UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

For the fiscal year ended March 1, 2014

Commission File Number 0-20214

BED BATH & BEYOND INC.

(Exact name of registrant as specified in its charter)

New York | 11-2250488 |

(State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

650 Liberty Avenue, Union, New Jersey 07083

(Address of principal executive offices) (Zip Code)

Registrant's telephone number, including area code: 908/688-0888

Title of each class | Name of each exchange on which registered |

Common stock, $.01 par value | The NASDAQ Stock Market LLC |

(NASDAQ Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [x] No [ ]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [x] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [x]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [x] | Accelerated filer [ ] |

| Non-accelerated filer [ ] | Smaller reporting company [ ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [x]

As of August 31, 2013, the aggregate market value of the common stock held by non-affiliates (which was computed by reference to the closing price on such date of such stock on the NASDAQ National Market) was $15,188,999,047 .*

The number of shares outstanding of the registrant's common stock (par value $0.01 per share) at March 29, 2014: 204,016,305.

Documents Incorporated by Reference

Portions of the Registrant's definitive proxy statement for the 2014 Annual Meeting of Shareholders to be filed pursuant to Regulation 14A are incorporated by reference in Part III hereof.

* | For purposes of this calculation, all outstanding shares of common stock have been considered held by non-affiliates other than the 8,765,040 shares beneficially owned by directors and executive officers, including in the case of the Co-Chairmen trusts and foundations affiliated with them. In making such calculation, the Registrant does not determine the affiliate or non-affiliate status of any shares for any other purpose. |

2

TABLE OF CONTENTS

Form 10-K | ||

Item No. | Name of Item | |

PART I | ||

Item 1. | Business | |

Item 1A. | Risk Factors | |

Item 1B. | Unresolved Staff Comments | |

Item 2. | Properties | |

Item 3. | Legal Proceedings | |

Item 4. | Mine Safety Disclosures | |

PART II | ||

Item 5. | Market for Registrant's Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities | |

Item 6. | Selected Financial Data | |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

Item 8. | Financial Statements and Supplementary Data | |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | |

Item 9A. | Controls and Procedures | |

Item 9B. | Other Information | |

PART III | ||

Item 10. | Directors, Executive Officers and Corporate Governance | |

Item 11. | Executive Compensation | |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters | |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

Item 14. | Principal Accounting Fees and Services | |

PART IV | ||

Item 15. | Exhibits, Financial Statement Schedules | |

3

PART I

Unless otherwise indicated, the term "Company" refers collectively to Bed Bath & Beyond Inc. and subsidiaries as of March 1, 2014. The Company's fiscal year is comprised of the 52 or 53 week period ending on the Saturday nearest February 28. Accordingly, fiscal 2013 and fiscal 2011 represented 52 weeks and ended on March 1, 2014 and February 25, 2012, respectively. Fiscal 2012 represented 53 weeks and ended on March 2, 2013. Unless otherwise indicated, all references herein to periods of time (e.g., quarters and years) are to fiscal periods.

ITEM 1 – | BUSINESS |

Introduction

Bed Bath & Beyond Inc. and subsidiaries (the "Company") is a retailer which operates under the names Bed Bath & Beyond ("BBB"), Christmas Tree Shops, Christmas Tree Shops andThat! or andThat! (collectively, "CTS"), Harmon or Harmon Face Values (collectively, "Harmon"), buybuy BABY ("Baby") and World Market, Cost Plus World Market or Cost Plus (collectively, "Cost Plus World Market"). Customers can purchase products from the Company either in store, online or through a mobile device. The Company has the developing ability to fulfill customer purchases by in store customer pick up or by direct shipment to the customer from the Company's distribution facilities, stores or vendors. The Company also operates Linen Holdings, a provider of a variety of textile products, amenities and other goods to institutional customers in the hospitality, cruise line, food service, healthcare and other industries. Additionally, the Company is a partner in a joint venture which operates four retail stores in Mexico under the name Bed Bath & Beyond.

The Company sells a wide assortment of domestics merchandise and home furnishings. Domestics merchandise includes categories such as bed linens and related items, bath items and kitchen textiles. Home furnishings include categories such as kitchen and tabletop items, fine tabletop, basic housewares, general home furnishings, consumables and certain juvenile products.

History

The Company was founded in 1971 by Leonard Feinstein and Warren Eisenberg, the Co-Chairmen of the Company. Each has more than 50 years of experience in the retail industry.

The Company commenced operations in 1971 with the opening of two stores, which primarily sold bed linens and bath accessories. In 1985, the Company introduced its first store carrying a full line of domestics merchandise and home furnishings. The Company began using the name "Bed Bath & Beyond" in 1987 in order to reflect the expanded product line offered by its stores and to distinguish its stores from conventional specialty retail stores offering only domestics merchandise or home furnishings. In 2002, the Company acquired Harmon, a health and beauty care retailer, which operated 27 stores at the time located in three states. In 2003, the Company acquired CTS, a retailer of giftware and household items, which operated 23 stores at the time located in six states. In 2007, the Company acquired Baby, a retailer of infant and toddler merchandise, which operated eight stores at the time located in four states. In 2007, the Company opened its first international BBB store in Ontario, Canada. In 2008, the Company became a partner in a joint venture which operated two stores at the time in the Mexico City market under the name "Home & More," which were rebranded as Bed Bath & Beyond in fiscal 2012. In June 2012, the Company acquired Linen Holdings, LLC ("Linen Holdings"), a provider of a variety of textile products, amenities and other goods to institutional customers in the hospitality, cruise line, food service, healthcare and other industries, and Cost Plus, Inc. ("Cost Plus World Market"), a retailer selling a wide range of home decorating items, furniture, gifts, holiday and other seasonal items, and specialty food and beverages, which operated 258 stores at the time located in 30 states under the names of World Market, Cost Plus World Market or Cost Plus.

4

The Company accounts for its operations as two operating segments: North American Retail and Institutional Sales. The Institutional Sales operating segment, which is comprised of Linen Holdings, does not meet the quantitative thresholds under U.S. generally accepted accounting principles and therefore is not a reportable segment.

Total net sales of the Company were $11.504 billion, $10.915 billion and $9.500 billion for fiscal 2013, 2012 and 2011, respectively. Net sales outside of the U.S. were not material for fiscal 2013, 2012 and 2011. Refer to Part II, Item 7 and Item 8 of this Form 10-K for additional financial information.

Operations

It is the Company's goal to offer quality merchandise at competitive prices; to maintain a wide and differentiated assortment of merchandise; to present merchandise in a distinctive manner designed to maximize customer convenience and reinforce customer perception of a wide selection; and to emphasize dedication to customer service and satisfaction. The Company continues to grow, differentiate and leverage its assortment across all channels, concepts and countries in which it operates. In addition, the Company strives to more efficiently and effectively understand its customers' needs and communicate with them through its growing analytic capabilities and omnichannel marketing approaches.

Pricing. The Company believes in maintaining competitive prices. The Company regularly monitors price levels at its competitors in order to ensure that its prices are in accordance with its pricing philosophy. The Company believes that the application of its pricing philosophy is an important factor in establishing its reputation among customers.

Merchandise Assortment. The Company sells a wide assortment of domestics merchandise and home furnishings. Domestics merchandise includes categories such as bed linens and related items, bath items and kitchen textiles. Home furnishings include categories such as kitchen and tabletop items, fine tabletop, basic housewares, general home furnishings, consumables and certain juvenile products. The Company strives to tailor its merchandise mix as appropriate to respond to changing trends and conditions. The Company, on an ongoing basis, tests new merchandise categories and adjusts the categories of merchandise carried as part of its assortment and may add new product categories as appropriate. Additionally, the Company continues to integrate the merchandise assortments among its concepts. The Company believes that the process of adding new product categories, integrating the Company's merchandise within concepts, and expanding or reducing the size of various product categories in response to changing conditions is an important part of its merchandising strategy.

Merchandise Presentation. The Company has developed a style of merchandise presentation where groups of related product lines are presented together. The Company believes that this approach to merchandise presentation makes it easy for customers to locate products and reinforces customer perception of a wide selection.

Advertising. In general, the Company relies on "word of mouth advertising," its reputation for offering a wide assortment of quality merchandise at competitive prices and the use of paid advertising. Primary vehicles of paid advertising used by the Company include full-color circulars and other advertising pieces distributed via direct mail or inserts, as well as digital media including email, mobile, social and search advertising. Also, to support the opening of new stores, the Company primarily uses "grand opening" newspaper and direct mail advertising and email.

Customer Service. Customer service is at the heart of the Company's culture as it encourages and trains its associates and implements technology to create a better shopping experience for each and every customer. Through its customer centric policies and emphasis on life stage events, the Company stresses the importance of each customer relationship. The Company continues to focus its efforts and investments on ensuring that it builds and maintains each of these customer relationships.

5

Suppliers

In fiscal 2013, the Company purchased its merchandise from approximately 8,300 suppliers with the Company's largest supplier accounting for approximately 5% of the Company's merchandise purchases and the Company's 10 largest suppliers accounting for approximately 17% of such purchases. The Company purchases substantially all of its merchandise in the United States, the majority from domestic sources and the balance from importers. The Company purchases a small amount of its merchandise directly from overseas sources. The Company has no long term contracts for the purchase of merchandise. The Company believes that most merchandise, other than brand name goods, is available from a variety of sources and that most brand name goods can be replaced with comparable merchandise.

Distribution of Merchandise

A substantial portion of the Company's merchandise is shipped to stores or customers through a combination of third party, or the Company's, distribution facilities which are primarily located throughout the United States. The remaining merchandise is shipped directly from vendors. Shipments are made by contract carriers on a regular basis depending upon location.

See Item 2 – Properties for additional information regarding the Company's distribution facilities.

Employees

As of March 1, 2014, the Company employed approximately 58,000 persons in full-time and part-time positions. The Company believes that its relations with its employees are very good and that the labor turnover rate among its management employees is lower than that generally experienced within the industry.

Seasonality

The Company's sales exhibit seasonality with sales levels generally higher in the calendar months of August, November and December, and generally lower in February.

Expansion Program

The Company is engaged in an ongoing expansion program involving the opening of new stores in both new and existing markets, the expansion or renovation of existing stores, the repositioning of stores within markets when appropriate, the evolution of its omnichannel shopping environment and the continuous review of strategic acquisitions.

In the 22-year period from the beginning of fiscal 1992 to the end of fiscal 2013, the chain has grown from 34 stores to 1,496 stores plus its various websites, other interactive platforms and distribution facilities. The Company's 1,496 stores operate in all 50 states, the District of Columbia, Puerto Rico and Canada, including: 1,014 BBB stores operating in all 50 states, the District of Columbia, Puerto Rico and Canada and through www.bedbathandbeyond.com and www.bedbathandbeyond.ca; 265 Cost Plus World Market stores operating in 31 states and the District of Columbia and through www.worldmarket.com; 90 Baby stores operating in 31 states and through www.buybuybaby.com; 77 CTS stores operating in 21 states and through www.christmastreeshops.com and www.andthat.com; and 50 Harmon stores operating in five states and through www.harmondiscount.com and www.facevalues.com. Total store square footage grew from approximately 0.9 million square feet at the beginning of fiscal 1992 to approximately 42.6 million square feet at the end of fiscal 2013. During fiscal 2013, the Company opened a total of 33 new stores, including 13 BBB stores throughout the United States and Canada and five Cost Plus World Market stores, eight Baby stores, four CTS stores and three Harmon stores throughout the United States. In addition, the Company continued to optimize its operations in a number of trade areas through renovating and repositioning stores in various markets, which included the closing of three BBB stores, four Cost Plus World Market stores and one CTS store. In fiscal 2013, consolidated store space, net of openings and closings for all concepts, increased by 0.6 million square feet. Additionally, the Company is a partner in a joint venture which opened one store during fiscal 2013 and as of March 1, 2014, operated a total of four retail stores in Mexico under the name Bed Bath & Beyond.

6

The Company expects to enhance its omnichannel capabilities as well as open new stores and expand existing stores as opportunities arise. The Company believes that throughout the United States and Canada, there is an opportunity to operate in excess of 1,300 BBB stores as well as grow Cost Plus World Market, CTS and Baby from coast to coast. Additionally, the Company will continue to open Harmon stores and place health and beauty care offerings in selected stores as well as specialty food and beverage departments in selected BBB stores. The Company is committed to the continued growth of its merchandise categories and channels.

The Company has built its management structure with a view toward its expansion and believes that, as a result, it has the management depth necessary to support its anticipated expansion program.

During fiscal 2012, the Company acquired Linen Holdings and Cost Plus World Market.

Competition

The Company operates in the fragmented and highly competitive retail industry. The Company competes with many different types of retailers, including omnichannel retailers, that sell many or most of the same products. Such competitors include, but are not limited to, department stores, specialty retailers, discount and mass merchandise retailers, national chains and online only retailers. In addition, the Company competes, to a more limited extent, with factory outlet stores. Other entities continue to introduce new concepts that include many of the product lines offered by the Company. There can be no assurance that the operation of competitors will not have a material adverse effect on the Company.

Tradenames and Service Marks

The Company uses the service marks "Bed Bath & Beyond," "buybuy BABY," "Christmas Tree Shops," "andThat!," "Harmon," "Face Values," "Cost Plus," "World Market" and "Cost Plus World Market" in connection with its retail services. The Company has registered trademarks and service marks or is seeking registrations for these and other trademarks and service marks with the United States Patent and Trademark Office. The Company also has registered or has applications pending with the trademark registries of several foreign countries, including having registered the "Bed Bath & Beyond" name and logo in Canada and Mexico. The Company also files patent applications and seeks copyright registrations where it deems such to be advantageous to the business. Management believes that its name recognition and service marks are important elements of the Company's merchandising strategy.

Available Information

The Company makes available as soon as reasonably practicable after filing with the Securities and Exchange Commission ("SEC"), free of charge, through its website, www.bedbathandbeyond.com, the Company's annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, electronically filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934.

Executive Officers of the Registrant

The following table sets forth the name, age and business experience of the Executive Officers of the Registrant:

7

Name | Age | Positions |

Warren Eisenberg | 83 | Co-Chairman and Director |

Leonard Feinstein | 77 | Co-Chairman and Director |

Steven H. Temares | 55 | Chief Executive Officer and Director |

Arthur Stark | 59 | President and Chief Merchandising Officer |

Matthew Fiorilli | 57 | Senior Vice President – Stores |

Eugene A. Castagna | 48 | Chief Operating Officer |

Susan E. Lattmann | 46 | Chief Financial Officer and Treasurer |

Warren Eisenberg is a Co-Founder of the Company and has served as Co-Chairman since 1999. He has served as a Director since 1971. Mr. Eisenberg served as Chairman from 1992 to 1999, and served as Co-Chief Executive Officer from 1971 to 2003.

Leonard Feinstein is a Co-Founder of the Company and has served as Co-Chairman since 1999. He has served as a Director since 1971. Mr. Feinstein served as President from 1992 to 1999, and served as Co-Chief Executive Officer from 1971 to 2003.

Steven H. Temares has been Chief Executive Officer since 2003 and has served as a Director since 1999. Mr. Temares was President and Chief Executive Officer from 2003 to 2006, President and Chief Operating Officer from 1999 to 2003 and Executive Vice President and Chief Operating Officer from 1997 to 1999. Mr. Temares joined the Company in 1992.

Arthur Stark has been President and Chief Merchandising Officer since 2006. Mr. Stark has served as Chief Merchandising Officer since 1999 and was a Senior Vice President from 1999 to 2006. Mr. Stark joined the Company in 1977.

Matthew Fiorilli has been Senior Vice President - Stores since 1999. Mr. Fiorilli joined the Company in 1973.

Eugene A. Castagna has been Chief Operating Officer since February 2014. Mr. Castagna served as Chief Financial Officer and Treasurer from 2006 to 2014, Assistant Treasurer from 2002 to 2006 and as Vice President - Finance from 2000 to 2006. Mr. Castagna is a certified public accountant and joined the Company in 1994.

Susan E. Lattmann has been Chief Financial Officer and Treasurer since February 2014. Ms. Lattmann served as Vice President – Finance from 2006 to 2014, Vice President - Controller from 2001 to 2006 and Controller from 2000 to 2001. Ms. Lattmann is a certified public accountant and joined the Company in 1996.

The Company's executive officers are elected by the Board of Directors for one-year terms and serve at the discretion of the Board of Directors. No family relationships exist between any of the executive officers or directors of the Company.

ITEM 1A – | RISK FACTORS |

FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended. The Company's actual results and future financial condition may differ materially from those expressed in any such forward-looking statements as a result of many factors. Such factors include the following:

8

General economic factors beyond the Company's control and changes in the economic climate could adversely affect the Company's performance.

General economic factors that are beyond the Company's control impact the Company's forecasts and actual performance. These factors include housing markets, recession, inflation, deflation, consumer credit availability, consumer debt levels, fuel and energy costs, interest rates, tax rates and policy, unemployment trends, the impact of natural disasters, civil disturbances and terrorist activities, conditions affecting the retail environment for products sold by the Company and other matters that influence consumer spending. Changes in the economic climate could adversely affect the Company's performance.

The Company operates in the highly competitive retail business where the use of emerging technologies as well as unanticipated changes in the pricing and other practices of competitors may adversely affect the Company's performance.

The retail business is highly competitive. The Company competes for customers, employees, locations, merchandise, technology, services and other important aspects of the business with many other local, regional and national retailers. Those competitors range from specialty retailers to department stores and discounters as well as online and multichannel retailers. Specifically, rapidly evolving technologies are altering the manner in which the Company and its competitors communicate and transact with customers; the Company's execution of its own omnichannel strategy to adapt to these changes, in relation to its competitors' actions as well as to its customers adoption of new technology, presents a specific risk. Further, unanticipated changes in the pricing and other practices of the Company's competitors, including promotional activity and rapid price fluctuation enabled by technology, may adversely affect the Company's performance.

The Company's failure to anticipate and respond in a timely fashion to changes in consumer preferences and demographic factors may adversely affect the Company's financial condition and results of operations.

The Company's success depends on its ability to anticipate and respond in a timely manner to changing merchandise trends, customer demands and demographics. The Company's failure to anticipate, identify or react appropriately to changes in customer tastes, preferences, shopping and spending patterns and other lifestyle decisions could lead to, among other things, excess inventories or a shortage of products and may adversely affect the Company's financial condition and results of operations.

Unusual weather patterns could adversely affect the Company's performance.

The Company's operating results could be negatively impacted by unusual weather patterns. Frequent or unusually heavy snow, ice or rain storms, hurricanes, floods, tornados or extended periods of unseasonable temperatures could adversely affect the Company's performance.

A major disruption of the Company's information technology systems could negatively impact operating results.

The Company's operating results could be negatively impacted by a major disruption of the Company's information technology systems. The Company relies heavily on these systems to process transactions, manage inventory replenishment, summarize results and control distribution of products. Despite numerous safeguards and careful contingency planning, these systems are still subject to power outages, computer viruses, telecommunication failures, security breaches and other catastrophic events. A major disruption of the systems and their backup mechanisms may cause the Company to incur significant costs to repair the systems, experience a critical loss of data and/or result in business interruptions.

9

A breach of the Company's data security systems or those of its third party service providers could have a negative impact on the Company's operating results and financial performance due to possible loss of consumer confidence, as well as potential government penalties and private litigation.

The Company processes, transmits, stores and maintains certain information about its customers and employees in the ordinary course of business. In connection with certain activities, including without limitation credit card processing, website hosting, data encryption and software support, the Company utilizes third party service providers, and the Company believes it takes appropriate steps to require such providers to secure such information and to assess their ability to do so. The Company invests considerable resources in protecting this sensitive information but is still subject to a possible security event, including but not limited to cybercrimes or cybersecurity attacks which may not be detected for a period of time. A breach of its security systems or those of its third party service providers resulting in unauthorized access to stored personal information could negatively impact the Company's operating results and financial performance. Certain aspects of the business, particularly the Company's websites, heavily depend on consumers entrusting personal financial information to be transmitted securely over public networks. A loss of consumer confidence from such a breach could result in lost future sales and have a material adverse effect on the Company's reputation. In addition, a breach could cause the Company to incur significant costs to restore the integrity of its systems, could require the devotion of significant management resources, and could result in significant costs in government penalties and private litigation.

A failure of the Company's suppliers to adhere to appropriate laws or standards could negatively impact its reputation.

The Company purchases substantially all of its merchandise in the United States, the majority from domestic sources and the balance from importers. The Company purchases a small amount of its merchandise directly from overseas sources. The failure of one of the Company's domestic or foreign suppliers to adhere to labor, environmental, health and safety laws and standards could negatively impact the Company's reputation and have an adverse effect on the Company's results of operations.

A failure to protect the reputation of the Company in any aspect of its operations could potentially impact its operating and financial results.

The Company's reputation is based, in part, on perceptions of subjective qualities, so incidents involving the Company, its products or the retail industry in general that erode customer trust or confidence could adversely affect the Company's reputation and its business. Challenges to the Company's compliance with a variety of social, product, labor and environmental standards could also jeopardize its reputation and lead to adverse publicity, especially in social media outlets. Damage to the reputation of the Company in any aspect of its operations could potentially impact its operating and financial results as well as require additional resources to rebuild its reputation.

Changes in statutory, regulatory, and other legal requirements at a local, state or provincial and national level could potentially impact the Company's operating and financial results.

The Company is subject to numerous statutory, regulatory and legal requirements at a local, state or provincial and national level. The Company's operating results could be negatively impacted by developments in these areas due to the costs of compliance in addition to possible government penalties and litigation in the event of deemed noncompliance. Changes in the regulatory environment in the area of product safety, environmental protection, privacy and information security, wage and hour laws, among others, could potentially impact the Company's operations and financial results.

New, or developments in existing, litigation, claims or assessments could potentially impact the Company's operating and financial results.

The Company is involved in litigation, claims and assessments incidental to the Company's business, the disposition of which is not expected to have a material effect on the Company's financial position or results of operations. It is possible, however, that future results of operations for any particular quarterly or annual period could be materially affected by changes in the Company's assumptions related to these matters. While outcomes of such actions vary, any such claim or assessment against the Company could potentially impact the Company's operations and financial results.

10

Changes to accounting rules, regulations and tax laws, or new interpretations of existing accounting standards or tax laws could negatively impact the Company's operating results and financial position.

The Company's operating results and financial position could be negatively impacted by changes to accounting rules and regulations or new interpretations of existing accounting standards. These changes may include, without limitation, changes to lease accounting standards. The Company's effective income tax rate could be impacted by changes in accounting standards as well as changes in tax laws or the interpretations of these tax laws by courts and taxing authorities which could negatively impact the Company's financial results.

The success of the Company is dependent, in part, on managing costs of labor, merchandise and other expenses that are subject to factors beyond the Company's control.

The Company's success depends, in part, on its ability to manage operating costs and to look for opportunities to reduce costs. The Company's ability to meet its labor needs while controlling costs is subject to external factors such as unemployment levels, prevailing wage rates, minimum wage legislation, labor organizing activities and changing demographics. The Company's ability to find qualified vendors and obtain access to products in a timely and efficient manner can be adversely affected by political instability, the financial instability of suppliers, suppliers' noncompliance with applicable laws, transportation costs and other factors beyond the Company's control.

The success of the Company is dependent, in part, on the ability of its employees in all areas of the organization to execute its business plan and, ultimately, to satisfy its customers.

The Company's ability to attract and retain qualified employees in all areas of the organization may be affected by a number of factors, including geographic relocation of employees, operations or facilities and the highly competitive markets in which the Company operates, including the markets for the types of skilled individuals needed to support the Company's continued success domestically, interactively and, over the longer term, internationally.

The success of the Company is dependent, in part, on its ability to open new stores, develop its omnichannel capabilities and operate profitably.

The Company's success depends, in part, on its ability to open new stores, develop its omnichannel capabilities and operate profitably. The Company's ability to open additional stores successfully will depend on a number of factors, including its identification and availability of suitable store locations; its success in negotiating leases on acceptable terms; its hiring and training of skilled store operating personnel, especially management; and its timely development of new stores, including the availability of construction materials and labor and the absence of significant construction and other delays in store openings based on weather or other events. The Company's ability to develop its omnichannel capabilities will depend on a number of factors, including its assessment and implementation of changing technologies. This increases the cost of doing business and the risk that the Company's business practices could result in liabilities that may adversely affect its performance, despite the exercise of reasonable care.

Disruptions in the financial markets could have an adverse effect on the Company's ability to access its cash and cash equivalents.

The Company may have amounts of cash and cash equivalents at financial institutions that are in excess of federally insured limits. While the Company closely manages its cash and cash equivalents balances to minimize risk, if there were disruptions in the financial markets, the Company can not be assured that it will not experience losses on its deposits.

11

The Company has acquired several businesses and continues to evaluate potential business initiatives, including acquisitions, any of which could adversely impact the Company's performance.

The Company believes it carefully evaluates and plans for the integration of newly acquired businesses, as well as carefully prepares for and executes on other business combinations and strategic initiatives that are part of the success of its business. However, such activities involve certain inherent risks, including the failure to retain key personnel from an acquired business; undisclosed or subsequently arising liabilities; challenges in the successful integration of operations, aligning standards, policies and systems; and the potential diversion of management resources from existing operations to respond to unforeseen issues arising in the context of the integration of a new business or initiative.

ITEM 1B – | UNRESOLVED STAFF COMMENTS |

None.

12

ITEM 2 – | PROPERTIES |

Most of the Company's stores are located in suburban areas of medium and large-sized cities. These stores are situated in strip and power strip shopping centers, as well as in major off-price and conventional malls, and in free standing buildings.

The Company's 1,496 stores are located in all 50 states, the District of Columbia, Puerto Rico and Canada and range in size from approximately 5,000 to 100,000 square feet, but are predominantly between 18,000 and 50,000 square feet. Approximately 85% to 90% of store space is used for selling areas.

The table below sets forth the locations of the Company's stores as of March 1, 2014:

Alabama | 21 | New Mexico | 9 | ||||||

Alaska | 2 | New York | 96 | ||||||

Arizona | 43 | North Carolina | 45 | ||||||

Arkansas | 7 | North Dakota | 2 | ||||||

California | 187 | Ohio | 51 | ||||||

Colorado | 34 | Oklahoma | 8 | ||||||

Connecticut | 24 | Oregon | 17 | ||||||

Delaware | 4 | Pennsylvania | 43 | ||||||

Florida | 98 | Rhode Island | 5 | ||||||

Georgia | 36 | South Carolina | 24 | ||||||

Hawaii | 2 | South Dakota | 3 | ||||||

Idaho | 9 | Tennessee | 27 | ||||||

Illinois | 57 | Texas | 112 | ||||||

Indiana | 24 | Utah | 15 | ||||||

Iowa | 10 | Vermont | 3 | ||||||

Kansas | 11 | Virginia | 44 | ||||||

Kentucky | 11 | Washington | 36 | ||||||

Louisiana | 19 | West Virginia | 3 | ||||||

Maine | 8 | Wisconsin | 16 | ||||||

Maryland | 22 | Wyoming | 2 | ||||||

Massachusetts | 43 | District of Columbia | 3 | ||||||

Michigan | 44 | Puerto Rico | 3 | ||||||

Minnesota | 14 | Alberta, Canada | 9 | ||||||

Mississippi | 7 | British Columbia, Canada | 7 | ||||||

Missouri | 24 | Manitoba, Canada | 1 | ||||||

Montana | 8 | New Brunswick, Canada | 2 | ||||||

Nebraska | 6 | Newfoundland, Canada | 1 | ||||||

Nevada | 13 | Novia Scotia, Canada | 1 | ||||||

New Hampshire | 14 | Ontario, Canada | 18 | ||||||

New Jersey | 87 | Prince Edward Island, Canada | 1 | ||||||

Total | 1,496 | ||||||||

The Company leases substantially all of its existing stores. The leases provide for original lease terms that generally range from 10 to 15 years and most leases provide for renewal options, often at increased rents. The Company evaluates leases on an ongoing basis which may lead to renegotiated lease terms, including rents during renewal options, or the possible relocation of stores. Certain leases provide for scheduled rent increases (which, in the case of fixed increases, the Company accounts for on a straight-line basis over the committed lease term, beginning when the Company obtains possession of the premises) and/or for contingent rent (based upon store sales exceeding stipulated amounts).

13

The Company has distribution facilities, which ship merchandise to stores or customers, totaling approximately 5.8 million square feet consisting of three owned and 11 leased facilities.

As of March 1, 2014, the Company occupied approximately 508,000 square feet of office space at seven locations for procurement and corporate office functions. The corporate headquarters within two owned facilities in Union, New Jersey includes approximately 306,000 square feet with the remaining approximately 202,000 square feet within owned and leased facilities in California, Florida, Massachusetts, New Jersey, New York and North Carolina. In addition, the Company has seven locations, totaling approximately 14,000 square feet, which are utilized primarily for institutional sales related functions.

ITEM 3 – | LEGAL PROCEEDINGS |

The Company is party to various legal proceedings arising in the ordinary course of business, which the Company does not believe to be material to the Company's business or financial condition.

ITEM 4 – | MINE SAFETY DISCLOSURES |

Not Applicable.

14

PART II

ITEM 5 – | MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The following table sets forth the high and low reported closing prices of the Company's common stock on the NASDAQ National Market System for the periods indicated.

High | Low | |||||||

Fiscal 2013: | ||||||||

1st Quarter | $ | 70.07 | $ | 56.75 | ||||

2nd Quarter | 78.18 | 66.98 | ||||||

3rd Quarter | 78.58 | 71.78 | ||||||

4th Quarter | 80.48 | 62.68 | ||||||

High | Low | |||||||

Fiscal 2012: | ||||||||

1st Quarter | $ | 72.47 | $ | 59.74 | ||||

2nd Quarter | 74.72 | 59.34 | ||||||

3rd Quarter | 71.60 | 56.40 | ||||||

4th Quarter | 60.39 | 54.91 | ||||||

The common stock is quoted through the NASDAQ National Market System under the symbol BBBY. On March 29, 2014, there were approximately 5,600 shareholders of record of the common stock (without including individual participants in nominee security position listings). On March 29, 2014, the last reported sale price of the common stock was $68.43.

The Company has not paid cash dividends on its common stock since its 1992 initial public offering and does not currently plan to pay dividends on its common stock. The payment of any future dividends will be determined by the Board of Directors in light of conditions then existing, including the Company's earnings, financial condition and requirements, business conditions and other factors. See Item 8 - Financial Statements and Supplementary Data.

Since 2004 through the end of fiscal 2013, the Company has repurchased approximately $6.3 billion of its common stock through share repurchase programs. The Company's purchases of its common stock during the fourth quarter of fiscal 2013 were as follows:

Period | Total Number of Shares Purchased (1) | Average Price Paid per Share (2) | Total Number of Shares Purchased as | Approximate Dollar Value of Shares | ||||||||||||

December 1, 2013 - December 28, 2013 | 1,717,400 | $ | 77.61 | 1,717,400 | $ | 1,532,716,191 | ||||||||||

December 29, 2013 - January 25, 2014 | 2,594,500 | $ | 72.77 | 2,594,500 | $ | 1,343,914,027 | ||||||||||

January 26, 2014 - March 1, 2014 | 3,237,100 | $ | 64.75 | 3,237,100 | $ | 1,134,319,018 | ||||||||||

Total | 7,549,000 | $ | 70.43 | 7,549,000 | $ | 1,134,319,018 | ||||||||||

(1) Between December 2004 and December 2012, the Company's Board of Directors authorized, through several share repurchase programs, the repurchase of $7.450 billion of its shares of common stock. The Company has authorization to make repurchases from time to time in the open market or through other parameters approved by the Board of Directors pursuant to existing rules and regulations. Shares purchased indicated in this table also include the withholding of a portion of restricted shares to cover taxes on vested restricted shares.

(2) Excludes brokerage commissions paid by the Company.

15

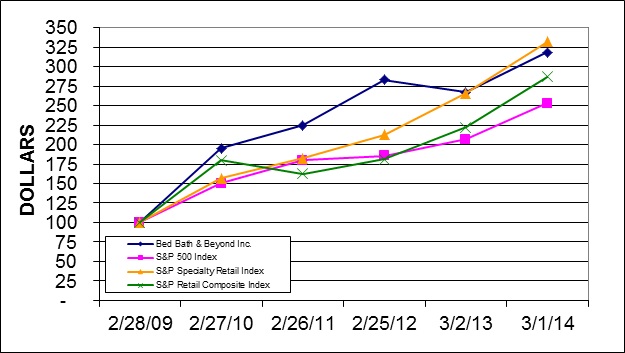

Stock Price Performance Graph

The graph shown below compares the performance of the Company's common stock with that of the S&P 500 Index, the S&P Specialty Retail Index and the S&P Retail Composite Index over the same period (assuming the investment of $100 in the Company's common stock and each of the three Indexes on February 28, 2009, and the reinvestment of dividends, if any).

16

ITEM 6 – | SELECTED FINANCIAL DATA |

Consolidated Selected Financial Data | Fiscal Year Ended (1) | |||||||||||||||||||

(in thousands, except per share | March 1, | March 2, | February 25, | February 26, | February 27, | |||||||||||||||

and selected operating data) | 2014 | 2013 (2) | 2012 | 2011 | 2010 | |||||||||||||||

Statement of Earnings Data: | ||||||||||||||||||||

Net sales | $ | 11,503,963 | $ | 10,914,585 | $ | 9,499,890 | $ | 8,758,503 | $ | 7,828,793 | ||||||||||

Gross profit | 4,565,582 | 4,388,755 | 3,930,933 | 3,622,929 | 3,208,119 | |||||||||||||||

Operating profit | 1,614,587 | 1,638,218 | 1,568,369 | 1,288,458 | 980,687 | |||||||||||||||

Net earnings | 1,022,290 | 1,037,788 | 989,537 | 791,333 | 600,033 | |||||||||||||||

Net earnings per share - Diluted | $ | 4.79 | $ | 4.56 | $ | 4.06 | $ | 3.07 | $ | 2.30 | ||||||||||

Selected Operating Data: | ||||||||||||||||||||

Number of stores open (at period end) | 1,496 | 1,471 | 1,173 | 1,139 | 1,100 | |||||||||||||||

Total square feet of store space (at period end) | 42,619,000 | 42,030,000 | 36,125,000 | 35,055,000 | 33,740,000 | |||||||||||||||

Percentage increase in comparable sales | 2.4 | % | 2.7 | % | 5.9 | % | 7.8 | % | 4.4 | % | ||||||||||

Comparable sales (in 000's) (3) | $ | 10,660,573 | $ | 9,819,904 | $ | 9,157,183 | $ | 8,339,112 | $ | 7,409,203 | ||||||||||

Number of comparable stores | 1,412 | 1,122 | 1,076 | 1,013 | 942 | |||||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||||

Working capital | $ | 1,974,651 | $ | 2,232,275 | $ | 2,803,809 | $ | 2,751,398 | $ | 2,413,791 | ||||||||||

Total assets | 6,356,033 | 6,279,952 | 5,724,546 | 5,646,193 | 5,152,130 | |||||||||||||||

Long-term sale/leaseback and capital lease obligations (4) | 108,046 | 108,364 | - | - | - | |||||||||||||||

Long-term debt | - | - | - | - | - | |||||||||||||||

Shareholders' equity (5) (6) | $ | 3,941,287 | $ | 4,079,730 | $ | 3,922,528 | $ | 3,931,659 | $ | 3,652,904 | ||||||||||

(1) Each fiscal year represents 52 weeks, except for fiscal 2012 (ended March 2, 2013) which represents 53 weeks.

(2) The Company acquired Linen Holdings, LLC. on June 1, 2012 and Cost Plus, Inc. on June 29, 2012.

(3) Comparable sales include sales for stores and websites which have been operating for twelve full months following the opening period (typically four to six weeks).

(4) As a result of the Cost Plus, Inc. acquisition, the Company assumed two sale/leaseback and various capital lease obligations.

(5) The Company has not declared any cash dividends in any of the fiscal years noted above.

(6) In fiscal 2013, 2012, 2011, 2010 and 2009, the Company repurchased approximately $1.284 billion, $1.001 billion, $1.218 billion, $688 million and $95 million of its common stock, respectively.

17

ITEM 7 – | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

OVERVIEW

Bed Bath & Beyond Inc. and subsidiaries (the "Company") is a retailer which operates under the names Bed Bath & Beyond ("BBB"), Christmas Tree Shops, Christmas Tree Shops andThat! or andThat! (collectively, "CTS"), Harmon or Harmon Face Values (collectively, "Harmon"), buybuy BABY ("Baby") and World Market, Cost Plus World Market and Cost Plus (collectively, "Cost Plus World Market"). Customers can purchase products from the Company either in store, online or through a mobile device. The Company has the developing ability to fulfill customer purchases by in store customer pick up or by direct shipment to the customer from the Company's distribution facilities, stores or vendors. The Company also operates Linen Holdings, a provider of a variety of textile products, amenities and other goods to institutional customers in the hospitality, cruise line, food service, healthcare and other industries. (See "Acquisitions," Note 2 in the consolidated financial statements for the acquisitions of Cost Plus World Market and Linen Holdings). Additionally, the Company is a partner in a joint venture which operates four retail stores in Mexico under the name Bed Bath & Beyond.

The Company accounts for its operations as two operating segments: North American Retail and Institutional Sales. The Institutional Sales operating segment, which is comprised of Linen Holdings, does not meet the quantitative thresholds under U.S. generally accepted accounting principles and therefore is not a reportable segment.

The Company sells a wide assortment of domestics merchandise and home furnishings. Domestics merchandise includes categories such as bed linens and related items, bath items and kitchen textiles. Home furnishings include categories such as kitchen and tabletop items, fine tabletop, basic housewares, general home furnishings, consumables and certain juvenile products.

The Company's objective is to be a customer's first choice for products and services in the categories offered, in the markets, channels and countries in which the Company operates. The Company's strategy is to achieve this objective through excellent customer service, an extensive breadth, depth and differentiated assortment in an omnichannel retail environment and the introduction of new merchandising offerings, supported by the continuous development and improvement of its infrastructure.

Operating in the highly competitive retail industry, the Company, along with other retail companies, is influenced by a number of factors including, but not limited to, general economic conditions including the housing market, relatively high unemployment and historically high commodity prices; the overall macroeconomic environment and related changes in the retailing environment; consumer preferences and spending habits; unusual weather patterns and natural disasters; competition from existing and potential competitors; evolving technology; and the ability to find suitable locations at acceptable occupancy costs and other terms to support the Company's expansion program. The Company cannot predict whether, when or the manner in which these factors could affect the Company's operating results.

For fiscal 2013, the results of operations include Linen Holdings and Cost Plus World Market from the beginning of the fiscal year. For fiscal 2012, the results of operations include Linen Holdings since the date of acquisition on June 1, 2012 and Cost Plus World Market since the date of acquisition on June 29, 2012.

The following represents an overview of the Company's financial performance for the periods indicated:

| · | Net sales in fiscal 2013 (fifty-two weeks) increased approximately 5.4% to $11.504 billion; net sales in fiscal 2012 (fifty-three weeks) increased approximately 14.9% to $10.915 billion over net sales of $9.500 billion in fiscal 2011 (fifty-two weeks). |

18

| · | Comparable sales for fiscal 2013 increased by approximately 2.4% as compared with an increase of approximately 2.7% in fiscal 2012 and an increase of approximately 5.9% in fiscal 2011. Comparable sales percentages are calculated based on an equivalent number of weeks for each annual period. |

Comparable sales include sales for stores and websites which have been operating for twelve full months following the opening period (typically four to six weeks). Stores relocated or expanded are excluded from comparable sales if the change in square footage would cause meaningful disparity in sales over the prior period. In the case of a store to be closed, such store's sales are not considered comparable once the store closing process has commenced. Linen Holdings is excluded from the comparable sales calculations and will continue to be excluded on an ongoing basis as it represents non-retail activity. Cost Plus World Market was excluded from the comparable sales calculations through the end of the fiscal first half of 2013, and is included beginning with the fiscal third quarter of 2013.

| · | Gross profit for fiscal 2013 was $4.566 billion or 39.7% of net sales compared with $4.389 billion or 40.2% of net sales for fiscal 2012 and $3.931 billion or 41.4% of net sales for fiscal 2011. |

| · | Selling, general and administrative expenses ("SG&A") for fiscal 2013 were $2.951 billion or 25.7% of net sales compared with $2.751 billion or 25.2% of net sales for fiscal 2012 and $2.363 billion or 24.9% of net sales for fiscal 2011. |

| · | The effective tax rate was 36.6%, 36.5% and 37.0% for fiscal years 2013, 2012 and 2011, respectively. The tax rate included discrete tax items resulting in net benefits of approximately $20.0 million, $26.7 million and $20.7 million, respectively, for fiscal 2013, 2012 and 2011. |

| · | For the fiscal year ended March 1, 2014 (fifty-two weeks), net earnings per diluted share were $4.79 ($1.022 billion), an increase of approximately 5%, as compared with net earnings per diluted share of $4.56 ($1.038 billion) for fiscal 2012 (fifty-three weeks), which was an increase of approximately 12% from net earnings per diluted share of $4.06 ($989.5 million) for fiscal 2011 (fifty-two weeks). For the fiscal year ended March 1, 2014, the increase in net earnings per diluted share is the result of the items described above and the impact of the Company's repurchases of its common stock, partially offset by a reduction of approximately $0.06 to $0.07 per diluted share as a result of the disruptive weather in the fiscal fourth quarter. For the fiscal year ended March 2, 2013, the increase in net earnings per diluted share is the result of the items described above, which includes an estimated $0.05 benefit related to the fifty-third week in fiscal year 2012 and the impact of the Company's repurchases of its common stock, partially offset by the negative impact of Hurricane Sandy in the fiscal third quarter. |

During fiscal 2013, the Company continued the integration of the two fiscal 2012 acquisitions as well as advanced initiatives including: enhanced the omnichannel experience for its customers by replatforming and adding improved functionality to its Baby and BBB websites, replatforming its mobile sites and applications and growing and developing its information technology, analytics, marketing and e-commerce groups; completed the construction of a new information technology data center and are engaged in equipping the facility which will enhance the Company's disaster recovery capabilities and support its overall information technology systems; installed energy efficient lighting, and heating and cooling systems in the Company's stores; and continued the ongoing deployment of new and enhanced systems and equipment to allow its stores to take advantage of new technologies and processes.

Capital expenditures for fiscal 2013, 2012 and 2011 were $317.2 million, $314.7 million and $243.4 million, respectively. The Company remains committed to making the required investments in its infrastructure to help position the Company for continued growth and success. The Company continues to review and prioritize its capital needs while continuing to make investments, principally for information technology enhancements, including omnichannel capabilities, new stores, existing store improvements, and other projects whose impact is considered important to its future.

19

During fiscal 2013, 2012 and 2011, the Company repurchased 18.3 million, 16.1 million and 21.5 million shares, respectively, of its common stock at a total cost of approximately $1.284 billion, $1.001 billion and $1.218 billion, respectively. Since the end of fiscal 2011, the Company has returned approximately 89% of its cash flows from operations to its shareholders through share repurchase programs.

During fiscal 2013, the Company opened a total of 33 new stores. In addition, the Company continued to optimize its operations in a number of trade areas through renovating and repositioning stores in various markets, which also included the closing of eight stores during fiscal 2013. The Company plans to continue to expand its operations and invest in its infrastructure to reach its long term objectives. In fiscal 2014, the Company expects to open approximately 30 new stores company-wide and will continue to renovate stores or reposition stores within various markets, when appropriate. Additionally, during fiscal 2014, the Company will continue to enhance its omnichannel capabilities, through, among other things, continuing to add new functionality and assortment to its selling websites, mobile sites and applications and opening an additional distribution facility for both direct to customer and store fulfillment.

RESULTS OF OPERATIONS

The following table sets forth for the periods indicated (i) selected statement of earnings data of the Company expressed as a percentage of net sales and (ii) the percentage change in dollar amounts from the prior year in selected statement of earnings data:

Fiscal Year Ended | ||||||||||||||||||||

Percentage | Percentage Change | |||||||||||||||||||

of Net Sales | from Prior Year | |||||||||||||||||||

March 1, | March 2, | February 25, | March 1, | March 2, | ||||||||||||||||

2014 | 2013 | 2012 | 2014 | 2013 | ||||||||||||||||

Net sales | 100.0 | % | 100.0 | % | 100.0 | % | 5.4 | % | 14.9 | % | ||||||||||

Cost of sales | 60.3 | 59.8 | 58.6 | 6.3 | 17.2 | |||||||||||||||

Gross profit | 39.7 | 40.2 | 41.4 | 4.0 | 11.6 | |||||||||||||||

Selling, general and administrative expenses | 25.7 | 25.2 | 24.9 | 7.3 | 16.4 | |||||||||||||||

Operating profit | 14.0 | 15.0 | 16.5 | (1.4 | ) | 4.5 | ||||||||||||||

Earnings before provision for income taxes | 14.0 | 15.0 | 16.5 | (1.3 | ) | 4.1 | ||||||||||||||

Net earnings | 8.9 | 9.5 | 10.4 | (1.5 | ) | 4.9 | ||||||||||||||

Net Sales

Since fiscal 2012 was a fifty-three week year, fiscal 2013 started a week later than fiscal 2012. The comparable sales calendar compares the same calendar weeks. The table below summarizes by fiscal quarter the time period for the financial reporting calendar and the comparable sales calendar.

20

Financial Reporting Calendar | ||||

Fiscal 2013 (fifty-two weeks) | Fiscal 2012 (fifty-three weeks) | |||

First Quarter | March 3, 2013 - June 1, 2013 | February 26, 2012 - May 26, 2012 | ||

Second Quarter | June 2, 2013 - August 31, 2013 | May 27, 2012 - August 25, 2012 | ||

Third Quarter | September 1, 2013 - November 30, 2013 | August 26, 2012 - November 24, 2012 | ||

Fourth Quarter | December 1, 2013 - March 1, 2014 | November 25, 2012 - March 2, 2013 | ||

Comparable Sales Calendar | ||||

Fiscal 2013 (fifty-two weeks) | Fiscal 2012 (fifty-two weeks) | |||

First Quarter | March 3, 2013 - June 1, 2013 | March 4, 2012 - June 2, 2012 | ||

Second Quarter | June 2, 2013 - August 31, 2013 | June 3, 2012 - September 1, 2012 | ||

Third Quarter | September 1, 2013 - November 30, 2013 | September 2, 2012 - December 1, 2012 | ||

Fourth Quarter | December 1, 2013 - March 1, 2014 | December 2, 2012 - March 2, 2013 | ||

Net sales in fiscal 2013 (fifty-two weeks) increased $589.4 million to $11.504 billion, representing an increase of 5.4% over $10.915 billion of net sales in fiscal 2012 (fifty-three weeks), which increased $1.415 billion or 14.9% over the $9.500 billion of net sales in fiscal 2011 (fifty-two weeks). For fiscal 2013, approximately 62% of the increase in net sales was attributable to the inclusion of Cost Plus World Market prior to its inclusion in comparable sales and Linen Holdings prior to the anniversary of its acquisition, approximately 42% of the increase was attributable to an increase in comparable sales and 26% of the increase was primarily attributable to an increase in the Company's new store sales and the post-acquisition period for Linen Holdings, partially offset by a decrease of approximately 30% as a result of the non-comparable additional week in fiscal 2012.

For fiscal 2013, comparable sales, which includes 1,412 stores, represented $10.661 billion of net sales; for fiscal 2012, comparable sales, which includes, 1,122 stores, represented $9.820 billion of net sales; and for fiscal 2011, comparable sales, which includes 1,076 stores, represented $9.157 billion of net sales. The number of stores includes only those which constituted a comparable store for the entire respective fiscal period. The increase in comparable sales, which includes Cost Plus World Market beginning with the fiscal third quarter and excludes Linen Holdings, was approximately 2.4% for fiscal 2013, as compared with an increase of approximately 2.7% for fiscal 2012. The increase in comparable sales for fiscal 2013 was due to an increase in the average transaction amount and a slight increase in the number of transactions. The increase in comparable sales for fiscal 2012 was due to an increase in the average transaction amount partially offset by a decrease in the number of transactions. Comparable sales are calculated based on an equivalent number of weeks for each annual period.

Sales of domestics merchandise accounted for approximately 36%, 39% and 40% of net sales in fiscal 2013, 2012 and 2011, respectively, of which the Company estimates that bed linens accounted for approximately 12% of net sales in fiscal 2013, 2012 and 2011, respectively. The remaining net sales in fiscal 2013, 2012 and 2011 of 64%, 61% and 60%, respectively, represented sales of home furnishings. No other individual product category accounted for 10% or more of net sales during fiscal 2013, 2012 or 2011.

Gross Profit

Gross profit in fiscal 2013, 2012 and 2011 was $4.566 billion or 39.7% of net sales, $4.389 billion or 40.2% of net sales and $3.931 billion or 41.4% of net sales, respectively. The decreases in the gross profit margin as a percentage of net sales between fiscal 2013 and 2012 and between fiscal 2012 and 2011 were primarily attributed to an increase in coupons, due to increases in both redemptions and the average coupon amount, and a shift in the mix of merchandise sold to lower margin categories.

21

Selling, General and Administrative Expenses

SG&A was $2.951 billion or 25.7% of net sales in fiscal 2013, $2.751 billion or 25.2% of net sales in fiscal 2012 and $2.363 billion or 24.9% of net sales in fiscal 2011. The increase in SG&A between fiscal 2013 and 2012 as a percentage of net sales was primarily due to higher technology expenses and depreciation and a relative increase in payroll and payroll-related items (including salaries, workers' compensation and medical insurance). The inclusion of the financial results of the acquisitions for the periods prior to each of their one year anniversaries, which occurred in the first half of fiscal 2013, also contributed to the increase in SG&A as a percentage of net sales. The increase in SG&A between fiscal 2012 and 2011 as a percentage of net sales was primarily due to a relative increase in advertising expenses. As a percentage of net sales, the relative increase in advertising expenses was higher due to the inclusion of the financial results of the acquisitions completed in fiscal 2012. In addition, the fifty-third week has relatively higher SG&A than the year to date fifty-two weeks and increased SG&A by approximately 10 basis points.

Operating Profit

Operating profit for fiscal 2013 was $1.615 billion or 14.0% of net sales, $1.638 billion or 15.0% of net sales in fiscal 2012 and $1.568 billion or 16.5% of net sales in fiscal 2011. The changes in operating profit as a percentage of net sales between fiscal 2013 and 2012 and between fiscal 2012 and 2011 were the result of the changes in gross profit margin and SG&A as a percentage of net sales as described above.

Interest (Expense) Income

Interest expense was $1.1 million and $4.2 million in fiscal 2013 and fiscal 2012, respectively and interest income was $1.1 million in fiscal 2011. Interest expense for fiscal 2012 increased from fiscal 2011 primarily due to the inclusion of interest expense related to the sale/leaseback obligations on the distribution facilities acquired as part of the fiscal 2012 acquisitions.

Income Taxes

The effective tax rate was 36.6% for fiscal 2013, 36.5% for fiscal 2012 and 37.0% for fiscal 2011. For fiscal 2013 and fiscal 2012, the tax rate included a net benefit of approximately $20.0 million and $26.7 million, respectively, primarily due to the recognition of favorable discrete state tax items. For fiscal 2011, the tax rate included an approximate $20.7 million net benefit primarily due to the settlement of certain discrete tax items from on-going examinations, the recognition of favorable discrete state tax items and from changing the blended state tax rate of deferred income taxes.

The Company expects continued volatility in the effective tax rate from year to year because the Company is required each year to determine whether new information changes the assessment of both the probability that a tax position will effectively be sustained and the appropriateness of the amount of recognized benefit.

EXPANSION PROGRAM

The Company is engaged in an ongoing expansion program involving the opening of new stores in both new and existing markets, the expansion or renovation of existing stores, the repositioning of stores within markets when appropriate, the evolution of its omnichannel shopping environment and the continuous review of strategic acquisitions.

In the 22-year period from the beginning of fiscal 1992 to the end of fiscal 2013, the chain has grown from 34 to 1,496 stores plus its various websites, other interactive platforms and distribution facilities. Total store square footage grew from approximately 0.9 million square feet at the beginning of fiscal 1992 to approximately 42.6 million square feet at the end of fiscal 2013. During fiscal 2013, the Company opened a total of 33 new stores. In addition, the Company continued to optimize its operations in a number of trade areas through renovating and repositioning stores in various markets, which included the closing of eight stores. In fiscal 2013, consolidated store space, net of openings and closings for all concepts, increased by 0.6 million square feet. Additionally, the Company is a partner in a joint venture which opened one store during fiscal 2013 and as of March 1, 2014, operated a total of four retail stores in Mexico under the name Bed Bath & Beyond.

22

During fiscal 2012, the Company acquired Linen Holdings and Cost Plus World Market.

The Company plans to continue to expand its operations and invest in its infrastructure to reach its long term objectives. In fiscal 2014, the Company expects to open approximately 30 new stores company-wide and will continue to renovate stores or reposition stores within various markets, when appropriate. Additionally, the Company will continue to place health and beauty care offerings in selected stores as well as specialty food and beverage departments in selected BBB stores. The continued growth of the Company is dependent, in part, upon the Company's ability to execute its expansion program successfully. Additionally, during fiscal 2014, the Company plans to enhance its omnichannel capabilities by continuing to add new functionality and assortment to its selling websites, mobile sites and applications; furthering the development work necessary for a new and more robust point of sale system; continuing the deployment of systems and equipment to allow the Company's stores to take advantage of new technologies and processes; continuing to strengthen its information technology, analytics, marketing and e-commerce groups and opening an additional distribution facility for both direct to customer and store fulfillment.

LIQUIDITY AND CAPITAL RESOURCES

The Company has been able to finance its operations, including its expansion program, entirely through internally generated funds. For fiscal 2014, the Company believes that it can continue to finance its operations, including its expansion program, share repurchase program and planned capital expenditures, entirely through existing and internally generated funds. Capital expenditures for fiscal 2014, principally for information technology enhancements, including omnichannel capabilities, new stores, existing store improvements, and other projects are planned to be approximately $350 million, subject to the timing and composition of the projects. In addition, the Company periodically reviews its alternatives with respect to optimizing its capital structure.

Fiscal 2013 compared to Fiscal 2012

Net cash provided by operating activities in fiscal 2013 was $1.383 billion, compared with $1.193 billion in fiscal 2012. Year over year, the Company experienced an increase in cash provided by the net components of working capital (primarily merchandise inventories, accounts payable and other current assets) and an increase in net earnings, as adjusted for non-cash expenses (primarily depreciation).

Retail inventory at cost per square foot was $59.68 as of March 1, 2014, as compared to $58.12 as of March 2, 2013.

Net cash used in investing activities in fiscal 2013 was $359.8 million, compared with $665.8 million in fiscal 2012. In fiscal 2013, net cash used in investing activities was primarily due to $317.2 million of capital expenditures and $39.1 million of purchases of investment securities, net of redemptions. In fiscal 2012, net cash used in investing activities was due to payments, net of cash acquired, of $643.1 million related to the Cost Plus World Market and Linen Holdings acquisitions, $314.7 million for capital expenditures and $40.0 million for the acquisition of trademarks, partially offset by redemptions of $332.0 million of investment securities, net of purchases.

Net cash used in financing activities for fiscal 2013 was $1.222 billion, compared with $965.4 million in fiscal 2012. The increase in net cash used was primarily due to an increase in common stock repurchases of $282.7 million, partially offset by a $25.5 million payment in the prior year for a credit facility assumed in connection with an acquisition.

23

Fiscal 2012 compared to Fiscal 2011

Net cash provided by operating activities in fiscal 2012 was $1.193 billion, compared with $1.225 billion in fiscal 2011. Year over year, the Company experienced an increase in cash used by the net components of working capital (primarily merchandise inventories, other current assets and accrued expenses and other current liabilities, partially offset by accounts payable and income taxes payable) and an increase in net earnings.

Retail inventory at cost per square foot was $58.12 as of March 2, 2013, as compared to $57.35 as of February 25, 2012.

Net cash used in investing activities in fiscal 2012 was $665.8 million, compared with $364.0 million in fiscal 2011. In fiscal 2012, net cash used in investing activities was due to payments, net of cash acquired, of $643.1 million related to the Cost Plus World Market and Linen Holdings acquisitions, $314.7 million for capital expenditures and $40.0 million for the acquisition of trademarks, partially offset by redemptions of $332.0 million of investment securities, net of purchases. In fiscal 2011, net cash used in investing activities was due to $243.4 million of capital expenditures and $120.6 million of purchases of investment securities, net of redemptions.

Net cash used in financing activities for fiscal 2012 was $965.4 million, compared with $1.042 billion in fiscal 2011. The decrease in net cash used was primarily due to a decrease in common stock repurchases of $216.7 million, partially offset by a $114.7 million decrease in cash proceeds from the exercise of stock options and a $25.5 million payment for a credit facility assumed in acquisition.

Auction Rate Securities

As of March 1, 2014, the Company held approximately $47.7 million of net investments in auction rate securities. Beginning in mid-February 2008, the auction process for the Company's auction rate securities failed and continues to fail. These failed auctions result in a lack of liquidity in the securities but do not affect the underlying collateral of the securities. All of these investments carry triple-A credit ratings from one or more of the major credit rating agencies. As of March 1, 2014, these securities had a temporary valuation adjustment of approximately $3.3 million to reflect their current lack of liquidity. Since this valuation adjustment is deemed to be temporary, it was recorded in accumulated other comprehensive loss, net of a related tax benefit, and did not affect the Company's net earnings for fiscal 2013. The Company will continue to monitor the market for these securities and will expense any permanent changes to the value of the remaining securities, if any, as they occur.

The Company does not anticipate that any continuing lack of liquidity in its auction rate securities will affect its ability to finance its operations, including its expansion program, share repurchase program, and planned capital expenditures. The Company continues to monitor efforts by the financial markets to find alternative means for restoring the liquidity of these investments. These investments will remain primarily classified as non-current assets until the Company has better visibility as to when their liquidity will be restored. The classification and valuation of these securities will continue to be reviewed quarterly.

Other Fiscal 2013 Information

At March 1, 2014, the Company maintained two uncommitted lines of credit of $100 million each, with expiration dates of September 2, 2014 and February 28, 2015, respectively. These uncommitted lines of credit are currently and are expected to be used for letters of credit in the ordinary course of business. During fiscal 2013, the Company did not have any direct borrowings under the uncommitted lines of credit. As of March 1, 2014, there was approximately $4.5 million of outstanding letters of credit. Although no assurances can be provided, the Company intends to renew both uncommitted lines of credit before the respective expiration dates. In addition, as of March 1, 2014, the Company maintained unsecured standby letters of credit of $74.3 million, primarily for certain insurance programs.

24

Between December 2004 and December 2012, the Company's Board of Directors authorized, through share repurchase programs, the repurchase of $7.450 billion of the Company's common stock.

Since 2004 through the end of fiscal 2013, the Company has repurchased approximately $6.3 billion of its common stock through share repurchase programs. The Company has approximately $1.1 billion remaining of authorized share repurchases as of March 1, 2014. The execution of the Company's share repurchase program will consider current business and market conditions.

The Company has authorization to make repurchases from time to time in the open market or through other parameters approved by the Board of Directors pursuant to existing rules and regulations.

The Company has contractual obligations consisting mainly of operating leases for stores, offices, distribution facilities and equipment, purchase obligations, long-term sale/leaseback and capital lease obligations and other long-term liabilities which the Company is obligated to pay as of March 1, 2014 as follows:

(in thousands) | Total | Less than 1 year | 1-3 years | 4-5 years | After 5 years | |||||||||||||||

Operating lease obligations (1) | $ | 3,249,546 | $ | 563,973 | $ | 974,162 | $ | 713,392 | $ | 998,019 | ||||||||||

Purchase obligations (2) | 1,118,369 | 1,118,369 | - | - | - | |||||||||||||||

Long-term sale/leaseback and capital lease obligations (3) | 342,386 | 9,827 | 19,787 | 20,014 | 292,758 | |||||||||||||||

Other long-term liabilities (4) | 466,741 | - | - | - | - | |||||||||||||||

Total Contractual Obligations | $ | 5,177,042 | $ | 1,692,169 | $ | 993,949 | $ | 733,406 | $ | 1,290,777 | ||||||||||

(1) The amounts presented represent the future minimum lease payments under non-cancelable operating leases. In addition to minimum rent, certain of the Company's leases require the payment of additional costs for insurance, maintenance and other costs. These additional amounts are not included in the table of contractual commitments as the timing and/or amounts of such payments are not known. As of March 1, 2014, the Company has leased sites for 21 locations planned for opening in fiscal 2014 or 2015, for which aggregate minimum rental payments over the term of the leases are approximately $76.5 million and are included in the table above.

(2) Purchase obligations primarily consist of purchase orders for merchandise.

(3) Long-term sale/leaseback and capital lease obligations represent future minimum lease payments under the sale/leaseback agreements and capital lease agreements.

(4) Other long-term liabilities are primarily comprised of income taxes payable, deferred rent, workers' compensation and general liability reserves and various other accruals and are recorded as Deferred Rent and Other Liabilities and Income Taxes Payable in the Consolidated Balance Sheet as of March 1, 2014. The amounts associated with these other long-term liabilities have been reflected only in the Total Column in the table above as the timing and/or amount of any cash payment is uncertain.

SEASONALITY

The Company's sales exhibit seasonality with sales levels generally higher in the calendar months of August, November and December, and generally lower in February.

25

INFLATION

The Company does not believe that its operating results have been materially affected by inflation during the past year. There can be no assurance, however, that the Company's operating results will not be affected by inflation in the future.

CRITICAL ACCOUNTING POLICIES