|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

(Mark One) |

|

R | Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

|

| For the quarterly period ended June 30, 2015 |

|

|

| or |

|

|

o | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

|

|

| For the transition period from __________ to __________ |

|

|

| Commission file number 1-3950 |

Ford Motor Company

(Exact name of Registrant as specified in its charter)

Delaware | 38-0549190 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

|

|

One American Road, Dearborn, Michigan | 48126 |

(Address of principal executive offices) | (Zip Code) |

313-322-3000

(Registrant's telephone number, including area code)

Indicate by check mark if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes R No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes R No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. Large accelerated filer R Accelerated filer o Non-accelerated filer o Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No R

As of July 21, 2015, Ford had outstanding 3,896,985,910 shares of Common Stock and 70,852,076 shares of Class B Stock.

62 |

|

FORD MOTOR COMPANY

QUARTERLY REPORT ON FORM 10-Q

For the Quarter Ended June 30, 2015

| Table of Contents |

| Page |

| Part I - Financial Information |

|

|

Item 1 | Financial Statements |

| 1 |

| Consolidated Income Statement |

| 1 |

| Consolidated Statement of Comprehensive Income |

| 1 |

| Sector Income Statement |

| 2 |

| Consolidated Balance Sheet |

| 3 |

| Sector Balance Sheet |

| 4 |

| Condensed Consolidated Statement of Cash Flows |

| 5 |

| Condensed Sector Statement of Cash Flows |

| 6 |

| Consolidated Statement of Equity |

| 7 |

| Notes to the Financial Statements |

| 8 |

| Report of Independent Registered Public Accounting Firm |

| 31 |

Item 2 | Management's Discussion and Analysis of Financial Condition and Results of Operations |

| 32 |

| Results of Operations |

| 32 |

| Automotive Sector |

| 33 |

| Financial Services Sector |

| 47 |

| Liquidity and Capital Resources |

| 50 |

| Production Volumes |

| 56 |

| Outlook |

| 57 |

| Accounting Standards Issued But Not Yet Adopted |

| 59 |

| Other Financial Information |

| 59 |

Item 3 | Quantitative and Qualitative Disclosures About Market Risk |

| 59 |

| Automotive Sector |

| 59 |

| Financial Services Sector |

| 59 |

Item 4 | Controls and Procedures |

| 59 |

|

|

|

|

| Part II - Other Information |

|

|

Item 1 | Legal Proceedings |

| 60 |

Item 1A | Risk Factors |

| 60 |

Item 2 | Unregistered Sales of Equity Securities and Use of Proceeds |

| 60 |

Item 6 | Exhibits |

| 60 |

| Signature |

| 61 |

| Exhibit Index |

| 62 |

i

PART I. FINANCIAL INFORMATION

ITEM 1. Financial Statements.

FORD MOTOR COMPANY AND SUBSIDIARIES

CONSOLIDATED INCOME STATEMENT

(in millions, except per share amounts)

| For the periods ended June 30, | ||||||||||||||

| 2015 |

| 2014 |

| 2015 |

| 2014 | ||||||||

| Second Quarter |

| First Half | ||||||||||||

| (unaudited) | ||||||||||||||

Revenues |

|

|

|

|

|

|

| ||||||||

Automotive | $ | 35,105 | |

| $ | 35,365 | |

| $ | 66,905 | |

| $ | 69,241 | |

Financial Services | 2,158 | |

| 2,046 | |

| 4,258 | |

| 4,046 | | ||||

Total revenues | 37,263 | |

| 37,411 | |

| 71,163 | |

| 73,287 | | ||||

|

|

|

|

|

|

|

| ||||||||

Costs and expenses |

| |

|

| |

|

|

|

| ||||||

Automotive cost of sales | 30,602 | |

| 31,247 | |

| 59,304 | |

| 62,268 | | ||||

Selling, administrative, and other expenses | 3,718 | |

| 3,476 | |

| 7,327 | |

| 6,848 | | ||||

Financial Services interest expense | 607 | |

| 683 | |

| 1,254 | |

| 1,361 | | ||||

Financial Services provision for credit and insurance losses | 106 | |

| 104 | |

| 179 | |

| 143 | | ||||

Total costs and expenses | 35,033 | |

| 35,510 | |

| 68,064 | |

| 70,620 | | ||||

|

|

|

|

|

|

|

| ||||||||

Automotive interest expense | 190 | |

| 207 | |

| 355 | |

| 415 | | ||||

|

|

|

|

|

|

|

| ||||||||

Automotive interest income and other income/(loss), net (Note 14) | 272 | |

| 270 | |

| 462 | |

| 484 | | ||||

Financial Services other income/(loss), net (Note 14) | 70 | |

| 87 | |

| 144 | |

| 155 | | ||||

Equity in net income of affiliated companies | 486 | |

| 67 | |

| 923 | |

| 486 | | ||||

Income before income taxes | 2,868 | |

| 2,118 | | | 4,273 | | | 3,377 | | ||||

Provision for/(Benefit from) income taxes (Note 16) | 982 | |

| 803 | |

| 1,462 | |

| 1,073 | | ||||

Net income | 1,886 | |

| 1,315 | |

| 2,811 | |

| 2,304 | | ||||

Less: Income/(Loss) attributable to noncontrolling interests | 1 | |

| 4 | |

| 2 | |

| 4 | | ||||

Net income attributable to Ford Motor Company | $ | 1,885 | |

| $ | 1,311 | |

| $ | 2,809 | |

| $ | 2,300 | |

|

|

|

|

|

|

|

| ||||||||

EARNINGS PER SHARE ATTRIBUTABLE TO FORD MOTOR COMPANY COMMON AND CLASS B STOCK (Note 18) | |||||||||||||||

Basic income | $ | 0.47 | |

| $ | 0.33 | |

| $ | 0.71 | |

| $ | 0.58 | |

Diluted income | 0.47 | |

| 0.32 | |

| 0.70 | |

| 0.57 | | ||||

|

|

|

|

|

|

|

| ||||||||

Cash dividends declared | 0.15 | |

| 0.125 | |

| 0.30 | |

| 0.25 | | ||||

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

(in millions)

| For the periods ended June 30, | ||||||||||||||

| 2015 |

| 2014 |

| 2015 |

| 2014 | ||||||||

| Second Quarter |

| First Half | ||||||||||||

| (unaudited) | ||||||||||||||

Net income | $ | 1,886 | |

| $ | 1,315 | |

| $ | 2,811 | |

| $ | 2,304 | |

Other comprehensive income/(loss), net of tax (Note 13) |

|

|

|

|

|

|

| ||||||||

Foreign currency translation | 328 | |

| 317 | |

| (308 | ) |

| 82 | | ||||

Derivative instruments | (76 | ) |

| (287 | ) |

| (166 | ) |

| (195 | ) | ||||

Pension and other postretirement benefits | (107 | ) |

| 53 | |

| 245 | |

| 236 | | ||||

Total other comprehensive income/(loss), net of tax | 145 | |

| 83 | |

| (229 | ) |

| 123 | | ||||

Comprehensive income | 2,031 | |

| 1,398 | |

| 2,582 | |

| 2,427 | | ||||

Less: Comprehensive income/(loss) attributable to noncontrolling interests | - | |

| 4 | |

| 1 | |

| 4 | | ||||

Comprehensive income attributable to Ford Motor Company | $ | 2,031 | |

| $ | 1,394 | |

| $ | 2,581 | |

| $ | 2,423 | |

The accompanying notes are part of the financial statements.

1

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

SECTOR INCOME STATEMENT

(in millions)

| For the periods ended June 30, | ||||||||||||||

| 2015 |

| 2014 |

| 2015 |

| 2014 | ||||||||

| Second Quarter |

| First Half | ||||||||||||

| (unaudited) | ||||||||||||||

AUTOMOTIVE |

|

|

|

|

|

|

| ||||||||

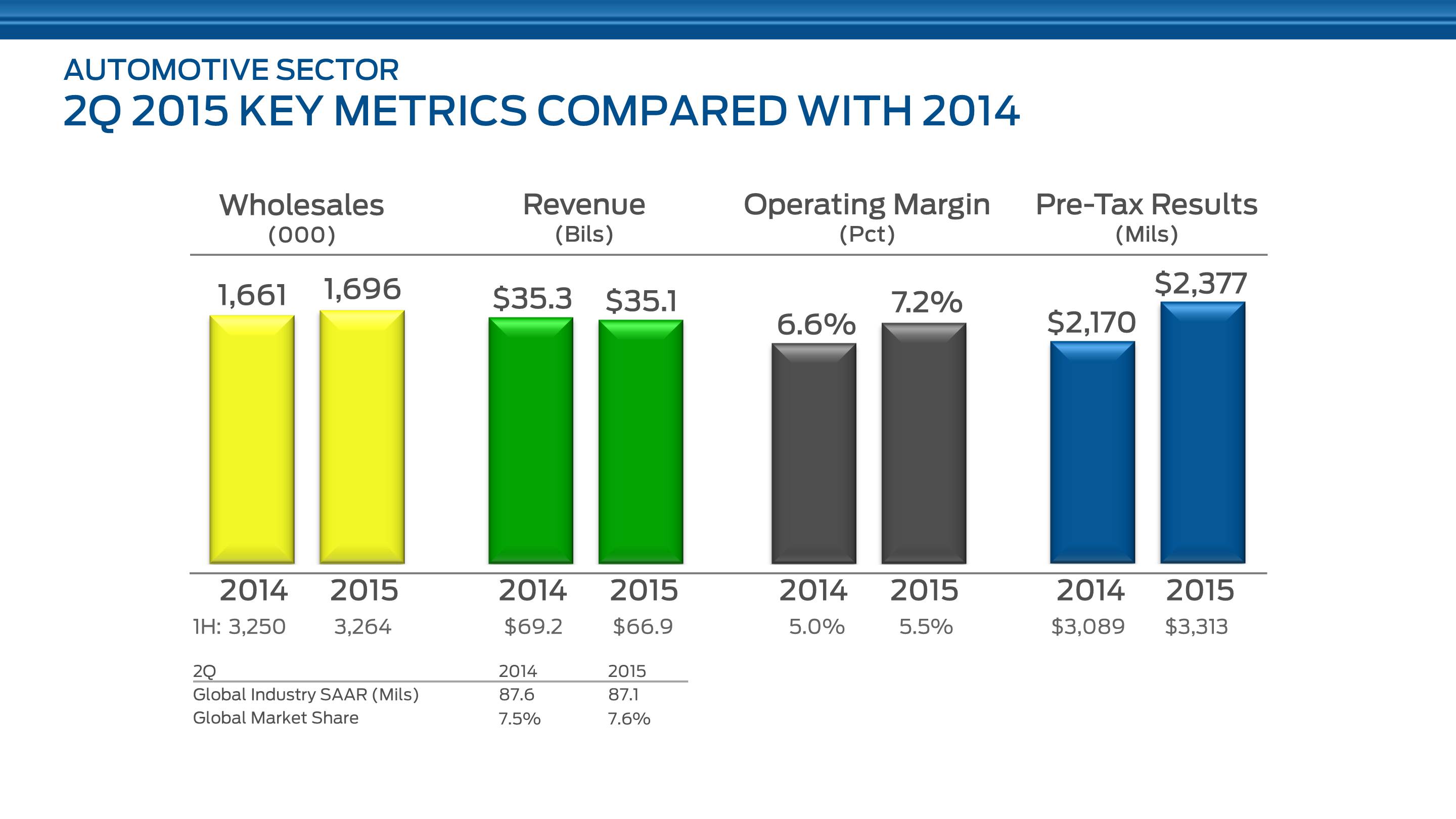

Revenues | $ | 35,105 | |

| $ | 35,365 | |

| $ | 66,905 | |

| $ | 69,241 | |

Costs and expenses |

|

|

|

|

|

|

| ||||||||

Cost of sales | 30,602 | |

| 31,247 | |

| 59,304 | |

| 62,268 | | ||||

Selling, administrative, and other expenses | 2,686 | |

| 2,551 | |

| 5,302 | |

| 5,027 | | ||||

Total costs and expenses | 33,288 | |

| 33,798 | |

| 64,606 | |

| 67,295 | | ||||

|

|

|

|

|

|

|

| ||||||||

Interest expense | 190 | |

| 207 | |

| 355 | |

| 415 | | ||||

|

|

|

|

|

|

|

| ||||||||

Interest income and other income/(loss), net (Note 14) | 272 | |

| 270 | |

| 462 | |

| 484 | | ||||

Equity in net income of affiliated companies | 478 | |

| 59 | |

| 907 | |

| 471 | | ||||

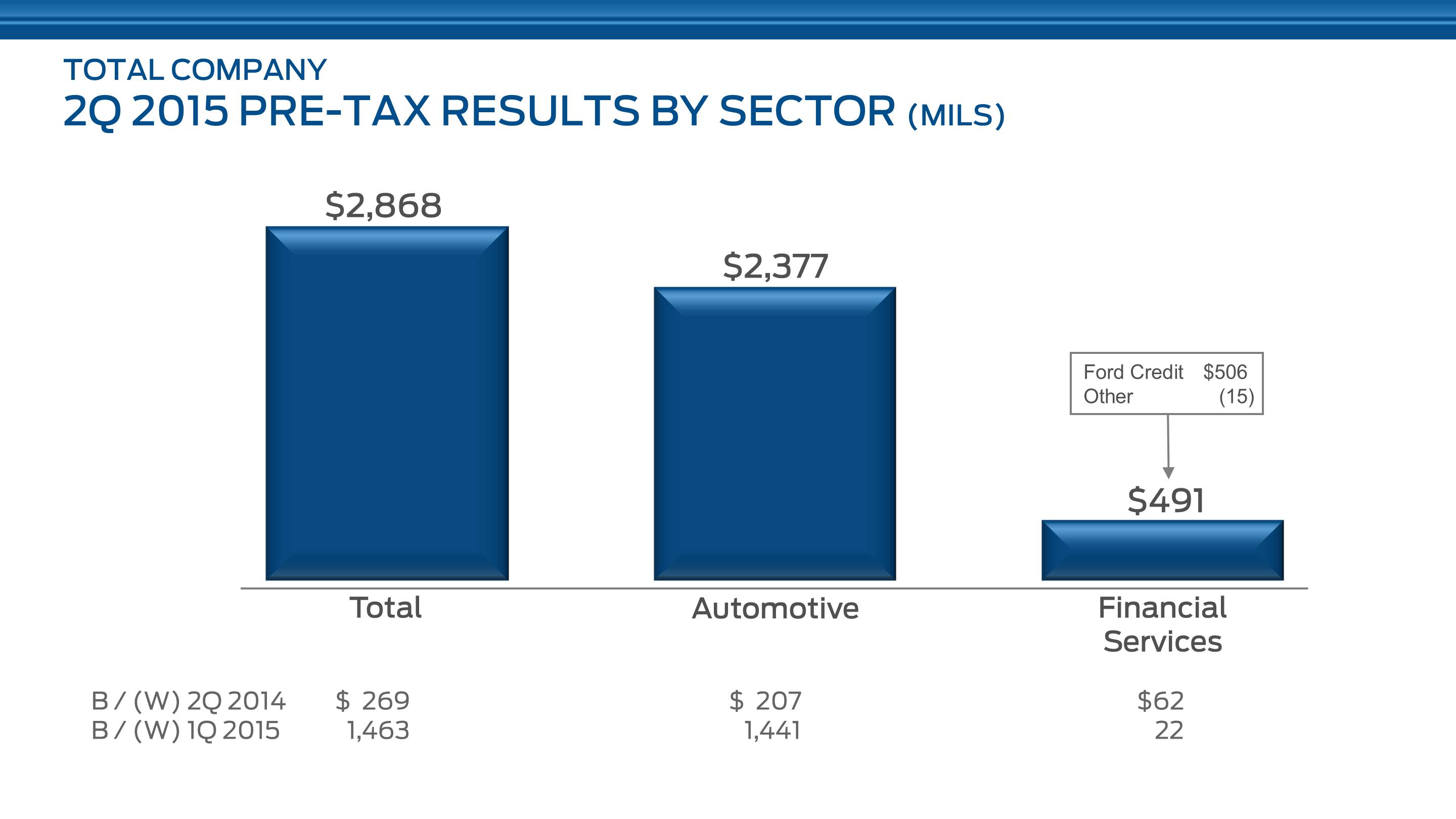

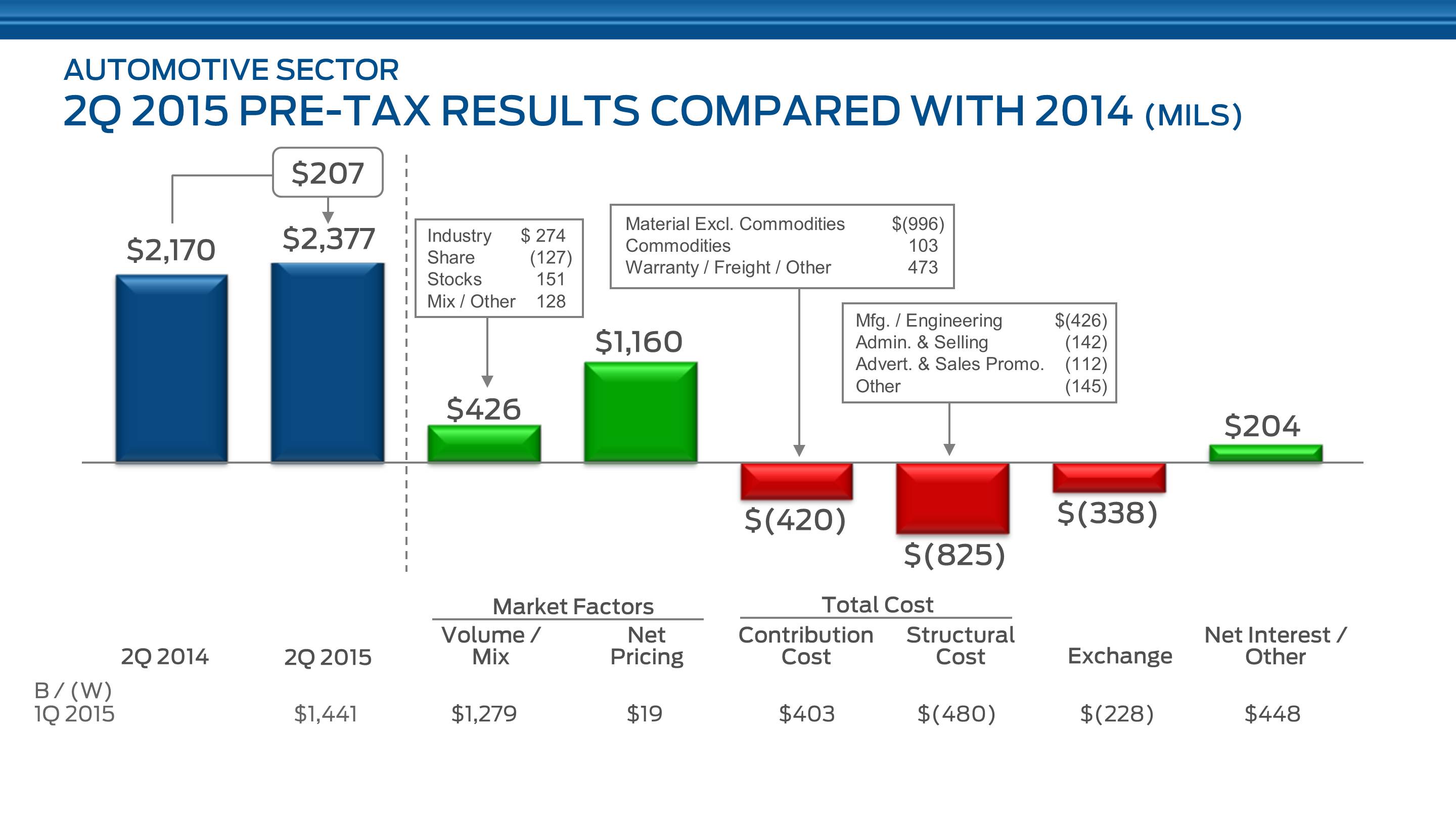

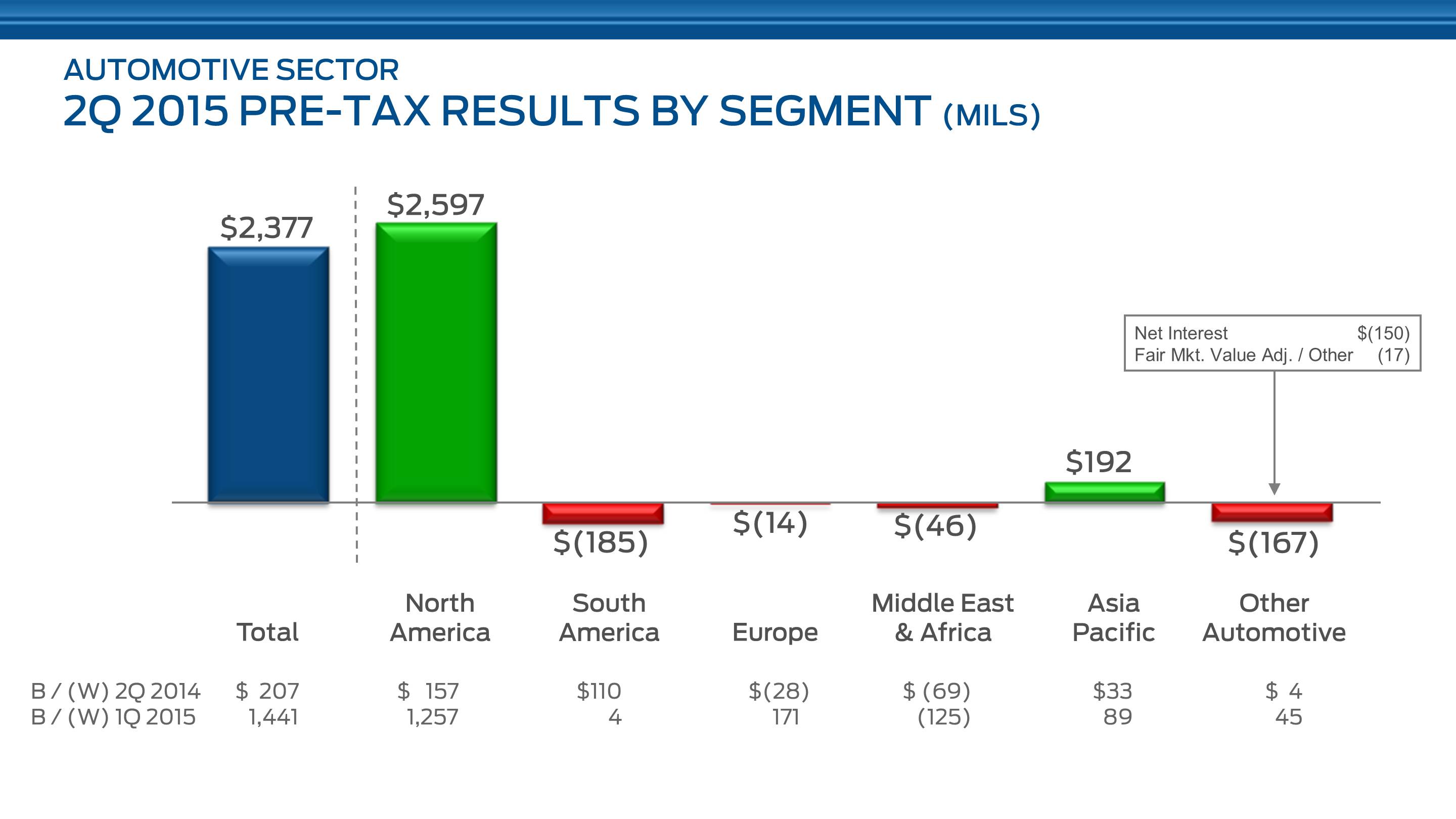

Income before income taxes - Automotive | 2,377 | |

| 1,689 | |

| 3,313 | |

| 2,486 | | ||||

|

|

|

|

|

|

|

| ||||||||

FINANCIAL SERVICES |

| |

|

| |

|

|

|

| ||||||

Revenues | 2,158 | |

| 2,046 | |

| 4,258 | |

| 4,046 | | ||||

Costs and expenses |

|

|

|

|

|

|

| ||||||||

Interest expense | 607 | |

| 683 | |

| 1,254 | |

| 1,361 | | ||||

Depreciation on vehicles subject to operating leases | 858 | |

| 742 | |

| 1,674 | |

| 1,448 | | ||||

Operating and other expenses | 174 | |

| 183 | |

| 351 | |

| 373 | | ||||

Provision for credit and insurance losses | 106 | |

| 104 | |

| 179 | |

| 143 | | ||||

Total costs and expenses | 1,745 | |

| 1,712 | |

| 3,458 | |

| 3,325 | | ||||

|

|

|

|

|

|

|

| ||||||||

Other income/(loss), net (Note 14) | 70 | |

| 87 | |

| 144 | |

| 155 | | ||||

Equity in net income of affiliated companies | 8 | |

| 8 | |

| 16 | |

| 15 | | ||||

Income before income taxes - Financial Services | 491 | |

| 429 | |

| 960 | |

| 891 | | ||||

|

|

|

|

|

|

|

| ||||||||

TOTAL COMPANY |

|

|

|

|

|

|

| ||||||||

Income before income taxes | 2,868 | |

| 2,118 | |

| 4,273 | |

| 3,377 | | ||||

Provision for/(Benefit from) income taxes (Note 16) | 982 | |

| 803 | |

| 1,462 | |

| 1,073 | | ||||

Net income | 1,886 | |

| 1,315 | |

| 2,811 | |

| 2,304 | | ||||

Less: Income/(Loss) attributable to noncontrolling interests | 1 | |

| 4 | |

| 2 | |

| 4 | | ||||

Net income attributable to Ford Motor Company | $ | 1,885 | |

| $ | 1,311 | |

| $ | 2,809 | |

| $ | 2,300 | |

The accompanying notes are part of the financial statements.

2

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEET

(in millions)

| June 30, |

| December 31, | ||||

| (unaudited) | ||||||

ASSETS |

|

|

| ||||

Cash and cash equivalents | $ | 12,897 | |

| $ | 10,757 | |

Marketable securities | 18,405 | |

| 20,393 | | ||

Finance receivables, net (Note 4) | 82,821 | |

| 81,111 | | ||

Other receivables, net | 12,666 | |

| 11,708 | | ||

Net investment in operating leases | 26,148 | |

| 23,217 | | ||

Inventories (Note 6) | 9,438 | |

| 7,866 | | ||

Equity in net assets of affiliated companies | 3,469 | |

| 3,357 | | ||

Net property | 30,750 | |

| 30,126 | | ||

Deferred income taxes | 12,497 | |

| 13,639 | | ||

Other assets | 6,954 | |

| 6,353 | | ||

Total assets | $ | 216,045 | |

| $ | 208,527 | |

|

|

|

| ||||

LIABILITIES |

| |

|

| | ||

Payables | $ | 21,844 | |

| $ | 20,035 | |

Other liabilities and deferred revenue (Note 7) | 43,649 | |

| 43,577 | | ||

Debt (Note 9) | 123,526 | |

| 119,171 | | ||

Deferred income taxes | 578 | |

| 570 | | ||

Total liabilities | 189,597 | |

| 183,353 | | ||

|

|

|

| ||||

Redeemable noncontrolling interest (Note 10) | 93 | |

| 342 | | ||

|

|

|

| ||||

EQUITY |

| |

|

| | ||

Capital stock |

| |

|

| | ||

Common Stock, par value $.01 per share (3,959 million shares issued of 6 billion authorized) | 40 | |

| 39 | | ||

Class B Stock, par value $.01 per share (71 million shares issued of 530 million authorized) | 1 | |

| 1 | | ||

Capital in excess of par value of stock | 21,317 | |

| 21,089 | | ||

Retained earnings | 26,175 | |

| 24,556 | | ||

Accumulated other comprehensive income/(loss) (Note 13) | (20,260 | ) |

| (20,032 | ) | ||

Treasury stock | (939 | ) |

| (848 | ) | ||

Total equity attributable to Ford Motor Company | 26,334 | |

| 24,805 | | ||

Equity attributable to noncontrolling interests | 21 | |

| 27 | | ||

Total equity | 26,355 | |

| 24,832 | | ||

Total liabilities and equity | $ | 216,045 | |

| $ | 208,527 | |

The following table includes assets to be used to settle liabilities of the consolidated variable interest entities ("VIEs"). These assets and liabilities are included in the consolidated balance sheet above. See Note 11 for additional information on our VIEs.

| June 30, |

| December 31, | ||||

| (unaudited) | ||||||

ASSETS |

|

|

| ||||

Cash and cash equivalents | $ | 2,355 | |

| $ | 2,094 | |

Finance receivables, net | 43,563 | |

| 39,522 | | ||

Net investment in operating leases | 11,878 | |

| 9,631 | | ||

Other assets | 55 | |

| 27 | | ||

LIABILITIES |

|

|

| ||||

Other liabilities and deferred revenue | $ | 30 | |

| $ | 22 | |

Debt | 40,595 | |

| 37,156 | | ||

The accompanying notes are part of the financial statements.

3

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

SECTOR BALANCE SHEET (in millions)

| June 30, |

| December 31, | ||||

ASSETS | (unaudited) | ||||||

Automotive |

|

|

| ||||

Cash and cash equivalents | $ | 6,130 | |

| $ | 4,567 | |

Marketable securities | 14,599 | |

| 17,135 | | ||

Total cash and marketable securities | 20,729 | |

| 21,702 | | ||

Receivables, less allowances of $403 and $455 | 5,793 | |

| 5,789 | | ||

Inventories (Note 6) | 9,438 | |

| 7,866 | | ||

Deferred income taxes | 2,779 | |

| 2,039 | | ||

Net investment in operating leases | 2,765 | |

| 1,699 | | ||

Other current assets | 1,372 | |

| 1,347 | | ||

Total current assets | 42,876 | |

| 40,442 | | ||

Equity in net assets of affiliated companies | 3,323 | |

| 3,216 | | ||

Net property | 30,623 | |

| 29,795 | | ||

Deferred income taxes | 12,151 | |

| 13,331 | | ||

Other assets | 3,555 | |

| 2,798 | | ||

Non-current receivable from Financial Services | - | |

| 497 | | ||

Total Automotive assets | 92,528 | |

| 90,079 | | ||

Financial Services |

| |

|

| | ||

Cash and cash equivalents | 6,767 | |

| 6,190 | | ||

Marketable securities | 3,806 | |

| 3,258 | | ||

Finance receivables, net (Note 4) | 88,796 | |

| 86,141 | | ||

Net investment in operating leases | 23,383 | |

| 21,518 | | ||

Equity in net assets of affiliated companies | 146 | |

| 141 | | ||

Other assets | 3,229 | |

| 3,613 | | ||

Receivable from Automotive | 256 | |

| 527 | | ||

Total Financial Services assets | 126,383 | |

| 121,388 | | ||

Intersector elimination | (256 | ) |

| (1,024 | ) | ||

Total assets | $ | 218,655 | |

| $ | 210,443 | |

LIABILITIES |

| |

|

| | ||

Automotive |

| |

|

| | ||

Payables | $ | 20,640 | |

| $ | 18,876 | |

Other liabilities and deferred revenue (Note 7) | 18,382 | |

| 17,934 | | ||

Deferred income taxes | 334 | |

| 270 | | ||

Debt payable within one year (Note 9) | 2,188 | |

| 2,501 | | ||

Current payable to Financial Services | 241 | |

| 527 | | ||

Total current liabilities | 41,785 | |

| 40,108 | | ||

Long-term debt (Note 9) | 11,525 | |

| 11,323 | | ||

Other liabilities and deferred revenue (Note 7) | 23,346 | |

| 23,793 | | ||

Deferred income taxes | 301 | |

| 367 | | ||

Non-current payable to Financial Services | 15 | |

| - | | ||

Total Automotive liabilities | 76,972 | |

| 75,591 | | ||

Financial Services |

| |

|

| | ||

Payables | 1,204 | |

| 1,159 | | ||

Debt (Note 9) | 109,813 | |

| 105,347 | | ||

Deferred income taxes | 2,553 | |

| 1,849 | | ||

Other liabilities and deferred income (Note 7) | 1,921 | |

| 1,850 | | ||

Payable to Automotive | - | |

| 497 | | ||

Total Financial Services liabilities | 115,491 | |

| 110,702 | | ||

Intersector elimination | (256 | ) |

| (1,024 | ) | ||

Total liabilities | 192,207 | |

| 185,269 | | ||

|

|

|

| ||||

Redeemable noncontrolling interest (Note 10) | 93 | |

| 342 | | ||

|

|

|

| ||||

EQUITY |

| |

|

| | ||

Capital stock |

| |

|

| | ||

Common Stock, par value $.01 per share (3,959 million shares issued of 6 billion authorized) | 40 | |

| 39 | | ||

Class B Stock, par value $.01 per share (71 million shares issued of 530 million authorized) | 1 | |

| 1 | | ||

Capital in excess of par value of stock | 21,317 | |

| 21,089 | | ||

Retained earnings | 26,175 | |

| 24,556 | | ||

Accumulated other comprehensive income/(loss) (Note 13) | (20,260 | ) |

| (20,032 | ) | ||

Treasury stock | (939 | ) |

| (848 | ) | ||

Total equity attributable to Ford Motor Company | 26,334 | |

| 24,805 | | ||

Equity attributable to noncontrolling interests | 21 | |

| 27 | | ||

Total equity | 26,355 | |

| 24,832 | | ||

Total liabilities and equity | $ | 218,655 | |

| $ | 210,443 | |

The accompanying notes are part of the financial statements.

4

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CASH FLOWS

(in millions)

| For the periods ended June 30, | ||||||

| 2015 |

| 2014 | ||||

| First Half | ||||||

| (unaudited) | ||||||

Cash flows from operating activities |

|

|

| ||||

Net cash provided by/(used in) operating activities | $ | 7,623 | |

| $ | 6,970 | |

|

|

|

| ||||

Cash flows from investing activities |

|

|

| ||||

Capital spending | (3,533 | ) |

| (3,428 | ) | ||

Acquisitions of finance receivables and operating leases | (26,505 | ) |

| (24,616 | ) | ||

Collections of finance receivables and operating leases | 18,844 | |

| 18,277 | | ||

Purchases of marketable securities | (21,282 | ) |

| (26,468 | ) | ||

Sales and maturities of marketable securities | 23,193 | |

| 24,397 | | ||

Settlements of derivatives | 192 | |

| 29 | | ||

Other | 141 | |

| 124 | | ||

Net cash provided by/(used in) investing activities | (8,950 | ) |

| (11,685 | ) | ||

|

|

|

| ||||

Cash flows from financing activities |

| |

|

| | ||

Cash dividends | (1,190 | ) |

| (987 | ) | ||

Purchases of Common Stock | (91 | ) |

| (862 | ) | ||

Net changes in short-term debt | 176 | |

| (3,188 | ) | ||

Proceeds from issuance of other debt | 24,912 | |

| 22,755 | | ||

Principal payments on other debt | (19,787 | ) |

| (15,925 | ) | ||

Other | (279 | ) |

| 9 | | ||

Net cash provided by/(used in) financing activities | 3,741 | |

| 1,802 | | ||

|

|

|

| ||||

Effect of exchange rate changes on cash and cash equivalents | (274 | ) |

| 18 | | ||

|

|

|

| ||||

Net increase/(decrease) in cash and cash equivalents | $ | 2,140 | |

| $ | (2,895 | ) |

|

|

|

| ||||

Cash and cash equivalents at January 1 | $ | 10,757 | |

| $ | 14,468 | |

Net increase/(decrease) in cash and cash equivalents | 2,140 | |

| (2,895 | ) | ||

Cash and cash equivalents at June 30 | $ | 12,897 | |

| $ | 11,573 | |

The accompanying notes are part of the financial statements.

5

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

CONDENSED SECTOR STATEMENT OF CASH FLOWS

(in millions)

| For the periods ended June 30, | ||||||||||||||

| 2015 |

| 2014 | ||||||||||||

| First Half | ||||||||||||||

| Automotive |

| Financial Services |

| Automotive |

| Financial Services | ||||||||

| (unaudited) | ||||||||||||||

Cash flows from operating activities |

|

|

|

|

|

|

| ||||||||

Net cash provided by/(used in) operating activities (a) | $ | 4,461 | |

| $ | 3,020 | |

| $ | 6,108 | |

| $ | 2,553 | |

|

|

|

|

|

|

|

| ||||||||

Cash flows from investing activities |

|

|

|

|

|

|

| ||||||||

Capital spending | (3,505 | ) |

| (28 | ) |

| (3,402 | ) |

| (26 | ) | ||||

Acquisitions of finance receivables and operating leases (excluding wholesale and other) | - | |

| (26,505 | ) |

| - | |

| (24,616 | ) | ||||

Collections of finance receivables and operating leases (excluding wholesale and other) | - | |

| 18,844 | |

| - | |

| 18,277 | | ||||

Net change in wholesale and other receivables (b) | - | |

| (1,273 | ) |

| - | |

| (3,256 | ) | ||||

Purchases of marketable securities | (14,583 | ) |

| (6,699 | ) |

| (19,465 | ) |

| (7,003 | ) | ||||

Sales and maturities of marketable securities | 17,050 | |

| 6,143 | |

| 18,499 | |

| 5,898 | | ||||

Settlements of derivatives | 29 | |

| 163 | |

| 91 | |

| (62 | ) | ||||

Other | 73 | |

| 68 | |

| 40 | |

| 84 | | ||||

Investing activity (to)/from Financial Services (c) | 28 | |

| - | |

| 21 | |

| - | | ||||

Interest supplements and residual value support from Automotive (a) | - | |

| 1,415 | |

| - | |

| 1,565 | | ||||

Net cash provided by/(used in) investing activities | (908 | ) | | (7,872 | ) | | (4,216 | ) | | (9,139 | ) | ||||

|

|

|

|

|

|

|

| ||||||||

Cash flows from financing activities |

|

|

|

|

|

|

| ||||||||

Cash dividends | (1,190 | ) |

| - | |

| (987 | ) |

| - | | ||||

Purchases of Common Stock | (91 | ) |

| - | |

| (862 | ) |

| - | | ||||

Net changes in short-term debt | 29 | |

| 147 | |

| 192 | |

| (3,380 | ) | ||||

Proceeds from issuance of other debt | 581 | |

| 24,331 | |

| 100 | |

| 22,655 | | ||||

Principal payments on other debt | (1,006 | ) |

| (18,781 | ) |

| (656 | ) |

| (15,269 | ) | ||||

Other | (223 | ) |

| (56 | ) |

| 75 | |

| (66 | ) | ||||

Financing activity to/(from) Automotive (c) | - | |

| (28 | ) |

| - | |

| (21 | ) | ||||

Net cash provided by/(used in) financing activities | (1,900 | ) |

| 5,613 | |

| (2,138 | ) |

| 3,919 | | ||||

|

|

|

|

|

|

|

| ||||||||

Effect of exchange rate changes on cash and cash equivalents | (90 | ) |

| (184 | ) |

| 23 | |

| (5 | ) | ||||

|

|

|

|

|

|

|

| ||||||||

Net increase/(decrease) in cash and cash equivalents | $ | 1,563 | | | $ | 577 | | | $ | (223 | ) | | $ | (2,672 | ) |

|

|

|

|

|

|

|

| ||||||||

Cash and cash equivalents at January 1 | $ | 4,567 | |

| $ | 6,190 | |

| $ | 4,959 | |

| $ | 9,509 | |

Net increase/(decrease) in cash and cash equivalents | 1,563 | |

| 577 | |

| (223 | ) |

| (2,672 | ) | ||||

Cash and cash equivalents at June 30 | $ | 6,130 | | | $ | 6,767 | | | $ | 4,736 | | | $ | 6,837 | |

_________

(a) | Operating activities include outflows of $1,415 million and $1,565 million for the periods ended June 30, 2015 and 2014 , respectively, of interest supplements and residual value support to Financial Services. Interest supplements and residual value support from Automotive to Financial Services are eliminated in the condensed consolidated statement of cash flows. |

(b) | Reclassified to operating activities in the condensed consolidated statement of cash flows. |

(c) | Eliminated in the condensed consolidated statement of cash flows. |

The accompanying notes are part of the financial statements.

6

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

CONSOLIDATED STATEMENT OF EQUITY

(in millions, unaudited)

| Equity Attributable to Ford Motor Company |

|

|

|

| ||||||||||||||||||||||||||

| Capital Stock |

| Cap. in Excess of Par Value of Stock |

| Retained Earnings |

| Accumulated Other Comprehensive Income/(Loss) (Note 13) |

| Treasury Stock |

| Total |

| Equity Attributable to Non-controlling Interests |

| Total Equity | ||||||||||||||||

Balance at December 31, 2014 | $ | 40 | |

| $ | 21,089 | |

| $ | 24,556 | |

| $ | (20,032 | ) |

| $ | (848 | ) |

| $ | 24,805 | |

| $ | 27 | |

| $ | 24,832 | |

Net income | - | |

| - | |

| 2,809 | |

| - | |

| - | |

| 2,809 | |

| 2 | |

| 2,811 | | ||||||||

Other comprehensive income/(loss), net of tax | - | |

| - | |

| - | |

| (228 | ) |

| - | |

| (228 | ) |

| (1 | ) |

| (229 | ) | ||||||||

Common stock issued (including share-based compensation impacts) | 1 | |

| 228 | |

| - | |

| - | |

| - | |

| 229 | |

| - | |

| 229 | | ||||||||

Treasury stock/other | - | |

| - | |

| - | |

| - | |

| (91 | ) |

| (91 | ) |

| (1 | ) |

| (92 | ) | ||||||||

Cash dividends declared | - | |

| - | |

| (1,190 | ) |

| - | |

| - | |

| (1,190 | ) |

| (6 | ) |

| (1,196 | ) | ||||||||

Balance at June 30, 2015 | $ | 41 | |

| $ | 21,317 | |

| $ | 26,175 | |

| $ | (20,260 | ) |

| $ | (939 | ) |

| $ | 26,334 | |

| $ | 21 | |

| $ | 26,355 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Balance at December 31, 2013 | $ | 40 | |

| $ | 21,422 | |

| $ | 23,386 | |

| $ | (18,230 | ) |

| $ | (506 | ) |

| $ | 26,112 | |

| $ | 33 | |

| $ | 26,145 | |

Net income | - | |

| - | |

| 2,300 | |

| - | |

| - | |

| 2,300 | |

| 4 | |

| 2,304 | | ||||||||

Other comprehensive income/(loss), net of tax | - | |

| - | |

| - | |

| 123 | |

| - | |

| 123 | |

| - | |

| 123 | | ||||||||

Common stock issued (including share-based compensation impacts) | - | |

| 201 | |

| - | |

| - | |

| - | |

| 201 | |

| - | |

| 201 | | ||||||||

Treasury stock/other | - | |

| (18 | ) |

| - | |

| - | |

| (955 | ) |

| (973 | ) |

| (4 | ) |

| (977 | ) | ||||||||

Cash dividends declared | - | |

| - | |

| (987 | ) |

| - | |

| - | |

| (987 | ) |

| (2 | ) |

| (989 | ) | ||||||||

Balance at June 30, 2014 | $ | 40 | |

| $ | 21,605 | |

| $ | 24,699 | |

| $ | (18,107 | ) |

| $ | (1,461 | ) |

| $ | 26,776 | |

| $ | 31 | |

| $ | 26,807 | |

The accompanying notes are part of the financial statements.

7

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

Table of Contents

Footnote |

| Page |

Note 1 | Presentation | 9 |

Note 2 | Accounting Standards Issued But Not Yet Adopted | 10 |

Note 3 | Fair Value Measurements | 11 |

Note 4 | Financial Services Sector Finance Receivables | 12 |

Note 5 | Financial Services Sector Allowance for Credit Losses | 15 |

Note 6 | Inventories | 16 |

Note 7 | Other Liabilities and Deferred Revenue | 16 |

Note 8 | Retirement Benefits | 17 |

Note 9 | Debt | 18 |

Note 10 | Redeemable Noncontrolling Interest | 19 |

Note 11 | Variable Interest Entities | 19 |

Note 12 | Derivative Financial Instruments and Hedging Activities | 20 |

Note 13 | Accumulated Other Comprehensive Income/(Loss) | 22 |

Note 14 | Other Income/(Loss) | 23 |

Note 15 | Employee Separation Actions and Exit and Disposal Activities | 24 |

Note 16 | Income Taxes | 25 |

Note 17 | Changes in Investments in Affiliates | 25 |

Note 18 | Capital Stock and Earnings Per Share | 26 |

Note 19 | Segment Information | 26 |

Note 20 | Commitments and Contingencies | 29 |

8

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 1. PRESENTATION

Our financial statements are presented in accordance with U.S. generally accepted accounting principles ("GAAP") for interim financial information and instructions to the Quarterly Report on Form 10-Q and Rule 10-01 of Regulation S-X. We show certain of our financial statements on both a consolidated and a sector basis for our Automotive and Financial Services sectors. Intercompany items have been eliminated in both the consolidated and sector balance sheets. Where the presentation of these intercompany eliminations or consolidated adjustments differs between the consolidated and sector financial statements, reconciliations of certain line items are explained below in this Note or in the related financial statements and footnotes.

In the opinion of management, these unaudited financial statements reflect a fair statement of the results of operations and financial condition of Ford Motor Company, its consolidated subsidiaries, and consolidated VIEs of which we are the primary beneficiary for the periods and at the dates presented. The results for interim periods are not necessarily indicative of results that may be expected for any other interim period or for the full year. Reference should be made to the financial statements contained in our Annual Report on Form 10-K for the year ended December 31, 2014 (" 2014 Form 10-K Report"). For purposes of this report, "Ford," the "Company," "we," "our," "us" or similar references mean Ford Motor Company, our consolidated subsidiaries, and our consolidated VIEs of which we are the primary beneficiary, unless the context requires otherwise.

We reclassified certain prior year amounts in our consolidated financial statements to conform to current year presentation.

Adoption of New Accounting Standards

Accounting Standards Update ("ASU") 2014-11, Transfers and Servicing - Repurchase-to-Maturity Transactions, Repurchase Financings and Disclosures. On January 1, 2015, we adopted the new accounting standard that changes the accounting for repurchase-to-maturity transactions and repurchase financing arrangements. The new standard also requires additional disclosures for certain transfers of financial assets with agreements that both entitle and obligate the transferor to repurchase the transferred assets from the transferee. The adoption of this accounting standard did not impact our financial statements or financial statement disclosures.

Reconciliations between Consolidated and Sector Financial Statements

Sector to Consolidated Deferred Tax Assets and Liabilities. The difference between the total assets and total liabilities as presented on our sector balance sheet and consolidated balance sheet is the result of netting deferred income tax assets and liabilities. The reconciliation between the totals for the sector and consolidated balance sheets was as follows (in millions):

| June 30, |

| December 31, | ||||

Sector balance sheet presentation of deferred income tax assets |

|

|

| ||||

Automotive sector current deferred income tax assets | $ | 2,779 | |

| $ | 2,039 | |

Automotive sector non-current deferred income tax assets | 12,151 | |

| 13,331 | | ||

Financial Services sector deferred income tax assets (a) | 177 | |

| 185 | | ||

Total | 15,107 | |

| 15,555 | | ||

Reclassification for netting of deferred income taxes | (2,610 | ) |

| (1,916 | ) | ||

Consolidated balance sheet presentation of deferred income tax assets | $ | 12,497 | |

| $ | 13,639 | |

|

|

|

| ||||

Sector balance sheet presentation of deferred income tax liabilities |

| |

|

| | ||

Automotive sector current deferred income tax liabilities | $ | 334 | |

| $ | 270 | |

Automotive sector non-current deferred income tax liabilities | 301 | |

| 367 | | ||

Financial Services sector deferred income tax liabilities | 2,553 | |

| 1,849 | | ||

Total | 3,188 | |

| 2,486 | | ||

Reclassification for netting of deferred income taxes | (2,610 | ) |

| (1,916 | ) | ||

Consolidated balance sheet presentation of deferred income tax liabilities | $ | 578 | |

| $ | 570 | |

__________

(a) | Financial Services deferred income tax assets are included in Financial Services Other assets on our sector balance sheet. |

9

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 2. ACCOUNTING STANDARDS ISSUED BUT NOT YET ADOPTED

ASU 2014-09, Revenue - Revenue from Contracts with Customers. In May 2014, the Financial Accounting Standards Board ("FASB") issued a new accounting standard that requires recognition of revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which we expect to be entitled in exchange for those goods or services. The new standard supersedes virtually all present U.S. GAAP guidance on revenue recognition and requires the use of more estimates and judgments than the present standards, as well as additional disclosures. The FASB has voted to approve a one-year deferral of the effective date from January 1, 2017 to January 1, 2018, while allowing for early adoption as of January 1, 2017. The new accounting standard is expected to have an impact to our income statement, balance sheet, and financial statement disclosures and we are reviewing our arrangements to evaluate the impact and method of adoption.

The FASB also issued the following standards, none of which are expected to have a material impact to our financial statements or financial statement disclosures.

| Standard |

| Effective Date | |

| 2015-09 | Insurance - Disclosures about Short-Duration Contracts |

| January 1, 2016 |

| 2015-07 | Fair Value Measurement - Disclosures for Investments in Certain Entities that Calculate Net Asset Value per Share (or Its Equivalent) |

| January 1, 2016 |

| 2015-05 | Internal-Use Software - Customer's Accounting for Fees Paid in a Cloud Computing Arrangement |

| January 1, 2016 |

| 2015-03 | Imputation of Interest - Simplifying the Presentation of Debt Issuance Costs |

| January 1, 2016 |

| 2015-02 | Consolidation - Amendments to the Consolidation Analysis |

| January 1, 2016 |

| 2015-01 | Extraordinary and Unusual Items - Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items |

| January 1, 2016 |

| 2014-16 | Derivatives and Hedging - Determining Whether the Host Contract in a Hybrid Financial Instrument Issued in the Form of a Share Is More Akin to Debt or to Equity |

| January 1, 2016 |

| 2014-13 | Consolidation - Measuring the Financial Assets and the Financial Liabilities of a Consolidated Collateralized Financing Entity |

| January 1, 2016 |

| 2014-12 | Stock Compensation - Accounting for Share-Based Payments When the Terms of an Award Provide That a Performance Target Could Be Achieved after the Requisite Service Period |

| January 1, 2016 |

| 2014-15 | Going Concern - Disclosure of Uncertainties about an Entity's Ability to Continue as a Going Concern |

| December 31, 2016 |

| 2015-11 | Inventory - Simplifying the Measurement of Inventory |

| January 1, 2017 |

10

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 3. FAIR VALUE MEASUREMENTS

Cash equivalents, marketable securities, and derivative financial instruments are remeasured and presented on our financial statements on a recurring basis at fair value, while other assets and liabilities are measured at fair value on a nonrecurring basis.

There have been no changes to the types of inputs used or the valuation techniques since year end.

Input Hierarchy of Items Measured at Fair Value on a Recurring Basis

The following table categorizes the fair values of items measured at fair value on a recurring basis on our balance sheet (in millions):

| June 30, 2015 |

| December 31, 2014 | ||||||||||||||||||||||||||||

| Level 1 |

| Level 2 |

| Level 3 |

| Total |

| Level 1 |

| Level 2 |

| Level 3 |

| Total | ||||||||||||||||

Automotive Sector |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Cash equivalents – financial instruments |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

U.S. government and agencies | $ | - | |

| $ | 8 | |

| $ | - | |

| $ | 8 | |

| $ | - | |

| $ | 64 | |

| $ | - | |

| $ | 64 | |

Non-U.S. government and agencies | - | |

| 249 | |

| - | |

| 249 | |

| - | |

| 122 | |

| - | |

| 122 | | ||||||||

Corporate debt | - | |

| 10 | |

| - | |

| 10 | |

| - | |

| 20 | |

| - | |

| 20 | | ||||||||

Total cash equivalents (a) | - | |

| 267 | |

| - | |

| 267 | |

| - | |

| 206 | |

| - | |

| 206 | | ||||||||

Marketable securities |

| |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

| |||||||||||||

U.S. government and agencies | 846 | |

| 3,706 | |

| - | |

| 4,552 | |

| 969 | |

| 5,789 | |

| - | |

| 6,758 | | ||||||||

Non-U.S. government and agencies | - | |

| 6,068 | |

| - | |

| 6,068 | |

| - | |

| 7,004 | |

| - | |

| 7,004 | | ||||||||

Corporate debt | - | |

| 3,617 | |

| - | |

| 3,617 | |

| - | |

| 2,738 | |

| - | |

| 2,738 | | ||||||||

Equities | 15 | |

| - | |

| - | |

| 15 | |

| 322 | |

| - | |

| - | |

| 322 | | ||||||||

Other marketable securities | - | |

| 347 | |

| - | |

| 347 | |

| - | |

| 313 | |

| - | |

| 313 | | ||||||||

Total marketable securities | 861 | |

| 13,738 | |

| - | |

| 14,599 | |

| 1,291 | |

| 15,844 | |

| - | |

| 17,135 | | ||||||||

Derivative financial instruments (b) | - | |

| 521 | |

| - | |

| 521 | |

| - | |

| 517 | |

| - | |

| 517 | | ||||||||

Total assets at fair value | $ | 861 | |

| $ | 14,526 | |

| $ | - | |

| $ | 15,387 | |

| $ | 1,291 | |

| $ | 16,567 | |

| $ | - | |

| $ | 17,858 | |

Liabilities |

| |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

| |||||||||||||

Derivative financial instruments (b) | $ | - | |

| $ | 991 | |

| $ | 1 | |

| $ | 992 | |

| $ | - | |

| $ | 710 | |

| $ | 3 | |

| $ | 713 | |

Total liabilities at fair value | $ | - | |

| $ | 991 | |

| $ | 1 | |

| $ | 992 | |

| $ | - | |

| $ | 710 | |

| $ | 3 | |

| $ | 713 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Financial Services Sector |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Cash equivalents – financial instruments |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Non-U.S. government and agencies | $ | - | |

| $ | 419 | |

| $ | - | |

| $ | 419 | |

| $ | - | |

| $ | 341 | |

| $ | - | |

| $ | 341 | |

Corporate debt | - | |

| 50 | |

| - | |

| 50 | |

| - | |

| 10 | |

| - | |

| 10 | | ||||||||

Total cash equivalents (a) | - | |

| 469 | |

| - | |

| 469 | |

| - | |

| 351 | |

| - | |

| 351 | | ||||||||

Marketable securities |

| |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

| |||||||||||||

U.S. government and agencies | 669 | |

| 700 | |

| - | |

| 1,369 | |

| 17 | |

| 1,251 | |

| - | |

| 1,268 | | ||||||||

Non-U.S. government and agencies | - | |

| 630 | |

| - | |

| 630 | |

| - | |

| 405 | |

| - | |

| 405 | | ||||||||

Corporate debt | - | |

| 1,780 | |

| - | |

| 1,780 | |

| - | |

| 1,555 | |

| - | |

| 1,555 | | ||||||||

Other marketable securities | - | |

| 27 | |

| - | |

| 27 | |

| - | |

| 30 | |

| - | |

| 30 | | ||||||||

Total marketable securities | 669 | |

| 3,137 | |

| - | |

| 3,806 | |

| 17 | |

| 3,241 | |

| - | |

| 3,258 | | ||||||||

Derivative financial instruments (b) | - | |

| 823 | |

| - | |

| 823 | |

| - | |

| 859 | |

| - | |

| 859 | | ||||||||

Total assets at fair value | $ | 669 | |

| $ | 4,429 | |

| $ | - | |

| $ | 5,098 | |

| $ | 17 | |

| $ | 4,451 | |

| $ | - | |

| $ | 4,468 | |

Liabilities |

| |

|

| |

|

| |

|

|

|

|

|

|

|

|

|

| |||||||||||||

Derivative financial instruments (b) | $ | - | |

| $ | 378 | |

| $ | - | |

| $ | 378 | |

| $ | - | |

| $ | 167 | |

| $ | - | |

| $ | 167 | |

Total liabilities at fair value | $ | - | |

| $ | 378 | |

| $ | - | |

| $ | 378 | |

| $ | - | |

| $ | 167 | |

| $ | - | |

| $ | 167 | |

__________

(a) | Excludes time deposits, certificates of deposit, money market accounts, and other cash equivalents reported at par value on our balance sheet totaling $4.6 billion and $3.3 billion for Automotive sector and $3.9 billion and $3.8 billion for Financial Services sector at June 30, 2015 and December 31, 2014 , respectively. In addition to these cash equivalents, we also had cash on hand totaling $1.2 billion and $1.1 billion for Automotive sector and $2.4 billion and $2 billion for Financial Services sector at June 30, 2015 and December 31, 2014 , respectively. |

(b) | See Note 12 for additional information regarding derivative financial instruments. |

11

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 4. FINANCIAL SERVICES SECTOR FINANCE RECEIVABLES

Our Financial Services sector, primarily Ford Credit, segments finance receivables into "consumer" and "non-consumer" portfolios. The receivables are generally secured by the vehicles, inventory, or other property being financed.

Finance receivables, net were as follows (in millions):

| June 30, |

| December 31, | ||||

Consumer |

|

|

| ||||

Retail financing, gross | $ | 57,646 | |

| $ | 55,856 | |

Unearned interest supplements | (1,739 | ) |

| (1,760 | ) | ||

Consumer finance receivables | 55,907 | |

| 54,096 | | ||

Non-Consumer |

| |

|

| | ||

Dealer financing | 32,093 | |

| 31,340 | | ||

Other financing | 1,131 | |

| 1,026 | | ||

Non-Consumer finance receivables | 33,224 | |

| 32,366 | | ||

Total recorded investment | $ | 89,131 | |

| $ | 86,462 | |

|

|

|

| ||||

Recorded investment in finance receivables | $ | 89,131 | |

| $ | 86,462 | |

Allowance for credit losses | (335 | ) |

| (321 | ) | ||

Finance receivables, net (a) | $ | 88,796 | |

| $ | 86,141 | |

|

|

|

| ||||

Net finance receivables subject to fair value (b) | $ | 87,026 | |

| $ | 84,468 | |

Fair value | 88,315 | |

| 85,941 | | ||

__________

(a) | On the consolidated balance sheet at June 30, 2015 and December 31, 2014 , $6 billion and $5 billion , respectively, are reclassified to Other receivables, net, resulting in Finance receivables, net of $82.8 billion and $81.1 billion , respectively. |

(b) | At June 30, 2015 and December 31, 2014 , excludes $1.8 billion and $1.7 billion , respectively, of certain receivables (primarily direct financing leases) that are not subject to fair value disclosure requirements. |

Excluded from finance receivables at June 30, 2015 and December 31, 2014 , was $185 million and $191 million , respectively, of accrued uncollected interest, which we report in Other assets on the balance sheet.

Included in the recorded investment in finance receivables at June 30, 2015 and December 31, 2014 were consumer receivables of $26.9 billion and $24.4 billion and non-consumer receivables of $23.1 billion and $21.8 billion , respectively, that have been sold for legal purposes in securitization transactions but continue to be reported in our consolidated financial statements. The receivables are available only for payment of the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions; they are not available to pay the other obligations or the claims of Ford Credit's other creditors. Ford Credit holds the right to receive the excess cash flows not needed to pay the debt issued by, and other obligations of, the securitization entities that are parties to those securitization transactions (see Note 11 for additional information).

12

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 4. FINANCIAL SERVICES SECTOR FINANCE RECEIVABLES (Continued)

Aging

For all finance receivables, we define "past due" as any payment, including principal and interest, that is at least 31 days past the contractual due date . The recorded investment of consumer receivables greater than 90 days past due and still accruing interest was $13 million and $17 million at June 30, 2015 and December 31, 2014 , respectively. The recorded investment of non-consumer receivables greater than 90 days past due and still accruing interest was $1 million and $3 million at June 30, 2015 and December 31, 2014 , respectively.

The aging analysis of our finance receivables balances were as follows (in millions):

| June 30, |

| December 31, | ||||

Consumer |

|

|

| ||||

31-60 days past due | $ | 566 | |

| $ | 718 | |

61-90 days past due | 85 | |

| 97 | | ||

91-120 days past due | 23 | |

| 29 | | ||

Greater than 120 days past due | 39 | |

| 52 | | ||

Total past due | 713 | |

| 896 | | ||

Current | 55,194 | |

| 53,200 | | ||

Consumer finance receivables | 55,907 | |

| 54,096 | | ||

|

|

|

| ||||

Non-Consumer |

|

|

| ||||

Total past due | 110 | |

| 117 | | ||

Current | 33,114 | |

| 32,249 | | ||

Non-Consumer finance receivables | 33,224 | |

| 32,366 | | ||

Total recorded investment | $ | 89,131 | |

| $ | 86,462 | |

Credit Quality

Consumer Portfolio. Credit quality ratings for consumer receivables are based on aging. Refer to the aging table above.

Consumer receivables credit quality ratings are as follows:

• | Pass – current to 60 days past due |

• | Special Mention – 61 to 120 days past due and in intensified collection status |

• | Substandard – greater than 120 days past due and for which the uncollectible portion of the receivables has already been charged off, as measured using the fair value of collateral |

Non-Consumer Portfolio. Dealers are assigned to one of four groups according to risk ratings as follows:

• | Group I – strong to superior financial metrics |

• | Group II – fair to favorable financial metrics |

• | Group III – marginal to weak financial metrics |

• | Group IV – poor financial metrics, including dealers classified as uncollectible |

13

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 4. FINANCIAL SERVICES SECTOR FINANCE RECEIVABLES (Continued)

The credit quality analysis of our dealer financing receivables was as follows (in millions):

| June 30, |

| December 31, | ||||

Dealer Financing |

|

|

| ||||

Group I | $ | 24,088 | |

| $ | 23,125 | |

Group II | 6,500 | |

| 6,350 | | ||

Group III | 1,402 | |

| 1,783 | | ||

Group IV | 103 | |

| 82 | | ||

Total recorded investment | $ | 32,093 | |

| $ | 31,340 | |

Impaired Receivables

Impaired consumer receivables include accounts that have been rewritten or modified in reorganization proceedings pursuant to the U.S. Bankruptcy Code that are considered to be troubled debt restructurings ("TDRs"), as well as all accounts greater than 120 days past due . Impaired non-consumer receivables represent accounts with dealers that have weak or poor financial metrics or dealer financing that has been modified in TDRs. The recorded investment of consumer receivables that were impaired at June 30, 2015 and December 31, 2014 was $380 million , or 0.7% of consumer receivables, and $415 million , or 0.8% of consumer receivables, respectively. The recorded investment of non-consumer receivables that were impaired at June 30, 2015 and December 31, 2014 was $126 million , or 0.4% of non-consumer receivables, and $105 million , or 0.3% of non-consumer receivables, respectively. Impaired finance receivables are evaluated both collectively and specifically.

14

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 5. FINANCIAL SERVICES SECTOR ALLOWANCE FOR CREDIT LOSSES

An analysis of the allowance for credit losses related to finance receivables for the periods ended June 30 was as follows (in millions):

| Second Quarter 2015 |

| First Half 2015 | ||||||||||||||||||||

| Consumer |

| Non-Consumer |

| Total |

| Consumer |

| Non-Consumer |

| Total | ||||||||||||

Allowance for credit losses |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Beginning balance | $ | 301 | |

| $ | 13 | |

| $ | 314 | |

| $ | 305 | |

| $ | 16 | |

| $ | 321 | |

Charge-offs | (70 | ) |

| (2 | ) |

| (72 | ) |

| (150 | ) |

| (1 | ) |

| (151 | ) | ||||||

Recoveries | 31 | |

| 1 | |

| 32 | |

| 61 | |

| 3 | |

| 64 | | ||||||

Provision for credit losses | 57 | |

| - | |

| 57 | |

| 110 | |

| (4 | ) |

| 106 | | ||||||

Other (a) | 3 | |

| 1 | |

| 4 | |

| (4 | ) |

| (1 | ) |

| (5 | ) | ||||||

Ending balance (b) | $ | 322 | |

| $ | 13 | |

| $ | 335 | |

| $ | 322 | |

| $ | 13 | |

| $ | 335 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of allowance for credit losses | |||||||||||||||||||||||

Collective impairment allowance |

|

|

|

|

|

| $ | 303 | |

| $ | 13 | |

| $ | 316 | | ||||||

Specific impairment allowance |

|

|

|

|

|

| 19 | |

| - | |

| 19 | | |||||||||

Ending balance (b) |

|

|

|

|

|

| 322 | |

| 13 | |

| 335 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of finance receivables |

|

|

|

|

|

| |||||||||||||||||

Collectively evaluated for impairment |

|

|

|

|

|

| 55,527 | |

| 33,098 | |

| 88,625 | | |||||||||

Specifically evaluated for impairment |

|

|

|

|

|

| 380 | |

| 126 | |

| 506 | | |||||||||

Recorded investment |

|

|

|

|

|

| 55,907 | |

| 33,224 | |

| 89,131 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Ending balance, net of allowance for credit losses |

|

|

| $ | 55,585 | |

| $ | 33,211 | |

| $ | 88,796 | | |||||||||

__________

(a) | Primarily represents amounts related to translation adjustments. |

(b) | Total allowance, including reserves for operating leases, was $380 million . |

| Second Quarter 2014 |

| First Half 2014 | ||||||||||||||||||||

| Consumer |

| Non-Consumer |

| Total |

| Consumer |

| Non-Consumer |

| Total | ||||||||||||

Allowance for credit losses |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Beginning balance | $ | 307 | |

| $ | 27 | |

| $ | 334 | |

| $ | 327 | |

| $ | 30 | |

| $ | 357 | |

Charge-offs | (58 | ) |

| (3 | ) |

| (61 | ) |

| (133 | ) |

| (5 | ) |

| (138 | ) | ||||||

Recoveries | 34 | |

| 1 | |

| 35 | |

| 68 | |

| 6 | |

| 74 | | ||||||

Provision for credit losses | 17 | |

| - | |

| 17 | |

| 40 | |

| (7 | ) |

| 33 | | ||||||

Other (a) | 3 | |

| (1 | ) |

| 2 | |

| 1 | |

| - | |

| 1 | | ||||||

Ending balance (b) | $ | 303 | |

| $ | 24 | |

| $ | 327 | |

| $ | 303 | |

| $ | 24 | |

| $ | 327 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of allowance for credit losses | |||||||||||||||||||||||

Collective impairment allowance |

|

|

|

|

|

| $ | 281 | |

| $ | 23 | |

| $ | 304 | | ||||||

Specific impairment allowance |

|

|

|

|

|

| 22 | |

| 1 | |

| 23 | | |||||||||

Ending balance (b) |

|

|

|

|

|

| 303 | |

| 24 | |

| 327 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Analysis of ending balance of finance receivables |

|

|

|

|

|

| |||||||||||||||||

Collectively evaluated for impairment |

|

|

|

|

|

| 51,505 | |

| 34,293 | |

| 85,798 | | |||||||||

Specifically evaluated for impairment |

|

|

|

|

|

| 419 | |

| 125 | |

| 544 | | |||||||||

Recorded investment |

|

|

|

|

|

| 51,924 | |

| 34,418 | |

| 86,342 | | |||||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Ending balance, net of allowance for credit losses |

| $ | 51,621 | |

| $ | 34,394 | |

| $ | 86,015 | | |||||||||||

__________

(a) | Primarily represents amounts related to translation adjustments. |

(b) | Total allowance, including reserves for operating leases, was $353 million . |

15

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 6. INVENTORIES

All inventories are stated at the lower of cost or market. Cost for a substantial portion of U.S. inventories is determined on a last-in, first-out ("LIFO") basis. LIFO was used for 33% and 28% of total inventories at June 30, 2015 and December 31, 2014 , respectively. Cost of other inventories is determined by costing methods that approximate a first-in, first-out ("FIFO") basis.

Inventories were as follows (in millions):

| June 30, |

| December 31, | ||||

Raw materials, work-in-process, and supplies | $ | 4,282 | |

| $ | 3,822 | |

Finished products | 6,151 | |

| 5,022 | | ||

Total inventories under FIFO | 10,433 | |

| 8,844 | | ||

LIFO adjustment | (995 | ) |

| (978 | ) | ||

Total inventories | $ | 9,438 | |

| $ | 7,866 | |

NOTE 7. OTHER LIABILITIES AND DEFERRED REVENUE

| June 30, |

| December 31, | ||||

Automotive Sector |

|

|

| ||||

Current |

|

|

| ||||

Dealer and dealers' customer allowances and claims | $ | 7,830 | |

| $ | 7,846 | |

Deferred revenue | 5,393 | |

| 3,923 | | ||

Employee benefit plans | 1,353 | |

| 1,994 | | ||

Accrued interest | 239 | |

| 222 | | ||

Other postretirement employee benefits ("OPEB") | 381 | |

| 397 | | ||

Pension (a) | 353 | |

| 374 | | ||

Other | 2,833 | |

| 3,178 | | ||

Total Automotive other liabilities and deferred revenue | 18,382 | |

| 17,934 | | ||

Non-current |

| |

|

| | ||

Pension (a) | 9,266 | |

| 9,721 | | ||

OPEB | 5,843 | |

| 5,991 | | ||

Dealer and dealers' customer allowances and claims | 2,843 | |

| 2,852 | | ||

Deferred revenue | 2,825 | |

| 2,686 | | ||

Employee benefit plans | 1,134 | |

| 1,149 | | ||

Other | 1,435 | |

| 1,394 | | ||

Total Automotive other liabilities and deferred revenue | 23,346 | |

| 23,793 | | ||

Total Automotive sector | 41,728 | |

| 41,727 | | ||

Financial Services Sector | 1,921 | |

| 1,850 | | ||

Total Company | $ | 43,649 | |

| $ | 43,577 | |

__________

(a) | Balances at June 30, 2015 reflect net pension liabilities at December 31, 2014 , updated for service and interest cost, expected return on assets, separation expense, actual benefit payments, cash contributions, and an adjustment recorded in the first quarter of 2015 (see Note 8 for additional information). The discount rate and rate of expected return assumptions are unchanged from year-end 2014 . |

16

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 8. RETIREMENT BENEFITS

In the first quarter of 2015, we recorded a $782 million adjustment to correct for an understatement in the year-end 2014 valuation of our U.S. pension benefit obligation. The adjustment reduced Other assets by $301 million and increased Other liabilities and deferred revenue by $481 million . The resulting after-tax adjustment to Other comprehensive income was a loss of $508 million . The adjustments were not material to current or prior period financial statements.

Defined Benefit Plans - Expense

| Second Quarter | ||||||||||||||||||||||

| Pension Benefits |

|

|

|

| ||||||||||||||||||

| U.S. Plans |

| Non-U.S. Plans |

| Worldwide OPEB | ||||||||||||||||||

| 2015 |

| 2014 |

| 2015 |

| 2014 |

| 2015 |

| 2014 | ||||||||||||

Service cost | $ | 146 | |

| $ | 126 | |

| $ | 133 | |

| $ | 120 | |

| $ | 15 | |

| $ | 14 | |

Interest cost | 455 | |

| 498 | |

| 232 | |

| 302 | |

| 59 | |

| 67 | | ||||||

Expected return on assets | (688 | ) |

| (678 | ) |

| (343 | ) |

| (383 | ) |

| - | |

| - | | ||||||

Amortization of: |

| |

|

| |

|

| |

|

| |

|

| |

|

| | ||||||

Prior service costs/(credits) | 39 | |

| 39 | |

| 11 | |

| 13 | |

| (52 | ) |

| (57 | ) | ||||||

(Gains)/Losses | 116 | |

| 52 | |

| 199 | |

| 148 | |

| 35 | |

| 25 | | ||||||

Separation programs/other | (1 | ) |

| 1 | |

| 12 | |

| 23 | |

| 3 | |

| (1 | ) | ||||||

Recognition of (gains)/losses due to: |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Curtailments | - | |

| - | |

| - | |

| - | |

| - | |

| - | | ||||||

Settlements | - | |

| - | |

| - | |

| - | |

| - | |

| - | | ||||||

Total expense/(income) | $ | 67 | |

| $ | 38 | |

| $ | 244 | |

| $ | 223 | |

| $ | 60 | |

| $ | 48 | |

| First Half | ||||||||||||||||||||||

| Pension Benefits |

|

|

|

| ||||||||||||||||||

| U.S. Plans |

| Non-U.S. Plans |

| Worldwide OPEB | ||||||||||||||||||

| 2015 |

| 2014 |

| 2015 |

| 2014 |

| 2015 |

| 2014 | ||||||||||||

Service cost | $ | 293 | |

| $ | 253 | |

| $ | 268 | |

| $ | 238 | |

| $ | 30 | |

| $ | 27 | |

Interest cost | 909 | |

| 996 | |

| 471 | |

| 602 | |

| 119 | |

| 134 | | ||||||

Expected return on assets | (1,377 | ) |

| (1,356 | ) |

| (692 | ) |

| (762 | ) |

| - | |

| - | | ||||||

Amortization of: |

|

|

| |

|

|

|

|

|

|

| | | ||||||||||

Prior service costs/(credits) | 78 | |

| 78 | |

| 23 | |

| 27 | |

| (103 | ) |

| (114 | ) | ||||||

(Gains)/Losses | 232 | |

| 103 | |

| 404 | |

| 296 | |

| 71 | |

| 49 | | ||||||

Separation programs/other | 1 | |

| 1 | |

| 19 | |

| 39 | |

| 2 | |

| - | | ||||||

Recognition of (gains)/losses due to: |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Curtailments | - | |

| - | |

| - | |

| - | |

| - | |

| - | | ||||||

Settlements | - | |

| - | |

| - | |

| 14 | |

| - | |

| - | | ||||||

Total expense/(income) | $ | 136 | |

| $ | 75 | |

| $ | 493 | |

| $ | 454 | |

| $ | 119 | |

| $ | 96 | |

Pension Plan Contributions

In 2015 , we expect to contribute $1.1 billion from Automotive cash and cash equivalents to our worldwide funded pension plans (most of which are mandatory contributions), and to make about $400 million of benefit payments to participants in unfunded plans, for a total of $1.5 billion . In the first half of 2015 , we contributed about $900 million to our worldwide funded pension plans and made about $200 million of benefit payments to participants in unfunded plans.

17

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

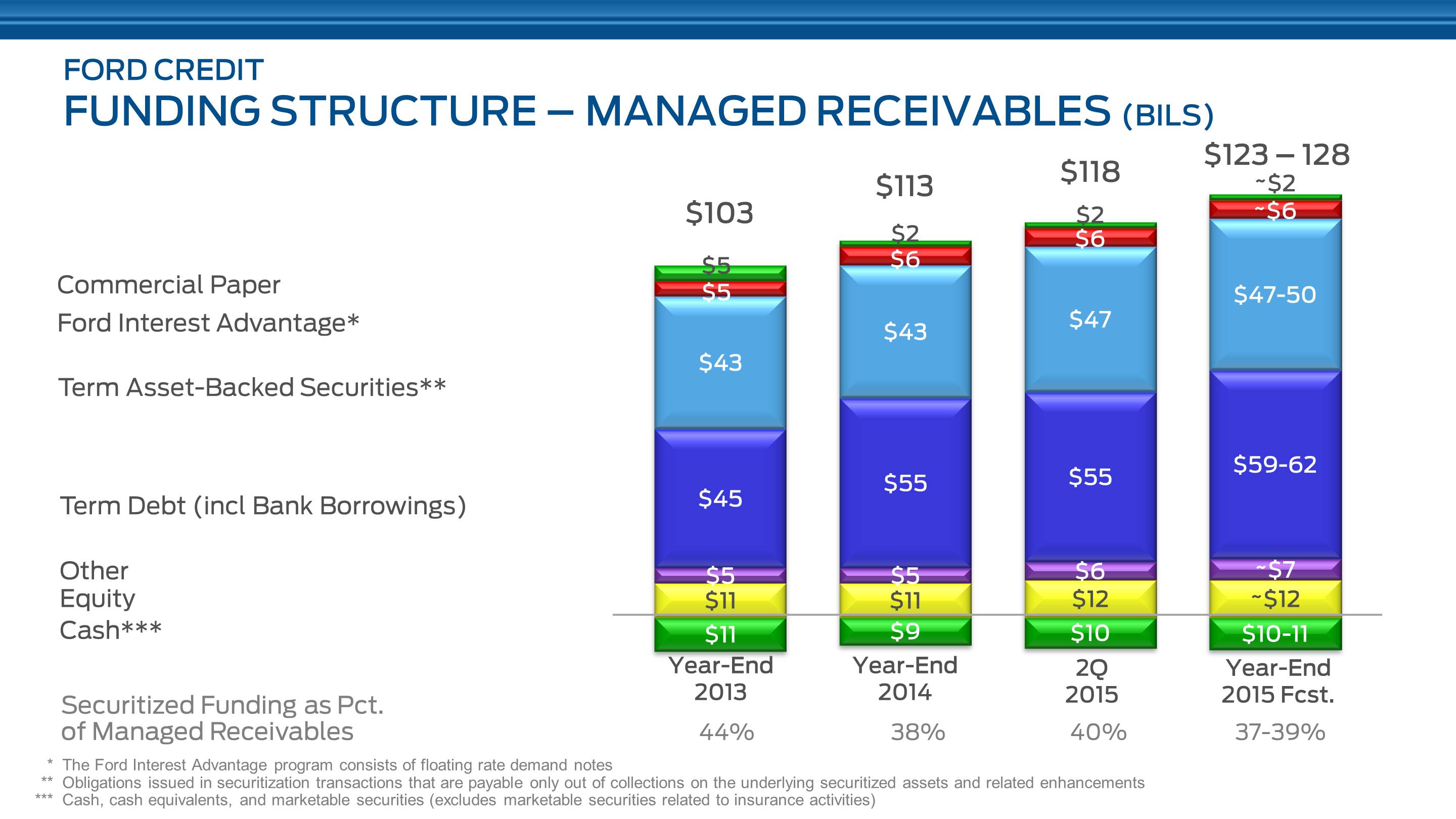

NOTE 9. DEBT

The carrying value of debt was $123.5 billion and $119.2 billion at June 30, 2015 and December 31, 2014 , respectively. The carrying value of Automotive sector and Financial Services sector debt was as follows (in millions):

Automotive Sector | June 30, |

| December 31, | ||||

Debt payable within one year |

|

|

| ||||

Short-term | $ | 458 | |

| $ | 373 | |

Long-term payable within one year |

| |

|

| | ||

U.S. Department of Energy ("DOE") Advanced Technology Vehicles Manufacturing ("ATVM") Incentive Program | 591 | |

| 591 | | ||

European Investment Bank ("EIB") loans | 709 | |

| 1,187 | | ||

Other debt | 430 | |

| 350 | | ||

Total debt payable within one year | 2,188 | |

| 2,501 | | ||

Long-term debt payable after one year |

| |

|

| | ||

Public unsecured debt securities | 6,594 | |

| 6,634 | | ||

DOE ATVM Incentive Program | 3,538 | |

| 3,833 | | ||

Other debt | 1,914 | |

| 1,000 | | ||

Unamortized (discount)/premium | (521 | ) |

| (144 | ) | ||

Total long-term debt payable after one year | 11,525 | |

| 11,323 | | ||

Total Automotive sector | $ | 13,713 | |

| $ | 13,824 | |

|

|

|

| ||||

Fair value of Automotive sector debt (a) | $ | 15,163 | |

| $ | 15,553 | |

|

|

|

| ||||

Financial Services Sector |

| |

|

| | ||

Short-term debt |

| |

|

| | ||

Unsecured debt | $ | 9,679 | |

| $ | 9,761 | |

Asset-backed debt | 1,583 | |

| 1,377 | | ||

Total short-term debt | 11,262 | |

| 11,138 | | ||

Long-term debt |

| |

|

| | ||

Unsecured debt |

| |

|

| | ||

Notes payable within one year | 8,535 | |

| 8,795 | | ||

Notes payable after one year | 44,734 | |

| 43,087 | | ||

Asset-backed debt |

| |

|

| | ||

Notes payable within one year | 17,354 | |

| 16,738 | | ||

Notes payable after one year | 27,591 | |

| 25,216 | | ||

Unamortized (discount)/premium | (44 | ) |

| (55 | ) | ||

Fair value adjustments (b) | 381 | |

| 428 | | ||

Total long-term debt | 98,551 | |

| 94,209 | | ||

Total Financial Services sector | $ | 109,813 | |

| $ | 105,347 | |

|

|

|

| ||||

Fair value of Financial Services sector debt (a) | $ | 111,662 | |

| $ | 107,758 | |

__________

(a) | The fair value of debt includes $272 million and $131 million of Automotive sector short-term debt and $9.7 billion and $9.8 billion of Financial Services sector short-term debt at June 30, 2015 and December 31, 2014 , respectively, carried at cost, which approximates fair value. All debt is categorized within Level 2 of the fair value hierarchy. |

(b) | Adjustments related to designated fair value hedges of unsecured debt. |

18

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 10. REDEEMABLE NONCONTROLLING INTEREST

The redeemable noncontrolling interest in our Ford Sollers joint venture is discussed in Note 17 .

AutoAlliance International, Inc. ("AAI") was a 50 / 50 joint venture between Ford and Mazda Motor Corporation ("Mazda") that owned an automobile assembly plant in Flat Rock, Michigan. In January 2015, Mazda exercised its put option and Ford purchased Mazda's 50% equity interest at the exercise price plus accrued interest of $342 million (included in Cash flows from financing activities in our statement of cash flows) and dissolved AAI.

NOTE 11. VARIABLE INTEREST ENTITIES

VIEs of Which We are Not the Primary Beneficiary

Certain of our joint ventures are VIEs, in which the power to direct economically significant activities is shared with the joint venture partner. Our investments in these joint ventures are accounted for as equity method investments. Our maximum exposure to any potential losses associated with these joint ventures is limited to our investment, including loans, and was $280 million and $307 million at June 30, 2015 and December 31, 2014 , respectively.

VIEs of Which We are the Primary Beneficiary

Securitization Entities Through Ford Credit, we securitize, transfer, and service financial assets associated with consumer finance receivables, operating leases, and wholesale loans. Our securitization transactions typically involve the legal transfer of financial assets to bankruptcy remote special purpose entities ("SPEs"). The third-party investors in these securitization entities have legal recourse only to the assets securing the debt and do not have recourse to us, except for the customary representation and warranty provisions. In addition, the cash flows generated by the assets are restricted only to pay such liabilities. We generally retain economic interests in the asset-backed securitization transactions, which are retained in the form of senior or subordinated interests, cash reserve accounts, residual interests, and servicing rights. For accounting purposes, we are precluded from recording the transfers of assets in securitization transactions as sales.

In most cases, the bankruptcy remote SPEs meet the definition of VIEs for which we have determined we have both the power to direct the activities of the entity that most significantly impact the entity's economic performance and the obligation to absorb losses or the right to receive benefits of the entity that could be significant, and would therefore also be consolidated. We account for all securitization transactions as if they were secured financing and therefore the assets, liabilities and related activity of these transactions are consolidated in our financial results and are included in amounts presented on the face of our consolidated balance sheet (see Note 4 for additional information).

19

Item 1. Financial Statements (Continued)

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 12. DERIVATIVE FINANCIAL INSTRUMENTS AND HEDGING ACTIVITIES

In the normal course of business, our operations are exposed to global market risks, including the effect of changes in foreign currency exchange rates, certain commodity prices, and interest rates. To manage these risks, we enter into highly effective derivatives contracts. We have elected to apply hedge accounting to certain derivatives. Derivatives that are designated in hedging relationships are evaluated for effectiveness using regression analysis at the time they are designated and throughout the hedge period. Some derivatives do not qualify for hedge accounting; for others, we elect not to apply hedge accounting.

Income Effect of Derivative Financial Instruments

The gains/(losses), by hedge designation, recorded in income for the periods ended June 30 were as follows (in millions):

| Second Quarter |

| First Half | ||||||||||||

| 2015 |

| 2014 |

| 2015 |

| 2014 | ||||||||

Automotive Sector |

|

|

|

|

|

|

| ||||||||

Cash flow hedges (a) |

|

|

|

|

|

|

| ||||||||

Reclassified from AOCI to income | $ | (90 | ) |

| $ | 92 | |

| $ | (136 | ) |

| $ | 160 | |

Ineffectiveness | - | |

| - | |

| - | |

| - | | ||||

Derivatives not designated as hedging instruments |

|

|

|

|

|

|

| ||||||||

Foreign currency exchange contracts | (116 | ) |

| (17 | ) |

| 145 | |

| (61 | ) | ||||

Commodity contracts | (15 | ) |

| 47 | |

| (25 | ) |

| 35 | | ||||

Total | $ | (221 | ) |

| $ | 122 | |

| $ | (16 | ) |

| $ | 134 | |

|

|

|

|

|

|

|

| ||||||||

Financial Services Sector |

|

|

|

|

|

|

| ||||||||

Fair value hedges |

|

|

|

|

|

|

| ||||||||

Interest rate contracts |

|

|

|

|

|

|

| ||||||||

Net interest settlements and accruals excluded from the assessment of hedge effectiveness | $ | 89 | |

| $ | 72 | |

| $ | 177 | |

| $ | 141 | |

Ineffectiveness (b) | (10 | ) |

| 5 | |

| (4 | ) |

| 10 | | ||||

Derivatives not designated as hedging instruments |

|

|

|

|

|

|

| ||||||||

Interest rate contracts | (18 | ) |

| (9 | ) |

| (61 | ) |

| (27 | ) | ||||

Foreign currency exchange contracts | (65 | ) |

| (25 | ) |

| - | |

| (30 | ) | ||||

Cross-currency interest rate swap contracts | (77 | ) |

| (11 | ) |

| 12 | |

| (16 | ) | ||||

Total | $ | (81 | ) |

| $ | 32 | |

| $ | 124 | |

| $ | 78 | |

__________