UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________________________

FORM

10-K

[X] Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended December 31, 2013

[ ] Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to

Commission File No. 1-13726

Chesapeake Energy Corporation

Oklahoma |

| 73-1395733 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

6100 North Western Avenue |

|

|

Oklahoma City, Oklahoma |

| 73118 |

(Address of principal executive offices) |

| (Zip Code) |

(405) 848-8000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: | ||

Title of Each Class |

| Name of Each Exchange on Which Registered |

Common Stock, par value $0.01 |

| New York Stock Exchange |

9.5% Senior Notes due 2015 |

| New York Stock Exchange |

3.25% Senior Notes due 2016 |

| New York Stock Exchange |

6.25% Senior Notes due 2017 |

| New York Stock Exchange |

6.5% Senior Notes due 2017 |

| New York Stock Exchange |

6.875% Senior Notes due 2018 |

| New York Stock Exchange |

7.25% Senior Notes due 2018 |

| New York Stock Exchange |

6.625% Senior Notes due 2020 |

| New York Stock Exchange |

6.875% Senior Notes due 2020 |

| New York Stock Exchange |

6.125% Senior Notes due 2021 |

| New York Stock Exchange |

5.375% Senior Notes due 2021 |

| New York Stock Exchange |

5.75% Senior Notes due 2023 |

| New York Stock Exchange |

2.75% Contingent Convertible Senior Notes due 2035 |

| New York Stock Exchange |

2.5% Contingent Convertible Senior Notes due 2037 |

| New York Stock Exchange |

2.25% Contingent Convertible Senior Notes due 2038 |

| New York Stock Exchange |

4.5% Cumulative Convertible Preferred Stock |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: | ||

None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES [X] NO [ ]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. YES [ ] NO [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES [X] NO [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES [X] NO [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer [X] Accelerated Filer [ ] Non-accelerated Filer [ ] Smaller Reporting Company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES [ ] NO [X]

The aggregate market value of our common stock held by non-affiliates on June 30, 2013 was approximately $13.6 billion . At February 11, 2014 , there were 666,212,515 shares of our $0.01 par value common stock outstanding.

________________________________________

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement for the 2014 Annual Meeting of Shareholders are incorporated by reference in Part III.

CHESAPEAKE ENERGY CORPORATION AND SUBSIDIARIES

2013 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| |||

| PART I |

|

|

|

|

| Page |

Item 1. | Business |

| 1 |

Item 1A. | Risk Factors |

| 23 |

Item 1B. | Unresolved Staff Comments |

| 31 |

Item 2. | Properties |

| 31 |

Item 3. | Legal Proceedings |

| 31 |

Item 4. | Mine Safety Disclosures |

| 32 |

PART II | |||

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

| 33 |

Item 6. | Selected Financial Data |

| 35 |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations |

| 37 |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk |

| 64 |

Item 8. | Financial Statements and Supplementary Data |

| 69 |

Item 9. | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure |

| 152 |

Item 9A. | Controls and Procedures |

| 152 |

Item 9B. | Other Information |

| 152 |

PART III | |||

Item 10. | Directors, Executive Officers and Corporate Governance |

| 153 |

Item 11. | Executive Compensation |

| 153 |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

| 153 |

Item 13. | Certain Relationships and Related Transactions and Director Independence |

| 153 |

Item 14. | Principal Accountant Fees and Services |

| 153 |

PART IV | |||

Item 15. | Exhibits and Financial Statement Schedules |

| 154 |

PART I

Item 1. | Business |

Unless the context otherwise requires, references to "Chesapeake", the "Company", "us", "we" and "our" in this report are to Chesapeake Energy Corporation together with its subsidiaries. Our principal executive offices are located at 6100 North Western Avenue, Oklahoma City, Oklahoma 73118, and our main telephone number at that location is (405) 848-8000. Definitions of natural gas and oil industry terms appearing in this report can be found under Glossary of Natural Gas and Oil Terms beginning on page 20. Please note that we have changed the oil and natural gas equivalent reporting convention from that used in our previous reports to oil equivalent. Combined natural gas, oil and NGL volume amounts are shown in barrels of oil equivalent (boe) rather than in thousand cubic feet of natural gas equivalent (mcfe). Oil equivalent is based on six thousand cubic feet of natural gas to one barrel of oil or NGL.

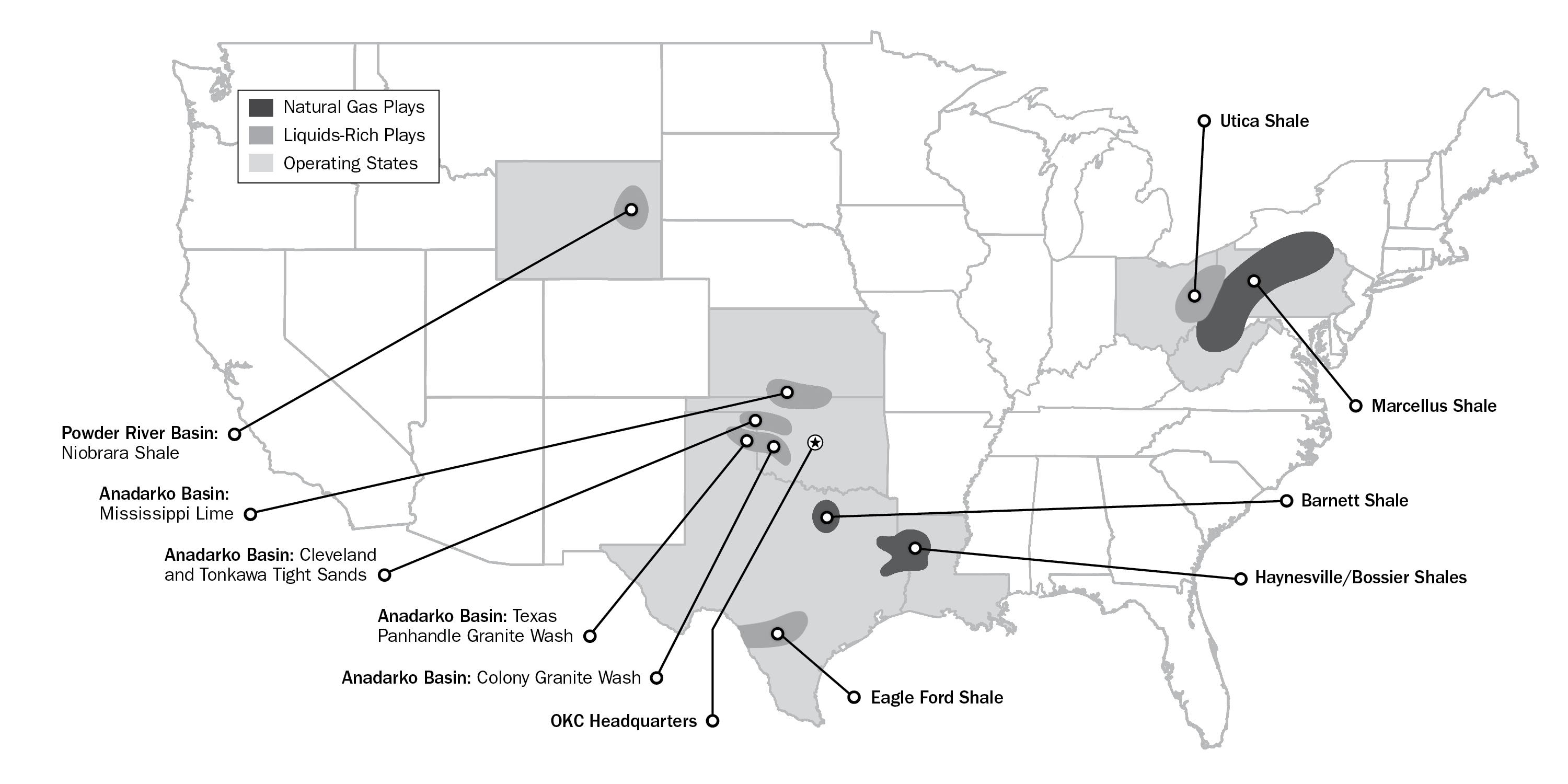

Our Business

The Company is currently the second-largest producer of natural gas and the tenth-largest producer of liquids in the U.S. We own interests in approximately 46,800 natural gas and oil wells that produced an average of approximately 665 mboe per day in the 2013 fourth quarter, net to our interest. We have a large and geographically diverse resource base of onshore U.S. unconventional natural gas and liquids assets. We have leading positions in the liquids-rich resource plays of the Eagle Ford Shale in South Texas; the Utica Shale in Ohio and Pennsylvania; the Granite Wash/Hogshooter, Cleveland, Tonkawa and Mississippi Lime plays in the Anadarko Basin in northwestern Oklahoma, the Texas Panhandle and southern Kansas; and the Niobrara Shale in the Powder River Basin in Wyoming. Our core natural gas resource plays are the Haynesville/Bossier Shales in northwestern Louisiana and East Texas; the Marcellus Shale in the northern Appalachian Basin of West Virginia and Pennsylvania; and the Barnett Shale in the Fort Worth Basin of north-central Texas. We also own substantial marketing, compression and oilfield services businesses.

The map below illustrates the locations of Chesapeake ' s natural gas and oil exploration and production operations.

The Company's estimated proved reserves as of December 31, 2013 were 2.678 bboe, an increase of 63 mmboe, or 2%, from 2.615 bboe at year-end 2012 . The 2013 proved reserve movement included 524 mmboe of extensions and discoveries, 162 mmboe of upward revisions resulting from higher natural gas and oil prices and 192 mmboe of downward revisions resulting from changes to previous estimates as further discussed below in Natural Gas, Oil and NGL Reserves and in Supplemental Disclosures About Natural Gas, Oil and NGL Producing Activities included in Item 8 of this report. In 2013 , we produced 244 mmboe, acquired 2 mmboe and divested 189 mmboe of estimated proved reserves. Natural gas and oil prices used in estimating proved reserves as of December 31, 2013 increased from prices as of December 31, 2012 using the trailing 12-month average prices required by the Securities and Exchange

1

Commission (SEC). Natural gas prices increased $0.91, or 33%, to $3.67 per mcf from $2.76 per mcf, and oil prices increased by $1.98, or 2%, to $96.82 per bbl from $94.84 per bbl. Proved developed reserves made up 68% of our proved reserves as of December 31, 2013 compared to 57% as of December 31, 2012.

Our daily production for 2013 averaged 670 mboe, an increase of 22 mboe, or 3%, over the 648 mboe of daily production for 2012 , and consisted of approximately 2.999 bcf of natural gas (75% on an oil equivalent basis), approximately 112,600 bbls of oil (17% on an oil equivalent basis) and approximately 57,200 bbls of NGL (8% on an oil equivalent basis). Our natural gas production in 2013 decreased 3%, or approximately 85 mmcf per day; our oil production increased 32%, or approximately 27,200 bbls per day; and our NGL production increased 19%, or approximately 9,100 bbls per day.

Information About Us

We make available free of charge on our website at www.chk.com our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. From time to time, we also post announcements, updates, events, investor information and presentations on our website in addition to copies of all recent news releases.

Business Strategy

With substantial leasehold positions in most of the premier U.S. onshore resource plays, Chesapeake is focused on finding and producing hydrocarbons in a responsible and efficient manner that seeks to maximize shareholder returns. We are committed to increasing our profitability and decreasing our corporate and balance sheet complexity through the execution of our business strategy, which consists of two fundamental tenets: financial discipline and profitable and efficient growth from captured resources.

We are applying financial discipline to all aspects of our business, with the primary goals of approximating capital expenditures with cash flow from operations, divesting noncore assets and affiliates, achieving investment grade metrics, lowering our per unit cost structure, and reducing financial and operational risk and complexity. As a result of our focus on financial discipline, average per unit production expenses during 2013 decreased 14% from 2012, while general and administrative expenses (excluding stock-based compensation and restructuring and other termination costs) decreased 17%. We anticipate further decreases in our per unit expenses during 2014 as we continue to exercise cost discipline.

The Company's substantial inventory of hydrocarbon resources provides a strong foundation for future growth. We believe that focusing on profitable and efficient growth from our captured resources will allow us to deliver attractive financial returns through all phases of the commodity price cycle. We have seen and continue to see increased efficiencies through our leveraging of first-well investments made in prior periods, including drilling on pre-existing pads. We have also implemented a competitive capital allocation process designed to optimize our asset portfolio and identify the highest quality projects for future investment. To better understand our opportunities for continuous improvement, we benchmark our performance against that of our peers and evaluate the performance of completed projects. We also pay careful attention to safety, regulatory compliance and environmental stewardship measures while executing our growth strategy.

In the 2013 second half, we conducted a company-wide review of our operations, assets and organizational structure to best position the Company to maximize shareholder value going forward as we execute our strategic priorities. We reorganized the Company into Northern and Southern operating divisions as well as an Exploration and Subsurface Technology unit and Operations and Technical Services unit that are supported by enterprise-wide service departments. The new organizational structure is designed to increase accountability and communication throughout the Company, while encouraging standardization, efficiency and continuous improvement. As part of the reorganization, we reduced our workforce by approximately 1,000 employees, including approximately 900 employees under a workforce reduction plan we implemented in September and October 2013. We anticipate the workforce reduction will result in future cost savings and help the Company demonstrate more profitable and efficient growth. See Note 17 of the notes to our consolidated financial statements included in Item 8 of this report and Results of Operations - Restructuring and Other Termination Costs in Item 7 of this report for further discussion of our workforce reductions. While furthering our strategic priorities, certain actions that would reduce financial leverage and complexity could negatively impact our future results of operations and/or liquidity. We expect to incur various cash and noncash charges, including but not limited to impairments of fixed assets, lease termination charges, financing extinguishment costs and charges for unused natural gas transportation and gathering capacity.

2

We are continuing to review and refine our portfolio for assets that fit best with the Company's strategy of profitable growth from captured resources. On February, 24, 2014, we announced that we are pursuing strategic alternatives for our oilfield services business, including a potential spin-off to Chesapeake shareholders or an outright sale. We believe that our oilfield services business can maximize its value to Chesapeake shareholders outside of the current ownership structure. See Oilfield Services below for a further description of our oilfield services business.

Operating Divisions

Chesapeake focuses its exploration, development, acquisition and production efforts in the two geographic operating divisions described below.

Southern Division . Includes the Eagle Ford Shale in South Texas, the Granite Wash/Hogshooter, Cleveland, Tonkawa and Mississippi Lime plays in the Anadarko Basin in northwestern Oklahoma, the Texas Panhandle and southern Kansas, the Haynesville/Bossier Shale in northwestern Louisiana and East Texas and the Barnett Shale in the Fort Worth Basin in north-central Texas.

Northern Division . Includes the Utica Shale in Ohio, West Virginia and Pennsylvania, the Marcellus Shale in the northern Appalachian Basin in West Virginia and Pennsylvania and the Niobrara Shale in the Powder River Basin in Wyoming.

Well Data

At December 31, 2013 , we had interests in approximately 46,800 gross (20,900 net) productive wells, including properties in which we held an overriding royalty interest. Of these wells, 38,100 gross (18,400 net) were classified as natural gas productive wells and 8,700 gross (2,500 net) were classified as oil productive wells. Chesapeake operates approximately 28,100 of its 46,800 productive wells. During 2013 , we completed 1,376 gross (899 net) wells and participated in another 564 gross (86 net) wells completed by other operators. We operate approximately 90% of our current daily production volumes.

Drilling Activity

The following table sets forth the wells we drilled or participated in during the periods indicated. In the table, "gross" refers to the total wells in which we had a working interest and "net" refers to gross wells multiplied by our working interest.

|

| 2013 |

| 2012 |

| 2011 | ||||||||||||||||||||||||||||||

|

| Gross |

| % |

| Net |

| % |

| Gross |

| % |

| Net |

| % |

| Gross |

| % |

| Net |

| % | ||||||||||||

Development: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Productive |

| 1,704 | |

| 99 | |

| 847 | |

| 99 | |

| 2,075 | |

| 99 | |

| 956 | |

| 99 | |

| 2,536 | |

| 99 | |

| 1,077 | |

| 99 | |

Dry |

| 21 | |

| 1 | |

| 9 | |

| 1 | |

| 21 | |

| 1 | |

| 5 | |

| 1 | |

| 10 | |

| 1 | |

| 3 | |

| 1 | |

Total |

| 1,725 | |

| 100 | |

| 856 | |

| 100 | |

| 2,096 | |

| 100 | |

| 961 | |

| 100 | |

| 2,546 | |

| 100 | |

| 1,080 | |

| 100 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Exploratory: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Productive |

| 209 | |

| 97 | |

| 124 | |

| 96 | |

| 495 | |

| 98 | |

| 305 | |

| 98 | |

| 430 | |

| 99 | |

| 201 | |

| 99 | |

Dry |

| 6 | |

| 3 | |

| 5 | |

| 4 | |

| 10 | |

| 2 | |

| 6 | |

| 2 | |

| 3 | |

| 1 | |

| 1 | |

| 1 | |

Total |

| 215 | |

| 100 | |

| 129 | |

| 100 | |

| 505 | |

| 100 | |

| 311 | |

| 100 | |

| 433 | |

| 100 | |

| 202 | |

| 100 | |

The following table shows the wells we drilled or participated in by operating division:

|

| 2013 |

| 2012 |

| 2011 | ||||||||||||

|

| Gross Wells |

| Net Wells |

| Gross Wells |

| Net Wells |

| Gross Wells |

| Net Wells | ||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||

Southern |

| 1,352 | |

| 698 | |

| 1,933 | |

| 982 | |

| 2,691 | |

| 1,166 | |

Northern |

| 588 | |

| 287 | |

| 668 | |

| 290 | |

| 288 | |

| 116 | |

Total |

| 1,940 | |

| 985 | |

| 2,601 | |

| 1,272 | |

| 2,979 | |

| 1,282 | |

At December 31, 2013 , we had 878 (335 net) wells in drilling or completing status.

3

Production, Sales, Prices and Expenses

The following table sets forth information regarding the production volumes, natural gas, oil and NGL sales, average sales prices received, other operating income and expenses for the periods indicated:

|

| Years Ended December 31, | ||||||||||

|

| 2013 |

| 2012 |

| 2011 | ||||||

Net Production: |

|

|

|

|

|

| ||||||

Natural gas (bcf) |

| 1,095 | |

| 1,129 | |

| 1,004 | | |||

Oil (mmbbl) |

| 41 | |

| 31 | |

| 17 | | |||

NGL (mmbbl) |

| 21 | |

| 18 | |

| 15 | | |||

Oil equivalent (mmboe) (a) |

| 244 | |

| 237 | |

| 199 | | |||

Natural Gas, Oil and NGL Sales ($ in millions): |

|

|

|

|

|

| ||||||

Natural gas sales |

| $ | 2,430 | |

| $ | 2,004 | |

| $ | 3,133 | |

Natural gas derivatives - realized gains (losses) |

| 9 | |

| 328 | |

| 1,656 | | |||

Natural gas derivatives - unrealized gains (losses) |

| (52 | ) |

| (331 | ) |

| (669 | ) | |||

Total natural gas sales |

| 2,387 | |

| 2,001 | |

| 4,120 | | |||

Oil sales |

| 3,911 | |

| 2,829 | |

| 1,523 | | |||

Oil derivatives - realized gains (losses) |

| (108 | ) |

| 39 | |

| (60 | ) | |||

Oil derivatives - unrealized gains (losses) |

| 280 | |

| 857 | |

| (128 | ) | |||

Total oil sales |

| 4,083 | |

| 3,725 | |

| 1,335 | | |||

NGL sales |

| 582 | |

| 526 | |

| 603 | | |||

NGL derivatives - realized gains (losses) |

| - | |

| (9 | ) |

| (42 | ) | |||

NGL derivatives - unrealized gains (losses) |

| - | |

| 35 | |

| 8 | | |||

Total NGL sales |

| 582 | |

| 552 | |

| 569 | | |||

Total natural gas, oil and NGL sales |

| $ | 7,052 | |

| $ | 6,278 | |

| $ | 6,024 | |

Average Sales Price (excluding gains (losses) on derivatives): |

|

|

|

|

|

| ||||||

Natural gas ($ per mcf) |

| $ | 2.22 | |

| $ | 1.77 | |

| $ | 3.12 | |

Oil ($ per bbl) |

| $ | 95.17 | |

| $ | 90.49 | |

| $ | 89.80 | |

NGL ($ per bbl) |

| $ | 27.87 | |

| $ | 29.89 | |

| $ | 40.96 | |

Oil equivalent ($ per boe) |

| $ | 28.33 | |

| $ | 22.61 | |

| $ | 26.42 | |

Average Sales Price (including realized gains (losses) on derivatives): |

|

|

|

|

| |||||||

Natural gas ($ per mcf) |

| $ | 2.23 | |

| $ | 2.07 | |

| $ | 4.77 | |

Oil ($ per bbl) |

| $ | 92.53 | |

| $ | 91.74 | |

| $ | 86.25 | |

NGL ($ per bbl) |

| $ | 27.87 | |

| $ | 29.37 | |

| $ | 38.12 | |

Oil equivalent ($ per boe) |

| $ | 27.92 | |

| $ | 24.12 | |

| $ | 34.23 | |

Other Operating Income (b) ($ in millions): |

|

|

|

|

|

| ||||||

Marketing, gathering and compression net margin |

| $ | 98 | |

| $ | 119 | |

| $ | 123 | |

Oilfield services net margin |

| $ | 159 | |

| $ | 142 | |

| $ | 119 | |

Expenses ($ per boe): |

|

|

|

|

|

| ||||||

Natural gas, oil and NGL production |

| $ | 4.74 | |

| $ | 5.50 | |

| $ | 5.39 | |

Production taxes |

| $ | 0.94 | |

| $ | 0.79 | |

| $ | 0.96 | |

General and administrative expenses (c) |

| $ | 1.86 | |

| $ | 2.26 | |

| $ | 2.75 | |

Natural gas, oil and NGL depreciation, depletion and amortization |

| $ | 10.59 | |

| $ | 10.58 | |

| $ | 8.20 | |

Depreciation and amortization of other assets |

| $ | 1.28 | |

| $ | 1.28 | |

| $ | 1.46 | |

Interest expense (d) |

| $ | 0.65 | |

| $ | 0.35 | |

| $ | 0.18 | |

4

___________________________________________

(a) | Oil equivalent is based on six mcf of natural gas to one barrel of oil or one barrel of NGL. This ratio reflects an energy content equivalency and not a price or revenue equivalency. In recent years, the price for a bbl of oil and NGL has been significantly higher than the price for six mcf of natural gas. |

(b) | Includes revenue and operating costs and excludes depreciation and amortization, general and administrative expenses, impairments of fixed assets and other, net gains or losses on sales of fixed assets and interest expense. See Depreciation and Amortization of Other Assets, Impairments of Fixed Assets and Other and Net (Gains) Losses on Sales of Fixed Assets under Results of Operations in Item 7 for details of the depreciation and amortization and impairments of assets and net gains or losses on sales of fixed assets associated with our marketing, gathering and compression and oilfield services operating segments. |

(c) | Includes stock-based compensation and excludes restructuring and other termination costs. |

(d) | Includes the effects of realized (gains) losses from interest rate derivatives, but excludes the effects of unrealized (gains) losses from interest rate derivatives; amount is shown net of amounts capitalized. Realized (gains) losses include settlements related to the current period interest accrual and the effect of (gains) losses on early terminated trades. Unrealized (gains) losses include changes in the fair value of open interest rate derivatives offset by amounts reclassified to realized (gains) losses during the period. |

Natural Gas, Oil and NGL Reserves

The tables below set forth information as of December 31, 2013 with respect to our estimated proved reserves, the associated estimated future net revenue and present value (discounted at an annual rate of 10%) of estimated future net revenue before and after future income taxes (standardized measure) at such date. Neither the pre-tax present value of estimated future net revenue nor the after-tax standardized measure is intended to represent the current market value of the estimated natural gas, oil and NGL reserves we own. All of our estimated natural gas and oil reserves are located within the U.S.

|

| December 31, 2013 | |||||||||||||

|

| Natural Gas |

| Oil |

| NGL |

| Total | |||||||

|

| (bcf) |

| (mmbbl) |

| (mmbbl) |

| (mmboe) | |||||||

Proved developed |

| 8,583 | |

| 201 | |

| 177 | |

| 1,809 | | |||

Proved undeveloped |

| 3,151 | |

| 223 | |

| 122 | |

| 869 | | |||

Total proved (a) |

| 11,734 | |

| 424 | |

| 299 | |

| 2,678 | | |||

|

|

|

|

|

|

|

|

| |||||||

|

| Proved Developed |

| Proved Undeveloped |

| Total Proved | |||||||||

|

| ($ in millions) | |||||||||||||

Estimated future net revenue (b) |

| $ | 30,414 | |

| $ | 17,921 | |

| $ | 48,335 | | |||

Present value of estimated future net revenue (b) |

| $ | 15,371 | |

| $ | 6,305 | |

| $ | 21,676 | | |||

Standardized measure (b)(c) |

| $ | 17,390 | | |||||||||||

Operating Division |

| Natural Gas |

| Oil |

| NGL |

| Oil Equivalent |

| Percent of Proved Reserves |

| Present Value |

| |||||||

|

| (bcf) |

| (mmbbl) |

| (mmbbl) |

| (mmboe) |

|

|

| ($ millions) |

| |||||||

Southern |

| 6,974 | |

| 383 | |

| 220 | |

| 1,766 | |

| 66 | % |

| $ | 15,087 | |

|

Northern |

| 4,760 | |

| 41 | |

| 79 | |

| 912 | |

| 34 | % |

| 6,589 | |

| |

Total |

| 11,734 | |

| 424 | |

| 299 | |

| 2,678 | |

| 100 | % |

| $ | 21,676 | | (b) |

(a) | Includes 61 bcf of natural gas, 2 mmbbl of oil and 6 mmbbl of NGL reserves owned by the Chesapeake Granite Wash Trust, 30 bcf of natural gas, 1 mmbbl of oil and 3 mmbbl of NGL of which are attributable to the noncontrolling interest holders. |

(b) | Estimated future net revenue represents the estimated future gross revenue to be generated from the production of proved reserves, net of estimated production and future development costs, using prices and costs under existing economic conditions as of December 31, 2013 . For the purpose of determining "prices", we used the unweighted arithmetic average of the prices on the first day of each month within the 12-month period ended December 31, 2013 . The prices used in our reserve reports were $3.67 per mcf of natural gas and $96.82 per barrel of oil, before price differential adjustments. Including the effect of price differential adjustments, the prices used in our reserve reports were $2.37 per mcf of natural gas, $95.89 per barrel of oil and $25.78 per barrel of |

5

NGL. These prices should not be interpreted as a prediction of future prices, nor do they reflect the value of our commodity derivative instruments in place as of December 31, 2013 . The amounts shown do not give effect to nonproperty-related expenses, such as corporate general and administrative expenses and debt service, or to depreciation, depletion and amortization. The present value of estimated future net revenue differs from the standardized measure only because the former does not include the effects of estimated future income tax expenses ($4.3 billion as of December 31, 2013 ).

Management uses future net revenue, which is calculated without deducting estimated future income tax expenses, and the present value thereof as a measure of the value of the Company's current proved reserves and to compare relative values among peer companies. We also understand that securities analysts and rating agencies use this measure in similar ways. While future net revenue and the present value thereof are based on prices, costs and discount factors which are consistent from company to company, the standardized measure of discounted future net cash flows is dependent on the unique tax situation of each individual company.

(c) | Additional information on the standardized measure is presented in Supplemental Disclosures About Natural Gas, Oil and NGL Producing Activities included in Item 8 of this report. |

As of December 31, 2013 , our reserve estimates included 869 mmboe of reserves classified as proved undeveloped, compared to 1.124 bboe as of December 31, 2012 . Presented below is a summary of changes in our proved undeveloped reserves (PUDs) for 2013 .

|

| Total | |

|

| (mmboe) | |

Proved undeveloped reserves, beginning of period |

| 1,124 | |

Extensions, discoveries and other additions |

| 351 | |

Revisions of previous estimates |

| (355 | ) |

Developed |

| (169 | ) |

Sale of reserves-in-place |

| (83 | ) |

Purchase of reserves-in-place |

| 1 | |

Proved undeveloped reserves, end of period |

| 869 | |

As of December 31, 2013 , there were no PUDs that had remained undeveloped for five years or more. In 2013 , we invested approximately $1.472 billion, net of drilling and completion cost carries of $79 million, to convert 169 mmboe of PUDs to proved developed reserves. In 2014, we estimate that we will invest approximately $1.506 billion, net of drilling and completion cost carries of $150 million, for PUD conversion. The downward revision of 355 mmboe of PUDs in 2013 related primarily to revised well spacing in our core development area in the Marcellus Shale, the extension of our development plan beyond five years for locations outside the core of our Eagle Ford Shale acreage , the removal of PUDs with only marginally economic estimated production, and a reduction in estimated PUD reserves per well in the Mississippi Lime play.

The future net revenue attributable to our estimated proved undeveloped reserves of $17.921 billion as of December 31, 2013 , and the $6.305 billion present value thereof, has been calculated assuming that we will expend approximately $8.567 billion to develop these reserves: $1.506 billion in 2014, $2.042 billion in 2015, $2.185 billion in 2016, $2.207 billion in 2017 and $600 million in 2018, although the amount and timing of these expenditures will depend on a number of factors, including actual drilling results, service costs, commodity prices and the availability of capital. Chesapeake's developmental drilling schedules are subject to revision and reprioritization throughout the year resulting from unknowable factors such as the relative success in an individual developmental drilling prospect leading to an additional drilling opportunity, title issues and infrastructure availability or constraints.

The SEC's rules for reporting reserves allow the booking of proved undeveloped reserves at locations greater distances from producing wells than immediate offsets. All proved reserves are required to meet reasonable certainty standards; thus, locations that are not direct offsets to producing wells must be shown to be underlain by the productive formation. Reasonable certainty also requires that the formation is continuous between the producing wells and the PUD locations and that the PUDs are economically viable.

6

Our proved reserves as of December 31, 2013 included PUDs more than directly offsetting producing wells in two resource plays: the Marcellus Shale and the Eagle Ford Shale. In all other areas, we restricted PUD locations to immediate offsets to producing wells. Within the Marcellus and Eagle Ford Shale plays, we used both public and proprietary geologic data to establish continuity of the formation and its producing properties. This included seismic data and interpretations (2-D, 3-D and micro seismic); open hole log information (collected both vertically and horizontally) and petrophysical analysis of the log data; mud logs; gas sample analysis; drill cutting samples; measurements of total organic content; thermal maturity; sidewall cores; whole cores; and data measured in our internal core analysis facility. After the geologic area was shown to be continuous, statistical analysis of existing producing wells was conducted to generate an area of reasonable certainty at distances from established production. Undrilled locations within this proved area could be booked as PUDs. However, due to other factors and requirements of SEC reserves reporting rules, numerous locations within the proved area of these two statistically evaluated plays have not yet been booked as PUDs.

Our annual net decline rate on producing properties is projected to be 30% from 2014 to 2015, 20% from 2015 to 2016, 15% from 2016 to 2017, 12% from 2017 to 2018 and 11% from 2018 to 2019. Of our 1.809 bboe of proved developed reserves as of December 31, 2013 , 183 mmboe, or approximately 10%, were non-producing.

Chesapeake's ownership interest used in calculating proved reserves and the associated estimated future net revenue was determined after giving effect to the assumed maximum participation by other parties to our farm-out and participation agreements. The prices used in calculating the estimated future net revenue attributable to proved reserves do not reflect market prices for natural gas and oil production sold subsequent to December 31, 2013 . The estimated proved reserves may not be produced and sold at the assumed prices.

The Company's estimated proved reserves and the standardized measure of discounted future net cash flows of the proved reserves as of December 31, 2013 , 2012 and 2011 , and the changes in quantities and standardized measure of such reserves for each of the three years then ended, are shown in Supplemental Disclosures About Natural Gas, Oil and NGL Producing Activities included in Item 8 of this report. No estimates of proved reserves comparable to those included herein have been included in reports to any federal agency other than the SEC.

There are numerous uncertainties inherent in estimating quantities of proved reserves and in projecting future rates of production and timing of development expenditures, including many factors beyond our control. The reserve data represent only estimates. Reserve engineering is a subjective process of estimating underground accumulations of natural gas and oil that cannot be measured exactly, and the accuracy of any reserve estimate is a function of the quality of available data and of engineering and geological interpretation and judgment. As a result, estimates made by different engineers often vary. In addition, results of drilling, testing and production subsequent to the date of an estimate may justify revision of such estimates, and such revisions may be material. Accordingly, reserve estimates often differ from the actual quantities of natural gas, oil and NGL that are ultimately recovered. Furthermore, the estimated future net revenue from proved reserves and the associated present value are based upon certain assumptions, including prices, future production levels and costs that may not prove correct. Future prices and costs may be materially higher or lower than the prices and costs as of the date of any estimate.

Reserves Estimation

Chesapeake's Corporate Reserves Department prepared approximately 19% of the proved reserves estimates (by volume) disclosed in this report. Those estimates were based upon the best available production, engineering and geologic data.

Chesapeake's Director - Corporate Reserves is the technical person primarily responsible for overseeing the preparation of the Company's reserve estimates. His qualifications include the following:

• | 16 years of practical experience in petroleum engineering, including eight years of this experience in the estimation and evaluation of reserves; |

• | Bachelor of Science degree in Chemical Engineering; and |

• | member in good standing of the Society of Petroleum Engineers. |

We ensure that the key members of the Department have appropriate technical qualifications to oversee the preparation of reserves estimates, including, with respect to our engineers, a minimum of an undergraduate degree in petroleum, mechanical or chemical engineering or other applicable technical discipline. With respect to our engineering technicians, a minimum of a four-year degree in mathematics, economics, finance or other technical/

7

business/science field is required. We maintain a continuous education program for our engineers and technicians on new technologies and industry advancements as well as refresher training on basic skills and analytical techniques.

We maintain internal controls such as the following to ensure the reliability of reserves estimations:

• | We follow comprehensive SEC-compliant internal policies to determine and report proved reserves. Reserves estimates are made by experienced reservoir engineers or under their direct supervision. |

• | The Corporate Reserves Department reviews all of the Company's proved reserves at the close of each quarter. |

• | Each quarter, Corporate Reserves Department managers, the Director - Corporate Reserves, the Vice Presidents of our business units, the Senior Vice Presidents of our operating divisions and the Senior Vice President of Corporate and Strategic Planning review all significant reserves changes and all new proved undeveloped reserves additions. |

• | The Corporate Reserves Department reports independently of our operating divisions. |

We engaged two third-party engineering firms to prepare portions of our reserves estimates comprising approximately 81% of our estimated proved reserves (by volume) at year-end 2013 . The portion of our estimated proved reserves prepared by each of our third-party engineering firms as of December 31, 2013 is presented below.

|

| % Prepared (by Volume) |

| Operating Division | |

Ryder Scott Company, L.P. |

| 51% |

| Northern, Southern | |

PetroTechnical Services, Division of Schlumberger Technology Corporation |

| 30% |

| Northern | |

Copies of the reports issued by the engineering firms are filed with this report as Exhibits 99.1 and 99.2. The qualifications of the technical person at each of these firms primarily responsible for overseeing his firm's preparation of the Company's reserve estimates are set forth below.

Ryder Scott Company, L.P.

• | over 30 years of practical experience in the estimation and evaluation of reserves |

• | registered professional engineer in the state of Texas |

• | Bachelor of Science degree in Electrical Engineering |

• | member in good standing of the Society of Petroleum Engineers and the Society of Petroleum Evaluation Engineers |

PetroTechnical Services, Division of Schlumberger Technology Corporation

• | over 20 years of practical experience in petroleum geology and in the estimation and evaluation of reserves |

• | registered professional geologist license in the Commonwealth of Pennsylvania |

• | certified petroleum geologist of the American Association of Petroleum Geologists |

• | Bachelor of Science degree in Petroleum and Natural Gas Engineering |

8

Costs Incurred in Natural Gas and Oil Property Acquisition, Exploration and Development

The following table sets forth historical costs incurred in natural gas and oil property acquisitions, exploration and development activities during the periods indicated:

|

| Years Ended December 31, | ||||||||||

|

| 2013 |

| 2012 |

| 2011 | ||||||

|

| ($ in millions) | ||||||||||

Acquisition of Properties: |

|

|

|

|

|

| ||||||

Proved properties |

| $ | 22 | |

| $ | 332 | |

| $ | 48 | |

Unproved properties |

| 997 | |

| 2,981 | |

| 4,736 | | |||

Exploratory costs |

| 699 | |

| 2,353 | |

| 2,261 | | |||

Development costs |

| 4,888 | |

| 6,733 | |

| 5,497 | | |||

Costs incurred (a)(b) |

| $ | 6,606 | |

| $ | 12,399 | |

| $ | 12,542 | |

___________________________________________

(a) | Exploratory and development costs are net of joint venture drilling and completion cost carries of $884 million , $784 million and $2.570 billion in 2013 , 2012 and 2011 , respectively. |

(b) | Includes capitalized interest and asset retirement cost as follows: |

Capitalized interest |

| $ | 815 | |

| $ | 976 | |

| $ | 727 | |

Asset retirement obligations |

| $ | 7 | |

| $ | 32 | |

| $ | 3 | |

A summary of our exploration and development, acquisition and divestiture activities in 2013 by operating division is as follows:

|

| Gross Wells Drilled |

| Net Wells Drilled |

| Exploration and Development |

| Acquisition of Unproved Properties |

| Acquisition of Proved Properties |

| Sales of Unproved Properties |

| Sales of Proved Properties |

| Total (a) | ||||||||||||||

|

| ($ in millions) | ||||||||||||||||||||||||||||

Southern |

| 1,352 | |

| 698 | |

| $ | 4,233 | |

| $ | 169 | |

| $ | 22 | |

| $ | (1,252 | ) |

| $ | (1,130 | ) |

| $ | 2,042 | |

Northern |

| 588 | |

| 287 | |

| 1,354 | |

| 828 | |

| - | |

| (570 | ) |

| (411 | ) |

| 1,201 | | ||||||

Total |

| 1,940 | |

| 985 | |

| $ | 5,587 | |

| $ | 997 | |

| $ | 22 | |

| $ | (1,822 | ) |

| $ | (1,541 | ) |

| $ | 3,243 | |

___________________________________________

(a) | Includes capitalized internal costs of $315 million and related capitalized interest of $815 million. |

Acreage

The following table sets forth as of December 31, 2013 the gross and net developed and undeveloped natural gas and oil leasehold and fee mineral acreage. "Gross" acres are the total number of acres in which we own a working interest. "Net" acres refer to gross acres multiplied by our fractional working interest. Acreage numbers do not include our unexercised options to acquire additional acreage.

|

| Developed Leasehold |

| Undeveloped Leasehold |

| Fee Minerals |

| Total | ||||||||||||||||

|

| Gross Acres |

| Net Acres |

| Gross Acres |

| Net Acres |

| Gross Acres |

| Net Acres |

| Gross Acres |

| Net Acres | ||||||||

|

| (in thousands) | ||||||||||||||||||||||

Southern |

| 6,528 | |

| 3,271 | |

| 4,376 | |

| 2,724 | |

| 127 | |

| 18 | |

| 11,031 | |

| 6,013 | |

Northern |

| 2,113 | |

| 1,505 | |

| 8,284 | |

| 4,806 | |

| 752 | |

| 466 | |

| 11,149 | |

| 6,777 | |

Total |

| 8,641 | |

| 4,776 | |

| 12,660 | |

| 7,530 | |

| 879 | |

| 484 | |

| 22,180 | |

| 12,790 | |

Most of our leases have a three- to five-year primary term, and we manage lease expirations to ensure that we do not experience unintended material expirations. Our leasehold management efforts include scheduling our drilling to establish production in paying quantities in order to hold leases by production, timely exercising our contractual rights to pay delay rentals to extend the terms of leases we value, planning noncore divestitures to high-grade our

9

lease inventory and letting some leases expire that are no longer part of our development plans. The following table sets forth as of December 31, 2013 the expiration periods of gross and net undeveloped leasehold acres.

|

| Acres Expiring | ||||

|

| Gross Acres |

| Net Acres | ||

|

| (in thousands) | ||||

Years Ending December 31: |

|

|

|

| ||

2014 |

| 3,335 | |

| 2,219 | |

2015 |

| 2,149 | |

| 1,288 | |

2016 |

| 1,845 | |

| 1,203 | |

After 2016 |

| 5,331 | |

| 2,820 | |

Total (a) |

| 12,660 | |

| 7,530 | |

___________________________________________

(a) | Includes 2.189 million gross (1.132 million net) held-by-production acres that will remain in force as our production continues on the subject leases, and other leasehold acreage where management anticipates the lease to remain in effect past the primary term of the agreement due to our contractual option to extend the lease term. |

Marketing, Gathering and Compression

Marketing

Chesapeake Energy Marketing, Inc., one of our wholly owned subsidiaries, provides natural gas, oil and NGL marketing services, including commodity price structuring, contract administration and nomination services for Chesapeake, other interest owners in Chesapeake-operated wells and other producers. We attempt to enhance the value of natural gas and oil production by aggregating volumes to be sold to various intermediary markets, end markets and pipelines. This aggregation allows us to attract larger, more creditworthy customers that in turn assist in maximizing the prices received.

Natural gas and oil production is generally sold under market-sensitive short-term or spot price contracts. Natural gas and NGL production is sold to purchasers under percentage-of-proceeds contracts, percentage-of-index contracts or spot price contracts. By the terms of the percentage-of-proceeds contracts, we receive a percentage of the resale price received from the ultimate purchaser. Under percentage-of-index contracts, the price we receive is tied to published indices. Although exact percentages vary daily, as of February 2014, approximately 80% of our natural gas production was primarily sold under short-term contracts at market-sensitive prices. There were no sales to individual purchasers constituting 10% or more of total revenues (before the effects of hedging) for the years ended December 31, 2013 and 2011 . Sales to Plains Marketing, L.P. represented 11% of our total revenues (before the effects of hedging) for the year ended December 31, 2012.

Our revenues and operating expenses from our marketing business increased substantially in 2013 compared to 2012. In 2013, we marketed significantly more oil and NGL from both Chesapeake-operated wells and for third parties while our marketing of natural gas was virtually unchanged. Due to the relative high prices of oil and NGL compared to natural gas, our revenues and expenses increased substantially. In addition, we entered into a variety of purchase and sales contracts with third parties for various commercial purposes including credit risk mitigation and to help meet certain of our pipeline delivery commitments. These transactions also increased our marketing revenues and operating expenses.

Midstream Gathering Operations

Historically, Chesapeake invested, directly and through affiliates, in gathering systems and processing facilities to complement our natural gas operations in regions where we had significant production and additional infrastructure was required. These systems were designed primarily to gather the Company's production for delivery into major intrastate or interstate pipelines. In addition, our midstream business provided services to joint working interest owners and other third-party customers. Chesapeake generated revenues from its gathering, treating and compression activities through various gathering rate structures. The Company also processed a portion of its natural gas at various third-party plants.

10

In 2013 and 2012, we sold substantially all of our midstream business and most of our gathering assets. We continue to own the following midstream assets: (i) certain gathering pipelines primarily associated with vertical well production in the northeastern U.S.; (ii) flowlines, which are generally between 200 feet and one mile in length, for our production in each operating area; and (iii) four natural gas processing facilities located in West Virginia. See Note 15 of the notes to the consolidated financial statements included in Item 8 of this report for further discussion of the midstream sale transactions.

Compression Operations

Since 2003, Chesapeake has built its compression business through its wholly owned subsidiary, MidCon Compression, L.L.C. (MidCon). MidCon operates wellhead and system compressors, with over 1.0 million horsepower of compression, to facilitate the transportation of natural gas primarily produced from Chesapeake-operated wells.

Our marketing activities, along with our midstream gathering and compression operations, constitute a reportable segment under accounting guidance for disclosure about segments of an enterprise and related information. See Note 20 of the notes to our consolidated financial statements included in Item 8 of this report.

Oilfield Services

We formed COS Holdings, L.L.C. (formerly Chesapeake Oilfield Services, L.L.C.) (COS) in 2011 to own and operate our oilfield services assets. COS is a diversified oilfield services company that provides a wide range of well site services, primarily to Chesapeake and its working interest partners. These services include drilling, hydraulic fracturing, oilfield rentals, rig relocation, fluid handling and disposal and manufacturing of natural gas compressor packages. These services are fundamental to establishing and maintaining the flow of natural gas and oil throughout the productive life of a well. A source of liquidity for COS's business is the $500 million oilfield services revolving bank credit facility described under Liquidity and Capital Resources in Item 7 of this report. Additionally, in October 2011, Chesapeake Oilfield Operating, L.L.C. (COO), a wholly owned subsidiary of COS, issued $650 million principal amount of 6.625% Senior Notes due 2019. Proceeds from this placement were used to make a cash distribution to its direct parent, COS, to enable it to reduce indebtedness under an intercompany note with Chesapeake. See Note 3 of the notes to the consolidated financial statements included in Item 8 of this report for further discussion of the revolving bank credit facility and senior notes.

Our oilfield services operations constitute a reportable segment under accounting guidance for disclosure about segments of an enterprise and related information. See Note 20 of the notes to our consolidated financial statements included in Item 8 of this report.

On February 24, 2014, we announced that we are pursuing strategic alternatives for COS, including a potential spin-off to Chesapeake shareholders or an outright sale. As of December 31, 2013, COS owned or leased 115 land drilling rigs, including 10 proprietary, fit-for-purpose PeakeRigs TM that utilize advanced electronic drilling technology. Also as of December 31, 2013, COS owned nine hydraulic fracturing fleets with an aggregate of 360,000 horsepower; a diversified oilfield rentals business; an oilfield trucking fleet consisting of 260 rig relocation trucks; 67 cranes and forklifts used to move drilling rigs and other heavy equipment; and 246 fluid hauling trucks.

Competition

We compete with both major integrated and other independent natural gas and oil companies in all aspects of our business to explore, develop and operate our properties and market our production. Some of our competitors may have larger financial and other resources than ours. Competitive conditions may be affected by future legislation and regulations as the U.S. develops new energy and climate-related policies. In addition, some of our larger competitors may have a competitive advantage when responding to factors that affect demand for natural gas and oil production, such as changing prices, domestic and foreign political conditions, weather conditions, the price and availability of alternative fuels, the proximity and capacity of natural gas pipelines and other transportation facilities, and overall economic conditions. We believe that our technological expertise, our exploration, land, drilling and production capabilities and the experience of our management generally enable us to compete effectively.

Derivative Activities

We utilize derivative instruments to provide downside price protection on a portion of our future natural gas and oil production and to manage interest rate exposure. See Item 7A. Quantitative and Qualitative Disclosures About Market Risk .

11

Regulation

General

All of our operations are conducted onshore in the U.S. The U.S. natural gas and oil industry is regulated at the federal, state and local levels, and some of the laws, rules and regulations that govern our operations carry substantial administrative, civil and criminal penalties for non-compliance. Although we believe we are in substantial compliance with all applicable laws and regulations, and that remaining in substantial compliance with existing requirements will not have a material adverse effect on our financial position, cash flows or results of operations, such laws and regulations could be, and frequently are, amended or reinterpreted. Additionally, currently unforeseen environmental incidents may occur or past non-compliance with environmental laws or regulations may be discovered. Therefore, we are unable to predict the future costs or impacts of compliance or non-compliance. Additional proposals and proceedings that affect the natural gas and oil industry are regularly considered by Congress, the states, the local governments, the courts and federal agencies, such as the U.S. Environmental Protection Agency (EPA), the Federal Energy Regulatory Commission (FERC), the Department of Transportation (DOT), the Department of Interior and the Department of Energy. We actively monitor regulatory developments regarding our industry in order to anticipate and design required compliance activities and systems.

Exploration and Production Operations

The laws and regulations applicable to our exploration and production operations include requirements for permits to drill and to conduct other operations and for provision of financial assurances (such as bonds) covering drilling and well operations. Other activities subject to such laws and regulations include, but are not limited to:

• | the location of wells; |

• | the method of drilling and completing wells; |

• | the surface use and restoration of properties upon which oil and gas facilities are located, including the construction of well pads, pipelines, impoundments and associated access roads; |

• | water withdrawal; |

• | the plugging and abandoning of wells; |

• | the recycling or disposal of fluids used or other substances handled in connection with operations; |

• | the marketing, transportation and reporting of production; and |

• | the valuation and payment of royalties. |

Our operations may require us to obtain permits for, among other things,

• | air emissions; |

• | construction activities, including in sensitive areas, such as wetlands, coastal regions or areas that contain endangered or threatened species or their habitats; |

• | the construction and operation of underground injection wells to dispose of produced water and other non-hazardous oilfield wastes; and |

• | the construction and operation of surface pits to contain drilling muds and other non-hazardous fluids associated with drilling operations. |

Delays in obtaining permits or an inability to obtain new permits or permit renewals could inhibit our ability to execute our drilling and production plans. Failure to comply with provisions of our permits could result in revocation of such permits and the imposition of fines and penalties.

Our exploration and production activities are also subject to various conservation regulations. These include the regulation of the size of drilling and spacing units (regarding the density of wells that may be drilled in a particular area) and the unitization or pooling of natural gas and oil properties. In this regard, some states, such as Oklahoma, allow the forced pooling or integration of tracts to facilitate exploration, while other states, such as Texas, West Virginia and Pennsylvania, rely on voluntary pooling of lands and leases. In areas where pooling is voluntary, it may be more difficult to form units and therefore, more difficult to fully develop a project if the operator owns or controls less than 100% of the leasehold. In addition, state conservation laws establish maximum rates of production from natural gas and oil wells, generally limit the venting or flaring of natural gas and impose certain requirements regarding the ratability of

12

production. The effect of these regulations is to limit the amount of natural gas and oil we can produce and to limit the number of wells and the locations at which we can drill.

Oilfield Services Operations

Our oilfield services business operates under the jurisdiction of a number of regulatory bodies that regulate worker safety standards, the handling of hazardous materials, the transportation of explosives and other hazardous materials, the protection of the environment and standards of operation for driving. Regulations concerning equipment certification create an ongoing need for regular maintenance that is incorporated into our operating procedures.

In providing trucking services, we operate as a motor carrier and therefore are subject to regulation by the DOT and various state agencies. These regulatory authorities exercise broad powers governing activities such as the authorization to engage in motor carrier operations and regulatory safety, financial reporting and certain mergers, consolidations and acquisitions. Interstate motor carrier operations are subject to safety requirements prescribed by the DOT and, to a large degree, intrastate motor carrier operations are subject to safety regulations that mirror federal regulations. Such matters as weight and dimension of equipment are also subject to federal and state regulations, and DOT regulations mandate drug testing of drivers. Additional regulations specifically relate to the trucking industry, including testing and specification of equipment and product handling requirements. Our compliance with certain DOT regulations is tracked by DOT's Federal Motor Carrier Safety Administration, which develops a company-specific safety rating based on inspections of our motor carrier operations. Our safety rating can directly affect the Company's ability to obtain and renew permits and authorizations.

The trucking industry is subject to possible regulatory and legislative changes that may affect the economics of the industry by requiring changes in operating practices or by changing the demand for common or contract carrier services or the cost of providing truckload services. Some of these possible changes include increasingly stringent environmental regulations, changes in the hours of service regulations that govern the amount of time a driver may drive in any specific period, onboard black box recorder devices or limits on vehicle weight and size. From time to time, various legislative proposals are introduced, such as proposals to increase federal, state, or local taxes, including taxes on motor fuels, which may increase our costs or adversely impact the recruitment of drivers. We cannot predict whether, or in what form, any increase in such taxes applicable to us will be enacted.

Midstream Operations

Historically, Chesapeake invested, directly and through an affiliate, in gathering systems and processing facilities to complement our natural gas operations in regions where we had significant production and additional infrastructure was required. In 2013 and 2012, we sold substantially all of our midstream business and most of our gathering assets. As a result, the impact on our business of compliance with the laws and regulations described below has decreased significantly beginning in late 2012.

In addition to the environmental, health and safety laws and regulations discussed below under Environmental, Health and Safety Matters , a small amount of our midstream facilities is subject to federal regulation by the Pipeline and Hazardous Materials Safety Administration (PHMSA) of the DOT pursuant to the Natural Gas Pipeline Safety Act of 1968 (NGPSA) and the Pipeline Safety Improvement Act of 2002 which was reauthorized and amended by the Pipeline Inspection, Protection, Enforcement and Safety Act of 2006. The NGPSA regulates safety requirements in the design, construction, operation and maintenance of gas pipeline facilities.

States are largely preempted by federal law from regulating pipeline safety for interstate lines but most are certified by the DOT to assume responsibility for enforcing federal intrastate pipeline regulations and inspection of intrastate pipelines. In practice, because states can adopt stricter standards for intrastate pipelines than those imposed by the federal government for interstate lines, states vary considerably in their assertion of authority and capacity to address pipeline safety. Our natural gas pipelines have inspection and compliance programs designed to keep the facilities in compliance with applicable pipeline safety and pollution control laws and regulations.

Natural gas gathering and intrastate transportation facilities are exempt from the jurisdiction of the FERC under the Natural Gas Act. Although the FERC has made no formal determinations with regard to any of our facilities, we believe that our natural gas pipelines and related facilities are engaged in exempt gathering and intrastate transportation and, therefore, are not subject to the FERC's jurisdiction.

FERC regulation affects our gathering and compression business generally. The FERC provides policies and practices across a range of natural gas regulatory activities, including, for example, its policies on open access transportation, market manipulation, ratemaking, capacity release and market transparency, and market center

13

promotion, which indirectly affect our gathering and compression business. In addition, the distinction between FERC-regulated transmission facilities and federally unregulated gathering and intrastate transportation facilities is a fact-based determination made by the FERC on a case-by-case basis; this distinction has also been the subject of regular litigation and change. The classification and regulation of our gathering and intrastate transportation facilities are subject to change based on future determinations by the FERC, the courts and Congress.

Our natural gas gathering operations are subject to ratable take and common purchaser statutes in most of the states in which we operate. These statutes generally require our gathering pipelines to take natural gas without undue discrimination as to source of supply or producer. These statutes are designed to prohibit discrimination in favor of one producer over another producer or one source of supply over another source of supply. The regulations under these statutes can have the effect of imposing restrictions on our ability as an owner of gathering facilities to decide with whom we contract to gather natural gas. The states in which we operate typically have adopted a complaint-based regulation of natural gas gathering activities, which allows natural gas producers and shippers to file complaints with state regulators in an effort to resolve grievances relating to gathering access and rate discrimination.

Environmental, Health and Safety Matters

Our operations are subject to stringent and complex federal, state and local laws and regulations relating to the protection of human health and safety, the environment and natural resources. These laws and regulations can restrict or impact our business activities in many ways, such as:

• | requiring the installation of pollution-control equipment or otherwise restricting the way we can handle or dispose of wastes and other substances connected with operations; |

• | limiting or prohibiting construction activities in sensitive areas, such as wetlands, coastal regions or areas that contain endangered or threatened species or their habitats; |

• | requiring investigatory and remedial actions to address pollution conditions caused by our operations or attributable to former operations; |

• | requiring noise mitigation, setbacks, landscaping, fencing, and other measures; |

• | prohibiting the operations of facilities deemed to be in non-compliance with permits issued pursuant to such environmental laws and regulations; and |

• | restricting access to certain equipment or areas to a limited set of employees or contractors who have proper certification or permits to conduct work (e.g., confined space entry and process safety maintenance requirements). |

Failure to comply with these laws and regulations may trigger a variety of administrative, civil and criminal enforcement measures, including the assessment of monetary penalties, the imposition of remedial or restoration obligations, and the issuance of orders enjoining future operations or imposing additional compliance requirements. Certain environmental statutes impose strict, joint and several liability for costs required to clean up and restore sites where hazardous substances, hydrocarbons or wastes have been disposed or otherwise released. Moreover, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the release of hazardous substances, hydrocarbons or other waste products into the environment. In addition, local land use restrictions, such as city ordinances, zoning laws, and traffic regulations, may restrict or prohibit the performance of well drilling in general or hydraulic fracturing in particular.

The trend in environmental regulation is to place more restrictions and limitations on activities that may affect the environment. We monitor developments at the federal, state and local levels to anticipate future regulatory requirements that might be imposed to reduce the costs of compliance with any such requirements. We also participate in industry groups that help formulate recommendations for addressing existing or future regulations and that share best practices and lessons learned in relation to pollution prevention and incident investigations.

Below is a discussion of the material environmental, health and safety laws and regulations that relate to our business. We believe that we are in substantial compliance with these laws and regulations. We do not believe that compliance with existing environmental, health and safety laws or regulations will have a material adverse effect on our financial condition, results of operations or cash flow. At this point, however, we cannot reasonably predict what applicable laws, regulations or guidance may eventually be adopted with respect to our operations or the ultimate cost to comply with such requirements.

14

Hazardous Substances and Waste

Federal and state laws, in particular the federal Resource Conservation and Recovery Act, or RCRA, regulate hazardous and non-hazardous solid wastes. In the course of our operations, we generate petroleum hydrocarbon wastes such as produced water and ordinary industrial wastes. Under a longstanding legal framework, certain of these wastes are not subject to federal regulations governing hazardous wastes, although they are regulated under other federal and state waste laws.

Federal, state and local laws may also require us to remove or remediate previously disposed wastes or hazardous substances otherwise released into the environment, including wastes or hazardous substances disposed of or released by us or prior owners or operators in accordance with current laws or otherwise, to suspend or cease operations at contaminated areas, or to perform remedial well plugging operations or response actions to reduce the risk of future contamination. Federal laws, including the Comprehensive Environmental Response, Compensation, and Liability Act, or CERCLA, and analogous state laws impose joint and several liability, without regard to fault or legality of the original conduct, on classes of persons who are considered legally responsible for releases of a hazardous substance into the environment. These persons include the owner or operator of the site where the release occurred, persons who disposed of or arranged for the disposal of hazardous substances at the site, and any person who accepted hazardous substances for transportation to the site. CERCLA and analogous state laws also authorize the EPA, state environmental agencies and, in some cases, third parties to take action to prevent or respond to threats to human health or the environment and to seek to recover from responsible classes of persons the costs of such actions.

The Safe Drinking Water Act (SDWA), Underground Injection Control (UIC) program prohibits any underground injection unless authorized by a permit. Chesapeake recycles and reuses some produced water and we also dispose of produced water in Class II UIC wells, which are designed and permitted to place the water into deep geologic formations, isolated from fresh water sources. Permits for Class II UIC wells may be issued by the EPA or by a state environmental agency if EPA has delegated its UIC Program authority.

Air Emissions

Our operations are subject to the federal Clean Air Act (CAA) and comparable state laws and regulations. These laws and regulations regulate emissions of air pollutants from various industrial sources, including our compressor stations, and impose various monitoring and reporting requirements. Permits and related compliance obligations under the CAA, each state's development and promulgation of regulatory programs to comport with federal requirements, as well as changes to state implementation plans for controlling air emissions in regional non-attainment or near-non-attainment areas, may require natural gas and oil exploration and production operators to incur future capital expenditures in connection with the addition or modification of existing air emission control equipment and strategies.

In 2012, the EPA published final New Source Performance Standards (NSPS) and National Emissions Standards for Hazardous Air Pollutants (NESHAP) that amended the existing NSPS and NESHAP standards for oil and gas facilities and created new NSPS standards for oil and gas production, transmission and distribution facilities. While these rules remain in effect, the EPA announced in 2013 that it would reexamine and reissue the rules over the next three years. The EPA has issued updated rules regarding storage tanks and additional rules are expected. In 2010, the EPA published rules that require monitoring and reporting of greenhouse gas emissions from petroleum and natural gas systems. We, along with other industry groups, filed suit challenging certain provisions of the rules and are engaged in settlement negotiations to amend and correct the rules. The EPA is also conducting a review of the National Ambient Air Quality Standards for ozone, but an expected completion date for that review is not currently known.

Water Discharges

The federal Water Pollution Control Act, or the Clean Water Act (CWA), and analogous state laws impose restrictions and strict controls regarding the discharge of pollutants into state waters as well as waters of the U.S. The placement of material into jurisdictional water or wetlands of the U.S. is prohibited, except in accordance with the terms of a permit issued by the United States Army Corps of Engineers. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the EPA or a state agency delegated with EPA's authority. Further, Chesapeake's corporate policy prohibits discharge of produced water to surface waters. See Item 3. Legal Proceedings for a description of a consent decree that we recently entered into with the U.S. and the West Virginia Department of Environmental Protection in connection with alleged civil violations of the CWA related to well pads, pond sites and a compressor station that we formerly owned in West Virginia. Spill prevention, control and countermeasure requirements of federal laws require appropriate containment berms and similar structures to help prevent the contamination of regulated waters in the event of a hydrocarbon tank spill, rupture or leak. In addition, the

15

CWA and analogous state laws require individual permits or coverage under general permits for discharges of storm water runoff from certain types of facilities.

The Oil Pollution Act of 1990 (OPA) establishes strict liability for owners and operators of facilities that are the site of a release of oil into waters of the U.S. The OPA and its associated regulations impose a variety of requirements on responsible parties related to the prevention of oil spills and liability for damages resulting from such spills. A ''responsible party'' under the OPA includes owners and operators of certain onshore facilities from which a release may affect waters of the U.S.

Health and Safety

The Occupational Safety and Health Act (OSHA) and comparable state laws regulate the protection of the health and safety of our employees. The federal Occupational Safety and Health Administration has established workplace safety standards that provide guidelines for maintaining a safe workplace in light of potential hazards, such as employee exposure to hazardous substances. OSHA also requires employee training and maintenance of records, and the OSHA hazard communication standard and EPA community right-to-know regulations under the Emergency Planning and Community Right-to-Know Act of 1986 require that we organize and/or disclose information about hazardous materials used or produced in our operations.

Hydraulic Fracturing

Vast quantities of natural gas, natural gas liquids and oil deposits exist in deep shale and other unconventional formations. It is customary in our industry to recover these resources through the use of hydraulic fracturing, combined with horizontal drilling. Hydraulic fracturing is the process of creating or expanding cracks, or fractures, in deep underground formations using water, sand and other additives pumped under high pressure into the formation. As with the rest of the industry, we use hydraulic fracturing as a means to increase the productivity of almost every well that we drill and complete. These formations are generally geologically separated and isolated from fresh ground water supplies by thousands of feet of impermeable rock layers.

We follow applicable legal requirements for groundwater protection in our operations that are subject to supervision by state and federal regulators (including the Bureau of Land Management (BLM) on federal acreage). Furthermore, our well construction practices require the installation of multiple layers of protective steel casing surrounded by cement that are specifically designed and installed to protect freshwater aquifers by preventing the migration of fracturing fluids into aquifers .

Injection rates and pressures are required to be monitored in real time at the surface during our hydraulic fracturing operations. Pressure is required to be monitored on both the injection string and the immediate annulus to the injection string. Hydraulic fracturing operations are required to be shut down if an abrupt change occurs to the injection pressure or annular pressure. These aspects of hydraulic fracturing operations are designed to prevent a pathway for the fracturing fluid to contact any aquifers during the hydraulic fracturing operations.

Hydraulic fracture stimulation requires the use of water. We use fresh water or recycled produced water in our fracturing treatments in accordance with applicable water management plans and laws. We strive to find alternative sources of water and reduce our reliance on fresh water resources. We have technical staff dedicated to the development of water recycling and re-use systems, and our Aqua Renew® program uses state-of-the-art technology in an effort to recycle produced water in our operations.