UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One):

x Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

For the fiscal year ended December 31, 2014

¨ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

For the transition period from to

Commission File Number: 001-14195

American Tower Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 65-0723837 | |

(State or other jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

116 Huntington Avenue

Boston, Massachusetts 02116

(Address of principal executive offices)

Telephone Number (617) 375-7500

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each Class | Name of exchange on which registered | |

| Common Stock, $0.01 par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well known seasoned issuer, as defined in Rule 405 of the Securities Act: Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act: Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check One):

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act): Yes ¨ No x

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of June 30, 2014 was approximately $35.3 billion, based on the closing price of the registrant's common stock as reported on the New York Stock Exchange as of the last business day of the registrant's most recently completed second quarter.

As of February 13, 2015, there were 396,708,636 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement (the "Definitive Proxy Statement") to be filed with the Securities and Exchange Commission relative to the Company's 2015 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report.

AMERICAN TOWER CORPORATION

TABLE OF CONTENTS

FORM 10-K ANNUAL REPORT

FISCAL YEAR ENDED DECEMBER 31, 2014

| Page | ||||||

Special Note Regarding Forward-Looking Statements | ii | |||||

PART I | ||||||

ITEM 1. | Business | 1 | ||||

Overview | 1 | |||||

Products and Services | 2 | |||||

Strategy | 4 | |||||

Recent Transactions | 6 | |||||

Regulatory Matters | 7 | |||||

Competition | 9 | |||||

Customer Demand | 9 | |||||

Employees | 10 | |||||

Available Information | 10 | |||||

ITEM 1A. | Risk Factors | 11 | ||||

ITEM 1B. | Unresolved Staff Comments | 20 | ||||

ITEM 2. | Properties | 21 | ||||

ITEM 3. | Legal Proceedings | 23 | ||||

ITEM 4. | Mine Safety Disclosures | 23 | ||||

PART II | ||||||

ITEM 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 24 | ||||

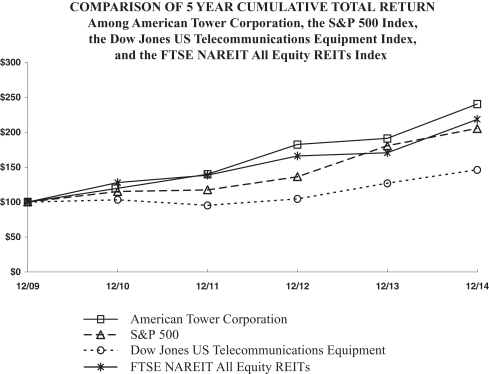

Dividends | 24 | |||||

Performance Graph | 25 | |||||

ITEM 6. | Selected Financial Data | 26 | ||||

ITEM 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 28 | ||||

Executive Overview | 28 | |||||

Non-GAAP Financial Measures | 32 | |||||

Results of Operations: Years Ended December 31, 2014 and 2013 | 33 | |||||

Results of Operations: Years Ended December 31, 2013 and 2012 | 39 | |||||

Liquidity and Capital Resources | 46 | |||||

Critical Accounting Policies and Estimates | 60 | |||||

Accounting Standards Updates | 63 | |||||

ITEM 7A. | Quantitative and Qualitative Disclosures About Market Risk | 64 | ||||

ITEM 8. | Financial Statements and Supplementary Data | 65 | ||||

ITEM 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 65 | ||||

i

AMERICAN TOWER CORPORATION

TABLE OF CONTENTS-(Continued)

FORM 10-K ANNUAL REPORT

FISCAL YEAR ENDED DECEMBER 31, 2014

| Page | ||||||

ITEM 9A. | Controls and Procedures | 65 | ||||

Disclosure Controls and Procedures | 65 | |||||

Management's Annual Report on Internal Control over Financial Reporting | 66 | |||||

Changes in Internal Control over Financial Reporting | 66 | |||||

Report of Independent Registered Public Accounting Firm | 67 | |||||

PART III | ||||||

ITEM 10. | Directors, Executive Officers and Corporate Governance | 68 | ||||

ITEM 11. | Executive Compensation | 70 | ||||

ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 70 | ||||

ITEM 13. | Certain Relationships and Related Transactions, and Director Independence | 70 | ||||

ITEM 14. | Principal Accounting Fees and Services | 70 | ||||

PART IV | ||||||

ITEM 15. | Exhibits, Financial Statement Schedules | 71 | ||||

Signatures | 72 | |||||

Index to Consolidated Financial Statements | F-1 | |||||

Index to Exhibits | EX-1 | |||||

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains statements about future events and expectations, or forward-looking statements, all of which are inherently uncertain. We have based those forward-looking statements on our current expectations and projections about future results. When we use words such as "anticipates," "intends," "plans," "believes," "estimates," "expects" or similar expressions, we do so to identify forward-looking statements. Examples of forward-looking statements include, but are not limited to, statements we make regarding the Proposed Verizon Transaction (as defined in this Annual Report), future prospects of growth in the communications site leasing industry, the effects of consolidation among companies in our industry and among our tenants and other competitive pressures, the level of future expenditures by companies in this industry and other trends in this industry, changes in zoning, tax and other laws and regulations, economic, political and other events, particularly those relating to our international operations, our substantial leverage and debt service obligations, our future financing transactions, our plans to fund our future liquidity needs, our ability to maintain or increase our market share, our future operating results, our ability to remain qualified for taxation as a real estate investment trust ("REIT"), the amount and timing of any future distributions including those we are required to make as a REIT, our future capital expenditure levels, our ability to protect our rights to the land under our towers and natural disasters and similar events. These statements are based on our management's beliefs and assumptions, which in turn are based on currently available information. These assumptions could prove inaccurate. These forward-looking statements may be found under the captions "Business" and "Management's Discussion and Analysis of Financial Condition and Results of Operations," as well as in this Annual Report generally.

ii

You should keep in mind that any forward-looking statement we make in this Annual Report or elsewhere speaks only as of the date on which we make it. New risks and uncertainties arise from time to time, and it is impossible for us to predict these events or how they may affect us. In any event, these and other important factors, including those set forth in Item 1A of this Annual Report under the caption "Risk Factors," may cause actual results to differ materially from those indicated by our forward-looking statements. We have no duty and do not intend to update or revise the forward-looking statements we make in this Annual Report, except as may be required by law. In light of these risks and uncertainties, you should keep in mind that the future events or circumstances described in any forward-looking statement we make in this Annual Report or elsewhere might not occur. References in this Annual Report to "we," "our" and the "Company" refer to American Tower Corporation and its predecessor, as applicable, individually and collectively with its subsidiaries as the context requires.

iii

PART I

| ITEM 1. BUSINESS |

Overview

We are a global independent owner, operator and developer of communications real estate. Our primary business is the leasing of space on multi-tenant communications sites to wireless service providers, radio and television broadcast companies, wireless data and data providers, government agencies and municipalities and tenants in a number of other industries. We refer to this business as our rental and management operations, which accounted for approximately 98% of our total revenues for the year ended December 31, 2014. Through our network development services business, we offer tower-related services domestically, which primarily support our site leasing business.

Our communications real estate portfolio of 75,594 communications sites, as of December 31, 2014, includes 28,566 communications towers domestically, 46,598 communications towers internationally and 430 distributed antenna system ("DAS") networks, which provide seamless coverage solutions in certain in-building and outdoor wireless environments. Our portfolio primarily consists of towers that we own and towers that we operate pursuant to long-term lease arrangements. In addition to the communications sites in our portfolio, we manage rooftop and tower sites for property owners under various contractual arrangements. We also hold property interests that we lease to communications service providers and third-party tower operators.

American Tower Corporation was originally created as a subsidiary of American Radio Systems Corporation in 1995 and was spun off into a free-standing public company in 1998. Since inception, we have grown our communications real estate portfolio through acquisitions, long-term lease arrangements and site development. We are a holding company and conduct our operations through our directly and indirectly owned subsidiaries and joint ventures. Our principal domestic operating subsidiaries are American Towers LLC and SpectraSite Communications, LLC. We conduct our international operations primarily through our subsidiary, American Tower International, Inc., which in turn conducts operations through its various international holding and operating subsidiaries and joint ventures.

On February 5, 2015, we signed a definitive agreement with Verizon Communications, Inc. ("Verizon") pursuant to which we expect to acquire the exclusive right to lease, acquire or otherwise operate and manage up to 11,489 wireless communications sites for $5.056 billion in cash at closing (the "Proposed Verizon Transaction"), subject to certain conditions and limited adjustments.

We operate as a REIT and therefore are generally not subject to U.S. federal income taxes on our income and gains that we distribute to our stockholders, including the income derived from leasing space on our towers. However, even as a REIT, we remain obligated to pay income taxes on earnings from our taxable REIT subsidiaries ("TRSs"). In addition, our international assets and operations, including those designated as direct or indirect qualified REIT subsidiaries or other disregarded entities of a REIT (collectively, "QRSs"), continue to be subject to taxation in the foreign jurisdictions where those assets are held or those operations are conducted.

The use of TRSs enables us to continue to engage in certain businesses while complying with REIT qualification requirements. We may, from time to time, change the election of previously designated TRSs to be treated as QRSs, and may reorganize and transfer certain assets or operations from our TRSs to other subsidiaries, including QRSs. During the year ended December 31, 2014, we restructured certain of our German subsidiaries and certain of our domestic TRSs, which included a portion of our network development services segment and indoor DAS networks business, to be treated as QRSs. As a result, as of December 31, 2014, our QRSs include our domestic tower leasing business, most of our operations in Costa Rica, Germany and Mexico and a portion of our network development services segment and indoor DAS networks business.

Our continuing operations are reported in three segments: (i) domestic rental and management, (ii) international rental and management and (iii) network development services. For more information about our

1

business segments, as well as financial information about the geographic areas in which we operate, see Item 7 of this Annual Report under the caption "Management's Discussion and Analysis of Financial Condition and Results of Operations" and note 21 to our consolidated financial statements included in this Annual Report.

Products and Services

Rental and Management Operations

Our rental and management operations accounted for approximately 98%, 98% and 97% of our total revenues for the years ended December 31, 2014, 2013 and 2012, respectively. Our revenue is primarily generated from tenant leases. Our tenants lease space on our communications real estate, where they install and maintain their individual communications network equipment. Rental payments vary considerably depending upon numerous factors, including, but not limited to, tower location, amount and type of tenant equipment on the tower, ground space required by the tenant and remaining tower capacity. Our tenant leases are typically non-cancellable and have annual rent escalations. Our primary costs typically include ground rent (which is primarily fixed, with annual cost escalations) and power and fuel costs, some of which may be passed through to our tenants, as well as property taxes and repairs and maintenance. Our rental and management operations have generated consistent incremental growth in revenue and have low cash flow volatility due to the following characteristics:

| • | Consistent demand for our sites. As a result of rapidly growing usage of wireless services and the corresponding wireless industry capital spending trends in the markets we serve, we anticipate consistent demand for our communications sites. We believe that our global asset base positions us well to benefit from the increasing proliferation of advanced wireless devices and the increasing usage of high bandwidth applications on those devices. We have the ability to add new tenants and new equipment for existing tenants on our sites, which typically results in incremental revenue. Our legacy site portfolio and our established tenant base provide us with a solid platform for new business opportunities, which has historically resulted in consistent and predictable organic revenue growth. |

| • | Long-term tenant leases with contractual rent escalations. In general, a tenant lease has an initial non-cancellable ten-year term with multiple renewal terms, with provisions that periodically increase the rent due under the lease, typically annually based on a fixed escalation percentage (approximately 3.0% in the United States) or an inflationary index in our international markets, or a combination of both. |

| • | High lease renewal rates. Our tenants tend to renew leases because suitable alternative sites may not exist or be available and repositioning a site in their network may be expensive and may adversely affect the quality of their network. Historically, churn has been approximately 1% to 2% of total rental and management revenue per year. We define churn as revenue lost when a tenant cancels or does not renew its lease and, in limited circumstances, such as a tenant bankruptcy, reductions in lease rates on existing leases. We derive our churn rate for a given year by dividing our cash revenue lost on this basis by our comparable year ago period cash rental and management segment revenue. |

| • | High operating margins. Incremental operating costs associated with adding new tenants to an existing communications site are relatively minimal. Therefore, as tenants are added, the substantial majority of incremental revenue flows through to operating profit. In addition, in many of our international markets, certain expenses, such as ground rent or fuel costs, are passed through and shared across our tenant base. |

| • | Low maintenance capital expenditures. On average, we require relatively low amounts of annual capital expenditures to maintain our communications sites. |

Our rental and management operations include the operation of communications towers, managed networks, the leasing of property interests and the provision of backup power through shared generators. Our domestic rental and management segment accounted for approximately 65%, 65% and 67% of our total revenues for the years ended December 31, 2014, 2013 and 2012, respectively.

2

Our international rental and management segment, which consists of communications sites in Brazil, Chile, Colombia, Costa Rica, Germany, Ghana, India, Mexico, Peru, South Africa and Uganda, provides a source of growth and diversification, including exposure to markets in various stages of wireless network development. In November 2014, we expanded our global footprint by signing an agreement to acquire over 4,800 communications sites in Nigeria. Our international rental and management segment accounted for approximately 33%, 33% and 30% of our total revenues for the years ended December 31, 2014, 2013 and 2012, respectively.

Communications Towers. Approximately 95%, 96% and 96% of revenue in our rental and management segments was attributable to our communications towers for the years ended December 31, 2014, 2013 and 2012, respectively.

We lease real estate on our communications towers to tenants providing a diverse range of communications services, including cellular voice and data, broadcasting, enhanced specialized mobile radio, mobile video and fixed microwave. Our top domestic and international tenants by revenue are as follows:

| • | Domestic: AT&T Mobility, Sprint Nextel, Verizon Wireless and T-Mobile USA accounted for an aggregate of approximately 84% of domestic rental and management segment revenue for the year ended December 31, 2014. |

| • | International: Telefónica (in Brazil, Chile, Colombia, Costa Rica, Germany, Mexico and Peru), MTN Group Limited (in Ghana, South Africa and Uganda), Nextel International (in Brazil, Chile and Mexico), Grupo Iusacell, S.A. de C.V. (in Mexico, acquired by AT&T in January 2015) and Vodafone (in Germany, Ghana, India and South Africa), accounted for an aggregate of approximately 57% of international rental and management segment revenue for the year ended December 31, 2014. |

Accordingly, we are subject to certain risks, as set forth in Item 1A of this Annual Report under the caption "Risk Factors-A substantial portion of our revenue is derived from a small number of tenants, and we are sensitive to changes in the creditworthiness and financial strength of our tenants." In addition, we are subject to risks related to our international operations, as set forth under the caption "Risk Factors-Our foreign operations are subject to economic, political and other risks that could materially and adversely affect our revenues or financial position, including risks associated with fluctuations in foreign currency exchange rates."

Managed Networks, Property Interests and Shared Generators. In addition to our communications sites, we also own and operate several types of managed network solutions, provide communications site management services to third parties, manage and lease property interests under carrier or other third-party communications sites and provide back-up power sources to tenants at our sites.

| • | Managed Networks. We own and operate DAS networks primarily in malls and casinos in the United States, Brazil, Chile, Colombia, Ghana, India and Mexico. We obtain rights from property owners to install and operate in-building DAS networks, and we grant rights to wireless service providers to attach their equipment to our installations. We also offer outdoor DAS networks as a complementary shared infrastructure solution for our tenants in the United States. Typically, we design, build and operate our outdoor DAS networks in areas in which zoning restrictions or other barriers may prevent or delay deployment of more traditional wireless communications sites. We also hold lease rights and easement interests on rooftops capable of hosting communications equipment in locations where towers are generally not a viable solution based on area characteristics. In addition, we provide management services to property owners in the United States who elect to retain full rights to their property while simultaneously marketing the rooftop for wireless communications equipment installation. As the demand for advanced wireless devices in urban markets evolves, we continue to evaluate infrastructure, such as small cell deployment, that may support our tenants' networks in these areas. |

| • | Property Interests . We own a portfolio of property interests in the United States under carrier or other third-party communications sites, which provides recurring cash flow under complementary leasing arrangements. |

3

| • | Shared Generators . We have contracts with certain of our tenants in the United States pursuant to which we provide access to shared backup power generators. |

Network Development Services

Through our network development services, we offer tower-related services domestically, including site acquisition, zoning and permitting services and structural analysis services. Network development services primarily support our site leasing business and the addition of new tenants and equipment on our sites, including in connection with provider network upgrades. This segment accounted for approximately 2%, 2% and 3% of our total revenues for the years ended December 31, 2014, 2013 and 2012, respectively.

Site Acquisition, Zoning and Permitting . We engage in site acquisition services on our own behalf in connection with our tower development projects, as well as on behalf of our tenants. We typically work with our tenants' engineers to determine the geographic areas where new communications sites will best address the tenants' needs and meet their coverage objectives. Once a new site is identified, we acquire the rights to the land or structure on which the site will be constructed, and we manage the permitting process to ensure all necessary approvals are obtained to construct and operate the communications site.

Structural Analysis. We offer structural analysis services to wireless carriers in connection with the installation of their communications equipment on our towers. Our team of engineers can evaluate whether a tower structure can support the additional burden of the new equipment or if an upgrade is needed, which enables our tenants to better assess potential sites before making an installation decision. Our structural analysis capabilities enable us to provide higher quality service to our existing tenants by, among other things, reducing the time required to achieve operational readiness, while also providing opportunities to offer structural analysis services to third parties.

Strategy

Operational Strategy

Our operational strategy is to capitalize on the global growth in the use of wireless communications services and the evolution of advanced wireless handsets, tablets and other mobile devices, and the corresponding expansion of communications infrastructure required to deploy current and future generations of wireless communications technologies. To achieve this, our primary focus is to (i) increase the leasing of our existing communications real estate portfolio, (ii) invest in and selectively grow our communications real estate portfolio, (iii) further improve upon our operational performance and (iv) maintain a strong balance sheet. We believe these efforts will further support and enhance our ability to capitalize on the growth in demand for wireless infrastructure.

| • | Increase the leasing of our existing communications real estate portfolio. We believe that our highest returns will be achieved by leasing additional space on our existing communications sites. Increasing demand for wireless services in the United States and in our international markets has resulted in significant capital spending by major wireless carriers. As a result, we anticipate consistent demand for our communications sites because they are attractively located for wireless service providers and have capacity available for additional tenants. In the United States, incremental carrier capital spending is being driven primarily by the build-out of fourth generation (4G) networks, while our international markets are in various stages of network development. As of December 31, 2014, we had a global average of approximately 1.9 tenants per tower. We believe that many of our towers have capacity for additional tenants and that substantially all of our towers that are currently at or near full structural capacity can be upgraded or augmented to meet future tenant demand with relatively modest capital investment. Therefore, we will continue to target our sales and marketing activities to increase the utilization and return on investment of our existing communications sites. |

4

| • | Invest in and selectively grow our communications real estate portfolio. We seek opportunities to invest in and grow our operations through our capital programs, new site construction and acquisitions. We believe we can achieve attractive risk-adjusted returns by pursuing such investments. In addition, we seek to secure property interests under our communications sites to improve operating margins as we reduce our cash operating expense related to ground leases. |

| • | Further improve upon our operational performance. We will continue to seek opportunities to improve our operational performance throughout the organization. This includes investing in our systems and people as we strive to improve our efficiencies and provide superior service to our customers. To achieve this, we intend to continue to focus on customer service, such as reducing cycle times for key functions, including lease processing and tower structural analysis. |

| • | Maintain a strong balance sheet. We remain committed to our disciplined financial policies, which we believe result in our ability to maintain a strong balance sheet and will support our overall strategy and focus on asset growth and operational excellence. As a result of these policies, we currently have investment grade ratings. We remain committed to reducing our net leverage through a combination of debt repayment and our continued growth. We continue to focus on maintaining a strong liquidity position and, as of December 31, 2014, had approximately $2.7 billion of available liquidity. We believe that our investment grade ratings provide us consistent access to the capital markets and our liquidity provides us the ability to selectively invest in our portfolio. |

Capital Allocation Strategy

The objective of our capital allocation strategy is to simultaneously increase adjusted funds from operations and our return on invested capital. To maintain our qualification for taxation as a REIT, we are required to distribute to our stockholders annually an amount equal to at least 90% of our REIT taxable income (determined before the deduction for distributed earnings and excluding any net capital gain). After complying with our REIT distribution requirements and paying dividends on our preferred stock, we plan to continue to allocate our available capital among investment alternatives that meet our return on investment criteria, while taking into account the repayment of debt, as necessary, to reduce our net leverage to be within our long-term target range.

| • | Capital expenditure program. We will continue to invest in and expand our existing communications real estate portfolio through our annual capital expenditure program. This includes capital expenditures associated with maintenance, increasing the capacity of our existing sites and projects such as new site construction, land interest acquisitions and shared generator installations. |

| • | Acquisitions. We intend to pursue acquisitions of communications sites in our existing or new markets where we can meet our risk-adjusted return on investment criteria. Our risk-adjusted hurdle rates consider additional risks such as the country and counter-parties involved, investment and economic climate, legal and regulatory conditions and industry risk. |

| • | Return excess capital to stockholders. If we have excess capital available after funding (i) our required distributions, (ii) our capital expenditures, (iii) repayment of debt, as necessary, to reduce our net leverage ratio toward our targeted range and (iv) anticipated future investments, including acquisition opportunities, we will seek to return such excess capital to stockholders. |

During 2014, we generated $2.1 billion of cash from operating activities, which along with incremental debt, was used to fund $1.9 billion of investments, including $1.0 billion of acquisitions and $974.4 million of capital expenditures. In addition, in 2014, we paid regular cash distributions in the aggregate of approximately $404.6 million to our common stockholders and approximately $16.0 million to our preferred stockholders.

International Growth Strategy

We believe that, in certain international markets, we can create substantial value by either establishing a new, or expanding our existing communications real estate leasing business. Therefore, we expect we will continue to seek international growth opportunities where we believe our risk-adjusted return objectives can be

5

achieved. We strive to maintain a diversified approach to our international growth strategy by complementing our presence in emerging markets with operations in more developed and established markets, which enables us to leverage multiple stages of wireless network development throughout our global footprint. Our international growth strategy includes a disciplined, individualized market evaluation, in which we conduct the following analyses:

| • | Country analysis. Prior to entering a new market, we conduct an extensive review of the country's historical and projected macroeconomic fundamentals, including inflation outlook and foreign currency exchange rate trends, capital markets, tax regime and investment alternatives, and the general business, political and legal environments, including property rights and regulatory regime. |

| • | Wireless industry analysis. To confirm the presence of sufficient demand to support an independent tower company, we analyze the competitiveness of the country's wireless market, such as the pricing environment, past and potential industry consolidation and the stage of its wireless network development. Characteristics that result in an attractive investment opportunity include (i) multiple competitive wireless service providers who are actively seeking to invest in deploying voice and data networks and (ii) incremental spectrum from auctions that have occurred or are anticipated to occur is being, or will be, deployed. |

| • | Opportunity and counterparty analysis. Once an investment opportunity is identified within a geographic area with an attractive wireless industry, we conduct a multifaceted opportunity and counterparty analysis. This includes evaluating (i) the type of transaction, (ii) its ability to meet our risk-adjusted return criteria given the country and the counterparties involved, including the anticipated anchor tenant and (iii) how the transaction fits within our long-term strategic objectives, including future potential investment and expansion within the region. |

Recent Transactions

Acquisitions

From January 1, 2014 through December 31, 2014, we increased our communications site portfolio by approximately 8,450 sites, including approximately 3,133 build-to-suits, and we believe the assets constructed and acquired will be accretive to our consolidated operating margins. Significant acquisitions during the year ended December 31, 2014 included the acquisition of (i) 100% of the equity interests of BR Towers S.A., a Brazilian telecommunications real estate company ("BR Towers"), which at closing owned, or held exclusive use rights for, 4,617 towers and 47 property interests in Brazil and (ii) entities holding a portfolio of 59 communications sites, which at the time of acquisition were leased primarily to radio and television broadcast tenants, and four property interests in the United States from Richland Properties LLC and other related entities ("Richland").

In addition, during the fourth quarter of 2014, we signed definitive agreements to acquire approximately 11,280 additional communications sites in Brazil and Nigeria, and in February 2015, we signed a definitive agreement for the Proposed Verizon Transaction to acquire the exclusive right to lease, acquire or otherwise operate and manage up to 11,489 wireless communications sites in the United States.

We continue to evaluate potential complementary services to supplement our growth and expansion strategy, as well as opportunities to acquire communications real estate portfolios that we believe we can effectively integrate into our existing business. For more information about our acquisitions, see note 6 to our consolidated financial statements included in this Annual Report.

Financing Transactions

During the year ended December 31, 2014, to complement our operational strategy to selectively invest in and grow our communications real estate portfolio, we strengthened our balance sheet by completing a number of

6

key financing initiatives, including those set forth below. For more information about our financing transactions, see Item 7 of this Annual Report under the caption "Management's Discussion and Analysis of Financial Condition and Results of Operations-Liquidity and Capital Resources" and note 8 to our consolidated financial statements included in this Annual Report.

Senior Notes Offerings. In January 2014, we completed a registered public offering through a reopening of our (i) 3.40% senior unsecured notes due 2019 (the "3.40% Notes"), in an aggregate principal amount of $250.0 million and our (ii) 5.00% senior unsecured notes due 2024 (the "5.00% Notes"), in an aggregate principal amount of $500.0 million. In August 2014, we completed a registered public offering of our 3.450% senior unsecured notes due 2021 (the "3.450% Notes") in an aggregate principal amount of $650.0 million. We used the net proceeds from each offering primarily to repay certain indebtedness under our existing credit facilities.

Mandatory Convertible Preferred Stock Offering. In May 2014, we completed a registered public offering of 6,000,000 shares of our 5.25% Mandatory Convertible Preferred Stock, Series A, par value $0.01 per share (the "Mandatory Convertible Preferred Stock"). We used the net proceeds from the offering to fund acquisitions initially funded by indebtedness incurred under our $2.0 billion multi-currency senior unsecured revolving credit facility (the "2013 Credit Facility").

Credit Facilities. In September 2014, we entered into an amendment and restatement of our $1.0 billion senior unsecured revolving credit facility (the "2012 Credit Facility", as amended and restated, the "2014 Credit Facility"), which, among other things, increased the commitments thereunder to $1.5 billion and extended the maturity date to January 31, 2020. As a result, as of December 31, 2014, we had the ability to borrow up to $2.4 billion under our existing credit facilities, net of any outstanding letters of credit.

Regulatory Matters

Towers and Antennas. Our domestic and international tower business is subject to national, state and local regulatory requirements with respect to the registration, siting, construction, lighting, marking and maintenance of our towers. In the United States, which accounted for approximately 66% of our total rental and management revenue for the year ended December 31, 2014, the construction of new towers or modifications to existing towers may require pre-approval by the Federal Communications Commission ("FCC") and the Federal Aviation Administration ("FAA"), depending on factors such as tower height and proximity to public airfields. Towers requiring pre-approval must be registered with the FCC and maintained in accordance with FAA standards. Similar requirements regarding pre-approval of the construction and modification of towers are imposed by regulators in other countries. Non-compliance with applicable tower-related requirements may lead to monetary penalties or site deconstruction orders.

Furthermore, in India, each of our subsidiaries holds an Infrastructure Provider Category-I license ("IP-I") issued by the Indian Ministry of Communications and Information Technology, which permits us to provide tower space to companies licensed as telecommunications service providers under the Indian Telegraph Act of 1885. As a condition to the IP-I, the Indian government has the right to take over telecommunications infrastructure in the case of emergency or war. In Ghana, our subsidiary holds a Communications Infrastructure License, issued by the National Communications Authority ("NCA"), which permits us to establish and maintain passive telecommunications infrastructure services and DAS networks for communications service providers licensed by the NCA. While we are required to provide tower space on a non-discriminatory basis, we may negotiate mutually agreeable terms and conditions with such service providers. In Chile, our subsidiary is classified as a Telecom Intermediate Service Provider. We have received a number of site specific concessions and are working with the Chilean Subsecretaria de Telecommunicaciones to receive concessions on our remaining sites in Chile.

Our international business operations may be subject to increased licensing fees or ownership restrictions. For example, in South Africa, the Broad-Based Black Economic Empowerment Act, 2003 (the "BBBEE Act")

7

has established a legislative framework for the promotion of economic empowerment of South African citizens disadvantaged by Apartheid. Accordingly, the BBBEE Act and related codes measure BBBEE Act compliance and good corporate practice by the inclusion of certain ownership, management control, employment equity and other metrics for companies that do business there. In addition, certain municipalities have sought to impose permit fees based upon structural or operational requirements of towers. Our foreign operations may be affected if a country's regulatory authority restricts or revokes spectrum licenses of certain wireless service providers or implements limitations on foreign ownership.

In all countries where we operate, we are subject to zoning restrictions and restrictive covenants imposed by local authorities or community organizations. While these regulations vary, they typically require tower owners or tenants to obtain approval from local authorities or community standards organizations prior to tower construction or the addition of a new antenna to an existing tower. Local zoning authorities and community residents often oppose construction in their communities, which can delay or prevent new tower construction, new antenna installation or site upgrade projects, thereby limiting our ability to respond to tenant demand. In addition, zoning regulations can increase costs associated with new tower construction, tower modifications, and additions of new antennas to a site or site upgrades. Existing regulatory policies may adversely affect the associated timing or cost of such projects and additional regulations may be adopted that cause delays or result in additional costs to us. These factors could materially and adversely affect our construction activities and operations. In the United States, the Telecommunications Act of 1996 prohibits any action by state and local authorities that would discriminate between different providers of wireless services or ban altogether the construction, modification or placement of communications sites. It also prohibits state or local restrictions based on the environmental effects of radio frequency emissions to the extent the facilities comply with FCC regulations. Further, in February 2012, the United States government adopted regulations requiring that local and state governments approve modifications or collocations that qualify as eligible facilities under the regulations.

Portions of our business are subject to additional regulations, for example, in a number of states throughout the United States, certain of our subsidiaries hold Competitive Local Exchange Carrier (CLEC) or other status, in connection with the operation of our outdoor DAS networks business. In addition, we or our domestic and international tenants may be subject to new regulatory policies in certain jurisdictions from time to time that may materially and adversely affect our business or the demand for our communications sites.

Environmental Matters. Our domestic and international operations are subject to various national, state and local environmental laws and regulations, including those relating to the management, use, storage, disposal, emission and remediation of, and exposure to, hazardous and non-hazardous substances, materials and wastes and the siting of our towers. We may be required to obtain permits, pay additional property taxes, comply with regulatory requirements and make certain informational filings related to hazardous substances or devices used to provide power such as batteries, generators and fuel at our sites. Violations of these types of regulations could subject us to fines or criminal sanctions.

Additionally, in the United States and many other international markets where we do business, before constructing a new tower or adding an antenna to an existing site, we must review and evaluate the impact of the action to determine whether it may significantly affect the environment and whether we must disclose any significant impacts in an environmental assessment. If a tower or new antenna might have a material adverse impact on the environment, FCC or other governmental approval of the tower or antenna could be significantly delayed.

Health and Safety. In the United States and in other countries where we operate, we are subject to various national, state and local laws regarding employee health and safety, including protection from radio frequency exposure.

8

Competition

We compete, both for new business and for the acquisition of assets, with other public tower companies, such as Crown Castle International Corp., SBA Communications Corporation and GTL Infrastructure Limited, wireless carrier tower consortia such as Indus Towers and private tower companies, independent wireless carriers, tower owners, broadcasters and owners of non-communications sites, including rooftops, utility towers, water towers and other alternative structures. We believe that site location and capacity, network density, price, quality and speed of service have been, and will continue to be, significant competitive factors affecting owners, operators and managers of communications sites.

Our network development services business competes with a variety of companies offering individual, or combinations of, competing services. The field of competitors includes site acquisition consultants, zoning consultants, real estate firms, right-of-way consultants, structural engineering firms, tower owners/managers, telecommunications equipment vendors who can provide turnkey site development services through multiple subcontractors and our tenants' personnel. We believe that our tenants base their decisions for network development services on various criteria, including a company's experience, local reputation, price and time for completion of a project.

Customer Demand

Our strategy is predicated on the belief that wireless service providers will continue to invest in the coverage, quality and capacity of their networks in both our domestic and international markets, driving demand for our communications sites.

| • | Domestic wireless network investments. According to industry data, aggregate annual wireless capital spending in the United States has averaged over $30 billion over the past three years, resulting in consistent demand for our sites. Demand for our domestic communications sites is driven by: |

| • | Increasing wireless data usage, which continues to incentivize wireless service providers to focus on network quality and make incremental investments in the coverage and capacity of their networks; |

| • | Subscriber adoption of advanced wireless data applications such as mobile Internet and video, increasingly advanced devices and the corresponding deployments and densification of advanced networks by wireless service providers to satisfy this incremental demand for high-bandwidth wireless data; |

| • | Deployment of newly acquired spectrum; and |

| • | Deployment of wireless and backhaul networks by new market entrants. |

As consumer demand for and use of advanced wireless services in the United States grow, wireless service providers may be compelled to deploy new technology and equipment, further increase the cell density of their existing networks and expand their network coverage.

| • | International wireless network investments. The wireless networks in most of our international markets are typically less advanced than those in our domestic market with respect to the density of voice networks and the current technologies generally deployed for wireless services. Accordingly, demand for our international communications sites is primarily driven by: |

| • | Incumbent wireless service providers investing in existing voice networks to improve or expand their coverage and increase capacity; |

| • | In certain of our international markets, increasing subscriber adoption of wireless data applications, such as email, Internet and video; |

| • | Spectrum auctions, which result in new market entrants, as well as initial and incremental data network deployments; and |

| • | The increasing availability of lower cost smartphones internationally. |

9

We believe demand for our communications sites will continue as wireless service providers seek to increase the quality, coverage area and capacity of their existing networks, while also investing in next generation data networks. To meet these network objectives, we believe wireless carriers will continue to outsource their communications site infrastructure needs as a means to accelerate network development and more efficiently use their capital, rather than construct and operate their own communications sites and maintain their own communications site operation and development capabilities. In addition, because our network development services are complementary to our rental and management business, we believe demand for our network development services will continue, consistent with industry trends.

Any increase in the use of network sharing, roaming or resale arrangements by wireless service providers could adversely affect customer demand for tower space. These arrangements enable a provider to serve its customers outside the provider's license area, to give licensed providers the right to enter into arrangements to serve overlapping license areas and to permit non-licensed providers to enter the wireless marketplace. Consolidation among wireless carriers could similarly impact customer demand for our communications sites because the existing networks of wireless carriers often overlap. In addition, wireless carriers sharing their sites or permitting equipment location swapping on their sites with other carriers to a significant degree could reduce demand for our communications sites. Further, our tenants may be subject to new regulatory policies from time to time that materially and adversely affect the demand for our communications sites.

In addition, our customer demand could be adversely affected by the emergence and growth of new technologies, which could make it possible for wireless carriers to increase the capacity and efficiency of their existing networks without the need for incremental cell sites. The increased use of spectrally efficient technologies or the availability of significant incremental spectrum in the marketplace could potentially relieve a portion of our tenants' network capacity problems, and as a result, could reduce the demand for tower-based antenna space. Additionally, certain complementary network technologies, such as small cell deployments, could shift a portion of our tenants' network investments away from the traditional tower-based networks, which may reduce the need for carriers to add more equipment at certain communications sites.

Employees

As of December 31, 2014, we employed 2,974 full-time individuals and consider our employee relations to be satisfactory.

Available Information

Our Internet website address is www.americantower.com . Information contained on our website is not incorporated by reference into this Annual Report, and you should not consider information contained on our website as part of this Annual Report. You may access, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, plus amendments to such reports as filed or furnished pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended ("Exchange Act"), through the "Investor Relations" portion of our website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission ("SEC").

We have adopted a written Code of Ethics and Business Conduct Policy (the "Code of Conduct") that applies to all of our employees and directors, including, but not limited to, our principal executive officer, principal financial officer and principal accounting officer or controller or persons performing similar functions. The Code of Conduct, our corporate governance guidelines and the charters of the audit, compensation and nominating and corporate governance committees of our Board of Directors are available at the "Investor Relations" portion of our website. In the event we amend the Code of Conduct, or provide any waivers under the Code of Conduct to our directors or executive officers, we will disclose these events on our website as required by the regulations of the New York Stock Exchange (the "NYSE") and applicable law.

10

In addition, paper copies of these documents may be obtained free of charge by writing us at the following address: 116 Huntington Avenue, Boston, Massachusetts 02116, Attention: Investor Relations; or by calling us at (617) 375-7500.

| ITEM 1A. | RISK FACTORS |

Decrease in demand for our communications sites would materially and adversely affect our operating results, and we cannot control that demand.

Factors affecting the demand for our communications sites and, to a lesser extent, our network development services, could materially and adversely affect our operating results. Those factors include:

| • | increased use of network sharing without compensation to us, roaming or resale arrangements by wireless service providers; |

| • | mergers or consolidations among wireless service providers; |

| • | zoning, environmental, health or other government regulations or changes in the application and enforcement thereof; |

| • | governmental licensing of spectrum or restricting or revoking spectrum licenses; |

| • | a decrease in consumer demand for wireless services due to general economic conditions or other factors, including inflation; |

| • | the ability and willingness of wireless service providers to maintain or increase capital expenditures on network infrastructure; |

| • | the financial condition of wireless service providers; |

| • | delays or changes in the deployment of next generation wireless technologies; and |

| • | technological changes. |

Any downturn in the economy or disruption in the financial and credit markets could impact consumer demand for wireless services. If wireless service subscribers significantly reduce their minutes of use, or fail to widely adopt and use wireless data applications, our wireless service provider tenants could experience a decrease in demand for their services. As a result, our tenants may scale back their capital expenditure plans, which could materially and adversely affect leasing demand for our communications sites and our network development services business, which could have a material adverse effect on our business, results of operations or financial condition.

If our tenants share site infrastructure to a significant degree or consolidate or merge, our growth, revenue and ability to generate positive cash flows could be materially and adversely affected.

Extensive sharing of site infrastructure, roaming or resale arrangements among wireless service providers as an alternative to leasing our communications sites without compensation to us may cause new lease activity to slow if carriers utilize shared equipment rather than deploy new equipment, or may result in the decommissioning of equipment on certain existing sites because portions of the tenants' networks may become redundant. In addition, significant consolidation among our tenants may materially and adversely affect our growth and revenues. Certain combined companies have rationalized duplicative parts of their networks or modernized their networks, and these and other tenants could determine not to renew leases with us as a result. Our ongoing contractual revenues and our future results may be negatively impacted if a significant number of these leases are not renewed.

Increasing competition for tenants in the tower industry may materially and adversely affect our pricing.

Our industry is highly competitive and our tenants have numerous alternatives in leasing antenna space. Competitive pricing for tenants on towers from competitors could materially and adversely affect our lease rates.

11

We may not be able to renew existing tenant leases or enter into new tenant leases, or if we are able to renew or enter new leases, it may be at rates lower than our current rates, resulting in a material adverse impact on our results of operations and growth rate. In addition, should inflation rates exceed our fixed escalator percentages in markets where the majority of our leases include fixed escalators, our income would be adversely affected. Increasing competition for tenants or significant increases in inflation rates could materially and adversely affect our business, results of operations or financial condition.

Competition for assets could adversely affect our ability to achieve our return on investment criteria.

We may experience increased competition, which could make the acquisition of high quality assets significantly more costly. Some of our competitors are larger and may have greater financial resources than we do, while other competitors may apply lower investment criteria than we do. In addition, we may not anticipate increased competition entering a particular market or competing for the same assets. Higher prices for assets could make it more difficult to achieve our return on investment criteria, which could materially and adversely affect our business, results of operations or financial condition.

Our business is subject to government regulations and changes in current or future laws or regulations could restrict our ability to operate our business as we currently do.

Our business and that of our tenants are subject to federal, state, local and foreign regulations. In certain jurisdictions, these regulations could be applied or enforced retroactively, which could require that we modify or dismantle an existing tower. Zoning authorities and community organizations are often opposed to the construction in their communities, which can delay, prevent or increase the cost of new tower construction, modifications, additions of new antennas to a site or site upgrades, thereby limiting our ability to respond to tenant demands and requirements. In addition, in certain foreign jurisdictions, we are required to pay annual license fees, and these fees may be subject to substantial increases by the government. Foreign jurisdictions in which we operate and currently are not required to pay license fees may enact license fees, which may apply retroactively. In certain foreign jurisdictions, there may be changes to zoning regulations or construction laws based on site location, which may result in increased costs to modify certain of our existing towers or decreased revenue due to the removal of certain towers to ensure compliance with such changes. Existing regulatory policies may materially and adversely affect the associated timing or cost of construction projects associated with our communications sites and additional regulations may be adopted that increase delays or result in additional costs to us, or that prevent such projects in certain locations. Furthermore, the tax laws, regulations and interpretations governing REITs may change at any time, perhaps with retroactive effect. In addition, some of these changes could have a more significant impact on us as compared to other REITs due to the nature of our business and our use of TRSs. These factors could materially and adversely affect our business, results of operations or financial condition. Furthermore, some foreign jurisdictions have implemented regulations governing investment funds or their managers, which may be interpreted to apply to REITs, and there is uncertainty as to the interpretation and implementation of these regulations.

Our leverage and debt service obligations may materially and adversely affect us.

Our leverage could render us unable to generate cash sufficient to pay when due the principal of, interest on, or other amounts due with respect to, our indebtedness. We are also permitted, subject to certain restrictions under our existing indebtedness, to draw down on our credit facilities and obtain additional long-term debt and working capital lines of credit to meet future financing needs.

Our leverage could have significant negative consequences to our business, results of operations or financial condition, including:

| • | impairing our ability to meet one or more of the financial ratio covenants contained in our debt agreements or to generate cash sufficient to pay interest or principal due under those agreements, which could result in an acceleration of some or all of our outstanding debt and the loss of the towers securing such debt if an uncured default occurs; |

12

| • | increasing our borrowing costs if our current investment grade debt ratings decline; |

| • | placing us at a possible competitive disadvantage to less leveraged competitors and competitors that may have better access to capital resources, including with respect to acquiring assets; |

| • | limiting our ability to obtain additional debt or equity financing, thereby increasing our vulnerability to general adverse economic and industry conditions; |

| • | requiring the dedication of a substantial portion of our cash flow from operations to service our debt, thereby reducing the amount of our cash flow available for other purposes, including capital expenditures, REIT distributions and preferred stock dividends; |

| • | requiring us to issue debt or equity securities or to sell some of our core assets, possibly on unfavorable terms, to meet payment obligations; |

| • | limiting our flexibility in planning for, or reacting to, changes in our business and the markets in which we compete; and |

| • | limiting our ability to repurchase our common stock or make distributions to our stockholders. |

In addition, to meet the REIT distribution requirements and maintain our qualification and taxation as a REIT, we may need to borrow funds, even if the then-prevailing market conditions are not favorable, and the REIT distribution requirements may increase the financing we need to fund capital expenditures, future growth and expansion initiatives. This would increase our total leverage.

Failure to successfully and efficiently integrate acquired or leased assets, including from the Proposed Verizon Transaction (the "Verizon Assets"), into our operations may adversely affect our business, operations and financial condition.

Integrating acquired portfolios of communications sites may require significant resources, as well as attention from our management team. In addition, we may incur certain non-recurring charges associated with the integration of acquired or leased assets or businesses into our operations. Further, the significant acquisition-related integration costs could materially and adversely affect our results of operations in the period in which such charges are recorded or our cash flow in the period in which any related costs are actually paid. For example, the integration of the Verizon Assets, which includes up to 11,489 towers, into our operations will be a significant undertaking, and we anticipate that we will incur certain non-recurring charges associated with the integration of the Verizon Assets into our operations, including costs for tasks such as tower visits and audits and ground and tenant lease verifications. Additional integration challenges include:

| • | transitioning all data related to the Verizon Assets, tenants and landlords to a common information technology system; |

| • | successfully marketing space on the Verizon Assets; |

| • | successfully transitioning the ground lease rent payment and the tenant billing and collection processes; |

| • | retaining existing tenants on the Verizon Assets; and |

| • | maintaining our standards, controls, procedures and policies with respect to the Verizon Assets. |

Additionally, we may fail to successfully integrate the assets we acquire or fail to utilize such assets to their full capacity. If we are not able to meet these integration challenges, we may not realize the benefits we expect from our acquired portfolios and businesses, including the Proposed Verizon Transaction, and our business, financial condition and results of operations will be adversely affected.

13

Our expansion initiatives involve a number of risks and uncertainties that could adversely affect our operating results, disrupt our operations or expose us to additional risk.

As we continue to acquire communications sites in our existing markets and expand into new markets, we are subject to a number of risks and uncertainties, including not meeting our return on investment criteria and financial objectives, increased costs, assumed liabilities and the diversion of managerial attention due to acquisitions. Achieving the benefits of acquisitions depends in part on timely and efficiently integrating operations, communications tower portfolios and personnel. Integration may be difficult and unpredictable for many reasons, including, among other things, differing systems and processes, cultural differences, customary business practices and conflicting policies, procedures and operations. In addition, integrating businesses may significantly burden management and internal resources, including the potential loss or unavailability of key personnel.

Furthermore, our international expansion initiatives are subject to additional risks such as those described in the risk factor immediately below, some of which may require additional resources and personnel.

In addition, as a result of prior acquisitions, we have a substantial amount of intangible assets and goodwill. In accordance with accounting principles generally accepted in the United States ("GAAP"), we are required to assess our goodwill and other intangible assets annually or more frequently in the event of circumstances indicating potential impairment to determine if they are impaired. If the testing performed indicates that an asset may not be recoverable, we are required to record a non-cash impairment charge for the difference between the carrying value of the goodwill or other intangible assets and the implied fair value of the goodwill or the estimated fair value of other intangible assets in the period the determination is made.

Our expansion initiatives may not be successful or we may be required to record impairment charges for our goodwill or for other intangible assets, which could have a material adverse effect on our business, results of operations or financial condition.

Our foreign operations are subject to economic, political and other risks that could materially and adversely affect our revenues or financial position, including risks associated with fluctuations in foreign currency exchange rates.

Our international business operations and our expansion into new markets in the future could result in adverse financial consequences and operational problems not typically experienced in the United States. We anticipate that our revenues from our international operations will continue to grow. Accordingly, our business is subject to risks associated with doing business internationally, including:

| • | changes to existing or new tax laws or methodologies impacting our international operations, or fees directed specifically at the ownership and operation of communications sites or our international acquisitions, any of which may be applied or enforced retroactively; |

| • | laws or regulations that tax or otherwise restrict repatriation of earnings or other funds or otherwise limit distributions of capital; |

| • | changes in a specific country's or region's political or economic conditions, including inflation or currency devaluation; |

| • | changes to zoning regulations or construction laws, which could be applied retroactively to our existing communications sites; |

| • | expropriation or governmental regulation restricting foreign ownership or requiring reversion or divestiture; |

| • | actions restricting or revoking spectrum licenses or suspending or terminating business under prior licenses; |

14

| • | failure to comply with anti-bribery laws such as the Foreign Corrupt Practices Act or similar local anti-bribery laws, or Office of Foreign Assets Control requirements; |

| • | material site security issues; |

| • | significant license surcharges; |

| • | increases in the cost of labor (as a result of unionization or otherwise), power and other goods and services required for our operations; |

| • | price setting or other similar laws for the sharing of passive infrastructure; and |

| • | uncertain or inconsistent laws, regulations, rulings or results from legal or judicial systems, which may be enforced retroactively, and delays in the judicial process. |

We also face risks associated with changes in foreign currency exchange rates, including those arising from our operations, investments and financing transactions related to our international business. Volatility in foreign currency exchange rates can also affect our ability to plan, forecast and budget for our international operations and expansion efforts. Our revenues earned from our international operations are primarily denominated in their respective local currencies. We have not historically engaged in significant currency hedging activities relating to our non-U.S. Dollar operations, and a weakening of these foreign currencies against the U.S. Dollar would negatively impact our reported revenues, operating profits and income.

In our international operations, many of our tenants are subsidiaries of global telecommunications companies. These subsidiaries may not have the explicit or implied financial support of their parent entities.

In addition, as we continue to invest in joint venture opportunities internationally, our partners may have business or economic goals that are inconsistent with ours, be in positions to take action contrary to our interests, policies or objectives, have competing interests in our, or other, markets that could create conflict of interest issues, withhold consents contrary to our requests or become unable or unwilling to fulfill their commitments, any of which could expose us to additional liabilities or costs, including requiring us to assume and fulfill the obligations of that joint venture.

A substantial portion of our revenue is derived from a small number of tenants, and we are sensitive to changes in the creditworthiness and financial strength of our tenants.

A substantial portion of our total operating revenues is derived from a small number of tenants. If any of these tenants is unwilling or unable to perform its obligations under our agreements with it, our revenues, results of operations, financial condition and liquidity could be materially and adversely affected. In the ordinary course of our business, we do occasionally experience disputes with our tenants, generally regarding the interpretation of terms in our leases. Historically, we have resolved these disputes in a manner that did not have a material adverse effect on us or our tenant relationships. However, it is possible that such disputes could lead to a termination of our leases with tenants or a material modification of the terms of those leases, either of which could have a material adverse effect on our business, results of operations or financial condition. If we are forced to resolve any of these disputes through litigation, our relationship with the applicable tenant could be terminated or damaged, which could lead to decreased revenue or increased costs, resulting in a corresponding adverse effect on our business, results of operations or financial condition.

Due to the long-term nature of our tenant leases, we depend on the continued financial strength of our tenants. Many wireless service providers operate with substantial leverage. Sometimes our tenants, or their parent companies, face financial difficulty or file for bankruptcy.

In addition, many of our tenants and potential tenants rely on capital raising activities to fund their operations and capital expenditures, which may be more difficult or expensive in the event of downturns in the economy or disruptions in the financial and credit markets. If our tenants or potential tenants are unable to raise

15

adequate capital to fund their business plans, they may reduce their spending, which could materially and adversely affect demand for our communications sites and our network development services business. If, as a result of a prolonged economic downturn or otherwise, one or more of our significant tenants experienced financial difficulties or filed for bankruptcy, it could result in uncollectible accounts receivable and an impairment of our deferred rent asset, tower asset, network location intangible asset or customer-related intangible asset. The loss of significant tenants, or the loss of all or a portion of our anticipated lease revenues from certain tenants, could have a material adverse effect on our business, results of operations or financial condition.

New technologies or changes in a tenant's business model could make our tower leasing business less desirable and result in decreasing revenues.

The development and implementation of new technologies designed to enhance the efficiency of wireless networks or changes in a tenant's business model could reduce the need for tower-based wireless services, decrease demand for tower space or reduce previously obtainable lease rates. In addition, tenants may have less of their budgets allocated to lease space on our towers, as the industry is trending towards deploying increased capital to the development and implementation of new technologies. Examples of these technologies include spectrally efficient technologies, which could relieve a portion of our tenants' network capacity needs and as a result, could reduce the demand for tower-based antenna space. Additionally, certain small cell complementary network technologies could shift a portion of our tenants' network investments away from the traditional tower-based networks, which may reduce the need for carriers to add more equipment at certain communications sites. Moreover, the emergence of alternative technologies could reduce the need for tower-based broadcast services transmission and reception. Further, a tenant may decide to no longer outsource tower infrastructure or otherwise change its business model, which would result in a decrease in our revenue. The development and implementation of any of these and similar technologies to any significant degree or changes in a tenant's business model could have a material adverse effect on our business, results of operations or financial condition.

If we fail to remain qualified as a REIT, we will be subject to tax at corporate income tax rates, which may substantially reduce funds otherwise available.

Effective for the taxable year beginning January 1, 2012, we began operating as a REIT for federal income tax purposes. If we fail to remain qualified as a REIT, we will be taxed at corporate income tax rates unless certain relief provisions apply.

Qualification as a REIT requires the application of certain highly technical and complex provisions of the Internal Revenue Code of 1986, as amended (the "Code"), which provisions may change from time to time, to our operations as well as various factual determinations concerning matters and circumstances not entirely within our control. Further, tax reform proposals, if enacted, may adversely affect our ability to remain qualified as a REIT or the benefits of remaining so qualified. There are limited judicial or administrative interpretations of the relevant provisions of the Code.

If, in any taxable year, we fail to qualify for taxation as a REIT and are not entitled to relief under the Code:

| • | we will not be allowed a deduction for distributions to stockholders in computing our taxable income; |

| • | we will be subject to federal and state income tax, including any applicable alternative minimum tax, on our taxable income at regular corporate tax rates; and |

| • | we will be disqualified from REIT tax treatment for the four taxable years immediately following the year during which we were so disqualified. |

Any corporate tax liability could be substantial and would reduce the amount of cash available for other purposes. If we fail to qualify for taxation as a REIT, we may need to borrow additional funds or liquidate some

16

investments to pay any additional tax liability. Accordingly, funds available for investment, operations and distribution would be reduced.

Furthermore, as a result of our acquisition of MIP Tower Holdings LLC ("MIPT"), we own an interest in a subsidiary REIT. The subsidiary REIT is independently subject to, and must comply with, the same REIT requirements that we must satisfy in order to qualify as a REIT, together with all other rules applicable to REITs. If the subsidiary REIT fails to qualify as a REIT, and certain relief provisions do not apply, then (i) the subsidiary REIT would become subject to federal income tax, (ii) the subsidiary REIT will be disqualified from treatment as a REIT for the four taxable years immediately following the year during which qualification was lost, (iii) our ownership of shares in such subsidiary REIT will cease to be a qualifying asset for purposes of the asset tests applicable to REITs and any dividend income or gains derived by us from such subsidiary REIT may cease to be treated as income that qualifies for purposes of the 75% gross income test and (iv) we may fail certain of the asset tests applicable to REITs, in which event we will fail to qualify as a REIT unless we are able to avail ourselves of specified relief provisions.

Complying with REIT requirements may limit our flexibility or cause us to forego otherwise attractive opportunities.

Our use of TRSs enables us to engage in non-REIT qualifying business activities. Under the Code, no more than 25% of the value of the assets of a REIT may be represented by securities of one or more TRSs and other non-qualifying assets. This limitation may hinder our ability to make certain attractive investments, including the purchase of non-qualifying assets, the expansion of non-real estate activities and investments in the businesses to be conducted by our TRSs, and to that extent limit our opportunities and our flexibility to change our business strategy.