UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended October 31, 2015

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-00566

(Exact name of Registrant as specified in its charter)

| State of Delaware | 31-4388903 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 425 Winter Road, Delaware, Ohio | 43015 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant's telephone number, including area code 740-549-6000

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

| Class A Common Stock | New York Stock Exchange | |

| Class B Common Stock | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the Registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant's knowledge, in the definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange). Yes ¨ No x

The aggregate market value of voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of the last business day of the Registrant's most recently completed second fiscal quarter was as follows:

Non-voting common equity (Class A Common Stock) – $998,275,979

Voting common equity (Class B Common Stock) – $262,993,353

The number of shares outstanding of each of the Registrant's classes of common stock, as of December 16, 2015, was as follows:

Class A Common Stock – 25,693,564

Class B Common Stock – 22,119,966

Listed hereunder are the documents, portions of which are incorporated by reference, and the parts of this Form 10-K into which such portions are incorporated:

1. The Registrant's Definitive Proxy Statement for use in connection with the Annual Meeting of Stockholders to be held on March 1, 2016 (the "2016 Proxy Statement"), portions of which are incorporated by reference into Parts II and III of this Form 10-K. The 2016 Proxy Statement will be filed within 120 days of October 31, 2015.

IMPORTANT INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

All statements, other than statements of historical facts, included in this Annual Report on Form 10-K of Greif, Inc. and subsidiaries (this "Form 10-K") or incorporated herein, including, without limitation, statements regarding our future financial position, business strategy, budgets, projected costs, goals and plans and objectives of management for future operations and initiatives, are forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). Forward-looking statements generally can be identified by the use of forward-looking terminology such as "may," "will," "expect," "intend," "estimate," "anticipate," "project," "believe," "continue," "on track" or "target" or the negative thereof or variations thereon or similar terminology. All forward-looking statements made in this Form 10-K are based on information currently available to our management. Forward-looking statements speak only as of the date the statements were made. Although we believe that the expectations reflected in forward-looking statements have a reasonable basis, we can give no assurance that these expectations will prove to be correct. Forward-looking statements are subject to risks and uncertainties that could cause actual events or results to differ materially from those expressed in or implied by the statements. For a discussion of the most significant risks and uncertainties that could cause our actual results to differ materially from those projected, see "Risk Factors" in Item 1A of this Form 10-K. The risks described in this Form 10-K are not all inclusive, and given these and other possible risks and uncertainties, investors should not place undue reliance on forward-looking statements as a prediction of actual results. All forward-looking statements made in this Form 10-K are expressly qualified in their entirety by reference to such risk factors. Except to the limited extent required by applicable law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

1

Index to Form 10-K Annual Report for the Year ended October 31, 2015

Form 10-K Item | Description | Page | ||||||

Part I | 1. | Business | 3 | |||||

(a) General Development of Business | 3 | |||||||

(b) Financial Information about Segments | 3 | |||||||

(c) Narrative Description of Business | 3 | |||||||

(d) Financial Information about Geographic Areas | 5 | |||||||

(e) Available Information | 5 | |||||||

(f) Other Matters | 5 | |||||||

| 1A. | Risk Factors | 5 | ||||||

| 1B. | Unresolved Staff Comments | 12 | ||||||

| 2. | Properties | 13 | ||||||

| 3. | Legal Proceedings | 16 | ||||||

| 4. | Mine Safety Disclosures | 16 | ||||||

Part II | 5. | Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 17 | |||||

| 6. | Selected Financial Data | 19 | ||||||

| 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 20 | ||||||

| 7A. | Quantitative and Qualitative Disclosures about Market Risk | 41 | ||||||

| 8. | Financial Statements and Supplementary Data | 44 | ||||||

Consolidated Statements of Income and Consolidated Statements of Comprehensive Income | 44 | |||||||

Consolidated Balance Sheets | 45 | |||||||

Consolidated Statements of Cash Flows | 47 | |||||||

Consolidated Statements of Changes in Shareholders' Equity | 48 | |||||||

Note 1 – Basis of Presentation and Summary of Significant Accounting Policies | 49 | |||||||

Note 2 – Acquisitions and Divestitures | 57 | |||||||

Note 3 – Sale of Non-United States Accounts Receivable | 58 | |||||||

Note 4 – Inventories | 59 | |||||||

Note 5 – Assets and Liabilities Held for Sale and Disposals of Property, Plant, and Equipment, Net | 59 | |||||||

Note 6 – Goodwill and Other Intangible Assets | 60 | |||||||

Note 7 – Restructuring Charges | 61 | |||||||

Note 8 – Consolidation of Variable Interest Entities | 62 | |||||||

Note 9 – Long-Term Debt | 64 | |||||||

Note 10 – Financial Instruments and Fair Value Measurements | 66 | |||||||

Note 11 – Stock-Based Compensation | 68 | |||||||

Note 12 – Income Taxes | 69 | |||||||

Note 13 – Post Retirement Benefit Plans | 72 | |||||||

Note 14 – Contingent Liabilities and Environmental Reserves | 79 | |||||||

Note 15 – Earnings Per Share | 80 | |||||||

Note 16 – Equity Earnings of Unconsolidated Affiliates, Net of Tax and Net Income Attributable to Noncontrolling Interests | 82 | |||||||

Note 17 – Leases | 82 | |||||||

Note 18 – Business Segment Information | 82 | |||||||

Note 19 – Comprehensive Income | 85 | |||||||

Note 20 – Quarterly Financial Data (Unaudited) | 85 | |||||||

Reports of Independent Registered Public Accounting Firms | 87 | |||||||

| 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosures | 89 | ||||||

| 9A. | Controls and Procedures | 89 | ||||||

Report of Independent Registered Public Accounting Firm | 91 | |||||||

| 9B. | Other Information | 92 | ||||||

Part III | 10. | Directors, Executive Officers and Corporate Governance | 92 | |||||

| 11. | Executive Compensation | 92 | ||||||

| 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 92 | ||||||

| 13. | Certain Relationships and Related Transactions, and Director Independence | 92 | ||||||

| 14. | Principal Accountant Fees and Services | 92 | ||||||

Part IV | 15. | Exhibits and Financial Statement Schedules | 93 | |||||

Signatures | 101 | |||||||

Schedules | Schedule II | 102 | ||||||

Exhibits | Exhibits and Certifications | |||||||

2

PART I

ITEM 1. BUSINESS

(a) General Development of Business

We are a leading global producer of industrial packaging products and services with manufacturing facilities located in over 50 countries. We offer a comprehensive line of rigid industrial packaging products, such as steel, fibre and plastic drums, rigid intermediate bulk containers, closure systems for industrial packaging products, transit protection products, water bottles and remanufactured and reconditioned industrial containers, and services, such as container life cycle management, blending, filling, logistics, warehousing and other packaging services. We also produce containerboard and corrugated products for niche markets in North America. We are also a leading global producer of flexible intermediate bulk containers. We sell timber to third parties from our timberland in the southeastern United States that we manage to maximize long-term value. In addition, we sell, from time to time, timberland and special use land, which consists of surplus land, higher and better use ("HBU") land, and development land. Our customers range from Fortune 500 companies to medium and small-sized companies in a cross section of industries.

We were founded in 1877 in Cleveland, Ohio, as "Vanderwyst and Greif," a cooperage shop co-founded by one of four Greif brothers. One year after our founding, the other three Greif brothers were invited to join the business, renamed Greif Bros. Company, making wooden barrels, casks and kegs to transport post-Civil War goods nationally and internationally. We later purchased nearly 300,000 acres of timberland to provide raw materials for our cooperage plants. We still own significant timber properties located in the southeastern United States. In 1926, we incorporated as a Delaware corporation and made a public offering as The Greif Bros. Cooperage Corporation. In 1951, we moved our headquarters from Cleveland, Ohio to Delaware, Ohio, which is in the Columbus metro-area, where our corporate headquarters are currently located. Since the latter half of the 1900s, we have transitioned from our keg and barrel heading mills, stave mills and cooperage facilities to a global producer of industrial packaging products. Following our acquisition of Van Leer Packaging in 2001, a global steel and plastic drum manufacturer, we changed our name to Greif, Inc.

Our fiscal year begins on November 1 and ends on October 31 of the following year. Any references in this Form 10-K to the years 2015, 2014 or 2013, or to any quarter of those years, relate to the fiscal year ended in that year.

As used in this Form 10-K, the terms "Greif," "the Company," "we," "us," and "our" refer to Greif, Inc. and its subsidiaries.

(b) Financial Information about Segments

We operate in five business segments, which are aggregated into four reportable business segments: Rigid Industrial Packaging & Services; Paper Packaging; Flexible Products & Services; and Land Management. Information related to each of these segments is included in Note 18 to the Notes to Consolidated Financial Statements included in Item 8 of this Form 10-K.

(c) Narrative Description of Business

Products and Services

In the Rigid Industrial Packaging & Services segment, we are a leading global producer of rigid industrial packaging products, including steel, fibre and plastic drums, rigid intermediate bulk containers, closure systems for industrial packaging products, transit protection products, water bottles and remanufactured and reconditioned industrial containers, and services, such as container life cycle management, blending, filling, logistics, warehousing and other packaging services. We sell our rigid industrial packaging products to customers in industries such as chemicals, paints and pigments, food and beverage, petroleum, industrial coatings, agricultural, pharmaceutical and mineral products, among others.

In the Paper Packaging segment, we sell containerboard, corrugated sheets, corrugated containers and other corrugated products to customers in North America in industries such as packaging, automotive, food and building products. Our corrugated container products are used to ship such diverse products as home appliances, small machinery, grocery products, automotive components, books and furniture, as well as numerous other applications.

In the Flexible Products & Services segment, we are a leading global producer of flexible intermediate bulk containers and related services. Our flexible intermediate bulk containers consist of a polypropylene-based woven fabric that is produced at our production sites, as well as sourced from strategic regional suppliers. Our flexible products are sold globally and service customers and market segments similar to those of our Rigid Industrial Packaging & Services segment. Additionally, our flexible products significantly expand our presence in the agricultural and food industries, among others.

3

In the Land Management segment, we are focused on the active harvesting and regeneration of our United States timber properties to achieve sustainable long-term yields. While timber sales are subject to fluctuations, we seek to maintain a consistent cutting schedule, within the limits of market and weather conditions. We also sell, from time to time, timberland and special use land, which consists of surplus land, HBU land and development land. As of October 31, 2015, we owned approximately 242,673 acres of timber property in the southeastern United States. During the fourth quarter 2015, we sold approximately 5,200 acres of development properties in Canada, which represented all of our remaining timber properties in Canada.

Customers

Due to the variety of our products, we have many customers buying different types of our products and due to the scope of our sales, no one customer is considered principal in our total operations.

Backlog

We supply a cross-section of industries, such as chemicals, paints and pigments, food and beverage, petroleum, industrial coatings, agricultural, pharmaceutical, mineral, packaging, automotive and building products, and must make spot deliveries on a day-to-day basis as our products are required by our customers. We do not operate on a backlog to any significant extent and maintain only limited levels of finished goods. Many customers place their orders weekly for delivery during the week.

Competition

The markets in which we sell our products are highly competitive with many participants. Although no single company dominates, we face significant competitors in each of our businesses. Our competitors include large vertically integrated companies as well as numerous smaller companies. The industries in which we compete are particularly sensitive to price fluctuations caused by shifts in industry capacity and other cyclical industry conditions. Other competitive factors include design, quality and service, with varying emphasis depending on product line.

In both the rigid industrial packaging industry and the flexible products industry, we compete by offering a comprehensive line of products on a global basis. In the paper packaging industry, we compete by concentrating on providing value-added, higher-margin corrugated products to niche markets. In addition, over the past several years we have closed higher cost facilities and otherwise restructured our operations, which we believe have significantly improved our cost competitiveness.

Compliance with Governmental Regulations Concerning Environmental Matters

Our operations are subject to extensive federal, state, local and international laws, regulations, rules and ordinances relating to pollution, the protection of the environment, the generation, storage, handling, transportation, treatment, disposal and remediation of hazardous substances and waste materials and numerous other environmental laws and regulations. In the ordinary course of business, we are subject to periodic environmental inspections and monitoring by governmental enforcement authorities. In addition, certain of our production facilities require environmental permits that are subject to revocation, modification and renewal.

Based on current information, we believe that the probable costs of the remediation of company-owned property will not have a material adverse effect on our financial condition or results of operations. We believe that we have adequately reserved for our liability for these matters as of October 31, 2015.

We do not believe that compliance with federal, state, local and international provisions, which have been enacted or adopted regulating the discharge of materials into the environment, or otherwise relating to the protection of the environment, has had or will have a material adverse effect upon our capital expenditures, earnings or competitive position. We do not anticipate any material capital expenditures related to environmental control in 2016.

Refer also to Note 14 to the Notes to Consolidated Financial Statements included in Item 8 of this Form 10-K for additional information concerning environmental expenses and cash expenditures for 2015, 2014 and 2013, and our reserves for environmental liabilities as of October 31, 2015.

Raw Materials

Steel, resin and containerboard, as well as used industrial packaging for reconditioning, are the principal raw materials for the Rigid Industrial Packaging & Services segment, resin is the primary raw material for the Flexible Products & Services segment, and pulpwood, old corrugated containers for recycling and containerboard are the principal raw materials for the Paper Packaging segment. We satisfy most of our needs for these raw materials through purchases on the open market or under short-term and long-term supply agreements. All of these raw materials are purchased in highly competitive, price-sensitive markets, which have historically exhibited price, demand and supply cyclicality. From time to time, some of these raw materials have been in short supply at certain of our manufacturing facilities. In those situations, we ship the raw materials in short supply from one or more of our other facilities with sufficient supply to the facility or facilities experiencing the shortage. To date, raw material shortages have not had a material adverse effect on our financial condition or results of operations.

4

Research and Development

While research and development projects are important to our continued growth, the amount expended in any year is not material in relation to our results of operations.

Other

Our businesses are not materially dependent upon patents, trademarks, licenses or franchises.

No material portion of our businesses is subject to renegotiation of profits or termination of contracts or subcontracts at the election of a governmental agency or authority.

The businesses of our segments are not seasonal to any material extent.

Employees

As of October 31, 2015, we had approximately 13,150 full time employees. A significant number of our full time employees are covered under collective bargaining agreements. We believe that our employee relations are generally good.

(d) Financial Information about Geographic Areas

Our operations are located in North and South America, Europe, the Middle East, Africa and the Asia Pacific regions. Information related to our geographic areas of operation is included in Note 18 to the Notes to Consolidated Financial Statements included in Item 8 of this Form 10-K. Refer to Quantitative and Qualitative Disclosures about Market Risk, included in Item 7A of this Form 10-K.

(e) Available Information

We maintain a website at www.greif.com. We file reports with the United States Securities and Exchange Commission ("SEC") and make available, free of charge, on or through our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy and information statements and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we have electronically filed such material with, or furnished it to, the SEC.

Any of the materials we file with the SEC may also be read and/or copied at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. Information on the operation of the SEC's Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov.

(f) Other Matters

Our common equity securities are listed on the New York Stock Exchange ("NYSE") under the symbols GEF and GEF.B. Our President and Chief Executive Officer has timely certified to the NYSE that, at the date of the certification, he was unaware of any violation by our Company of the NYSE's corporate governance listing standards. In addition, our Chief Executive Officer and Chief Financial Officer have provided certain certifications in this Form 10-K regarding the quality of our public disclosures. Refer to Exhibits 31.1 and 31.2 to this Form 10-K.

ITEM 1A. RISK FACTORS

Statements contained in this Form 10-K may be "forward-looking" within the meaning of Section 21E of the Exchange Act. Such forward-looking statements are subject to certain risks and uncertainties that could cause our operating results to differ materially from those projected. The following factors, among others, in some cases have affected, and in the future could affect, our actual financial or operational performance, or both.

Historically, Our Business has been Sensitive to Changes in General Economic or Business Conditions.

Our customers generally consist of other manufacturers and suppliers who purchase industrial packaging products and containerboard and related corrugated products for their own containment and shipping purposes. Because we supply a cross section of industries, such as chemicals, paints and pigments, food and beverage, petroleum, industrial coatings, agricultural, pharmaceutical, mineral products, packaging, automotive, and building products industries, and have operations in many countries, demand for our products and services has historically corresponded to changes in general economic and business conditions of the industries and countries in which we operate. Accordingly, our financial performance is substantially dependent upon the general economic and business conditions existing in these industries and countries, and any prolonged or substantial economic downturn in the markets in which we operate could have a material adverse effect on our business, results of operations and financial condition.

5

Our Operations Subject Us to Currency Exchange and Political Risks that Could Adversely Affect Our Results of Operations.

We have operations in over 50 countries. Management of global operations is extremely complex, and operations outside the United States are subject to additional risks that may not exist, or be as significant, in the United States. As a result of our global operations, we are subject to certain risks that could disrupt our operations or force us to incur unanticipated costs.

The company also has indebtedness, agreements to purchase raw materials and agreements to sell finished products that are denominated in Euros, Turkish Lira, Russian Rubles and other currencies. Our operating performance is affected by fluctuations in currency exchange rates by:

| • | translations into United States dollars for financial reporting purposes of the assets and liabilities of our non-U.S. operations conducted in local currencies; and |

| • | gains or losses from transactions conducted in currencies other than the operation's functional currency. |

We are subject to various other risks associated with operating in countries outside the U.S., such as the following:

| • | political, social, economic and labor instability which has commonly been associated with developing countries but presently is also impacting several industrialized countries; |

| • | war, invasion, civil disturbance or acts of terrorism; |

| • | taking of property by nationalization or expropriation without fair compensation; |

| • | changes in government policies and regulations; |

| • | loss or non-renewal of treaties or similar agreements with foreign tax authorities; |

| • | difficulties in enforcement of contractual obligations; |

| • | imposition of limitations on conversions of currencies into United States dollars or remittance of dividends and other payments by international subsidiaries; |

| • | imposition or increase of withholding and other taxes on income remittances and other payments by international subsidiaries; |

| • | hyperinflation, currency devaluation or defaults in certain countries; |

| • | impositions or increase of investment and other restrictions or requirements by non-United States governments |

| • | national and regional labor strikes, whether legal or illegal and other labor or social actions; and |

| • | restrictive governmental trade policies, customs, import/export and other trade compliance regulations. |

The Current and Future Challenging Global Economy and Disruption and Volatility of the Financial and Credit Markets may Adversely Affect Our Business.

The current global economic conditions are challenging to our global business operations. Such conditions have had, and may continue to have, a negative impact on our financial results. Future economic downturns, either in the United States, Europe or in other regions in which we do business could negatively affect our business and results of operations. The volatility of the current economic climate, especially in relation to ongoing uncertainties related to geopolitical events around the world, makes it difficult for us to predict the complete impact of the forgoing matters on our business and results of operations. Due to these current and future economic conditions, our customers may face financial difficulties, the unavailability of or reduction in commercial credit, or both, that may result in decreased sales by and revenues to our company. Certain of our customers may cease operations or seek bankruptcy protection, which would reduce our cash flows and adversely impact our results of operations. Our customers that are financially viable and not experiencing economic distress may nevertheless elect to reduce the volume of orders for our products or close facilities in an effort to remain financially stable or as a result of the unavailability of commercial credit which would negatively affect our results of operations. We may experience difficulties in servicing, renewing or repaying our outstanding debt due to continued volatility in the global economy. We may also have difficulty accessing the global credit markets due to the downgrade of the U.S. credit rating and the resulting tightening of commercial credit availability and the financial difficulties of our customers, which would result in decreased ability to fund capital-intensive strategic projects.

Further, we may experience challenges in forecasting revenues and operating results due to these global economic conditions. The difficulty in forecasting revenues and operating results may result in volatility in the market price of our common stock.

In addition, the lenders under our senior secured credit agreement and other borrowing facilities described in Item 7 of this Form 10-K under "Liquidity and Capital Resources – Borrowing Arrangements" and the counterparties with whom we maintain interest rate swap agreements, currency forward contracts and derivatives and other hedge agreements may be unable to perform their lending or payment obligations in whole or in part, or may cease operations or seek bankruptcy protection, which would negatively affect our cash flows and our results of operations.

A downgrade in our credit rating could also impact our ability to effectively finance our operations and could lead to increased borrowing costs and limits on our access to capital.

6

The Continuing Consolidation of Our Customer Base and Suppliers may Intensify Pricing Pressure.

Over the last few years, many of our large industrial packaging, containerboard and corrugated products customers have acquired, or been acquired by, companies with similar or complementary product lines. In addition, many of our suppliers of raw materials such as steel, resin and paper, have undergone a similar process of consolidation. This consolidation has increased the concentration of our largest customers, resulting in increased pricing pressures from our customers. The consolidation of our largest suppliers has resulted in limited sources of supply and increased cost pressures from our suppliers. Any future consolidation of our customer base or our suppliers could negatively impact our business, results of operations and financial condition. Furthermore, if one or more of our major customers reduces, delays or cancels substantial orders, if one or more of our major suppliers is unable to timely produce and deliver our orders our business, results of operations, financial condition and cash flows may be materially and adversely affected, particularly for the period in which the reduction, delay or cancellation occurs and also possibly for subsequent periods.

We Operate in Highly Competitive Industries.

Each of our business segments operates in highly competitive industries. The most important competitive factors we face are price, quality and service. To the extent that one or more of our competitors become more successful with respect to any of these key competitive factors, we could lose customers and our sales could decline. In addition, due to the tendency of certain customers to diversify their suppliers, we could be unable to increase or maintain sales volumes with particular customers. Certain of our competitors are substantially larger and have significantly greater financial resources.

Our Business is Sensitive to Changes in Industry Demands.

Industry demand for containerboard in the United States and certain of our industrial packaging products in our United States, European and other international markets has varied in recent years causing competitive pricing pressures for those products. We compete in industries that are capital intensive, which generally leads to continued production as long as prices are sufficient to cover marginal costs. As a result, changes in industry demands, including any resulting industry over-capacity, may cause substantial price competition and, in turn, negatively impact our business, results of operations and financial condition.

Raw Material and Energy Price Fluctuations and Shortages may Adversely Impact Our Manufacturing Operations and Costs.

The principal raw materials used in the manufacture of our products are steel, resin, pulpwood, old corrugated containers for recycling, used industrial packaging for reconditioning, and containerboard, which we purchase or otherwise acquire in highly competitive, price sensitive markets. These raw materials have historically exhibited price and demand cyclicality. Some of these materials have been, and in the future may be, in short supply. For example, the availability of these raw materials and/or our ability to purchase and transport these raw materials may be unexpectedly disrupted by adverse weather conditions, natural disasters or a substantial economic downturn in the industries that provide any of those products. However, we have not recently experienced any significant difficulty in obtaining our principal raw materials. We have long-term supply contracts in place for obtaining a portion of our principal raw materials. The cost of producing our products is also sensitive to the price of energy (including its impact on transport costs). We have, from time to time, entered into short-term contracts to hedge certain of our energy costs. Energy prices, in particular oil and natural gas, have fluctuated in recent years, with a corresponding effect on our production costs. Potential legislation, regulatory action and international treaties related to climate change, especially those related to the regulation of greenhouse gases, may result in significant increases in raw material and energy costs. There can be no assurance that we will be able to recoup any past or future increases in the cost of energy and raw materials.

We may Encounter Difficulties Arising from Acquisitions.

We have in recent years invested a substantial amount of capital in acquisitions, joint ventures and strategic investments and we expect that we will continue to do so in the foreseeable future. We are continually evaluating acquisitions and strategic investments that are significant to our business both in the United States and internationally. Acquisitions, joint ventures and strategic investments involve numerous risks, including the failure to identify suitable acquisition candidates, complete acquisitions on acceptable terms and conditions, retain key customers, employees and contracts, the inability to integrate businesses without material disruption, unanticipated costs incurred in connection with integrating businesses, the incurrence of liabilities greater than anticipated or operating results that are less than anticipated, the inability to realize the projected value, and the inability to realize projected synergies. In addition, acquisitions, joint ventures and strategic investments and associated integration activities require time and attention of management and other key personnel, and other companies in our industries have similar acquisition and investment strategies. There can be no assurance that any acquisitions, joint ventures and strategic investments will be successfully integrated into our operations, that competition for acquisitions will not intensify or that we will be able to complete such acquisitions, joint ventures and strategic investments on acceptable terms and conditions. The costs of unsuccessful acquisition, joint venture and strategic investment efforts may adversely affect our results of operations, financial condition or prospects.

We may Incur Additional Restructuring Costs and there is no Guarantee that Our Efforts to Reduce Costs will be Successful.

We have restructured portions of our operations from time to time in recent years, particularly following acquisitions of businesses and periods of economic downturn due to recent and current global economic conditions. We are implementing a strategy to improve our business portfolio, address underperforming assets and generate additional cash. This strategy includes SG&A reductions throughout the company and has and will likely continue to result in the rationalization of manufacturing facilities.

7

The rationalization of our manufacturing facilities may result in temporary constraints upon our ability to produce the quantity of products necessary to fill orders and thereby complete sales in a timely manner. In addition, system upgrades at our manufacturing facilities that impact ordering, production scheduling and other related manufacturing processes are complex, and could impact or delay production targets. A prolonged delay in our ability to fill orders on a timely basis could affect customer demand for our products and increase the size of our product inventories, causing future reductions in our manufacturing schedules and adversely affecting our results of operations. Moreover, our continuous development and production of new products will often involve the retooling of existing manufacturing facilities. This retooling may limit our production capacity at certain times in the future, which could adversely affect our results of operations and financial condition. In addition, the expansion and reconfiguration of existing manufacturing facilities could increase the risk of production delays, as well as require significant investments of capital.

While we expect these initiatives to result in significant profit opportunities and savings throughout our organization, our estimated profits and savings are based on several assumptions that may prove to be inaccurate, and as a result, there can be no assurance that we will realize these profits and cost savings or that, if realized, these profits and cost savings will be sustained. Failure to achieve or delays in achieving projected levels of efficiencies and cost savings from such measures, or unanticipated inefficiencies resulting from manufacturing and administrative reorganization actions in progress or contemplated, could adversely affect the Company's results of operation and, financial condition and harm our reputation.

Tax Legislation Initiatives or Challenges to Our Tax Positions May Adversely Impact Our Results or Condition.

We are a large multinational corporation with operations in the United States and international jurisdictions. As such, we are subject to the tax laws and regulations of the U.S. federal, state and local governments and of many international jurisdictions. Due to widely varying tax rates in the taxing jurisdictions applicable to our business, a change in income generation to higher taxing jurisdictions or away from lower taxing jurisdictions may have an adverse effect on our financial condition and results of operations.

From time to time, various legislative initiatives may be proposed that could adversely affect our tax positions. There can be no assurance that our effective tax rate or tax payments will not be adversely affected by these initiatives. In addition, U.S. federal, state and local, as well as international, tax laws and regulations, are extremely complex and subject to varying interpretations. There can be no assurance that our tax positions will not be challenged by relevant tax authorities or that we would be successful in any such challenge.

Full realization of our deferred tax assets may be affected by a number of factors.

We have deferred tax assets, including U.S. and foreign operating loss carryforwards, capital loss carryforwards, employee and retiree benefit items, and other accruals not yet deductible for tax purposes. We have established valuation allowances to reduce those deferred tax assets to an amount that is more likely than not to be realized. Our ability to use these deferred tax assets depends in part upon our having future taxable income during the periods in which these temporary differences reverse or our ability to carry back any losses created by the deduction of these temporary differences. We expect to realize these assets over an extended period. However, if we were unable to generate sufficient future taxable income in the U.S. and certain foreign jurisdictions, or if there were a significant change in the time period within which the underlying temporary differences became taxable or deductible, we could be required to increase our valuation allowances against our deferred tax assets, which would increase our effective tax rate which could have a material adverse effect on our reported results of operations.

Several Operations are Conducted by Joint Ventures that we cannot Operate Solely for Our Benefit.

Several operations, particularly in developing countries, are conducted through joint ventures, such as a significant joint venture in our Flexible Products & Services segment. In countries that require us to conduct business through a joint venture with a local joint venture partner, the loss of a joint venture partner or a joint venture partner's loss of its ability to conduct business in such country may impact our ability to conduct business in that country.

In joint ventures, we share ownership and, in some instances, management of a company with one or more parties who may or may not have the same goals, strategies, priorities or resources as we do. In general, joint ventures are intended to be operated for the benefit of all co-owners, rather than for our exclusive benefit. Operating a business as a joint venture often requires additional organizational formalities as well as time-consuming procedures for sharing information, accounting and making decisions. In certain cases, our joint venture partners must agree in order for the applicable joint venture to take certain actions, including acquisitions, the sale of assets, budget approvals, borrowing money and granting liens on joint venture property. Our inability to take unilateral action that we believe is in our best interests may have an adverse effect on the financial performance of the joint venture and the return on our investment. In joint ventures, we believe our relationship with our co-owners is an important factor to the success of the joint venture, and if a co-owner changes, our relationship may be adversely affected. In addition, the benefits from a successful joint venture are shared among the co-owners, so that we do not receive all the benefits from our successful joint ventures. Finally, we may be required on a legal or practical basis or both, to accept liability for obligations of a joint venture beyond our economic interest, including in cases where our co-owner becomes bankrupt or is otherwise unable to meet its commitments. For additional information with respect to the joint venture relating to our Flexible Products & Services segment, refer to Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operation – Variable Interest Entities.

8

Our Ability to Attract, Develop and Retain Talented and Qualified Employees, Managers and Executives is Critical to Our Success.

Our ability to attract, develop and retain talented and qualified employees, including executives and other key managers, is important to our business. This is becoming more difficult in the current highly competitive hiring and retention environment. The retirement of or unforeseen loss of key officers and employees without appropriate succession planning or the ability to develop or hire replacements could hinder our strategic planning and execution and make it difficult to manage our business and meet our objectives resulting in a material adverse effect on our business, results of operations and financial condition.

Our Business may be Adversely Impacted by Work Stoppages and Other Labor Relations Matters.

We are subject to risk of work stoppages and other labor relations matters because a significant number of our employees are represented by unions. We have experienced work stoppages and strikes in the past, and there may be work stoppages and strikes in the future. Any prolonged work stoppage or strike at any one of our principal manufacturing facilities could have a negative impact on our business, results of operations and financial condition. In addition, upon the expiration of existing collective bargaining agreements, we may not reach new agreements without union action and any such new agreements may not be on terms satisfactory to us.

Our Pension Plans Are Underfunded and will Require Future Cash Contributions, And Our Required Future Cash Contributions Could Be Higher Than We Expect, Each Of Which Could Have A Material Adverse Effect On Our Financial Condition And Liquidity.

We sponsor various pension and similar benefit plans worldwide.

Our U.S. and non-U.S. pension plans were underfunded by an aggregate of $133.8 million and $22.2 million, respectively, as of October 31, 2015. We are legally required to make cash contributions to our pension plans in the future, and those cash contributions could be material.

In fiscal 2016, we expect to make cash contributions of approximately $13.4 million and $3.8 million to our U.S. and non-U.S. pension plans, respectively, which we believe will be sufficient to meet the minimum funding requirements under applicable laws. However, our future funding obligations for our pension plans depend upon the levels of benefits provided for by these plans, the future performance of assets set aside for these plans, the rates of interest used to determine funding levels, the impact of potential business dispositions, actuarial data and experience, and any changes in government laws and regulations. Accordingly, our 2016 funding requirements for our pension plans could be higher than expected, which could have a material adverse effect on our financial condition and liquidity.

In addition, our pension plans hold a significant amount of equity securities. If the market values of these securities decline, our pension expense and funding requirements will increase, which could have a material adverse effect on our financial condition and liquidity.

Any decrease in interest rates and asset returns, if and to the extent not offset by contributions, could increase our obligations under our pension plans. If the performance of assets held in these pension plans does not meet our expectations, our cash contributions for these plans could be higher than we expect, which could have a material adverse effect on our financial condition and liquidity.

We may be Subject to Losses that Might not be Covered in Whole or in Part by Existing Insurance Reserves or Insurance Coverage.

We are self-insured for certain of the claims made under our employee medical and dental insurance programs and for certain of our workers' compensation claims. We establish reserves for estimated costs related to pending claims, administrative fees and claims incurred but not reported. Because establishing reserves is an inherently uncertain process involving estimates, currently established reserves may not be adequate to cover the actual liability for claims made under our employee medical and dental insurance programs and for certain of our workers' compensation claims. If we conclude that our estimates are incorrect and our reserves are inadequate for these claims, we will need to increase our reserves, which could adversely affect our financial condition and results of operations.

We carry comprehensive liability, fire and extended coverage insurance on most of our facilities, with policy specifications and insured limits customarily carried for similar properties. However, there are certain types of losses, such as losses resulting from wars, acts of terrorism, wind storm, flood, earthquake or other natural disasters, that may be uninsurable or subject to restrictive policy conditions. In these instances, should a loss occur in excess of insured limits, we could lose capital invested in that property, as well as the anticipated future revenues derived from the manufacturing activities conducted at that property, while remaining obligated for any mortgage indebtedness or other financial obligations related to the property. Any such loss would adversely impact our business, financial condition and results of operations.

We purchase insurance policies covering general liability and product liability with substantial policy limits. However, there can be no assurance that any liability claim would be adequately covered by our applicable insurance policies or it would not be excluded from coverage based on the terms and conditions of the policy. This could also apply to any applicable contractual indemnity.

We also purchase environmental liability policies where legally required and may elect to purchase coverage in other circumstances in order to transfer all or a portion of environmental liability risk through insurance. However, there can be no assurance that any environmental liability claim would be adequately covered by our applicable insurance policies or that it would not be excluded from coverage based on the terms and conditions of the policy.

9

Our Business Depends on the Uninterrupted Operations of Our Facilities, Systems and B usiness Functions, including Our Information Technology (IT) and Other Business Systems.

Our business is dependent upon our ability to execute, in an efficient and uninterrupted fashion, necessary business functions, such as accessing key business data, financial information, order processing, invoicing and the operation of IT dependent manufacturing equipment. In addition, a significant portion of the communication between our employees, customers and suppliers around the world depends on our IT systems. A shut-down of or inability to access one or more of our facilities, a power outage, a pandemic, or a failure of one or more of our IT, telecommunications or other systems could significantly impair our ability to perform such functions on a timely basis.

Our IT systems exist on platforms in over 50 countries, many of which have been acquired in connection with business acquisitions, resulting in a complex technical infrastructure. Such complexity creates difficulties and inefficiencies in monitoring business results and consolidating financial data and could result in a material adverse effect on our business, results of operations and financial condition. In order to reduce this complexity, we are in the process of implementing a standard IT platform project to transition from many of the former systems to a single system. Given its scope, this project will take several years to complete and will require significant human and financial resources. There can be no assurance that this project will be successful, and even if successful, there can be no assurance that other difficulties and inefficiencies will not exist in our systems.

We have established a business continuity plan in an effort to ensure the continuation of core business operations in the event that normal operations could not be performed due to a catastrophic event. While we continue to test and assess our business continuity plan to ensure it meets the needs of our core business operations and addresses multiple business interruption events, there is no assurance that core business operations could be performed upon the occurrence of such an event.

A Security Breach of Customer, Employee, Supplier or Company Information may have a Material Adverse Effect on our Business, Financial Condition and Results of Operations.

In the conduct of our business, we collect, use, transmit, store and report data on information systems and interact with customers, vendors and employees. Increased global IT security threats and more sophisticated and targeted computer crime pose a risk to the security of our systems and networks and the confidentiality, availability and integrity of our data. Despite our security measures, our IT systems and infrastructure may be vulnerable to computer viruses, cyber-attacks, security breaches caused by employee error or malfeasance or other disruptions. Any such threat could compromise our networks and the information stored there could be accessed, publicly disclosed, lost or stolen. A security breach of our computer systems could interrupt or damage our operations or harm our reputation. In addition, we could be subject to legal claims or proceedings, liability under laws that protect the privacy of personal information and regulatory penalties if confidential information relating to customers, suppliers, employees or other parties is misappropriated from our computer system.

Similar security threats exist with respect to the IT systems of our lenders, suppliers, consultants, advisors and other third parties with whom we conduct business. A security breach of those computer systems could result in the loss, theft or disclosure of confidential information and could also interrupt or damage our operations, harm our reputation and subject us to legal claims.

Legislation/Regulation Related to Environmental and Health and Safety Matters and Corporate Social Responsibility Could Negatively Impact our Operations and Financial Performance.

We must comply with extensive laws, rules and regulations in the United States and in each of the countries where we conduct business regarding environmental matters, such as air, soil and water quality and waste disposal. We must also comply with extensive laws, rules and regulations regarding safety, health and corporate responsibility matters. There can be no assurance that compliance with existing and new laws, rules and regulations will not require significant expenditures.

For example, the Patient Protection and Affordable Care Act, which was adopted in 2010 and is being phased in over several years, could significantly increase the cost of the health care benefits provided to our U.S. employees. In addition, the failure to comply materially with such existing and new laws, rules and regulations could adversely affect our business, results of operations and financial condition.

We are also subject to transportation safety regulations promulgated by the U.S. Department of Transportation (DOT) and agencies in other jurisdictions. Both the DOT regulations and standards issued by the United Nations and adopted by various jurisdictions outside the United States set forth requirements related to the transportation of both hazardous and nonhazardous materials in some of our packaging products and subject our company to random inspections and testing to ensure compliance. Failure to comply could result in fines to our company and could affect our business, results of operations and financial condition.

We are subject to laws, rules and regulations relating to some of the raw materials, such as resins and epoxy-based coatings, used in our rigid container business. These materials may contain Bisphenol-A (BPA), a chemical monomer that can be toxic in sufficient quantities, and is used in several food contact applications. Regulatory agencies in several jurisdictions worldwide have found these materials to be safe for food contact at current levels, but a significant change in regulatory rulings concerning BPA could have an adverse effect on our business.

Our customers in the food industry are subject to increasing laws, rules and regulations relating to food safety. As a result, customers may demand that changes be made to our products or facilities, as well as other aspects of our production processes, that may require the investment of capital. The failure to comply with these requests could adversely affect our relationships with some customers and result in negative effects on our business, results of operations and financial condition.

10

In 2012, the SEC, as directed by Section 1502 of The Dodd-Frank Wall Street Reform and Consumer Protection Act, enacted new annual disclosure and reporting requirements for companies regarding the use of "conflict minerals" from the Democratic Republic of the Congo and adjoining countries. These requirements could affect the sourcing, availability and cost of minerals used in the manufacture of certain of our products. We have incurred and will continue to incur costs associated with complying with the supply chain due diligence procedures required by the SEC. In addition, because our supply chain is complex, we may face reputation challenges with our customers and other stakeholders if we are unable to sufficiently verify the origins of all minerals used in our products through the due diligence procedures that we implement.

Although there may be adverse financial impact (including compliance costs, potential permitting delays and increased cost of energy, raw materials and transportation) associated with any legislation, regulation or other action, the extent and magnitude of that impact cannot be reliably or accurately estimated due to the fact that some requirements have only recently been adopted and the present uncertainty regarding other additional measures and how they will be implemented.

Product Liability Claims and Other Legal Proceedings Could Adversely Affect our Operations and Financial Performance .

We produce products and provide services related to other parties' products. While we have built extensive operational processes to ensure that the design and manufacture of our products meet rigorous quality standards, there can be no assurance that we or our customers will not experience operational process failures that could result in potential product, safety, regulatory or environmental claims and associated litigation. We are also subject to a variety of legal proceedings and legal compliance risks in our areas of operation around the globe. Any such claims, whether with or without merit, could be time consuming and expensive to defend and could divert management's attention and resources. In accordance with customary practice, we maintain insurance against some, but not all, of these potential claims. In the future, we may not be able to maintain insurance at commercially acceptable premium levels at all. In addition, the levels of insurance we maintain may not be adequate to fully cover any and all losses or liabilities. If any significant judgment or claim is not fully insured or indemnified against, it could have a material adverse impact on our business, financial condition and results of operations.

We and the industries in which we operate are at times being reviewed or investigated by regulators and other governmental authorities, which could lead to enforcement actions, fines and penalties or the assertion of private litigation claims and damages. Simply responding to actual or threatened litigation or government investigations of our compliance with regulatory standards may require significant expenditures of time and other resources. While we believe that we have adopted appropriate risk management and compliance programs, the global and diverse nature of our operations means that legal and compliance risks will continue to exist and legal proceedings and other contingencies, the outcome of which cannot be predicted with certainty, will arise from time to time that could adversely affect our business, results of operations and financial condition.

We may Incur Fines or Penalties, Damage to Our Reputation or Other Adverse Consequences if Our Employees, Agents or Business Partners Violate, or are Alleged to Have Violated, Anti-bribery, Competition or Other Laws.

We cannot provide assurance that our internal controls will always protect us from reckless or criminal acts committed by our employees, agents or business partners that would violate U.S. and/or non-U.S. laws, including anti-bribery, competition, trade sanctions and regulation, and other laws. Any such improper actions could subject us to civil or criminal investigations in the U.S. and in other jurisdictions, could lead to substantial civil or criminal monetary and non-monetary penalties against us or our subsidiaries, and could damage our reputation. Even the allegation or appearance of our employees, agents or business partners acting improperly or illegally could damage our reputation and result in significant expenditures in investigating and responding to such actions.

Changing Climate, Climate Change Regulations and Greenhouse Gas Effects may Adversely Affect Our Operations and Financial Performance.

There is continuing concern from members of the scientific community and the general public that emissions of greenhouse gases (GHG) and other human activities have or will cause significant changes in weather patterns and increase the frequency or severity of weather events, wildfires and flooding. Climate change creates physical and financial risk. Physical risks from climate change include an increase in sea level and changes in weather conditions, such as an increase in precipitation, droughts and extreme weather events. These types of events may adversely impact the Company, our suppliers, our customers and their ability to purchase our products and our ability to manufacture and transport our products on a timely basis and could result in a material adverse effect on our business, results of operations and financial condition.

We believe it is likely that the scientific and political attention to issues concerning the extent and causes of climate change will continue, with the potential for further legislation and regulations that could affect our results of operations and financial condition. Foreign, federal, state and local regulatory and legislative bodies have proposed various legislative and regulatory measures relating to climate change, regulating GHG emissions and energy policies. If such legislation or regulations are enacted, we could incur increased energy, environmental and other costs and capital expenditures to comply with the limitations. Failure to comply with these regulations could result in fines to our company and could affect our business, results of operations and financial condition.

11

We, along with other companies in many business sectors, including our customers, are considering and implementing ways to reduce GHG emissions. As a result, our customers may request that changes be made to our products or facilities, as well as other aspects of our production processes, that increase costs and may require the investment of capital. The failure to comply with these requests could adversely affect our relationships with some customers, which in turn could adversely affect our business, results of operations and financial condition.

We could face increased costs related to defending and resolving legal claims and other litigation related to climate change and the alleged impact of our operations on climate change.

The Frequency and Volume of Our Timber and Timberland Sales will Impact Our Financial Performance.

We have a significant inventory of standing timber and timberland and approximately 21,175 acres of special use properties in the United States as of October 31, 2015. The frequency, demand for and volume of sales of timber, timberland and special use properties will have an effect on our financial condition and results of operations. In addition, volatility in the real estate market for special use properties could negatively affect our results of operations.

Changes in U.S. Generally Accepted Accounting Principles (U.S. GAAP) and SEC Rules and Regulations could Materially Impact Our Reported Results.

U.S. GAAP and SEC accounting and reporting changes have become more frequent and significant in the past several years. These changes could have significant effects on our reported results when compared to prior periods and other companies and may even require us to retrospectively adjust prior periods from time to time. Additionally, material changes to the presentation of transactions in the consolidated financial statements could impact key ratios that analysts and credit rating agencies use to rate our company, increase our cost of borrowing and ultimately our ability to access the credit markets in an efficient manner.

If the Company Fails to Maintain an Effective System of Internal Control, the Company may not be able to Accurately Report Financial Results or Prevent Fraud.

Effective internal controls are necessary to provide reliable financial reports and to assist in the effective prevention of fraud. We must annually evaluate our internal control procedures to satisfy the requirements of Section 404 of the Sarbanes-Oxley Act of 2002, which requires management and auditors to assess the effectiveness of internal controls. As further described in Item 9A of this Form 10-K, management has concluded that, because of material weaknesses in internal controls over financial reporting related to international income taxes, including accounting for deferred income taxes and uncertain tax positions, and information technology controls, our disclosure controls and procedures were not effective as of October 31, 2015. If we fail to correct these material weaknesses in our internal controls, or having corrected such material weaknesses, thereafter failing to maintain the adequacy of our internal controls, we could be subjected to regulatory scrutiny, civil or criminal penalties or shareholder litigation. In addition, continued or future failure to maintain adequate internal controls could result in financial statements that do not accurately reflect our financial condition.

The Company has a Significant Amount of Goodwill and Long-lived Assets which, if Impaired in the Future, would Adversely Impact our Results of Operations.

Our goodwill could be impaired if the fair value of any particular reporting unit is less than the carrying value of that reporting unit. Impairment of the Company's goodwill would reduce the Company's net income in the period of any such write down. At October 31, 2015, the carrying value of the Company's goodwill was $807.1 million. The Company is required to evaluate goodwill reflected on its balance sheet at least annually, or when circumstances indicate a potential impairment. If it determines that the goodwill is impaired, the Company would be required to write off a portion or all of the goodwill. As further described in Item 7 and Note 6 of Item 8 of this Form 10-K, in 2014, the Company recorded an impairment for all of the goodwill associated with the Flexible Products & Services segment.

We may be required to record future impairments of our long-lived assets as we continue to transform and restructure our business. Decisions to sell or close plants could reduce the hold period of an asset group or indicate that the fair value of the asset group is less than the carrying value. We may also experience declines in particular businesses due to competition or other outside forces indicating our long-lived assets are not recoverable. Any resulting impairments will impact net income in the period in which the triggering event occurs and could be significant, which could have a material adverse effect on our results of operations.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

12

ITEM 2. PROPERTIES

The following are our principal operating locations and the products manufactured at such facilities or the use of such facilities. We consider our operating properties to be in satisfactory condition and adequate to meet our present needs. However, we expect to make further additions, improvements and consolidations of our properties to support our business.

Location | Products or Use | Owned | Leased | |||

RIGID INDUSTRIAL PACKAGING & SERVICES | ||||||

Algeria | Steel drums | - | 1 | |||

Argentina | Steel and plastic drums, water bottles and distribution centers | 2 | 1 | |||

Australia | Closures | - | 2 | |||

Austria | Steel drums and reconditioned containers and services | - | 1 | |||

Belgium | Steel and plastic drums, reconditioned containers and services and shared services | 3 | 1 | |||

Brazil | Steel and plastic drums, water bottles, closures, intermediate bulk containers, warehouse and general office | 5 | 7 | |||

Canada | Fibre, steel and plastic drums and blending and packaging services | 2 | 2 | |||

Chile | Steel drums, water bottles and distribution centers | 1 | 1 | |||

China | Steel drums, closures, blending and packaging services and general offices | 8 | - | |||

Colombia | Steel and plastic drums and water bottles | 1 | 1 | |||

Costa Rica | Steel Drums | - | 1 | |||

Czech Republic | Steel drums | 1 | - | |||

Denmark | Fibre drums | - | 1 | |||

Egypt | Steel drums | 1 | - | |||

France | Steel and plastic drums, closures and distribution centers | 3 | - | |||

Germany | Fibre, steel and plastic drums, closures, intermediate bulk containers, reconditioned containers and services, and distribution centers | 5 | 2 | |||

Greece | Steel drums and warehouse | 1 | - | |||

Guatemala | Steel drums | 1 | - | |||

Hungary | Steel drums and shared services | 1 | 1 | |||

Israel | Fibre, steel and plastic drums and intermediate bulk containers | - | 1 | |||

Italy | Steel and plastic drums, closures, water bottles, intermediate bulk containers and distribution center | 1 | 5 | |||

Jamaica | Water bottles and distribution center | - | 1 | |||

13

Location | Products or Use | Owned | Leased | |||

Kazakhstan | Distribution center | - | 1 | |||

Kenya | Steel and plastic drums | - | 1 | |||

Malaysia | Steel and plastic drums | 1 | - | |||

Mexico | Fibre, steel and plastic drums, closures and distribution centers | 1 | 3 | |||

Morocco | Steel and plastic drums | 1 | - | |||

Netherlands | Fibre, steel and plastic drums, closures, reconditioned containers and services, paints and linings, research center and general offices | 4 | 3 | |||

Nigeria | Steel and plastic drums | - | 1 | |||

Norway | Steel and plastic drums | - | 1 | |||

Philippines | Steel drums and water bottles | - | 1 | |||

Poland | Steel drums and water bottles | 1 | - | |||

Portugal | Steel drums | 1 | - | |||

Russia | Steel drums, water bottles and intermediate bulk containers | 6 | 1 | |||

Saudi Arabia | Steel drums | - | 1 | |||

Singapore | Steel drums, plastic drums and steel parts | 1 | - | |||

Spain | Steel drums and distribution center | 2 | 1 | |||

Sweden | Steel drums, plastic drums, intermediate bulk containers and distribution center | - | 1 | |||

Turkey | Steel drums and water bottles | 1 | - | |||

Ukraine | Distribution center and water bottles | - | 1 | |||

United Arab Emirates | Idle | - | 1 | |||

United Kingdom | Steel and plastic drums, water bottles, reconditioned containers and services and distribution centers | 3 | - | |||

United States | Fibre, steel and plastic drums, intermediate bulk containers, reconditioned containers and services, closures, steel parts, distribution centers and blending and packaging services | 19 | 27 | |||

Venezuela | Steel and plastic drums | 2 | - | |||

Vietnam | Steel drums | 1 | - |

14

Location | Products or Use | Owned | Leased | |||

FLEXIBLE PRODUCTS & SERVICES: | ||||||

Belgium | Manufacturing plant | - | 1 | |||

Brazil | Distribution center | - | 1 | |||

China | Manufacturing plant | - | 1 | |||

Chile | Distribution center | - | 1 | |||

Finland | Manufacturing plant | 1 | - | |||

France | Manufacturing plant and distribution centers | 1 | 3 | |||

Germany | Distribution centers | - | 2 | |||

India | General office | - | 1 | |||

Ireland | Distribution center | - | 1 | |||

Mexico | Manufacturing plant | - | 1 | |||

Morocco | Manufacturing plant | - | 1 | |||

Netherlands | Manufacturing plant, distribution centers and general office | - | 3 | |||

Pakistan | Manufacturing plants | - | 3 | |||

Portugal | Manufacturing plant | - | 1 | |||

Romania | Manufacturing plants | - | 2 | |||

Saudi Arabia | Idle | - | 1 | |||

Spain | Distribution center | - | 1 | |||

Turkey | Manufacturing plants | - | 3 | |||

Ukraine | Manufacturing plant | 1 | - | |||

United Kingdom | Manufacturing plant | - | 1 | |||

United States | Distribution centers | - | 2 | |||

Vietnam | Manufacturing plant | - | 1 | |||

15

Location | Products or Use | Owned | Leased | |||

PAPER PACKAGING: | ||||||

United States | Corrugated sheets, containers and other products, containerboard, investment property, general offices and distribution centers | 12 | - | |||

LAND MANAGEMENT: | ||||||

United States | General offices | 2 | 1 | |||

CORPORATE: | ||||||

Luxembourg | General office | - | 1 | |||

United States | Principal and general offices | 2 | - |

We also own a substantial amount of timber properties. Our timber properties consisted of approximately 242,673 acres in the southeastern United States as of October 31, 2015.

ITEM 3. LEGAL PROCEEDINGS

We are not a party to any pending legal proceedings that are material to our business or financial condition.

From time to time, we have been a party to legal proceedings arising at the country, state or local level involving environmental sites to which we have shipped, directly or indirectly, small amounts of toxic waste, such as paint solvents. As of the filing date of this Form 10-K, we have been classified only as a "de minimis" participant, and such proceedings do not involve monetary sanctions in excess of $100,000.

ITEM 4. MINE SAFETY DISCLOSURES

None.

16

PART II

ITEM 5. MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Shares of our Class A and Class B Common Stock are listed on the New York Stock Exchange under the symbols GEF and GEF.B, respectively.

Financial information regarding our two classes of common stock, as well as the number of holders of each class and the high, low and closing sales prices for each class for each quarterly period for the two most recent years, is included in Note 20 to the Notes to Consolidated Financial Statements in Item 8 of this Form 10-K.

We pay quarterly dividends of varying amounts computed on the basis described in Note 15 to the Notes to Consolidated Financial Statements included in Item 8 of this Form 10-K. The annual dividends paid for the last two years are as follows:

2015 Dividends per Share – Class A $1.68; Class B $2.51

2014 Dividends per Share – Class A $1.68; Class B $2.51

The terms of our current credit agreement limit our ability to make "restricted payments," which include dividends and purchases, redemptions and acquisitions of our equity interests. The payment of dividends and other restricted payments are subject to the condition that certain defaults not exist under the terms of our current credit agreement and, in the event that certain defaults exist, are limited in amount by a formula based, in part, on our consolidated net income. Refer to "Liquidity and Capital Resources – Borrowing Arrangements" in Item 7 of this Form 10-K.

We did not purchase any of our shares of Class A and Class B Common Stock during 2015.

17

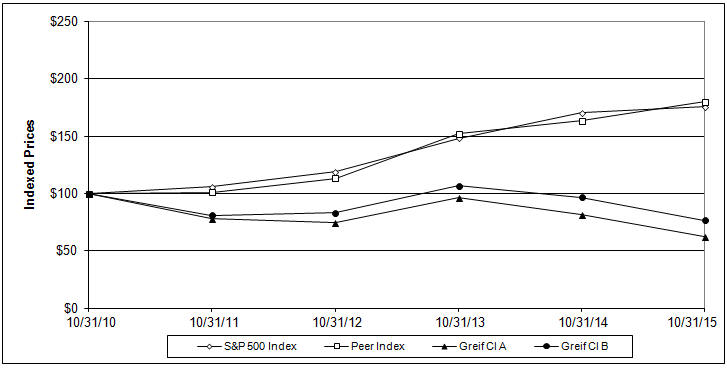

Performance Graph

The following graph compares the performance of shares of our Class A and B Common Stock to that of the Standard and Poor's 500 Index and our industry group (Peer Index) assuming $100 invested on October 31, 2010 and reinvestment of dividends for each subsequent year. The graph does not purport to represent our value.

The Peer Index comprises the containers and packaging index as shown by Dow Jones.

Equity compensation plan information required by Items 201(d) of Regulation S-K will be found under the caption "Equity Compensation Plan Information" in the 2016 Proxy Statement, which information is incorporated herein by reference.

18

ITEM 6. SELECTED FINANCIAL DATA

The five-year selected financial data is as follows (Dollars in millions, except per share amounts):

| As of and for the years ended October 31, | 2015 | 2014 | 2013 | 2012 | 2011 | |||||||||||||||

Net sales | $ | 3,616.7 | $ | 4,239.1 | $ | 4,219.9 | $ | 4,129.5 | $ | 4,107.4 | ||||||||||

Net income attributable to Greif, Inc. | $ | 71.9 | $ | 91.5 | $ | 144.7 | $ | 118.1 | $ | 173.6 | ||||||||||

Total assets | $ | 3,315.7 | $ | 3,667.4 | $ | 3,886.7 | $ | 3,855.9 | $ | 4,191.0 | ||||||||||

Long-term debt, including current portion of long-term debt | $ | 1,146.9 | $ | 1,105.0 | $ | 1,217.2 | $ | 1,200.3 | $ | 1,383.9 | ||||||||||

Basic earnings per share: | ||||||||||||||||||||

Class A Common Stock | $ | 1.23 | $ | 1.56 | $ | 2.47 | $ | 2.03 | $ | 2.98 | ||||||||||

Class B Common Stock | $ | 1.83 | $ | 2.33 | $ | 3.70 | $ | 3.03 | $ | 4.46 | ||||||||||

Diluted earnings per share: | ||||||||||||||||||||

Class A Common Stock | $ | 1.23 | $ | 1.56 | $ | 2.47 | $ | 2.03 | $ | 2.97 | ||||||||||

Class B Common Stock | $ | 1.83 | $ | 2.33 | $ | 3.70 | $ | 3.03 | $ | 4.46 | ||||||||||

Dividends per share: | ||||||||||||||||||||

Class A Common Stock | $ | 1.68 | $ | 1.68 | $ | 1.68 | $ | 1.68 | $ | 1.68 | ||||||||||

Class B Common Stock | $ | 2.51 | $ | 2.51 | $ | 2.51 | $ | 2.51 | $ | 2.51 | ||||||||||

19

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The terms "Greif," "the Company," "we," "us" and "our" as used in this discussion refer to Greif, Inc. and its subsidiaries.

Greif Business System and Transformation Initiative