|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

(Mark One) |

|

R | Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

|

| For the quarterly period ended June 30, 2017 |

|

|

or | |

|

|

o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

|

| For the transition period from __________ to __________ |

|

|

| Commission file number 1-3950 |

Ford Motor Company

(Exact name of Registrant as specified in its charter)

Delaware | 38-0549190 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

|

|

One American Road, Dearborn, Michigan | 48126 |

(Address of principal executive offices) | (Zip Code) |

313-322-3000

(Registrant's telephone number, including area code)

Indicate by check mark if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. Large accelerated filer R Accelerated filer o Non-accelerated filer o Smaller reporting company o Emerging growth company o

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No R

As of July 19, 2017, Ford had outstanding 3,900,903,065 shares of Common Stock and 70,852,076 shares of Class B Stock.

77 |

|

FORD MOTOR COMPANY

QUARTERLY REPORT ON FORM 10-Q

For the Quarter Ended June 30, 2017

| Table of Contents |

| Page |

| Part I - Financial Information |

|

|

Item 1 | Financial Statements |

| 1 |

| Consolidated Income Statement |

| 1 |

| Consolidated Statement of Comprehensive Income |

| 1 |

| Consolidated Balance Sheet |

| 2 |

| Condensed Consolidated Statement of Cash Flows |

| 3 |

| Consolidated Statement of Equity |

| 4 |

| Notes to the Financial Statements |

| 5 |

| Report of Independent Registered Public Accounting Firm |

| 31 |

Item 2 | Management's Discussion and Analysis of Financial Condition and Results of Operations |

| 32 |

| Overview |

| 32 |

| Results of Operations |

| 33 |

| Automotive Segment |

| 35 |

| Financial Services Segment |

| 50 |

| All Other |

| 54 |

| Special Items |

| 54 |

| Taxes |

| 55 |

| Liquidity and Capital Resources |

| 55 |

| Credit Ratings |

| 62 |

| Production Volumes |

| 64 |

| Outlook |

| 65 |

| Non-GAAP Financial Measure Reconciliations |

| 67 |

| Supplemental Financial Information |

| 69 |

| Risk Factors |

| 72 |

| Accounting Standards Issued But Not Yet Adopted |

| 73 |

| Other Financial Information |

| 73 |

Item 3 | Quantitative and Qualitative Disclosures About Market Risk |

| 74 |

Item 4 | Controls and Procedures |

| 75 |

|

|

|

|

| Part II - Other Information |

|

|

Item 1 | Legal Proceedings |

| 75 |

Item 2 | Unregistered Sales of Equity Securities and Use of Proceeds |

| 75 |

Item 6 | Exhibits |

| 75 |

| Signature |

| 76 |

| Exhibit Index |

| 77 |

i

PART I. FINANCIAL INFORMATION

ITEM 1. Financial Statements.

FORD MOTOR COMPANY AND SUBSIDIARIES

CONSOLIDATED INCOME STATEMENT

(in millions, except per share amounts)

| For the periods ended June 30, | ||||||||||||||

| 2016 |

| 2017 |

| 2016 |

| 2017 | ||||||||

| Second Quarter |

| First Half | ||||||||||||

| (unaudited) | ||||||||||||||

Revenues |

|

|

|

|

|

|

| ||||||||

Automotive | $ | 36,932 | |

| $ | 37,113 | |

| $ | 72,189 | |

| $ | 73,588 | |

Financial Services | 2,553 | |

| 2,738 | |

| 5,014 | |

| 5,407 | | ||||

Other | - | |

| 2 | |

| - | |

| 4 | | ||||

Total revenues (Note 3) | 39,485 | |

| 39,853 | |

| 77,203 | |

| 78,999 | | ||||

|

|

|

|

|

|

|

| ||||||||

Costs and expenses |

| |

|

| |

|

|

|

| ||||||

Cost of sales | 32,522 | |

| 33,349 | |

| 63,039 | |

| 66,057 | | ||||

Selling, administrative, and other expenses | 2,784 | |

| 2,756 | |

| 5,474 | |

| 5,520 | | ||||

Financial Services interest, operating, and other expenses | 2,258 | |

| 2,217 | |

| 4,318 | |

| 4,449 | | ||||

Total costs and expenses | 37,564 | |

| 38,322 | |

| 72,831 | |

| 76,026 | | ||||

|

|

|

|

|

|

|

| ||||||||

Interest expense on Automotive debt | 212 | |

| 277 | |

| 412 | |

| 556 | | ||||

|

|

|

|

|

|

|

| ||||||||

Non-Financial Services other income/(loss), net (Note 4) | 686 | |

| 658 | |

| 1,454 | |

| 1,370 | | ||||

Financial Services other income/(loss), net (Note 4) | 82 | |

| 74 | |

| 173 | |

| 96 | | ||||

Equity in net income of affiliated companies | 398 | |

| 273 | |

| 939 | |

| 619 | | ||||

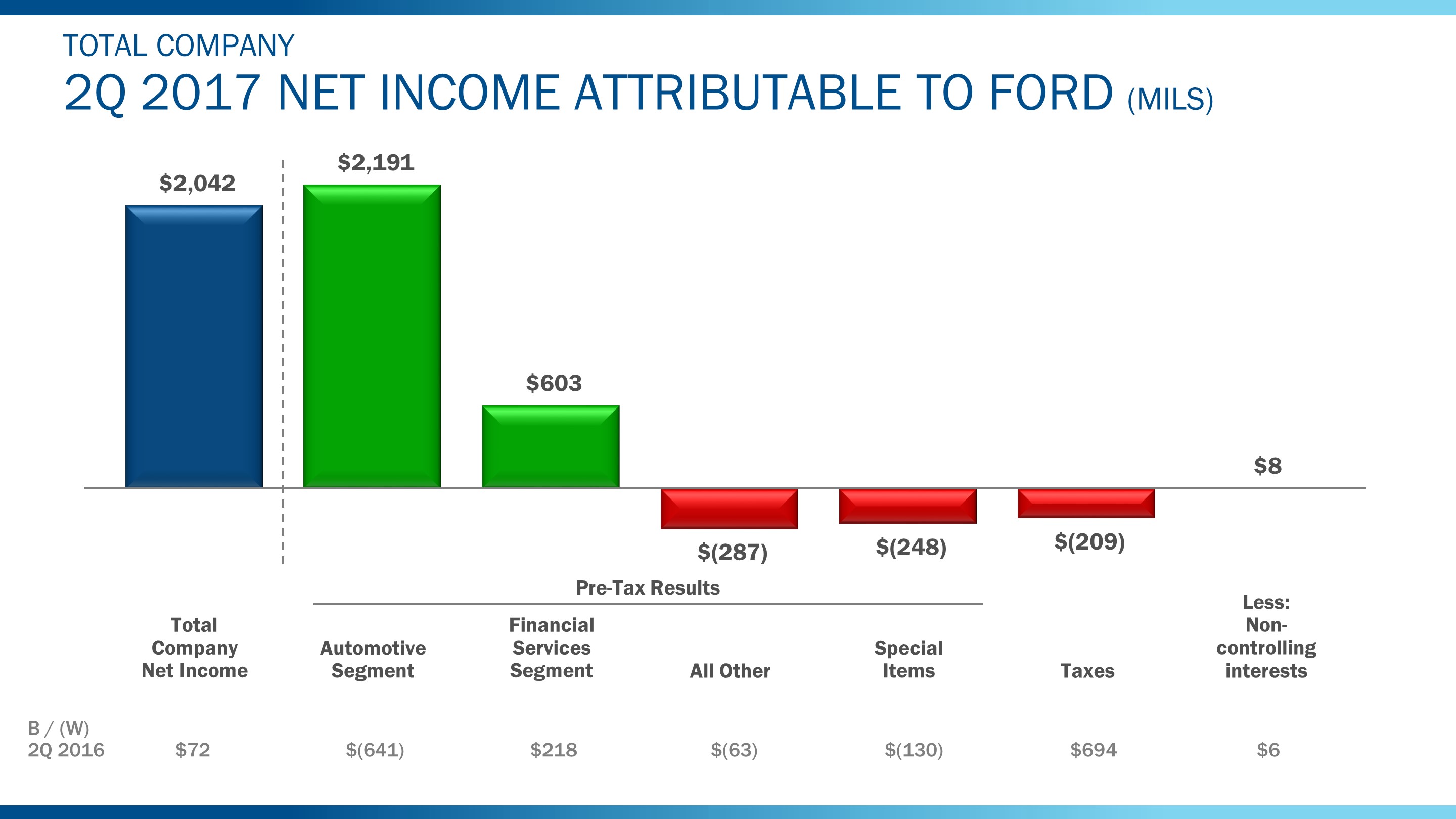

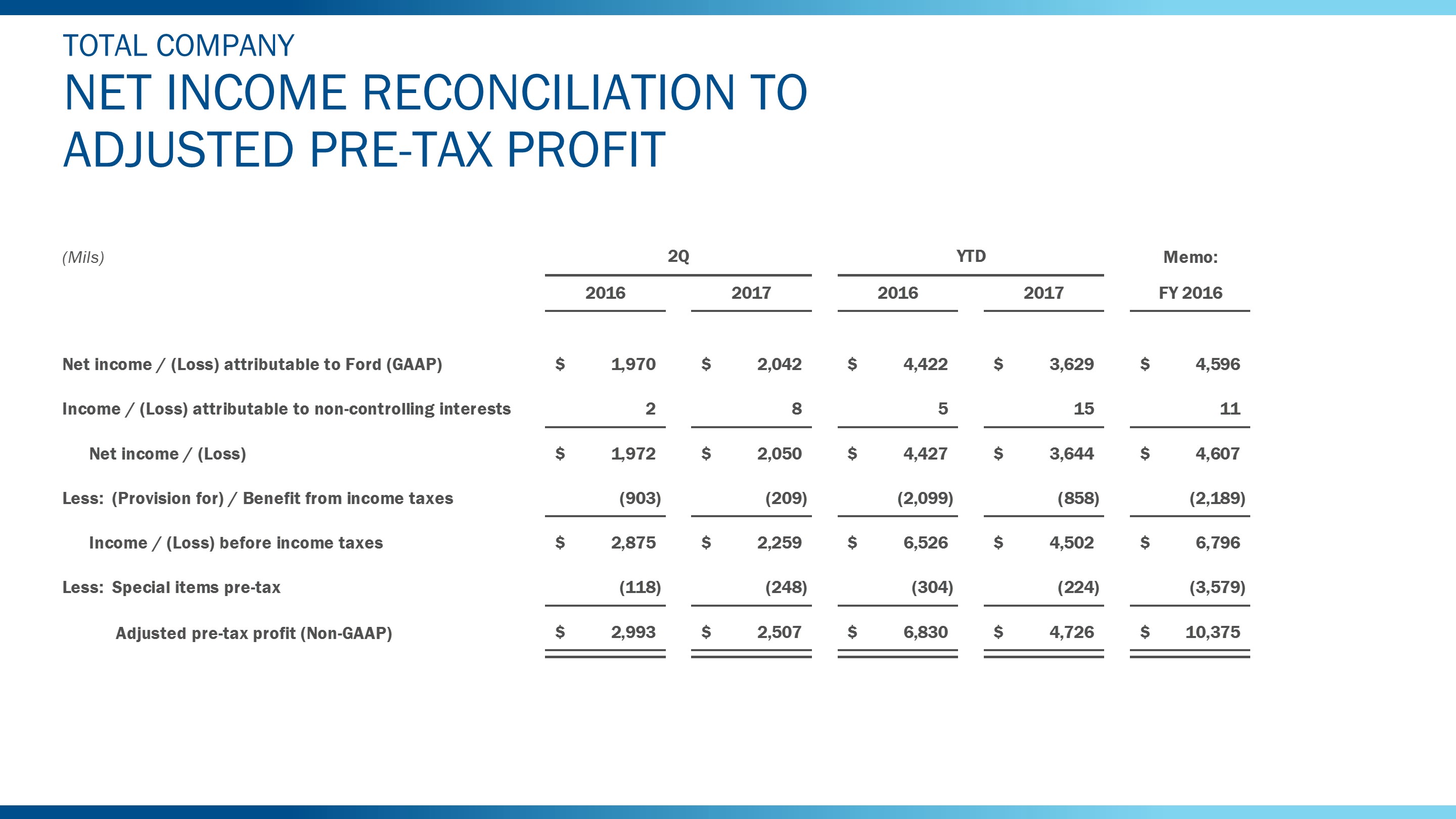

Income before income taxes | 2,875 | |

| 2,259 | | | 6,526 | | | 4,502 | | ||||

Provision for/(Benefit from) income taxes | 903 | |

| 209 | |

| 2,099 | |

| 858 | | ||||

Net income | 1,972 | |

| 2,050 | |

| 4,427 | |

| 3,644 | | ||||

Less: Income/(Loss) attributable to noncontrolling interests | 2 | |

| 8 | |

| 5 | |

| 15 | | ||||

Net income attributable to Ford Motor Company | $ | 1,970 | |

| $ | 2,042 | |

| $ | 4,422 | |

| $ | 3,629 | |

|

|

|

|

|

|

|

| ||||||||

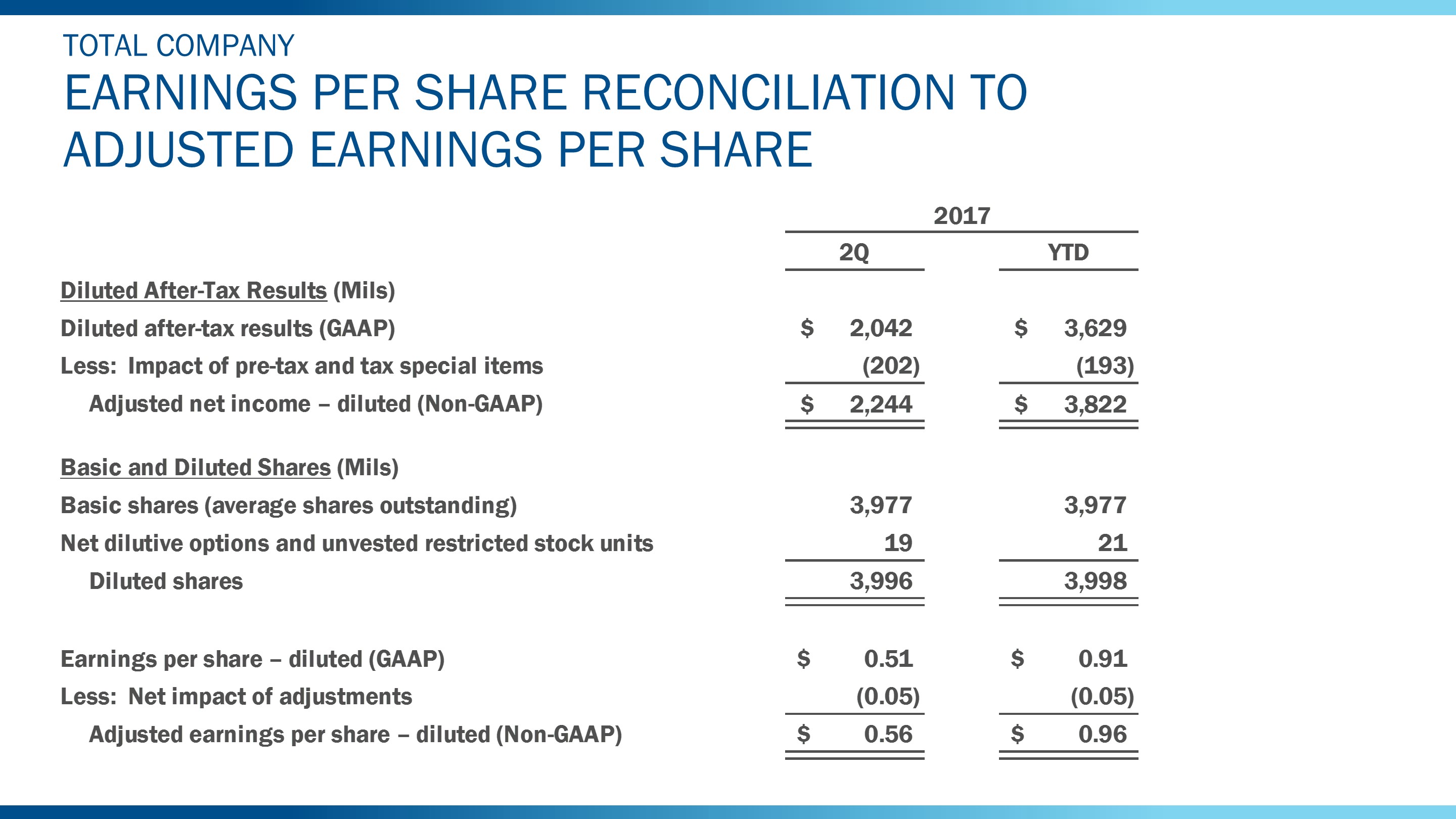

EARNINGS PER SHARE ATTRIBUTABLE TO FORD MOTOR COMPANY COMMON AND CLASS B STOCK (Note 6) | |||||||||||||||

Basic income | $ | 0.50 | |

| $ | 0.51 | |

| $ | 1.11 | |

| $ | 0.91 | |

Diluted income | 0.49 | |

| 0.51 | |

| 1.11 | |

| 0.91 | | ||||

|

|

|

|

|

|

|

| ||||||||

Cash dividends declared | 0.15 | |

| 0.15 | |

| 0.55 | |

| 0.35 | | ||||

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

(in millions)

| For the periods ended June 30, | ||||||||||||||

| 2016 |

| 2017 |

| 2016 |

| 2017 | ||||||||

| Second Quarter |

| First Half | ||||||||||||

| (unaudited) | ||||||||||||||

Net income | $ | 1,972 | |

| $ | 2,050 | |

| $ | 4,427 | |

| $ | 3,644 | |

Other comprehensive income/(loss), net of tax (Note 15) |

|

|

|

|

|

|

| ||||||||

Foreign currency translation | (58 | ) |

| 84 | |

| (122 | ) |

| 326 | | ||||

Marketable securities | - | |

| 4 | |

| 6 | |

| 3 | | ||||

Derivative instruments | 111 | |

| 137 | |

| 357 | |

| (31 | ) | ||||

Pension and other postretirement benefits | 17 | |

| (12 | ) |

| 39 | |

| (3 | ) | ||||

Total other comprehensive income/(loss), net of tax | 70 | |

| 213 | |

| 280 | |

| 295 | | ||||

Comprehensive income | 2,042 | |

| 2,263 | |

| 4,707 | |

| 3,939 | | ||||

Less: Comprehensive income/(loss) attributable to noncontrolling interests | 2 | |

| 8 | |

| 4 | |

| 13 | | ||||

Comprehensive income attributable to Ford Motor Company | $ | 2,040 | |

| $ | 2,255 | |

| $ | 4,703 | |

| $ | 3,926 | |

The accompanying notes are part of the financial statements.

1

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEET

(in millions)

| December 31, |

| June 30, | ||||

| (unaudited) | ||||||

ASSETS |

|

|

| ||||

Cash and cash equivalents (Note 7) | $ | 15,905 | |

| $ | 16,223 | |

Marketable securities (Note 7) | 22,922 | |

| 22,886 | | ||

Financial Services finance receivables, net (Note 8) | 46,266 | |

| 49,888 | | ||

Trade and other receivables, less allowances of $392 and $416 | 11,102 | |

| 10,159 | | ||

Inventories (Note 10) | 8,898 | |

| 11,092 | | ||

Other assets | 3,368 | |

| 3,291 | | ||

Total current assets | 108,461 | |

| 113,539 | | ||

|

|

|

| ||||

Financial Services finance receivables, net (Note 8) | 49,924 | |

| 51,551 | | ||

Net investment in operating leases | 28,829 | |

| 28,597 | | ||

Net property | 32,072 | |

| 33,794 | | ||

Equity in net assets of affiliated companies | 3,304 | |

| 3,241 | | ||

Deferred income taxes | 9,705 | |

| 10,145 | | ||

Other assets | 5,656 | |

| 6,602 | | ||

Total assets | $ | 237,951 | |

| $ | 247,469 | |

|

|

|

| ||||

LIABILITIES |

| |

|

| | ||

Payables | $ | 21,296 | |

| $ | 23,568 | |

Other liabilities and deferred revenue (Note 11) | 19,316 | |

| 19,958 | | ||

Automotive debt payable within one year (Note 13) | 2,685 | |

| 2,911 | | ||

Financial Services debt payable within one year (Note 13) | 46,984 | |

| 47,862 | | ||

Total current liabilities | 90,281 | |

| 94,299 | | ||

|

|

|

| ||||

Other liabilities and deferred revenue (Note 11) | 24,395 | |

| 24,840 | | ||

Automotive long-term debt (Note 13) | 13,222 | |

| 13,277 | | ||

Financial Services long-term debt (Note 13) | 80,079 | |

| 81,959 | | ||

Deferred income taxes | 691 | |

| 735 | | ||

Total liabilities | 208,668 | |

| 215,110 | | ||

|

|

|

| ||||

Redeemable noncontrolling interest | 96 | |

| 97 | | ||

|

|

|

| ||||

EQUITY |

| |

|

| | ||

Common Stock, par value $.01 per share (3,986 million shares issued of 6 billion authorized) | 40 | |

| 40 | | ||

Class B Stock, par value $.01 per share (71 million shares issued of 530 million authorized) | 1 | |

| 1 | | ||

Capital in excess of par value of stock | 21,630 | |

| 21,735 | | ||

Retained earnings | 15,634 | |

| 18,437 | | ||

Accumulated other comprehensive income/(loss) (Note 15) | (7,013 | ) |

| (6,716 | ) | ||

Treasury stock | (1,122 | ) |

| (1,253 | ) | ||

Total equity attributable to Ford Motor Company | 29,170 | |

| 32,244 | | ||

Equity attributable to noncontrolling interests | 17 | |

| 18 | | ||

Total equity | 29,187 | |

| 32,262 | | ||

Total liabilities and equity | $ | 237,951 | |

| $ | 247,469 | |

The following table includes assets to be used to settle liabilities of the consolidated variable interest entities ("VIEs"). These assets and liabilities are included in the consolidated balance sheet above. | |||||||

| December 31, |

| June 30, | ||||

| (unaudited) | ||||||

ASSETS |

|

|

| ||||

Cash and cash equivalents | $ | 3,047 | |

| $ | 2,608 | |

Financial Services finance receivables, net | 50,857 | |

| 53,359 | | ||

Net investment in operating leases | 11,761 | |

| 11,003 | | ||

Other assets | 25 | |

| 39 | | ||

LIABILITIES |

|

|

| ||||

Other liabilities and deferred revenue | $ | 5 | |

| $ | 2 | |

Debt | 43,730 | |

| 43,051 | | ||

The accompanying notes are part of the financial statements.

2

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(in millions)

| For the periods ended June 30, | ||||||

| 2016 |

| 2017 | ||||

| First Half | ||||||

| (unaudited) | ||||||

Cash flows from operating activities |

|

|

| ||||

Net cash provided by/(used in) operating activities | $ | 11,891 | |

| $ | 9,951 | |

|

|

|

| ||||

Cash flows from investing activities |

|

|

| ||||

Capital spending | (3,206 | ) |

| (3,264 | ) | ||

Acquisitions of finance receivables and operating leases | (27,501 | ) |

| (27,379 | ) | ||

Collections of finance receivables and operating leases | 19,732 | |

| 21,636 | | ||

Purchases of equity and debt securities | (16,757 | ) |

| (16,931 | ) | ||

Sales and maturities of equity and debt securities | 15,491 | |

| 16,906 | | ||

Settlements of derivatives | 111 | |

| 154 | | ||

Other | 21 | |

| 16 | | ||

Net cash provided by/(used in) investing activities | (12,109 | ) |

| (8,862 | ) | ||

|

|

|

| ||||

Cash flows from financing activities |

| |

|

| | ||

Cash dividends | (2,184 | ) |

| (1,392 | ) | ||

Purchases of common stock | (145 | ) |

| (131 | ) | ||

Net changes in short-term debt | 934 | |

| 72 | | ||

Proceeds from issuance of other debt | 25,574 | |

| 20,467 | | ||

Principal payments on other debt | (21,104 | ) |

| (19,952 | ) | ||

Other | (87 | ) |

| (102 | ) | ||

Net cash provided by/(used in) financing activities | 2,988 | |

| (1,038 | ) | ||

|

|

|

| ||||

Effect of exchange rate changes on cash and cash equivalents | 21 | |

| 267 | | ||

|

|

|

| ||||

Net increase/(decrease) in cash and cash equivalents | $ | 2,791 | |

| $ | 318 | |

|

|

|

| ||||

Cash and cash equivalents at January 1 | $ | 14,272 | |

| $ | 15,905 | |

Net increase/(decrease) in cash and cash equivalents | 2,791 | |

| 318 | | ||

Cash and cash equivalents at June 30 | $ | 17,063 | |

| $ | 16,223 | |

The accompanying notes are part of the financial statements.

3

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF EQUITY

(in millions, unaudited)

| Equity Attributable to Ford Motor Company |

|

|

|

| ||||||||||||||||||||||||||

| Capital Stock |

| Cap. in Excess of Par Value of Stock |

| Retained Earnings |

| Accumulated Other Comprehensive Income/(Loss) (Note 15) |

| Treasury Stock |

| Total |

| Equity Attributable to Non-controlling Interests |

| Total Equity | ||||||||||||||||

Balance at December 31, 2015 | $ | 41 | |

| $ | 21,421 | |

| $ | 14,414 | |

| $ | (6,257 | ) |

| $ | (977 | ) |

| $ | 28,642 | |

| $ | 15 | |

| $ | 28,657 | |

Net income | - | |

| - | |

| 4,422 | |

| - | |

| - | |

| 4,422 | |

| 5 | |

| 4,427 | | ||||||||

Other comprehensive income/(loss), net of tax | - | |

| - | |

| - | |

| 281 | |

| - | |

| 281 | |

| (1 | ) |

| 280 | | ||||||||

Common stock issued (including share-based compensation impacts) | - | |

| 125 | |

| - | |

| - | |

| - | |

| 125 | |

| - | |

| 125 | | ||||||||

Treasury stock/other | - | |

| - | |

| - | |

| - | |

| (145 | ) |

| (145 | ) |

| (1 | ) |

| (146 | ) | ||||||||

Cash dividends declared | - | |

| - | |

| (2,184 | ) |

| - | |

| - | |

| (2,184 | ) |

| (5 | ) |

| (2,189 | ) | ||||||||

Balance at June 30, 2016 | $ | 41 | |

| $ | 21,546 | |

| $ | 16,652 | |

| $ | (5,976 | ) |

| $ | (1,122 | ) |

| $ | 31,141 | |

| $ | 13 | |

| $ | 31,154 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Balance at December 31, 2016 | $ | 41 | |

| $ | 21,630 | |

| $ | 15,634 | |

| $ | (7,013 | ) |

| $ | (1,122 | ) |

| $ | 29,170 | |

| $ | 17 | |

| $ | 29,187 | |

Adoption of accounting standards | - | |

| 6 | |

| 566 | |

| - | |

| - | |

| 572 | |

| - | |

| 572 | | ||||||||

Net income | - | |

| - | |

| 3,629 | |

| - | |

| - | |

| 3,629 | |

| 15 | |

| 3,644 | | ||||||||

Other comprehensive income/(loss), net of tax | - | |

| - | |

| - | |

| 297 | |

| - | |

| 297 | |

| (2 | ) |

| 295 | | ||||||||

Common stock issued (including share-based compensation impacts) | - | |

| 99 | |

| - | |

| - | |

| - | |

| 99 | |

| - | |

| 99 | | ||||||||

Treasury stock/other | - | |

| - | |

| - | |

| - | |

| (131 | ) |

| (131 | ) |

| (1 | ) |

| (132 | ) | ||||||||

Cash dividends declared | - | |

| - | |

| (1,392 | ) |

| - | |

| - | |

| (1,392 | ) |

| (11 | ) |

| (1,403 | ) | ||||||||

Balance at June 30, 2017 | $ | 41 | |

| $ | 21,735 | |

| $ | 18,437 | |

| $ | (6,716 | ) |

| $ | (1,253 | ) |

| $ | 32,244 | |

| $ | 18 | |

| $ | 32,262 | |

The accompanying notes are part of the financial statements.

4

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

Table of Contents

Footnote |

| Page |

Note 1 | Presentation | 6 |

Note 2 | New Accounting Standards | 6 |

Note 3 | Revenue | 10 |

Note 4 | Other Income/(Loss) | 12 |

Note 5 | Income Taxes | 13 |

Note 6 | Capital Stock and Earnings Per Share | 13 |

Note 7 | Cash, Cash Equivalents, and Marketable Securities | 14 |

Note 8 | Financial Services Finance Receivables | 17 |

Note 9 | Financial Services Allowance for Credit Losses | 20 |

Note 10 | Inventories | 21 |

Note 11 | Other Liabilities and Deferred Revenue | 21 |

Note 12 | Retirement Benefits | 22 |

Note 13 | Debt | 23 |

Note 14 | Derivative Financial Instruments and Hedging Activities | 24 |

Note 15 | Accumulated Other Comprehensive Income/(Loss) | 26 |

Note 16 | Commitments and Contingencies | 27 |

Note 17 | Segment Information | 29 |

5

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 1. PRESENTATION

For purposes of this report, "Ford," the "Company," "we," "our," "us," or similar references mean Ford Motor Company, our consolidated subsidiaries, and our consolidated VIEs of which we are the primary beneficiary, unless the context requires otherwise. Our financial statements are presented in accordance with U.S. generally accepted accounting principles ("GAAP") for interim financial information, instructions to Quarterly Report on Form 10-Q, and Rule 10-01 of Regulation S-X.

In the opinion of management, these unaudited financial statements reflect a fair statement of our results of operations and financial condition for the periods, and at the dates, presented. The results for interim periods are not necessarily indicative of results that may be expected for any other interim period or for the full year. Reference should be made to the financial statements contained in our Annual Report on Form 10-K for the year ended December 31, 2016 (" 2016 Form 10-K Report"). We reclassified certain prior year amounts in our consolidated financial statements to conform to the current year presentation.

NOTE 2. NEW ACCOUNTING STANDARDS

Adoption of New Accounting Standards

Accounting Standards Update ("ASU") 2016-09, Stock Compensation - Improvements to Employee Share-Based Payment Accounting . On January 1, 2017, we adopted the amendments to accounting standards codification ("ASC") 718 which simplify accounting for share-based payment transactions. Prior to this amendment, excess tax benefits resulting from the difference between the deduction for tax purposes and the compensation costs recognized for financial reporting were not recognized until the deduction reduced taxes payable. Under the new method, we will recognize excess tax benefits in the current accounting period. In addition, prior to January 1, 2017, the employee share-based compensation expense was recorded net of estimated forfeiture rates and subsequently adjusted at the vesting date, as appropriate. As part of the amendment, we have elected to recognize the actual forfeitures by reducing the employee share-based compensation expense in the same period as the forfeitures occur. We have adopted these changes in accounting method using the modified retrospective method by recognizing one-time adjustments to retained earnings for excess tax benefits previously unrecognized and the change in accounting for forfeited awards.

ASU 2014-09, Revenue - Revenue from Contracts with Customers. On January 1, 2017, we adopted the new accounting standard ASC 606, Revenue from Contracts with Customers and all the related amendments ("new revenue standard") to all contracts using the modified retrospective method. We recognized the cumulative effect of initially applying the new revenue standard as an adjustment to the opening balance of retained earnings. The comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods. We expect the impact of the adoption of the new revenue standard to be immaterial to our net income on an ongoing basis.

A majority of our sales revenue continues to be recognized when products are shipped from our manufacturing facilities. For certain vehicle sales where revenue was previously deferred, such as vehicles subject to a guaranteed resale value recognized as a lease and transactions in which a Ford-owned entity delivered vehicles, we now recognize revenue when vehicles are shipped in accordance with the new revenue standard.

The new revenue standard also provided additional clarity that resulted in reclassifications to or from Revenue , Cost of sales , and Financial Services other income/(loss), net .

6

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 2. NEW ACCOUNTING STANDARDS (Continued)

The cumulative effect of the changes made to our consolidated January 1, 2017 balance sheet for the adoption of ASU 2016-09, Stock Compensation - Improvements to Employee Share-Based Payment Accounting and ASU 2014-09, Revenue - Revenue from Contracts with Customers were as follows (in millions):

| Balance at December 31, 2016 |

| Adjustments Due to |

| Adjustments Due to ASU 2014-09 |

| Balance at January 1, 2017 | ||||||||

Balance Sheet |

|

|

|

|

|

|

| ||||||||

Assets |

|

|

|

|

|

|

| ||||||||

Trade and other receivables | $ | 11,102 | |

| $ | - | |

| $ | (17 | ) |

| $ | 11,085 | |

Inventories | 8,898 | |

| - | |

| (9 | ) |

| 8,889 | | ||||

Other assets, current | 3,368 | |

| - | |

| 307 | |

| 3,675 | | ||||

Net investment in operating leases | 28,829 | |

| - | |

| (1,078 | ) |

| 27,751 | | ||||

Deferred income taxes | 9,705 | |

| 536 | |

| (13 | ) |

| 10,228 | | ||||

|

|

|

|

|

|

| | | |||||||

Liabilities |

|

|

|

|

|

| | | |||||||

Payables | 21,296 | |

| - | |

| 262 | |

| 21,558 | | ||||

Other liabilities and deferred revenue, current | 19,316 | |

| - | |

| (1,429 | ) |

| 17,887 | | ||||

Automotive debt payable within one year | 2,685 | |

| - | |

| 326 | |

| 3,011 | | ||||

Other liabilities and deferred revenue, non-current | 24,395 | |

| - | |

| (5 | ) |

| 24,390 | | ||||

|

|

|

|

|

|

| | | |||||||

Equity |

|

|

|

|

|

| | | |||||||

Capital in excess of par value of stock | 21,630 | |

| 6 | |

| - | |

| 21,636 | | ||||

Retained earnings | 15,634 | |

| 530 | |

| 36 | |

| 16,200 | | ||||

As part of ASU 2016-09, we retrospectively reclassified cash paid to taxing authorities related to shares withheld for tax purposes from operating activities to financing activities on our consolidated statement of cash flows. Cash paid to taxing authorities related to shares withheld for tax purposes was about $57 million and $56 million for the first half of 2016 and 2017 , respectively. This standard did not have a material impact on our second quarter and first half 2017 consolidated income statement or June 30, 2017 consolidated balance sheet .

7

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 2. NEW ACCOUNTING STANDARDS (Continued)

In accordance with the new revenue standard requirements, the disclosure of the impact of adoption on our consolidated income statement and balance sheet for the periods ended June 30, 2017 was as follows (in millions):

| Second Quarter |

| First Half | ||||||||||||||||||||

| As Reported |

| Balances Without Adoption of ASC 606 |

| Effect of Change |

| As Reported |

| Balances Without Adoption of ASC 606 |

| Effect of Change | ||||||||||||

Income statement |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Revenues |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Automotive | $ | 37,113 | |

| $ | 36,898 | |

| $ | 215 | |

| $ | 73,588 | |

| $ | 73,040 | |

| $ | 548 | |

Financial Services | 2,738 | |

| 2,641 | |

| 97 | |

| 5,407 | |

| 5,221 | |

| 186 | | ||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Costs and expenses |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Cost of sales | 33,349 | |

| 33,184 | |

| 165 | |

| 66,057 | |

| 65,630 | |

| 427 | | ||||||

Interest expense on Automotive debt | 277 | |

| 266 | |

| 11 | |

| 556 | |

| 528 | |

| 28 | | ||||||

Non-Financial Services other income/(loss), net | 658 | |

| 679 | |

| (21 | ) |

| 1,370 | |

| 1,411 | |

| (41 | ) | ||||||

Financial Services other income/(loss), net | 74 | |

| 171 | |

| (97 | ) |

| 96 | |

| 282 | |

| (186 | ) | ||||||

Provision for/(Benefit from) income taxes | 209 | |

| 204 | |

| 5 | |

| 858 | |

| 846 | |

| 12 | | ||||||

Net income | 2,050 | |

| 2,037 | |

| 13 | |

| 3,644 | |

| 3,604 | |

| 40 | | ||||||

| June 30, 2017 | ||||||||||

| As Reported |

| Balances Without Adoption of ASC 606 |

| Effect of Change | ||||||

Balance Sheet |

|

|

|

|

| ||||||

Assets |

|

|

|

|

| ||||||

Trade and other receivables | $ | 10,159 | |

| $ | 10,199 | |

| $ | (40 | ) |

Other assets, current | 3,291 | |

| 2,951 | |

| 340 | | |||

Net investment in operating leases | 28,597 | |

| 29,553 | |

| (956 | ) | |||

Deferred income taxes | 10,145 | |

| 10,170 | |

| (25 | ) | |||

|

|

|

|

|

| ||||||

Liabilities |

|

|

|

|

| ||||||

Payables | 23,568 | |

| 23,285 | |

| 283 | | |||

Other liabilities and deferred revenue, current | 19,958 | |

| 21,393 | |

| (1,435 | ) | |||

Automotive debt payable within one year | 2,911 | |

| 2,511 | |

| 400 | | |||

Other liabilities and deferred revenue, non-current | 24,840 | |

| 24,845 | |

| (5 | ) | |||

Deferred income taxes | 735 | |

| 735 | |

| - | | |||

|

|

|

|

|

| ||||||

Equity |

|

|

|

|

| ||||||

Retained earnings | 18,437 | |

| 18,361 | |

| 76 | | |||

8

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 2. NEW ACCOUNTING STANDARDS (Continued)

ASU 2017-07, Retirement Benefits - Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost . On January 1, 2017, we adopted the amendments to ASC 715 that improve the presentation of net periodic pension and postretirement benefit costs. We retrospectively adopted the presentation of service cost separate from the other components of net periodic costs. The interest cost, expected return on assets, amortization of prior service costs, net remeasurement, and other costs have been reclassified from Cost of Sales and Selling, administrative, and other expenses to Non-Financial Services other income/(loss), net. We elected to apply the practical expedient which allows us to reclassify amounts disclosed previously in the retirement benefits note as the basis for applying retrospective presentation for comparative periods as it is impracticable to determine the disaggregation of the cost components for amounts capitalized and amortized in those periods. On a prospective basis, the other components of net periodic benefit costs will not be included in amounts capitalized in inventory or property, plant, and equipment.

The effect of the retrospective presentation change related to the net periodic cost of our defined benefit pension and other postretirement employee benefits ("OPEB") plans on our consolidated income statement for the periods ended June 30, 2016 was as follows (in millions):

| Second Quarter |

| First Half | ||||||||||||||||||||

| As Revised |

| Previously Reported |

| Effect of Change |

| As Revised |

| Previously Reported |

| Effect of Change | ||||||||||||

Income statement |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Cost of sales | $ | 32,522 | |

| $ | 32,348 | |

| $ | 174 | |

| $ | 63,039 | |

| $ | 62,629 | |

| $ | 410 | |

Selling, administrative, and other expenses | 2,784 | |

| 2,661 | |

| 123 | |

| 5,474 | |

| 5,223 | |

| 251 | | ||||||

Non-Financial Services other income/(loss), net | 686 | |

| 389 | |

| 297 | |

| 1,454 | |

| 793 | |

| 661 | | ||||||

We also adopted the following standards during 2017 , none of which had a material impact to our financial statements or financial statement disclosures:

Standard |

| Effective Date | |

2017-05 | Gains and Losses from the Derecognition of Nonfinancial Assets - Clarifying the Scope of Asset Derecognition Guidance |

| January 1, 2017 |

2017-04 | Goodwill and Other - Simplifying the Test for Goodwill Impairment |

| January 1, 2017 |

2017-03 | Accounting Changes and Error Corrections and Investments - Equity Method and Joint Ventures |

| January 1, 2017 |

2017-01 | Business Combinations - Clarifying the Definition of a Business |

| January 1, 2017 |

2016-17 | Consolidation - Interests Held through Related Parties That Are under Common Control |

| January 1, 2017 |

2016-07 | Equity Method and Joint Ventures - Simplifying the Transition to the Equity Method of Accounting |

| January 1, 2017 |

2016-06 | Derivatives and Hedging - Contingent Put and Call Options in Debt Instruments |

| January 1, 2017 |

2016-05 | Derivatives and Hedging - Effect of Derivative Contract Novations on Existing Hedge Accounting Relationships |

| January 1, 2017 |

2016-04 | Extinguishments of Liabilities - Recognition of Breakage for Certain Prepaid Stored-Value Products |

| January 1, 2017 |

2017-09 | Stock Compensation - Scope of Modification Accounting |

| April 1, 2017 |

Accounting Standards Issued But Not Yet Adopted

The following represent the standards that will, or are expected to, result in a significant change in practice and/or have a significant financial impact to Ford.

ASU 2016-13, Credit Losses - Measurement of Credit Losses on Financial Instruments . In June 2016, the Financial Accounting Standards Board ("FASB") issued a new accounting standard which replaces the current incurred loss impairment method with a method that reflects expected credit losses. The new standard is effective as of January 1, 2020, and early adoption is permitted as of January 1, 2019. We will adopt the new credit loss guidance by recognizing the cumulative effect of initially applying the new standard as an adjustment to the opening balance of retained earnings. We are assessing the potential impact to our financial statements and disclosures.

9

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 2. NEW ACCOUNTING STANDARDS (Continued)

ASU 2016-02, Leases . In February 2016, the FASB issued a new accounting standard which provides guidance on the recognition, measurement, presentation, and disclosure of leases. The new standard supersedes the present U.S. GAAP standard on leases and requires substantially all leases to be reported on the balance sheet as right-of-use assets and lease obligations. We plan to adopt the new standard at its effective date of January 1, 2019. We anticipate adoption of the standard will add between $1.5 billion and $2 billion in right-of-use assets and lease obligations to our balance sheet and will not significantly impact pre-tax profit. We are in the early stages of implementation.

NOTE 3. REVENUE

The following table disaggregates our revenue by major source for the periods ended June 30, 2017 (in millions):

| Second Quarter | ||||||||||||||

| Automotive |

| Financial Services |

| All Other |

| Consolidated | ||||||||

Vehicles, parts, and accessories | $ | 35,746 | |

| $ | - | |

| $ | - | |

| $ | 35,746 | |

Sale of used vehicles | 708 | |

| - | |

| - | |

| 708 | | ||||

Extended service contracts | 332 | |

| - | |

| - | |

| 332 | | ||||

Other (a) | 202 | |

| 55 | |

| 2 | |

| 259 | | ||||

Revenues from sales and services | 36,988 | |

| 55 | |

| 2 | |

| 37,045 | | ||||

|

|

|

|

|

|

|

| ||||||||

Leasing income | 125 | |

| 1,381 | |

| - | |

| 1,506 | | ||||

Financing income | - | |

| 1,260 | |

| - | |

| 1,260 | | ||||

Insurance income | - | |

| 42 | |

| - | |

| 42 | | ||||

Total revenues | $ | 37,113 | |

| $ | 2,738 | |

| $ | 2 | |

| $ | 39,853 | |

|

|

|

|

|

|

|

| ||||||||

| First Half | ||||||||||||||

| Automotive |

| Financial Services |

| All Other |

| Consolidated | ||||||||

Vehicles, parts, and accessories | $ | 70,742 | |

| $ | - | |

| $ | - | |

| $ | 70,742 | |

Sale of used vehicles | 1,581 | |

| - | |

| - | |

| 1,581 | | ||||

Extended service contracts | 607 | |

| - | |

| - | |

| 607 | | ||||

Other (a) | 426 | |

| 104 | |

| 4 | |

| 534 | | ||||

Revenues from sales and services | 73,356 | |

| 104 | |

| 4 | |

| 73,464 | | ||||

|

|

|

|

|

|

|

| ||||||||

Leasing income | 232 | |

| 2,747 | |

| - | |

| 2,979 | | ||||

Financing income | - | |

| 2,474 | |

| - | |

| 2,474 | | ||||

Insurance income | - | |

| 82 | |

| - | |

| 82 | | ||||

Total revenues | $ | 73,588 | |

| $ | 5,407 | |

| $ | 4 | |

| $ | 78,999 | |

__________

(a) | Primarily includes commissions and vehicle-related design and testing services. |

Revenue is recognized when obligations under the terms of a contract with our customer are satisfied; generally this occurs with the transfer of control of our vehicles, parts, accessories, or services. Revenue is measured as the amount of consideration we expect to receive in exchange for transferring goods or providing services. Sales, value add, and other taxes we collect concurrent with revenue-producing activities are excluded from revenue. Incidental items that are immaterial in the context of the contract are recognized as expense. The expected costs associated with our base warranties and field service actions continue to be recognized as expense when the products are sold (see Note 16 ). We recognize revenue for vehicle service contracts that extend mechanical and maintenance beyond our base warranties over the life of the contract.

10

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 3. REVENUE (Continued)

Automotive Segment

Vehicles, Parts, and Accessories. For the majority of vehicles, parts, and accessories, we transfer control and recognize a sale when we ship the product from our manufacturing facility to our customer (dealers and distributors). The amount of consideration we receive and revenue we recognize varies with changes in marketing incentives and returns we offer to our customers and their customers. When we give our dealers the right to return eligible parts and accessories, we estimate the expected returns based on an analysis of historical experience. We adjust our estimate of revenue at the earlier of when the most likely amount of consideration we expect to receive changes or when the consideration becomes fixed. As a result we recognized a decrease to revenue from prior periods in the second quarter of 2017 of $259 million .

Depending on the terms of the arrangement, we may also defer the recognition of a portion of the consideration received because we have to satisfy a future obligation (e.g., free extended service contracts). We use an observable price to determine the stand-alone selling price for separate performance obligations or a cost plus margin approach when one is not available. We have elected to recognize the cost for freight and shipping when control over vehicles, parts, or accessories have transferred to the customer as an expense in Cost of sales .

We sell vehicles to daily rental companies and guarantee that we will pay them the difference between an agreed amount and the value they are able to realize upon resale. At the time of transfer of vehicles to the daily rental companies, we record the probable amount we will pay under the guarantee to Other liabilities and deferred revenue.

Sale of Used Vehicles. We sell used vehicles both at auction and through our consolidated dealerships. Proceeds from the sale of these vehicles are recognized in Automotive revenues upon transfer of control of the vehicle to the customer and the related vehicle carrying value is recognized in Cost of sales .

Extended Service Contracts. We sell separately-priced service contracts that extend mechanical and maintenance coverages beyond our base warranty agreements to vehicle owners. The separately priced service contracts range from 12 months to 120 months . We receive payment at the inception of the contract and recognize revenue over the term of the agreement in proportion to the costs expected to be incurred in satisfying the obligations under the contract. At January 1, 2017, $3.5 billion of unearned revenue associated with outstanding contracts was reported in Other Liabilities and deferred revenue, $271 million and $541 million of this was recognized as revenue during the second quarter and first half of 2017 , respectively. At June 30, 2017 , the unearned amount was $3.7 billion . We expect to recognize approximately $550 million of the unearned amount in 2017, $950 million in 2018, and $2.2 billion thereafter. We record a premium deficiency reserve to the extent we estimate the future costs associated with these contracts exceed the unrecognized revenue. Amounts paid to dealers to obtain these contracts are deferred and recorded as Other assets . These costs are amortized to expense consistent with how the related revenue is recognized. We had a balance of $239 million in deferred costs as of June 30, 2017 and recognized $14 million and $29 million of amortization during the second quarter and first half of 2017 , respectively.

Other Revenue. Other revenue consists primarily of net commissions received for serving as the agent in facilitating the sale of a third party's products or services to our customers and payments for vehicle - related design and testing services we perform for others. We have applied the practical expedient to recognize Automotive revenues for vehicle-related design and testing services over the two to three year term of these agreements in proportion to the amount we have the right to invoice.

Leasing Income. We sell vehicles to daily rental companies with an obligation to repurchase the vehicles for a guaranteed amount, exercisable at the option of the customer. The transactions are accounted for as operating leases. Upon the transfer of vehicles to the daily rental companies, we record proceeds received in Other liabilities and deferred revenue. The difference between the proceeds received and the guaranteed repurchase amount is recorded in Automotive revenues over the term of the lease using a straight-line method. The cost of the vehicle is recorded in Net investment in operating leases on our consolidated balance sheet and the difference between the cost of the vehicle and the estimated auction value is depreciated in Cost of sales over the term of the lease.

11

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 3. REVENUE (Continued)

Financial Services Segment

Leasing Income. Ford Credit offers leasing plans to retail consumers through Ford and Lincoln brand dealers who originate the leases. Upon the purchase of a lease from the dealer, Ford Credit takes ownership of the vehicle and records an operating lease. The retail consumer makes lease payments representing the difference between Ford Credit's purchase price of the vehicle and the contractual residual value of the vehicle, plus lease fees that we recognize on a straight-line basis over the term of the lease agreement. Depreciation and the gain or loss upon disposition of the vehicle is recorded in Financial Services interest, operating, and other expenses .

Financing Income. Ford Credit originates and purchases finance installment contracts. Financing income represents interest earned on the finance receivables (including direct financing leases). Interest is recognized using the interest method, and includes the amortization of certain direct origination costs.

Insurance Income. Income from insurance contracts is recognized evenly over the term of the agreement. Insurance commission revenue is recognized on a net basis at the time of sale of the third party's product or service to our customer.

NOTE 4. OTHER INCOME/(LOSS)

Non-Financial Services

The amounts included in Non-Financial Services other income/(loss), net for the periods ended June 30 were as follows (in millions):

| Second Quarter |

| First Half | ||||||||||||

| 2016 |

| 2017 |

| 2016 |

| 2017 | ||||||||

Net periodic pension and OPEB income/(cost), excluding service cost | $ | 297 | |

| $ | 389 | |

| $ | 661 | |

| $ | 779 | |

Investment-related interest income | 52 | |

| 85 | |

| 113 | |

| 156 | | ||||

Interest income/(expense) on income taxes | 1 | |

| (1 | ) |

| (1 | ) |

| 2 | | ||||

Realized and unrealized gains/(losses) on cash equivalents and marketable securities | (7 | ) |

| (24 | ) |

| 65 | |

| 25 | | ||||

Gains/(Losses) on changes in investments in affiliates | 147 | |

| (1 | ) |

| 181 | |

| (2 | ) | ||||

Royalty income | 137 | |

| 150 | |

| 320 | |

| 304 | | ||||

Other | 59 | |

| 60 | |

| 115 | |

| 106 | | ||||

Total | $ | 686 | |

| $ | 658 | |

| $ | 1,454 | |

| $ | 1,370 | |

Financial Services

The amounts included in Financial Services other income/(loss), net for the periods ended June 30 were as follows (in millions):

| Second Quarter |

| First Half | ||||||||||||

| 2016 |

| 2017 |

| 2016 |

| 2017 | ||||||||

Investment-related interest income | $ | 20 | |

| $ | 24 | |

| $ | 39 | |

| $ | 45 | |

Interest income/(expense) on income taxes | 15 | |

| 1 | |

| 13 | |

| (1 | ) | ||||

Insurance premiums earned | 41 | |

| - | |

| 80 | |

| - | | ||||

Other | 6 | |

| 49 | |

| 41 | |

| 52 | | ||||

Total | $ | 82 | |

| $ | 74 | |

| $ | 173 | |

| $ | 96 | |

12

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

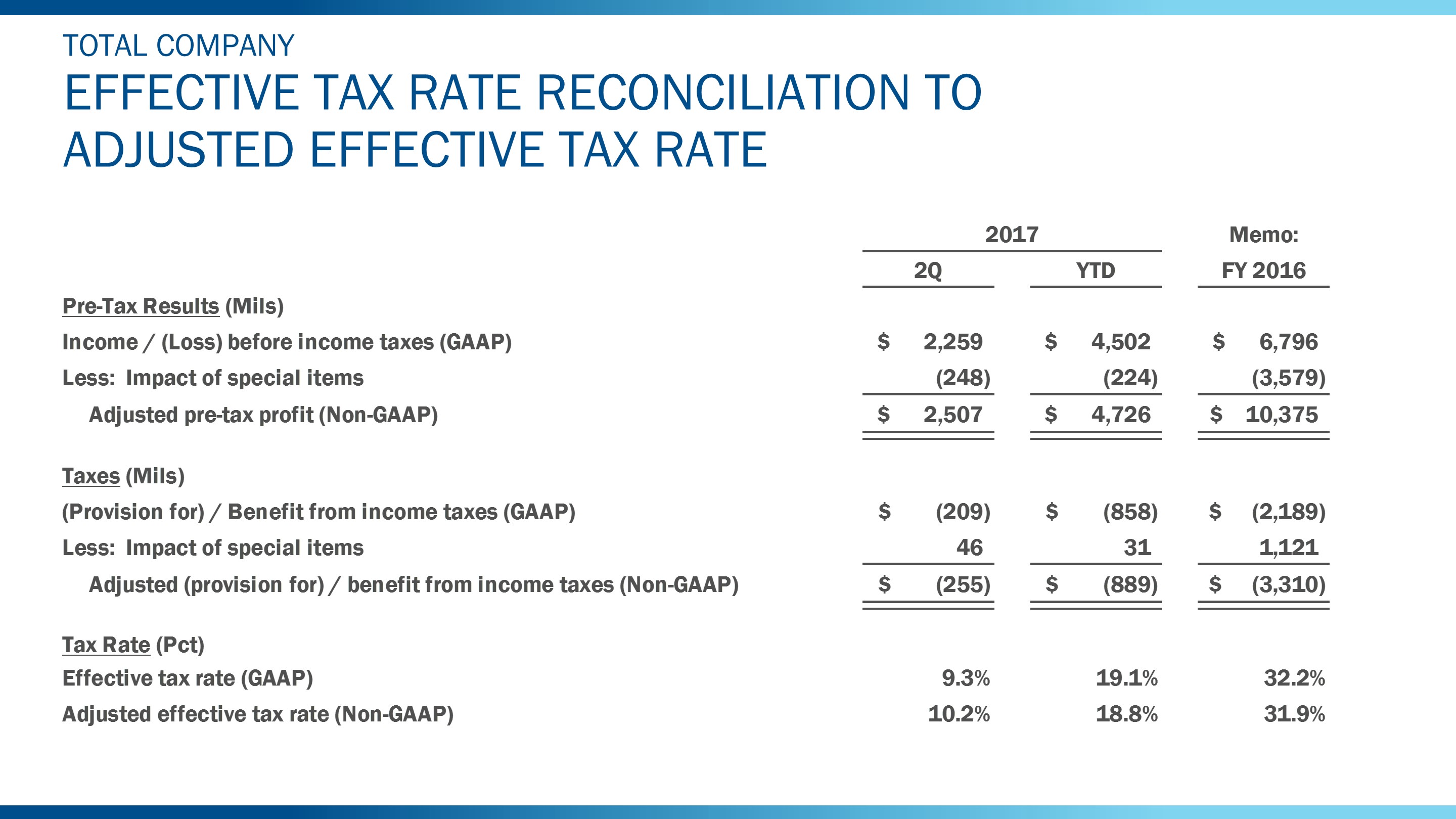

NOTE 5. INCOME TAXES

For interim tax reporting, we estimate one single effective tax rate for tax jurisdictions not subject to a valuation allowance, which is applied to the year-to-date ordinary income/(loss). Tax effects of significant unusual or infrequently occurring items are excluded from the estimated annual effective tax rate calculation and recognized in the interim period in which they occur.

For the second quarter of 2016 and 2017 , our effective tax rates were 31.4% and 9.3% , respectively. During the second quarter of 2017 , we recognized a $421 million benefit for foreign tax credits expected to be realized in the foreseeable future. The tax benefit relates to investments in certain non-U.S. subsidiaries previously determined to be indefinitely reinvested in operations outside the United States. Our change in assertion for these investments is related to planned distributions in anticipation of potential U.S. corporate tax reform.

NOTE 6. CAPITAL STOCK AND EARNINGS PER SHARE

Earnings Per Share Attributable to Ford Motor Company Common and Class B Stock

Basic and diluted income per share were calculated using the following (in millions):

| Second Quarter |

| First Half | ||||||||||||

| 2016 |

| 2017 |

| 2016 |

| 2017 | ||||||||

Basic and Diluted Income Attributable to Ford Motor Company |

|

|

|

|

|

|

| ||||||||

Basic income | $ | 1,970 | |

| $ | 2,042 | |

| $ | 4,422 | |

| $ | 3,629 | |

Diluted income | 1,970 | |

| 2,042 | |

| 4,422 | |

| 3,629 | | ||||

|

|

|

|

|

|

|

| ||||||||

Basic and Diluted Shares |

| |

|

| |

|

|

|

| ||||||

Basic shares (average shares outstanding) | 3,973 | |

| 3,977 | |

| 3,972 | |

| 3,977 | | ||||

Net dilutive options and unvested restricted stock units | 24 | |

| 19 | |

| 24 | |

| 21 | | ||||

Diluted shares | 3,997 | |

| 3,996 | |

| 3,996 | |

| 3,998 | | ||||

13

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 7. CASH, CASH EQUIVALENTS, AND MARKETABLE SECURITIES

The fair values of cash, cash equivalents, and marketable securities measured at fair value on a recurring basis on our balance sheet were as follows (in millions):

|

|

| December 31, 2016 | ||||||||||||||

| Fair Value Level |

| Automotive |

| Financial Services |

| All Other |

| Consolidated | ||||||||

Cash and cash equivalents |

|

|

|

|

|

|

|

|

| ||||||||

U.S. government | 1 |

| $ | 888 | |

| $ | 924 | |

| $ | - | |

| $ | 1,812 | |

U.S. government agencies | 2 |

| - | |

| - | |

| - | |

| - | | ||||

Non-U.S. government and agencies | 2 |

| 200 | |

| 142 | |

| - | |

| 342 | | ||||

Corporate debt | 2 |

| 100 | |

| - | |

| - | |

| 100 | | ||||

Total marketable securities classified as cash equivalents |

|

| 1,188 | |

| 1,066 | |

| - | |

| 2,254 | | ||||

Cash, time deposits, and money market funds |

|

| 6,632 | |

| 7,011 | |

| 8 | |

| 13,651 | | ||||

Total cash and cash equivalents |

|

| $ | 7,820 | |

| $ | 8,077 | |

| $ | 8 | |

| $ | 15,905 | |

|

|

|

|

|

|

|

|

|

| ||||||||

Marketable securities |

|

|

|

|

|

|

|

|

| ||||||||

U.S. government | 1 |

| $ | 8,099 | |

| $ | 1,634 | |

| $ | - | |

| $ | 9,733 | |

U.S. government agencies | 2 |

| 2,244 | |

| 505 | |

| - | |

| 2,749 | | ||||

Non-U.S. government and agencies | 2 |

| 4,751 | |

| 632 | |

| - | |

| 5,383 | | ||||

Corporate debt | 2 |

| 4,329 | |

| 475 | |

| - | |

| 4,804 | | ||||

Equities | 1 |

| 165 | |

| - | |

| - | |

| 165 | | ||||

Other marketable securities | 2 |

| 54 | |

| 34 | |

| - | |

| 88 | | ||||

Total marketable securities |

|

| $ | 19,642 | |

| $ | 3,280 | |

| $ | - | |

| $ | 22,922 | |

|

|

|

|

|

|

|

|

|

| ||||||||

|

|

| June 30, 2017 | ||||||||||||||

| Fair Value Level |

| Automotive |

| Financial Services |

| All Other |

| Consolidated | ||||||||

Cash and cash equivalents |

|

|

|

|

|

|

|

|

| ||||||||

U.S. government | 1 |

| $ | 300 | |

| $ | 182 | |

| $ | - | |

| $ | 482 | |

U.S. government agencies | 2 |

| 624 | |

| 100 | |

| - | |

| 724 | | ||||

Non-U.S. government and agencies | 2 |

| 270 | |

| 342 | |

| - | |

| 612 | | ||||

Corporate debt | 2 |

| - | |

| 75 | |

| - | |

| 75 | | ||||

Total marketable securities classified as cash equivalents |

|

| 1,194 | |

| 699 | |

| - | |

| 1,893 | | ||||

Cash, time deposits, and money market funds |

|

| 7,659 | |

| 6,667 | |

| 4 | |

| 14,330 | | ||||

Total cash and cash equivalents |

|

| $ | 8,853 | |

| $ | 7,366 | |

| $ | 4 | |

| $ | 16,223 | |

|

|

|

|

|

|

|

|

|

| ||||||||

Marketable securities |

|

|

|

|

|

|

|

|

| ||||||||

U.S. government | 1 |

| $ | 5,365 | |

| $ | 977 | |

| $ | - | |

| $ | 6,342 | |

U.S. government agencies | 2 |

| 3,677 | |

| 663 | |

| - | |

| 4,340 | | ||||

Non-U.S. government and agencies | 2 |

| 6,036 | |

| 790 | |

| - | |

| 6,826 | | ||||

Corporate debt | 2 |

| 4,284 | |

| 854 | |

| - | |

| 5,138 | | ||||

Equities | 1 |

| 177 | |

| | |

| - | |

| 177 | | ||||

Other marketable securities | 2 |

| 36 | |

| 27 | |

| - | |

| 63 | | ||||

Total marketable securities |

|

| $ | 19,575 | |

| $ | 3,311 | |

| $ | - | |

| $ | 22,886 | |

14

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 7. CASH, CASH EQUIVALENTS, AND MARKETABLE SECURITIES (Continued)

The cash equivalents and marketable securities accounted for as available-for-sale ("AFS") securities on our balance sheet were as follows (in millions):

| December 31, 2016 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

| Fair Value of Securities with Contractual Maturities | ||||||||||||||||||

| Amortized Cost |

| Gross Unrealized Gains |

| Gross Unrealized Losses |

| Fair Value |

| Within 1 Year |

| After 1 Year through 5 Years |

| After 5 Years through 10 Years | ||||||||||||||

Automotive |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

U.S. government | $ | 3,703 | |

| $ | 2 | |

| $ | (14 | ) |

| $ | 3,691 | |

| $ | 727 | |

| $ | 2,776 | |

| $ | 188 | |

U.S. government agencies | 308 | |

| - | |

| (2 | ) |

| 306 | |

| - | |

| 306 | |

| - | | |||||||

Non-U.S. government and agencies | 1,443 | |

| 1 | |

| (11 | ) |

| 1,433 | |

| 148 | |

| 1,285 | |

| - | | |||||||

Corporate debt | 1,079 | |

| - | |

| - | |

| 1,079 | |

| 1,031 | |

| 48 | |

| - | | |||||||

Total | $ | 6,533 | |

| $ | 3 | |

| $ | (27 | ) |

| $ | 6,509 | |

| $ | 1,906 | |

| $ | 4,415 | |

| $ | 188 | |

|

|

|

|

|

|

|

| |

|

|

|

|

|

| |||||||||||||

| June 30, 2017 | ||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

| Fair Value of Securities with Contractual Maturities | ||||||||||||||||||

| Amortized Cost |

| Gross Unrealized Gains |

| Gross Unrealized Losses |

| Fair Value |

| Within 1 Year |

| After 1 Year through 5 Years |

| After 5 Years through 10 Years | ||||||||||||||

Automotive |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||

U.S. government | $ | 2,587 | |

| $ | - | |

| $ | (7 | ) |

| $ | 2,580 | |

| $ | 524 | |

| $ | 2,056 | |

| $ | - | |

U.S. government agencies | 1,982 | |

| 1 | |

| (4 | ) |

| 1,979 | |

| 677 | |

| 1,237 | |

| 65 | | |||||||

Non-U.S. government and agencies | 2,961 | |

| 5 | |

| (5 | ) |

| 2,961 | |

| 248 | |

| 2,688 | |

| 25 | | |||||||

Corporate debt | 1,398 | |

| - | |

| (2 | ) |

| 1,396 | |

| 756 | |

| 633 | |

| 7 | | |||||||

Total | $ | 8,928 | |

| $ | 6 | |

| $ | (18 | ) |

| $ | 8,916 | |

| $ | 2,205 | |

| $ | 6,614 | |

| $ | 97 | |

Sales proceeds from investments classified as AFS and sold prior to maturity were $0 and $1.3 billion in the second quarter of 2016 and 2017 , respectively, and $69 million and $2.6 billion in the first half of 2016 and 2017 , respectively. The gross realized gains from the sale of AFS securities were $0 and $2 million in the second quarter of 2016 and 2017 , respectively, and $1 million and $3 million in the first half of 2016 and 2017 , respectively. Gross realized losses from the sale of AFS securities were $0 and $6 million in the second quarter of 2016 and 2017 , respectively, and $0 and $8 million in the first half of 2016 and 2017 , respectively.

15

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 7. CASH, CASH EQUIVALENTS, AND MARKETABLE SECURITIES (Continued)

The present fair values and gross unrealized losses for cash equivalents and marketable securities accounted for as AFS securities that were in an unrealized loss position, aggregated by investment category and the length of time that individual securities have been in a continuous loss position, were as follows (in millions):

| December 31, 2016 | ||||||||||||||||||||||

| Less than 1 year |

| 1 Year or Greater |

| Total | ||||||||||||||||||

| Fair Value |

| Unrealized Losses |

| Fair Value |

| Unrealized Losses |

| Fair Value |

| Unrealized Losses | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Automotive |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

U.S. government | $ | 1,474 | |

| $ | (14 | ) |

| $ | - | |

| $ | - | |

| $ | 1,474 | |

| $ | (14 | ) |

U.S. government agencies | 261 | |

| (2 | ) |

| - | |

| - | |

| 261 | |

| (2 | ) | ||||||

Non-U.S. government and agencies | 1,137 | |

| (11 | ) |

| - | |

| - | |

| 1,137 | |

| (11 | ) | ||||||

Corporate debt | - | |

| - | |

| - | |

| - | |

| - | |

| - | | ||||||

Total | $ | 2,872 | |

| $ | (27 | ) |

| $ | - | |

| $ | - | |

| $ | 2,872 | |

| $ | (27 | ) |

|

| |

|

|

|

|

|

|

|

|

|

| |||||||||||

| June 30, 2017 | ||||||||||||||||||||||

| Less than 1 year |

| 1 Year or Greater |

| Total | ||||||||||||||||||

| Fair Value |

| Unrealized Losses |

| Fair Value |

| Unrealized Losses |

| Fair Value |

| Unrealized Losses | ||||||||||||

Automotive |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

U.S. government | $ | 2,580 | |

| $ | (7 | ) |

| $ | - | |

| $ | - | |

| $ | 2,580 | |

| $ | (7 | ) |

U.S. government agencies | 1,172 | |

| (4 | ) |

| - | |

| - | |

| 1,172 | |

| (4 | ) | ||||||

Non-U.S. government and agencies | 1,555 | |

| (5 | ) |

| - | |

| - | |

| 1,555 | |

| (5 | ) | ||||||

Corporate debt | 517 | |

| (2 | ) |

| - | |

| - | |

| 517 | |

| (2 | ) | ||||||

Total | $ | 5,824 | |

| $ | (18 | ) |

| $ | - | |

| $ | - | |

| $ | 5,824 | |

| $ | (18 | ) |

We determine other-than-temporary impairments on cash equivalents and marketable securities using a specific identification method. During the six months ended June 30, 2016 and 2017 , we did not recognize any other-than-temporary impairment loss.

Other Securities

Investments in entities that we do not control and over which we do not have the ability to exercise significant influence are recorded at cost and reported in Other assets in the non-current assets section of our consolidated balance sheet. These cost method investments were $219 million and $221 million at December 31, 2016 and June 30, 2017 , respectively.

16

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

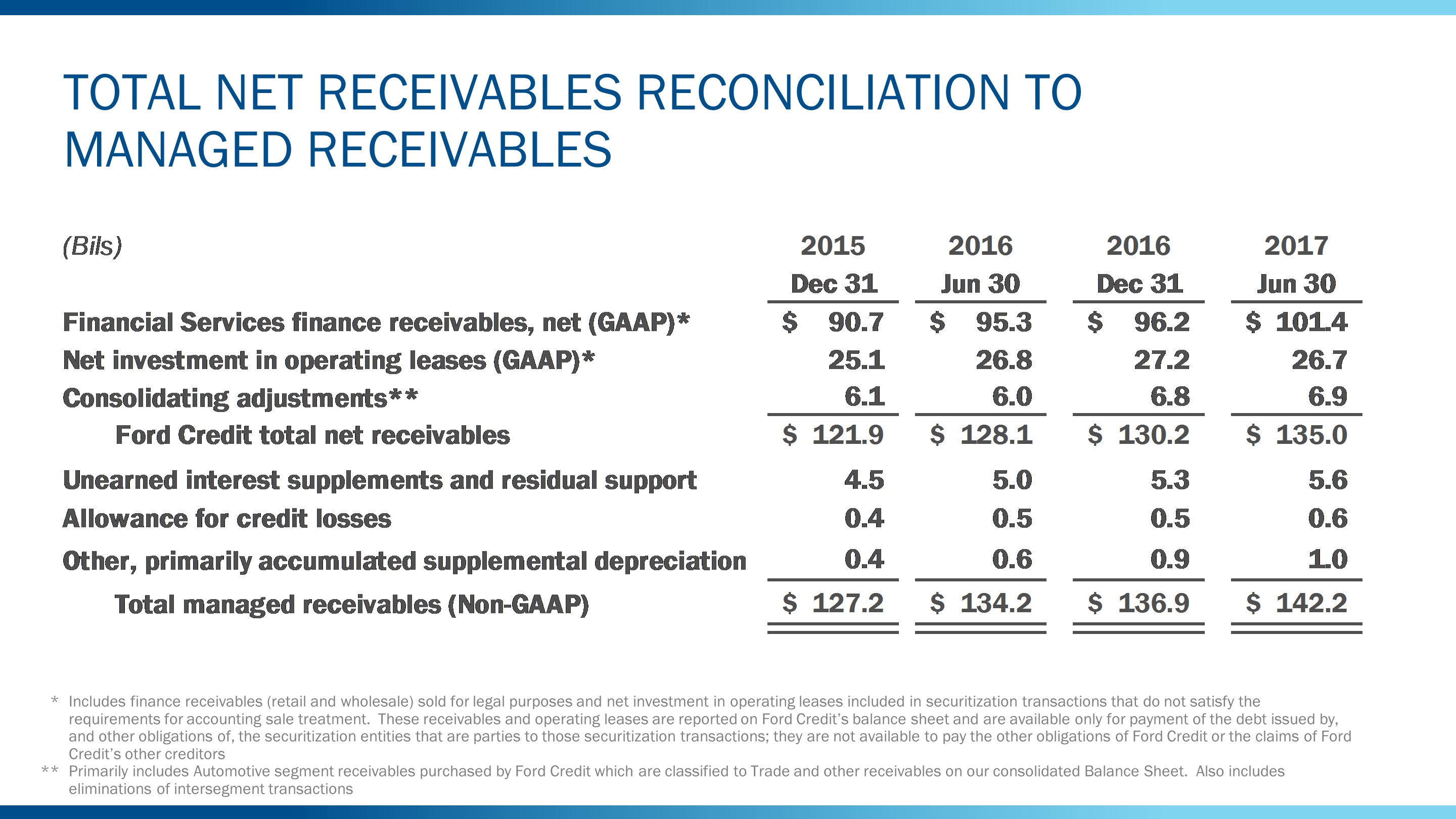

NOTE 8. FINANCIAL SERVICES FINANCE RECEIVABLES

Our Financial Services segment, primarily Ford Credit, manages finance receivables as "consumer" and "non-consumer" portfolios. The receivables are generally secured by the vehicles, inventory, or other property being financed.

Finance receivables, net were as follows (in millions):

| December 31, |

| June 30, | ||||

Consumer |

|

|

| ||||

Retail financing, gross | $ | 68,121 | |

| $ | 71,079 | |

Unearned interest supplements | (2,783 | ) |

| (2,926 | ) | ||

Consumer finance receivables | 65,338 | |

| 68,153 | | ||

Non-Consumer |

| |

|

| | ||

Dealer financing | 31,336 | |

| 33,808 | | ||

Non-Consumer finance receivables | 31,336 | |

| 33,808 | | ||

Total recorded investment | $ | 96,674 | |

| $ | 101,961 | |

|

|

|

| ||||

Recorded investment in finance receivables | $ | 96,674 | |

| $ | 101,961 | |

Allowance for credit losses | (484 | ) |

| (522 | ) | ||

Finance receivables, net | $ | 96,190 | |

| $ | 101,439 | |

|

|

|

| ||||

Current portion | $ | 46,266 | |

| $ | 49,888 | |

Non-current portion | 49,924 | |

| 51,551 | | ||

Finance receivables, net | $ | 96,190 | |

| $ | 101,439 | |

|

|

|

| ||||

Net finance receivables subject to fair value (a) | $ | 94,066 | |

| $ | 98,916 | |

Fair value | 94,785 | |

| 98,872 | | ||

__________

(a) | At December 31, 2016 and June 30, 2017 , Finance receivables, net includes $2.1 billion and $2.5 billion , respectively, of direct financing leases that are not subject to fair value disclosure requirements. The fair value of finance receivables is categorized within Level 3 of the fair value hierarchy. |

Excluded from finance receivables at both December 31, 2016 and June 30, 2017 , was $223 million of accrued uncollected interest, which is reported as Other assets in the current assets section of our consolidated balance sheet.

Included in the recorded investment in finance receivables at December 31, 2016 and June 30, 2017 were consumer receivables of $32.5 billion and $33.1 billion , respectively, and non-consumer receivables of $26 billion and $26.1 billion , respectively, that have been sold for legal purposes in securitization transactions but continue to be reported in our consolidated financial statements. The receivables are available only for payment of the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions; they are not available to pay the other obligations or the claims of Ford Credit's other creditors. Ford Credit holds the right to receive the excess cash flows not needed to pay the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions.

17

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 8. FINANCIAL SERVICES FINANCE RECEIVABLES (Continued)

Aging

For all finance receivables, we define "past due" as any payment, including principal and interest, that is at least 31 days past the contractual due date. The recorded investment of consumer receivables greater than 90 days past due and still accruing interest was $21 million and $23 million at December 31, 2016 and June 30, 2017 , respectively. The recorded investment of non-consumer receivables greater than 90 days past due and still accruing interest was de minimis at December 31, 2016 and $1 million at June 30, 2017 .

The aging analysis of our finance receivables balances were as follows (in millions):

| December 31, |

| June 30, | ||||

Consumer |

|

|

| ||||

31-60 days past due | $ | 760 | |

| $ | 643 | |

61-90 days past due | 114 | |

| 106 | | ||

91-120 days past due | 34 | |

| 36 | | ||

Greater than 120 days past due | 39 | |

| 36 | | ||

Total past due | 947 | |

| 821 | | ||

Current | 64,391 | |

| 67,332 | | ||

Consumer finance receivables | 65,338 | |

| 68,153 | | ||

|

|

|

| ||||

Non-Consumer |

|

|

| ||||

Total past due | 107 | |

| 133 | | ||

Current | 31,229 | |

| 33,675 | | ||

Non-Consumer finance receivables | 31,336 | |

| 33,808 | | ||

Total recorded investment | $ | 96,674 | |

| $ | 101,961 | |

Credit Quality

Consumer Portfolio. Credit quality ratings for consumer receivables are based on aging. Refer to the aging table above.

Consumer receivables credit quality ratings are as follows:

• | Pass – current to 60 days past due |

• | Special Mention – 61 to 120 days past due and in intensified collection status |

• | Substandard – greater than 120 days past due and for which the uncollectible portion of the receivables has already been charged off, as measured using the fair value of collateral less costs to sell |

Non-Consumer Portfolio. Dealers are assigned to one of four groups according to risk ratings as follows:

• | Group I – strong to superior financial metrics |

• | Group II – fair to favorable financial metrics |

• | Group III – marginal to weak financial metrics |

• | Group IV – poor financial metrics, including dealers classified as uncollectible |

18

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 8. FINANCIAL SERVICES FINANCE RECEIVABLES (Continued)

The credit quality analysis of our dealer financing receivables was as follows (in millions):

| December 31, |

| June 30, | ||||

Dealer Financing |

|

|

| ||||

Group I | $ | 24,315 | |

| $ | 26,688 | |

Group II | 5,552 | |

| 5,589 | | ||

Group III | 1,376 | |

| 1,364 | | ||

Group IV | 93 | |

| 167 | | ||

Total recorded investment | $ | 31,336 | |

| $ | 33,808 | |

Impaired Receivables. Impaired consumer receivables include accounts that have been rewritten or modified in reorganization proceedings pursuant to the U.S. Bankruptcy Code that are considered to be Troubled Debt Restructurings ("TDRs"), as well as all accounts greater than 120 days past due. Impaired non-consumer receivables represent accounts with dealers that have weak or poor financial metrics or dealer financing that has been modified in TDRs. The recorded investment of consumer receivables that were impaired at December 31, 2016 and June 30, 2017 was $367 million , or 0.6% of consumer receivables, and $381 million , or 0.6% of consumer receivables, respectively. The recorded investment of non-consumer receivables that were impaired at December 31, 2016 and June 30, 2017 was $107 million , or 0.3% of non-consumer receivables, and $181 million , or 0.5% of non-consumer receivables, respectively. Impaired finance receivables are evaluated both collectively and specifically.

19

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 9. FINANCIAL SERVICES ALLOWANCE FOR CREDIT LOSSES

An analysis of the allowance for credit losses related to finance receivables for the periods ended June 30 was as follows (in millions):

| Second Quarter 2016 |

| First Half 2016 | ||||||||||||||||||||

| Consumer |

| Non-Consumer |

| Total |

| Consumer |

| Non-Consumer |

| Total | ||||||||||||

Allowance for credit losses |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Beginning balance | $ | 390 | |

| $ | 20 | |

| $ | 410 | |

| $ | 357 | |

| $ | 16 | |

| $ | 373 | |

Charge-offs | (94 | ) |

| (3 | ) |

| (97 | ) |

| (196 | ) |

| (2 | ) |

| (198 | ) | ||||||

Recoveries | 31 | |

| 2 | |

| 33 | |

| 60 | |

| 3 | |

| 63 | | ||||||

Provision for credit losses | 109 | |

| (1 | ) |

| 108 | |

| 211 | |

| - | |

| 211 | | ||||||

Other (a) | (4 | ) |

| (1 | ) |

| (5 | ) |

| - | |

| - | |

| - | | ||||||

Ending balance (b) | $ | 432 | |

| $ | 17 | |

| $ | 449 | |

| $ | 432 | |

| $ | 17 | |

| $ | 449 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of allowance for credit losses | |||||||||||||||||||||||

Collective impairment allowance |

|

|

|

|

|

| $ | 414 | |

| $ | 13 | |

| $ | 427 | | ||||||

Specific impairment allowance |

|

|

|

|

|

| 18 | |

| 4 | |

| 22 | | |||||||||

Ending balance (b) |

|

|

|

|

|

| 432 | |

| 17 | |

| 449 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of finance receivables |

|

|

|

|

|

| |||||||||||||||||

Collectively evaluated for impairment |

|

|

|

|

|

| 61,819 | |

| 33,425 | |

| 95,244 | | |||||||||

Specifically evaluated for impairment |

|

|

|

|

|

| 366 | |

| 126 | |

| 492 | | |||||||||

Recorded investment |

|

|

|

|

|

| 62,185 | |

| 33,551 | |

| 95,736 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Ending balance, net of allowance for credit losses |

|

|

| $ | 61,753 | |

| $ | 33,534 | |

| $ | 95,287 | | |||||||||

__________

(a) | Primarily represents amounts related to translation adjustments. |

(b) | Total allowance, including reserves for operating leases, was $512 million . |

| Second Quarter 2017 |

| First Half 2017 | ||||||||||||||||||||

| Consumer |

| Non-Consumer |

| Total |

| Consumer |

| Non-Consumer |

| Total | ||||||||||||

Allowance for credit losses |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Beginning balance | $ | 504 | |

| $ | 13 | |

| $ | 517 | |

| $ | 469 | |

| $ | 15 | |

| $ | 484 | |

Charge-offs | (110 | ) |

| (2 | ) |

| (112 | ) |

| (233 | ) |

| (4 | ) |

| (237 | ) | ||||||

Recoveries | 35 | |

| 3 | |

| 38 | |

| 69 | |

| 3 | |

| 72 | | ||||||

Provision for credit losses | 73 | |

| - | |

| 73 | |

| 194 | |

| - | |

| 194 | | ||||||

Other (a) | 5 | |

| 1 | |

| 6 | |

| 8 | |

| 1 | |

| 9 | | ||||||

Ending balance (b) | $ | 507 | |

| $ | 15 | |

| $ | 522 | |

| $ | 507 | |

| $ | 15 | |

| $ | 522 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of allowance for credit losses | |||||||||||||||||||||||

Collective impairment allowance |

|

|

|

|

|

| $ | 487 | |

| $ | 13 | |

| $ | 500 | | ||||||

Specific impairment allowance |

|

|

|

|

|

| 20 | |

| 2 | |

| 22 | | |||||||||

Ending balance (b) |

|

|

|

|

|

| 507 | |

| 15 | |

| 522 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of finance receivables |

|

|

|

|

|

| |||||||||||||||||

Collectively evaluated for impairment |

|

|

|

|

|

| 67,772 | |

| 33,627 | |

| 101,399 | | |||||||||

Specifically evaluated for impairment |

|

|

|

|

|

| 381 | |

| 181 | |

| 562 | | |||||||||

Recorded investment |

|

|

|

|

|

| 68,153 | |

| 33,808 | |

| 101,961 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Ending balance, net of allowance for credit losses |

| $ | 67,646 | |

| $ | 33,793 | |

| $ | 101,439 | | |||||||||||

__________

(a) | Primarily represents amounts related to translation adjustments. |

(b) | Total allowance, including reserves for operating leases, was $588 million . |

20

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 10. INVENTORIES

All inventories are stated at the lower of cost and net realizable value. Cost for a substantial portion of U.S. inventories is determined on a last-in, first-out ("LIFO") basis. LIFO was used for 30% and 34% of total inventories at December 31, 2016 and June 30, 2017 , respectively. Cost of other inventories is determined by costing methods that approximate a first-in, first-out ("FIFO") basis.

Inventories were as follows (in millions):

| December 31, |

| June 30, | ||||

Raw materials, work-in-process, and supplies | $ | 3,843 | |

| $ | 4,090 | |

Finished products | 5,943 | |

| 7,904 | | ||

Total inventories under FIFO | 9,786 | |

| 11,994 | | ||

LIFO adjustment | (888 | ) |

| (902 | ) | ||

Total inventories | $ | 8,898 | |

| $ | 11,092 | |

NOTE 11. OTHER LIABILITIES AND DEFERRED REVENUE

| December 31, |

| June 30, | ||||

Current |

|

|

| ||||

Dealer and dealers' customer allowances and claims | $ | 9,542 | |

| $ | 11,034 | |

Deferred revenue | 3,866 | |

| 2,443 | | ||

Employee benefit plans | 1,469 | |

| 1,436 | | ||

Accrued interest | 974 | |

| 1,034 | | ||

OPEB (a) | 349 | |

| 351 | | ||

Pension (a) | 247 | |

| 252 | | ||

Other | 2,869 | |

| 3,408 | | ||

Total current other liabilities and deferred revenue | $ | 19,316 | |

| $ | 19,958 | |

Non-current |

| |

|

| | ||

Pension (a) | $ | 10,150 | |

| $ | 10,218 | |

OPEB (a) | 5,516 | |

| 5,526 | | ||

Dealer and dealers' customer allowances and claims | 2,564 | |

| 2,806 | | ||

Deferred revenue | 3,687 | |

| 3,832 | | ||

Employee benefit plans | 1,063 | |

| 1,105 | | ||

Other | 1,415 | |

| 1,353 | | ||

Total non-current other liabilities and deferred revenue | $ | 24,395 | |

| $ | 24,840 | |

__________