UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

| (Mark One) | ||

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

to Commission File No. 1-10299 FOOT LOCKER, INC.(Exact name of Registrant as specified in its charter)

| New York | 13-3513936 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 112 West 34 th Street, New York, New York | 10120 | |

| (Address of principal executive offices) | (Zip Code) |

| Title of each class | Name of each exchange on which registered | |

| Common Stock, par value $0.01 | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

| Number of shares of Common Stock outstanding at March 21, 2011: | 154,717,295 | |||

| The aggregate market value of voting stock held by non-affiliates of the Registrant computed by reference to the closing price as of the last business day of the Registrant's most recently completed second fiscal quarter, July 30, 2010, was approximately: | $ | 1,617,588,691* | ||

| * | For purposes of this calculation only (a) all directors plus one executive officer and owners of five percent or more of the Registrant are deemed to be affiliates of the Registrant and (b) shares deemed to be "held" by such persons include only outstanding shares of the Registrant's voting stock with respect to which such persons had, on such date, voting or investment power. |

Portions of the Registrant's definitive Proxy Statement (the "Proxy Statement") to be filed in connection with the Annual Meeting of Shareholders to be held on May 18, 2011: Parts III and IV.

TABLE OF CONTENTS

| PART I | |||||

Item 1 Business | 1 | ||||

Item 1A Risk Factors | 2 | ||||

Item 1B Unresolved Staff Comments | 9 | ||||

Item 2 Properties | 9 | ||||

Item 3 Legal Proceedings | 9 | ||||

Item 4 [Removed and Reserved] | 10 | ||||

| PART II | |||||

Item 5 Market for the Company's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 11 | ||||

Item 6 Selected Financial Data | 12 | ||||

Item 7 Management's Discussion and Analysis of Financial Condition and Results of Operations | 13 | ||||

Item 7A Quantitative and Qualitative Disclosures About Market Risk | 30 | ||||

Item 8 Consolidated Financial Statements and Supplementary Data | 30 | ||||

Item 9 Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 65 | ||||

Item 9A Controls and Procedures | 65 | ||||

Item 9B Other Information | 67 | ||||

| PART III | |||||

Item 10 Directors, Executive Officers and Corporate Governance | 67 | ||||

Item 11 Executive Compensation | 67 | ||||

Item 12 Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 67 | ||||

Item 13 Certain Relationships and Related Transactions, and Director Independence | 67 | ||||

Item 14 Principal Accounting Fees and Services | 67 | ||||

| PART IV | |||||

Item 15 Exhibits and Financial Statement Schedules | 68 | ||||

PART I

| Item 1. | Business |

Foot Locker, Inc., incorporated under the laws of the State of New York in 1989, is a leading global retailer of athletic footwear and apparel, operating 3,426 primarily mall-based stores in the United States, Canada, Europe, Australia, and New Zealand as of January 29, 2011. Foot Locker, Inc. and its subsidiaries hereafter are referred to as the "Registrant," "Company," "we," "our," or "us." Information regarding the business is contained under the "Business Overview" section in "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations."

The Company maintains a website on the Internet at www.footlocker-inc.com . The Company's filings with the Securities and Exchange Commission, including its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports are available free of charge through this website as soon as reasonably practicable after they are filed with or furnished to the SEC by clicking on the "SEC Filings" link. The Corporate Governance section of the Company's corporate website contains the Company's Corporate Governance Guidelines, Committee Charters, and the Company's Code of Business Conduct for directors, officers and employees, including the Chief Executive Officer, Chief Financial Officer, and Chief Accounting Officer. Copies of these documents may also be obtained free of charge upon written request to the Company's Corporate Secretary at 112 West 34 th Street, New York, NY 10120. The Company intends to promptly disclose amendments to the Code of Business Conduct and waivers of the Code for directors and executive officers on the Corporate Governance section of the Company's corporate website.

Information Regarding Business Segments and Geographic AreasThe financial information concerning business segments, divisions and geographic areas is contained under the "Business Overview" and "Segment Information" sections in "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations." Information regarding sales, operating results and identifiable assets of the Company by business segment and by geographic area is contained under the Segment Information note in "Item 8. Consolidated Financial Statements and Supplementary Data."

The service marks and trademarks appearing on this page and elsewhere in this report (except for Nike, Inc., Alshaya Trading Co. W.L.L., and Northern Group) are owned by Foot Locker, Inc. or its subsidiaries.

EmployeesThe Company and its consolidated subsidiaries had 12,688 full-time and 25,319 part-time employees at January 29, 2011. The Company considers employee relations to be satisfactory.

CompetitionFinancial information concerning competition is contained under the "Business Risk" section in the Financial Instruments and Risk Management note in "Item 8. Consolidated Financial Statements and Supplementary Data."

Merchandise PurchasesFinancial information concerning merchandise purchases is contained under the "Liquidity" section in "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations" and under the "Business Risk" section in the Financial Instruments and Risk Management note in "Item 8. Consolidated Financial Statements and Supplementary Data."

1

| Item 1A. | Risk Factors |

The statements contained in this Annual Report on Form 10-K ("Annual Report") that are not historical facts, including, but not limited to, statements regarding our expected financial position, business and financing plans found in "Item 1. Business" and "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations," constitute "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Please also see "Disclosure Regarding Forward-Looking Statements." Our actual results may differ materially due to the risks and uncertainties discussed in this Annual Report, including those discussed below. Additional risks and uncertainties that we do not presently know about or that we currently consider to be insignificant may also affect our business operations and financial performance.

Our inability to implement our strategic long range plan may have an adverse affect on our future results.Our ability to successfully implement and execute our long range plan is dependent on many factors. Our strategies may require significant capital investment and management attention, which may result in the diversion of these resources from our core business and other business issues and opportunities. Additionally, any new initiative is subject to certain risks including customer acceptance, competition, product differentiation, and the ability to attract and retain qualified personnel. If we cannot successfully execute our strategic growth initiatives or if the long range plan does not adequately address the challenges or opportunities we face, our financial condition and results of operations may be adversely affected.

The industry in which we operate is dependent upon fashion trends, customer preferences, and other fashion-related factors.The athletic footwear and apparel industry is subject to changing fashion trends and customer preferences. We cannot guarantee that our merchandise selection will accurately reflect customer preferences when it is offered for sale or that we will be able to identify and respond quickly to fashion changes, particularly given the long lead times for ordering much of our merchandise from vendors. A substantial portion of our highest margin sales are to young males (ages 12–25), many of whom we believe purchase athletic footwear and athletic and licensed apparel as a fashion statement and are frequent purchasers. Any shift in fashion trends that would make athletic footwear or licensed apparel less attractive to these customers could have a material adverse effect on our business, financial condition, and results of operations. Both the NFL and NBA have collective bargaining agreements that are due to expire in the current year. The possibility of a strike of either one or both of these leagues may result in a decline of sales of licensed product as well as player endorsed footwear.

The businesses in which we operate are highly competitive.The retail athletic footwear and apparel business is highly competitive with relatively low barriers to entry. Our athletic footwear and apparel operations compete primarily with athletic footwear specialty stores, sporting goods stores and superstores, department stores, discount stores, traditional shoe stores, and mass merchandisers, many of which are units of national or regional chains that have significant financial and marketing resources. The principal competitive factors in our markets are price, quality, selection of merchandise, reputation, store location, advertising, and customer service. Our success also depends on our ability to differentiate ourselves from our competitors with respect to shopping convenience, a quality assortment of available merchandise and superior customer service. We cannot assure you that we will continue to be able to compete successfully against existing or future competitors. Our expansion into markets served by our competitors and entry of new competitors or expansion of existing competitors into our markets could have a material adverse effect on our business, financial condition, and results of operations. Although we sell merchandise via the Internet, a significant shift in customer buying patterns to purchasing athletic footwear, athletic apparel, and sporting goods via the Internet could have a material adverse effect on our business results.

In addition, all of our significant vendors distribute products directly through the Internet and others may follow. Some vendors operate retail stores and some have indicated that further retail stores will open. Should this continue to occur, and if our customers decide to purchase directly from our vendors, it could have a material adverse effect on our business, financial condition, and results of operations.

2

If we do not successfully manage our inventory levels, our operating results will be adversely affected.

We must maintain sufficient inventory levels to operate our business successfully. However, we also must guard against accumulating excess inventory. For example, we order the bulk of our athletic footwear four to six months prior to delivery to our stores. If we fail to anticipate accurately either the market for the merchandise in our stores or our customers' purchasing habits, we may be forced to rely on markdowns or promotional sales to dispose of excess or slow moving inventory, which could have a material adverse effect on our business, financial condition, and results of operations.

We depend on mall traffic and our ability to identify suitable store locations.Our stores in the United States and Canada are located primarily in enclosed regional and neighborhood malls. Our sales are dependent, in part, on the volume of mall traffic. Mall traffic may be adversely affected by, among other things, economic downturns, the closing of anchor department stores, and a decline in the popularity of mall shopping among our target customers. Further, any terrorist act, natural disaster, or public health concern that decreases the level of mall traffic, which affects our ability to open and operate stores in affected areas, could have a material adverse effect on our business.

To take advantage of customer traffic and the shopping preferences of our customers, we need to maintain or acquire stores in desirable locations such as in regional and neighborhood malls anchored by major department stores. We cannot be certain that desirable mall locations will continue to be available. Some traditional enclosed malls are experiencing significantly lower levels of customer traffic, driven by the overall poor economic conditions, as well as the closure of certain mall anchor tenants.

Several large landlords dominate the ownership of prime malls, particularly in the United States, and because of our dependence upon these landlords for a substantial number of our locations, any significant erosion of their financial condition or our relationships with these landlords would negatively affect our ability to obtain and retain store locations. Additionally, further landlord consolidation may negatively affect our ability to negotiate favorable lease terms.

The effects of natural disasters, terrorism, acts of war, and public health issues may adversely affect our business.Natural disasters, including earthquakes, hurricanes, floods, and tornados may affect store and distribution center operations. In addition, acts of terrorism, acts of war, and military action both in the United States and abroad can have a significant effect on economic conditions and may negatively affect our ability to purchase merchandise from vendors for sale to our customers. Public health issues, such as flu or other pandemics, whether occurring in the United States or abroad, could disrupt our operations and result in a significant part of our workforce being unable to operate or maintain our infrastructure or perform other tasks necessary to conduct our business. Additionally, public health issues may disrupt the operations of our suppliers, our operations, our customers, or have an adverse effect on customer demand. We may be required to suspend operations in some or all of our locations, which could have a material adverse effect on our business, financial condition, and results of operations. Any significant declines in public safety concerns or uncertainties regarding future economic prospects that affect customer spending habits could have a material adverse effect on customer purchases of our products.

A change in the relationship with any of our key vendors or the unavailability of our key products at competitive prices could affect our financial health.Our business is dependent to a significant degree upon our ability to obtain exclusive product and the ability to purchase brand-name merchandise at competitive prices. In addition, our vendors provide volume discounts, cooperative advertising, and markdown allowances, as well as the ability to negotiate returns of excess or unneeded merchandise. We cannot be certain that such assistance from our vendors will continue in the future.

3

The Company purchased approximately 82 percent of its merchandise in 2010 from its top five vendors and expects to continue to obtain a significant percentage of its athletic product from these vendors in future periods. Approximately 63 percent was purchased from one vendor - Nike, Inc. ("Nike"). Each of our operating divisions is highly dependent on Nike; they individually purchase 46 to 81 percent of their merchandise from Nike. Merchandise that is high profile and in high demand is allocated by our vendors based upon their internal criteria. Although we have generally been able to purchase sufficient quantities of this merchandise in the past, we cannot be certain that our vendors will continue to allocate sufficient amounts of such merchandise to us in the future. Our inability to obtain merchandise in a timely manner from major suppliers (particularly Nike) as a result of business decisions by our suppliers or any disruption in the supply chain could have a material adverse effect on our business, financial condition, and results of operations. Because of our strong dependence on Nike, any adverse development in Nike's reputation, financial condition or results of operations or the inability of Nike to develop and manufacture products that appeal to our target customers could also have an adverse effect on our business, financial condition, and results of operations. We cannot be certain that we will be able to acquire merchandise at competitive prices or on competitive terms in the future.

These risks could have a material adverse effect on our business, financial condition, and results of operations.

Significant increases in costs associated with the production of promotional materials may adversely affect our operating income.We advertise and promote our merchandise through print catalogs and other promotional materials mailed to consumers or displayed in our stores. As a result, significant increases in paper, printing, and postage costs could increase the cost of producing promotional and other materials and, as a result, may have a material adverse effect on our operating income.

We may experience fluctuations in and cyclicality of our comparable-store sales results.Our comparable-store sales have fluctuated significantly in the past, on both an annual and a quarterly basis, and we expect them to continue to fluctuate in the future. A variety of factors affect our comparable-store sales results, including, among others, fashion trends, the highly competitive retail store sales environment, economic conditions, timing of promotional events, changes in our merchandise mix, calendar shifts of holiday periods, and weather conditions. Many of our products, particularly high-end athletic footwear and licensed apparel, represent discretionary purchases. Accordingly, customer demand for these products could decline in a recession or if our customers develop other priorities for their discretionary spending. These risks could have a material adverse effect on our business, financial condition, and results of operations.

Legislative or regulatory initiatives related to global warming/climate change concerns may negatively affect our business.There has been an increasing focus and continuous debate on global climate change recently, including increased attention from regulatory agencies and legislative bodies globally. This increased focus may lead to new initiatives directed at regulating an as yet unspecified array of environmental matters. Legislative, regulatory or other efforts in the United States to combat climate change could result in future increases in taxes or in the cost of transportation and utilities, which could decrease our operating profits and could necessitate future additional investments in facilities and equipment. We are unable to predict the potential effects that any such future environmental initiatives may have on our business.

Our operations may be adversely affected by economic or political conditions in other countries.A significant portion of our sales and operating income for 2010 were attributable to our operations in Europe, Canada, New Zealand, and Australia. As a result, our business is subject to the risks associated with doing business outside of the United States such as foreign customer preferences, political unrest, disruptions or delays in shipments, and changes in economic conditions in countries in which we operate. Although we enter into forward foreign exchange contracts and option contracts to reduce the effect of foreign currency exchange rate fluctuations, our operations may be adversely affected by significant changes in the value of the U.S. dollar as it relates to certain foreign currencies.

4

In addition, because we and our suppliers have a substantial amount of our products manufactured in foreign countries, our ability to obtain sufficient quantities of merchandise on favorable terms may be affected by governmental regulations, trade restrictions, and economic, labor, and other conditions in the countries from which our suppliers obtain their product.

We operate in many different jurisdictions and we could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-corruption laws.The U.S. Foreign Corrupt Practices Act ("FCPA") and similar worldwide anti-corruption laws, including the U.K. Bribery Act of 2010, which it is anticipated will become effective in 2011 and is broader in scope than the FCPA, generally prohibit companies and their intermediaries from making improper payments to non-U.S. officials for the purpose of obtaining or retaining business. Our internal policies mandate compliance with these anti-corruption laws. Despite our training and compliance programs, we cannot be assured that our internal control policies and procedures will always protect us from reckless or criminal acts committed by our employees or agents. Our continued expansion outside the U.S., including in developing countries, could increase the risk of such violations in the future. Violations of these laws, or allegations of such violations, could disrupt our business and result in a material adverse effect on our results of operations or financial condition.

The current global economic conditions have adversely affected, and may continue to adversely affect our business and results of operations.The Company's performance is subject to global economic conditions and the related impact on consumer spending levels. Some of the factors affecting consumer spending are employment, levels of consumer debt, reductions in net worth as a result of market declines, residential real estate and mortgage markets, taxation, fuel and energy prices, interest rates, and consumer confidence, as well as other macroeconomic factors. Consumer purchases of discretionary items, including merchandise we sell, generally decline during recessionary periods and other periods where disposable income is adversely affected and customers may be hesitant to use available credit. The downturn in the global economy may continue to affect customer purchases for the foreseeable future and may adversely impact our business, financial condition, and results of operations. In addition, declines in our profitability could result in a charge to earnings for the impairment of long-lived assets, goodwill and other intangible assets, which would not affect our cash flow but could decrease our earnings, and our stock price could be adversely affected.

Instability in the financial markets may adversely affect our business.Uncertain economic conditions may constrain our ability to obtain credit. Domestic and global credit and equity markets have recently undergone significant disruption, making it difficult for many businesses to obtain financing on acceptable terms or at all. Although we currently have a revolving credit agreement in place until 2013 and do not have any borrowings under it (other than amounts used for standby letters of credit), tightening of credit markets could make it more difficult for us to access funds, refinance our existing indebtedness, enter into agreements for new indebtedness or obtain funding through the issuance of the Company's securities. Additionally, our borrowing costs can be affected by independent rating agencies' ratings, which are based largely on our performance as measured by credit metrics, including lease-adjusted leverage ratios.

In addition, instability in the financial markets may have a negative effect on businesses around the world, and the impact on our major suppliers cannot be predicted. The Company relies on a few key vendors for a majority of its merchandise purchases (including a significant portion from one key vendor). The inability of key suppliers to access liquidity, or the insolvency of key suppliers, could lead to their failure to deliver our merchandise. Our inability to obtain merchandise in a timely manner from major suppliers could have a material adverse effect on our business, financial condition, and results of operations.

5

If our long-lived assets, goodwill or other intangible assets become impaired, we may need to record significant non-cash impairment charges.

We review our long-lived assets, goodwill and other intangible assets when events indicate that the carrying value of such assets may be impaired. Goodwill and other indefinite lived intangible assets are reviewed for impairment if impairment indicators arise and, at a minimum, annually. We determine fair value based on a combination of a discounted cash flow approach and market-based approach. If an impairment trigger is identified, the carrying value is compared to its estimated fair value and provisions for impairment are recorded as appropriate. Impairment losses are significantly affected by estimates of future operating cash flows and estimates of fair value. Our estimates of future operating cash flows are identified from our three-year plans, which are based upon our experience, knowledge, and expectations; however, these estimates can be affected by such factors as our future operating results, future store profitability, and future economic conditions, all of which can be difficult to predict. Similar to others in our industry, the recent macroeconomic conditions have affected our performance and it is difficult to predict how long these economic conditions will continue and which aspects of our business may be adversely affected. The continuation of these conditions could affect the fair value of our long-lived assets, goodwill and other intangible assets and could result in future impairment charges, which would adversely affect our results of operations.

Material changes in the market value of the securities we hold may adversely affect our results of operations and financial condition.At January 29, 2011, our cash and cash equivalents totaled $696 million. The majority of our investments were short-term deposits in highly-rated banking institutions. We retain a substantial portion of our cash in foreign jurisdictions for future reinvestment. We regularly monitor our counterparty credit risk and mitigate our exposure by making short-term investments only in highly-rated institutions and by limiting the amount we invest in any one institution. The Company continually monitors the creditworthiness of its counterparties. At January 29, 2011, most of the investments were in institutions rated A or better from a major credit rating agency. Despite those ratings, it is possible that the value or liquidity of our investments may decline due to any number of factors, including general market conditions and bank-specific credit issues.

The trust which holds the assets of our U.S. pension plan has assets totaling $511 million at January 29, 2011. The fair values of these assets held in the trust are compared to the plan's projected benefit obligation to determine the pension funding liability. We attempt to mitigate risk through diversification, and we regularly monitor investment risk on our portfolio through quarterly investment portfolio reviews and periodic asset and liability studies. Despite these measures, it is possible that the value of our portfolio may decline in the future due to any number of factors, including general market conditions and credit issues. Such declines could have an impact on the funded status of our pension plans and future funding requirements.

Our financial results may be adversely impacted by higher-than-expected tax rates or exposure to additional tax liabilities.We are a U.S.-based multinational company subject to tax in multiple U.S. and foreign tax jurisdictions. Our provision for income taxes is based on a jurisdictional mix of earnings, statutory rates, and enacted tax rules, including transfer pricing. Significant judgment is required in determining our provision for income taxes and in evaluating our tax positions on a worldwide basis. Our effective tax rate could be adversely affected by a number of factors, including shifts in the mix of pretax profits and losses by tax jurisdiction, our ability to use tax credits, changes in tax laws or related interpretations in the jurisdictions in which we operate, and tax assessments and related interest and penalties resulting from income tax audits.

A substantial portion of our cash and investments is invested outside of the U.S. As we plan to permanently reinvest our foreign earnings, in accordance with U.S. GAAP, we have not provided for U.S. federal and state income taxes or foreign withholding taxes that may result from future remittances of undistributed earnings of foreign subsidiaries. Recent proposals to reform U.S. tax rules may result in a reduction or elimination of the deferral of U.S. income tax on our foreign earnings, which could adversely affect our effective tax rate. Any of these changes could have an adverse effect on our results of operations and financial condition.

6

In addition, our products are subject to import and excise duties and/or sales or value-added taxes in many jurisdictions. Fluctuations in tax rates and duties and changes in tax legislation or regulation could have a material adverse effect on our results of operations and financial condition.

Complications in our distribution centers and other factors affecting the distribution of merchandise may affect our business.We operate four distribution centers worldwide to support our businesses. In addition to the distribution centers that we operate, we have third-party arrangements to support our operations in the U.S., Canada, Australia, and New Zealand. If complications arise with any facility or any facility is severely damaged or destroyed, the Company's other distribution centers may not be able to support the resulting additional distribution demands. This may adversely affect our ability to deliver inventory on a timely basis. We depend upon third-party carriers for shipment of a significant amount of merchandise. An interruption in service by these carriers for any reason could cause temporary disruptions in our business, a loss of sales and profits, and other material adverse effects.

Our freight cost is affected by changes in fuel prices through surcharges. Increases in fuel prices and surcharges and other factors may increase freight costs and thereby increase our cost of sales. We enter into diesel fuel forward and option contracts to mitigate a portion of the risk associated with the variability caused by these surcharges.

A major failure of our information systems could harm our business.We depend on information systems to process transactions, manage inventory, operate our websites, purchase, sell and ship goods on a timely basis, and maintain cost-efficient operations. Any material disruption or slowdown of our systems could cause information to be lost or delayed, which could have a negative effect on our business. We may experience operational problems with our information systems as a result of system failures, viruses, computer "hackers" or other causes. We cannot be assured that our systems will be adequate to support future growth.

Risks associated with Internet operations.Our Internet operations are subject to numerous risks, including risks related to the failure of the computer systems that operate our websites and their related support systems, including computer viruses, telecommunications failures and similar disruptions. Also, we may require additional capital in the future to sustain or grow our online commerce.

Business risks related to online commerce include risks associated with the need to keep pace with rapid technological change, Internet security risks, risks of system failure or inadequacy, governmental regulation and legal uncertainties with respect to the Internet, and collection of sales or other taxes by additional states or foreign jurisdictions. If any of these risks materializes, it could have a material adverse effect on the Company's business.

Unauthorized disclosure of sensitive or confidential customer information, whether through a breach of the Company's computer systems or otherwise, could severely harm our business.As part of the Company's normal course of business, it collects, processes, and retains sensitive and confidential customer information. Despite the security measures the Company has in place, its facilities and systems, and those of its third party providers may be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming and/or human error, or other similar events. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential information by the Company could severely damage its reputation, expose it to the risks of litigation and liability, disrupt its operations and harm its business.

7

Our reliance on key management, store and field associates.

Future performance will depend upon our ability to attract, retain, and motivate our executive and senior management team, as well as store personnel and field management. Our success depends to a significant extent both upon the continued services of our current executive and senior management team, as well as our ability to attract, hire, motivate, and retain additional qualified management in the future. Competition for key executives in the retail industry is intense, and our operations could be adversely affected if we cannot attract and retain qualified associates. Many of the store and field associates are in entry level or part-time positions with historically high rates of turnover. Our ability to meet our labor needs while controlling costs is subject to external factors such as unemployment levels, prevailing wage rates, minimum wage legislation, and changing demographics. If we are unable to attract and retain quality associates, our ability to meet our growth goals or to sustain expected levels of profitability may be compromised. In addition, a large number of our retail employees are paid the prevailing minimum wage, which if increased would negatively affect our profitability.

We face risks arising from possible union legislation in the United States.There is a possibility that regulations or legislation may be enacted in the United States along the lines of the proposed Employee Free Choice Act, which, if adopted or enacted, could significantly change the nature of labor relations in the United States, specifically, how union elections and contract negotiations are conducted. It would be easier for unions to win elections and we could face arbitrator-imposed labor scheduling, costs, and standards. Therefore, this legislation or regulations could impose more labor relations requirements and union activity on our business, thereby potentially increasing our costs, and could have a material adverse effect on our overall competitive position.

Health care reform could adversely affect our business.In 2010, Congress enacted comprehensive health care reform legislation which, among other things, includes guaranteed coverage requirements, eliminates pre-existing condition exclusions and annual and lifetime maximum limits, restricts the extent to which policies can be rescinded, and imposes new and significant taxes on health insurers and health care benefits. Due to the breadth and complexity of the health reform legislation, the current lack of implementing regulations and interpretive guidance, and the phased-in nature of the implementation, it is difficult to predict the overall effect of the statute and related regulations on our business over the coming years. Possible adverse effects of the health reform legislation include increased costs, exposure to expanded liability and requirements for us to revise ways in which we conduct business.

We may be adversely affected by regulatory and litigation developments.We are exposed to the risk that federal or state legislation may negatively impact our operations. Changes in federal or state wage requirements, employee rights, health care, social welfare or entitlement programs such as health insurance, paid leave programs, or other changes in workplace regulation or tax rates could increase our cost of doing business or otherwise adversely affect our operations. Additionally, we are regularly involved in various litigation matters, including class actions and patent infringement claims, which arise in the ordinary course of our business. Litigation or regulatory developments could adversely affect our business operations and financial performance.

Failure to fully comply with Section 404 of the Sarbanes-Oxley Act of 2002 could negatively affect our business, the price of our common stock and market confidence in our reported financial information.We must continue to document, test, monitor, and enhance our internal controls over financial reporting in order to satisfy all of the requirements of Section 404 of the Sarbanes-Oxley Act of 2002. We cannot be assured that our disclosure controls and procedures and our internal controls over financial reporting required under Section 404 of the Sarbanes-Oxley Act will prove to be completely adequate in the future. Failure to fully comply with Section 404 of the Sarbanes-Oxley Act of 2002 could negatively affect our business, the price of our common stock, and market confidence in our reported financial information.

8

| Item 1B. | Unresolved Staff Comments |

None.

| Item 2. | Properties |

The properties of the Company and its consolidated subsidiaries consist of land, leased stores, administrative facilities, and distribution centers. Gross square footage and total selling area for the Athletic Stores segment at the end of 2010 were approximately 12.64 and 7.54 million square feet, respectively. These properties, which are primarily leased, are located in the United States, Canada, various European countries, Australia, and New Zealand.

The Company currently operates four distribution centers, of which two are owned and two are leased, occupying an aggregate of 2.4 million square feet. Three of the four distribution centers are located in the United States and one is in the Netherlands.

| Item 3. | Legal Proceedings |

Information regarding the Company's legal proceedings is contained in the "Legal Proceedings" note under "Item 8. Consolidated Financial Statements and Supplementary Data."

9

| Item 4. | [Removed and Reserved] |

Information with respect to Executive Officers of the Company, as of March 28, 2011, is set forth below:

| Chairman of the Board, President and Chief Executive Officer | Ken C. Hicks | |

| President and Chief Executive Officer - Foot Locker, Inc. - International | Ronald J. Halls | |

| President and Chief Executive Officer - Foot Locker U.S., Lady Foot Locker, Kids Foot Locker and Footaction | Richard A. Johnson | |

| Executive Vice President and Chief Financial Officer | Robert W. McHugh | |

| Senior Vice President, General Counsel and Secretary | Gary M. Bahler | |

| Senior Vice President - Real Estate | Jeffrey L. Berk | |

| Senior Vice President - Chief Information Officer | Peter D. Brown | |

| Senior Vice President and Chief Accounting Officer | Giovanna Cipriano | |

| Senior Vice President - Strategic Planning | Lauren B. Peters | |

| Senior Vice President - Human Resources | Laurie J. Petrucci | |

| Vice President, Treasurer and Investor Relations | John A. Maurer |

Ken C. Hicks, age 58, has served as Chairman of the Board since January 31, 2010 and President and Chief Executive Officer since August 17, 2009. Mr. Hicks served as President and Chief Merchandising Officer of J.C. Penney Company, Inc. ("JC Penney") from 2005 through 2009. He was President and Chief Operating Officer of Stores and Merchandise Operations of JC Penney from 2002 through 2004, and he served as President of Payless ShoeSource, Inc. from 1999 to 2002. Mr. Hicks is also a director of Avery Dennison Corporation.

Ronald J. Halls, age 57, has served as President and Chief Executive Officer of Foot Locker, Inc. - International since October 2006. He served as President and Chief Executive Officer of Champs Sports, an operating division of the Company, from February 2003 to October 2006 and as Chief Operating Officer of Champs Sports from February 2000 to February 2003.

Richard A. Johnson, age 53, has served as President and Chief Executive Officer of Foot Locker U.S., Lady Foot Locker, Kids Foot Locker, and Footaction since January 2010. He served as President and Chief Executive Officer of Foot Locker Europe, an operating division of the Company, from August 2007 to January 2010; President and Chief Executive Officer of Footlocker.com/Eastbay, an operating division of the Company, from April 2003 to August 2007 and President and Chief Operating Officer of Footlocker.com/Eastbay from July 2000 to April 2003.

Robert W. McHugh, age 52, has served as Executive Vice President and Chief Financial Officer since May 2009. He served as Senior Vice President and Chief Financial Officer from November 2005 through April 2009. He served as Vice President and Chief Accounting Officer from January 2000 to November 2005.

Gary M. Bahler, age 59, has served as Senior Vice President since August 1998, General Counsel since February 1993 and Secretary since February 1990.

Jeffrey L. Berk, age 55, has served as Senior Vice President - Real Estate since February 2000.

Peter D. Brown, age 56, has served as Senior Vice President - Chief Information Officer since February 2011. He served as Senior Vice President, Chief Information Officer and Investor Relations from September 2006 to February 2011; and as Vice President - Investor Relations and Treasurer from October 2001 to September 2006.

Giovanna Cipriano, age 41, has served as Senior Vice President and Chief Accounting Officer since May 2009. Ms. Cipriano served as Vice President and Chief Accounting Officer from November 2005 through April 2009. She served as Divisional Vice President, Financial Controller from June 2002 to November 2005.

Lauren B. Peters, age 49, has served as Senior Vice President - Strategic Planning since April 2002. Ms. Peters served as Vice President - Planning from January 2000 to April 2002.

Laurie J. Petrucci, age 52, has served as Senior Vice President - Human Resources since May 2001.

John A. Maurer, age 51, has served as Vice President, Treasurer and Investor Relations since February 2011. Mr. Maurer served as Vice President and Treasurer from September 2006 to February 2011. He served as Divisional Vice President and Assistant Treasurer from April 2006 to September 2006 and as Assistant Treasurer from April 2002 to April 2006.

There are no family relationships among the executive officers or directors of the Company.

10

PART II

| Item 5. | Market for the Company's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Foot Locker, Inc. common stock is listed on The New York Stock Exchange as well as on the Börse Stuttgart stock exchange in Germany. In addition, the stock is traded on the Cincinnati stock exchange. At January 29, 2011, the Company had 19,286 shareholders of record owning 154,620,118 common shares. During each of the quarters of 2010 and 2009, the Company declared dividends of $0.15 per share. The following table sets forth, for the period indicated, the intra-day high and low sales prices for the Company's common stock:

| 2010 | 2009 | |||||||||||||||

| High | Low | High | Low | |||||||||||||

| 1 st Quarter | $ | 16.76 | $ | 11.30 | $ | 12.29 | $ | 7.09 | ||||||||

| 2 nd Quarter | 15.79 | 12.27 | 12.95 | 9.38 | ||||||||||||

| 3 rd Quarter | 16.09 | 11.59 | 12.31 | 9.91 | ||||||||||||

| 4 th Quarter | 20.08 | 15.63 | 12.55 | 9.46 | ||||||||||||

The following table provides information with respect to shares of the Company's common stock that the Company repurchased during the thirteen weeks ended January 29, 2011.

| Date Purchased | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Program (1) | Approximate Dollar Value of Shares that may yet be Purchased Under the Program (1) | ||||||||||||

| Oct. 31, 2010 through Nov. 27, 2010 | - | $ | - | - | $ | 214,406,176 | ||||||||||

| Nov. 28, 2010 through Jan. 1, 2011 | 615,000 | 19.38 | 615,000 | $ | 202,484,858 | |||||||||||

| Jan. 2, 2011 through Jan. 29, 2011 | 90,000 | 19.75 | 90,000 | $ | 200,707,001 | |||||||||||

| 705,000 | $ | 19.43 | 705,000 | |||||||||||||

| (1) | On February 16, 2010, the Company's Board of Directors approved the extension of the Company's 2007 common share repurchase program for an additional three years in the amount of $250 million. During 2010, the Company repurchased 3,215,000 shares of common stock at a cost of approximately $50 million. The Company repurchased 705,000 shares of common stock during the fourth quarter at a cost of approximately $14 million. |

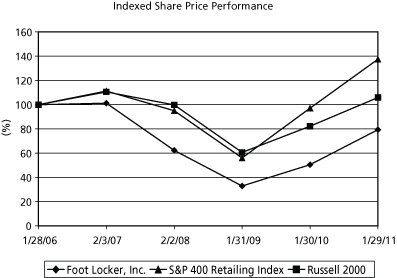

The following graph compares the cumulative five-year total return to shareholders on Foot Locker, Inc.'s common stock relative to the total returns of the S&P 400 Retailing Index and the Russell 2000 Index.

11

| Item 6. | Selected Financial Data |

The selected financial data below should be read in conjunction with the Consolidated Financial Statements and the Notes thereto and other information contained elsewhere in this report.

| ($ in millions, except per share amounts) | 2010 | 2009 | 2008 | 2007 | 2006 (1) | |||||||||||||||

| Summary of Continuing Operations | ||||||||||||||||||||

| Sales | $ | 5,049 | 4,854 | 5,237 | 5,437 | 5,750 | ||||||||||||||

| Gross margin | 1,516 | 1,332 | 1,460 | 1,420 | 1,736 | |||||||||||||||

| Selling, general, and administrative expenses | 1,138 | 1,099 | 1,174 | 1,176 | 1,163 | |||||||||||||||

| Impairment and other charges | 10 | 41 | 259 | 128 | 17 | |||||||||||||||

| Depreciation and amortization | 106 | 112 | 130 | 166 | 175 | |||||||||||||||

| Interest expense, net | 9 | 10 | 5 | 1 | 3 | |||||||||||||||

| Other income | (4 | ) | (3 | ) | (8 | ) | (1 | ) | (14 | ) | ||||||||||

| Income (loss) from continuing operations | 169 | 47 | (79 | ) | 43 | 247 | ||||||||||||||

| Cumulative effect of accounting change (2) | - | - | - | - | 1 | |||||||||||||||

| Basic earnings per share from continuing operations | 1.08 | 0.30 | (0.52 | ) | 0.29 | 1.59 | ||||||||||||||

| Basic earnings per share from cumulative effect of accounting change (2) | - | - | - | - | 0.01 | |||||||||||||||

| Diluted earnings per share from continuing operations | 1.07 | 0.30 | (0.52 | ) | 0.28 | 1.58 | ||||||||||||||

| Diluted earnings per share from cumulative effect of accounting change (2) | - | - | - | - | - | |||||||||||||||

| Common stock dividends declared per share | 0.60 | 0.60 | 0.60 | 0.50 | 0.40 | |||||||||||||||

| Weighted-average common shares outstanding (in millions) | 155.7 | 156.0 | 154.0 | 154.0 | 155.0 | |||||||||||||||

| Weighted-average common shares outstanding assuming dilution (in millions) | 156.7 | 156.3 | 154.0 | 155.6 | 156.8 | |||||||||||||||

| Financial Condition | ||||||||||||||||||||

| Cash, cash equivalents, and short-term investments | $ | 696 | 589 | 408 | 493 | 470 | ||||||||||||||

| Merchandise inventories | 1,059 | 1,037 | 1,120 | 1,281 | 1,303 | |||||||||||||||

| Property and equipment, net | 386 | 387 | 432 | 521 | 654 | |||||||||||||||

| Total assets | 2,896 | 2,816 | 2,877 | 3,243 | 3,249 | |||||||||||||||

| Long-term debt and obligations under capital leases | 137 | 138 | 142 | 221 | 234 | |||||||||||||||

| Total shareholders' equity | 2,025 | 1,948 | 1,924 | 2,261 | 2,295 | |||||||||||||||

| Financial Ratios | ||||||||||||||||||||

| Operating profit (loss) as a % of sales | 5.2 | % | 1.6 | (2.0 | ) | (0.9 | ) | 6.6 | ||||||||||||

| Earnings before interest and taxes | $ | 266 | 83 | (95 | ) | (49 | ) | 395 | ||||||||||||

| Income (loss) from continuing operations as a % of sales | 3.3 | % | 1.0 | (1.5 | ) | 0.8 | 4.3 | |||||||||||||

| Return on assets (ROA) | 5.9 | % | 1.7 | (2.6 | ) | 1.3 | 7.5 | |||||||||||||

| Net debt capitalization percent (3) | 39.0 | % | 43.0 | 46.7 | 45.1 | 44.4 | ||||||||||||||

| Current ratio | 4.0 | 4.1 | 4.2 | 4.0 | 3.9 | |||||||||||||||

| Sales per average gross square foot (4) | $ | 360 | 333 | 350 | 352 | 372 | ||||||||||||||

| Other Data | ||||||||||||||||||||

| Capital expenditures | $ | 97 | 89 | 146 | 148 | 165 | ||||||||||||||

| Number of stores at year end | 3,426 | 3,500 | 3,641 | 3,785 | 3,942 | |||||||||||||||

| Total selling square footage at year end (in millions) | 7.54 | 7.74 | 8.09 | 8.50 | 8.74 | |||||||||||||||

| Total gross square footage at year end (in millions) | 12.64 | 12.96 | 13.50 | 14.12 | 14.55 | |||||||||||||||

| (1) | 2006 represents the 53 weeks ended February 3, 2007. |

| (2) | 2006 relates to the adoption of authoritative accounting guidance for share-based compensation. |

| (3) | Represents total debt, net of cash, cash equivalents, and short-term investments and includes the effect of interest rate swaps. The effect of interest rate swaps increased/(decreased) debt by $17 million, $18 million, $19 million, $4 million, and $(4) million, at January 29, 2011, January 30, 2010, January 31, 2009, February 2, 2008, and February 3, 2007, respectively. Additionally, this calculation includes the present value of operating leases, and accordingly is considered a non-GAAP measure. |

| (4) | Calculated as Athletic Store sales divided by the average monthly ending gross square footage of the last thirteen months. |

12

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations |

Foot Locker, Inc., through its subsidiaries, operates in two reportable segments - Athletic Stores and Direct-to-Customers. The Athletic Stores segment is one of the largest athletic footwear and apparel retailers in the world, whose formats include Foot Locker, Lady Foot Locker, Kids Foot Locker, Champs Sports, Footaction, and CCS. The Direct-to-Customers segment reflects CCS and Footlocker.com, Inc., which sells, through its affiliates, including Eastbay, Inc., to customers through catalogs, mobile devices, and Internet websites.

The Foot Locker brand is one of the most widely recognized names in the market segments in which the Company operates, epitomizing high quality for the active lifestyle customer. This brand equity has aided the Company's ability to successfully develop and increase its portfolio of complementary retail store formats, specifically Lady Foot Locker and Kids Foot Locker, as well as Footlocker.com, its direct-to-customers business. Through various marketing channels, including broadcast, digital, print, and sponsorships of various sporting events, the Company reinforces its image with a consistent message- namely, that it is the destination store for athletically inspired shoes and apparel with a wide selection of merchandise in a full-service environment.

Store Profile

| At January 30, 2010 | Opened | Closed | At January 29, 2011 | |||||||||||||

| Foot Locker | 1,911 | 27 | 43 | 1,895 | ||||||||||||

| Lady Foot Locker | 415 | - | 37 | 378 | ||||||||||||

| Kids Foot Locker | 301 | 5 | 12 | 294 | ||||||||||||

| Champs Sports | 552 | 1 | 13 | 540 | ||||||||||||

| Footaction | 319 | - | 12 | 307 | ||||||||||||

| CCS | 2 | 10 | - | 12 | ||||||||||||

| Total Athletic Stores | 3,500 | 43 | 117 | 3,426 | ||||||||||||

The Company operates 3,426 stores in the Athletic Stores segment. The following is a brief description of the Athletic Stores segment's operating businesses:

Foot Locker - "Sneaker Central" - Foot Locker is a leading global athletic footwear and apparel retailer. Its stores offer the latest in athletic-inspired performance products, manufactured primarily by the leading athletic brands. Foot Locker offers products for a wide variety of activities including basketball, running, and training. Its 1,895 stores are located in 21 countries including 1,144 in the United States, Puerto Rico, U.S. Virgin Islands, and Guam, 129 in Canada, 529 in Europe, and a combined 93 in Australia and New Zealand. The domestic stores have an average of 2,400 selling square feet and the international stores have an average of 1,500 selling square feet.

Lady Foot Locker - "The Place for Her" - Lady Foot Locker is a leading U.S. retailer of athletic footwear, apparel and accessories for active women. Its stores carry major athletic footwear and apparel brands, as well as casual wear and an assortment of apparel designed for a variety of activities, including running, walking, training, and fitness. Its 378 stores are located in the United States, Puerto Rico, and the U.S. Virgin Islands, and have an average of 1,300 selling square feet.

Kids Foot Locker - "Where Kids Come First" - Kids Foot Locker is a national children's athletic retailer that offers the largest selection of brand-name athletic footwear, apparel and accessories for children. Its stores feature an environment geared to appeal to both parents and children. Its 294 stores are located in the United States, Puerto Rico, and the U.S. Virgin Islands and have an average of 1,400 selling square feet.

Champs Sports - "Official Providers of Game" - Champs Sports is one of the largest mall-based specialty athletic footwear and apparel retailers in North America. Its product categories include athletic footwear, apparel and accessories, and a focused assortment of equipment. This combination allows Champs Sports to differentiate itself from other mall-based stores by presenting complete product assortments in a select number of sporting activities. Its 540 stores are located throughout the United States, Canada, Puerto Rico, and the U.S. Virgin Islands. The Champs Sports stores have an average of 3,500 selling square feet.

13

Footaction - "Head to Toe Sport Inspired Style" - Footaction is a national athletic footwear and apparel retailer. The primary customers are young males that seek street-inspired athletic styles. Its 307 stores are located throughout the United States and Puerto Rico and focus on marquee footwear and branded apparel. The Footaction stores have an average of 2,900 selling square feet.

CCS - "Largest Deck Selection" - CCS serves the needs of the 10-18 year old skateboard enthusiast while maintaining credibility with core skaters of all ages. This format complements the CCS catalog and internet business, which was acquired in November 2008. During 2009, the Company opened two stores under the banner of CCS. This concept was expanded to 12 stores in 2010, all of which are located in the United States and average 1,700 selling square feet.

Direct-to-CustomersThe Company's Direct-to-Customers segment is multi-branded and multi-channeled. This segment sells, through its affiliates, directly to customers through catalogs and its Internet websites. Eastbay, one of the affiliates, is among the largest direct marketers in the United States, providing the high school athlete with a complete sports solution including athletic footwear, apparel, equipment, team licensed, and private-label merchandise. In 2008, the Company purchased CCS, an Internet and catalog retailer of skateboard equipment, apparel, footwear, and accessories targeted primarily to teenaged boys. The retail store operations of CCS are included in the Athletic Stores segment. The Direct-to-Customers segment operates the website for eastbay.com, final-score.com, and teamsales.eastbay.com. Additionally this segment operates websites aligned with the brand names of its store banners (footlocker.com, ladyfootlocker.com, kidsfootlocker.com, footaction.com, champssports.com, and ccs.com).

Franchise OperationsIn March of 2006, the Company entered into a ten-year area development agreement with the Alshaya Trading Co. W.L.L., in which the Company agreed to enter into separate license agreements for the operation of Foot Locker stores located within the Middle East, subject to certain restrictions. Additionally, in March 2007, the Company entered into a ten-year agreement with another third party for the exclusive right to open and operate Foot Locker stores in the Republic of Korea. A total of 26 franchised stores were operating at January 29, 2011. Royalty income from the franchised stores was not significant for any of the periods presented. These stores are not included in the Company's operating store count above.

Overview of Consolidated ResultsThe Company recorded net income from continuing operations of $169 million or $1.07 per diluted share for 2010; this compares with $47 million or $0.30 per diluted share for the prior-year period. Other highlights include:

| • | Sales increased by 4.0 percent and comparable-store sales increased by 5.8 percent as compared with the corresponding prior-year period. |

| • | Gross margin increased 260 basis points in 2010 as compared with 2009. Included in cost of sales for 2009 is a $14 million charge to reserve for inventory as the Company began its transition to a new apparel strategy. |

| • | The Company recorded a charge of $10 million in 2010 to impair the CCS tradename intangible asset due to the lower projected revenues for this division. Included in 2009 are impairment charges totaling $36 million, of which $32 million was recorded to impair store long-lived assets within the Athletic Stores segment and $4 million related to a write-off of certain software development costs within the Direct-to-Customers segment. |

| • | The Company recorded a $2 million gain in 2010 on the settlement on its money-market investment in the Reserve International Liquidity Fund, Ltd. (the "Fund"). During 2008, the Company had recognized an impairment loss of $3 million representing the decreased value of the underlying securities of Lehman Brothers held in the Fund. These amounts were recorded with no tax expense or benefit. |

14

Other highlights include:

| • | Cash and cash equivalents at January 29, 2011 were $696 million, representing an increase of $114 million. |

| • | Cash flow provided from operations was $326 million, which included the payment on the settlement of the net investment hedge of $24 million and qualified pension contribution totaling $32 million. The funded status of the qualified plans improved to 93 percent as compared with 87 percent in 2009. |

| • | Dividends totaling $93 million were declared and paid. Effective with the first quarter 2011 dividend payment, the dividend was increased by 10 percent to $0.165 per share. |

In March 2010, the Company announced a new strategic plan, which includes a series of operating initiatives and long-term financial objectives. We consider the following financial objectives in assessing our performance pursuant to the strategic plan:

| • | Sales of $6 billion |

| • | Sales per gross square foot of $400 |

| • | EBIT margin of 8 percent |

| • | Net income margin of 5 percent |

| • | Return on Invested Capital of 10 percent |

In the following tables, the Company has presented certain financial measures and ratios identified as non-GAAP. The Company believes this non-GAAP information is a useful measure to investors because it allows for a more direct comparison of the Company's performance for 2010 as compared with 2009 and is useful in assessing the Company's progress in achieving its long-term financial objectives noted above. The following represents a reconciliation of the non-GAAP measures:

| 2010 | 2009 | 2008 | ||||||||||

| (in millions) | ||||||||||||

| Pre-tax income: | ||||||||||||

| Income (loss) from continuing operations before income taxes – Reported | $ | 257 | $ | 73 | $ | (100 | ) | |||||

| Pre-tax amounts excluded from GAAP | ||||||||||||

| Impairment of goodwill and other intangible assets | 10 | - | 169 | |||||||||

| Impairment of assets | - | 36 | 67 | |||||||||

| Reorganization costs | - | 5 | - | |||||||||

| Store closing program | - | - | 5 | |||||||||

| Money market impairment | - | - | 3 | |||||||||

| Northern Group note impairment | - | - | 15 | |||||||||

| Impairment and other charges | 10 | 41 | 259 | |||||||||

| Inventory reserve – recorded within cost of sales | - | 14 | - | |||||||||

| Money market realized gain – recorded within other income | (2 | ) | - | - | ||||||||

| Total pre-tax amounts excluded | $ | 8 | $ | 55 | $ | 259 | ||||||

| Income (loss) from continuing operations before income taxes – Adjusted | $ | 265 | $ | 128 | $ | 159 | ||||||

| Calculation of EBIT: | ||||||||||||

| Income (loss) from continuing operations before income taxes – Reported | $ | 257 | $ | 73 | $ | (100 | ) | |||||

| Interest expense, net | 9 | 10 | 5 | |||||||||

| EBIT | $ | 266 | $ | 83 | $ | (95 | ) | |||||

| EBIT margin % | 5.3 | % | 1.7 | % | (1.8%) | |||||||

| Income (loss) from continuing operations before income taxes – Adjusted | $ | 265 | $ | 128 | $ | 159 | ||||||

| Interest expense, net | 9 | 10 | 5 | |||||||||

| Adjusted EBIT | $ | 274 | $ | 138 | $ | 164 | ||||||

| Adjusted EBIT margin % | 5.4 | % | 2.8 | % | 3.1 | % | ||||||

15

Reconciliation of the non-GAAP measures, continued:

| 2010 | 2009 | 2008 | ||||||||||

| (in millions, except per share amounts) | ||||||||||||

| After-tax income: | ||||||||||||

| Income (loss) from continuing operations – Reported | $ | 169 | $ | 47 | $ | (79 | ) | |||||

| After-tax amounts excluded | 4 | 34 | 185 | |||||||||

| Canadian tax rate changes excluded | - | 4 | - | |||||||||

| Income (loss) from continuing operations after-tax – Adjusted | $ | 173 | $ | 85 | $ | 106 | ||||||

| Net income margin % | 3.3 | % | 1.0 | % | (1.5%) | |||||||

| Adjusted Net income margin % | 3.4 | % | 1.8 | % | 2.0 | % | ||||||

| Diluted earnings per share: | ||||||||||||

| Income (loss) from continuing operations – Reported | $ | 1.07 | $ | 0.30 | $ | (0.52 | ) | |||||

| Impairment and other charges | 0.04 | 0.16 | 1.20 | |||||||||

| Inventory reserve | - | 0.06 | - | |||||||||

| Money-market realized gain | (0.01 | ) | - | - | ||||||||

| Canadian tax rate changes | - | 0.02 | - | |||||||||

| Income from continuing operations – Adjusted | $ | 1.10 | $ | 0.54 | $ | 0.68 | ||||||

When assessing Return on Invested Capital ("ROIC"), the Company adjusts its results to reflect its operating leases as if they qualified for capital lease treatment. Operating leases are the primary financing vehicle used to fund store expansion and, therefore, we believe that the presentation of these leases as capital leases is appropriate. Accordingly, the asset base and net income amounts in the calculation of ROIC are adjusted to reflect this. ROIC, subject to certain adjustments, is also used as a measure in executive long-term incentive compensation. The closest GAAP measure is Return on Assets ("ROA") and is also represented below. ROA increased to 5.9 percent as compared with 1.7 percent in the prior year reflecting the Company's overall strong performance in 2010.

| 2010 | 2009 | 2008 | ||||||||||

| ROA (1) | 5.9 | % | 1.7 | % | (2.6%) | |||||||

| ROIC % (2) | 8.3 | % | 5.3 | % | 5.4 | % | ||||||

| (1) | Represents income (loss) from continuing operations of $169 million, $47 million, and $(79) million divided by average total assets of $2,856 million, $2,847 million, and $3,060 million for 2010, 2009, and 2008, respectively. |

| (2) | See below for the calculation of ROIC. |

| 2010 | 2009 | 2008 | ||||||||||

| (in millions) | ||||||||||||

| Adjusted EBIT | $ | 274 | $ | 138 | $ | 164 | ||||||

| + Rent expense less depreciation on capitalized operating leases (3) | 156 | 156 | 162 | |||||||||

| - Adjusted income tax expense (3) | (153 | ) | (104 | ) | (114 | ) | ||||||

| = Adjusted return after taxes | $ | 277 | $ | 190 | $ | 212 | ||||||

| Average total assets | $ | 2,856 | $ | 2,847 | $ | 3,060 | ||||||

| - Average cash, cash equivalents and short-term investments | (642 | ) | (499 | ) | (451 | ) | ||||||

| - Average non-interest bearing current liabilities | (461 | ) | (425 | ) | (464 | ) | ||||||

| - Average merchandise inventories | (1,048 | ) | (1,079 | ) | (1,201 | ) | ||||||

| + Average estimated asset base of capitalized operating leases (3) | 1,443 | 1,500 | 1,580 | |||||||||

| + 13-month average merchandise inventories | 1,177 | 1,268 | 1,378 | |||||||||

| = Average invested capital | $ | 3,325 | $ | 3,612 | $ | 3,902 | ||||||

| ROIC % | 8.3 | % | 5.3 | % | 5.4 | % | ||||||

| (3) | The determination of the capitalized assets and the adjustments to income have been calculated on a lease-by-lease basis and have been consistently calculated in each of the years presented above. The adjusted income tax expense represents the tax on adjusted pre-tax return. |

16

The following table represents a summary of sales and operating results, reconciled to income (loss) from continuing operations before income taxes.

| 2010 | 2009 | 2008 | ||||||||||

| (in millions) | ||||||||||||

| Sales | ||||||||||||

| Athletic Stores | $ | 4,617 | $ | 4,448 | $ | 4,847 | ||||||

| Direct-to-Customers | 432 | 406 | 390 | |||||||||

| $ | 5,049 | $ | 4,854 | $ | 5,237 | |||||||

| Operating Results | ||||||||||||

| Athletic Stores (1) | $ | 329 | $ | 114 | $ | (59 | ) | |||||

| Direct-to-Customers (2) | 30 | 32 | 43 | |||||||||

| 359 | 146 | (16 | ) | |||||||||

| Restructuring income (3) | - | 1 | - | |||||||||

| Division profit (loss) | 359 | 147 | (16 | ) | ||||||||

| Less: Corporate expense (4) | 97 | 67 | 87 | |||||||||

| Operating profit (loss) | 262 | 80 | (103 | ) | ||||||||

| Other income (5) | 4 | 3 | 8 | |||||||||

| Earnings before interest expense and income taxes | 266 | 83 | (95 | ) | ||||||||

| Interest expense, net | 9 | 10 | 5 | |||||||||

| Income (loss) from continuing operations before income taxes | $ | 257 | $ | 73 | $ | (100 | ) | |||||

| (1) | The year ended January 30, 2010 includes non-cash impairment charges totaling $32 million, which were recorded to write-down long-lived assets such as store fixtures and leasehold improvements at the Company's Lady Foot Locker, Kids Foot Locker, Footaction, and Champs Sports divisions. The year ended January 31, 2009 includes a $241 million charge representing long-lived store asset impairment, goodwill and other intangibles impairment, and store closing costs related to the Company's U.S. operations. |

| (2) | Included in the results for the year ended January 29, 2011 is a non-cash impairment charge of $10 million to write-down the CCS tradename intangible asset. Included in the results for the year ended January 30, 2010 is a non-cash impairment charge of $4 million to write off software development costs. |

| (3) | During the year ended January 30, 2010, the Company adjusted its 1999 restructuring reserves to reflect a favorable lease termination. |

| (4) | During the fourth quarter of 2009, the Company restructured its organization by consolidating the Lady Foot Locker, Foot Locker U.S., Kids Foot Locker, and Footaction businesses in addition to reducing corporate staff, resulting in a $5 million charge. Included in corporate expense for the year ended January 31, 2009 is a $3 million other-than-temporary impairment charge related to the investment in the Reserve International Liquidity Fund. Additionally, for the year ended January 31, 2009 the Company recorded a $15 million impairment charge on the Northern Group note receivable. |

| (5) | Other income includes non-operating items, such as gains from insurance recoveries, gains on the repurchase and retirement of bonds, royalty income, the changes in fair value, premiums paid and realized gains associated with foreign currency option contracts. Included in the year ended January 29, 2011 is a $2 million gain to reflect the Company's settlement of its investment in the Reserve International Liquidity Fund. |

All references to comparable-store sales for a given period relate to sales from stores that are open at the period-end, that have been open for more than one year, and exclude the effect of foreign currency fluctuations. Accordingly, stores opened and closed during the period are not included. Sales from the Direct-to-Customers segment are included in the calculation of comparable-store sales for all periods presented. Sales from acquired businesses that include the purchase of inventory are included in the computation of comparable-store sales after 15 months of operations. Accordingly, effective with the first quarter of 2010, CCS internet and catalog sales have been included in the computation of comparable-store sales.

Sales increased to $5,049 million, or by 4.0 percent as compared with 2009. Excluding the effect of foreign currency fluctuations, sales increased 4.6 percent as compared with 2009. Comparable-store sales increased by 5.8 percent.

Sales of $4,854 million in 2009 decreased by 7.3 percent from sales of $5,237 million in 2008. Excluding the effect of foreign currency fluctuations, sales declined 6.1 percent as compared with 2008. Comparable-store sales decreased by 6.3 percent.

17

Gross Margin

Gross margin as a percentage of sales was 30.0 percent in 2010 increasing 260 basis points as compared with 2009. In 2009, the Company recorded a $14 million inventory reserve on certain aged apparel as part of its new apparel strategy. Excluding this charge, gross margin would have increased by 230 basis points as compared with 2009. This increase reflected an increase of 150 basis points in the merchandise margin rate reflecting lower markdowns as the Company was less promotional during the year as compared with the prior year. Lower vendor allowances during the current year, reflecting the overall lower promotional activity, negatively affected gross margin by 10 basis points. The increase in the gross margin also reflected a decrease of 80 basis points in the occupancy and buyers salary expense rate reflecting improved leverage and expense reductions.

Gross margin as a percentage of sales was 27.4 percent in 2009 decreasing 50 basis points as compared with 2008. The decrease in the gross margin reflected an increase of 30 basis points in the merchandise margin rate due to lower markdowns, offset by an 80 basis point increase in the occupancy rate due to lower sales. Vendor allowances were essentially the same as compared with 2008 and did not significantly affect the gross margin rate. Excluding the $14 million inventory reserve recorded in 2009, gross margin would have declined by 20 basis points as compared with 2008.

Selling, General and Administrative ExpensesSelling, general and administrative ("SG&A") expenses increased by $39 million to $1,138 million in 2010, or by 3.5 percent, as compared with 2009. SG&A as a percentage of sales decreased to 22.5 percent as compared with 22.6 percent in 2009, due to expense management and the increase in sales. Excluding the effect of foreign currency fluctuations in 2010, SG&A increased by $47 million. This increase primarily reflects higher incentive compensation costs totaling $45 million, partially offset by expense management efforts.

SG&A expenses decreased by $75 million to $1,099 million in 2009, or by 6.4 percent, as compared with 2008. SG&A as a percentage of sales increased to 22.6 percent as compared with 22.4 percent in 2008, due to the decline in sales. Excluding the effect of foreign currency fluctuations in 2009, SG&A decreased by $64 million. This decrease reflects lower divisional expenses primarily due to operating fewer stores and compensation expense, offset, in part, by increased pension expense of $13 million.

Corporate ExpenseCorporate expense consists of unallocated general and administrative expenses as well as depreciation and amortization related to the Company's corporate headquarters, centrally managed departments, unallocated insurance and benefit programs, certain foreign exchange transaction gains and losses, and other items.

Corporate expense increased by $30 million to $97 million in 2010 as compared with 2009. Depreciation and amortization included in corporate expense was $12 million in 2010 and $13 million in 2009. Incentive compensation costs included within corporate expense represent an increase of $29 million as a result of the Company's outperformance as compared with plan. Additionally, 2009 included a $5 million charge related to the reorganization of its operations and corporate staff reductions.

Corporate expense decreased by $20 million to $67 million in 2009 as compared with 2008. Depreciation and amortization included in corporate expense was $13 million in both 2009 and 2008. Included in 2008 corporate expense were charges that totaled $18 million, which represented a $3 million other-than-temporary impairment charge related to a short-term investment and a $15 million impairment charge related to the Northern Group note receivable. The balance of the change represents lower incentive compensation costs as well as income of $3 million related to the final settlement of the Visa/MasterCard litigation. These reductions in corporate expense were offset, in part, by higher pension expense.

Depreciation and AmortizationDepreciation and amortization of $106 million decreased by 5.4 percent in 2010 from $112 million in 2009. This decrease primarily reflects reduced depreciation and amortization resulting from store long-lived asset impairment charges recorded in 2009. Additionally, foreign currency fluctuations reduced depreciation and amortization expense by $1 million.

18

Depreciation and amortization of $112 million decreased by 13.8 percent in 2009 from $130 million in 2008. This decrease primarily reflects the effect of the impairment charges offset, in part, by increased depreciation and amortization related to the Company's capital spending, as well as the amortization expense associated with the CCS customer list intangible. The effect of foreign currency fluctuations was not significant.

Interest Expense, Net

| 2010 | 2009 | 2008 | ||||||||||

| (in millions) | ||||||||||||

| Interest expense | $ | 14 | $ | 13 | $ | 16 | ||||||

| Interest income | (5 | ) | (3 | ) | (11 | ) | ||||||

| Interest expense, net | $ | 9 | $ | 10 | $ | 5 | ||||||

| Weighted-average interest rate (excluding fees): | ||||||||||||

| Long-term debt | 7.6 | % | 7.3 | % | 6.2 | % | ||||||

Interest expense of $14 million increased by $1 million as compared with 2009. The increase in interest expense primarily relates to higher fees associated with the revolving credit facility. Interest expense in 2010 includes $1 million in amortization of the gain realized from the termination of the interest rate swap. The Company did not have any short-term borrowings for any of the periods presented. Interest income of $5 million increased from $3 million in 2009 primarily reflecting income earned on higher cash and cash equivalent balances.