Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended July 31, 2014

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 1-14959

BRADY CORPORATION

(Exact name of registrant as specified in charter)

Wisconsin |

| 39-0178960 |

(State or other jurisdiction of incorporation or organization) |

| (IRS Employer Identification No.) |

6555 West Good Hope Road, Milwaukee, WI |

| 53223 |

(Address of principal executive offices) |

| (Zip Code) |

(414) 358-6600

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

Class A Nonvoting Common Stock, Par Value $.01 per share |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer", "accelerated filer", and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | x |

| Accelerated filer | ¨ |

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) |

| Smaller reporting company | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

The aggregate market value of the non-voting common stock held by non-affiliates of the registrant as of January 31, 2014, was approximately $1,258,833,135 based on closing sale price of $27.36 per share on that date as reported for the New York Stock Exchange. As of September 24, 2014, there were 47,708,274 outstanding shares of Class A Nonvoting Common Stock (the "Class A Common Stock"), and 3,538,628 shares of Class B Common Stock. The Class B Common Stock, all of which is held by affiliates of the registrant, is the only voting stock.

Table of Contents

INDEX

PART I | Page |

Item.1 Business | 3 |

General Development of Business | 3 |

Financial Information About Industry Segments | 3 |

Narrative Description of Business | 3 |

Overview | 3 |

Research and Development | 5 |

Operations | 6 |

Environment | 6 |

Employees | 6 |

Financial Information About Foreign and Domestic Operations and Export Sales | 6 |

Information Available on the Internet | 6 |

Item 1A. Risk Factors | 7 |

Item 1B. Unresolved Staff Comments | 12 |

Item 2. Properties | 12 |

Item 3. Legal Proceedings | 12 |

Item 4. Mine Safety Disclosures | 12 |

PART II |

|

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 13 |

Item 6. Selected Financial Data | 15 |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations | 16 |

Item 7A. Quantitative and Qualitative Disclosures About Market Risk | 32 |

Item 8. Financial Statements and Supplementary Data | 33 |

Item 9. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | 73 |

Item 9A. Controls and Procedures | 74 |

Item 9B. Other Information | 76 |

PART III |

|

Item 10. Directors and Executive Officers of the Registrant | 76 |

Item 11. Executive Compensation | 81 |

Compensation Discussion and Analysis | 81 |

Management Development and Compensation Committee Interlocks and Insider Participation | 94 |

Management Development and Compensation Committee Report | 94 |

Compensation Policies and Practices | 95 |

Summary Compensation Table | 95 |

Grants of Plan-Based Awards for 201 4 | 97 |

Outstanding Equity Awards at 2014 Fiscal Year End | 97 |

Option Exercises and Stock Vested for Fiscal 201 4 | 99 |

Non-Qualified Deferred Compensation for Fiscal 201 4 | 100 |

Potential Payments Upon Termination or Change in Control | 100 |

Compensation of Directors | 102 |

Director Compensation Table - Fiscal 201 4 | 103 |

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 104 |

Item 13. Certain Relationships, Related Transactions, and Director Independence | 106 |

Item 14. Principal Accounting Fees and Services | 107 |

PART IV |

|

Item 15. Exhibits and Financial Statement Schedules | 108 |

Signatures | 114 |

2

PART I

Item 1. Business

(a) General Development of Business

Brady Corporation ("Brady," "Company," "we," "us," "our") was incorporated under the laws of the state of Wisconsin in 1914. The Company's corporate headquarters are located at 6555 West Good Hope Road, Milwaukee, Wisconsin 53223, and the telephone number is (414) 358-6600.

Brady Corporation is a global manufacturer and supplier of identification solutions, specialty materials, and workplace safety products that identify and protect premises, products and people. The ability to provide customers with a broad range of proprietary, customized, and diverse products for use in various applications, along with a commitment to quality and service, a global footprint and multiple sales channels, have made Brady a world leader in many of its markets.

The Company's primary objective is to build upon its market position and increase shareholder value by improving in the following key competencies:

• | Global leadership position in niche markets |

• | Innovation advantage - Internally developed products drive growth and sustain gross profit margins |

• | Operational excellence - Continuous productivity improvement, business simplification and process transformation |

• | Customer service - Focus on the customer and understanding customer needs |

• | Compliance expertise |

Over the last two years, we made significant portfolio and management decisions designed to better position the Company for growth in the future. These changes were a meaningful shift from the more volatile and less profitable consumer electronics Die-Cut business, which was partially divested in fiscal 2014, to an expansion of our core Identification Solutions ("ID Solutions" or "IDS") business to focus on markets with long-term growth trends. In our Workplace Safety ("WPS") business, our strategy to return to growth included a focus on workplace safety critical industries in addition to increased investment in e-commerce expertise.

Key initiatives supporting the strategy in fiscal 2014 included:

• | Enhanced the WPS segment's multi-channel direct marketing model and increased its offering of identification and workplace safety products with a heightened focus on proprietary and customized product offerings. |

• | Increased investment in the WPS segment with an emphasis on e-commerce capabilities. |

• | Modified the healthcare strategy to focus on key accounts, the development of proprietary new products, and expansion of the sales focus on alternate healthcare sites. |

• | Expanded the Company's IDS business through sales force expansion in the United States and EMEA, increased focus on strategic accounts, and developed innovative proprietary new products. |

• | Divested the Company's less profitable Die-Cut business in Asia and Europe. |

• | Reduced the Company's cost structure through the consolidation of selected manufacturing facilities in the Americas and EMEA. |

• | Focused on the development of high quality products and improvements in customer service. |

In fiscal 2014, the Company entered into an agreement with LTI Flexible Products, Inc. (d/b/a Boyd Corporation) for the sale of its Die-Cut business. The first phase of the divestiture closed on May 1, 2014 and included the Company's European Die-Cut business and the portions of the Asia Die-Cut business operated in Korea, Thailand and Malaysia, together with the transfer of certain of the Company's employees in the United States supporting those operations. The second phase of the divestiture was for the Company's Die-Cut businesses located in China and closed on August 1, 2014, subsequent to the fiscal year ended July 31, 2014.

(b) Financial Information About Industry Segments

The information required by this Item is provided in Note 9 of the Notes to Consolidated Financial Statements contained in Item 8 - Financial Statements and Supplementary Data.

(c) Narrative Description of Business

Overview

The Company is organized and managed on a global basis within two business platforms: Identification Solutions and Workplace Safety, which are the reportable segments.

Table of Contents

The IDS segment includes high-performance and innovative identification and healthcare products that are manufactured internally under the Brady brand, and are primarily sold through distribution to a broad range of MRO and OEM customers and through other channels, including direct sales, catalog marketing, and the Internet.

The WPS segment includes workplace safety and compliance products, which are sold under multiple brand names through catalog and e-business to a broad range of MRO customers. Approximately half of the WPS business is resale product and half is manufactured internally.

Below is a summary of sales by reportable segments for the fiscal years ended July 31:

|

| 2014 |

| 2013 |

| 2012 | |||

IDS |

| 67.4 | % |

| 63.8 | % |

| 59.4 | % |

WPS |

| 32.6 | % |

| 36.2 | % |

| 40.6 | % |

Total |

| 100 | % |

| 100 | % |

| 100 | % |

ID Solutions

Within the ID Solutions platform, the primary product categories include:

• | Facility identification, which includes safety signs, pipe markers, labeling systems, spill control products, and lockout/tagout devices |

• | Product identification, which includes materials and printing systems for product identification, brand protection labeling, work in process labeling, and finished product identification |

• | Wire identification, which includes hand-held printers, wire markers, sleeves, and tags |

• | People identification, which includes self-expiring name tags, badges, lanyards, and access control software |

• | Patient identification, which includes wristbands and labels used in hospitals for tracking and improving the safety of patients |

• | Custom wristbands used in the leisure and entertainment industry such as theme parks, concerts and festivals |

Approximately 73% of ID Solutions products are sold under the Brady brand. In the United States, identification products for the utility industry are marketed under the Electromark brand; spill-control products are marketed under the SPC brand; and security and identification badges and systems are marketed under the B.I.G., Identicard/Identicam, STOPware, PromoVision, and Brady People ID brands. Wire identification products are marketed under the Modernotecnica brand in Italy and lockout/tagout products are offered under the Scafftag brand in the U.K. Custom labels and nameplates are available under the Stickolor brand in Brazil; and identification and patient safety products in the healthcare industry and custom wristbands for the leisure and entertainment industry are available under the PDC Innovative brand in the U.S. and Europe.

The ID Solutions platform offers high quality products with rapid response and superior service to provide solutions to customers. The business markets and sells products through multiple channels including distributors, direct sales, catalog marketing, and the Internet. The businesses' sales force partners with end-users and distributors by providing technical application and product expertise.

ID Solutions serves customers in many industries, which include industrial manufacturing, electronic manufacturing, healthcare, chemical, oil, gas, food and beverage, aerospace, defense, mass transit, electrical contractors, leisure and entertainment and telecommunications, among others.

The ID Solutions platform manufactures differentiated, proprietary products, most of which have been internally developed. These internally developed products include materials, printing systems, and software. IDS competes for business principally on the basis of production capabilities, engineering, research and development capabilities, materials expertise, global account management where needed, customer service, product quality and price. Competition is highly fragmented, ranging from smaller companies offering minimal product variety, to some of the world's largest major adhesive and electrical product companies offering competing products as part of their overall product lines.

Workplace Safety

Within the Workplace Safety business platform, the primary product categories are workplace safety and compliance products, which include informational signs, tags, security, safety and traffic compliance related products, first aid supplies, material handling, asset identification, safety and facility identification, and workplace regulatory products.

Products within the Workplace Safety platform are sold under a variety of brands including: safety and facility identification products offered under the Seton, Emedco, Signals, Personnel Concepts, Safety Signs Service and Pervaco brands; first aid supplies under the Accidental Health and Safety, Trafalgar, and Securimed brands; industrial, office equipment under the Runelandhs brand; and wire identification products marketed under the Carroll brand.

4

Table of Contents

Workplace Safety markets and sells products through multiple channels, including catalog, telemarketing and e-commerce. The business serves customers in many industries, including process industries, manufacturers, government, education, construction, and utilities.

The Workplace Safety platform manufactures a broad range of stock and custom identification products, and also sells a broad range of related resale products. Historically, both the Company and many of our competitors focused their businesses on catalog marketing, often with varying product niches. However, the competitive landscape is changing with the continued evolution of e-commerce channels. Many of our competitors extensively utilize e-commerce to promote the sale of their products. A consequence of this shift is price transparency, as prices on non-proprietary products can be easily compared. Dynamic pricing capabilities and enhanced customer experience are critical to convert customers from traditional catalog channels to the Internet.

Discontinued Operations

Discontinued operations include the Asia Die-Cut and Balkhausen Die-Cut businesses ("Die-Cut"), which were announced as held for sale in the third and fourth quarters of fiscal 2013, respectively. In fiscal 2014, the Company entered into an agreement with LTI Flexible Products, Inc. (d/b/a Boyd Corporation) for the sale of Die-Cut. The first phase of the divestiture closed in May 2014 and the second phase of the divestiture closed in August 2014. The assets and liabilities of the businesses included in the second phase were classified as held for sale on the consolidated balance sheet as of July 31, 2014. The operating results of the Die-Cut businesses were reflected as discontinued operations in the consolidated statements of earnings for the years ended July 31, 2014, 2013 and 2012. In addition, the following previously divested businesses were reported within discontinued operations: Brady Medical and Varitronics (divested in fiscal 2013) and Etimark (divested in fiscal 2012). These divested businesses were part of the IDS business platform.

The Die-Cut business consisted of the manufacture and sale of precision converted products such as gaskets, meshes, heat-dissipation materials, antennae, dampers, filters, and similar products sold primarily to the electronics industry with a concentration in the mobile-handset and hard-disk drive industries and other traditional die-cut parts and thermal management products used in the automotive, electronics and telecommunications industries. Products within the Die-Cut business were sold primarily under the Brady brand, with some European business marketed under the Balkhausen brand. The business sold through a technical direct sales force and was supported by global strategic account management. The Die-Cut business served customers in many industries, including mobile handset, hard disk drive, consumer electronics, and other computing devices, as well as products for the automotive and medical equipment industries.

Research and Development

The Company focuses its research and development ("R&D") efforts on pressure sensitive materials, printing systems and software, and it mainly supports the IDS segment. Material development involves the application of surface chemistry concepts for top coatings and adhesives applied to a variety of base materials. Systems design integrates materials, embedded software and a variety of printing technologies to form a complete solution for customer applications. In addition, the research and development team supports production and marketing efforts by providing application and technical expertise.

The Company owns patents and tradenames relating to certain products in the United States and internationally. Although the Company believes that patents are a significant driver in maintaining its position for certain products, technology in the areas covered by many of the patents continues to evolve and may limit the value of such patents. The Company's business is not dependent on any single patent or group of patents. Patents applicable to specific products extend for up to 20 years according to the date of patent application filing or patent grant, depending upon the legal term of patents in the various countries where patent protection is obtained. The Company's tradenames are valid ten years from the date of registration, and are typically renewed on an ongoing basis.

The Company spent $35.0 million , $33.6 million , and $34.5 million during the fiscal years ended July 31, 2014 , 2013 , and 2012 , respectively, on its R&D activities related to continuing operations. The increase in R&D spending in 2014 was primarily due to increased investment in new products. In addition, in fiscal 2014, the Company realigned the R&D processes in order to accelerate new product innovation and invested in emerging technologies such as RFID and sensing technology for harsh environments and mobile applications that allow users to work with a variety of electronic devices. As of July 31, 2014 , 198 employees were engaged in research and development activities for the Company.

5

Table of Contents

Operations

The materials used in the products manufactured consist primarily of a variety of plastic and synthetic films, paper, metal and metal foil, cloth, fiberglass, inks, dyes, adhesives, pigments, natural and synthetic rubber, organic chemicals, polymers, and solvents for consumable identification products in addition to electronic components, molded parts and sub-assemblies for printing systems. The Company operates a coating facility that manufactures bulk rolls of label stock for internal and external customers. In addition, the Company purchases finished products for resale.

The Company purchases raw materials, components and finished products from many suppliers. Overall, the Company is not dependent upon any single supplier for its most critical base materials or components; however, the Company has chosen in certain situations to sole source, or limit the sources of materials, components, or finished items for design or cost reasons. As a result, disruptions in supply could have an impact on results for a period of time, but we believe any disruptions would simply require qualification of new suppliers and the disruption would be modest. In certain instances, the qualification process could be more costly or take a longer period of time and in rare circumstances, such as a global shortage of critical materials or components, the financial impact could be significant. The Company currently operates 50 manufacturing or distribution facilities globally.

The Company carries working capital mainly related to accounts receivable and inventory. Inventory consists of raw materials, work in process and finished goods. Generally, custom products are made to order while an on-hand quantity of stock product is maintained to provide customers with timely delivery. Normal and customary payment terms range from net 30 to 90 days from date of invoice and varies by geographies.

The Company has a broad customer base, and no individual customer is 5% or more of total net sales.

Average delivery time for customer orders varies from same-day delivery to one month, depending on the type of product, customer request, and whether the product is stock or custom-designed and manufactured. The Company's backlog is not material, does not provide significant visibility for future business and is not pertinent to an understanding of the business.

Environment

Compliance with federal, state and local environmental protection laws during fiscal 2014 did not have a material impact on the Company's business, financial condition or results of operations.

Employees

As of July 31, 2014 , the Company employed approxima tely 7,200 ind ividuals. Brady has never experienced a material work stoppage due to a labor dispute and considers its relations with employees to be good.

(d) Financial Information About Foreign and Domestic Operations and Export Sales

The information required by this Item is provided in Note 9 of the Notes to Consolidated Financial Statements contained in Item 8 - Financial Statements and Supplementary Data.

(e) Information Available on the Internet

The Company's Corporate Internet address is http://www.bradycorp.com. The Company makes available, free of charge, on or through its Internet website copies of its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to all such reports as soon as reasonably practicable after such reports are electronically filed with or furnished to the SEC. The Company is not including the information contained on or available through its website as part of, or incorporating such information by reference into, this Annual Report on Form 10-K.

6

Table of Contents

Item 1A. Risk Factors

Investors should carefully consider the risks set forth below and all other information contained in this report and other documents we file with the SEC. The risks and uncertainties described below are those that we have identified as material, but are not the only risks and uncertainties facing us. Our business is also subject to general risk and uncertainties that affect many other companies, such as market conditions, geopolitical events, changes in laws or accounting rules, fluctuations in interest rates, terrorism, wars or conflicts, major health concerns, natural disasters or other disruptions of expected economic or business conditions. Additional risks and uncertainties not currently known to us or that we currently believe are immaterial also may impair our business, including our results of operations, liquidity and financial conditions.

Business Risks

Failure to successfully implement our strategy in the Healthcare sector, or if successfully implemented, failure to realize the benefits expected from the strategy, may adversely affect our business, sales, results of operations, cash flow and liquidity.

In December 2012, Brady acquired Precision Dynamics Corporation ("PDC") to establish a base for our healthcare strategy. In fiscal 2014, PDC represented 12.5% of our total sales from continuing operations. Sales declined approximately 2% at PDC in fiscal 2014 and the healthcare industry continues to be in a state of change with the uncertainty relating to government healthcare reforms. During fiscal 2014, we recorded impairment charges of $148.6 million, primarily related to the goodwill and other intangible assets in the PeopleID reporting unit, which consists primarily of the PDC business. The Company's strategy to grow this business includes: key account focus offering customers a broad range of products to meet their complete identification needs, development and launch of proprietary new products, full continuum of care in the healthcare industry, and international sales penetration. There is a risk that the Company will not be able to return the business to growth and grow the business consistently, the strategy will fail, or the business will face increased levels of competition and pricing pressure. If these risks materialize, their effects could adversely impact our business, sales, results of operations, cash flow and liquidity.

Failure to successfully implement our Workplace Safety strategy, or if successfully implemented, failure to realize the benefits expected from the strategy, may adversely affect our business, sales, results of operations, cash flow and liquidity.

In fiscal 2014, the Workplace Safety segment represented 32.6% of our total sales from continuing operations. Beginning in the second quarter of fiscal 2012, the WPS segment experienced deterioration in sales and profits due to a reduction in direct catalog mailings, increased e-commerce competition, and pricing adjustments. While traditional direct marketing channels such as catalogs are important means of selling WPS products, an increasing number of customers are purchasing products on the Internet. The Company's strategy to grow this business includes: increased volume of catalog mailings, expanded e-commerce presence, further developed pricing capabilities, growing the customer base, and the expansion of products offered. The rate of sales decline in fiscal 2014 lessened each quarter and the segment returned to positive organic growth of 0.9% in the fourth quarter of fiscal 2014 as the strategy began to take hold. There is a risk that the Company will not continue to successfully implement this strategy, or if successfully implemented, not realize its expected benefits, due to the continued levels of increased competition and pricing pressure brought about by the Internet. There is also a risk that the Company may not be able to permanently reverse the downward trends in this business and return the segment to historic levels of sales and profits. If these risks materialize, their effects could adversely impact our business, sales, results of operations, cash flow and liquidity.

Failure to compete effectively or remain competitive may have a negative impact on our business, sales, results of operations, cash flow and liquidity.

We actively compete with companies that produce and market the same or similar products, and in some instances, with companies that sell different products that are designed for the same end user. Additionally, we continue to face competition through the Internet in our entire business. Competition may force us to reduce prices or incur additional costs to remain competitive. We compete on the basis of price, customer support, product innovation, product offering, product quality, expertise, production capabilities, and for multinational customers, our global footprint. Present or future competitors may develop and introduce new and enhanced products, offer products based on alternative technologies and processes , accept lower profit, have greater financial, technical or other resources, or lower production costs or other pricing advantages. Any of these could put us at a disadvantage by threatening our share of sales or reducing our profit margins, which could adversely impact our results of operations, cash flow and liquidity. Additionally, throughout our global business, distributors and customers may seek lower cost sourcing opportunities, which could result in a loss of business that may adversely impact our business, sales, results of operations, cash flow and liquidity.

Failure to successfully complete our facility consolidation plans may adversely impact our business, sales, results of operations, cash flow and liquidity.

We continue to implement measures to reduce our cost structure, simplify our business structure, and standardize our processes. In fiscal 2013, we incurred approximately $26 million in restructuring costs associated with the reorganization of the

7

Table of Contents

Company along global product lines, which included the standardization of business systems and a restructuring of the global workforce. At the end of fiscal 2013 and into fiscal 2014, our focus turned to the consolidation of facilities, which resulted in approximately $15 million of restructuring expense in fiscal 2014. Facility consolidation activities will extend into fiscal 2015 as we slowed certain consolidation activities to ensure the highest levels of quality and delivery throughout the transition. Successfully completing the facilities consolidations is critical to our future competitiveness and to improve profitability. Facility consolidations will result in a higher concentration of operations in certain locations. Risks related to facility consolidations include poor execution impacting customer service, customer acceptance of these changes, inability to implement standard processes and systems, resource allocation among competing priorities, employee disruption and turnover, inability to manufacture and supply products in the event of a material casualty event at one of our principal facilities, and additional or higher than anticipated charges related to these actions. These actions to reduce our cost structure and the charges related to these actions could have a material adverse impact on our business, sales, results of operations, cash flow and liquidity.

Deterioration of or instability in the global economy and financial markets may adversely affect our business, sales, results of operations, cash flow and liquidity.

Our business and operating results could be affected by global economic conditions. In fiscal 2013, our business was negatively impacted by the weak economy in Europe, Australia and Brazil. In fiscal 2014, Brazil continued to weaken. When global economic conditions deteriorate or economic uncertainty continues, customers and potential customers may experience deterioration of their businesses, which may result in the delay or cancellation of plans to purchase our products. Our sensitivity to economic cycles and any related fluctuations in the businesses of our customers or potential customers could have a material adverse impact on our business, sales, results of operations, cash flow and liquidity.

Our failure or the failure of third-party service providers to protect our sites, networks and systems against security breaches, or otherwise to protect our confidential information, may substantially harm our business, sales, results of operations, cash flow and liquidity.

Our business systems collect, maintain, transmit and store data about our customers, vendors and others, including credit card information and personally identifiable information, as well as other confidential and proprietary information. We also employ third-party service providers that store, process and transmit proprietary, personal and confidential information on our behalf. We rely on encryption and authentication technology licensed from third parties in an effort to securely transmit confidential and sensitive information, including credit card numbers. Our security measures, and those of our third-party service providers, may not detect or prevent all attempts to hack our systems, denial-of-service attacks, viruses, malicious software, break-ins, phishing attacks, social engineering, security breaches or other attacks and similar disruptions that may jeopardize the security of information stored in or transmitted by our sites, networks and systems or that we or our third-party service providers otherwise maintain. We and our service providers may not have the resources or technical sophistication to anticipate or prevent all types of attacks, and techniques used to obtain unauthorized access to or sabotage systems change frequently and may not be known until launched against us or our third-party service providers. In addition, security breaches can also occur as a result of non-technical issues, including intentional or inadvertent breaches by our employees or by persons with whom we have commercial relationships. Although we maintain privacy, data breach and network security liability insurance, we cannot be certain that our coverage will be adequate for liabilities actually incurred or that insurance will continue to be available to us on economically reasonable terms, or at all. Any compromise or breach of our security measures, or those of our third-party service providers, could adversely impact our ability to conduct business, violate applicable privacy, data security and other laws, and cause significant legal and financial exposure, adverse publicity, and a loss of confidence in our security measures, which could have an adverse and material effect on our business, sales, results of operations, cash flow and liquidity.

The global nature of our business exposes us to foreign currency fluctuations that could adversely affect sales, results of operations, cash flow, and liquidity.

Approximately 50% of our sales are derived outside the United States. Sales and purchases in currencies other than the U.S. dollar expose us to fluctuations in foreign currencies relative to the U.S. dollar, and may adversely affect our financial statements. Increased strength of the U.S. dollar will increase the effective price of our products sold in currencies other than U.S. dollars into other countries. Decreased strength of the U.S. dollar could adversely affect the cost of materials, products, and services purchased overseas. Our sales and expenses are translated into U.S. dollars for reporting purposes, and the strengthening or weakening of the U.S. dollar could result in unfavorable translation effects. In addition, certain of our subsidiaries may invoice customers in a currency other than its functional currency, which could result in unfavorable translation effects on sales, results of operations, cash flow and liquidity.

8

Table of Contents

Failure to develop new products or gain acceptance of new products could adversely impact our sales, results of operations, cash flow and liquidity.

Development of proprietary products is a driver of core growth and reasonable gross profit margins both currently and in the future, particularly within our ID Solutions segment. Therefore, we must continue to develop new and innovative products, as well as acquire and retain the necessary intellectual property rights in these products. We continue to invest in the development and marketing of new products. These expenditures do not always result in products that will be accepted by our customers. Failure to develop successful new products may also cause customers to buy from a competitor or may cause us to lower our prices in order to compete. If we fail to make innovations, if we launch products with quality problems, or if customers do not accept our new products, then our sales, results of operations, cash flows, and liquidity could be adversely affected.

Inability to identify, complete, and integrate acquisitions and grow acquired companies, may adversely impact our sales, results of operations, cash flow and liquidity.

Our historical growth has included acquisitions, and our future growth strategy may include acquisition opportunities. For example, in fiscal 2013 the Company acquired PDC, a manufacturer of identification products primarily for the healthcare sector, for $301.2 million. We have not met the sales growth synergies identified at the time of the PDC acquisition, which, in addition to other factors, resulted in the Company recording impairment charges of $148.6 million during fiscal 2014, primarily related to the goodwill and other intangible assets in the PeopleID reporting unit, which consists primarily of the PDC business. Failure to achieve these synergies for PDC or other acquired companies may adversely impact our sales, results of operations, cash flow and liquidity. We may not focus on acquisitions as part of our growth strategy, or if we do, we may not be able to identify acquisition targets or successfully complete acquisitions in the future due to the absence of quality companies in our target markets, economic conditions, or price expectations from sellers. If we do not complete additional acquisitions, our growth may be limited.

Acquisitions place significant demands on management, operational, and financial resources. Recent and future acquisitions will require integration of operations, sales and marketing, information technology, finance, and administrative operations, which could decrease the time available to focus on our other growth strategies. We cannot assure that we will be able to successfully integrate acquisitions, that these acquisitions will operate profitably, or that we will be able to achieve the desired sales growth or operational success. Our sales, results of operations, cash flow, and liquidity could be adversely affected if we do not successfully integrate the newly acquired businesses, or if our other businesses suffer due to the increased focus on the acquired businesses.

Demand for our products may be adversely affected by numerous factors, some of which we cannot predict or control. This could adversely affect our sales, results of operations, cash flow and liquidity.

Numerous factors may affect the demand for our products, including:

• Future financial performance of major markets served

• Consolidation in the marketplace, allowing competitors and customers to be more efficient and more price competitive

• Future competitors entering the marketplace

• | Decreasing product life cycles |

• | Changes in customer preferences |

If any of these factors occur, the demand for our products could suffer, and this could adversely impact our sales, results of operations, cash flows and liquidity.

A large customer loss could significantly affect sales, results of operations, cash flow, and liquidity.

While we have a broad customer base and no individual customer represents 5% or more of total sales, we conduct business with several large customers and distribution companies. Our dependence on these customers makes relationships with them important. We cannot guarantee that these relationships will be retained in the future. Because these large customers account for a significant portion of sales, they may possess a greater capacity to negotiate reduced prices. If we are unable to provide products to our customers at the quality and prices acceptable to them, some of our customers may shift their business to competitors or may substitute another manufacturer's products. If one of the large customers consolidates, is acquired, or loses market share, the result of that event may have an adverse impact on our business. The loss of or reduction of business from one or more of these large customers could have a material adverse impact on our sales, results of operations, cash flows, and liquidity.

We depend on key employees and the loss of these individuals could have an adverse effect on our operations.

Our success depends to a large extent upon the continued services of our key executives, managers and other skilled employees. Over the past two fiscal years, we have experienced the loss of several key executives. We cannot ensure that we will be able to retain our key executives, managers and employees. The departure of our key personnel without adequate replacement could disrupt our business operations. Additionally, we need qualified managers and skilled employees with technical and industry

9

Table of Contents

experience to operate our business successfully. If we are unable to attract and retain qualified individuals or our costs to do so increase significantly, our operations could be materially adversely affected.

Divestitures could negatively impact our business and contingent liabilities from divested businesses could adversely affect our results of operations, cash flow and liquidity.

We continually assess the strategic fit of our existing businesses and may divest businesses that we determine do not align with our strategic plan, or that are not achieving the desired return on investment. For example, over the last three fiscal years, we have divested our Etimark, Brady Medical, and Varitronics businesses, and our Asia Die-Cut and Balkhausen Die-Cut businesses. Divestitures pose risks and challenges that could negatively impact our business. For example, when we decide to sell a business or assets, we may be unable to do so on satisfactory terms and within our anticipated time-frame, and even after reaching a definitive agreement to sell a business, the sale is typically subject to satisfaction of pre-closing conditions which may not be satisfied. In addition, the impact of the divestiture on our revenue and net earnings may be larger than projected, which could distract management, and disputes may arise with buyers. Also, we have retained responsibility for and have agreed to indemnify buyers against some contingent liabilities related to a number of businesses that we have recently sold. The resolution of these contingencies has not had a material adverse impact on our results of operations, cash flow and liquidity, but we cannot be certain that this favorable pattern will continue.

We are a global company headquartered in the United States. We are subject to extensive regulations by U.S. and non-U.S. governmental and self-regulatory entities at various levels of the governing bodies. Failure to comply with laws and regulations could adversely affect our sales, results of operations, cash flow and liquidity.

Our operations are subject to the risks of doing business domestically and globally, including the following:

• | Delays or disruptions in product deliveries and payments in connection with international manufacturing and sales |

• | Political and economic instability and disruptions |

• | Imposition of duties and tariffs |

• | Import, export and economic sanction laws |

• | Current and changing governmental policies, regulatory, and business environments |

• | Disadvantages from competing against companies from countries that are not subject to U.S. laws and regulations, including the Foreign Corrupt Practices Act |

• | Local labor market conditions |

• | Regulations relating to climate change, air emissions, wastewater discharges, handling and disposal of hazardous materials and wastes |

• | Regulations relating to health, safety and the protection of the environment |

• | Specific country regulations where our products are manufactured or sold |

• | Laws and regulations that apply to companies doing business with the government, including audit requirements of government contracts related to procurement integrity, export control, employment practices, and the accuracy of records and recording of costs |

Further , these laws and regulations are constantly evolving and it is impossible to accurately predict the effect they may have upon our sales, results of operations, cash flows and liquidity.

We cannot provide assurance that our internal controls and compliance systems will always protect us from acts committed by employees, agents or business partners that would violate U.S. and/or non-U.S. laws, including the laws governing payments to government officials, bribery, fraud, anti-kickback and false claims rules, competition, export and import compliance, money laundering and data privacy. Any such improper actions could subject us to civil or criminal investigations in the U.S. and in other jurisdictions, could lead to substantial civil or criminal, monetary and non-monetary penalties and related shareholder lawsuits, could damage our reputation, and could adversely impact our results of operations, cash flow and liquidity.

Product liability claims could adversely impact our financial condition, results of operations, cash flows, and reputation.

Our business exposes us to potential product liability risk, as well as warranty and recall claims that are inherent in the design, manufacture, sale and use of our products. We sell products in industries such as aerospace, defense, healthcare, chemical, and energy where the impact of product liability risk is high. To date, we have not incurred material costs related to these types of claims. However, in the event our products actually or allegedly fail to perform as expected and we are subject to such claims above the amount of insurance coverage, outside the scope of our coverage, or for which we do not have coverage, our financial condition, results of operations and cash flows, as well as our reputation, could be materially and adversely affected.

10

Table of Contents

Financial/Ownership Risks

Failure to execute our strategies could result in impairment of goodwill or other intangible assets, which may negatively impact earnings and profitability .

We have goodwill of $ 515.0 million and other intangible assets of $91.0 million as of July 31, 2014, which represents 48.3% of our total assets. During fiscal 2014, we recorded impairment charges of $148.6 million , primarily related to the goodwill and other intangible assets in the PeopleID reporting unit. During fiscal 2013, we recorded impairment charges of $204.4 million primarily related to goodwill in the WPS Americas and IDS APAC reporting units. We evaluate goodwill for impairment on an annual basis, or more frequently if impairment indicators are present, based upon the fair value of each reporting unit. We assess the impairment of other intangible assets on an annual basis, or more frequently if impairment indicators are present, based upon the expected future cash flows of the respective assets. These valuations include management's estimates of sales, profitability, cash flow generation, capital structure, cost of debt, interest rates, capital expenditures, and other assumptions. Significant negative industry or economic trends, disruptions to our business, inability to achieve sales projections or cost savings, inability to effectively integrate acquired businesses, unexpected significant changes or planned changes in use of the assets or in entity structure, and divestitures may adversely impact the assumptions used in the valuations. If the estimated fair value of our reporting units changes in future periods, we may be required to record an impairment charge related to goodwill or other intangible assets, which would reduce earnings and profit in such period.

Changes in tax legislation or tax rates could adversely affect results of operations and financial statements. Additionally, audits by taxing authorities could result in tax payments for prior periods.

We are subject to income taxes in the U.S. and in many non-U.S. jurisdictions. As such, our earnings are subject to risk due to changing tax laws and tax rates around the world. At any point in time, there are a number of tax proposals at various stages of legislation throughout the globe. While it is impossible for us to predict whether some or all of these proposals will be enacted, it likely would have an impact on our earnings.

Our tax filings are subject to audit by U.S. federal, state and local tax authorities and by non-U.S. tax authorities. If these audits result in payments or assessments that differ from our reserves, our future net earnings may be adversely impacted.

We review the probability of the realization of our deferred tax assets on a quarterly basis based on forecasts of taxable income in both the U.S. and foreign jurisdictions. As part of this review, we utilize historical results, projected future operating results, eligible carry-forward periods, tax planning opportunities, and other relevant considerations. Adverse changes in profitability and financial outlook in both the U.S. and/or foreign jurisdictions, or changes in our geographic footprint may require changes in the valuation allowances in order to reduce our deferred tax assets. Such changes could result in a material impact on earnings.

Our annual cash needs could require us to repatriate cash to the U.S. from foreign jurisdictions, which may result in tax charges. For example, in fiscal 2014, we repatriated cash to the U.S. in connection with the sale of the Die Cut businesses, which resulted in a tax charge of $4.0 million in continuing operations. In fiscal 2013, we repatriated cash to the U.S. in connection with the acquisition of PDC, which resulted in a tax charge of $26.6 million.

Substantially all of our voting stock is controlled by members of the Brady family, while our public investors hold non-voting stock. The interests of the voting and non-voting shareholders could differ, potentially resulting in decisions that unfavorably affect the value of the non-voting shares.

Substantially all of our voting stock is controlled by Elizabeth P. Pungello, one of the Directors, and William H. Brady III, both of whom are descendants of the Company's founder. All of our publicly traded shares are non-voting. Therefore, Ms. Pungello and Mr. Brady have control in most matters requiring approval or acquiescence by shareholders, including the composition of our Board of Directors and many corporate actions. Such concentration of ownership may discourage a potential acquirer from making a purchase offer that our public shareholders may find favorable, which in turn could adversely affect the market price of our common stock or prevent our shareholders from realizing a premium over our stock price. Furthermore, this concentration of voting share ownership may adversely affect the trading price for our non-voting common stock because investors may perceive disadvantages in owning stock in companies whose voting stock is controlled by a limited number of shareholders.

Failure to meet certain financial covenants required by our debt agreements may adversely affect our assets, results of operations, cash flows, and liquidity.

As of July 31, 2014, we had $263.2 million in outstanding indebtedness. In addition, based on the availability under our credit facilities as of July 31, 2014, we had the ability to incur an additional $404.4 million under our revolving credit agreement. Our current revolving credit agreement and long-term debt obligations also impose certain restrictions on us. Refer to Management's

11

Table of Contents

Discussion and Analysis of Financial Condition and Results of Operations ("MD&A") within Item 7 for more information regarding our credit agreement and long-term debt obligations. If we breach any of these restrictions or covenants and do not obtain a waiver from the lenders, then subject to applicable cure periods, the outstanding indebtedness (and any other indebtedness with cross-default provisions) could be declared immediately due and payable, which could adversely affect our assets, results of operations, cash flows and liquidity.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The Company currently operates 50 manufacturing or distribution facilities across the globe and are split by reporting segment as follows:

IDS: Thirty-seven facilities are used for our IDS business. Ten of which are located within the United States; five each are located in Belgium and Mexico; four in China; three each in the United Kingdom and Brazil; and one each in Canada, India, Italy, Hong Kong, Japan, Malaysia, and Singapore.

WPS: Thirteen facilities are used for our WPS business. Three of which are located in France; two each are located in Australia, Germany, and the United States; and one each in the Netherlands, Poland, Sweden, and the United Kingdom.

The Company's present operating facilities contain a total of approximately 2.8 million square feet of space, of which approximately 2.1 million square feet is leased. The Company believes that its equipment and facilities are modern, well maintained, and adequate for present needs.

Item 3. Legal Proceedings

The Company is, and may in the future be, party to litigation arising in the normal course of business. The Company is not currently a party to any material pending legal proceedings in which management believes the ultimate resolution would have a material effect on the Company's consolidated financial statements.

Item 4. Mine Safety Disclosures

Not applicable.

12

Table of Contents

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

(a) | Market Information |

Brady Corporation Class A Nonvoting Common Stock trades on the New York Stock Exchange under the symbol BRC. The following table sets forth the range of high and low daily closing sales prices for the Company's Class A stock as reported on the New York Stock Exchange for each of the quarters in the fiscal years ended July 31:

|

| 2014 |

| 2013 |

| 2012 | ||||||||||||||||||

|

| High |

| Low |

| High |

| Low |

| High |

| Low | ||||||||||||

4th Quarter |

| $ | 30.75 | |

| $ | 24.26 | |

| $ | 35.58 | |

| $ | 29.76 | |

| $ | 31.28 | |

| $ | 25.15 | |

3rd Quarter |

| $ | 27.89 | |

| $ | 25.15 | |

| $ | 36.33 | |

| $ | 31.51 | |

| $ | 34.37 | |

| $ | 29.41 | |

2nd Quarter |

| $ | 31.61 | |

| $ | 27.36 | |

| $ | 35.00 | |

| $ | 30.18 | |

| $ | 34.40 | |

| $ | 27.09 | |

1st Quarter |

| $ | 35.54 | |

| $ | 29.19 | |

| $ | 31.22 | |

| $ | 26.34 | |

| $ | 32.24 | |

| $ | 24.73 | |

There is no trading market for the Company's Class B Voting Common Stock.

(b) | Holders |

As of September 24, 2014 , there were 1,023 Class A Common Stock shareholders of record and approximately 10,467 beneficial shareholders. There are three Class B Common Stock shareholders.

(c) | Issuer Purchases of Equity Securities |

The Company has a share repurchase program of the Company's Class A Nonvoting Common Stock. The plan may be implemented by purchasing shares in the open market or in privately negotiated transactions, with repurchased shares available for use in connection with the Company's stock-based plans and for other corporate purposes. During the three months ended July 31, 2014 , the Company purchased 287,717 shares of its Class A Nonvoting Common Stock under this plan for $7.2 million . As of July 31, 2014 , there remained 966,242 shares to purchase in connection with this share repurchase program.

Period |

| Total Number of Shares Purchased |

| Average Price Paid per Share |

| Total Number of Shares Purchased as Part of Publicly Announced Plans |

| Maximum Number of Shares that May Yet Be Purchased Under the Plan | |||||

May 1, 2014 - May 31, 2014 |

| 287,717 | |

| $ | 25.18 | |

| 287,717 | |

| 966,242 | |

June 1, 2014 - June 30, 2014 |

| - | |

| - | |

| - | |

| 966,242 | ||

July 1, 2014 - July 31, 2014 |

| - | |

| - | |

| - | |

| 966,242 | ||

Total |

| 287,717 | |

| $ | 25.18 | |

| 287,717 | |

| 966,242 | |

(d) | Dividends |

The Company has historically paid quarterly dividends on outstanding common stock. Before any dividend may be paid on the Class B Common Stock, holders of the Class A Common Stock are entitled to receive an annual, noncumulative cash dividend of $0.01665 per share (subject to adjustment in the event of future stock splits, stock dividends or similar events involving shares of Class A Common Stock). Thereafter, any further dividend in that fiscal year must be paid on all shares of Class A Common Stock and Class B Common Stock on an equal basis. The Company believes that based on its historic dividend practice, this requirement will not impede it in following a similar dividend practice in the future.

During the two most recent fiscal years and for the first quarter of fiscal 2015 , the Company declared the following dividends per share on its Class A and Class B Common Stock for the years ended July 31:

|

| 2015 |

| 2014 |

| 2013 | ||||||||||||||||||||||||||||||

|

| 1st Qtr |

| 1st Qtr |

| 2nd Qtr |

| 3rd Qtr |

| 4th Qtr |

| 1st Qtr |

| 2nd Qtr |

| 3rd Qtr |

| 4th Qtr | ||||||||||||||||||

Class A |

| $ | 0.20 | |

| $ | 0.195 | |

| $ | 0.195 | |

| $ | 0.195 | |

| $ | 0.195 | |

| $ | 0.19 | |

| $ | 0.19 | |

| $ | 0.19 | |

| $ | 0.19 | |

Class B |

| 0.18335 | |

| 0.17835 | |

| 0.195 | |

| 0.195 | |

| 0.195 | |

| 0.17335 | |

| 0.19 | |

| 0.19 | |

| 0.19 | | |||||||||

13

Table of Contents

(e) | Common Stock Price Performance Graph |

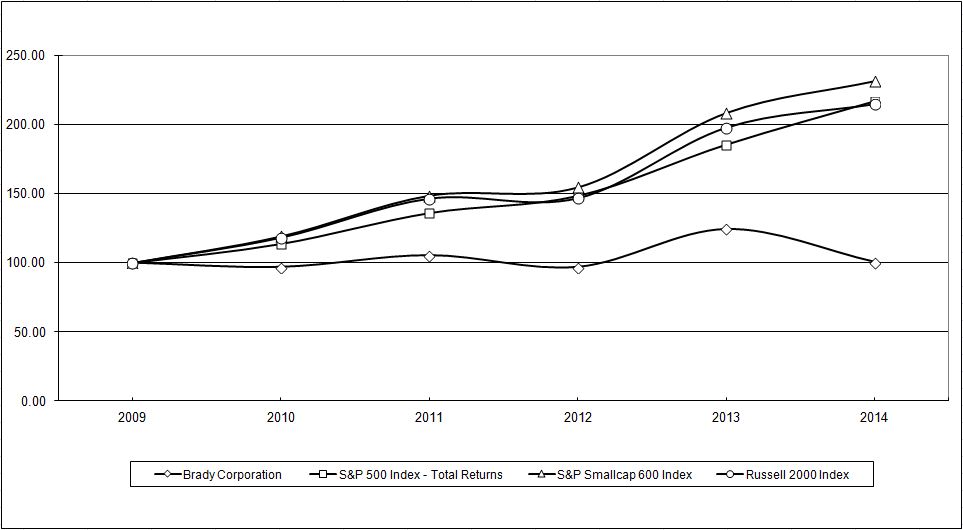

The graph below shows a comparison of the cumulative return over the last five fiscal years had $100 been invested at the close of business on July 31, 2009 , in each of Brady Corporation Class A Common Stock, the Standard & Poor's (S&P) 500 Index, the Standard and Poor's SmallCap 600 Index, and the Russell 2000 Index.

Comparison of 5 Year Cumulative Total Return*

Among Brady Corporation, the S&P 500 Index,

the S&P SmallCap 600 Index, and the Russell 2000 Index

* | $100 invested on July 31, 2009 in stock or index-including reinvestment of dividends. Fiscal years ended July 31: |

|

| 2009 |

| 2010 |

| 2011 |

| 2012 |

| 2013 |

| 2014 | ||||||||||||

Brady Corporation |

| $ | 100.00 | |

| $ | 96.90 | |

| $ | 105.43 | |

| $ | 96.91 | |

| $ | 124.47 | |

| $ | 100.49 | |

S&P 500 Index |

| 100.00 | |

| 113.84 | |

| 136.21 | |

| 148.64 | |

| 185.80 | |

| 217.28 | | ||||||

S&P SmallCap 600 Index |

| 100.00 | |

| 119.17 | |

| 148.63 | |

| 154.56 | |

| 208.31 | |

| 231.31 | | ||||||

Russell 2000 Index |

| 100.00 | |

| 118.33 | |

| 146.65 | |

| 146.94 | |

| 198.06 | |

| 215.02 | | ||||||

Copyright (C) 2014, Standard & Poor's, a division of The McGraw-Hill Companies, Inc. All rights reserved.

14

Table of Contents

Item 6. Selected Financial Data

CONSOLIDATED STATEMENTS OF INCOME AND SELECTED FINANCIAL DATA

Years Ended July 31, 2010 through 2014

|

| 2014 |

| 2013 |

| 2012 |

| 2011 |

| 2010 | ||||||||||

Operating Data (1) |

|

|

|

|

|

|

|

|

|

| ||||||||||

Net Sales |

| $ | 1,225,034 | |

| $ | 1,157,792 | |

| $ | 1,071,504 | |

| $ | 1,059,355 | |

| $ | 966,070 | |

Gross Margin |

| 609,564 | |

| 609,348 | |

| 590,969 | |

| 587,950 | |

| 546,413 | | |||||

Operating Expenses: |

|

|

|

|

|

|

|

|

|

| ||||||||||

Research and development |

| 35,048 | |

| 33,552 | |

| 34,528 | |

| 38,268 | |

| 38,279 | | |||||

Selling, general and administrative |

| 452,164 | |

| 427,858 | |

| 392,694 | |

| 397,472 | |

| 381,071 | | |||||

Restructuring charges (2) |

| 15,012 | |

| 26,046 | |

| 6,084 | |

| 6,451 | |

| 12,640 | | |||||

Impairment charges (3) |

| 148,551 | |

| 204,448 | |

| - | |

| - | |

| - | | |||||

Total operating expenses |

| 650,775 | |

| 691,904 | |

| 433,306 | |

| 442,191 | |

| 431,990 | | |||||

Operating (Loss) Income |

| (41,211 | ) |

| (82,556 | ) |

| 157,663 | |

| 145,759 | |

| 114,423 | | |||||

Other Income (Expense): |

|

|

|

|

|

|

|

|

|

| ||||||||||

Investment and other income-net |

| 2,402 | |

| 3,523 | |

| 2,082 | |

| 3,989 | |

| 1,169 | | |||||

Interest expense |

| (14,300 | ) |

| (16,641 | ) |

| (19,090 | ) |

| (22,124 | ) |

| (21,222 | ) | |||||

Net other expense |

| (11,898 | ) |

| (13,118 | ) |

| (17,008 | ) |

| (18,135 | ) |

| (20,053 | ) | |||||

(Loss) earnings from continuing operations before income taxes |

| (53,109 | ) |

| (95,674 | ) |

| 140,655 | |

| 127,624 | |

| 94,370 | | |||||

Income Taxes (4) |

| (4,963 | ) |

| 42,583 | |

| 37,162 | |

| 21,667 | |

| 18,605 | | |||||

(Loss) earnings from continuing operations |

| $ | (48,146 | ) |

| $ | (138,257 | ) |

| $ | 103,493 | |

| $ | 105,957 | |

| $ | 75,765 | |

Earnings (loss) from discontinued operations, net of income taxes (5) |

| 2,178 | |

| (16,278 | ) |

| (121,404 | ) |

| 2,695 | |

| 6,191 | | |||||

Net (loss) earnings |

| $ | (45,968 | ) |

| $ | (154,535 | ) |

| $ | (17,911 | ) |

| $ | 108,652 | |

| $ | 81,956 | |

(Loss) earnings from continuing operations per Common Share- (Diluted): |

|

|

|

|

|

|

|

|

|

| ||||||||||

Class A nonvoting |

| $ | (0.93 | ) |

| $ | (2.70 | ) |

| $ | 1.95 | |

| $ | 1.99 | |

| $ | 1.43 | |

Class B voting |

| $ | (0.95 | ) |

| $ | (2.71 | ) |

| $ | 1.94 | |

| $ | 1.97 | |

| $ | 1.41 | |

Earnings (loss) from discontinued operations per Common Share - (Diluted): |

|

|

|

|

|

|

|

|

|

| ||||||||||

Class A nonvoting |

| $ | 0.04 | |

| $ | (0.32 | ) |

| $ | (2.29 | ) |

| $ | 0.05 | |

| $ | 0.12 | |

Class B voting |

| $ | 0.05 | |

| $ | (0.32 | ) |

| $ | (2.30 | ) |

| $ | 0.05 | |

| $ | 0.12 | |

Cash Dividends on: |

|

|

|

|

|

|

|

|

|

| ||||||||||

Class A common stock |

| $ | 0.78 | |

| $ | 0.76 | |

| $ | 0.74 | |

| $ | 0.72 | |

| $ | 0.70 | |

Class B common stock |

| $ | 0.76 | |

| $ | 0.74 | |

| $ | 0.72 | |

| $ | 0.70 | |

| $ | 0.68 | |

Balance Sheet at July 31: |

|

|

|

|

|

|

|

|

|

| ||||||||||

Total assets |

| 1,253,665 | |

| 1,438,683 | |

| 1,607,719 | |

| 1,861,505 | |

| 1,746,231 | | |||||

Long-term obligations, less current maturities |

| 159,296 | |

| 201,150 | |

| 254,944 | |

| 331,914 | |

| 382,940 | | |||||

Stockholders' investment |

| 733,076 | |

| 830,797 | |

| 1,009,353 | |

| 1,156,192 | |

| 1,005,027 | | |||||

Cash Flow Data: |

|

|

|

|

|

|

|

|

|

| ||||||||||

Net cash provided by operating activities |

| $ | 93,420 | |

| $ | 143,503 | |

| $ | 144,705 | |

| $ | 167,350 | |

| $ | 165,238 | |

Net cash provided by (used in) investing activities |

| 10,207 | |

| (325,766 | ) |

| (64,604 | ) |

| (22,631 | ) |

| (48,681 | ) | |||||

Net cash (used in) provided by financing activities |

| (115,387 | ) |

| (33,060 | ) |

| (147,824 | ) |

| (91,574 | ) |

| 15,275 | | |||||

Depreciation and amortization |

| 44,598 | |

| 48,725 | |

| 43,987 | |

| 48,827 | |

| 53,022 | | |||||

Capital expenditures |

| (43,398 | ) |

| (35,687 | ) |

| (24,147 | ) |

| (20,532 | ) |

| (26,296 | ) | |||||

(1) | Operating data has been impacted by the reclassification of the Die-Cut businesses into discontinued operations. The Company has elected to not separately disclose the cash flows related to discontinued operations. Refer to Note 15 within Item 8 for further information on discontinued operations. The operating data is also impacted by the acquisitive nature |

15

Table of Contents

of the Company as one, three, one, and three acquisitions were completed in fiscal years ended July 31, 2013, 2012, 2011, and 2010, respectively. There were no acquisitions during fiscal 2014. Refer to Note 2 within Item 8 for further information on the acquisitions that were completed.

(2) | In fiscal 2009, in response to the global economic downturn, the Company initiated several measures to address its cost structure, including a reduction in its workforce and decreased discretionary spending. The Company continued certain of these measures during fiscal 2010, 2011, and 2012. During fiscal 2013, the Company executed a business simplification project which included various measures to address its cost structure and resulted in restructuring charges during fiscal 2013 and into fiscal 2014. In addition, in fiscal 2014, the Company approved a plan to consolidate facilities in North America, Europe, and Asia in order to enhance customer service, improve efficiency of operations, and reduce operating expenses. This plan resulted in restructuring charges during fiscal 2014. |

(3) | The Company recognized an impairment charge of $148.6 million during the three months ended July 31, 2014, primarily related to the PeopleID reporting unit. The Company recognized an impairment charge of $204.4 million during the three months ended July 31, 2013, primarily related to the WPS segment. Refer to Note 3 within Item 8 for further information regarding the impairment charges. |

(4) | Fiscal 2014 was significantly impacted by the goodwill impairment charge of $100.4 million recorded on the PeopleID reporting unit and a tax charge of $4.0 million in continuing operations associated with the repatriation of the cash proceeds from the sale of the Die-Cut business. Fiscal 2013 was impacted by the goodwill impairment charge of $190.5 million recorded on the WPS Americas and IDS APAC reporting units, as well as a tax charge of $26.6 million associated with the funding of the PDC acquisition. |

(5) | The earnings from discontinued operations in fiscal 2014 include a $1.2 million net loss on the sale of the Die-Cut business. The loss from discontinued operations in fiscal 2013 was primarily attributable to a $15.7 million write-down of the Die-Cut business to its estimated fair value less costs to sell. The loss from discontinued operations in fiscal 2012 was primarily attributable to the $115.7 million goodwill impairment charge recorded during the three months ending January 31, 2012, which was related to the Die-Cut disposal group. Refer to Note 15 within Item 8 for further information regarding discontinued operations. |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

Overview

In fiscal 2014 , the Company posted sales of $1,225.0 million and a net loss from continuing operations of $48.1 million . Sales increased by 5.8% from fiscal 2013 . Organic sales increased by 0.2% , currency fluctuations decreased sales by 0.1% and the acquisition of PDC increased sales by 5.7% . Fiscal 2014 sales growth was driven by the ID Solutions segment which grew by 11.6% from 2013 to 2014 primarily due to the acquisition, which was partially offset by the decline in sales in the Workplace Safety segment of 4.5% .

The fiscal 2014 net loss from continuing operations of $48.1 million was primarily due to non-cash impairment charges of $148.6 million and restructuring charges of $15.0 million .

The fiscal 2014 operating loss from continuing operations was $41.2 million . Excluding the impairment charges of $148.6 million and restructuring charges of $15.0 million , the Company generated operating income from continuing operations of $122.4 million in fiscal 2014 . Fiscal 2013 operating loss from continuing operations was $82.6 million . Excluding the impairment charges of $204.4 million and restructuring charges of $26.0 million , the Company generated operating income from continuing operations of $147.9 million in fiscal 2013 . This decline of $25.5 million was primarily due to the decrease in segment profit in the WPS business segment. The decline in operating results within the WPS business segment was primarily due to a 4.6% organic sales decline, incremental investment to drive key initiatives and growth, and increased costs from facility consolidation projects.

16

Table of Contents

Results of Operations

A comparison of results of Operating (loss) income from continuing operations for the fiscal years ended July 31, 2014 , 2013 , and 2012 is as follows:

(Dollars in thousands) |

| 2014 |

| % Sales |

| % Change |

| 2013 |

| % Sales |

| % Change |

| 2012 |

| % Sales | |||||||||||

Net Sales |

| $ | 1,225,034 | |

| | |

| 5.8 | % |

| $ | 1,157,792 | |

| | |

| 8.1 | % |

| $ | 1,071,504 | |

| | |

Gross Margin |

| 609,564 | |

| 49.8 | % |

| - | % |

| 609,348 | |

| 52.6 | % |

| 3.1 | % |

| 590,969 | |

| 55.2 | % | |||

Operating Expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||

Research and Development |

| 35,048 | |

| 2.9 | % |

| 4.5 | % |

| 33,552 | |

| 2.9 | % |

| (2.8 | )% |

| 34,528 | |

| 3.2 | % | |||

Selling, General & Administrative |

| 452,164 | |

| 36.9 | % |

| 5.7 | % |

| 427,858 | |

| 37.0 | % |

| 9.0 | % |

| 392,694 | |

| 36.6 | % | |||

Restructuring charges |

| 15,012 | |

| 1.2 | % |

| (42.4 | )% |

| 26,046 | |

| 2.2 | % |

| 328.1 | % |

| 6,084 | |

| 0.6 | % | |||

Impairment charges |

| 148,551 | |

| 12.1 | % |

| (27.3 | )% |

| 204,448 | |

| 17.7 | % |

| - | % |

| - | |

| - | % | |||

Total operating expenses |

| 650,775 | |

| 53.1 | % |

| (5.9 | )% |

| 691,904 | |

| 59.8 | % |

| 59.7 | % |

| 433,306 | |

| 40.4 | % | |||

Operating (loss) income |

| $ | (41,211 | ) |

| (3.4 | )% |

| 50.1 | % |

| $ | (82,556 | ) |

| (7.1 | )% |

| (152.4 | )% |

| $ | 157,663 | |

| 14.7 | % |

During fiscal 2014 , net sales increased 5.8% from fiscal 2013 , which consisted of organic growth of 0.2% , currency impact of a negative 0.1% , and growth from acquisitions of 5.7% . The acquisition growth was from the acquisition of PDC within the IDS segment in fiscal 2013. Organic sales within the IDS segment were up 2.9% , while organic sales within the WPS segment declined by 4.6% .

During fiscal 2013 , net sales increased 8.1% from fiscal 2012 , which consisted of an organic decline of 2.4% , currency impact of a negative 0.8% and growth from acquisitions of 11.3% . Over 90% of the acquisition growth was from the acquisition of PDC in fiscal 2013, with the remainder attributable to the acquisitions of Grafo in the IDS segment and Runelandhs and Pervaco in the WPS segment in fiscal 2012. Organic sales within the IDS segment were up 0.8% , while organic sales within the WPS platform declined by 7.0% .

Gross margin as a percentage of sales declined to 49.8% in fiscal 2014 from 52.6% in fiscal 2013 . The decline was primarily due to the sales decline and increased pricing actions in the WPS business, and an increase in facility consolidation costs in both segments. In the WPS segment, gross margin declined due to increased costs for facility consolidation projects, growth initiatives, and reduced sales as compared to the same period in the prior year. In the IDS segment, gross margin was negatively impacted by facility consolidation related expenses and product mix.

Gross margin as a percentage of sales declined to 52.6% in fiscal 2013 from 55.2% in fiscal 2012 . Approximately half of the decline was due to the acquisition of PDC, as it is a lower gross margin business compared to the remainder of the Company. The other half of the decline was attributed to the WPS segment in which the decline in sales, increased pricing actions, and the challenging global economy contributed to the reduced gross margin.

Research and development expenses increased to $35.0 million in fiscal 2014 from $33.6 million in fiscal 2013 . The increase was primarily due to increased investment in new products. In addition, in fiscal 2014, the Company realigned the R&D processes in order to accelerate new product innovation and invested in emerging technologies such as RFID and sensing technology for harsh environments and mobile applications that allow users to work with a variety of electronic devices. R&D expenses decreased to $33.6 million in fiscal 2013 from $34.5 million in 2012 due to the global consolidation of the project management office, which reduced costs while streamlining reporting processes globally.

Selling, general and administrative ("SG&A") expenses include selling costs directly attributed to the IDS and WPS segments, as well as administrative expenses including finance, information technology, human resources and legal. SG&A expenses increased to $452.2 million in fiscal 2014 compared to $427.9 million in fiscal 2013 . The increase was primarily due to incremental SG&A associated with the PDC business of approximately $22 million. In addition, the Company expanded its sales force in multiple geographies within the IDS segment in fiscal 2014 and increased spending in both on-line advertising as well as traditional print advertising within the WPS segment.

SG&A expense increased to $427.9 million in fiscal 2013 compared to $392.7 million in fiscal 2012 . The increase was primarily due to the addition of PDC, which also contributed to an incremental $6.0 million of amortization of intangible assets. The total increase in SG&A was partially offset by a reduction in variable incentive compensation from fiscal 2012 to fiscal 2013.

17

Table of Contents

In fiscal 2014, the Company announced a restructuring plan to consolidate facilities in North America, Europe and Asia. The Company implemented this restructuring plan to enhance customer service, improve efficiency of operations and reduce operating expenses, with expected annual pre-tax operational savings of approximately $10 million. The cash expenditures for these restructuring activities were funded with cash generated from operations. Facility consolidation activities will extend into fiscal 2015 as the Company slowed certain consolidation activities to ensure the highest levels of quality and delivery throughout the transition, and will result in approximately $15 million of additional restructuring charges. In fiscal 2013, the Company announced a restructuring action to reduce its global workforce by approximately 5-7% in order to address its cost structure.

In connection with these restructuring actions, the Company incurred restructuring charges of $15.0 million in fiscal 2014 . These charges consisted of $9.3 million of employee separation costs, $4.4 million of facility closure related costs, $1.0 million of contract termination costs, and $0.3 million of non-cash asset write-offs. The charges for employee separation costs consisted of severance pay, outplacement services, medical and other benefits. Non-cash asset write-offs consist mainly of indefinite-lived tradenames written off in conjunction with brand consolidations. Of the $15.0 million recognized in fiscal 2014, $9.0 million was incurred within the IDS segment and $6.0 million was incurred within the WPS segment.