UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 26, 2015. |

| or |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to . |

Commission File Number 000-06217

|

INTEL CORPORATION

(Exact name of registrant as specified in its charter)

Delaware |

| 94-1672743 |

State or other jurisdiction of incorporation or organization |

| (I.R.S. Employer Identification No.) |

|

|

|

2200 Mission College Boulevard, Santa Clara, California |

| 95054-1549 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code (408) 765-8080

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Common stock, $0.001 par value |

| The NASDAQ Global Select Market* |

Securities registered pursuant to Section 12(g) of the Act:

None

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every interactive data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer x |

| Accelerated filer ¨ |

| Non-accelerated filer ¨ |

| Smaller reporting company ¨ |

|

| |

| (Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

Aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of June 26, 2015 , based upon the closing price of the common stock as reported by The NASDAQ Global Select Market on such date, was

$147.3 billion

4,724 million shares of common stock outstanding as of February 5, 2016

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's proxy statement related to its 2016 Annual Stockholders' Meeting to be filed subsequently are incorporated by reference into Part III of this Annual Report on Form 10-K. Except as expressly incorporated by reference, the registrant's proxy statement shall not be deemed to be part of this report.

INTEL CORPORATION

FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 26, 2015

INDEX

| Page | |

| ||

PART I | ||

Item 1. | Business | 1 |

Item 1A. | Risk Factors | 20 |

Item 1B. | Unresolved Staff Comments | 28 |

Item 2. | Properties | 28 |

Item 3. | Legal Proceedings | 28 |

Item 4. | Mine Safety Disclosures | 28 |

| ||

PART II | ||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 29 |

Item 6. | Selected Financial Data | 31 |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 32 |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 56 |

Item 8. | Financial Statements and Supplementary Data | 58 |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 124 |

Item 9A. | Controls and Procedures | 124 |

Item 9B. | Other Information | 125 |

| ||

PART III | ||

Item 10. | Directors, Executive Officers and Corporate Governance | 126 |

Item 11. | Executive Compensation | 126 |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 127 |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 127 |

Item 14. | Principal Accounting Fees and Services | 127 |

| ||

PART IV | ||

Item 15. | Exhibits, Financial Statement Schedules | 128 |

Table of Contents

PART I

ITEM 1. | BUSINESS |

Company Overview

We are a leader in the design and manufacturing of advanced integrated digital technology platforms. A platform consists of a microprocessor and chipset, and may be enhanced by additional hardware, software, and services. We sell these platforms primarily to original equipment manufacturers (OEMs), original design manufacturers (ODMs), and industrial and communications equipment manufacturers in the computing and communications industries . Our platforms are used across the compute continuum, in notebooks (including Ultrabook ™ devices), 2 in 1 systems, desktops, servers, tablets, phones, and the Internet of Things (including wearables, retail devices, and manufacturing devices). We also develop and sell software and services primarily focused on security and technology integration. We were incorporated in California in 1968 and reincorporated in Delaware in 1989.

Company Strategy

Our vision is if it is smart and connected, it is best with Intel ® . As a result, our strategy is to offer complete and connected platform computing solutions, consisting of both hardware and software, and to continue to drive "Moore's Law." Through enhanced energy-efficient performance, connectivity, and security, we enable platform solutions that span the compute continuum, from high-performance computing systems running trillions of operations per second to embedded applications consuming milliwatts of power.

The boundaries of computing itself are expanding, with billions of devices connected to the Internet and to one another. Computing is becoming increasingly personal and enhancing nearly all aspects of life, an evolution that we refer to as the "personalization of compute." As the personalization of compute continues, we believe the following three key assumptions are critical to our strategy:

• | sensification of compute - as computing becomes increasingly personal, users will demand that it capture the human senses such as sight, sound, and touch; |

• | smart and connected - more and more devices will be able to process data and connect to the cloud, other devices, or people; and |

• | extension of you - increasingly personal digital devices and their many form factors will become even more ubiquitous in our lives. |

1

Table of Contents

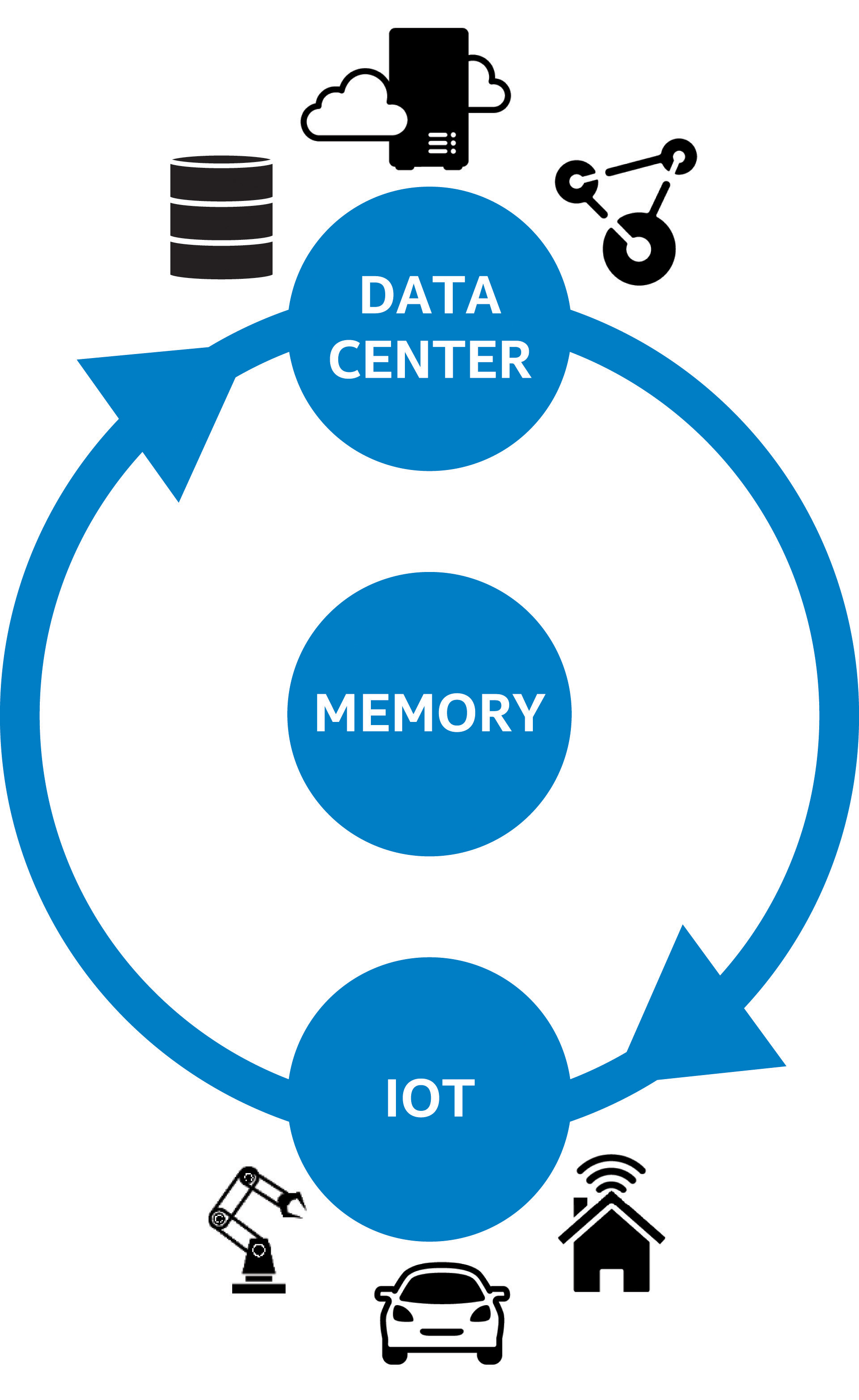

As more devices become smart and connected, specifically in the Internet of Things (IOT), there is greater demand for data centers to not only connect these devices, but also to capture and analyze the data they create. In addition, improvements in memory technology are enabling faster and more efficient microprocessors. We call the cycle of growth that occurs as these three market segments feed each other the "Virtuous Cycle of Growth." As we execute to our strategy, these market segments will continue to have greater impact on our results and our future as a company. We expect that our acquisition of Altera Corporation (Altera), completed subsequent to fiscal year-end 2015, will benefit this cycle of growth. The Altera acquisition is an example of our efforts to expand our reach within the compute continuum, as we believe that combining our leading-edge products and manufacturing process with Altera's leading field-programmable gate array (FPGA) technology will enable new classes of platforms that meet customer needs in the data center and Internet of Things market segments. | Virtuous Cycle of Growth |

| |

To succeed in this changing computing environment, we have the following key objectives:

• | relentlessly pursue Moore's Law to maximize and extend our manufacturing technology leadership; |

• | strive to ensure that Intel ® technology is the best choice across the compute continuum and across any operating system; |

• | enable smart and connected devices through continued development of industry-leading communications and connectivity technology; |

• | expand platforms into adjacent market segments to bring compelling new platform solutions and user experiences to form factors across the compute continuum; |

• | increase the utilization of our investments in intellectual property and research and development (R&D) across all market segments; |

• | expand the data center, the Internet of Things, and next-generation memory; |

• | scale our manufacturing capabilities into foundry; and |

• | strive to increase the diversity and inclusion of our workforce, reduce the environmental footprint of our products and operations, and be an asset to the communities where we conduct business. |

We use our core assets to meet these objectives. We believe that applying our core assets to our key objectives provides us with the scale, capacity, and global reach to establish new technologies and respond to customers' needs quickly. Our core assets and key objectives include the following:

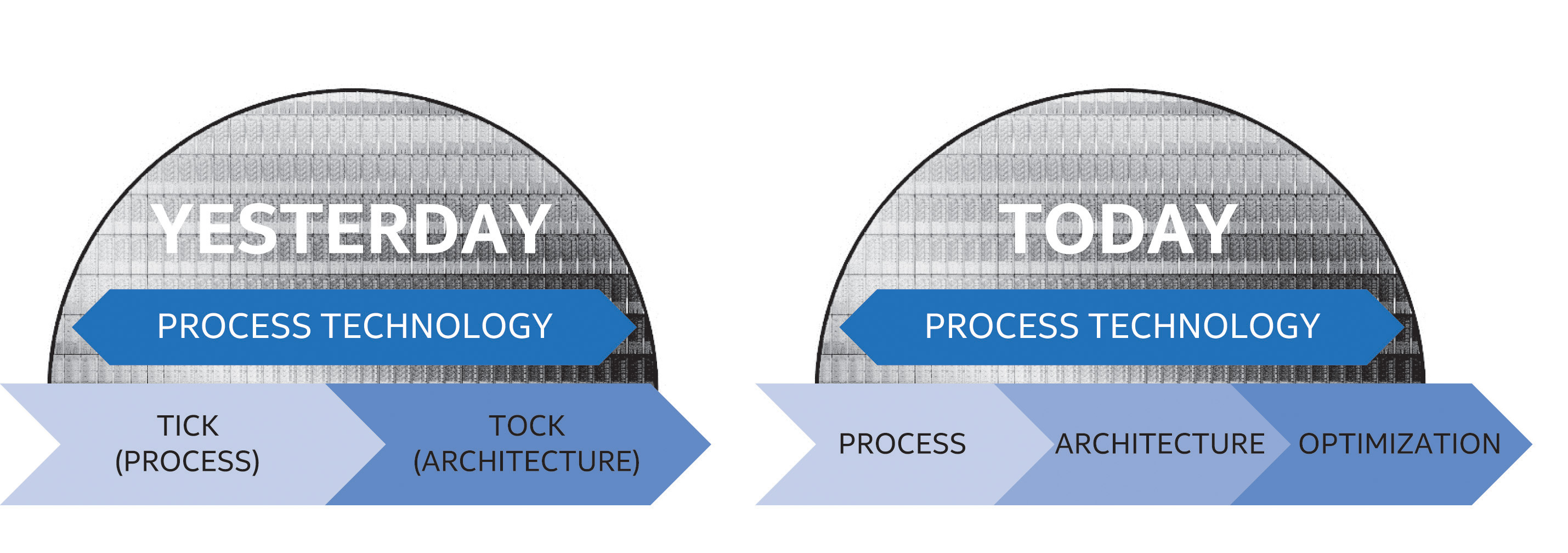

• | Silicon and Manufacturing Technology Leadership. We have long been a leader in silicon process technology and manufacturing, and we aim to continue our lead through investment and innovation in this critical area. Intel co-founder Gordon Moore predicted, in what has become known as Moore's Law, that transistor density on integrated circuits would double about every two years. We continue executing to Moore's Law by enabling new devices with higher functionality and complexity while controlling power, cost, and size. In keeping with Moore's Law, we drive a regular and predictable upgrade cycle-introducing the next generation of silicon process technology approximately every two to three years. Through this cycle, we continue to push progress by designing and putting transistor innovations into high-volume production. We aim to have the best process technology, and unlike many semiconductor companies, we primarily manufacture our products in our own facilities. This in-house manufacturing capability enables us to optimize performance, shorten our time-to-market, and scale new products more rapidly. We believe this competitive advantage will be extended in the future as the costs to build leading-edge fabrication facilities increase, and as fewer semiconductor companies will be able to leverage platform design and manufacturing. |

2

Table of Contents

• | Architecture and Platforms. We believe that users want consistent computing experiences and interoperable devices, and that users and developers value consistency of a standardized architecture. This standardized architecture provides a common framework that results in shortened time-to-market, increased innovation, and the ability to leverage technologies across multiple form factors. We have an advantage over most competitors because we are able to share intellectual property across our platforms and operating segments, which reduces our costs and provides a higher return on capital in our growth market segments (e.g., the data center, Internet of Things, and memory) . The combination of our shared intellectual property portfolio and our interchangeable manufacturing and assembly and test assets allows us to seamlessly shift our production capabilities to respond to market demand. We believe that we can meet the needs of users and developers by offering complete solutions across the compute continuum through our partnership with the industry on open, standards-based platform innovation around Intel ® architecture. We continue to invest in improving Intel architecture to deliver increased value to our customers and expand the capabilities of the architecture in adjacent market segments. For example, we focus on delivering improved energy-efficient performance, which involves balancing higher performance with the lowest power. In addition, the personalization of compute continues to drive our strategy as we focus on technologies such as perceptual computing, which brings exciting experiences through devices that sense, perceive, and interact with the user's actions. |

• | Software and Services. We offer software and services that provide solutions through a combination of hardware and software for consumer and corporate environments. Additionally, we seek to enable and advance the computing ecosystem by providing development tools and support to assist software developers in creating software applications that take advantage of our platforms. We seek to expedite growth in various market segments through our software offerings. We continue to collaborate with companies to develop software platforms that are optimized for Intel ® processors, and that support multiple hardware architectures and operating systems. |

• | Security . Through our expertise in hardware and software, we are able to embed security into many facets of computing and bring unique hardware, software, and end-to-end security solutions to the market. We offer proactive solutions and services to help secure the world's most critical systems and networks. Additionally, through our McAfee ® security products, we protect consumers and businesses of all sizes by helping detect and eliminate ever-evolving security threats. |

• | Customer Orientation. We focus on providing compelling user experiences by developing our next generation of products based on customer needs and expectations. In turn, our products help enable the design and development of new user experiences, form factors, and usage models for businesses and consumers. For example, we enhance the computing experience by providing Intel ® RealSense ™ technology, password elimination, and our next-generation Thunderbolt ™ 3 technology. Our latest Thunderbolt technology significantly increases the speed at which data and video can be transferred on a single cable, while simultaneously supplying power. We offer platforms that incorporate various components and capabilities designed and configured to work together to provide an optimized solution that customers can easily integrate into their products. Additionally, we have entered into strategic partnerships across multiple industries with a variety of manufacturers, including: Microsoft Corporation; Fossil Group, Inc.; LVMH Moët Hennessy Louis Vuitton SE; SMS Audio, LLC; Opening Ceremony, LLC; and others. Furthermore, we promote industry standards that we believe will yield innovation and improved technologies for users. |

3

Table of Contents

• | Acquisitions and Strategic Investments. In Q1 2016, we completed the acquisition of Altera. Altera is a global semiconductor company that designs and sells programmable semiconductors and related products, including programmable logic devices-which incorporate FPGAs and complex programmable logic devices-and highly integrated System-on-Chip (SoC) devices. As a result of the acquisition, we expect to integrate approximately 3,000 Altera employees. The acquisition of Altera reflects our strategy to drive Moore's Law and fuel growth in the data center and Internet of Things market segments. As we develop future platforms, the integration of PLDs into our platform solutions will improve the overall performance and lower the cost of ownership for our customers. Additionally, we make investments in companies around the world that we believe will further our vision, mission, and strategic objectives; support our key business initiatives; and generate financial returns. Our investments-including those made through Intel Capital-generally focus on companies and initiatives that we believe will stimulate growth in the digital economy, create new business opportunities for Intel, and expand global markets for our products. During 2015, we invested $966 million in Beijing UniSpreadtrum Technology Ltd. (UniSpreadtrum), a holding company under Tsinghua Unigroup Ltd. (an operating subsidiary of Tsinghua Holdings Co. Ltd.), to, among other things, jointly develop Intel architecture-based and communications-based solutions for phones. Additionally, we plan to continue to purchase and license intellectual property to support our current and expanding business. |

• | Corporate Responsibility. Diversity and inclusion are integral parts of Intel's competitive strategy and vision. In January 2015, Intel announced the Diversity in Technology initiative, setting a goal to achieve higher representation of women and underrepresented minorities in Intel's U.S. workforce by 2020. We are also investing $300 million to help build the STEM pipeline, to support hiring and retaining more women and underrepresented minorities, and to fund programs to support more positive representation within the technology and gaming industries. We are committed to empowering people and expanding economic opportunity through education and technology, driven by our corporate and Intel Foundation programs, policy leadership, and collaborative engagements. In addition, we strive to cultivate an inclusive work environment in which engaged, energized employees can thrive in their jobs and in their communities. We work to develop energy-efficient technology solutions that can be used to address major global problems while reducing our environmental impact. We have also led the industry on the "conflict minerals" issue and have worked extensively since 2008 to put in place processes and systems to develop ethical sourcing of tin, tantalum, tungsten, and gold for Intel and to prevent profits from the sale of those minerals from funding conflict in the Democratic Republic of the Congo (DRC) and adjoining countries. |

We strive to strengthen our competitive position as we enter and expand into adjacent market segments. These market segments change rapidly, and we need to adapt to new environments. A key characteristic of these adjacent market segments is low power consumption based on SoC products. We are making significant investments in this area with the accelerated development of our SoC solutions based on the 64-bit Intel ® Atom ™ microarchitecture and Intel ® Quark ™ technology. We are also optimizing our server products for energy-efficient performance, as we believe that increased Internet traffic and the use of mobile devices, the Internet of Things, and data center applications have created the need for improved data center infrastructure and energy efficiency.

4

Table of Contents

Business Organization

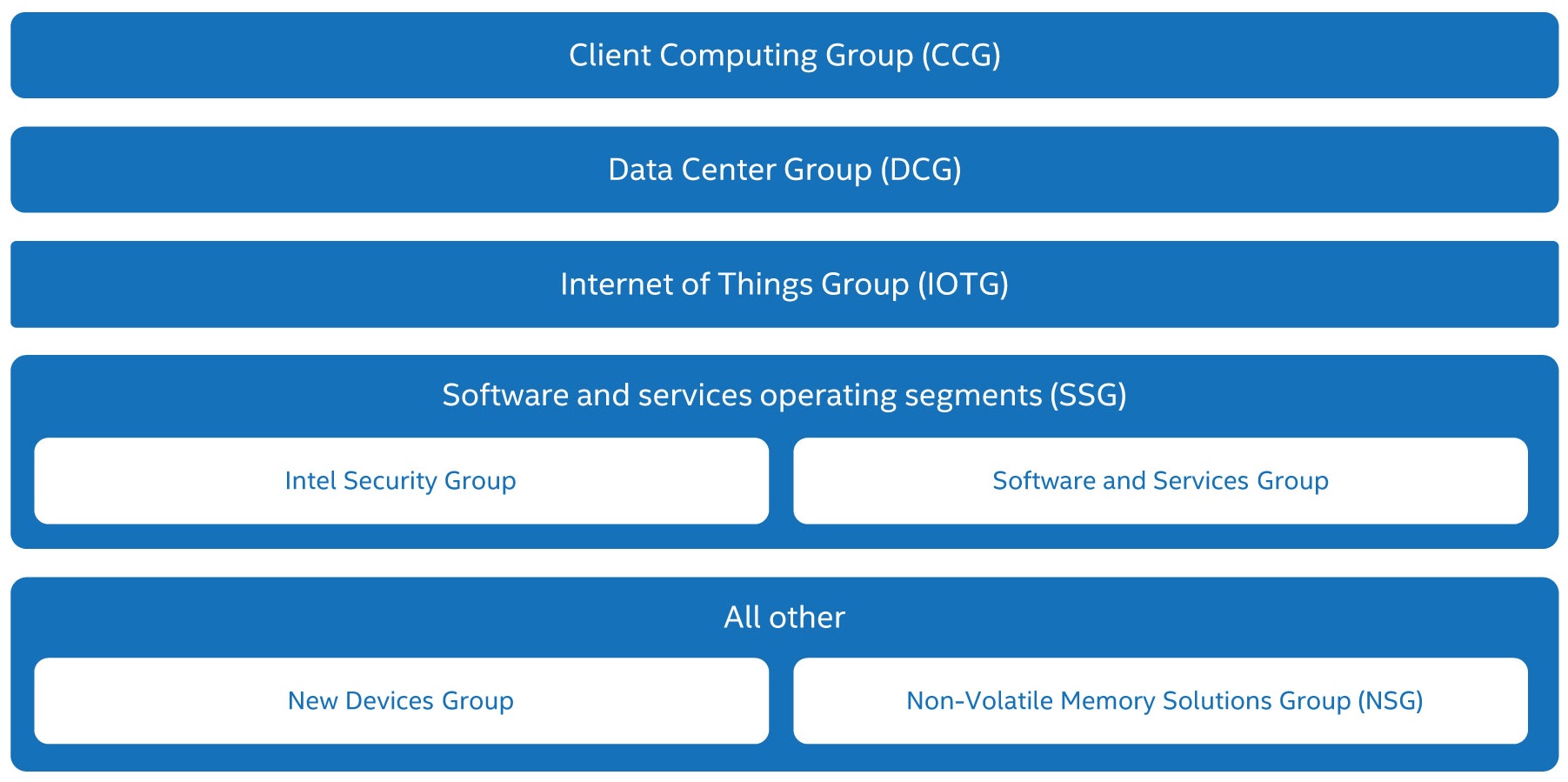

In Q1 2015, we made changes in our organizational structure to reflect our strategy to address all aspects of the client computing market segment and utilize our intellectual property to offer compelling customer solutions. As of December 26, 2015 , we manage our business through the following operating segments:

For a description of our operating segments, see " Note 26: Operating Segments and Geographic Information " in Part II, Item 8 of this Form 10-K.

Products

Platforms

We offer platforms that incorporate various components and technologies, including a microprocessor and chipset, a stand-alone SoC, or a multichip package. A platform may be enhanced by additional hardware, software, and services.

A microprocessor-the central processing unit (CPU) of a computer system-processes system data and controls other devices in the system. We offer microprocessors with one or multiple processor cores. Multi-core microprocessors can enable improved multitasking and energy-efficient performance by distributing computing tasks across two or more cores. In addition, many of our processor families integrate graphics functionality onto the processor die.

A chipset sends data between the microprocessor and input, display, and storage devices, such as the keyboard, mouse, monitor, hard drive or solid-state drive, and optical disc drives. Chipsets extend the audio, video, and other capabilities of many systems and perform essential logic functions, such as balancing the performance of the system and removing bottlenecks.

We offer and continue to develop SoC products that integrate our CPUs with other system components, such as graphics, audio, imaging, communication and connectivity, and video, onto a single chip. SoC products are designed to reduce total cost of ownership, provide improved performance due to higher integration and the lowest power, and enable form factors such as tablets, phones, Ultrabook devices, and 2 in 1 systems, as well as notebooks, desktops, data center products, and the Internet of Things.

We offer a multichip package that integrates the chipset on one die, with the CPU and graphics on another die, connected via a lower-power, on-package interface. Similar to an SoC, the multichip package can provide improved performance due to higher integration coupled with the lowest power consumption, which enables smaller form factors. In 2015, we released our 6th generation Intel ® Core ™ processor, formerly code-named Skylake.

5

Table of Contents

We also offer features designed to improve our platform capabilities, such as:

• | Intel vPro™ technology, a solution for manageability, security, and business user experiences in the notebook, desktop, and 2 in 1 systems and select Internet of Things market segments. Intel vPro technology is designed to provide businesses with increased manageability, upgradeability, energy-efficient performance, and security while lowering the total cost of ownership; |

• | Intel RealSense technology, which-in conjunction with the latest Intel processors-enables a device to perceive depth similar to how a person does. This technology brings new opportunities for the personalization of compute to evolve; and |

• | True Key ™ technology, which allows users to access devices through facial recognition and other biometric technologies, thereby eliminating the need for log-in passwords. |

6

Table of Contents

We offer a range of platforms based upon the following microprocessors:

Intel Security Products

Through our McAfee products, we deliver innovative solutions that secure computers, mobile devices, and networks. Our security solutions follow the threat defense life cycle (protect, detect, correct) to defend consumers, small businesses, and enterprises from malware and emerging online threats. In 2015, Intel launched McAfee ® Endpoint Security 10.X, which enables customers to tackle the threat defense life cycle with reduced complexity and better performance. McAfee Endpoint Security 10.X introduces a new platform built to enable real-time communication between threat defenses for more effective protection against emerging threats.

7

Table of Contents

Communication and Connectivity

Our communication and connectivity offerings for tablets, phones, and other connected devices include baseband processors, radio frequency transceivers, and power management integrated circuits. We also offer comprehensive tablet, phone, and Internet of Things solutions, which include multimode 4G LTE* modems, Bluetooth ® technology and GPS receivers, software solutions, customization, and essential interoperability tests.

Non-Volatile Memory Solutions

We offer NAND flash memory products primarily used in solid-state drives. Our NAND flash memory products are manufactured by IM Flash Technologies, LLC (IMFT) and Micron Technology, Inc. (Micron). In 2015, Intel announced 3D XPoint ™ technology, a non-volatile memory that has the potential to revolutionize devices, applications, or services that benefit from fast access to large sets of data. Jointly developed with Micron, 3D XPoint technology combines the performance, density, power, non-volatility, and cost advantages of existing NAND and conventional memories like DRAM.

Intel Custom Foundry

We offer manufacturing technologies and design services for our customers. Our foundry offerings include full custom silicon, packaging, and manufacturing test services. We also provide semi-custom services to tailor Intel architecture-based solutions with customers' intellectual property blocks. To enable our customers to use our custom foundry services, we offer industry-standard design kits, intellectual property blocks, and design services.

Products and Product Strategy by Operating Segment

Our Client Computing Group (CCG) operating segment is responsible for all aspects of the client computing continuum, which includes platforms that are incorporated in notebook (including Ultrabook devices), 2 in 1 systems, desktop computers for consumers and businesses, tablets, and phones. In addition, CCG offers home gateway products and set-top box components, and focuses on a broad range of wireless connectivity options that combine Intel ® WiFi technology with our 2G and 3G technologies and accelerate industry adoption of 4G LTE. We have an array of innovative wired solutions such as Thunderbolt technology and client Ethernet solutions .

In 2015, we released the 6th generation Intel Core processor family for use in notebooks and desktops. These processors use 14-nanometer (nm) transistors and our Tri-Gate transistor technology. Our Tri-Gate transistor technology extends Moore's Law by providing improved performance and energy efficiency. In combination, these enhancements can provide significant power savings and performance gains when compared to previous-generation processors.

In mobile communications, we expanded our product portfolio with the release of our Intel ® Atom ™ x5 and x7 processors, formerly code named Cherry Trail and designed for mainstream and premium tablet platforms. These processors may be paired with our second-generation 4G LTE solution, featuring CAT6 and carrier aggregation. We also released our Intel ® Atom ™ x3 processor, formerly coded named SoFIA 3G, our first integrated baseband and SoC application processor designed for entry and value phone and tablet platforms.

Notebook

Our strategy for the notebook computing market segment is to offer notebook technologies designed to bring exciting new user experiences to life and improve performance, battery life, wireless connectivity, manageability, and security. In addition, we design for innovative smaller, lighter, and thinner form factors. Our 6th generation Intel Core processor continues to deliver or enable increasing levels of performance, graphics, and energy efficiency, and will provide our customers and end users with multiple choices in processor cores, graphic performance, and battery life.

We have worked to help our customers develop a new class of personal computing devices that includes Ultrabook devices and 2 in 1 systems. These computers combine the energy-efficient performance and capabilities of today's notebooks and tablets with enhanced graphics and improved user interfaces such as touch and voice in thin, light form factors that are highly responsive and secure, and that can seamlessly connect to the Internet. We believe the renewed innovation in the PC industry that we fostered with Ultrabook devices and expanded to 2 in 1 systems will continue.

8

Table of Contents

Desktop

Our strategy for the desktop computing market segment is to offer exciting new user experiences and products that provide increased manageability, security, and energy-efficient performance. For example, in 2015 we introduced a new user experience in the Intel ® Compute Stick, a device that allows users to transform HDMI-capable monitors or TVs into complete computers to get the most out of their display devices. We also focus on lowering the total cost of ownership for businesses. The desktop computing market segment includes all-in-one products, which combine traditionally separate desktop components into one form factor. Additionally, all-in-one computers have transformed into portable and flexible form factors that offer users increased portability and new multi-user applications and uses. For desktop consumers, we also focus on the design of products for high-end enthusiast PCs and mainstream PCs with rapidly increasing audio and media capabilities.

Our Data Center Group (DCG) operating segment offers products designed to provide leading energy-efficient performance for all server, network, and storage platforms. In addition, DCG focuses on lowering the total cost of ownership and on other specific optimizations for the enterprise, cloud, communications infrastructure, and technical computing segments. In 2015, we launched the Intel ® Xeon ® processor D family, our first Intel Xeon processor-based SoC product family, which extends our portfolio for network, storage, and high-density servers. In addition, we launched the Intel Xeon processor E7 v3 family, targeted at platforms requiring four or more CPUs; this processor family delivers performance advancements over previous generations, along with industry-leading reliability, availability, and serviceability. We also released the Intel Xeon processor E3 v5 family on our 14nm process technology, targeted for entry-level servers and workstations. In 2016, we expect to release our next-generation Intel Xeon E5 and E7 families on our 14nm process technology. Additionally, we expect to release in 2016 our next-generation Intel ® Xeon Phi ™ product family, code-named "Knights Landing," with up to 72 high-performance Intel processor cores, integrated memory and fabric, and a common software programming model with Intel Xeon processors. Knights Landing is designed for highly parallel compute- and memory bandwidth-intensive workloads. Intel Xeon Phi coprocessors are positioned to increase the performance of supercomputers, enabling trillions of calculations per second, and to address emerging data analytics solutions.

Our Internet of Things Group (IOTG) operating segment offers platforms designed for retail, transportation, industrial, buildings and home use, along with a broad range of other market segments. In addition, IOTG focuses on establishing an end-to-end manageable architecture that captures actionable information for consumers. In 2015, we announced three new Intel Quark processors, including the Intel ® Quark ™ SE SoC and the Intel Quark microcontrollers D1000 and D2000.

Our software and services operating segments seek to create differentiated user experiences on Intel ® -based platforms. We differentiate by combining Intel platform features with enhanced software and services, and partnering closely with the external software developer ecosystem. Our three primary initiatives are:

• | enabling platforms that can be used across multiple operating systems, applications, and services across all Intel products; |

• | optimizing features and performance by enabling the software ecosystem to quickly take advantage of new platform features and capabilities; and |

• | protecting consumers, small businesses, and enterprises from malware and emerging online threats. |

9

Table of Contents

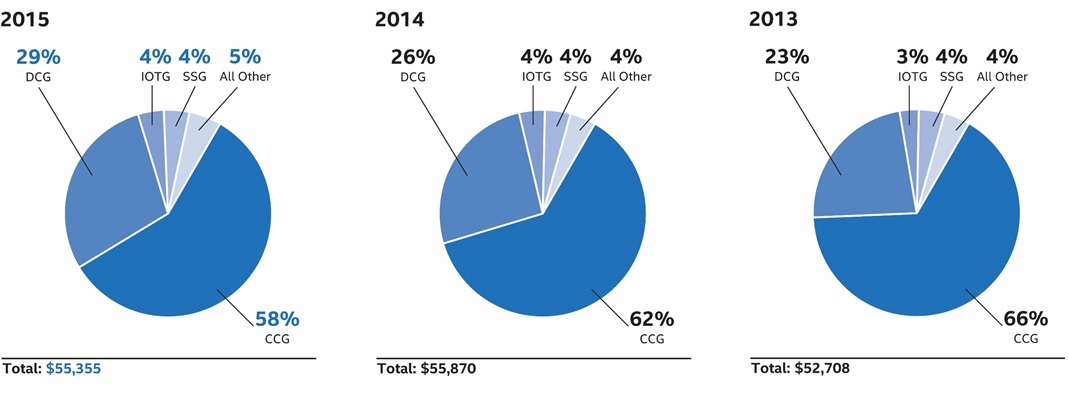

Revenue by Major Operating Segment

Net revenue for the Client Computing Group (CCG) operating segment, the Data Center Group (DCG) operating segment, the Internet of Things Group (IOTG) operating segment, and the aggregated software and services (SSG) operating segments is presented as a percentage of our consolidated net revenue. SSG includes Intel Security Group and the Software and Services Group operating segments. The "all other" category consists primarily of revenue from the Non-Volatile Memory Solutions Group (NSG) and the New Devices Group operating segments.

Percentage of Revenue by Major Operating Segment

(Dollars in Millions)

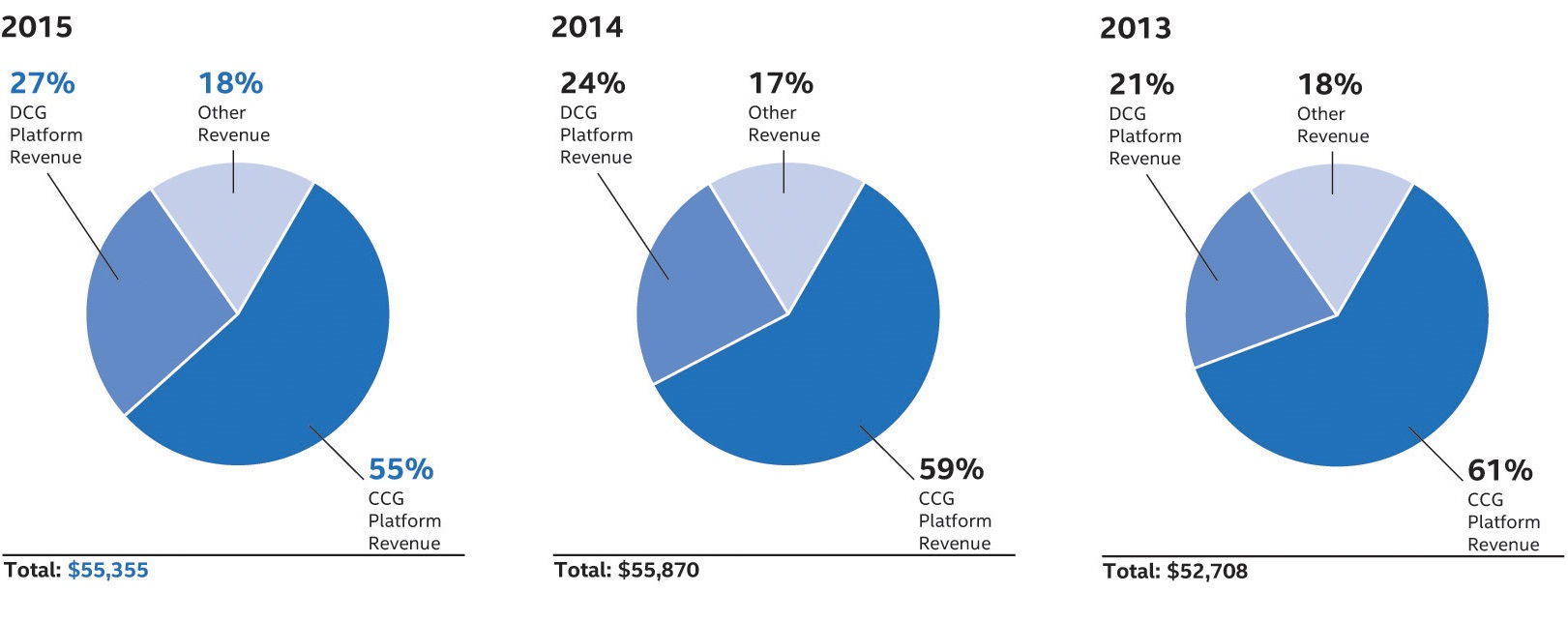

Percentage of Revenue by Principal Product from Reportable Segments

(Dollars in Millions)

10

Table of Contents

Competition

The computing industry continuously evolves with new and enhanced technologies and products from existing and new providers. The marketplace can change quickly in response to the introduction of such technologies and products and other factors such as changes in customer and end-user requirements, expectations, and preferences. As technologies evolve and new market segments emerge, the boundaries between the market segments that we compete in are also subject to change.

Intel faces significant competition in the development and market acceptance of our products in this environment. Our platforms, based on Intel architecture, are positioned to compete across the compute continuum, from the lowest power and mobile devices to the most powerful data center servers. Our platforms, which have integrated hardware and software, offer customers benefits such as ease of use, savings in total cost of ownership, and the ability to scale systems to accommodate increased usage.

Competitors

We compete against other companies that make and sell platforms, other silicon components, and software to businesses that build and sell computing and communications devices to end users. Our competitors also include companies that sell goods and services to businesses that use them for their internal and/or customer-facing processes (e.g., businesses running large data centers). In addition, we face competition from OEMs, ODMs, and other industrial and communications equipment manufacturers that, to some degree, choose to vertically integrate their own proprietary semiconductor and software assets. By doing so, these competitors may be attempting to offer greater differentiation in their products and to increase their share of the profits for each finished product they sell. Continuing changes in industry participants through, for example, acquisitions or business collaborations could also have a significant impact on our competitive position.

In the PC market segment, we are a leading provider of platforms for traditional desktops and notebooks. We face existing and emerging competition in these product areas. Tablets, phones, and other mobile devices offered by numerous vendors are significant competitors to traditional PCs for many usages. We are relatively recent providers of platforms for tablets and phones, and face strong competition from vendors that use applications processors based on the ARM* architecture; feature low-power, long battery-life operation; and are built in SoC formats that integrate numerous functions on one chip.

In the data center market segment, we are a leading provider of data center platforms and face competition from companies using ARM architecture or other technologies. Internet cloud computing, storage, and networking are areas of significant targeted growth for us in the data center segment, and we face strong competition in these market segments.

In the Internet of Things market segment, we have a long-standing position as a supplier of components and software for embedded products. This marketplace continues to significantly expand with increasing types and numbers of smart and connected devices for industrial, commercial, and consumer uses such as wearables. As this market segment evolves, we face numerous large and small incumbent competitors as well as new entrants that use ARM architecture and other operating systems and software.

Our security business operates in highly competitive, fragmented, and rapidly changing market segments. We are a major provider of cybersecurity products and services to both businesses and consumers. For businesses, we compete with companies selling individual point security products and companies selling multiple security products. We offer to businesses a portfolio of products that are integrated into a comprehensive security solution. For consumers, we primarily compete against other major security companies and providers of free security products. Our consumer offerings are designed to protect user data, identity, and devices across the compute continuum.

In the memory market segment, we compete against other providers of NAND flash memory products. We focus our efforts primarily on incorporating NAND flash memory into solution products, such as solid-state drives supporting consumer and enterprise applications. We believe that our memory offerings, including innovative developments such as 3D XPoint technology, will complement our other product offerings in our other segments.

Our products primarily compete based on performance, energy efficiency, integration, innovative design, features, price, quality, reliability, brand recognition, technical support, and availability. The importance of these factors varies by the type of end system for the products. For example, performance might be among the most important factors for our products for data center servers, while price and integration might be among the most important factors for our products for tablets, phones, and other mobile devices.

11

Table of Contents

Competitive Advantages

Our key competitive advantages include:

• | Transitions to next-generation technologies . We have a market lead in transitioning to the next-generation process technology and bringing products to market using such technology. Our products utilizing our 14nm process technology are in the market and we are continuing to work on the development of our next-generation 10nm process technology. We believe that these advancements will offer significant improvements in one or more of the following areas: performance, new features, energy efficiency, and cost. |

• | Combination of our network of manufacturing and assembly and test facilities with our global architecture design teams . We have made significant capital and R&D investments into our integrated manufacturing network, which enables us to have more direct control over our design, development, and manufacturing processes; quality control; product cost; production timing; performance; power consumption; and manufacturing yield. The increased cost of constructing new fabrication facilities to support smaller transistor geometries and larger wafers has led to a reduced number of companies that can build and equip leading-edge manufacturing facilities. Most of our competitors rely on third-party foundries and subcontractors for manufacturing and assembly and test needs. We provide foundry services as an alternative to such foundries. |

• | Products optimized to operate on multiple operating systems . Through our collaboration with our customers and other third parties, many of our products can operate on multiple operating systems in end-user products and platforms. |

Manufacturing and Assembly and Test

As of December 26, 2015 , 55% of our wafer fabrication, including microprocessors and chipsets, was conducted within the U.S. at our facilities in Arizona, Oregon, and New Mexico. Our Massachusetts fabrication facility was our last manufacturing facility on 200 millimeter (mm) wafers and ceased production in Q1 2015. The remaining 45% of our wafer fabrication was conducted outside the U.S. at our facilities in Ireland, Israel, and China. Our fabrication facility in Ireland has transitioned to our 14nm process technology, with manufacturing continuing to ramp in 2016. Wafer fabrication conducted within and outside the U.S. may be impacted by the timing of a facility's transition to a newer process technology, as well as a facility's capacity utilization.

Products |

| Wafer Size |

| Process Technology |

| Locations |

Microprocessors and other products |

| 300mm |

| 14nm |

| Arizona, Oregon, Ireland |

Microprocessors and other products |

| 300mm |

| 22nm |

| Israel, Arizona, Oregon |

Microprocessors and chipsets |

| 300mm |

| 32nm |

| New Mexico |

Microprocessors |

| 300mm |

| 45nm |

| New Mexico |

Microprocessors and chipsets |

| 300mm |

| 65nm |

| China |

As of December 26, 2015 , our microprocessors were manufactured on 300mm wafers, with a substantial majority manufactured using our 14nm, 22nm, and 32nm process technologies. As we move to each succeeding generation of manufacturing process technology, we incur significant start-up costs to prepare each factory for manufacturing. However, continuing to advance our process technology provides benefits that we believe justify these costs. The benefits of moving to each succeeding generation of manufacturing process technology can include using less space per transistor, reducing heat output from each transistor, and increasing the number of integrated features on each chip. These advancements can enable us to introduce new devices with higher functionality and complexity while controlling power, cost, and size. In addition, with each shift to a new process technology, we are able to produce more microprocessors per square foot of our wafer fabrication facilities. The costs to develop newer process technologies are significantly less than adding capacity by building additional wafer fabrication facilities using older process technologies.

We use third-party foundries to manufacture wafers for certain components, including communications, connectivity, and networking products. For example, the Intel Atom x3 processor is fabricated by a third-party foundry. In addition, we primarily use subcontractors to manufacture board-level products and systems. We purchase certain communications and connectivity products from external vendors primarily in the Asia-Pacific region.

Following the manufacturing process, the majority of our components are subject to assembly and test. We perform our components assembly and test at facilities in Malaysia, China, and Vietnam . To augment capacity, we use subcontractors to perform assembly and test of certain products, primarily chipsets and communications and connectivity products.

12

Table of Contents

Our NAND flash memory products are manufactured by IMFT and Micron using 20nm or 25nm process technology, and assembly and test of these products is performed by Micron and other external subcontractors. For further information, see " Note 5: Cash and Investments " in Part II, Item 8 of this Form 10-K. Additionally, in the second half of 2016, we will start using our facility in Dalian, China to help expand our manufacturing capacity in next-generation memory. The expansion is part of our multi-source supply strategy and will allow us to best serve our customers.

Our employment and operating practices are consistent with, and we expect our suppliers and subcontractors to abide by, local country law. Intel expects all suppliers to comply with our Code of Conduct and the Electronic Industry Citizenship Coalition (EICC) Code of Conduct, both of which set standards that address the rights of workers to safe and healthy working conditions, environmental responsibility, compliance with privacy and data security obligations, and compliance with applicable laws.

We have thousands of suppliers, including subcontractors, providing our various materials, equipment, and service needs. We set expectations for supplier performance and reinforce those expectations with periodic assessments and audits. We communicate those expectations to our suppliers regularly and work with them to implement improvements when necessary. Where possible, we seek to have several sources of supply for all of these materials and resources, but we may rely on a single or limited number of suppliers, or upon suppliers in a single country. In those cases, we develop and implement plans and actions to reduce the exposure that would result from a disruption in supply. We have entered into long-term contracts with certain suppliers to help ensure a stable supply of silicon and semiconductor manufacturing tools.

Our products are typically manufactured at multiple Intel facilities around the world or by subcontractors. However, some products are manufactured in only one Intel or subcontractor facility, and we seek to implement action plans to reduce the exposure that would result from a disruption at any such facility. See "Risk Factors" in Part I, Item 1A of this Form 10-K.

13

Table of Contents

Research and Development

We are committed to investing in world-class technology development, particularly in the design and manufacture of integrated circuits. R&D expenditures were $12.1 billion in 2015 ( $11.5 billion in 2014 and $10.6 billion in 2013 ).

Our R&D activities are directed toward the delivery of solutions consisting of hardware and software platforms and supporting services across a wide range of computing devices. We are focused on developing the technology innovations that we believe will deliver our next generation of products, which will in turn enable new form factors and usage models for businesses and consumers. We focus our R&D efforts on advanced computing technologies, developing new microarchitectures, advancing our silicon manufacturing process technology, delivering the next generation of platforms, improving our platform initiatives, developing new solutions in emerging technologies (including memory and the Internet of Things), and developing software solutions and tools. Our R&D efforts are intended to enable new levels of performance and address areas such as energy efficiency, system-level integration, security, scalability for multi-core architectures, system manageability, and ease of use.

As part of our R&D efforts, we plan to introduce a new Intel Core microarchitecture for desktops, notebooks (including Ultrabook devices and 2 in 1 systems), and Intel Xeon processors on a regular cadence. We expect to lengthen the amount of time we will utilize our 14nm and our next-generation 10nm process technologies, further optimizing our products and process technologies while meeting the yearly market cadence for product introductions.

Advances in our silicon technology have enabled us to continue making Moore's Law a reality. In 2014, we began manufacturing our 5th generation Intel Core processor family using our 14nm process technology. In 2015, we released a new microarchitecture (our 6th generation Intel Core processor family), using our 14nm process technology. We also plan to introduce a third 14nm product, code-named "Kaby Lake." This product will have key performance enhancements as compared to our 6th generation Intel Core processor family. We are also developing 10nm manufacturing process technology, our next-generation process technology.

We have continued expanding on the advances anticipated by Moore's Law by bringing new capabilities into silicon and producing new products optimized for a wider variety of applications. We expect these advances will result in a significant reduction in transistor leakage, lower active power, and an increase in transistor density to enable more smaller form factors, such as powerful, feature-rich phones and tablets with a longer battery life. For instance, we have accelerated the Intel Atom processor-based SoC roadmap for our mobile form factors (including tablets and phones), notebooks (including Ultrabook devices and 2 in 1 systems), the Internet of Things, and data center applications, on our 32nm, 22nm, and 14nm process technologies. In addition, we offer the Intel Quark SoC, an ultra-low-power and low-cost architecture designed for the Internet of Things such as industrial machines and wearable devices.

With our continued focus on silicon and manufacturing technology leadership, we entered into a series of agreements with ASML Holding N.V. (ASML) in 2012, certain of which were amended in 2014 to further define the commercial terms between the parties. These amended agreements, in which Intel agreed to provide R&D funding over five years, are intended to accelerate the development of extreme ultraviolet (EUV) lithography projects and deep ultraviolet immersion lithography projects, including generic developments applicable to both 300mm and 450mm.

14

Table of Contents

Our R&D activities range from designing and developing new products and manufacturing processes to researching future technologies and products. We continue to make significant R&D investments in the development of SoC devices to enable growth in mobile form factors. In addition, we continue to make significant investments in communications and connectivity for tablets, phones, and other connected devices, including multimode LTE modems. Our investment in Cloudera, Inc. (Cloudera), completed in 2014, is evidence of our drive to bring big data analytics to the mainstream market through the joining of Cloudera's software platform and our data center architecture based on Intel Xeon processors. We also continue to invest in leading-edge foundry platforms and ecosystem partner development, graphics, high-performance computing, and communication and connectivity.

Our R&D model is based on a global organization that emphasizes a collaborative approach to identifying and developing new technologies, leading standards initiatives, and influencing regulatory policies to accelerate the adoption of new technologies, including joint pathfinding conducted between researchers at Intel Labs and our business groups. We centrally manage key cross-business group product initiatives to align and prioritize our R&D activities across these groups. In addition, we may augment our R&D activities by investing in companies or entering into agreements with companies that have similar R&D focus areas, as well as directly purchasing or licensing technology applicable to our R&D initiatives. To drive innovation and gain efficiencies, we intend to utilize our investments in intellectual property and R&D across our market segments.

Employees

As of December 26, 2015 , we had 107,300 employees worldwide, with approximately 51% of those employees located in the U.S.

Sales and Marketing

Customers

We sell our products primarily to OEMs and ODMs. ODMs provide design and manufacturing services to branded and unbranded private-label resellers. In addition, we sell our products to other manufacturers, including makers of a wide range of industrial and communications equipment. Our customers also include those who buy PC components and our other products through distributor, reseller, retail, and OEM channels throughout the world.

Our worldwide reseller sales channel consists of thousands of indirect customers-systems builders that purchase Intel ® microprocessors and other products from our distributors. We have a program that allows distributors to sell our microprocessors and other products in small quantities to customers of systems builders. Our microprocessors and other products are also available in direct retail outlets.

Hewlett-Packard Company, our largest customer in 2014, separated into HP Inc. and Hewlett Packard Enterprise Company on November 1, 2015. In 2015, these entities collectively accounted for 18% of our net revenue ( 18% in 2014 and 17% in 2013 ), Dell Inc. accounted for 15% of our net revenue ( 16% in 2014 and 15% in 2013 ), and Lenovo Group Limited accounted for 13% of our net revenue ( 12% in 2014 and 12% in 2013 ). No other customer accounted for more than 10% of our net revenue during such periods. For information about net revenue and operating income by operating segment, and net revenue from unaffiliated customers by country, see " Note 26: Operating Segments and Geographic Information " in Part II, Item 8 of this Form 10-K.

Sales Arrangements

Our products are sold through sales offices throughout the world. Sales of our products are frequently made via purchase order acknowledgments that contain standard terms and conditions covering matters such as pricing, payment terms, and warranties, as well as indemnities for issues specific to our products, such as patent and copyright indemnities. From time to time, we may enter into additional agreements with customers covering, for example, changes from our standard terms and conditions, new product development and marketing, private-label branding, and other matters. Our sales are routinely made using electronic and web-based processes that allow the customer to review inventory availability and track the progress of specific goods ordered. Pricing on particular products may vary based on volumes ordered and other factors. We also offer discounts, rebates, and other incentives to customers to increase acceptance of our products and technology.

15

Table of Contents

Our products are generally shipped under terms that transfer title to the customer, even in arrangements for which the recognition of revenue and related cost of sales is deferred. Our standard terms and conditions of sale typically provide that payment is due at a later date, usually 30 days after shipment or delivery. We assess credit risk through quantitative and qualitative analysis. From this analysis, we establish shipping and credit limits, and determine whether we will seek to use one or more credit support protection devices, such as obtaining a parent guarantee, standby letter of credit, or credit insurance. Credit losses may still be incurred due to bankruptcy, fraud, or other failure of the customer to pay. For information about our allowance for doubtful receivables, see "Schedule II-Valuation and Qualifying Accounts" in Part IV of this Form 10-K.

Our sales to distributors are typically made under agreements allowing for price protection on unsold merchandise and a right of return on stipulated quantities of unsold merchandise. Under the price protection program, we give distributors credits for the difference between the original price paid and the current price that we offer. Our products typically have no contractual limit on the amount of price protection, nor is there a limit on the time horizon under which price protection is granted. The right of return granted generally consists of a stock rotation program in which distributors are able to exchange certain products based on the number of qualified purchases made by the distributor. We have the option to grant credit for, repair, or replace defective products, and there is no contractual limit on the amount of credit that may be granted to a distributor for defective products.

Distribution

Distributors typically handle a wide variety of products, including those that compete with our products, and fill orders for many customers. Customers may place orders directly with us or through distributors. We have several distribution warehouses that are located in proximity to key customers.

Backlog

Over time, our larger customers have generally moved to lean-inventory or just-in-time operations rather than maintaining larger inventories of our products. As our customers continue to lower their inventories, our processes to fulfill their orders have evolved to meet their needs. As a result, our manufacturing production is based on estimates and advance non-binding commitments from customers as to future purchases. Our order backlog as of any particular date is a mix of these commitments and specific firm orders that are primarily made pursuant to standard purchase orders for delivery of products. Only a small portion of our orders are non-cancelable, and the dollar amount associated with the non-cancelable portion is not significant.

Seasonal Trends

Historically, our net revenue has typically been higher in the second half of the year than in the first half of the year, accelerating in the third quarter and peaking in the fourth quarter.

Marketing

Our global marketing objectives are to build a strong, well-known Intel corporate brand that connects with businesses and consumers, and to offer a limited number of meaningful and valuable brands in our portfolio to aid businesses and consumers in making informed choices about technology purchases. The Intel Core processor family and the Intel Quark, Intel Atom, Intel ® Celeron ® , Intel ® Pentium ® , Intel Xeon, Intel Xeon Phi, and Intel ® Itanium ® trademarks make up our processor brands.

We promote brand awareness and preference, and generate demand through our own direct marketing as well as through co-marketing programs. Our direct marketing activities primarily include advertising through digital and social media and television, as well as consumer and trade events, industry and consumer communications, and press relations. We market to consumer and business audiences, and focus on building awareness and generating demand for new form factors such as tablets, all-in-one devices, and 2 in 1 systems powered by Intel. Our key messaging focuses on increased performance, improved energy efficiency, and other capabilities such as connectivity, communications, and security.

16

Table of Contents

Purchases by customers often allow them to participate in cooperative advertising and marketing programs such as the Intel Inside ® program. This program broadens the reach of our brands beyond the scope of our own direct marketing. Through the Intel Inside program, certain customers are licensed to place Intel ® logos on computing devices containing our microprocessors and processor technologies, and to use our brands in their marketing activities. The program includes a market development component that accrues funds based on purchases and partially reimburses customers for marketing activities for products featuring Intel ® brands, subject to customers meeting defined criteria. These marketing activities primarily include advertising through digital and social media and television, as well as press relations. We have also entered into joint marketing arrangements with certain customers.

Intellectual Property Rights and Licensing

Intel owns significant intellectual property (IP) and related IP rights around the world that relate to our products, services, R&D, and other activities and assets. Our IP portfolio includes patents, copyrights, trade secrets, trademarks, trade dress rights, and maskwork rights. We actively seek to protect our global IP rights and to deter unauthorized use of our IP and other assets. Such efforts can be difficult, however, particularly in countries that provide less protection to IP rights and in the absence of harmonized international IP standards. While our IP rights are important to our success, our business as a whole is not significantly dependent on any single patent, copyright, or other IP right. See "Risk Factors" in Part I, Item 1A, and " Note 25: Contingencies " in Part II, Item 8 of this Form 10-K.

We have obtained patents in the U.S. and other countries. Because of the fast pace of innovation and product development, and the comparative pace of governments' patenting processes, our products are often obsolete before the patents related to them expire; in some cases, our products may be obsolete before the patents related to them are granted. As we expand our products into new industries, we also seek to extend our patent development efforts to patent such products. In addition to developing patents based on our own R&D efforts, we purchase patents from third parties to supplement our patent portfolio. Established competitors in existing and new industries, as well as companies that purchase and enforce patents and other IP, may already have patents covering similar products. There is no assurance that we will be able to obtain patents covering our own products, or that we will be able to obtain licenses from other companies on favorable terms or at all.

The software that we distribute, including software embedded in our component-level and platform products, is entitled to copyright and other IP protection. To distinguish our products from our competitors' products, we have obtained trademarks and trade names for our products, and we maintain cooperative advertising programs with customers to promote our brands and to identify products containing genuine Intel components. We also protect details about our processes, products, and strategies as trade secrets, keeping confidential the information that we believe provides us with a competitive advantage.

Compliance with Environmental, Health, and Safety Regulations

Our compliance efforts focus on monitoring regulatory and resource trends and setting company-wide performance targets for key resources and emissions. These targets address several parameters, including product design; chemical, energy, and water use; waste recycling; the source of certain minerals used in our products; climate change; and emissions.

As a company, we focus on reducing natural resource use, the solid and chemical waste by-products of our manufacturing processes, and the environmental impact of our products. We currently use a variety of materials in our manufacturing process that have the potential to adversely impact the environment and are subject to a variety of environmental, health, and safety (EHS) laws and regulations. Over the past several years, we have significantly reduced the use of lead and halogenated flame retardants in our products and manufacturing processes.

We work with non-governmental organizations (NGOs), OEMs, and retailers to help manage e-waste (including electronic products nearing the end of their useful lives) and to promote recycling. The European Union requires producers of certain electrical and electronic equipment to develop programs that let consumers return products for recycling. Many U.S. states and countries in Latin America and Asia also have or are developing similar e-waste take-back laws. Although these laws are typically targeted at the end electronic product and not components such as microprocessors, the inconsistency of many e-waste take-back laws, changes in our product offerings, and the lack of local e-waste management options in many areas pose a challenge for our compliance efforts.

17

Table of Contents

We are an industry leader in our efforts to build ethical sourcing of minerals for our products, including "conflict minerals" from the DRC and adjoining countries. In 2013, we accomplished our goal to manufacture microprocessors that are DRC conflict-free for tantalum, tin, tungsten, and gold. We continue our work to establish DRC conflict-free supply chains for our company and our industry, and are moving beyond microprocessors to validate our broader product base as DRC conflict-free in 2016 for these four minerals.

We seek to reduce our global greenhouse gas emissions by investing in energy conservation projects in our factories and working with suppliers to improve energy efficiency. We take a holistic approach to power management, addressing the challenge at the silicon, package, circuit, microarchitecture, macroarchitecture, platform, and software levels. We recognize that climate change may cause general economic risk. For further information on the risks of climate change, see "Risk Factors" in Part I, Item 1A of this Form 10-K. We see a potential for higher energy costs driven by climate change regulations. This could include items applied to utility companies that are passed along to customers, such as carbon taxes or costs associated with obtaining permits for our manufacturing operations, emission cap and trade programs, or renewable portfolio standards.

We are committed to sustainability and take a leadership position in promoting voluntary environmental initiatives and working proactively with governments, environmental groups, and industry to promote global environmental sustainability. We believe that technology will be fundamental to finding solutions to the world's environmental challenges, and we are joining forces with industry, business, and governments to find and promote ways that technology can be used as a tool to combat climate change.

We have been purchasing renewable energy at some of our major sites for several years. We purchase renewable energy certificates under a multi-year contract. This purchase has placed Intel at the top of the U.S. Environmental Protection Agency Green Power Partnership rankings for the past eight years and is intended to help stimulate the market for green power, leading to additional generating capacity and, ultimately, lower costs.

Distribution of Company Information

Our Internet address is www.intel.com . We publish voluntary reports on our website that outline our performance with respect to corporate responsibility, including EHS compliance.

We use our Investor Relations website, www.intc.com , as a routine channel for distribution of important information, including news releases, analyst presentations, and financial information. We post filings on our website the same day they are electronically filed with, or furnished to, the U.S. Securities and Exchange Commission (SEC), including our annual and quarterly reports on Forms 10-K and 10-Q and current reports on Form 8-K; our proxy statements; and any amendments to those reports or statements. We post our quarterly and annual earnings results at www.intc.com/results.cfm , and do not distribute our financial results via a news wire service. All such postings and filings are available on our Investor Relations website free of charge. In addition, our Investor Relations website allows interested persons to sign up to automatically receive e-mail alerts when we post financial information. The SEC's website, www.sec.gov , contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. The content on any website referred to in this Form 10-K is not incorporated by reference in this Form 10-K unless expressly noted.

18

Table of Contents

Executive Officers of the Registrant

The following sets forth certain information with regard to our executive officers as of February 12, 2016 (ages are as of December 26, 2015 ):

Andy D. Bryant , age 65 |

| Gregory R. Pearson , age 55 | ||||

• 2012 – present |

| Chairman of the Board |

| • 2014 – present |

| Senior VP; General Manager, Sales and Marketing Group |

• 2011 – 2012 |

| Vice Chairman of the Board, Executive VP, Technology, Manufacturing and Enterprise Services; Chief Administrative Officer |

|

|

| |

|

|

| • 2008 – 2013 |

| General Manager, Worldwide Sales and Operations Group | |

|

|

|

|

| ||

• 2009 – 2011 |

| Executive VP, Technology, Manufacturing, and Enterprise Services; Chief Administrative Officer |

| • Joined Intel in 1983 | ||

|

|

|

|

|

| |

|

|

| Dr. Venkata S.M. "Murthy" Renduchintala , age 50 | |||

• 2007 – 2009 |

| Executive VP, Finance and Enterprise Services; Chief Administrative Officer |

| • 2015 – present |

| Executive VP; President, Client and Internet of Things (IoT) Businesses and Systems Architecture Group |

|

|

|

|

| ||

• 2001 – 2007 |

| Executive VP; Chief Financial and Enterprise Services Officer |

|

|

| |

|

|

| • Joined Intel in 2015 | |||

• Member of Intel Corporation Board of Directors |

|

| ||||

• Member of Columbia Sportswear Company Board of Directors |

| Stacy J. Smith , age 53 | ||||

| • 2012 – present |

| Executive VP; Chief Financial Officer | |||

• Member of McKesson Corporation Board of Directors |

| • 2010 – 2012 |

| Senior VP; Chief Financial Officer | ||

• Joined Intel in 1981 |

| • 2007 – 2010 |

| VP; Chief Financial Officer | ||

|

| • 2006 – 2007 |

| VP; Assistant Chief Financial Officer | ||

William M. Holt , age 63 |

| • 2004 – 2006 |

| VP; Finance and Enterprise Services, Chief Information Officer | ||

• 2013 – present |

| Executive VP; General Manager, Technology and Manufacturing Group |

|

|

| |

|

|

| • Member of Autodesk, Inc. Board of Directors | |||

• 2006 – 2013 |

| Senior VP; General Manager, Technology and Manufacturing Group |

| • Member of Virgin America, Inc. Board of Directors | ||

|

|

| • Joined Intel in 1988 | |||

• 2005 – 2006 |

| VP; Co-General Manager, Technology and Manufacturing Group |

|

| ||

|

|

|

| |||

• Joined Intel in 1974 |

|

| ||||

|

|

| ||||

Brian M. Krzanich , age 55 |

|

| ||||

• 2013 – present |

| Chief Executive Officer |

|

| ||

• 2012 – 2013 |

| Executive VP; Chief Operating Officer |

|

| ||

• 2010 – 2012 |

| Senior VP; General Manager, Manufacturing and Supply Chain |

|

| ||

|

|

|

| |||

• 2006 – 2010 |

| VP; General Manager, Assembly and Test |

|

| ||

• Member of Deere & Company Board of Directors |

|

| ||||

• Joined Intel in 1982 |

|

| ||||

19

Table of Contents

ITEM 1A. | RISK FACTORS |

The following risks could materially and adversely affect our business, financial condition, and results of operations, and the trading price of our common stock could decline. These risk factors do not identify all risks that we face; our operations could also be affected by factors that are not presently known to us or that we currently consider to be immaterial to our operations. Due to risks and uncertainties, known and unknown, our past financial results may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods. You should also refer to the other information set forth in this Annual Report on Form 10-K, including "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our financial statements and the related notes.

Changes in product demand can harm our results of operation and financial condition.

Demand for our products is variable and hard to predict. Changes in the demand for our products may reduce our revenue, increase our costs, lower our gross margin percentage, or require us to write down the value of our assets. Important factors that could lead to variation in the demand for our products include changes in:

• | business conditions, including downturns in the computing industry, or in the global or regional economies; |

• | consumer confidence or income levels caused by changes in market conditions, including changes in government borrowing, taxation, or spending policies; the credit market; or expected inflation, employment, and energy or other commodity prices; |

• | the level of our customers' inventories; |

• | competitive and pricing pressures, including actions taken by competitors; |

• | customer product needs; |

• | market acceptance and industry support of our new and maturing products; and |

• | the technology supply chain, including supply constraints caused by natural disasters or other events. |

We face significant competition. The industry in which we operate is highly competitive and subject to rapid technological and market developments, changes in industry standards, changes in customer needs, and frequent product introductions and improvements. If we do not anticipate and respond to these developments, our competitive position may weaken, and our products or technologies might be uncompetitive or obsolete. In recent years, our business focus has expanded and now includes the design and production of platforms for tablets, phones, and other devices across the compute continuum, including products for the Internet of Things, and related services. As a result, we face new sources of competition, including, in certain of these market segments, from incumbent competitors with established customer bases and greater brand recognition. To be successful, we need to cultivate new industry relationships with customers and partners in these market segments. In addition, we must continually improve the cost, integration, and energy efficiency of our products, as well as expand our software capabilities to provide customers with comprehensive computing solutions. Despite our ongoing efforts, there is no guarantee that we will achieve or maintain consumer and market demand or acceptance for our products and services in these various market segments.

To compete successfully, we must maintain a successful R&D effort, develop new products and production processes, and improve our existing products and processes ahead of competitors. For example, we invest substantially in our network of manufacturing and assembly and test facilities, including the construction of new fabrication facilities to support smaller transistor geometries and larger wafers. Our R&D efforts are critical to our success and are aimed at solving complex problems, and we do not expect all of our projects to be successful. We may be unable to develop and market new products successfully, and the products we invest in and develop may not be well-received by customers. Our R&D investments may not generate significant operating income or contribute to our future operating results for several years, and such contributions may not meet our expectations or even cover the costs of such investments. Additionally, the products and technologies offered by others may affect demand for, or pricing of, our products.

If we are not able to compete effectively, our financial results will be adversely affected, including increased costs and reduced revenue and gross margin, and we may be required to accelerate the write-down of the value of certain assets.

20

Table of Contents

Changes in the mix of products sold may harm our financial results. Prices differ widely among the platforms we offer in our various market segments due to differences in features offered or manufacturing costs. For example, product offerings range from lower-priced and entry-level platforms, such as those based on Intel Quark or Intel Atom processors, to higher-end platforms based on Intel Xeon and Intel Itanium processors. If demand shifts from our higher-priced to lower-priced platforms in any of our market segments, our gross margin and revenue would decrease. In addition, when products are introduced, they tend to have higher costs because of initial development costs and lower production volumes relative to the previous product generation, which can impact gross margin.

We operate globally and are subject to significant risks in many jurisdictions.

Global or regional conditions may harm our financial results. We have manufacturing, assembly and test, R&D, sales, and other operations in many countries, and some of our business activities may be concentrated in one or more geographic areas. Moreover, sales outside the U.S. accounted for approximately 80% of our revenue for the fiscal year ended December 26, 2015 . As a result, our operations and our financial results, including our ability to manufacture, assemble and test, design, develop, or sell products, may be adversely affected by a number of factors outside of our control, including:

• | global and local economic conditions; |

• | geopolitical and security issues, such as armed conflict and civil or military unrest, crime, political instability, and terrorist activity; |

• | natural disasters, public health issues, and other catastrophic events; |

• | inefficient infrastructure and other disruptions, such as supply chain interruptions and large-scale outages or unreliable provision of services from utilities, transportation, data hosting, or telecommunications providers; |

• | government restrictions on, or nationalization of our operations in any country, or restrictions on our ability to repatriate earnings from a particular country; |

• | differing employment practices and labor issues; |

• | formal or informal imposition of new or revised export and/or import and doing-business regulations, which could be changed without notice; |

• | ineffective legal protection of our IP rights in certain countries; and |

• | local business and cultural factors that differ from our normal standards and practices. |

We are subject to laws and regulations worldwide, which may differ among jurisdictions, affecting our operations in areas including, but not limited to: IP ownership and infringement, tax, import and export requirements, anti-corruption, foreign exchange controls and cash repatriation restrictions, data privacy requirements, anti-competition, advertising, employment, environment, health, and safety. Compliance with such requirements may be onerous and expensive, and may otherwise impact our business operations negatively. Although we have policies, controls, and procedures designed to help ensure compliance with applicable laws, there can be no assurance that our employees, contractors, suppliers, and/or agents will not violate such laws or our policies. Violations of these laws and regulations could result in fines; criminal sanctions against us, our officers, or our employees; prohibitions on the conduct of our business; and damage to our reputation.