UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549-1004

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended August 31, 2016

or

¨ Transition Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

for the transition period from to

Commission File No. 1-13146

THE GREENBRIER COMPANIES, INC.

(Exact name of Registrant as specified in its charter)

| Oregon | 93-0816972 | |

| (State of Incorporation) | (I.R.S. Employer Identification No.) |

One Centerpointe Drive, Suite 200, Lake Oswego, OR 97035

(Address of principal executive offices)

(503) 684-7000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| (Title of Each Class) | (Name of Each Exchange on Which Registered) | |||

| Common Stock without par value | New York Stock Exchange | |||

| Securities registered pursuant to Section 12(g) of the Act: | ||||

| None | ||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes X No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15 (d) of the Act. Yes No X

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes X No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one)

Large accelerated filer X Accelerated filer Non-accelerated filer Smaller reporting company

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No X

Aggregate market value of the Registrant's Common Stock held by non-affiliates as of February 29, 2016 (based on the closing price of such shares on such date) was $684,081,392.

The number of shares outstanding of the Registrant's Common Stock on October 19, 2016 was 28,363,846 without par value.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the Registrant's definitive Proxy Statement prepared in connection with the Annual Meeting of Stockholders to be held on January 6, 2017 are incorporated by reference into Parts II and III of this Report.

THE GREENBRIER COMPANIES, INC.

FORM 10-K

TABLE OF CONTENTS

PAGE | ||||||

FORWARD-LOOKING STATEMENTS | 1 | |||||

PART I | ||||||

Item 1. | BUSINESS | 4 | ||||

Item 1A. | RISK FACTORS | 12 | ||||

Item 1B. | UNRESOLVED STAFF COMMENTS | 29 | ||||

Item 2. | PROPERTIES | 29 | ||||

Item 3. | LEGAL PROCEEDINGS | 30 | ||||

Item 4. | MINE SAFETY DISCLOSURES | 30 | ||||

PART II | ||||||

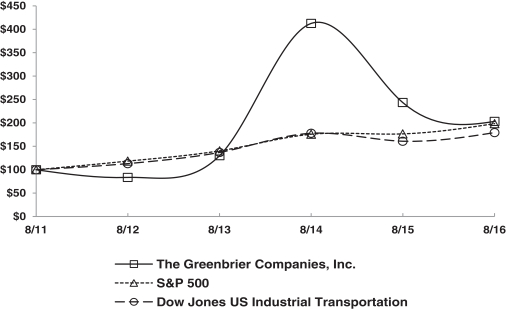

Item 5. | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES | 31 | ||||

Item 6. | SELECTED FINANCIAL DATA | 33 | ||||

Item 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 34 | ||||

Item 7A. | QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 49 | ||||

Item 8. | FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | 51 | ||||

Item 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 83 | ||||

Item 9A. | CONTROLS AND PROCEDURES | 83 | ||||

Item 9B. | OTHER INFORMATION | 86 | ||||

PART III | ||||||

Item 10. | DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE | 86 | ||||

Item 11. | EXECUTIVE COMPENSATION | 86 | ||||

Item 12. | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS | 86 | ||||

Item 13. | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE | 86 | ||||

Item 14. | PRINCIPAL ACCOUNTING FEES AND SERVICES | 86 | ||||

PART IV | ||||||

Item 15. | EXHIBITS AND FINANCIAL STATEMENT SCHEDULES | 87 | ||||

SIGNATURES | 91 | |||||

CERTIFICATIONS | 92 | |||||

| The Greenbrier Companies 2016 Annual Report |

Forward-Looking Statements

From time to time, The Greenbrier Companies, Inc. and its subsidiaries (Greenbrier or the Company) or their representatives have made or may make forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including, without limitation, statements as to expectations, beliefs and strategies regarding the future. Such forward-looking statements may be included in, but not limited to, press releases, oral statements made with the approval of an authorized executive officer or in various filings made by us with the Securities and Exchange Commission, including this filing on Form 10-K and in the Company's President's letter to stockholders that is typically distributed to the stockholders in conjunction with this Form 10-K and the Company's Proxy Statement. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. These forward-looking statements rely on a number of assumptions concerning future events and include statements relating to:

| • | availability of financing sources and borrowing base for working capital, other business development activities, capital spending and leased railcars for syndication (sale of railcars with lease attached); |

| • | ability to renew, maintain or obtain sufficient credit facilities and financial guarantees on acceptable terms; |

| • | ability to utilize beneficial tax strategies; |

| • | ability to grow our businesses; |

| • | ability to obtain lease and sales contracts which provide adequate protection against attempted modifications or cancellations, changes in interest rates and increased costs of materials and components; |

| • | ability to obtain adequate insurance coverage at acceptable rates; |

| • | ability to convert backlog of railcar orders and obtain and execute lease syndication commitments; |

| • | ability to obtain adequate certification and licensing of products; and |

| • | short-term and long-term revenue and earnings effects of the above items. |

The following factors, among others, could cause actual results or outcomes to differ materially from the forward-looking statements:

| • | fluctuations in demand for newly manufactured railcars or marine barges; |

| • | fluctuations in demand for wheels, repair services and parts; |

| • | delays in receipt of orders, risks that contracts may be canceled or modified during their term, not renewed, unenforceable or breached by the customer and that customers may not purchase the amount of products or services under the contracts as anticipated; |

| • | ability to maintain sufficient availability of credit facilities and to maintain compliance with or to obtain appropriate amendments to covenants under various credit agreements; |

| • | domestic and global economic conditions including such matters as embargoes or quotas; |

| • | global political or security conditions in the U.S., Europe, Latin America, the Gulf Cooperation Council (GCC) and other areas including such matters as terrorism, war, civil disruption and crime; |

| • | sovereign risk related to international governments that includes, but is not limited to, governments stopping payments, repudiating their contracts, nationalizing private businesses and assets or altering foreign exchange regulations; |

| • | growth or reduction in the surface transportation industry; |

| • | ability to maintain good relationships with our labor force, third party labor providers and collective bargaining units representing our direct and indirect labor force; |

| • | ability to maintain good relationships with our customers and suppliers; |

| • | ability to renew or replace expiring customer contracts on satisfactory terms; |

| • | ability to obtain and execute suitable lease contracts for leased railcars for syndication; |

| • | steel and specialty component price fluctuations and availability, scrap surcharges, steel scrap prices and other commodity price fluctuations and availability and their impact on product demand and margin; |

| • | delay or failure of acquired businesses or joint ventures, assets, start-up operations, or new products or services to compete successfully; |

| • | changes in product mix and the mix of revenue levels among reporting segments; |

| • | labor disputes, energy shortages or operating difficulties that might disrupt operations or the flow of cargo; |

| • | production difficulties and product delivery delays as a result of, among other matters, costs or inefficiencies associated with expansion, start-up, or changing of production lines or changes in production rates, |

| The Greenbrier Companies 2016 Annual Report | 1 |

equipment failures, changing technologies, transfer of production between facilities or non-performance of alliance partners, subcontractors or suppliers; |

| • | lower than anticipated lease renewal rates, earnings on utilization based leases or residual values for leased equipment; |

| • | discovery of defects in railcars or services resulting in increased warranty costs or litigation; |

| • | physical damage, business interruption or product or service liability claims that exceed our insurance coverage; |

| • | commencement of and ultimate resolution or outcome of pending or future litigation and investigations; |

| • | natural disasters or severe or unusual weather patterns that may affect either us, our suppliers or our customers; |

| • | loss of business from, or a decline in the financial condition of, any of the principal customers that represent a significant portion of our total revenues; |

| • | competitive factors, including introduction of competitive products, new entrants into certain of our markets, price pressures, limited customer base, and competitiveness of our manufacturing facilities and products; |

| • | industry overcapacity and our manufacturing capacity utilization; |

| • | decreases or write-downs in carrying value of inventory, goodwill, intangibles or other assets due to impairment; |

| • | severance or other costs or charges associated with lay-offs, shutdowns, or reducing the size and scope of operations; |

| • | changes in future maintenance or warranty requirements; |

| • | ability to adjust to the cyclical nature of the industries in which we operate; |

| • | changes in interest rates and financial impacts from interest rates; |

| • | ability and cost to maintain and renew operating permits; |

| • | actions or failures to act by various regulatory agencies including changing tank car or other rail car regulations; |

| • | potential environmental remediation obligations; |

| • | changes in commodity prices, including oil and gas; |

| • | risks associated with our intellectual property rights or those of third parties, including infringement, maintenance, protection, validity, enforcement and continued use of such rights; |

| • | expansion of warranty and product support terms beyond those which have traditionally prevailed in the rail supply industry; |

| • | availability of a trained work force at a reasonable cost and with reasonable terms of employment; |

| • | availability and/or price of essential raw materials, specialties or components, including steel castings, to permit manufacture of units on order; |

| • | failure to successfully integrate joint ventures or acquired businesses; |

| • | discovery of previously unknown liabilities associated with acquired businesses; |

| • | failure of or delay in implementing and using new software or other technologies; |

| • | the impact of cybersecurity risks and the costs of mitigating and responding to a data security breach; |

| • | ability to replace maturing lease and management services revenue and earnings with revenue and earnings from new commercial transactions, including new railcar leases, additions to the lease fleet and new management services contracts; |

| • | credit limitations upon our ability to maintain effective hedging programs; |

| • | financial impacts from currency fluctuations and currency hedging activities in our worldwide operations; |

| • | increased costs or other impacts due to changes in legislation, regulations or accounting pronouncements; and |

| • | fraud, misconduct by employees and potential exposure to liabilities under the Foreign Corrupt Practices Act and other anti-corruption laws and regulations. |

Any forward-looking statements should be considered in light of these factors. Words such as "anticipates," "believes," "forecast," "potential," "goal," "contemplates," "expects," "intends," "plans," "projects," "hopes," "seeks," "estimates," "could," "would," "will," "may," "can," "designed to," "foreseeable future" and similar expressions identify forward-looking statements. These forward-looking statements are not guarantees of future performance and are subject to risks and uncertainties that could cause actual results to differ materially from the results contemplated by the forward-looking statements. Many of the important factors that will determine these results and values are beyond our ability to control or predict. You are cautioned not to put undue reliance on any forward-looking statements. Except as otherwise required by law, we do not assume any obligation to update any forward-looking statements.

| 2 | The Greenbrier Companies 2016 Annual Report |

In assessing forward-looking statements contained herein, readers are urged to read carefully all cautionary statements contained in this Form 10-K, including, without limitation, those contained under the heading, "Risk Factors," contained in Part I, Item 1A of this Form 10-K.

All references to years refer to the fiscal years ended August 31 st unless otherwise noted.

The Greenbrier Companies is a registered trademark of The Greenbrier Companies, Inc. Gunderson, Maxi-Stack, Auto-Max and YSD are registered trademarks of Gunderson LLC.

| The Greenbrier Companies 2016 Annual Report | 3 |

PART I

| Item 1. | BUSINESS |

Introduction

We are one of the leading designers, manufacturers and marketers of railroad freight car equipment in North America and Europe. We manufacture railcars in Brazil through a strategic investment and are a manufacturer and marketer of marine barges in North America. Recently through our European manufacturing operations, we also began delivery of railcars for the Saudi Arabian market. We are a leading provider of wheel services, parts, leasing and other services to the railroad and related transportation industries in North America and a provider of railcar repair, refurbishment and retrofitting services in North America through a joint venture partnership. Through unconsolidated joint ventures we also produce rail castings, tank heads and other components.

We operate an integrated business model in North America that combines freight car manufacturing, wheel services, repair, refurbishment, retrofitting, component parts, leasing and fleet management services. Our model is designed to provide customers with a comprehensive set of freight car solutions utilizing our substantial engineering, mechanical and technical capabilities as well as our experienced commercial personnel. This model allows us to develop cross-selling opportunities and synergies among our various business segments and to enhance our margins. We believe our integrated model is difficult to duplicate and provides greater value for our customers.

We operate in four reportable segments: Manufacturing; Wheels & Parts; Leasing & Services; and GBW Joint Venture. Financial information about our business segments as well as geographic information is located in Note 19 Segment Information to our Consolidated Financial Statements.

The Greenbrier Companies, Inc., which was incorporated in Delaware in 1981, consummated a merger on February 28, 2006 with its affiliate, Greenbrier Oregon, Inc., an Oregon corporation, for the sole purpose of changing its state of incorporation from Delaware to Oregon. Greenbrier Oregon survived the merger and assumed the name, The Greenbrier Companies, Inc. Our principal executive offices are located at One Centerpointe Drive, Suite 200, Lake Oswego, Oregon 97035, our telephone number is (503) 684-7000 and our Internet website is located at http://www.gbrx.com .

Products and Services

Manufacturing

North American Railcar Manufacturing - We manufacture a broad array of railcar types in North America, which includes most railcar types other than coal cars. We have demonstrated an ability to capture high market shares in many of the car types we produce. The primary products we produce for the North American market are:

Intermodal Railcars – We manufacture a comprehensive range of intermodal railcars. Our most important intermodal product is our articulated double-stack railcar. The double-stack railcar is designed to transport containers stacked two-high on a single platform and provides significant operating and capital savings over other types of intermodal railcars.

Tank Cars – We produce a variety of tank cars, including both general and certain pressurized tank cars, which are designed for the transportation of products such as crude oil, ethanol, liquefied petroleum gas, caustic soda, urea ammonium nitrate, vegetable oils, bio-diesel and various other products and we continue to expand our product lines.

Automotive – We manufacture a full line of railcar equipment specifically designed for the transportation of automotive products. Our automotive offerings include our proprietary Auto-Max railcar, Multi-Max auto rack and flat cars for automotive transportation.

| 4 | The Greenbrier Companies 2016 Annual Report |

Conventional Railcars - We produce a wide range of boxcars, which are used in the transport of forest products, perishables, general merchandise and commodities. We also produce a variety of covered hopper cars for the grain, fertilizer, sand, cement and petrochemical industries as well as gondolas for the steel, metals and aggregate markets and various other conventional railcar types. Our flat car products include center partition cars for the forest products industry, bulkhead flat cars and solid waste service flat cars.

European Railcar Manufacturing - Our European manufacturing operation produces a variety of tank, automotive and conventional freight railcar (wagon) types, including a comprehensive line of pressurized tank cars for liquid petroleum gas and ammonia and non-pressurized tank cars for light oil, chemicals and other products. In addition, we produce flat cars, coil cars for the steel and metals market, coal cars, gondolas, sliding wall cars and automobile transporter cars for both the continental European and United Kingdom markets. In 2016, we began production of tank cars to support industrial mining operations for the Saudi Arabian market for delivery beginning in 2017.

Marine Vessel Fabrication - Our Portland, Oregon manufacturing facility, located on a deep-water port on the Willamette River, includes marine vessel fabrication capabilities. The marine facilities also increase utilization of steel plate burning and fabrication capacity providing flexibility for railcar production. United States (U.S.) coastwise law, commonly referred to as the Jones Act, requires all commercial vessels transporting merchandise between ports in the U.S. to be built, owned, operated and manned by U.S. citizens and to be registered under the U.S. flag. We manufacture a broad range of Jones Act ocean-going and river barges for transporting merchandise between ports within the U.S. including conventional deck barges, double-hull tank barges, railcar/deck barges, barges for aggregates and other heavy industrial products and dump barges. Our primary focus is on the larger ocean-going vessels although the facility has the capability to compete in other marine-related products.

Wheels & Parts

Wheel Services and Component Parts Manufacturing - We operate a large wheel services and component parts network in North America. Our wheel shops, operating in ten locations, provide complete wheel services including reconditioning of wheels and axles in addition to new axle machining and finishing and axle downsizing. Our component parts facilities, operating in four locations, recondition and manufacture railcar cushioning units, couplers, yokes, side frames, bolsters and various other parts. We also produce roofs, doors and associated parts for boxcars.

GBW Joint Venture

Railcar Repair, Refurbishment, Maintenance and Retrofitting - GBW Railcar Services LLC (GBW), an unconsolidated 50/50 joint venture, became our fourth reportable segment (GBW Joint Venture) upon formation in July 2014. The results of GBW are included as part of Earnings (loss) from unconsolidated affiliates as we account for our interest in GBW under the equity method of accounting. GBW operates the largest independent railcar repair shop network in North America consisting of over 30 Repair shops including more than 10 tank car repair shops certified by the Association of American Railroads (AAR). This network of Repair shops performs heavy railcar repair and refurbishment, as well as routine railcar maintenance for third parties, as well as for our leased and managed fleet.

Leasing & Services

Leasing - Our relationships with financial institutions, combined with our ownership of a lease fleet of approximately 8,900 railcars (6,600 railcars held as equipment on operating leases, 2,200 held as leased railcars for syndication and 100 held as finished goods inventory), enables us to offer flexible financing programs including operating leases and "by the mile" leases to our customers. In addition, we frequently originate leases of railcars, which are either newly built or refurbished by us, or buy railcars from the secondary market, and sell the railcars and attached leases to financial institutions and subsequently provide such institutions with management services under multi-year agreements. As an equipment owner and an originator of leases, we participate principally in the operating lease segment of the market. The majority of our leases are "full service" leases whereby we are responsible for maintenance and administration. Maintenance of the fleet is provided, in

| The Greenbrier Companies 2016 Annual Report | 5 |

part, through GBW. Assets from our owned lease fleet are periodically sold to take advantage of market conditions, manage risk and maintain liquidity.

Management Services - Our management services business offers a broad array of software and services that include railcar maintenance management, railcar accounting services (such as billing and revenue collection, car hire receivable and payable administration), total fleet management (including railcar tracking using proprietary software), administration and railcar remarketing. We currently own or provide management services for a fleet of approximately 273,000 railcars for railroads, shippers, carriers, institutional investors and other leasing and transportation companies in North America. In 2017, we formed our Regulatory Services Group which offers regulatory, engineering, process consulting and advocacy support to the tank car and petrochemical rail shipper community, among other services.

| Fleet Profile (1) As of August 31, 2016 | ||||||||||||

Owned Units (2) | Managed Units | Total Units | ||||||||||

Customer Profile: | ||||||||||||

Leasing Companies | 68 | 113,736 | 113,804 | |||||||||

Class I Railroads | 1,922 | 97,311 | 99,233 | |||||||||

Shipping Companies | 4,645 | 39,136 | 43,781 | |||||||||

Non-Class I Railroads | 915 | 13,981 | 14,896 | |||||||||

En route to Customer Location | 426 | 2 | 428 | |||||||||

Off-lease | 973 | – | 973 | |||||||||

| ||||||||||||

Total Units | 8,949 | 264,166 | 273,115 | |||||||||

| ||||||||||||

| (1) | Each platform of a railcar is treated as a separate unit. |

| (2) | The percentage of owned units on lease excluding newly manufactured railcars not yet on lease and a recent railcar portfolio acquisition was 91.0% at August 31, 2016 with an average remaining lease term of 2.5 years. The average age of owned units is 13 years. |

Backlog

Subsequent to August 31, 2016, we reached agreements to restructure certain railcar contracts for favorable financial and other considerations resulting in a reduction of approximately 1,200 units. The adjustment is reflected as of August 31, 2016. The following table depicts our reported third party railcar backlog in number of railcars and estimated future revenue value attributable to such backlog, at the dates shown:

| August 31, | ||||||||||||

| 2016 | 2015 | 2014 | ||||||||||

New railcar backlog units (1) | 27,500 | 41,300 | 31,500 | |||||||||

Estimated future revenue value (in millions) (2) | $ | 3,190 | $ | 4,710 | $ | 3,330 | ||||||

| (1) | Each platform of a railcar is treated as a separate unit. |

| (2) | Subject to change based on finalization of product mix. |

Our total manufacturing backlog of railcar units as of August 31, 2016 included 23,500 units for direct sales, 3,700 units intended for syndications to third parties with a lease attached and 300 units intended to be placed into our owned lease fleet.

Based on current production schedules, approximately 12,000 units in the August 31, 2016 backlog are scheduled for delivery in 2017. The balance of the production is scheduled for delivery in 2018 and beyond. Multi-year supply agreements are a part of rail industry practice. A portion of the orders included in backlog reflects an assumed product mix. Under terms of the orders, the exact mix will be determined in the future, which may impact the dollar amount of backlog. Marine backlog as of August 31, 2016 was $114 million compared to $52 million as of August 31, 2015.

Our backlog of railcar units and marine vessels is not necessarily indicative of future results of operations. Certain orders in backlog are subject to customary documentation and completion of terms. Customer orders

| 6 | The Greenbrier Companies 2016 Annual Report |

contain terms and conditions customary in the industry. Customers may attempt to cancel or modify orders in backlog. Historically, little variation has been experienced between the quantity ordered and the quantity actually delivered, though the timing of deliveries has been modified from time to time. Backlog as of August 31, 2016 includes an aggregate of 3,800 covered hopper railcars for use in energy related sand transportation; customers may seek to cancel, settle or modify a portion of these railcars. We cannot guarantee that our reported railcar backlog will convert to revenue in any particular period, if at all.

Customers

Our customers include railroads, leasing companies, financial institutions, shippers, carriers and transportation companies. We have strong, long-term relationships with many of our customers. We believe that our customers' preference for high quality products, our technological leadership in developing innovative products and competitive pricing of our railcars have helped us maintain our long-standing relationships with our customers.

In 2016, revenue from two customers, TTX Company (TTX) and CIT Group Inc. (CIT), accounted for approximately 31% of total revenue, 38% of Manufacturing revenue and 14% of Wheels & Parts revenue. No other customers accounted for greater than 10% of total revenue.

Raw Materials and Components

Our products require a supply of materials including steel and specialty components such as brakes, wheels and axles. Specialty components purchased from third parties represent a significant amount of the cost of most freight cars. Our customers often specify particular components and suppliers of such components. Although the number of alternative suppliers of certain specialty components has declined in recent years, there are at least two suppliers for these components.

Certain materials and components are periodically in short supply which could potentially impact production at our new railcar and refurbishment facilities. In an effort to mitigate shortages and reduce supply chain costs, we have entered into strategic alliances and multi-year arrangements for the global sourcing of certain materials and components, we operate a replacement parts business and we continue to pursue strategic opportunities to protect and enhance our supply chain. We periodically make advance purchases to avoid possible shortages of material due to capacity limitations of component suppliers, shipping and transportation delays and possible price increases.

In 2016, the top ten suppliers for all inventory purchases accounted for approximately 46% of total purchases. Amsted Rail Company, Inc. accounted for 21% of total inventory purchases in 2016. No other suppliers accounted for more than 10% of total inventory purchases. The Company believes it maintains good relationships with its suppliers.

Competition

There are currently six major railcar manufacturers competing in North America. In addition, a number of small manufacturers have recently entered the market. We believe that in Europe we are in the top tier of railcar manufacturers. European freight car manufacturers are largely located in central and eastern Europe where labor rates are lower and work rules are more flexible. In all railcar markets, we compete on the basis of quality, price, reliability of delivery, product design and innovation, reputation and customer service and support.

Competition in the marine industry is dependent on the type of product produced. There are two principal competitors that build product types similar to ours. We compete on the basis of experienced labor, launch ways capacity, quality, price and reliability of delivery.

Competition in the wheels & parts and repair businesses is dependent on the type of product or service provided. There are many competitors in the railcar repair and refurbishment business and an increasing number of competitors in the wheel services and other parts businesses. We compete primarily on the basis of quality, timeliness of delivery, customer service, location of shops, price and engineering expertise.

| The Greenbrier Companies 2016 Annual Report | 7 |

There are at least twenty institutions that provide railcar leasing and services similar to ours. Many of them are also customers that buy new railcars from our manufacturing facilities and used railcars from our lease fleet, as well as utilize our management services. Many of these institutions have greater resources than we do on our own balance sheet. We compete primarily on the basis of quality, price, delivery, reputation, service offerings and deal structuring and syndication ability. We believe our strong servicing capability and our ability to sell railcars with a lease attached (syndicate railcars), integrated with our manufacturing, repair shops, railcar specialization and expertise in particular lease structures provide a strong competitive position.

Marketing and Product Development

In North America, we use an integrated marketing and sales effort to coordinate relationships in our various segments. We provide our customers with a diverse range of equipment and financing alternatives designed to satisfy each customer's unique needs, whether the customer is buying new equipment, refurbishing existing equipment or seeking to outsource the maintenance or management of equipment. These custom programs may involve a combination of railcar products, leasing, refurbishing and remarketing services. In addition, we provide customized maintenance management, equipment management, accounting and compliance services and proprietary software solutions.

Outside of North America, we maintain relationships with customers through country-specific sales personnel. Our engineering and technical staff works closely with their customer counterparts on the design and certification of railcars. Many European railroads are state-owned and are subject to European Union (EU) regulations covering the tender of government contracts.

Through our customer relationships, insights are derived into the potential need for new products and services. Marketing and engineering personnel collaborate to evaluate opportunities and develop new products and features. For example, we continue to expand our tank car and covered hopper product offerings in North America. Research and development costs incurred during the years ended August 31, 2016, 2015 and 2014 were $2.7 million, $2.5 million and $3.6 million.

Patents and Trademarks

We have a number of U.S. and non-U.S. patents of varying duration, and pending patent applications, registered trademarks, copyrights and trade names that are important to our products and product development efforts. The protection of our intellectual property is important to our business and we have a proactive program aimed at protecting our intellectual property and the results from our research and development.

Environmental Matters

We are subject to national, state and local environmental laws and regulations concerning, among other matters, air emissions, wastewater discharge, solid and hazardous waste disposal and employee health and safety. Prior to acquiring facilities, we usually conduct investigations to evaluate the environmental condition of subject properties and may negotiate contractual terms for allocation of environmental exposure arising from prior uses. We operate our facilities in a manner designed to maintain compliance with applicable environmental laws and regulations. Environmental studies have been conducted on certain of our owned and leased properties that indicate additional investigation and some remediation on certain properties may be necessary.

Our Portland, Oregon manufacturing facility is located adjacent to the Willamette River. We have entered into a Voluntary Clean-up Agreement with the Oregon Department of Environmental Quality (DEQ) in which we agreed to conduct an investigation of whether, and to what extent, past or present operations at the Portland property may have released hazardous substances to the environment. We are also conducting groundwater remediation relating to a historical spill on the property that preceded our ownership.

Portland Harbor Site

In December 2000, the U.S. Environmental Protection Agency (EPA) classified portions of the Willamette River bed known as the Portland Harbor, including the portion fronting our manufacturing facility, as a federal

| 8 | The Greenbrier Companies 2016 Annual Report |

"National Priority List" or "Superfund" site due to sediment contamination (the Portland Harbor Site). We and more than 140 other parties have received a "General Notice" of potential liability from the EPA relating to the Portland Harbor Site. The letter advised us that we may be liable for the costs of investigation and remediation (which liability may be joint and several with other potentially responsible parties) as well as for natural resource damages resulting from releases of hazardous substances to the site. At this time, ten private and public entities, including us (the Lower Willamette Group or LWG), have signed an Administrative Order on Consent (AOC) to perform a remedial investigation/feasibility study (RI/FS) of the Portland Harbor Site under EPA oversight, and several additional entities have not signed such consent, but are nevertheless contributing money to the effort. The EPA-mandated RI/FS is being produced by the LWG and has cost over $110 million during a 15-year period. We have agreed to initially bear a percentage of the total costs incurred by the LWG in connection with the investigation. Our aggregate expenditure has not been material during the 15-year period. Some or all of any such outlay may be recoverable from other responsible parties.

Eighty-three parties, including the State of Oregon and the federal government, have entered into a non-judicial mediation process to try to allocate costs associated with the Portland Harbor site. Approximately 110 additional parties have signed tolling agreements related to such allocations. On April 23, 2009, we and the other AOC signatories filed suit against 69 other parties due to a possible limitations period for some such claims; Arkema Inc. et al v. A & C Foundry Products, Inc. et al , U.S. District Court, District of Oregon, Case #3:09-cv-453-PK. All but 12 of these parties elected to sign tolling agreements and be dismissed without prejudice, and the case has now been stayed by the court, pending the EPA's Record of Decision, currently scheduled by the EPA for December 31, 2016.

On June 8, 2016, the EPA issued its Feasibility Study (FS) and Proposed Plan for the Portland Harbor Site. The EPA accepted comments from the public on its Proposed Plan through September 6, 2016. The EPA's FS includes remediation alternatives that would take from 4 to 62 years of active remediation, with an estimated undiscounted cost ranging from $642 million to $10.2 billion and a net present value assuming a 7% discount rate ranging between $451 million and $9.4 billion. The Proposed Plan identifies the alternative currently favored by the EPA, which it assigns an estimated undiscounted cost of between $1.1 and $1.2 billion and a net present value of between $746 and $811 million. The EPA expects its cost estimates to be accurate within a range of +50 to -30 percent. EPA estimates that the remedy in the Proposed Plan would take 7 years of active remediation followed by 30 years of monitoring. The EPA's FS and its Proposed Plan identify 13 Sediment Decision Units. One of the units, RM9W, includes the nearshore area of the river sediments offshore of our Portland, Oregon manufacturing facility as well as upstream and downstream of the facility. It also includes a portion of our riverbank. Neither the FS nor the Proposed Plan breaks down total remediation costs by unit.

Neither the EPA's FS nor its Proposed Plan addresses responsibility for the costs of clean-up, allocates such costs among the potentially responsible parties, or defines precise boundaries for the cleanup. Responsibility for funding and implementing the EPA's selected cleanup option will be determined after the issuance of the Record of Decision, currently scheduled by the EPA for December 31, 2016. Based on the investigation to date, we believe that we did not contribute in any material way to contamination in the river sediments or the damage of natural resources in the Portland Harbor Site and that the damage in the area of the Portland Harbor Site adjacent to our property precedes its ownership of the Portland, Oregon manufacturing facility. Because these environmental investigations are still underway, sufficient information is currently not available to determine our liability, if any, for the cost of any required remediation or restoration of the Portland Harbor Site or to estimate a range of potential loss. Based on the results of the pending investigations and future assessments of natural resource damages, we may be required to incur costs associated with additional phases of investigation or remedial action, and may be liable for damages to natural resources. In addition, we may be required to perform periodic maintenance dredging in order to continue to launch vessels from its launch ways in Portland, Oregon, on the Willamette River, and the river's classification as a Superfund site could result in some limitations on future dredging and launch activities. Any of these matters could adversely affect our business and Consolidated Financial Statements, or the value of our Portland property.

We have also signed an Order on Consent with the DEQ to finalize the investigation of potential onsite sources of contamination that may have a release pathway to the Willamette River. Interim precautionary measures are also required in the order and we are currently discussing with the DEQ potential remedial actions which may be

| The Greenbrier Companies 2016 Annual Report | 9 |

required. Our aggregate expenditure has not been material, however we could incur significant expenses for remediation. Some or all of any such outlay may be recoverable from other responsible parties.

Regulation

The Federal Railroad Administration in the U.S. and Transport Canada in Canada administer and enforce laws and regulations relating to railroad safety. These regulations govern equipment and safety appliance standards for freight cars and other rail equipment used in interstate commerce. The AAR promulgates a wide variety of rules and regulations governing the safety and design of equipment, relationships among railroads and other railcar owners with respect to railcars in interchange, and other matters. The AAR also certifies railcar builders and component manufacturers that provide equipment for use on North American railroads. These regulations require us to maintain our certifications with the AAR as a railcar builder, repair and service provider and component manufacturer, and products sold and leased by us in North America must meet AAR, Transport Canada, and Federal Railroad Administration standards.

The primary regulatory and industry authorities involved in the regulation of the ocean-going barge industry are the U.S. Coast Guard, the Maritime Administration of the U.S. Department of Transportation, and private industry organizations such as the American Bureau of Shipping.

The regulatory environment in Europe consists of a combination of EU regulations and country specific regulations, including a harmonized set of Technical Standards for Interoperability of freight wagons throughout the EU.

Tank Car Regulation

On May 1, 2015 the U.S. Department of Transportation's Pipeline and Hazardous Materials Safety Administration (PHMSA) released new regulations related to new railcar manufacturing and retrofitting modification standards for tank cars in flammable liquids service (the PHMSA Rules). In December 2015, the U.S. Congress passed the Fixing America's Surface Transportation Act (FAST Act), which changed certain requirements of the PHMSA Rules. Under the PHMSA Rules as amended by the FAST Act, the deadlines for modifying or removing existing tank cars from flammables service currently range from January 2018 to May 2029, depending on the type of car and the type of commodity carried. Transport Canada, separately and concurrent with PHMSA, issued final rules on May 1, 2015, establishing new design standards for tank cars carrying flammable liquids in Canada. On July 25, 2016, Transport Canada announced that certain older tank cars, commonly referred to as "DOT 111" tank cars, must be removed from crude oil service effective October 31, 2016.

These regulatory changes, along with prevailing market conditions, could materially affect new tank railcar manufacturing and retrofitting activities industry-wide, and activities related to ownership and management of tank cars, including negative impacts to customer demand for products and services offered by Greenbrier and its related entities.

Employees

As of August 31, 2016, we had 9,418 full-time employees, consisting of 8,635 employees in Manufacturing, 545 in Wheels & Parts and 238 employees in Leasing & Services and corporate. In Manufacturing, 5,092 employees, all of whom are located in Mexico and Poland, are represented by unions. At our Wheels & Parts locations, 19 employees are represented by a union. We believe that our relations with our employees are generally good.

Additional Information

We are a reporting company and file annual, quarterly, current and special reports, proxy statements and other information with the Securities and Exchange Commission (SEC). Through a link on the Investor Relations section of our website, http://www.gbrx.com , we make available the following filings as soon as reasonably

| 10 | The Greenbrier Companies 2016 Annual Report |

practicable after they are electronically filed with or furnished to the SEC: our Annual Report on Form 10-K; Quarterly Reports on Form 10-Q; Current Reports on Form 8-K; and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended. All such filings are available free of charge. Copies of our Audit Committee Charter, Compensation Committee Charter, Nominating and Corporate Governance Committee Charter and the Company's Corporate Governance Guidelines are also available on our web site at http://www.gbrx.com . In addition, each of the reports and documents listed above are available free of charge by contacting our Investor Relations Department at The Greenbrier Companies, Inc., One Centerpointe Drive, Suite 200, Lake Oswego, Oregon 97035.

| The Greenbrier Companies 2016 Annual Report | 11 |

| Item 1A. | RISK FACTORS |

In addition to the risks outlined in this annual report under the heading "Forward-Looking Statements," as well as other comments included herein regarding risks and uncertainties, the following risk factors should be carefully considered when evaluating our company. Our business, financial condition or financial results could be materially and adversely affected by any of these risks.

During economic downturns or a rising interest rate environment, the cyclical nature of our business results in lower demand for our products and services and reduced revenue.

Our business is cyclical. Overall economic conditions and the purchasing practices of buyers have a significant effect upon our business due to the impact on demand for our products and services. As a result, during downturns, we could operate with a lower level of backlog and may slow down or halt production at some or all of our facilities. Economic conditions that result in higher interest rates increase the cost of new leasing arrangements, which could cause some of our leasing customers to lease fewer of our railcars or demand shorter lease terms. An economic downturn or increase in interest rates may reduce demand for our products and services, resulting in lower sales volumes, lower prices, lower lease utilization rates and decreased profits.

Currently, interest rates remain at historically low levels. Higher interest rates could increase the cost of, or potentially deter, new leasing arrangements with our customers, reduce our ability to syndicate railcars under lease to financial institutions, or impact the sales price we may receive on such syndications, any of which could materially adversely affect our business, financial condition and results of operations.

A change in our product mix due to shifts in demand could have an adverse effect on our profitability.

We manufacture and, through GBW, repair a variety of railcars. The demand for specific types of these railcars and mix of refurbishment work varies from time to time. These shifts in demand could affect our revenue and margins and could have an adverse effect on our profitability.

A prolonged decline in performance of the rail freight industry would have an adverse effect on our financial condition and results of operations.

Our future success depends in part upon the performance of the rail freight industry, which in turn depends on the health of the economy. If railcar loadings, railcar and railcar components replacement rates or refurbishment rates or industry demand for our railcar products weaken or otherwise do not materialize, if railcar transportation becomes more efficient from an increase in velocity or a decrease in dwell times, or if the rail freight industry becomes oversupplied, our financial condition and results of operations would be adversely affected.

Our backlog is not necessarily indicative of the level of our future revenues.

Our manufacturing backlog represents future production for which we have written orders from our customers in various periods, and estimated potential revenue attributable to those orders. Some of this backlog is subject to certain conditions, including potential adjustment to prices due to changes in prevailing market prices, or due to lower prices for new orders accepted by us from other customers for similar cars on similar terms and conditions during relevant time periods. Our reported backlog may not be converted to revenue in any particular period and some of our contracts permit cancellations with limited compensation that would not replace lost revenue or margins. In addition, some customers may attempt to cancel or modify a contract even if the contract does not allow for such cancellation or modification, and we may not be able to recover all revenue or earnings lost due to a breach of contract. The likelihood of attempted cancellations or modifications of contracts generally increases during periods of market weakness. Actual revenue from such contracts may not equal our anticipated revenues based on our backlog, and therefore, our backlog is not necessarily indicative of the level of our future revenues.

A portion of our backlog and Leased railcars for syndication relates to the energy sector. A decline in energy prices could negatively impact the creditworthiness of our customers, lead to attempted modifications or

| 12 | The Greenbrier Companies 2016 Annual Report |

cancellations of contracts or negatively impact our ability to syndicate our railcars, all of which could materially adversely affect our business, financial condition and results of operations. Backlog as of August 31, 2016 includes an aggregate of 3,800 covered hopper railcars for use in energy related sand transportation; customers may seek to cancel, settle or modify a portion of these railcars. We cannot guarantee that our reported railcar backlog will convert to revenue in any particular period, if at all.

We derive a significant amount of our revenue from a limited number of customers, the loss of or reduction of business from one or more of which could have an adverse effect on our business.

A significant portion of our revenue is generated from a few major customers. Although we have some long-term contractual relationships with our major customers, we cannot be assured that our customers will continue to use our products or services or that they will continue to do so at historical levels. A reduction in the purchase or leasing of our products or a termination of our services by one or more of our major customers could have an adverse effect on our business and operating results.

We could be unable to lease railcars at satisfactory rates, remarket leased railcars on favorable terms upon lease termination or realize the expected residual values upon lease termination, which could reduce our revenue and decrease our overall return or effect our ability to sell leased assets in the future.

The profitability of our railcar leasing business depends on our ability to lease railcars to our customers at satisfactory rates, and to re-market or sell railcars we own or manage upon the expiration of existing lease terms. The total rental payments we receive under our operating leases do not fully amortize the acquisition costs of the leased equipment, which exposes us to risks associated with remarketing the railcars. Our ability to lease or remarket leased railcars profitably is dependent upon several factors, including, but not limited to, market and industry conditions, cost of and demand for competing used or newer models, costs associated with the refurbishment of the railcars, market demand or governmental mandate for refurbishment, and interest rates. A downturn in the industries in which our lessees operate and decreased demand for railcars could also increase our exposure to re-marketing risk because lessees may demand shorter lease terms, requiring us to re-market leased railcars more frequently. Furthermore, the resale market for previously leased railcars has a limited number of potential buyers. From 2014 to 2016, the percentage of railcars in the fleet on lease has declined from approximately 98% to 91%. Our inability to lease, re-market or sell leased railcars on favorable terms could result in reduced revenues and margins or net gain on disposition of equipment and decrease our overall returns and affect our ability to syndicate railcars to investors.

Risks related to our operations outside of the U.S. could adversely affect our operating results.

Our current operations outside of the U.S. and any future expansion of our international operations are subject to the risks associated with cross-border business transactions and activities. Political, legal, trade, financial market or economic changes or instability could limit or curtail our foreign business activities and operations. Some foreign countries in which we operate or may operate have regulatory authorities that regulate railroad safety, railcar design and railcar component part design, performance and manufacturing. If we fail to obtain and maintain certifications of our railcars and railcar parts within the various foreign countries where we operate or may operate, we may be unable to market and sell our railcars in those countries. In addition, unexpected changes in regulatory requirements, tariffs and other trade barriers, more stringent rules relating to labor or the environment, adverse tax consequences and currency and price exchange controls could limit operations and make the manufacture and distribution of our products difficult. The uncertainty of the legal environment or geo-political risks in these and other areas could limit our ability to enforce our rights effectively. Because we have operations outside the U.S., we could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-corruption laws. We operate in parts of the world that have experienced governmental corruption to some degree, and in certain circumstances, strict compliance with anti-corruption laws may conflict with local customs and practices. The failure to comply with laws governing international business practices may result in substantial penalties and fines. Any international expansion or acquisition that we undertake could amplify these risks related to operating outside of the U.S.

| The Greenbrier Companies 2016 Annual Report | 13 |

In addition, in 2015, we began to establish a presence in the GCC region and Latin America and are exploring market opportunities in Eastern Europe and other emerging markets. Our development of customer relationships in these areas may expose us to certain additional risks, including, but not limited to, the following:

| • | Ongoing instability or changes in a country's or region's economic or political conditions, including inflation, recession, currency fluctuations and actual or anticipated civil and political unrest, terrorist actions, armed hostilities, kidnapping and extortion; |

| • | Longer payment cycles and difficulty in collecting accounts receivable; |

| • | Sovereign risk related to international governments that include, but may not be limited to, governments stopping payments or repudiating their contracts, nationalizing private businesses and assets or altering foreign exchange regulations; |

| • | Renegotiation or nullification of existing contracts; |

| • | An inability to effectively protect intellectual property; |

| • | Uncertainties arising from local business practices, cultural considerations and international political and trade tensions; and |

| • | Our limited knowledge of this market or our inability to protect our interests. |

If we are unable to successfully manage the risks associated with our global business, our results of operations, financial condition, liquidity and cash flows may be negatively impacted.

We may pursue strategic opportunities, including new joint ventures, acquisitions and new business endeavors that involve inherent risks, any of which may cause us not to realize anticipated benefits and we could have difficulty integrating the operations of any companies that we acquire or joint ventures we enter into, which could adversely affect our results of operations.

We may not be able to successfully identify suitable joint venture, acquisition and new business endeavors or complete these transactions on acceptable terms. Our identification of suitable joint venture opportunities, acquisition candidates and new business endeavors involve risks inherent in assessing the values, strengths, weaknesses, risks and profitability of these opportunities. Our failure to identify suitable joint ventures, acquisition opportunities and new business endeavors may restrict our ability to grow our business. If we are successful in pursuing such opportunities, we may be required to expend significant funds or incur additional debt, which could materially adversely affect our results of operations and limit our ability to obtain financing for working capital or other purposes and we may be more vulnerable to economic downturns and competitive pressures.

The success of our acquisition and joint venture strategy depends upon our ability to successfully complete acquisitions, to enter into joint ventures and integrate any businesses that we acquire into our existing business. The integration of acquired business operations could disrupt our business by causing unforeseen operating difficulties, diverting management's attention from day-to-day operations and requiring significant financial resources that would otherwise be used for the ongoing development of our business. The difficulties of integration could be increased by the necessity of coordinating geographically dispersed organizations, integrating personnel with disparate business backgrounds and combining different corporate cultures. Each of these circumstances could be more likely to occur or more severe in consequence in the case of an acquisition or joint venture involving a business that is outside of our core areas of expertise. In addition, we could be unable to retain key employees or customers of the combined businesses. We could face integration issues pertaining to the internal controls, information systems and operational functions of the acquired companies and we also could fail to realize cost efficiencies or synergies that we anticipated when selecting our acquisition candidates and joint ventures. Any of these items could adversely affect our results of operations.

Our relationships with our joint venture and alliance partners could be unsuccessful, which could adversely affect our business.

We have entered into several joint venture agreements and other alliances with other companies to increase our sourcing alternatives, reduce costs, to produce new railcars and repair and retrofit railcars. We may seek to

| 14 | The Greenbrier Companies 2016 Annual Report |

expand our relationships or enter into new agreements with other companies. If our joint venture or alliance partners are unable to fulfill their contractual obligations or if these relationships are otherwise not successful in the future, our manufacturing and other costs could increase, we could encounter production disruptions, growth opportunities could fail to materialize, or we could be required to fund such joint venture or alliances in amounts significantly greater than initially anticipated, any of which could adversely affect our business.

If any of our joint ventures generate significant losses, including future potential intangible asset or goodwill impairment charges, it could adversely affect our results of operations or cause our investment to be impaired.

We have potential exposure to environmental liabilities, which could increase costs or have an adverse effect on results of operations.

We are subject to extensive national, state, provincial and local environmental laws and regulations concerning, among other things, air emissions, water discharge, solid waste and hazardous substances handling and disposal and employee health and safety. These laws and regulations are complex and frequently change. We could incur unexpected costs, penalties and other civil and criminal liability if we fail to comply with environmental laws or permits issued to us pursuant to those laws. We also could incur costs or liabilities related to off-site waste disposal or remediating soil or groundwater contamination at our properties, including these set forth below and in the "Environmental Matters" section of this Report. In addition, future environmental laws and regulations may require significant capital expenditures or changes to our operations.

In addition to environmental, health and safety laws, the transportation of commodities by railcar raises potential risks in the event of a derailment or other accident. Generally, liability under existing law in the U.S. and Canada for accidents such as derailments depends on the negligence of the party. However, for certain hazardous commodities being shipped, strict liability concepts may apply.

Our Portland, Oregon manufacturing facility is located adjacent to the Willamette River. We have entered into a Voluntary Cleanup Agreement with the Oregon Department of Environmental Quality (DEQ) in which we agreed to conduct an investigation of whether, and to what extent, past or present operations at the Portland property may have released hazardous substances to the environment. We are also conducting groundwater remediation relating to a historical spill on the property which preceded our ownership.

The U.S. Environmental Protection Agency (EPA) has classified portions of the river bed of the Portland Harbor, including the portion fronting the Company's manufacturing facility, as a federal "National Priority List" or "Superfund" site due to sediment contamination (the Portland Harbor Site). We, along with more than 140 other parties, have received a "General Notice" of potential liability from the EPA relating to the Portland Harbor Site. The letter advised us that we may be liable for the costs of investigation and remediation (which liability may be joint and several with other potentially responsible parties) as well as for natural resource damages resulting from releases of hazardous substances to the site. We are part of a group that signed an Administrative Order on Consent (AOC) to perform a remedial investigation/feasibility study (RI/FS) of the Portland Harbor Site under EPA oversight, and several additional entities have not signed such consent, but are nevertheless contributing money to the effort. We have agreed to initially bear a percentage of the total costs incurred in connection with the investigation. We cannot provide assurance that any such costs will be recoverable from third parties.

On June 8, 2016, the EPA issued its Feasibility Study (FS) and Proposed Plan for the Portland Harbor Site. The EPA accepted comments from the public on its Proposed Plan through September 6, 2016. The EPA's FS includes remediation alternatives that would take from 4 to 62 years of active remediation, with an estimated undiscounted cost ranging from $642 million to $10.2 billion and a net present value assuming a 7% discount rate ranging between $451 million and $9.4 billion. The Proposed Plan identifies the alternative currently favored by the EPA, which it assigns an estimated undiscounted cost of between $1.1 and $1.2 billion and a net present value of between $746 and $811 million. The EPA expects its cost estimates to be accurate within a range of +50 to -30 percent. The EPA estimates that the remedy in the Proposed Plan would take 7 years of active remediation followed by 30 years of monitoring. The EPA's FS and its Proposed Plan identify 13 Sediment Decision Units. One of the units, RM9W, includes the nearshore area of the river sediments offshore of our Portland,

| The Greenbrier Companies 2016 Annual Report | 15 |

Oregon manufacturing facility as well as upstream and downstream of the facility. It also includes a portion of our riverbank. Neither the FS nor the Proposed Plan breaks down total remediation costs by unit. Neither the feasibility study nor the Proposed Plan addresses responsibility for the costs of clean-up or allocates such costs among potentially responsible parties. Responsibility for funding and implementing the EPA's selected cleanup option will be determined after the issuance of the Record of Decision, which is scheduled for December 31, 2016.

We have also signed an Order on Consent with the DEQ to finalize the investigation of potential onsite sources of contamination that may have a release pathway to the Willamette River. Interim precautionary measures are also required in the order and we are currently discussing with the DEQ potential remedial actions which may be required. Our aggregate expenditure has not been material during the 14-year period, however, we could incur significant expenses for remediation. Some or all of any such outlay may be recoverable from other responsible parties. However, we cannot assure that any such costs will be recoverable from third parties.

Because these environmental investigations are still underway, sufficient information is currently not available to determine our liability, if any, for the cost of any required remediation of the Portland Harbor Site on our adjacent land or to estimate a range of potential loss. Based on the results of the pending investigations and future assessments of natural resource damages, we may be required to incur costs associated with additional phases of investigation or remedial action, and may be liable for damages to natural resources. In addition, we may be required to perform periodic maintenance dredging in order to continue to launch vessels from our launch ways in Portland, Oregon, on the Willamette River, and the river's classification as a Superfund site could result in some limitations on future dredging and launch activities. Any of these matters could adversely affect our business and Consolidated Financial Statements, or the value of our Portland property.

The timing of our asset sales and related revenue recognition could cause significant differences in our quarterly results and liquidity.

We may build railcars or marine barges in anticipation of a customer order, or that are leased to a customer and ultimately planned to be sold to a third party. The difference in timing of production and the ultimate sale is subject to risk. In addition, we periodically sell railcars from our own lease fleet and the timing and volume of such sales is difficult to predict. As a result, comparisons of our manufacturing revenue, deliveries, quarterly net gain on disposition of equipment, income and liquidity between quarterly periods within one year and between comparable periods in different years may not be meaningful and should not be relied upon as indicators of our future performance.

We depend on our senior management team and other key employees, and significant attrition within our management team or unsuccessful succession planning for members of our senior management team and other key employees who are at or nearing retirement age, could adversely affect our business.

Our success depends in part on our ability to attract, retain and motivate senior management and other key employees. Achieving this objective may be difficult due to many factors, including fluctuations in global economic and industry conditions, competitors' hiring practices, cost reduction activities, and the effectiveness of our compensation programs. Competition for qualified personnel can be very intense. We must continue to recruit, retain and motivate senior management and other key employees sufficient to maintain our current business and support our future projects. We are vulnerable to attrition among our current senior management team and other key employees. A loss of any such personnel, or the inability to recruit and retain qualified personnel in the future, could have an adverse effect on our business, financial condition and results of operations.

Many members of our senior management team and other key employees are at or nearing retirement age. If we are unsuccessful in our succession planning efforts, the continuity of our business and results of operations could be adversely affected.

| 16 | The Greenbrier Companies 2016 Annual Report |

The rail freight industry could become oversupplied and the use of railcars as a significant mode of transporting freight could decline, become more efficient over time, experience a shift in types of modal transportation, and/or certain railcar types could become obsolete.

The rail freight industry could become oversupplied due to overbuilding which could have a significant impact on the demand for new railcars. In addition, if railcar transportation becomes more efficient from an increase in velocity or a decrease in idle times coupled with lower freight volumes, some of which may be permanent due to a reduction in coal volumes, this could significantly reduce the demand for our products and could adversely affect our results of operations. As the freight transportation markets we serve continue to evolve and become more efficient, the use of railcars may decline in favor of other more economic modes of transportation. Features and functionality specific to certain railcar types could result in those railcars becoming obsolete as customer requirements for freight delivery change. Our operations may be adversely impacted by changes in the preferred method used by customers to ship their products or changes in demand for particular products. The industries in which our customers operate are driven by dynamic market forces and trends, which are in turn influenced by economic and political factors. Demand for our railcars may be significantly affected by changes in the markets in which our customers operate. A significant reduction in customer demand for transportation or manufacture of a particular product or change in the preferred method of transportation used by customers to ship their products could result in the economic obsolescence of our railcars, including those leased by our customers.

We face aggressive competition by a concentrated group of competitors and a number of factors may influence our performance. If we are unable to compete successfully, our market share, margin and results of operations may be adversely affected.

We face aggressive competition by a concentrated group of competitors in all geographic markets and in each area of our business. In addition, several companies have recently attempted to enter the market. The railcar manufacturing and repair industry is intensely competitive and we expect it to remain so in the foreseeable future. Competitive factors, including introduction of competitive products, new entrants into certain of our markets, price pressures, limited customer base and the relative competitiveness of our manufacturing facilities and products affect our ability to compete effectively. In addition, new technologies or the introduction of new railcars or other product offerings by our competitors could render our products obsolete or less competitive. If we do not compete successfully, our market share, margin and results of operation may be adversely affected.

A number of factors may influence our performance, including without limitation: fluctuations in the demand for newly manufactured railcars or marine barges; fluctuations in demand for wheels, repair and parts; our ability to adjust to the cyclical nature of the industries in which we operate; delays in receipt of orders, risks that contracts may be canceled during their term or not renewed and that customers may not purchase the amount of products or services under the contracts as anticipated; our customers may be financially unable to pay for products and services already provided; domestic and global economic conditions including such matters as embargoes or quotas; growth or reduction in the surface transportation industry; steel and specialty component price fluctuations and availability, scrap surcharges, steel scrap prices and other commodity price fluctuations and their impact on product demand and margin; loss of business from, or a decline in the financial condition of, any of the principal customers that represent a significant portion of our total revenues; industry overcapacity and our manufacturing capacity utilization; and other risks, uncertainties and factors. If we are unfavorably affected by any of these factors, our market share, margin and results of operation may be adversely affected.

Changes in the credit markets and the financial services industry could negatively impact our business, results of operations, financial condition or liquidity.

The credit markets and the financial services industry may experience volatility which can result in tighter availability of credit on more restrictive terms and limit our ability to sell railcar assets. Our liquidity, financial condition and results of operations could be negatively impacted if our ability to borrow money to finance operations, obtain credit from trade creditors, offer leasing products to our customers or sell railcar assets were to be impaired. In addition, scarcity of capital could also adversely affect our customers' ability to purchase or pay for products from us or our suppliers' ability to provide us with product, either of which could negatively affect our business and results of operations.

| The Greenbrier Companies 2016 Annual Report | 17 |

Exposure to fluctuations in commodity and energy prices may impact our results of operations.

Fluctuations in commodity and energy prices, including crude oil and gas prices, could negatively impact the activities of our customers resulting in a corresponding adverse effect on the demand for our products and services. These shifts in demand could affect our results of operations and could have an adverse effect on our profitability. Demand for railcars that are used to transport crude oil and other energy related products is dependent on the demand for these commodities. Prices for oil and gas are subject to large fluctuations in response to relatively minor changes in the supply of, and demand for, oil and gas, market uncertainty and a variety of other economic factors that are beyond our control.

In recent years, oil and gas prices and, therefore, the level of exploration, development and production activity, have experienced significant fluctuations. Worldwide economic, political and military events, including war, terrorist activity, events in the Middle East and initiatives by the Organization of the Petroleum Exporting Countries (OPEC), have contributed, and are likely to continue to contribute, to price and volume volatility. Increasing global supply of oil in conjunction with weakening demand from slowing economic growth in Europe and Asia and increased fuel-efficiency has created downward pressure on crude oil prices.

Volatility in the global financial markets may adversely affect our business, financial condition and results of operation.

During periods of volatility in the global financial markets, certain of our customers could delay or otherwise reduce their purchases of railcars and other products and services. If volatile conditions in the global credit markets impact our customers' access to credit, product order volumes may decrease or customers may default on payments owed to us.

Likewise, if our suppliers face challenges obtaining credit, or otherwise operating their businesses, the supply of materials we purchase from them to manufacture our products may be interrupted. Any of these conditions or events could result in reductions in our revenues, increased price competition, or increased operating costs, which could adversely affect our business, financial condition and results of operations.

On June 23, 2016, the United Kingdom (UK) held a non-binding advisory referendum in which voters voted for the UK to exit the EU (Brexit). Brexit has caused volatility in global stock markets and currency exchange rate fluctuations, including the strengthening of the U.S. dollar against foreign currencies. Brexit may create further uncertainty in European and worldwide markets, which may cause our customers or potential customers to delay or reduce spending on our products or services, and may limit our suppliers' access to credit. Any of these effects of Brexit, among others, could negatively impact our business, results of operations and financial condition.

Our actual results may differ significantly from our announced strategic initiatives.