UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________

FORM 10-Q

_________________________

(Mark One)

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended June 30, 2016

or

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to __________

Commission File No. 1-10410

_________________________

CAESARS ENTERTAINMENT CORPORATION

(Exact name of registrant as specified in its charter)

_________________________

Delaware |

| 62-1411755 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

One Caesars Palace Drive, Las Vegas, Nevada |

| 89109 |

(Address of principal executive offices) |

| (Zip Code) |

(702) 407-6000

(Registrant's telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

_________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | o | Accelerated filer | x |

|

|

|

|

Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

Class | Outstanding at August 1, 2016 |

Common stock, $0.01 par value | 146,922,790 |

CAESARS ENTERTAINMENT CORPORATION

|

|

|

PART I. FINANCIAL INFORMATION | Page | |

Item 1. | Unaudited Financial Statements |

|

| Consolidated Condensed Balance Sheets | 3 |

| Consolidated Condensed Statements of Operations | 4 |

| Consolidated Condensed Statements of Stockholders' Equity/(Deficit) | 5 |

| Consolidated Condensed Statements of Cash Flows | 6 |

| Notes to Consolidated Condensed Financial Statements | 7 |

Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 40 |

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 57 |

Item 4. | Controls and Procedures | 57 |

|

|

|

PART II. OTHER INFORMATION |

| |

Item 1. | Legal Proceedings | 58 |

Item 1A. | Risk Factors | 59 |

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 59 |

Item 3. | Defaults Upon Senior Securities | 59 |

Item 4. | Mine Safety Disclosures | 59 |

Item 5. | Other Information | 59 |

Item 6. | Exhibits | 60 |

SIGNATURE S | 63 | |

2

PART I-FINANCIAL INFORMATION

Item 1. Unaudited Financial Statements

CAESARS ENTERTAINMENT CORPORATION

CONSOLIDATED CONDENSED BALANCE SHEETS

(UNAUDITED)

(In millions) | June 30, 2016 | | December 31, 2015 | ||||

Assets |

| |

| ||||

Current assets |

| |

| ||||

Cash and cash equivalents ($1,133 and $1,060 attributable to our VIEs) | $ | 1,525 | | | $ | 1,338 | |

Restricted cash ($4 and $4 attributable to our VIEs) | 56 | |

| 59 | | ||

Receivables, net ($129 and $123 attributable to our VIEs) | 200 | | | 193 | | ||

Due from affiliates ($25 and $32 attributable to our VIEs) | 25 | |

| 32 | | ||

Prepayments and other current assets ($58 and $51 attributable to our VIEs) | 126 | | | 128 | | ||

Inventories ($5 and $7 attributable to our VIEs) | 16 | | | 21 | | ||

Total current assets | 1,948 | | | 1,771 | | ||

Property and equipment, net ($2,576 and $2,620 attributable to our VIEs) | 7,511 | | | 7,598 | | ||

Goodwill ($294 and $294 attributable to our VIEs) | 1,696 | | | 1,696 | | ||

Intangible assets other than goodwill ($233 and $251 attributable to our VIEs) | 500 | | | 543 | | ||

Restricted cash ($5 and $9 attributable to our VIEs) | 5 | | | 109 | | ||

Deferred income taxes ($20 and $28 attributable to our VIEs) | 20 | |

| 28 | | ||

Deferred charges and other assets ($250 and $260 attributable to our VIEs) | 437 | | | 450 | | ||

Total assets | $ | 12,117 | | | $ | 12,195 | |

|

|

|

| ||||

Liabilities and Stockholders' Equity/(Deficit) |

| |

| ||||

Current liabilities |

| |

| ||||

Accounts payable ($116 and $141 attributable to our VIEs) | $ | 165 | | | $ | 179 | |

Due to affiliates ($15 and $15 attributable to our VIEs) | 17 | |

| 16 | | ||

Accrued expenses and other current liabilities ($245 and $272 attributable to our VIEs) | 631 | | | 588 | | ||

Accrued restructuring and support expenses | 3,170 | |

| 905 | | ||

Interest payable ($36 and $37 attributable to our VIEs) | 127 | | | 131 | | ||

Current portion of long-term debt ($23 and $70 attributable to our VIEs) | 71 | |

| 187 | | ||

Total current liabilities | 4,181 | | | 2,006 | | ||

Long-term debt ($2,262 and $2,267 attributable to our VIEs) | 6,763 | | | 6,777 | | ||

Deferred income taxes ($2 and $4 attributable to our VIEs) | 1,004 | | | 991 | | ||

Deferred credits and other liabilities ($218 and $138 attributable to our VIEs) | 265 | | | 188 | | ||

Total liabilities | 12,213 | | | 9,962 | | ||

Commitments and contingencies (Note 8) | | |

| | | ||

Stockholders' equity/(deficit) |

| |

| ||||

Caesars stockholders' equity/(deficit) | (1,394 | ) | | 987 | | ||

Noncontrolling interests | 1,298 | | | 1,246 | | ||

Total stockholders' equity/(deficit) | (96 | ) | | 2,233 | | ||

Total liabilities and stockholders' equity/(deficit) | $ | 12,117 | | | $ | 12,195 | |

See accompanying Notes to Consolidated Condensed Financial Statements.

3

CAESARS ENTERTAINMENT CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF OPERATIONS

(UNAUDITED)

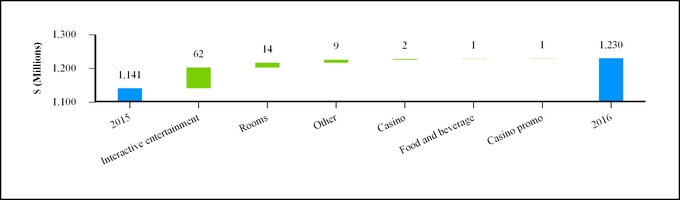

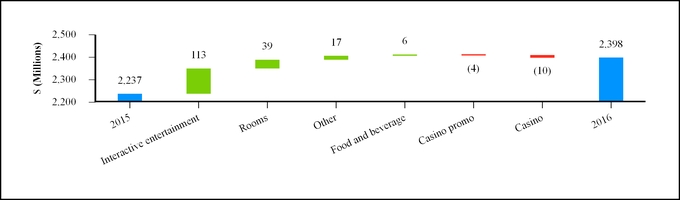

| Three Months Ended June 30, |

| Six Months Ended June 30, | ||||||||||||

(In millions, except per share data) | 2016 |

| 2015 |

| 2016 |

| 2015 | ||||||||

Revenues |

|

|

|

|

|

|

| ||||||||

Casino | $ | 545 | |

| $ | 543 | |

| $ | 1,075 | |

| $ | 1,203 | |

Food and beverage | 204 | |

| 203 | |

| 410 | |

| 429 | | ||||

Rooms | 235 | |

| 221 | |

| 464 | |

| 443 | | ||||

Interactive entertainment | 248 | |

| 186 | |

| 476 | |

| 363 | | ||||

Other revenue | 130 | |

| 121 | |

| 245 | |

| 246 | | ||||

Less: casino promotional allowances | (132 | ) |

| (133 | ) |

| (272 | ) |

| (289 | ) | ||||

Net revenues | 1,230 | |

| 1,141 | |

| 2,398 | |

| 2,395 | | ||||

Operating expenses |

|

|

|

|

|

|

| ||||||||

Direct |

|

|

|

|

|

|

| ||||||||

Casino | 279 | |

| 278 | |

| 564 | |

| 634 | | ||||

Food and beverage | 100 | |

| 99 | |

| 193 | |

| 202 | | ||||

Rooms | 63 | |

| 57 | |

| 122 | |

| 113 | | ||||

Platform fees | 68 | |

| 51 | |

| 132 | |

| 100 | | ||||

Property, general, administrative, and other | 385 | |

| 305 | |

| 716 | |

| 655 | | ||||

Depreciation and amortization | 109 | |

| 96 | |

| 228 | |

| 198 | | ||||

Corporate expense | 41 | |

| 45 | |

| 82 | |

| 91 | | ||||

Other operating costs | 21 | |

| 24 | |

| 43 | |

| 72 | | ||||

Total operating expenses | 1,066 | |

| 955 | |

| 2,080 | |

| 2,065 | | ||||

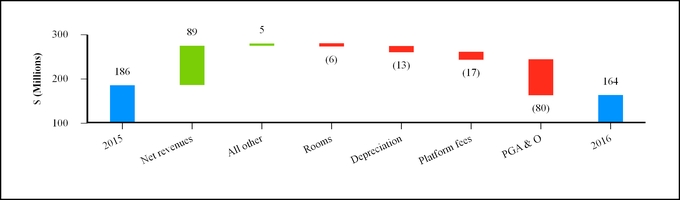

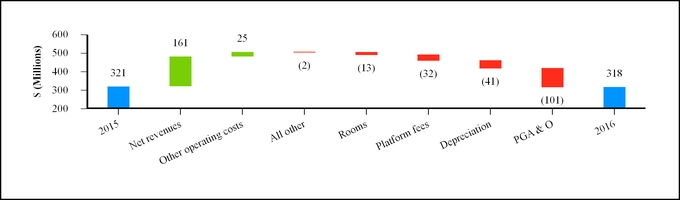

Income from operations | 164 | |

| 186 | |

| 318 | |

| 330 | | ||||

Interest expense | (150 | ) |

| (147 | ) |

| (301 | ) |

| (384 | ) | ||||

Deconsolidation and restructuring of CEOC and other | (2,026 | ) |

| 7 | |

| (2,263 | ) |

| 7,096 | | ||||

Income/(loss) from continuing operations before income taxes | (2,012 | ) |

| 46 | |

| (2,246 | ) |

| 7,042 | | ||||

Income tax benefit/(provision) | (31 | ) |

| 4 | |

| (71 | ) |

| (188 | ) | ||||

Income/(loss) from continuing operations, net of income taxes | (2,043 | ) |

| 50 | |

| (2,317 | ) |

| 6,854 | | ||||

Loss from discontinued operations, net of income taxes | - | |

| - | |

| - | |

| (7 | ) | ||||

Net income/(loss) | (2,043 | ) |

| 50 | |

| (2,317 | ) |

| 6,847 | | ||||

Net income attributable to noncontrolling interests | (34 | ) |

| (35 | ) |

| (68 | ) |

| (60 | ) | ||||

Net income/(loss) attributable to Caesars | $ | (2,077 | ) |

| $ | 15 | |

| $ | (2,385 | ) |

| $ | 6,787 | |

|

|

|

|

|

|

|

| ||||||||

Earnings/(loss) per share - basic and diluted | | | |

| | | | | | | |||||

Basic earnings/(loss) per share from continuing operations | $ | (14.25 | ) | | $ | 0.10 | | | $ | (16.39 | ) | | $ | 46.93 | |

Basic loss per share from discontinued operations | - | | | - | | | - | | | (0.04 | ) | ||||

Basic earnings/(loss) per share | $ | (14.25 | ) |

| $ | 0.10 | |

| $ | (16.39 | ) |

| $ | 46.89 | |

|

|

|

|

|

|

|

| ||||||||

Diluted earnings/(loss) per share from continuing operations | $ | (14.25 | ) |

| $ | 0.10 | |

| $ | (16.39 | ) |

| $ | 46.31 | |

Diluted loss per share from discontinued operations | - | |

| - | |

| - | |

| (0.04 | ) | ||||

Diluted earnings/(loss) per share | $ | (14.25 | ) |

| $ | 0.10 | |

| $ | (16.39 | ) |

| $ | 46.27 | |

|

|

|

|

|

|

|

| ||||||||

Weighted-average common shares outstanding - basic | 146 | |

| 145 | |

| 146 | |

| 145 | | ||||

Weighted-average common shares outstanding - diluted | 146 | |

| 147 | |

| 146 | |

| 147 | | ||||

See accompanying Notes to Consolidated Condensed Financial Statements.

4

CAESARS ENTERTAINMENT CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF STOCKHOLDERS' EQUITY/(DEFICIT)

(UNAUDITED)

| Caesars Stockholders' Equity/(Deficit) |

|

|

|

| ||||||||||||||||||||||||||

(In millions) | Common Stock |

| Treasury Stock |

| Additional Paid-in- Capital |

| Accumulated Deficit |

| Accumulated Other Comprehensive Income/(Loss) |

| Total Caesars Stockholders' Equity/(Deficit) |

| Noncontrolling Interests |

| Total Equity/(Deficit) | ||||||||||||||||

Balance as of December 31, 2014 | $ | 1 | |

| $ | (19 | ) |

| $ | 8,140 | |

| $ | (13,104 | ) |

| $ | (15 | ) |

| $ | (4,997 | ) |

| $ | 255 | |

| $ | (4,742 | ) |

Net income | - | |

| - | |

| - | |

| 6,787 | |

| - | |

| 6,787 | |

| 60 | |

| 6,847 | | ||||||||

Share-based compensation | - | |

| (2 | ) |

| 31 | |

| - | |

| - | |

| 29 | |

| - | |

| 29 | | ||||||||

Elimination of CEOC noncontrolling interest and deconsolidation (1) | - | |

| - | |

| - | |

| - | |

| 16 | |

| 16 | |

| 854 | |

| 870 | | ||||||||

Decrease in noncontrolling interests, net of distributions and contributions | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| (8 | ) |

| (8 | ) | ||||||||

Other | - | |

| - | |

| (4 | ) |

| - | |

| 1 | |

| (3 | ) |

| 15 | |

| 12 | | ||||||||

Balance as of June 30, 2015 | $ | 1 | |

| $ | (21 | ) |

| $ | 8,167 | |

| $ | (6,317 | ) |

| $ | 2 | |

| $ | 1,832 | |

| $ | 1,176 | |

| $ | 3,008 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||

Balance as of December 31, 2015 | $ | 1 | |

| $ | (21 | ) |

| $ | 8,191 | |

| $ | (7,185 | ) |

| $ | 1 | |

| $ | 987 | |

| $ | 1,246 | |

| $ | 2,233 | |

Net income/(loss) | - | |

| - | |

| - | |

| (2,385 | ) |

| - | |

| (2,385 | ) |

| 68 | |

| (2,317 | ) | ||||||||

Share-based compensation | - | |

| (5 | ) |

| 24 | |

| - | |

| - | |

| 19 | |

| - | |

| 19 | | ||||||||

CIE stock transactions, net | - | |

| - | |

| (15 | ) |

| - | |

| - | |

| (15 | ) |

| (5 | ) |

| (20 | ) | ||||||||

Change in noncontrolling interest, net of distributions and contributions | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| (8 | ) |

| (8 | ) | ||||||||

Other | - | |

| - | |

| - | |

| - | |

| - | |

| - | |

| (3 | ) |

| (3 | ) | ||||||||

Balance as of June 30, 2016 | $ | 1 | |

| $ | (26 | ) |

| $ | 8,200 | |

| $ | (9,570 | ) |

| $ | 1 | |

| $ | (1,394 | ) |

| $ | 1,298 | |

| $ | (96 | ) |

____________________

(1) | The effect of the deconsolidation of CEOC. See Note 1 . |

See accompanying Notes to Consolidated Condensed Financial Statements.

5

CAESARS ENTERTAINMENT CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| Six Months Ended June 30, | ||||||

(In millions) | 2016 |

| 2015 | ||||

Cash flows provided by operating activities | $ | 366 | |

| $ | 101 | |

Cash flows from investing activities |

|

|

| ||||

Acquisitions of property and equipment, net of change in related payables | (106 | ) |

| (227 | ) | ||

Deconsolidation of CEOC cash | - | |

| (958 | ) | ||

Increase in restricted cash | (6 | ) |

| (30 | ) | ||

Decrease in restricted cash | 113 | |

| 41 | | ||

Proceeds from the sale and maturity of investments | 24 | |

| - | | ||

Payments to acquire investments | (8 | ) |

| - | | ||

Other | (1 | ) |

| - | | ||

Cash flows provided by/(used in) investing activities | 16 | |

| (1,174 | ) | ||

Cash flows from financing activities |

|

|

| ||||

Proceeds from long-term debt and revolving credit facilities | 80 | |

| 190 | | ||

Repayments of long-term debt and revolving credit facilities | (221 | ) |

| (258 | ) | ||

Payment of contingent consideration | - | |

| (32 | ) | ||

Repurchase of CIE management shares | (43 | ) |

| (38 | ) | ||

Distributions to noncontrolling interest owners | (13 | ) |

| (15 | ) | ||

Other | 2 | |

| 6 | | ||

Cash flows used in financing activities | (195 | ) |

| (147 | ) | ||

Cash flows from discontinued operations |

|

|

| ||||

Cash flows used in operating activities | - | |

| (7 | ) | ||

Cash used in discontinued operations | - | |

| (7 | ) | ||

Net increase/(decrease) in cash and cash equivalents | 187 | |

| (1,227 | ) | ||

Cash and cash equivalents, beginning of period | 1,338 | |

| 2,806 | | ||

Cash and cash equivalents, end of period | $ | 1,525 | |

| $ | 1,579 | |

|

|

|

| ||||

Supplemental Cash Flow Information: |

|

|

| ||||

Cash paid for interest | $ | 290 | |

| $ | 403 | |

Cash paid for income taxes | 46 | |

| 35 | | ||

Non-cash investing and financing activities: |

|

|

| ||||

Change in accrued capital expenditures | (8 | ) |

| (11 | ) | ||

See accompanying Notes to Consolidated Condensed Financial Statements.

6

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS

(UNAUDITED)

In this filing, the name "CEC" refers to the parent holding company, Caesars Entertainment Corporation, exclusive of its consolidated subsidiaries and variable interest entities, unless otherwise stated or the context otherwise requires. The words "Company," "Caesars," "Caesars Entertainment," "we," "our," and "us" refer to Caesars Entertainment Corporation, inclusive of its consolidated subsidiaries and variable interest entities, unless otherwise stated or the context otherwise requires.

This Form 10-Q should be read in conjunction with our Annual Report on Form 10-K for the year ended December 31, 2015 (" 2015 10-K").

We also refer to (i) our Consolidated Condensed Financial Statements as our "Financial Statements," (ii) our Consolidated Condensed Statements of Operations and Comprehensive Income as our "Statements of Operations," and (iii) our Consolidated Condensed Balance Sheets as our "Balance Sheets."

Note 1

-

Description of Business

Organization

CEC is primarily a holding company with no independent operations of its own. CEC owns 100% of Caesars Entertainment Resort Properties, LLC ("CERP") and an interest in Caesars Growth Partners, LLC ("CGP"). We also consolidate the results of Caesars Interactive Entertainment, Inc. ("CIE"), a majority owned subsidiary of CGP that operates an online games business and owns the World Series of Poker ("WSOP") tournaments and brand (see Note 16 ). As of June 30, 2016 , CERP and CGP owned a total of 12 casino properties in the United States, eight of which are in Las Vegas. These eight casino properties represented 53% of consolidated net revenues for both the three and six months ended June 30, 2016 .

CEC also holds a majority interest in Caesars Entertainment Operating Company, Inc. ("CEOC"). The results of CEOC and its subsidiaries are no longer consolidated with Caesars subsequent to CEOC and certain of its United States subsidiaries (the "Debtors") voluntarily filing for reorganization under Chapter 11 of the United States Bankruptcy Code (the "Bankruptcy Code") on January 15, 2015 .

Caesars Enterprise Services, LLC

Caesars Enterprise Services, LLC ("CES") is a services joint venture formed by CERP, CEOC, and Caesars Growth Properties Holdings, LLC ("CGPH") (collectively, the "Members"). CES provides certain corporate and administrative services for the Members' casino properties and related entities, including substantially all of the 28 casino properties owned by CEOC, and 7 casinos owned by unrelated third parties (including four Indian tribal casinos). CES manages certain assets for the casinos to which it provides services and the other assets it owns, licenses or controls, and employs certain of the corresponding employees. Under the terms of the joint venture and the Omnibus License and Enterprise Services Agreement, CEC and its operating subsidiaries continue to have access to the services historically provided to us by CEOC and its employees, its trademarks, and its programs despite the CEOC bankruptcy filing.

Reportable Segments

We view each casino property and CIE as operating segments and currently aggregate all such casino properties and CIE into three reportable segments based on management's view, which aligns with their ownership and underlying credit structures: CERP, Caesars Growth Partners Casino Properties and Developments ("CGP Casinos"), and CIE. CGP Casinos is comprised of all subsidiaries of CGP excluding CIE. CEOC remained a reportable segment until its deconsolidation effective January 15, 2015 .

Announced Merger with Caesars Acquisition Company

In 2014, Caesars and Caesars Acquisition Company ("CAC") entered into a merger agreement, which was amended and restated on July 9, 2016 (the "Merger Agreement"). Pursuant to the Merger Agreement, among other things, CAC will merge with and into Caesars, with Caesars as the surviving company (the "Merger"). Subject to the terms and conditions of the Merger Agreement, upon consummation of the Merger, each share of CAC common stock issued and outstanding immediately prior to the effective date of the Merger will be converted into, and become exchangeable for, shares of CEC common stock in a ratio to ensure that holders of CAC common stock receive shares equal to 27% of the outstanding CEC common stock on a fully diluted basis (prior to the conversion of the CEC Convertible Notes being issued as part of the Restructuring, as defined below) (the "Exchange Ratio").

7

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

The Exchange Ratio may be subject to change, and Caesars or CAC may terminate the Merger Agreement under certain circumstances.

We expect the Merger to be accounted for as a transaction among entities under common control, which will result in CAC being consolidated into Caesars at book value as an equity transaction.

Going Concern

Overview

As a result of the following circumstances, we have substantial doubt about CEC's ability to continue as a going concern:

• | we have limited cash available to meet the financial commitments of CEC, primarily resulting from significant expenditures made to (1) defend against the litigation matters disclosed below and (2) support a plan of reorganization for CEOC (the "Restructuring"); |

• | we have made material future commitments to support the Restructuring described below; and |

• | we are a defendant in litigation relating to certain CEOC transactions dating back to 2010 and other legal matters (see Note 3 ) that could result in one or more adverse rulings against us. |

The completion of the Merger is expected to aid CEC in meeting its previously disclosed financial commitments to support the Restructuring. While the cash forecast at CEC currently contemplates liquidity to be sufficient through the end of the year, the CEC cash balance will be consumed by expenses associated with the Restructuring unless we identify additional sources of liquidity to meet CEC's ongoing obligations as well as its commitments to support the Restructuring. We are evaluating whether we are able to obtain additional sources of cash. Furthermore, if the Merger is not completed for any reason, CEC would still be liable for many of these obligations.

Under the terms of the Restructuring, all related litigation is expected to be resolved. However, if CEC is unable to obtain additional sources of cash when needed, in the event of a material adverse ruling on one or all of the litigation matters disclosed below, or if CEOC does not emerge from bankruptcy on a timely basis on terms and under circumstances satisfactory to CEC, it is likely that CEC would seek reorganization under Chapter 11 of the Bankruptcy Code.

We believe that CERP and CGP's cash and cash equivalents, their cash flows from operations, and/or financing available under their separate revolving credit facilities will be sufficient to meet their normal operating requirements, to fund planned capital expenditures, and to fund debt service during the next 12 months and the foreseeable future.

CEOC Reorganization

On June 28, 2016, the Debtors filed an amended plan of reorganization (the "Amended Plan") with the United States Bankruptcy Court for the Northern District of Illinois in Chicago (the "Bankruptcy Court") that replaces and provides for different terms than the Initial Plan filed in October 2015. CEC, CAC, the Debtors and multiple CEOC creditor groups have agreed to support and vote in favor of the Amended Plan. The confirmation hearing for the Amended Plan has been scheduled for January 2017.

In connection with the Amended Plan, the following agreements with respect to the CEOC reorganization were either entered into or amended (collectively, the "RSAs"):

(a) | First Amended Restructuring Support and Forbearance Agreement dated June 20, 2016, with certain parties holding claims under CEOC's first lien credit agreement (the "First Lien Bank RSA"); |

(b) | Restructuring Support and Forbearance Agreement dated June 21, 2016, with certain parties holding claims under CEOC's subsidiary guaranteed notes (the "SGN RSA"); |

(c) | First Amended and Restated Restructuring Support, Settlement, and Contribution Agreement dated July 9, 2016, with CEOC (the "CEC RSA"); |

(d) | Amended and Restated Restructuring Support Agreement dated July 9, 2016, with CAC and CEOC (the "CAC RSA"); |

8

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

(e) | Restructuring Support and Settlement Agreement dated June 22, 2016, with the unsecured claimholders' committee in the Chapter 11 cases (the "UCC RSA"); and |

(f) | Restructuring Support and Forbearance Agreement dated July 31, 2016, with certain parties holding claims under CEOC's second lien note agreements (the "Second Lien Note RSA") (see Note 16 ). |

The "Effective Date" of the Restructuring (the material terms of which are contained in the RSAs and the Amended Plan) is the date upon which all required conditions of the Restructuring have been satisfied or waived and on which the CEOC reorganization and related transactions become effective.

Due to the amount of consensus indicated among the Amended Plan and the RSAs and the status of negotiations with certain of CEOC's other creditor groups, we believe it is probable that certain obligations described in the Amended Plan and the RSAs will ultimately be settled, and therefore, we have accrued the items described in the table below that are estimable in accrued restructuring and support expenses on the balance sheets. During the second quarter of 2016 , we updated our accruals based on the terms of the Amended Plan and the RSAs and recorded an additional $2.0 billion in deconsolidation and restructuring of CEOC and other in the statement of operations, which increased our total expense to $2.3 billion for the six months ended June 30, 2016 .

To estimate the amount of the restructuring accrual, we allocated the estimated fair value of the total consideration to the acquisition of OpCo (as defined below) with the residual amounts being allocated to the restructuring accrual. We believe our accruals represent the best estimate of our obligations under the Restructuring. However, because (1) negotiations between the various parties are ongoing and (2) the Amended Plan is pending approval by the Bankruptcy Court and the receipt of required gaming regulatory approvals, our accruals are subject to change. Additionally, a substantial amount of the accrual relates to the expected issuance of CEC equity and convertible notes. Although, pursuant to the terms of the Amended Plan, as certain obligations will ultimately be settled in exchange for CEC equity and convertible notes, we have used the estimated current fair value of the CEC equity and convertible notes for accrual purposes. The value of the CEC common stock and convertible notes issuable upon consummation of the Merger and other transactions as contemplated in the Amended Plan are subject to change and will likely differ from the current value of such instruments. As a result, we expect to adjust the fair value of the accrual on a quarterly basis pending the determination of the actual fair value of the securities issued upon the consummation of the Merger and the Amended Plan. See Note 7 for additional information on our fair value measurements.

We are also party to the Fifth Amended and Restated Restructuring Support and Forbearance Agreement dated October 7, 2015, with certain parties holding claims under CEOC's first lien notes (the "First Lien Bond RSA") that includes terms different than those included in the Amended Plan and the RSAs listed above, but has not yet been amended or terminated. However, our accruals with respect to such claims have been adjusted based on the more current terms in the Amended Plan, which exceed the amounts contemplated by the First Lien Bond RSA. Additionally, although a majority of the parties holding claims under CEOC second lien notes have not yet agreed to the terms contemplated in the Second Lien Note RSA, we have accrued such amounts, as appropriate, as they exceed the amounts contemplated by the Amended Plan, and our accrual represents our best estimate of our obligations.

.

9

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

Accrued Restructuring and Support Expenses | |||||||||||||||

|

|

|

|

| Accrued as of | ||||||||||

(Dollars in millions) | Initial Plan Terms |

| Amended Plan |

| June 30, 2016 |

| December 31, 2015 | ||||||||

Cash to Debtors and forbearance fees ("Fixed Payments") in connection with the Restructuring (1) | $ | 406 | |

| $ | 406 | |

| $ | 320 | |

| $ | 320 | |

Contingent payment to CEOC if there is insufficient liquidity at the Effective Date (2) | 75 | |

| - | |

| - | |

| - | | ||||

"Additional Consideration" for the period from February 1, 2016 through the Effective Date for the benefit of the First Lien Noteholders (2) | $25 per month |

| - | |

| - | |

| 162 | | |||||

"Upfront Payments" to certain First Lien Bank Lenders (3) | 63 | |

| 63 | |

| 2 | |

| 2 | | ||||

"Bank Guaranty Settlement" to purchase from the Settling First Lien Bank Lenders 100% of their respective First Lien Bank Obligations that survive the Effective Date (4) | 460 | |

| 579 | |

| 579 | |

| 386 | | ||||

Issuance of CEC convertible notes for the settlement of litigation claims and potential claims against CEC (5) | - | |

| 1,000 | |

| 1,060 | |

| - | | ||||

Issuance of CEC common shares for the settlement of litigation claims and potential claims against CEC (6) | - | |

| - | |

| 1,167 | |

| - | | ||||

Professional fees for subsidiary guaranteed note lenders | - | |

| 2 | |

| 2 | |

| - | | ||||

Consideration for general unsecured claims | - | |

| 5 | |

| 5 | |

| - | | ||||

Total accrued |

|

|

|

| $ | 3,135 | |

| $ | 870 | | ||||

____________________

(1) | $86 million was paid in fourth quarter of 2015. |

(2) | This provision is included in the First Lien Bond RSA, but has been omitted from the Amended Plan and the other RSAs. |

(3) | $61 million was paid in fourth quarter of 2015. |

(4) | Amount payable is subject to the excess cash projected to be held by CEOC on the Effective Date. |

(5) | Accrual represents the estimated fair value of the $1.0 billion in face value of convertible notes CEC expects to issue as part of the Amended Plan. The convertible notes mature within seven years of issuance, prior to which they can be converted to a number of shares equal to 12.195% of CEC's fully diluted outstanding shares as of the Effective Date (subject to limitation). See Note 7 for additional information on fair value measurements. |

(6) | Accrual represents the estimated fair value of the portion of CEC common shares expected to be issued as part of the Amended Plan for the settlement of claims. This fair value does not include the value of CEC common shares expected to be issued in exchange for OpCo preferred stock, described below. See Note 7 for additional information on fair value measurements. |

10

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

Other Commitments Under the Amended Plan

The following represents other commitments or potential obligations that CEC has agreed to as part of the Amended Plan and certain of the RSAs, none of which have been accrued as of June 30, 2016.

Purchase 100% of OpCo common stock for $700 million (1) |

Issuance of CEC common shares in exchange for OpCo preferred stock |

Purchase 5% of PropCo equity for $91 million (2) |

PropCo has right of first refusal on all new domestic non-Las Vegas gaming facility opportunities, with CEC or OpCo leasing such properties |

PropCo receives a call right to purchase listed properties: Harrah's Atlantic City, Harrah's Laughlin, and Harrah's New Orleans (subject to the terms of the CERP and CGPH credit agreements) |

Guarantee of OpCo's payment obligations to PropCo under the leases of the CEOC Properties |

Guarantee of OpCo debt received by the First Lien Bank Lenders and First Lien Noteholders |

____________________

(1) | "OpCo" refers to the proposed entity resulting from the Restructuring that will operate the CEOC Properties under a lease with PropCo. "CEOC Properties" refers to those properties owned by CEOC as of the Petition Date. |

(2) | "PropCo" refers to the proposed entity resulting from the Restructuring that will own the CEOC Properties as of the Effective Date. This commitment is dependent on the ultimate legal structure of the entities formed as part of the Restructuring. |

The acquisitions of OpCo equity and PropCo equity represent future investment transactions and will be recorded when (or if) the transactions are consummated. The PropCo right of refusal and call right to purchase the listed properties are either not estimable or not financial obligations that would require accrual. The guarantee of OpCo payment or debt obligations relate to contracts or debt instruments that do not yet exist, and thus do not give rise to any obligations for CEC as of June 30, 2016.

Payment to CEOC . In addition, and separate from the transactions and agreements described above, because there was not a comprehensive out-of-court restructuring of CEOC's debt securities or a prepackaged or prearranged in-court restructuring with requisite voting support from each of the first and second lien secured creditor classes by February 15, 2016, the agreement contemplates an additional payment to CEOC of $35 million from CEC, which CEOC has demanded. During the first quarter of 2015, we accrued this liability in accrued restructuring and support expenses on the consolidated balance sheet, and this amount is currently due and payable.

CEC Liquidity

Caesars Entertainment (which includes CEC and its consolidated subsidiaries and VIEs) is a highly-leveraged company and had $7.0 billion in consolidated debt outstanding as of June 30, 2016 . As a result, a significant portion of our liquidity needs are for debt service, including significant interest payments. As detailed in Note 9 , our consolidated estimated debt service (including principal and interest) for the remainder of 2016 is $312 million and $9.4 billion thereafter to maturity. See Note 9 for details of our debt outstanding and related restrictive covenants. This includes, among other information, details of our individual borrowings outstanding and each subsidiary's annual maturities of long-term debt as of June 30, 2016 .

Cash and Available Revolver Capacity | |||||||||||||||

| June 30, 2016 | ||||||||||||||

(In millions) | CERP |

| CES |

| CGP |

| Other | ||||||||

Cash and cash equivalents | $ | 191 | |

| $ | 104 | |

| $ | 1,029 | |

| $ | 201 | |

Revolver capacity | 270 | |

| - | |

| 160 | |

| - | | ||||

Revolver capacity drawn or committed to letters of credit | (15 | ) |

| - | |

| - | |

| - | | ||||

Total | $ | 446 | |

| $ | 104 | |

| $ | 1,189 | |

| $ | 201 | |

11

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

Consolidated cash and cash equivalents, excluding restricted cash, as shown in the table above include amounts held by CERP, CGP, and CES, which are not readily available to CEC. "Other" reflects CEC and certain of its direct subsidiaries, including its insurance captives.

CEC is primarily a holding company with no independent operations, employees, or material debt issuances of its own. Its primary assets as of June 30, 2016 , consist of $201 million in cash and cash equivalents and its ownership interests in CEOC, CERP and CGP. CEC's cash includes $103 million held by its insurance captives. Provisions included in certain debt arrangements entered into by CERP and CGP (and/or their respective subsidiaries) substantially restrict the ability of CERP, CGP, and their subsidiaries to provide dividends to CEC. In addition, CEC does not receive any financial benefit from CEOC during CEOC's bankruptcy, as all earnings and cash flows are retained by CEOC for the benefit of its creditors.

CEC has no requirement to fund the operations of CERP, CGP, or their subsidiaries. Accordingly, CEC cash outflows are primarily used for corporate development opportunities and other corporate-level activity, including defending itself in the litigation in which it has been named as a defendant (see Note 3 ). CEC is generally limited to raising additional capital through borrowings or equity transactions because it has no operations of its own and the restrictions on its subsidiaries under lending arrangements generally prevent the distribution of cash from the subsidiaries to CEC, except for certain restricted payments that CERP and CGPH are authorized to make in accordance with their lending arrangements. In the first quarter of 2016, $100 million in cash that had previously been restricted by management for use in a casino development project became available for CEC's use in operations.

Guarantee of Collection

In 2014, CEOC amended its senior secured credit facilities (the "Bank Amendment") resulting in, among other things, a modification of CEC's guarantee under the senior secured credit facilities such that CEC's guarantee was limited to a guarantee of collection ("CEC Collection Guarantee") with respect to obligations owed to the lenders who consented to the Bank Amendment. The CEC Collection Guarantee requires the creditors to exhaust all rights and remedies at law and in equity that the creditors or their agents may have against CEOC or any of its subsidiaries and its and their respective property to collect, or obtain payment of, the guaranteed amounts. As part of the Bank Guaranty Settlement disclosed above, the CEOC creditors have agreed to eliminate the CEC Collection Guarantee, and we recorded $579 million as an estimate of the liability based on the terms of the Bank Guaranty Settlement agreement.

Litigation

In addition to financial commitments described above, we have the following outstanding uncertainties for which we have not accrued any amounts, all of which are described in Note 3 :

• | Litigation commenced by Wilmington Savings Fund Society, FSB on August 4, 2014 (the "Delaware Second Lien Lawsuit"); |

• | Litigation commenced by parties on September 3, 2014 and October 2, 2014 (the "Senior Unsecured Lawsuits"); |

• | Litigation commenced by UMB Bank on November 25, 2014 (the "Delaware First Lien Lawsuit"); |

• | Demands for payment made by Wilmington Savings Fund Society, FSB on February 13, 2015 (the "February 13 Notice"); |

• | Demands for payment made by BOKF, N.A., on February 18, 2015 (see "February 18 Notice"); |

• | Litigation commenced by BOKF, N.A. on March 3, 2015 (the "New York Second Lien Lawsuit"); |

• | Litigation commenced by UMB Bank on June 15, 2015 (the "New York First Lien Lawsuit"); |

• | Litigation commenced by Wilmington Trust, National Association on October 20, 2015 (the "New York Senior Notes Lawsuit"); and |

• | Litigation commenced by Trustees of the National Retirement Fund in January 2015 ("NRF Litigation"). |

Report of Bankruptcy Examiner

The Bankruptcy Court previously engaged an examiner to investigate possible claims CEOC might have against CEC and/or other entities and individuals. On March 15, 2016, the examiner released his report, which identifies a variety of potential claims against

12

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

CEC and certain individuals related to a number of transactions dating back to 2009. Most of the examiner's findings are premised on his view that CEOC was "insolvent" at the time of the applicable transactions and that CEOC did not receive fair value for assets transferred. The examiner's report includes his conclusions on the relative strengths of these possible claims, many of which are described in Note 3 . The examiner calculates an estimated range of potential damages for these potential claims from $3.6 billion to $5.1 billion , and such calculation does not account for probability of success, likelihood of collection, or the time or cost of litigation.

While this report was prepared at the request of the Bankruptcy Court, none of the findings included therein are legally binding on the Bankruptcy Court or any party. CEC contests most of the examiner's findings, including his findings that CEOC was insolvent at relevant times, that there were breaches of fiduciary duty, that CEOC did not receive fair value for assets transferred, that there were fraudulent transfers, and as to the calculation of damages. CEC believes that each of the challenged transactions was undertaken to provide CEOC with the liquidity and resources required to sustain it and provide time to recover from significant market challenges.

CEC believes that the conclusion of the examination and the release of the report was a necessary step to facilitate ongoing settlement discussions in the CEOC bankruptcy proceedings. In April 2016, CEC, CEOC, and various other constituents began mediation with Joseph Farnan, the former chief judge of the United States District Court for the District of Delaware, seeking to reach a mutually agreeable plan of reorganization of CEOC. Despite its disagreements with the examiner's conclusions, CEC has offered to provide substantial value to creditors in settlement as part of the plan of reorganization for CEOC. The mediation is ongoing, with further sessions scheduled over the next few weeks. CEC has been in regular, direct contact with both of CEOC's official creditors' committees, as well as other major creditor constituents, in an ongoing effort to arrive at a consensual plan providing for the timely emergence of CEOC from bankruptcy.

Note 2

-

Basis of Presentation and Consolidation

Basis of Presentation

The accompanying unaudited consolidated condensed financial statements of Caesars have been prepared under the rules and regulations of the Securities and Exchange Commission applicable for interim periods, and therefore, do not include all information and footnotes necessary for complete financial statements in conformity with accounting principles generally accepted in the United States ("GAAP"). The results for the interim periods reflect all adjustments (consisting primarily of normal recurring adjustments) that management considers necessary for a fair presentation of financial position, results of operations, and cash flows. The results of operations for our interim periods are not necessarily indicative of the results of operations that may be achieved for the entire 2016 fiscal year. All amounts presented in these consolidated condensed financial statements and notes thereto exclude the operating results and cash flows of CEOC subsequent to January 15, 2015 , and the assets, liabilities, and equity of CEOC as of June 30, 2016 and December 31, 2015 .

Consolidation of Subsidiaries and Variable Interest Entities

We consolidate into our financial statements the accounts of all subsidiaries in which we have a controlling financial interest and variable interest entities ("VIEs") for which we or one of our consolidated subsidiaries is the primary beneficiary. Control generally equates to ownership percentage, whereby (1) affiliates that are more than 50% owned are consolidated; (2) investments in affiliates of 50% or less but greater than 20% are generally accounted for using the equity method where we have determined that we have significant influence over the entities; and (3) investments in affiliates of 20% or less are generally accounted for using the cost method.

Consolidation of CGP

Because the equity holders in CGP receive returns disproportionate to their voting interests and substantially all the activities of CGP are related to Caesars, CGP has been determined to be a VIE. CAC is the sole voting member of CGP. Common control exists between CAC and Caesars through the majority beneficial ownership of both by Hamlet Holdings (as defined in Note 15 ). The assets held by CGP originally came from Caesars and continue to be intrinsically closely associated with Caesars through the nature of the business, as well as ongoing service and management agreements. Additionally, CEC is expected to receive the majority of the benefits or absorb the majority of the losses from its higher economic participation in CGP. Since CEC is more closely associated with CGP than CAC, we have determined that CEC is the primary beneficiary of CGP and is required to

13

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

consolidate them. Neither CAC nor CGP guarantees any of CEC's debt, and the creditors or beneficial holders of CGP have no recourse to the general credit of CEC.

CGP generated net revenues of $672 million and $574 million for the three months ended June 30, 2016 and 2015 , respectively, and $1.3 billion and $1.1 billion for the six months ended June 30, 2016 and 2015 , respectively. Net loss attributable to Caesars related to CGP was $16 million and $12 million for the three and six months ended June 30, 2016 , respectively. Net income attributable to Caesars related to CGP was $8 million and $6 million for the three and six months ended June 30, 2015 , respectively.

CGP was obligated to issue non-voting membership units to CEC in 2016 to the extent that the earnings from CIE's social and mobile games business exceeded a specified threshold amount as of December 31, 2015 . In April 2016, CGP issued 32 million Class B non-voting units to CEC, resulting in CEC's economic ownership in CGP increasing from 57.4% to 61.2% . However, there was no effect on our financial statements from this transaction.

Consolidation of CES

A steering committee acts in the role of a board of managers for CES with each Member entitled to appoint one representative to the steering committee. Each Member, through its representative, is entitled to a single vote on the steering committee; accordingly, the voting power of the Members does not equate to their ownership percentages. Therefore, w hen CES was formed, we determined that it was a VIE, and we concluded that CERP was required to consolidate it.

Effective January 1, 2016, we implemented the Financial Accounting Standard Board's (the "FASB") Accounting Standard Update ("ASU") No. 2015-02, which amended Topic 810, Consolidations . Applying the amended guidance had no effect on our consolidated financial statements.

Under the guidance in effect prior to ASU No. 2015-02, CERP was determined to be the primary beneficiary of CES, and we consolidated CES through our consolidation of CERP. Under the amended guidance, in determining whether an entity is the primary beneficiary of a VIE, the entity must evaluate whether it has the power to direct the activities of the VIE that most significantly impact the VIE's economic performance through both its direct economic interests in the VIE and its indirect economic interests in the VIE held through related parties. Under the new criteria, when a decision maker exists that holds both power and benefits through its related parties and neither related party holds such power and benefits on their own, the decision maker is determined to be the primary beneficiary. Therefore, we concluded that CEC is the primary beneficiary because our combined economic interest in CES, through our subsidiaries, represents a controlling financial interest.

Expenses incurred by CES are allocated to the casino properties directly or to the Members according to their allocation percentages, subject to annual review. Therefore, CES is a "pass-through" entity that serves as an agent on behalf of the Members at a cost-basis, and is contractually required to fully allocate its costs. CES is designed to have no operating cash flows of its own, and any net income or loss is generally immaterial and is typically subject to allocation to the Members in the subsequent period.

Consolidation Considerations for CEOC

CEOC's filing for reorganization was a reconsideration event for Caesars Entertainment to reevaluate whether consolidation of CEOC continued to be appropriate. We concluded that CEOC is a VIE and that we are not the primary beneficiary of CEOC; therefore, we no longer consolidate CEOC.

Transactions with CEOC are treated as related party transactions for Caesars Entertainment. These transactions include items such as casino management fees paid to CEOC, insurance expenses related to insurance coverage provided to CEOC by Caesars Entertainment, and rent payments by CEOC to CERP under the Octavius Tower lease agreement. See Note 15 for additional information on related party transactions and on the carrying amounts and classification of assets and liabilities that relate to our variable interest in CEOC.

14

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

Note 3

-

Litigation

Litigation

Noteholder Disputes

On August 4, 2014 , Wilmington Savings Fund Society, FSB, solely in its capacity as successor Indenture Trustee for the 10.00% Second-Priority Senior Secured Notes due 2018 (the "10.00% Second-Priority Notes"), on behalf of itself and, it alleges, derivatively on behalf of CEOC , filed a lawsuit (the "Delaware Second Lien Lawsuit") in the Court of Chancery in the State of Delaware against CEC and CEOC, CGP, CAC,CERP, CES, Eric Hession, Gary Loveman, Jeffrey D. Benjamin, David Bonderman, Kelvin L. Davis, Marc C. Rowan, David B. Sambur, and Eric Press . The lawsuit alleges claims for breach of contract, intentional and constructive fraudulent transfer, breach of fiduciary duty, aiding and abetting breach of fiduciary duty, and corporate waste. The lawsuit seeks (1) an award of money damages; (2) to void certain transfers, the earliest of which dates back to 2010; (3) an injunction directing the recipients of the assets in these transactions to return them to CEOC; (4) a declaration that CEC remains liable under the parent guarantee formerly applicable to the 10.00% Second-Priority Notes; (5) to impose a constructive trust or equitable lien on the transferred assets; and (6) an award to plaintiffs for their attorneys' fees and costs. CEC believes this lawsuit is without merit and is defending itself vigorously. A motion to dismiss this action was filed by CEC and other defendants in September 2014, and the motion was argued in December 2014. During the pendency of its Chapter 11 bankruptcy proceedings, the action has been automatically stayed with respect to CEOC. The motion to dismiss with respect to CEC was denied on March 18, 2015. In a Verified Supplemental Complaint filed on August 3, 2015, the plaintiff stated that due to CEOC's bankruptcy filing, the continuation of all claims was stayed pursuant to the bankruptcy except for Claims II, III, and X. These are claims against CEC only, for breach of contract in respect of the release of the parent guarantee formerly applicable to the CEOC 10.00% Second-Priority Notes, for declaratory relief in respect of the release of this guarantee, and for violations of the Trust Indenture Act in respect of the release of this guarantee. Fact discovery in the case is complete, and cross-motions for summary judgment have been filed by the parties. On June 15, 2016, the Bankruptcy Court granted CEOC's motion for a temporary stay of this proceeding (and others). The stay will remain in effect until August 29, 2016, unless extended.

On September 3, 2014 , holders of approximately $21 million of CEOC 6.50% Senior Unsecured Notes due 2016 and 5.75% Senior Unsecured Noted due 2017 (collectively, the "Senior Unsecured Notes") filed suit in federal district court in Manhattan against CEC and CEOC , claiming broadly that an August 12, 2014 Note Purchase and Support Agreement between CEC and CEOC (on the one hand) and certain other holders of the Senior Unsecured Notes (on the other hand) impaired their own rights under the Trust Indenture Act of 1939 and the indentures governing the Senior Unsecured Notes. The lawsuit seeks both declaratory and monetary relief. On October 2, 2014, a holder of CEOC's 6.50% Senior Unsecured Notes due 2016 purporting to represent a class of all persons who held these Notes from August 11, 2014 to the present filed a substantially similar suit in the same court, against the same defendants, relating to the same transactions. Both lawsuits (the "Senior Unsecured Lawsuits") were assigned to the same judge. The claims against CEOC have been automatically stayed during its Chapter 11 bankruptcy proceedings. The court denied a motion to dismiss both lawsuits with respect to CEC. The parties have completed fact discovery with respect to both plaintiffs' claims against CEC. On October 23, 2015, plaintiffs in the Senior Unsecured Lawsuits moved for partial summary judgment, and on December 29, 2015, those motions were denied. On December 4, 2015, plaintiff in the action brought on behalf of holders of CEOC's 6.50% Senior Unsecured Notes moved for class certification and briefing has been completed. The judge presiding over these cases recently retired, and a new judge has been appointed to preside over these lawsuits. That judge set a new summary judgment briefing schedule for May and June of 2016 and had indicated his intention to rule on these summary judgment motions on or before July 22, 2016, while also setting trial of remaining issues for August 22, 2016. On June 15, 2016, the Bankruptcy Court granted CEOC's motion for a temporary stay of these proceedings (and others). The stay will remain in effect until August 29, 2016, unless extended.

On November 25, 2014 , UMB Bank ("UMB"), as successor indenture trustee for CEOC's 8.50% Senior Secured Notes due 2020 (the "8.50% Senior Secured Notes") , filed a verified complaint (the "Delaware First Lien Lawsuit") in Delaware Chancery Court against CEC, CEOC, CERP, CAC, CGP, CES, and against individual past and present Board members Loveman, Benjamin, Bonderman, Davis, Press, Rowan, Sambur, Hession, Colvin, Kleisner, Swann, Williams, Housenbold, Cohen, Stauber, and Winograd , alleging generally that defendants improperly stripped CEOC of certain assets, wrongfully effected a release of CEC's parent guarantee of the 8.50% Senior Secured Notes and committed other wrongs. Among other things, UMB asked the court to appoint a receiver over CEOC. In addition, the suit pleads claims for fraudulent conveyances/transfers, insider preferences, illegal dividends, declaratory judgment (for breach of contract as regards to the parent guarantee and also as to certain covenants in the bond indenture), tortious interference with contract, breach of fiduciary duty, usurpation of corporate opportunities, and unjust

15

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

enrichment, and seeks monetary, equitable and declaratory relief. The lawsuit has been automatically stayed with respect to CEOC during its Chapter 11 bankruptcy process. Pursuant to the First Lien Bond RSA, the lawsuit also has been stayed in its entirety, with the consent of all of the parties to it. The consensual stay will expire upon the termination of the First Lien Bond RSA.

On February 13, 2015, Caesars Entertainment received a Demand For Payment of Guaranteed Obligations (the "February 13 Notice") from Wilmington Savings Fund Society, FSB, in its capacity as successor Trustee for CEOC's 10.00% Second-Priority Notes. The February 13 Notice alleges that CEOC's commencement of its voluntary Chapter 11 bankruptcy case constituted an event of default under the indenture governing the 10.00% Second-Priority Notes; that all amounts due and owing on the 10.00% Second-Priority Notes therefore immediately became payable; and that Caesars Entertainment is responsible for paying CEOC's obligations on the 10.00% Second-Priority Notes, including CEOC's obligation to timely pay all principal, interest, and any premium due on these notes, as a result of a parent guarantee provision contained in the indenture governing the notes that the February 13 Notice alleges is still binding. The February 13 Notice accordingly demands that Caesars Entertainment immediately pay Wilmington Savings Fund Society, FSB, cash in an amount of not less than $3.7 billion, plus accrued and unpaid interest (including without limitation the $184 million interest payment due December 15, 2014 that CEOC elected not to pay) and accrued and unpaid attorneys' fees and other expenses. The February 13 Notice also alleges that the interest, fees and expenses continue to accrue.

On February 18, 2015, Caesars Entertainment received a Demand For Payment of Guaranteed Obligations (the "February 18 Notice") from BOKF, N.A. ("BOKF"), in its capacity as successor Trustee for CEOC's 12.75% Second-Priority Senior Secured Notes due 2018 (the "12.75% Second-Priority Notes"). The February 18 Notice alleges that CEOC's commencement of its voluntary Chapter 11 bankruptcy case constituted an event of default under the indenture governing the 12.75% Second-Priority Notes; that all amounts due and owing on the 12.75% Second-Priority Notes therefore immediately became payable; and that CEC is responsible for paying CEOC's obligations on the 12.75% Second-Priority Notes, including CEOC's obligation to timely pay all principal, interest and any premium due on these notes, as a result of a parent guarantee provision contained in the indenture governing the notes that the February 18 Notice alleges is still binding. The February 18 Notice therefore demands that CEC immediately pay BOKF cash in an amount of not less than $750 million, plus accrued and unpaid interest, accrued and unpaid attorneys' fees, and other expenses. The February 18 Notice also alleges that the interest, fees and expenses continue to accrue.

In accordance with the terms of the applicable indentures, CEC is not subject to the above-described guarantees. As a result, we believe the demands for payment are meritless.

On March 3, 2015, BOKF filed a lawsuit (the "New York Second Lien Lawsuit") against CEC in federal district court in Manhattan, in its capacity as successor trustee for CEOC's 12.75% Second-Priority Notes. On June 15, 2015, UMB filed a lawsuit (the "New York First Lien Lawsuit") against CEC, also in federal district court in Manhattan, in its capacity as successor trustee for CEOC's 11.25% Senior Secured Notes due 2017, 8.50% Senior Secured Notes due 2020, and 9.00% Senior Secured Notes due 2020. Plaintiffs in these actions allege that CEOC's filing of its voluntary Chapter 11 bankruptcy case constitutes an event of default under the indentures governing these notes, causing all principal and interest to become immediately due and payable, and that CEC is obligated to make those payments pursuant to parent guarantee provisions in the indentures governing these notes that plaintiffs allege are still binding. Both plaintiffs bring claims for violation of the Trust Indenture Act of 1939, breach of contract, breach of duty of good faith and fair dealing and for declaratory relief and BOKF brings an additional claim for intentional interference with contractual relations. The cases were both assigned to the same judge presiding over the other Parent Guarantee Lawsuits (as defined below) that are taking place in Manhattan. CEC filed its answer to the BOKF complaint on March 25, 2015, and to the UMB complaint on August 10, 2015. On June 25, 2015, and June 26, 2015, BOKF and UMB, respectively, moved for partial summary judgment, specifically on their claims alleging a violation of the Trust Indenture Act of 1939, seeking both declaratory relief and damages. On August 27, 2015, those motions were denied. The court, on its own motion, certified its order with respect to the interpretation of the Trust Indenture Act for interlocutory appeal to the United States Court of Appeals for the Second Circuit, and on December 22, 2015, the appellate court denied our motion for leave to appeal. On November 20, 2015, BOKF and UMB again moved for partial summary judgment. These motions likewise were denied. The judge presiding over these cases recently retired, and a new judge has been appointed to preside over these lawsuits. That judge set a new summary judgment briefing schedule for May and June of 2016 and had indicated his intention to rule on these summary judgment motions on or before July 22, 2016, while also setting trial of remaining issues for August 22, 2016. On June 15, 2016, the Bankruptcy Court granted CEOC's motion for a temporary stay of the BOKF proceedings (and others). UMB has consented to application of the temporary stay to its lawsuit as well. The stay will remain in effect until August 29, 2016, unless extended.

16

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

On October 20, 2015, Wilmington Trust, National Association ("Wilmington Trust"), filed a lawsuit (the "New York Senior Notes Lawsuit" and, together with the Delaware Second Lien Lawsuit, the Delaware First Lien Lawsuit, the Senior Unsecured Lawsuits, the New York Second Lien Lawsuit, and the New York First Lien Lawsuit, the "Parent Guarantee Lawsuits") against CEC in federal district court in Manhattan in its capacity as successor indenture trustee for CEOC's 10.75% Senior Notes due 2016 (the "10.75% Senior Notes"). Plaintiff alleges that CEC is obligated to make payment of amounts due on the 10.75% Senior Notes pursuant to a parent guarantee provision in the indenture governing those notes that plaintiff alleges is still in effect. Plaintiff raises claims for violations of the Trust Indenture Act of 1939, breach of contract, breach of the implied duty of good faith and fair dealing, and for declaratory judgment, and seeks monetary and declaratory relief. CEC filed its answer to the complaint on November 23, 2015. As with the other parent guaranty lawsuits taking place in Manhattan, the judge presiding over these cases recently retired, and a new judge has been appointed to preside over these lawsuits. That judge set a new summary judgment briefing schedule for May and June of 2016 and had indicated his intention to rule on these summary judgment motions on or before July 22, 2016, while also setting trial of remaining issues for August 22, 2016. On June 15, 2016, the Bankruptcy Court granted CEOC's motion for a temporary stay of many of the Parent Guarantee Lawsuits. Wilmington Trust has consented to application of the temporary stay to this lawsuit. The stay will remain in effect until August 29, 2016, unless extended.

We believe that the claims and demands described above against CEC are without merit and we intend to defend the Company vigorously. The claims against CEOC have been stayed due to the Chapter 11 process and, except as described above, the actions against CEC have been allowed to continue. See additional disclosure relating to CEOC's Chapter 11 filing in Note 1. We believe that the Noteholder Disputes and the Parent Guarantee Lawsuits have a reasonably possible likelihood of an adverse outcome. Should these matters ultimately be resolved through litigation outside of the financial restructuring of CEOC (the "Financial Restructuring"), and should a court find in favor of the claimants in some or all of the Noteholder Disputes, such determination would likely lead to a CEC reorganization under Chapter 11 of the Bankruptcy Code (see Note 1). We are not able to estimate a range of reasonably possible losses should any of the Noteholder Disputes ultimately be resolved against us, although they could potentially exceed $11 billion.

CEC-CAC Merger Litigation

On December 30, 2014 , Nicholas Koskie, on behalf of himself and, he alleges, all others similarly situated , filed a lawsuit (the "Merger Lawsuit") in the Clark County District Court in the State of Nevada against CAC, CEC and members of the CAC board of directors Marc Beilinson, Philip Erlanger, Dhiren Fonseca, Don Kornstein, Karl Peterson, Marc Rowan, and David Sambur (the individual defendants collectively, the "CAC Directors") . The Merger Lawsuit alleges claims for breach of fiduciary duty against the CAC Directors and aiding and abetting breach of fiduciary duty against CAC and CEC. It seeks (1) an order directing the CAC Directors to fulfill alleged fiduciary duties to CAC in connection with the proposed merger between CAC and CEC announced on December 22, 2014, specifically by announcing their intention to (a) cooperate with bona fide interested parties proposing alternative transactions, (b) ensure that no conflicts exist between the CAC Directors' personal interests and their fiduciary duties to maximize shareholder value in the Merger, or resolve all such conflicts in favor of the latter, and (c) act independently to protect the interests of the shareholders; (2) an order directing the CAC Directors to account for all damages suffered or to be suffered by plaintiff and the putative class as a result of the Merger; and (3) an award to plaintiff for his costs and attorneys' fees. It is unclear whether the Merger Lawsuit also seeks to enjoin the Merger. CEC believes that this lawsuit is without merit and will defend itself vigorously. The deadline to respond to the Merger Lawsuit has been adjourned without a date by agreement of the parties.

Employee Benefit Obligations

In December 1998, Hilton Hotels Corporation ("Hilton") spun-off its gaming operations as Park Place Entertainment Corporation ("Park Place"). In connection with the spin-off, Hilton and Park Place entered into various agreements, including an Employee Benefits and Other Employment Allocation Agreement dated December 31, 1998 (the "Allocation Agreement") whereby Park Place assumed or retained, as applicable, certain liabilities and excess assets, if any, related to the Hilton Hotels Retirement Plan (the "Hilton Plan") based on the benefits of Hilton employees and Park Place employees. CEOC is the ultimate successor to this Allocation Agreement. In 2013, a lawsuit was settled related to the Hilton Plan, which retroactively and prospectively increased total benefits to be paid under the Hilton Plan. In 2009, we received a letter from Hilton, notifying us of a lawsuit related to the Hilton Plan that alleged that CEC had a potential liability for the additional claims under the terms of the Allocation Agreement.

On December 24, 2014, Hilton sued CEC and CEOC in federal court in Virginia primarily under the Employee Retirement Income Security Act ("ERISA"), and also under state contract and unjust enrichment law theories, for monetary and equitable relief in connection with this ongoing dispute.

17

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

On June 9, 2016, CEC, CEOC and the applicable Hilton parties entered into a settlement of the Hilton claims. Under the settlement, Hilton will receive a claim in CEOC's bankruptcy case for an amount equal to $51 million plus 31.75% for amounts paid by Hilton to the retirement plan due after July 16, 2016. For periods following the effective date of CEOC's plan of reorganization, CEC shall assume all of CEOC's obligation under the Allocation Agreement. In exchange, Hilton shall turn over to CEC the distributions on account of $24.5 million of Hilton's claim in the CEOC bankruptcy. The settlement amount is fully accrued in liabilities subject to compromise at CEOC, and the settlement is subject to Bankruptcy Court approval and the effectiveness of CEOC's plan of reorganization.

National Retirement Fund

In January 2015, a majority of the Trustees of the National Retirement Fund ("NRF"), a multi-employer defined benefit pension plan, voted to expel the five indirect subsidiaries of CEC which were required to make contributions to the legacy plan of the NRF (the "Five Employers"). The NRF contended that the financial condition of the Five Employers' controlled group (the "CEC Controlled Group") and CEOC's then-potential bankruptcy presented an "actuarial risk" to the plan because, depending on the outcome of any CEOC bankruptcy proceedings, CEC might no longer be liable to the plan for any partial or complete withdrawal liability. As a result, the NRF claimed that the expulsion of the Five Employers constituted a complete withdrawal of the CEC Controlled Group from the plan. CEOC, in its bankruptcy proceedings, has to date not rejected the contribution obligations to the NRF of any of its subsidiary employers. The NRF has advised the CEC Controlled Group (which includes CERP) that the expulsion of the Five Employers has triggered a joint and several withdrawal liability with a present value of approximately $360 million, payable in 80 quarterly payments of about $6 million.

Prior to the NRF's vote to expel the Five Employers, the Five Employers reiterated their commitments to remain in the plan and not seek rejection of any collective bargaining agreement in which the obligation to contribute to NRF exists. The Five Employers were current with respect to pension contributions at the time of their expulsion, and are current with respect to pension contributions as of today pursuant to the Standstill Agreement referred to below.

We have opposed the various NRF expulsion actions.

On January 8, 2015, prior to the NRF's vote to expel the Five Employers, CEC filed an action in the United States District Court for the Southern District of New York (the "S.D.N.Y.") against the NRF and its Board of Trustees, seeking a declaratory judgment that they did not have the authority to expel the Five Employers and thus allegedly trigger withdrawal liability for the CEC Controlled Group (the "CEC Action"). On December 25, 2015, the District Judge entered an order dismissing the CEC Action on the ground that CEC's claims in this action must first be arbitrated under ERISA. CEC has appealed this decision to the United States Court of Appeals for the Second Circuit.

On March 6 and March 27, 2015, CEOC and certain of its subsidiaries filed in the CEOC bankruptcy proceedings two motions to void (a) the purported expulsion of the Five Employers and based thereon the alleged triggering of withdrawal liability for the non-debtor members of the CEC Controlled Group, and (b) a notice and payment demand for quarterly payments of withdrawal liability subsequently made by the NRF to certain non-debtor members of the CEC Controlled Group, respectively, on the ground that each of these actions violated the automatic stay (the "362 Motions"). On November 12, 2015, Bankruptcy Judge Goldgar issued a decision denying the 362 Motions on the ground that the NRF's actions were directed at non-debtors and therefore did not violate the automatic stay. CEOC has appealed this decision to the federal district court in Chicago.

On March 6, 2015, CEOC commenced an adversary proceeding against the NRF and its Board of Trustees in the Bankruptcy Court (the "Adversary Proceeding"). On March 11, 2015, CEOC filed a motion in that Adversary Proceeding to extend the automatic stay in the CEOC bankruptcy proceedings to apply to the NRF's expulsion of the Five Employers (the "105 Motion"). Judge Goldgar has not yet decided the 105 Motion.

On March 20, 2015, CEC, CEOC and CERP, on behalf of themselves and others, entered into a Standstill Agreement with the NRF and its Board of Trustees that, among other things, stayed each member of the CEC Controlled Group's purported obligation to commence making quarterly payments of withdrawal liability and instead required the Five Employers to continue making monthly contribution payments to the NRF, unless and until each of the 362 Motions and the 105 Motion had been denied. As the 105 Motion has not yet been decided, the Standstill Agreement remains in effect.

If both the 105 Motion and CEC's appeal of the CEC Action are denied, then CEC could be required to pay to the NRF joint and several withdrawal liability with a present value of approximately $360 million , payable in 80 quarterly payments of about $6

18

CAESARS ENTERTAINMENT CORPORATION

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (CONTINUED)

(UNAUDITED)

million, while CEC simultaneously arbitrates whether the NRF and its Board of Trustees had the authority to expel the Five Employers and trigger withdrawal liability for the CEC Controlled Group.

Also, on March 18, 2015, the NRF and its fund manager commenced a collection action in the S.D.N.Y. against CEC, CERP and all non-debtor members of the CEC Controlled Group for the payment of the first quarterly payment of withdrawal liability, which the NRF contended was due on March 15, 2015 (the "NRF Action"). On December 25, 2015, the District Judge denied the defendants' motion to dismiss the NRF Action on the ground that the arguments raised by the defendants must first be arbitrated under ERISA. On February 26, 2016, the NRF and its fund manager filed a motion for summary judgment against CEC and CERP for payment of the first quarterly payment of withdrawal liability and for interest, liquidated damages, attorneys' fees and costs. On May 5, 2016, the Magistrate Judge recommended that the NRF Action plaintiffs' motion for summary judgment be granted on the ground that the further arguments raised by CEC and CERP must first be arbitrated under ERISA. On May 19, 2016, CEC and CERP filed their objections to the Report and Recommendation (the "Objections"). On June 2, 2016, the NRF Action plaintiffs filed their response to the Objections. The District Judge has not yet ruled on the Objections. If the District Judge adopts the Magistrate Judge's Report and Recommendation, then a judgment could be entered against CEC and CERP for approximately $8 million comprising the first quarterly payment of withdrawal liability referred to above, interest and liquidated damages under ERISA, which amount would be paid or bonded pending an appeal.

We believe our legal arguments against the actions undertaken by NRF are strong and will pursue them vigorously, and will defend vigorously against the claims raised by the NRF in the NRF Action. Because legal proceedings with respect to this matter are at the preliminary stages, we cannot currently provide assurance as to the ultimate outcome of the matters at issue.

Other Matters

In recent years, governmental authorities have been increasingly focused on anti-money laundering ("AML") policies and procedures, with a particular focus on the gaming industry. In October 2013, CEOC's subsidiary, Desert Palace, Inc. (the owner of and referred to herein as Caesars Palace), received a letter from the Financial Crimes Enforcement Network of the United States Department of the Treasury ("FinCEN"), stating that FinCEN was investigating Caesars Palace for alleged violations of the Bank Secrecy Act to determine whether it is appropriate to assess a civil penalty and/or take additional enforcement action against Caesars Palace. Caesars Palace responded to FinCEN's letter in January 2014. Additionally, we were informed in October 2013 that a federal grand jury investigation regarding anti-money laundering practices of the Company and its subsidiaries had been initiated. CEC and Caesars Palace have been cooperating with FinCEN, the Department of Justice and the Nevada Gaming Control Board (the "GCB") on this matter. On September 8, 2015, FinCEN announced a settlement pursuant to which Caesars Palace agreed to an $8 million civil penalty for its violations of the Bank Secrecy Act, which penalty shall be treated as a general unsecured claim in Caesars Palace's bankruptcy proceedings. In addition, Caesars Palace agreed to conduct periodic external audits and independent testing of its AML compliance program, report to FinCEN on mandated improvements, adopt a rigorous training regime, and engage in a "look-back" for suspicious transactions. The terms of the FinCEN settlement were approved by the Bankruptcy Court on October 19, 2015.

CEOC and the GCB reached a settlement on the same facts as above, wherein CEC agreed to pay $1.5 million and provide to the GCB the same information that is reported to FinCEN and to resubmit its updated AML policies. On September 17, 2015, the settlement agreement was approved by the Nevada Gaming Commission. CEOC continues to cooperate with the Department of Justice in its investigation of this matter.