SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED December 31, 2014

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File No. 1-10410

CAESARS ENTERTAINMENT CORPORATION

(Exact name of registrant as specified in its charter)

Delaware |

| 62-1411755 |

(State of incorporation) |

| (I.R.S. Employer Identification No.) |

|

|

|

One Caesars Palace Drive, Las Vegas, Nevada |

| 89109 |

(Address of principal executive offices) |

| (Zip code) |

Registrant's telephone number, including area code:

(702) 407-6000

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

Title of each class Name of each exchange on which registered

Common stock, $0.01 par value NASDAQ Global Select Market

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

|

| (Do not check if a smaller reporting company) |

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of common stock held by non-affiliates of the registrant as of June 30, 2014 was $1,024 million .

As of March 1, 2015 , the registrant had 144,677,371 shares of Common Stock outstanding.

CAESARS ENTERTAINMENT CORPORATION

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

|

| Page |

Part I |

|

|

| Item 1 – Business | 1 |

| Item 1A – Risk Factors | 8 |

| Item 1B – Unresolved Staff Comments | 30 |

| Item 2 – Properties | 31 |

| Item 3 – Legal Proceedings | 32 |

| Item 4 – Mine Safety Disclosure | 35 |

Part II |

|

|

| Item 5 – Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 36 |

| Item 6 – Selected Financial Data | 38 |

| Item 7 – Management's Discussion and Analysis of Financial Condition and Results of Operations | 39 |

| Item 7A – Quantitative and Qualitative Disclosures About Market Risk | 61 |

| Item 8 – Financial Statements and Supplementary Data | 62 |

| Report of Independent Registered Public Accounting Firm | 62 |

| Consolidated Financial Statements | 63 |

| Notes to Consolidated Financial Statements | 68 |

| Item 9 – Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 127 |

| Item 9A – Controls and Procedures | 127 |

| Item 9B – Other Information | 132 |

Part III |

|

|

| Item 10 – Directors, Executive Officers and Corporate Governance | 133 |

| Item 11 – Executive Compensation | 133 |

| Item 12 – Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 133 |

| Item 13 – Certain Relationships and Related Transactions, and Director Independence | 133 |

| Item 14 – Principal Accounting Fees and Services | 133 |

Part IV |

|

|

| Item 15 – Exhibits, Financial Statement Schedules | 134 |

|

| |

Signatures | 164 | |

We have proprietary rights to a number of trademarks used in this Annual Report on Form 10-K for the fiscal year ended December 31, 2014 (this "Form 10-K"), that are important to our business, including, without limitation, Caesars, Caesars Entertainment, Caesars Palace, Harrah's, Total Rewards, Horseshoe, Paris Las Vegas, Flamingo, and Bally's. In addition, Caesars Interactive Entertainment, Inc., which is a majority-owned subsidiary of Caesars Growth Partners, LLC, has proprietary rights to the World Series of Poker ("WSOP"), Slotomania, Bingo Blitz, and Playtika trademarks. We have omitted the registered trademark (®) and trademark (™) symbols for such trademarks named in this Form 10-K.

PART I

In order to make this report easier to read, we also refer throughout to (i) our Consolidated Financial Statements as our "Financial Statements," (ii) our Consolidated Statements of Operations as our "Statements of Operations," and (iii) our Consolidated Balance Sheets as our "Balance Sheets." References throughout to numbered "Notes" refer to the numbered Notes to our Financial Statements that we included in Item 8, " Financial Statements and Supplementary Data ."

ITEM 1. | Business |

Overview

Caesars Entertainment Corporation (referred to in this discussion, together with its consolidated entities where appropriate, as "Caesars," "Caesars Entertainment," "CEC," the "Company," "we," "our," and "us"), a Delaware corporation, is a casino-entertainment and hospitality services provider. We are the world's most diversified casino-entertainment company with entertainment facilities in more areas throughout the United States than any other participant in the gaming industry. We have established a rich history of industry-leading growth and expansion since we commenced operations in 1937. Our facilities typically include gaming offerings, food and beverage outlets, hotel and convention space, and non-gaming entertainment options. In addition to our brick and mortar assets, we operate an online gaming business that provides social and mobile offerings as well as real money games in certain jurisdictions.

As of December 31, 2014 , through our consolidated entities we owned and operated or managed 49 casinos in 14 U.S. states and 5 countries. Our facilities had an aggregate of over three million square feet of gaming space and over 39,000 hotel rooms. Of the 49 casinos, 37 were in the United States and primarily consist of land-based and riverboat or dockside casinos. Our 12 international casinos were land-based casinos, most of which are located in England.

Caesars Entertainment is primarily a holding company with no independent operations of its own and, as of December 31, 2014 , operated the business through the following consolidated entities (see Item 2, " Properties "):

• | Caesars Entertainment Resort Properties, LLC. Operated six casinos in the United States along with The LINQ promenade and owned Octavius Tower at Caesars Palace Las Vegas ("Octavius Tower"). |

• | Caesars Growth Partners, LLC. Operated six casinos in the United States and, through its subsidiary Caesars Interactive Entertainment, Inc., owned and operated (1) an online gaming business providing social and mobile games and regulated online real money gaming and (2) the World Series of Poker ("WSOP") tournaments and brand. |

• | Caesars Entertainment Operating Company, Inc. Owned and operated 19 casinos in the United States and 9 internationally, most of which are located in England. Managed 15 casinos, which includes the 6 Caesars Growth Partners, LLC casinos and 9 casinos for unrelated third parties. Effective October 2014, substantially all our properties are managed by Caesars Enterprise Services, LLC (and the remaining properties will be transitioned upon regulatory approval). |

• | Caesars Enterprise Services, LLC . A joint venture by and among certain of CEC's subsidiaries that manages certain enterprise assets and the other assets it owns, licenses or controls, and employs certain of the corresponding employees and other employees who provided services to CEC and our subsidiaries. |

CEOC Financial Restructuring Plan

As a result of CEOC's highly-leveraged capital structure and the general decline in its gaming results since 2007, on January 15, 2015 , CEOC and certain of its U.S. subsidiaries voluntarily filed for reorganization under Chapter 11 of the United States Bankruptcy Code (the "Bankruptcy Code") in the United States Bankruptcy Court for the Northern District of Illinois in Chicago (the "Bankruptcy Court"). Because CEOC is under the control of the Bankruptcy Court, CEC deconsolidated this subsidiary effective January 15, 2015 . As illustrated in Item 2, " Properties ," CEOC's casinos account for approximately two million square feet of gaming space, 40,000 slot machines, and 15,000 hotel rooms (see Note 23 , " Subsequent Events - CEOC Bankruptcy and Deconsolidation ").

1

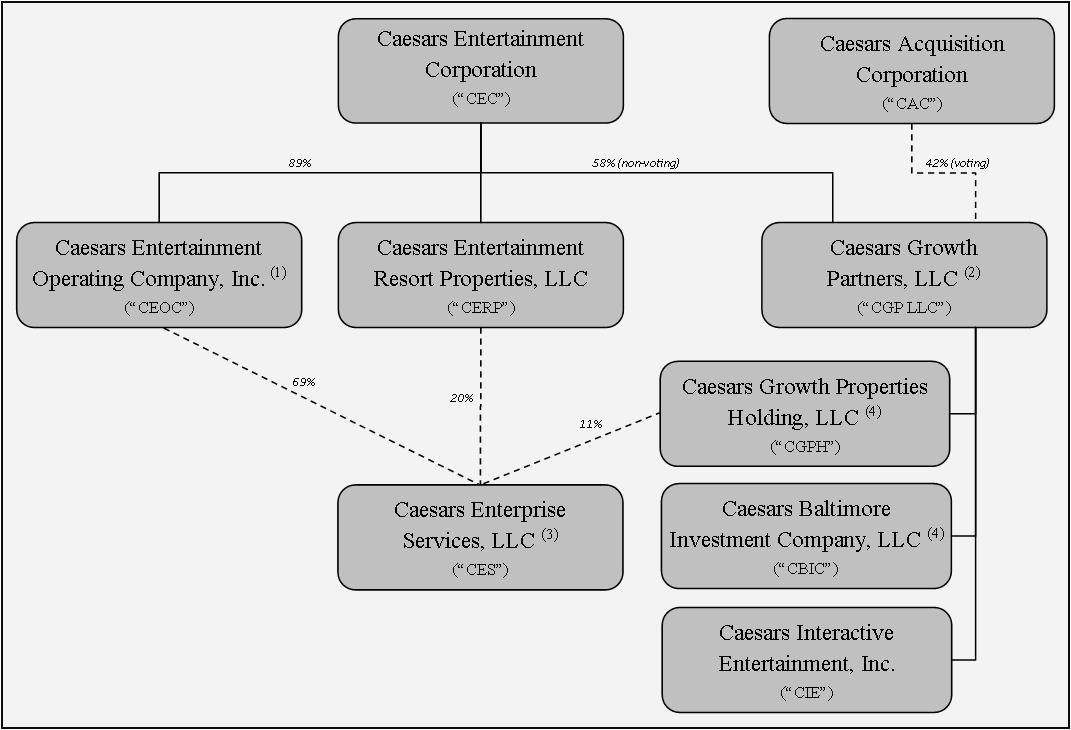

Caesars Entertainment Organizational Structure

The following diagram illustrates the key entities and subsidiaries in the Caesars Entertainment organizational structure. This diagram does not include all legal entities and subsidiaries.

____________________

____________________ (1) | On January 15, 2015, CEOC filed for bankruptcy protection under Chapter 11 of the US Bankruptcy Code. See Note 23 , " Subsequent Events - CEOC Bankruptcy and Deconsolidation ." |

(2) | CAC is party to the series of transactions that formed CGP LLC, and owns 100% of the voting membership units in CGP LLC. CEC owns 100% of the non-voting membership units in CGP LLC and consolidates CGP LLC as a variable interest entity. See Note 2 , " Basis of Presentation and Principles of Consolidation ." See information about CEC's announced merger with CAC in Note 1 , " Description of Business ." |

(3) | CES is a services joint venture formed by CEOC, CERP, and CGPH. See Note 2 , " Basis of Presentation and Principles of Consolidation ." |

(4) | CGPH and CBIC and their subsidiaries together represent the primary operations of Caesars Growth Partners Casino Properties and Developments ("CGP LLC Casinos"). |

Reportable Segments

We view each casino property and CIE as operating segments and aggregate all such casino properties and CIE into the following reportable segments as of December 31, 2014 based on management's view of these properties, which aligns with their ownership and underlying credit structures:

• | Caesars Entertainment Operating Company |

• | Caesars Entertainment Resort Properties |

• | Caesars Growth Partners Casino Properties and Developments |

• Caesars Interactive Entertainment

CGP LLC Casinos is comprised of all subsidiaries of CGP LLC excluding CIE. CIE is comprised of the subsidiaries that operate CGP LLC's social and mobile gaming operations and WSOP.

2

We revised our presentation from one reportable segment to the four listed above effective October 1, 2014, in conjunction with CES' commencing of operations, as the way in which CEC management assesses results and allocates resources was realigned in accordance with these segments.

Business Operations

All of our segments are generally composed of five distinct, but complementary businesses that reinforce, cross-promote, and build upon each other: casino entertainment, food and beverage, rooms and hotel, casino management, and other business operations.

Casino Entertainment Operations

Our casino entertainment operations include revenues from over 55,000 slot machines and 3,600 table games, as well as other games such as keno, poker, and race and sports books that comprised approximately 64% of our total net revenues in 2014 . Slot revenues generate the majority of our gaming revenue and are a key driver of revenue, particularly in our properties located outside of the Las Vegas and Atlantic City markets. During 2014, we opened or redeveloped three casino properties:

The Cromwell. The Cromwell's gaming floor opened in April 2014, featuring 450 slot machines and 60 table games. Its 188 hotel rooms became available to guests starting in May 2014. It features luxurious accommodations in an intimate, Parisian-inspired atmosphere where each room gives guests a VIP experience. The hotel's blend of modern and vintage design is another unique element.

Horseshoe Baltimore. Horseshoe Baltimore's 122,000 square feet of casino space opened in August 2014, featuring over 2,500 slot machines, including 150 video poker machines; as well as a 25-table WSOP Poker Room; over 150 table games; and an exclusive high-limit gambling area.

The LINQ Hotel & Casino ("The LINQ Hotel"). The LINQ Hotel is a complete re-imagination of the former Quad Hotel & Casino featuring over 2,200 newly renovated rooms and suites and unique gambling experiences, including high-energy gaming pits; over 750 slot machines; and a sports book with stadium seating, more than 230 individual televisions, and 12 big screens.

Food and Beverage Operations

Our food and beverage operations generate revenues primarily from over 180 buffets, restaurants, bars, nightclubs, and lounges located throughout our casinos, as well as banquets and room service, and represented approximately 18% of our total net revenues in 2014 . Many of our properties include several dining options, ranging from upscale dining experiences to moderately-priced restaurants and buffets. We recently opened a number of new food and beverage offerings, including:

Gordon Ramsay Steak. Set within the Paris Las Vegas, the high-energy restaurant offers guests a taste of the exclusive beef aging program created under the direction of Chef Ramsay and his culinary team. The menu selections range from traditional steakhouse fare to Ramsay's signature entrées.

Giada. In the first restaurant from celebrity chef, Giada De Laurentiis, Giada boasts al fresco dining and breathtaking views of the Las Vegas Strip. Located on the second level of The Cromwell, Giada's includes an open and airy kitchen that gives guests the opportunity to watch chefs prepare the specialty pasta of the day, create flatbreads and bake desserts.

Drai's . Operating as two venues in one, Drai's Beach Club - Nightclub offers panoramic partying on The Cromwell's rooftop in a combined space that features 65,000-square-feet and a view of the Las Vegas Strip from 11 stories high. For a daytime experience, the Las Vegas Strip's only rooftop pool deck includes multiple pool areas. After dark, the beach club turns into a lively nighttime destination, where guests can party throughout the entire indoor and outdoor space.

Rooms and Hotel Operations

Rooms and hotel operations revenue comprised approximately 14% of our total net revenues in 2014 and is primarily generated from hotel stays at one of our casino properties and our over 39,000 guest rooms and suites worldwide.

Our properties operate at various price and service points allowing us to host a variety of casino guests, who are visiting our properties for gaming and other casino entertainment options, and non-casino guests, who are visiting our properties for other purposes, such as vacation travel or conventions.

Casino Management Operations

Our casino management operations represented approximately 1% of our consolidated net revenues in 2014 . CEOC earns revenue from fees paid by unrelated third parties for the management of nine casinos and CGP LLC for its six casinos. However,

3

the consolidated results for Caesars Entertainment eliminate all intercompany accounts and transactions, including the management fee revenues recognized by CEOC for the CGP LLC managed properties (see Note 2 , " Basis of Presentation and Principles of Consolidation ").

Effective October 2014, a majority of our properties are managed by CES (with the remaining properties being transitioned in the future). However, the related management fee revenues pass through CES and are ultimately paid to CEOC. Therefore, following the deconsolidation of CEOC described above, we will no longer recognize management fee revenues paid by unrelated third parties, but we will recognize management fee expense incurred for the CGP LLC managed properties.

Other Business Operations

Our other operations include retail and entertainment options within our casino facilities; The LINQ promenade, including the High Roller; social and mobile gaming offerings and WSOP from CIE; and third-party leasing.

We provide a variety of retail and entertainment offerings in our casinos and The LINQ promenade. Our retail stores offer guests a wide range of options from high-end brands and accessories to souvenirs and decorative items. The LINQ promenade is an open-air dining, entertainment, and retail development located between The LINQ Hotel & Casino and the Flamingo Las Vegas. Our entertainment options are diverse and include concerts, comedy shows, and variety acts featuring many well-known artists and entertainers, as well as The High Roller, our 550-foot observation wheel at The LINQ promenade.

CIE owns the WSOP tournaments and brand, and we license trademarks for a variety of products and businesses related to this brand. CIE also operates an online gaming business providing social games on Facebook and other social media websites and mobile application platforms and certain real money games in Nevada and New Jersey; and "play for fun" offerings in other jurisdictions.

Third party lease revenue is derived from retail, dining, and entertainment outlets featured in our casinos and along The LINQ promenade that complement the company-owned operations.

Sales and Marketing

We believe that our North American distribution system of casino entertainment enables us to capture a disproportionate share of our customers' entertainment spending when they travel among markets, which is core to our cross-market strategy. In addition, where we have multiple properties in markets or regions, we believe that we are able to capture more of our customers' gaming dollars than in markets where we have single properties competing individually against outside competition. For instance, in Las Vegas, we believe a high concentration of properties in the center of the Las Vegas Strip generates increased revenues.

We believe our industry-leading customer loyalty program, Total Rewards, in conjunction with this distribution system, allows us to capture a growing share of our customers' entertainment spending and compete more effectively. Total Rewards is structured in tiers, providing customers an incentive to consolidate their entertainment spending at our casinos. We use the Total Rewards system to market promotions and to generate customer play across our network of properties. We believe our collection of distinctly branded properties tied together through Total Rewards enables us to capture a greater share of customer spending than we would otherwise achieve, particularly in Las Vegas.

Total Rewards has over 45 million members. Members earn Reward Credits at all of our casino entertainment facilities located in the United States and Canada for on-property entertainment expenses, including gaming, hotel, dining, and retail shopping. Total Rewards members can redeem Reward Credits for on-property amenities or other off-property items such as merchandise, gift cards, and travel. Members earn status within the Total Rewards program based on their level of engagement with us in a calendar year. Total Rewards tiers are designated as Gold, Platinum, Diamond, or Seven Stars, each with increasing member benefits and privileges.

Separately, members are provided promotional offers and rewards based on their engagement with us, aspects of their casino gaming play, and their preferred spending choices outside of gaming. We also use this information for marketing promotions, including direct mail campaigns, the use of electronic mail, our website, mobile devices, social media, and interactive slot machines. These benefits and communications encourage new customers to join Total Rewards and provide existing customers with incentives to consolidate their entertainment spend at our casinos. Additionally, members can earn Reward Credits through the Total Rewards Visa credit card and can redeem Reward Credits with our many partners, including Starwood Hotels and Resorts and Norwegian Cruise Line.

4

Intellectual Property

The development of intellectual property is part of our overall business strategy. We regard our intellectual property to be an important element of our success. While our business as a whole is not substantially dependent on any one patent, trademark, copyright or combination of several of our intellectual property rights, we seek to establish and maintain our proprietary rights in our business operations and technology through the use of patents, trademarks, copyrights, and trade secret laws. We file applications for and obtain patents, trademarks, and copyrights in the United States and foreign countries where we believe filing for such protection is appropriate, including U.S. and foreign patent applications covering certain proprietary technology of CEOC and CIE. We also seek to maintain our trade secrets and confidential information by nondisclosure policies and through the use of appropriate confidentiality agreements. CEOC's U.S. patents have varying expiration dates, the last of which is 2031.

We have not applied for the registration of all of our patents, trademarks, copyrights, proprietary technology or other intellectual property rights, as the case may be, and may not be successful in obtaining all intellectual property rights for which we have applied. Despite our efforts to protect our proprietary rights, parties may infringe upon our intellectual property and use information that we regard as proprietary and our rights may be invalidated or unenforceable. The laws of some foreign countries do not protect proprietary rights or intellectual property to as great an extent as do the laws of the United States. In addition, others may independently develop substantially equivalent intellectual property.

We own proprietary rights to a number of trademarks that we consider, along with the associated name recognition, to be valuable to our business, including the following:

• | CEOC's marks include Caesars, Harrah's, Horseshoe and Total Rewards; |

• | CERP's marks include Rio, Flamingo and Paris; |

• | CIE's marks include World Series of Poker, Playtika, Slotomania and Bingo Blitz; and |

• | CGP LLC holds a license for the Planet Hollywood mark used in connection with the Planet Hollywood resort and casino in Las Vegas. |

Under the terms of the CES joint venture and the Omnibus License and Enterprise Services Agreement described below, we believe that CEC and its other operating subsidiaries will continue to have access to the services historically provided to us by CEOC and its employees, trademarks, and programs despite the CEOC bankruptcy filing.

Omnibus License and Enterprise Services Agreement

As described in more detail in Note 2 , " Basis of Presentation and Principles of Consolidation ," CEOC, CERP, and CGPH (collectively, the "Members" and each a "Member") entered into an Omnibus License and Enterprise Services Agreement (the "Omnibus Agreement") in May 2014, which granted various licenses to the Members and certain of their affiliates in connection with the implementation of CES. Under the Omnibus Agreement, CEOC, Caesars License Company, LLC ("CLC"), Caesars World, Inc. ("CWI") and certain of our subsidiaries that are the owners of our properties granted CES a non-exclusive, irrevocable, world-wide, royalty-free license in and to all intellectual property owned or used by such licensors, including all intellectual property (a) currently used, or contemplated to be used, in connection with the properties owned by the Members and their respective affiliates, including any and all intellectual property related to the Total Rewards program, and (b) necessary for the provision of services contemplated by the Omnibus Agreement and by the applicable management agreement for any such property (collectively, the "Enterprise Assets"). CERP also granted CES non-exclusive licenses to certain other intellectual property, including intellectual property that is specific to properties controlled by CERP or its subsidiaries.

Competition

Casinos

The casino entertainment business is highly competitive. The industry is comprised of a diverse group of competitors that vary considerably in size and geographic diversity, quality of facilities and amenities available, marketing and growth strategies, and financial condition. In most markets, including Las Vegas and Atlantic City, we compete directly with other casino facilities operating in the immediate and surrounding market areas, while in other markets we face additional competition from nearby markets. Our Las Vegas Strip hotels and casinos also compete, in part, with each other. We also compete with other non-gaming resorts and vacation areas, various other entertainment businesses, and other forms of gaming, such as state lotteries, on-and off-track wagering, and card parlors. Our non-gaming offerings also compete with other retail facilities, amusement attractions, and food and beverage offerings.

5

In recent years, many casino operators, including us, have been reinvesting in existing markets to attract new customers or to gain market share. In addition, there has been a concerted effort to expand existing facilities, develop new facilities, and acquire established facilities in existing markets. These reinvestment and expansion efforts combined with aggressive marketing strategies by us and many of our competitors have resulted in increased competition in many markets in which we compete.

The expansion of casino entertainment into new markets also presents competitive issues for us that have had a negative impact on our financial results. The Atlantic City gaming market, in particular, has seen a decline of nearly 50% compared with 2006 levels, primarily due to the addition of gaming and room capacity associated with the expansion of gaming in Maryland, New York, and Pennsylvania. This has resulted in several casino closings in recent years, including our Showboat Atlantic City casino and three competitor casinos in 2014.

Interactive Entertainment

The social and mobile games industry is intensely competitive and rapidly evolving. Moreover, the casino-themed game segment has become one of the most competitive social and mobile games sectors due to the attractive underlying qualities of the segment, including, among others, high average revenue per user, familiar game mechanics, and longer than average game life spans. CIE faces significant competition in all aspects of this business. Specifically, CIE competes for the leisure time, attention, and discretionary spending of its players with other social and mobile games developers on the basis of a number of factors, including, among others, the quality of player experience, brand awareness, reputation, and access to distribution channels. However, other developers of social and mobile casino-themed games could develop more compelling content that competes with CIE's games and adversely affect CIE's ability to attract and retain players and their entertainment time. These competitors, including companies about whom CIE may not be currently aware, may take advantage of social networks, access to a large user base and their network effects to grow rapidly.

See Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations." See also Exhibit 99.1, "Gaming Overview," to this Form 10-K. In addition, for a summary of key developments in 2014, see " Summary of 2014 Events " in Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations."

Governmental Regulation

The gaming industry is highly regulated, and we must maintain our licenses and pay gaming taxes to continue our operations. Each of our casinos is subject to extensive regulation under the laws, rules, and regulations of the jurisdiction in which it is located. These laws, rules, and regulations generally concern the responsibility, financial stability, and character of the owners, managers, and persons with financial interests in the gaming operations. Violations of laws in one jurisdiction could result in disciplinary action in other jurisdictions. A more detailed description of the regulations to which we are subject is contained in Exhibit 99.1, "Gaming Overview," to this Form 10-K.

Our businesses are subject to various foreign, federal, state, and local laws and regulations, in addition to gaming regulations. These laws and regulations include, but are not limited to, restrictions and conditions concerning alcoholic beverages, smoking, environmental matters, employees, currency transactions, taxation, zoning and building codes, construction, land use, and marketing and advertising. We also deal with significant amounts of cash in our operations and are subject to various reporting and anti-money laundering regulations. Such laws and regulations could change or could be interpreted differently in the future, or new laws and regulations could be enacted. Material changes, new laws or regulations, or material differences in interpretations by courts or governmental authorities could adversely affect our operating results. See Item 1A, "Risk Factors" for additional discussion.

Employee Relations

We have approximately 68,000 employees throughout our organization, of which approximately 34,000 are employees of CEOC. There is a clear relationship between employee engagement and customer service. The more engaged our employees, the more our guests benefit from memorable experiences. Engaging employees is therefore a backbone and a driver of our success. We engage our employees in many ways, including fostering open and constructive dialogue, investing in policies and programs that make us a great, diverse and inclusive place to work, caring for our employees' safety, health and wellness, and providing opportunities for personal growth and development.

Approximately 28,000 of our employees are covered by collective bargaining agreements with certain of our subsidiaries, relating to certain casino, hotel, and restaurant employees, of which approximately 12,000 are employees of CEOC. Most of our employees covered by collective bargaining agreements are employed at properties in Las Vegas and Atlantic City. Our collective bargaining agreements covering most of our unionized work force in Atlantic City expire in 2015. We reached new collective bargaining agreements covering most of our Las Vegas employees in January 2014. In February 2014, we reached agreement with Transport Workers Union Local 721, the union which represents approximately 1,200 employees at the following properties: Paris

6

Las Vegas, Bally's Las Vegas, and Harrah's Las Vegas. The new agreement expires in five years. See Item 1A, "Risk Factors" for additional discussion.

Corporate Citizenship

Our Board of Directors and senior executives are committed to maintaining Caesars' position as an industry leader in the area of corporate social responsibility and sustainability. We maintain an Environmental, Social, and Governance Council to guide our activities and allocate the necessary resources. We establish long-term and annual targets in key areas and, by engaging employees throughout our entire organization, we drive the Company's performance accordingly.

Code of Commitment

Our Code of Commitment is a guiding framework for our approach to responsible and ethical business. First published in 2000, our Code of Commitment is a public pledge to our employees, guests and communities that we will honor the trust they have placed in us. Our Code of Commitment is deeply embedded in our organization's communications and culture and widely displayed in all our properties for our guests and all who visit. We create a dynamic and innovative working culture where individual growth is rewarded, recognized, and celebrated. We also use training events to reinforce our expectations of all employees with regard to ethics, diversity, compliance, and anti-corruption at all levels of the business.

Environmental Stewardship

As part of our Code of Commitment, we accept our duty to help preserve the planet for current and future generations. For the past six years, we have been advancing a strategy to reduce our effect on the environment in our main areas of impact. Our multi-year strategy, CodeGreen, is a structured, data-driven and disciplined program that leverages the passion of our employees and engages our guests and suppliers. Since our baseline year of 2007 through the end of 2013, we reduced our energy consumption by 20%, and greenhouse gas emissions by 24%. We reduced water consumption by 18% between 2008 and 2013, and 35% of our total waste was recycled in 2013. Additionally, all 31 of our properties with hotels in North America have received Green Key certifications with most of these at the four key level.

Caesars Foundation and Community Support

Established in 2002, the Caesars Foundation (the "Foundation") is a private charitable foundation funded by a portion of operating income from resorts owned and operated or managed by Caesars. The Foundation's objective is to strengthen organizations and programs in the communities where our employees and their families live and work, and include our employees in volunteer efforts associated with the causes we support. We have maintained our Foundation commitment each year and since its inception, the Foundation has gifted more than $66 million to help support our local communities. For more information, visit www.caesarsfoundation.com . We encourage our employees to take part in community engagement and in 2013, our volunteers contributed over 164,000 hours in more than 600 volunteering events to support a wide range of social and environmental causes.

Available Information

Our Internet address is www.caesars.com. We make available free of charge, on or through our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (the "SEC"). We also make available through our website all filings of our executive officers and directors on Forms 3, 4, and 5 under Section 16 of the Exchange Act. These filings are also available on the SEC's website at www.sec.gov. Our Code of Business Conduct and Ethics is available on our website under the "Investor Relations" link. We will provide a copy of these documents without charge to any person upon receipt of a written request addressed to Caesars Entertainment Corporation, Attn: Corporate Secretary, One Caesars Palace Drive, Las Vegas, Nevada 89109. Reference in this document to our website address does not constitute incorporation by reference of the information contained on the website.

7

ITEM 1A. Risk Factors

Risk Related to the CEC's Ability to Continue as a Going Concern

Due to uncertainties relating to the Noteholder Disputes, there is substantial doubt regarding CEC's ability to continue as a going concern.

As described more fully in Item 3, "Legal Proceedings" under the heading "Noteholder Disputes," and in Note 22, "Subsequent Events - Other," under the heading "Demands for Payment," we are subject to currently pending or threatened litigation (the "Litigation") and demands for payment by certain creditors asserting CEC is obligated under the former parent guarantee of certain CEOC defaulted debt (the "Demands" and, together with the Litigation, the "Noteholder Disputes"). The Litigation pending against CEOC, and in certain cases against CEC and its other subsidiaries, have been stayed due to the Chapter 11 bankruptcy process, however, certain Litigation and the Demands against CEC are continuing outside of the Chapter 11 bankruptcy process. We believe that the Litigation claims and Demands against CEC are without merit and intend to defend ourselves vigorously. At the present time, we believe it is not probable that a material loss will result from the outcome of these matters. The Noteholder Disputes are in their very preliminary stages and discovery has begun on the Unsecured Note Lawsuits (as defined in Note 15 , " Litigation, Contractual Commitments, and Contingent Liabilities "). We cannot provide assurance as to the outcome of the Noteholder Disputes or of the range of potential losses should the Noteholder Disputes ultimately be resolved against us, due to the inherent uncertainty of litigation and the stage of the related litigation. Should these matters ultimately be resolved through litigation outside of the CEOC Financial Restructuring, and were a court to find in favor of the claimants in any of these Noteholder Disputes, such determination could have a material adverse effect on our business, financial condition, results of operations, and cash flows. Accordingly, we have concluded that the material uncertainty related to certain of the Litigation proceeding against CEC raises substantial doubt about the Company's ability to continue as a going concern.

Risks Related to the Bankruptcy Proceedings

CEOC and a substantial majority of its wholly owned subsidiaries filed voluntary petitions for relief under Chapter 11 of the Bankruptcy Code, and are subject to the risks and uncertainties associated with bankruptcy proceedings.

As a result of CEOC's highly-leveraged capital structure and the general decline in its gaming results since 2007, on January 15, 2015, CEOC and certain of its U.S. subsidiaries (collectively, the "Debtors") voluntarily filed for reorganization under Chapter 11 of the Bankruptcy Code in the Bankruptcy Court. Because CEOC is under the control of the Bankruptcy Court, CEC deconsolidated this subsidiary effective January 15, 2015 (see Note 23 , " Subsequent Events - CEOC Bankruptcy and Deconsolidation ").

We are subject to a number of risks and uncertainties associated with the Chapter 11 proceedings, which may lead to potential adverse effects on our liquidity, results of operations, or business prospects. We cannot assure you of the outcome of the Chapter 11 proceedings. Risks associated with the Chapter 11 proceedings include the following:

• | the ability of the Debtors to continue as a going concern; |

• | the ability of the Debtors to obtain bankruptcy court approval with respect to motions in the Chapter 11 proceedings and the outcomes of bankruptcy court rulings of the proceedings in general; |

• | risks associated with involuntary bankruptcy proceedings filed in the United States Bankruptcy Court for the District of Delaware and now pending in the Bankruptcy Court; |

• | the ability of the Debtors to comply with and to operate under the cash collateral order and any cash management orders entered by the Bankruptcy Court from time to time; |

• | the length of time the Debtors will operate under the Chapter 11 proceedings and their ability to successfully emerge, including with respect to obtaining any necessary regulatory approvals; |

• | the ability of the Debtors to negotiate, confirm and consummate a plan of reorganization with respect to the Chapter 11 proceedings; |

• | the likelihood of Caesars Entertainment losing control over the operation of the Debtors as a result of the restructuring process; |

• | risks associated with third party motions, proceedings and litigation in the Chapter 11 proceedings, which may interfere with the Debtors' plan of reorganization; |

8

• | the ability to maintain sufficient liquidity throughout the Chapter 11 proceedings; |

• | increased costs related to the bankruptcy filing and other litigation; |

• | our ability to manage contracts that are critical to our operation, and to obtain and maintain appropriate credit and other terms with customers, suppliers and service providers; |

• | our ability to attract, retain and motivate key employees; |

• | our ability to fund and execute our business plan; |

• | whether our non-Debtor subsidiaries continue to operate their business in the normal course; |

• | the disposition or resolution of all pre-petition claims against us and the Debtors; and |

• | our ability to maintain existing customers and vendor relationships and expand sales to new customers. |

The Chapter 11 proceedings may disrupt our business and may materially and adversely affect our operations.

We have attempted to minimize the adverse effect of the Debtors' Chapter 11 proceedings on our relationships with our employees, suppliers, customers and other parties. Nonetheless, our relationships with our customers, suppliers, and employees may be adversely impacted by negative publicity or otherwise and our operations could be materially and adversely affected. In addition, the Chapter 11 proceedings could negatively affect our ability to attract new employees and retain existing high performing employees or executives, which could materially and adversely affect our operations.

The Chapter 11 proceedings limit the flexibility of our management team in running the Debtors' business.

While the Debtors' operate their businesses as debtors-in-possession under supervision by the Bankruptcy Court, the Bankruptcy Court approval is required with respect to the Debtors' business, and in some cases certain holders of claims in respect of claims under CEOC's first lien notes and other indebtedness ("Consenting Creditors") who have entered into a Third Amended and Restated Restructuring Support and Forbearance Agreement, dated as of January 14, 2015 (the "RSA") with us and CEOC, prior to engaging in activities or transactions outside the ordinary course of business. Bankruptcy Court approval of non-ordinary course activities entails preparation and filing of appropriate motions with the Bankruptcy Court, negotiation with various parties-in-interest, including any statutory committees appointed in the Chapter 11 proceedings, and one or more hearings. Such committees and parties-in-interest may be heard at any Bankruptcy Court hearing and may raise objections with respect to these motions. This process could delay major transactions and limit the Debtors ability to respond quickly to opportunities and events in the marketplace. Furthermore, in the event the Bankruptcy Court does not approve a proposed activity or transaction, the Debtors could be prevented from engaging in activities and transactions that they believe are beneficial to them.

Additionally, the terms of the interim cash collateral order entered by the Bankruptcy Court will limit the Debtors' ability to undertake certain business initiatives. These limitations may include, among other things, the Debtors' ability to:

• | sell assets outside the normal course of business; |

• | consolidate, merge, sell or otherwise dispose of all or substantially all of the Debtors' assets; |

• | grant liens; |

• | incur debt for borrowed money outside the ordinary course of business; |

• | prepay prepetition obligations; and |

• | finance the Debtors' operations, investments or other capital needs or to engage in other business activities that would be in the Debtors' interests. |

9

The RSA is subject to significant conditions and milestones which may be difficult for us to satisfy.

We, CEOC and the Consenting Creditors entered into the RSA, pursuant to which, among other things, CEOC agreed to file a plan of reorganization in accordance with the terms of the RSA (the "Plan"). While the Consenting Creditors have agreed to vote in favor of the Plan when properly solicited to do so, there are certain material conditions CEOC must satisfy under the RSA, including the timely satisfaction of milestones in the Chapter 11 proceedings such as obtaining orders from the Bankruptcy Court with respect to the use of cash collateral, approval of the disclosure statement and confirmation of the Plan. The Debtors' ability to timely complete such milestones is subject to risks and uncertainties that may be beyond our control. If the Consenting Creditors are not required to vote for the Plan, the Plan may not be confirmed, in which case the Debtors would need to develop an alternative plan of reorganization.

The Debtors may not be able to obtain Bankruptcy Court confirmation of the Plan or may have to modify the terms of the Plan.

Even if approved by each class of holders of claims and interests entitled to vote (a "Voting Class"), the Bankruptcy Court may, as a court of equity, exercise substantial discretion and could choose not to confirm the Plan. Bankruptcy Code Section 1129 requires, among other things, a showing that confirmation of the Plan will not be followed by liquidation or the need for further financial reorganization for the Debtors, and that the value of distributions to dissenting holders of claims and interests will not be less than the value such holders would receive if the Debtors liquidated under Chapter 7 of the Bankruptcy Code. Although we believe that the Plan will satisfy such tests, there can be no assurance that the Bankruptcy Court will reach the same conclusion.

Confirmation of the Plan will also be subject to certain conditions. These conditions may not be met, and there can be no assurance that we and a requisite amount of the Consenting Creditors under the RSA will agree to modify or waive such conditions. Further, changed circumstances may necessitate changes to the Plan. Any such modifications could result in less favorable treatment of any non-accepting class, as well as any classes junior to such non-accepting class, than the treatment that will currently be provided in the Plan in accordance with the RSA. Such less favorable treatment could include a distribution of property (including new securities) to the class affected by the modification of a lesser value than what the RSA contemplates will be provided in the Plan or no distribution of property whatsoever under the Plan. In addition, any changes to the Plan, including any changes that would result in Caesars Entertainment no longer controlling the operations of CEOC, could have an adverse effect on Caesars Entertainment and its remaining operations. Changes to the Plan may also delay the confirmation of the Plan and the Debtors' emergence from bankruptcy.

If the Plan is confirmed, Caesars Entertainment will be required to invest and pay significant amounts of cash in connection with the restructuring of CEOC, which may have a negative impact on Caesars Entertainment's business and operating condition.

If the Bankruptcy Court approves the Plan, in connection with the Debtors' emergence from Chapter 11, Caesars Entertainment will be required to (i) contribute over $400 million to pay a forbearance fee, for general corporate purposes and to fund sources and uses and (ii) purchase up to approximately $1.0 billion of new equity in the restructured Debtors. As a result of these payments and investments, Caesars Entertainment may have less cash available in future periods for investments and operating expenses and, as a result, the confirmation of the Plan and emergence of the Debtors may have a negative impact on Caesars Entertainment's business and operating conditions.

If the Plan is confirmed, Caesars Entertainment will be required to guarantee the lease payments owed by the restructured operating company to the restructured property companies and, if the restructured operating company is unable to or does not pay amounts due under the leases, Caesars Entertainment will be obligated to pay the full amount.

If the Bankruptcy Court approves the Plan, in connection with the Debtors' emergence from Chapter 11, Caesars Entertainment will guarantee the two leases between the restructured operating company ("OpCo") and the restructured property companies ("CPLV PropCo" and "Non-CPLV PropCo", collectively "PropCo"), under which CPLV PropCo and Non-CPLV PropCo will lease properties to OpCo: (1) for the Caesars Palace Las Vegas ("CPLV") property (the "CPLV Lease") and (2) for certain properties currently owned by CEOC other than CPLV (the "Non-CPLV PropCo Lease" and, together with the CPLV Lease, the "Leases"). Under the terms of a proposed management lease support agreement, Caesars Entertainment will guarantee the payment and performance of all monetary obligations of OpCo under the Leases. If OpCo is unable to meet its monetary obligations under the Leases, Caesars Entertainment may be subject to significant obligations, which would have a negative impact on Caesars Entertainment's business and operating conditions.

10

The merger with CAC is subject to various closing conditions, including governmental approvals, and other uncertainties and there can be no assurances as to whether and when it may be completed.

On December 21, 2014, Caesars Entertainment entered into the Merger Agreement with CAC, under which CAC will merge with and into Caesars Entertainment, with Caesars Entertainment continuing as the surviving corporation. The consummation of the merger is subject to a number of closing conditions, many of which are not within Caesars Entertainment's control, and failure to satisfy such conditions may prevent, delay or otherwise materially adversely affect the completion of the transaction. These conditions include, among other things, (a) obtaining any necessary licenses, consents or other approvals, including from gaming authorities, to effect the merger, (b) the Plan having been confirmed by the Bankruptcy Court, (c) minimum cash conditions for each of (i) CGP LLC and its subsidiaries and (ii) Caesars Entertainment and CERP, (d) receipt of certain tax opinions or rulings regarding certain tax aspects of the restructuring of CEOC and (e) a threshold amount of tax costs to Caesars Entertainment related to certain aspects of the restructuring of CEOC. It also is possible that a change, event, fact, effect or circumstance that could lead to a material adverse effect on Caesars Entertainment may occur, which may result in CAC not being obligated to complete the merger. We cannot predict with certainty whether and when any of the required closing conditions will be satisfied or if an uncertainty resulting in a material adverse effect on Caesars Entertainment may arise. If the merger does not receive, or timely receive, the required regulatory approvals and clearances, or if another event occurs delaying or preventing the merger, such delay or failure to complete the merger may cause uncertainty or other negative consequences that may materially and adversely affect Caesars Entertainment's business, financial performance and operating results and the price per share for Caesar Entertainment's common stock.

In the event that the pending merger with CAC is not completed, the trading price of our common stock and our future business and financial results may be negatively impacted.

As noted above, the conditions to the completion of the merger with CAC may not be satisfied, and even if the Plan is confirmed, under certain circumstances the exchange ratio between shares of CAC Class A common stock and CEC common stock may be adjusted or the merger agreement may be terminated. If the merger with CAC is not completed for any reason, we would still be liable for significant transaction costs and the focus of our management would have been diverted from seeking other potential opportunities without realizing any benefits of the completed merger. If we do not complete the merger, certain litigation against us will remain outstanding and not be released. If we do not complete the merger, the price of our common stock may decline significantly from the current market price, which may reflect a market assumption that the merger will be completed.

CEOC may have insufficient liquidity for its business operations during the Chapter 11 proceedings.

Although we believe that CEOC will have sufficient liquidity to operate its businesses during the pendency of the Chapter 11 proceedings, there can be no assurance that the revenue generated by CEOC's business operations and cash made available to CEOC under the cash collateral order or otherwise in its restructuring process will be sufficient to fund its operations, especially as we expect CEOC to incur substantial professional and other fees related to its restructuring. CEOC has not made arrangements for financing in the form of a debtor-in-possession credit facility, or DIP facility. In the event that revenue flows and other available cash are not sufficient to meet CEOC's liquidity requirements, CEOC may be required to seek additional financing. There can be no assurance that such additional financing would be available or, if available, offered on terms that are acceptable. If, for one or more reasons, CEOC is unable to obtain such additional financing, CEOC could be required to seek a sale of the company or certain of its material assets or its businesses and assets may be subject to liquidation under chapter 7 of the Bankruptcy Code, and CEOC may cease to continue as a going concern.

Any plan of reorganization that the Debtors may implement will be based in large part upon assumptions and analyses developed by CEOC. If these assumptions and analyses prove to be incorrect, the Debtors' plan may be unsuccessful in its execution.

Any plan of reorganization that the Debtors may implement could affect both the Debtors' capital structure and the ownership, structure and operation of the Debtors' businesses and will reflect assumptions and analyses based on CEOC's experience and perception of historical trends, current conditions and expected future developments, as well as other factors that CEOC considers appropriate under the circumstances. Whether actual future results and developments will be consistent with CEOC's expectations and assumptions depends on a number of factors, including but not limited to (i) CEOC's ability to substantially change the Debtors' capital structure; (ii) CEOC's ability to restructure the Debtors as a separate operating company and property company, with a real estate investment trust directly or indirectly owning and controlling the property company, (iii) the ability of the Debtors to obtain adequate liquidity and financing sources; (iv) our ability to maintain customers' confidence in our viability as a continuing entity and to attract and retain sufficient business from them; (v) the Debtors' ability to retain key employees; and (vi) the overall strength and stability of general economic conditions in the U.S. and in global markets. The failure of any of these factors could materially adversely affect the successful reorganization of the Debtors' businesses.

11

In addition, any plan of reorganization will rely upon financial projections, including with respect to revenues; earnings before interest, taxes, depreciation and amortization ("EBITDA"), capital expenditures, debt service, and cash flow. Financial forecasts are necessarily speculative, and it is likely that one or more of the assumptions and estimates that are the basis of these financial forecasts will not be accurate. The forecasts for the Debtors will be even more speculative than normal, because they may involve fundamental changes in the nature of the Debtors' capital structure and corporate structure. Accordingly, CEOC expects that its actual financial condition and results of operations will differ, perhaps materially, from what CEOC has anticipated. Consequently, there can be no assurance that the results or developments contemplated by any plan of reorganization implemented by the Debtors will occur or, even if they do occur, that they will have the anticipated effects on the Debtors and their subsidiaries or businesses or operations. The failure of any such results or developments to materialize as anticipated could materially adversely affect the successful execution of any plan of reorganization.

As a result of the Chapter 11 proceedings, our historical financial information will not be indicative of our future financial performance.

Our capital structure and our corporate structure will likely be significantly altered under any plan of reorganization ultimately confirmed by the Bankruptcy Court. As of the Petition Date, CEOC was deconsolidated from our financial statements. Consequently, our results of operations following the deconsolidation will not be comparable to the financial condition and results of operations reflected in our historical financial statements.

Risks Related to our Business

Our substantial indebtedness and the fact that a significant portion of our cash flow is used to make interest payments could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry and prevent us from making debt service payments.

We are a highly-leveraged company, primarily resulting from the leverage of CEOC. We had $25.6 billion in consolidated face value of debt outstanding as of December 31, 2014 , including $18.4 billion outstanding at CEOC, $4.8 billion outstanding at CERP, and $2.4 billion outstanding at CGP LLC. As of December 31, 2014, our consolidated estimated debt service obligation for 2015 is $18.8 billion , consisting of $18.0 billion in principal maturities and $764 million in required interest payments. Of those totals, CEOC's estimated debt service obligation for 2015 is $18.2 billion , consisting of $18.0 billion in principal maturities and $184 million in required interest payments.

Our substantial indebtedness and the restrictive covenants under the agreements governing such indebtedness could:

• | limit our ability to borrow money for our working capital, capital expenditures, development projects, debt service requirements, strategic initiatives or other purposes; |

• | make it more difficult for us to satisfy our obligations with respect to our indebtedness, and any failure to comply with the obligations of any of our debt instruments, including restrictive covenants and borrowing conditions, could result in an event of default under the agreements governing our indebtedness; |

• | require us to dedicate a substantial portion of our cash flow from operations to the payment of interest and repayment of our indebtedness thereby reducing funds available to us for other purposes; |

• | limit our flexibility in planning for, or reacting to, changes in our operations or business; |

• | make us more highly-leveraged than some of our competitors, which may place us at a competitive disadvantage; |

• | make us more vulnerable to downturns in our business or the economy; |

• | restrict us from making strategic acquisitions, developing new gaming facilities, introducing new technologies or exploiting business opportunities; |

• | affect our ability to renew gaming and other licenses; |

• | limit, along with the financial and other restrictive covenants in our indebtedness, among other things, our ability to borrow additional funds or dispose of assets; and |

• | expose us to the risk of increased interest rates as certain of our borrowings are at variable rates of interest. |

Any of the foregoing could have a material adverse effect on our business, financial condition, results of operations, prospects and ability to satisfy our outstanding debt obligations.

12

There is substantial doubt regarding CEOC's ability to continue as a going concern.

We do not currently expect that CEOC's cash flows from operations will be sufficient to repay its indebtedness and, accordingly, CEOC has sought a reorganization under Chapter 11 of the Bankruptcy Code. CEOC's ability to continue as a going concern is contingent upon, among other things, its ability to: (i) develop and successfully implement a restructuring plan within the timeframe of the RSA, (ii) comply with the covenants contained in the cash collateral order, including compliance with the approved budget, and in any post-restructuring financing, (iii) reduce debt and other liabilities through the restructuring process, (iv) return to profitability, (v) generate sufficient cash flow from operations, and (vi) obtain financing sources to meet its future obligations. CEOC's restructuring plan could result in the separation of its business into a separate operating company and a REIT, with the REIT owning substantially all of its real estate assets. We believe the consummation of a successful restructuring is critical to CEOC's continued viability and long-term liquidity. While CEOC is working towards achieving these objectives, there can be no certainty that it will be successful in doing so, and we cannot guarantee that its success or failure will not have an impact on our business.

We may be unable to generate sufficient cash to service all of our indebtedness, and may be forced to take other actions to satisfy our obligations under our indebtedness that may not be successful.

We may be unable to generate sufficient cash flow from operations, or unable to draw under our senior secured credit facilities or otherwise, in an amount sufficient to fund our liquidity needs. Our operating cash inflows are typically used for operating expenses, debt service costs, working capital needs, and capital expenditures in the normal course of business. Our operating cash flows are consumed by our cash interest payments, which totaled $2.1 billion in 2014. We experienced negative operating cash flows of $735 million in 2014, and we also expect to experience negative operating cash flows in 2015.

We may incur significantly more debt, which could adversely affect our ability to pursue certain opportunities.

We and our subsidiaries may be able to incur substantial indebtedness at any time, and from time to time, including in the near future. Although the terms of the agreements governing our indebtedness contain restrictions on our ability to incur additional indebtedness, these restrictions are subject to a number of important qualifications and exceptions, and the indebtedness incurred in compliance with these restrictions could be substantial.

For example, as of December 31, 2014, CERP had $90 million of additional borrowing capacity available under its revolving credit facility. CGP LLC had $150 million of additional borrowing capacity available under its revolving credit facility. None of our existing indebtedness limits the amount of debt that may be incurred by Caesars Entertainment.

Our subsidiary debt agreements allow for one or more future issuances of additional secured notes or loans, which may include, in each case, indebtedness secured on a pari passu basis with the obligations under CGP LLC or CERP's credit facilities and first lien notes. This indebtedness could be used for a variety of purposes, including financing capital expenditures, refinancing or repurchasing our outstanding indebtedness, including existing unsecured indebtedness, or for general corporate purposes. We have raised and expect to continue to raise debt, including secured debt, to directly or indirectly refinance our outstanding unsecured debt on an opportunistic basis, as well as development and acquisition opportunities.

Our debt agreements contain restrictions that limit our flexibility in operating our business.

Our debt agreements contain, and any future indebtedness of ours would likely contain, a number of covenants that impose significant operating and financial restrictions, including restrictions on the issuer of the debt's ability to, among other things:

• | incur additional debt or issue certain preferred shares; |

• | pay dividends on or make distributions in respect of our capital stock or make other restricted payments; |

• | make certain investments; |

• | sell certain assets; |

• | create liens on certain assets; |

• | consolidate, merge, sell or otherwise dispose of all or substantially all of our assets; |

• | enter into certain transactions with our affiliates; and |

• | designate our subsidiaries as unrestricted subsidiaries. |

13

As a result of these covenants, we are limited in the manner in which we conduct our business, and we may be unable to engage in favorable business activities or finance future operations or capital needs.

We have pledged and will pledge a significant portion of our assets as collateral under our subsidiaries' debt agreements. If any of our lenders accelerate the repayment of borrowings, there can be no assurance that we will have sufficient assets to repay our indebtedness.

We are required to satisfy and maintain specified financial ratios under our debt agreements. See Note 10 , " Debt ," for further information. Our ability to meet the financial ratios under our debt agreements can be affected by events beyond our control, and there can be no assurance that we will be able to continue to meet those ratios.

A failure to comply with the covenants contained in our indebtedness could result in an event of default under the facilities or the existing agreements, which, if not cured or waived, could have a material adverse effect on our business, financial condition and results of operations. In the event of any default under the indebtedness of CERP or CGP LLC, the lenders thereunder:

• | will not be required to lend any additional amounts to such borrowers; |

• | could elect to declare all borrowings outstanding, together with accrued and unpaid interest and fees, to be due and payable and terminate all commitments to extend further credit; or |

• | require such borrowers to apply all of our available cash to repay these borrowings. |

Such actions by the lenders under CERP's or CGP LLC's indebtedness could cause cross defaults under the other indebtedness of CERP and CGP LLC, respectively. For instance, if CERP were unable to repay those amounts, the lenders under CERP's credit facilities and the holders of CERP's secured notes could proceed against the collateral granted to them to secure that indebtedness.

If the indebtedness under CERP's or CGP LLC's credit facilities, or other indebtedness were to be accelerated, there can be no assurance that their assets would be sufficient to repay such indebtedness in full.

Repayment of our subsidiaries' debt is dependent on cash flow generated by our subsidiaries.

Our subsidiaries currently own a significant portion of our assets and conduct a significant portion of our operations. Accordingly, repayment of our subsidiaries' indebtedness is dependent, to a significant extent, on the generation of cash flow by our subsidiaries and their ability to make such cash available by dividend, debt repayment or otherwise. Our subsidiaries do not have any obligation to pay amounts due on our other subsidiaries' indebtedness or to make funds available for that purpose. Our subsidiaries may not be able to, or may not be permitted to, make distributions to enable us to make payments in respect of our other subsidiaries' indebtedness. Each subsidiary is a distinct legal entity and, under certain circumstances, legal and contractual restrictions may limit our ability to obtain cash from our subsidiaries.

We are or may become involved in legal proceedings that, if adversely adjudicated or settled, could have a material adverse effect on our business, financial condition, results of operations, and prospects.

During the second half of 2014, CAC, CGP LLC, Caesars Entertainment, CEOC and CERP received letters from unnamed parties who purport to hold debt issued by CEOC objecting to various transactions undertaken by CEOC and its affiliated entities in 2013 and 2014. In addition, as described in Item 3, "Legal Proceedings," Caesars Entertainment and CEOC were served with the Second Lien Lawsuit, the Unsecured Note Lawsuits, and the First Lien Lawsuit; Caesars Entertainment and CAC were served with the Merger Lawsuit; and Caesars Entertainment was sued in the BOKF Lawsuit. CEOC has also received purported notices of default with respect to certain of its outstanding indebtedness. Although these proceedings pending against CEOC, and in certain cases against CEC and its subsidiaries, have been stayed due to the Chapter 11 bankruptcy process, certain litigation and demands against CEC are continuing outside the Chapter 11 bankruptcy process. If a court were to find in favor of the claimants in any of these disputes, such determination could have a material adverse effect on our business, financial condition, results of operations, and prospects and on the ability of lenders and noteholders to recover on claims under our indebtedness.

As well, from time to time, we are defendants in various lawsuits or other legal proceedings relating to matters incidental to our business. The nature of our business subjects us to the risk of lawsuits filed by customers, past and present employees, competitors, business partners, Indian tribes and others in the ordinary course of business. As with all legal proceedings, no assurance can be provided as to the outcome of these matters and in general, legal proceedings can be expensive and time consuming. For example, we may have potential liability arising from a class action lawsuit against Hilton Hotels Corporation relating to employee benefit obligations. We may not be successful in the defense or prosecution of these lawsuits, which could result in settlements or damages that could significantly impact our business, financial condition and results of operations.

14

The loss of the services of key personnel could have a material adverse effect on our business.

The leadership of our chief executive officer and other executive officers has been a critical element of our success. Our chief executive officer is in the process of transitioning his role to a new chief executive officer. Any unforeseen loss of a chief executive officer's services, or any negative market or industry perception with respect to him or arising from his loss, could have a material adverse effect on our businesses. Our other executive officers and other members of senior management have substantial experience and expertise in our businesses that we believe will make significant contributions to our growth and success. The unexpected loss of services of one or more of these individuals could also adversely affect us. We do not have key man or similar life insurance policies covering members of our senior management. We have employment agreements with our executive officers, but these agreements do not guarantee that any given executive will remain with us, and there can be no assurance that any such officers will remain with us.

If we cannot attract, retain and motivate employees, we may be unable to compete effectively, and lose the ability to improve and expand our businesses.

Our success and ability to grow depend, in part, on our ability to hire, retain, and motivate sufficient numbers of talented people with the increasingly diverse skills needed to serve clients and expand our business, in many locations around the world. We face intense competition for highly qualified, specialized technical, managerial, and consulting personnel. Recruiting, training, retention and benefit costs place significant demands on our resources. Additionally, our substantial indebtedness and the recent downturn in the gaming, travel and leisure sectors have made recruiting executives to our businesses more difficult, which may become even more difficult as a result of the Debtors' Chapter 11 proceedings. The inability to attract qualified employees in sufficient numbers to meet particular demands or the loss of a significant number of our employees could have an adverse effect on us.

We may sell or divest different properties or assets as a result of our evaluation of our portfolio of businesses. Such sales or divestitures could affect our costs, revenues, profitability and financial position.

From time to time, we evaluate our properties and our portfolio of businesses and may, as a result, sell or attempt to sell, divest or spin-off different properties or assets. For example, in June 2014 and August 2014, we closed Harrah's Tunica and Showboat Atlantic City, respectively. In addition, in May 2014, CGP LLC (or one or more of its designated direct or indirect subsidiaries) acquired from CEOC (or one or more of its affiliates) The Cromwell (f/k/a Bill's Gamblin' Hall & Saloon), The LINQ Hotel & Casino (f/k/a The Quad Resort & Casino), Bally's Las Vegas and Harrah's New Orleans as well as a financial stake in the management fee stream for all of those properties.

These sales or divestitures affect our costs, revenues, profitability, financial position, liquidity and our ability to comply with our debt covenants. Divestitures have inherent risks, including possible delays in closing transactions (including potential difficulties in obtaining regulatory approvals), the risk of lower-than-expected sales proceeds for the divested businesses, and potential post-closing claims for indemnification. In addition, current economic conditions and relatively illiquid real estate markets may result in fewer potential bidders and unsuccessful sales efforts. Expected costs savings, which are offset by revenue losses from divested properties, may also be difficult to achieve or maximize due to our fixed cost structure.

15

Reduction in discretionary consumer spending resulting from the downturn in the national economy over the past few years, the volatility and disruption of the capital and credit markets, adverse changes in the global economy and other factors could negatively impact our financial performance and our ability to access financing.

Changes in discretionary consumer spending or consumer preferences are driven by factors beyond our control, such as perceived or actual general economic conditions; high energy, fuel and other commodity costs; the cost of travel; the potential for bank failures; a soft job market; an actual or perceived decrease in disposable consumer income and wealth; the recent increase in payroll taxes; increases in gaming taxes or fees; fears of recession and changes in consumer confidence in the economy; and terrorist attacks or other global events. Our business is particularly susceptible to any such changes because our casino properties offer a highly discretionary set of entertainment and leisure activities and amenities. Gaming and other leisure activities we offer represent discretionary expenditures and participation in such activities may decline if discretionary consumer spending declines, including during economic downturns, during which consumers generally earn less disposable income. The economic downturn that began in 2008 and adverse conditions in the local, regional, national and global markets have negatively affected our business and results of operations and may continue to negatively affect our operations in the future. In addition, the Atlantic City gaming market in particular has seen a massive decline. For example, according to the UNLV Center for Gaming Research, reported gaming revenues for Atlantic City properties have declined from $5.2 billion in 2006 to $2.7 billion in 2014 . During periods of economic contraction, our revenues may decrease while most of our costs remain fixed and some costs even increase, resulting in decreased earnings. While economic conditions have improved, our revenues may continue to decrease. For example, while the gaming industry has partially recovered from 2006, there are no assurances that the gaming industry will continue to grow as a result of economic downturn or other factors. Any decrease in the gaming industry could adversely affect consumer spending and adversely affect our operations.

Additionally, key determinants of our revenues and operating performance include hotel average daily rate ("ADR"), number of gaming trips and average spend per trip by our customers. Given that 2007 was the peak year for our financial performance and the gaming industry in the United States in general, we may not attain those financial levels in the near term, or at all. If we fail to increase ADR or any other similar metric in the near term, our revenues may not increase and, as a result, we may not be able to pay down our existing debt, fund our operations, fund planned capital expenditures or achieve expected growth rates, all of which could have a material adverse effect on our business, financial condition, results of operations and cash flow. Even an uncertain economic outlook may adversely affect consumer spending in our gaming operations and related facilities, as consumers spend less in anticipation of a potential economic downturn. Furthermore, other uncertainties, including national and global economic conditions, terrorist attacks or other global events, could adversely affect consumer spending and adversely affect our operations.

Growth in consumer demand for non-gaming offerings could negatively impact our gaming revenue.