with 2011 primarily due to accelerated Rack growth, which carries a lower gross profit rate relative to our other channels, and overall occupancy costs that outpace sales in the early years following a store opening. With Rack's high sales productivity and return on invested capital, as well as the availability of what we believe are numerous quality locations, we plan to continue to grow our Rack channel.

Our inventory turnover rate decreased to 5.37 times in 2012, from 5.56 times in 2011. This was primarily due to our increased investment in pack and hold inventory at Nordstrom Rack, which involves the acquisition of merchandise from some of our top brands in advance of the upcoming selling seasons in order to take advantage of strategic buying opportunities. We hold this inventory in our warehouses for six months on average until the next selling season and it represents approximately 10% of our total inventory at the end of 2012 compared with 3% in 2011. On a per square foot basis, we ended the year with a 15.8% increase in our ending inventory on a 9.0% increase in sales compared with 2011. The increase in ending inventory per square foot relative to the increase in sales per square foot is primarily due to Rack's growth.

GROSS PROFIT – 2011 VS 2010

Retail gross profit increased $501 in 2011 compared with 2010 primarily due to higher sales and merchandise margin, partially offset by increases in occupancy costs for stores opened during both 2011 and 2010 . Our gross profit rate improved 54 basis points compared with 2010 primarily due to leveraging buying and occupancy costs on higher net sales. Our increase in ending inventory per square foot of 13.3% on an 8.5% increase in sales per square foot is a result of our growth initiatives including expansion of our Rack business.

Fiscal year | 2012 | |

| 2011 | |

| 2010 | | |||

Selling, general and administrative expenses | | $3,166 | |

| | $2,807 | |

| | $2,412 | |

Selling, general and administrative rate | 26.9 | % |

| 26.7 | % |

| 25.9 | % | |||

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES – 2012 VS 2011

Our Retail selling, general and administrative expenses ("Retail SG&A") increased $359 in 2012 compared with 2011 . This increase reflects the investments we made to improve the customer experience across all channels and specifically in our e-commerce business as we expanded our capabilities and increased the speed of fulfillment and delivery. The increase also reflected higher sales volume and the opening of 16 stores in 2012 . Our Retail SG&A rate increased 18 basis points for 2012 compared with 2011 due to the increased investments, partially offset by leverage on increased sales.

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES – 2011 VS 2010

Our Retail SG&A expenses increased $395 in 2011 compared with 2010 . This increase reflects initiatives to improve the shopping experience across all channels and specifically to grow our e-commerce business. The increase was also due in part to higher sales volume and the opening of 22 stores in 2011 . As a result, our Retail SG&A rate increased 84 basis points for 2011 compared with 2010 . We continued to leverage SG&A expense in our stores, with an improvement of approximately 35 basis points in 2011 , compared with 2010 .

Nordstrom, Inc. and subsidiaries 19

Table of Contents

Credit Segment

The Nordstrom credit and debit card products are designed to strengthen customer relationships and grow retail sales by providing loyalty benefits, valuable services and payment products. We believe that owning all aspects of our credit business allows us to build deeper relationships with our customers by fully integrating our rewards program with our retail stores and providing better service, which in turn fosters greater customer loyalty. Our cardholders tend to visit our stores more frequently and spend more with us than non-cardholders, and we believe the Nordstrom Fashion Rewards ® program helps drive sales in our Retail segment. Our Nordstrom private label credit and debit cards can be used only in our Nordstrom full-line and Rack stores and on our website ("inside volume"), while our Nordstrom VISA cards also may be used for purchases outside of Nordstrom ("outside volume"). Cardholders participate in the Nordstrom Fashion Rewards program through which customers accumulate points based on their level of spending. Upon reaching a certain threshold, customers receive Nordstrom Notes ® , which can be redeemed for goods or services in our full-line stores, at Nordstrom Rack and online. Fashion Rewards customers receive a credit for complimentary alterations and a personal triple points day, in addition to early access to sales events. With increased spending, they can receive additional amounts of these benefits as well as access to exclusive fashion and shopping events.

The table below provides a detailed view of the operational results of our Credit segment, consistent with the segment disclosure provided in the Notes to Consolidated Financial Statements. In order to better reflect the economic contribution of our credit and debit card program, intercompany merchant fees are also included in the table below, which represents the estimated costs that would be incurred if our customers used third-party cards.

Fiscal year |

| 2012 |

| 2011 |

| 2010 | |||||||||||||||

|

| Amount | |

| % of average credit card receivables | |

| Amount | |

| % of average credit card receivables | |

| Amount | |

| % of average credit card receivables | | |||

Credit card revenues |

| | $386 | |

| 18.6 | % |

| | $380 | |

| 18.6 | % |

| | $390 | |

| 18.7 | % |

Interest expense |

| (26 | ) |

| (1.2 | %) |

| (13 | ) |

| (0.7 | %) |

| (21 | ) |

| (1.0 | %) | |||

Net credit card income |

| 360 | |

| 17.3 | % |

| 367 | |

| 17.9 | % |

| 369 | |

| 17.7 | % | |||

Cost of sales and related buying and occupancy costs – loyalty program |

| (114 | ) |

| (5.5 | %) |

| (75 | ) |

| (3.7 | %) |

| (66 | ) |

| (3.2 | %) | |||

Selling, general and administrative expenses |

| (205 | ) |

| (9.8 | %) |

| (229 | ) |

| (11.2 | %) |

| (273 | ) |

| (13.1 | %) | |||

Total expense |

| (319 | ) |

| (15.3 | %) |

| (304 | ) |

| (14.9 | %) |

| (339 | ) |

| (16.3 | %) | |||

Credit segment earnings before income taxes, as presented in segment disclosure |

| 41 | |

| 2.0 | % |

| 63 | |

| 3.1 | % |

| 30 | |

| 1.4 | % | |||

Intercompany merchant fees |

| 89 | |

| 4.3 | % |

| 71 | |

| 3.5 | % |

| 58 | |

| 2.8 | % | |||

Credit segment contribution, before income taxes |

| | $130 | |

| 6.3 | % |

| | $134 | |

| 6.6 | % |

| | $88 | |

| 4.2 | % |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

Credit and debit card volume: |

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

Outside |

| | $4,305 | |

|

|

| | $4,101 | |

|

|

| | $3,838 | |

|

| |||

Inside |

| 4,484 | |

|

|

| 3,596 | |

|

|

| 2,953 | |

|

| ||||||

Total volume |

| | $8,789 | |

|

|

| | $7,697 | |

|

|

| | $6,791 | |

|

| |||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||

Average credit card receivables |

| | $2,076 | |

|

|

| | $2,047 | |

|

|

| | $2,088 | |

|

| |||

Average credit card receivable investment 1 |

| | $415 | |

|

|

| | $409 | |

|

|

| | $418 | |

|

| |||

Credit segment contribution 2 |

| 19.4 | % |

|

|

| 20.0 | % |

|

|

| 12.8 | % |

|

| ||||||

2 Net of tax, calculated as a percentage of our average credit card receivable investment.

20

Table of Contents

Fiscal year | 2012 | |

| 2011 | |

| 2010 | | |||

Finance charge revenue | | $254 | |

| | $251 | |

| | $266 | |

Interchange - third party | 84 | |

| 82 | |

| 76 | | |||

Late fees and other revenue | 48 | |

| 47 | |

| 48 | | |||

Total credit card revenues | | $386 | |

| | $380 | |

| | $390 | |

Credit card revenues include finance charges, interchange fees, late fees and other revenue. Finance charges represent interest earned on unpaid balances while interchange fees are earned from the use of Nordstrom VISA credit cards at merchants outside of Nordstrom. Late fees are assessed when a credit card account becomes delinquent. We consider an account delinquent if the minimum payment is not received by the payment due date.

CREDIT CARD REVENUES – 2012 VS 2011

Credit card revenues increased $6 in 2012 compared with 2011 primarily due to an extra week (the 53 rd week) of revenue in 2012 as a result of our 4-5-4 retail reporting calendar. The increase is also due to growth in total volume that was offset by continued improvements in customer payment rates. Our average credit card receivable balance in 2012 was $2,076 , an increase of $29 , or 1.4% , from 2011 .

CREDIT CARD REVENUES – 2011 VS 2010

Credit card revenues decreased $10 in 2011 compared with 2010 primarily due to a decrease in finance charge revenue resulting from continued improvements in customer payment rates that drove lower finance charge yields and slightly lower receivables. Our average credit card receivable balance in 2011 was $2,047 , a decrease of $41 , or 1.9% , from 2010 . These decreases were partially offset by an increase in interchange revenue due to increased use of our Nordstrom VISA credit cards at third parties.

Credit Segment Interest Expense

Interest expense increased to $26 in 2012 from $13 in 2011 and $21 in 2010 primarily due to higher average interest rates applicable to the Credit segment.

Credit Segment Cost of Sales and Related Buying and Occupancy Costs

COST OF SALES AND RELATED BUYING AND OCCUPANCY COSTS – 2012 VS 2011

Cost of sales and related buying and occupancy costs, which include the estimated cost of Nordstrom Notes that we expect to issue and ultimately be redeemed and complimentary alterations under our Fashion Rewards program, increased to $114 in 2012 compared with $75 in 2011 . The increase was due to enhancements to our Fashion Rewards program and increases in Nordstrom credit and debit card volumes of 14.2% . We provide the Fashion Rewards benefits to our members, as participation in the program enhances customer loyalty and drives incremental sales in our stores and online.

COST OF SALES AND RELATED BUYING AND OCCUPANCY COSTS – 2011 VS 2010

Cost of sales and related buying and occupancy costs increased to $75 in 2011 compared with $66 in 2010 . The increase was due to additional expenses related to the Fashion Rewards program as a result of a 13.3% increase in volume on Nordstrom credit and debit cards and increased utilization of program benefits.

Credit Segment Selling, General and Administrative Expenses

Fiscal year | 2012 | |

| 2011 | |

| 2010 | | |||

Operational and marketing expenses | | $149 | |

| | $128 | |

| | $124 | |

Bad debt provision | 56 | |

| 101 | |

| 149 | | |||

Total Credit selling, general and administrative expenses | | $205 | |

| | $229 | |

| | $273 | |

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES – 2012 VS 2011

Total Credit SG&A decreased $24 in 2012 compared with 2011 , due to lower bad debt expense, partially offset by increases in operational and marketing expenses. The decrease in bad debt expense reflects continued improvement in our portfolio delinquencies and write-off results, which are further discussed below. The increase in operational and marketing expenses was primarily driven by enhancements in our Fashion Rewards benefits.

SELLING, GENERAL AND ADMINISTRATIVE EXPENSES – 2011 VS 2010

Total Credit SG&A decreased $44 in 2011 compared with 2010, due primarily to lower bad debt expense. The decrease in bad debt expense reflected continued improvement in our portfolio trends, the overall performance of our credit portfolio and economic trends.

Nordstrom, Inc. and subsidiaries 21

Table of Contents

Allowance for Credit Losses and Credit Trends

Fiscal year | 2012 | |

| 2011 | |

| 2010 | | |||

Allowance at beginning of year | | $115 | |

| | $145 | |

| | $190 | |

Bad debt provision | 56 | |

| 101 | |

| 149 | | |||

Write-offs | (111 | ) |

| (153 | ) |

| (211 | ) | |||

Recoveries | 25 | |

| 22 | |

| 17 | | |||