|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

For the Fiscal Year Ended February 3, 2018 |

| Commission File Number: 1-13536 |

7 West Seventh Street

Cincinnati, Ohio 45202

(513) 579-7000

and

151 West 34th Street

New York, New York 10001

(212) 494-1602

Incorporated in Delaware |

| I.R.S. No. 13-3324058 |

Securities Registered Pursuant to Section 12(b) of the Act:

Title of Each Class |

| Name of Each Exchange on Which Registered |

Common Stock, par value $.01 per share |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ý |

| Accelerated filer o |

| Non-accelerated filer o (Do not check if a smaller reporting company) |

| Smaller reporting company o |

| Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

The aggregate market value of the registrant's common stock held by non-affiliates of the registrant as of the last business day of the registrant's most recently completed second fiscal quarter (July 29, 2017) was approximately $7,288,096,032 .

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

Class |

| Outstanding at March 3, 2018 |

Common Stock, $0.01 par value per share |

| 305,322,583 shares |

DOCUMENTS INCORPORATED BY REFERENCE

Document | Parts Into Which Incorporated |

Proxy Statement for the Annual Meeting of Stockholders to be held May 18, 2018 | Part III |

|

Unless the context requires otherwise, references to "Macy's" or the "Company" are references to Macy's and its subsidiaries and references to " 2017 ," " 2016 ," " 2015 ," " 2014 " and " 2013 " are references to the Company's fiscal years ended February 3, 2018 , January 28, 2017 , January 30, 2016 , January 31, 2015 and February 1, 2014 , respectively. Fiscal year 2017 included 53 weeks; fiscal years 2016, 2015, 2014 and 2013 included 52 weeks.

Forward-Looking Statements

This report and other reports, statements and information previously or subsequently filed by the Company with the Securities and Exchange Commission (the "SEC") contain or may contain forward-looking statements. Such statements are based upon the beliefs and assumptions of, and on information available to, the management of the Company at the time such statements are made. The following are or may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995: (i) statements preceded by, followed by or that include the words "may," "will," "could," "should," "believe," "expect," "future," "potential," "anticipate," "intend," "plan," "think," "estimate" or "continue" or the negative or other variations thereof, and (ii) statements regarding matters that are not historical facts. Such forward-looking statements are subject to various risks and uncertainties, including risks and uncertainties relating to:

• | the possible invalidity of the underlying beliefs and assumptions; |

• | competitive pressures from department and specialty stores, general merchandise stores, manufacturers' outlets, off-price and discount stores, and all other retail channels, including the Internet, catalogs and television; |

• | the Company's ability to remain competitive and relevant as consumers' shopping behaviors migrate to other shopping channels and to maintain its brand and reputation; |

• | general consumer-spending levels, including the impact of general economic conditions, consumer disposable income levels, consumer confidence levels, the availability, cost and level of consumer debt, the costs of basic necessities and other goods and the effects of the weather or natural disasters; |

• | conditions to, or changes in the timing of, proposed transactions, including planned store closures, and changes in expected synergies, cost savings and non-recurring charges; |

• | the success of the Company's operational decisions (e.g., product curation and marketing programs) and strategic initiatives; |

• | possible systems failures and/or security breaches, including, any security breach that results in the theft, transfer or unauthorized disclosure of customer, employee or company information, or the failure to comply with various laws applicable to the Company in the event of such a breach; |

• | the cost of employee benefits as well as attracting and retaining quality employees; |

• | transactions involving our real estate portfolio; |

• | the seasonal nature of the Company's business; |

• | possible changes or developments in social, economic, business, industry, market, legal and regulatory circumstances and conditions; |

• | possible actions taken or omitted to be taken by third parties, including customers, suppliers, business partners, competitors and legislative, regulatory, judicial and other governmental authorities and officials; |

• | changes in relationships with vendors and other product and service providers; |

• | currency, interest and exchange rates and other capital market, economic and geo-political conditions; |

• | unstable political conditions, civil unrest, terrorist activities and armed conflicts; |

• | the possible inability of the Company's manufacturers or transporters to deliver products in a timely manner or meet the Company's quality standards; |

• | the Company's reliance on foreign sources of production, including risks related to the disruption of imports by labor disputes, regional health pandemics, and regional political and economic conditions; and |

• | duties, taxes, other charges and quotas on imports |

In addition to any risks and uncertainties specifically identified in the text surrounding such forward-looking statements, the statements in the immediately preceding sentence and the statements under captions such as "Risk Factors" in reports, statements and information filed by the Company with the SEC from time to time constitute cautionary statements identifying important factors that could cause actual amounts, results, events and circumstances to differ materially from those expressed in or implied by such forward-looking statements.

Item 1. | Business. |

General

The Company is a corporation organized under the laws of the State of Delaware in 1985. The Company and its predecessors have been operating department stores since 1830. The Company operates approximately 850 stores in 44 states, the District of Columbia, Guam and Puerto Rico. As of February 3, 2018 , the Company's operations were conducted through Macy's, Bloomingdale's, Bloomingdale's The Outlet, Macy's Backstage, bluemercury and Macy's China Limited. In addition, Bloomingdale's in Dubai, United Arab Emirates and Al Zahra, Kuwait are operated under license agreements with Al Tayer Insignia, a company of Al Tayer Group, LLC.

The Company sells a wide range of merchandise, including apparel and accessories (men's, women's and children's), cosmetics, home furnishings and other consumer goods. The specific assortments vary by size of store, merchandising assortments and character of customers in the trade areas. Most stores are located at urban or suburban sites, principally in densely populated areas across the United States.

For 2017 , 2016 and 2015 , the following merchandise constituted the following percentages of sales:

| 2017 |

| 2016 |

| 2015 | |||

Women's Accessories, Intimate Apparel, Shoes, Cosmetics and Fragrances | 38 | % |

| 38 | % |

| 38 | % |

Women's Apparel | 23 | |

| 23 | |

| 23 | |

Men's and Children's | 23 | |

| 23 | |

| 23 | |

Home/Miscellaneous | 16 | |

| 16 | |

| 16 | |

| 100 | % |

| 100 | % |

| 100 | % |

In 2017 , the Company's subsidiaries provided various support functions to the Company's retail operations on an integrated, company-wide basis.

• | The Company's bank subsidiary, FDS Bank, provides credit processing, certain collections, customer service and credit marketing services in respect of all credit card accounts that are owned either by Department Stores National Bank ("DSNB"), a subsidiary of Citibank, N.A., or FDS Bank and that constitute a part of the credit programs of the Company's retail operations. |

• | Macy's Systems and Technology, Inc. ("MST"), a wholly-owned indirect subsidiary of the Company, provides operational electronic data processing and management information services to all of the Company's operations other than bluemercury and Macy's China Limited. |

• | Macy's Merchandising Group, Inc. ("MMG"), a wholly-owned direct subsidiary of the Company, and its subsidiary Macy's Merchandising Group International, LLC, are responsible for the design, development and marketing of Macy's private label brands and certain licensed brands. Bloomingdale's uses MMG for a small portion of its private label merchandise. The Company believes that its private label merchandise differentiates its merchandise assortments from those of its competitors and delivers exceptional value to its customers. MMG also offers its services, either directly or indirectly, to unrelated third parties. |

• | Macy's Logistics and Operations ("Macy's Logistics"), a division of a wholly-owned indirect subsidiary of the Company, provides warehousing and merchandise distribution services for the Company's operations and digital customer fulfillment. |

The Company's executive offices are located at 7 West 7 th Street, Cincinnati, Ohio 45202, telephone number: (513) 579-7000 and 151 West 34 th Street, New York, New York 10001, telephone number: (212) 494-1602.

Employees

As of February 3, 2018 , excluding seasonal employees, the Company had approximately 130,000 employees, primarily including regular full-time and part-time. Because of the seasonal nature of the retail business, the number of employees peaks in the holiday season. Approximately 7% of the Company's employees were represented by unions as of February 3, 2018 .

Seasonality

The retail business is seasonal in nature with a high proportion of sales and operating income generated in the months of November and December. Working capital requirements fluctuate during the year, increasing in mid-summer in anticipation of the fall merchandising season and increasing substantially prior to the holiday season when the Company carries significantly higher inventory levels.

Purchasing

The Company purchases merchandise from many suppliers, no one of which accounted for more than 5% of the Company's purchases during 2017 . The Company has no material long-term purchase commitments with any of its suppliers, and believes that it is not dependent on any one supplier. The Company considers its relations with its suppliers to be good.

Private Label Brands and Related Trademarks

The principal private label brands currently offered by the Company include Alfani, American Rag, Aqua, Bar III, Belgique, Charter Club, Club Room, Epic Threads, first impressions, Giani Bernini, Greg Norman for Tasso Elba, Holiday Lane, Home Design, Hotel Collection, Hudson Park, Ideology, I-N-C, jenni, JM Collection, John Ashford, Karen Scott, lune+aster, M-61, Maison Jules, Martha Stewart Collection, Material Girl, Morgan Taylor, Oake, Sky, Style & Co., Sutton Studio, Tasso Elba, Thalia Sodi, the cellar, and Tools of the Trade.

The trademarks associated with the Company's aforementioned private label brands, other than American Rag, Greg Norman for Tasso Elba, Martha Stewart Collection, Material Girl and Thalia Sodi are owned by the Company. The American Rag, Greg Norman, Martha Stewart Collection, Material Girl and Thalia Sodi brands are owned by third parties, which license the trademarks associated with such brands to Macy's pursuant to agreements which have renewal rights that extend through 2050, 2020, 2025, 2030 and 2030, respectively.

Competition

The retail industry is intensely competitive. The Company's operations compete with many retail formats, including department stores, specialty stores, general merchandise stores, off-price and discount stores, manufacturers' outlets, online retailers, catalogs and television shopping, among others. The Company seeks to attract customers by offering most wanted selections, obvious value, and distinctive marketing in stores that are located in premier locations, and by providing an exciting shopping environment and superior service through an omnichannel experience. Other retailers may compete for customers on some or all of these bases, or on other bases, and may be perceived by some potential customers as being better aligned with their particular preferences.

Available Information

The Company makes its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act available free of charge through its internet website at http://www.macysinc.com as soon as reasonably practicable after it electronically files such material with, or furnishes it to, the SEC. The public also may read and copy any of these filings at the SEC's Public Reference Room, 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-732-0330. The SEC also maintains an Internet site that contains the Company's filings; the address of that site is http://www.sec.gov . In addition, the Company has made the following available free of charge through its website at http://www.macysinc.com :

• | Charters of the Audit Committee, Compensation and Management Development Committee, Finance Committee, and Nominating and Corporate Governance Committee, |

• | Corporate Governance Principles, |

• | Lead Independent Director Policy, |

• | Non-Employee Director Code of Business Conduct and Ethics, |

4

• | Code of Conduct, |

• | Standards for Director Independence, |

• | Related Party Transaction Policy, and |

• | Method to Facilitate Receipt, Retention and Treatment of Communications. |

Any of these items are also available in print to any shareholder who requests them. Requests should be sent to the Corporate Secretary of Macy's, Inc. at 7 West 7 th Street, Cincinnati, OH 45202.

Executive Officers of the Registrant

The following table sets forth certain information as of March 23, 2018 regarding the executive officers of the Company:

Name |

| Age |

| Position with the Company | |

Jeff Gennette |

| 56 | |

| Chairman of the Board and Chief Executive Officer; Director |

Elisa D. Garcia |

| 60 | |

| Chief Legal Officer and Secretary |

Karen M. Hoguet |

| 61 | |

| Chief Financial Officer |

Danielle L. Kirgan |

| 42 | |

| Chief Human Resources Officer |

Harry A. Lawton III |

| 43 | |

| President |

Felicia Williams |

| 52 | |

| Executive Vice President, Controller and Enterprise Risk Officer |

Executive Officer Biographies

Jeff Gennette has been Chief Executive Officer of the Company since March 2017 and Chairman of the Board since January 2018; prior thereto he was President from March 2014 to August 2017, Chief Merchandising Officer from February 2009 to March 2014, Chairman and Chief Executive Officer of Macy's West in San Francisco from February 2008 to February 2009 and Chairman and Chief Executive Officer of Seattle-based Macy's Northwest from February 2006 through February 2008.

Elisa D. Garcia has been Chief Legal Officer and Secretary of the Company since September 2016; prior thereto she served as Chief Legal Officer of Office Depot, Inc. from 2013 to September 2016, and Executive Vice President, General Counsel and Secretary from 2007 to 2013.

Karen M. Hoguet has been Chief Financial Officer of the Company since October 1997.

Danielle L. Kirgan has been Chief Human Resources Officer of the Company since October 2017; prior thereto she served as Senior Vice President, People at American Airlines Group, Inc. from October 2016 to October 2017, Chief Human Resources Officer at Darden Restaurants, Inc. from 2010 to 2016, Vice President, Global Human Resources at ACI Worldwide, Inc. in 2009, and Vice President, Human Resources at Conagra Foods, Inc. from 2004 to 2008.

Harry (Hal) A. Lawton III has been President of the Company since September 2017; prior thereto he served as Senior Vice President, North America at eBay, Inc. from 2015 to September 2017 and held a number of leadership positions at Home Depot, Inc. from 2005 to 2015, including Senior Vice President of Merchandising and head of Home Depot's online business.

Felicia Williams has been Executive Vice President, Controller and Enterprise Risk Officer of the Company since June 2016; prior thereto she served as Senior Vice President, Finance and Risk Management from February 2011 to June 2016, Senior Vice President, Treasury and Risk Management from September 2009 to February 2011, Vice President, Finance and Risk Management from October 2008 to September 2009, and Vice President, Internal Audit from March 2004 to October 2008.

Recent Developments

On April 4, 2018, the Company issued a press release announcing that Karen M. Hoguet has decided to retire. At the Company's request, Ms. Hoguet will remain with the Company until February 2019 to ensure a smooth transition.

Item 1A. | Risk Factors. |

5

In evaluating Macy's, the risks described below and the matters described in "Forward-Looking Statements" should be considered carefully. Such risks and matters are numerous and diverse, may be experienced continuously or intermittently, and may vary in intensity and effect. Any of such risks and matters, individually or in combination, could have a material adverse effect on our business, prospects, financial condition, results of operations and cash flows, as well as on the attractiveness and value of an investment in Macy's securities.

Strategic, Operational and Competitive Risks

Macy's strategic initiatives may not be successful, which could negatively affect our profitability and growth.

We are pursuing strategic initiatives to achieve our objective of accelerating profitable growth in our stores and our digital operations. This includes the adoption of new technologies, merchandising strategies and customer service initiatives all designed to improve the shopping experience. Our ability to achieve profitable growth is subject to the successful implementation of our strategic plans. If these investments or initiatives do not perform as expected or create implementation or operational difficulties, we may incur impairment charges and our profitability and growth could suffer.

Our sales and operating results depend on consumer preferences and consumer spending.

The fashion and retail industries are subject to sudden shifts in consumer trends and consumer spending. Our sales and operating results depend in part on our ability to predict or respond to changes in fashion trends and consumer preferences in a timely manner. We develop new retail concepts and continuously adjust our industry position in certain major and private-label brands and product categories in an effort to satisfy customers. Any sustained failure to anticipate, identify and respond to emerging trends in lifestyle and consumer preferences could negatively affect our business and results of operations.

Our sales are significantly affected by discretionary spending by consumers. Consumer spending may be affected by many factors outside of our control, including general economic conditions, consumer disposable income levels, consumer confidence levels, the availability, cost and level of consumer debt and consumer behaviors towards incurring and paying debt, the costs of basic necessities and other goods, the strength of the U.S. Dollar relative to foreign currencies and the effects of the weather or natural disasters. Any decline in discretionary spending by consumers could negatively affect our business and results of operations.

As we rely on the ability of our physical retail locations to remain relevant, providing desirable and sought-out shopping experiences is paramount to our financial success. Changes in consumer shopping habits, financial difficulties at other anchor tenants, significant mall vacancy issues, mall violence and new mall developments could each adversely impact the traffic at current retail locations and lead to a decline in our financial condition or performance.

We may not be able to successfully execute our real estate strategy.

We continue to explore opportunities to monetize our real estate portfolio, including sales of stores as well as non-store real estate such as warehouses, outparcels and parking garages. We also continue to evaluate our real estate portfolio to identify opportunities where the redevelopment value of our real estate exceeds the value of non-strategic operating locations. This strategy is multi-pronged and may include transactions, strategic alliances or other arrangements with mall developers or unrelated third-parties. Due to the cyclical nature of real estate markets, the performance of our real estate strategy is inherently volatile and could have a significant impact on our results of operations or financial condition.

Macy's revenues and cash requirements are affected by the seasonal nature of our business.

Our business is seasonal, with a high proportion of revenues and operating cash flows generated during the second half of the year, which includes the fall and holiday selling seasons. A disproportionate amount of our revenues fall in the fourth quarter, which coincides with the holiday season. We incur significant additional expenses in the period leading up to the months of November and December in anticipation of higher sales volume in those periods, including for additional inventory, advertising and employees.

We depend on our ability to attract and retain quality employees.

Our business is dependent upon attracting and retaining quality employees. Macy's has a large number of employees, many of whom are in entry level or part-time positions with historically high rates of turnover. Macy's ability to meet our labor needs while controlling the costs associated with hiring and training new employees is subject to external factors such as unemployment levels, prevailing wage rates, minimum wage legislation and changing demographics. In addition, as a large and complex enterprise operating in a highly competitive and challenging business environment, Macy's is highly dependent upon management personnel to develop and effectively execute successful business strategies and tactics. Any

6

circumstances that adversely impact our ability to attract, train, develop and retain quality employees throughout the organization could negatively affect our business and results of operations.

Macy's depends on the success of advertising and marketing programs.

Our business depends on effective marketing and high customer traffic. Macy's has many initiatives in this area, and we often change advertising and marketing programs. There can be no assurance as to our continued ability to effectively execute our advertising and marketing programs, and any failure to do so could negatively affect our business and results of operations.

If cash flows from our private label credit card decrease, our financial and operational results may be negatively impacted.

We sold most of our credit accounts and related receivables to Citibank. Following the sale, we share in the economic performance of the credit card program with Citibank. Deterioration in economic or political conditions could adversely affect the volume of new credit accounts, the amount of credit card program balances and the ability of credit card holders to pay their balances. These conditions could result in Macy's receiving lower payments under the credit card program.

Credit card operations are subject to many federal and state laws that may impose certain requirements and limitations on credit card providers. Citibank and our subsidiary bank, FDS Bank, may be required to comply with regulations that may negatively impact the operation of our private label credit card. In turn, this negative impact may affect our revenue streams derived from the sale of such credit card accounts and negatively impact our financial results.

Gross margins could suffer if we are unable to effectively manage our inventory.

Our profitability depends on our ability to manage inventory levels and respond to shifts in consumer demand patterns. Overestimating customer demand for merchandise will likely result in the need to record inventory markdowns and sell excess inventory at clearance prices which would negatively impact our gross margins and operating results. Underestimating customer demand for merchandise can lead to inventory shortages, missed sales opportunities and negative customer experiences.

Our defined benefit plan funding requirements or plan settlement expense could impact our financial results and cash flow.

Significant changes in interest rates, decreases in the fair value of plan assets and benefit payments could affect the funded status of our plans and could increase future funding requirements of the plans. A significant increase in future funding requirements could have a negative impact on our cash flows, financial condition or results of operations.

As of February 3, 2018 , we had unrecognized actuarial losses of $992 million for the funded defined benefit pension plan (the "Pension Plan") and $244 million for the unfunded defined benefit supplementary retirement plan (the "SERP"). These plans allow eligible retiring employees to receive lump sum distributions of benefits earned. Under applicable accounting rules, if annual lump sum distributions exceed an actuarially determined threshold of the total of the annual service and interest costs, we would be required to recognize in the current period of operations a settlement expense of a portion of the unrecognized actuarial loss and could have a negative impact on our results of operations.

Increases in the cost of employee benefits could impact our financial results and cash flow.

Our expenses relating to employee health benefits are significant. Unfavorable changes in the cost of such benefits could negatively affect our financial results and cash flow. Healthcare costs have risen significantly in recent years, and recent legislative and private sector initiatives regarding healthcare reform have resulted and could continue to result in significant changes to the U.S. healthcare system. Due to uncertainty regarding legislative or regulatory changes, we are not able to fully determine the impact that future healthcare reform will have on our company-sponsored medical plans.

If our company's reputation and brand are not maintained at a high level, our operations and financial results may suffer.

We believe our reputation and brand are partially based on the perception that we act equitably and honestly in dealing with our customers, employees, business partners and shareholders. Our reputation and brand may be deteriorated by any incident that erodes the trust or confidence of our customers or the general public, particularly if the incident results in significant adverse publicity or governmental inquiry. In addition, information concerning us, whether or not true, may be instantly and easily posted on social media platforms at any time, which information may be adverse to our reputation or brand. The harm may be immediate without affording us an opportunity for redress or correction. If our reputation or

7

brand is damaged, our customers may refuse to continue shopping with us, potential employees may be unwilling to work for us, business partners may be discouraged from seeking future business dealings with us and, as a result, our operations and financial results may suffer.

Macy's faces significant competition in the retail industry and we depend on our ability to differentiate Macy's in retail's ever-changing environment.

We conduct our retail merchandising business under highly competitive conditions. Although Macy's is one of the nation's largest retailers, we have numerous and varied competitors at the national and local levels, including department stores, specialty stores, general merchandise stores, off-price and discount stores, manufacturers' outlets, online retailers, catalogs and television shopping, among others. Competition may intensify as our competitors enter into business combinations or alliances. Competition is characterized by many factors, including assortment, advertising, price, quality, service, location, reputation and credit availability. Any failure by us to compete effectively could negatively affect our business and results of operations.

As consumers continue to migrate online, we face pressures to not only compete from a price perspective with our competitors, some of whom sell the same products, but also to differentiate Macy's to stay relevant in retail's ever-changing industry. We continue to significantly invest in our omnichannel capabilities in order to provide a seamless shopping experience to our customers between our brick and mortar locations and our online and mobile environments. Insufficient, untimely or misguided investments in this area could significantly impact our profitability and growth and affect our ability to attract new customers, as well as maintain our existing ones.

In addition, declining customer store traffic and migration of sales from brick and mortar stores to digital platforms could lead to store closures, restructuring and other costs that could adversely impact our results of operations and cash flows.

Our sales and operating results could be adversely affected by product safety concerns.

If Macy's merchandise offerings do not meet applicable safety standards or consumers' expectations regarding safety, we could experience decreased sales, increased costs and/or be exposed to legal and reputational risk. Events that give rise to actual, potential or perceived product safety concerns could expose Macy's to government enforcement action and/or private litigation. Reputational damage caused by real or perceived product safety concerns could negatively affect our business and results of operations.

Technology and Data Security Risks

A material disruption in our computer systems could adversely affect our business or results of operations.

We rely extensively on our computer systems to process transactions, summarize results and manage our business. Our computer systems are subject to damage or interruption from power outages, computer and telecommunications failures, computer viruses, cyber-attack or other security breaches, catastrophic events such as fires, floods, earthquakes, tornadoes, hurricanes, acts of war or terrorism, and usage errors by our employees. If our computer systems are damaged or cease to function properly, including a material disruption in our ability to authorize and process transactions at our stores or on our online systems, we may have to make a significant investment to fix or replace them, and we may suffer loss of critical data and interruptions or delays in our operations. Any material interruption in our computer systems could negatively affect our business and results of operations.

If our technology-based e-commerce systems do not function properly, our operating results could be materially adversely affected.

Customers are increasingly using computers, tablets and smart phones to shop online and to do price and comparison shopping. We strive to anticipate and meet our customers' changing expectations and are focused on building a seamless shopping experience across our omnichannel business. Any failure to provide user-friendly, secure e-commerce platforms that offer a variety of merchandise at competitive prices with low cost and quick delivery options that meet customers' expectations could place us at a competitive disadvantage, result in the loss of e-commerce and other sales, harm our reputation with customers and have a material adverse impact on the growth of our business and our operating results.

A breach of information technology systems could adversely affect our reputation, business partner and customer relationships, operations and result in high costs.

Through our sales, marketing activities, and use of third-party information, we collect and store certain non-public personal information that customers provide to purchase products or services, enroll in promotional programs, register on websites, or otherwise communicate to us. This may include phone numbers, driver license numbers, contact preferences, personal information stored on electronic devices, and payment information, including credit and debit card data. We

8

gather and retain information about employees in the normal course of business. We may share information about such persons with vendors that assist with certain aspects of our business. In addition, our online operations depend upon the transmission of confidential information over the Internet, such as information permitting cashless payments.

We employ safeguards for the protection of this information and have made significant investments to secure access to our information technology network. For instance, we have implemented authentication protocols, installed firewalls and anti-virus/anti-malware software, conducted continuous risk assessments, and established data security breach preparedness and response plans. We also employ encryption and other methods to protect our data, promote security awareness with our associates and work with business partners in an effort to create secure and compliant systems.

However, these protections may be compromised as a result of third-party security breaches, burglaries, cyberattack, errors by employees or employees of third-party vendors, or contractors, misappropriation of data by employees, vendors or unaffiliated third-parties, or other irregularities that may result in persons obtaining unauthorized access to company data.

Retail data frequently targeted by cybercriminals is consumer credit card data, personally identifiable information, including social security numbers, and health care information. For retailers, point of sale and e-commerce websites are often attacked through compromised credentials, including those obtained through phishing, vishing and credential stuffing. Other methods of attack include advanced malware, the exploitation of software and operating vulnerabilities, and physical device tampering/skimming at card reader units and we believe these attack methods will continue to evolve.

Despite instituting controls for the protection of such information, no commercial or government entity can be entirely free of vulnerability to attack or compromise given that the techniques used to obtain unauthorized access, disable or degrade service change frequently. During the normal course of business, we have experienced and expect to continue to experience attempts to compromise our information systems. Unauthorized parties may attempt to gain access to our systems or facilities, or those of third parties with whom we do business, through fraud, trickery, or other forms of deception to employees, contractors, vendors and temporary staff. We may be unable to protect the integrity of our systems or company data. An alleged or actual unauthorized access or unauthorized disclosure of non-public personal information could:

• | materially damage our reputation and brand, negatively affect customer satisfaction and loyalty, expose us to individual claims or consumer class actions, administrative, civil or criminal investigations or actions, and infringe on proprietary information; and |

• | cause us to incur substantial costs, including costs associated with remediation of information technology systems, customer protection costs and incentive payments for the maintenance of business relationships, litigation costs, lost revenues resulting from negative changes in consumer shopping patterns, unauthorized use of proprietary information or the failure to retain or attract customers following an attack. While we maintain insurance coverage that may, subject to policy terms and conditions, cover certain aspects of cyber risks, such insurance coverage may be unavailable or insufficient to cover all losses or all types of claims that may arise in the continually evolving area of cyber risk. |

Supply Chain and Third Party Risks

Macy's depends upon designers, vendors and other sources of merchandise, goods and services. Our business could be affected by disruptions in, or other legal, regulatory, political or economic issues associated with, our supply network.

Our relationships with established and emerging designers have been a significant contributor to Macy's past success. Our ability to find qualified vendors and access products in a timely and efficient manner is often challenging, particularly with respect to goods sourced outside the United States. Our procurement of goods and services from outside the United States is subject to risks associated with political or financial instability, trade restrictions, tariffs, currency exchange rates, transport capacity and costs and other factors relating to foreign trade. We source the majority of our merchandise from manufacturers located outside of the U.S., primarily Asia, and any major changes in tax policy or trade relations, such as the disallowance of tax deductions for imported merchandise or the imposition of unilateral tariffs on imported goods, could have a material adverse effect on our business, results of operations and liquidity. In addition, the procurement of all our goods and services are subject to the effects of price increases which we may or may not be able to pass through to our customers. All of these factors may affect our ability to access suitable merchandise on acceptable terms, are beyond our control and could negatively affect our business and results of operations

Disruption of global sourcing activities and Macy's own brands' quality concerns could negatively impact brand reputation and earnings.

9

Economic and civil unrest in areas of the world where we source products, as well as shipping and dockage issues, could adversely impact the availability or cost of our products, or both. Most of Macy's goods imported to the U.S. arrive from Asia through ports located on the U.S. west coast and are subject to potential disruption due to labor unrest, security issues or natural disasters affecting any or all of these ports. In addition, in recent years, we have substantially increased the number and types of merchandise that are sold under Macy's proprietary brands. While we have focused on the quality of our proprietary branded products, we rely on third-parties to manufacture these products. Such third-party manufacturers may prove to be unreliable, the quality of our globally sourced products may vary from expectations and standards, the products may not meet applicable regulatory requirements which may require us to recall these products, or the products may infringe upon the intellectual property rights of other third-parties. As we seek indemnities from manufacturers of these products, the uncertainty of recovering on such indemnity and the lack of understanding of U.S. product liability laws in certain foreign jurisdictions make it more likely that we may have to respond to claims or complaints from customers.

Parties with whom Macy's does business may be subject to insolvency risks or may otherwise become unable or unwilling to perform on their obligations to us.

Macy's is a party to contracts, transactions and business relationships with various third parties, including, without limitation, vendors, suppliers, service providers, lenders and participants in joint ventures, strategic alliances and other joint commercial relationships, pursuant to which such third parties have performance, payment and other obligations to Macy's. In some cases, we depend upon such third parties to provide essential leaseholds, products, services or other benefits, including with respect to store and distribution center locations, merchandise, advertising, software development and support, logistics, other agreements for goods and services in order to operate our business in the ordinary course, extensions of credit, credit card accounts and related receivables, and other vital matters. Current economic, industry and market conditions could result in increased risks to Macy's associated with the potential financial distress or insolvency of such third parties. If any of these third parties were to become subject to bankruptcy, receivership or similar proceedings, the rights and benefits with respect to our contracts, transactions and business relationships with such third parties could be terminated, modified in a manner adverse to us, or otherwise impaired. We may be unable to arrange for alternate or replacement contracts, transactions or business relationships on terms as favorable as existing contracts, transactions or business relationships. Our inability to do so could negatively affect our cash flows, financial condition and results of operations.

Global, Legal and External Risks

Macy's business is subject to unfavorable economic and political conditions and other related risks.

Unfavorable global, domestic or regional economic or political conditions and other developments and risks could negatively affect our business and results of operations. For example, unfavorable changes related to interest rates, rates of economic growth, fiscal and monetary policies of governments, inflation, deflation, consumer credit availability, consumer debt levels, consumer debt payment behaviors, tax rates and policy, unemployment trends, energy prices, and other matters that influence the availability and cost of merchandise, consumer confidence, spending and tourism could negatively affect our business and results of operations. In addition, unstable political conditions, civil unrest, terrorist activities and armed conflicts may disrupt commerce and could negatively affect our business and results of operations.

Our effective tax rate is impacted by a number of factors, including changes in federal or state tax law, interpretation of existing laws and the ability to defend and support the tax positions taken on historical tax returns. Certain changes in any of these factors could materially impact the effective tax rate and net income.

Our business could be affected by extreme weather conditions, regional or global health pandemics or natural disasters.

Extreme weather conditions in the areas in which our stores are located could negatively affect our business and results of operations. For example, frequent or unusually heavy snowfall, ice storms, rainstorms or other extreme weather conditions over a prolonged period could make it difficult for our customers to travel to our stores and thereby reduce our sales and profitability. Our business is also susceptible to unseasonable weather conditions. For example, extended periods of unseasonably warm temperatures during the winter season or cool weather during the summer season could reduce demand for a portion of our inventory and thereby reduce our sales and profitability. In addition, extreme weather conditions could result in disruption or delay of production and delivery of materials and products in our supply chain and cause staffing shortages in our stores.

Our business and results of operations could also be negatively affected if a regional or global health pandemic were to occur, depending upon its location, duration and severity. To halt or delay the spread of disease, local, regional or national governments might limit or ban public gatherings or customers might avoid public places, such as our stores. A

10

regional or global health pandemic might also result in disruption or delay of production and delivery of materials and products in our supply chain and cause staffing shortages in our stores.

Natural disasters such as hurricanes, tornadoes and earthquakes, or a combination of these or other factors, could damage or destroy our facilities or make it difficult for customers to travel to our stores, thereby negatively affecting our business and results of operations.

Litigation, legislation or regulatory developments could adversely affect our business and results of operations.

We are subject to various federal, state and local laws, rules, regulations, inquiries and initiatives in connection with both our core business operations and our credit card and other ancillary operations (including the Credit Card Act of 2009 and the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010). Recent and future developments relating to such matters could increase our compliance costs and adversely affect the profitability of our credit card and other operations. We are also subject to anti-bribery, customs, child labor, truth-in-advertising and other laws, including consumer protection regulations and zoning and occupancy ordinances that regulate retailers generally and/or govern the importation, promotion and sale of merchandise and the operation of retail stores and warehouse facilities. Although we undertake to monitor changes in these laws, if these laws change without our knowledge, or are violated by importers, designers, manufacturers, distributors or agents, we could experience delays in shipments and receipt of goods or be subject to fines or other penalties under the controlling regulations, any of which could negatively affect our business and results of operations. In addition, we are regularly involved in various litigation matters that arise in the ordinary course of our business. Adverse outcomes in current or future litigation could negatively affect our financial condition, results of operations and cash flows.

Financial Risks

Inability to access capital markets could adversely affect our business or financial condition.

Changes in the credit and capital markets, including market disruptions, limited liquidity and interest rate fluctuations, may increase the cost of financing or restrict our access to this potential source of future liquidity. A decrease in the ratings that rating agencies assign to Macy's short and long-term debt may negatively impact our access to the debt capital markets and increase our cost of borrowing. In addition, our bank credit agreements require us to maintain specified interest coverage and leverage ratios. Our ability to comply with the ratios may be affected by events beyond our control, including prevailing economic, financial and industry conditions. If our results of operations or operating ratios deteriorate to a point where we are not in compliance with our debt covenants, and we are unable to obtain a waiver, much of our debt would be in default and could become due and payable immediately. Our assets may not be sufficient to repay in full this indebtedness, resulting in a need for an alternate source of funding. We cannot make any assurances that we would be able to obtain such an alternate source of funding on satisfactory terms, if at all, and our inability to do so could cause the holders of our securities to experience a partial or total loss of their investments in Macy's.

Factors beyond our control could affect Macy's stock price.

Macy's stock price, like that of other retail companies, is subject to significant volatility because of many factors, including factors beyond our control. These factors may include:

• | general economic, stock, credit and real estate market conditions; |

• | risks relating to Macy's business and industry, including those discussed above; |

• | strategic actions by us or our competitors; |

• | variations in our quarterly results of operations; |

• | future sales or purchases of Macy's Common Stock; and |

• | investor perceptions of the investment opportunity associated with Macy's Common Stock relative to other investment alternatives. |

We may fail to meet the expectations of our stockholders or of analysts at some time in the future. If the analysts that regularly follow Macy's stock lower their rating or lower their projections for future growth and financial performance, Macy's stock price could decline. Also, sales of a substantial number of shares of Macy's Common Stock in the public market or the appearance that these shares are available for sale could adversely affect the market price of Macy's Common Stock.

11

Item 1B. | Unresolved Staff Comments. |

None.

Item 2. | Properties. |

The properties of the Company consist primarily of stores and related facilities, including a logistics network. The Company also owns or leases other properties, including corporate office space in Cincinnati and New York and other facilities at which centralized operational support functions are conducted. As of February 3, 2018 , the operations of the Company included 852 stores in 44 states, the District of Columbia, Puerto Rico and Guam, comprising a total of approximately 128 million square feet. Of such stores, 370 were owned, 359 were leased, 118 stores were operated under arrangements where the Company owned the building and leased the land and five stores were comprised of partly owned and partly leased buildings. All owned properties are held free and clear of mortgages. Pursuant to various shopping center agreements, the Company is obligated to operate certain stores for periods of up to 20 years. Some of these agreements require that the stores be operated under a particular name. Most leases require the Company to pay real estate taxes, maintenance and other costs; some also require additional payments based on percentages of sales and some contain purchase options. Certain of the Company's real estate leases have terms that extend for a significant number of years and provide for rental rates that increase or decrease over time.

12

The Company's operations were conducted through the following branded store locations:

| 2017 |

| 2016 |

| 2015 | |||

Macy's | 660 | |

| 673 | |

| 737 | |

Bloomingdale's | 55 | |

| 55 | |

| 54 | |

bluemercury | 137 | |

| 101 | |

| 77 | |

| 852 | |

| 829 | |

| 868 | |

Store count activity was as follows:

| 2017 |

| 2016 |

| 2015 | |||

Store count at beginning of fiscal year | 829 | |

| 868 | |

| 823 | |

Stores opened | 38 | |

| 27 | |

| 26 | |

Acquisition of bluemercury stores | - | |

| - | |

| 62 | |

Stores closed or consolidated into existing centers | (15 | ) |

| (66 | ) |

| (43 | ) |

Store count at end of fiscal year | 852 | |

| 829 | |

| 868 | |

Additional information about the Company's stores as of February 3, 2018 is as follows:

Geographic Region |

| Total |

| Owned |

| Leased |

| Subject to a Ground Lease |

| Partly Owned and Partly Leased | |||||

North Central |

| 144 | |

| 81 | |

| 43 | |

| 19 | |

| 1 | |

Northeast |

| 258 | |

| 88 | |

| 140 | |

| 30 | |

| - | |

Northwest |

| 131 | |

| 44 | |

| 63 | |

| 21 | |

| 3 | |

South |

| 188 | |

| 110 | |

| 53 | |

| 25 | |

| - | |

Southwest |

| 131 | |

| 47 | |

| 60 | |

| 23 | |

| 1 | |

|

| 852 | |

| 370 | |

| 359 | |

| 118 | |

| 5 | |

The five geographic regions detailed in the foregoing table are based on the Company's Macy's-branded operational structure. The Company's retail stores are located at urban or suburban sites, principally in densely populated areas across the United States.

13

Additional information about the Company's logistics network as of February 3, 2018 is as follows:

Location |

| Primary Function |

| Owned or Leased |

| Square Footage (thousands) | |

Cheshire, CT |

| Direct to customer |

| Owned |

| 565 | |

Chicago, IL |

| Stores |

| Owned |

| 861 | |

Denver, CO |

| Stores |

| Leased |

| 20 | |

Goodyear, AZ |

| Direct to customer |

| Owned |

| 960 | |

Hayward, CA |

| Stores |

| Owned |

| 386 | |

Houston, TX |

| Stores |

| Owned |

| 1,124 | |

Joppa, MD |

| Stores |

| Owned |

| 850 | |

Kapolei, HI |

| Stores |

| Leased |

| 260 | |

Los Angeles, CA |

| Stores |

| Owned |

| 1,178 | |

Martinsburg, WV |

| Direct to customer |

| Owned |

| 1,300 | |

Miami, FL |

| Stores |

| Leased |

| 535 | |

Portland, TN |

| Direct to customer |

| Owned |

| 950 | |

Raritan, NJ |

| Stores |

| Owned |

| 980 | |

Sacramento, CA |

| Direct to customer |

| Leased |

| 385 | |

Secaucus, NJ |

| Stores |

| Leased |

| 675 | |

South Windsor, CT |

| Stores |

| Owned |

| 510 | |

Stone Mountain, GA |

| Stores |

| Owned |

| 1,000 | |

Tampa, FL |

| Stores |

| Owned |

| 670 | |

Tulsa, OK |

| Direct to customer |

| Owned |

| 1,300 | |

Tukwila, WA |

| Stores |

| Leased |

| 500 | |

Union City, CA |

| Stores |

| Leased |

| 165 | |

Youngstown, OH |

| Stores |

| Owned |

| 851 | |

Item 3. | Legal Proceedings. |

The Company and its subsidiaries are involved in various proceedings that are incidental to the normal course of their businesses. As of the date of this report, the Company does not expect that any of such proceedings will have a material adverse effect on the Company's financial position or results of operations.

14

PART II

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

The Company's Common Stock is listed on the NYSE under the trading symbol "M." As of February 3, 2018 , the Company had approximately 15,300 stockholders of record. The following table sets forth for each quarter during 2017 and 2016 the high and low sales prices per share of Common Stock as reported on the NYSE and the dividends declared with respect to each quarter on each share of Common Stock.

| 2017 |

| 2016 | ||||||||||||||

| Low |

| High |

| Dividend |

| Low |

| High |

| Dividend | ||||||

1st Quarter | 27.72 | |

| 34.37 | |

| 0.3775 | |

| 37.71 | |

| 45.50 | |

| 0.3600 | |

2nd Quarter | 20.85 | |

| 29.83 | |

| 0.3775 | |

| 29.94 | |

| 40.15 | |

| 0.3775 | |

3rd Quarter | 19.32 | |

| 24.45 | |

| 0.3775 | |

| 31.02 | |

| 40.98 | |

| 0.3775 | |

4th Quarter | 17.41 | |

| 27.64 | |

| 0.3775 | |

| 28.55 | |

| 45.41 | |

| 0.3775 | |

The declaration and payment of future dividends will be at the discretion of the Company's Board of Directors, are subject to restrictions under the Company's credit facility and may be affected by various other factors, including the Company's earnings, financial condition and legal or contractual restrictions.

The following table provides information regarding the Company's purchases of Common Stock during the fourth quarter of 2017 .

| Total Number of Shares Purchased |

| Average Price per Share ($) |

| Number of Shares Purchased under Program (1) |

| Open Authorization Remaining ($)(1) | ||||

| (thousands) |

|

|

| (thousands) |

| (millions) | ||||

October 29, 2017 – November 25, 2017 | - | |

| - | |

| - | |

| 1,716 | |

November 26, 2017 – December 30, 2017 | - | |

| - | |

| - | |

| 1,716 | |

December 31, 2017 – February 3, 2018 | - | |

| - | |

| - | |

| 1,716 | |

| - | |

| - | |

| - | |

|

| |

___________________

(1) | Commencing in January 2000, the Company's Board of Directors has from time to time approved authorizations to purchase, in the aggregate, up to $18 billion of Common Stock. All authorizations are cumulative and do not have an expiration date. As of February 3, 2018 , $1,716 million of authorization remained unused. The Company may continue, discontinue or resume purchases of Common Stock under these or possible future authorizations in the open market, in privately negotiated transactions or otherwise at any time and from time to time without prior notice. |

15

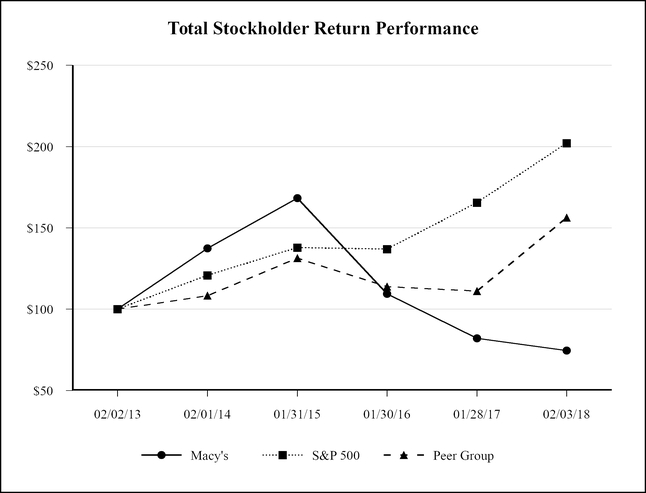

The following graph compares the cumulative total stockholder return on the Company's Common Stock with the Standard & Poor's 500 Composite Index and the Company's peer group for the period from February 2, 2013 through February 3, 2018, assuming an initial investment of $100 and the reinvestment of all dividends, if any.

The companies included in the peer group are Bed, Bath & Beyond, Dillard's, Gap, J.C. Penney, Kohl's, L Brands, Nordstrom, Ross Stores, Sears Holdings, Target, TJX Companies and Wal-Mart.

16

Item 6. | Selected Financial Data. |

The selected financial data set forth below should be read in conjunction with the Consolidated Financial Statements and the notes thereto and the other information contained elsewhere in this report.

| 2017* |

| 2016 |

| 2015 |

| 2014 |

| 2013 | ||||||||||

| (millions, except per share) | ||||||||||||||||||

Consolidated Statement of Income Data: |

|

|

|

|

|

|

|

|

| ||||||||||

Net sales | $ | 24,837 | |

| $ | 25,778 | |

| $ | 27,079 | |

| $ | 28,105 | |

| $ | 27,931 | |

Cost of sales | (15,152 | ) |

| (15,621 | ) |

| (16,496 | ) |

| (16,863 | ) |

| (16,725 | ) | |||||

Gross margin | 9,685 | |

| 10,157 | |

| 10,583 | |

| 11,242 | |

| 11,206 | | |||||

Selling, general and administrative expenses | (8,131 | ) |

| (8,474 | ) |

| (8,468 | ) |

| (8,447 | ) |

| (8,514 | ) | |||||

Gains on sale of real estate | 544 | |

| 209 | |

| 212 | |

| 92 | |

| 74 | | |||||

Restructuring, impairment, store closing and other costs | (186 | ) |

| (479 | ) |

| (288 | ) |

| (87 | ) |

| (88 | ) | |||||

Settlement charges | (105 | ) |

| (98 | ) |

| - | |

| - | |

| - | | |||||

Operating income | 1,807 | |

| 1,315 | |

| 2,039 | |

| 2,800 | |

| 2,678 | | |||||

Interest expense | (321 | ) |

| (367 | ) |

| (363 | ) |

| (395 | ) |

| (390 | ) | |||||

Net premiums on early retirement of debt | 10 | |

| - | |

| - | |

| (17 | ) |

| - | | |||||

Interest income | 11 | |

| 4 | |

| 2 | |

| 2 | |

| 2 | | |||||

Income before income taxes | 1,507 | |

| 952 | |

| 1,678 | |

| 2,390 | |

| 2,290 | | |||||

Federal, state and local income tax benefit (expense) (a) | 29 | |

| (341 | ) |

| (608 | ) |

| (864 | ) |

| (804 | ) | |||||

Net income | 1,536 | |

| 611 | |

| 1,070 | |

| 1,526 | |

| 1,486 | | |||||

Net loss attributable to noncontrolling interest | 11 | |

| 8 | |

| 2 | |

| - | |

| - | | |||||

Net income attributable to Macy's, Inc. shareholders | $ | 1,547 | |

| $ | 619 | |

| $ | 1,072 | |

| $ | 1,526 | |

| $ | 1,486 | |

|

|

|

|

|

|

|

|

|

| ||||||||||

Basic earnings per share attributable to | $ | 5.07 | |

| $ | 2.01 | |

| $ | 3.26 | |

| $ | 4.30 | |

| $ | 3.93 | |

Diluted earnings per share attributable to | $ | 5.04 | |

| $ | 1.99 | |

| $ | 3.22 | |

| $ | 4.22 | |

| $ | 3.86 | |

Average number of shares outstanding | 305.4 | |

| 308.5 | |

| 328.4 | |

| 355.2 | |

| 378.3 | | |||||

Cash dividends paid per share | $ | 1.5100 | |

| $ | 1.4925 | |

| $ | 1.3925 | |

| $ | 1.1875 | |

| $ | .9500 | |

Depreciation and amortization | $ | 991 | |

| $ | 1,058 | |

| $ | 1,061 | |

| $ | 1,036 | |

| $ | 1,020 | |

Capital expenditures | $ | 760 | |

| $ | 912 | |

| $ | 1,113 | |

| $ | 1,068 | |

| $ | 863 | |

Balance Sheet Data (at year end): |

|

|

|

|

|

|

|

|

| ||||||||||

Cash and cash equivalents | $ | 1,455 | |

| $ | 1,297 | |

| $ | 1,109 | |

| $ | 2,246 | |

| $ | 2,273 | |

Property and Equipment - net | 6,672 | |

| 7,017 | |

| 7,616 | |

| 7,800 | |

| 7,930 | | |||||

Total assets | 19,381 | |

| 19,851 | |

| 20,576 | |

| 21,330 | |

| 21,499 | | |||||

Short-term debt | 22 | |

| 309 | |

| 642 | |

| 76 | |

| 463 | | |||||

Long-term debt | 5,861 | |

| 6,562 | |

| 6,995 | |

| 7,233 | |

| 6,688 | | |||||

Total Shareholders' equity | 5,661 | |

| 4,322 | |

| 4,253 | |

| 5,378 | |

| 6,249 | | |||||

___________________

* | 53 weeks |

(a) The income tax benefit in 2017 is due to U.S. federal tax reform that led to the recognition of an income tax benefit of $571 million associated with the remeasurement of the Company's deferred tax balances.

17

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. |

The discussion in this Item 7 should be read in conjunction with the Consolidated Financial Statements and the related notes included elsewhere in this report. The discussion in this Item 7 contains forward-looking statements that reflect the Company's plans, estimates and beliefs. The Company's actual results could materially differ from those discussed in these forward-looking statements. Factors that could cause or contribute to those differences include, but are not limited to, those discussed below and elsewhere in this report, particularly in "Risk Factors" and "Forward-Looking Statements."

Overview

The Company is an omnichannel retail organization operating stores, websites and mobile applications under three brands (Macy's, Bloomingdale's and bluemercury) that sell a wide range of merchandise, including apparel and accessories (men's, women's and children's), cosmetics, home furnishings and other consumer goods. The Company operates approximately 850 stores in 44 states, the District of Columbia, Guam and Puerto Rico. As of February 3, 2018 , the Company's operations were conducted through Macy's, Bloomingdale's, Bloomingdale's The Outlet, Macy's Backstage, bluemercury and Macy's China Limited which are aggregated into one reporting segment in accordance with the Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") Topic 280, Segment Reporting.

The Company continues to implement its North Star strategy to transform its omnichannel business and focus on key growth areas, embrace customer centricity, and optimize value in its real estate portfolio. Inspired by the North Star, there are five points to this strategy.

1. | From Familiar to Favorite includes everything the Company does to further its brand awareness and identity to its core customers. Actions include understanding and anticipating customers' needs, strengthening the Company's fashion authority and executing initiatives around its loyalty and pricing strategies. It celebrates the Company's iconic events and includes strategies to appeal to more value-oriented customers. |

2. | It Must Be Macy's encompasses delivering the products and experiences customers love and are exclusive to the Company. This includes styles and home fashion for every day and special occasions, from the Company's leading private brands, as well as exclusive national brands or assortments. |

3. | Every Experience Matters , in-store and online. The Company's competitive advantage is the ability to combine the human touch in its physical stores with cutting-edge technology in its mobile applications and websites. Key to this point is the enhancement of a customer's experience as they explore our stores, mobile applications and websites, find their favorite styles, sizes and colors, and receive their purchases through the shopping channels they prefer. |

4. | Funding our Future represents the decisions and actions the Company takes to identify and realize resources to fuel growth. This involves a focus on cost reduction and reinvestment as well as creating value from the Company's real estate portfolio. |

5. | What's New, What's Next explores and develops innovations to turn consumer and technology trends to the Company's advantage and to drive growth. This includes exploring previously unmet customer needs and making smart investment decisions based on customer insights and analytics. |

The Company has taken a number of key steps over the past couple of years to position itself to successfully implement the North Star strategy. In 2017, the Company continued its investment in technology, reengineered its merchandising and marketing structure, improved its curation of merchandise and expanded different Company initiatives to stores throughout its portfolio. The Company also launched a new Macy's Star Rewards loyalty program in October 2017 that focused on strengthening relationships with the Company's best customers, migrating existing customers to higher spending levels and attracting new or infrequent customers. The initial launch of the rewards program focused on proprietary cardholders with additional enhancements and expansion beyond proprietary cardholders planned for the future.

In August 2017, the Company announced a restructuring which included the consolidation of three functions (merchandising, planning and private brands) into a single merchandising function. During the third quarter of 2017, the Company recognized $33 million of costs primarily associated with this restructuring effort as well as a restructuring within the marketing function. Additional financial and operational impacts of such restructuring actions are expected to include future annual savings of approximately $38 million, all of which may be used for reinvestment in the business in 2018.

18

In January 2018, the Company announced actions to continue improvements in organizational efficiency and to allocate resources to support its growth strategy. Major components of these restructuring activities included staffing adjustments across the stores organization with reductions in some stores and increases in others, further streamlining of some non-store functions and the closure of 11 stores in early 2018.

In 2017, the Company continued to execute on its real estate strategy through both monetization and redevelopment of certain assets:

• | Overall, the Company had asset sale gains of $544 million, totaling $411 million in cash proceeds, in 2017. These gains and proceeds include the sale of its store and parking facility in downtown Minneapolis, the sale of an additional two floors of the downtown Seattle Macy's store (four floors were sold in a similar transaction in fiscal 2015) and additional gains and proceeds from Macy's Brooklyn transaction executed in 2015. In addition, the gains recognized in 2017 include those related to the 2016 sale of the Company's Union Square Men's store in San Francisco. |

• | In 2016, the Company finalized the formation of a strategic alliance with Brookfield Asset Management ("Brookfield"), a leading global alternative asset manager, to create increased value in its real estate portfolio. Under the alliance, Brookfield has an exclusive right for up to 24 months to create a "pre-development plan" for each of approximately 50 Macy's real estate assets, with an option for Macy's to continue to identify and add assets into the alliance. Currently, the Company expects approximately two-thirds of these real estate assets to have potential for redevelopment. In February 2018, the Company announced that it had agreed to allow Brookfield to redevelop nine of these assets once it has received the necessary approvals. Upon the completion of approval and entitlements, Macy's will either sell its interests in the individual assets to Brookfield or contribute them into individual joint ventures. If sold, the cumulative value of the nine properties is estimated to be approximately $50 million plus a retained participation in the upside profits of the three largest assets. |

• | In February 2018, the Company signed an agreement to sell the upper seven floors of its State Street store in Chicago to a private real estate fund sponsored by Brookfield. The Company expects to receive a total of $30 million upfront for the transaction, which includes a $3 million contribution towards redevelopment costs for migrating operations to the floors the Company will continue to own. In addition, the Company will receive a percentage of profit earned over and above a threshold internal rate of return. |

In 2017, the Company opened new Macy's stores in Murray, UT and Los Angeles, CA as well as a Bloomingdale's store in Kuwait under a license agreement with Al Tayer Group, LLC. The Company expects to open two additional Bloomingdale's stores in San Jose, CA and Norwalk, CT in fiscal 2019.

Both Macy's off-price business, Macy's Backstage, and its clearance strategy, Last Act, have been successful in providing unique value opportunities to both existing and new Macy's customers. The Company has rolled out Last Act to all families of business and is currently focused on opening new Macy's Backstage stores within existing Macy's store locations. As of February 3, 2018, the Company has a total of 52 Macy's Backstage locations (7 freestanding and 45 inside Macy's stores).

The Company is focused on accelerating the growth of its luxury beauty products and spa retailer, bluemercury, by opening additional freestanding bluemercury stores in urban and suburban markets, enhancing its online capabilities and adding bluemercury products and boutiques to Macy's stores. As of February 3, 2018, the Company is operating 157 bluemercury locations (137 freestanding and 20 inside Macy's stores).

In August 2015, the Company established a joint venture, Macy's China Limited, of which the Company holds a sixty-five percent ownership interest and Hong Kong-based Fung Retailing Limited holds the remaining thirty-five percent ownership interest. Macy's China Limited began selling merchandise in China in the fourth quarter of 2015 through an e-commerce presence on Alibaba Group's Tmall Global. The Company's reporting includes the financial operations of Macy's China Limited, with the thirty-five percent ownership reported as a noncontrolling interest.

19

2017 Overview

2017 saw the implementation of the Company's North Star strategy and included the roll-outs of different initiatives that had been tested by the Company on a smaller scale. 2017 ended with a strong fourth quarter and selected results of 2017 include:

• | Net sales, which include a 53rd week of operations, decreased 3.7% compared to 2016. |

• | Comparable sales on an owned basis decreased 2.2% and comparable sales on an owned plus licensed basis decreased 1.9%. |

• | Operating income for 2017 was $1,807 million or 7.3% of sales; while operating income, excluding restructuring, impairment, store closing and other costs and settlement charges, was $2,098 million or 8.4% of sales. |

• | Federal, state, and local income tax benefit for 2017 was $29 million compared to expense of $341 million in 2016, due to U.S. federal tax reform which led to a non-cash tax benefit of $571 million associated with the remeasurement of the Company's deferred tax balances. |

• | Net income attributable to Macy's, Inc. shareholders for 2017 was $1,547 million , an increase of $928 million from $619 million in 2016. |

• | Diluted earnings per share attributable to Macy's, Inc. shareholders increased to $5.04 in 2017 compared to $1.99 in 2016. Diluted earnings per share attributable to Macy's, Inc. shareholders, excluding certain items, increased to $3.77 in 2017 from $3.11 in 2016. |

• | Adjusted EBITDA (earnings before interest, taxes, depreciation and amortization, restructuring, impairment, store closing and other costs and settlement charges) as a percent to net sales was 12.4% in 2017, as compared to 11.4% in 2016. |

• | Return on invested capital ("ROIC"), a key measure of operating productivity, was 20.8% for 2017. |

• | The Company repurchased or repaid approximately $950 million of debt in 2017, consisting of $247 million of debt repurchased in the open market, $300 million of a debt maturity and $400 million of debt repurchased in a tender offer ("tender offer"). |

See pages 29 to 32 for reconciliations of the non-GAAP financial measures presented above to the most comparable U.S. generally accepted accounting principles ("GAAP") financial measures and other important information.

20

Results of Operations

|

| 2017 |

|

| 2016 |

|

| 2015 |

| |||||||||||||||

|

| Amount |

| % to Sales |

|

| Amount |

| % to Sales |

|

| Amount |

| % to Sales |

| |||||||||

|

| (dollars in millions, except per share figures) |

| |||||||||||||||||||||

Net sales |

| $ | 24,837 | |

|

|

|

| $ | 25,778 | |

|

|

|

| $ | 27,079 | |

|

|

| |||

Decrease in sales |

| (3.7 | ) | % |

|

| (4.8 | ) | % |

|

| (3.7 | ) | % |

| |||||||||

Decrease in comparable sales |

| (2.2 | ) | % |

|

| (3.5 | ) | % |

|

| (3.0 | ) | % |

| |||||||||

Cost of sales |

| (15,152 | ) |

| (61.0 | ) | % | (15,621 | ) |

| (60.6 | ) | % | (16,496 | ) |

| (60.9 | ) | % | |||||

Gross margin |

| 9,685 | |

| 39.0 | | % | 10,157 | |

| 39.4 | | % | 10,583 | |

| 39.1 | | % | |||||

Selling, general and administrative expenses |

| (8,131 | ) |

| (32.8 | ) | % | (8,474 | ) |

| (32.8 | ) | % | (8,468 | ) |

| (31.3 | ) | % | |||||

Gains on sale of real estate |

| 544 | |

| 2.2 | | % | 209 | |

| 0.8 | | % | 212 | |

| 0.8 | | % | |||||

Restructuring, impairment, store closing and other costs |

| (186 | ) |

| (0.7 | ) | % | (479 | ) |

| (1.9 | ) | % | (288 | ) |

| (1.1 | ) | % | |||||

Settlement charges |

| (105 | ) |

| (0.4 | ) | % | (98 | ) |

| (0.4 | ) | % | - | |

| - | | % | |||||

Operating income |

| 1,807 | |

| 7.3 | | % | 1,315 | |

| 5.1 | | % | 2,039 | |

| 7.5 | | % | |||||

Interest expense - net |

| (310 | ) |

|

|

|

| (363 | ) |

|

|

|

| (361 | ) |

|

|

| ||||||

Net premiums on early retirement of debt |

| 10 | |

|

|

|

| - | |

|

|

|

| - | |

|

|

| ||||||

Income before income taxes |

| 1,507 | |

|

|

|

| 952 | |

|

|

|

| 1,678 | |

|

|

| ||||||

Federal, state and local income tax benefit (expense) |

| 29 | |

|

|

|

| (341 | ) |

|