UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended January 28, 2017

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 1-33338

American Eagle Outfitters, Inc.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | No. 13-2721761 (I.R.S. Employer Identification No.) |

|

|

77 Hot Metal Street, Pittsburgh, PA | 15203-2329 |

(Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code:

(412) 432-3300

Securities registered pursuant to Section 12(b) of the Act:

Common Shares, $0.01 par value (Title of class) | New York Stock Exchange (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☒ NO ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Sections 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for at the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☒ NO ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☒ |

| Accelerated filer | ☐ |

Non-accelerated filer | ☐ | (Do not check if a smaller reporting company) | Smaller reporting company | ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ☐ NO ☒

The aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of July 30, 2016 was $2,983,485,568.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date: 182,221,528 Common Shares were outstanding at March 6, 2017.

DOCUMENTS INCORPORATED BY REFERENCE

Part III - Proxy Statement for 2017 Annual Meeting of Stockholders, in part, as indicated.

AMERICAN EAGLE OUTFITTERS, INC.

TABLE OF CONTENTS

| Page Number |

PART I |

|

Item 1. Business | 3 |

Item 1A. Risk Factors | 9 |

Item 1B. Unresolved Staff Comments | 13 |

Item 2. Properties | 13 |

Item 3. Legal Proceedings | 14 |

Item 4. Mine Safety Disclosures | 14 |

|

|

PART II |

|

Item 5. Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 14 |

Item 6. Selected Consolidated Financial Data | 17 |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations | 18 |

Item 7A. Quantitative and Qualitative Disclosures About Market Risk | 31 |

Item 8. Financial Statements and Supplementary Data | 32 |

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 59 |

Item 9A. Controls and Procedures | 59 |

Item 9B. Other Information | 62 |

|

|

PART III |

|

Item 10. Directors, Executive Officers and Corporate Governance | 62 |

Item 11. Executive Compensation | 62 |

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 62 |

Item 13. Certain Relationships and Related Transactions, and Director Independence | 62 |

Item 14. Principal Accounting Fees and Services | 62 |

|

|

PART IV |

|

Item 15. Exhibits, Financial Statement Schedules | 63 |

2

PART I

Item 1. Business.

General

American Eagle Outfitters, Inc., ("AEO Inc.," the "Company," "we," "our") a Delaware corporation, was founded in 1977. We are a leading multi-brand specialty retailer, operating over 1,000 retail stores and online at www.ae.com and www.aerie.com in the U.S. and internationally. We offer a broad assortment of apparel and accessories for men and women under the American Eagle Outfitters brand, and intimates, apparel and personal care products for women under the Aerie brand. AEO Inc. operates stores in the United States, Canada, Mexico, Hong Kong, China and the United Kingdom. We also have license agreements with third-parties to operate American Eagle Outfitters and Aerie stores throughout Asia, Europe, Latin America and the Middle East. As of January 28, 2017, we operated 943 American Eagle Outfitters stores and 102 Aerie stand-alone stores. Our licensed store base has grown to 176 locations in 23 countries. We also acquired two emerging brands to complement our existing brands, Tailgate, a vintage sports-inspired apparel brand, and Todd Snyder New York, a premium menswear brand.

Information concerning our segment and certain geographic information is contained in Note 2 of the Consolidated Financial Statements included in this Form 10-K and is incorporated herein by reference. Additionally, a five-year summary of certain financial and operating information can be found in Part II, Item 6, Selected Consolidated Financial Data, of this Form 10-K. See also Part II, Item 8, Financial Statements and Supplementary Data.

Brands

American Eagle Outfitters Brand ("AEO Brand")

We are an American brand rooted in our denim heritage and passionate about providing the highest-quality products. American Eagle Outfitters is a style movement that's 40 years in the making. Our innovative fabrics and fits have positioned us as America's favorite jeans brand-and while jeans are our heart and soul, we also design a high-quality assortment of apparel and accessories that reflects our customer's individual style-at a value that is approachable by all. AEO's brand platform, #WeAllCan TM , celebrates the power and individuality of young America.

As of January 28, 2017, the AEO brand operated 943 stores and online at www.ae.com.

Aerie

Aerie is an intimates brand in operation for over 10 years and is committed to making all girls feel good about their REAL selves. We offer bras, undies, swim, sleep, apparel and more and have grown into a body-positive movement that has changed the industry. Empowering. Honest. Fun. Smart. Strong and Sexy. #AerieREAL is a campaign that means more than no retouching, it's about loving your real self from the inside out .

As of January 28, 2017, the Aerie brand operates 102 stand-alone stores and 88 side-by-side stores connected to AEO brand stores. In addition, the Aerie brand merchandise is sold online at www.aerie.com and certain items are sold in AEO brand stores.

Other brands

Tailgate is a vintage, sports-inspired apparel brand with a college town store concept. As of January 28, 2017, the Tailgate brand operates 4 stand-alone stores and is available online at www.ae.com.

Todd Snyder New York is a premium menswear brand. As of January 28, 2017, the Todd Snyder brand operates 1 stand-alone store and online at www.ToddSnyder.com.

3

Business Priorities & Strategy

We are focused on driving our brands forward and delivering an exceptional customer experience across channels. Our current priorities include:

• | Delivering innovation, quality and outstanding value to our customers |

• | Strengthening our brands, customer experience and engagement |

• | Leveraging omni-channel and enhancing capabilities to gain market share through a focus on our customers and where they choose to shop |

• | Growing Aerie to be the leading intimates brand in the marketplace |

• | Strengthening our financial discipline including inventory and expense management, delivering profitable revenue growth and focus on high return investments among other areas |

Real Estate

We ended Fiscal 2016 with a total of 1,226 stores, consisting of 1,050 Company owned stores and 176 licensed store locations. Our AEO brand stores average approximately 6,600 gross square feet and approximately 4,600 on a selling square foot basis. Our Aerie brand stand-alone stores average approximately 3,800 gross square feet and approximately 3,000 on a selling square foot basis. The gross square footage of our Company owned stores increased by 0.3% to 6.6 million during Fiscal 2016.

Company-Owned Stores

Our Company owned retail stores are located in shopping malls, lifestyle centers and street locations in the U.S., Canada, Mexico, China, Hong Kong and the United Kingdom.

Refer to Note 16 to the Consolidated Financial Statements for additional information regarding impairment and restructuring charges in China, Hong Kong and the United Kingdom.

The following table provides the number of our Company-owned stores in operation as of January 28, 2017 and January 30, 2016.

|

| January 28, |

|

| January 30, |

| ||

|

| 2017 |

|

| 2016 |

| ||

AEO Brand: |

|

|

|

|

|

|

|

|

United States |

|

| 812 |

|

|

| 822 |

|

Canada |

|

| 84 |

|

|

| 86 |

|

Mexico |

|

| 28 |

|

|

| 23 |

|

China |

|

| 10 |

|

|

| 9 |

|

Hong Kong |

|

| 6 |

|

|

| 6 |

|

United Kingdom |

|

| 3 |

|

|

| 3 |

|

Total AEO Brand |

|

| 943 |

|

|

| 949 |

|

Aerie Brand: |

|

|

|

|

|

|

|

|

United States |

|

| 86 |

|

|

| 82 |

|

Canada |

|

| 16 |

|

|

| 15 |

|

Total Aerie Brand |

|

| 102 |

|

|

| 97 |

|

Tailgate |

|

| 4 |

|

|

| 1 |

|

Todd Snyder |

|

| 1 |

|

|

| - |

|

Total Consolidated |

|

| 1,050 |

|

|

| 1,047 |

|

4

The following table provides the changes in the number of our Company-owned stores for the past five fiscal years:

Fiscal Year |

| Beginning of Year |

|

| Opened |

|

| Closed |

|

| End of Year |

| ||||

2016 |

|

| 1,047 |

|

|

| 29 |

|

|

| (26 | ) |

|

| 1,050 |

|

2015 |

|

| 1,056 |

|

|

| 23 |

|

|

| (32 | ) |

|

| 1,047 |

|

2014 |

|

| 1,066 |

|

|

| 60 |

|

|

| (70 | ) |

|

| 1,056 |

|

2013 |

|

| 1,044 |

|

|

| 64 |

|

|

| (42 | ) |

|

| 1,066 |

|

2012 |

|

| 1,069 |

|

|

| 16 |

|

|

| (41 | ) |

|

| 1,044 |

|

Licensed Stores

In addition to our Company owned stores, our merchandise is sold at stores operated by third-party licensees. Under these agreements, our merchandise is sold at American Eagle Outfitters and Aerie stores owned and operated by third-party operators. Revenue recognized under license agreements generally consists of royalties earned and recognized upon sale of merchandise by license partners to retail customers.

As of January 28, 2017, our products were sold in 176 locations operated by licensees in 23 countries as provided in the following table. We continue to increase the number of locations under these types of arrangements as part of our disciplined approach to global expansion.

|

| January 28, |

|

| 2017 |

Israel |

| 41 |

Japan |

| 34 |

South Korea |

| 19 |

Chile |

| 12 |

Colombia |

| 12 |

Philippines |

| 9 |

UAE |

| 9 |

Saudi Arabia |

| 8 |

Thailand |

| 6 |

Egypt |

| 3 |

Greece |

| 3 |

Kuwait |

| 3 |

Lebanon |

| 3 |

Morocco |

| 2 |

Panama |

| 2 |

Qatar |

| 2 |

Singapore |

| 2 |

Bahrain |

| 1 |

Costa Rica |

| 1 |

Curacao |

| 1 |

Guatemala |

| 1 |

Jordan |

| 1 |

Oman |

| 1 |

Total Licensed Stores |

| 176 |

AEO Direct

We sell merchandise through our digital channels, ae.com, aerie.com and our AEO apps, both domestically and internationally in 81 countries. The digital channels reinforce each particular brand platform, and are designed to complement the in-store experience.

Over the past several years, we have invested in building our technologies and digital capabilities. We focused our investments in three key areas: making significant advances in mobile technology, investing in digital marketing and improving the desktop and tablet experience.

5

Omni-Channel

In addition to our investments in technology, we have invested in building omni-channel capabilities to better serve customers and gain operational efficiencies. These upgraded technologies have provided a single view of inventory across channels, connecting physical stores directly to our digital store, providing our customers with a more convenient and improved shopping experience. Our two distribution centers are fully omni-channel and service both stores and digital businesses. We offer the ability for customers to seamlessly return product via any channel regardless of where it was originally purchased. Our store-to-door capability enables store customers to make purchases from online inventory while shopping in our stores. Additionally, we fulfill online orders at stores through our buy online, ship from store capability, maximizing inventory exposure to digital traffic. We also offer a reserve online, pick up in store service to our customers and give them the ability to lookup in-store inventory from all digital channels. We will continue to optimize these tools and services to build ongoing improvements to the customer shopping experience.

Merchandise Suppliers

We design our merchandise, which is manufactured by third-party factories. During Fiscal 2016, we purchased substantially all of our merchandise from non-North American suppliers. For the year, we sourced merchandise through approximately 300 vendors located throughout the world, primarily in Asia, and did not source more than 10% of our merchandise from any single factory or supplier during the year.

We maintain a quality control department at our distribution centers to inspect incoming merchandise shipments for overall quality of manufacturing. Inspections are also made by our employees and agents at manufacturing facilities to identify quality issues prior to shipment of merchandise.

We uphold an extensive factory inspection program to monitor compliance with our Vendor Code of Conduct. New garment factories must pass an initial inspection in order to do business with us and we continue to review their social compliance performance both through internal audits by our compliance team and through the use of third-party monitors. We strive to partner with suppliers who respect local laws and share our dedication to utilize best practices in human rights, labor rights, environmental practices and workplace safety. We have been a certified member of the Customs-Trade Partnership Against Terrorism program ("C-TPAT") since 2004. C-TPAT is a voluntary program offered by the Bureau of Customs and Border Protection ("CBP") in which an importer agrees to work with CBP to strengthen overall supply chain security. As of September 2016, we were accepted into the Apparel, Footwear and Textiles Center, one of CBP's Centers of Excellence and Expertise ("CEE"). The CEE was created to ensure uniformity, create efficiencies, reduce redundancies, enhance industry expertise and facilitate trade, all with a final goal of reduced costs at the border and allowing CBP to focus on high-risk shipments.

Inventory and Distribution

Merchandise is shipped directly from our vendors to our U.S. distribution centers in Hazleton, Pennsylvania and Ottawa, Kansas, or to our Canadian distribution center in Mississauga, Ontario. Additionally, an increasing amount of product is shipped directly to stores which reduces transit times and lowers operating costs. We contract with third-party distribution centers in Mexico, Hong Kong, China and the Netherlands to service our Company owned stores in those regions.

Regulation

We and our products are subject to regulation by various federal, state, local and foreign regulatory authorities. Virtually all of our products are manufactured by foreign suppliers and imported by us, and we are subject to a variety of trade laws, customs regulations and international trade agreements. Apparel and other products sold by us are under the jurisdiction of multiple governmental agencies and regulations, including, in the U.S., the Federal Trade Commission and the Consumer Products Safety Commission. These regulations relate principally to product labeling, marketing, licensing requirements, and consumer product safety requirements and regulatory testing. We are also subject to regulations governing our employees both globally and in the U.S., and by disclosure and reporting requirements for publicly traded companies established under existing or new federal or state laws, including the Sarbanes-Oxley Act of 2002, the Securities and Exchange Commission ("SEC") and New York Stock Exchange ("NYSE").

Our licensing partners, buying/sourcing agents, and the vendors and factories with which we contract for the manufacture and distribution of our products are also subject to regulation. Our agreements require our licensing partners, buying/sourcing agents, vendors, and factories to operate in compliance with all applicable laws and regulations, and we

6

are not aware of any violations which could reasonably be expected to have a material adverse effect on our business or operating results.

Competition

The global retail apparel industry is highly competitive both in stores and online. We compete with various local, national, and global apparel retailers, as well as the casual apparel and footwear departments of department stores and discount retailers, primarily on the basis of quality, fashion, service, selection and price.

Trademarks and Service Marks

We have registered AMERICAN EAGLE OUTFITTERS ® , AMERICAN EAGLE ® , AE ® , AEO ® , #WeAllCan TM , LIVE YOUR LIFE ® , Aerie ® and the Flying Eagle Design with the United States Patent and Trademark Office. We also have registered or have applied to register substantially all of these trademarks with the registries of the foreign countries in which our stores and/or manufacturers are located and/or where our product is shipped.

We have registered AMERICAN EAGLE OUTFITTERS ® , AMERICAN EAGLE ® , AEO ® , LIVE YOUR LIFE ® , Aerie ® and the Flying Eagle Design with the Canadian Intellectual Property Office. In addition, we have acquired rights in AE TM for clothing products and registered AE ® in connection with certain non-clothing products.

In the U.S. and in other countries around the world, we also have registered, or have applied to register, a number of other marks used in our business, including our pocket stitch designs.

Our registered trademarks are renewable indefinitely, and their registrations are properly maintained in accordance with the laws of the country in which they are registered. We believe that the recognition associated with these trademarks makes them extremely valuable and, therefore, we intend to use and renew our trademarks in accordance with our business plans.

Employees

As of January 28, 2017, we had approximately 38,700 employees in the United States, Canada, Mexico, Hong Kong, China and the United Kingdom of whom approximately 32,100 were part-time or seasonal hourly employees.

Executive Officers of the Registrant

Jennifer M. Foyle, age 50, has served as our Global Brand President – Aerie since January 2015. Prior thereto, Ms. Foyle served as Executive Vice President, Chief Merchandising Officer – Aerie from February 2014 to January 2015 and Senior Vice President, Chief Merchandising Officer – Aerie from August 2010 to February 2014. Prior to joining us, Ms. Foyle was President of Calypso St. Barth from 2009 to 2010. In addition, she held various positions at J. Crew Group, Inc., including Chief Merchandising Officer, from 2003 to 2009. Early in her career Ms. Foyle was the Women's Divisional Merchandise Manager for Gap Inc. from 1999 – 2003 and held various roles at Bloomingdales from 1988-1999.

Peter Z. Horvath , age 59, has served as our Chief Global Commercial and Administrative Officer since May 2016. Prior to joining us, Mr. Horvath served as Chief Executive Officer and Chairman of Mission Essential Personnel, LLC, from January 2012 to June 2015. Prior to that time, he served as Executive Vice President and Chief Operating Officer of Victoria's Secret Stores, Limited Brands from July 2008 to December 2010. From January 2005 to June 2008, Mr. Horvath was President of DSW, Inc. From 1985 to 2004, he held a variety of positions at Limited Brands, including Chief Financial Officer, Apparel Merchandising from 1997 to 2002 and Senior Vice President, Enterprise Merchandise Planning and Allocation from 2002 to 2004. Early in his career, Mr. Horvath worked at Bristol Myers, Inc. and W.R. Grace and Co. Retail Group.

Charles F. Kessler , age 44, has served as our Global Brand President – American Eagle Outfitters since January 2015. Prior thereto, he served as our Executive Vice President, Chief Merchandising and Design Officer – American Eagle Outfitters from February 2014 to January 2015. Prior to joining us, Mr. Kessler served as Chief Merchandising Officer at Urban Outfitters, Inc. from October 2011 to November 2013 and as Senior Vice President, Corporate Merchandising at Coach, Inc. from July 2010 to October 2011. Prior to that time, Mr. Kessler held various positions with Abercrombie & Fitch Co. from 1994 to 2010, including Executive Vice President, Female Merchandising from 2008 to 2010.

7

Robert L. Madore , age 52, has served as our Executive Vice President and Chief Financial Officer since October 2016. Prior to joining us, Mr. Madore served as the Chief Financial Offi cer of Ralph Lauren Corporation from April 2015 to September 2016. Prior to that role, he held a number of key financial and operational roles at the Ralph Lauren Corporation, including Senior Vice President of Corporate Finance from December 2010 to March 2015, and Senior Vice President of Operations and Chief Financial Officer of its retail division from 2004 to December 2010. Prior to that time, Mr. Madore was Chief Financial Officer for New York & Company from 2003 to 2004, and served as Chief Operating Officer and Chief Financial Officer of FutureBrand, a division of McCann Erickson, from 2001 to 2003. Prior thereto, he held various executive management positions at Nine West Group, Inc. starting in 1995. Mr. Madore began his career in 1987 at Deloitte & Touche until 1995.

Michael R. Rempell, age 43, has served as our Executive Vice President and Chief Operations Officer since June 2012. Prior thereto, he served as our Executive Vice President and Chief Operating Officer, New York Design Center, from April 2009 to June 2012, as Senior Vice President and Chief Supply Chain Officer from May 2006 to April 2009, and in various other positions since joining us in February 2000.

Jay L. Schottenstein, age 62, has served as our Executive Chairman, Chief Executive Officer since December 2015. Prior thereto, Mr. Schottenstein served as our Executive Chairman, Interim Chief Executive Officer from January 2014 to December 2015. He has also served as the Chairman of the Company and its predecessors since March 1992. He served as our Chief Executive Officer from March 1992 until December 2002 and prior to that time, he served as a Vice President and Director of our predecessors since 1980. He has also served as Chairman of the Board and Chief Executive Officer of Schottenstein Stores Corporation ("SSC") since March 1992 and as President since 2001. Prior thereto, Mr. Schottenstein served as Vice Chairman of SSC from 1986 to 1992. He has been a Director of SSC since 1982. Mr. Schottenstein also served as Chief Executive Officer from March 2005 to April 2009 and as Chairman of the Board since March 2005 of DSW Inc., a company traded on the NYSE. He has also served as a member of the Board of Directors for AB Acquisition LLC (Albertsons/Safeway) since 2006. He has also served as an office and director of various other entities owned or controlled by members of his family since 1976.

Fiscal Year

Our fiscal year ends on the Saturday nearest to January 31. As used herein, "Fiscal 2017" refers to the 53-week period ending February 3, 2018. "Fiscal 2016", "Fiscal 2015" and "Fiscal 2014" refer to the 52-week periods ended January 28, 2017, January 30, 2016 and January 31, 2015, respectively.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports are available under the Investors section of our website at www.ae.com. These reports are available as soon as reasonably practicable after such material is electronically filed with the SEC.

Our corporate governance materials, including our corporate governance guidelines, the charters of our audit, compensation, and nominating and corporate governance committees, and our code of ethics may also be found under the Investors section of our website at www.ae.com. Any amendments or waivers to our code of ethics will also be available on our website. A copy of the corporate governance materials is also available upon written request.

Additionally, our investor presentations are available under the Investors section of our website at www.ae.com. These materials are available as soon as reasonably practicable after they are presented at investor conferences.

Certifications

As required by the NYSE Corporate Governance Standards Section 303A.12(a), on June 2, 2016, our Chief Executive Officer submitted to the NYSE a certification that he was not aware of any violation by the Company of NYSE corporate governance listing standards. Additionally, we filed and furnished, as applicable, with this Form 10-K, the Principal Executive Officer and Principal Financial Officer certifications required under Sections 302 and 906 of the Sarbanes-Oxley Act of 2002.

8

Item 1A. Ri sk Factors

Our inability to anticipate and respond to changing consumer preferences, fashion trends and a competitive environment in a timely manner

Our future success depends, in part, upon our ability to identify and respond to fashion trends in a timely manner. The specialty retail apparel business fluctuates according to changes in the economy and customer preferences, dictated by fashion and season. These fluctuations especially affect the inventory owned by apparel retailers because merchandise typically must be ordered well in advance of the selling season. While we endeavor to test many merchandise items before ordering large quantities, we are still susceptible to changing fashion trends and fluctuations in customer demands.

In addition, the cyclical nature of the retail business requires that we carry a significant amount of inventory, especially during our peak selling seasons. We enter into agreements for the manufacture and purchase of our private label apparel well in advance of the applicable selling season. As a result, we are vulnerable to changes in consumer demand, pricing shifts and the timing and selection of merchandise purchases. The failure to enter into agreements for the manufacture and purchase of merchandise in a timely manner could, among other things, lead to a shortage of inventory and lower sales. Changes in fashion trends, if unsuccessfully identified, forecasted or responded to by us, could, among other things, lead to lower sales, excess inventories and higher markdowns, which in turn could have a material adverse effect on our results of operations and financial condition.

The effect of economic pressures and other business factors on consumer spending

The success of our operations depends to a significant extent upon a number of factors relating to discretionary consumer spending, including economic conditions affecting disposable consumer income such as income taxes, payroll taxes, employment, consumer debt, interest rates, increases in energy costs and consumer confidence. There can be no assurance that consumer spending will not be further negatively affected by general, local or international economic conditions, thereby adversely impacting our business and results of operations.

Seasonality

Historically, our operations have been seasonal, with a large portion of total net revenue and operating income occurring in the third and fourth fiscal quarters, reflecting increased demand during the back-to-school and year-end holiday selling seasons, respectively. As a result of this seasonality, any factors negatively affecting us during the third and fourth fiscal quarters of any year, including adverse weather or unfavorable economic conditions, could have a material adverse effect on our financial condition and results of operations for the entire year. Our quarterly results of operations also may fluctuate based upon such factors as the timing of certain holiday seasons, the number and timing of new store openings, the acceptability of seasonal merchandise offerings, the timing and level of markdowns, store closings and remodels, competitive factors, weather and general economic and political conditions.

Our efforts to execute on our key business priorities

Our success depends on our ability to execute on our key priorities, which are centered on driving our brands forward and delivering an exceptional customer experience across channels, including:

| • | Delivering innovation, quality and outstanding value to our customers |

| • | Strengthening our brands, customer experience and engagement |

| • | Leveraging omni-channel and enhancing capabilities to gain market share through a focus on our customers and where they choose to shop |

| • | Growing Aerie to be the leading intimates brand in the marketplace |

| • | Strengthening our financial discipline including inventory and expense management, delivering profitable revenue growth and focus on high return investments among other areas |

Our inability to react to raw material cost, labor and energy cost increases

Increases in our costs, such as raw materials, labor and energy may reduce our overall profitability. Specifically, fluctuations in the cost associated with the manufacture of merchandise we purchase from our suppliers impacts our cost

9

of sales. We have strategies in place to help mitigate these costs; however, our overall profitability depends on the success of those strategies. Additionally, inc reases in other costs, including labor, energy and additional duties and taxes on imports, could further reduce our profitability if not mitigated.

Our inability to achieve planned store financial performance

The results achieved by our stores may not be indicative of long-term performance or the potential performance of stores in other locations. The failure of stores to achieve acceptable results could result in store asset impairment charges, which could adversely affect our results of operations and financial condition.

Our ability to gain market share in the face of declining shopping center traffic

Customer shopping patterns have been evolving from shopping center and store locations to digital marketplaces. We have Company owned stores in shopping centers that have experienced declining traffic trends while our digital channels continue to grow. Our ability to grow revenue and acquire new customers is contingent on our ability to drive traffic to both store locations and digital channels so we are accessible to our customers when and where they want to shop.

We locate our brick and mortar stores in prominent locations within successful shopping malls or street locations. Our stores benefit from the ability of the malls' "anchor" tenants, generally large department stores and other area attractions, to generate consumer traffic in the vicinity of our stores. We cannot control the increasing impact of digital channels on shopping center traffic; the loss of an anchor or other significant tenant in a shopping mall in which we have a store; the development of new shopping malls in the U.S. or around the world; the availability or cost of appropriate locations; competition with other retailers for prominent locations; or the success of individual shopping malls. All of these factors may impact our ability to meet our productivity targets and could have a material adverse effect on our financial results.

Our inability to grow our e-commerce channel and leverage omni-channel capabilities

We sell merchandise through our digital channels, both domestically and internationally. We have invested in building technologies and digital capabilities in three key areas: mobile technology, digital marketing and desktop experience. We have made significant capital investments in these areas but there is no assurance that we will be able to continue to successfully maintain or expand our e-commerce business. As omni-channel retailing continues to evolve, our customers are increasingly more likely to shop across multiple channels that work in tandem to meet their needs. Our inability to respond to these changes and successfully maintain and expand our omni-channel business may have an adverse impact on our results of operations.

Our efforts to expand internationally

We are actively pursuing additional international expansion initiatives, which include Company owned stores and stores operated by third-parties in select international markets. The effect of international expansion arrangements on our business and results of operations is uncertain and will depend upon various factors, including the demand for our products in new markets internationally. Furthermore, although we provide store operation training, literature and support, to the extent that a licensee does not operate its stores in a manner consistent with our requirements regarding our brand and customer experience standards, our business results and the value of our brand could be negatively impacted.

A failure to properly implement our expansion initiatives, or the adverse impact of political or economic risks in these international markets, could have a material adverse effect on our results of operations and financial condition. We have limited prior experience operating internationally, where we face established competitors. In many of these locations, the real estate, labor and employment, transportation and logistics and other operating requirements differ dramatically from those in the locations where we have more experience. Consumer demand and behavior, as well as tastes and purchasing trends, may differ substantially, and as a result, sales of our products may not be successful, or the margins on those sales may not be in line with those we currently anticipate. Any differences that we encounter as we expand internationally may divert financial, operational and managerial resources from our existing operations, which could adversely impact our financial condition and results of operations. In addition, we are increasingly exposed to foreign currency exchange rate risk with respect to our revenue, profits, assets, and liabilities denominated in currencies other than the U.S. dollar. We may use instruments to hedge certain foreign currency risks; however, these measures may not

10

succeed in offsetting all of the negative impact of foreign currency rate movements on our business and results of operatio ns.

As we pursue our international expansion initiatives, we are subject to certain laws, including the Foreign Corrupt Practices Act, as well as the laws of the foreign countries in which we operate. Violations of these laws could subject us to sanctions or other penalties that could have an adverse effect on our reputation, operating results and financial condition.

Our international merchandise sourcing strategy

Our merchandise is manufactured by suppliers worldwide. Although we purchase a significant portion of our merchandise through a single international buying agent, we do not maintain any exclusive commitments to purchase from any one vendor. Because we have a global supply chain, any event causing the disruption of imports, including the insolvency of a significant supplier or a major labor slow-down, strike or dispute including any such actions involving ports, trans loaders, consolidators or shippers, could have an adverse effect on our operations. Given the volatility and risk in the current markets, our reliance on external vendors leaves us subject to certain risks should one or more of these external vendors become insolvent. Although we monitor the financial stability of our key vendors and plan for contingencies, the financial failure of a key vendor could disrupt our operations and have an adverse effect on our cash flows, results of operations and financial condition. Recently, uncertainty has increased with respect to tax and trade policies, border adjustments, tariffs and government regulations affecting trade between the U.S. and other countries. We source the majority of our merchandise from manufacturers located outside of the U.S., primarily in Asia. Major developments in tax policy or trade relations, such as the disallowance of tax deductions for imported merchandise or the imposition of unilateral tariffs on imported products, could have a material adverse effect on our business, results of operations and liquidity.

We have a Vendor Code of Conduct (the "Code") that provides guidelines for our vendors regarding working conditions, employment practices and compliance with local laws. A copy of the Code is posted on our website, www.ae.com , and is also included in our vendor manual in English and multiple other languages. We have a factory compliance program to audit for compliance with the Code. However, there can be no assurance that all violations can be eliminated in our supply chain. Publicity regarding violation of our Code or other social responsibility standards by any of our vendor factories could adversely affect our reputation, sales and financial performance.

There is a risk of terrorist activity on a global basis. Such activity might take the form of a physical act that impedes the flow of imported goods or the insertion of a harmful or injurious agent to an imported shipment. We have instituted policies and procedures designed to reduce the chance or impact of such actions. Examples include, but are not limited to, factory audits and self-assessments, including audit protocols on all critical security issues; the review of security procedures of our other international trading partners, including forwarders, consolidators, shippers and brokers; and the cancellation of agreements with entities who fail to meet our security requirements. In addition, CBP has recognized us as a validated participant of the C-TPAT program, a voluntary program in which an importer agrees to work with customs to strengthen overall supply chain security. However, there can be no assurance that terrorist activity can be prevented entirely and we cannot predict the likelihood of any such activities or the extent of their adverse impact on our operations.

Our reliance on our ability to implement and sustain information technology systems

We regularly evaluate our information technology systems and are currently implementing modifications and/or upgrades to the information technology systems that support our business. Modifications include replacing legacy systems with successor systems, making changes to legacy systems or acquiring new systems with new functionality. We are aware of inherent risks associated with operating, replacing and modifying these systems, including inaccurate system information and system disruptions. We believe we are taking appropriate action to mitigate the risks through testing, training, staging implementation and in-sourcing certain processes, as well as securing appropriate commercial contracts with third-party vendors supplying such replacement and redundancy technologies; however, there is a risk that information technology system disruptions and inaccurate system information, if not anticipated and/or promptly and appropriately mitigated, could have a material adverse effect on our results of operations.

11

Our inability to safeguard against security breaches with respect to our information technology systems

Our business employs systems and websites that allow for the storage and transmission of proprietary or confidential information regarding our business, customers and employees including credit card information. Security breaches could expose us to a risk of loss or misuse of this information and potential liability. We may not be able to anticipate or prevent rapidly evolving types of cyber-attacks. Actual or anticipated attacks may cause us to incur increasing costs including costs to deploy additional personnel and protection technologies, train employees and engage third-party experts and consultants. Advances in computer capabilities, new technological discoveries or other developments may result in the technology used by us to protect transaction or other data being breached or compromised. Data and security breaches can also occur as a result of non-technical issues including intentional or inadvertent breach by employees or persons with whom we have commercial relationships that result in the unauthorized release of personal or confidential information. Any compromise or breach could result in a violation of applicable privacy and other laws, significant financial exposure and a loss of confidence in our security measures, which could have an adverse effect on our results of operations and our reputation.

Our reliance on key personnel

Our success depends to a significant extent upon our ability to attract and retain qualified key personnel, including senior management. Collective or individual changes in our senior management and other key personnel could have an adverse effect on our ability to determine and execute our strategies, which could adversely affect our business and results of operations. There is a high level of competition for senior management and other key personnel, and we cannot be assured we will be able to attract, retain and develop a sufficient number of qualified senior managers and other key personnel.

Failure to comply with regulatory requirements

As a public company, we are subject to numerous regulatory requirements, including those imposed by the Sarbanes-Oxley Act of 2002, the SEC and the NYSE. In addition, we are subject to numerous domestic and foreign laws and regulations affecting our business, including those related to labor, employment, worker health and safety, competition, privacy, consumer protection, import/export and anti-corruption, including the Foreign Corrupt Practices Act. Although we have put into place policies and procedures aimed at ensuring legal and regulatory compliance, our employees, subcontractors, vendors and suppliers could take actions that violate these requirements, which could have a material adverse effect on our reputation, financial condition and on the market price of our common stock. In addition, regulatory developments regarding the use of "conflict minerals," certain minerals originating from the Democratic Republic of Congo and adjoining countries, could affect the sourcing and availability of raw materials used by suppliers and subject us to costs associated with the regulations, including for the diligence pertaining to the presence of any conflict minerals used in our products, possible changes to products, processes or sources of our inputs, and reporting requirements.

Fluctuations in foreign currency exchange rates

We have foreign currency exchange rate risk with respect to revenues, expenses, assets and liabilities denominated in currencies other than the U.S. dollar. We currently do not utilize hedging instruments to mitigate foreign currency exchange risks. Specifically, fluctuations in the value of the Canadian Dollar, Mexican Peso, Chinese Yuan, Hong Kong Dollar, British Pound and Euro against the U.S. Dollar could have a material adverse effect on our results of operations, financial condition and cash flows.

Fluctuations in our tax obligations and effective tax rate

We are subject to income taxes in many U.S. and certain foreign jurisdictions. We record tax expense based on our estimates of future payments, which include reserves for uncertain tax positions in multiple tax jurisdictions. At any one time, multiple tax years are subject to audit by various taxing authorities. The results of these audits and negotiations with taxing authorities may affect the ultimate settlement of these issues. In addition, the tax laws and regulations in the countries where we operate may change or there may be changes in interpretation and enforcement of existing tax laws. Significant tax law changes are being evaluated by the Federal Government of the United States, our most significant country of operation. Such tax law changes, including a border adjustment tax, if enacted, could materially increase our income tax expense, which would have a material adverse effect on our results of operations. As a result, we expect that throughout the year there could be ongoing variability in our quarterly tax rates as events occur and

12

exposures are evaluated. In addition, our effective tax rate in a given financial statement period may be materially impacted by changes in the mix and level of earnings by jurisdiction or by changes to existing accounting rules or regulations.

Impact of various legal proceedings, lawsuits, disputes, and claims

As a multinational company, we are subject to various proceedings, lawsuits, disputes, and claims ("Actions") arising in the ordinary course of our business. Many of these Actions raise complex factual and legal issues and are subject to uncertainties. Actions filed against us from time to time include commercial, intellectual property, customer, employment, and data privacy claims, including class action lawsuits. Actions are in various procedural stages and some are covered in part by insurance. We cannot predict with assurance the outcome of Actions brought against us. Accordingly, developments, settlements, or resolutions may occur and impact income in the quarter of such development, settlement, or resolution. An unfavorable outcome could have an adverse impact on our business, financial condition and results of operations.

Other risk factors

Additionally, other factors could adversely affect our financial performance, including factors such as: our ability to successfully acquire and integrate other businesses; any interruption of our key infrastructure systems, including exceeding capacity in our distribution centers; any disaster or casualty resulting in the interruption of service from our distribution centers or in a large number of our stores; any interruption of our business related to an outbreak of a pandemic disease in a country where we source or market our merchandise; extreme weather conditions or changes in climate conditions or weather patterns; the effects of changes in interest rates; and international and domestic acts of terror.

The impact of any of the previously discussed factors, some of which are beyond our control, may cause our actual results to differ materially from expected results in these statements and other forward-looking statements we may make from time-to-time.

Item 1B. Unresolved Staff Comments.

Not applicable.

Item 2. Properties.

We own two buildings in urban Pittsburgh, Pennsylvania which house our corporate headquarters. These buildings total 186,000 square feet and 150,000 square feet, respectively.

In suburban Pittsburgh, Pennsylvania, we own a 45,000 square foot building, which houses our data center and additional office space and lease an additional location of approximately 18,000 square feet, which is used for storage space. This lease expires in 2017.

We rent approximately 182,000 square feet of office space in New York, New York for our designers and sourcing and production teams. The lease for this space expires in 2026.

We lease 9,200 square feet of office space in San Francisco, California that functions as a technology center for our engineers and digital marketing team focused on our omni-channel strategy. The lease for this space expires in 2019.

We also lease offices in international locations including 6,600 square feet in Mexico City expiring in 2020, 15,400 square feet in Hong Kong expiring in 2017 and 11,300 square feet in Shanghai, China expiring in 2019.

We own distribution facilities in Ottawa, Kansas and Hazleton, Pennsylvania consisting of approximately 1.2 million and 1.0 million square feet, respectively. These facilities are used to support new and existing growth initiatives, including AEO Direct and Aerie.

We lease a building in Mississauga, Ontario with approximately 294,000 square feet, which houses our Canadian distribution center. The lease expires in 2028.

13

All of our stores are leased and generally have initial terms of 10 years. Certain leases also include early termination options, which can be exercised under specific conditions. Most of these leases provide for base rent and require the payment of a percentage of sales as additional contingent r ent when sales reach specified levels. Under our store leases, we are typically responsible for tenant occupancy costs, including maintenance and common area charges, real estate taxes and certain other expenses. We have generally been successful in negoti ating renewals as leases near expiration.

Item 3. Legal Proceedings.

We are involved, from time to time, in actions associated with or incidental to our business, including, among other things, matters involving credit card fraud, trademark and other intellectual property, licensing, importation of products, taxation, and employee relations. We believe at present that the resolution of currently pending matters will not individually or in the aggregate have a material adverse effect on our financial position or results of operations. However, our assessment of any litigation or other legal claims could potentially change in light of the discovery of facts not presently known or determinations by judges, juries, or other finders of fact which are not in accord with management's evaluation of the possible liability or outcome of such litigation or claims.

Item 4. Mine Safety Disclosures.

Not Applicable.

PART II

Item 5. Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is traded on the NYSE under the symbol "AEO". As of March 6, 2017, there were 511 stockholders of record. However, when including associates who own shares through our employee stock purchase plan, and others holding shares in broker accounts under street name, we estimate the stockholder base at approximately 50,000. The following table sets forth the range of high and low closing prices of the common stock as reported on the NYSE during the periods indicated.

|

| Market Price |

|

| Cash Dividends per |

| ||||||

For the Quarters Ended |

| High |

|

| Low |

|

| Common Share |

| |||

January 28, 2017 |

| $ | 18.91 |

|

| $ | 14.45 |

|

| $ | 0.125 |

|

October 29, 2016 |

| $ | 19.37 |

|

| $ | 16.80 |

|

| $ | 0.125 |

|

July 30, 2016 |

| $ | 17.92 |

|

| $ | 13.39 |

|

| $ | 0.125 |

|

April 30, 2016 |

| $ | 16.90 |

|

| $ | 13.12 |

|

| $ | 0.125 |

|

January 30, 2016 |

| $ | 16.64 |

|

| $ | 13.24 |

|

| $ | 0.125 |

|

October 31, 2015 |

| $ | 18.35 |

|

| $ | 14.68 |

|

| $ | 0.125 |

|

August 1, 2015 |

| $ | 18.31 |

|

| $ | 15.74 |

|

| $ | 0.125 |

|

May 2, 2015 |

| $ | 17.90 |

|

| $ | 13.96 |

|

| $ | 0.125 |

|

During Fiscal 2016 and Fiscal 2015, we paid quarterly dividends as shown in the table above. The payment of future dividends is at the discretion of our Board of Directors (the "Board") and is based on future earnings, cash flow, financial condition, capital requirements, changes in U.S. taxation and other relevant factors. It is anticipated that any future dividends paid will be declared on a quarterly basis.

14

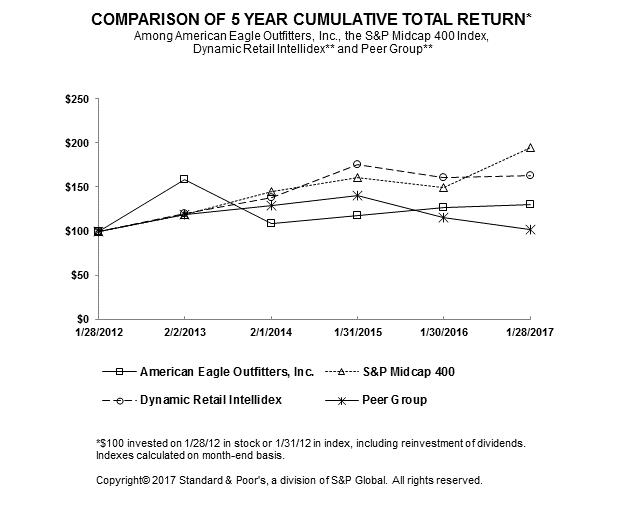

Performan ce Graph

The following Performance Graph and related information shall not be deemed "soliciting material" or to be filed with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Exchange Act of 1934, each as amended, except to the extent that we specifically incorporate it by reference into such filing.

The following graph compares the changes in the cumulative total return to holders of our common stock with that of the S&P Midcap 400, the Dynamic Retail Intellidex and our peer group as described below. The comparison of the cumulative total returns for each investment assumes that $100 was invested in our common stock and the respective index on January 28, 2012 and includes reinvestment of all dividends. The plotted points are based on the closing price on the last trading day of the fiscal year indicated.

|

| 1/28/12 |

| 2/2/13 |

| 2/1/14 |

| 1/31/15 |

| 1/30/16 |

| 1/28/17 |

| ||||||

American Eagle Outfitters, Inc. |

|

| 100.00 |

|

| 158.72 |

|

| 109.00 |

|

| 117.59 |

|

| 126.39 |

|

| 130.52 |

|

S&P Midcap 400 |

|

| 100.00 |

|

| 118.56 |

|

| 144.48 |

|

| 160.22 |

|

| 149.49 |

|

| 194.59 |

|

Dynamic Retail Intellidex |

|

| 100.00 |

|

| 120.40 |

|

| 138.36 |

|

| 175.44 |

|

| 160.52 |

|

| 163.21 |

|

Peer Group |

|

| 100.00 |

|

| 118.50 |

|

| 128.89 |

|

| 140.18 |

|

| 115.04 |

|

| 102.18 |

|

**For Fiscal 2016, we compared our cumulative total return to a custom peer group that consisted of the following companies: Abercrombie & Fitch Co., Ascena Retail Group. Inc., Burberry Group PLC, Chico's FAS, Inc., Coach, Inc., Express, Inc., Gap, Inc., Guess?, Inc., Hanesbrands Inc., L Brands Inc., Lululemon Athletica, Inc., Michael Kors Holdings LTD, PVH Corp, Ralph Lauren Corp., Tailored Brands Inc., Under Armour Inc, and Urban Outfitters, Inc. Prior to Fiscal 2016, we compared our cumulative total return to the published Dynamic Retail Intellidex. We believe that the comparison

15

to a custom peer group provides a more accurate index of organizations that we benchmark against and therefore will provide a more accurate compa rison of stock performance.

The following table provides information regarding our repurchases of common stock during the three months ended January 28, 2017.

Issuer Purchases of Equity Securities

|

|

|

|

|

|

|

|

|

| Total Number of |

|

| Maximum Number of |

| ||

|

| Total |

|

| Average |

|

| Shares Purchased as |

|

| Shares that May |

| ||||

|

| Number of |

|

| Price Paid |

|

| Part of Publicly |

|

| Yet be Purchased |

| ||||

Period |

| Shares Purchased |

|

| Per Share |

|

| Announced Programs |

|

| Under the Program |

| ||||

|

| (1) |

|

| (2) |

|

| (1) (3) |

|

| (3) |

| ||||

Month #1 (October 30, 2016 through November 26, 2016) |

|

| 7,605 |

|

| $ | 16.53 |

|

|

| - |

|

|

| 27,837,016 |

|

Month #2 (November 27, 2016 through December 31, 2016) |

|

| 531 |

|

| $ | 16.54 |

|

|

|

|

|

|

| 27,837,016 |

|

Month #3 (January 1, 2017 through January 28, 2017) |

|

| 3 |

|

| $ | 15.17 |

|

|

|

|

|

|

| 25,000,000 |

|

Total |

|

| 8,139 |

|

| $ | 16.53 |

|

|

| - |

|

|

| 25,000,000 |

|

(1) | There were no shares repurchased as part of our publicly announced share repurchase program during the three months ended January 28, 2017 and there were 8,139 shares repurchased for the payment of taxes in connection with the vesting of share-based payments. |

(2) | Average price paid per share excludes any broker commissions paid. |

(3) | In January 2013, our Board authorized the repurchase of 20.0 million shares of our common stock. The authorization of the remaining 2.8 million shares that may yet be purchased expired on January 28, 2017. During Fiscal 2016 our Board authorized 25.0 million shares under a new share repurchase program which expires on January 30, 2021. |

The following table sets forth additional information as of the end of Fiscal 2016, about shares of our common stock that may be issued upon the exercise of options and other rights under our existing equity compensation plans and arrangements, divided between plans approved by our stockholders and plans or arrangements not submitted to our stockholders for approval. The information includes the number of shares covered by, and the weighted average exercise price of, outstanding options and other rights and the number of shares remaining available for future grants excluding the shares to be issued upon exercise of outstanding options, warrants and other rights.

Equity Compensation Plan Table

|

| Column (a) |

|

| Column (b) |

|

| Column (c) |

| |||

|

|

|

|

|

|

|

|

|

| Number of securities |

| |

|

|

|

|

|

|

|

|

|

| remaining available |

| |

|

| Number of securities |

|

| Weighted-average |

|

| for issuance under |

| |||

|

| to be issued upon |

|

| exercise price of |

|

| equity compensation |

| |||

|

| exercise of outstanding |

|

| outstanding options, |

|

| plans (excluding |

| |||

|

| options, |

|

| warrants and |

|

| securities reflected |

| |||

|

| warrants and rights (1) |

|

| rights (1) |

|

| in column (a)) (1) |

| |||

Equity compensation plans approved by stockholders |

|

| 2,313,889 |

|

| $ | 15.33 |

|

|

| 3,364,255 |

|

Equity compensation plans not approved by stockholders |

|

| - |

|

|

| - |

|

|

| - |

|

Total |

|

| 2,313,889 |

|

| $ | 15.33 |

|

|

| 3,364,255 |

|

(1) | Equity compensation plans approved by stockholders include the 2005 Stock Award and Incentive Plan, as amended (the "2005 Plan") and the 2014 Stock Award and Incentive Plan (the "2014 Plan"). |

16

Item 6. Selected Consol idated Financial Data.

The following Selected Consolidated Financial Data should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations," included under Item 7 below and the Consolidated Financial Statements and Notes thereto, included in Item 8 below. Most of the selected Consolidated Financial Statements data presented below is derived from our Consolidated Financial Statements, if applicable, which are filed in response to Item 8 below. The selected Consolidated Statement of Operations data for the years ended February 1, 2014 and February 2, 2013 and the selected Consolidated Balance Sheet data as of January 31, 2015, February 1, 2014 and February 2, 2013 are derived from audited Consolidated Financial Statements not included herein.

|

| For the Years Ended (1) |

| |||||||||||||||||

(In thousands, except per share amounts, ratios and other |

| January 28 , |

|

| January 30, |

|

| January 31, |

|

| February 1, |

|

| February 2, |

| |||||

non-financial information) |

| 2017 |

|

| 2016 |

|

| 2015 |

|

| 2014 |

|

| 2013 |

| |||||

Summary of Operations (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total net revenue |

| $ | 3,609,865 |

|

| $ | 3,521,848 |

|

| $ | 3,282,867 |

|

| $ | 3,305,802 |

|

| $ | 3,475,802 |

|

Comparable sales increase (decrease) (3) |

|

| 3 | % |

|

| 7 | % |

|

| (5 | )% |

|

| (6 | )% |

|

| 9 | % |

Gross profit |

| $ | 1,366,927 |

|

| $ | 1,302,734 |

|

| $ | 1,154,674 |

|

| $ | 1,113,999 |

|

| $ | 1,390,322 |

|

Gross profit as a percentage of net sales |

|

| 37.9 | % |

|

| 37.0 | % |

|

| 35.2 | % |

|

| 33.7 | % |

|

| 40.0 | % |

Operating income |

| $ | 331,476 |

|

| $ | 319,878 |

|

| $ | 155,765 |

|

| $ | 141,055 |

|

| $ | 394,606 |

|

Operating income as a percentage of net sales |

|

| 9.2 | % |

|

| 9.1 | % |

|

| 4.7 | % |

|

| 4.3 | % |

|

| 11.4 | % |

Income from continuing operations |

| $ | 212,449 |

|

| $ | 213,291 |

|

| $ | 88,787 |

|

| $ | 82,983 |

|

| $ | 264,098 |

|

Income from continuing operations as a percentage of net sales |

|

| 5.9 | % |

|

| 6.1 | % |

|

| 2.6 | % |

|

| 2.5 | % |

|

| 7.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Share Results |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income from continuing operations per common share-basic |

| $ | 1.17 |

|

| $ | 1.10 |

|

| $ | 0.46 |

|

| $ | 0.43 |

|

| $ | 1.35 |

|

Income from continuing operations per common share-diluted |

| $ | 1.16 |

|

| $ | 1.09 |

|

| $ | 0.46 |

|

| $ | 0.43 |

|

| $ | 1.32 |

|

Weighted average common shares outstanding – basic |

|

| 181,429 |

|

|

| 194,351 |

|

|

| 194,437 |

|

|

| 192,802 |

|

|

| 196,211 |

|

Weighted average common shares outstanding – diluted |

|

| 183,835 |

|

|

| 196,237 |

|

|

| 195,135 |

|

|

| 194,475 |

|

|

| 200,665 |

|

Cash dividends per common share |

| $ | 0.50 |

|

| $ | 0.50 |

|

| $ | 0.50 |

|

| $ | 0.38 |

|

| $ | 2.05 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance Sheet Information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total cash and short-term investments |

| $ | 378,613 |

|

| $ | 260,067 |

|

| $ | 410,697 |

|

| $ | 428,935 |

|

| $ | 630,992 |

|

Long-term investments |

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

Total assets |

| $ | 1,782,660 |

|

| $ | 1,612,246 |

|

| $ | 1,696,908 |

|

| $ | 1,694,164 |

|

| $ | 1,756,053 |

|

Long & short-term debt |

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

| $ | - |

|

Stockholders' equity |

| $ | 1,204,569 |

|

| $ | 1,051,376 |

|

| $ | 1,139,746 |

|

| $ | 1,166,178 |

|

| $ | 1,221,187 |

|

Working capital |

| $ | 407,446 |

|

| $ | 259,693 |

|

| $ | 368,947 |

|

| $ | 462,604 |

|

| $ | 647,668 |

|

Current ratio |

|

| 1.83 |

|

|

| 1.56 |

|

|

| 1.80 |

|

|

| 2.11 |

|

|

| 2.49 |

|

Average return on stockholders' equity (5) |

|

| 18.8 | % |

|

| 19.9 | % |

|

| 7.0 | % |

|

| 7.0 | % |

|

| 17.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Financial Information (2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total stores at year-end |

|

| 1,050 |

|

|

| 1,047 |

|

|

| 1,056 |

|

|

| 1,066 |

|

|

| 1,044 |

|

Capital expenditures |

| $ | 161,494 |

|

| $ | 153,256 |

|

| $ | 245,002 |

|

| $ | 278,499 |

|

| $ | 93,939 |

|

Total net revenue per average selling square foot (4) |

| $ | 534 |

|

| $ | 545 |

|

| $ | 525 |

|

| $ | 547 |

|

| $ | 602 |

|

Total selling square feet at end of period |

|

| 5,311,659 |

|

|

| 5,285,025 |

|

|

| 5,294,744 |

|

|

| 5,205,948 |

|

|

| 4,962,923 |

|

Total net revenue per average gross square foot (4) |

| $ | 428 |

|

| $ | 436 |

|

| $ | 420 |

|

| $ | 444 |

|

| $ | 489 |

|

Total gross square feet at end of period |

|

| 6,619,267 |

|

|

| 6,601,112 |

|

|

| 6,613,100 |

|

|

| 6,503,486 |

|

|

| 6,023,278 |

|

Number of employees at end of period |

|

| 38,700 |

|

|

| 37,800 |

|

|

| 38,000 |

|

|

| 40,400 |

|

|

| 40,100 |

|

(1) | Except for the fiscal year ended February 2, 2013, which includes 53 weeks, a ll fiscal years presented include 52 weeks. |

17

(2) | All amounts presented are from continuing operations for all periods presented. Refer to Note 15 to the accompanying Consolidated Financial Statements for additional information regarding the discontinued operations of 77kids in 2012. |

(3) | The comparable sales increase for Fiscal 2012 ended February 2, 2013 is compared to the corresponding 53 week period in Fiscal 2011. Additionally, comparable sales for all periods include AEO Direct sales. |

(4) | Total net revenue per average square foot is calculated using retail store sales for the year divided by the straight average of the beginning and ending square footage for the year. |

(5) | Average return on stockholders' equity is calculated by using the annual reported net income divided by the straight average of the beginning and ending stockholders' equity balances from the consolidated balance sheets. |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis of financial condition and results of operations are based upon our Consolidated Financial Statements and should be read in conjunction with those statements and notes thereto.

This report contains various "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which represent our expectations or beliefs concerning future events, including the following:

• | the planned opening of approximately 15 to 20 American Eagle Outfitters stores and 15 Aerie stores, and conversion of 30 to 35 Aerie side-by-side format stores in North America during Fiscal 2017; |

• | the success of our efforts to expand internationally, engage in future franchise/license agreements, and/or growth through acquisitions or joint ventures; |

• | the selection of approximately 60 to 65 American Eagle Outfitters stores in the United States and Canada for remodeling and refurbishing during Fiscal 2017; |

• | the potential closure of approximately 15 to 20 American Eagle Outfitters and 8 to 10 Aerie stores primarily in North America during Fiscal 2017; |

• | the planned opening of approximately 30 new international third-party operated American Eagle Outfitters stores during Fiscal 2017; |

• | the success of our core American Eagle Outfitters and Aerie brands through our omni-channel and licensed outlets within North America and internationally; |

• | the success of our business priorities and strategies; |

• | the expected payment of a dividend in future periods; |

• | the possibility that our credit facilities may not be available for future borrowings; |

• | the possibility that rising prices of raw materials, labor, energy and other inputs to our manufacturing process, if unmitigated, will have a significant impact to our profitability; and |

• | the possibility that we may be required to take additional store impairment charges related to underperforming stores. |

We caution that these forward-looking statements, and those described elsewhere in this report, involve material risks and uncertainties and are subject to change based on factors beyond our control, as discussed within Part I, Item 1A of this Form 10-K. Accordingly, our future performance and financial results may differ materially from those expressed or implied in any such forward-looking statement.

Critical Accounting Policies

Our Consolidated Financial Statements are prepared in accordance with accounting principles generally accepted in the United States ("GAAP"), which require us to make estimates and assumptions that may affect the reported financial condition and results of operations should actual results differ from these estimates. We base our estimates and assumptions on the best available information and believe them to be reasonable for the circumstances. We believe that of our significant accounting policies, the following involve a higher degree of judgment and complexity. Refer to Note 2 to the Consolidated Financial Statements for a complete discussion of our significant accounting policies. Management has reviewed these critical accounting policies and estimates with the Audit Committee of our Board.

18

Revenue Recognition. We record revenue for store sales upon the purchase of merchandise by customers. Our e-commerce operation records revenue upon the estimated customer receipt date of the merchandise. Revenue is not recorde d on the purchase of gift cards. A current liability is recorded upon purchase, and revenue is recognized when the gift card is redeemed for merchandise.

We estimate gift card breakage and recognize revenue in proportion to actual gift card redemptions as a component of total net revenue. We determine an estimated gift card breakage rate by continuously evaluating historical redemption data and the time when there is a remote likelihood that a gift card will be redeemed.

Revenue is recorded net of estimated and actual sales returns and deductions for coupon redemptions and other promotions. The estimated sales return reserve is based on projected merchandise returns determined through the use of historical average return percentages. We do not believe there is a reasonable likelihood that there will be a material change in the future estimates or assumptions we use to calculate our sales return reserve. However, if the actual rate of sales returns increases significantly, our operating results could be adversely affected.

We recognize royalty revenue generated from our license or franchise agreements based upon a percentage of merchandise sales by the licensee/franchisee. This revenue is recorded as a component of total net revenue when earned.

Merchandise Inventory. Merchandise inventory is valued at the lower of average cost or market, utilizing the retail method. Average cost includes merchandise design and sourcing costs and related expenses. We record merchandise receipts at the time which both title and risk of loss for the merchandise transfers to us.

We review our inventory in order to identify slow-moving merchandise and generally use markdowns to clear merchandise. Additionally, we estimate a markdown reserve for future planned markdowns related to current inventory. If inventory exceeds customer demand for reasons of style, seasonal adaptation, changes in customer preference, lack of consumer acceptance of fashion items, competition, or if it is determined that the inventory in stock will not sell at its currently ticketed price, additional markdowns may be necessary. These markdowns may have a material adverse impact on earnings, depending on the extent and amount of inventory affected.

We estimate an inventory shrinkage reserve for anticipated losses for the period between the last physical count and the balance sheet date. The estimate for the shrinkage reserve is calculated based on historical percentages and can be affected by changes in merchandise mix and changes in actual shrinkage trends. We do not believe there is a reasonable likelihood that there will be a material change in the future estimates or assumptions we use to calculate our inventory shrinkage reserve. However, if actual physical inventory losses differ significantly from our estimate, our operating results could be adversely affected.

Asset Impairment. In accordance with Financial Accounting Standards Board ("FASB") Accounting Standard Codification ("ASC") 360, Property, Plant, and Equipment ("ASC 360"), we evaluate long-lived assets for impairment at the individual store level, which is the lowest level at which individual cash flows can be identified. Impairment losses are recorded on long-lived assets used in operations when events and circumstances indicate that the assets might be impaired and the undiscounted cash flows estimated to be generated by those assets are less than the carrying amounts of the assets. When events such as these occur, the impaired assets are adjusted to their estimated fair value and an impairment loss is recorded separately as a component of operating income.