Table of Contents

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended March 31, 2018

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 1-768

CATERPILLAR INC.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation) |

| 37-0602744 (IRS Employer I.D. No.) |

|

|

|

510 Lake Cook Road, Suite 100, Deerfield, Illinois (Address of principal executive offices) |

| 60015 (Zip Code) |

Registrant's telephone number, including area code: (224) 551-4000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x | Accelerated filer | o |

|

|

|

|

Non-accelerated filer | o | (Do not check if a smaller reporting company) |

|

|

|

|

|

|

| Smaller reporting company | o |

|

|

|

|

|

| Emerging growth company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

At March 31, 2018 , 597,904,900 shares of common stock of the registrant were outstanding.

|

Table of Contents

Table of Contents

Part I. Financial Information |

|

|

Item 1. | Financial Statements | 3 |

Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 51 |

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 74 |

Item 4. | Controls and Procedures | 74 |

|

|

|

Part II. Other Information |

|

|

Item 1. | Legal Proceedings | 75 |

Item 1A. | Risk Factors | * |

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 75 |

Item 3. | Defaults Upon Senior Securities | * |

Item 4. | Mine Safety Disclosures | * |

Item 5. | Other Information | * |

Item 6. | Exhibits | 76 |

* Item omitted because no answer is called for or item is not applicable.

2

Table of Contents

Part I. FINANCIAL INFORMATION

Item 1. Financial Statements

Caterpillar Inc.

Consolidated Statement of Results of Operations

(Unaudited)

(Dollars in millions except per share data)

| Three Months Ended | ||||||

| 2018 |

| 2017 | ||||

Sales and revenues: |

|

|

| ||||

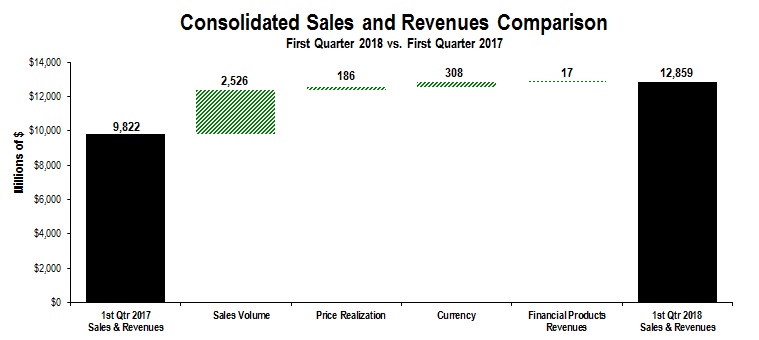

Sales of Machinery, Energy & Transportation | $ | 12,150 | |

| $ | 9,130 | |

Revenues of Financial Products | 709 | |

| 692 | | ||

Total sales and revenues | 12,859 | |

| 9,822 | | ||

|

|

|

| ||||

Operating costs: |

| |

|

| | ||

Cost of goods sold | 8,566 | |

| 6,801 | | ||

Selling, general and administrative expenses | 1,276 | |

| 1,061 | | ||

Research and development expenses | 443 | |

| 425 | | ||

Interest expense of Financial Products | 166 | |

| 159 | | ||

Other operating (income) expenses | 300 | |

| 996 | | ||

Total operating costs | 10,751 | |

| 9,442 | | ||

|

|

|

| ||||

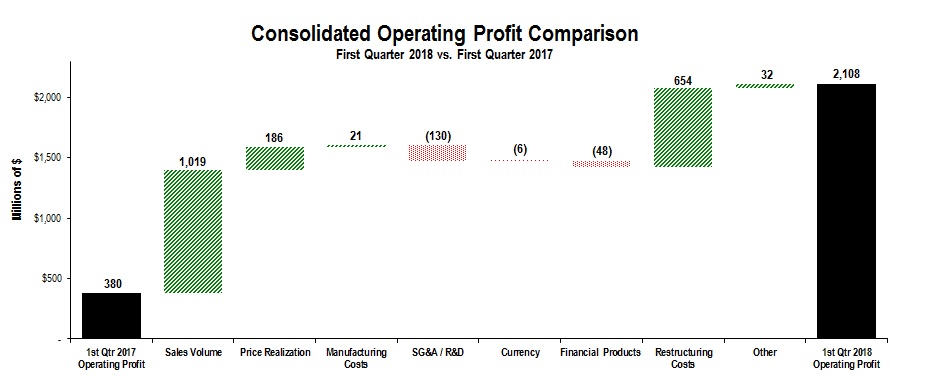

Operating profit | 2,108 | |

| 380 | | ||

|

|

|

| ||||

Interest expense excluding Financial Products | 101 | |

| 123 | | ||

Other income (expense) | 127 | |

| 32 | | ||

|

|

|

| ||||

Consolidated profit before taxes | 2,134 | |

| 289 | | ||

|

|

|

| ||||

Provision (benefit) for income taxes | 472 | |

| 90 | | ||

Profit of consolidated companies | 1,662 | |

| 199 | | ||

|

|

|

| ||||

Equity in profit (loss) of unconsolidated affiliated companies | 5 | |

| (5 | ) | ||

|

|

|

| ||||

Profit of consolidated and affiliated companies | 1,667 | |

| 194 | | ||

|

|

|

| ||||

Less: Profit (loss) attributable to noncontrolling interests | 2 | |

| 2 | | ||

|

|

|

| ||||

Profit 1 | $ | 1,665 | |

| $ | 192 | |

|

|

|

| ||||

Profit per common share | $ | 2.78 | |

| $ | 0.33 | |

|

|

|

| ||||

Profit per common share – diluted 2 | $ | 2.74 | |

| $ | 0.32 | |

|

|

|

| ||||

Weighted-average common shares outstanding (millions) |

| |

|

| | ||

– Basic | 598.0 | |

| 587.5 | | ||

– Diluted 2 | 608.0 | |

| 593.2 | | ||

|

|

|

| ||||

Cash dividends declared per common share | $ | - | |

| $ | - | |

1 Profit attributable to common shareholders.

2 Diluted by assumed exercise of stock-based compensation awards using the treasury stock method.

See accompanying notes to Consolidated Financial Statements.

3

Table of Contents

Caterpillar Inc .

Consolidated Statement of Comprehensive Income

(Unaudited)

(Dollars in millions)

| Three Months Ended | ||||||

| 2018 |

| 2017 | ||||

|

|

|

| ||||

Profit of consolidated and affiliated companies | $ | 1,667 | |

| $ | 194 | |

Other comprehensive income (loss), net of tax: |

|

|

| ||||

Foreign currency translation, net of tax (provision)/benefit of: 2018 - $15; 2017 - $7 | 184 | |

| 147 | | ||

|

|

|

| ||||

Pension and other postretirement benefits: | |

|

| ||||

Current year prior service credit (cost), net of tax (provision)/benefit of: 2018 - $1; 2017 - $(4) | (2 | ) |

| 8 | | ||

Amortization of prior service (credit) cost, net of tax (provision)/benefit of: 2018 - $2; 2017 - $1 | (7 | ) |

| (4 | ) | ||

|

|

|

| ||||

Derivative financial instruments: |

|

|

| ||||

Gains (losses) deferred, net of tax (provision)/benefit of: 2018 - $(1); 2017 - $(5) | 5 | |

| 10 | | ||

(Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2018 - $(6); 2017 - $(22) | 18 | |

| 40 | | ||

|

|

|

| ||||

Available-for-sale securities: |

|

|

| ||||

Gains (losses) deferred, net of tax (provision)/benefit of: 2018 - $2; 2017 - $(6) | (11 | ) |

| 8 | | ||

(Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2018 - $0; 2017 - $(1) | - | |

| 3 | | ||

|

|

|

| ||||

Total other comprehensive income (loss), net of tax | 187 | |

| 212 | | ||

Comprehensive income | 1,854 | |

| 406 | | ||

Less: comprehensive income attributable to the noncontrolling interests | (2 | ) |

| (2 | ) | ||

Comprehensive income attributable to shareholders | $ | 1,852 | |

| $ | 404 | |

|

|

|

| ||||

See accompanying notes to Consolidated Financial Statements.

4

Table of Contents

Caterpillar Inc .

Consolidated Statement of Financial Position

(Unaudited)

(Dollars in millions)

| March 31, |

| December 31, | ||||

Assets |

|

|

| ||||

Current assets: |

| |

|

| | ||

Cash and short-term investments | $ | 7,888 | |

| $ | 8,261 | |

Receivables – trade and other | 7,894 | |

| 7,436 | | ||

Receivables – finance | 8,772 | |

| 8,757 | | ||

Prepaid expenses and other current assets | 1,856 | |

| 1,772 | | ||

Inventories | 10,947 | |

| 10,018 | | ||

Total current assets | 37,357 | |

| 36,244 | | ||

|

|

|

| ||||

Property, plant and equipment – net | 13,912 | |

| 14,155 | | ||

Long-term receivables – trade and other | 1,004 | |

| 990 | | ||

Long-term receivables – finance | 13,359 | |

| 13,542 | | ||

Noncurrent deferred and refundable income taxes | 1,687 | |

| 1,693 | | ||

Intangible assets | 2,163 | |

| 2,111 | | ||

Goodwill | 6,376 | |

| 6,200 | | ||

Other assets | 2,156 | |

| 2,027 | | ||

Total assets | $ | 78,014 | |

| $ | 76,962 | |

|

|

|

| ||||

Liabilities |

| |

|

| | ||

Current liabilities: |

| |

|

| | ||

Short-term borrowings: |

| |

|

| | ||

Machinery, Energy & Transportation | $ | 7 | |

| $ | 1 | |

Financial Products | 5,726 | |

| 4,836 | | ||

Accounts payable | 6,938 | |

| 6,487 | | ||

Accrued expenses | 3,551 | |

| 3,220 | | ||

Accrued wages, salaries and employee benefits | 1,474 | |

| 2,559 | | ||

Customer advances | 1,399 | |

| 1,426 | | ||

Dividends payable | - | |

| 466 | | ||

Other current liabilities | 1,890 | |

| 1,742 | | ||

Long-term debt due within one year: |

| |

|

| | ||

Machinery, Energy & Transportation | 8 | | | 6 | | ||

Financial Products | 6,409 | |

| 6,188 | | ||

Total current liabilities | 27,402 | |

| 26,931 | | ||

|

|

|

| ||||

Long-term debt due after one year: |

| |

|

| | ||

Machinery, Energy & Transportation | 7,980 | |

| 7,929 | | ||

Financial Products | 15,185 | |

| 15,918 | | ||

Liability for postemployment benefits | 8,233 | |

| 8,365 | | ||

Other liabilities | 3,942 | |

| 4,053 | | ||

Total liabilities | 62,742 | |

| 63,196 | | ||

Commitments and contingencies (Notes 10 and 13) | | |

| | | ||

Shareholders' equity |

| |

|

| | ||

Common stock of $1.00 par value: |

| |

|

| | ||

Authorized shares: 2,000,000,000 | 5,640 | |

| 5,593 | | ||

Treasury stock (3/31/18 – 216,989,724 shares; 12/31/17 – 217,268,852 shares) at cost | (17,347 | ) |

| (17,005 | ) | ||

Profit employed in the business | 27,929 | |

| 26,301 | | ||

Accumulated other comprehensive income (loss) | (1,016 | ) |

| (1,192 | ) | ||

Noncontrolling interests | 66 | |

| 69 | | ||

Total shareholders' equity | 15,272 | |

| 13,766 | | ||

Total liabilities and shareholders' equity | $ | 78,014 | |

| $ | 76,962 | |

See accompanying notes to Consolidated Financial Statements.

5

Table of Contents

Caterpillar Inc.

Consolidated Statement of Changes in Shareholders' Equity

(Unaudited)

(Dollars in millions)

| Common stock |

| Treasury stock |

| Profit employed in the business |

| Accumulated other comprehensive income (loss) |

| Noncontrolling interests |

| Total | ||||||||||||

Three Months Ended March 31, 2017 |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Balance at December 31, 2016 | $ | 5,277 | |

| $ | (17,478 | ) |

| $ | 27,377 | |

| $ | (2,039 | ) |

| $ | 76 | |

| $ | 13,213 | |

Adjustment to adopt stock-based compensation guidance 1 | - | |

| - | |

| 15 | |

| - | |

| - | |

| 15 | | ||||||

Balance at January 1, 2017 | $ | 5,277 | |

| $ | (17,478 | ) |

| $ | 27,392 | |

| $ | (2,039 | ) |

| $ | 76 | |

| $ | 13,228 | |

Profit of consolidated and affiliated companies | - | |

| - | |

| 192 | |

| - | |

| 2 | |

| 194 | | ||||||

Foreign currency translation, net of tax | - | |

| - | |

| - | |

| 147 | |

| - | |

| 147 | | ||||||

Pension and other postretirement benefits, net of tax | - | |

| - | |

| - | |

| 4 | |

| - | |

| 4 | | ||||||

Derivative financial instruments, net of tax | - | |

| - | |

| - | |

| 50 | |

| - | |

| 50 | | ||||||

Available-for-sale securities, net of tax | - | |

| - | |

| - | |

| 11 | |

| - | |

| 11 | | ||||||

Distribution to noncontrolling interests | - | |

| - | |

| - | |

| - | |

| (6 | ) |

| (6 | ) | ||||||

Common shares issued from treasury stock for stock-based compensation: 2,604,284 | (106 | ) |

| 87 | |

| - | |

| - | |

| - | |

| (19 | ) | ||||||

Stock-based compensation expense | 49 | |

| - | |

| - | |

| - | |

| - | |

| 49 | | ||||||

Other | 2 | |

| - | |

| - | |

| - | |

| - | |

| 2 | | ||||||

Balance at March 31, 2017 | $ | 5,222 | |

| $ | (17,391 | ) |

| $ | 27,584 | |

| $ | (1,827 | ) |

| $ | 72 | |

| $ | 13,660 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Three Months Ended March 31, 2018 |

| |

|

| |

|

| |

|

| |

|

| |

|

| | ||||||

Balance at December 31, 2017 | $ | 5,593 | |

| $ | (17,005 | ) |

| $ | 26,301 | |

| $ | (1,192 | ) |

| $ | 69 | |

| $ | 13,766 | |

Adjustments to adopt new accounting guidance 1 |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Revenue recognition | - | |

| - | |

| (12 | ) |

| - | |

| - | |

| $ | (12 | ) | |||||

Tax accounting for intra-entity asset transfers | - | |

| - | |

| (35 | ) |

| - | |

| - | |

| $ | (35 | ) | |||||

Recognition and measurement of financial assets and liabilities | - | |

| - | |

| 11 | |

| (11 | ) |

| - | |

| $ | - | | |||||

Balance at January 1, 2018 | $ | 5,593 | |

| $ | (17,005 | ) |

| $ | 26,265 | |

| $ | (1,203 | ) |

| $ | 69 | |

| $ | 13,719 | |

Profit of consolidated and affiliated companies | - | |

| - | |

| 1,665 | |

| - | |

| 2 | |

| 1,667 | | ||||||

Foreign currency translation, net of tax | - | |

| - | |

| - | |

| 184 | |

| - | |

| 184 | | ||||||

Pension and other postretirement benefits, net of tax | - | |

| - | |

| - | |

| (9 | ) |

| - | |

| (9 | ) | ||||||

Derivative financial instruments, net of tax | - | |

| - | |

| - | |

| 23 | |

| - | |

| 23 | | ||||||

Available-for-sale securities, net of tax | - | |

| - | |

| - | |

| (11 | ) |

| - | |

| (11 | ) | ||||||

Change in ownership from noncontrolling interests | 2 | |

| - | |

| - | |

| - | |

| (5 | ) |

| (3 | ) | ||||||

Dividends declared | - | |

| - | |

| (1 | ) |

| - | |

| - | |

| (1 | ) | ||||||

Common shares issued from treasury stock for stock-based compensation: 3,426,757 | (9 | ) |

| 158 | |

| - | |

| - | |

| - | |

| 149 | | ||||||

Stock-based compensation expense | 50 | |

| - | |

| - | |

| - | |

| - | |

| 50 | | ||||||

Common shares repurchased: 3,147,629 2 | - | |

| (500 | ) |

| - | |

| - | |

| - | |

| (500 | ) | ||||||

Other | 4 | |

| - | |

| - | |

| - | |

| - | |

| 4 | | ||||||

Balance at March 31, 2018 | $ | 5,640 | |

| $ | (17,347 | ) |

| $ | 27,929 | |

| $ | (1,016 | ) |

| $ | 66 | |

| $ | 15,272 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

1 See Note 2 for additional information. |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

2 See Note 11 for additional information. |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

See accompanying notes to Consolidated Financial Statements.

6

Table of Contents

Caterpillar Inc.

Consolidated Statement of Cash Flow

(Unaudited)

(Millions of dollars)

| Three Months Ended | ||||||

| 2018 |

| 2017 | ||||

Cash flow from operating activities: |

|

|

| ||||

Profit of consolidated and affiliated companies | $ | 1,667 | |

| $ | 194 | |

Adjustments for non-cash items: |

| |

|

| | ||

Depreciation and amortization | 681 | |

| 710 | | ||

Other | 148 | |

| 302 | | ||

Changes in assets and liabilities, net of acquisitions and divestitures: |

| |

|

| | ||

Receivables – trade and other | (326 | ) |

| (353 | ) | ||

Inventories | (803 | ) |

| (444 | ) | ||

Accounts payable | 486 | |

| 732 | | ||

Accrued expenses | 66 | |

| 132 | | ||

Accrued wages, salaries and employee benefits | (1,110 | ) |

| 360 | | ||

Customer advances | (46 | ) |

| 234 | | ||

Other assets – net | 165 | |

| (261 | ) | ||

Other liabilities – net | 7 | |

| (64 | ) | ||

Net cash provided by (used for) operating activities | 935 | |

| 1,542 | | ||

|

|

|

| ||||

Cash flow from investing activities: |

| |

|

| | ||

Capital expenditures – excluding equipment leased to others | (412 | ) |

| (204 | ) | ||

Expenditures for equipment leased to others | (345 | ) |

| (305 | ) | ||

Proceeds from disposals of leased assets and property, plant and equipment | 258 | |

| 234 | | ||

Additions to finance receivables | (2,621 | ) |

| (2,122 | ) | ||

Collections of finance receivables | 2,671 | |

| 2,272 | | ||

Proceeds from sale of finance receivables | 69 | |

| 17 | | ||

Investments and acquisitions (net of cash acquired) | (340 | ) |

| (18 | ) | ||

Proceeds from sale of businesses and investments (net of cash sold) | 12 | |

| - | | ||

Proceeds from sale of securities | 89 | |

| 89 | | ||

Investments in securities | (197 | ) |

| (65 | ) | ||

Other – net | 16 | |

| 9 | | ||

Net cash provided by (used for) investing activities | (800 | ) |

| (93 | ) | ||

|

|

|

| ||||

Cash flow from financing activities: |

| |

|

| | ||

Dividends paid | (467 | ) |

| (452 | ) | ||

Common stock issued, including treasury shares reissued | 149 | |

| (19 | ) | ||

Common shares repurchased | (500 | ) |

| - | | ||

Proceeds from debt issued (original maturities greater than three months): |

| |

|

| | ||

Machinery, Energy & Transportation | - | |

| 360 | | ||

Financial Products | 1,541 | |

| 2,355 | | ||

Payments on debt (original maturities greater than three months): |

| |

|

| | ||

Machinery, Energy & Transportation | (1 | ) |

| (4 | ) | ||

Financial Products | (2,408 | ) |

| (1,974 | ) | ||

Short-term borrowings – net (original maturities three months or less) | 1,151 | |

| 618 | | ||

Other – net | (3 | ) |

| (6 | ) | ||

Net cash provided by (used for) financing activities | (538 | ) |

| 878 | | ||

Effect of exchange rate changes on cash | 10 | |

| 9 | | ||

Increase (decrease) in cash and short-term investments and restricted cash | (393 | ) |

| 2,336 | | ||

Cash and short-term investments and restricted cash at beginning of period | 8,320 | |

| 7,199 | | ||

Cash and short-term investments and restricted cash at end of period | $ | 7,927 | |

| $ | 9,535 | |

All short-term investments, which consist primarily of highly liquid investments with original maturities of three months or less, are considered to be cash equivalents .

See accompanying notes to Consolidated Financial Statements.

7

Table of Contents

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. | A. Nature of operations |

Information in our financial statements and related commentary are presented in the following categories:

Machinery, Energy & Transportation (ME&T) – Represents the aggregate total of Construction Industries, Resource Industries, Energy & Transportation and All Other operating segments and related corporate items and eliminations.

Financial Products – Primarily includes the company's Financial Products Segment. This category includes Caterpillar Financial Services Corporation (Cat Financial), Caterpillar Insurance Holdings Inc. (Insurance Services) and their respective subsidiaries.

B. Basis of presentation

In the opinion of management, the accompanying unaudited financial statements include all adjustments, consisting only of normal recurring adjustments, necessary for a fair statement of (a) the consolidated results of operations for the three months ended March 31, 2018 and 2017 , (b) the consolidated comprehensive income for the three months ended March 31, 2018 and 2017 , (c) the consolidated financial position at March 31, 2018 and December 31, 2017 , (d) the consolidated changes in shareholders' equity for the three months ended March 31, 2018 and 2017 and (e) the consolidated cash flow for the three months ended March 31, 2018 and 2017 . The financial statements have been prepared in conformity with generally accepted accounting principles in the United States of America (U.S. GAAP) and pursuant to the rules and regulations of the Securities and Exchange Commission (SEC).

Interim results are not necessarily indicative of results for a full year. The information included in this Form 10-Q should be read in conjunction with the audited financial statements and notes thereto included in our company's annual report on Form 10-K for the year ended December 31, 2017 ( 2017 Form 10-K).

The December 31, 2017 financial position data included herein is derived from the audited consolidated financial statements included in the 2017 Form 10-K but does not include all disclosures required by U.S. GAAP. Certain amounts for prior periods have been reclassified to conform to the current period financial statement presentation. See Note 2 for more information. In addition, deferred revenue of $233 million was reclassified from Other current liabilities to Customer advances in the December 31, 2017 Consolidated Statement of Financial Position.

Unconsolidated Variable Interest Entities (VIEs)

We have affiliates, suppliers and dealers that are VIEs of which we are not the primary beneficiary. Although we have provided financial support, we do not have the power to direct the activities that most significantly impact the economic performance of each entity.

Our maximum exposure to loss from VIEs for which we are not the primary beneficiary was as follows:

|

|

|

|

|

| ||||

(Millions of dollars) |

| March 31, 2018 |

| December 31, 2017 |

| ||||

Receivables - trade and other |

| $ | 30 | |

| $ | 34 | |

|

Receivables - finance |

| 43 | |

| 42 | |

| ||

Long-term receivables - finance |

| 34 | |

| 38 | |

| ||

Investments in unconsolidated affiliated companies |

| 30 | |

| 39 | |

| ||

Guarantees 1 |

| - | |

| 259 | |

| ||

Total |

| $ | 137 | |

| $ | 412 | |

|

|

|

|

|

|

| ||||

1 Related contract was terminated during the first quarter of 2018. No payments were made under the guarantee.

|

|

|

|

|

8

Table of Contents

In addition, Cat Financial has end-user customers that are VIEs of which we are not the primary beneficiary. Although we have provided financial support to these entities and therefore have a variable interest, we do not have the power to direct the activities that most significantly impact their economic performance. Our maximum exposure to loss from our involvement with these VIEs is limited to the credit risk inherently present in the financial support that we have provided. These risks are evaluated and reflected in our financial statements as part of our overall portfolio of finance receivables and related allowance for credit losses.

2. New accounting guidance

Revenue recognition – In May 2014, the Financial Accounting Standards Board (FASB) issued new revenue recognition guidance to provide a single, comprehensive revenue recognition model for all contracts with customers. Under the new guidance, an entity will recognize revenue to depict the transfer of promised goods or services to customers at an amount that the entity expects to be entitled to in exchange for those goods or services. A five step model has been introduced for an entity to apply when recognizing revenue. The new guidance also includes enhanced disclosure requirements. The guidance was effective January 1, 2018, and was applied to contracts that were not completed at the date of initial application on a modified retrospective basis through a cumulative effect adjustment to retained earnings as of January 1, 2018. The prior period comparative information has not been recasted and continues to be reported under the accounting guidance in effect for those periods.

Under the new guidance, sales of certain turbine machinery units changed to a point-in-time recognition model. Under previous guidance, we accounted for these sales under an over-time model following the percentage-of-completion method as the product was manufactured. In addition, under the new guidance we began to recognize an asset for the value of expected replacement part returns and discontinued lease accounting treatment for certain product sales containing residual value guarantees.

See Note 3 for additional information.

The cumulative effect of initially applying the new revenue recognition guidance to our consolidated financial statements on January 1, 2018 was as follows:

Consolidated Statement of Financial Position |

|

|

|

|

|

| ||||||

(Millions of dollars) |

| Balance as of December 31, 2017 |

| Cumulative Impact from Adopting New Revenue Guidance |

| Balance as of January 1, 2018 | ||||||

Assets |

|

|

|

|

|

| ||||||

Receivables - trade and other |

| $ | 7,436 | |

| $ | (66 | ) |

| $ | 7,370 | |

Prepaid expenses and other current assets |

| $ | 1,772 | |

| $ | 327 | |

| $ | 2,099 | |

Inventories |

| $ | 10,018 | |

| $ | 4 | |

| $ | 10,022 | |

Property, plant and equipment - net |

| $ | 14,155 | |

| $ | (190 | ) |

| $ | 13,965 | |

Noncurrent deferred and refundable income taxes |

| $ | 1,693 | |

| $ | 2 | |

| $ | 1,695 | |

|

|

|

|

|

|

| ||||||

Liabilities |

|

|

|

|

|

| ||||||

Accrued expenses |

| $ | 3,220 | |

| $ | 226 | |

| $ | 3,446 | |

Customer advances |

| $ | 1,426 | |

| $ | 46 | |

| $ | 1,472 | |

Other current liabilities |

| $ | 1,742 | |

| $ | (17 | ) |

| $ | 1,725 | |

Other liabilities |

| $ | 4,053 | |

| $ | (166 | ) |

| $ | 3,887 | |

|

|

|

|

|

|

| ||||||

Shareholders' equity |

|

|

|

|

|

| ||||||

Profit employed in the business |

| $ | 26,301 | |

| $ | (12 | ) |

| $ | 26,289 | |

|

|

|

|

|

|

| ||||||

9

Table of Contents

The impact from adopting the new revenue recognition guidance on our consolidated financial statements was as follows:

|

| Three Months Ended March 31, 2018 | ||||||||||

(Millions of dollars) |

| As Reported |

| Previous Accounting Guidance |

| Impact from Adopting New Revenue Guidance | ||||||

Consolidated Statement of Results of Operations |

|

|

|

|

|

| ||||||

Sales of Machinery, Energy & Transportation |

| $ | 12,150 | |

| $ | 12,145 | |

| $ | 5 | |

Cost of goods sold |

| $ | 8,566 | |

| $ | 8,560 | |

| $ | 6 | |

Other operating (income) expenses |

| $ | 300 | |

| $ | 306 | |

| $ | (6 | ) |

Operating profit |

| $ | 2,108 | |

| $ | 2,103 | |

| $ | 5 | |

Consolidated profit before taxes |

| $ | 2,134 | |

| $ | 2,129 | |

| $ | 5 | |

Provision (benefit) for income taxes |

| $ | 472 | |

| $ | 471 | |

| $ | 1 | |

Profit (loss) of consolidated companies |

| $ | 1,662 | |

| $ | 1,658 | |

| $ | 4 | |

Profit (loss) of consolidated and affiliated companies |

| $ | 1,667 | |

| $ | 1,663 | |

| $ | 4 | |

Profit |

| $ | 1,665 | |

| $ | 1,661 | |

| $ | 4 | |

|

|

|

|

|

|

| ||||||

Consolidated Statement of Financial Position |

|

|

|

|

|

| ||||||

Assets |

|

|

|

|

|

| ||||||

Receivables - trade and other |

| $ | 7,894 | |

| $ | 7,907 | |

| $ | (13 | ) |

Prepaid expenses and other current assets |

| $ | 1,856 | |

| $ | 1,568 | |

| $ | 288 | |

Inventories |

| $ | 10,947 | |

| $ | 10,956 | |

| $ | (9 | ) |

Noncurrent deferred and refundable income taxes |

| $ | 1,687 | |

| $ | 1,686 | |

| $ | 1 | |

|

|

|

|

|

|

| ||||||

Liabilities |

|

|

|

|

|

| ||||||

Accrued expenses |

| $ | 3,551 | |

| $ | 3,325 | |

| $ | 226 | |

Customer advances |

| $ | 1,399 | |

| $ | 1,350 | |

| $ | 49 | |

|

|

|

|

|

|

| ||||||

Shareholders' equity |

|

|

|

|

|

| ||||||

Profit employed in the business |

| $ | 27,929 | |

| $ | 27,937 | |

| $ | (8 | ) |

|

|

|

|

|

|

| ||||||

Recognition and measurement of financial assets and financial liabilities – In January 2016, the FASB issued accounting guidance that affects the accounting for equity investments, financial liabilities accounted for under the fair value option and the presentation and disclosure requirements for financial instruments. Under the new guidance, all equity investments in unconsolidated entities (other than those accounted for using the equity method of accounting) will generally be measured at fair value through earnings. There will no longer be an available-for-sale classification for equity securities with readily determinable fair values. For financial liabilities when the fair value option has been elected, changes in fair value due to instrument-specific credit risk will be recognized separately in other comprehensive income. In addition, the FASB clarified guidance related to the valuation allowance assessment when recognizing deferred tax assets resulting from unrealized losses on available-for-sale debt securities. The guidance was effective January 1, 2018, and was applied on a modified retrospective basis through a cumulative effect adjustment to retained earnings as of January 1, 2018. The adoption did not have a material impact on our financial statements.

Lease accounting – In February 2016, the FASB issued accounting guidance that revises the accounting for leases. Under the new guidance, lessees are required to recognize a right-of-use asset and a lease liability for substantially all leases. The new guidance will continue to classify leases as either financing or operating, with classification affecting the pattern of expense recognition. The accounting applied by a lessor under the new guidance will be substantially equivalent to current lease accounting guidance. The new guidance is effective January 1, 2019, with early adoption permitted. The new standard is required to be applied with a modified retrospective approach to each prior reporting period presented and provides for certain practical expedients. An implementation team is currently designing new processes and controls and evaluating our population of leased assets to assess the effect of the new guidance on our financial statements. We plan to adopt the new guidance effective January 1, 2019.

10

Table of Contents

Measurement of credit losses on financial instruments – In June 2016, the FASB issued accounting guidance to introduce a new model for recognizing credit losses on financial instruments based on an estimate of current expected credit losses. The new guidance will apply to loans, accounts receivable, trade receivables, other financial assets measured at amortized cost, loan commitments and other off-balance sheet credit exposures. The new guidance will also apply to debt securities and other financial assets measured at fair value through other comprehensive income. The new guidance is effective January 1, 2020, with early adoption permitted beginning January 1, 2019. We are in the process of evaluating the effect of the new guidance on our financial statements.

Classification for certain cash receipts and cash payments – In August 2016, the FASB issued accounting guidance related to the presentation and classification of certain transactions in the statement of cash flows where diversity in practice exists. The guidance was effective January 1, 2018, and was applied on a retrospective basis. The adoption did not have a material impact on our financial statements.

Tax accounting for intra-entity asset transfers – In October 2016, the FASB issued accounting guidance that requires the recognition of tax expense from the sales of intra-entity assets in the seller's tax jurisdiction at the time of transfer. The new guidance does not apply to intra-entity transfers of inventory. Under previous guidance, the tax effects of these assets were deferred until the transferred asset was sold to a third party or otherwise recovered through use. The guidance was effective January 1, 2018, and was applied on a modified retrospective basis through a cumulative effect adjustment to retained earnings as of January 1, 2018. The adoption did not have a material impact on our financial statements.

Classification of restricted cash – In November 2016, the FASB issued accounting guidance related to the presentation and classification of changes in restricted cash on the statement of cash flows where diversity in practice exists. The guidance was effective January 1, 2018, and was applied on a retrospective basis. The adoption did not have a material impact on our financial statements.

Presentation of net periodic pension costs and net periodic postretirement benefit costs – In March 2017, the FASB issued accounting guidance that requires that an employer disaggregate the service cost component from the other components of net benefit cost. Service cost is required to be reported in the same line item or items as other compensation costs arising from services rendered by the pertinent employees during the period. The other components of net periodic benefit cost are required to be reported outside the subtotal for income from operations. Additionally, only the service cost component of net benefit costs is eligible for capitalization. The guidance was effective January 1, 2018. We applied the presentation changes retrospectively and the capitalization change prospectively. The adoption primarily resulted in the reclassification of other components of net periodic benefit cost outside of Operating profit in the Consolidated Statement of Results of Operations.

Consolidated Statement of Results of Operations | Three Months Ended March 31, 2017 | ||||||||||

(Millions of dollars) | As Revised |

| Previously Reported |

| Effect of Change | ||||||

Cost of goods sold | $ | 6,801 | |

| $ | 6,758 | |

| $ | 43 | |

Selling, general and administrative expenses | $ | 1,061 | |

| $ | 1,045 | |

| $ | 16 | |

Research and development expenses | $ | 425 | |

| $ | 418 | |

| $ | 7 | |

Other operating (income) expenses | $ | 996 | |

| $ | 1,025 | |

| $ | (29 | ) |

Total operating costs | $ | 9,442 | |

| $ | 9,405 | |

| $ | 37 | |

Operating profit | $ | 380 | |

| $ | 417 | |

| $ | (37 | ) |

Other income (expense) | $ | 32 | |

| $ | (5 | ) |

| $ | 37 | |

|

|

|

|

|

| ||||||

Premium amortization on purchased callable debt securities – In March 2017, the FASB issued accounting guidance related to the amortization period for certain purchased callable debt securities held at a premium. Securities held at a premium will be required to be amortized to the earliest call date rather than the maturity date. The new standard is required to be applied with a modified retrospective approach through a cumulative-effect adjustment directly to retained earnings as of the beginning of the period of adoption. The guidance is effective January 1, 2019, with early adoption permitted. We do not expect the adoption to have a material impact on our financial statements.

Clarification on stock-based compensation – In May 2017, the FASB issued accounting guidance to clarify which changes to the terms or conditions of a share-based payment award require an entity to apply modification accounting.

11

Table of Contents

The guidance was effective January 1, 2018, and was applied prospectively. The adoption did not have a material impact on our financial statements.

Derivatives and hedging – In August 2017, the FASB issued accounting guidance to better align hedge accounting with a company's risk management activities, simplify the application of hedge accounting and improve the disclosures of hedging arrangements. The new guidance is required to be applied on a modified retrospective basis, resulting in a cumulative-effect adjustment to opening retained earnings in the period of adoption. The guidance is effective January 1, 2019, with early adoption permitted. The impact on our financial statements at the time of adoption will primarily be reclassification of our gains (losses) for designated ME&T foreign exchange contracts from Other income (expense) to components of Operating profit in the Consolidated Statement of Results of Operations.

Reclassification of certain tax effects from accumulated other comprehensive income – In February 2018, the FASB issued accounting guidance to allow a reclassification from accumulated other comprehensive income to retained earnings for stranded tax effects resulting from U.S. tax reform legislation. The new guidance is required to be applied either in the period of adoption or retrospectively to each period affected by U.S. tax reform legislation. The guidance is effective January 1, 2019, with early adoption permitted. We are in the process of evaluating the effect of the new guidance on our financial statements.

3. | Sales and revenue recognition |

A. Sales of Machinery, Energy & Transportation

Sales of Machinery, Energy & Transportation are recognized when all the following criteria are satisfied: (i) a contract with an independently owned and operated dealer or an end user exists which has commercial substance; (ii) it is probable we will collect the amount charged to the dealer or end user; and (iii) we have completed our performance obligation whereby the dealer or end user has obtained control of the product. A contract with commercial substance exists once we receive and accept a purchase order under a dealer sales agreement, or once we enter into a contract with an end user. If collectability is not probable, the sale is deferred and not recognized until collection is probable or payment is received. Control of our products typically transfers when title and risk of ownership of the product has transferred to the dealer or end user. Typically, where product is produced and sold in the same country, title and risk of ownership transfer when the product is shipped. Products that are exported from a country for sale typically transfer title and risk of ownership at the border of the destination country.

Our remanufacturing operations are primarily focused on the remanufacture of Cat engines and components and rail related products. In this business, used engines and related components (core) are inspected, cleaned and remanufactured. In connection with the sale of our remanufactured product to dealers, we collect a deposit that is repaid if the dealer returns an acceptable core within a specified time period. Caterpillar owns and has title to the cores when they are returned from dealers. The rebuilt engine or component (the core plus any new content) is then sold as a remanufactured product to dealers and end users. Revenue is recognized pursuant to the same criteria as Machinery, Energy & Transportation sales noted above (title and risk of ownership of the entire remanufactured product passes to the dealer or end user upon sale). At the time of sale, the deposit is recognized in Other current liabilities in the Consolidated Statement of Financial Position, and the core to be returned is recognized as an asset in Prepaid expenses and other current assets in the Consolidated Statement of Financial Position at the estimated replacement cost (based on historical experience with usable cores). Upon receipt of an acceptable core, we repay the deposit and relieve the liability. The returned core is then included in inventory. In the event that the deposit is forfeited (i.e. upon failure by the dealer to return an acceptable core in the specified time period), we recognize the core deposit and the cost of the core in Sales and Cost of goods sold, respectively.

We provide discounts to dealers through merchandising programs. We have numerous programs that are designed to promote the sale of our products. The most common dealer programs provide a discount when the dealer sells a product to a targeted end user. Generally, the cost of these discounts is estimated for each product by model by geographic region based on historical experience and known changes in merchandising programs. The cost of these discounts is reported as a reduction to the transaction price when the product sale is recognized. A corresponding post-sale discount reserve is accrued in the Consolidated Statement of Financial Position, which represents discounts we expect to pay on previously sold units. If discounts paid differ from those estimated, the difference is reported as a change in the transaction price.

Except for replacement parts, no right of return exists on the sale of our products. We estimate replacement part returns based on historical experience and recognize a parts return asset in Prepaid expenses and other current assets in the

12

Table of Contents

Consolidated Statement of Financial Position, which represents our right to recover replacement parts we expect will be returned. We also recognize a refund liability in Other current liabilities in the Consolidated Statement of Financial Position for the refund we expect to pay for returned parts. If actual replacement part returns differ from those estimated, the difference in the estimated replacement part return asset and refund liability is recognized in Cost of goods sold and Sales, respectively.

Our standard dealer invoice terms are established by marketing region. Our invoice terms for end user sales are established by the responsible business unit. Payments from dealers are due shortly after the time of sale. When a sale is made to a dealer, the dealer is responsible for payment even if the product is not sold to an end user. Dealers and end users must make payment within the established invoice terms to avoid potential interest costs. Interest at or above prevailing market rates may be charged on any past due balance, and generally our practice is to not forgive this interest. In addition, Cat Financial provides wholesale inventory financing for a dealer's purchase of inventory. Wholesale inventory receivables have varying payment terms and are included in Receivables - trade and other and Long-term receivables - trade and other in the Consolidated Statement of Financial Position. Trade receivables from dealers and end users were $6,821 million and $6,399 million as of March 31, 2018 and January 1, 2018, respectively, and are recognized in Receivables - trade and other in the Consolidated Statement of Financial Position. Long-term trade receivables from dealers and end users were $614 million and $639 million as of March 31, 2018 and January 1, 2018, respectively, and are recognized in Long-term receivables - trade and other in the Consolidated Statement of Financial Position.

We establish a bad debt allowance for Machinery, Energy & Transportation receivables when it becomes probable that the receivable will not be collected. Our allowance for bad debts is not significant.

We invoice in advance of recognizing the sale of certain products. Advanced customer payments are recognized as a contract liability in Customer advances and Other liabilities in the Consolidated Statement of Financial Position. Long-term customer advances recognized in Other liabilities in the Consolidated Statement of Financial Position were $424 million and $396 million as of March 31, 2018 and January 1, 2018, respectively. We reduce the contract liability when revenue is recognized. During the three-month period ending March 31, 2018 , we recognized $617 million of revenue that was recorded as a contract liability at the beginning of the period.

We have elected the practical expedient to not adjust the amount of revenue to be recognized under a contract with a dealer or end user for the effects of time value of money when the timing difference between receipt of payment and recognition of revenue is less than one year.

As of March 31, 2018 , we have entered into contracts with dealers and end users for which sales have not been recognized as we have not satisfied our performance obligations and transferred control of the products. The dollar amount of unsatisfied performance obligations for contracts with an original duration greater than one year is $5.5 billion , of which $2.4 billion is expected to be completed and revenue recognized in the twelve months following March 31, 2018 . We have elected the practical expedient to not disclose unsatisfied performance obligations with an original contract duration of one year or less. Contracts with an original duration of one year or less are primarily sales to dealers for machinery, engines and replacement parts.

Sales and other related taxes are excluded from the transaction price. Shipping and handling costs associated with outbound freight after control over a product has transferred are accounted for as a fulfillment cost and are included in Cost of goods sold.

We provide a standard manufacturer's warranty of our products at no additional cost. At the time a sale is recognized, we record estimated future warranty costs. See Note 10 for further discussion of our product warranty liabilities.

See Note 15 for further disaggregated sales and revenues information.

B. Revenues of Financial Products

Revenues of Financial Products are generated primarily from finance revenue on finance receivables and rental payments on operating leases. Finance revenue is recorded over the life of the related finance receivable using the interest method, including the accretion of certain direct origination costs that are deferred. Revenue from rental payments received on operating leases is recognized on a straight-line basis over the term of the lease.

13

Table of Contents

Recognition of finance revenue and rental revenue is suspended and the account is placed on non-accrual status when management determines that collection of future income is not probable (generally after 120 days past due). Recognition is resumed, and previously suspended income is recognized, when the account becomes current and collection of remaining amounts is considered probable. See Note 16 for more information.

Revenues are presented net of sales and other related taxes.

4. Stock-based compensation

Accounting for stock-based compensation requires that the cost resulting from all stock-based payments be recognized in the financial statements based on the grant date fair value of the award. Our stock-based compensation primarily consists of stock options, restricted stock units (RSUs), performance-based restricted stock units (PRSUs) and stock-settled stock appreciation rights (SARs).

Beginning with the 2018 grant, RSU and PRSU awards are credited with dividend equivalent units on each date that a cash dividend is paid to holders of Common Stock. The fair value of the RSU and PRSU awards granted in 2018 was determined as the closing stock price on the date of grant. Prior to 2018, RSU and PRSU awards were not credited with dividend equivalent units and the fair value was determined by reducing the stock price on the date of grant by the present value of the estimated dividends to be paid during the vesting period. The estimated dividends were based on Caterpillar's quarterly dividend per share at the time of grant.

We recognized pretax stock-based compensation expense of $50 million and $49 million for the three months ended March 31, 2018 and 2017, respectively.

The following table illustrates the type and fair value of the stock-based compensation awards granted during the three months ended March 31, 2018 and 2017 , respectively:

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

| Three Months Ended March 31, 2018 |

| Three Months Ended March 31, 2017 | ||||||||||||||||||

| Shares Granted |

| Weighted-Average Fair Value Per Share |

| Weighted-Average Grant Date Stock Price |

| Shares Granted |

| Weighted-Average Fair Value Per Share |

| Weighted-Average Grant Date Stock Price | ||||||||||

Stock options | 1,566,788 | |

| $ | 46.18 | |

| $ | 151.12 | |

| 2,701,644 | |

| $ | 25.01 | |

| $ | 95.66 | |

RSUs | 676,228 | |

| $ | 151.12 | |

| $ | 151.12 | |

| 906,068 | |

| $ | 89.76 | |

| $ | 95.63 | |

PRSUs | 339,559 | |

| $ | 151.12 | |

| $ | 151.12 | |

| 437,385 | |

| $ | 86.78 | |

| $ | 95.66 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

The following table provides the assumptions used in determining the fair value of the stock-based awards for the three months ended March 31, 2018 and 2017 , respectively:

|

|

|

|

| Grant Year | ||

| 2018 |

| 2017 |

Weighted-average dividend yield | 2.70% |

| 3.42% |

Weighted-average volatility | 30.2% |

| 29.2% |

Range of volatilities | 21.5-33.0% |

| 22.1-33.0% |

Range of risk-free interest rates | 2.02-2.87% |

| 0.81-2.35% |

Weighted-average expected lives | 8 years |

| 8 years |

|

|

|

|

As of March 31, 2018 , the total remaining unrecognized compensation expense related to nonvested stock-based compensation awards was $327 million , which will be amortized over the weighted-average remaining requisite service periods of approximately 2.0 years.

14

Table of Contents

5. Derivative financial instruments and risk management

Our earnings and cash flow are subject to fluctuations due to changes in foreign currency exchange rates, interest rates and commodity prices. Our Risk Management Policy (policy) allows for the use of derivative financial instruments to prudently manage foreign currency exchange rate, interest rate and commodity price exposures. Our policy specifies that derivatives are not to be used for speculative purposes. Derivatives that we use are primarily foreign currency forward, option and cross currency contracts, interest rate contracts and commodity forward and option contracts. Our derivative activities are subject to the management, direction and control of our senior financial officers. Risk management practices, including the use of financial derivative instruments, are presented to the Audit Committee of the Board of Directors at least annually.

All derivatives are recognized on the Consolidated Statement of Financial Position at their fair value. On the date the derivative contract is entered into, we designate the derivative as (1) a hedge of the fair value of a recognized asset or liability (fair value hedge), (2) a hedge of a forecasted transaction or the variability of cash flow (cash flow hedge) or (3) an undesignated instrument. Changes in the fair value of a derivative that is qualified, designated and highly effective as a fair value hedge, along with the gain or loss on the hedged recognized asset or liability that is attributable to the hedged risk, are recorded in current earnings. Changes in the fair value of a derivative that is qualified, designated and highly effective as a cash flow hedge are recorded in Accumulated other comprehensive income (loss) (AOCI), to the extent effective, on the Consolidated Statement of Financial Position until they are reclassified to earnings in the same period or periods during which the hedged transaction affects earnings. Changes in the fair value of undesignated derivative instruments and the ineffective portion of designated derivative instruments are reported in current earnings. Cash flows from designated derivative financial instruments are classified within the same category as the item being hedged on the Consolidated Statement of Cash Flow. Cash flows from undesignated derivative financial instruments are included in the investing category on the Consolidated Statement of Cash Flow.

We formally document all relationships between hedging instruments and hedged items, as well as the risk-management objective and strategy for undertaking various hedge transactions. This process includes linking all derivatives that are designated as fair value hedges to specific assets and liabilities on the Consolidated Statement of Financial Position and linking cash flow hedges to specific forecasted transactions or variability of cash flow.

We also formally assess, both at the hedge's inception and on an ongoing basis, whether the designated derivatives that are used in hedging transactions are highly effective in offsetting changes in fair values or cash flow of hedged items. When a derivative is determined not to be highly effective as a hedge or the underlying hedged transaction is no longer probable, we discontinue hedge accounting prospectively, in accordance with the derecognition criteria for hedge accounting.

Foreign Currency Exchange Rate Risk

Foreign currency exchange rate movements create a degree of risk by affecting the U.S. dollar value of sales made and costs incurred in foreign currencies. Movements in foreign currency rates also affect our competitive position as these changes may affect business practices and/or pricing strategies of non-U.S.-based competitors. Additionally, we have balance sheet positions denominated in foreign currencies, thereby creating exposure to movements in exchange rates.

Our Machinery, Energy & Transportation operations purchase, manufacture and sell products in many locations around the world. As we have a diversified revenue and cost base, we manage our future foreign currency cash flow exposure on a net basis. We use foreign currency forward and option contracts to manage unmatched foreign currency cash inflow and outflow. Our objective is to minimize the risk of exchange rate movements that would reduce the U.S. dollar value of our foreign currency cash flow. Our policy allows for managing anticipated foreign currency cash flow for up to five years. As of March 31, 2018 , the maximum term of these outstanding contracts was approximately 51 months .

We generally designate as cash flow hedges at inception of the contract any Australian dollar, Brazilian real, British pound, Canadian dollar, Chinese yuan, Indian rupee, Japanese yen, Mexican peso, Singapore dollar or Thailand baht forward or option contracts that meet the requirements for hedge accounting and the maturity extends beyond the current quarter-end. Designation is performed on a specific exposure basis to support hedge accounting. The remainder of Machinery, Energy & Transportation foreign currency contracts are undesignated.

As of March 31, 2018 , $16 million of deferred net gains, net of tax, included in equity (AOCI in the Consolidated Statement of Financial Position), are expected to be reclassified to current earnings (Other income (expense) in the Consolidated Statement of Results of Operations) over the next twelve months when earnings are affected by the hedged

15

Table of Contents

transactions. The actual amount recorded in Other income (expense) will vary based on exchange rates at the time the hedged transactions impact earnings.

In managing foreign currency risk for our Financial Products operations, our objective is to minimize earnings volatility resulting from conversion and the remeasurement of net foreign currency balance sheet positions, and future transactions denominated in foreign currencies. Our policy allows the use of foreign currency forward, option and cross currency contracts to offset the risk of currency mismatch between our assets and liabilities, and exchange rate risk associated with future transactions denominated in foreign currencies. Our foreign currency forward and option contracts are primarily undesignated. We designate fixed-to-fixed cross currency contracts as cash flow hedges to protect against movements in exchange rates on foreign currency fixed-rate assets and liabilities.

Interest Rate Risk

Interest rate movements create a degree of risk by affecting the amount of our interest payments and the value of our fixed-rate debt. Our practice is to use interest rate contracts to manage our exposure to interest rate changes.

Our Machinery, Energy & Transportation operations generally use fixed-rate debt as a source of funding. Our objective is to minimize the cost of borrowed funds. Our policy allows us to enter into fixed-to-floating interest rate contracts and forward rate agreements to meet that objective. We designate fixed-to-floating interest rate contracts as fair value hedges at inception of the contract, and we designate certain forward rate agreements as cash flow hedges at inception of the contract.

Financial Products operations has a match-funding policy that addresses interest rate risk by aligning the interest rate profile (fixed or floating rate) of Cat Financial's debt portfolio with the interest rate profile of their receivables portfolio within predetermined ranges on an ongoing basis. In connection with that policy, we use interest rate derivative instruments to modify the debt structure to match assets within the receivables portfolio. This matched funding reduces the volatility of margins between interest-bearing assets and interest-bearing liabilities, regardless of which direction interest rates move.

Our policy allows us to use fixed-to-floating, floating-to-fixed and floating-to-floating interest rate contracts to meet the match-funding objective. We designate fixed-to-floating interest rate contracts as fair value hedges to protect debt against changes in fair value due to changes in the benchmark interest rate. We designate most floating-to-fixed interest rate contracts as cash flow hedges to protect against the variability of cash flows due to changes in the benchmark interest rate.

We have, at certain times, liquidated fixed-to-floating and floating-to-fixed interest rate contracts at both Machinery, Energy & Transportation and Financial Products. The gains or losses associated with these contracts at the time of liquidation are amortized into earnings over the original term of the previously designated hedged item.

Commodity Price Risk

Commodity price movements create a degree of risk by affecting the price we must pay for certain raw material. Our policy is to use commodity forward and option contracts to manage the commodity risk and reduce the cost of purchased materials.

Our Machinery, Energy & Transportation operations purchase base and precious metals embedded in the components we purchase from suppliers. Our suppliers pass on to us price changes in the commodity portion of the component cost. In addition, we are subject to price changes on energy products such as natural gas and diesel fuel purchased for operational use.

Our objective is to minimize volatility in the price of these commodities. Our policy allows us to enter into commodity forward and option contracts to lock in the purchase price of a portion of these commodities within a five -year horizon. All such commodity forward and option contracts are undesignated.

16

Table of Contents

The location and fair value of derivative instruments reported in the Consolidated Statement of Financial Position are as follows:

|

|

|

|

|

| ||||

(Millions of dollars) | Consolidated Statement of Financial |

| Asset (Liability) Fair Value | ||||||

| Position Location |

| March 31, 2018 |

| December 31, 2017 | ||||

Designated derivatives |

|

|

|

|

| ||||

Foreign exchange contracts |

|

|

| |

|

| | ||

Machinery, Energy & Transportation | Receivables – trade and other |

| $ | 24 | |

| $ | 8 | |

Machinery, Energy & Transportation | Long-term receivables – trade and other |

| 13 | |

| 4 | | ||

Machinery, Energy & Transportation | Accrued expenses |

| (4 | ) |

| (14 | ) | ||

Machinery, Energy & Transportation | Other liabilities |

| - | |

| (2 | ) | ||

Financial Products | Long-term receivables – trade and other |

| 1 | |

| 7 | | ||

Financial Products | Accrued expenses |

| (94 | ) |

| (57 | ) | ||

Interest rate contracts |

|

|

|

|

| | |||

Financial Products | Long-term receivables – trade and other |

| 2 | |

| 3 | | ||

Financial Products | Accrued expenses |

| (3 | ) |

| (2 | ) | ||

|

|

| $ | (61 | ) |

| $ | (53 | ) |

Undesignated derivatives |

|

|

| |

|

| | ||

Foreign exchange contracts |

|

|

| |

|

| | ||

Machinery, Energy & Transportation | Receivables – trade and other |

| $ | 19 | |

| $ | 19 | |

Machinery, Energy & Transportation | Accrued expenses |

| (3 | ) |

| (9 | ) | ||

Financial Products | Receivables – trade and other |

| 14 | |

| 12 | | ||

Financial Products | Accrued expenses |

| (19 | ) |

| (9 | ) | ||

Commodity contracts |

|

|

|

|

| | |||

Machinery, Energy & Transportation | Receivables – trade and other |

| 9 | |

| 21 | | ||

Machinery, Energy & Transportation | Accrued expenses |

| (3 | ) |

| - | | ||

|

|

| $ | 17 | |

| $ | 34 | |

|

|

|

|

|

| ||||

The total notional amounts of the derivative instruments are as follows:

|

|

|

|

| ||||

(Millions of dollars) |

| March 31, 2018 |

| December 31, 2017 | ||||

|

|

|

|

| ||||

Machinery, Energy & Transportation |

| $ | 2,683 | |

| $ | 3,190 | |

Financial Products |

| $ | 5,360 | |

| $ | 3,691 | |

|

|

|

|

| ||||

The notional amounts of the derivative financial instruments do not represent amounts exchanged by the parties. The amounts exchanged by the parties are calculated by reference to the notional amounts and by other terms of the derivatives, such as foreign currency exchange rates, interest rates or commodity prices.

The effect of derivatives designated as hedging instruments on the Consolidated Statement of Results of Operations is as follows:

Fair Value Hedges |

|

|

|

|

|

| ||||||||||||

|

|

| Three Months Ended |

| Three Months Ended |

| ||||||||||||

(Millions of dollars) | Classification |

| Gains (Losses) on Derivatives |

| Gains (Losses) on Borrowings |

| Gains (Losses) on Derivatives |

| Gains (Losses) on Borrowings |

| ||||||||

Interest rate contracts |

|

|

|

|

|

|

|

|

| |

| |||||||

Financial Products | Other income (expense) |

| $ | (2 | ) |

| $ | 2 | |

| $ | (1 | ) |

| $ | 1 | |

|

|

|

| $ | (2 | ) |

| $ | 2 | |

| $ | (1 | ) |

| $ | 1 | |

|

|

|

|

|

|

17

Table of Contents

|

|

|

|

|

|

|

|

| ||||||

Cash Flow Hedges |

|

|

|

|

|

|

|

| ||||||

| Three Months Ended March 31, 2018 |

| ||||||||||||

|

|

| Recognized in Earnings |

| ||||||||||

(Millions of dollars) | Amount of Gains (Losses) Recognized in AOCI (Effective Portion) |

| Classification of Gains (Losses) |

| Amount of Gains (Losses) Reclassified from AOCI to Earnings |

| Recognized in Earnings (Ineffective Portion) |

| ||||||

Foreign exchange contracts |

| |

|

|

|

| |

|

| |

| |||

Machinery, Energy & Transportation | $ | 39 | |

| Other income (expense) |

| $ | 1 | |

| $ | - | |

|

Financial Products | (33 | ) |

| Other income (expense) |

| (29 | ) |

| - | |

| |||

Financial Products | - | |

| Interest expense of Financial Products |

| 3 | |

| - | |

| |||

Interest rate contracts |

|

|

|

|

|

|

|

| ||||||

Machinery, Energy & Transportation | - | |

| Interest expense excluding Financial Products |

| - | |

| - | |

| |||

Financial Products | - | |

| Interest expense of Financial Products |

| 1 | |

| - | | | |||

| $ | 6 | |

|

|

| $ | (24 | ) |

| $ | - | |

|

| Three Months Ended March 31, 2017 |

| ||||||||||||

|

|

| Recognized in Earnings |

| ||||||||||

| Amount of Gains (Losses) Recognized in AOCI (Effective Portion) |

| Classification of Gains (Losses) |

| Amount of Gains (Losses) Reclassified from AOCI to Earnings |

| Recognized in Earnings (Ineffective Portion) |

| ||||||

Foreign exchange contracts |

|

|

|

|

|

|

|

| ||||||

Machinery, Energy & Transportation | $ | 33 | |

| Other income (expense) |

| $ | (39 | ) |

| $ | - | |

|

Financial Products | (18 | ) |

| Other income (expense) |

| (22 | ) |

| - | |

| |||

Interest rate contracts |

| |

|

|

|

| |

|

| |

| |||

Machinery, Energy & Transportation | - | |

| Interest expense excluding Financial Products |

| (2 | ) |

| - | |

| |||

Financial Products | - | |

| Interest expense of Financial Products |

| 1 | |

| - | | | |||

| $ | 15 | |

|

|

| $ | (62 | ) |

| $ | - | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The effect of derivatives not designated as hedging instruments on the Consolidated Statement of Results of Operations is as follows:

|

|

|

| |

|

| |||

(Millions of dollars) | Classification of Gains (Losses) |

| Three Months Ended |

| Three Months Ended | ||||

Foreign exchange contracts |

|

|

|

|

| ||||

Machinery, Energy & Transportation | Other income (expense) |

| $ | 16 | |

| $ | 13 | |

Financial Products | Other income (expense) |

| (7 | ) |

| (7 | ) | ||

Commodity contracts |

|

|

| |

|

| |||

Machinery, Energy & Transportation | Other income (expense) |

| (9 | ) |

| 1 | | ||

|

|

| $ | - | |

| $ | 7 | |

|

|

|

|

|

| ||||

We enter into International Swaps and Derivatives Association (ISDA) master netting agreements within Machinery, Energy & Transportation and Financial Products that permit the net settlement of amounts owed under their respective derivative contracts. Under these master netting agreements, net settlement generally permits the company or the counterparty to determine the net amount payable for contracts due on the same date and in the same currency for similar types of derivative transactions. The master netting agreements generally also provide for net settlement of all outstanding contracts with a counterparty in the case of an event of default or a termination event.

Collateral is generally not required of the counterparties or of our company under the master netting agreements. As of March 31, 2018 and December 31, 2017 , no cash collateral was received or pledged under the master netting agreements.

18

Table of Contents

The effect of the net settlement provisions of the master netting agreements on our derivative balances upon an event of default or termination event is as follows:

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

March 31, 2018 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Assets |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Assets Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Received |

| Net Amount of Assets | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | 65 | |

| $ | - | |

| $ | 65 | |

| $ | (9 | ) |

| $ | - | |

| $ | 56 | |

Financial Products |

| 17 | |

| - | |

| 17 | |

| (4 | ) |

| - | |

| 13 | | ||||||

Total |

| $ | 82 | |

| $ | - | |

| $ | 82 | |

| $ | (13 | ) |

| $ | - | |

| $ | 69 | |

March 31, 2018 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Liabilities |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Liabilities Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Pledged |

| Net Amount of Liabilities | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | (10 | ) |

| $ | - | |

| $ | (10 | ) |

| $ | 9 | |

| $ | - | |

| $ | (1 | ) |

Financial Products |

| (116 | ) |

| - | |

| (116 | ) |

| 4 | |

| - | |

| (112 | ) | ||||||

Total |

| $ | (126 | ) |

| $ | - | |

| $ | (126 | ) |

| $ | 13 | |

| $ | - | |

| $ | (113 | ) |

December 31, 2017 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Assets |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Assets Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Received |

| Net Amount of Assets | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | 52 | |

| $ | - | |

| $ | 52 | |

| $ | (22 | ) |

| $ | - | |

| $ | 30 | |

Financial Products |

| 22 | |

| - | |

| 22 | |

| (10 | ) |

| - | |

| 12 | | ||||||

Total |

| $ | 74 | |

| $ | - | |

| $ | 74 | |

| $ | (32 | ) |

| $ | - | |

| $ | 42 | |

December 31, 2017 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Liabilities |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Liabilities Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Pledged |

| Net Amount of Liabilities | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | (25 | ) |

| $ | - | |

| $ | (25 | ) |

| $ | 22 | |

| $ | - | |

| $ | (3 | ) |

Financial Products |

| (68 | ) |

| - | |

| (68 | ) |

| 10 | |

| - | |

| (58 | ) | ||||||

Total |

| $ | (93 | ) |

| $ | - | |

| $ | (93 | ) |

| $ | 32 | |

| $ | - | |

| $ | (61 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

19

Table of Contents

6. Inventories

Inventories (principally using the last-in, first-out (LIFO) method) are comprised of the following:

|

|

|

| ||||

(Millions of dollars) | March 31, |

| December 31, | ||||

Raw materials | $ | 3,179 | |

| $ | 2,802 | |

Work-in-process | 2,465 | |

| 2,254 | | ||

Finished goods | 5,114 | |

| 4,761 | | ||

Supplies | 189 | |

| 201 | | ||

Total inventories | $ | 10,947 | |

| $ | 10,018 | |

|

|

|

| ||||

7. Intangible assets and goodwill

A. Intangible assets

Intangible assets are comprised of the following:

|

|

|

|

|

|

|

| ||||||

|

|

| March 31, 2018 | ||||||||||

(Millions of dollars) | Weighted Amortizable Life (Years) |

| Gross Carrying Amount |

| Accumulated Amortization |

| Net | ||||||

Customer relationships | 15 |

| $ | 2,527 | |

| $ | (1,159 | ) |

| $ | 1,368 | |

Intellectual property | 11 |

| 1,569 | |

| (878 | ) |

| 691 | | |||

Other | 13 |

| 197 | |

| (93 | ) |

| 104 | | |||

Total finite-lived intangible assets | 14 |

| $ | 4,293 | |