UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

☒ | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2016.

☐ | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-21898

ARROWHEAD PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

Delaware |

| 46-0408024 |

(State of incorporation) |

| (I.R.S. Employer Identification No.) |

225 S. Lake Avenue, Suite 1050

Pasadena, California 91101

(626) 304-3400

(Address and telephone number of principal executive offices)

Securities registered under Section 12(b) of the Exchange Act:

Title of each class |

| Name of each exchange on which registered |

Common Stock, $0.001 par value |

| The NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Exchange Act:

None

Indicate by a check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by a check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ |

| Accelerated filer ☒ |

| Non-accelerated filer ☐ |

| Smaller Reporting Company ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

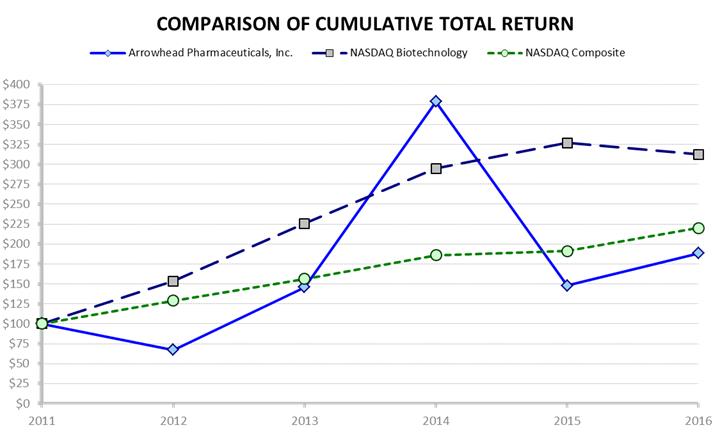

The aggregate market value of issuer's voting and non-voting outstanding Common Stock held by non-affiliates was approximately $290 million based upon the closing stock price of issuer's Common Stock on March 31, 2016. Shares of common stock held by each officer and director and by each person who is known to own 10% or more of the outstanding Common Stock have been excluded in that such persons may be deemed to be affiliates of the Company. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of December 12, 2016, 74,173,484 shares of the issuer's Common Stock were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Definitive Proxy Statement to be filed for Arrowhead Pharmaceuticals Inc.'s 2016 Annual Meeting of Stockholders are incorporated by reference into Part III hereof.

PART I |

|

|

|

|

|

|

| ||

I TEM 1. |

| B USINESS |

| 1 |

I TEM 1A. |

| R ISK F ACTORS |

| 24 |

I TEM 1B. |

| U NRESOLVED S TAFF C OMMENTS |

| 34 |

I TEM 2. |

| P ROPERTIES |

| 35 |

I TEM 3. |

| L EGAL P ROCEEDINGS |

| 35 |

I TEM 4. |

| M INE S AFETY D ISCLOSURES |

| 35 |

|

|

| ||

PART II |

|

|

|

|

|

|

| ||

I TEM 5. |

| M ARKET FOR THE R EGISTRANT ' S C OMMON E QUITY , R ELATED S TOCKHOLDER M ATTERS AND I SSUER P URCHASES OF E QUITY S ECURITIES |

| 35 |

I TEM 6. |

| S ELECTED F INANCIAL D ATA |

| 37 |

I TEM 7. |

| M ANAGEMENT ' S D ISCUSSION AND A NALYSIS OF F INANCIAL C ONDITION AND R ESULTS OF O PERATIONS |

| 38 |

I TEM 7A. |

| Q UANTITATIVE AND Q UALITATIVE D ISCLOSURES A BOUT M ARKET R ISK |

| 53 |

I TEM 8. |

| F INANCIAL S TATEMENTS AND S UPPLEMENTARY D ATA |

| 53 |

I TEM 9. |

| C HANGES IN AND D ISAGREEMENTS WITH A CCOUNTANTS ON A CCOUNTING AND F INANCIAL D ISCLOSURE |

| 53 |

I TEM 9A. |

| C ONTROLS AND P ROCEDURES |

| 53 |

I TEM 9B. |

| O THER I NFORMATION |

| 54 |

|

|

| ||

PART III |

|

|

|

|

|

|

| ||

I TEM 10. |

| D IRECTORS , E XECUTIVE O FFICERS , AND C ORPORATE G OVERNANCE |

| 54 |

I TEM 11. |

| E XECUTIVE C OMPENSATION |

| 54 |

I TEM 12. |

| S ECURITY O WNERSHIP OF C ERTAIN B ENEFICIAL O WNERS AND M ANAGEMENT AND R ELATED S TOCKHOLDERS |

| 54 |

I TEM 13. |

| C ERTAIN R ELATIONSHIPS , R ELATED T RANSACTIONS AND D IRECTORS I NDEPENDENCE |

| 54 |

I TEM 14. |

| P RINCIPAL A CCOUNTANT F EES AND S ERVICES |

| 54 |

|

|

| ||

PART IV |

|

|

|

|

|

|

| ||

I TEM 15. |

| E XHIBITS AND F INANCIAL S TATEMENT S CHEDULES |

| 54 |

|

| |||

SIGNATURE |

| 58 | ||

|

| |||

INDEX TO FINANCIAL STATEMENTS AND SCHEDULES |

| F-1 | ||

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, and we intend that such forward-looking statements be subject to the safe harbors created thereby. For this purpose, any statements contained in this Annual Report on Form 10-K except for historical information may be deemed to be forward-looking statements. Without limiting the generality of the foregoing, words such as "may," "will," "expect," "believe," "anticipate," "intend," "could," "estimate," or "continue" or the negative or other variations thereof or comparable terminology are intended to identify forward-looking statements. In addition, any statements that refer to projections of our future financial performance, trends in our businesses, or other characterizations of future events or circumstances are forward-looking statements.

The forward-looking statements included herein are based on current expectations of our management based on available information and involve a number of risks and uncertainties, all of which are difficult or impossible to predict accurately and many of which are beyond our control. As such, our actual results may differ significantly from those expressed in any forward-looking statements. Factors that may cause or contribute to such differences include, but are not limited to, those discussed in more detail in Item 1 (Business) and Item 1A (Risk Factors) of Part I and Item 7 (Management's Discussion and Analysis of Financial Condition and Results of Operations) of Part II of this Annual Report on Form 10-K. Readers should carefully review these risks, as well as the additional risks described in other documents we file from time to time with the Securities and Exchange Commission. In light of the significant risks and uncertainties inherent in the forward-looking information included herein, the inclusion of such information should not be regarded as a representation by us or any other person that such results will be achieved, and readers are cautioned not to place undue reliance on such forward-looking information. Except as may be required by law, we disclaim any intent to revise the forward-looking statements contained herein to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

PART I

Unless otherwise noted, (1) the term "Arrowhead" refers to Arrowhead Pharmaceuticals, Inc., a Delaware corporation formerly known as Arrowhead Research Corporation and its Subsidiaries, (2) the terms "Company," "we," "us," and "our," refer to the ongoing business operations of Arrowhead and its Subsidiaries, whether conducted through Arrowhead or a subsidiary of Arrowhead, (3) the term "Subsidiaries" refers collectively to Arrowhead Madison Inc. ("Arrowhead Madison"), Arrowhead Australia Pty Ltd ("Arrowhead Australia") and Ablaris Therapeutics, Inc. ("Ablaris"), (4) the term "Common Stock" refers to Arrowhead's Common Stock, (5) the term "Preferred Stock" refers to Arrowhead's Preferred Stock and (6) the term "Stockholder(s)" refers to the holders of Arrowhead Common Stock.

ITEM 1 . | BUSINESS |

Description of Business

Arrowhead develops medicines that treat intractable diseases by silencing the genes that cause them. Using a broad portfolio of RNA chemistries and efficient modes of delivery, Arrowhead therapies trigger the RNA interference mechanism to induce rapid, deep and durable knockdown of target genes. RNA interference, or RNAi, is a mechanism present in living cells that inhibits the expression of a specific gene, thereby affecting the production of a specific protein. Deemed to be one of the most important recent discoveries in life science with the potential to transform medicine, the discoverers of RNAi were awarded a Nobel Prize in 2006 for their work. Arrowhead's RNAi-based therapeutics leverage this natural pathway of gene silencing.

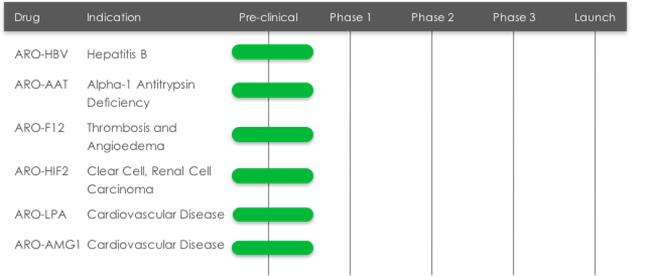

Pre-clinical Stage Drug Candidates

| • | Subcutaneous: |

| • | ARO-HBV is being developed to treat chronic hepatitis B virus infection by reducing the expression and release of new viral particles and key viral proteins with the goal of achieving a functional cure. |

| • | ARO-AAT is being developed to treat liver disease associated with alpha-1 antitrypsin deficiency (AATD), a rare genetic disease that can severely damage the liver and lungs of affected individuals. The goal of treatment with ARO- AAT is to reduce the production of the mutant Z-AAT protein to prevent and potentially reverse accumulation-related liver injury and fibrosis. |

| • | ARO-LPA is designed to reduce production of apolipoprotein A, a key component of lipoprotein(a), which has been genetically linked with increased risk of cardiovascular diseases, independent of cholesterol and LDL levels. Amgen, Inc. ("Amgen") acquired a worldwide, exclusive license in September 2016 to develop and commercialize ARO-LPA. |

| • | ARO-AMG1 is being developed against an undisclosed genetically validated cardiovascular target under a license and collaboration agreement with Amgen. |

| • | ARO-F12 is in preclinical development as a potential treatment for factor 12 (F12) mediated diseases such as hereditary angioedema (HAE) and thromboembolic disorders. Factor 12 initiates the intrinsic coagulation pathway, and reducing its production using Arrowhead's RNAi technology may present opportunities in both disease areas. |

| • | Extra-Hepatic: |

| • | ARO-HIF2 is being developed as a new drug candidate for the treatment of clear cell renal cell carcinoma (ccRCC). ARO-HIF2 is designed to inhibit the production of HIF-2α, which has been linked to tumor progression and metastasis in ccRCC. Arrowhead believes it is an attractive target for intervention because over 90% of ccRCC tumors express a mutant form of the Von Hippel-Landau protein that is unable to degrade HIF-2α, leading to its accumulation during tumor hypoxia and promoting tumor growth. ARO-HIF2 is Arrowhead's first drug candidate using a new delivery vehicle designed to target tissues outside of the liver. |

1

Recent Events

Arrowhead made announcements throughout fiscal 2016 discussing progress towards the company's goals as well as key developments. The following are highlights of those developments:

| • | Discontinued development of ARC-520, ARC-521 and ARC-AAT in November 2016 |

| • | The Company announced that it would be discontinuing these clinical programs, which utilized the intravenously administered DPC iv , or EX1, delivery vehicle, and redeploying its resources and focus toward utilizing the Company's new proprietary subcutaneous and extra-hepatic delivery systems. |

| • | The decision to discontinue development of EX1-containing programs was based primarily on two factors. |

| ▪ | During ongoing discussions with regulatory agencies and outside experts, it became apparent that there would be substantial delays in all clinical programs that utilize EX1, while the Company further explored the cause of deaths in a non-clinical toxicology study in non-human primates exploring doses of EX1 higher than those planned to be used in humans. |

| ▪ | The Company has made substantial advances in RNA chemistry and targeting resulting in large potency gains for subcutaneous administered and extra-hepatic RNAi-based development programs. |

| • | Because of the discontinuation of its existing clinical programs, the Company also reduced its workforce by approximately 30%, while maintaining resources necessary to support current and potential partner-based programs and the Company's pipeline. |

| • | Entered into two collaboration and license agreements with Amgen, Inc. ("Amgen") |

| • | Total deal value of up to $673.5 million |

| • | Arrowhead received $56.5 million upfront: |

| ▪ | $35 million in upfront cash payments, $21.5 million equity investment |

| • | Up to low double-digit royalties for ARO-LPA and single-digit royalties for the undisclosed target, ARO- AMG1 |

| • | Amgen receives: |

| ▪ | Exclusive license to ARO-LPA program |

| ▪ | Option for an additional candidate against an undisclosed target, ARO-AMG1 |

| • | Amgen will be wholly responsible for funding and conducting all clinical development and commercialization |

| • | Continued progress on preclinical candidates including ARO-HBV, ARO-AAT, ARO-F12, ARO-LPA and ARO-HIF2 |

| • | Regarding ARO-F12 and ARO-LPA: |

| ▪ | Presented preclinical data at the American Heart Association's Scientific Sessions 2016 for two development programs using Arrowhead's proprietary subcutaneous delivery platform: |

| ▪ | RNAi triggers against Factor 12 (F12) showed dose dependent reductions in serum F12 |

| ▪ | A statistically significant reduction (p=0.002) in thrombus weight was observed at greater than 95% F12 knockdown in a rat arterio-venous shunt model |

2

| ▪ | There was no increased bleeding risk in AR O - F12 -treated mice, even with greater than 99% knockdown of F12 levels |

| ▪ | RNAi triggers against Lipoprotein (a) [Lp(a)] led to greater than 98% maximum knockdown after a single 3 mg/kg SQ dose in Transgenic mice |

| ▪ | In an atherosclerosis model, data suggest that RNAi triggers can be effectively delivered to a fatty liver using the subcutaneous delivery platform |

| • | Regarding ARO-HIF2 |

| ▪ | Presented preclinical data showing that ARO-HIF2 inhibited renal cell carcinoma growth and promoted tumor cell death in its preclinical studies. |

| • | Strengthened the Company's balance sheet with August 2016 private offering and Amgen agreement upfronts |

| • | In August 2016, the Company sold 7.6 million shares of Common Stock to certain institutional investors and received net proceeds of approximately $43.2 million. |

| • | As part of the collaboration and license agreements as well as a Common Stock Purchase Agreement with Amgen, $14 million of the total $56.5 million upfront cash payments and equity investments were received in September 2016, and the remaining $42.5 million was received in November 2016. |

| • | Continued progress of on former drug candidates prior to the discontinuations |

| • | Presented preclinical and clinical data on former drug candidate ARC-AAT at the Liver Meeting |

| • | In a first-in-human clinical study, ARC-AAT was well tolerated and induced deep and durable reduction of the target AAT protein |

| • | The preclinical data suggest a possible improvement of liver health and arrest of further damage from treatment with ARC-AAT |

| • | Advanced former drug candidate ARC-521 into a Phase 1/2 study |

| • | Conducted multiple dose and combination studies of former drug candidate ARC-520 |

Acquisition of Roche and Novartis RNAi assets

The last five years have brought substantial change to Arrowhead's research and development (R&D) capabilities and strategy. We are now an integrated RNAi therapeutics company, developing novel drugs that silence disease-causing genes based on our broad RNAi technology platform.

The most significant step in this transition was our 2011 acquisition of the RNAi therapeutics business of Hoffmann-La Roche, Inc. and F. Hoffmann-La Roche Ltd. (collectively, "Roche"). Roche built this business unit in a manner that only a large pharmaceutical company is capable of: backed by expansive capital resources, Roche systematically acquired technologies, licensed expansive intellectual property rights, attracted leading scientists, and developed new technologies internally. At a time when the markets were questioning whether RNAi could become a viable therapeutic modality, we saw great promise in the technology broadly and the quality of what Roche built specifically. The acquisition provided us with two primary sources of value:

| • | Broad freedom to operate with respect to key patents directed to the primary RNAi-trigger formats: canonical, UNA, meroduplex, and dicer substrate structures; and |

| • | A large team of scientists experienced in RNAi and oligonucleotide delivery. |

3

In addition, in March 2015 we acquired the entire RNAi research and development portfolio and associated assets of Novartis. Novartis had been working in the R NAi field for over a decade and made some very important advancements in their developments of proprietary oligonucleotide formatting and modifications . Key aspects of the acquisition include the following:

| • | Multiple patent families covering RNAi-trigger design rules and modifications that fall outside of key patents controlled by competitors, which we believe provides freedom to operate for any target and indication; |

| • | Novel intracellular targeting ligands that enhance the activity of RNAi-triggers by targeting the RNA-induced silencing complex (RISC) more effectively and improving stability once RISC is loaded; |

| • | An assignment of Novartis' license from Alnylam Pharmaceuticals, Inc. ("Alnylam") granting Arrowhead access to certain Alnylam intellectual property, excluding delivery, for 30 gene targets; and |

| • | A pipeline of three candidates initiated by Novartis for which Novartis has developed varying amounts of preclinical data. |

We see the Roche and Novartis acquisitions as a powerful combination of intellectual property, R&D infrastructure, and RNAi delivery experts. We believe we are the only company with access to all primary RNAi-trigger structures now including additional novel structures discovered by Novartis. This enables us to optimize our drug candidates on a target-by-target basis and use the structure and modifications that yield the most potent RNAi trigger. Our R&D team and facility enable rapid innovation and drive to the clinic.

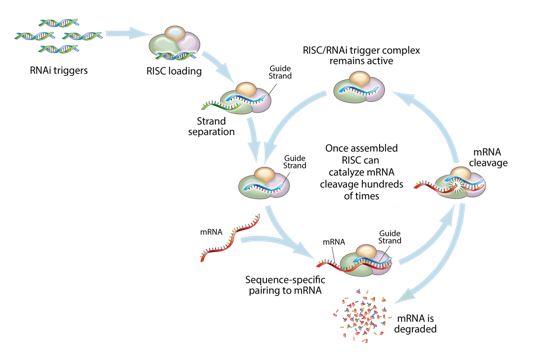

RNA Interference & the Benefits of RNAi Therapeutics

RNA interference (RNAi) is a mechanism present in living cells that inhibits the expression of a specific gene, thereby affecting the production of a specific protein. Deemed to be one of the most important recent discoveries in life science with the potential to transform medicine, the discoverers of RNAi were awarded a Nobel Prize in 2006 for their work. RNAi-based therapeutics may leverage this natural pathway of gene silencing to target and shut down specific disease-causing genes.

Figure 1: Mechanism of RNA interference

Small molecule and antibody drugs have proven effective at inhibiting certain cell surface, intracellular, and extracellular targets. However, other drug targets such as intranuclear genes and some proteins have proven difficult to inhibit with traditional drug-based and biologic therapeutics. Developing effective drugs for these targets would have the potential to address large underserved

4

marke ts for the treatment of many diseases. Using the ability to specifically silence any gene, RNAi therapeutics may be able to address previously "undruggable" targets, unlocking the market potential of such targets.

Advantages of RNAi as a Therapeutic Modality

| • | Silences the expression of disease causing genes; |

| • | Potential to address any target in the transcriptome including previously "undruggable" targets; |

| • | Rapid lead identification; |

| • | High specificity; |

| • | Opportunity to use multiple RNA sequences in one drug product for synergistic silencing of related targets; and |

RNAi therapeutics are uniquely suited for personalized medicine through target and cell specific delivery and gene knockdown.

Pipeline Overview

Arrowhead is focused on developing innovative drugs for diseases with a genetic basis, characterized by the overproduction of one or more proteins. The depth and versatility of our RNAi technologies enable us to address conditions in virtually any therapeutic area and pursue disease targets that are not otherwise druggable by small molecules and biologics. Our preclinical pipeline of RNAi therapeutics includes both subcutaneously administered liver-targeted candidates and extra-hepatic candidates.

Internal Programs

Hepatitis B Virus Infection

We see the need for a next generation HBV treatment with a finite treatment period and an attractive dosing regimen, and that can be used at earlier stages of disease. We believe a novel therapeutic approach that can effectively treat or provide a functional cure (seroclearance of HBsAg and with or without development of excess patient antibodies against HBsAg) has the potential to take significant market share and may expand the available market to include patients that are currently untreated.

Chronic Hepatitis B Virus

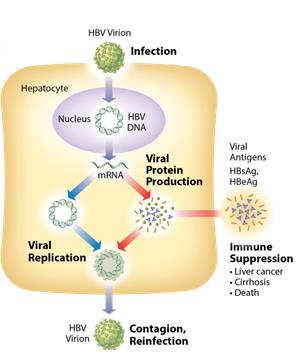

According to the World Health Organization, 240 million people worldwide are chronically infected with hepatitis B virus, of which 500,000 to 1,000,000 people die each year from HBV-related liver disease. Chronic HBV infection is defined by the presence of hepatitis B surface antigen (HBsAg) for more than six months. In the immune tolerant phase of chronic infection, which can last for many years, the infected person typically produces very high levels of viral DNA and viral antigens. However, the infection is not cytotoxic and the carrier may have no symptoms of illness. Over time, the ongoing production of viral antigens causes inflammation

5

and necrosis, leading to elevation of liver enzymes such as alanine and aspartate transaminases, hepa titis, fibrosis, and liver cancer ( hepatocellular carcinoma, or HCC). If untreated, as many as 25% to 40% of chronic HBV carriers ultimately develop cirrhosis or HCC. Antiviral therapy is generally prescribed when liver enzymes become elevated.

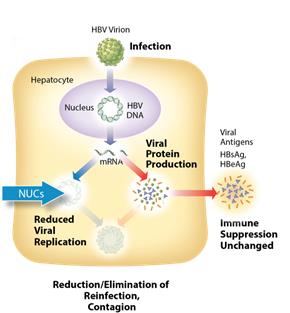

Current Treatments

The current standard of care for treatment of chronic HBV infection is a daily oral dose of nucleotide/nucleoside analogs (NUCs) or a regimen of interferon injections for approximately one year. NUCs are generally well tolerated, but patients may need lifetime treatment because viral replication often rebounds upon cessation of treatment. Interferon therapeutics can result in a functional cure in 10-20% of some patient types, but treatment is often associated with significant side effects, including severe flu-like symptoms, marrow suppression, and autoimmune disorders.

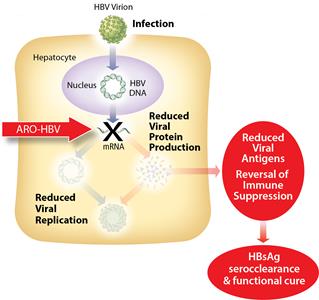

ARO-HBV

ARO-HBV is an RNAi therapeutic candidate for the treatment of chronic hepatitis B infection with the goal of achieving a functional cure. This is a next-generation subcutaneously administered compound that follows previous generation HBV compounds ARC-520 and ARC-521, which were in Phase 2b and Phase 1/2 studies respectively when development was discontinued in November 2016.

Goal of ARO-HBV Treatment

ARO-HBV is designed to silence the production of all HBV gene products with the goal of achieving a functional cure. The siRNAs target multiple components of HBV production including the pregenomic RNA that would be reverse transcribed to generate the viral DNA. The siRNAs intervene at the mRNA level, upstream of where NUCs act, and target the mRNAs that produce HBsAg proteins, the viral polymerase, the core protein that forms the capsid, the pre-genomic RNA, the HBeAg, and the hepatitis B X antigen (HBxAg). NUCs are effective at reducing production of viral particles, but are ineffective at controlling production of HBsAg and other HBV gene products. Arrowhead believes that a reduction in the production of HBsAg and other proteins that NUCs are ineffective at controlling is necessary to effective HBV therapy, because those proteins are thought to be major contributors to repression of the immune system and the persistence of liver disease secondary to HBV infection.

Figure 1: Chronic HBV mechanism untreated

6

Figure 2: Mechanism of action NUCs

Figure 3: Mechanism of action ARO-HBV

Alpha-1 Antitrypsin Deficiency (AATD)

AATD is a genetic disorder associated with liver disease in children and adults, and pulmonary disease in adults. AAT is a circulating glycoprotein protease inhibitor that is primarily synthesized and secreted by liver hepatocytes. Its physiologic function is the inhibition of neutrophil proteases to protect healthy tissues during inflammation and prevent tissue damage. The most common disease variant, the Z mutant, has a single amino acid substitution that results in improper folding of the protein. The mutant protein cannot be effectively secreted and accumulates in globules in the hepatocytes. This triggers continuous hepatocyte injury, leading to fibrosis, cirrhosis, and increased risk of hepatocellular carcinoma.

Current Treatments

Individuals with the homozygous PiZZ genotype have severe deficiency of functional AAT leading to pulmonary disease and hepatocyte injury and liver disease. Lung disease is frequently treated with AAT augmentation therapy. However, augmentation therapy does nothing to treat liver disease, and there is no specific therapy for hepatic manifestations. There is a significant unmet need as liver transplant, with its attendant morbidity and mortality, is currently the only available cure.

7

ARO -AAT

Arrowhead is developing a therapeutic candidate (ARO-AAT) for the treatment of liver disease associated with AATD. ARO-AAT is designed to knock down the Alpha-1 antitrypsin (AAT) gene transcript and reduce the hepatic production of the mutant AAT protein. This is a next-generation subcutaneously administered compound that follows previous generation AAT compound ARC-AAT, which was in a Phase 2 study when development was discontinued in November 2016.

Goal of ARO-AAT Treatment

The goal of treatment with ARO-AAT is prevention and potential reversal of Z-AAT accumulation-related liver injury and fibrosis. Reduction of inflammatory Z-AAT protein, which has been clearly defined as the cause of progressive liver disease in AATD patients, is important as it is expected to halt the progression of liver disease and allow fibrotic tissue repair.

The Alpha-1 Project

Arrowhead has an agreement with The Alpha-1 Project (TAP), the venture philanthropy subsidiary of the Alpha-1 Foundation. TAP's mission is to support organizations in pursuit of cures and therapies for lung and liver disease caused by AATD. Under the terms of the agreement, TAP has partially funded development of ARO-AAT. In addition to the funding, TAP will make its scientific advisors available to Arrowhead, assist with patient recruitment for clinical trials with its Alpha-1 Foundation Patient Research Registry, and engage in other collaborative efforts that support development of ARO-AAT.

ARO-F12

ARO-F12 is an RNAi-based therapeutic designed to reduce the production of factor 12 with the goal of providing a prophylactic treatment for hereditary angioedema (HAE) and thromboembolic diseases. Arrowhead is conducting relevant disease models and is considering other potential studies to support advancement of ARO-F12 into clinical trials.

ARO-HIF2

ARO-HIF2 is an RNAi-based therapeutic designed to reduce the production of hypoxia-inducible factor 2α (HIF-2α) to treat clear cell renal cell carcinoma. It is the first drug candidate using a new delivery vehicle designed to target tissues outside of the liver.

Partner-based Programs

ARO-LPA and ARO-AMG1

ARO-LPA is designed to reduce production of apolipoprotein A, a key component of lipoprotein(a), which has been genetically linked with increased risk of cardiovascular diseases, independent of cholesterol and LDL levels. Amgen acquired a worldwide, exclusive license in September 2016 to develop and commercialize ARO-LPA.

ARO-AMG1 is being developed against an undisclosed genetically-validated cardiovascular target under a license and collaboration agreement with Amgen.

Under the terms of the agreements taken together for ARO-LPA and ARO-AMG1, the Company will receive $35 million in upfront payments, $21.5 million in the form of an equity investment by Amgen in the Company's Common Stock, and the Company is eligible to receive up to $617 million in option payments and development, regulatory and sales milestone payments. The Company is further eligible to receive single-digit royalties for sales of products under the ARO-AMG1 agreement and up to low double-digit royalties for sales of products under the ARO-LPA agreement.

Intellectual Property and Key Agreements

The Company controls approximately 359 issued patents (including 70 for DPCs; 23 for hydrodynamic gene delivery; 23 for pH labile molecules; 6 for protease cleavable molecules; 7 for polyampholyte; (expired) 18 for delivery polymers; 163 for RNAi trigger molecules; 4 for targeting molecules; 1 for liver expression vector; and 29 for Homing Peptides), including European validations, and 256 patent applications (117 applications in 22 families for DPC-related technologies (includes conjugates, polymers, linkages, etc); 135 applications in 28 families for RNAi trigger targets; and 8 for Homing Peptides). The pending applications have been filed throughout the world, including, in the United States, Argentina, ARIPO (Africa Regional Intellectual Property Organization), Australia, Brazil, Canada, Chile, China, Eurasian Patent Organization, Europe, Hong Kong, Israel, India, Indonesia, Iraq, Jordan, Japan, Republic of Korea, Mexico, New Zealand, OAPI (African Intellectual Property Organization), Peru, Philippines, Russian Federation, Saudi Arabia, Singapore, Thailand, Taiwan, Venezuela, Vietnam, and South Africa.

8

RNAi Triggers

The Company owns patents directed to RNAi triggers targeted to reduce expression of hepatitis B viral proteins as well the RRM2 gene.

Patent Group | Estimated Year of Expiration |

RNAi Triggers | |

Patents directed to HBV RNAi triggers | 2032, 2036 |

Patent directed to RRM2 RNAi triggers | 2031 |

HIF2α | 2034, 2036 |

AAT | 2035 |

Factor 12 | 2036, 2037 |

LPA | 2036 |

Patents directed to α-ENaC | 2028 |

Patents directed to β-ENaC | 2031 |

β-Catenin | 2033 |

KRAS | 2033 |

Patents directed to HSF1 | 2030, 2032 |

APOC3 | 2035 |

Patents directed to Cx43 | 2029 |

Patents directed to HIF1A | 2026 |

Patents directed to FRP-1 | 2026 |

Patents directed to HCV | 2023 |

Patents directed to PDtype4 | 2026 |

Patents directed to PI4Kinase | 2028 |

Patents directed to HRH1 | 2027 |

Patents directed to SYK | 2027 |

Patents directed to TNF-α | 2027, 2028 |

RNAi agent design (26mer) | 2036 |

RNAi agent design (26mer) | 2037 |

RNAi agent design (5′-cyclo-phosphonate) | 2037 |

9

Dynamic Polyconjugates

The DPC-related patents have issued in the United States, Australia, Canada, Europe, France, Germany, Italy, Spain, Switzerland, United Kingdom, India, Japan, Mexico, New Zealand, Philippines, Russia, South Korea, Singapore, and South Africa. The Company also controls a number of patents directed to hydrodynamic nucleic acid delivery, which issued in the United States, Australia and Europe (validated in Austria, Belgium, Switzerland, Germany, Denmark, Spain, Finland, France, the United Kingdom, Hungary, Ireland, Italy, Netherlands and Sweden). The approximate year of expiration for each of these various groups of patents are set forth below:

Patent Group | Estimated Year of Expiration |

Dynamic Polyconjugates (DPC) | |

Dynamic Polyconjugates | 2027 |

Dynamic Polyconjugates – second iteration | 2031 |

Membrane Active Polymers | 2027 |

Membrane Active Polymers – Additional Iterations | 2024 |

Membrane Active Polymers – Additional Iterations | 2032 |

Membrane Active Polymers – Additional Iterations | 2033 |

Copolymer Systems | 2024 |

Polynucleotide-Polymer Composition | 2024 |

ARC-520 Polymer | 2031 |

ACR-520 manufacture | 2037 |

ARC-521 Composition | 2036 |

Masking Chemistry | 2031 |

Masking Chemistry | 2032 |

Masking Chemistry | 2036 |

Polyampholyte Delivery | 2017 |

pH Labile Molecules | 2020 |

Endosomolytic Polymers | 2020 |

Targeting groups (Gal trimer-PK) | 2031 |

Targeting groups (αvβ3 integrin) | 2035 |

Targeting groups (αvβ6 integrin) | 2037 |

Targeting groups (GalNAc trimer) | 2037 |

Hydrodynamic delivery | |

Second iteration | 2020 |

Third iteration | 2024 |

The RNAi and drug delivery patent landscapes are complex and rapidly evolving. As such, we may need to obtain additional patent licenses prior to commercialization of our candidates. You should review the factors identified in "Risk Factors" in Part I, Item 1A of this Annual Report on Form 10-K.

Homing Peptides

We also control patents related to our Homing Peptide platforms, related to Adipotide, our drug candidate for the treatment for obesity and related metabolic disorders. Approximately seven of these patents are United States patents and the remaining patents are validated in Belgium, Switzerland, Germany, Spain, France, Japan, the United Kingdom, Ireland, Greece, Italy, Netherlands, Portugal, Sweden and Turkey.

Patent Group | Estimated Year of Expiration |

Adipotide ® | |

Targeting moieties and conjugates | 2021 |

Targeted Pharmaceutical Compositions | 2021 |

Homing Peptides | |

EphA5 Targeting Peptides | 2027 |

IL-11R Targeting Peptides | 2022 |

10

Non-Exclusively Licensed Patent Rights obtained from Roche

Roche and the Company entered into a Stock and Asset Purchase Agreement on October 21, 2011, pursuant to which Roche assigned to Arrowhead its entire rights under certain licenses including: the License and Collaboration Agreement between Roche and Alnylam dated July 8, 2007 (the "Alnylam License"); the Non-Exclusive Patent License Agreement between Roche and MDRNA, Inc. dated February 12, 2009 ("MDRNA License"); and the Non-Exclusive License Agreement between Roche and City of Hope dated September 19, 2011 (the "COH License") (Collectively the "RNAi Licenses"). The RNAi Licenses provide the Company with non-exclusive, worldwide, perpetual, irrevocable, royalty-bearing rights and the right to sublicense a broad portfolio of intellectual property relating to the discovery, development, manufacture, characterization, and use of therapeutic products that function through the mechanism of RNA interference for specified targets.

Terms of the 2007 Alnylam License

The Alnylam License provides us with a non-exclusive, worldwide, perpetual, irrevocable, royalty-bearing right and sublicensable license under Alnylam's rights in certain intellectual property existing as of its effective date, to engage in discovery, development, commercialization and manufacturing activities, including to make, have made, use, offer for sale, sell and import certain licensed products in certain fields. The fields include the treatment or prophylaxis of indications comprising an RNAi compound complementary to, and function in mediating the RNAi of, a target known or believed to be primarily implicated in one or more primary therapeutic areas. The primary therapeutic areas are cancer, hepatic, metabolic disease and pulmonary disease. The hepatic therapeutic area specifically excludes targets of infectious pathogen.

The Alnylam License excludes access to intellectual property specifically related to "Blocked Targets." "Blocked Targets" are those targets that are subject to a contractual obligation of a pre-existing agreement between Alnylam and its alliance partners.

Under the Alnylam License, we may be obligated to pay development and sales milestone payments of up to the mid to upper double-digit millions of dollars for each licensed product that progresses through clinical trials in a particular indication, receives marketing approval for that indication and is the subject of a first commercial sale. Additionally, we may be obligated to pay mid to high single-digit percentage royalties on sales of such products.

Core Patents relating to RNAi

The RNAi Licenses include patents relating to the general structure, architecture, and design of double-stranded oligonucleotide molecules, which engage RNA interference mechanisms in a cell. These rights include the "Tuschl II" patents, including issued U.S. Patent Nos. 7,056,704; 7,078,196; 7,078,196; 8,329,463; 8,362,231; 8,372,968; and 8,445,327; "Tuschl I" patents, including U.S. Patent Nos. 8,394,628 and 8,420,391; and allowed "Tuschl I" patent application, U.S. Publication No. 2011024446; "City of Hope" patents, including U.S. Patent No. 8,084,599; and "Kreutzer-Limmer" patents assigned to Alnylam, including U.S. Patent Nos. 7,829,693; 8,101,594; 8,119,608; 8,202,980; and 8,168,776.

Thomas Tuschl is the first named inventor on "Tuschl I" and "Tuschl II." "Tuschl I" patents refers to the patents arising from the patent application entitled "The Uses of 21-23 Sequence-Specific Mediators of Double-Stranded RNA Interference as a Tool to Study Gene Function and as a Gene-Specific Therapeutic." "Tuschl II" patents refer to the patents and patent applications arising from the patent application entitled "RNA Interference Mediating Small RNA Molecules." "City of Hope" is the first named assignee of certain core RNAi trigger patents. The second named assignee of these patents is Integrated DNA Technologies, Inc. Kreutzer-Limmer patents refer to the Alnylam patents and patent applications, relating to core siRNA IP, which includes inventors Roland Kreutzer and Stefan Limmer.

Chemical modifications of double-stranded oligonucleotides

The RNAi Licenses also include patents related to modifications of double-stranded oligonucleotides, including modifications to the base, sugar, or internucleoside linkage, nucleotide mimetics, and end modifications, which do not abolish the RNAi activity of the double-stranded oligonucleotides. Also included are patents relating to modified double-stranded oligonucleotides, such as meroduplexes described in in U.S. Publication No. 20100209487 assigned to Marina Biotech (f/k/a MDRNA, Inc.), and microRNAs described in U.S. Patent Nos. 7,582,744; 7,674,778, and 7,772,387 assigned to Alnylam as well as U.S. Patent No. 8,314,227 related to unlocked nucleic acids (UNA). The ‘227 patent was assigned by Marina Biotech to Arcturus Therapeutics, Inc. but remains part of the MDRNA License. The RNAi Licenses also include rights from INEX/Tekmira relating to lipid-nucleic acid particles, and oligonucleotide modifications to improve pharmacokinetic activity including resistance to degradation, increased stability, and more specific targeting of cells from Alnylam and ISIS Pharmaceuticals, Inc.

11

Manufacturing techniques for the double-stranded oligonucleotide molecules or chemical modifications

The RNAi Licenses also include patents relating to the synthesis and manufacture of double-stranded oligonucleotide molecules for use in RNA interference, as well as chemical modifications of such molecules, as described above. These include methods of synthesizing the double-stranded oligonucleotide molecules such as in the core "Tuschl I" allowed U.S. Application No. 12/897,749, the core "Tuschl II" U.S. Patent Nos. 7,056,704; 7,078,196; and 8,445,327; and Alnylam's U.S. Patent Nos. 8,168,776, as well as methods of making chemical modifications of the double-stranded oligonucleotides such as described in Alnylam's U.S. Patent No. 7,723,509 and INEX's U.S. Patent Nos. 5,976,567; 6,858,224; and 8,484,282. Patent applications are currently pending that further cover manufacturing techniques for double-stranded oligonucleotide molecules or chemical modifications.

Uses and Applications of Double-Stranded Oligonucleotide Molecules or Chemical modifications

The RNAi Licenses also include patents related to uses of the double-stranded oligonucleotides that function through the mechanism of RNA interference. These include for example, the core "Tuschl I" U.S. Patent No. 8,394,628 and "Tuschl II" U.S. Patent No. 8,329,463; Alnylam's U.S. Patent Nos. 7,763,590; 8,101,594, and 8,119,608, and City of Hope‘s U.S. Patent No. 8,084,599. Other more specific uses have been acquired and patent applications are currently pending that cover additional end uses and applications of double-stranded oligonucleotides functioning through RNA interference.

2012 License from Alnylam

In January 2012, we obtained a license from Alnylam under its rights in certain RNAi intellectual property to develop and commercialize RNAi-based products targeting RNAs encoded by the genome of HBV.

Alnylam granted us a worldwide non-exclusive sublicensable royalty bearing license under Alnylam's general RNAi intellectual property estate to research, develop and commercialize RNAi-based products targeting HBV RNAs in combination with DPC technology. Alnylam further granted us a worldwide sublicensable exclusive royalty bearing license under its target-specific RNAi patent rights to research, develop and commercialize RNAi-based products targeting HBV RNAs in combination with DPC technology. Alnylam further agreed to forego the development of any RNAi-based products targeting HBV RNAs in combination with DPC technology.

Under the license from Alnylam, we may be obligated to pay development and sales milestone payments of up to the low double-digit millions of dollars for each licensed product that progresses through clinical trials, receives marketing approval and is the subject of a first commercial sale. Additionally, we may be obligated to pay low single-digit percentage royalties on sales of such products.

2012 License to Alnylam

In consideration for the licenses from Alnylam, in January 2012 we granted Alnylam a worldwide non-exclusive, sublicensable royalty bearing license under our broad and target-specific DPC intellectual property rights to research, develop and commercialize RNAi-based products against a single undisclosed target in combination with DPC technology. Under the license to Alnylam, Alnylam may be obligated to pay us development and sales milestone payments of up to the low double digit millions of dollars for each licensed product that progresses through clinical trials, receives marketing approval and is the subject of a first commercial sale. Additionally, Alnylam may be obligated to pay us low single digit percentage royalties on sales of such products.

Acquisition of Assets from Novartis

On March 3, 2015, the Company entered into an Asset Purchase and Exclusive License Agreement (the "RNAi Purchase Agreement") with Novartis pursuant to which the Company acquired Novartis' RNAi assets and rights thereunder. Pursuant to the RNAi Purchase Agreement, the Company acquired or licensed certain patents and patent applications owned or controlled by Novartis related to RNAi therapeutics, assignment of Novartis's rights under a license from Alnylam (the "Alnylam-Novartis License"), rights to three pre-clinical RNAi candidates, and a license to certain Novartis assets (the "Licensed Novartis Assets"). The patents acquired from Novartis include multiple patent families covering delivery technologies and RNAi-trigger design rules and modifications. The Licensed Novartis Assets include an exclusive, worldwide right and license, solely in the RNAi field, with the right to grant sublicenses through multiple tiers under or with respect to certain patent rights and know how relating to delivery technologies and RNAi-trigger design rules and modifications. Under the assigned Alnylam-Novartis License, the Company has acquired a worldwide, royalty-bearing, exclusive license with limited sublicensing rights to existing and future Alnylam intellectual property (coming under Alnylam's control on or before March 31, 2016), excluding intellectual property concerning delivery technology, to research, develop and commercialize 30 undisclosed gene targets.

12

Cardiovascular Collaboration and License Agreements with Amgen

On September 28, 2016, the Company entered into two Collaboration and License agreements, and a Common Stock Purchase Agreement with Amgen. Under the First Collaboration and License Agreement, Amgen will receive an option to a worldwide, exclusive license for an RNAi therapy for ARO-AMG1 , an undisclosed genetically validated cardiovascular target. Under the Second Collaboration and License, Amgen will receive a worldwide, exclusive license to Arrowhead's novel, RNAi ARO-LPA program. These RNAi molecules are designed to reduce elevated lipoprotein(a), which is a genetically validated, independent risk factor for atherosclerotic cardiovascular disease. In both agreements, Amgen will be wholly responsible for clinical development and commercialization. Under the terms of the agreements taken together, the Company will receive $35 million in upfront payments, $21.5 million in the form of an equity investment by Amgen in the Company's Common Stock, and up to $617 million in option payments and development, regulatory and sales milestone payments. The Company is further eligible to receive single-digit royalties for sales of products under the ARO-AMG1 agreement and up to low double-digit royalties for sales of products under the ARO-LPA agreement.

Research and Development Facility

Arrowhead's research and development operations are located in Madison, Wisconsin. Substantially all of the Company's assets are located either in this facility or in our corporate headquarters in Pasadena. A summary of our research and development resources is provided below:

| • | Approximately 60 scientists currently; |

| • | State-of-the-art laboratories consisting of 61,000 total sq. ft.; |

| • | Complete small animal facility; |

| • | Primate colony housed at the Wisconsin National Primate Research Center, an affiliate of the University of Wisconsin; |

| • | In-house histopathology capabilities; |

| • | Animal models for metabolic, viral, and oncologic diseases; |

| • | Animal efficacy and safety assessment; |

| • | Polymer, peptide, oligonucleotide and small molecule synthesis and analytics capabilities (HPLC, NMR, MS, etc.); |

| • | Polymer, peptide and oligonucleotide PK, biodistribution, clearance methodologies; and |

| • | Conventional and confocal microscopy, flow cytometry, Luminex platform, qRT-PCR, clinical chemistry analytics. |

Research and Development Expenses

Research and development (R&D) expenses consist of costs incurred in discovering, developing and testing our clinical and preclinical candidates and platform technologies. R&D expenses also include costs related to clinical trials, including costs of contract research organizations to recruit patients and manage clinical trials. Other costs associated with clinical trials include manufacturing of clinical supplies, as well as good laboratory practice ("GLP") toxicology studies necessary to support clinical trials, both of which are outsourced to cGMP-compliant manufacturers and GLP-compliant laboratories. Total research and development expense for fiscal 2016 was $41.5 million, a decrease from $47.3 million in 2015 and an increase from $23.1 million in 2014.

At September 30, 2016, we employed approximately 94 employees in an R&D function, primarily working from our facility in Madison, Wisconsin. Due to the discontinuation of our clinical candidates in November 2016, we reduced our R&D workforce and currently employ approximately 77 employees in an R&D function. These employees are engaged in various areas of research on Arrowhead candidate and platform development including synthesis and analytics, PK/biodistribution, formulation, CMC and analytics, tumor and extra-hepatic targeting, bioassays, live animal research, toxicology/histopathology, clinical and regulatory operations, and other areas. Salaries and payroll-related expenses for our R&D activities were $13.9 million in fiscal 2016, $11.6 million in fiscal 2015, and $7.8 million in fiscal 2014. Laboratory supplies including animal-related costs for in-vivo studies were $4.3 million, $3.1 million, and $2.3 million in fiscal 2016, 2015, and 2014, respectively.

Costs related to manufacture of clinical supplies, GLP toxicology studies and other outsourced lab studies, as well as clinical trial costs were $32.6 million, $41.8 million, and $18.8 million in fiscal 2016, 2015, and 2014, respectively.

Facility-related costs, primarily rental costs for our leased laboratory in Madison, Wisconsin were $1.3 million, $1.0 million, and $0.9 million in fiscal 2016, 2015, and 2014, respectively. Other research and development expenses were $3.2 million, $1.4

13

million, and $1. 2 million in fiscal 201 6 , 201 5 and 201 4 , respectively. These expenses are primaril y related to milestone payments, which can vary from period to period depending on the nature of our various license agreements, and the timing of reaching various development milestones requiring payment.

Government Regulation

Government authorities in the United States, at the federal, state, and local levels, and in other countries and jurisdictions, including the European Union, extensively regulate, among other things, the research, development, testing, product approval, manufacture, quality control, manufacturing changes, packaging, storage, recordkeeping, labeling, promotion, advertising, sales, distribution, marketing, and import and export of drugs and biologic products. All of our foreseeable product candidates are expected to be regulated as drugs. The processes for obtaining regulatory approval in the U.S. and in foreign countries and jurisdictions, along with compliance with applicable statutes and regulations and other regulatory authorities both pre- and post-commercialization, are a significant factor in the production and marketing of our products and our R&D activities and require the expenditure of substantial time and financial resources.

Review and Approval of Drugs in the United States

In the U.S., the FDA and other government entities regulate drugs under the Federal Food, Drug, and Cosmetic Act (the "FDCA"), the Public Health Service Act, and the regulations promulgated under those statutes, as well as other federal and state statutes and regulations. Failure to comply with applicable legal and regulatory requirements in the U.S. at any time during the product development process, approval process, or after approval, may subject us to a variety of administrative or judicial sanctions, such as a delay in approving or refusal by the FDA to approve pending applications, withdrawal of approvals, delay or suspension of clinical trials, issuance of warning letters and other types of regulatory letters, product recalls, product seizures, total or partial suspension of production or distribution, injunctions, fines, civil monetary penalties, refusals of or debarment from government contracts, exclusion from the federal healthcare programs, restitution, disgorgement of profits, civil or criminal investigations by the FDA, U.S. Department of Justice, State Attorneys General, and/or other agencies, False Claims Act suits and/or other litigation, and/or criminal prosecutions.

An applicant seeking approval to market and distribute a new drug in the U.S. must typically undertake the following:

(1) completion of pre-clinical laboratory tests, animal studies, and formulation studies in compliance with the FDA's GLP regulations;

(2) submission to the FDA of an Investigational New Drug Application ("IND") for human clinical testing, which must become effective without FDA objection before human clinical trials may begin;

(3) approval by an independent institutional review board ("IRB"), representing each clinical site before each clinical trial may be initiated;

(4) performance of adequate and well-controlled human clinical trials in accordance with the FDA's current good clinical practice ("cGCP") regulations, to establish the safety and effectiveness of the proposed drug product for each indication for which approval is sought;

(5) preparation and submission to the FDA of a New Drug Application ("NDA");

(6) satisfactory review of the NDA by an FDA advisory committee, where appropriate or if applicable,

(7) satisfactory completion of one or more FDA inspections of the manufacturing facility or facilities at which the drug product, and the active pharmaceutical ingredient or ingredients thereof, are produced to assess compliance with current good manufacturing practice ("cGMP") regulations and to assure that the facilities, methods, and controls are adequate to ensure the product's identity, strength, quality, and purity;

(8) payment of user fees, as applicable, and securing FDA approval of the NDA; and

(9) compliance with any post-approval requirements, such as any Risk Evaluation and Mitigation Strategies ("REMS") or post-approval studies required by the FDA.

14

Preclinical Studies and an IND

Preclinical studies can include in vitro and animal studies to assess the potential for adverse events and, in some cases, to establish a rationale for therapeutic use. The conduct of preclinical studies is subject to federal regulations and requirements, including GLP regulations. Other studies include laboratory evaluation of the purity, stability and physical form of the manufactured drug substance or active pharmaceutical ingredient and the physical properties, stability and reproducibility of the formulated drug or drug product. An IND sponsor must submit the results of the preclinical tests, together with manufacturing information, analytical data, any available clinical data or literature and plans for clinical studies, among other things, to the FDA as part of an IND. Some preclinical testing, such as longer-term toxicity testing, animal tests of reproductive adverse events and carcinogenicity, may continue after the IND is submitted. An IND automatically becomes effective 30 days after receipt by the FDA, unless before that time the FDA raises concerns or questions related to a proposed clinical trial and places the trial on clinical hold. In such a case, the IND sponsor and the FDA must resolve any outstanding concerns before the clinical trial can begin. As a result, submission of an IND may not result in the FDA allowing clinical trials to commence.

Following commencement of a clinical trial under an IND, the FDA may place a clinical hold on that trial. A clinical hold is an order issued by the FDA to the sponsor to delay a proposed clinical investigation or to suspend an ongoing investigation. A partial clinical hold is a delay or suspension of only part of the clinical work requested under the IND. For example, a specific protocol or part of a protocol is not allowed to proceed, while other protocols may do so. No more than 30 days after imposition of a clinical hold or partial clinical hold, the FDA will provide the sponsor a written explanation of the basis for the hold. Following issuance of a clinical hold or partial clinical hold, an investigation may only resume after the FDA has notified the sponsor that the investigation may proceed. The FDA will base that determination on information provided by the sponsor correcting the deficiencies previously cited or otherwise satisfying the FDA that the investigation can proceed.

Human Clinical Studies in Support of an NDA

Clinical trials involve the administration of the investigational product to human subjects under the supervision of qualified investigators in accordance with cGCP requirements, which include, among other things, the requirement that all research subjects provide their informed consent in writing before their participation in any clinical trial. Clinical trials are conducted under written study protocols detailing, among other things, the objectives of the study, the parameters to be used in monitoring safety and the effectiveness criteria to be evaluated. A protocol for each clinical trial and any subsequent protocol amendments must be submitted to the FDA as part of the IND. In addition, an IRB representing each institution participating in the clinical trial must review and approve the plan for any clinical trial before it commences at that institution, and the IRB must conduct continuing review and reapprove the study at least annually. The IRB must review and approve, among other things, the study protocol and informed consent information to be provided to study subjects. An IRB must operate in compliance with FDA regulations. Information about certain clinical trials must be submitted within specific timeframes to the NIH for public dissemination on its ClinicalTrials.gov website.

Human clinical trials are typically conducted in three sequential phases, which may overlap or be combined:

Phase 1: The product candidate is initially introduced into healthy human subjects or patients with the target disease or condition and tested for safety, dosage tolerance, absorption, metabolism, distribution, excretion and, if possible, to gain an early indication of its effectiveness.

Phase 2: The product candidate is administered to a limited patient population to identify possible adverse effects and safety risks, to preliminarily evaluate the efficacy of the product for specific targeted diseases and to determine dosage tolerance and optimal dosage.

Phase 3: The product candidate is administered to an expanded patient population, generally at geographically dispersed clinical trial sites, in well-controlled clinical trials to generate enough data to statistically evaluate the efficacy and safety of the product for approval, to establish the overall risk-benefit profile of the product, and to provide adequate information for the labeling of the product.

Progress reports detailing the results of the clinical trials must be submitted at least annually to the FDA and more frequently if serious adverse events occur. Phase 1, Phase 2, and Phase 3 clinical trials may not be completed successfully within any specified period, or at all. Furthermore, the FDA or the sponsor may suspend or terminate a clinical trial at any time on various grounds, including a finding that the research subjects are being exposed to an unacceptable health risk. Similarly, an IRB can suspend or terminate approval of a clinical trial at its institution, or an institution it represents, if the clinical trial is not being conducted in accordance with the IRB's requirements or if the drug has been associated with unexpected serious harm to patients. The FDA will typically inspect one or more clinical sites in late-stage clinical trials to assure compliance with cGCP and the integrity of the clinical data submitted.

15

Submission of an NDA to the FDA

Assuming successful completion of required clinical testing and other requirements, the results of the preclinical and clinical studies, together with detailed information relating to the product's chemistry, manufacture, controls and proposed labeling, among other things, are submitted to the FDA as part of an NDA requesting approval to market the drug product for one or more indications. Under federal law, the submission of most NDAs is additionally subject to an application user fee, currently exceeding $2.4 million, and the sponsor of an approved NDA is also subject to annual product and establishment user fees, currently exceeding $114,450 per product and $585,200 per establishment. These fees are typically increased annually.

Under certain circumstances, the FDA will waive the application fee for the first human drug application that a small business, defined as a company with less than 500 employees, or its affiliate, submits for review. An affiliate is defined as a business entity that has a relationship with a second business entity if one business entity controls, or has the power to control, the other business entity, or a third party controls, or has the power to control, both entities. In addition, an application to market a prescription drug product that has received orphan designation is not subject to a prescription drug user fee unless the application includes an indication for other than the rare disease or condition for which the drug was designated.

The FDA conducts a preliminary review of an NDA within 60 days of its receipt and informs the sponsor by the 74th day after the FDA's receipt of the submission to determine whether the application is sufficiently complete to permit substantive review. The FDA may request additional information rather than accept an NDA for filing. In this event, the application must be resubmitted with the additional information. The resubmitted application is also subject to review before the FDA accepts it for filing. Once the submission is accepted for filing, the FDA begins an in-depth substantive review. The FDA has agreed to specified performance goals in the review process of NDAs. Most such applications are meant to be reviewed within ten months from the date of filing, and most applications for "priority review" products are meant to be reviewed within six months of filing. The review process may be extended by the FDA for three additional months to consider new information or clarification provided by the applicant to address an outstanding deficiency identified by the FDA following the original submission.

Before approving an NDA, the FDA typically will inspect the facility or facilities where the product is manufactured. The FDA will not approve an application unless it determines that the manufacturing processes and facilities are in compliance with cGMP requirements and adequate to assure consistent production of the product within required specifications. Additionally, before approving an NDA, the FDA will typically inspect one or more clinical sites to assure compliance with cGCP.

The FDA also may require submission of an REMS plan to mitigate any identified or suspected serious risks. The REMS plan could include medication guides, physician communication plans, assessment plans, and elements to assure safe use, such as restricted distribution methods, patient registries, or other risk minimization tools.

The FDA is required to refer an application for a novel drug to an advisory committee or explain why such referral was not made. Typically, an advisory committee is a panel of independent experts, including clinicians and other scientific experts, that reviews, evaluates and provides a recommendation as to whether the application should be approved and under what conditions. The FDA is not bound by the recommendations of an advisory committee, but it considers such recommendations carefully when making decisions.

The FDA's Decision on an NDA

On the basis of the FDA's evaluation of the NDA and accompanying information, including the results of the inspection of the manufacturing facilities, the FDA may issue an approval letter or a complete response letter. An approval letter authorizes commercial marketing of the product with specific prescribing information for specific indications. A complete response letter generally outlines the deficiencies in the submission and may require substantial additional testing or information in order for the FDA to reconsider the application. If and when those deficiencies have been addressed to the FDA's satisfaction in a resubmission of the NDA, the FDA will issue an approval letter. The FDA has committed to reviewing such resubmissions in two or six months depending on the type of information included. Even with submission of this additional information, the FDA ultimately may decide that the application does not satisfy the regulatory criteria for approval.

16

If the FDA approves a product, it may limit the approved indications for use for the product, require that contraindicati ons, warnings or precautions be included in the product labeling, require that post-approval studies, including Phase 4 clinical trials, be conducted to further assess the drug's safety after approval, require testing and surveillance programs to monitor t he product after commercialization, or impose other conditions, including distribution restrictions or other risk management mechanisms, including REMS, which can materially affect the potential market and profitability of the product. The FDA may prevent or limit further marketing of a product based on the results of post-market studies or surveillance programs. After approval, some types of changes to the approved product, such as adding new indications, manufacturing changes and additional labeling claim s, are subject to further testing requirements and FDA review and approval.

The product may also be subject to official lot release, meaning that the manufacturer is required to perform certain tests on each lot of the product before it is released for distribution. If the product is subject to official release, the manufacturer must submit samples of each lot, together with a release protocol showing a summary of the history of manufacture of the lot and the results of all of the manufacturer's tests performed on the lot, to the FDA. The FDA may in addition perform certain confirmatory tests on lots of some products before releasing the lots for distribution. Finally, the FDA will conduct laboratory research related to the safety and effectiveness of drug products.

Under the Orphan Drug Act, the FDA may grant orphan drug designation to a drug intended to treat a rare disease or condition, which is generally a disease or condition that affects fewer than 200,000 individuals in the United States, or more than 200,000 individuals in the U.S. and for which there is no reasonable expectation that the cost of developing and making available in the U.S. a drug for this type of disease or condition will be recovered from sales in the U.S. for that drug. Orphan drug designation must be requested before submitting an NDA, and both the drug and the disease or condition must meet certain criteria specified in the Orphan Drug Act and FDA's implementing regulations at 21 C.F.R. Part 316. The granting of an orphan drug designation does not alter the standard regulatory requirements and process for obtaining marketing approval. Safety and effectiveness of a drug must be established through adequate and well-controlled studies.

After the FDA grants orphan drug designation, the identity of the therapeutic agent and its potential orphan use are disclosed publicly by the FDA. If a product that has orphan drug designation subsequently receives the first FDA approval for the disease for which it has such designation, the product is entitled to orphan product exclusivity, which means that the FDA may not approve any other application to market the same drug for the same indication, except in very limited circumstances, for seven years.

Post-Approval Requirements

Drugs manufactured or distributed pursuant to FDA approvals are subject to pervasive and continuing regulation by the FDA, including, among other things, requirements relating to recordkeeping, periodic reporting, product sampling and distribution, advertising and promotion and reporting of adverse experiences with the product. After approval, most changes to the approved product, such as adding new indications or other labeling claims, are subject to prior FDA review and approval. There also are continuing, annual user fee requirements for any marketed products and the establishments at which such products are manufactured, as well as new application fees for supplemental applications with clinical data.

In addition, drug manufacturers and other entities involved in the manufacture and distribution of approved drugs are required to register their establishments with the FDA and state agencies, and are subject to periodic unannounced inspections by the FDA and these state agencies for compliance with cGMP requirements. Changes to the manufacturing process are strictly regulated and often require prior FDA approval before being implemented. FDA regulations also require investigation and correction of any deviations from cGMP and impose reporting and documentation requirements upon the sponsor and any third-party manufacturers that the sponsor may decide to use. Accordingly, manufacturers must continue to expend time, money, and effort in the area of production and quality control to maintain cGMP compliance.

Once an approval is granted, the FDA may withdraw the approval if compliance with regulatory requirements and standards is not maintained or if problems occur after the product reaches the market. Later discovery of previously unknown problems with a product, including adverse events or problems with manufacturing processes of unanticipated severity or frequency, or failure to comply with regulatory requirements, may result in revisions to the approved labeling to add new safety information; imposition of post-market studies or clinical trials to assess new safety risks; or imposition of distribution or other restrictions under a REMS program. Other potential consequences include, among other things:

| • | restrictions on the marketing or manufacturing of the product, complete withdrawal of the product from the market or product recalls; |

| • | fines, warning letters or holds on post-approval clinical trials; |

| • | refusal of the FDA to approve pending NDAs or supplements to approved NDAs, or suspension or revocation of product license approvals; |

17

| • | product seizure or detention, or refusal to permit the import or export of products; or |

| • | injunctions or the imposition of civil or criminal penalties. |

The FDA strictly regulates marketing, labeling, advertising and promotion of products that are placed on the market. Drugs may be promoted only for the approved indications and in accordance with the provisions of the approved label. The FDA and other agencies actively enforce the laws and regulations prohibiting the promotion of off-label uses, and a company that is found to have improperly promoted off-label uses may be subject to significant liability.

In addition, the distribution of prescription pharmaceutical products is subject to the Prescription Drug Marketing Act (PDMA), which regulates the distribution of drugs and drug samples at the federal level, and sets minimum standards for the registration and regulation of drug distributors by the states. Both the PDMA and state laws limit the distribution of prescription pharmaceutical product samples and impose requirements to ensure accountability in distribution.

Abbreviated New Drug Applications for Generic Drugs

In 1984, with passage of the Drug Price Competition and Patent Term Restoration Act of 1984 (commonly referred to as the "Hatch-Waxman Amendments") amending the FDCA, Congress authorized the FDA to approve generic drugs that are the same as drugs previously approved by the FDA under the NDA provisions of the statute. To obtain approval of a generic drug, an applicant must submit an abbreviated new drug application (ANDA) to the agency. In support of such applications, a generic manufacturer may rely on the preclinical and clinical testing previously conducted for a drug product previously approved under an NDA, known as the reference listed drug, or RLD. To reference that information, however, the ANDA applicant must demonstrate, and the FDA must conclude, that the generic drug does, in fact, perform in the same way as the RLD it purports to copy. Specifically, in order for an ANDA to be approved, the FDA must find that the generic version is identical to the RLD with respect to the active ingredients, the route of administration, the dosage form, and the strength of the drug.

At the same time, the FDA must also determine that the generic drug is "bioequivalent" to the innovator drug. Under the statute, a generic drug is bioequivalent to a RLD if "the rate and extent of absorption of the generic drug do not show a significant difference from the rate and extent of absorption of the RLD." Upon approval of an ANDA, the FDA indicates that the generic product is "therapeutically equivalent" to the RLD and it assigns a therapeutic equivalence rating to the approved generic drug in its publication "Approved Drug Products with Therapeutic Equivalence Evaluations," also referred to as the "Orange Book." Physicians and pharmacists consider the therapeutic equivalence rating to mean that a generic drug is fully substitutable for the RLD. In addition, by operation of certain state laws and numerous health insurance programs, the FDA's designation of a therapeutic equivalence rating often results in substitution of the generic drug without the knowledge or consent of either the prescribing physician or patient.

Under the Hatch-Waxman Amendments, the FDA may not approve an ANDA until any applicable period of nonpatent exclusivity for the RLD has expired. The FDCA provides a period of five years of data exclusivity for new drug containing a new chemical entity. In cases where such exclusivity has been granted, an ANDA may not be filed with the FDA until the expiration of five years unless the submission is accompanied by a Paragraph IV certification, in which case the applicant may submit its application four years following the original product approval. The FDCA also provides for a period of three years of exclusivity if the NDA includes reports of one or more new clinical investigations, other than bioavailability or bioequivalence studies, that were conducted by or for the applicant and are essential to the approval of the application. This three-year exclusivity period often protects changes to a previously approved drug product, such as a new dosage form, route of administration, combination or indication.

Hatch-Waxman Patent Certification and the 30 Month Stay

Upon approval of an NDA or a supplement thereto, NDA sponsors are required to list with the FDA each patent with claims that cover the applicant's product or a method of using the product. Each of the patents listed by the NDA sponsor is published in the Orange Book. When an ANDA applicant files its application with the FDA, the applicant is required to certify to the FDA concerning any patents listed for the reference product in the Orange Book, except for patents covering methods of use for which the ANDA applicant is not seeking approval.

Specifically, the applicant must certify with respect to each patent that:

| • | the required patent information has not been filed; |

| • | the listed patent has expired; |

| • | the listed patent has not expired, but will expire on a particular date and approval is sought after patent expiration; or |

| • | the listed patent is invalid, unenforceable or will not be infringed by the new product. |

18

A certification that the new product will not infringe the already approved product's listed patents or that such patents are invalid or unenforceable is called a Paragraph IV certification. If the applicant does not challenge the listed patents or indicat e that it is not seeking approval of a patented method of use, the ANDA application will not be approved until all the listed patents claiming the referenced product have expired. If the ANDA applicant has provided a Paragraph IV certification to the FDA, the applicant must also send notice of the Paragraph IV certification to the NDA and patent holders once the ANDA has been accepted for filing by the FDA. The NDA and patent holders may then initiate a patent infringement lawsuit in response to the notice of the Paragraph IV certification. The filing of a patent infringement lawsuit within 45 days after the receipt of a Paragraph IV certification automatically prevents the FDA from approving the ANDA until the earlier of 30 months, expiration of the patent, settlement of the lawsuit or a decision in the infringement case that is favorable to the ANDA applicant.

To the extent that a Section 505(b)(2) applicant is relying on studies conducted for an already approved product, the applicant is required to certify to the FDA concerning any patents listed for the approved product in the Orange Book to the same extent that an ANDA applicant would. As a result, approval of a 505(b)(2) NDA can be stalled until all the listed patents claiming the referenced product have expired, until any non-patent exclusivity, such as exclusivity for obtaining approval of a new chemical entity, listed in the Orange Book for the referenced product has expired, and, in the case of a Paragraph IV certification and subsequent patent infringement suit, until the earlier of 30 months, settlement of the lawsuit or a decision in the infringement case that is favorable to the Section 505(b)(2) applicant.

Pediatric Studies and Exclusivity