UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☑ | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended January 30, 2016 | |

¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

| For the transition period from to |

Commission File Number 1-7562

THE GAP, INC.

(Exact name of registrant as specified in its charter)

Delaware | 94-1697231 |

(State of Incorporation) | (I.R.S. Employer Identification No.) |

Two Folsom Street, San Francisco, California | 94105 |

(Address of principal executive offices) | (Zip code) |

Registrant's telephone number, including area code: (415) 427-0100

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.05 par value | The New York Stock Exchange |

(Title of class) | (Name of exchange where registered) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ☑ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act:

Large accelerated filer ☑ |

| Accelerated filer ¨ |

| Non-accelerated filer ¨ |

| Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ☑

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of July 31, 2015 was approximately $10 billion based upon the last price reported for such date in the NYSE-Composite transactions.

The number of shares of the registrant's common stock outstanding as of March 15, 2016 was 397,140,119 .

Documents Incorporated by Reference

Portions of the registrant's Proxy Statement for the Annual Meeting of Shareholders to be held on May 17, 2016 (hereinafter referred to as the " 2016 Proxy Statement") are incorporated into Part III.

Special Note on Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. All statements other than those that are purely historical are forward-looking statements. Words such as "expect," "anticipate," "believe," "estimate," "intend," "plan," "project," and similar expressions also identify forward-looking statements. Forward-looking statements include, but are not limited to, statements regarding the following:

• | target cash balance and ability to provide for our working capital needs and for unexpected business downturns; |

• | continuing to evolve our customer experience, with particular focus on the mobile and digital expressions of our brands; |

• | attracting, retaining, and training great talent in our businesses and functions; |

• | improving sales performance through a more consistent, on-trend product offering; |

• | continued focus on our responsive supply chain and inventory management initiatives; |

• | continuing our investment in mobile digital capabilities; |

• | enhancing our shopping experience for our customers; |

• | continuing growth through new stores with a focus on Asia, outlet, and Athleta; |

• | impact of foreign exchange rate fluctuations in fiscal 2016; |

• | net store openings in fiscal 2016; |

• | square footage for company-operated stores in fiscal 2016; |

• | operating margin in fiscal 2016; |

• | current cash balances and cash flows being sufficient to support our business operations, including growth initiatives, planned capital expenditures, and repayment of debt; |

• | ability to supplement near-term liquidity, if necessary, with our $500 million revolving credit facility or other available market instruments; |

• | the impact of the seasonality of our operations; |

• | cash spending for purchases of property and equipment in fiscal 2016; |

• | dividend payments in fiscal 2016; |

• | the estimates and assumptions we use in our accounting policies; |

• | the impact of accounting pronouncements; |

• | unrealized gains and losses from designated cash flow hedges; |

• | total gross unrecognized tax benefits; |

• | expected payments to International Business Machines Corporation ("IBM"); |

• | the impact of losses due to indemnification obligations; |

• | the outcome of proceedings, lawsuits, disputes, and claims; and |

• | the impact of changes in internal control over financial reporting. |

Because these forward-looking statements involve risks and uncertainties, there are important factors that could cause our actual results to differ materially from those in the forward-looking statements. These factors include, without limitation, the following:

• | the risk that the adoption of new accounting pronouncements will impact future results; |

• | the risk that we or our franchisees will be unsuccessful in gauging apparel trends and changing consumer preferences; |

• | the risk that changes in global economic conditions or consumer spending patterns could adversely impact our results of operations; |

• | the highly competitive nature of our business in the United States and internationally; |

• | the risk that if we are unable to manage our inventory effectively, our gross margins will be adversely affected; |

• | the risk that the failure to attract and retain key personnel, or effectively manage succession, could have an adverse impact on our results of operations; |

• | the risk that we are subject to data or other security breaches that may result in increased costs, violations of law, significant legal and financial exposure, and a loss of confidence in our security measures, which could have an adverse effect on our results of operations and our reputation; |

• | the risks to our efforts to expand internationally, including our ability to operate under a global brand structure and operating in regions where we have less experience; |

• | the risk that foreign currency exchange rate fluctuations could adversely impact our financial results; |

• | the risks to our business, including our costs and supply chain, associated with global sourcing and manufacturing; |

• | the risks to our reputation or operations associated with importing merchandise from foreign countries, including failure of our vendors to adhere to our Code of Vendor Conduct; |

• | the risk that trade matters could increase the cost or reduce the supply of apparel available to us and adversely affect our business, financial condition, and results of operations; |

• | the risk that our franchisees' operation of franchise stores is not directly within our control and could impair the value of our brands; |

• | the risk that we or our franchisees will be unsuccessful in identifying, negotiating, and securing new store locations and renewing, modifying, or terminating leases for existing store locations effectively; |

• | the risk that our investments in omni-channel shopping initiatives may not deliver the results we anticipate; |

• | the risk that comparable sales and margins will experience fluctuations; |

• | the risk that changes in our credit profile or deterioration in market conditions may limit our access to the capital markets and adversely impact our financial results or our business initiatives; |

• | the risk that updates or changes to our information technology ("IT") systems may disrupt our operations; |

• | the risk that failure to maintain, enhance and protect our brand image could have an adverse effect on our results of operations; |

• | the risk that natural disasters, public health crises, political crises, or other catastrophic events could adversely affect our operations and financial results, or those of our franchisees or vendors; |

• | the risk that changes in the regulatory or administrative landscape could adversely affect our financial condition, strategies, and results of operations; |

• | the risk that we do not repurchase some or all of the shares we anticipate purchasing pursuant to our repurchase program; and |

• | the risk that we will not be successful in defending various proceedings, lawsuits, disputes, claims, and audits. |

Additional information regarding factors that could cause results to differ can be found in this Annual Report on Form 10-K and our other filings with the U.S. Securities and Exchange Commission ("SEC").

Future economic and industry trends that could potentially impact net sales and profitability are difficult to predict. These forward-looking statements are based on information as of March 21, 2016 , and we assume no obligation to publicly update or revise our forward-looking statements even if experience or future changes make it clear that any projected results expressed or implied therein will not be realized.

THE GAP, INC.

2015

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

|

| Page |

PART I | ||

|

|

|

Item 1. | Business | 1 |

|

|

|

Item 1A. | Risk Factors | 4 |

|

|

|

Item 1B. | Unresolved Staff Comments | 11 |

|

|

|

Item 2. | Properties | 11 |

|

|

|

Item 3. | Legal Proceedings | 12 |

|

|

|

Item 4. | Mine Safety Disclosures | 12 |

| ||

PART II | ||

|

|

|

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 13 |

|

|

|

Item 6. | Selected Financial Data | 16 |

|

|

|

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 18 |

|

|

|

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 31 |

|

|

|

Item 8. | Financial Statements and Supplementary Data | 32 |

|

|

|

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 69 |

|

|

|

Item 9A. | Controls and Procedures | 69 |

|

|

|

Item 9B. | Other Information | 69 |

| ||

PART III | ||

|

|

|

Item 10. | Directors, Executive Officers and Corporate Governance | 69 |

|

|

|

Item 11. | Executive Compensation | 69 |

|

|

|

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 70 |

|

|

|

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 70 |

|

|

|

Item 14. | Principal Accounting Fees and Services | 70 |

| ||

PART IV | ||

|

|

|

Item 15. | Exhibits, Financial Statement Schedules | 71 |

Part I

Item 1. Business.

General

The Gap, Inc. (Gap Inc., the "Company," "we," and "our") was incorporated in the State of California in July 1969 and was reincorporated under the laws of the State of Delaware in May 1988.

Gap Inc. is a leading global apparel retail company. We offer apparel, accessories, and personal care products for men, women, and children under the Gap, Banana Republic, Old Navy, Athleta, and Intermix brands. Our portfolio of distinct brands across multiple channels and geographies gives us a competitive advantage in the global retail marketplace.

Gap Inc. has Company-operated stores in the United States, Canada, the United Kingdom, France, Ireland, Japan, Italy, China, Hong Kong, Taiwan, and beginning in October 2015, Mexico. We also have franchise agreements with unaffiliated franchisees to operate Gap, Banana Republic, and Old Navy stores throughout Asia, Australia, Europe, Latin America, the Middle East, and Africa. Under these agreements, third parties operate, or will operate, stores that sell apparel and related products under our brand names. Our products are also available to customers online through Company-owned websites and through the use of third parties that provide logistics and fulfillment services. Most of the products sold under our brand names are designed by us and manufactured by independent sources. We also sell products that are designed and manufactured by branded third parties, especially at our Intermix brand.

In addition to operating in the specialty, outlet, online, and franchise channels, Gap Inc. is a leader among apparel retailers in using omni-channel capabilities to bridge the digital world and physical stores, creating world-class shopping experiences regardless of where or how customers shop. The Company's suite of omni-channel services, including order-in-store, reserve-in-store, find-in-store, and ship-from-store, as well as enhanced mobile experiences, are uniquely tailored across its portfolio of brands.

Gap. Gap is one of the world's most iconic apparel and accessories brands anchored in optimistic, casual, American style. Founded in San Francisco in 1969, our collections continue to build the foundation of modern wardrobes - all things denim, tees, button-downs, and khakis, along with must-have trends.

Gap is designed to build the foundation of modern wardrobes through every stage of life with apparel and accessories for adult men and women under the Gap name, in addition to GapKids, babyGap, GapMaternity, GapBody, and GapFit collections. Beginning in 1987 with the opening of our first store outside North America in London, Gap continues to connect with customers around the world through specialty stores, online, and franchise stores. In addition, we bring the brand to our value-conscious customers, with exclusively designed collections for Gap Outlet and Gap Factory stores and websites.

Banana Republic. Acquired with two stores in 1983 as a travel and adventure outfitter, Banana Republic is now a global apparel and accessories brand focused on delivering versatile, contemporary classics, designed for today with style that endures. Banana Republic offers clothing, eyewear, jewelry, shoes, handbags, and fragrances with detailed craftsmanship and luxurious materials. Customers can purchase Banana Republic products globally in our specialty and outlet stores, online, and in franchise stores.

Old Navy. Old Navy is a global apparel and accessories brand that believes in the democracy of style, making current, on-trend American essentials accessible to every family. Old Navy opened its first store in 1994 in the United States, and expanded globally in 2012 with its first store outside North America in Japan. Since then, Old Navy has continued to expand its global presence, with its first Company-operated stores in China and franchise stores in the Philippines in 2014. Customers can purchase Old Navy products globally in stores, online, and in franchise stores.

1

Athleta. Acquired in September 2008, Athleta is Gap Inc.'s premier fitness and lifestyle brand in the rapidly growing women's active apparel market. Athleta creates versatile and fashionable performance and lifestyle apparel for the fitness-minded woman who lives life on the go. Athleta offers apparel and gear for a range of activities from yoga to strength training and running, as well as seasonal sports, including skiing and tennis. Customers can purchase Athleta products in stores, online, and through its catalogs.

Intermix. Acquired in December 2012, Intermix curates must-have styles from the most coveted emerging and established designers. Known for styling on-trend pieces in unexpected ways, Intermix delivers a unique point of view and an individualized approach to shopping and personal style. Customers can shop in stores in the United States and Canada, and online.

Piperlime. Launched in 2006, Piperlime offered a mix of private label and branded apparel and accessories. As previously announced in January 2015, the Company closed the Piperlime brand during the first half of fiscal 2015, including the Piperlime e-commerce site, social channels, and one store in New York City.

All sales to customers are tendered for cash, debit cards, credit cards, or personal checks. We also issue and redeem gift cards through our brands. Gap, Banana Republic, Old Navy, and Athleta each have a private label credit card program and a co-branded credit card program through which frequent customers receive benefits. Private label and co-branded credit cards are provided by a third-party financing company.

The range of merchandise displayed in each store varies depending on the selling season and the size and location of the store. Stores are generally open seven days per week (where permitted by law) and most holidays.

We ended fiscal 2015 with 3,721 Company-operated and franchise store locations. For more information on the number of stores by brand and region, see the table in "Management's Discussion and Analysis of Financial Condition and Results of Operations" included in Part II, Item 7 of this Form 10-K.

Certain financial information about international operations is set forth under the heading "Segment Information" in Note 16 of Notes to Consolidated Financial Statements included in Part II, Item 8 of this Form 10-K.

Merchandise Vendors

We purchase private label and non-private label merchandise from about 1,000 vendors. Our vendors have factories in about 40 countries. Our two largest vendors each accounted for about 5 percent of the dollar amount of our total fiscal 2015 purchases. Of our merchandise purchased during fiscal 2015 , approximately 99 percent of purchases, by dollar value, were from factories outside the United States, while the remaining 1 percent of all purchases were from domestic factories. Approximately 24 percent of our fiscal 2015 purchases, by dollar value, were from factories in China. Product cost increases or events causing disruption of imports from China or other foreign countries, including the imposition of additional import restrictions or vendors potentially failing due to political, financial, or regulatory issues, could have an adverse effect on our operations. Substantially all of our foreign purchases of merchandise are negotiated and paid for in U.S. dollars. Also see the sections entitled "Risk Factors-Our business, including our costs and supply chain, is subject to risks associated with global sourcing and manufacturing," "Risk Factors-Risks associated with importing merchandise from foreign countries, including failure of our vendors to adhere to our Code of Vendor Conduct, could harm our business," and "Risk Factors-Trade matters may disrupt our supply chain" in Item 1A of this Form 10-K.

Seasonal Business

Our business follows a seasonal pattern, with sales peaking during the end-of-year holiday period.

Brand Building

Our ability to develop and evolve our existing brands is a key to our success. We believe our distinct brands are among our most important assets. With the exception of Intermix, virtually all aspects of brand development, from product design and distribution to marketing, merchandising and shopping environments, are controlled by Gap Inc. employees. With respect to Intermix, we control all aspects of brand development except for product design related to third-party products. We continue to invest in our business and enhance the customer experience through significant investments in marketing and our omni-channel capabilities, enhancement of our online shopping sites, international expansion, remodeling of existing stores, and investments in our supply chain.

2

Trademarks and Service Marks

Gap, GapKids, babyGap, GapMaternity, GapBody, GapFit, Banana Republic, Old Navy, Athleta, and Intermix trademarks and service marks, and certain other trademarks, have been registered, or are the subject of pending trademark applications, with the United States Patent and Trademark Office and with the registries of many foreign countries and/or are protected by common law.

Franchising

We have franchise agreements with unaffiliated franchisees to operate Gap, Banana Republic, and Old Navy stores in a number of countries throughout Asia, Australia, Europe, Latin America, the Middle East, and Africa. Under these agreements, third parties operate, or will operate, stores that sell apparel and related products under our brand names. For additional information on risks related to our franchise business, see the sections entitled "Risk Factors-Our efforts to expand internationally may not be successful" and "Risk Factors-Our franchise business is subject to certain risks not directly within our control that could impair the value of our brands" in Item 1A of this Form 10-K.

Inventory

The nature of the retail business requires us to carry a significant amount of inventory, especially prior to peak holiday selling season when we, along with other retailers, generally build up inventory levels. We maintain a large part of our inventory in distribution centers. We review our inventory levels in order to identify slow-moving merchandise and broken assortments (items no longer in stock in a sufficient range of sizes or colors) and we primarily use promotions and markdowns to clear merchandise. Also see the sections entitled "Risk Factors-We must successfully gauge apparel trends and changing consumer preferences to succeed" and "Risk Factors-If we are unable to manage our inventory effectively, our gross margins could be adversely affected" in Item 1A of this Form 10-K.

Competitors

The global apparel retail industry is highly competitive. We compete with local, national, and global apparel retailers. We are also faced with competition in European, Japanese, Chinese, and Canadian markets from established regional and national chains, and our franchisees face significant competition in the markets in which they operate. Also see the section entitled "Risk Factors-Our business is highly competitive" in Item 1A of this Form 10-K.

Employees

As of January 30, 2016 , we had a workforce of approximately 141,000 employees, which includes a combination of part-time and full-time employees. We also hire seasonal employees, primarily during the peak end-of-year holiday period.

To remain competitive in the apparel retail industry, we must attract, develop, and retain skilled employees in our design, merchandising, marketing, and other functions. Competition for such personnel is intense. Our success is dependent to a significant degree on the continued contributions of key employees. Also see the section entitled "Risk Factors-The failure to attract and retain key personnel, or effectively manage succession, could have an adverse impact on our results of operations" in Item 1A of this Form 10-K.

Available Information

We make available on our website, www.gapinc.com, under "Investors, Financial Information, SEC Filings," free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after we electronically file or furnish them to the SEC.

Our Board of Directors Committee Charters (Audit and Finance, Compensation and Management Development, and Governance and Sustainability Committees) and Corporate Governance Guidelines are also available on our website under "Investors, Governance." Our Code of Business Conduct can be found on our website under "Investors, Corporate Compliance, Code of Business Conduct." Any amendments and waivers to the Code will also be available on the website.

3

Executive Officers of the Registrant

The following are our executive officers:

Name, Age, Position, and Principal Occupation:

Arthur Peck , 60, Director and Chief Executive Officer since February 2015; President, Growth, Innovation, and Digital division from November 2012 to January 2015; President, Gap North America from February 2011 to November 2012; Executive Vice President of Strategy and Operations from May 2005 to February 2011; President, Gap Inc. Outlet from October 2008 to February 2011; Acting President, Gap Inc. Outlet from February 2008 to October 2008.

Paul Chapman , 58, Executive Vice President, Chief Information Officer since December 2015; Senior Vice President and Chief Information Officer from January 2014 to December 2015; Senior Vice President, Information Technology, from 2010 to 2015; Vice President, Information Technology from 2004 to 2010.

Solomon Goldfarb , 51, Executive Vice President, Digital and Customer Experience since February 2015; Senior Vice President, Digital Platform Strategy and Product Management from February 2013 to January 2015; Senior Vice President, Enterprise Product Management from March 2012 to February 2013; Vice President, International E-Commerce and Product Management from March 2009 to March 2012; Vice President, Growth, Innovation, and Digital Product Management from March 2006 to March 2009.

Julie Gruber , 50, Executive Vice President, Global General Counsel, Corporate Secretary, and Chief Compliance Officer since February 2016; Senior Vice President and General Counsel from March 2015 to February 2016; Vice President and Deputy General Counsel from 2007 to 2015; Associate General Counsel from 2003 to 2007.

Jeff Kirwan, 49, Global President, Gap since December 2014; Executive Vice President and President, Gap China from February 2013 to December 2014; Senior Vice President, Managing Director and Chief Operating Officer, Gap China from May 2011 to February 2013; Senior Vice President, Stores and Operations, Old Navy from August 2008 to May 2011; Senior Vice President and General Manager, Old Navy Canada from March 2008 to August 2008; Vice President and General Manager, Old Navy Canada from April 2007 to March 2008.

Andi Owen, 50, Global President, Banana Republic since January 2015; Executive Vice President and General Manager, Global Gap Outlet from January 2013 to January 2015; Senior Vice President and General Manager, Gap Outlet / Shared Services from January 2008 to January 2013; Vice President, Merchandising - Outlet from July 2006 to January 2008.

Bobbi Silten, 55, Executive Vice President, Global Talent and Sustainability since May 2015; Senior Vice President, Global Responsibility & President, Gap Foundation, 2010 to 2015; Chief Foundation Officer, Gap Foundation, 2005 to 2010.

Sabrina Simmons , 52, Executive Vice President and Chief Financial Officer since January 2008; Executive Vice President, Corporate Finance from September 2007 to January 2008; Senior Vice President, Corporate Finance and Treasurer from March 2003 to September 2007; Vice President and Treasurer from September 2001 to March 2003.

Sonia Syngal , 46, Executive Vice President, Global Supply Chain and Product Operations since February 2015; Executive Vice President, Global Supply Chain from November 2013 to January 2015; Senior Vice President , Old Navy International from February 2013 to November 2013; Senior Vice President and Managing Director, Europe from May 2011 to February 2013; Senior Vice President and General Manager , International Outlets from January 2010 to May 2011; Vice President of Global Production, Supply Chain - Outlet from July 2006 to January 2010; Vice President , Corporate Sourcing from July 2004 to July 2006.

Item 1A. Risk Factors.

Our past performance may not be a reliable indicator of future performance because actual future results and trends may differ materially depending on a variety of factors, including but not limited to the risks and uncertainties discussed below. In addition, historical trends should not be used to anticipate results or trends in future periods.

4

We must successfully gauge apparel trends and changing consumer preferences to succeed.

Our success is largely dependent upon our ability to gauge the tastes of our customers and to provide merchandise that satisfies customer demand in a timely manner. However, lead times for many of our design and purchasing decisions may make it more difficult for us to respond rapidly to new or changing apparel trends or consumer acceptance of our products. The global apparel retail business fluctuates according to changes in consumer preferences, dictated in part by apparel trends and season. To the extent we misjudge the market for our merchandise or the products suitable for local markets or fail to execute trends and deliver product to market as timely as our competitors, our sales will be adversely affected, and the markdowns required to move the resulting excess inventory will adversely affect our operating results. For example, during fiscal 2015, product acceptance at Banana Republic and Gap brand, in particular, was below expectations, and as a result, our financial results were negatively impacted.

Global economic conditions and the impact on consumer spending patterns could adversely impact our results of operations.

The Company's performance is subject to global economic conditions and their impact on levels of consumer spending worldwide. Some of the factors that may influence consumer spending include high levels of unemployment, higher consumer debt levels, reductions in net worth based on market declines and uncertainty, home foreclosures and reductions in home values, fluctuating interest rates and credit availability, government austerity measures, fluctuating fuel and other energy costs, fluctuating commodity prices, and general uncertainty regarding the overall future economic environment. Consumer purchases of discretionary items, including our merchandise, generally decline during periods when disposable income is adversely affected or there is economic uncertainty.

Adverse economic changes in any of the regions in which we and our franchisees sell our products could reduce consumer confidence, and thereby could negatively affect earnings and have a material adverse effect on our results of operations. In challenging and uncertain economic environments, we cannot predict whether or when such circumstances may improve or worsen, or what impact, if any, such circumstances could have on our business, results of operations, cash flows, and financial position.

Our business is highly competitive.

The global apparel retail industry is highly competitive. We and our franchisees compete with local, national, and global department stores, specialty and discount store chains, independent retail stores, and online businesses that market similar lines of merchandise. We face a variety of competitive challenges including:

• | anticipating and quickly responding to changing apparel trends and customer demands; |

• | attracting customer traffic both in stores and online; |

• | competitively pricing our products and achieving customer perception of value; |

• | maintaining favorable brand recognition and effectively marketing our products to customers in several diverse market segments and geographic locations; |

• | anticipating and responding to changing customer shopping preferences and practices, including the increasing shift to digital brand engagement, social media communication, and online shopping; |

• | developing innovative, high-quality products in sizes, colors, and styles that appeal to customers of varying age groups and tastes; |

• | purchasing and stocking merchandise to match seasonal weather patterns, and our ability to react to shifts in weather that impact consumer demand; and |

• | sourcing merchandise efficiently. |

If we or our franchisees are not able to compete successfully in the United States or internationally, our results of operations would be adversely affected.

5

If we are unable to manage our inventory effectively, our gross margins could be adversely affected.

Fluctuations in the global apparel retail markets impact the levels of inventory owned by apparel retailers. The nature of the global apparel retail business requires us to carry a significant amount of inventory, especially prior to the peak holiday selling season when we build up our inventory levels. Merchandise usually must be ordered well in advance of the season and frequently before apparel trends are confirmed by customer purchases. We must enter into contracts for the purchase and manufacture of merchandise well in advance of the applicable selling season. As a result, we are vulnerable to demand and pricing shifts and to suboptimal selection and timing of merchandise purchases. In the past, we have not always predicted our customers' preferences and acceptance levels of our trend items with accuracy. If sales do not meet expectations, too much inventory may cause excessive markdowns and, therefore, lower than planned margins.

We have key strategic initiatives designed to optimize our inventory levels and increase the efficiency and responsiveness of our supply chain, including vendor fabric platforming, product demand testing, and in-season rapid response to demand. These initiatives involve significant systems and operational changes and we have limited experience operating in this manner. If we are unable to implement these initiatives successfully, we may not realize the return on our investments that we anticipate, and our operating results could be adversely affected.

The failure to attract and retain key personnel, or effectively manage succession, could have an adverse impact on our results of operations.

Our ability to anticipate and effectively respond to changing apparel trends depends in part on our ability to attract and retain key personnel in our design, merchandising, marketing, and other functions. In addition, several of our strategic initiatives, including our technology initiatives and supply chain initiatives require that we hire and/or develop employees with appropriate experience. Competition for this personnel is intense, and we cannot be sure that we will be able to attract and retain a sufficient number of qualified personnel in future periods. If we are unable to retain, attract, and motivate talented employees with the appropriate skill sets, or if changes to our organizational structure, operating results, or business model adversely affect morale or retention, we may not achieve our objectives and our results of operations could be adversely impacted. In addition, the loss of one or more of our key personnel or the inability to effectively identify a suitable successor to a key role could have a material adverse effect on our business. At the end of fiscal 2014 and beginning of fiscal 2015, there were several changes made to our senior leadership team, including our Chief Executive Officer; Global President, Gap; and Global President, Banana Republic. In October 2015, our Global President, Old Navy left the Company, and a search for a new global brand president is underway. The effectiveness of the new leaders in these roles, and any further transition as a result of these changes, could have a significant impact on our results of operations.

We are subject to data security risks, which could have an adverse effect on our results of operations and consumer confidence in our security measures.

As part of our normal operations, we receive and maintain confidential, proprietary, and personally identifiable information, including credit card information, about our customers, our employees, job applicants, and other third parties. Our business employs systems and websites that allow for the secure storage and transmission of this information. However, despite our safeguards and security processes and protections, security breaches could expose us to a risk of loss or misuse of this information, litigation, and potential liability. The retail industry, in particular, has been the target of many recent cyber-attacks. We may not have the resources to anticipate or prevent rapidly evolving types of cyber-attacks. Attacks may be targeted at us, our customers, or others who have entrusted us with information. In addition, even if we take appropriate measures to safeguard our information security and privacy environment from security breaches, we could still expose our customers and our business to risk. Actual or anticipated attacks may disrupt or impair our technology capabilities, and may cause us to incur increasing costs, including costs to deploy additional personnel and protection technologies, train employees, and engage third-party experts and consultants. Advances in computer capabilities, new technological discoveries, or other developments may result in the technology used by us to protect transaction or other data being breached or compromised. Measures we implement to protect against cyber-attacks may also have the potential to impact our customers' shopping experience or decrease activity on our websites by making them more difficult to use. Data and security breaches can also occur as a result of non-technical issues, including intentional or inadvertent breach by our employees or by persons with whom we have commercial relationships that result in the

6

unauthorized release of personal or confidential information. In addition, the regulatory environment surrounding information security, cybersecurity, and privacy is increasingly demanding, with new and changing requirements, and customers have a high expectation that the Company will adequately protect their personal information from cyber-attack or other security breaches. Security breaches and cyber incidents could result in a violation of applicable privacy and other laws, significant legal and financial exposure, and a loss of consumer confidence in our security measures, which could have an adverse effect on our results of operations and our reputation.

Our efforts to expand internationally may not be successful.

Our current strategies include pursuing continued international expansion in a number of countries around the world through a number of channels. We currently plan to open additional Old Navy stores outside of the United States, including in Mexico, Japan, and China, open additional Gap stores in China, open additional international outlet stores, and continue to grow online sales internationally. Our franchisees plan to open additional stores internationally. We have limited experience operating or franchising in some of these locations. In many of these locations, we face major, established competitors. In addition, in many of these locations, the real estate, employment and labor, transportation and logistics, regulatory, and other operating requirements differ dramatically from those in the places where we have more experience. Consumer tastes and trends may differ in many of these locations and, as a result, the sales of our products may not be successful or result in the margins we anticipate. If our international expansion plans are unsuccessful or do not deliver an appropriate return on our investments, our operations and financial results could be materially, adversely affected.

Our business is exposed to the risks of foreign currency exchange rate fluctuations and our hedging strategies may not be effective in mitigating those risks.

We are exposed to foreign currency exchange rate risk with respect to our sales, inventory purchases, operating expenses, profits, assets, and liabilities generated or incurred outside the U.S. Although we use financial instruments to hedge certain foreign currency risks, these measures may not succeed in fully offsetting the negative impact of foreign currency rate movements and generally only delay the impact of adverse foreign currency rate movements on our business and financial results. For example, in fiscal year 2015, foreign exchange fluctuations, in particular the depreciation of the currencies in Canada and Japan where we have significant retail operations, had a significant impact on our financial results. We expect this impact to continue in fiscal year 2016.

Our business, including our costs and supply chain, is subject to risks associated with global sourcing and manufacturing.

Independent third parties manufacture all of our products for us. As a result, we are directly impacted by increases in the cost of those products .

If we experience significant increases in demand or need to replace an existing vendor, there can be no assurance that additional manufacturing capacity will be available when required on terms that are acceptable to us or that any vendor would allocate sufficient capacity to us in order to meet our requirements. In addition, for any new manufacturing source, we may encounter delays in production and added costs as a result of the time it takes to train our vendors in our methods, products, quality control standards, and environmental, labor, health, and safety standards. Moreover, in the event of a significant disruption in the supply of the fabrics or raw materials used by our vendors in the manufacture of our products, our vendors might not be able to locate alternative suppliers of materials of comparable quality at an acceptable price. Any delays, interruption, or increased costs in the manufacture of our products could result in lower sales and net income. In addition, certain countries represent a larger portion of our global sourcing. For example, approximately 24 percent of our merchandise, by dollar value, is purchased from factories in China. Accordingly, any delays in production and added costs in China could have a more significant impact on our results of operations.

Because independent vendors manufacture virtually all of our products outside of our principal sales markets, third parties must transport our products over large geographic distances. Delays in the shipment or delivery of our products due to the availability of transportation, work stoppages, port strikes, infrastructure congestion, or other factors, and costs and delays associated with transitioning between vendors, could adversely impact our

7

financial performance. For example, the work slowdowns and stoppages at U.S. West Coast ports at the end of fiscal 2014 and beginning of fiscal 2015 created product delivery delays that impacted our ability to effectively manage our inventory and deliver seasonally correct product in a timely manner, which impacted our financial results for fiscal 2015. Manufacturing delays, transportation delays, or unexpected demand for our products may require us to use faster, but more expensive, transportation methods such as aircraft, which could adversely affect our gross margins. In addition, the cost of fuel is a significant component in transportation costs, so increases in the price of petroleum products can adversely affect our gross margins.

Risks associated with importing merchandise from foreign countries, including failure of our vendors to adhere to our Code of Vendor Conduct, could harm our business.

We purchase nearly all merchandise from third-party vendors in many different countries and we require those vendors to adhere to a Code of Vendor Conduct, which includes environmental, labor, health, and safety standards. From time to time, contractors or their subcontractors may not be in compliance with these standards or applicable local laws. Although we have implemented policies and procedures to facilitate our compliance with laws and regulations relating to doing business in foreign markets and importing merchandise into various countries, there can be no assurance that suppliers and other third parties with whom we do business will not violate such laws and regulations or our policies. Significant or continuing noncompliance with such standards and laws by one or more vendors could have a negative impact on our reputation, could subject us to liability, and could have an adverse effect on our results of operations.

Trade matters may disrupt our supply chain.

Trade restrictions, including increased tariffs or quotas, embargoes, safeguards, and customs restrictions against apparel items, as well as U.S. or foreign labor strikes, work stoppages, or boycotts, could increase the cost or reduce the supply of apparel available to us and adversely affect our business, financial condition, and results of operations. We cannot predict whether any of the countries in which our merchandise currently is manufactured or may be manufactured in the future will be subject to additional trade restrictions imposed by the United States or other foreign governments, including the likelihood, type, or effect of any such restrictions. In addition, we face the possibility of anti-dumping or countervailing duties lawsuits from U.S. domestic producers. We are unable to determine the impact of the changes to the quota system or the impact that potential tariff lawsuits could have on our global sourcing operations. Our sourcing operations may be adversely affected by trade limits or political and financial instability, resulting in the disruption of trade from exporting countries, significant fluctuation in the value of the U.S. dollar against foreign currencies, restrictions on the transfer of funds, and/or other trade disruptions.

Our franchise business is subject to certain risks not directly within our control that could impair the value of our brands.

We enter into franchise agreements with unaffiliated franchisees to operate stores and, in limited circumstances, websites, in many countries around the world. Under these agreements, third parties operate, or will operate, stores and websites that sell apparel and related products under our brand names. The effect of these arrangements on our business and results of operations is uncertain and will depend upon various factors, including the demand for our products in new markets internationally and our ability to successfully identify appropriate third parties to act as franchisees, distributors, or in a similar capacity. In addition, certain aspects of these arrangements are not directly within our control, such as franchisee financial stability and the ability of these third parties to meet their projections regarding store locations, store openings, and sales. Other risks that may affect these third parties include general economic conditions in specific countries or markets, foreign exchange rates, changes in diplomatic and trade relationships, restrictions on the transfer of funds, and political instability. Moreover, while the agreements we have entered into and plan to enter into in the future provide us with certain termination rights, the value of our brands could be impaired to the extent that these third parties do not operate their stores in a manner consistent with our requirements regarding our brand identities and customer experience standards. Failure to protect the value of our brands, or any other harmful acts or omissions by a franchisee, could have an adverse effect on our results of operations and our reputation.

8

The market for prime real estate is competitive.

Our ability to effectively obtain real estate - to open new stores, distribution centers, and corporate offices nationally and internationally - depends on the availability of real estate that meets our criteria for traffic, square footage, co-tenancies, lease economics, demographics, and other factors. We also must be able to effectively renew our existing store leases. In addition, from time to time, we may seek to downsize, consolidate, reposition, relocate, or close some of our real estate locations, which in most cases requires a modification of an existing store lease. Failure to secure adequate new locations or successfully modify existing locations, or failure to effectively manage the profitability of our existing fleet of stores, could have a material adverse effect on our results of operations.

Additionally, the economic environment may at times make it difficult to determine the fair market rent of real estate properties within the United States and internationally. This could impact the quality of our decisions to exercise lease options at previously negotiated rents and the quality of our decisions to renew expiring leases at negotiated rents. Any adverse effect on the quality of these decisions could impact our ability to retain real estate locations adequate to meet our targets or efficiently manage the profitability of our existing fleet of stores and could have a material adverse effect on our results of operations.

Our investments in omni-channel shopping initiatives may not deliver the results we anticipate.

One of our strategic priorities is to further develop an omni-channel shopping experience for our customers through the integration of our store and digital shopping channels. Examples of our recent omni-channel initiatives include our ship-from-store, reserve-in-store, and order-in-store programs. We continue to explore additional ways to develop an omni-channel shopping experience, including further digital integration and customer personalization. These initiatives involve significant investments in IT systems and significant operational changes. In addition, our competitors are also investing in omni-channel initiatives, some of which may be more successful than our initiatives . If the implementation of our omni-channel initiatives is not successful, or we do not realize the return on our omni-channel investments that we anticipate, our operating results would be adversely affected.

We experience fluctuations in our comparable sales and margins.

Our success depends in part on our ability to improve sales, in particular at our largest brands. A variety of factors affect comparable sales or margins, including apparel trends, competition, current economic conditions, the timing of new merchandise releases and promotional events, changes in our merchandise mix, the success of marketing programs, foreign currency fluctuations, and weather conditions. These factors may cause our comparable sales results to differ materially from prior periods and from expectations. Our comparable sales, including the associated comparable online sales, have fluctuated significantly in the past on an annual, quarterly, and monthly basis. Over the past fiscal year, our reported quarterly comparable sales have ranged from a high of negative 2 percent in the second and third quarters of fiscal 2015 to a low of negative 7 percent in the fourth quarter of fiscal 2015. Over the past five years, our reported gross margins have ranged from a high of 39.4 percent in fiscal 2012 to a low of 36.2 percent in fiscal 2015 and fiscal 2011. In addition, over the past five years, our reported operating margins have ranged from a high of 13.3 percent in fiscal 2013 to a low of 9.6 percent in fiscal 2015.

Our ability to deliver strong comparable sales results and margins depends in large part on accurately forecasting demand and apparel trends, selecting effective marketing techniques, providing an appropriate mix of merchandise for our broad and diverse customer base, managing inventory effectively, using effective pricing strategies, and optimizing store performance. Failure to meet the expectations of investors, securities analysts, or credit rating agencies in one or more future periods could reduce the market price of our common stock and cause our credit ratings to decline.

9

Changes in our credit profile or deterioration in market conditions may limit our access to the capital markets and adversely impact our financial results or our business initiatives.

In April 2011, we issued $ 1.25 billion aggregate principal amount of 5.95 percent notes due April 2021 . As a result, we have additional costs that include interest payable semiannually on the notes. In January 2014, we also entered into a 15 billion Japanese yen, four-year, unsecured term loan due January 2018. In October 2015, we entered into a $400 million unsecured term loan due October 2016, but that may be extended until October 2017.

Our cash flows from operations are the primary source of funds for these debt service payments. In this regard, we have generated annual cash flow from operating activities in excess of $1 billion per year for well over a decade and ended fiscal 2015 with $1.4 billion of cash and cash equivalents on our balance sheet. We are also able to supplement near-term liquidity, if necessary, with our $ 500 million revolving credit facility. We continue to target a cash balance between $1.0 billion to $1.2 billion, which provides not only for our working capital needs, but also a reserve for unexpected business downturns. However, if our cash flows from operating activities decline significantly, we may be required to reprioritize our business initiatives to ensure that we can continue to service or refinance our debt with favorable rates and terms. In addition, any future reduction in our long-term senior unsecured credit ratings could result in reduced access to the credit and capital markets and higher interest costs, and potentially increased lease or hedging costs.

For further information on our debt and credit facilities, see Part II, Item 8, Financial Statements and Supplementary Data, Notes 4 and 5 of Notes to Consolidated Financial Statements of this Form 10-K.

Updates or changes to our IT systems may disrupt operations.

We continue to evaluate and implement upgrades and changes to our IT systems, some of which are significant. Upgrades involve replacing existing systems with successor systems, making changes to existing systems, or cost-effectively acquiring new systems with new functionality. We are aware of inherent risks associated with replacing these systems, including accurately capturing data and system disruptions, and believe we are taking appropriate action to mitigate the risks through testing, training, and staging implementation, as well as ensuring appropriate commercial contracts are in place with third-party vendors supplying or supporting our IT initiatives. However, there can be no assurances that we will successfully launch these systems as planned or that they will be implemented without disruptions to our operations. IT system disruptions, if not anticipated and appropriately mitigated, or failure to successfully implement new or upgraded systems, could have a material adverse effect on our results of operations.

Failure to maintain our reputation and brand image could negatively impact our results of operations.

Our brands have wide recognition, and our success has been due in large part to our ability to maintain, enhance and protect our brand image and reputation, and our customers' connection to our brands. Our continued success depends in part on our ability to adapt to a rapidly changing media environment, including our increasing reliance on social media and online dissemination of advertising campaigns. Even if we react appropriately to negative posts or comments about us and/or our brands on social media and online, our customers' perception of our brand image and our reputation could be negatively impacted. Failure to maintain, enhance and protect our brand image could have a material adverse effect on our results of operations.

10

Our results could be adversely affected by natural disasters, public health crises, political crises, or other catastrophic events.

Natural disasters, such as hurricanes, tornadoes, floods, earthquakes, and other adverse weather and climate conditions; unforeseen public health crises, such as pandemics and epidemics; political crises, such as terrorist attacks, war, labor unrest, and other political instability; or other catastrophic events, such as disasters occurring at our vendors' manufacturing facilities, whether occurring in the United States or internationally, could disrupt our operations, the operations of our franchisees, or the operations of one or more of our vendors. In particular, these types of events could impact our product supply chain from or to the impacted region and could impact our ability or the ability of our franchisees or other third parties to operate our stores or websites. In addition, these types of events could negatively impact consumer spending in the impacted regions or depending upon the severity, globally. Disasters occurring at our vendors ' manufacturing facilities could impact our reputation and our customers ' perception of our brands. To the extent any of these events occur, our operations and financial results could be adversely affected.

Changes in the regulatory or administrative landscape could adversely affect our financial condition and results of operations.

Laws and regulations at the local, state, federal, and international levels frequently change, and the ultimate cost of compliance cannot be precisely estimated. In addition, we cannot predict the impact that may result from changes in the regulatory or administrative landscape. Any changes in regulations, the imposition of additional regulations, or the enactment of any new or more stringent legislation that impacts employment and labor, trade, product safety, transportation and logistics, health care, tax, privacy, operations, or environmental issues, among others, could have an adverse impact on our financial condition and results of operations.

We are subject to various proceedings, lawsuits, disputes, and claims from time to time, which could adversely affect our business, financial condition and results of operations.

As a multinational company, we are subject to various proceedings, lawsuits, disputes, and claims ("Actions") arising in the ordinary course of our business. Many of these Actions raise complex factual and legal issues and are subject to uncertainties. Actions filed against us from time to time include commercial, intellectual property, customer, employment, and data privacy claims, including class action lawsuits. The plaintiffs in some Actions seek unspecified damages or injunctive relief, or both. Actions are in various procedural stages and some are covered in part by insurance. We cannot predict with assurance the outcome of Actions brought against us. Accordingly, developments, settlements, or resolutions may occur and impact income in the quarter of such development, settlement, or resolution. An unfavorable outcome could have an adverse impact on our business, financial condition and results of operations.

Item 1B. Unresolved Staff Comments.

None.

Item 2. Properties.

We have Company-operated stores in the United States, Canada, the United Kingdom, France, Ireland, Japan, Italy, China, Hong Kong, Taiwan, and beginning in October 2015, Mexico. As of January 30, 2016 , we had 3,275 Company-operated stores, which aggregated to approximately 37.9 million square feet. Almost all of these stores are leased, typically with one or more renewal options after our initial term. Economic terms vary by type and location of store.

11

We own approximately 1.1 million square feet of corporate office space located in San Francisco, San Bruno, Pleasanton, and Rocklin, California, of which approximately 184,000 square feet is leased to and occupied by others. We lease approximately 925,000 square feet of corporate office space located in San Francisco, Rocklin, Petaluma, and Pleasanton, California; New York, New York; Albuquerque, New Mexico; and Toronto, Ontario, Canada. We also lease regional offices in North America and in various international locations. We own approximately 8.6 million square feet of distribution space located in Fresno, California; Fishkill, New York; Groveport, Ohio; Gallatin, Tennessee; Brampton, Ontario, Canada; and Rugby, England. Of the 8.6 million square feet of owned distribution space, approximately 117,000 square feet is leased to and occupied by others. We lease approximately 1.2 million square feet of distribution space located in Phoenix, Arizona; Grove City, Ohio; Erlanger and Hebron, Kentucky; and Bolton and Mississauga, Ontario, Canada. Third-party logistics companies provide logistics services to us through distribution warehouses in Chiba, Japan; and Shanghai and Hong Kong, China.

Item 3. Legal Proceedings.

We do not believe that the outcome of any current Action would have a material effect on our Consolidated Financial Statements.

Item 4. Mine Safety Disclosures.

Not applicable.

12

Part II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

The principal market on which our stock is traded is the New York Stock Exchange. The number of holders of record of our stock as of March 15, 2016 was 7,016. The table below sets forth the market prices and dividends declared and paid for each of the fiscal quarters in fiscal 2015 and 2014 .

|

| Market Prices |

| Dividends Declared and Paid | ||||||||||||||||||||

|

| Fiscal 2015 |

| Fiscal 2014 |

| Fiscal Year | ||||||||||||||||||

|

| High |

| Low |

| High |

| Low |

| 2015 |

| 2014 | ||||||||||||

1st Quarter |

| $ | 43.90 | |

| $ | 39.37 | |

| $ | 44.59 | |

| $ | 37.00 | |

| $ | 0.23 | |

| $ | 0.22 | |

2nd Quarter |

| $ | 40.64 | |

| $ | 35.58 | |

| $ | 42.37 | |

| $ | 38.38 | |

| 0.23 | |

| 0.22 | | ||

3rd Quarter |

| $ | 36.50 | |

| $ | 25.97 | |

| $ | 46.85 | |

| $ | 35.46 | |

| 0.23 | |

| 0.22 | | ||

4th Quarter |

| $ | 28.65 | |

| $ | 21.57 | |

| $ | 43.85 | |

| $ | 37.10 | |

| 0.23 | |

| 0.22 | | ||

|

|

|

|

|

|

|

|

|

| $ | 0.92 | |

| $ | 0.88 | | ||||||||

13

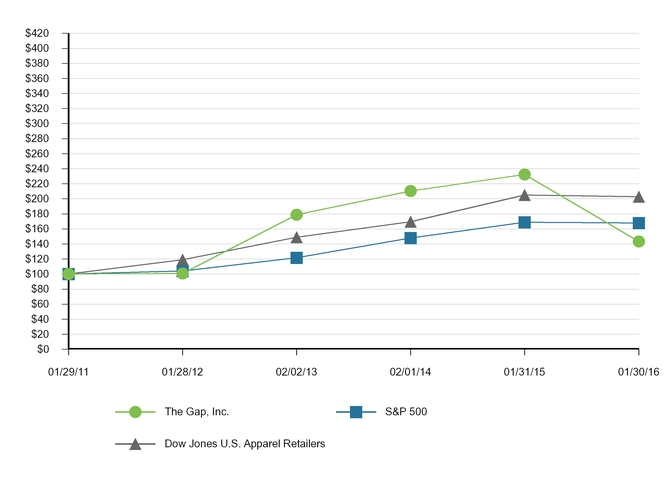

Stock Performance Graph

The graph below compares the percentage changes in our cumulative total stockholder return on our common stock for the five-year period ended January 30, 2016 , with (i) the cumulative total return of the Dow Jones U.S. Retail Apparel Index and (ii) the S&P 500 Index. The total stockholder return for our common stock assumes quarterly reinvestment of dividends.

TOTAL RETURN TO STOCKHOLDERS

(Assumes $100 investment on 1/29/2011)

Total Return Analysis

|

| 1/29/2011 |

| 1/28/2012 |

| 2/2/2013 |

| 2/1/2014 |

| 1/31/2015 |

| 1/30/2016 | ||||||||||||

The Gap, Inc. |

| $ | 100.00 | |

| $ | 100.95 | |

| $ | 178.81 | |

| $ | 210.28 | |

| $ | 232.33 | |

| $ | 143.41 | |

S&P 500 |

| $ | 100.00 | |

| $ | 104.22 | |

| $ | 121.71 | |

| $ | 147.89 | |

| $ | 168.93 | |

| $ | 167.81 | |

Dow Jones U.S. Apparel Retailers |

| $ | 100.00 | |

| $ | 119.05 | |

| $ | 149.07 | |

| $ | 169.51 | |

| $ | 205.28 | |

| $ | 202.64 | |

Source: Research Data Group, Inc. (415) 643-6000 (www.researchdatagroup.com)

14

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

The following table presents information with respect to purchases of common stock of the Company made during the thirteen weeks ended January 30, 2016 by The Gap, Inc. or any affiliated purchaser, as defined in Exchange Act Rule 10b-18(a)(3):

|

| Total Number of Shares Purchased |

| Average Price Paid Per Share Including Commissions |

| Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

| Maximum Number (or approximate dollar amount) of Shares that May Yet be Purchased Under the Plans or Programs (1) | ||||

Month #1 (November 1 - November 28) |

| 2,075,029 | |

| $ | 26.84 | |

| 2,075,029 | |

| $439 million |

Month #2 (November 29 - January 2) |

| 3,672,952 | |

| $ | 25.66 | |

| 3,672,952 | |

| $345 million |

Month #3 (January 3 - January 30) |

| 1,894,349 | |

| $ | 22.70 | |

| 1,894,349 | |

| $302 million |

Total |

| 7,642,330 | |

| $ | 25.25 | |

| 7,642,330 | |

|

|

__________

(1) | On February 26, 2015, we announced that the Board of Directors approved a $1 billion share repurchase authorization (the "February 2015 repurchase program"). On February 25, 2016, we announced that the Board of Directors approved a new $1 billion share repurchase authorization (the "February 2016 repurchase program"). The February 2015 repurchase program, which had $302 million remaining, was superseded and replaced by the February 2016 repurchase program, which has no expiration date. |

15

Item 6. Selected Financial Data.

The following selected financial data are derived from the Consolidated Financial Statements of the Company. We have also included certain non-financial data to enhance your understanding of our business. The data set forth below should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Item 7 and the Company's Consolidated Financial Statements and related notes in Item 8.

|

| Fiscal Year (number of weeks) | ||||||||||||||||||

|

| 2015 (52) |

| 2014 (52) |

| 2013 (52) |

| 2012 (53) |

| 2011 (52) | ||||||||||

Operating Results ($ in millions) |

|

|

|

|

|

|

|

|

|

| ||||||||||

Net sales |

| $ | 15,797 | |

| $ | 16,435 | |

| $ | 16,148 | |

| $ | 15,651 | |

| $ | 14,549 | |

Gross margin |

| 36.2 | % |

| 38.3 | % |

| 39.0 | % |

| 39.4 | % |

| 36.2 | % | |||||

Operating margin |

| 9.6 | % |

| 12.7 | % |

| 13.3 | % |

| 12.4 | % |

| 9.9 | % | |||||

Net income |

| $ | 920 | |

| $ | 1,262 | |

| $ | 1,280 | |

| $ | 1,135 | |

| $ | 833 | |

Cash dividends paid |

| $ | 377 | |

| $ | 383 | |

| $ | 321 | |

| $ | 240 | |

| $ | 236 | |

Per Share Data (number of shares in millions) |

|

|

|

|

|

|

|

|

|

| ||||||||||

Basic earnings per share |

| $ | 2.24 | |

| $ | 2.90 | |

| $ | 2.78 | |

| $ | 2.35 | |

| $ | 1.57 | |

Diluted earnings per share |

| $ | 2.23 | |

| $ | 2.87 | |

| $ | 2.74 | |

| $ | 2.33 | |

| $ | 1.56 | |

Weighted-average number of shares-basic |

| 411 | |

| 435 | |

| 461 | |

| 482 | |

| 529 | | |||||

Weighted-average number of shares-diluted |

| 413 | |

| 440 | |

| 467 | |

| 488 | |

| 533 | | |||||

Cash dividends declared and paid per share |

| $ | 0.92 | |

| $ | 0.88 | |

| $ | 0.70 | |

| $ | 0.50 | |

| $ | 0.45 | |

Balance Sheet Information ($ in millions) |

|

|

|

|

|

|

|

|

|

| ||||||||||

Merchandise inventory |

| $ | 1,873 | |

| $ | 1,889 | |

| $ | 1,928 | |

| $ | 1,758 | |

| $ | 1,615 | |

Total assets |

| $ | 7,473 | |

| $ | 7,690 | |

| $ | 7,849 | |

| $ | 7,470 | |

| $ | 7,422 | |

Working capital (1) |

| $ | 1,450 | |

| $ | 2,083 | |

| $ | 1,985 | |

| $ | 1,788 | |

| $ | 2,181 | |

Total long-term debt, less current maturities (2) |

| $ | 1,310 | |

| $ | 1,332 | |

| $ | 1,369 | |

| $ | 1,246 | |

| $ | 1,606 | |

Stockholders' equity |

| $ | 2,545 | |

| $ | 2,983 | |

| $ | 3,062 | |

| $ | 2,894 | |

| $ | 2,755 | |

Other Data ($ and square footage in millions) |

|

|

|

|

|

|

|

|

|

| ||||||||||

Cash used for purchases of property and equipment |

| $ | 726 | |

| $ | 714 | |

| $ | 670 | |

| $ | 659 | |

| $ | 548 | |

Acquisition of business, net of cash acquired (3) |

| $ | - | |

| $ | - | |

| $ | - | |

| $ | 129 | |

| $ | - | |

Percentage increase (decrease) in comparable sales (4) |

| (4 | )% |

| - | % |

| 2 | % |

| 5 | % |

| (4 | )% | |||||

Number of Company-operated store locations open at year-end |

| 3,275 | |

| 3,280 | |

| 3,164 | |

| 3,095 | |

| 3,036 | | |||||

Number of franchise store locations open at year-end |

| 446 | |

| 429 | |

| 375 | |

| 312 | |

| 227 | | |||||

Number of store locations open at year-end (5) |

| 3,721 | |

| 3,709 | |

| 3,539 | |

| 3,407 | |

| 3,263 | | |||||

Square footage of Company-operated store space at year-end |

| 37.9 | |

| 38.1 | |

| 37.2 | |

| 36.9 | |

| 37.2 | | |||||

Percentage increase (decrease) in square footage of Company-operated store space at year-end |

| (0.5 | )% |

| 2.4 | % |

| 0.8 | % |

| (0.8 | )% |

| (2.6 | )% | |||||

Number of employees at year-end |

| 141,000 | |

| 141,000 | |

| 137,000 | |

| 136,000 | |

| 132,000 | | |||||

(1) | In fiscal year 2015, we adopted the Financial Accounting Standards Board, Accounting Standard Update No. 2015-17, Income Taxes. The adoption reduced current portion of deferred tax assets as a result of classifying all net deferred tax assets as noncurrent as of January 30, 2016. |

16

(2) | In April 2012, we made the first scheduled payment of $40 million related to our $400 million term loan and in August 2012, we repaid the remaining $360 million balance in full. |

(3) | On December 31, 2012, we acquired all of the outstanding capital stock of Intermix, a multi-brand specialty retailer of luxury and contemporary apparel and accessories, for an aggregate purchase price of $129 million . |

(4) | Includes the associated comparable online sales. |

(5) | Includes Company-operated and franchise store locations. |

17

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

Overview

We are a global retailer offering apparel, accessories, and personal care products for men, women, and children under the Gap, Banana Republic, Old Navy, Athleta, and Intermix brands. We have Company-operated stores in the United States, Canada, the United Kingdom, France, Ireland, Japan, Italy, China, Hong Kong, Taiwan, and beginning in October 2015, Mexico. We have franchise agreements with unaffiliated franchisees to operate Gap, Banana Republic, and Old Navy stores throughout Asia, Australia, Europe, Latin America, the Middle East, and Africa. Under these agreements, third parties operate, or will operate, stores that sell apparel and related products under our brand names. Our products are also available to customers online through Company-owned websites and through the use of third parties that provide logistics and fulfillment services. In addition to operating in the specialty, outlet, online, and franchise channels, we also use our omni-channel capabilities to bridge the digital world and physical stores to further enhance our shopping experience for our customers. Our omni-channel services, including order-in-store, reserve-in-store, find-in-store, and ship-from-store, as well as enhanced mobile experiences, are tailored uniquely across our portfolio of brands. Most of the products sold under our brand names are designed by us and manufactured by independent sources. We also sell products that are designed and manufactured by branded third parties, primarily at our Intermix brand.

We identify our operating segments according to how our business activities are managed and evaluated. As of January 30, 2016 , our operating segments included Gap Global, Old Navy Global, Banana Republic Global, Athleta, and Intermix. We have determined that each of our operating segments share similar economic and other qualitative characteristics, and therefore the results of our operating segments are aggregated into one reportable segment.

As previously announced in January 2015, we closed the Piperlime brand during the first half of fiscal 2015, including its online platform and the store in New York.

Financial results for fiscal 2015 are as follows:

• | Net sales for fiscal 2015 decreased 4 percent to $15.8 billion compared with $16.4 billion for fiscal 2014 . Excluding the impact of foreign exchange, our net sales decreased 2 percent for fiscal 2015 compared with fiscal 2014 . See Net Sales discussion for impact of foreign exchange. |

• | Comparable ("Comp") sales for fiscal 2015 decreased 4 percent compared with flat for last year. |

• | Gross profit for fiscal 2015 was $5.7 billion compared with $6.3 billion for fiscal 2014 . Gross margin for fiscal 2015 was 36.2 percent compared with 38.3 percent for fiscal 2014 . |

• | Operating margin for fiscal 2015 was 9.6 percent compared with 12.7 percent for fiscal 2014 . Operating margin is defined as operating income as a percentage of net sales. |

• | Net income for fiscal 2015 was $920 million compared with $1.3 billion for fiscal 2014 . Diluted earnings per share was $2.23 for fiscal 2015 compared with $2.87 for fiscal 2014 . |

• | During fiscal 2015 , we distributed $1.4 billion to shareholders through share repurchases and dividends. |

In June 2015, we announced a series of strategic actions to position Gap brand for improved business performance in the future, including right-sizing the Gap brand store fleet, streamlining the brand's headquarter workforce, and developing a clear, on-brand product aesthetic framework that will help strengthen the Gap brand to compete more successfully on the global stage. During fiscal 2015, the Company completed the closure of about 150 global specialty stores related to the strategic actions. The Company also incurred certain charges during fiscal 2015 in connection with the strategic actions, primarily consisting of impairment of store assets, lease termination fees and lease losses, employee related expenses, and impairment of inventory that did not meet brand standards.

18

The charges incurred related to the Company's strategic actions primarily related to Gap brand are as follows:

($ in millions) |

| Cost of Goods Sold and Occupancy Expenses |

| Operating Expenses |

| Total Charges | ||||||

Fiscal 2015 |

|

|

| |||||||||

Store closures and workforce reduction: |

|

|

|

|

|

| ||||||

Lease termination fees and lease losses |

| $ | - | |

| $ | 33 | |

| $ | 33 | |

Employee related expenses |

| 7 | |

| 17 | |

| 24 | | |||

Store asset impairment |

| 5 | |

| 5 | |

| 10 | | |||

Other |

| 2 | |

| 5 | |

| 7 | | |||

Total |

| 14 | |

| 60 | |

| 74 | | |||

|

|

|

|

|

|

| ||||||

Other charges: |

|

|

|

|

|

| ||||||

Store asset impairment related to underperforming stores |

| - | |

| 33 | |

| 33 | | |||

Inventory impairment |

| 20 | |

| - | |

| 20 | | |||

Other intangible asset impairment |

| - | |

| 5 | |

| 5 | | |||

Total |

| 20 | |

| 38 | |

| 58 | | |||

Total charges related to strategic actions |

| $ | 34 | |

| $ | 98 | |

| $ | 132 | |

Our business priorities in 2016 include:

• | offering product that is consistently brand-appropriate and on-trend with high customer acceptance; |

• | continuing to evolve our customer experience, with particular focus on the mobile and digital expressions of our brands; and |

• | attracting and retaining great talent in our businesses and functions. |

For fiscal 2016 , our top objective is to improve sales performance through a more consistent, on-trend, product offering. To enable this, we have several product initiatives underway, and in addition, we plan to continue focus on our responsive supply chain and inventory management. Further, we expect to continue our investment in our mobile digital capabilities and to enhance our shopping experience for our customers. We also plan to continue growth through new stores with a focus on Asia, outlet, and Athleta.