United States Securities and Exchange Commission

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One) |

☑ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

For the fiscal year ended December 31, 2017 |

or |

¨ Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

For the transition period from ___________to ___________ |

|

Commission file number 001-00035 |

|

General Electric Company(Exact name of registrant as specified in charter) |

New York |

|

|

| 14-0689340 |

(State or other jurisdiction of incorporation or organization) |

|

|

| (I.R.S. Employer Identification No.) |

|

|

|

|

|

41 Farnsworth Street, Boston, MA |

| 02210 |

| (617) 443-3000 |

(Address of principal executive offices) |

| (Zip Code) |

| (Telephone No.) |

|

|

|

|

|

Securities Registered Pursuant to Section 12(b) of the Act: | ||||

Title of each class |

| Name of each exchange on which registered | ||

Common stock, par value $0.06 per share |

| New York Stock Exchange | ||

Securities Registered Pursuant to Section 12(g) of the Act: |

|

(Title of class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10‑K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ☑ | Accelerated filer ¨ |

Non-accelerated filer ¨ | Smaller reporting company ¨ |

Emerging growth company ¨ |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ☑

The aggregate market value of the outstanding common equity of the registrant not held by affiliates as of the last business day of the registrant's most recently completed second fiscal quarter was at least $231.5 billion . There were 8,682,576,000 shares of voting common stock with a par value of $0.06 outstanding at January 31, 2018 .

DOCUMENTS INCORPORATED BY REFERENCE

The definitive proxy statement relating to the registrant's Annual Meeting of Shareowners, to be held April 25, 2018, is incorporated by reference into Part III to the extent described therein.

TABLE OF CONTENTS

| Page |

|

|

10-K Introduction & Summary | 3 |

Forward Looking Statements | 11 |

About General Electric | 12 |

Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A) | 14 |

Key Performance Indicators | 18 |

Consolidated Results | 20 |

Segment Operations | 25 |

GE Corporate Items and Eliminations | 58 |

Other Consolidated Information | 62 |

Statement of Financial Position | 69 |

Financial Resources and Liquidity | 71 |

Critical Accounting Estimates | 82 |

Other Items | 89 |

Supplemental Information | 93 |

Other Financial Data | 104 |

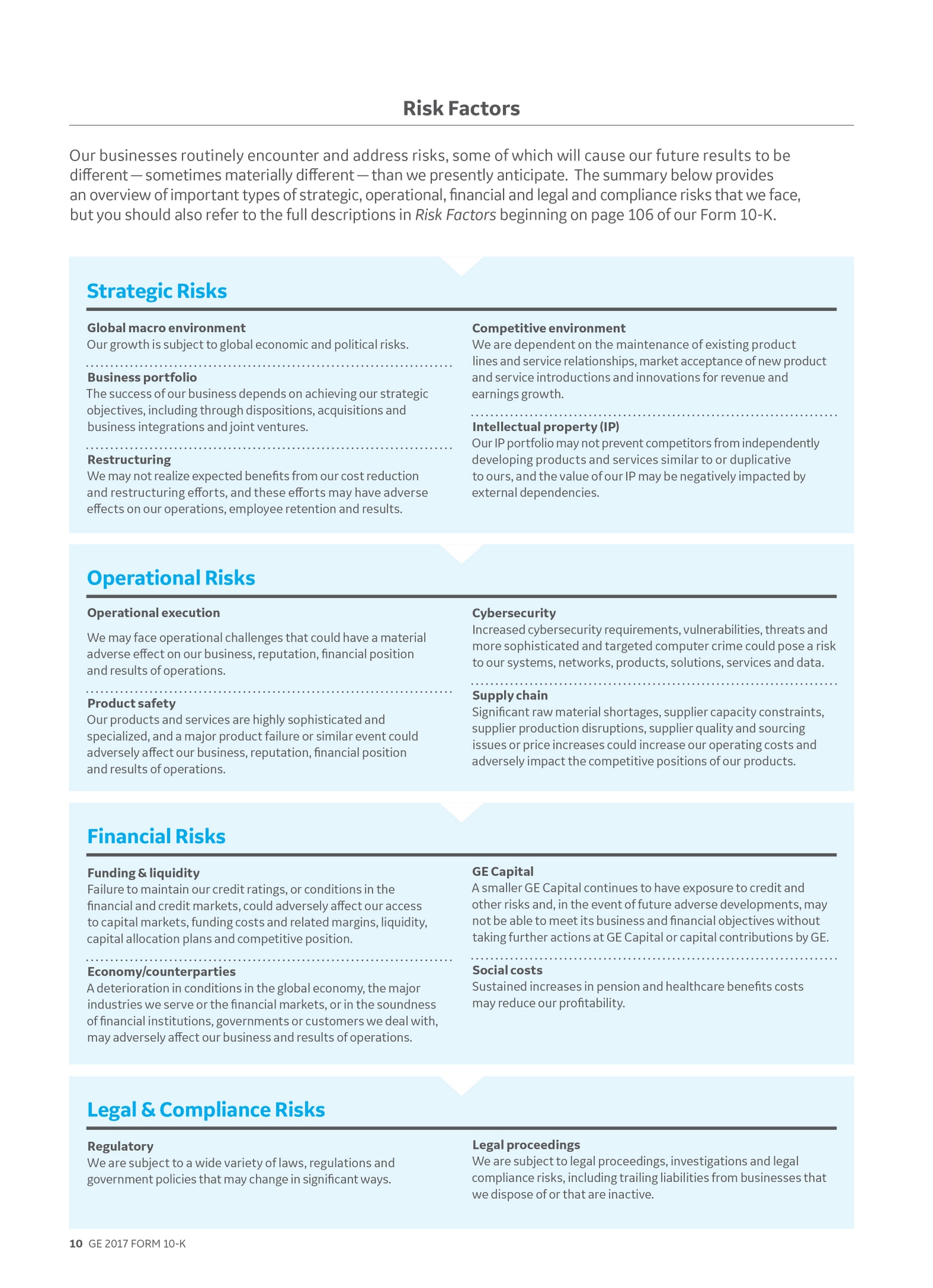

Risk Factors | 106 |

Legal Proceedings | 112 |

Management and Auditor's Reports | 115 |

Audited Financial Statements and Notes | 119 |

Directors, Executive Officers and Corporate Governance | 200 |

Exhibits and Financial Statement Schedules | 201 |

Form 10-K Cross Reference Index | 205 |

Signatures | 206 |

See "Key Performance Indicators" section on page 18 and "Consolidated Results" section on page 20

See "2017 Significant Developments" section on page 20 and "Supplemental Information" section on page 93

See "Segment Operations" section on page 25

See "Segment Operations" section on page 25

See "Segment Operations" section on page 25

See "GE Corporate Items & Eliminations" section on page 58 , "Financial Resources & Liquidity" section on page 71 and "Other Items" section on page 89

See "Risk Factors" section on page 106

FORWARD LOOKING STATEMENTS |

|

|

FORWARD LOOKING STATEMENTS

Our public communications and SEC filings may contain "forward-looking statements" - that is, statements related to future, not past, events. In this context, forward-looking statements often address our expected future business and financial performance and financial condition, and often contain words such as "expect," "anticipate," "intend," "plan," "believe," "seek," "see," "will," "would," "estimate," "forecast," "target," "preliminary," or "range."

Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements about our intention to exit $20 billion or more of assets in 2018 and 2019; charges and capital contributions that may be required in connection with GE Capital's run-off insurance operations, and related GE Capital portfolio actions; revenues; organic growth; cash flows and cash conversion, including the impact of working capital, contract assets and pension funding contributions; earnings per share, including the impact of the new revenue recognition accounting standard; growth and productivity associated with our Digital and Additive businesses; profit margins; cost structure and plans to reduce costs; restructuring, goodwill impairment or other financial charges; tax rates; transaction-related synergies, proceeds and gains; returns on capital and investment; capital allocation, including liquidity, organic investment, dividends and other priorities; or capital structure and access to funding, including credit ratings, debt-to-earnings ratios and leverage.

For us, particular uncertainties that could cause our actual results to be materially different than those expressed in our forward-looking statements include:

• | our execution of Industrial and GE Capital business or asset dispositions, including sale prices, the timing of disposition proceeds and potential trailing liabilities, as well as our ongoing portfolio review; |

• | the amount and timing of our Industrial cash flows and earnings, which may be impacted by customer, competitive, contractual and other dynamics and conditions; |

• | our capital allocation plans, as such plans may change including with respect to the timing and amount of GE dividends, organic investments, including research and development, investments in Digital and capital expenditures, pension funding contributions, acquisitions, joint ventures and other strategic actions; |

• | our ability to maintain our current short- and long-term credit ratings and the impact on our funding costs and competitive position if we do not do so; |

• | customer actions or market developments such as reduced demand for equipment and services in our Power business as a result of increased market penetration by renewables, shifts in the competitive landscape for our products and services, changes in economic conditions, including oil prices, early aircraft retirements and other factors that may affect the level of demand and financial performance of the major industries and customers we serve; |

• | changes in law, economic and financial conditions, including the enactment of tax reform or other tax law changes, interest and exchange rate volatility, commodity and equity prices and the value of financial assets; |

• | the impact of conditions in the financial and credit markets on GE Capital's ability to sell financial assets, the availability and cost of GE Capital funding and GE Capital's exposure to counterparties; |

• | pending and future mortgage loan repurchase claims, other litigation claims and the U.S. Department of Justice's investigation under the Financial Institutions Reform, Recovery and Enforcement Act of 1989 and other investigations in connection with WMC, which may affect our estimates of liability, including possible loss estimates; |

• | our ability to launch new products in a cost-effective manner; |

• | our ability to increase margins through restructuring and other cost reduction measures; |

• | our ability to convert pre-order commitments/wins into orders/bookings; |

• | the price we realize on orders/bookings since commitments/wins are stated at list prices; |

• | the impact of regulation and regulatory, investigative and legal proceedings and legal compliance risks, including the impact of WMC, Alstom and other investigative and legal proceedings; |

• | our success in completing, including obtaining regulatory approvals and satisfying other closing conditions for, announced transactions, such as our plans to sell our Industrial Solutions business, the substantial majority of our Lighting segment or other dispositions that we may pursue; |

• | our success in integrating acquired businesses and operating joint ventures, and our ability to realize revenue and cost synergies from announced transactions, acquired businesses and joint ventures, including Alstom and Baker Hughes, a GE company (BHGE); |

• | the impact of potential information technology, cybersecurity or data security breaches; |

• | the other factors that are described in "Forward-Looking Statements" in Baker Hughes, a GE company's, most recent earnings release or SEC filing; and |

• | the other factors that are described in the Risk Factors section of this Form 10-K report. |

These or other uncertainties may cause our actual future results to be materially different than those expressed in our forward-looking statements. We do not undertake to update our forward-looking statements. This document includes certain forward-looking projected financial information that is based on current estimates and forecasts. Actual results could differ materially.

GE 2017 FORM 10-K 11

ABOUT GENERAL ELECTRIC |

| |

ABOUT GENERAL ELECTRIC

OUR BUSINESS AND HOW WE TALK ABOUT IT

We are a global digital industrial company, transforming industry with software-defined machines and solutions that are connected, responsive and predictive. With products and services ranging from aircraft engines, power generation and oil and gas production equipment to medical imaging, financing and industrial products, we serve customers in over 180 countries and employ approximately 313,000 people worldwide. Since our incorporation in 1892, we have developed or acquired new technologies and services that have considerably broadened and changed the scope of our activities.

OUR INDUSTRIAL OPERATING SEGMENTS

| Power (a) |  | Aviation |  | Lighting (a) |

| Renewable Energy |  | Healthcare |

|

|

| Oil & Gas (b) | Transportation |

|

| |

OUR FINANCIAL SERVICES OPERATING SEGMENT

| Capital |

(a) | Beginning in the third quarter of 2017, the Energy Connections business within the former Energy Connections & Lighting segment was combined with the Power segment and presented as one reporting segment called Power. As a result of this combination, our GE Lighting and Current, powered by GE (Current) businesses are now reported as a separate segment called Lighting. |

(b) | Beginning in the third quarter of 2017, our Oil & Gas segment is comprised of our ownership interest of approximately 62.5% in BHGE. We consolidate 100% of BHGE's revenues and cash flows, while our Oil & Gas segment profit and net income are derived net of minority interest of approximately 37.5% attributable to BHGE's Class A shareholders. |

Business, operation and financial overviews for our operating segments are provided in the Segment Operations section within the Management's Discussion and Analysis of Financial Condition and Results of Operations (MD&A) section.

COMPETITIVE CONDITIONS AND ENVIRONMENT

In all of our global business activities, we encounter aggressive and able competition. In many instances, the competitive climate is characterized by changing technology that requires continuing research and development. With respect to manufacturing operations, we believe that, in general, we are one of the leading firms in most of the major industries in which we participate. The businesses in which GE Capital engages are subject to competition from various types of financial institutions.

As a diverse global company, we are affected by world economies, instability in certain regions, commodity prices, such as the price of oil, foreign currency volatility and policies regarding trade and imports. Other factors impacting our business include:

• | product development cycles for many of our products are long and product quality and efficiency are critical to success, |

• | research and development expenditures are important to our business, |

• | many of our products are subject to a number of regulatory standards and |

• | changing end markets, including shifts in energy sources and demand and the impact of technology changes. |

These factors are discussed throughout MD&A.

12 GE 2017 FORM 10-K

ABOUT GENERAL ELECTRIC |

| |

OUR EMPLOYEES AND EMPLOYEE RELATIONS

At year-end 2017 , General Electric Company and consolidated affiliates employed approximately 313,000 persons, of whom approximately 106,000 were employed in the United States.

Approximately 8,600 GE manufacturing and service employees in the United States are represented for collective bargaining purposes by one of 9 unions (approximately 41 different locals within such unions). A majority of such employees are represented by union locals that are affiliated with the IUE-CWA, The Industrial Division of the Communication Workers of America, AFL-CIO, CLC. In June 2015, we negotiated new four-year collective bargaining agreements with most of our U.S. unions. These agreements continue to provide employees with good wages and benefits while addressing competitive realities facing the Company.

Other GE affiliates are parties to labor contracts with various labor unions, also with varying terms and expiration dates that cover approximately 1,700 employees.

PROPERTIES

Manufacturing operations are carried out at 191 manufacturing plants located in 38 states in the United States and Puerto Rico and at 348 manufacturing plants located in 43 other countries.

CORPORATE INFORMATION AND WEBSITES

General Electric's address is 1 River Road, Schenectady, NY 12345-6999; we also maintain executive offices at 41 Farnsworth Street, Boston, MA 02210.

GE's Internet address at www.ge.com , Investor Relations website at www.ge.com/investor-relations and our corporate blog at www.gereports.com , as well as GE's Facebook page, Twitter accounts and other social media, including @GE_Reports, contain a significant amount of information about GE, including financial and other information for investors. GE encourages investors to visit these websites from time to time, as information is updated and new information is posted.

Additional information on non-financial matters, including environmental and social matters and our integrity policies, is available in GE's Integrated Summary Report and at www.ge.com/sustainability .

Website references in this report are provided as a convenience and do not constitute, and should not be viewed as, incorporation by reference of the information contained on, or available through, the websites. Therefore, such information should not be considered part of this report.

Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are available, without charge, on our website, www.ge.com/investor-relations/events-reports , as soon as reasonably practicable after they are filed electronically with the U.S. Securities and Exchange Commission (SEC). Copies are also available, without charge, from GE Corporate Investor Communications, 41 Farnsworth Street, Boston, MA 02210.

Reports filed with the SEC may be viewed at www.sec.gov or obtained at the SEC Public Reference Room in Washington, D.C. Information about the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

GE 2017 FORM 10-K 13

MD&A |

|

|

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (MD&A)

PRESENTATION

The consolidated financial statements of General Electric Company (the Company) combine the industrial manufacturing and services businesses of General Electric Company (GE) with the financial services businesses of GE Capital Global Holdings, LLC (GE Capital or Financial Services) and its predecessor, General Electric Capital Corporation.

We believe that investors will gain a better understanding of our company if they understand how we measure and talk about our results. Because of the diversity in our businesses, we present our financial statements in a three-column format, which allows investors to see our industrial operations separately from our Financial Services operations. We believe that this provides useful information to investors. When used in this report, unless otherwise indicated by the context, we use the terms to mean the following:

• | General Electric or the Company – the parent company, General Electric Company. |

• | GE – the adding together of all affiliates except GE Capital, whose continuing operations are presented on a one-line basis, giving effect to the elimination of transactions among such affiliates. As GE presents the continuing operations of GE Capital on a one-line basis, certain intercompany profits resulting from transactions between GE and GE Capital have been eliminated at the GE level. We present the results of GE in the center column of our consolidated statements of earnings, financial position and cash flows. An example of a GE metric is GE cash from operating activities (GE CFOA). |

• | General Electric Capital Corporation or GECC – predecessor to GE Capital Global Holdings, LLC. |

• | GE Capital Global Holdings, LLC or GECGH – the adding together of all affiliates of GECGH, giving effect to the elimination of transactions among such affiliates. |

• | GE Capital or Financial Services – refers to GECGH, or its predecessor GECC, and is the adding together of all affiliates of GE Capital giving effect to the elimination of transactions among such affiliates. We present the results of GE Capital in the right-side column of our consolidated statements of earnings, financial position and cash flows. |

• | GE consolidated – the adding together of GE and GE Capital, giving effect to the elimination of transactions between the two. We present the results of GE consolidated in the left-side column of our consolidated statements of earnings, financial position and cash flows. |

• | GE Industrial – GE excluding the continuing operations of GE Capital. We believe that this provides investors with a view as to the results of our industrial businesses and corporate items. An example of a GE Industrial metric is GE Industrial CFOA (Non-GAAP), as defined in Other Terms Used by GE below. |

• | Industrial segment – the sum of our seven industrial reporting segments, without giving effect to the elimination of transactions among such segments and between these segments and our Financial Services segment. This provides investors with a view as to the results of our industrial segments, without inter-segment eliminations and corporate items. An example of an industrial segment metric is industrial segment revenue growth. |

• | Baker Hughes, a GE company or BHGE - following the combination of our Oil & Gas business with Baker Hughes Incorporated, our Oil & Gas segment is comprised of our ownership interest of approximately 62.5% in the new company formed in the transaction, Baker Hughes, a GE Company (BHGE). We consolidate 100% of BHGE's revenues and cash flows, while our Oil & Gas segment profit and net income are derived net of minority interest of approximately 37.5% attributable to BHGE's Class A shareholders. References to "Baker Hughes" represent legacy Baker Hughes Incorporated operating activities which, in certain cases, have been excluded from our results for comparative purposes. |

• | Total segment – the sum of our seven industrial segments and one financial services segment, without giving effect to the elimination of transactions between such segments. This provides investors with a view as to the results of all of our segments, without inter-segment eliminations and corporate items. |

• | Verticals or GE Capital Verticals – the adding together of GE Capital businesses, principally its vertical financing businesses-GE Capital Aviation Services (GECAS), Energy Financial Services (EFS) and Industrial Finance (which includes Healthcare Equipment Finance, Working Capital Solutions and Industrial Financing Solutions)-that relate to the Company's core industrial domain and other operations, including our run-off insurance operations, and allocated corporate costs. |

14 GE 2017 FORM 10-K

MD&A |

|

|

We integrate acquisitions as quickly as possible. Revenues and earnings from the date we complete the acquisition through the end of the fourth quarter following the acquisition are considered the acquisition effect of such businesses.

Amounts reported in billions in graphs within this report are computed based on the amounts in millions. As a result, the sum of the components reported in billions may not equal the total amount reported in billions due to rounding. Certain columns and rows within the tables may not add due to the use of rounded numbers. Percentages presented are calculated from the underlying numbers in millions.

Discussions throughout this MD&A are based on continuing operations unless otherwise noted.

The MD&A should be read in conjunction with the Financial Statements and Notes to the consolidated financial statements.

OTHER TERMS USED BY GE

• | Backlog – unfilled customer orders for products and product services (expected life of contract sales for product services). |

• | Borrowings as a percentage of total capital invested – for GE, the sum of borrowings and mandatorily redeemable preferred stock, divided by the sum of borrowings, mandatorily redeemable preferred stock, redeemable noncontrolling interest, noncontrolling interests and total shareowners' equity. |

• | Continuing earnings – we refer to the caption "earnings from continuing operations attributable to GE common shareowners" as continuing earnings. |

• | Continuing earnings per share (EPS) – when we refer to continuing earnings per share, it is the diluted per-share amount of "earnings from continuing operations attributable to GE common shareowners." |

• | Digital revenues – revenues related to internally developed software (including Predix TM ) and associated hardware, and software solutions that improve our customers' asset performance. In 2016, we reassessed the span of our digital product offerings, which now excludes software-enabled product upgrades. These revenues are largely generated from our operating businesses and are included in their segment results. Revenues of "Non-GE Verticals" refer to GE Digital revenues from customers operating in industries where GE does not have a presence. |

• | Equipment leased to others (ELTO) – rental equipment we own that is available to rent and is stated at cost less accumulated depreciation. |

• | GE Capital Exit Plan - our plan, announced on April 10, 2015, to reduce the size of our financial services businesses through the sale of most of the assets of GE Capital, and to focus on continued investment and growth in our industrial businesses. |

• | GE Industrial CFOA (Non-GAAP) – GE CFOA excluding the effects of dividends from GE Capital. Adjusted GE Industrial CFOA (Non-GAAP) is GE Industrial CFOA excluding deal-related taxes, GE Pension Plan funding and Oil & Gas CFOA, and including dividends received from BHGE. |

• | GE Industrial free cash flow (Non-GAAP) – Adjusted GE Industrial CFOA (Non-GAAP) adjusted for gross GE additions to property, plant and equipment and internal-use software, which are included in cash flows from investing activities, and excluding gross Oil & Gas additions to property, plant and equipment and internal-use software. |

• | GE Industrial margin – GE revenues and other income excluding GE Capital earnings (loss) from continuing operations (GE Industrial revenues) minus GE total costs and expenses less GE interest and other financial charges divided by GE Industrial revenues. |

• | GE Industrial operating profit margin (Non-GAAP) – Industrial segment profit plus corporate items and eliminations (excluding gains, restructuring, and pre-tax non-operating pension cost) divided by industrial segment revenues plus corporate items and eliminations (excluding gains and GE-GE Capital eliminations). |

• | GE Industrial return on total capital (GE Industrial ROTC) (Non-GAAP) – earnings from continuing operations attributable to GE common shareowners less GE Capital earnings from continuing operations plus GE after-tax interest, divided by average GE shareowners' equity, less average GE Capital's shareowners' equity, plus average debt and other, net. |

• | GE Industrial structural costs (Non-GAAP) – Industrial structural costs include segment structural costs excluding the impact of business acquisitions and dispositions, plus total Corporate operating profit excluding pre-tax non-operating pension cost, restructuring and other charges and gains. |

• | GE shareowners' equity and GE Capital shareowner's equity – for purposes of the GE Industrial ROTC calculation excludes the effects of discontinued operations and is calculated on an annual basis using a five-point average. |

• | Global Growth Organization (GGO ) – The GGO provides leadership in global markets, particularly within emerging and developing markets. The organization creates and identifies cross-business commercial opportunities and collaborates with businesses to capitalize on them. The GGO is heavily involved in government advocacy, shaping policy and regulation. Additionally, the GGO provides regional commercial finance capabilities and customer financing solutions, in collaboration with certain of our GE Capital businesses, and works to build the GE brand and protect GE's reputation. |

• | Net earnings – we refer to the caption "net earnings attributable to GE common shareowners" as net earnings. |

GE 2017 FORM 10-K 15

MD&A |

|

|

• | Net earnings per share (EPS) – when we refer to net earnings per share, it is the diluted per-share amount of "net earnings attributable to GE common shareowners." |

• | Non-operating pension cost (Non-GAAP) – comprises the expected return on plan assets, interest cost on benefit obligations and net actuarial gain (loss) amortization for our principal pension plans. |

• | Operating earnings (Non-GAAP) – GE earnings from continuing operations attributable to common shareowners excluding the impact of non-operating pension cost. |

• | Operating earnings per share (Non-GAAP) – when we refer to operating earnings per share, it is the diluted per-share amount of "operating earnings." |

• | Operating pension cost (Non-GAAP) – comprises the service cost of benefits earned, prior service cost amortization and curtailment gain (loss) for our principal pension plans. |

• | Organic revenues (Non-GAAP) – revenues excluding the effects of acquisitions, dispositions and translational foreign currency exchange. |

• | Product services agreements – contractual commitments, with multiple-year terms, to provide specified services for products in our Power, Renewable Energy, Oil & Gas, Aviation and Transportation installed base – for example, monitoring, maintenance, service and spare parts for a gas turbine/generator set installed in a customer's power plant. |

• | Revenues – revenues comprise sales of goods, sales of services and other income for our industrial businesses and GE Capital revenues from services for our financial services businesses. |

• | Segment profit – refers to the operating profit of the industrial segments and the net earnings of the Financial Services segment. See the Segment Operations section within the MD&A for a description of the basis for segment profits. |

• | Services – for purposes of the financial statement display of sales and costs of sales in our Statement of Earnings (Loss), "goods" is required by SEC regulations to include all sales of tangible products, and "services" must include all other sales, including other services activities. In our MD&A section of this report, we refer to sales under product services agreements and sales of both goods (such as spare parts and equipment upgrades) and related services (such as monitoring, maintenance and repairs) as sales of "services," which is an important part of our operations. |

• | Shared Services – sharing of business processes in order to standardize and consolidate services to provide value to the businesses in the form of simplified processes, reduced overall costs and increased service performance. |

16 GE 2017 FORM 10-K

MD&A |

|

|

NON-GAAP FINANCIAL MEASURES

In the accompanying analysis of financial information, we sometimes use information derived from consolidated financial data but not presented in our financial statements prepared in accordance with U.S. generally accepted accounting principles (GAAP). Certain of these data are considered "non-GAAP financial measures" under the SEC rules. Specifically, we have referred, in various sections of this report, to:

• | Industrial segment organic revenues |

• | Industrial segment organic operating profit |

• | Operating and non-operating pension cost |

• | GE Industrial structural costs and GE Industrial structural costs, excluding acquisitions and dispositions |

• | GE pre-tax earnings (loss) from continuing operations, excluding GE Capital earnings (loss) from continuing operations and the corresponding effective tax rates, and the reconciliation of the U.S. federal statutory income tax rate to GE effective tax rate, excluding GE Capital earnings |

• | GE Industrial operating earnings and GE Capital earnings (loss) from continuing operations and EPS |

• | GE Industrial operating + Verticals earnings and EPS |

• | GE Industrial operating profit and operating profit margin (excluding certain items) |

• | Average GE shareowners' equity, excluding effects of discontinued operations |

• | Average GE Capital shareowner's equity, excluding effects of discontinued operations |

• | GE Industrial return on total capital (GE Industrial ROTC) |

• | GE Industrial cash flows from operating activities (GE Industrial CFOA), adjusted GE Industrial CFOA and GE Industrial free cash flow (FCF) |

• | 2018 operating framework including 2018 Adjusted EPS and GE Industrial free cash flow |

The reasons we use these non-GAAP financial measures and the reconciliations to their most directly comparable GAAP financial measures are included in the Supplemental Information section within the MD&A. Non-GAAP financial measures referred to in this report are either labeled as "non-GAAP" or designated as such with an asterisk (*).

GE 2017 FORM 10-K 17

MD&A | KEY PERFORMANCE INDICATORS |

|

KEY PERFORMANCE INDICATORS

REVENUES PERFORMANCE |

|

| ||

| 2017 | | 2016 | |

Industrial Segment | 3 | % | 4 | % |

Industrial Segment Organic (Non-GAAP)(a) | - | % | (1)% / 1% | |

Financial Services | (17 | )% | 1 | % |

(a) Included the results of Alstom for November and December of both 2016 and 2015.

GE INDUSTRIAL ORDERS AND BACKLOG |

|

|

| ||||||

(Dollars in billions) | 2017 | | 2016 | | 2015 | | |||

|

|

|

| ||||||

Orders |

|

|

| ||||||

Equipment | $ | 58.2 | | $ | 55.2 | | $ | 56.5 | |

Services | 60.6 | | 55.7 | | 49.5 | | |||

Total(a) | $ | 118.8 | | $ | 110.9 | | $ | 105.9 | |

|

|

|

| ||||||

Backlog |

|

|

| ||||||

Equipment | $ | 84.7 | | $ | 84.1 | | $ | 88.6 | |

Services | 256.7 | | 236.8 | | 225.9 | | |||

Total | $ | 341.3 | | $ | 320.9 | | $ | 314.5 | |

(a) Included $5.2 billion related to Baker Hughes in 2017.

GE INDUSTRIAL COSTS |

|

| ||||

(Dollars in billions) | 2017 | | 2016 | | ||

|

|

| ||||

GE Industrial costs excluding interest and financial charges (GAAP) | $ | 108.3 | | $ | 101.8 | |

GE Industrial structural costs, excluding business development activity (Non-GAAP) | 23.0 | | 24.7 | | ||

GE INDUSTRIAL MARGINS (GAAP) AND GE INDUSTRIAL OPERATING PROFIT MARGINS (NON-GAAP) | ||||||

(Dollars in billions) | 2017 | | 2016 | | 2015 | |

|

|

|

| |||

GE Industrial margins (GAAP) | 5.7 | % | 11.4 | % | 11.7 | % |

GE Industrial operating profit margins (Non-GAAP)(a) | 12.1 | % | 14.0 | % | 14.8 | % |

(a) | Excluded gains on disposals, non-operating pension cost, restructuring and other charges, noncontrolling interests and GE Capital preferred stock dividends |

EARNINGS | |||||||||

(Dollars in billions; per-share amounts in dollars) | 2017 | | 2016 | | 2015 | | |||

|

|

|

| ||||||

Continuing earnings (loss) (GAAP) | $ | (5.9 | ) | $ | 9.1 | | $ | 1.7 | |

Net earnings (loss) (GAAP) | (6.2 | ) | 8.2 | | (6.1 | ) | |||

Operating earnings (loss) (Non-GAAP) | (4.4 | ) | 10.5 | | 3.5 | | |||

GE Industrial operating + verticals earnings (loss) (Non-GAAP) | (3.9 | ) | 13.6 | | 13.1 | | |||

|

|

|

| ||||||

Continuing earnings (loss) per share (GAAP) | $ | (0.68 | ) | $ | 1.00 | | $ | 0.17 | |

Net earnings (loss) per share (GAAP) | (0.72 | ) | 0.89 | | (0.61 | ) | |||

Operating earnings (loss) per share (Non-GAAP) | (0.51 | ) | 1.14 | | 0.35 | | |||

GE Industrial operating + verticals earnings (loss) per share (Non-GAAP) | (0.45 | ) | 1.49 | | 1.31 | | |||

GE CFOA AND GE INDUSTRIAL FREE CASH FLOW (NON-GAAP) |

|

|

| ||||||

(Dollars in billions) | 2017 | | 2016 | | 2015 | | |||

|

|

|

| ||||||

GE CFOA (GAAP)(a) | $ | 11.0 | | $ | 30.0 | | $ | 16.4 | |

GE Industrial CFOA (Non-GAAP)(a) | 7.0 | | 9.9 | | 12.1 | | |||

Adjusted Industrial CFOA (Non-GAAP) | 9.7 | | 11.6 | | 12.2 | | |||

GE Industrial free cash flow (Non-GAAP) | 5.6 | | 7.1 | | 7.7 | | |||

(a) | Included $0.5 billion related to Baker Hughes in 2017. |

18 GE 2017 FORM 10-K

MD&A | KEY PERFORMANCE INDICATORS |

|

KEY PERFORMANCE INDICATORS

(Dollars in billions; per-share amounts in dollars)

SHAREOWNER INFORMATION | |

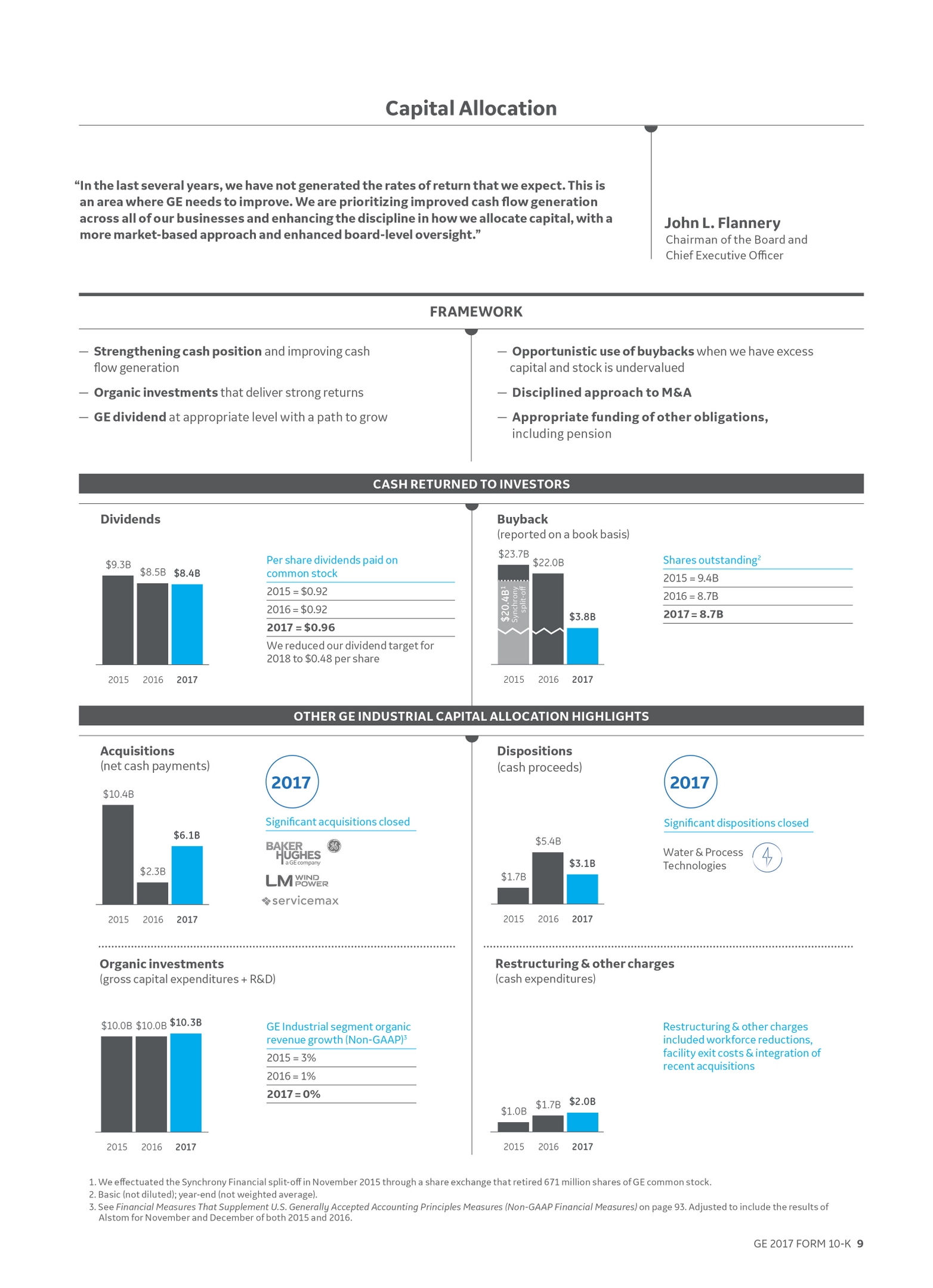

RETURNED $12.1 BILLION TO SHAREOWNERS IN 2017 Dividends $8.4 billion Stock buyback $3.8 billion | ANNUAL MEETING General Electric's 2018 Annual Meeting of Shareowners will be held on April 25, 2018, in Imperial, PA |

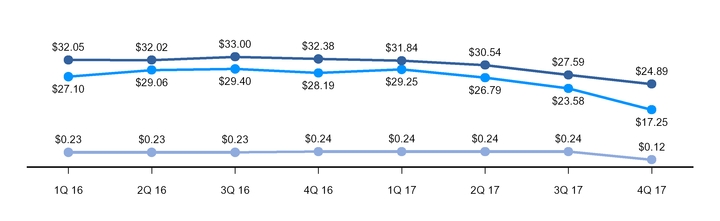

FIVE-YEAR PERFORMANCE GRAPH |

|

The annual changes for the five-year period shown in the graph on this page are based on the assumption that $100 had been invested in General Electric common stock, the Standard & Poor's 500 Stock Index (S&P 500) and the Dow Jones Industrial Average (DJIA) on December 31, 2012, and that all quarterly dividends were reinvested. The cumulative dollar returns shown on the graph represent the value that such investments would have had on December 31 for each year indicated.

STOCK PRICE RANGE AND DIVIDENDS |

|

With respect to "Market Information," in the United States, General Electric common stock is listed on the New York Stock Exchange (its principal market). General Electric common stock is also listed on the London Stock Exchange, Euronext Paris, the SIX Swiss Exchange and the Frankfurt Stock Exchange. The chart above shows trading prices, as reported on the New York Stock Exchange, Inc., Composite Transactions Tape.

As of January 31, 2018, there were approximately 418,000 shareowner accounts of record.

On February 9, 2018, our Board of Directors approved a quarterly dividend of $0.12 per share of common stock, which is payable April 25, 2018, to shareowners of record at close of business on February 26, 2018.

GE 2017 FORM 10-K 19

MD&A | CONSOLIDATED RESULTS | |

CONSOLIDATED RESULTS

PRESENTATION

When used in this report, unless otherwise indicated by the context, we use the terms to mean the following:

• | Continuing earnings – we refer to the caption "earnings from continuing operations attributable to GE common shareowners" as continuing earnings. |

• | Continuing earnings per share (EPS) – when we refer to continuing earnings per share, it is the diluted per-share amount of "earnings from continuing operations attributable to GE common shareowners." |

• | GE Industrial margin – GE revenues and other income excluding GE Capital earnings (loss) from continuing operations (GE Industrial revenues) minus GE total costs and expenses less GE interest and other financial charges divided by GE Industrial revenues. |

• | Net earnings – we refer to the caption "net earnings attributable to GE common shareowners" as net earnings. |

• | Net earnings per share (EPS) – when we refer to net earnings per share, it is the diluted per-share amount of "net earnings attributable to GE common shareowners." |

• | Operating earnings (Non-GAAP) – GE earnings from continuing operations attributable to common shareowners excluding the impact of non-operating pension costs. |

• | Organic revenues (Non-GAAP) – revenues excluding the effects of acquisitions, dispositions and translational foreign currency exchange. |

• | Revenues – revenues comprise sales of goods, sales of services and other income for our industrial businesses and GE Capital revenues from services for our financial services businesses. |

• | Segment profit – refers to the operating profit of the industrial segments and the net earnings of the Financial Services segment. See the Segment Operations section within the MD&A for a description of the basis for segment profits. |

• | Services – for purposes of the financial statement display of sales and costs of sales in our Statement of Earnings (Loss), "goods" is required by SEC regulations to include all sales of tangible products, and "services" must include all other sales, including other services activities. In our MD&A section of this report, we refer to sales under product services agreements and sales of both goods (such as spare parts and equipment upgrades) and related services (such as monitoring, maintenance and repairs) as sales of "services," which is an important part of our operations. |

2017 SIGNIFICANT DEVELOPMENTS

LEADERSHIP CHANGES

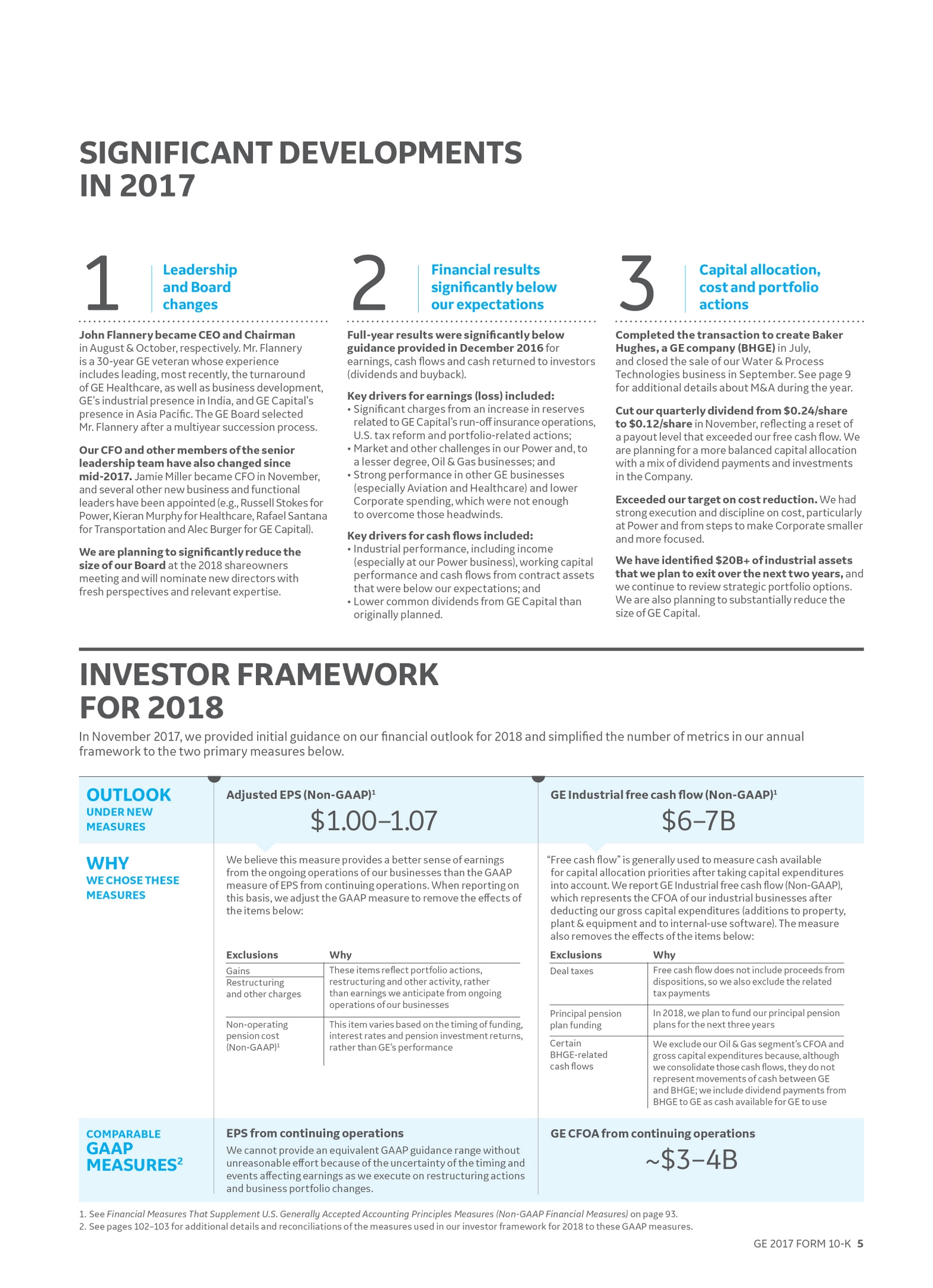

As announced on June 12, 2017, Jeffery R. Immelt retired as Chief Executive Officer (CEO) on July 31, 2017, and John L. Flannery succeeded Mr. Immelt as CEO effective August 1, 2017. Mr. Flannery also joined the Board of Directors (the Board) on that date. Mr. Immelt remained Chairman of the Board for a transition period through October 2, 2017, at which point Mr. Flannery succeeded Mr. Immelt as Chairman.

On October 6, 2017, we announced that, effective November 1, 2017, Jamie S. Miller, would become Chief Financial Officer, succeeding Jeffrey S. Bornstein. Mr. Bornstein remained a Vice Chairman through December 31, 2017. Ms. Miller also serves as a director at Baker Hughes, a GE company.

On October 9, 2017, we announced that Robert Lane retired from the Board after 12 years of service, effective that same date. In addition, the Board elected Edward P. Garden as a director to fill the resulting vacancy, effective on that date. Mr. Garden is the Chief Investment Officer and a Founding Partner of Trian Fund Management, L.P. (Trian), an investment management firm. On December 8, 2017, we announced that Lowell C. McAdam resigned from the Board. We are also planning to significantly reduce the size of our Board at the 2018 annual meeting of shareowners and will nominate new directors with fresh perspectives and relevant expertise.

20 GE 2017 FORM 10-K

MD&A | CONSOLIDATED RESULTS | |

2017 SIGNIFICANT DEVELOPMENTS

• | On January 10, 2017, we completed the acquisition of ServiceMax, a leader in cloud-based field service management (FSM) solutions, for $0.9 billion, net of cash acquired. |

• | On April 20, 2017, we completed the acquisition of LM Wind Power, one of the world's largest wind turbine blade manufacturers for approximately $1.7 billion, net of cash acquired. |

• | On July 3, 2017, we completed the transaction to create Baker Hughes, a GE company (BHGE). We combined our Oil & Gas business and Baker Hughes Incorporated (Baker Hughes) to create a new company in which GE holds an ownership interest of approximately 62.5% and former Baker Hughes shareholders hold an ownership interest of approximately 37.5%. Baker Hughes shareholders also received a cash dividend funded by a $7.5 billion cash contribution from GE. Effective July 3, 2017, the operations of Baker Hughes are reported in our Oil & Gas segment. |

• | On March 8, 2017, we signed an agreement to sell our Water business within our Power segment to Suez Environnement S.A. (Suez). On September 30, 2017, we completed the sale for consideration of $3.1 billion , net of obligations assumed and cash transferred (including $0.1 billion from the sale of receivables originated in our Water business and sold from GE Capital to Suez), and recognized a pre-tax gain of $1.9 billion in the third quarter of 2017. |

• | In the first quarter of 2017, we classified our Industrial Solutions business within our Power segment as held for sale. In September 2017, we announced an agreement to sell the business for approximately $2.6 billion to ASEA Brown Boveri (ABB), a Swiss-based engineering company. The deal is expected to close in mid-2018, subject to customary closing conditions and regulatory approval. |

• | In the fourth quarter of 2017, we classified the substantial majority of our Lighting segment and two nonstrategic Aviation businesses as held for sale. In connection with this determination, we adjusted the carrying value of each business classified as held for sale to fair value, less cost to sell, which resulted in a pre-tax loss of $0.8 billion related to Lighting and $0.6 billion related to Aviation. These losses have been recorded at Corporate. In February 2018, we entered into an agreement to sell our GE Lighting business in Europe, the Middle East, Africa and Turkey and our Global Automotive Lighting business to a company controlled by a former GE executive in the region. The proposed transaction is expected to close in mid-2018, subject to customary closing conditions and local agreements. |

• | On December 22, 2017, the U.S. enacted the Tax Cuts and Jobs Act ("U.S. tax reform") that lowers the statutory tax rate on U.S. earnings, taxes historic foreign earnings at a reduced rate of tax, establishes a territorial tax system and enacts new taxes associated with global operations. As a result of the enactment of U.S. tax reform, we have recorded tax expense of $3.3 billion in 2017 to reflect our provisional estimate of both the transition tax on historic foreign earnings ($1.2 billion) and the revaluation of deferred taxes ($2.2 billion). |

• | On January 16, 2018, GE reported the results of a review of premium deficiency assumptions related to GE Capital's run-off insurance business. With the completion of that review and of the annual premium deficiency test, GE recorded an increase in future policy benefit reserves of $8.9 billion and $0.6 billion of related intangible asset write-off for the fourth quarter of 2017. This resulted in an after-tax charge of $6.2 billion to GE's earnings in the fourth quarter of 2017. In addition, GE Capital will contribute approximately $15 billion of capital to its run-off insurance business over the next seven years. GE Capital plans to make its first contribution of approximately $3.5 billion in the first quarter of 2018 and expects to make further contributions of approximately $2 billion per year in each of the six following years, subject to ongoing monitoring by the Kansas Insurance Department, its primary regulator. GE Capital plans to fund the capital contributions with its excess liquidity and other GE Capital portfolio actions and does not expect to make a common share dividend distribution to GE for the foreseeable future. |

• | GE also announced that it plans to take actions to make GE Capital smaller and more focused, including a substantial reduction in the size of GE Capital's Energy Financial Services and Industrial Finance businesses over the next 24 months. Those actions resulted in goodwill and other asset impairment charges of $1.8 billion on an after-tax basis in the fourth quarter of 2017. |

SUMMARY OF 2017 RESULTS

Overall, our consolidated results for the year were significantly below our expectations. After adjusting for incremental Baker Hughes revenues of $5.2 billion, the Water gain of $1.9 billion, fair market value adjustments on businesses classified as held for sale of $1.4 billion and the 2016 gains on Appliances and GE Asset Management of $3.1 billion and $0.4 billion, respectively, adjusted consolidated revenues*, which includes other income, were $116.3 billion, down $3.8 billion or 3%. This decrease was largely driven by the net effect of dispositions on industrial segment revenues of $3.3 billion, primarily attributable to Appliances. Industrial segment revenues increased $0.1 billion organically* driven principally by our Aviation, Renewable Energy and Healthcare segments. Excluding our Power and Oil & Gas segments, industrial segment revenues increased $1.7 billion, or 3%, organically*.

Continuing earnings (loss) per share was $(0.68), and Industrial operating plus Verticals earnings per share* was $(0.45), driven by a 16% decrease in industrial segment profit as well as $1.49 of charges recognized in the fourth quarter as follows: GE Capital insurance-related charges of $0.91 per share, including $0.71 related to the completion of GE Capital's insurance premium deficiency review and $0.20 related to EFS impairments; tax-reform related charges of $0.40 per share; Industrial portfolio-related charges of $0.18 per share, including $0.15 per share related to fair market value adjustments on businesses classified as held for sale and $0.13 related to goodwill impairment in our Power Conversation business.

*Non-GAAP Financial Measure

GE 2017 FORM 10-K 21

MD&A | CONSOLIDATED RESULTS | |

For the twelve months ended December 31, 2017, restructuring and other charges were $0.46 per sh are, including $0.05 per share related to BHGE integration and synergy investment. In total, restructuring and other items were $5.3 billion before tax, with restructuring charges totaling about $2.7 billion and businesses development charges totaling $0.8 billion. Subsequent to the Baker Hughes transaction and beginning in the third quarter of 2017, $0.5 billion of restructuring charges and $0.2 billion of business development charges related to BHGE are reported under our Oil & Gas segment. Restructuring charges were higher than originally planned, driven by the accelerated restructuring actions taken a t Corporate. Additionally, within restructuring and other charges, we recognized two significant impairments in the year totaling $0.16 per share, which included non-cash pre-tax impairment charges of $1.2 billion related to goodwill in our Power Conversion business and $0.3 billion related to a power plant asset. See Note 8 to the consolidated financial statements for further information.

For the twelve months ended December 31, 2017, GE Industrial profit was $6.6 billion and GE Industrial margins were 5.7%, down $6.5 billion, or 570 basis points, primarily driven by a reduction in industrial segment profit of $2.9 billion, or 16%, as well as increased non-cash charges recorded at Corporate of $2.9 billion, including impairment charges and charges associated with businesses classified as held for sale, and lower gains of $1.5 billion from disposed businesses, partially offset by decreased restructuring and other charges of $0.5 billion and lower Corporate costs of $0.5 billion. The decline in industrial segment profit was primarily due to lower results within our Power and Oil & Gas segments, partially offset by the performance of our Aviation and Healthcare segments. In 2017, we exceeded our structural cost* reduction target for the year of $1.0 billion, delivering $1.7 billion of structural cost* reduction, excluding the effects of acquisition and disposition activity.

Beginning in the third quarter of 2017, the Energy Connections business within the former Energy Connections & Lighting segment was combined with the Power segment and presented as one reporting segment called Power. For the year ended December 31, 2017, the Power segment experienced a revenue decline of 2% and a segment profit decline of 45% versus 2016. Power revenues were $36.0 billion, with service revenues down 6% and equipment revenues up 2%.

The decline in Power segment results was primarily driven by market demands that were softer than expected, resulting in 55 fewer shipments of aeroderivative units as well as 65 fewer Advanced Gas Path upgrades when compared to the year ended December 31, 2016. In addition, we recorded pre-tax charges of $0.9 billion in the fourth quarter primarily related to slow moving and obsolete inventory across several businesses within Power, a litigation settlement and a bankruptcy of a distributor.

In response to these conditions, in 2017, Power focused on cost reduction actions, removing $0.8 billion of structural costs, excluding the effects of acquisition and disposition activity. Refer to the Power segment results section within this MD&A for further information.

Beginning in the third quarter of 2017, our Oil & Gas segment is comprised of our ownership interest of approximately 62.5% in the combined BHGE entity. We consolidate 100% of BHGE's revenues and cash flows while segment profit and net income are derived net of minority ownership interest of approximately 37.5% attributable to BHGE's Class A shareholders. Also, the segment profit we report for our Oil & Gas segment is adjusted for GE reporting conventions, such as excluding restructuring and other charges. Therefore, our segment profit of approximately 62.5% will differ from BHGE's operating income as reported in its standalone financial statements.

For the year ended December 31, 2017, Oil & Gas reported revenues of $17.2 billion, an increase of 34% versus the year ended December 31, 2016, driven by the effects of the Baker Hughes transaction. Adjusting for the Baker Hughes transaction, segment revenues* were $12.0 billion in the year, down 7% due to continued weakness in the oil and gas market. Segment profit was $220 million, or $899 million after adjusting for restructuring and other charges reported in the segment*. The decline in segment profit (after adjusting for restructuring and other charges reported in the segment*) of 35% was primarily driven by longer cycle oilfield equipment business. Refer to the Oil & Gas segment results section within this MD&A for further information.

GE CFOA was $11.0 billion and $29.9 billion for the twelve months ended December 31, 2017 and 2016, respectively. The decline in GE CFOA is primarily due to a $16.1 billion decrease in dividends from GE Capital, reflecting a decrease in proceeds from disposals related to the GE Capital Exit Plan . GE CFOA was also impacted by lower earnings from Power and Oil & Gas, as well as lower cash generated from working capital compared to 2016 . Additionally, GE CFOA was negatively impacted by GE Pension Plan payments of $1.7 billion in 2017, compared to $0.3 billion in the prior year. GE did not receive a common share dividend distribution from GE Capital in the second half of 2017, and it does not expect to receive such dividend distributions from GE Capital for the foreseeable future. Refer to the GE Cash Flows and Critical Accounting Estimates sections within this MD&A for further information.

*Non-GAAP Financial Measure

22 GE 2017 FORM 10-K

MD&A | CONSOLIDATED RESULTS | |

CONSOLIDATED RESULTS

REVENUES

REVENUES |

|

|

| ||||||

(Dollars in billions) | 2017 | | 2016 | | 2015 | | |||

|

|

|

| ||||||

Consolidated revenues(a) | $ | 122.1 | | $ | 123.7 | | $ | 117.4 | |

|

|

|

| ||||||

Industrial segment revenues(b) | $ | 116.2 | | $ | 112.8 | | $ | 108.6 | |

Corporate revenues and Industrial eliminations | (1.2 | ) | 2.1 | | (0.2 | ) | |||

GE Industrial revenues(b) | $ | 114.9 | | $ | 114.9 | | $ | 108.4 | |

|

|

|

| ||||||

Financial services revenues | $ | 9.1 | | $ | 10.9 | | $ | 10.8 | |

(a) | Included $ 1.6 billion, $ 4.0 billion, and $ 2.2 billion of Other income primarily attributable to net gains on purchases and sales of business interests of $0.7 billion, $3.7 billion, and $1.0 billion in 2017, 2016, and 2015, respectively. See Note 17 to the consolidated financial statements for further information. |

(b) | GE Industrial refers to GE excluding the continuing operations of GE Capital. Industrial segment refers to the sum of our seven industrial reporting segments, without giving effect to corporate items or the elimination of transactions among such segments and between these segments and our Financial Services segment. |

REVENUES COMMENTARY: 2017 – 2016 |

Consolidated revenues decreased $ 1.6 billion, or 1% , primarily driven by decreased Financial Services revenues of $ 1.8 billion and decreased Corporate revenues of $ 3.1 billion, partially offset by increased industrial segment revenues of $ 3.3 billion. The overall foreign currency impact on consolidated revenues was an increase of $0.6 billion. Below are descriptions of the components:

• | GE Industrial revenues remained flat for the year due to an increase in industrial segment revenues of $ 3.3 billion offset by a decrease in Corporate revenues and Industrial eliminations of $3.3 billion. |

Industrial segment revenues increased $ 3.3 billion, or 3% , as increases at Oil & Gas, Renewable Energy, Aviation and Healthcare were partially offset by decreases at Power, Transportation and Lighting. This increase was driven by the net effects of acquisitions of $6.0 billion, primarily attributable to Baker Hughes, and the effects of a weaker U.S. dollar of $0.6 billion, partially offset by the net effects of dispositions of $3.4 billion, primarily attributable to Appliances. Excluding the effects of acquisitions, dispositions and translational currency exchange, industrial segment organic revenues* increased $0.1 billion.

Corporate revenues and Industrial eliminations decreased $3.3 billion primarily driven by lower gains on disposed businesses and higher non-cash held for sale charges. Included in 2016 were gains of $3.1 billion from the sale of our Appliances business and $0.4 billion from the sale of GE Asset Management, while 2017 included a gain of $1.9 billion from the sale of our Water business as well as charges associated with businesses classified as held for sale including the substantial majority of our Lighting segment for $0.8 billion and two nonstrategic Aviation businesses for $0.6 billion.

• | Financial Services revenues decreased $ 1.8 billion, or 17% , primarily due to higher impairments and organic revenue declines. |

REVENUES COMMENTARY: 2016 – 2015 |

Consolidated revenues increased $ 6.3 billion, or 5% , primarily driven by increased industrial segment revenues of $ 4.2 billion, increased Corporate revenues of $ 2.0 billion and increased Financial Services revenues of $ 0.1 billion. The overall foreign currency impact on consolidated revenues was a decrease of $1.3 billion. Below are descriptions of the components:

• | GE Industrial revenues increased $ 6.6 billion, or 6% , driven by increased industrial segment revenues of $ 4.2 billion and increased Corporate revenues and Industrial eliminations of $2.3 billion. |

Industrial segment revenues increased $ 4.2 billion, or 4% , as increases at Power, Renewable Energy, Aviation and Healthcare were partially offset by decreases at Oil & Gas, Transportation and Lighting. This increase in industrial segment revenues was driven by the net effects of acquisitions of $11.2 billion, primarily attributable to Alstom, offset by the net effects of dispositions of $5.6 billion , primarily attributable to Appliances, and the effects of a stronger U.S. dollar of $0.8 billion. Excluding the effects of acquisitions, dispositions and translational currency exchange, industrial segment organic revenues* decreased $0.5 billion.

Corporate revenues and Industrial eliminations increased $2.3 billion driven by higher gains of $1.9 billion. Included in 2016 are gains of $3.1 billion from the sale of our Appliances business and $0.4 billion from the sale of GE Asset Management, while 2015 included gains of $0.6 billion from the sale of our Signaling business and $0.5 billion from a settlement related to the NBCU transaction.

• | Financial Services revenues increased $ 0.1 billion, or 1% , primarily due to lower impairments, higher gains and the effects of acquisitions, partially offset by organic revenue declines, the effects of dispositions and the effects of translational currency exchange. |

*Non-GAAP Financial Measure

GE 2017 FORM 10-K 23

MD&A | CONSOLIDATED RESULTS | |

EARNINGS

EARNINGS (LOSS) AND EARNINGS (LOSS) PER SHARE |

|

|

| ||||||

(Dollars in billions; per-share amounts in dollars) | 2017 | | 2016 | | 2015 | | |||

|

|

|

| ||||||

Continuing earnings (loss)(a) | $ | (5.9 | ) | $ | 9.1 | | $ | 1.7 | |

|

|

|

| ||||||

Continuing earnings (loss) per share | $ | (0.68 | ) | $ | 1.00 | | $ | 0.17 | |

(a) Also referred to as "Earnings (loss) from continuing operations attributable to GE common shareowners"

EARNINGS COMMENTARY: 2017 – 2016 |

• | GE Industrial earnings decreased $ 6.5 billion, or 49% , driven by a decrease in Corporate profit of $3.6 billion and a decrease in industrial segment profit of $2.9 billion. |

Corporate profit decreased $3.6 billion primarily attributable to increased non-cash charges of $2.9 billion including goodwill impairment of $1.2 billion, a power plant asset impairment of $0.3 billion, and charges associated with businesses classified as held for sale including the substantial majority of our Lighting segment for $0.8 billion and two nonstrategic Aviation businesses for $0.6 billion. In addition, Corporate recorded lower gains of $1.5 billion. Included in 2016 were gains of $3.1 billion from the sale of our Appliances business and $0.4 billion from the disposition of GE Asset Management, while 2017 included a gain of $1.9 billion from the sale of our Water business. P ension costs were also $0.2 billion higher, partially offset by decreased restructuring and other costs of $0.5 billion and decreased adjusted Corporate operating costs* of $0.5 billion.

Industrial segment profit decreased $ 2.9 billion, or 16% , with decreases at Power, Oil & Gas and Transportation partially offset by higher earnings at Aviation, Healthcare, Renewable Energy and Lighting. This decrease in industrial segment profit was primarily driven by restructuring costs related to Baker Hughes of $0.7 billion and the net effects of dispositions of $0.2 billion, largely associated with Appliances, partially offset by the net effects of acquisitions $0.3 billion, largely associated with Baker Hughes. Excluding these items, industrial segment organic profit* decreased $2.3 billion.

• | Foreign exchange adversely affected Industrial operating earnings by an insignificant amount in 2017. |

• | Financial Services losses increased $ 5.5 billion, primarily due to a $6.2 billion after-tax charge related to the completion of GE Capital's insurance premium deficiency review, as well as EFS strategic actions resulting in $1.8 billion of after-tax charges in addition to higher impairments, partially offset by lower headquarters and treasury operation expenses associated with the GE Capital Exit Plan, higher tax benefits including the effects of U.S. tax reform and lower preferred dividend expenses associated with the January 2016 preferred equity exchange. |

EARNINGS COMMENTARY: 2016 – 2015 |

• | GE Industrial earnings increased $0.5 billion due to an increase in Corporate profit of $0.9 billion, partially offset by a decrease in industrial segment profit of $0.4 billion. |

Corporate profit increased $0.9 billion, or 17%, driven by higher gains of $1.9 billion. I ncluded in 2016 are gains of $3.1 billion from the sale of our Appliances business and $0.4 billion from the sale of GE Asset Management, while 2015 included gains of $0.6 billion from the sale of our Signaling business and $0.5 billion from a settlement related to the NBCU transaction. In addition, pension costs were $0.7 billion lower, partially offset by $1.8 billion of higher restructuring and other charges primarily related to Alstom.

Industrial segment profit decreased $0.4 billion, or 2%, with decreases at Oil & Gas, Lighting, and Transportation partially offset by increases at Aviation, Power, Healthcare and Renewable Energy. This decrease in industrial segment profit was primarily driven by the net effects of dispositions of $0.5 billion, largely associated with Appliances, offset by the net effect of acquisitions of $0.9 billion, largely associated with Alstom . Excluding these items, industrial segment organic profit* decreased $0.8 billion.

• | Interest and other financial charges increased $ 0.3 billion, while GE Industrial income taxes decreased $ 0.5 billion. |

• | Foreign exchange adversely affected Industrial operating earnings by $0.3 billion in 2016. |

• | Financial Services losses decreased $6.7 billion, or 84%, primarily due to the nonrecurrence of the 2015 charges associated with the GE Capital Exit Plan. |

See Segment Results and Corporate Items & Eliminations sections within the MD&A for more information. Also, see the Other Consolidated Information section within the MD&A for a discussion of postretirement benefit plans costs, income taxes and geographic data.

*Non-GAAP Financial Measure

24 GE 2017 FORM 10-K

MD&A | CONSOLIDATED RESULTS | |

GE DIGITAL

GE Digital's activities are focused on assisting in the market development of our digital product offerings through software design, fulfillment and product management, while also interfacing with our customers. Digital revenues include internally developed software and associated hardware, including Predix and software solutions that improve our customers' asset performance. These revenues and associated costs are largely generated from our operating businesses and are included in their segment results.

Revenues were $4.0 billion for the year ended December 31, 2017, an increase of $0.4 billion or 12% compared to revenues of $3.6 billion for the year ended December 31, 2016. These increases were principally driven by Power, Renewable Energy and Non-GE Verticals. Revenues were $3.6 billion for the year ended December 31, 2016, an increase of $0.5 billion or 16% compared to revenues of $3.1 billion for the year ended December 31, 2015. These increases were principally driven by Power, Oil & Gas and Non-GE Verticals.

Orders were $5.2 billion for the year ended December 31, 2017, an increase of $1.1 billion or 27% compared to orders of $4.1 billion for the year ended December 31, 2016. These increases were principally driven by Oil & Gas, Non-GE Verticals, Power and Renewable Energy. Orders were $4.1 billion for the year ended December 31, 2016, an increase of $0.7 billion or 22% compared to orders of $3.3 billion for the year ended December 31, 2015. These increases were principally driven by Power, Oil & Gas, Non-GE Verticals and Renewable Energy.

SEGMENT OPERATIONS

REVENUES AND PROFIT

Segment revenues include revenues and other income related to the segment.

Segment profit is determined based on internal performance measures used by the Chief Executive Officer (CEO) to assess the performance of each business in a given period. In connection with that assessment, the CEO may exclude matters, such as charges for restructuring, rationalization and other similar expenses, acquisition costs and other related charges, technology and product development costs, certain gains and losses from acquisitions or dispositions, and litigation settlements or other charges, for which responsibility preceded the current management team. Subsequent to the Baker Hughes transaction, restructuring and other charges are included in the determination of segment profit for our Oil & Gas segment. See the Corporate Items and Eliminations section within this MD&A for additional information about costs excluded from segment profit.

Segment profit excludes results reported as discontinued operations and material accounting changes. Segment profit also excludes the portion of earnings or loss attributable to noncontrolling interests of consolidated subsidiaries, and as such only includes the portion of earnings or loss attributable to our share of the consolidated earnings or loss of consolidated subsidiaries.

Segment profit excludes or includes interest and other financial charges, income taxes, and preferred stock dividends according to how a particular segment's management is measured:

• | Interest and other financial charges, income taxes and GE preferred stock dividends are excluded in determining segment profit (which we sometimes refer to as "operating profit") for the industrial segments. |

• | Interest and other financial charges, income taxes and GE Capital preferred stock dividends are included in determining segment profit (which we sometimes refer to as "net earnings") for the Capital segment. |

Certain corporate costs, such as shared services, employee benefits, and information technology, are allocated to our segments based on usage. A portion of the remaining corporate costs is allocated based on each segment's relative net cost of operations.

SIGNIFICANT SEGMENT DEVELOPMENTS

INCLUSION OF ENERGY CONNECTIONS IN POWER REPORTING SEGMENT

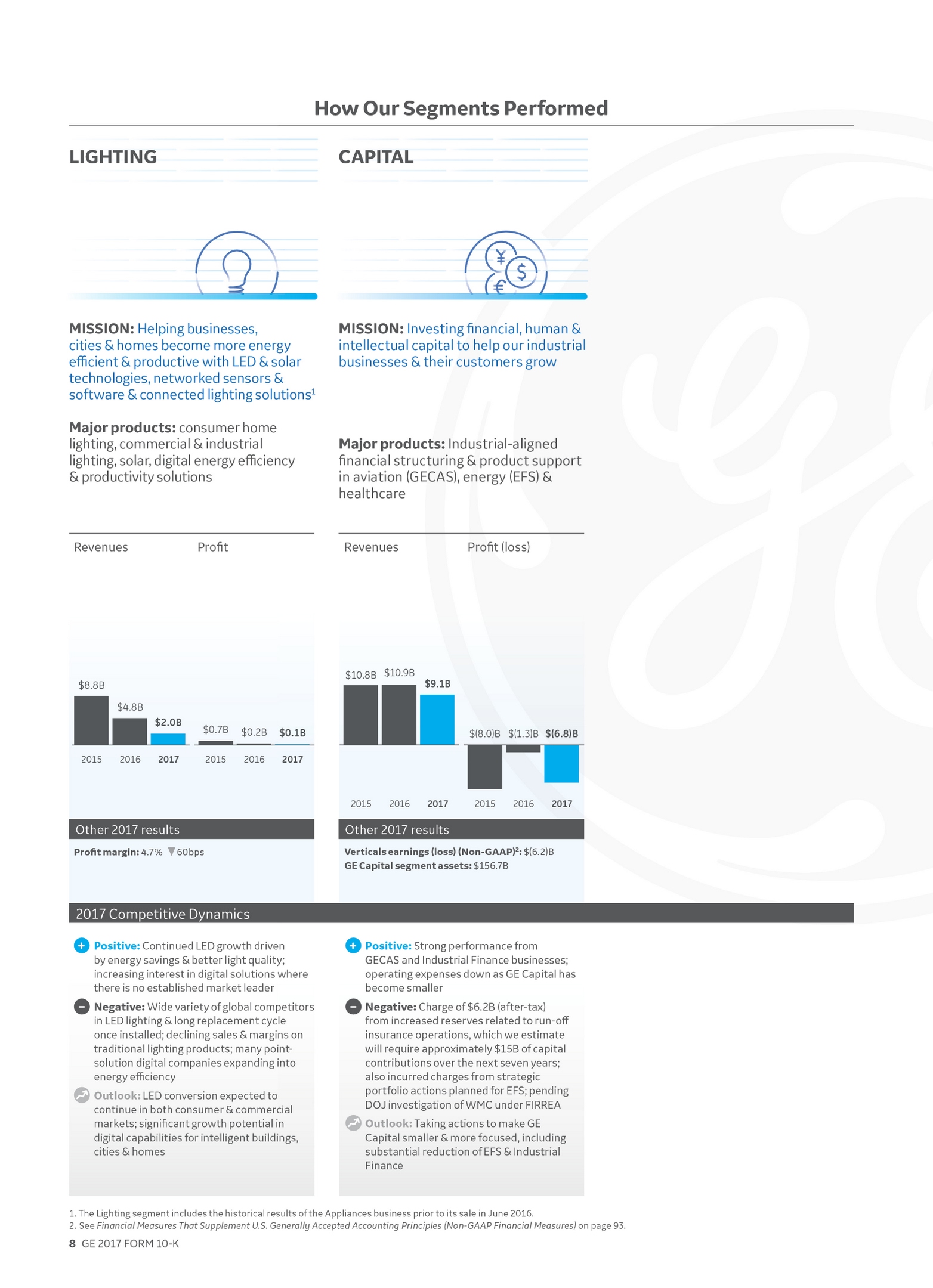

Beginning in the third quarter of 2017, the Energy Connections business within the former Energy Connections & Lighting segment was combined with the Power segment and presented as one reporting segment called Power. As a result of the combination, our GE Lighting and Current, powered by GE (Current) businesses are now reported as a separate segment called Lighting.

CLASSIFICATION OF THE SUBSTANTIAL MAJORITY OF OUR LIGHTING SEGMENT AS HELD FOR SALE

In the fourth quarter of 2017, we classified the substantial majority of our Lighting segment as held for sale. In connection with this determination, we adjusted the carrying value of each business classified as held for sale to fair value, less cost to sell, which resulted in a pre-tax loss of $0.8 billion. This loss has been recorded at Corporate.

GE 2017 FORM 10-K 25

MD&A | SEGMENT OPERATIONS |

|

SUMMARY OF OPERATING SEGMENTS | |||||||||||||||

|

|

|

|

|

| ||||||||||

| General Electric Company and consolidated affiliates | ||||||||||||||

(In millions) | 2017 | | 2016 | | 2015 | | 2014 | | 2013 | | |||||

|

|

|

|

|

| ||||||||||

Revenues |

|

|

|

|

| ||||||||||

Power | $ | 35,990 | | $ | 36,795 | | $ | 28,903 | | $ | 27,746 | | $ | 26,770 | |

Renewable Energy | 10,280 | | 9,033 | | 6,273 | | 6,399 | | 4,824 | | |||||

Oil & Gas | 17,231 | | 12,898 | | 16,450 | | 19,085 | | 17,341 | | |||||

Aviation | 27,375 | | 26,261 | | 24,660 | | 23,990 | | 21,911 | | |||||

Healthcare | 19,116 | | 18,291 | | 17,639 | | 18,299 | | 18,200 | | |||||

Transportation | 4,178 | | 4,713 | | 5,933 | | 5,650 | | 5,885 | | |||||

Lighting(a) | 1,987 | | 4,823 | | 8,751 | | 8,404 | | 8,338 | | |||||

Total industrial segment revenues | 116,157 | | 112,814 | | 108,609 | | 109,574 | | 103,269 | | |||||

Capital | 9,070 | | 10,905 | | 10,801 | | 11,320 | | 11,267 | | |||||

Total segment revenues | 125,227 | | 123,719 | | 119,410 | | 120,894 | | 114,536 | | |||||

Corporate items and eliminations | (3,135 | ) | (26 | ) | (2,024 | ) | (3,709 | ) | (1,292 | ) | |||||

Consolidated revenues | $ | 122,092 | | $ | 123,693 | | $ | 117,386 | | $ | 117,184 | | $ | 113,245 | |

|

|

|

|

|

| ||||||||||

Segment profit |

|

|

|

|

| ||||||||||

Power | $ | 2,786 | | $ | 5,091 | | $ | 4,772 | | $ | 4,731 | | $ | 4,437 | |

Renewable Energy | 727 | | 576 | | 431 | | 694 | | 485 | | |||||

Oil & Gas(b) | 220 | | 1,392 | | 2,427 | | 2,758 | | 2,357 | | |||||

Aviation | 6,642 | | 6,115 | | 5,507 | | 4,973 | | 4,345 | | |||||

Healthcare | 3,448 | | 3,161 | | 2,882 | | 3,047 | | 3,048 | | |||||

Transportation | 824 | | 1,064 | | 1,273 | | 1,130 | | 1,166 | | |||||

Lighting(a) | 93 | | 199 | | 674 | | 431 | | 381 | | |||||

Total industrial segment profit | 14,740 | | 17,598 | | 17,966 | | 17,764 | | 16,220 | | |||||

Capital | (6,765 | ) | (1,251 | ) | (7,983 | ) | 1,209 | | 401 | | |||||

Total segment profit | 7,975 | | 16,347 | | 9,983 | | 18,973 | | 16,621 | | |||||

Corporate items and eliminations | (7,871 | ) | (4,226 | ) | (5,108 | ) | (6,225 | ) | (6,002 | ) | |||||

GE interest and other financial charges | (2,753 | ) | (2,026 | ) | (1,706 | ) | (1,579 | ) | (1,333 | ) | |||||

GE provision for income taxes | (3,259 | ) | (967 | ) | (1,506 | ) | (1,634 | ) | (1,667 | ) | |||||

Earnings (loss) from continuing operations |

|

|

|

|

| ||||||||||

attributable to GE common shareowners | (5,907 | ) | 9,128 | | 1,663 | | 9,535 | | 7,618 | | |||||

Earnings (loss) from discontinued operations, net of taxes | (309 | ) | (954 | ) | (7,495 | ) | 5,855 | | 5,475 | | |||||

Less net earnings (loss) attributable to |

|

|

|

|

| ||||||||||

noncontrolling interests, discontinued operations | 6 | | (1 | ) | 312 | | 157 | | 36 | | |||||

Earnings (loss) from discontinued operations, |

|

|

|

|

| ||||||||||

net of taxes and noncontrolling interests | (315 | ) | (952 | ) | (7,807 | ) | 5,698 | | 5,439 | | |||||

Consolidated net earnings (loss) |

|

|

|

|

| ||||||||||

attributable to GE common shareowners | $ | (6,222 | ) | $ | 8,176 | | $ | (6,145 | ) | $ | 15,233 | | $ | 13,057 | |

(a) | Lighting segment included Appliances for the years ended December 31, 2013, 2014, 2015, and through its disposition in the second quarter of 2016. |

(b) | Subsequent to the Baker Hughes transaction, restructuring and other charges are included in the determination of segment profit for our Oil & Gas segment. Oil & Gas segment profit excluding restructuring and other charges* was $899 million for the year ended December 31, 2017. |

*Non-GAAP Financial Measure

26 GE 2017 FORM 10-K

MD&A | SEGMENT OPERATIONS |

|

SEGMENT RESULTS

INDUSTRIAL SEGMENT REVENUES |

|

|

| ||||||

(Dollars in billions) | 2017 | | 2016 | | 2015 | | |||

|

|

|

| ||||||

Revenues |

|

|

| ||||||

Equipment(a)(c) | $ | 58.5 | | $ | 60.6 | | $ | 60.9 | |

Services(b)(c) | 57.7 | | 52.3 | | 47.8 | | |||

Total(d) | $ | 116.2 | | $ | 112.8 | | $ | 108.6 | |

(a) | In 2017, $ 56.3 billion, excluding $ 2.2 billion related to Baker Hughes*. |

(b) | In 2017, $ 54.6 billion, excluding $ 3.1 billion related to Baker Hughes*. |

(c) | For the purposes of the MD&A, "services" refers to sales under product services agreements and sales of both goods (such as spare parts and equipment upgrades) and related services (such as monitoring, maintenance and repairs). For the purposes of the financial statement display of sales and costs of sales in our Statement of Earnings (Loss), "goods" is required by SEC regulations to include all sales of tangible products, and "services" must include all other sales, including other services activities. |

(d) | Industrial segment refers to the sum of our seven industrial reporting segments, without giving effect to corporate items or the elimination of transactions among such segments and between these segments and our Financial Services segment. Therefore, industrial segment revenues will not agree to GE revenues as shown in the Statement of Earnings (Loss). |

INDUSTRIAL SEGMENT PROFIT AND PROFIT MARGIN |

|

|

| ||||||

(Dollars in billions) | 2017 | | 2016 | | 2015 | | |||

|

|

|

| ||||||

Segment profit(a) | $ | 14.7 | | $ | 17.6 | | $ | 18.0 | |

Segment profit margin | 13.3 | % | 15.6 | % | 16.5 | % | |||

(a) | In 2017, $ 15.1 billion, excluding $ (0.4) billion related to Baker Hughes*. |

2017 – 2016 COMMENTARY | ||||

• | Industrial segment revenues increased $ 3.3 billion, or 3% , driven by increases at Oil & Gas primarily due to Baker Hughes, Renewable Energy, Aviation and Healthcare, partially offset by decreases at Power, Transportation and Lighting. |

• | Industrial segment profit decreased $ 2.9 billion, or 16% , primarily due to lower earnings at Power driven by negative variable cost productivity, Oil & Gas primarily due to restructuring costs associated with Baker Hughes, and Transportation driven by lower volume and negative variable cost productivity. These decreases were partially offset by higher earnings at Aviation, Healthcare, Renewable Energy and Lighting. |

• | Industrial segment margin decreased 230 basis points to 13.3% in 2017 from 15.6% in 2016 driven by negative cost productivity, price pressure and business mix. The decrease in industrial segment margin reflects decreases at Power, Oil & Gas and Transportation, offset by increases at Aviation, Renewable Energy, Healthcare and Lighting. |

2016 – 2015 COMMENTARY |

• | Industrial segment revenues increased $ 4.2 billion, or 4% , primarily driven by increases at Power and Renewable Energy, mainly due to the effects of the Alstom acquisition, as well as an organic* increase at Renewable Energy, partially offset by lower revenues at Oil & Gas and Transportation, including the effects of foreign currency exchange of $0.3 billion at Oil & Gas. |

• | Industrial segment acquisition revenues, driven by Alstom, were partially offset by the effects of disposition revenues related to the sale of Appliances in the second quarter of 2016 and sales of Meters, Intelligent Platforms Embedded Systems Products and Signaling businesses in 2015. |

• | Industrial segment profit decreased $0.4 billion, or 2%, mainly driven by lower earnings organically* at Oil & Gas, Lighting and Transportation, as well as an unfavorable impact of foreign exchange, partially offset by higher earnings at Aviation, Power, Healthcare and Renewable Energy. |

• | Industrial segment profit margin decreased 90 basis points to 15.6% in 2016 from 16.5% in 2015, primarily driven by the effects of Alstom results. Excluding Alstom*, industrial segment profit margin was 16.8%, compared with 17.0% in 2015, reflecting core decreases at Power, Oil & Gas and Lighting, that more than offset increases at Aviation, Healthcare and Transportation. |

*Non-GAAP Financial Measure

GE 2017 FORM 10-K 27

MD&A | SEGMENT OPERATIONS | POWER | |

POWER

BUSINESS OVERVIEW

Leader: Russell Stokes |

| Headquarters & Operations | ||

| • Senior Vice President, GE and President & CEO, GE Power • Over 20 years of service with General Electric |

|  | • 29% of total segment revenues • 31% of industrial segment revenues • 19% of industrial segment profit • Headquarters: Schenectady, NY • Serving customers in 150+ countries • Employees: approximately 83,500 |

Products & Services |