UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One) | ||

[X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the fiscal year ended December 31, 2009 | ||

or | ||

[ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

For the Transition Period From to

Commission File Number: 001-33664

Charter Communications, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 43-1857213 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

12405 Powerscourt Drive | ||

St. Louis, Missouri 63131 | (314) 965-0555 | |

(Address of principal executive offices including zip code) | (Registrant's telephone number, including area code) |

Securities registered pursuant to section 12(b) of the Act: None

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "accelerated filer," "large accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer o Non-accelerated filer ☑ Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ☑

The aggregate market value of the registrant of outstanding Class A common stock held by non-affiliates of the registrant at June 30, 2009 was approximately $8 million, computed based on the closing sale price as quoted on the OTC Bulletin Board on that date. For purposes of this calculation only, directors, executive officers and the principal controlling shareholder or entities controlled by such controlling shareholder of the registrant are deemed to be affiliates of the registrant.

APPLICABLE ONLY TO REGISTRANTS INVOLVED IN BANKRUPTCY

PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☑ No o

There were 112,593,860 shares of Class A common stock outstanding as of January 31, 2010. There were 2,241,299 shares of Class B common stock outstanding as of the same date.

Documents Incorporated By Reference

The following documents are incorporated into this Annual Report by reference: None

CHARTER COMMUNICATIONS, INC.

| Page No. | |||

PART I | ||||

Item 1 | Business | 1 | ||

Item 1A | Risk Factors | 16 | ||

Item 1B | Unresolved Staff Comments | 27 | ||

Item 2 | Properties | 27 | ||

Item 3 | Legal Proceedings | 27 | ||

Item 4 | Submission of Matters to a Vote of Security Holders | 30 | ||

PART II | ||||

Item 5 | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 31 | ||

Item 6 | Selected Financial Data | 33 | ||

Item 7 | Management's Discussion and Analysis of Financial Condition and Results of Operations | 34 | ||

Item 7A | Quantitative and Qualitative Disclosure About Market Risk | 58 | ||

Item 8 | Financial Statements and Supplementary Data | 59 | ||

Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 59 | ||

Item 9A | Controls and Procedures | 59 | ||

Item 9B | Other Information | 60 | ||

PART III | ||||

Item 10 | Directors, Executive Officers and Corporate Governance | 61 | ||

Item 11 | Executive Compensation | 66 | ||

Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 87 | ||

Item 13 | Certain Relationships and Related Transactions, and Director Independence | 91 | ||

Item 14 | Principal Accounting Fees and Services | 95 | ||

PART IV | ||||

Item 15 | Exhibits and Financial Statement Schedules | 96 | ||

Signatures | S-1 | |||

Exhibit Index | E-1 | |||

This Annual Report on Form 10-K is for the year ended December 31, 2009. The Securities and Exchange Commission ("SEC") allows us to "incorporate by reference" information that we file with the SEC, which means that we can disclose important information to you by referring you directly to those documents. Information incorporated by reference is considered to be part of this Annual Report. In addition, information that we file with the SEC in the future will automatically update and supersede information contained in this Annual Report. In this annual report, "we," "us" and "our" refer to Charter Communications, Inc., Charter Communications Holding Company, LLC and their subsidiaries.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), regarding, among other things, our plans, strategies and prospects, both business and financial, including, without limitation, the forward-looking statements set forth in Part I. Item 1. and in Part II. Item 7. under the heading "Management's Discussion and Analysis of Financial Condition and Results of Operations" in this annual report. Although we believe that our plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, we cannot assure you that we will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions, including, without limitation, the factors described in Part I. Item 1A. under the heading "Risk Factors" and in Part II. Item 7. under the heading, "Management's Discussion and Analysis of Financial Condition and Results of Operations" in this annual report. Many of the forward-looking statements contained in this annual report may be identified by the use of forward-looking words such as "believe," "expect," "anticipate," "should," "planned," "will," "may," "intend," "estimated," "aim," "on track," "target," "opportunity" and "potential," among others. Important factors that could cause actual results to differ materially from the forward-looking statements we make in this annual report are set forth in this annual report and in other reports or documents that we file from time to time with the SEC, and include, but are not limited to:

· | our ability to sustain and grow revenues and cash flows from operating activities by offering video, high-speed Internet, telephone and other services to residential and commercial customers, and to maintain and grow our customer base, particularly in the face of increasingly aggressive competition and the difficult economic conditions in the United States; |

· | the impact of competition from other distributors, including but not limited to incumbent telephone companies, direct broadcast satellite operators, wireless broadband providers, and digital subscriber line ("DSL") providers and competition from video provided over the Internet; |

· | general business conditions, economic uncertainty or downturn and the significant downturn in the housing sector and overall economy; |

· | our ability to obtain programming at reasonable prices or to raise prices to offset, in whole or in part, the effects of higher programming costs (including retransmission consents); |

· | our ability to adequately deliver customer service; |

· | the effects of governmental regulation on our business; |

· | the availability and access, in general, of funds to meet our debt obligations, prior to or when they become due, and to fund our operations and necessary capital expenditures, either through (i) cash on hand, (ii) cash flows from operating activities, (iii) access to the capital or credit markets including through new issuances, exchange offers or otherwise, especially given recent volatility and disruption in the capital and credit markets, or (iv) other sources and our ability to fund debt obligations (by dividend, investment or otherwise) to the applicable obligor of such debt; and |

· | our ability to comply with all covenants in our indentures and credit facilities, any violation of which, if not cured in a timely manner, could trigger a default of our other obligations under cross-default provisions. |

All forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by this cautionary statement. We are under no duty or obligation to update any of the forward-looking statements after the date of this annual report.

ii

PART I

Item 1. Business.

Introduction

Charter Communications, Inc. ("Charter") is among the largest providers of cable services in the United States, offering a variety of entertainment, information and communications solutions to residential and commercial customers in 27 states. Charter operates in a heavily regulated industry pursuant to various franchises from local and state governments and licenses granted by state and federal governments including the Federal Communications Commission (the "FCC"). Our infrastructure consists of a hybrid of fiber and coaxial cable plant passing approximately 11.9 million homes, through which we offer our residential and commercial customers traditional video cable programming, high-speed Internet access, advanced broadband cable services (such as high definition television, OnDemand™ ("OnDemand") video programming and digital video recorder ("DVR") service) and telephone service. See "Item 1. Business - Products and Services" for further description of these terms and services, including "customers."

As of December 31, 2009, we served approximately 5.3 million customers. We served approximately 4.8 million video customers, of which approximately 67% were digital video customers. We also served approximately 3.1 million high-speed Internet customers and we provided telephone service to approximately 1.6 million customers. We sell our cable video programming, high-speed Internet and telephone services primarily on a subscription basis, often in a bundle of two or more services, providing savings and convenience to our customers. Approximately 57% of our customers subscribe to a bundle of services.

Through Charter Business®, we provide scalable, tailored broadband communications solutions to business organizations, such as business-to-business Internet access, data networking, fiber connectivity to cellular towers, video and music entertainment services and business telephone. As of December 31, 2009, we served approximately 224,300 business customers, including small- and medium-sized commercial customers.

Charter is a holding company whose principal asset is a controlling common equity interest in Charter Communications Holding Company, LLC ("Charter Holdco"). Charter Holdco is the sole owner of our subsidiaries where the underlying operations reside, which are collectively referred to herein as the "Company." All significant intercompany accounts and transactions among consolidated entities have been eliminated.

We have a history of net losses. Our net losses were principally attributable to insufficient revenue to cover the combination of operating expenses and interest expenses we incurred because of our debt, impairment of franchises and depreciation expenses resulting from the capital investments we have made and continue to make in our cable properties. As discussed below, we emerged from bankruptcy protection on November 30, 2009 and reduced our debt by approximately $8 billion, reducing our interest expense by approximately $830 million annually.

Our principal executive offices are located at Charter Plaza, 12405 Powerscourt Drive, St. Louis, Missouri 63131. Our telephone number is (314) 965-0555, and we have a website accessible at www.charter.com. Since January 1, 2002, our annual reports, quarterly reports and current reports on Form 8-K, and all amendments thereto, have been made available on our website free of charge as soon as reasonably practicable after they have been filed. The information posted on our website is not incorporated into this annual report.

Bankruptcy Proceedings and Recent Events

On March 27, 2009, we and certain affiliates (collectively, the "Debtors") filed voluntary petitions in the United States Bankruptcy Court for the Southern District of New York (the "Bankruptcy Court"), to reorganize under Chapter 11 of the United States Bankruptcy Code (the "Bankruptcy Code"). The Chapter 11 cases were jointly administered under the caption In re Charter Communications, Inc., et al. , Case No. 09-11435. On May 7, 2009, we filed a Joint Plan of Reorganization (the "Plan") and a related disclosure statement (the "Disclosure Statement") with the Bankruptcy Court. The Plan was confirmed by order of the Bankruptcy Court on November 17, 2009 ("Confirmation Order"), and became effective on November 30, 2009 (the "Effective Date"), the date on which we emerged from protection under Chapter 11 of the Bankruptcy Code.

As provided in the Plan and the Confirmation Order, (i) the notes and bank debt of Charter Communications Operating, LLC ("Charter Operating") and CCO Holdings, LLC ("CCO Holdings") remained outstanding; (ii) holders of approximately $1.5 billion of notes issued by CCH II, LLC ("CCH II") received new CCH II notes (the

1

"Notes Exchange"); (iii) holders of notes issued by CCH I, LLC ("CCH I") received 21.1 million shares of new Charter Class A common stock; (iv) holders of notes issued by CCH I Holdings, LLC ("CIH") received 6.4 million warrants to purchase shares of new Charter Class A common stock with an exercise price of $46.86 per share that expire five years from the date of issuance; (v) holders of notes issued by Charter Communications Holdings, LLC ("Charter Holdings") received 1.3 million warrants to purchase shares of new Charter Class A common stock with an exercise price of $51.28 per share that expire five years from the date of issuance; (vi) holders of convertible notes issued by Charter received $25 million and 5.5 million shares of preferred stock issued by Charter; and (vii) all previously outstanding shares of Charter Class A and Class B common stock were cancelled. In addition, as part of the Plan, the holders of CCH I notes received and transferred to Mr. Paul G. Allen, Charter's principal stockholder, $85 million of new CCH II notes.

The consummation of the Plan was funded with cash on hand, the Notes Exchange, and net proceeds of approximately $1.6 billion of an equity rights offering (the "Rights Offering") in which holders of CCH I notes purchased new Charter Class A common stock.

In connection with the Plan, Charter, Mr. Allen and Charter Investment, Inc. ("CII") entered into a separate restructuring agreement (as amended, the "Allen Agreement"), in settlement and compromise of their legal, contractual and equitable rights, claims and remedies against Charter and its subsidiaries In addition to any amounts received by virtue of CII's holding other claims against Charter and its subsidiaries, on the Effective Date, CII was issued 2.2 million shares of the new Charter Class B common stock equal to 2% of the equity value of Charter, after giving effect to the Rights Offering, but prior to issuance of warrants and equity-based awards provided for by the Plan and 35% (determined on a fully diluted basis) of the total voting power of all new capital stock of Charter. Each share of new Charter Class B common stock is convertible, at the option of the holder, into one share of new Charter Class A common stock, and is subject to significant restrictions on transfer and conversion. Certain holders of new Charter Class A common stock (and securities convertible into or exercisable or exchangeable therefore) and new Charter Class B common stock received certain customary registration rights with respect to their shares. On the Effective Date, CII received: (i) 4.7 million warrants to purchase shares of new Charter Class A common stock, (ii) $85 million principal amount of new CCH II notes (transferred from CCH I noteholders), (iii) $25 million in cash for amounts previously owed to CII under a management agreement, (iv) $20 million in cash for reimbursement of fees and expenses in connection with the Plan, and (v) an additional $150 million in cash. The warrants described above have an exercise price of $19.80 per share and expire seven years after the date of issuance. In addition, on the Effective Date, CII retained a minority equity interest in reorganized Charter Holdco of 1% and a right to exchange such interest into new Charter Class A common stock. On December 28, 2009, CII exchanged 81% of its interest in Charter Holdco, and on February 8, 2010 the remaining interest was exchanged after which Charter Holdco became 100% owned by Charter. Further, Mr. Allen transferred his preferred equity interest in CC VIII, LLC ("CC VIII") to Charter. Mr. Allen has the right to elect up to four of Charter's eleven board members.

On January 22, 2010, we announced that our President and Chief Executive Officer, Neil Smit, would resign effective February 28, 2010 and our Chief Operating Officer, Michael J. Lovett, would assume the additional title of Interim President and Chief Executive Officer at that time.

The terms "Charter," "we," "our" and "us," when used in this report with respect to the period prior to Charter's emergence from bankruptcy, are references to the Debtors ("Predecessor") and, when used with respect to the period commencing after Charter's emergence, are references to Charter ("Successor"). These references include the subsidiaries of Predecessor or Successor, as the case may be, unless otherwise indicated or the context requires otherwise.

2

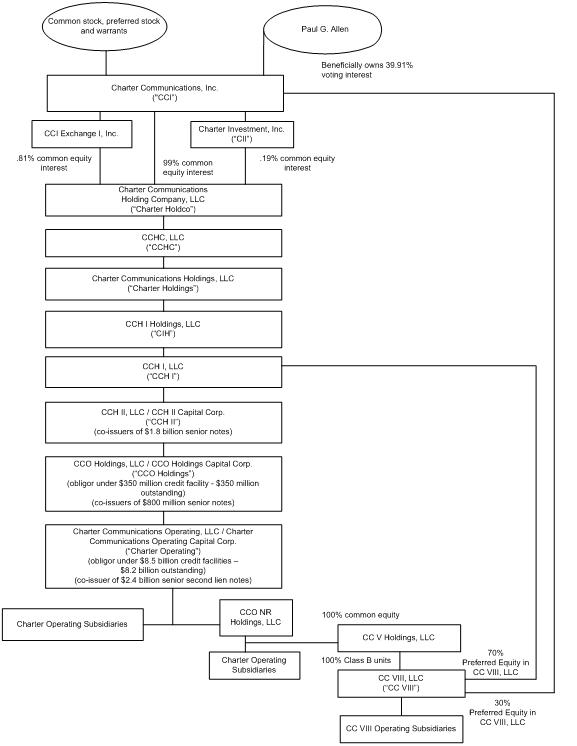

The chart below sets forth our entity structure and that of our direct and indirect subsidiaries. This chart does not include all of our affiliates and subsidiaries and, in some cases, we have combined separate entities for presentation purposes. The equity ownership and voting percentages shown below are approximations as of February 15, 2010, and do not give effect to any exercise of then outstanding warrants. Indebtedness amounts shown below are principal amounts as of December 31, 2009. See Note 8 to the accompanying consolidated financial statements contained in "Item 8. Financial Statements and Supplementary Data," which also includes the accreted values of the indebtedness described below.

3

Charter Communications, Inc. Charter owns 100% of Charter Holdco. Charter Holdco, through its subsidiaries, owns cable systems and certain strategic investments. As sole manager under applicable operating agreements, Charter controls the affairs of Charter Holdco and its limited liability company subsidiaries. In addition, Charter provides management services to Charter Holdco and its subsidiaries under a management services agreement.

Charter Communications Holding Company, LLC. Charter Holdco, a Delaware limited liability company formed on May 25, 1999, is the indirect 100% parent of Charter's subsidiaries including debt issuers and operating subsidiaries. At December 31, 2009, the common membership units of Charter Holdco were owned approximately 99.81% by Charter and 0.19% by CII. All of the outstanding common membership units in Charter Holdco, that were held by CII at December 31, 2009, were controlled by Mr. Allen and were exchangeable at any time for shares of new Charter Class A common stock. On February 8, 2010, Mr. Allen exercised his remaining right to exchange Charter Holdco units for shares of Class A common stock after which Charter Holdco became 100% owned by Charter.

Interim Holding Company Debt Issuers. As indicated in the organizational chart above, our interim holding company debt issuers indirectly own the subsidiaries that own or operate all of our cable systems, subject to a CC VIII minority interest held by CCH I as described below. For a description of the debt issued by these issuers please see "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations - Description of Our Outstanding Debt."

Preferred Equity in CC VIII. At December 31, 2009, Charter owned 30% of the CC VIII preferred membership interests. CCH I, a direct subsidiary of CIH and indirect subsidiary of Charter, directly owned the remaining 70% of these preferred interests. The common membership interests in CC VIII are indirectly owned by Charter Operating. See Note 11 to our accompanying consolidated financial statements contained in "Item 8. Financial Statements and Supplementary Data."

Products and Services

Through our hybrid fiber and coaxial cable network, we offer our customers traditional cable video services (basic and digital, which we refer to as "video" services), high-speed Internet services, and telephone services, as well as advanced broadband services (such as OnDemand, high definition television, and DVR service). Our telephone services are primarily provided using voice over Internet protocol ("VoIP") technology, to transmit digital voice signals over our systems. Our video, high-speed Internet, and telephone services are offered to residential and commercial customers on a subscription basis, with prices and related charges that vary primarily based on the types of service selected, whether the services are sold as a "bundle" or on an individual basis, and the equipment necessary to receive the services, with some variation in prices.

The following table approximates our customer statistics for video, residential high-speed Internet and telephone as of December 31, 2009 and 2008.

Approximate as of | ||||||||

December 31, | December 31, | |||||||

2009 (a) | 2008 (a) | |||||||

Residential (non-bulk) basic video customers (b) | 4,562,900 | 4,779,000 | ||||||

Multi-dwelling (bulk) and commercial unit customers (c) | 261,100 | 257,400 | ||||||

Total basic video customers (b) (c) | 4,824,000 | 5,036,400 | ||||||

Digital video customers (d) | 3,218,100 | 3,133,400 | ||||||

Residential high-speed Internet customers (e) | 3,062,300 | 2,875,200 | ||||||

Telephone customers (f) | 1,595,900 | 1,348,800 | ||||||

Total Revenue Generating Units (g) | 12,700,300 | 12,393,800 | ||||||

After giving effect to sales and acquisitions of cable systems in 2008 and 2009, basic video customers, digital video customers, high-speed Internet customers, and telephone customers would have been 5,024,000, 3,132,200, 2,875,600, and 1,348,800, respectively, as of December 31, 2008.

| (a) | Our billing systems calculate the aging of customer accounts based on the monthly billing cycle for each account. On that basis, at December 31, 2009 and 2008, "customers" include approximately 25,900 and |

4

|

| 36,000 persons, respectively, whose accounts were over 60 days past due in payment, approximately 3,500 and 5,300 persons, respectively, whose accounts were over 90 days past due in payment, and approximately 2,200 and 2,700 persons, respectively, whose accounts were over 120 days past due in payment. |

| (b) | "Basic video customers" include all residential customers who receive video cable services. |

| (c) | Included within "basic video customers" are those in commercial and multi-dwelling structures, which are calculated on an equivalent bulk unit ("EBU") basis. In the second quarter of 2009, we began calculating EBUs by dividing the bulk price charged to accounts in an area by the published rate charged to non-bulk residential customers in that market for the comparable tier of service rather than the most prevalent price charged as was used previously. This EBU method of estimating basic video customers is consistent with the methodology used in determining costs paid to programmers and is consistent with the methodology used by other multiple system operators ("MSOs"). EBUs presented as of December 31, 2008 decreased by 9,300 as a result of the change in methodology. As we increase our published video rates to residential customers without a corresponding increase in the prices charged to commercial service or multi-dwelling customers, our EBU count will decline even if there is no real loss in commercial service or multi-dwelling customers. |

| (d) | "Digital video customers" include all basic video customers that have one or more digital set-top boxes or cable cards deployed. |

| (e) | "Residential high-speed Internet customers" represent those residential customers who subscribe to our high-speed Internet service. |

| (f) | "Telephone customers" include all customers receiving telephone service. |

| (g) | "Revenue generating units" represent the sum total of all basic video, digital video, high-speed Internet and telephone customers, not counting additional outlets within one household. For example, a customer who receives two types of service (such as basic video and digital video) would be treated as two revenue generating units and, if that customer added on high-speed Internet service, the customer would be treated as three revenue generating units. This statistic is computed in accordance with the guidelines of the National Cable & Telecommunications Association ("NCTA"). |

Video Services

In 2009, video services represented approximately 51% of our total revenues. Our video service offerings include the following:

• | Basic Video. All of our video customers receive a package of basic programming which generally consists of local broadcast television, local community programming, including governmental and public access, and limited satellite-delivered or non-broadcast channels, such as weather, shopping and religious programming. Our basic channel line-up generally has between 9 and 35 channels. | ||

• | Expanded Basic Video. This expanded programming level includes a package of satellite-delivered or non-broadcast channels and generally has between 20 and 60 channels in addition to the basic channel line-up. | ||

• | Digital Video. We offer digital video services including a digital set-top box, an interactive electronic programming guide with parental controls, an expanded menu of pay-per-view channels, including OnDemand (available nearly everywhere), digital quality music channels and the option to also receive a cable card. In addition to video programming, digital video service enables customers to receive our advanced broadband services such as OnDemand, DVRs, and high definition television. Charter also offers its digital sports tier in combination with premium sports content on charter.net. | ||

• | Premium Channels. These channels provide original programming, commercial-free movies, sports, and other special event entertainment programming. Although we offer subscriptions to premium channels on an individual basis, we offer an increasing number of digital video channel packages and premium channel packages, and we offer premium channels combined with our advanced broadband services. | ||

• | Pay-Per-View. These channels allow customers to pay on a per event basis to view a single showing of a |

5

| recently released movie, a one-time special sporting event, music concert, or similar event on a commercial-free basis. |

• | OnDemand and Subscription OnDemand . OnDemand service allows customers to select from hundreds of movies and other programming at any time. These programming options may be accessed for a fee or, in some cases, for no additional charge. In some areas we also offer subscription OnDemand for a monthly fee or included in a digital tier premium channel subscription. | ||

• | High Definition Television . High definition television offers our digital customers certain video programming at a higher resolution to improve picture quality versus standard basic or digital video images. | ||

• | Digital Video Recorder. DVR service enables customers to digitally record programming and to pause and rewind live programming. |

High-Speed Internet Services

In 2009, residential high-speed Internet services represented approximately 22% of our total revenues. We currently offer several tiers of high-speed Internet services with speeds ranging up to 60 megabytes per second download speed to our residential customers via cable modems attached to personal computers. We also offer home networking gateways to these customers, which permit customers to connect up to five computers in their home to the Internet simultaneously.

Telephone Services

In 2009, telephone services represented approximately 10% of our total revenues. We provide voice communications services primarily using VoIP technology to transmit digital voice signals over our systems. Charter Telephone includes unlimited nationwide and in-state calling, voicemail, call waiting, caller ID, call forwarding and other features. Charter Telephone® also provides international calling either by the minute or in a package of 250 minutes per month.

Commercial Services

In 2009, commercial services represented approximately 7% of our total revenues. Commercial services, offered through Charter Business™, include scalable broadband communications solutions for business organizations, such as business-to-business Internet access, data networking, video and music entertainment services, and business telephone.

Sale of Advertising

In 2009, sales of advertising represented approximately 4% of our total revenues. We receive revenues from the sale of local advertising on satellite-delivered networks such as MTV®, CNN® and ESPN®. In any particular market, we generally insert local advertising on up to 40 channels. We also provide cross-channel advertising to some programmers.

From time to time, certain of our vendors, including programmers and equipment vendors, have purchased advertising from us. For the years ending December 31, 2009, 2008 and 2007, we had advertising revenues from vendors of approximately $41 million, $39 million, and $15 million, respectively. These revenues resulted from purchases at market rates pursuant to binding agreements.

Pricing of Our Products and Services

Our revenues are derived principally from the monthly fees customers pay for the services we offer. We typically charge a one-time installation fee which is sometimes waived or discounted during certain promotional periods. The prices we charge for our products and services vary based on the level of service the customer chooses and the geographic market. In accordance with FCC rules, the prices we charge for video cable-related equipment, such as set-top boxes and remote control devices, and for installation services, are based on actual costs plus a permitted rate of return in regulated markets.

6

We offer reduced-price service for promotional periods in order to attract new customers, to promote the bundling of two or more services and to retain existing customers. There is no assurance that these customers will remain as customers when the promotional pricing period expires. When customers bundle services, generally the prices are lower per service than if they had only purchased a single service.

Our Network Technology

Our network utilizes the hybrid fiber coaxial cable ("HFC") architecture, which combines the use of fiber optic cable with coaxial cable. In most systems, we deliver our signals via fiber optic cable from the headend to a group of nodes, and use coaxial cable to deliver the signal from individual nodes to the homes passed served by that node. On average, our system design enables up to 400 homes passed to be served by a single node and provides for six strands of fiber to each node, with two strands activated and four strands reserved for spares and future services. We believe that this hybrid network design provides high capacity and signal quality. The design also provides two-way signal capacity for the addition of future services.

HFC architecture benefits include:

• | bandwidth capacity to enable traditional and two-way video and broadband services; | ||

• | dedicated bandwidth for two-way services, which avoids return signal interference problems that can occur with two-way communication capability; and | ||

• | signal quality and high service reliability. |

The following table sets forth the technological capacity of our systems as of December 31, 2009 based on a percentage of homes passed:

Less than 550 | 550 | 750 | 860/870 | Two-way | ||||

megahertz | megahertz | megahertz | megahertz | activated | ||||

4% | 5% | 45% | 46% | 96% |

Approximately 96% of our homes passed are served by systems that have bandwidth of 550 megahertz or greater. This bandwidth capacity enables us to offer digital television, high-speed Internet services, telephone service and other advanced services.

Through system upgrades and divestitures of non-strategic systems, we have reduced the number of headends that serve our customers from 1,138 at January 1, 2001 to 252 at December 31, 2009. Headends are the control centers of a cable system. Reducing the number of headends reduces related equipment, service personnel, and maintenance expenditures. As of December 31, 2009, approximately 92% of our customers were served by headends serving at least 10,000 customers.

As of December 31, 2009, our cable systems consisted of approximately 200,000 aerial and underground miles of coaxial cable, and approximately 55,000 aerial and underground miles of fiber optic cable, passing approximately 11.9 million households and serving approximately 5.3 million customers.

Charter has built and activated a national transport backbone inter-connecting 95% of Charter's local and regional networks. The backbone is highly scalable enabling efficient and timely transport of Internet traffic, voice traffic, and high definition video content distribution.

Management, Customer Care and Marketing

Our corporate office, which includes employees of Charter, is responsible for coordinating and overseeing operations including establishing company-wide policies and procedures. The corporate office performs certain financial and administrative functions on a centralized basis and performs these services on a cost reimbursement basis pursuant to a management services agreement. Our field operations are managed within two operating groups with shared service centers for our field sales and marketing function, human resources and training function, finance, and certain areas of customer operations.

Our customer care centers are managed centrally. We have eight internal customer care locations plus several third-party call center locations that through technology and procedures function as an integrated system. We provide

7

service to our customers 24 hours a day, seven days a week. We also utilize our website to enable our customers to view and pay their bills online, obtain useful information, and perform various equipment troubleshooting procedures. Our customers may also obtain support through our on-line chat and e-mail functionality.

Our marketing strategy emphasizes our bundled services through targeted marketing programs to existing and potential customers. Marketing expenditures increased by $4 million, or 1%, over the year ended December 31, 2008 to $272 million for the year ended December 31, 2009. Our marketing organization creates and executes marketing programs intended to increase customer relationships, retain existing customers and cross-sell additional products to current customers. We monitor the effectiveness of our marketing efforts, customer perception, competition, pricing, and service preferences, among other factors, to increase our responsiveness to our customers.

Programming

General

We believe that offering a wide variety of programming influences a customer's decision to subscribe to and retain our cable services. We rely on market research, customer demographics and local programming preferences to determine channel offerings in each of our markets. We obtain basic and premium programming from a number of suppliers, usually pursuant to written contracts. Our programming contracts generally continue for a fixed period of time, usually from three to ten years, and are subject to negotiated renewal. Some programming suppliers offer financial incentives to support the launch of a channel and/or ongoing marketing support. We also negotiate volume discount pricing structures. Programming costs are usually payable each month based on calculations performed by us and are generally subject to annual cost escalations and audits by the programmers.

Costs

Programming is usually made available to us for a license fee, which is generally paid based on the number of customers to whom we make such programming available. Such license fees may include "volume" discounts available for higher numbers of customers, as well as discounts for channel placement or service penetration. Some channels are available without cost to us for a limited period of time, after which we pay for the programming. For home shopping channels, we receive a percentage of the revenue attributable to our customers' purchases, as well as, in some instances, incentives for channel placement.

Our cable programming costs have increased in every year we have operated in excess of customary inflationary and cost-of-living type increases. We expect them to continue to increase, and at a higher rate than in 2009, due to a variety of factors including amounts paid for retransmission consent, annual increases imposed by programmers and additional programming, including high-definition and OnDemand programming. In particular, sports programming costs have increased significantly over the past several years. In addition, contracts to purchase sports programming sometimes provide for optional additional programming to be available on a surcharge basis during the term of the contract.

Federal law allows commercial television broadcast stations to make an election between "must-carry" rights and an alternative "retransmission-consent" regime. When a station opts for the retransmission-consent regime, we are not allowed to carry the station's signal without the station's permission. Continuing demands by owners of broadcast stations for carriage of other services or cash payments to those broadcasters in exchange for retransmission consent will likely increase our programming costs or require us to cease carriage of popular programming, potentially leading to a loss of customers in affected markets.

Over the past several years, our video service rates have not fully offset increasing programming costs, and with the impact of increasing competition and other marketplace factors, we do not expect them to do so in the foreseeable future. In addition, our inability to fully pass these programming cost increases on to our video customers has had and is expected in the future to have an adverse impact on our cash flow and operating margins associated with the video product. In order to mitigate reductions of our operating margins due to rapidly increasing programming costs, we continue to review our pricing and programming packaging strategies, and we plan to continue to migrate certain program services from our basic level of service to our digital tiers. As we migrate our programming to our digital tier packages, certain programming that was previously available to all of our customers via an analog signal may only be part of an elective digital tier package offered to our customers for an additional fee. As a result, we expect that the customer base upon which we pay programming fees will proportionately decrease, and the overall expense for providing that service will also decrease. However, reductions in the size of certain programming customer bases may result in the loss of specific volume discount benefits.

8

We have programming contracts that have expired and others that will expire at or before the end of 2010. We will seek to renegotiate the terms of these agreements. There can be no assurance that these agreements will be renewed on favorable or comparable terms. To the extent that we are unable to reach agreement with certain programmers on terms that we believe are reasonable, we have been, and may in the future be, forced to remove such programming channels from our line-up, which may result in a loss of customers.

Franchises

As of December 31, 2009, our systems operated pursuant to a total of approximately 3,200 franchises, permits, and similar authorizations issued by local and state governmental authorities. Such governmental authorities often must approve a transfer to another party. Most franchises are subject to termination proceedings in the event of a material breach. In addition, most franchises require us to pay the granting authority a franchise fee of up to 5.0% of revenues as defined in the various agreements, which is the maximum amount that may be charged under the applicable federal law. We are entitled to and generally do pass this fee through to the customer.

Prior to the scheduled expiration of most franchises, we generally initiate renewal proceedings with the granting authorities. This process usually takes three years but can take a longer period of time. The Communications Act of 1934, as amended (the "Communications Act"), which is the primary federal statute regulating interstate communications, provides for an orderly franchise renewal process in which granting authorities may not unreasonably withhold renewals. In connection with the franchise renewal process, many governmental authorities require the cable operator to make certain commitments, such as building out certain of the franchise areas, customer service requirements, and supporting and carrying public access channels. Historically we have been able to renew our franchises without incurring significant costs, although any particular franchise may not be renewed on commercially favorable terms or otherwise. Our failure to obtain renewals of our franchises, especially those in the major metropolitan areas where we have the most customers, could have a material adverse effect on our consolidated financial condition, results of operations, or our liquidity, including our ability to comply with our debt covenants. See "- Regulation and Legislation - Video Services - Franchise Matters."

Competition

We face competition in the areas of price, service offerings, and service reliability. We compete with other providers of video, high-speed Internet access, telephone services, and other sources of home entertainment. We operate in a very competitive business environment, which can adversely affect the results of our business and operations. We cannot predict the impact on us of broadband services offered by our competitors.

In terms of competition for customers, we view ourselves as a member of the broadband communications industry, which encompasses multi-channel video for television and related broadband services, such as high-speed Internet, telephone, and other interactive video services. In the broadband industry, our principal competitor for video services throughout our territory is direct broadcast satellite ("DBS") and our principal competitor for high-speed Internet services is DSL provided by telephone companies. Our principal competitors for telephone services are established telephone companies, other telephone service providers, and other carriers, including VoIP providers. Based on telephone companies' entry into video service and the upgrades of their networks, they will become increasingly more significant competitors for both high-speed Internet and video customers. At this time, we do not consider other cable operators to be significant competitors in our overall market, as overbuilds are infrequent and geographically spotty (although in any particular market, a cable operator overbuilder would likely be a significant competitor at the local level).

Our key competitors include:

DBS

Direct broadcast satellite is a significant competitor to cable systems. The DBS industry has grown rapidly over the last several years, and now serves more than 32 million subscribers nationwide. DBS service allows the subscriber to receive video services directly via satellite using a dish antenna.

Video compression technology and high powered satellites allow DBS providers to offer more than 280 digital channels from a single satellite, thereby surpassing the traditional analog cable system. In 2009, major DBS competitors offered a greater variety of channel packages, and were especially competitive with promotional pricing for more basic services. While we continue to believe that the initial investment by a DBS customer exceeds that of

9

a cable customer, the initial equipment cost for DBS has decreased substantially, as the DBS providers have aggressively marketed offers to new customers of incentives for discounted or free equipment, installation, and multiple units. DBS providers are able to offer service nationwide and are able to establish a national image and branding with standardized offerings, which together with their ability to avoid franchise fees of up to 5% of revenues and property tax, leads to greater efficiencies and lower costs in the lower tiers of service. Also, DBS providers are currently offering more high definition programming, including local high definition programming. However, we believe that cable-delivered OnDemand and Subscription OnDemand services, which include HD programming, are superior to DBS service, because cable headends can provide two-way communication to deliver many titles which customers can access and control independently, whereas DBS technology can only make available a much smaller number of titles with DVR-like customer control. However, joint marketing arrangements between some DBS providers and telecommunications carriers allow similar bundling of services in certain areas. DBS providers have also made attempts at deployment of high-speed Internet access services via satellite, but those services have been technically constrained and of limited appeal.

Telephone Companies and Utilities

Our telephone service competes directly with established telephone companies and other carriers, including Internet-based VoIP providers, for voice service customers. Because we offer voice services, we are subject to considerable competition from telephone companies and other telecommunications providers, including wireless providers with an increasing number of consumers abandoning wired telephone services. The telecommunications industry is highly competitive and includes competitors with greater financial and personnel resources, strong brand name recognition, and long-standing relationships with regulatory authorities and customers. Moreover, mergers, joint ventures and alliances among our competitors have resulted in providers capable of offering cable television, Internet, and telephone services in direct competition with us.

Most telephone companies, which already have plant, an existing customer base, and other operational functions in place (such as billing and service personnel), offer DSL service. DSL service allows Internet access to subscribers at data transmission speeds greater than those available over conventional telephone lines. We believe DSL service is competitive with high-speed Internet service and is often offered at prices lower than our Internet services, although often at speeds lower than the speeds we offer. However, DSL providers may currently be in a better position to offer data services to businesses since their networks tend to be more complete in commercial areas. They may also have the ability to bundle telephone with Internet services for a higher percentage of their customers. We expect DSL to remain a significant competitor to our high-speed Internet services. In addition, the continuing deployment of fiber optics into telephone companies' networks (primarily by Verizon Communications, Inc. ("Verizon")) will enable them to provide even higher bandwidth Internet services.

Telephone companies, including AT&T Inc. ("AT&T") and Verizon, offer video and other services in competition with us, and we expect they will increasingly do so in the future. Upgraded portions of these networks carry two-way video, data services and provide digital voice services similar to ours. In the case of Verizon, high-speed data services (fiber optic service ("FiOS")) operate at speeds as high as or higher than ours. In addition, these companies continue to offer their traditional telephone services, as well as service bundles that include wireless voice services provided by affiliated companies. Based on internal estimates, we believe that AT&T and Verizon are offering video services in areas serving approximately 26% to 31% of our estimated homes passed as of December 31, 2009 and we have experienced increased customer losses in these areas. AT&T and Verizon have also launched campaigns to capture more of the multiple dwelling unit ("MDU") market. Additional upgrades and product launches are expected in markets in which we operate.

In addition to telephone companies obtaining franchises or alternative authorizations in some areas and seeking them in others, they have been successful through various means in reducing or streamlining the franchising requirements applicable to them. They have had significant success at the federal and state level, securing an FCC ruling and numerous state franchise laws that facilitate their entry into the video marketplace. Because telephone companies have been successful in avoiding or reducing the franchise and other regulatory requirements that remain applicable to cable operators like us, their competitive posture has often been enhanced. The large scale entry of major telephone companies as direct competitors in the video marketplace has adversely affected the profitability and valuation of our cable systems.

Additionally, we are subject to limited competition from utilities that possess fiber optic transmission lines capable of transmitting signals with minimal signal distortion. Certain utilities are also developing broadband over power line technology, which may allow the provision of Internet and other broadband services to homes and offices.

10

Broadcast Television

Cable television has long competed with broadcast television, which consists of television signals that the viewer is able to receive without charge using an "off-air" antenna. The extent of such competition is dependent upon the quality and quantity of broadcast signals available through "off-air" reception, compared to the services provided by the local cable system. Traditionally, cable television has provided higher picture quality and more channel offerings than broadcast television. However, the recent licensing of digital spectrum by the FCC now provides traditional broadcasters with the ability to deliver high definition television pictures and multiple digital-quality program streams, as well as advanced digital services such as subscription video and data transmission.

Traditional Overbuilds

Cable systems are operated under non-exclusive franchises historically granted by state and local authorities. More than one cable system may legally be built in the same area. It is possible that a franchising authority might grant a second franchise to another cable operator and that such franchise might contain terms and conditions more favorable than those afforded us. In addition, entities willing to establish an open video system, under which they offer unaffiliated programmers non-discriminatory access to a portion of the system's cable system, may be able to avoid local franchising requirements. Well-financed businesses from outside the cable industry, such as public utilities that already possess fiber optic and other transmission lines in the areas they serve, may over time become competitors. There are a number of cities that have constructed their own cable systems, in a manner similar to city-provided utility services. There also has been interest in traditional cable overbuilds by private companies not affiliated with established local exchange carriers. Constructing a competing cable system is a capital intensive process which involves a high degree of risk. We believe that in order to be successful, a competitor's overbuild would need to be able to serve the homes and businesses in the overbuilt area with equal or better service quality, on a more cost-effective basis than we can. Any such overbuild operation would require access to capital or access to facilities already in place that are capable of delivering cable television programming.

As of December 31, 2009, excluding telephone companies, we are aware of traditional overbuild situations impacting approximately 8% to 9% of our total homes passed and potential traditional overbuild situations in areas servicing approximately an additional 1% of our total homes passed. Additional overbuild situations may occur, especially given the potential for broadband overbuilds funded by the "American Recovery and Reinvestment Act."

Private Cable

Additional competition is posed by satellite master antenna television systems, or SMATV systems, serving MDUs, such as condominiums, apartment complexes, and private residential communities. Private cable systems can offer improved reception of local television stations, and many of the same satellite-delivered program services that are offered by cable systems. Although disadvantaged from a programming cost perspective, SMATV systems currently benefit from operating advantages not available to franchised cable systems, including fewer regulatory burdens and no requirement to service low density or economically depressed communities. The FCC previously adopted regulations that favor SMATV and private cable operators serving MDU complexes, allowing them to continue to secure exclusive contracts with MDU owners. The FCC is currently considering whether to restrict their ability to enter into similar exclusive arrangements. This sort of regulatory disparity would provide a competitive advantage to certain of our current and potential competitors.

Other Competitors

Local wireless Internet services have recently begun to operate in markets using available unlicensed radio spectrum. Some cellular phone service operators are also marketing PC cards offering wireless broadband access to their cellular networks. These service options offer another alternative to cable-based Internet access.

Internet Delivered Video

High-speed Internet access facilitates the streaming of video into homes and businesses. As the quality and availability of video streaming over the Internet improves, we expect video streaming to compete with the traditional delivery of video programming services over cable systems. It is possible that programming suppliers will consider bypassing cable operators and market their services directly to the consumer through video streaming over the Internet. If customers were to choose to receive video over the Internet rather than through our basic or digital video services, we could experience a reduction in our video revenues.

11

Regulation and Legislation

The following summary addresses the key regulatory and legislative developments affecting the cable industry and our three primary services: video service, high-speed Internet service, and telephone service. Cable system operations are extensively regulated by the federal government (primarily the FCC), certain state governments, and many local governments. A failure to comply with these regulations could subject us to substantial penalties. Our business can be dramatically impacted by changes to the existing regulatory framework, whether triggered by legislative, administrative, or judicial rulings. Congress and the FCC have frequently revisited the subject of communications regulation often designed to increase competition to the cable industry, and they are likely to do so in the future. We could be materially disadvantaged in the future if we are subject to new regulations that do not equally impact our key competitors. We cannot provide assurance that the already extensive regulation of our business will not be expanded in the future.

Video Service

Cable Rate Regulation. The cable industry has operated under a federal rate regulation regime for more than a decade. The regulations currently restrict the prices that cable systems charge for the minimum level of video programming service, referred to as "basic service," and associated equipment. All other cable offerings are now universally exempt from rate regulation. Although basic service rate regulation operates pursuant to a federal formula, local governments, commonly referred to as local franchising authorities, are primarily responsible for administering this regulation. The majority of our local franchising authorities have never been certified to regulate basic service cable rates (and order rate reductions and refunds), but they generally retain the right to do so (subject to potential regulatory limitations under state franchising laws), except in those specific communities facing "effective competition," as defined under federal law. We have already secured FCC recognition of effective competition, and become rate deregulated, in many of our communities.

There have been frequent calls to impose expanded rate regulation on the cable industry. Confronted with rapidly increasing cable programming costs, it is possible that Congress may adopt new constraints on the retail pricing or packaging of cable programming. For example, there has been legislative and regulatory interest in requiring cable operators to offer historically combined programming services on an à la carte basis. Any such mandate could adversely affect our operations.

Federal rate regulations generally require cable operators to allow subscribers to purchase premium or pay-per-view services without the necessity of subscribing to any tier of service, other than the basic service tier. The applicability of this rule in certain situations remains unclear, and adverse decisions by the FCC could affect our pricing and packaging of services. As we attempt to respond to a changing marketplace with competitive pricing practices, such as targeted promotions and discounts, we may face Communications Act uniform pricing requirements that impede our ability to compete.

Must Carry/Retransmission Consent. There are two alternative legal methods for carriage of local broadcast television stations on cable systems. Federal "must carry" regulations require cable systems to carry local broadcast television stations upon the request of the local broadcaster. Alternatively, federal law includes "retransmission consent" regulations, by which popular commercial television stations can prohibit cable carriage unless the cable operator first negotiates for "retransmission consent," which may be conditioned on significant payments or other concessions. Broadcast stations must elect "must carry" or "retransmission consent" every three years, with the election date of October 1, 2008, for the current period of 2009 through 2011. Either option has a potentially adverse effect on our business by utilizing bandwidth capacity. In addition, popular stations invoking "retransmission consent" increasingly have been demanding cash compensation in their negotiations with cable operators.

In September 2007, the FCC adopted an order increasing the cable industry's existing must-carry obligations by requiring cable operators to offer "must carry" broadcast signals in both analog and digital format (dual carriage) for a three year period after the broadcast television industry completed its ongoing transition from an analog to digital format, which occurred on June 12, 2009. The burden could increase further if cable systems were ever required to carry multiple program streams included within a single digital broadcast transmission (multicast carriage), which the recent FCC order did not address. Additional government-mandated broadcast carriage obligations could disrupt existing programming commitments, interfere with our preferred use of limited channel capacity, and limit our ability to offer services that appeal to our customers and generate revenues. We may need to take additional operational steps and/or make further operating and capital investments to ensure that customers not otherwise equipped to receive digital programming, retain access to broadcast programming.

12

Access Channels. Local franchise agreements often require cable operators to set aside certain channels for public, educational, and governmental access programming. Federal law also requires cable systems to designate a portion of their channel capacity for commercial leased access by unaffiliated third parties, who generally offer programming that our customers do not particularly desire. The FCC adopted new rules in 2007 mandating a significant reduction in the rates that operators can charge commercial leased access users and imposing additional administrative requirements that would be burdensome on the cable industry. The effect of the FCC's new rules was stayed by a federal court, pending a cable industry appeal and a finding that the new rules did not comply with the requirements of the Office of Management and Budget. Under federal statute, commercial leased access programmers are entitled to use up to 15% of a cable system's capacity. Increased activity in this area could further burden the channel capacity of our cable systems, and potentially limit the amount of services we are able to offer and may necessitate further investments to expand our network capacity.

Access to Programming. The Communications Act and the FCC's "program access" rules generally prevent satellite cable programming vendors in which a cable operator has an attributable interest and satellite broadcast programming vendors from favoring cable operators over competing multichannel video distributors, such as DBS, and limit the ability of such vendors to offer exclusive programming arrangements to cable operators. Given the heightened competition and media consolidation that we face, it is possible that we will find it increasingly difficult to gain access to popular programming at favorable terms. Such difficulty could adversely impact our business.

Ownership Restrictions. Federal regulation of the communications field traditionally included a host of ownership restrictions, which limited the size of certain media entities and restricted their ability to enter into competing enterprises. Through a series of legislative, regulatory, and judicial actions, most of these restrictions have been either eliminated or substantially relaxed. Changes in this regulatory area could alter the business environment in which we operate.

Pole Attachments. The Communications Act requires most utilities owning utility poles to provide cable systems with access to poles and conduits and simultaneously subjects the rates charged for this access to either federal or state regulation. The Communications Act specifies that significantly higher rates apply if the cable plant is providing "telecommunications" services rather than only video services. Although the FCC previously determined that the lower rate was applicable to the mixed use of a pole attachment for the provision of both video and Internet access services (a determination upheld by the U.S. Supreme Court), the FCC issued a Notice of Proposed Rulemaking ("NPRM") on November 20, 2007, in which it "tentatively concludes" that such mixed use determination would likely be set aside. Under this NPRM, the FCC is seeking comment on its proposal to apply a single rate for all pole attachments over which a cable operator provides Internet access and other services, that allocates to the cable operators the additional cost associated with the "unusable space" of the pole. Such rate change could likely result in a substantial increase in our pole attachment costs.

Cable Equipment. In 1996, Congress enacted a statute seeking to promote the "competitive availability of navigational devices" by allowing cable subscribers to use set-top boxes obtained from third parties, including third-party retailers. The FCC has undertaken several steps to implement this statute designed to promote the retail sale of set-top boxes and other equipment that can be used to receive video services. The FCC requires that security functions (which allow a cable operator to control who may access its services and remains under the operator's exclusive control) be unbundled from the basic channel navigation functions and requires that those security functions be made available through "CableCARDs" that connect to customer-owned televisions and other devices equipped to receive one-way analog and digital video service without the need for an operator-provided set-top box. Effective July 1, 2007, cable operators were prohibited from acquiring for deployment integrated set-top boxes that combine both channel navigation and security functions.

The FCC has been considering regulatory proposals for "plug-and-play" retail devices that could access two-way cable services. In April 2008, we joined a multi-party contract, among major consumer electronics and information technology companies and the six largest cable operators in the United States, to agree on how technology we use to support our current generation set-top boxes will be deployed in cable networks and navigation devices to enable retail devices to access two-way cable services without impairing our ability to innovate. In December 2009, the FCC commenced a preliminary inquiry into these and alternative approaches to set-top boxes and consumer electronics. Some of the alternative approaches, if adopted, could impose substantial costs on us and impair out ability to innovate.

MDUs / Inside Wiring . The FCC has adopted a series of regulations designed to spur competition to established cable operators in MDU complexes. These regulations allow our competitors to access certain existing cable wiring inside MDUs. The FCC also adopted regulations limiting the ability of established cable operators, like us, to enter

13

into exclusive service contracts for MDU complexes. Significantly, it has not yet imposed a similar restriction on private cable operators and SMATV systems serving MDU properties but the issue is still pending before the FCC. In their current form, the FCC's regulations in this area favor our competitors.

Privacy Regulation . The Communications Act limits our ability to collect and disclose subscribers' personally identifiable information for our video, telephone, and high-speed Internet services, as well as provides requirements to safeguard such information. We are subject to additional federal, state, and local laws and regulations that impose additional subscriber and employee privacy restrictions. Further, the FCC, FTC, and many states regulate and restrict the marketing practices of cable operators, including telemarketing and online marketing efforts.

Other FCC Regulatory Matters. FCC regulations cover a variety of additional areas, including, among other things: (1) equal employment opportunity obligations; (2) customer service standards; (3) technical service standards; (4) mandatory blackouts of certain network, syndicated and sports programming; (5) restrictions on political advertising; (6) restrictions on advertising in children's programming; (7) restrictions on origination cablecasting; (8) restrictions on carriage of lottery programming; (9) sponsorship identification obligations; (10) closed captioning of video programming; (11) licensing of systems and facilities; (12) maintenance of public files; and (13) emergency alert systems. Each of these regulations restricts our business practices to varying degrees.

It is possible that Congress or the FCC will expand or modify its regulation of cable systems in the future, and we cannot predict at this time how that might impact our business.

Copyright. Cable systems are subject to a federal copyright compulsory license covering carriage of television and radio broadcast signals. The possible modification or elimination of this compulsory copyright license is the subject of continuing legislative and administrative review and could adversely affect our ability to obtain desired broadcast programming. There is uncertainty regarding certain applications of the compulsory copyright license, including the royalty treatment of distant broadcast signals that are not available to all cable system subscribers served by a single headend. The Copyright Office is currently conducting an inquiry to consider a variety of issues affecting cable's compulsory copyright license, including how the compulsory copyright license should apply to newly-offered digital broadcast signals. Current uncertainty regarding the compulsory copyright license could lead to legislative proposals, new administrative rules, or judicial decisions that would increase our compulsory copyright payments for the carriage of broadcast signals including legislation that is now pending in Congress. Legislation is now pending in Congress that would resolve much of the current uncertainty regarding this compulsory copyright license. In particular, the legislation would confirm that copyright fees associated with the delivery of distant broadcast signals are limited to the cable system subscribers who actually receive those signals. The new legislation, if adopted, would also require cable systems to pay an additional royalty fee for each digital multicast of a retransmitted distant broadcast signal and would provide copyright owners with a new right to audit our semi-annual royalty filings.

Copyright clearances for non-broadcast programming services are arranged through private negotiations. Cable operators also must obtain music rights for locally originated programming and advertising from the major music performing rights organizations. These licensing fees have been the source of litigation in the past, and we cannot predict with certainty whether license fee disputes may arise in the future.

Franchise Matters. Cable systems generally are operated pursuant to nonexclusive franchises granted by a municipality or other state or local government entity in order to utilize and cross public rights-of-way. Although some state franchising laws grant indefinite franchises, cable franchises generally are granted for fixed terms and in many cases include monetary penalties for noncompliance and may be terminable if the franchisee fails to comply with material provisions. The specific terms and conditions of cable franchises vary significantly between jurisdictions. Each franchise generally contains provisions governing cable operations, franchise fees, system construction, maintenance, technical performance, customer service standards, and changes in the ownership of the franchisee. A number of states subject cable systems to the jurisdiction of centralized state government agencies, such as public utility commissions. Although local franchising authorities have considerable discretion in establishing franchise terms, certain federal protections benefit cable operators. For example, federal law caps local franchise fees and includes renewal procedures designed to protect incumbent franchisees from arbitrary denials of renewal. Even if a franchise is renewed, however, the local franchising authority may seek to impose new and more onerous requirements as a condition of renewal. Similarly, if a local franchising authority's consent is required for the purchase or sale of a cable system, the local franchising authority may attempt to impose more burdensome requirements as a condition for providing its consent.

14

The traditional cable franchising regime is currently undergoing significant change as a result of various federal and state actions. In a series of recent rulemakings, the FCC adopted new rules that streamlined entry for new competitors (particularly those affiliated with telephone companies) and reduced certain franchising burdens for these new entrants. The FCC adopted more modest relief for existing cable operators.

At the same time, a substantial number of states have adopted franchising laws. Again, these laws were principally designed to streamline entry for new competitors, and they often provide advantages for these new entrants that are not immediately available to existing cable operators. In many instances, these franchising regimes do not apply to established cable operators until the existing franchise expires or a competitor directly enters the franchise territory. In a number of instances, however, incumbent cable operators have the ability to immediately "opt into" the new franchising regime, which can provide significant regulatory relief. The exact nature of these state franchising laws, and their varying application to new and existing video providers, will impact our franchising obligations and our competitive position.

Internet Service

Over the past several years, proposals have been advanced at the FCC and Congress to adopt "net neutrality" rules that would require cable operators offering Internet service to provide non-discriminatory access of customers to their networks and could interfere with the ability of cable operators to manage their networks. The FCC issued a non-binding policy statement in 2005 establishing four basic principles to guide its ongoing policymaking activities regarding high-speed Internet and related services. These principles provide that consumers are entitled to: (i) access lawful Internet content of their choice; (ii) run applications and services of their choice, subject to the needs of law enforcement; (iii) connect their choice of legal devices that do not harm the network; and (iv) enjoy competition among network providers, application and service providers, and content providers. In August 2008, the FCC issued an order concerning one Internet network management practice in use by another cable operator, effectively treating the four principles as rules and ordering a change in network management practices. This decision is on appeal. In October 2009, the FCC released a NPRM seeking additional comment on draft rules to codify these principles and to consider further network neutrality requirements, including two new principles. The first new rule would prohibit discrimination against lawful content, specifically stating that broadband providers cannot discriminate against particular Internet content or applications and cannot block or degrade lawful traffic over their networks or favor some content or applications over others. The second new rule would require "transparency" in advising customers in greater detail about the terms of service, including network management tools utilized by the service provider. In addition to possible FCC action, legislative proposals have been introduced in Congress to mandate how broadband providers manage their networks, and the broadband provisions of the newly enacted American Recovery and Reinvestment Act already mandate adherence to the FCC's 2005 principles as a condition to the receipt of broadband funding. The FCC's Rulemaking and additional proposals for new legislation could impose additional obligations on high-speed Internet providers. Any such rules or statutes could limit our ability to manage our cable systems (including use for other services), to obtain value for use of our cable systems and respond to competition.

As the Internet has matured, it has become the subject of increasing regulatory interest. Congress and federal regulators have adopted a wide range of measures directly or potentially affecting Internet use, including, for example, consumer privacy, copyright protections (which afford copyright owners certain rights against us that could adversely affect our relationship with a customer accused of violating copyright laws), defamation liability, taxation, obscenity, and unsolicited commercial e-mail. Additionally, the FCC and Congress are considering subjecting high-speed Internet access services to the Universal Service funding requirements. This would impose significant new costs on our high-speed Internet service. State and local governmental organizations have also adopted Internet-related regulations. These various governmental jurisdictions are also considering additional regulations in these and other areas, such as pricing, service and product quality, and intellectual property ownership. The adoption of new Internet regulations or the adaptation of existing laws to the Internet could adversely affect our business.

Telephone Service