| ||||

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

T Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended December 31, 2015

OR

£ Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from to

Commission File No. 1-13696

AK STEEL HOLDING CORPORATION

(Exact name of registrant as specified in its charter)

Delaware |

| 31-1401455 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

9227 Centre Pointe Drive, West Chester, Ohio |

| 45069 |

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code: (513) 425-5000

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class |

| Name of Each Exchange on Which Registered |

Common Stock $0.01 Par Value |

| New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes T No £

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes £ No T

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes T No £

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes T No £

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. T

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

Large accelerated filer | T |

| Accelerated filer | £ |

Non-accelerated filer | £ |

| Smaller reporting company | £ |

Indicate by check mark whether the registrant is a shell company, as defined in Rule 12b-2 of the Securities Exchange Act of 1934. Yes £ No T

Aggregate market value of the registrant's voting stock held by non-affiliates at June 30, 2015 : $680,365,760

There were 178,344,667 shares of common stock outstanding as of February 17, 2016 .

DOCUMENTS INCORPORATED BY REFERENCE

The information required to be furnished pursuant to Part III of this Form 10-K will be set forth in, and incorporated by reference from, the registrant's definitive proxy statement for the annual meeting of stockholders (the " 2016 Proxy Statement"), which will be filed with the Securities and Exchange Commission not later than 120 days after the end of the fiscal year ended December 31, 2015 .

|

|

|

|

|

AK Steel Holding Corporation

Table of Contents

|

| Page |

PART I |

|

|

|

|

|

Item 1. | Business | 1 |

Item 1A. | Risk Factors | 5 |

Item 1B. | Unresolved Staff Comments | 10 |

Item 2. | Properties | 10 |

Item 3. | Legal Proceedings | 11 |

Item 4. | Mine Safety Disclosures | 11 |

|

|

|

PART II |

|

|

|

|

|

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 12 |

Item 6. | Selected Financial Data | 14 |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 14 |

Item 7A. | Quantitative and Qualitative Disclosure about Market Risk | 32 |

Item 8. | Financial Statements and Supplementary Data | 34 |

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 84 |

Item 9A. | Controls and Procedures | 84 |

Item 9B. | Other Information | 87 |

|

|

|

PART III |

|

|

|

|

|

Item 10. | Directors, Executive Officers and Corporate Governance | 87 |

Item 11. | Executive Compensation | 87 |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 87 |

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 87 |

Item 14. | Principal Accounting Fees and Services | 87 |

|

|

|

PART IV |

|

|

|

|

|

Item 15. | Exhibits, Financial Statement Schedules | 89 |

|

|

|

| Signatures | 95 |

- i -

Table of Contents

(Dollars in millions, except per share and per ton amounts or as otherwise specifically noted)

PART I

Item 1. | Business. |

Operations Overview

AK Steel Holding Corporation ("AK Holding") is a corporation formed under the laws of Delaware in 1993 and is an integrated producer of flat-rolled carbon, stainless and electrical steels and tubular products through its wholly-owned subsidiary, AK Steel Corporation ("AK Steel"). AK Steel is the successor through merger in 1999 to Armco Inc., which was formed in 1900. Unless the context indicates otherwise, references to "we," "us" and "our" refer to AK Holding and its subsidiaries.

We operate eight steelmaking and finishing plants, two coke plants and two tube manufacturing plants across six states-Indiana, Kentucky, Michigan, Ohio, Pennsylvania and West Virginia. These operations produce flat-rolled carbon, specialty stainless and electrical steels that we sell in sheet and strip form, and carbon and stainless steel that we finish into welded steel tubing. We also produce metallurgical coal through our AK Coal Resources, Inc. ("AK Coal") subsidiary. In addition, we operate trading companies in Mexico and Europe that buy and sell steel and steel products and other materials.

In 2014, we acquired Severstal Dearborn, LLC ("Dearborn"). The assets acquired include the integrated steelmaking assets located in Dearborn, Michigan ("Dearborn Works"), the Mountain State Carbon, LLC ("Mountain State Carbon") cokemaking facility located in Follansbee, West Virginia, and interests in joint ventures that process flat-rolled steel products.

Customers and Markets

We sell flat-rolled carbon steel products, consisting of coated, cold-rolled, and hot-rolled carbon steel products, primarily to automotive manufacturers and their suppliers, as well as to customers in the infrastructure and manufacturing market. The infrastructure and manufacturing market primarily includes electrical transmission, heating, ventilation and air conditioning equipment, and appliances. We also sell carbon steel products to distributors, service centers and converters, who may further process these products before reselling them. Our goal is to carry appropriate inventory levels that will meet our customers' needs, particularly for the "just-in-time" delivery requirements necessary to service the demanding automotive market. During 2015, we began to implement a strategy to target markets for our carbon steel products that deliver higher margins, where possible, and reduce amounts sold into the lower margin carbon steel spot market, which experienced a sharp decline in pricing as a result of a deluge of low-priced imports of foreign steel. As a result, in late 2015 we temporarily idled the blast furnace and steelmaking operations (the "Hot End") at our Ashland Works in Kentucky to improve capacity utilization at our Middletown Works and our Dearborn Works and our overall profitability.

We sell our stainless steel products to manufacturers and their suppliers in the automotive industry, to manufacturers of food handling, chemical processing, pollution control, medical and health equipment, and to distributors and service centers.

For carbon and stainless steels, we target customers who require the highest quality flat-rolled steel with precise "just-in-time" delivery and technical support. Our enhanced product quality and delivery capabilities, as well as our emphasis on collaborative customer technical support and product planning, are critical factors in our ability to serve these markets.

We sell our electrical steel products in the infrastructure and manufacturing market primarily to manufacturers of power transmission and distribution transformers, both for new and replacement installation. We also sell electrical steel products to manufacturers of electrical motors and generators. We target our electrical steel products to customers who desire the highest quality iron-silicon alloys that provide low core loss and high permeability required for more efficient and economical electrical transformers. Our electrical steels are among the most energy efficient in the world. As with customers of our other steel products, we provide our electrical steel customers outstanding technical support and product development assistance.

For our carbon steel, stainless steel and electrical steel products, we intentionally limit our participation in the commodity portions of those markets, where attributes such as high quality, technical support and innovation are less valued and where selling prices and product margins are generally lower.

Because of our focus on shipments to the automotive industry and our decision to ship fewer tons to the spot market, Ford Motor Company and Fiat Chrysler Automobiles accounted for 12% and 11% of our net sales in 2015. No customer accounted for more than 10% of our net sales in 2014 or 2013. The following table presents the percentage of our net sales to each of our markets:

- 1 -

Table of Contents

Market |

| 2015 |

| 2014 |

| 2013 | |||

Automotive |

| 60 | % |

| 53 | % |

| 51 | % |

Infrastructure and Manufacturing |

| 16 | % |

| 18 | % |

| 20 | % |

Distributors and Converters |

| 24 | % |

| 29 | % |

| 29 | % |

We sell our carbon steel products principally to customers in the United States. We sell our electrical and stainless steel products both domestically and internationally. Our customer base is geographically diverse and there is no single country outside the United States where our sales are material compared to our total net sales. We do not have any material long-lived assets located outside the United States. The following shows net sales by geographic area and as a percentage of worldwide net sales:

|

| 2015 |

| 2014 |

| 2013 | |||||||||||||||

Geographic Area |

| Net Sales |

| % |

| Net Sales |

| % |

| Net Sales |

| % | |||||||||

United States |

| $ | 5,837.2 | |

| 87 | % |

| $ | 5,750.3 | |

| 88 | % |

| $ | 4,862.4 | |

| 87 | % |

Foreign countries |

| 855.7 | |

| 13 | % |

| 755.4 | |

| 12 | % |

| 708.0 | |

| 13 | % | |||

Total |

| $ | 6,692.9 | |

| 100 | % |

| $ | 6,505.7 | |

| 100 | % |

| $ | 5,570.4 | |

| 100 | % |

We shipped approximately 81% of our flat-rolled steel products in 2015 to contract customers, with the balance to customers in the spot market at prevailing prices at the time of sale. We have contracts with all of our major automotive and most of our infrastructure and manufacturing market customers. These contracts include prices for each product during contract periods, which are generally one year or less. In 2015, approximately 58% of our shipments to contract customers allowed price adjustments during the contract period. Changes in steel price indices trigger contract price adjustments for about one-fourth of our shipments to contract customers. When adjustments occur, the resulting adjustments typically occur at three- or six-month intervals. In certain circumstances, we adjust contract prices if particular raw material price changes exceed agreed-upon parameters.

The automotive market is an important element of our business and growth strategy and, therefore, North American light vehicle production has a significant impact on our total sales and shipments. In 2015, automotive manufacturers experienced a record year in North America, as light vehicle production was approximately 17.5 million units, representing a 3% increase from the prior year. The improvement in the automotive market and our increased share of that market resulted in increased sales and shipments of our steel in 2015. We remain keenly focused on capturing additional market share in the automotive sector and most automotive manufacturers are predicting a further increase in total North American light vehicle production volumes for 2016.

In 2015 , housing starts in the United States reached levels not achieved since 2007. We typically benefit from increasing housing starts since it generally results in increased production by power transmission and distribution transformer manufacturers, to whom we sell electrical steels, and appliance manufacturers, to whom we sell stainless and carbon steels. Although we saw improvements in higher value electrical steel prices and demand during 2015 , low prices resulting from the high level of commodity steel imports from foreign producers into the United States resulted in lower shipments to the spot markets. Electrical steel sales and shipments to customers in foreign countries also have been negatively affected by excess global production capacity and what we believe to be preferential trade practices by certain countries that make our products more expensive to sell in that country.

Raw Materials and Other Inputs

Our steel manufacturing operations require iron ore, coal, coke, chrome, nickel, silicon, manganese, zinc, limestone, and carbon and stainless steel scrap as primary raw materials. We also use large volumes of natural gas, electricity and industrial gases. In addition, in past years we have purchased carbon steel slabs from other steel producers to supplement our production from our own steelmaking facilities. We purchased approximately 126,000 tons of carbon steel slabs in 2015 , all of which were purchased in the first quarter of the year. We do not currently anticipate purchasing carbon slabs in 2016.

We typically purchase carbon and stainless steel scrap, natural gas, a substantial portion of our electricity, carbon steel slabs, and most other raw materials at prevailing market prices, which may fluctuate with market supply and demand. However, we make most of our purchases of iron ore, coke, industrial gases and a portion of our electricity at negotiated prices under annual or multi-year agreements with periodic price adjustments. We typically purchase coal under annual fixed-price agreements. Additionally, we may hedge portions of our energy and raw materials purchases to reduce volatility.

We also attempt to reduce the risk of future supply shortages and price volatility in other ways. If multi-year contracts are available in the marketplace, we may use these contracts to secure enough supply to satisfy our key raw material needs. When multi-year contracts are not available, or are not available on acceptable terms, we enter into annual contracts or make spot purchases to meet the remainder of our raw materials needs. We also regularly evaluate using alternative sources and substitute materials.

- 2 -

Table of Contents

We believe that we have secured, or will be able to secure, adequate supply sources for our raw materials and energy requirements for 2016 and for at least the next three to five years. However, our raw material suppliers may experience production disruptions, which could create shortages of raw materials in 2016 or beyond.

Research and Development

We conduct a broad range of research and development activities aimed at improving existing products and manufacturing processes and developing new products and processes. In recent years, we have increased our focus and spending on new product innovation, with particular focus on advanced high-strength steels ("AHSS") for the automotive market. We produce virtually every grade of AHSS that our customers currently need, but our goal is to develop the next generation of AHSS with even greater strength and formability. We have developed many new steel products and steel processes during our history and have recently reinvigorated our focus on research and innovation. For example, we are implementing new process technology to produce both coated and cold-rolled Next-Generation AHSS on the hot-dip galvanizing line at Dearborn Works, which we expect to complete by late 2016. Our goal is to ship Next-Generation AHSS to our customers by early 2017. We have doubled our investment in research and innovation during the past three years from $13.2 in 2013 to $27.6 in 2015 . To accelerate innovation, we are building a new research and innovation center in Middletown, Ohio with completion planned for late 2016. The facility will include pilot lines and feature new operational simulators that replicate critical steel manufacturing operations to allow our researchers, scientists and engineers to continue their leading-edge research, applications engineering, advanced engineering, product development and customer technical services.

Employees

At December 31, 2015 , we employed approximately 8,500 people, of which approximately 6,300 are represented by labor unions. The labor contracts covering these represented employees expire between 2016 and 2019 . See the discussion under Labor Agreements in Item 7 for additional information on these agreements.

Competition

We compete with domestic and foreign flat-rolled carbon, stainless and electrical steel and tubular product producers (both integrated steel producers and mini-mill producers) and producers of plastics, aluminum and other materials that may be used as a substitute for flat-rolled steels in manufactured products. Mini-mills generally offer a narrower range of products than integrated steel mills, but can have some competitive cost advantages as a result of their different production processes and lower labor costs associated with what are often non-union workforces. Price, quality, on-time delivery, customer service and product innovation are the primary competitive factors in the steel industry and vary in relative importance according to the product category and customer requirements.

Steel producers that sell to the automotive market are facing increasing competition from aluminum manufacturers (and, to a lesser extent, other materials) as automotive manufacturers attempt to develop vehicles that will enable them to satisfy more stringent government-imposed fuel efficiency standards. To address automotive manufacturers' lightweighting needs that the aluminum industry is targeting, we and others in the steel industry continue to develop grades of AHSS that we believe are stronger, less costly, more sustainable, easier to repair and more environmentally friendly than aluminum.

Domestic steel producers, including us, face significant competition from foreign producers. For many reasons, these foreign producers often are able to sell products in the United States at prices substantially lower than domestic producers. Depending on the country of production, these reasons may include generous government subsidies; lower labor, raw material, energy and regulatory costs; less stringent environmental regulations; the maintenance of artificially low exchange rates against the U.S. dollar; and preferential trade practices in their home countries. In recent years, the annual level of imports of foreign steel into the United States also has been increasing and is affected to varying degrees by the relative level of overcapacity of steel production in those countries, the strength of demand for steel outside the United States and the relative strength or weakness of the U.S. dollar against various foreign currencies. In 2014 and 2015, and through the first half of 2015 in particular, the combination of overcapacity and slowing domestic demand in countries such as China resulted in imports of low-priced foreign steel into the United States at levels significantly higher than recent historical periods, resulting in increased downward pressure on the price of flat-rolled steels in the American marketplace. Imports of finished steel into the United States accounted for approximately 29% , 28% and 23% of domestic steel market sales in 2015 , 2014 and 2013 . We believe that a large amount of the carbon flat-rolled steel imports into the United States are unfairly traded and we have initiated four trade cases in 2015 and 2016 against a number of importers of carbon and stainless steel. See Trade Cases in Note 10 to the consolidated financial statements for more information.

We continue to provide pension and healthcare benefits to a great number of our retirees, resulting in a competitive disadvantage compared to certain other domestic integrated steel companies and mini-mills that do not provide such benefits to any or most of their retirees. However, we have taken a number of actions to reduce pension and healthcare benefits costs, including negotiating

- 3 -

Table of Contents

progressive labor agreements that have significantly reduced total employment costs at all of our union-represented facilities, transferring all responsibility for healthcare benefits for various groups of retirees to Voluntary Employee Benefits Association trusts, offering voluntary lump-sum settlements to pension plan participants and lowering retiree benefit costs for salaried employees. These actions have increased our ability to compete in the highly competitive global steel market and we continue to seek opportunities to reduce pension and healthcare benefits costs.

Environmental

Information about our environmental compliance, remediation and proceedings is included in Note 10 to the consolidated financial statements in Item 8 and is incorporated herein by reference.

Executive Officers of the Registrant

The following table provides the name, age and principal position of each of our executive officers as of February 17, 2016 :

Name |

| Age |

| Position |

Roger K. Newport |

| 51 |

| Chief Executive Officer |

Kirk W. Reich |

| 47 |

| President and Chief Operating Officer |

Joseph C. Alter |

| 38 |

| Vice President, General Counsel and Corporate Secretary |

Stephanie S. Bisselberg |

| 45 |

| Vice President, Human Resources |

Renee S. Filiatraut |

| 52 |

| Vice President, Litigation, Labor and External Affairs |

Gregory A. Hoffbauer |

| 49 |

| Vice President, Controller and Chief Accounting Officer |

Scott M. Lauschke |

| 46 |

| Vice President, Sales and Customer Service |

Eric S. Petersen |

| 46 |

| Vice President, Research and Innovation |

Maurice A. Reed |

| 53 |

| Vice President, Engineering, Raw Materials and Energy |

Jaime Vasquez |

| 53 |

| Vice President, Finance and Chief Financial Officer |

Roger K. Newport has served as Chief Executive Officer since January 2016. Prior to that Mr. Newport served as Executive Vice President, Finance and Chief Financial Officer since May 2015. Prior to that, Mr. Newport served as Senior Vice President, Finance and Chief Financial Officer since May 2014, as Vice President, Finance and Chief Financial Officer since May 2012 and as Vice President, Business Planning and Development since June 2010. Mr. Newport was named Controller and Chief Accounting Officer in July 2004 and Controller in September 2001. Prior to that, Mr. Newport served in a variety of other capacities since joining us in 1985, including Assistant Treasurer, Investor Relations, Manager-Financial Planning and Analysis, Product Manager, Senior Product Specialist and Senior Auditor.

Kirk W. Reich has served as President and Chief Operating Officer since January 2016. Prior to that Mr. Reich served as Executive Vice President, Manufacturing since May 2015. Before assuming that role, Mr. Reich served as Senior Vice President, Manufacturing since May 2014, as Vice President, Procurement and Supply Chain Management since May 2012 and as Vice President, Specialty Steel Operations since June 2010. Mr. Reich was named General Manager, Middletown Works in October 2006. Prior to that, Mr. Reich served in a variety of other capacities since joining us in 1989, including Manager-Mobile Maintenance/Maintenance Technology, General Manager-Mansfield Works, Manager-Processing and Shipping, Technical Manager, Process Manager and Civil Engineer.

Joseph C. Alter has served as Vice President, General Counsel and Corporate Secretary since May 2015. Prior to that, Mr. Alter served as Vice President, General Counsel and Chief Compliance Officer since May 2014 and Assistant General Counsel, Corporate and Chief Compliance Officer since December 2012. Mr. Alter became Corporate Counsel and Chief Compliance Officer in May 2011. Before joining us as Corporate Counsel in August 2009, Mr. Alter was Corporate Counsel at Convergys Corporation and, before that, an attorney with the law firm of Keating Muething & Klekamp PLL.

Stephanie S. Bisselberg has served as Vice President, Human Resources since April 2013. Prior to that, Ms. Bisselberg served as Assistant General Counsel, Labor from October 2010. She also served as Labor Counsel from January 2005 and Assistant Labor Counsel upon joining us in 2004. Prior to joining us, Ms. Bisselberg was an attorney in the Labor and Employment department of the Cincinnati law firm of Taft, Stettinius and Hollister LLP.

Renee S. Filiatraut has served as Vice President, Litigation, Labor and External Affairs since May 2014. Prior to that, Ms. Filiatraut served as Assistant General Counsel, Litigation since December 2012. Before joining us as Litigation Counsel in March 2011, Ms. Filiatraut was a Partner with Thompson Hine LLP from January 1998.

- 4 -

Table of Contents

Gregory A. Hoffbauer has served as Vice President, Controller and Chief Accounting Officer since January 2016. Prior to that, Mr. Hoffbauer served as Controller and Chief Accounting Officer since February 2013. Before joining us as Assistant Controller in January 2011, Mr. Hoffbauer was Director of Accounting with NewPage Corporation. Mr. Hoffbauer also was Controller for Day International, Inc. and served in a number of increasingly responsible accounting and auditing positions for Deloitte & Touche LLP, including Audit Senior Manager.

Scott Lauschke has served as Vice President, Sales and Customer Service since February 2015. Before joining us, Mr. Lauschke was Vice President and General Manager of AFGlobal Corporation from July 2013 through November 2014. Before that, Mr. Lauschke served in various roles of increasing responsibility at The Timken Company from May 2000, including General Sales Manager from May 2009 through April 2013.

Eric S. Petersen has served as Vice President, Research and Innovation since February 2015. Prior to that, Mr. Petersen was Vice President, Sales and Customer Service since July 2013 as Director, Specialty and International Sales since November 2012 and Director, Research and Innovation since June 2010. He was named Director, Customer Technical Services and Research in March 2007. Prior to that, Mr. Petersen served in a variety of other capacities since joining us in 1991, including General Manager, Quality Assurance; General Manager, Carbon Steel Technology; General Manager, Rockport Works; Manager of various departments at Rockport Works and Middletown Works; Quality Control and Operations Management positions and Associate Process Engineer, Associate Metallurgist and Assistant Metallurgist at Middletown Works.

Maurice A. Reed has served as Vice President, Engineering, Raw Materials and Energy since May 2012. Prior to that, Mr. Reed was Director, Engineering and Raw Materials from March 2011. Prior to that, Mr. Reed served in a variety of other capacities since joining us in 1996, including Director of Engineering and Energy from June 2010, General Manager-Engineering, Operations Support and Primary Process Research from March 2009 and General Manager-Engineering from May 2006. Before joining us, Mr. Reed held a number of increasingly responsible engineering technology positions for National Steel Corporation.

Jaime Vasquez has served as Vice President, Finance and Chief Financial Officer since January 2016. Before joining us in September 2014 as Director, Finance, Mr. Vasquez held several positions with Carpenter Technology Corporation, including Vice President, Chief Financial Officer for the Performance Engineered Products Group from October 2013; Vice President, Corporate Development from July 2011; President, Asia Pacific from May 2008; and Vice President, Treasurer, and Investor Relations from March 2001.

Available Information

We maintain a website at www.aksteel.com. Information about us is available on the website free of charge, including the annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934. Such information is posted to the website as soon as reasonably practicable after submission to the Securities and Exchange Commission. Information on our website is not incorporated by reference into this report.

Item 1A. | Risk Factors. |

We caution readers that our business activities involve risks and uncertainties that could cause actual results to differ materially from those we currently expect. While the items listed below represent the most significant risks to us, we regularly monitor and report risks to the Board of Directors through a formal Total Enterprise Risk Management program.

Risk of reduced selling prices, shipments and profits associated with a highly competitive and cyclical industry . The competitive landscape in the steel industry reflects an improving, but uneven, domestic economy; uncertain, and in some cases, slowing foreign economies; an uneven recovery within certain sectors of the domestic and global economies; continued intense competition from domestic steel competitors; and increased competition from foreign steel competitors, much of which we believe is unfair. These conditions directly impact our pricing. It is impossible to predict whether the domestic and/or global economies or industry sectors of those economies that are key to our sales will continue to improve and generate enough demand to take up more of the existing excess capacity in the steel industry. Also, we cannot know how customers or competitors will react to these and other factors and how their actions could affect market dynamics and sales of, and prices for, our products. Market price and demand for steel are very hard to predict and we could be hurt by decreases in either. In addition, our direct sales to the automotive industry generate approximately 60% of our revenue and we make additional sales to distributors and converters whom, we believe, ultimately resell some of that volume to the automotive market. If automotive demand should decline substantially or we lose market share to competitors, our sales, financial results and cash flows could be severely impacted.

Risk of increased global steel production and imports . An increase in global capacity and new or expanded production capacity in the United States in recent years has caused and continues to cause capacity to exceed demand globally, as well as in our primary

- 5 -

Table of Contents

markets in North America, which has and may continue to result in lower prices and shipments of our products. In fact, significant increases in production capacity in the United States by our competitors already have occurred in recent years as new carbon and stainless steelmaking and finishing facilities have begun production. In addition, foreign competitors have substantially increased their production capacity in the last few years, and in some instances appear to have targeted the U.S. market for imports. Also, some foreign economies, such as China, are slowing relative to recent historical norms, resulting in an increased volume of steel products that cannot be consumed by industries in those foreign steel producers' own countries. These and other factors have contributed to a high and growing level of imports of foreign steel into the United States in recent years and create a risk of even greater levels of imports, depending upon foreign market and economic conditions, the value of the U.S. dollar relative to other currencies, and other variables beyond our control. A significant further increase in domestic capacity or foreign imports could adversely affect our sales, financial results and cash flows.

Risk of changes in the cost of raw materials and energy . The price that we pay for energy and key raw materials, such as electricity, natural gas, industrial gases, iron ore, coal and scrap, can fluctuate significantly based on market factors. The prices at which we sell steel will not necessarily change in tandem with changes in our raw material and energy costs. A portion of our shipments are in the spot market, and pricing for these products fluctuates based on prevailing market conditions. The remainder of our shipments are under contracts typically spanning one year or less. Most of those contracts contain fixed prices that do not allow us to pass through changes if there are increases or decreases in raw material and energy costs. Some of our shipments to contract customers are under contracts with variable-pricing mechanisms allowing us to adjust the total sales price based upon changes in specified raw material and energy costs. Those adjustments, however, do not always reflect all of our underlying raw material and energy cost changes. The scope of the adjustment may be limited by the terms of the negotiated language including limitations on when the adjustment occurs. Even under our contracts that contain variable-pricing mechanisms, we typically do not recover all of our underlying raw material and energy cost increases. For shipments made to the spot market, market conditions or timing of sales may not allow us to recover the full amount of an increase in raw material or energy costs. In such circumstances, a significant increase in raw material or energy costs likely would adversely impact our financial results and cash flows. Conversely, in certain circumstances, our financial results and cash flows may suffer when raw material prices decline. This can occur when we lock in the price of a raw material over a set period and the spot market price for the material declines during that period. Because there often is a correlation between the price of finished steel and the raw materials used to make it, a decline in raw material prices may coincide with lower steel prices, compressing our margins. Our need to consume existing inventories may also delay the impact of a change in raw materials prices. New inventory may not be purchased until some portion of the existing inventory is consumed. The impact of this risk is particularly significant for iron ore, coke and scrap because of the volume used. We manage our exposure to the risk of iron ore price increases by hedging a portion of our annual iron ore supply and by entering supply agreements where the IODEX, the global iron ore price index, is only one factor affecting our price of iron ore pellets. Our investment in and development of AK Coal has reduced the risk to us from price increases for metallurgical coal. Although AK Coal is only expected to supply approximately 13% of our coal needs in 2016, we could expand its production relatively quickly if coal prices increase significantly. However, there is a risk that the volume of coal supplied to us by our mining operations will be insufficient if there are delays in development or otherwise, or if the cost of raw materials from these operations are higher than expected or above market prices. If we must acquire iron ore and coal at market prices, these prices are sensitive to global demand and have been volatile in recent years. Future cost increases could be significant for iron ore and coal, as well as certain other raw materials, such as scrap. The impact of significant fluctuations in the price we pay for raw materials can be increased by our "last in, first out" ("LIFO") accounting method for valuing inventories. Using the LIFO method means that we treat the last coil of steel completed as the first one sold, which means that our inventory value can reflect earlier input costs that do not reflect current input costs. The impact of LIFO accounting may be particularly significant in period-to-period comparisons.

Risk from our significant amount of debt and other obligations. On December 31, 2015 , we had $2,405.5 of indebtedness (excluding unamortized discount and debt issuance costs) and additional obligations outstanding. We also had pension and other postretirement benefit obligations totaling $1,224.6 . No contributions to the master pension trust are required for 2016 . Based on current funding projections, contributions to the master pension trust of approximately $50.0 and $75.0 are required for 2017 and 2018 , though funding projections in 2017 and beyond could be affected by differences between expected and actual returns on plan assets, actuarial data and assumptions relating to plan participants, the interest rate used to measure the pension obligations and changes to regulatory funding requirements. We can borrow additional amounts under our $1,500.0 revolving credit facility. At December 31, 2015 , we had outstanding borrowings of $550.0 from this credit facility and outstanding letters of credit of $72.9 , resulting in maximum remaining availability of $877.1 under the credit facility (subject to customary borrowing conditions, including a borrowing base). Borrowing capacity under the credit facility is determined by the value of eligible collateral less outstanding borrowings and letters of credit. At December 31, 2015 , borrowing availability under the credit facility was $652.3 based on eligible collateral at that time. Our debt and pension obligations, along with other financial obligations, could have important consequences. For example, it could increase our vulnerability to general adverse economic and industry conditions; require a substantial portion of our cash flows to be dedicated to interest payments, reducing the amount of cash flows available for other purposes, such as working capital, capital expenditures, acquisitions, joint ventures or general corporate purposes; limit our ability to obtain future additional financing; reduce our planning flexibility for, or ability to react to, changes in the our business and the industry; and place us at a competitive disadvantage with competitors who may have less indebtedness and other obligations or greater access to financing.

- 6 -

Table of Contents

Risk of severe financial hardship or bankruptcy of one or more of our major customers or key suppliers. Sales and operations of a majority of our customers are sensitive to general economic conditions, especially as they affect the North American automotive and housing industries. If there is a significant weakening of current economic conditions, whether because of secular or cyclical issues, it could lead to financial difficulties or even bankruptcy filings by our customers. The concentration of customers in a specific industry, such as the automotive industry, may increase our risk because of the likelihood that circumstances may affect multiple customers at the same time. Such financial hardships or bankruptcies will likely harm us. The nature of that impact would likely include lost sales or losses associated with the potential inability to collect all outstanding accounts receivables. Such an event could negatively impact our financial results and cash flows. In addition, many of our key suppliers, particularly those who supply us with critical raw materials for the steelmaking process, have recently faced severe financial challenges or bankruptcy and other suppliers may face such circumstances in the future. For example, the significant decline in commodity prices during 2015 led to increased economic distress and even bankruptcy filings for several of our principal sources of metallurgical coal, as well as one of our key iron ore suppliers, Magnetation LLC. These suppliers facing financial hardship or operating in bankruptcy could experience operational disruption or even face liquidation, which could result in our inability to secure replacement raw materials on a timely basis, or at all, or cause us to incur increased costs to do so. Such events could adversely impact our operations, financial results and cash flows.

Risk of reduced demand in key product markets due to competition from aluminum or other alternatives to steel . The automotive market is an important element of our business. Automotive manufacturers are under pressure to meet increasing government-mandated fuel economy standards through 2025. One major automotive company recently elected to substitute aluminum for carbon steel in the body of one of its vehicles, and may increase the use of aluminum in others. Other automotive manufacturers are currently investigating the potential use of aluminum and other alternatives to steels. If demand from one or more of our major automotive customers were to significantly decline because of increased use of aluminum or other competing materials in substitution for steel, it likely would negatively affect our sales, financial results and cash flows.

Risks of excess inventory of raw materials. We have certain raw material supply contracts which include minimum annual purchases, subject to exceptions for force majeure and other circumstances. If our need for a particular raw material is reduced for an extended period significantly below what we projected at the contract's inception, or what we projected at the time an annual nomination was made under that contract, we could be required to purchase quantities of raw materials that exceed our anticipated annual needs. Our decision to temporarily idle the Ashland Works Hot End increases this risk, as those operations are a major consumer of several key raw materials for which we have take-or-pay obligations, including iron ore and coke. If our existing supply contracts require us to purchase raw materials in quantities beyond our needs, and if we do not succeed in reaching an agreement with a particular raw material supplier to reduce the quantity of raw materials we purchase from that supplier, then we would likely be required to purchase more of a particular raw material in a given year than we need, negatively affecting our financial results, liquidity and cash flows. Changes in our raw material, finished and semi-finished inventory levels and our LIFO method for valuing inventories could increase the negative impact on our financial results.

Risk of supply chain disruptions or poor quality of raw materials. Our sales, financial results and cash flows could be adversely affected by transportation, raw material or energy supply disruptions, or poor quality of raw materials, particularly scrap, coal, coke, iron ore and alloys. For example, extreme cold weather conditions in the United States and Canada can impact shipping on the Great Lakes and could disrupt the delivery of iron ore to us and/or increase our costs for iron ore. Such disruptions or quality issues, whether the result of severe financial hardships or bankruptcies of suppliers, natural or man-made disasters, other adverse weather events, or other unforeseen events, could reduce production or increase costs at one or more of our plants and potentially adversely affect customers or markets to which we sell our products. Any such significant disruption or quality issue would adversely affect our sales, financial results and cash flows.

Risk of production disruption or reduced production levels . When business conditions permit, we attempt to operate our facilities at production levels at or near capacity. High production levels are important to our financial results because they enable us to spread fixed costs over a greater number of production tons. During 2015, we began to implement a strategy to target markets for our products that deliver higher margins, where possible, and reduce amounts sold into the lower margin spot markets. This strategy relies on our ability to sell higher margin products that overcome the effects of lower production volumes on our fixed costs. If we are unable to implement this strategy successfully, it would adversely affect our sales, financial results and cash flows. Production disruptions could be caused by unanticipated plant outages or equipment failures, particularly under circumstances where we lack adequate redundant facilities, such as our Middletown Works hot mill. In addition, the occurrence of natural or man-made disasters, adverse weather conditions, or similar events could significantly disrupt our operations, negatively impact the operations of other companies or contractors we depend upon, or adversely affect customers or markets who buy our products. Any such significant disruption or reduced level of production would adversely affect our sales, financial results and cash flows.

Risks associated with our healthcare obligations . We provide healthcare coverage to our active employees and to a significant portion of our retirees, as well as certain members of their families. We are self-insured for substantially all of our healthcare coverage. While we have substantially reduced our exposure to rising healthcare costs through cost sharing, cost caps and VEBA trusts, the cost

- 7 -

Table of Contents

of providing such healthcare coverage may be greater on a relative basis for us than for our competitors because they either provide a lesser level of benefits, require that their participants pay more for their benefits, or do not provide coverage to as broad a group of participants (e.g., they do not provide retiree healthcare benefits). In addition, our costs for retiree healthcare obligations could be affected by fluctuations in interest rates or by federal healthcare legislation.

Risks associated with our pension obligations . We have a substantial pension obligation that, along with the related pension expense (income) and funding requirements, is directly affected by various changes in assumptions, including the selection of appropriate mortality assumptions and discount rates. These items also are affected by the rate and timing of employee retirements, actual experience compared to actuarial projections and asset returns in the securities markets. Such changes could increase the cost to us of those obligations, which could have a material adverse effect on our results and ability to meet those obligations. In addition, changes in the law for pension funding could also materially adversely affect our costs and ability to meet our pension obligations. Also, under the method of accounting we use for pension obligation reporting, we recognize into our results of operations, as a "corridor" adjustment, any unrecognized actuarial net gains or losses that exceed 10% of the larger of projected benefit obligations or plan assets. These corridor adjustments are driven mainly by changes in assumptions and by events and circumstances beyond our control, primarily changes in interest rates, performance of the financial markets, and mortality and retirement projections. A corridor adjustment, if required after a re-measurement of our pension obligations, historically has been recorded in the fourth quarter of the fiscal year. Corridor adjustments can have a significant negative impact on our financial statements in the year a charge is recorded, although the immediate recognition of the charge in that year has the beneficial effect of reducing the impact of unrealized gains or losses on future years. The recognition of a corridor charge does not have any immediate impact on our cash flows. We also contribute to multiemployer pension plans according to collective bargaining agreements that cover certain union-represented employees. Participating in these multiemployer plans exposes us to potential liabilities if the multiemployer plan is unable to pay its unfunded obligations or we choose to stop participating in the plan.

Risk of not reaching new labor agreements on a timely basis . Most of our hourly employees are represented by various labor unions and are covered by collective bargaining agreements with expiration dates between March 2016 and May 2019 . Two of those contracts are scheduled to expire in 2016 . The labor contract with the United Auto Workers, Local 3462 , which represents approximately 330 hourly employees at our Coshocton Works located in Coshocton, Ohio, expires on March 31, 2016 . An agreement with the United Auto Workers, Local 3303 , which represents approximately 1,240 employees at our Butler Works located in Butler, Pennsylvania, is scheduled to expire on October 1, 2016 . We intend to negotiate with these unions to reach new, competitive labor agreements in advance of the current expiration dates. We cannot predict, however, when new, competitive labor agreements with the unions will be reached or what the impact of such agreements will be on our operating costs, operating income and cash flows. There is the potential of work stoppages at these locations in 2016 if we cannot reach timely agreements in contract negotiations before the contract expirations. If work stoppages occur, they could have a material impact on our operations, financial results and cash flows. For labor contracts we have with unions at other locations which expire after 2016 , a similar risk applies.

Risks associated with major litigation, arbitrations, environmental issues and other contingencies . We have described several significant legal and environmental proceedings in Note 10 to the consolidated financial statements in Item 8. For environmental issues, changes in application or scope of regulations applicable to us could have significant adverse impacts, including requiring capital expenditures to ensure compliance with the regulations, increased difficulty in obtaining future permits or meeting future permit requirements, incurring costs for emission allowances, restriction of production, and higher prices for certain raw materials. One or more of these adverse developments could negatively impact our operations, financial results and cash flows. For litigation, arbitrations and other legal proceedings, it is not possible to predict with certainty the outcome of such matters and we could incur future judgments, fines or penalties or enter into settlements of lawsuits, arbitrations and claims that could have an adverse effect on our business, results of operations and financial condition. In addition, while we maintain insurance coverage for certain claims, we may not be able to obtain insurance on acceptable terms in the future and, if we obtain such insurance, it may not provide adequate coverage against all claims. We establish reserves based on our assessment of contingencies, including contingencies for claims asserted against us in connection with litigation, arbitrations and environmental issues. Adverse developments in litigation, arbitrations, environmental issues or other legal proceedings may affect our assessment and estimates of the loss contingency recorded as a reserve and require us to make payments in excess of our reserves, which could negatively affect our operations, financial results and cash flows.

Risk associated with regulatory compliance and changes. Our business and the businesses of our customers and suppliers are subject to a wide variety of government oversight and regulation, including those relating to environmental permitting requirements. The regulations promulgated or adopted by various government agencies, and the interpretations and application of such regulations, are dynamic and constantly evolving. If new regulations arise, the application of existing regulations expands, or the interpretation of applicable regulations changes, we may incur additional costs for compliance, including capital expenditures. For example, the United States Environmental Protection Agency ("EPA") is required to routinely reassess the National Ambient Air Quality Standards ("NAAQS") for criteria pollutants like nitrogen dioxide, sulfur dioxide, lead, ozone and particulate matter. These standards are frequently subject to litigation and revision. Revisions to the NAAQS could require us to make significant capital expenditures to ensure compliance and could make it more difficult for us to obtain required permits in the future. These risks are higher for our

- 8 -

Table of Contents

facilities that are located in non-attainment areas. For AK Coal, the coal mining industry is subject to numerous and extensive federal, state and local environmental laws and regulations, including laws and regulations related to permitting and licensing requirements, air quality standards, plant and wildlife protection, reclamation and restoration of mining properties, the discharge of materials into the environment, the storage, treatment and disposal of wastes, surface subsidence from underground mining and the effects of mining on groundwater quality and availability. We may also be indirectly affected through regulatory changes that impact our customers or suppliers. Regulatory changes that impact our customers could reduce the quantity of our products they demand or the price of our products that they are willing to pay. Regulatory changes that impact our suppliers could decrease the supply of products or availability of services they sell to us or could increase the price they demand for products or services they sell to us.

Risks associated with climate change and greenhouse gas emission limitations . Our operations may become subject to legislation intended to limit climate change or greenhouse gas emissions. It is possible that limitations on greenhouse gas emissions may be imposed in the United States through federally-enacted legislation or regulation. For example, the EPA has issued and/or proposed regulations addressing greenhouse gas emissions, including regulations that will require large sources and suppliers in the United States to report greenhouse gas emissions. In addition, the United States Congress has introduced from time to time legislation aimed at limiting carbon emissions from carbon-intensive business operations. Among other potential material items, such bills could include a system of carbon emission credits issued to certain companies, similar to the European Union's existing "cap and trade" system. It is impossible, however, to forecast the terms of the final regulations and legislation, if any, and the resulting effects on us. Depending upon the terms of any such regulations or legislation, however, we could suffer negative financial impacts because of increased energy, environmental and other costs to comply with the limitations that would be imposed on greenhouse gas emissions. In addition, depending upon whether similar limitations are imposed globally, the regulations and/or legislation could negatively impact our ability to compete with foreign steel companies situated in areas not subject to such limitations. Unless and until all of the terms of such regulation and legislation are known, however, we cannot reasonably or reliably estimate their impact on our financial condition, operating performance or ability to compete.

Risks associated with financial, credit, capital and banking markets . In the ordinary course of business, we seek to access financial, credit, capital and/or banking markets at competitive rates. Currently, we believe we have adequate access to these markets to meet our reasonably anticipated business needs. We both provide to our customers and receive from our suppliers normal trade financing. If access to competitive financial, credit, capital and/or banking markets by us, or our customers or suppliers, is impaired, our operations, financial results and cash flows could be adversely impacted.

Risk associated with derivative contracts to hedge commodity pricing volatility . We use cash-settled commodity price swaps and options to reduce pricing volatility for (1) a portion of our raw material and energy purchases and (2) the sale of certain of our commodity steel products (hot roll carbon steel coils). We employ a systematic approach in order to mitigate the risk of potential volatile movements in the price of certain raw materials. This approach is intended to protect us against a sharp rise in the price of raw materials. However, engaging in the use of swaps, options and similar agreements for hedging entails a variety of risks. For example, if the price of an underlying commodity falls below the price at which we hedged the commodity, we will benefit from the lower market price for the commodity purchased, but may not realize the full benefit of the lower commodity price because of the hedged transaction. In certain circumstances we also could be required to provide collateral for a potential derivative liability or close our hedging transaction for the commodity. Additionally, there may be a timing lag (particularly for iron ore) between a decline in the price of a commodity underlying a derivative contract, which could require us to make payments in the short-term to provide collateral or settle the relevant hedging transaction, and the period when we experience the benefits of the lower cost input through physical purchases of the commodity the hedge covers. Further, for derivatives designated as cash-flow hedges, we initially record the effective gains and losses in accumulated other comprehensive income (loss) and reclassify them to earnings in the same period we recognize the effect of the associated hedged transaction. We record all gains or losses from derivatives for which hedge accounting treatment has not been elected or from hedge ineffectiveness to earnings in the period the gain or loss occurs. Changes in the fair value of derivatives for which hedge accounting treatment has not been elected or greater hedge ineffectiveness than we anticipated on cash-flow hedges may result in increased volatility in our reported earnings. Each of these risks related to our hedging transactions could adversely affect our financial results and cash flows.

Risks related to the potential permanent idling of facilities. We have embarked on a strategic review of our business, which includes evaluating each of our plants and operating units to assess their viability and strategic benefits. As part of this review, we may idle-whether temporarily or permanently-certain of our existing facilities in order to exit participation in markets where we determine that our returns are not acceptable. For example, in December 2015 we temporarily idled the Ashland Works Hot End in order to mitigate our exposure to the carbon steel spot market. If we decide to permanently idle the Ashland Works Hot End or any other facility, we are likely to incur significant cash expenses, including those relating to labor benefit obligations, take-or-pay supply agreements and accelerated environmental remediation costs, as well as substantial non-cash charges for impairment of those assets and the effects on pension and OPEB liabilities. If we elect to permanently idle material facilities or assets, it could adversely affect our operations, financial results and cash flows.

- 9 -

Table of Contents

Risk of inability to fully realize benefits of margin enhancement initiatives. In recent years we have undertaken several significant projects in an effort to lower costs and enhance margins. In addition, we have identified and implemented many initiatives to achieve synergies in connection with our acquisition and integration of Dearborn. These projects and initiatives include efforts to focus production and sales on higher margin products, increase our operating rates and lower our costs. We identified a number of areas for enhancing profitability, including increasing our percentage of contract sales, producing and selling a higher-margin mix of products (including lowering our sales to the carbon steel spot market, which drove our decision to temporarily idle the Ashland Works Hot End) and developing new products that can command higher prices from customers. If one or more of these key cost-savings or margin enhancement projects are unsuccessful, or are significantly less effective in achieving the level and timing of combined cost savings or margin enhancement than we anticipated, or that we do not achieve results as quickly as anticipated, our financial results and cash flows could be adversely impacted.

Risk of information technology ("IT") security threats and cybercrime. We rely on IT systems and networks in almost every aspect of our business activities. In addition, we and certain of our third-party data processing providers collect and store sensitive data. We have taken, and intend to continue to take, what we believe are appropriate and reasonable steps to prevent security breaches in our systems and networks. In recent years, however, both the number and sophistication of IT security threats and cybercrimes have increased. These IT security threats and increasingly sophisticated cybercrimes, including advanced persistent attacks, pose a risk to system security and the confidentiality, availability and integrity of our data. A breach in security could expose us to risks of production downtimes and operations disruptions, misuse of information or systems, or the compromising of confidential information, which in turn could adversely affect our reputation, competitive position, business and financial results.

Item 1B. | Unresolved Staff Comments. |

None.

Item 2. | Properties. |

We lease a building in West Chester, Ohio, that we use as our corporate headquarters. The initial term of the building lease expires in 2019 and there are two five-year options to extend the lease. We own a research building located in Middletown, Ohio, and are currently constructing a new research and innovation center in Middletown to replace the existing building. We also lease administration buildings located in Dearborn, Michigan.

Our operations consist primarily of eight steelmaking and finishing plants, two coke plants and two tube manufacturing plants across six states-Indiana, Kentucky, Michigan, Ohio, Pennsylvania and West Virginia. We own all of these facilities.

Ashland Works is located in Ashland, Kentucky, and produces carbon steel. It consists of a blast furnace, basic oxygen furnaces and continuous caster for the production of carbon steel and a coating line that helps to complete the finishing operation of material processed at Middletown Works. In December 2015, we temporarily idled the blast furnace, basic oxygen furnaces and continuous caster in response to excess global supply and the increase in low-priced imports into the United States. We elected not to idle the coating line at Ashland Works, which principally finishes steel for the automotive market.

Butler Works is located in Butler, Pennsylvania, and produces stainless, electrical and carbon steel. Melting takes place in a highly-efficient electric arc furnace that feeds an argon-oxygen decarburization unit for the specialty steels. A ladle metallurgy furnace feeds two double-strand continuous casters. Butler Works also includes a hot rolling mill, annealing and pickling units and two fully automated tandem cold rolling mills. It also has various intermediate and finishing operations for both stainless and electrical steels.

Coshocton Works is located in Coshocton, Ohio, and consists of a stainless steel finishing plant containing two Sendzimer mills and two Z-high mills for cold reduction, four annealing and pickling lines, nine bell annealing furnaces, four hydrogen annealing furnaces, two bright annealing lines and other processing equipment, including temper rolling, slitting and packaging facilities.

Dearborn Works is located in Dearborn, Michigan, and was acquired in 2014. The operations include carbon steel melting, casting, hot and cold rolling and finishing operations for carbon steel. It consists of a blast furnace, basic oxygen furnaces, two ladle metallurgy furnaces, a vacuum degasser and two slab casters. Dearborn Works also has a hot rolling mill, a pickle line/tandem cold mill, batch anneal shops, a temper mill and a hot-dip galvanizing line for finishing products.

Mansfield Works is located in Mansfield, Ohio, and produces stainless steel. Operations include a melt shop with two electric arc furnaces, a ladle metallurgy furnace, an argon-oxygen decarburization unit, a thin-slab continuous caster and a hot rolling mill.

- 10 -

Table of Contents

Middletown Works is located in Middletown, Ohio. It melts carbon and processes carbon and stainless steel. It consists of a coke facility, blast furnace, basic oxygen furnaces and continuous caster for the production of carbon steel. Middletown Works also has a hot rolling mill, cold rolling mill, two pickling lines, four annealing facilities, two temper mills and three coating lines for finishing products.

Rockport Works is located near Rockport, Indiana, and consists of a continuous cold rolling mill, a continuous hot-dip galvanizing and galvannealing line, a continuous carbon and stainless steel pickling line, a continuous stainless steel annealing and pickling line, hydrogen annealing facilities and a temper mill.

Zanesville Works is located in Zanesville, Ohio, and consists of a finishing plant for some of the stainless and electrical steel produced at Butler Works and Mansfield Works and has a Sendzimer cold rolling mill, annealing and pickling lines, high temperature box anneal and other decarburization and coating units.

AK Tube LLC, a subsidiary, has a plant in Walbridge, Ohio, which operates six electric resistance welder tube mills and a slitter. AK Tube also has a plant in Columbus, Indiana, which operates eight electric resistance welder and two laser welder tube mills.

AK Coal, another subsidiary, produces metallurgical coal from reserves in Somerset County, Pennsylvania.

Mountain State Carbon, LLC, a subsidiary, is located in Follansbee, West Virginia. It is a cokemaking facility acquired in 2014 and consists of four batteries with total permitted cokemaking capacity of approximately 700,000 tons per year.

Item 3. | Legal Proceedings. |

Information for this item may be found in Note 10 to the consolidated financial statements in Item 8, which is incorporated herein by reference.

Item 4. | Mine Safety Disclosures. |

The operation of AK Coal's North Fork Mine and Coal Innovations, LLC coal wash plant (collectively, the "AK Coal Operations") are subject to regulation by the Mine Safety and Health Administration ("MSHA") under the Federal Mine Safety and Health Act of 1977, as amended ("Mine Act"). MSHA inspects mining and processing operations, such as the AK Coal Operations, on a regular basis and issues various citations and orders when it believes a violation has occurred under the Mine Act. Exhibit 95.1 to this Annual Report presents citations and orders from MSHA and other regulatory matters required to be disclosed by Section 1503(a) of the Dodd-Frank Wall Street Reform and Consumer Protection Act or otherwise under this Item 4.

- 11 -

Table of Contents

PART II

Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

AK Holding's common stock has been listed on the New York Stock Exchange since April 5, 1995 (symbol: AKS). The reported high and low sales prices of the common stock for each quarter are presented below:

| 2015 |

| 2014 | ||||||||||||

| High |

| Low |

| High |

| Low | ||||||||

First Quarter | $ | 6.17 | |

| $ | 3.62 | |

| $ | 8.24 | |

| $ | 5.79 | |

Second Quarter | 5.93 | |

| 3.81 | |

| 7.99 | |

| 5.97 | | ||||

Third Quarter | 3.93 | |

| 2.05 | |

| 11.37 | |

| 7.98 | | ||||

Fourth Quarter | 3.25 | |

| 1.99 | |

| 8.00 | |

| 5.08 | | ||||

As of February 17, 2016 , there were 178,344,667 shares of common stock outstanding and held of record by 3,920 stockholders. The closing stock price on February 17, 2016 , was $2.57 per share. Because depositories, brokers and other nominees held many of these shares, the number of record holders is not representative of the number of beneficial holders. There were no unregistered sales of equity securities in the quarter or year ended December 31, 2015 .

Although we have elected to suspend our dividend program, no covenant restrictions currently would restrict our ability to declare and pay a dividend to our stockholders. Our $1,500.0 asset-backed revolving credit facility (the "Credit Facility") contains certain restrictive covenants which could, under certain circumstances, restrict the dividend payments, but none of those circumstances currently apply. Under these covenants, dividends are permitted as long as (i) availability exceeds $337.5 or (ii) availability exceeds $262.5 and we meet a fixed charge coverage ratio of one to one as of the most recently ended fiscal quarter. If we cannot meet either of these thresholds, dividend payments would be limited to $12.0 annually. At December 31, 2015 , the availability under the Credit Facility significantly exceeded $337.5 .

Period |

| Total Number of Shares Purchased (a) |

| Average Price Paid Per Share (a) |

| Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs (b) |

| Approximate Dollar Value of Shares that May Yet be Purchased Under the Plans or Programs (b) | ||||||

October 2015 |

| 459 | |

| $ | 2.86 | |

| - | |

|

| ||

November 2015 |

| 2,180 | |

| 2.75 | |

| - | |

|

| |||

December 2015 |

| 910 | |

| 2.16 | |

| - | |

|

| |||

Total |

| 3,549 | |

| 2.61 | |

| - | |

| $ | 125.6 | | |

(a) | During the quarter, we repurchased common stock owned by participants in our restricted stock awards program under the terms of the AK Steel Holding Corporation Stock Incentive Plan. To pay federal, state and local taxes due upon the vesting of the restricted stock, employees may have us withhold shares that have a fair market value equal to the minimum statutory withholding rate that tax authorities could impose on the transaction. We repurchase the withheld shares at the quoted average of the reported high and low sales prices on the day we withhold the shares. |

(b) | On October 21, 2008, the Board of Directors authorized us to repurchase, from time to time, up to $150.0 of our outstanding equity securities. The Board of Directors' authorization specified no expiration date. |

- 12 -

Table of Contents

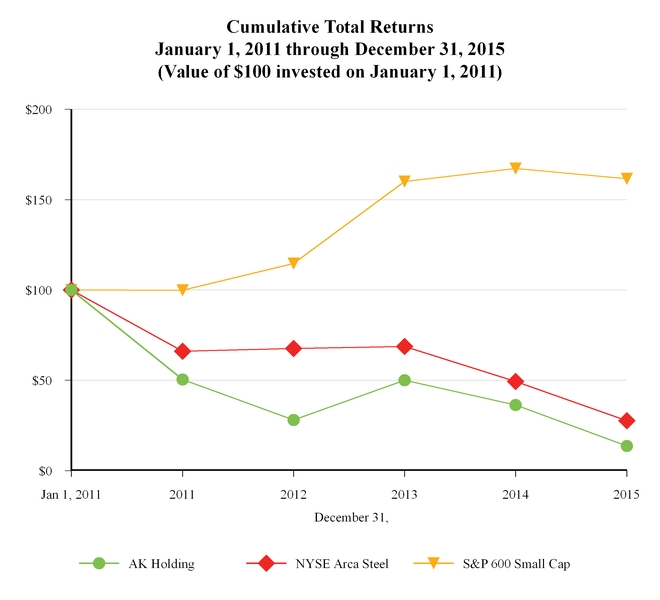

The following graph compares cumulative total stockholder return on AK Holding's common stock for the five-year period from January 1, 2011 through December 31, 2015 , with the cumulative total return for the same period of (i) the Standard & Poor's Small Cap 600 Stock Index, and (ii) the New York Stock Exchange Arca Steel Index. These comparisons assume an investment of $100 at the beginning of the period and reinvestment of dividends.

| January 1, |

| December 31, | ||||||||||||||||||||

| 2011 |

| 2011 |

| 2012 |

| 2013 |

| 2014 |

| 2015 | ||||||||||||

AK Holding | $ | 100 | |

| $ | 50 | |

| $ | 28 | |

| $ | 50 | |

| $ | 36 | |

| $ | 14 | |

NYSE Arca Steel | 100 | |

| 66 | |

| 68 | |

| 69 | |

| 49 | |

| 28 | | ||||||

S&P 600 Small Cap | 100 | |

| 100 | |

| 115 | |

| 160 | |

| 167 | |

| 162 | | ||||||

- 13 -

Table of Contents

Item 6. | Selected Financial Data. |

The following selected historical consolidated financial data for each of the five years in the period ended December 31, 2015 are from the audited consolidated financial statements. This data should be read along with the consolidated financial statements presented in Item 8 and Management's Discussion and Analysis of Financial Condition and Results of Operations presented in Item 7.

| 2015 |

| 2014 |

| 2013 |

| 2012 |

| 2011 | ||||||||||

| (dollars in millions, except per share and per ton data) | ||||||||||||||||||

Statement of Operations Data: |

|

|

|

|

|

|

|

|

| ||||||||||

Net sales | $ | 6,692.9 | |

| $ | 6,505.7 | |

| $ | 5,570.4 | |

| $ | 5,933.7 | |

| $ | 6,468.0 | |

Pension/OPEB corridor charge (credit) | 131.2 | |

| 2.0 | |

| - | |

| 157.3 | |

| 268.1 | | |||||

Operating profit (loss) (a) | 86.7 | |

| 139.4 | |

| 135.8 | |

| (128.1 | ) |

| (201.3 | ) | |||||

Net income (loss) attributable to AK Steel Holding Corporation (b) | (509.0 | ) |

| (96.9 | ) |

| (46.8 | ) |

| (1,027.3 | ) |

| (155.6 | ) | |||||

Basic and diluted earnings (loss) per share (b) | (2.86 | ) |

| (0.65 | ) |

| (0.34 | ) |

| (9.06 | ) |

| (1.41 | ) | |||||

Other Data: |

|

|

|

|

|

|

|

|

| ||||||||||

Cash dividends declared per common share | $ | - | |

| $ | - | |

| $ | - | |

| $ | 0.10 | |

| $ | 0.20 | |

Total shipments (in thousands of tons) | 7,089.2 | |

| 6,132.7 | |

| 5,275.9 | |

| 5,431.3 | |

| 5,698.8 | | |||||

Selling price per ton | $ | 942 | |

| $ | 1,058 | |

| $ | 1,056 | |

| $ | 1,092 | |

| $ | 1,131 | |

Balance Sheet Data: |

|

|

|

|

|

|

|

|

| ||||||||||

Cash and cash equivalents | $ | 56.6 | |

| $ | 70.2 | |

| $ | 45.3 | |

| $ | 227.0 | |

| $ | 42.0 | |

Working capital (c) | 763.6 | |

| 832.8 | |

| 372.2 | |

| 557.1 | |

| (79.2 | ) | |||||

Total assets (c) | 4,084.4 | |

| 4,828.0 | |

| 3,579.1 | |

| 3,873.7 | |

| 4,439.7 | | |||||

Current portion of long-term debt (d) | - | |

| - | |

| 0.8 | |

| 0.7 | |

| 250.7 | | |||||

Long-term debt (excluding current portion) (c) | 2,354.1 | |

| 2,422.0 | |

| 1,479.6 | |

| 1,381.8 | |

| 639.8 | | |||||

Current portion of pension and other postretirement benefit obligations | 77.7 | |

| 55.6 | |

| 85.9 | |

| 108.6 | |

| 130.0 | | |||||

Pension and other postretirement benefit obligations (excluding current portion) | 1,146.9 | |

| 1,225.3 | |

| 965.4 | |

| 1,661.7 | |

| 1,744.8 | | |||||

Total equity (deficit) (e) | (595.6 | ) |

| (77.0 | ) |

| 192.7 | |

| (91.0 | ) |

| 377.2 | | |||||

(a) | Under our method of accounting for pensions and other postretirement benefits, we recorded pension corridor charges of $144.3 , $2.0 , $157.3 and $268.1 in 2015, 2014, 2012 and 2011. In 2015, we also recorded an OPEB corridor credit of $13.1 , and a charge for a facility idling of $28.1 . |

(b) | Included in net income (loss) attributable to AK Steel Holding Corporation for 2015 were charges for the impairments of our investments in Magnetation of $256.3 , or $1.44 per diluted share, and AFSG of $41.6 , or $0.23 per diluted share, and for 2012 was a charge to income tax expense of $865.5 , or $7.63 per diluted share, for an increase in the valuation allowance on deferred tax assets. |

(c) | Balances in 2014, 2013, 2012 and 2011 have been conformed to the 2015 presentation for the classification of deferred tax assets of $67.7 , $69.6 , $73.2 and $216.5 , and debt issuance costs of $30.5 , $26.6 , $29.4 and $10.2 . |

(d) | Includes borrowings under our revolving credit facility classified as short-term. |

(e) | As of December 31, 2012, the advances to SunCoke Middletown were classified as noncontrolling interests because of financing activities performed by its parent, SunCoke Energy, Inc. We included this in other non-current liabilities in prior periods. |

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. |

Operations Overview

We operate eight steelmaking and finishing plants, two coke plants and two tube manufacturing plants across six states-Indiana, Kentucky, Michigan, Ohio, Pennsylvania and West Virginia. These operations produce flat-rolled carbon steels, including premium-quality coated, cold-rolled and hot-rolled carbon steel products, and specialty stainless and electrical steels that we sell in sheet and strip form, as well as carbon and stainless steel that we finish into welded steel tubing. We sell these products to our customers in three markets: (i) automotive; (ii) infrastructure and manufacturing; and (iii) distributors and converters markets. We sell carbon steel products principally to domestic customers and electrical and stainless steel products both domestically and internationally. We also produce carbon and stainless steel that we finish into welded steel tubing used in the automotive, large truck, industrial and construction markets. In addition, we operate Mexican and European trading companies that buy and sell steel and steel products and other materials.

- 14 -

Table of Contents