Table of Contents

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2015

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number: 1-768

CATERPILLAR INC.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation) |

| 37-0602744 (IRS Employer I.D. No.) |

|

|

|

100 NE Adams Street, Peoria, Illinois (Address of principal executive offices) |

| 61629 (Zip Code) |

Registrant's telephone number, including area code:

(309) 675-1000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x | Accelerated filer | o |

|

|

|

|

Non-accelerated filer | o | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

At June 30, 2015 , 602,632,543 shares of common stock of the registrant were outstanding.

|

Table of Contents

Table of Contents

Part I. Financial Information |

|

|

Item 1. | Financial Statements | 3 |

Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 59 |

Item 3. | Quantitative and Qualitative Disclosures About Market Risk | 95 |

Item 4. | Controls and Procedures | 95 |

|

|

|

Part II. Other Information |

|

|

Item 1. | Legal Proceedings | 96 |

Item 1A. | Risk Factors | * |

Item 2. | Unregistered Sales of Equity Securities and Use of Proceeds | 96 |

Item 3. | Defaults Upon Senior Securities | * |

Item 4. | Mine Safety Disclosures | * |

Item 5. | Other Information | * |

Item 6. | Exhibits | 97 |

* Item omitted because no answer is called for or item is not applicable.

2

Table of Contents

Part I. FINANCIAL INFORMATION

Item 1. Financial Statements

Caterpillar Inc.

Consolidated Statement of Results of Operations

(Unaudited)

(Dollars in millions except per share data)

| Three Months Ended | ||||||

| 2015 |

| 2014 | ||||

Sales and revenues: |

|

|

| ||||

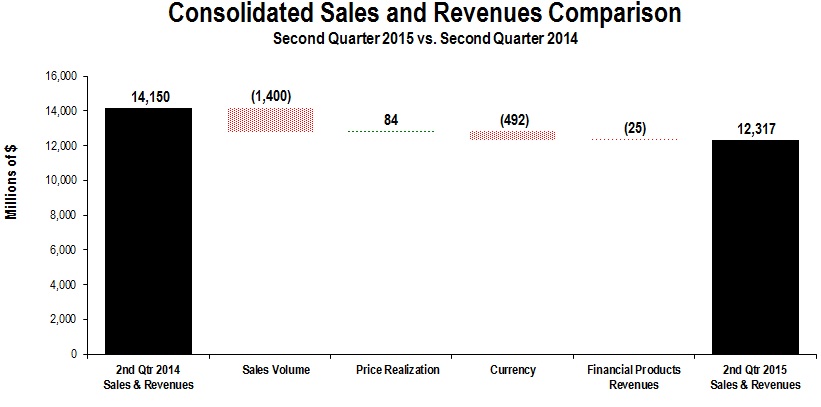

Sales of Machinery, Energy & Transportation | $ | 11,583 | |

| $ | 13,391 | |

Revenues of Financial Products | 734 | |

| 759 | | ||

Total sales and revenues | 12,317 | |

| 14,150 | | ||

|

|

|

| ||||

Operating costs: |

| |

|

| | ||

Cost of goods sold | 8,762 | |

| 10,197 | | ||

Selling, general and administrative expenses | 1,389 | |

| 1,437 | | ||

Research and development expenses | 532 | |

| 516 | | ||

Interest expense of Financial Products | 148 | |

| 153 | | ||

Other operating (income) expenses | 356 | |

| 372 | | ||

Total operating costs | 11,187 | |

| 12,675 | | ||

|

|

|

| ||||

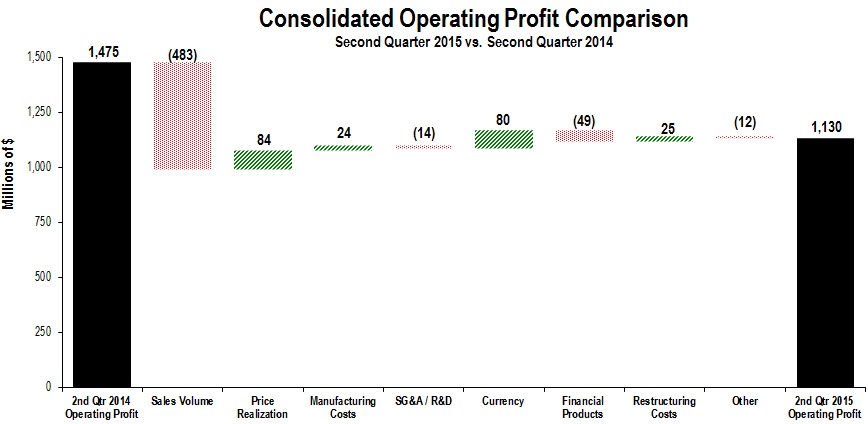

Operating profit | 1,130 | |

| 1,475 | | ||

|

|

|

| ||||

Interest expense excluding Financial Products | 125 | |

| 120 | | ||

Other income (expense) | (13 | ) |

| 65 | | ||

|

|

|

| ||||

Consolidated profit before taxes | 992 | |

| 1,420 | | ||

|

|

|

| ||||

Provision (benefit) for income taxes | 283 | |

| 419 | | ||

Profit of consolidated companies | 709 | |

| 1,001 | | ||

|

|

|

| ||||

Equity in profit (loss) of unconsolidated affiliated companies | 2 | |

| 1 | | ||

|

|

|

| ||||

Profit of consolidated and affiliated companies | 711 | |

| 1,002 | | ||

|

|

|

| ||||

Less: Profit (loss) attributable to noncontrolling interests | 1 | |

| 3 | | ||

|

|

|

| ||||

Profit 1 | $ | 710 | |

| $ | 999 | |

|

|

|

| ||||

Profit per common share | $ | 1.18 | |

| $ | 1.60 | |

|

|

|

| ||||

Profit per common share – diluted 2 | $ | 1.16 | |

| $ | 1.57 | |

|

|

|

| ||||

Weighted-average common shares outstanding (millions) |

| |

|

| | ||

– Basic | 603.2 | |

| 626.3 | | ||

– Diluted 2 | 610.7 | |

| 638.3 | | ||

|

|

|

| ||||

Cash dividends declared per common share | $ | 1.47 | |

| $ | 1.30 | |

1 Profit attributable to common stockholders.

2 Diluted by assumed exercise of stock-based compensation awards using the treasury stock method.

See accompanying notes to Consolidated Financial Statements.

3

Table of Contents

Caterpillar Inc .

Consolidated Statement of Comprehensive Income

(Unaudited)

(Dollars in millions)

| Three Months Ended | ||||||

| 2015 |

| 2014 | ||||

|

|

|

| ||||

Profit of consolidated and affiliated companies | $ | 711 | |

| $ | 1,002 | |

Other comprehensive income (loss), net of tax: |

|

|

| ||||

Foreign currency translation, net of tax (provision)/benefit of: 2015 - $30; 2014 - $(8) | 216 | |

| 28 | | ||

|

|

|

| ||||

Pension and other postretirement benefits: | |

|

| ||||

Current year actuarial gain (loss), net of tax (provision)/benefit of: 2015 - $(12); 2014 - $(5) | 19 | |

| 10 | | ||

Amortization of actuarial (gain) loss, net of tax (provision)/benefit of: 2015 - $(56); 2014 - $(44) | 109 | |

| 86 | | ||

Current year prior service credit (cost), net of tax (provision)/benefit of: 2015 - $0; 2014 - $0 | - | |

| 1 | | ||

Amortization of prior service (credit) cost, net of tax (provision)/benefit of: 2015 - $5; 2014 - $4 | (9 | ) |

| (6 | ) | ||

|

|

|

| ||||

Derivative financial instruments: |

|

|

| ||||

Gains (losses) deferred, net of tax (provision)/benefit of: 2015 - $(7); 2014 - $6 | 11 | |

| (11 | ) | ||

(Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2015 - $(15); 2014 - $3 | 25 | |

| (5 | ) | ||

|

|

|

| ||||

Available-for-sale securities: |

|

|

| ||||

Gains (losses) deferred, net of tax (provision)/benefit of: 2015 - $4; 2014 - $(8) | (6 | ) |

| 15 | | ||

(Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2015 - $0; 2014 - $0 | (1 | ) |

| - | | ||

|

|

|

| ||||

Total other comprehensive income (loss), net of tax | 364 | |

| 118 | | ||

Comprehensive income | 1,075 | |

| 1,120 | | ||

Less: comprehensive income attributable to the noncontrolling interests | 7 | |

| (3 | ) | ||

Comprehensive income attributable to stockholders | $ | 1,082 | |

| $ | 1,117 | |

|

|

|

| ||||

See accompanying notes to Consolidated Financial Statements.

4

Table of Contents

Caterpillar Inc.

Consolidated Statement of Results of Operations

(Unaudited)

(Dollars in millions except per share data)

| Six Months Ended | ||||||

| 2015 |

| 2014 | ||||

Sales and revenues: |

|

|

| ||||

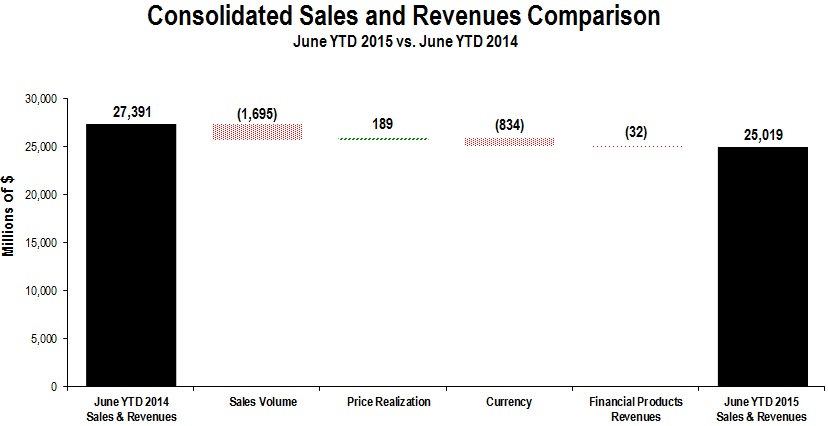

Sales of Machinery, Energy & Transportation | $ | 23,544 | |

| $ | 25,884 | |

Revenues of Financial Products | 1,475 | |

| 1,507 | | ||

Total sales and revenues | 25,019 | |

| 27,391 | | ||

|

|

|

| ||||

Operating costs: |

| |

|

| | ||

Cost of goods sold | 17,605 | |

| 19,634 | | ||

Selling, general and administrative expenses | 2,707 | |

| 2,729 | | ||

Research and development expenses | 1,078 | |

| 1,024 | | ||

Interest expense of Financial Products | 298 | |

| 313 | | ||

Other operating (income) expenses | 674 | |

| 818 | | ||

Total operating costs | 22,362 | |

| 24,518 | | ||

|

|

|

| ||||

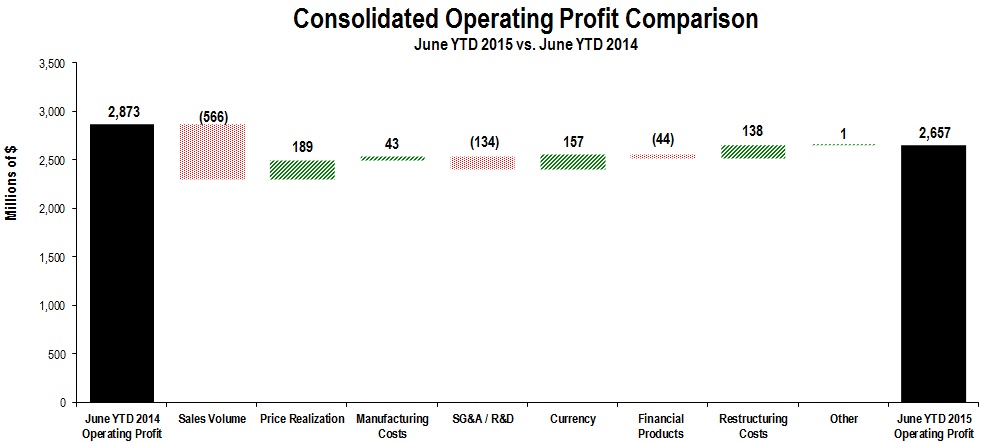

Operating profit | 2,657 | |

| 2,873 | | ||

|

|

|

| ||||

Interest expense excluding Financial Products | 254 | |

| 230 | | ||

Other income (expense) | 144 | |

| 119 | | ||

|

|

|

| ||||

Consolidated profit before taxes | 2,547 | |

| 2,762 | | ||

|

|

|

| ||||

Provision (benefit) for income taxes | 726 | |

| 837 | | ||

Profit of consolidated companies | 1,821 | |

| 1,925 | | ||

|

|

|

| ||||

Equity in profit (loss) of unconsolidated affiliated companies | 4 | |

| 2 | | ||

|

|

|

| ||||

Profit of consolidated and affiliated companies | 1,825 | |

| 1,927 | | ||

|

|

|

| ||||

Less: Profit (loss) attributable to noncontrolling interests | 4 | |

| 6 | | ||

|

|

|

| ||||

Profit 1 | $ | 1,821 | |

| $ | 1,921 | |

|

|

|

| ||||

Profit per common share | $ | 3.01 | |

| $ | 3.06 | |

|

|

|

| ||||

Profit per common share – diluted 2 | $ | 2.98 | |

| $ | 3.00 | |

|

|

|

| ||||

Weighted-average common shares outstanding (millions) |

|

|

| | |||

– Basic | 604.1 | |

| 626.8 | | ||

– Diluted 2 | 611.8 | |

| 639.3 | | ||

|

|

|

| ||||

Cash dividends declared per common share | $ | 1.47 | |

| $ | 1.30 | |

1 Profit attributable to common stockholders.

2 Diluted by assumed exercise of stock-based compensation awards using the treasury stock method.

See accompanying notes to Consolidated Financial Statements.

5

Table of Contents

Caterpillar Inc .

Consolidated Statement of Comprehensive Income

(Unaudited)

(Dollars in millions)

| Six Months Ended | ||||||

| 2015 |

| 2014 | ||||

|

|

|

| ||||

Profit of consolidated and affiliated companies | $ | 1,825 | |

| $ | 1,927 | |

Other comprehensive income (loss), net of tax: |

|

|

| ||||

Foreign currency translation, net of tax (provision)/benefit of: 2015 - $(55); 2014 - $(8) | (575 | ) |

| 67 | | ||

|

|

|

| ||||

Pension and other postretirement benefits: |

|

|

| ||||

Current year actuarial gain (loss), net of tax (provision)/benefit of: 2015 - $(14); 2014 - $(5) | 24 | |

| 10 | | ||

Amortization of actuarial (gain) loss, net of tax (provision)/benefit of: 2015 - $(112); 2014 - $(88) | 218 | |

| 172 | | ||

Current year prior service credit (cost), net of tax (provision)/benefit of: 2015 - $0; 2014 - $0 | - | |

| 1 | | ||

Amortization of prior service (credit) cost, net of tax (provision)/benefit of: 2015 - $9; 2014 - $7 | (18 | ) |

| (12 | ) | ||

|

|

|

| ||||

Derivative financial instruments: |

|

|

| ||||

Gains (losses) deferred, net of tax (provision)/benefit of: 2015 - $2; 2014 - $16 | (3 | ) |

| (27 | ) | ||

(Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2015 - $(29); 2014 - $6 | 49 | |

| (10 | ) | ||

|

|

|

| ||||

Available-for-sale securities: |

|

|

| ||||

Gains (losses) deferred, net of tax (provision)/benefit of: 2015 - $0; 2014 - $(11) | 2 | |

| 23 | | ||

(Gains) losses reclassified to earnings, net of tax (provision)/benefit of: 2015 - $1; 2014 - $4 | (3 | ) |

| (10 | ) | ||

|

|

|

| ||||

Total other comprehensive income (loss), net of tax | (306 | ) |

| 214 | | ||

Comprehensive income | 1,519 | |

| 2,141 | | ||

Less: comprehensive income attributable to the noncontrolling interests | 4 | |

| (5 | ) | ||

Comprehensive income attributable to stockholders | $ | 1,523 | |

| $ | 2,136 | |

|

|

|

| ||||

See accompanying notes to Consolidated Financial Statements.

6

Table of Contents

Caterpillar Inc .

Consolidated Statement of Financial Position

(Unaudited)

(Dollars in millions)

| June 30, |

| December 31, | ||||

Assets |

|

|

| ||||

Current assets: |

| |

|

| | ||

Cash and short-term investments | $ | 7,821 | |

| $ | 7,341 | |

Receivables – trade and other | 7,212 | |

| 7,737 | | ||

Receivables – finance | 9,213 | |

| 9,027 | | ||

Deferred and refundable income taxes | 1,441 | |

| 1,739 | | ||

Prepaid expenses and other current assets | 859 | |

| 818 | | ||

Inventories | 11,681 | |

| 12,205 | | ||

Total current assets | 38,227 | |

| 38,867 | | ||

|

|

|

| ||||

Property, plant and equipment – net | 16,136 | |

| 16,577 | | ||

Long-term receivables – trade and other | 1,290 | |

| 1,364 | | ||

Long-term receivables – finance | 13,698 | |

| 14,644 | | ||

Investments in unconsolidated affiliated companies | 229 | |

| 257 | | ||

Noncurrent deferred and refundable income taxes | 1,473 | |

| 1,404 | | ||

Intangible assets | 2,863 | |

| 3,076 | | ||

Goodwill | 6,550 | |

| 6,694 | | ||

Other assets | 1,776 | |

| 1,798 | | ||

Total assets | $ | 82,242 | |

| $ | 84,681 | |

|

|

|

| ||||

Liabilities |

| |

|

| | ||

Current liabilities: |

| |

|

| | ||

Short-term borrowings: |

| |

|

| | ||

Machinery, Energy & Transportation | $ | 14 | |

| $ | 9 | |

Financial Products | 6,226 | |

| 4,699 | | ||

Accounts payable | 5,862 | |

| 6,515 | | ||

Accrued expenses | 3,311 | |

| 3,548 | | ||

Accrued wages, salaries and employee benefits | 1,597 | |

| 2,438 | | ||

Customer advances | 1,754 | |

| 1,697 | | ||

Dividends payable | 463 | |

| 424 | | ||

Other current liabilities | 1,744 | |

| 1,754 | | ||

Long-term debt due within one year: |

| |

|

| | ||

Machinery, Energy & Transportation | 12 | | | 510 | | ||

Financial Products | 4,623 | |

| 6,283 | | ||

Total current liabilities | 25,606 | |

| 27,877 | | ||

|

|

|

| ||||

Long-term debt due after one year: |

| |

|

| | ||

Machinery, Energy & Transportation | 9,497 | |

| 9,493 | | ||

Financial Products | 17,948 | |

| 18,291 | | ||

Liability for postemployment benefits | 8,759 | |

| 8,963 | | ||

Other liabilities | 3,271 | |

| 3,231 | | ||

Total liabilities | 65,081 | |

| 67,855 | | ||

Commitments and contingencies (Notes 10 and 13) | | |

| | | ||

Stockholders' equity |

| |

|

| | ||

Common stock of $1.00 par value: |

| |

|

| | ||

Authorized shares: 2,000,000,000 | 5,142 | |

| 5,016 | | ||

Treasury stock (6/30/15 – 212,262,081 shares; 12/31/14 – 208,728,065 shares) at cost | (16,144 | ) |

| (15,726 | ) | ||

Profit employed in the business | 34,823 | |

| 33,887 | | ||

Accumulated other comprehensive income (loss) | (6,729 | ) |

| (6,431 | ) | ||

Noncontrolling interests | 69 | |

| 80 | | ||

Total stockholders' equity | 17,161 | |

| 16,826 | | ||

Total liabilities and stockholders' equity | $ | 82,242 | |

| $ | 84,681 | |

See accompanying notes to Consolidated Financial Statements.

7

Table of Contents

Caterpillar Inc.

Consolidated Statement of Changes in Stockholders' Equity

(Unaudited)

(Dollars in millions)

| Common stock |

| Treasury stock |

| Profit employed in the business |

| Accumulated other comprehensive income (loss) |

| Noncontrolling interests |

| Total | ||||||||||||

Six Months Ended June 30, 2014 |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Balance at December 31, 2013 | $ | 4,709 | |

| $ | (11,854 | ) |

| $ | 31,854 | |

| $ | (3,898 | ) |

| $ | 67 | |

| $ | 20,878 | |

Profit of consolidated and affiliated companies | - | |

| - | |

| 1,921 | |

| - | |

| 6 | |

| 1,927 | | ||||||

Foreign currency translation, net of tax | - | |

| - | |

| - | |

| 68 | |

| (1 | ) |

| 67 | | ||||||

Pension and other postretirement benefits, net of tax | - | |

| - | |

| - | |

| 171 | |

| - | |

| 171 | | ||||||

Derivative financial instruments, net of tax | - | |

| - | |

| - | |

| (37 | ) |

| - | |

| (37 | ) | ||||||

Available-for-sale securities, net of tax | - | |

| - | |

| - | |

| 13 | |

| - | |

| 13 | | ||||||

Change in ownership from noncontrolling interests | - | |

| - | |

| - | |

| - | |

| 2 | |

| 2 | | ||||||

Dividends declared | - | |

| - | |

| (814 | ) |

| - | |

| - | |

| (814 | ) | ||||||

Distribution to noncontrolling interests | - | |

| - | |

| - | |

| - | |

| (7 | ) |

| (7 | ) | ||||||

Common shares issued from treasury stock for stock-based compensation: 8,134,995 | (86 | ) |

| 280 | |

| - | |

| - | |

| - | |

| 194 | | ||||||

Stock-based compensation expense | 137 | |

| - | |

| - | |

| - | |

| - | |

| 137 | | ||||||

Net excess tax benefits from stock-based compensation | 130 | |

| - | |

| - | |

| - | |

| - | |

| 130 | | ||||||

Common shares repurchased: 18,110,735 1 | - | |

| (1,738 | ) |

| - | |

| - | |

| - | |

| (1,738 | ) | ||||||

Balance at June 30, 2014 | $ | 4,890 | |

| $ | (13,312 | ) |

| $ | 32,961 | |

| $ | (3,683 | ) |

| $ | 67 | |

| $ | 20,923 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Six Months Ended June 30, 2015 |

| |

|

| |

|

| |

|

| |

|

| |

|

| | ||||||

Balance at December 31, 2014 | $ | 5,016 | |

| $ | (15,726 | ) |

| $ | 33,887 | |

| $ | (6,431 | ) |

| $ | 80 | |

| $ | 16,826 | |

Profit of consolidated and affiliated companies | - | |

| - | |

| 1,821 | |

| - | |

| 4 | |

| 1,825 | | ||||||

Foreign currency translation, net of tax | - | |

| - | |

| - | |

| (567 | ) |

| (8 | ) |

| (575 | ) | ||||||

Pension and other postretirement benefits, net of tax | - | |

| - | |

| - | |

| 224 | |

| - | |

| 224 | | ||||||

Derivative financial instruments, net of tax | - | |

| - | |

| - | |

| 46 | |

| - | |

| 46 | | ||||||

Available-for-sale securities, net of tax | - | |

| - | |

| - | |

| (1 | ) |

| - | |

| (1 | ) | ||||||

Dividends declared | - | |

| - | |

| (885 | ) |

| - | |

| - | |

| (885 | ) | ||||||

Distribution to noncontrolling interests | - | |

| - | |

| - | |

| - | |

| (7 | ) |

| (7 | ) | ||||||

Common shares issued from treasury stock for stock-based compensation: 2,674,058 | (74 | ) |

| 107 | |

| - | |

| - | |

| - | |

| 33 | | ||||||

Stock-based compensation expense | 193 | |

| - | |

| - | |

| - | |

| - | |

| 193 | | ||||||

Net excess tax benefits from stock-based compensation | 7 | |

| - | |

| - | |

| - | |

| - | |

| 7 | | ||||||

Common shares repurchased: 6,208,074 1 | - | |

| (525 | ) |

| - | |

| - | |

| - | |

| (525 | ) | ||||||

Balance at June 30, 2015 | $ | 5,142 | |

| $ | (16,144 | ) |

| $ | 34,823 | |

| $ | (6,729 | ) |

| $ | 69 | |

| $ | 17,161 | |

1 | See Note 11 regarding shares repurchased. |

See accompanying notes to Consolidated Financial Statements.

8

Table of Contents

Caterpillar Inc.

Consolidated Statement of Cash Flow

(Unaudited)

(Millions of dollars)

| Six Months Ended | ||||||

| 2015 |

| 2014 | ||||

Cash flow from operating activities: |

|

|

| ||||

Profit of consolidated and affiliated companies | $ | 1,825 | |

| $ | 1,927 | |

Adjustments for non-cash items: |

| |

|

| | ||

Depreciation and amortization | 1,514 | |

| 1,570 | | ||

Other | 120 | |

| 240 | | ||

Changes in assets and liabilities, net of acquisitions and divestitures: |

| |

|

| | ||

Receivables – trade and other | 383 | |

| 251 | | ||

Inventories | 332 | |

| (439 | ) | ||

Accounts payable | (326 | ) |

| 438 | | ||

Accrued expenses | (71 | ) |

| 7 | | ||

Accrued wages, salaries and employee benefits | (801 | ) |

| 283 | | ||

Customer advances | 98 | |

| (14 | ) | ||

Other assets – net | 85 | |

| (105 | ) | ||

Other liabilities – net | 199 | |

| (24 | ) | ||

Net cash provided by (used for) operating activities | 3,358 | |

| 4,134 | | ||

|

|

|

| ||||

Cash flow from investing activities: |

| |

|

| | ||

Capital expenditures – excluding equipment leased to others | (656 | ) |

| (710 | ) | ||

Expenditures for equipment leased to others | (815 | ) |

| (825 | ) | ||

Proceeds from disposals of leased assets and property, plant and equipment | 367 | |

| 442 | | ||

Additions to finance receivables | (4,577 | ) |

| (5,760 | ) | ||

Collections of finance receivables | 4,477 | |

| 4,719 | | ||

Proceeds from sale of finance receivables | 74 | |

| 104 | | ||

Investments and acquisitions (net of cash acquired) | (63 | ) |

| (15 | ) | ||

Proceeds from sale of businesses and investments (net of cash sold) | 168 | |

| 139 | | ||

Proceeds from sale of securities | 128 | |

| 222 | | ||

Investments in securities | (119 | ) |

| (673 | ) | ||

Other – net | (75 | ) |

| (25 | ) | ||

Net cash provided by (used for) investing activities | (1,091 | ) |

| (2,382 | ) | ||

|

|

|

| ||||

Cash flow from financing activities: |

| |

|

| | ||

Dividends paid | (846 | ) |

| (757 | ) | ||

Distribution to noncontrolling interests | (7 | ) |

| (7 | ) | ||

Contribution from noncontrolling interests | - | |

| 2 | | ||

Common stock issued, including treasury shares reissued | 33 | |

| 194 | | ||

Treasury shares purchased | (525 | ) |

| (1,738 | ) | ||

Excess tax benefit from stock-based compensation | 18 | |

| 131 | | ||

Proceeds from debt issued (original maturities greater than three months): |

| |

|

| | ||

Machinery, Energy & Transportation | 3 | |

| 1,990 | | ||

Financial Products | 3,688 | |

| 4,961 | | ||

Payments on debt (original maturities greater than three months): |

| |

|

| | ||

Machinery, Energy & Transportation | (509 | ) |

| (770 | ) | ||

Financial Products | (5,580 | ) |

| (5,574 | ) | ||

Short-term borrowings – net (original maturities three months or less) | 1,972 | |

| 1,749 | | ||

Net cash provided by (used for) financing activities | (1,753 | ) |

| 181 | | ||

Effect of exchange rate changes on cash | (34 | ) |

| (87 | ) | ||

Increase (decrease) in cash and short-term investments | 480 | |

| 1,846 | | ||

Cash and short-term investments at beginning of period | 7,341 | |

| 6,081 | | ||

Cash and short-term investments at end of period | $ | 7,821 | |

| $ | 7,927 | |

All short-term investments, which consist primarily of highly liquid investments with original maturities of three months or less, are considered to be cash equivalents .

See accompanying notes to Consolidated Financial Statements.

9

Table of Contents

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. | A. Nature of operations |

Information in our financial statements and related commentary are presented in the following categories:

Machinery, Energy & Transportation – Represents the aggregate total of Construction Industries, Resource Industries, Energy & Transportation and All Other operating segments and related corporate items and eliminations.

Financial Products – Primarily includes the company's Financial Products Segment. This category includes Caterpillar Financial Services Corporation (Cat Financial), Caterpillar Financial Insurance Services (Insurance Services) and their respective subsidiaries.

B. Basis of presentation

In the opinion of management, the accompanying financial statements include all adjustments, consisting only of normal recurring adjustments, necessary for a fair statement of (a) the consolidated results of operations for the three and six month periods ended June 30, 2015 and 2014 , (b) the consolidated comprehensive income for the three and six month periods ended June 30, 2015 and 2014 , (c) the consolidated financial position at June 30, 2015 and December 31, 2014 , (d) the consolidated changes in stockholders' equity for the six month periods ended June 30, 2015 and 2014 and (e) the consolidated cash flow for the six month periods ended June 30, 2015 and 2014 . The financial statements have been prepared in conformity with generally accepted accounting principles in the United States of America (U.S. GAAP) and pursuant to the rules and regulations of the Securities and Exchange Commission. Certain amounts for prior periods have been reclassified to conform to the current period financial statement presentation.

As previously disclosed, in connection with the preparation of our Quarterly Report on Form 10-Q for the quarter ended June 30, 2014, we concluded that certain non-cash transactions should be excluded from both changes in Receivables-trade and other and Accounts payable when preparing our Consolidated Statement of Cash Flow. Accordingly, we prepared our Consolidated Statement of Cash Flow for the six and nine months ended June 30, 2014 and September 30, 2014 on that basis. We subsequently concluded that our prior policy of including those transactions in the changes in Receivables-trade and other and Accounts payable is acceptable. Accordingly, we prepared our Consolidated Statement of Cash Flow for the year ended December 31, 2014 using our prior policy. We have revised our Consolidated Statement of Cash Flow to increase Receivables-trade and other and decrease Accounts payable by $113 million for the six months ended June 30, 2014. We will revise our Consolidated Statement of Cash Flow for the nine months ended September 30, 2014 the next time it is filed to increase Receivables-trade and other and decrease Accounts payable by $149 million . The revisions do not impact net cash provided by operating activities.

Interim results are not necessarily indicative of results for a full year. The information included in this Form 10-Q should be read in conjunction with the audited financial statements and notes thereto included in our Company's annual report on Form 10-K for the year ended December 31, 2014 ( 2014 Form 10-K).

The December 31, 2014 financial position data included herein is derived from the audited consolidated financial statements included in the 2014 Form 10-K but does not include all disclosures required by U.S. GAAP.

Unconsolidated Variable Interest Entities (VIEs)

We have affiliates, suppliers and dealers that are VIEs of which we are not the primary beneficiary. Although we have provided financial support, we do not have the power to direct the activities that most significantly impact the economic performance of each entity.

10

Table of Contents

Our maximum exposure to loss from VIEs for which we are not the primary beneficiary was as follows:

|

|

|

|

|

| ||||

(Millions of dollars) |

| June 30, 2015 |

| December 31, 2014 |

| ||||

Receivables - trade and other |

| $ | 53 | |

| $ | 36 | |

|

Receivables - finance |

| 504 | |

| 216 | |

| ||

Long-term receivables - finance |

| 57 | |

| 285 | |

| ||

Investments in unconsolidated affiliated companies |

| 32 | |

| 83 | |

| ||

Guarantees |

| 83 | |

| 129 | |

| ||

Total |

| $ | 729 | |

| $ | 749 | |

|

|

|

|

|

|

| ||||

2. New accounting guidance

Reporting discontinued operations and disclosures of disposals of components of an entity – In April 2014, the Financial Accounting Standards Board (FASB) issued accounting guidance for determining which disposals can be presented as discontinued operations and modifies related disclosure requirements. The guidance defines a discontinued operation as a disposal of a component or group of components that is disposed of or is classified as held for sale and represents a strategic shift that has (or will have) a major effect on an entity's operations and financial results. This guidance was effective January 1, 2015 and did not have a material impact on our financial statements.

Revenue recognition – In May 2014, the FASB issued new revenue recognition guidance to provide a single, comprehensive revenue recognition model for all contracts with customers. Under the new guidance, an entity will recognize revenue to depict the transfer of promised goods or services to customers at an amount that the entity expects to be entitled to in exchange for those goods or services. A five step model has been introduced for an entity to apply when recognizing revenue. The new guidance also includes enhanced disclosure requirements, and is effective January 1, 2018, with early adoption permitted for January 1, 2017. Entities have the option to apply the new guidance under a retrospective approach to each prior reporting period presented, or a modified retrospective approach with the cumulative effect of initially applying the new guidance recognized at the date of initial application within the Consolidated Statement of Changes in Stockholders' Equity. We are in the process of evaluating the application and implementation of the new guidance.

Variable interest entities (VIE) – In February 2015, the FASB issued accounting guidance on the consolidation of VIEs. The new guidance revises previous guidance by establishing an analysis for determining whether a limited partnership or similar entity is a VIE and whether outsourced decision-maker fees are considered variable interests. In addition, the new guidance revises how a reporting entity evaluates economics and related parties when assessing who should consolidate a VIE. This guidance is effective January 1, 2016. We do not expect the adoption to have a material impact on our financial statements.

Presentation of debt issuance costs – In April 2015, the FASB issued accounting guidance which requires debt issuance costs to be presented in the balance sheet as a direct deduction from the carrying value of the associated debt liability. Prior to the issuance of the standard, debt issuance costs were required to be presented in the balance sheet as an asset. This guidance is effective January 1, 2016. We do not expect the adoption to have a material impact on our financial statements.

Fair value disclosures for investments in certain entities that calculate net asset value per share – In May 2015, the FASB issued accounting guidance which removes the requirement to categorize within the fair value hierarchy investments measured at net asset value (or its equivalent). The new guidance requires that the amount of these investments continue to be disclosed to reconcile the fair value hierarchy disclosure to the balance sheet. The guidance is effective January 1, 2016 and will be applied retrospectively with early adoption permitted. We do not expect the adoption to have a material impact on our financial statements.

Simplifying the measurement of inventory – In July 2015, the FASB issued accounting guidance which requires that inventory be measured at the lower of cost and net realizable value. Prior to the issuance of the new guidance, inventory was measured at the lower of cost or market. Replacing the concept of market with the single measurement of net realizable value is intended to create efficiencies for preparers. Inventory measured using the last-in, first-out (LIFO)

11

Table of Contents

method and the retail inventory method are not impacted by the new guidance. The guidance is effective January 1, 2017. We do not expect the adoption to have a material impact on our financial statements.

3. Stock-based compensation

Accounting for stock-based compensation requires that the cost resulting from all stock-based payments be recognized in the financial statements based on the grant date fair value of the award. Stock-based compensation primarily consists of stock options, restricted stock units (RSUs) and stock-settled stock appreciation rights (SARs). Stock-based compensation awards granted prior to 2015 will vest three years after the date of grant (cliff vesting). The awards granted in 2015 will vest according to a three -year graded vesting schedule. One-third of the award will become vested on the first anniversary of the grant date, one-third of the award will become vested on the second anniversary of the grant date and one-third of the award will become vested on the third anniversary of the grant date. Stock-based compensation expense will be recognized on a straight-line basis over the requisite service period for awards with terms that specify cliff or graded vesting and contain only service conditions.

Upon separation from service, if the participant is 55 years of age or older with more than five years of service, the participant meets the criteria for a "Long Service Separation". Prior to 2015, our stock-based compensation award terms allowed for the immediate vesting upon separation for employees who met the criteria for a "Long Service Separation" and fulfilled a requisite service period of six months . For these employees, compensation expense was recognized over the period from the grant date to the end date of the six -month requisite service period. Our stock-based compensation award terms for the 2015 grant allowed for the immediate vesting upon separation for employees who met the criteria for a "Long Service Separation" with no requisite service period. For these employees, compensation expense for the 2015 grant was recognized immediately on the grant date. For employees who become eligible for immediate vesting under a "Long Service Separation" subsequent to the grant date and prior to the completion of the vesting period, compensation expense is recognized over the period from grant date to the date eligibility is achieved. If the "Long Service Separation" criteria are met, the vested options/SARs will have a life that is the lesser of ten years from the original grant date or five years from the separation date.

We recognized pretax stock-based compensation expense in the amount of $58 million and $193 million for the three and six months ended June 30, 2015 , respectively; and $84 million and $137 million for the three and six months ended June 30, 2014 , respectively. The change in stock-based compensation expense was primarily due to the change in award terms for participants that met the criteria for a "Long Service Separation", as the removal of the six -month requisite service period results in higher expense in the first quarter (period of grant) and lower expense over the following two quarters.

The following table illustrates the type and fair value of the stock-based compensation awards granted during the six month periods ended June 30, 2015 and 2014 , respectively:

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

| 2015 |

| 2014 | ||||||||||||||||||

| Shares Granted |

| Weighted-Average Fair Value Per Share |

| Weighted-Average Grant Date Stock Price |

| Shares Granted |

| Weighted-Average Fair Value Per Share |

| Weighted-Average Grant Date Stock Price | ||||||||||

Stock options | 7,939,497 | |

| $ | 23.61 | |

| $ | 83.34 | |

| 4,448,218 | |

| $ | 29.52 | |

| $ | 96.31 | |

RSUs | 1,822,729 | |

| $ | 77.54 | |

| $ | 83.01 | |

| 1,429,512 | |

| $ | 89.18 | |

| $ | 96.31 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||

12

Table of Contents

The following table provides the assumptions used in determining the fair value of the stock-based awards for the six month periods ended June 30, 2015 and 2014 , respectively:

|

|

|

|

| Grant Year | ||

| 2015 |

| 2014 |

Weighted-average dividend yield | 2.27% |

| 2.15% |

Weighted-average volatility | 28.4% |

| 28.2% |

Range of volatilities | 19.9-35.9% |

| 18.4-36.2% |

Range of risk-free interest rates | 0.22-2.08% |

| 0.12-2.60% |

Weighted-average expected lives | 8 years |

| 8 years |

|

|

|

|

As of June 30, 2015 , the total remaining unrecognized compensation expense related to nonvested stock-based compensation awards was $310 million , which will be amortized over the weighted-average remaining requisite service periods of approximately 2.2 years.

4. Derivative financial instruments and risk management

Our earnings and cash flow are subject to fluctuations due to changes in foreign currency exchange rates, interest rates and commodity prices. Our Risk Management Policy (policy) allows for the use of derivative financial instruments to prudently manage foreign currency exchange rate, interest rate and commodity price exposures. Our policy specifies that derivatives are not to be used for speculative purposes. Derivatives that we use are primarily foreign currency forward, option, and cross currency contracts, interest rate swaps, and commodity forward and option contracts. Our derivative activities are subject to the management, direction and control of our senior financial officers. Risk management practices, including the use of financial derivative instruments, are presented to the Audit Committee of the Board of Directors at least annually.

All derivatives are recognized on the Consolidated Statement of Financial Position at their fair value. On the date the derivative contract is entered into, we designate the derivative as (1) a hedge of the fair value of a recognized asset or liability (fair value hedge), (2) a hedge of a forecasted transaction or the variability of cash flow to be paid (cash flow hedge) or (3) an undesignated instrument. Changes in the fair value of a derivative that is qualified, designated and highly effective as a fair value hedge, along with the gain or loss on the hedged recognized asset or liability that is attributable to the hedged risk, are recorded in current earnings. Changes in the fair value of a derivative that is qualified, designated and highly effective as a cash flow hedge are recorded in Accumulated other comprehensive income (loss) (AOCI), to the extent effective, on the Consolidated Statement of Financial Position until they are reclassified to earnings in the same period or periods during which the hedged transaction affects earnings. Changes in the fair value of undesignated derivative instruments and the ineffective portion of designated derivative instruments are reported in current earnings. Cash flow from designated derivative financial instruments are classified within the same category as the item being hedged on the Consolidated Statement of Cash Flow. Cash flow from undesignated derivative financial instruments are included in the investing category on the Consolidated Statement of Cash Flow.

We formally document all relationships between hedging instruments and hedged items, as well as the risk-management objective and strategy for undertaking various hedge transactions. This process includes linking all derivatives that are designated as fair value hedges to specific assets and liabilities on the Consolidated Statement of Financial Position and linking cash flow hedges to specific forecasted transactions or variability of cash flow.

We also formally assess, both at the hedge's inception and on an ongoing basis, whether the designated derivatives that are used in hedging transactions are highly effective in offsetting changes in fair values or cash flow of hedged items. When a derivative is determined not to be highly effective as a hedge or the underlying hedged transaction is no longer probable, we discontinue hedge accounting prospectively, in accordance with the derecognition criteria for hedge accounting.

Foreign Currency Exchange Rate Risk

Foreign currency exchange rate movements create a degree of risk by affecting the U.S. dollar value of sales made and costs incurred in foreign currencies. Movements in foreign currency rates also affect our competitive position as these changes may affect business practices and/or pricing strategies of non-U.S.-based competitors. Additionally, we have balance sheet positions denominated in foreign currencies, thereby creating exposure to movements in exchange rates.

13

Table of Contents

Our Machinery, Energy & Transportation operations purchase, manufacture and sell products in many locations around the world. As we have a diversified revenue and cost base, we manage our future foreign currency cash flow exposure on a net basis. We use foreign currency forward and option contracts to manage unmatched foreign currency cash inflow and outflow. Our objective is to minimize the risk of exchange rate movements that would reduce the U.S. dollar value of our foreign currency cash flow. Our policy allows for managing anticipated foreign currency cash flow for up to five years.

We generally designate as cash flow hedges at inception of the contract any Australian dollar, Brazilian real, British pound, Canadian dollar, Chinese yuan, euro, Indian rupee, Japanese yen, Mexican peso, Singapore dollar or Swiss franc forward or option contracts that meet the requirements for hedge accounting and the maturity extends beyond the current quarter-end. Designation is performed on a specific exposure basis to support hedge accounting. The remainder of Machinery, Energy & Transportation foreign currency contracts are undesignated, including any hedges designed to protect our competitive exposure.

As of June 30, 2015 , $28 million of deferred net losses, net of tax, included in equity (AOCI in the Consolidated Statement of Financial Position), are expected to be reclassified to current earnings (Other income (expense) in the Consolidated Statement of Results of Operations) over the next twelve months when earnings are affected by the hedged transactions. The actual amount recorded in Other income (expense) will vary based on exchange rates at the time the hedged transactions impact earnings.

In managing foreign currency risk for our Financial Products operations, our objective is to minimize earnings volatility resulting from conversion and the remeasurement of net foreign currency balance sheet positions, and future transactions denominated in foreign currencies. Our policy allows the use of foreign currency forward, option and cross currency contracts to offset the risk of currency mismatch between our receivables and debt, and exchange rate risk associated with future transactions denominated in foreign currencies. Substantially all such foreign currency forward, option and cross currency contracts are undesignated.

Interest Rate Risk

Interest rate movements create a degree of risk by affecting the amount of our interest payments and the value of our fixed-rate debt. Our practice is to use interest rate derivatives to manage our exposure to interest rate changes.

Our Machinery, Energy & Transportation operations generally use fixed-rate debt as a source of funding. Our objective is to minimize the cost of borrowed funds. Our policy allows us to enter into fixed-to-floating interest rate swaps and forward rate agreements to meet that objective. We designate fixed-to-floating interest rate swaps as fair value hedges at inception of the contract, and we designate certain forward rate agreements as cash flow hedges at inception of the contract.

As of June 30, 2015 , $4 million of deferred net losses, net of tax, included in equity (AOCI in the Consolidated Statement of Financial Position), related to Machinery, Energy & Transportation forward rate agreements, are expected to be reclassified to current earnings (Interest expense excluding Financial Products in the Consolidated Statement of Results of Operations) over the next twelve months.

Financial Products operations has a match-funding policy that addresses interest rate risk by aligning the interest rate profile (fixed or floating rate) of Cat Financial's debt portfolio with the interest rate profile of their receivables portfolio within predetermined ranges on an ongoing basis. In connection with that policy, we use interest rate derivative instruments to modify the debt structure to match assets within the receivables portfolio. This matched funding reduces the volatility of margins between interest-bearing assets and interest-bearing liabilities, regardless of which direction interest rates move.

Our policy allows us to use fixed-to-floating, floating-to-fixed and floating-to-floating interest rate swaps to meet the match-funding objective. We designate fixed-to-floating interest rate swaps as fair value hedges to protect debt against changes in fair value due to changes in the benchmark interest rate. We designate most floating-to-fixed interest rate swaps as cash flow hedges to protect against the variability of cash flows due to changes in the benchmark interest rate.

As of June 30, 2015 , $1 million of deferred net losses, net of tax, included in equity (AOCI in the Consolidated Statement of Financial Position), related to Financial Products floating-to-fixed interest rate swaps, are expected to be reclassified to current earnings (Interest expense of Financial Products in the Consolidated Statement of Results of Operations) over

14

Table of Contents

the next twelve months. The actual amount recorded in Interest expense of Financial Products will vary based on interest rates at the time the hedged transactions impact earnings.

We have, at certain times, liquidated fixed-to-floating and floating-to-fixed interest rate swaps at both Machinery, Energy & Transportation and Financial Products. The gains or losses associated with these swaps at the time of liquidation are amortized into earnings over the original term of the previously designated hedged item.

Commodity Price Risk

Commodity price movements create a degree of risk by affecting the price we must pay for certain raw material. Our policy is to use commodity forward and option contracts to manage the commodity risk and reduce the cost of purchased materials.

Our Machinery, Energy & Transportation operations purchase base and precious metals embedded in the components we purchase from suppliers. Our suppliers pass on to us price changes in the commodity portion of the component cost. In addition, we are subject to price changes on energy products such as natural gas and diesel fuel purchased for operational use.

Our objective is to minimize volatility in the price of these commodities. Our policy allows us to enter into commodity forward and option contracts to lock in the purchase price of a portion of these commodities within a five -year horizon. All such commodity forward and option contracts are undesignated.

The location and fair value of derivative instruments reported in the Consolidated Statement of Financial Position are as follows:

|

|

|

|

|

| ||||

(Millions of dollars) | Consolidated Statement of Financial |

| Asset (Liability) Fair Value | ||||||

| Position Location |

| June 30, 2015 |

| December 31, 2014 | ||||

Designated derivatives |

|

|

|

|

| ||||

Foreign exchange contracts |

|

|

| |

|

| | ||

Machinery, Energy & Transportation | Receivables – trade and other |

| $ | 15 | |

| $ | 25 | |

Machinery, Energy & Transportation | Accrued expenses |

| (59 | ) |

| (134 | ) | ||

Interest rate contracts |

|

|

|

|

| | |||

Financial Products | Receivables – trade and other |

| 2 | |

| 6 | | ||

Financial Products | Long-term receivables – trade and other |

| 62 | |

| 73 | | ||

Financial Products | Accrued expenses |

| (5 | ) |

| (8 | ) | ||

|

|

| $ | 15 | |

| $ | (38 | ) |

Undesignated derivatives |

|

|

| |

|

| | ||

Foreign exchange contracts |

|

|

| |

|

| | ||

Machinery, Energy & Transportation | Receivables – trade and other |

| $ | 5 | |

| $ | 2 | |

Machinery, Energy & Transportation | Accrued expenses |

| (23 | ) |

| (43 | ) | ||

Financial Products | Receivables – trade and other |

| 5 | |

| 5 | | ||

Financial Products | Long-term receivables – trade and other |

| 26 | |

| 17 | | ||

Financial Products | Accrued expenses |

| (6 | ) |

| (15 | ) | ||

Commodity contracts |

|

|

|

|

| | |||

Machinery, Energy & Transportation | Accrued expenses |

| (11 | ) |

| (14 | ) | ||

|

|

| $ | (4 | ) |

| $ | (48 | ) |

|

|

|

|

|

| ||||

The total notional amounts of the derivative instruments are as follows:

|

|

|

|

| ||||

(Millions of dollars) |

| June 30, 2015 |

| December 31, 2014 | ||||

|

|

|

|

| ||||

Machinery, Energy & Transportation |

| $ | 2,063 | |

| $ | 3,128 | |

Financial Products |

| $ | 4,098 | |

| $ | 5,249 | |

|

|

|

|

| ||||

15

Table of Contents

The notional amounts of the derivative financial instruments do not represent amounts exchanged by the parties. The amounts exchanged by the parties are calculated by reference to the notional amounts and by other terms of the derivatives, such as foreign currency exchange rates, interest rates or commodity prices.

The effect of derivatives designated as hedging instruments on the Consolidated Statement of Results of Operations is as follows:

Fair Value Hedges |

|

|

|

|

|

| ||||||||||||

|

|

| Three Months Ended |

| Three Months Ended |

| ||||||||||||

(Millions of dollars) | Classification |

| Gains (Losses) on Derivatives |

| Gains (Losses) on Borrowings |

| Gains (Losses) on Derivatives |

| Gains (Losses) on Borrowings |

| ||||||||

Interest rate contracts |

|

|

|

|

|

|

|

|

| |

| |||||||

Financial Products | Other income (expense) |

| $ | (13 | ) |

| $ | 12 | |

| $ | (6 | ) |

| $ | 8 | |

|

|

|

| $ | (13 | ) |

| $ | 12 | |

| $ | (6 | ) |

| $ | 8 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

|

|

| Six Months Ended |

| Six Months Ended |

| ||||||||||||

| Classification |

| Gains (Losses) on Derivatives |

| Gains (Losses) on Borrowings |

| Gains (Losses) on Derivatives |

| Gains (Losses) on Borrowings |

| ||||||||

Interest rate contracts |

|

|

|

|

|

|

|

|

|

| ||||||||

Financial Products | Other income (expense) |

| $ | (14 | ) |

| $ | 13 | |

| $ | (19 | ) |

| $ | 23 | |

|

|

|

| $ | (14 | ) |

| $ | 13 | |

| $ | (19 | ) |

| $ | 23 | |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

|

|

|

|

|

16

Table of Contents

|

|

|

|

|

|

|

|

| ||||||

Cash Flow Hedges |

|

|

|

|

|

|

|

| ||||||

| Three Months Ended June 30, 2015 |

| ||||||||||||

|

|

| Recognized in Earnings |

| ||||||||||

(Millions of dollars) | Amount of Gains (Losses) Recognized in AOCI (Effective Portion) |

| Classification of Gains (Losses) |

| Amount of Gains (Losses) Reclassified from AOCI to Earnings |

| Recognized in Earnings (Ineffective Portion) |

| ||||||

Foreign exchange contracts |

| |

|

|

|

| |

|

| |

| |||

Machinery, Energy & Transportation | $ | 18 | |

| Other income (expense) |

| $ | (37 | ) |

| $ | - | |

|

Interest rate contracts |

|

|

|

|

|

|

|

| ||||||

Machinery, Energy & Transportation | - | |

| Interest expense excluding Financial Products |

| (1 | ) |

| - | |

| |||

Financial Products | - | |

| Interest expense of Financial Products |

| (2 | ) |

| - | | | |||

| $ | 18 | |

|

|

| $ | (40 | ) |

| $ | - | |

|

| Three Months Ended June 30, 2014 |

| ||||||||||||

|

|

| Recognized in Earnings |

| ||||||||||

| Amount of Gains (Losses) Recognized in AOCI (Effective Portion) |

| Classification of Gains (Losses) |

| Amount of Gains (Losses) Reclassified from AOCI to Earnings |

| Recognized in Earnings (Ineffective Portion) |

| ||||||

Foreign exchange contracts |

|

|

|

|

|

|

|

| ||||||

Machinery, Energy & Transportation | $ | 12 | |

| Other income (expense) |

| $ | 10 | |

| $ | - | |

|

Interest rate contracts |

| |

|

|

|

| |

|

| |

| |||

Machinery, Energy & Transportation | (26 | ) |

| Interest expense excluding Financial Products |

| (1 | ) |

| - | |

| |||

Financial Products | (3 | ) |

| Interest expense of Financial Products |

| (1 | ) |

| - | | | |||

| $ | (17 | ) |

|

|

| $ | 8 | |

| $ | - | |

|

|

|

|

|

|

|

|

|

| ||||||

| Six Months Ended June 30, 2015 |

| ||||||||||||

|

|

| Recognized in Earnings |

| ||||||||||

| Amount of Gains (Losses) Recognized in AOCI (Effective Portion) |

| Classification of Gains (Losses) |

| Amount of Gains (Losses) Reclassified from AOCI to Earnings |

| Recognized in Earnings (Ineffective Portion) |

| ||||||

Foreign exchange contracts |

|

|

|

|

|

|

|

| ||||||

Machinery, Energy & Transportation | $ | (7 | ) |

| Other income (expense) |

| $ | (72 | ) | | $ | - | |

|

Interest rate contracts |

|

|

|

|

| |

|

| |

| ||||

Machinery, Energy & Transportation | - | |

| Interest expense excluding Financial Products |

| (3 | ) |

| - | |

| |||

Financial Products | 2 | |

| Interest expense of Financial Products |

| (3 | ) |

| - | | | |||

| $ | (5 | ) |

|

|

| $ | (78 | ) |

| $ | - | |

|

|

|

|

|

|

|

|

|

| ||||||

| Six Months Ended June 30, 2014 |

| ||||||||||||

|

|

| Recognized in Earnings |

| ||||||||||

| Amount of Gains (Losses) Recognized in AOCI (Effective Portion) |

| Classification of Gains (Losses) |

| Amount of Gains (Losses) Reclassified from AOCI to Earnings |

| Recognized in Earnings (Ineffective Portion) |

| ||||||

Foreign exchange contracts |

|

|

|

|

|

|

|

| ||||||

Machinery, Energy & Transportation | $ | 25 | |

| Other income (expense) |

| $ | 20 | | | $ | - | |

|

Interest rate contracts |

| |

|

|

|

| |

|

| |

| |||

Machinery, Energy & Transportation | (63 | ) |

| Interest expense excluding Financial Products |

| (2 | ) |

| - | |

| |||

Financial Products | (5 | ) |

| Interest expense of Financial Products |

| (2 | ) |

| - | | | |||

| $ | (43 | ) |

|

|

| $ | 16 | |

| $ | - | |

|

|

|

|

|

|

|

|

|

| ||||||

|

|

|

|

|

17

Table of Contents

The effect of derivatives not designated as hedging instruments on the Consolidated Statement of Results of Operations is as follows:

|

|

|

| |

|

| |||

(Millions of dollars) | Classification of Gains (Losses) |

| Three Months Ended |

| Three Months Ended | ||||

Foreign exchange contracts |

|

|

|

|

| ||||

Machinery, Energy & Transportation | Other income (expense) |

| $ | 26 | |

| $ | (2 | ) |

Financial Products | Other income (expense) |

| 4 | |

| (12 | ) | ||

Commodity contracts |

|

|

| |

|

| |||

Machinery, Energy & Transportation | Other income (expense) |

| (1 | ) |

| 4 | | ||

|

|

| $ | 29 | |

| $ | (10 | ) |

|

|

|

|

|

| ||||

| Classification of Gains (Losses) |

| Six Months Ended |

| Six Months Ended | ||||

Foreign exchange contracts |

|

|

|

|

| ||||

Machinery, Energy & Transportation | Other income (expense) |

| $ | (29 | ) |

| $ | 9 | |

Financial Products | Other income (expense) |

| (24 | ) |

| (17 | ) | ||

Commodity contracts |

|

|

|

|

| ||||

Machinery, Energy & Transportation | Other income (expense) |

| (7 | ) |

| 3 | | ||

|

|

| $ | (60 | ) |

| $ | (5 | ) |

|

|

|

|

|

| ||||

We enter into International Swaps and Derivatives Association (ISDA) master netting agreements within Machinery, Energy & Transportation and Financial Products that permit the net settlement of amounts owed under their respective derivative contracts. Under these master netting agreements, net settlement generally permits the company or the counterparty to determine the net amount payable for contracts due on the same date and in the same currency for similar types of derivative transactions. The master netting agreements generally also provide for net settlement of all outstanding contracts with a counterparty in the case of an event of default or a termination event.

Collateral is generally not required of the counterparties or of our company under the master netting agreements. As of June 30, 2015 and December 31, 2014 , no cash collateral was received or pledged under the master netting agreements.

18

Table of Contents

The effect of the net settlement provisions of the master netting agreements on our derivative balances upon an event of default or termination event is as follows:

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

June 30, 2015 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Assets |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Assets Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Received |

| Net Amount of Assets | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | 20 | |

| $ | - | |

| $ | 20 | |

| $ | (20 | ) |

| $ | - | |

| $ | - | |

Financial Products |

| 95 | |

| - | |

| 95 | |

| (7 | ) |

| - | |

| 88 | | ||||||

Total |

| $ | 115 | |

| $ | - | |

| $ | 115 | |

| $ | (27 | ) |

| $ | - | |

| $ | 88 | |

June 30, 2015 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Liabilities |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Liabilities Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Pledged |

| Net Amount of Liabilities | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | (93 | ) |

| $ | - | |

| $ | (93 | ) |

| $ | 20 | |

| $ | - | |

| $ | (73 | ) |

Financial Products |

| (11 | ) |

| - | |

| (11 | ) |

| 7 | |

| - | |

| (4 | ) | ||||||

Total |

| $ | (104 | ) |

| $ | - | |

| $ | (104 | ) |

| $ | 27 | |

| $ | - | |

| $ | (77 | ) |

December 31, 2014 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Assets |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Assets Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Received |

| Net Amount of Assets | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | 27 | |

| $ | - | |

| $ | 27 | |

| $ | (27 | ) |

| $ | - | |

| $ | - | |

Financial Products |

| 101 | |

| - | |

| 101 | |

| (8 | ) |

| - | |

| 93 | | ||||||

Total |

| $ | 128 | |

| $ | - | |

| $ | 128 | |

| $ | (35 | ) |

| $ | - | |

| $ | 93 | |

December 31, 2014 |

|

|

|

|

|

|

| Gross Amounts Not Offset in the Statement of Financial Position |

|

| ||||||||||||||

(Millions of dollars) |

| Gross Amount of Recognized Liabilities |

| Gross Amounts Offset in the Statement of Financial Position |

| Net Amount of Liabilities Presented in the Statement of Financial Position |

| Financial Instruments |

| Cash Collateral Pledged |

| Net Amount of Liabilities | ||||||||||||

Derivatives |

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Machinery, Energy & Transportation |

| $ | (191 | ) |

| $ | - | |

| $ | (191 | ) |

| $ | 27 | |

| $ | - | |

| $ | (164 | ) |

Financial Products |

| (23 | ) |

| - | |

| (23 | ) |

| 8 | |

| - | |

| (15 | ) | ||||||

Total |

| $ | (214 | ) |

| $ | - | |

| $ | (214 | ) |

| $ | 35 | |

| $ | - | |

| $ | (179 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

19

Table of Contents

5. Inventories

Inventories (principally using the last-in, first-out (LIFO) method) are comprised of the following:

|

|

|

| ||||

(Millions of dollars) | June 30, |

| December 31, | ||||

Raw materials | $ | 2,932 | |

| $ | 2,986 | |

Work-in-process | 2,099 | |

| 2,455 | | ||

Finished goods | 6,397 | |

| 6,504 | | ||

Supplies | 253 | |

| 260 | | ||

Total inventories | $ | 11,681 | |

| $ | 12,205 | |

|

|

|

| ||||

6. Investments in unconsolidated affiliated companies

Combined financial information of the unconsolidated affiliated companies accounted for by the equity method (generally on a lag of 3 months or less) was as follows:

|

|

|

|

|

|

|

| ||||||||

Results of Operations of unconsolidated affiliated companies: (Millions of dollars) | Three Months Ended |

| Six Months Ended | ||||||||||||

| 2015 |

| 2014 |

| 2015 |

| 2014 | ||||||||

Sales | $ | 190 | |

| $ | 410 | |

| $ | 353 | |

| $ | 800 | |

Cost of sales | 146 | |

| 316 | |

| 271 | |

| 617 | | ||||

Gross profit | $ | 44 | |

| $ | 94 | |

| $ | 82 | |

| $ | 183 | |

|

|

|

|

|

|

|

| ||||||||

Profit (loss) | $ | 4 | |

| $ | 4 | |

| $ | 8 | |

| $ | (10 | ) |

|

|

|

|

|

|

|

| ||||||||

|

|

|

| ||||

Financial Position of unconsolidated affiliated companies: ( Millions of dollars ) | June 30, |

| December 31, | ||||

Assets: |

| |

|

| | ||

Current assets | $ | 507 | |

| $ | 716 | |

Property, plant and equipment – net | 187 | |

| 653 | | ||

Other assets | 190 | |

| 557 | | ||

| 884 | |

| 1,926 | | ||

Liabilities: |

| |

|

| | ||

Current liabilities | 287 | |

| 518 | | ||

Long-term debt due after one year | 181 | |

| 867 | | ||

Other liabilities | 13 | |

| 215 | | ||

| 481 | |

| 1,600 | | ||

Equity | $ | 403 | |

| $ | 326 | |

|

|

|

| ||||

|

|

|

| ||||

Caterpillar's investments in unconsolidated affiliated companies: (Millions of dollars) | June 30, |

| December 31, | ||||

Investments in equity method companies | $ | 193 | |

| $ | 248 | |

Plus: Investments in cost method companies | 36 | |

| 9 | | ||

Total investments in unconsolidated affiliated companies | $ | 229 | |

| $ | 257 | |

|

|

|

| ||||

The changes in the 2015 results of operations, financial position and investments in equity method companies noted above are primarily related to the sale of Caterpillar's 35 percent equity interest in a third party logistics business, formerly Caterpillar Logistics Services LLC, which occurred in February, 2015 (see Note 18).

20

Table of Contents

7. Intangible assets and goodwill

A. Intangible assets

Intangible assets are comprised of the following:

|

|

|

|

|

|

|

| ||||||

|

|

| June 30, 2015 | ||||||||||

(Millions of dollars) | Weighted Amortizable Life (Years) |

| Gross Carrying Amount |

| Accumulated Amortization |

| Net | ||||||

Customer relationships | 15 |

| $ | 2,432 | |

| $ | (736 | ) |

| $ | 1,696 | |

Intellectual property | 11 |

| 1,681 | |

| (619 | ) |

| 1,062 | | |||

Other | 11 |

| 248 | |

| (143 | ) |

| 105 | | |||

Total finite-lived intangible assets | 13 |

| $ | 4,361 | |

| $ | (1,498 | ) |

| $ | 2,863 | |

|

|

| December 31, 2014 | ||||||||||

| Weighted Amortizable Life (Years) |

| Gross Carrying Amount |

| Accumulated Amortization |

| Net | ||||||

Customer relationships | 15 |

| $ | 2,489 | |

| $ | (669 | ) |

| $ | 1,820 | |

Intellectual property | 11 |

| 1,724 | |

| (578 | ) |

| 1,146 | | |||

Other | 11 |

| 239 | |

| (129 | ) |

| 110 | | |||

Total finite-lived intangible assets | 14 |

| $ | 4,452 | |

| $ | (1,376 | ) |

| $ | 3,076 | |

|

|

|

|

|

|

|

| ||||||

Amortization expense for the three and six months ended June 30, 2015 was $87 million and $174 million , respectively. Amortization expense for the three and six months ended June 30, 2014 was $93 million and $185 million , respectively. Amortization expense related to intangible assets is expected to be:

(Millions of dollars) | ||||||||||

2015 |

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| Thereafter |

$338 |

| $318 |

| $318 |

| $311 |

| $310 |

| $1,442 |

|

|

|

|

|

|

|

|

|

|

|

B. Goodwill

We test goodwill for impairment annually and whenever events or circumstances make it more likely than not that an impairment may have occurred. We perform our annual goodwill impairment test as of October 1 and monitor for interim triggering events on an ongoing basis. Goodwill is reviewed for impairment utilizing a qualitative assessment or a two-step process. We have an option to make a qualitative assessment of a reporting unit's goodwill for impairment. If we choose to perform a qualitative assessment and determine the fair value more likely than not exceeds the carrying value, no further evaluation is necessary. For reporting units where we perform the two-step process, the first step requires us to compare the fair value of each reporting unit, which we primarily determine using an income approach based on the present value of discounted cash flows, to the respective carrying value, which includes goodwill. If the fair value of the reporting unit exceeds its carrying value, the goodwill is not considered impaired. If the carrying value is higher than the fair value, there is an indication that an impairment may exist and the second step is required. In step two, the implied fair value of goodwill is calculated as the excess of the fair value of a reporting unit over the fair values assigned to its assets and liabilities. If the implied fair value of goodwill is less than the carrying value of the reporting unit's goodwill, the difference is recognized as an impairment loss. No goodwill was impaired during the three and six months ended June 30, 2015 or 2014 .

21

Table of Contents

The changes in carrying amount of goodwill by reportable segment for the six months ended June 30, 2015 were as follows:

|

|

|

|

|

|

| ||||||

(Millions of dollars) |

| December 31, |

| Other Adjustments 1 |

| June 30, | ||||||

Construction Industries |

|

|

|

|

| | | |||||

Goodwill |

| $ | 275 | |

| $ | (11 | ) |

| $ | 264 | |

Resource Industries |

|

|

|

|

|

| ||||||

Goodwill |

| 4,287 | |

| (94 | ) |

| 4,193 | | |||

Impairments |

| (580 | ) |

| - | |

| (580 | ) | |||

Net goodwill |

| 3,707 | |

| (94 | ) |

| 3,613 | | |||

Energy & Transportation |

|

|

|

|

|

| ||||||

Goodwill |

| 2,542 | |

| (36 | ) |

| 2,506 | | |||

All Other 2 |

|

|

|

|

|

| ||||||

Goodwill |

| 192 | |

| (3 | ) |

| 189 | | |||

Impairments |

| (22 | ) |

| - | |

| (22 | ) | |||

Net goodwill |

| 170 | |

| (3 | ) |

| 167 | | |||

Consolidated total |

|

|

|

|

|

| ||||||

Goodwill |

| 7,296 | |

| (144 | ) |

| 7,152 | | |||

Impairments |

| (602 | ) |

| - | |

| (602 | ) | |||

Net goodwill |

| $ | 6,694 | |

| $ | (144 | ) |

| $ | 6,550 | |

1 Other adjustments are comprised primarily of foreign currency translation.

2 Includes All Other operating segments (See Note 15).

|

|

|

|

|

8. Available-for-sale securities

We have investments in certain debt and equity securities, primarily at Insurance Services, that have been classified as available-for-sale and recorded at fair value based upon quoted market prices. These investments are primarily included in Other assets in the Consolidated Statement of Financial Position. Unrealized gains and losses arising from the revaluation of available-for-sale securities are included, net of applicable deferred income taxes, in equity (Accumulated other comprehensive income (loss) in the Consolidated Statement of Financial Position). Realized gains and losses on sales of investments are generally determined using the specific identification method for debt and equity securities and are included in Other income (expense) in the Consolidated Statement of Results of Operations.

22

Table of Contents

| June 30, 2015 |

| December 31, 2014 | ||||||||||||||||||||

(Millions of dollars) | Cost Basis |

| Unrealized Pretax Net Gains (Losses) |

| Fair Value |

| Cost Basis |

| Unrealized Pretax Net Gains (Losses) |

| Fair Value | ||||||||||||

Government debt |

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

U.S. treasury bonds | $ | 10 | |

| $ | - | |

| $ | 10 | |

| $ | 10 | |

| $ | - | |

| $ | 10 | |

Other U.S. and non-U.S. government bonds | 89 | |

| 1 | |

| 90 | |

| 94 | |

| - | |

| 94 | | ||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Corporate bonds |

| |

|

| |

|

|

|

| |

|

| |

|

| | |||||||

Corporate bonds | 669 | |

| 15 | |

| 684 | |

| 677 | |

| 16 | |

| 693 | | ||||||

Asset-backed securities | 98 | |

| 1 | |

| 99 | |

| 103 | |

| 2 | |

| 105 | | ||||||

|

|

|

|

|

|

|

|

|

|

|

| ||||||||||||

Mortgage-backed debt securities |

|

|

|

|

|

|

| |

|

| |

|

| | |||||||||