UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| ☑ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) |

| OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the Fiscal Year Ended January 28, 2012 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) |

| OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 1-33338

American Eagle Outfitters, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | No. 13-2721761 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 77 Hot Metal Street, Pittsburgh, PA | 15203-2329 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant's telephone number, including area code:

(412) 432-3300

Securities registered pursuant to Section 12(b) of the Act:

| Common Shares, $0.01 par value | New York Stock Exchange | |

| (Title of class) | (Name of each exchange on which registered) |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☑ NO ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Sections 15(d) of the Act. YES ¨ NO ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for at the past 90 days. YES ☑ NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ☑ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☑ | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ¨ NO ☑

The aggregate market value of voting and non-voting common equity held by non-affiliates of the registrant as of July 30, 2011 was $2,334,798,008.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date: 194,539,858 Common Shares were outstanding at March 12, 2012.

DOCUMENTS INCORPORATED BY REFERENCE

Part III - Proxy Statement for 2012 Annual Meeting of Stockholders, in part, as indicated.

AMERICAN EAGLE OUTFITTERS, INC.

TABLE OF CONTENTS

| Page Number | ||||||

| PART I | ||||||

Item 1. | Business | 2 | ||||

Item 1A. | Risk Factors | 9 | ||||

Item 1B. | Unresolved Staff Comments | 12 | ||||

Item 2. | Properties | 12 | ||||

Item 3. | Legal Proceedings | 13 | ||||

Item 4. | Mine Safety Disclosures | 13 | ||||

| PART II | ||||||

Item 5. | Market for the Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 14 | ||||

Item 6. | Selected Consolidated Financial Data | 17 | ||||

Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | 18 | ||||

Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 32 | ||||

Item 8. | Financial Statements and Supplementary Data | 33 | ||||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 68 | ||||

Item 9A. | Controls and Procedures | 68 | ||||

Item 9B. | Other Information | 70 | ||||

| PART III | ||||||

Item 10. | Directors, Executive Officers and Corporate Governance | 70 | ||||

Item 11. | Executive Compensation | 70 | ||||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 70 | ||||

Item 13. | Certain Relationships and Related Transactions, and Director Independence | 70 | ||||

Item 14. | Principal Accounting Fees and Services | 70 | ||||

| PART IV | ||||||

Item 15. | Exhibits, Financial Statement Schedules | 70 | ||||

1

PART I

ITEM 1. BUSINESS.

General

American Eagle Outfitters, Inc. a Delaware corporation (the "Company"), operates under the American Eagle ® , aerie ® by American Eagle ® , and 77kids by american eagle ® brands. The Company operated the MARTIN+OSA ® brand ("M+O") until its closure during Fiscal 2010.

Founded in 1977, American Eagle Outfitters ® is a leading specialty retailer that operates more than 1,000 retail stores in the U.S. and Canada, and online at ae.com ® . Through our family of brands, American Eagle Outfitters, Inc. offers high quality, on-trend clothing, accessories and personal care products at affordable prices. Our online business, AEO Direct, ships to 77 countries worldwide.

As used in this report, all references to "we," "our" and the "Company" refer to American Eagle Outfitters, Inc. ("AEO, Inc.") and its wholly-owned subsidiaries. "American Eagle Outfitters," "American Eagle," "AE" and the "AE Brand" refer to our U.S. and Canadian American Eagle Outfitters ® stores. "AEO Direct" refers to our e-commerce operations, ae.com ® , aerie.com and 77kids.com. "MARTIN+OSA" or "M+O" refers to the MARTIN+OSA stores and e-commerce operation which we operated until its closure during Fiscal 2010.

Our financial year is a 52/53 week year that ends on the Saturday nearest to January 31. As used herein, "Fiscal 2012" refers to the 53 week period ending February 2, 2013. "Fiscal 2011," "Fiscal 2010," "Fiscal 2009," "Fiscal 2008" and "Fiscal 2007" refer to the 52 week periods ended January 28, 2012, January 29, 2011, January 30, 2010, January 31, 2009 and February 2, 2008, respectively. "Fiscal 2006" refers to the 53 week period ended February 3, 2007.

On March 5, 2010, our Board of Directors (the "Board") approved management's recommendation to proceed with the closure of the M+O brand. We completed the closure of M+O stores and its e-commerce operation during the second quarter of Fiscal 2010. The Consolidated Financial Statements reflect the presentation of M+O as a discontinued operation. Refer to Note 15 to the Consolidated Financial Statements for additional information regarding the discontinued operations of M+O.

As of January 28, 2012, we operated 911 American Eagle Outfitters stores, 158 aerie stand-alone stores and 21 77kids stores. We also had 21 franchised stores operated by our franchise partners in 10 countries.

Information concerning our segments and certain geographic information is contained in Note 2 of the Consolidated Financial Statements included in this Form 10-K and is incorporated herein by reference. Additionally, a five-year summary of certain financial and operating information can be found in Part II, Item 6, Selected Consolidated Financial Data, of this Form 10-K. See also Part II, Item 8, Financial Statements and Supplementary Data.

Growth Strategy

Our primary growth strategies are focused on the following key areas of opportunity:

AE Brand

The American Eagle Outfitters ® brand targets 15 to 25-year old men and women. Denim is the cornerstone of the American Eagle ® product assortment, which is complemented by other key categories including sweaters, graphic t-shirts, fleece, outerwear and accessories. American Eagle ® is honest, real, individual and fun. American Eagle ® is priced to be worn by everyone, everyday, delivering value through quality and style.

2

Gaining market share in key categories, such as knit tops and fleece, is a primary focus within the AE Brand. In addition, we will build upon our leading position in denim. Delivering value, variety and versatility to our customers remains a top priority. We will offer value at all levels of the assortment, punctuated with promotions. We are reducing production lead-times, which enables us to react more quickly to emerging trends. Finally, we continue to innovate our store experience to be more impactful from front to back.

aerie by American Eagle

In the fall of 2006, the Company launched aerie ® by American Eagle ® ("aerie"), a collection of Dormwear ® , intimates and personal care products for the AE ® girl. The collection is available in 158 stand-alone aerie stores throughout the United States and Canada, online at aerie.com and at select American Eagle ® stores. aerie, with intimates at the core, is beautiful, feminine, soft, sensuous, yet comfortable.

77kids by american eagle

Introduced in October of 2008 as an online-only brand, 77kids by american eagle ® ("77kids") offers on-trend, high-quality clothing and accessories for kids ages two to 14 and babies under the brand name little77 TM . 77kids is available in 21 stores throughout the United States. The brand draws from the strong heritage of American Eagle Outfitters ® , with a point-of-view that is thoughtful, playful and real. Like American Eagle ® clothing, 77kids focuses on great fit, value and style. All 77kids ® clothing is backed by the brand's 77wash TM and 77soft TM guarantees to maintain size, shape and quality and to be extremely soft and comfortable through dozens of washes.

AEO Direct

We sell merchandise via our e-commerce operations, ae.com ® , aerie.com and 77kids.com, which are extensions of the lifestyle that we convey in our stores. We currently ship to 77 countries. In addition to purchasing items online, customers can experience AEO Direct in-store through Store-to-Door. Store-to-Door enables store associates to sell any item available online to an in-store customer in a single transaction. Customers are taking advantage of Store-to-Door by purchasing extended sizes that are not available in-store, as well as finding a certain size or color that happens to be out-of-stock at the time of their visit. The ordered items are shipped to the customer's home free of charge. We accept PayPal ® and Bill Me Later ® as a means of payment from our ae.com ® , aerie.com and 77kids.com customers. We are continuing to focus on the growth of AEO Direct through various initiatives, including improved site efficiency and faster check-out, expansion of sizes and styles, on-line specialty shops and targeted marketing strategies.

Real Estate

We continue to remain focused on the real-estate strategies that we have in place to grow our business and strengthen our financial performance utilizing our most productive formats.

We continue the expansion of our brands throughout the United States. At the end of Fiscal 2011, we operated in all 50 states, Puerto Rico and Canada. During Fiscal 2011, we opened 33 new stores, consisting of 11 AE stores, 10 aerie stores and 12 77kids stores. These store openings, partially offset by 29 store closings, increased our total store base to 1,090 stores.

Our stores average approximately 5,870 gross square feet and approximately 4,690 on a selling square foot basis. Our gross square footage increased by approximately 1% during Fiscal 2011, with approximately 54% attributable to the incremental square footage from store remodels and the remaining 46% attributable to new store openings.

During Fiscal 2011, we remodeled and refurbished a total of 106 AE stores. Five stores were remodeled with an expansion to their existing locations, 10 stores were relocated to a larger space within the mall, two stores were remodeled within their existing locations and 89 stores were refurbished as discussed below.

3

Remodeling of our AE stores into our current store format is important to enhance our customer's shopping experience. In order to maintain a balanced presentation and to accommodate additional product categories, we selectively enlarge our stores during the remodeling process to an average of 6,400 gross square feet, either within their existing location or by upgrading the store location within the mall. We believe the larger format can better accommodate our expansion of merchandise categories. We select stores for expansion or relocation based on market demographics and store volume forecasts.

We maintain a cost effective store refurbishment program targeted towards our lower volume stores, typically located in smaller markets. Stores selected as part of this program maintain their current location and size but are updated to include certain aspects of our current store format, including paint and new fixtures.

In Fiscal 2012, we plan to open approximately 14 AE and one 77kids store. We also plan to remodel and refurbish approximately 100 existing AE stores and close approximately 20 to 30 stores. Our square footage growth is expected to decrease slightly in Fiscal 2012. We believe that there are attractive retail locations where we can continue to open American Eagle stores and our other brands in enclosed regional malls, urban areas and lifestyle centers.

The table below shows certain information relating to our historical store growth from continuing operations.

| Fiscal 2011 | Fiscal 2010 | Fiscal 2009 | Fiscal 2008 | Fiscal 2007 | ||||||||||||||||

Consolidated stores at beginning of period | 1,086 | 1,075 | 1,070 | 968 | 906 | |||||||||||||||

Consolidated stores opened during the period | 33 | 34 | 29 | 112 | 66 | |||||||||||||||

Consolidated stores closed during the period | (29 | ) | (23 | ) | (24 | ) | (10 | ) | (4 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total consolidated stores at end of period | 1,090 | 1,086 | 1,075 | 1,070 | 968 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| Fiscal 2011 | Fiscal 2010 | Fiscal 2009 | Fiscal 2008 | Fiscal 2007 | ||||||||||||||||

AE Brand stores at beginning of period | 929 | 938 | 954 | 929 | 903 | |||||||||||||||

AE Brand stores opened during the period | 11 | 14 | 8 | 35 | 30 | |||||||||||||||

AE Brand stores closed during the period | (29 | ) | (23 | ) | (24 | ) | (10 | ) | (4 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total AE Brand stores at end of period | 911 | 929 | 938 | 954 | 929 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| Fiscal 2011 | Fiscal 2010 | Fiscal 2009 | Fiscal 2008 | Fiscal 2007 | ||||||||||||||||

aerie stores at beginning of period | 148 | 137 | 116 | 39 | 3 | |||||||||||||||

aerie stores opened during the period | 10 | 11 | 21 | 77 | 36 | |||||||||||||||

aerie stores closed during the period | - | - | - | - | - | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total aerie stores at end of period | 158 | 148 | 137 | 116 | 39 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

| Fiscal 2011 | Fiscal 2010 | Fiscal 2009 | Fiscal 2008 | Fiscal 2007 | ||||||||||||||||

77kids stores at beginning of period | 9 | - | - | - | - | |||||||||||||||

77kids stores opened during the period | 12 | 9 | - | - | - | |||||||||||||||

77kids stores closed during the period | - | - | - | - | - | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total 77kids stores at end of period | 21 | 9 | - | - | - | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

4

Consolidated Store Locations

As of January 28, 2012, we operated 1,090 stores in the United States and Canada under the American Eagle Outfitters, aerie and 77kids brands as shown below:

United States, including the Commonwealth of Puerto Rico - 994 stores

Alabama | 17 | Indiana | 22 | Nebraska | 7 | Rhode Island | 4 | |||||||||||||||

Alaska | 5 | Iowa | 12 | Nevada | 4 | South Carolina | 17 | |||||||||||||||

Arizona | 16 | Kansas | 9 | New Hampshire | 9 | South Dakota | 3 | |||||||||||||||

Arkansas | 8 | Kentucky | 14 | New Jersey | 28 | Tennessee | 25 | |||||||||||||||

California | 71 | Louisiana | 14 | New Mexico | 3 | Texas | 73 | |||||||||||||||

Colorado | 11 | Maine | 5 | New York | 70 | Utah | 11 | |||||||||||||||

Connecticut | 20 | Maryland | 19 | North Carolina | 31 | Vermont | 3 | |||||||||||||||

Delaware | 5 | Massachusetts | 35 | North Dakota | 4 | Virginia | 28 | |||||||||||||||

Florida | 52 | Michigan | 34 | Ohio | 37 | Washington | 19 | |||||||||||||||

Georgia | 32 | Minnesota | 22 | Oklahoma | 12 | West Virginia | 9 | |||||||||||||||

Hawaii | 4 | Mississippi | 8 | Oregon | 12 | Wisconsin | 19 | |||||||||||||||

Idaho | 4 | Missouri | 19 | Pennsylvania | 65 | Wyoming | 2 | |||||||||||||||

Illinois | 34 | Montana | 2 | Puerto Rico | 5 |

Canada - 96 stores

| Alberta | 13 | New Brunswick | 4 | Ontario | 49 | |||||||||||||||

| British Columbia | 13 | Newfoundland | 1 | Quebec | 9 | |||||||||||||||

| Manitoba | 2 | Nova Scotia | 3 | Saskatchewan | 2 |

International Expansion

We have entered into franchise agreements with multiple partners to expand our brands internationally. Through these franchise agreements, we plan to open and operate a series of American Eagle stores in the Middle East, Northern Africa, Eastern Europe, Hong Kong, China, Israel and Japan. As of January 28, 2012, we had 21 franchised stores operated by our franchise partners in 10 countries. These franchise agreements do not involve a capital investment from AEO and require minimal operational involvement. We continue to evaluate additional opportunities to expand internationally. International franchise stores are not included in the consolidated store data or the total gross square feet calculation.

Purchasing

We purchase merchandise from suppliers who either manufacture their own merchandise, supply merchandise manufactured by others or both. During Fiscal 2011, we purchased a majority of our merchandise from non-North American suppliers.

All of our merchandise suppliers receive a vendor compliance manual that describes our quality standards and shipping instructions. We maintain a quality control department at our distribution centers to inspect incoming merchandise shipments for uniformity of sizes and colors and for overall quality of manufacturing. Periodic inspections are also made by our employees and agents at manufacturing facilities to identify quality problems prior to shipment of merchandise.

Corporate Responsibility

The Company is firmly committed to the principle that the people who make our clothes should be treated with dignity and respect. We seek to work with apparel suppliers throughout the world who share our commitment to providing safe and healthy workplaces. At a minimum, we require our suppliers to maintain a workplace environment that complies with local legal requirements and meets universally-accepted human rights standards.

5

Our Vendor Code of Conduct (the "Code"), which is based on universally-accepted human rights principles, sets forth our expectations for suppliers. The Code must be posted in every factory that manufactures our clothes in the local language of the workers. All suppliers must agree to abide by the terms of our Code before we will place production with them.

We maintain an extensive factory inspection program, through our Hong Kong compliance office, to monitor compliance with our Code. The Hong Kong team validates the inspection reporting of our third-party vendor compliance auditors and works with new and existing factories on remediation of issues. New garment factories must pass an initial inspection in order to do business with us. Once new factories are approved, we then strive to re-inspect them at least once a year. We review the outcome of these inspections with factory management with the goal of helping them to continuously improve their performance. Although our primary goal is to remediate issues and build long term relationships with our vendors, in cases where a factory is unable or unwilling to meet our standards, we will take steps up to and including the severance of our business relationship.

In September 2011, we published our first publicly available Corporate Responsibility Report, AE Better World, on our website at www.ae.com. This Report focuses on four key areas of our company: Supply Chain, Environment, Associates and Communities. Where possible, the report references relevant indicators from the Global Reporting Initiative ("GRI") G3 Guidelines and GRI Apparel & Footwear Sector Supplement.

Security Compliance

During recent years, there has been an increasing focus within the international trade community on concerns related to global terrorist activity. Various security issues and other terrorist threats have brought increased demands from the Bureau of Customs and Border Protection ("CBP") and other agencies within the Department of Homeland Security that importers take responsible action to secure their supply chains. In response, we became a certified member of the Customs - Trade Partnership Against Terrorism program ("C-TPAT") during 2004. C-TPAT is a voluntary program offered by CBP in which an importer agrees to work with CBP to strengthen overall supply chain security. Our internal security procedures were reviewed by CBP during February 2005 and a validation of processes with respect to our external partners was completed in June 2005 and then re-evaluated in June 2008. We received formal written validations of our security procedures from CBP during Fiscal 2006 and Fiscal 2008, each indicating the highest level of benefits afforded to C-TPAT members.

Historically, we took significant steps to expand the scope of our security procedures, including, but not limited to: a significant increase in the number of factory audits performed; a revision of the factory audit format to include a review of all critical security issues as defined by CBP; and a requirement that all of our international logistics partners, including forwarders, consolidators, shippers and brokers be certified members of C-TPAT. In Fiscal 2007, we further increased the scope of our inspection program to strive to include pre-inspections of all potential production facilities. In Fiscal 2009, we again expanded the program to require all suppliers that have passed pre-inspections and reached a satisfactory level of security compliance through annual factory re-audits to provide us with security self-assessments on at least an annual basis. Additionally, in Fiscal 2009, we began evaluating additional oversight options for high-risk security countries and among other things, implemented full third-party audits on an annual basis.

Trade Compliance

We act as the importer of record for substantially all of the merchandise we purchase overseas from foreign suppliers. Accordingly, we have an affirmative obligation to comply with the rules and regulations established for importers by the CBP regarding issues such as merchandise classification, valuation and country of origin. We have developed and implemented a comprehensive series of trade compliance procedures to assure that we adhere to all CBP requirements. In its most recent review and audit of our import operations and procedures, CBP found no material, unacceptable risks of non-compliance.

6

Product Safety

We are strongly committed to the safety and well being of our customers. We require our products to meet U.S. state and federal and Canadian national laws and regulations. In certain cases, we also voluntarily adopt industry standards and best practices that may be higher than legally required or where no clear laws exist.

To ensure compliance with our product safety standards, we maintain an extensive set of testing protocols for each category of products. All of the products we sell are tested by an independent testing laboratory in accordance with applicable regulatory requirements. In rare cases where a safety issue has been discovered in a product that has reached our store shelves, we respond with a comprehensive recall process for all of our brands. In accordance with Consumer Product Safety Commission requirements, we publicly maintain a list of product recalls conducted on our e-commerce website.

Merchandise Inventory, Replenishment and Distribution

Merchandise is generally shipped directly from our vendors and routed through third-party transloaders at key ports of entry to our three U.S. distribution centers, one in Warrendale, Pennsylvania and the other two in Ottawa, Kansas, or to our Canadian distribution center in Mississauga, Ontario. Additionally, certain product is eligible to be shipped directly to stores, by-passing our distribution centers.

Upon receipt at one of our distribution centers, merchandise is processed and prepared for shipment to the stores or forwarded to a warehouse holding area to be used as store replenishment goods. The allocation of merchandise among stores varies based upon a number of factors, including geographic location, customer demographics and store size. Merchandise is shipped to our stores two to five times per week depending upon the season and store requirements.

The expansion of our Kansas distribution center in Fiscal 2007 enabled us to bring fulfillment services for AEO Direct in-house. The second phase of this expansion was completed in Fiscal 2008 to enhance operating efficiency and support our future growth.

Customer Credit and Returns

We offer a co-branded credit card (the "AEO Visa Card") and a private label credit card (the "AEO Credit Card") under the AE, aerie and 77kids brands. These credit cards are issued by a third-party bank (the "Bank"), and we have no liability to the Bank for bad debt expense, provided that purchases are made in accordance with the Bank's procedures. Once a customer is approved to receive the AEO Visa Card or the AEO Credit Card and the card is activated, the customer is eligible to participate in our credit card rewards program. Customers who make purchases at AE, aerie and 77kids earn discounts in the form of savings certificates when certain purchase levels are reached. Also, AEO Visa Card customers who make purchases at other retailers where the card is accepted earn additional discounts. Savings certificates are valid for 90 days from issuance. AEO Credit Card holders will also receive special promotional offers and advance notice of all American Eagle in-store sales events. The AEO Credit Card is accepted at all of our U.S. stores and at ae.com, aerie.com and 77kids.com. The AEO Visa Card is accepted in all of our stores and AEO Direct sites as well as merchants worldwide that accept Visa ® .

Customers in our U.S. and Canada stores may also pay for their purchases with American Express ® , Discover ® , MasterCard ® , Visa ® , bank debit cards, cash or check. Our AEO Direct customers may pay for their purchases using American Express ® , Discover ® , MasterCard ® and Visa ® . They may also pay for their purchases using PayPal ® and Bill Me Later ® .

Customers may also use gift cards to pay for their purchases. AE, aerie and 77kids gift cards can be purchased in our American Eagle, aerie and 77kids stores, respectively, and can be used both in-store and online. In addition, AE, aerie and 77kids gift cards are available for purchase through ae.com, aerie.com or 77kids.com. When the recipient uses the gift card, the value of the purchase is electronically deducted from the card and any remaining value can be used for future purchases. Our gift cards do not expire and we do not charge a service fee on inactive gift cards.

7

We offer our retail customers a hassle-free return policy. We believe that our competitors offer similar credit card and customer service policies.

Competition

The retail apparel industry, including retail stores and e-commerce, is highly competitive. We compete with various individual and chain specialty stores, as well as the casual apparel and footwear departments of department stores and discount retailers, primarily on the basis of quality, fashion, service, selection and price.

Trademarks and Service Marks

We have registered AMERICAN EAGLE OUTFITTERS ® , AMERICAN EAGLE ® , AE ® and AEO ® with the United States Patent and Trademark Office. We have also registered or have applied to register these trademarks with the registries of the foreign countries in which our stores and/or manufacturers are located and/or where our product is shipped.

We have registered AMERICAN EAGLE OUTFITTERS ® and AMERICAN EAGLE ® with the Canadian Intellectual Property Office. In addition, we are exclusively licensed in Canada to use AE tm and AEO ® in connection with the sale of a wide range of clothing products.

In the United States and around the world, we have also registered, or have applied to register, a number of other marks used in our business, including aerie ® , 77kids by american eagle ® and little77 by american eagle ® .

These trademarks are renewable indefinitely and their registrations are properly maintained in accordance with the laws of the country in which they are registered. We believe that the recognition associated with these trademarks makes them extremely valuable and, therefore, we intend to use and renew our trademarks in accordance with our business plans.

Employees

As of January 28, 2012, we had approximately 39,600 employees in the United States and Canada, of whom approximately 33,100 were part-time and seasonal hourly employees. We consider our relationship with our employees to be good.

Seasonality

Historically, our operations have been seasonal, with a large portion of net sales and operating income occurring in the third and fourth fiscal quarters, reflecting increased demand during the back-to-school and year-end holiday selling seasons, respectively. As a result of this seasonality, any factors negatively affecting us during the third and fourth fiscal quarters of any year, including adverse weather or unfavorable economic conditions, could have a material adverse effect on our financial condition and results of operations for the entire year. Our quarterly results of operations also may fluctuate based upon such factors as the timing of certain holiday seasons, the number and timing of new store openings, the acceptability of seasonal merchandise offerings, the timing and level of markdowns, store closings and remodels, competitive factors, weather and general economic conditions.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports are available, free of charge, under the "About AEO, Inc." section of our website at www.ae.com. These reports are available as soon as reasonably practicable after such material is electronically filed with the Securities and Exchange Commission (the "SEC").

8

Our corporate governance materials, including our corporate governance guidelines, the charters of our audit, compensation, and nominating and corporate governance committees, and our code of ethics may also be found under the "About AEO, Inc." section of our website at www.ae.com. Any amendments or waivers to our code of ethics will also be available on our website. A copy of the corporate governance materials is also available upon written request.

Additionally, our investor presentations are available under the "About AEO, Inc." section of our website at www.ae.com. These presentations are available as soon as reasonably practicable after they are presented at investor conferences.

Certifications

As required by the New York Stock Exchange ("NYSE") Corporate Governance Standards Section 303A.12(a), on July 5, 2011 our Chief Executive Officer submitted to the NYSE a certification that he was not aware of any violation by the Company of NYSE corporate governance listing standards. Additionally, we filed with this Form 10-K, the Principal Executive Officer and Principal Financial Officer certifications required under Sections 302 and 906 of the Sarbanes-Oxley Act of 2002.

ITEM 1A. RISK FACTORS

Our ability to anticipate and respond to changing consumer preferences, fashion trends and a competitive environment in a timely manner

Our future success depends, in part, upon our ability to identify and respond to fashion trends in a timely manner. The specialty retail apparel business fluctuates according to changes in the economy and customer preferences, dictated by fashion and season. These fluctuations especially affect the inventory owned by apparel retailers because merchandise typically must be ordered well in advance of the selling season. While we endeavor to test many merchandise items before ordering large quantities, we are still susceptible to changing fashion trends and fluctuations in customer demands.

In addition, the cyclical nature of the retail business requires that we carry a significant amount of inventory, especially during our peak selling seasons. We enter into agreements for the manufacture and purchase of our private label apparel well in advance of the applicable selling season. As a result, we are vulnerable to changes in consumer demand, pricing shifts and the timing and selection of merchandise purchases. The failure to enter into agreements for the manufacture and purchase of merchandise in a timely manner could, among other things, lead to a shortage of inventory and lower sales. Changes in fashion trends, if unsuccessfully identified, forecasted or responded to by us, could, among other things, lead to lower sales, excess inventories and higher markdowns, which in turn could have a material adverse effect on our results of operations and financial condition.

The effect of economic pressures and other business factors

The success of our operations depends to a significant extent upon a number of factors relating to discretionary consumer spending, including economic conditions affecting disposable consumer income such as employment, consumer debt, interest rates, increases in energy costs and consumer confidence. There can be no assurance that consumer spending will not be further negatively affected by general or local economic conditions, thereby adversely impacting our continued growth and results of operations.

Our ability to react to raw material, labor and energy cost increases

Increases in our costs, such as raw materials, labor and energy, may reduce our overall profitability. Specifically, fluctuations in the price of cotton that is used in the manufacture of merchandise we purchase from our suppliers has negatively impacted our cost of sales. We have strategies in place to help mitigate the rising cost of raw materials and our overall profitability depends on the success of those strategies. Additionally, increases in other costs, including labor and energy, could further reduce our profitability if not mitigated.

9

Our ability to grow through new store openings and existing store remodels and expansions

Our continued growth and success will depend in part on our ability to open and operate new stores and expand and remodel existing stores on a timely and profitable basis. During Fiscal 2012, we plan to open approximately 14 new American Eagle stores in the U.S. and Canada and one 77kids store. Additionally, we plan to remodel and refurbish approximately 100 existing American Eagle stores during Fiscal 2012. Accomplishing our new and existing store expansion goals will depend upon a number of factors, including the ability to obtain suitable sites for new and expanded stores at acceptable costs, the hiring and training of qualified personnel, particularly at the store management level, the integration of new stores into existing operations and the expansion of our buying and inventory capabilities. There can be no assurance that we will be able to achieve our store expansion goals, manage our growth effectively, successfully integrate the planned new stores into our operations or operate our new and remodeled stores profitably.

Our ability to achieve planned store financial performance

The results achieved by our stores may not be indicative of long-term performance or the potential performance of stores in other locations. The failure of stores to achieve acceptable results could result in additional store asset impairment charges, which could adversely affect our continued growth and results of operations.

Our ability to grow through the internal development of new brands

We launched our new brand concepts, aerie and 77kids, during Fiscal 2006 and Fiscal 2008, respectively. Our ability to succeed in these new brands requires significant expenditures and management attention. Additionally, any new brand is subject to certain risks including customer acceptance, competition, product differentiation, the ability to attract and retain qualified personnel, including management and designers, and the ability to obtain suitable sites for new stores at acceptable costs. There can be no assurance that these new brands will grow or become profitable. If we are unable to succeed in developing profitable new brands, this could adversely impact our continued growth and results of operations.

Our international merchandise sourcing strategy

Substantially all of our merchandise is purchased from foreign suppliers. Although we purchase a significant portion of our merchandise through a single foreign buying agent, we do not maintain any exclusive commitments to purchase from any vendor. Since we rely on a small number of foreign sources for a significant portion of our purchases, any event causing the disruption of imports, including the insolvency of a significant supplier or a significant labor dispute, could have an adverse effect on our operations. Other events that could also cause a disruption of imports include the imposition of additional trade law provisions or import restrictions, such as increased duties, tariffs, anti-dumping provisions, increased CBP enforcement actions, or political or economic disruptions.

We have a Vendor Code of Conduct (the "Code") that provides guidelines for all of our vendors regarding working conditions, employment practices and compliance with local laws. A copy of the Code is posted on our website, www.ae.com, and is also included in our vendor manual in English and multiple other languages. We have a factory compliance program to audit for compliance with the Code. However, there can be no assurance that our factory compliance program will be fully effective in discovering all violations. Publicity regarding violation of our Code or other social responsibility standards by any of our vendor factories could adversely affect our sales and financial performance.

We believe that there is a risk of terrorist activity on a global basis, and such activity might take the form of a physical act that impedes the flow of imported goods or the insertion of a harmful or injurious agent to an imported shipment. We have instituted policies and procedures designed to reduce the chance or impact of such actions including, but not limited to, factory audits and self-assessments, including audit protocols on all critical

10

security issues; the review of security procedures of our other international trading partners, including forwarders, consolidators, shippers and brokers; and the cancellation of agreements with entities who fail to meet our security requirements. In addition, the United States CBP has recognized us as a validated, tier three member of the Customs - Trade Partnership Against Terrorism program, a voluntary program in which an importer agrees to work with customs to strengthen overall supply chain security. However, there can be no assurance that terrorist activity can be prevented entirely and we cannot predict the likelihood of any such activities or the extent of their adverse impact on our operations.

Our reliance on external vendors

Given the volatility and risk in the current markets, our reliance on external vendors leaves us subject to certain risks should one or more of these external vendors become insolvent. Although we monitor the financial stability of our key vendors and plan for contingencies, the financial failure of a key vendor could disrupt our operations and have an adverse effect on our cash flows, results of operations and financial condition.

Seasonality

Historically, our operations have been seasonal, with a large portion of net sales and operating income occurring in the third and fourth fiscal quarters, reflecting increased demand during the back-to-school and year-end holiday selling seasons, respectively. As a result of this seasonality, any factors negatively affecting us during the third and fourth fiscal quarters of any year, including adverse weather or unfavorable economic conditions, could have a material adverse effect on our financial condition and results of operations for the entire year. Our quarterly results of operations also may fluctuate based upon such factors as the timing of certain holiday seasons, the number and timing of new store openings, the acceptability of seasonal merchandise offerings, the timing and level of markdowns, store closings and remodels, competitive factors, weather and general economic conditions.

Our reliance on our ability to implement and sustain information technology systems

We regularly evaluate our information technology systems and are currently implementing modifications and/or upgrades to the information technology systems that support our business. Modifications include replacing legacy systems with successor systems, making changes to legacy systems or acquiring new systems with new functionality. We are aware of inherent risks associated with replacing and modifying these systems, including inaccurate system information and system disruptions. We believe we are taking appropriate action to mitigate the risks through testing, training, staging implementation and in-sourcing certain processes, as well as securing appropriate commercial contracts with third-party vendors supplying such replacement and redundancy technologies. Information technology system disruptions and inaccurate system information, if not anticipated and appropriately mitigated, could have a material adverse effect on our results of operations.

Our ability to safeguard against any security breach with respect to our information technology systems

During the course of business, we regularly obtain and transmit confidential customer information through our information technology systems. If our information technology systems are breached, an unauthorized third party may obtain access to confidential customer information. Any compromise or breach of our systems that results in unauthorized access to confidential customer information could cause us to incur significant legal and financial liabilities, damage to our reputation and a loss of customer confidence. These impacts could have a material adverse effect on our business and results of operations.

Our reliance on key personnel

Our success depends to a significant extent upon the continued services of our key personnel, including senior management, as well as our ability to attract and retain qualified key personnel and skilled employees in the future. Our operations could be adversely affected if, for any reason, one or more key executive officers ceased to be active in our management.

11

Failure to comply with regulatory requirements

As a public company, we are subject to numerous regulatory requirements. Our policies, procedures and internal controls are designed to comply with all applicable laws and regulations, including those imposed by the Sarbanes-Oxley Act of 2002, the SEC and the NYSE. Failure to comply with such laws and regulations could have a material adverse effect on our reputation, financial condition and on the market price of our common stock.

Our ability to obtain and/or maintain our credit facilities

We believe that we have sufficient cash flows from operating activities to meet our operating requirements. In addition, the banks participating in our various credit facilities are currently rated as investment grade, and all of the amounts under the credit facilities are currently available to us at the discretion of the respective financial institutions. We draw on our credit facilities to increase our cash position to add financial flexibility. Although we expect to continue to generate positive cash flow despite the current economy, there can be no assurance that we will be able to successfully generate positive cash flow in the future. Continued negative trends in the credit markets and/or continued financial institution failures could lead to lowered credit availability as well as difficulty in obtaining financing. In the event of limitations on our access to credit facilities, our liquidity, continued growth and results of operations could be adversely affected.

Our efforts to expand internationally

We have entered into franchise agreements with multiple franchisees to open and operate stores throughout the Middle East, Northern Africa, Eastern Europe, Hong Kong, China, Israel and Japan over the next several years. While the franchise arrangements do not involve a capital investment from us and require minimal operational involvement, the effect of these arrangements on our business and results of operations is uncertain and will depend upon various factors, including the demand for our products in new markets internationally. Furthermore, although we provide store operation training, literature and support, to the extent that the franchisee does not operate its stores in a manner consistent with our requirements regarding our brand and customer experience standards, the value of our brand could be negatively impacted. A failure to protect the value of our brand or any other adverse actions by a franchisee could have an adverse effect on our results of operations and our reputation.

Other risk factors

Additionally, other factors could adversely affect our financial performance, including factors such as: our ability to successfully acquire and integrate other businesses; any interruption of our key infrastructure systems; any disaster or casualty resulting in the interruption of service from our distribution centers or in a large number of our stores; any interruption of our business related to an outbreak of a pandemic disease in a country where we source or market our merchandise; changes in weather patterns; the effects of changes in current exchange rates and interest rates; and international and domestic acts of terror.

The impact of any of the previously discussed factors, some of which are beyond our control, may cause our actual results to differ materially from expected results in these statements and other forward-looking statements we may make from time-to-time.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not applicable.

ITEM 2. PROPERTIES.

We own two buildings in urban Pittsburgh, Pennsylvania which house our corporate headquarters. These buildings total 186,000 square feet and 150,000 square feet, respectively. We lease one location near our headquarters, which is used primarily for store and corporate support services, totaling approximately 51,000 square feet. This lease expires in 2024.

12

We own a 423,000 square foot building located in a suburban area near Pittsburgh, Pennsylvania, which houses our distribution center and contains approximately 120,000 square feet of office space. We also own a 45,000 square foot building, which houses our data center and additional office space. We lease an additional location of approximately 18,000 square feet, which is used for storage space. This lease expires in 2015.

We rent approximately 131,000 square feet of office space in New York, New York for our designers and sourcing and production teams. The lease for this space expires in May 2016. We also lease an additional 47,300 square feet of office space in New York, New York, with various terms expiring through 2018.

We own a distribution facility in Ottawa, Kansas consisting of approximately 1,220,000 total square feet, including two expansions of 544,000 square feet and 280,000 square feet, respectively. This expanded facility is used to support new and existing growth initiatives, including AEO Direct, aerie and 77kids.

We lease a building in Mississauga, Ontario with approximately 294,000 square feet, which houses our Canadian distribution center. The lease expires in 2017.

We lease our flagship store in the Times Square area of New York, New York. The 25,000 square foot location has an initial term of 15 years with three options to renew for five years each. This flagship store opened in November 2009 and the initial lease term expires in 2024.

All of our stores in the United States and Canada are leased. The store leases generally have initial terms of 10 years. Certain leases also include early termination options, which can be exercised under specific conditions. Most of these leases provide for base rent and require the payment of a percentage of sales as additional contingent rent when sales reach specified levels. Under our store leases, we are typically responsible for tenant occupancy costs, including maintenance and common area charges, real estate taxes and certain other expenses. We have generally been successful in negotiating renewals as leases near expiration.

ITEM 3. LEGAL PROCEEDINGS.

We are a party to various legal actions incidental to our business, including certain actions in which we are the plaintiff. At this time, our management does not expect the results of any of the legal actions to be material to our financial position or results of operations.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

13

PART II

| ITEM 5. | MARKET FOR THE REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Our common stock is traded on the NYSE under the symbol "AEO". As of March 12, 2012, there were 590 stockholders of record. However, when including associates who own shares through our employee stock purchase plan, and others holding shares in broker accounts under street name, we estimate the stockholder base at approximately 45,000. The following table sets forth the range of high and low closing prices of the common stock as reported on the NYSE during the periods indicated.

| Market Price | Cash Dividends

per Common Share | |||||||||||

For the Quarters Ended | High | Low | ||||||||||

January 28, 2012 | $ | 15.72 | $ | 12.89 | $ | 0.11 | ||||||

October 29, 2011 | $ | 13.60 | $ | 10.17 | $ | 0.11 | ||||||

July 30, 2011 | $ | 15.71 | $ | 12.49 | $ | 0.11 | ||||||

April 30, 2011 | $ | 16.18 | $ | 14.46 | $ | 0.11 | ||||||

January 29, 2011 | $ | 17.16 | $ | 14.02 | $ | 0.61 | ||||||

October 30, 2010 | $ | 17.36 | $ | 12.04 | $ | 0.11 | ||||||

July 31, 2010 | $ | 17.13 | $ | 11.60 | $ | 0.11 | ||||||

May 1, 2010 | $ | 19.34 | $ | 15.73 | $ | 0.10 | ||||||

During Fiscal 2011 and Fiscal 2010, we paid quarterly dividends as shown in the table above. Cash dividends per common share for the quarter ended January 29, 2011 consisted of a regular quarterly dividend of $0.11 per common share and a special cash dividend of $0.50 per common share. The payment of future dividends is at the discretion of our Board and is based on future earnings, cash flow, financial condition, capital requirements, changes in U.S. taxation and other relevant factors. It is anticipated that any future dividends paid will be declared on a quarterly basis.

14

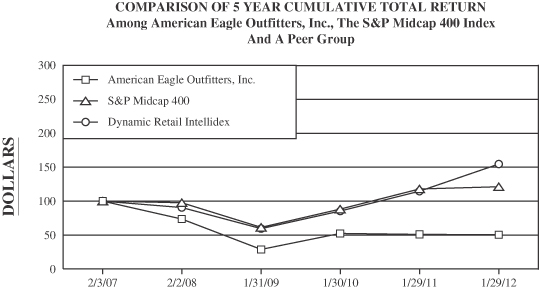

Performance Graph

The following Performance Graph and related information shall not be deemed "soliciting material" or to be filed with the SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Exchange Act of 1934, each as amended, except to the extent that we specifically incorporate it by reference into such filing.

The following graph compares the changes in the cumulative total return to holders of our common stock with that of the S&P Midcap 400 and the Dynamic Retail Intellidex. The comparison of the cumulative total returns for each investment assumes that $100 was invested in our common stock and the respective index on February 3, 2007 and includes reinvestment of all dividends. The plotted points are based on the closing price on the last trading day of the fiscal year indicated.

| 2/3/07 | 2/2/08 | 1/31/09 | 1/30/10 | 1/29/11 | 1/28/12 | |||||||||||||||||||

American Eagle Outfitters, Inc. | 100.00 | 73.96 | 29.19 | 52.89 | 51.49 | 51.13 | ||||||||||||||||||

S&P Midcap 400 | 100.00 | 97.77 | 61.62 | 88.34 | 117.90 | 121.10 | ||||||||||||||||||

Dynamic Retail Intellidex | 100.00 | 90.69 | 59.97 | 85.41 | 114.86 | 154.71 | ||||||||||||||||||

15

The following table provides information regarding our repurchases of common stock during the three months ended January 28, 2012.

Issuer Purchases of Equity Securities

Period | Total Number of Shares Purchased(1) | Average Price Paid Per Share(2) | Total Number

of Shares Purchased as Part of Publicly Announced Programs(1)(3) | Maximum Number

of Shares that May Yet be Purchased Under the Program(3) | ||||||||||||

Month #1 (October 30, 2011 through November 26, 2011) | - | $ | - | - | 13,134,545 | |||||||||||

Month #2 (November 27, 2011 through December 31, 2011) | - | $ | - | - | 13,134,545 | |||||||||||

Month #3 (January 1, 2012 through January 28, 2012) | - | $ | - | - | 13,134,545 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Total | - | $ | - | - | 13,134,545 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | There were no shares repurchased as part of our publicly announced share repurchase program during the three months ended January 28, 2012 and there were no shares repurchased for the payment of taxes in connection with the vesting of share-based payments. |

| (2) | Average price paid per share excludes any broker commissions paid. |

| (3) | In January 2008, our Board authorized the repurchase of 60.0 million shares of our common stock. The authorization of the remaining 13.1 million shares that may yet be purchased has been extended through the end of Fiscal 2012. |

The following table sets forth additional information as of the end of Fiscal 2011, about shares of our common stock that may be issued upon the exercise of options and other rights under our existing equity compensation plans and arrangements, divided between plans approved by our stockholders and plans or arrangements not submitted to our stockholders for approval. The information includes the number of shares covered by and the weighted average exercise price of, outstanding options and other rights and the number of shares remaining available for future grants excluding the shares to be issued upon exercise of outstanding options, warrants and other rights.

Equity Compensation Plan Table

| Column (a) | Column (b) | Column (c) | ||||||||||

| Number of securities to be issued upon exercise of outstanding options, warrants and rights(1) | Weighted-average exercise price of outstanding options, warrants and rights(1) | Number of securities remaining available for issuance under equity compensation plans (excluding securities reflected in column (a))(1) | ||||||||||

Equity compensation plans approved by stockholders | 11,197,595 | $ | 15.31 | 25,251,492 | ||||||||

Equity compensation plans not approved by stockholders | - | - | - | |||||||||

|

|

|

|

|

| |||||||

Total | 11,197,595 | $ | 15.31 | 25,251,492 | ||||||||

| (1) | Equity compensation plans approved by stockholders include the 1994 Stock Option Plan, the 1999 Stock Incentive Plan and the 2005 Stock Award and Incentive Plan, as amended (the "2005 Plan"). |

16

ITEM 6. SELECTED CONSOLIDATED FINANCIAL DATA.

The following Selected Consolidated Financial Data should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations," included under Item 7 below and the Consolidated Financial Statements and Notes thereto, included in Item 8 below. Most of the selected data presented below is derived from our Consolidated Financial Statements, if applicable, which are filed in response to Item 8 below. The selected Consolidated Statement of Operations data for the years ended January 31, 2009 and February 2, 2008 and the selected Consolidated Balance Sheet data as of January 30, 2010, January 31, 2009 and February 2, 2008 are derived from audited Consolidated Financial Statements not included herein.

| For the Years Ended(1) | ||||||||||||||||||||

| January 28, 2012 | January 29, 2011 | January 30, 2010 | January 31, 2009 | February 2, 2008 | ||||||||||||||||

| (In thousands, except per share amounts, ratios and other financial information) | ||||||||||||||||||||

Summary of Operations (2) | ||||||||||||||||||||

Net sales | $ | 3,159,818 | $ | 2,967,559 | $ | 2,940,269 | $ | 2,948,679 | $ | 3,041,158 | ||||||||||

Comparable store sales increase (decrease)(3) | 3 | % | (1 | )% | (4 | )% | (10 | )% | 1 | % | ||||||||||

Gross profit | $ | 1,128,341 | $ | 1,170,959 | $ | 1,173,430 | $ | 1,197,186 | $ | 1,438,236 | ||||||||||

Gross profit as a percentage of net sales | 35.7 | % | 39.5 | % | 39.9 | % | 40.6 | % | 47.3 | % | ||||||||||

Operating income | $ | 231,136 | $ | 317,261 | $ | 310,392 | $ | 382,797 | $ | 652,201 | ||||||||||

Operating income as a percentage of net sales | 7.3 | % | 10.7 | % | 10.6 | % | 13.0 | % | 21.4 | % | ||||||||||

Income from continuing operations | $ | 151,705 | $ | 181,934 | $ | 213,398 | $ | 229,984 | $ | 433,507 | ||||||||||

Income from continuing operations as a percentage of net sales | 4.8 | % | 6.1 | % | 7.3 | % | 7.8 | % | 14.3 | % | ||||||||||

Per Share Results | ||||||||||||||||||||

Income from continuing operations per common share-basic | $ | 0.78 | $ | 0.91 | $ | 1.04 | $ | 1.12 | $ | 2.01 | ||||||||||

Income from continuing operations per common share-diluted | $ | 0.77 | $ | 0.90 | $ | 1.02 | $ | 1.11 | $ | 1.97 | ||||||||||

Weighted average common shares outstanding - basic | 194,445 | 199,979 | 206,171 | 205,169 | 216,119 | |||||||||||||||

Weighted average common shares outstanding - diluted | 196,314 | 201,818 | 209,512 | 207,582 | 220,280 | |||||||||||||||

Cash dividends per common share | $ | 0.44 | $ | 0.93 | $ | 0.40 | $ | 0.40 | $ | 0.38 | ||||||||||

Balance Sheet Information | ||||||||||||||||||||

Total cash and short-term investments | $ | 745,044 | $ | 734,695 | $ | 698,635 | $ | 483,853 | $ | 619,939 | ||||||||||

Long-term investments | $ | 847 | $ | 5,915 | $ | 197,773 | $ | 251,007 | $ | 165,810 | ||||||||||

Total assets | $ | 1,950,802 | $ | 1,879,998 | $ | 2,138,148 | $ | 1,963,676 | $ | 1,867,680 | ||||||||||

Short-term debt | $ | - | $ | - | $ | 30,000 | $ | 75,000 | $ | - | ||||||||||

Long-term debt | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||

Stockholders' equity | $ | 1,416,851 | $ | 1,351,071 | $ | 1,578,517 | $ | 1,409,031 | $ | 1,340,464 | ||||||||||

Working capital | $ | 882,087 | $ | 786,573 | $ | 758,075 | $ | 523,596 | $ | 644,656 | ||||||||||

Current ratio | 3.18 | 3.03 | 2.85 | 2.30 | 2.71 | |||||||||||||||

Average return on stockholders' equity | 11.0 | % | 9.6 | % | 11.3 | % | 13.0 | % | 29.0 | % | ||||||||||

17

| For the Years Ended(1) | ||||||||||||||||||||

| January 28, 2012 | January 29, 2011 | January 30, 2010 | January 31, 2009 | February 2, 2008 | ||||||||||||||||

| (In thousands, except per share amounts, ratios and other financial information) | ||||||||||||||||||||

Other Financial Information (2) | ||||||||||||||||||||

Total stores at year-end | 1,090 | 1,086 | 1,075 | 1,070 | 968 | |||||||||||||||

Capital expenditures | $ | 100,135 | $ | 84,259 | $ | 127,080 | $ | 243,564 | $ | 249,640 | ||||||||||

Net sales per average selling square foot(4) | $ | 545 | $ | 524 | $ | 526 | $ | 563 | $ | 644 | ||||||||||

Total selling square feet at end of period | 5,115,770 | 5,067,489 | 4,981,595 | 4,920,285 | 4,492,198 | |||||||||||||||

Net sales per average gross square foot(4) | $ | 436 | $ | 420 | $ | 422 | $ | 452 | $ | 522 | ||||||||||

Total gross square feet at end of period | 6,398,034 | 6,339,469 | 6,215,355 | 6,139,663 | 5,581,769 | |||||||||||||||

Number of employees at end of period | 39,600 | 39,900 | 38,800 | 36,900 | 38,400 | |||||||||||||||

| (1) | All fiscal years presented include 52 weeks. |

| (2) | All amounts presented are from continuing operations and exclude MARTIN+OSA's results of operations for all periods. Refer to Note 15 to the accompanying Consolidated Financial Statements for additional information regarding the discontinued operations of MARTIN+OSA. |

| (3) | The comparable store sales increase for the period ended February 2, 2008 is compared to the corresponding 52 week period in Fiscal 2006. |

| (4) | Net sales per average square foot is calculated using retail store sales for the year divided by the straight average of the beginning and ending square footage for the year. |

| ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

The following discussion and analysis of financial condition and results of operations are based upon our Consolidated Financial Statements and should be read in conjunction with those statements and notes thereto.

This report contains various "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which represent our expectations or beliefs concerning future events, including the following:

| • | the planned opening of approximately 14 new American Eagle stores and one new 77kids store during Fiscal 2012; |

| • | the selection of approximately 100 American Eagle stores in the United States and Canada for remodeling and refurbishing during Fiscal 2012; |

| • | the potential closure of approximately 20 to 30 American Eagle stores in the United States and Canada during Fiscal 2012; |

| • | the planned opening of approximately 31 new franchised American Eagle stores during Fiscal 2012; |

| • | the success of aerie by American Eagle and aerie.com; |

| • | the success of 77kids by american eagle and 77kids.com; |

| • | the expected payment of a dividend in future periods; |

| • | the possibility of engaging in future franchise agreements, growth through acquisitions, and/or internally developing additional new brands; |

| • | the possibility that our credit facilities may not be available for future borrowings; |

| • | the possibility that rising prices of raw materials, labor, energy and other inputs to our manufacturing process, if unmitigated, will continue to have a significant impact to our profitability; and |

18

| • | the possibility that we may be required to take additional store impairment charges related to underperforming stores. |

We caution that these forward-looking statements, and those described elsewhere in this report, involve material risks and uncertainties and are subject to change based on factors beyond our control, as discussed within Part I, Item 1A of this Form 10-K. Accordingly, our future performance and financial results may differ materially from those expressed or implied in any such forward-looking statement.

Critical Accounting Policies

Our Consolidated Financial Statements are prepared in accordance with accounting principles generally accepted in the United States ("GAAP"), which require us to make estimates and assumptions that may affect the reported financial condition and results of operations should actual results differ from these estimates. We base our estimates and assumptions on the best available information and believe them to be reasonable for the circumstances. We believe that of our significant accounting policies, the following involve a higher degree of judgment and complexity. Refer to Note 2 to the Consolidated Financial Statements for a complete discussion of our significant accounting policies. Management has reviewed these critical accounting policies and estimates with the Audit Committee of our Board.

Revenue Recognition. We record revenue for store sales upon the purchase of merchandise by customers. Our e-commerce operation records revenue upon the estimated customer receipt date of the merchandise. Revenue is not recorded on the purchase of gift cards. A current liability is recorded upon purchase, and revenue is recognized when the gift card is redeemed for merchandise.

Revenue is recorded net of estimated and actual sales returns and deductions for coupon redemptions and other promotions. The estimated sales return reserve is based on projected merchandise returns determined through the use of historical average return percentages. We do not believe there is a reasonable likelihood that there will be a material change in the future estimates or assumptions we use to calculate our sales return reserve. However, if the actual rate of sales returns increases significantly, our operating results could be adversely affected.

We estimate gift card breakage and recognize revenue in proportion to actual gift card redemptions as a component of net sales. We determine an estimated gift card breakage rate by continuously evaluating historical redemption data and the time when there is a remote likelihood that a gift card will be redeemed.

We recognize royalty revenue generated from our franchise agreements based upon a percentage of merchandise sales by the franchisee. This revenue is recorded as a component of net sales when earned.

Merchandise Inventory. Merchandise inventory is valued at the lower of average cost or market, utilizing the retail method. Average cost includes merchandise design and sourcing costs and related expenses. The Company records merchandise receipts at the time merchandise is delivered to the foreign shipping port by the manufacturer (FOB port). This is the point at which title and risk of loss transfer to us.

We review our inventory in order to identify slow-moving merchandise and generally use markdowns to clear merchandise. Additionally, we estimate a markdown reserve for future planned markdowns related to current inventory. If inventory exceeds customer demand for reasons of style, seasonal adaptation, changes in customer preference, lack of consumer acceptance of fashion items, competition, or if it is determined that the inventory in stock will not sell at its currently ticketed price, additional markdowns may be necessary. These markdowns may have a material adverse impact on earnings, depending on the extent and amount of inventory affected.

We estimate an inventory shrinkage reserve for anticipated losses for the period between the last physical count and the balance sheet date. The estimate for the shrinkage reserve is calculated based on historical

19

percentages and can be affected by changes in merchandise mix and changes in actual shrinkage trends. We do not believe there is a reasonable likelihood that there will be a material change in the future estimates or assumptions we use to calculate our inventory shrinkage reserve. However, if actual physical inventory losses differ significantly from our estimate, our operating results could be adversely affected.

Asset Impairment. In accordance with Financial Accounting Standards Board ("FASB") Accounting Standard Codification ("ASC") 360, Property, Plant, and Equipment , we evaluate long-lived assets for impairment at the individual store level, which is the lowest level at which individual cash flows can be identified. Impairment losses are recorded on long-lived assets used in operations when events and circumstances indicate that the assets might be impaired and the undiscounted cash flows estimated to be generated by those assets are less than the carrying amounts of the assets. When events such as these occur, the impaired assets are adjusted to their estimated fair value and an impairment loss is recorded separately as a component of operating income under loss on impairment of assets.

Our impairment loss calculations require management to make assumptions and to apply judgment to estimate future cash flows and asset fair values, including forecasting useful lives of the assets and selecting the discount rate that reflects the risk inherent in future cash flows. We do not believe there is a reasonable likelihood that there will be a material change in the estimates or assumptions we use to calculate long-lived asset impairment losses. However, if actual results are not consistent with our estimates and assumptions, our operating results could be adversely affected.

Investment Securities. In accordance with ASC 820, Fair Value Measurements and Disclosures ("ASC 820"), we measure our investment securities using Level 1, Level 2 and Level 3 inputs. Level 1 and Level 2 inputs are valued using quoted market prices while we use a discounted cash flow ("DCF") model to determine the fair value of our Level 3 investments. The assumptions in our DCF model include different recovery periods depending on the type of security and varying discount factors for yield and illiquidity. These assumptions are subjective and they are based on our current judgment and our view of current market conditions. The use of different assumptions would result in a different valuation and related charge. Future adverse changes in market conditions, continued poor operating results of underlying investments or other factors could result in further losses that may not be reflected in an investment's current carrying value, possibly requiring an additional net impairment loss recognized in earnings in the future.

We evaluate our investments for impairment in accordance with ASC 320, Investments – Debt and Equity Securities ("ASC 320"). ASC 320 provides guidance for determining when an investment is considered impaired, whether impairment is other-than-temporary, and measurement of an impairment loss. An investment is considered impaired if the fair value of the investment is less than its cost. If, after consideration of all available evidence to evaluate the realizable value of its investment, impairment is determined to be other-than-temporary, then an impairment loss is recognized in the Consolidated Statement of Operations equal to the difference between the investment's cost and its fair value. Additionally, ASC 320 requires additional disclosures relating to debt and equity securities both in the interim and annual periods as well as requires us to present total other-than-temporary impairment ("OTTI") with an offsetting reduction for any non-credit loss impairment amount recognized in other comprehensive income ("OCI").

Share-Based Payments. We account for share-based payments in accordance with the provisions of ASC 718, Compensation - Stock Compensation ("ASC 718"). To determine the fair value of our stock option awards, we use the Black-Scholes option pricing model, which requires management to apply judgment and make assumptions to determine the fair value of our awards. These assumptions include estimating the length of time employees will retain their vested stock options before exercising them (the "expected term") and the estimated volatility of the price of our common stock over the expected term.

We calculate a weighted-average expected term based on historical experience. Expected stock price volatility is based on a combination of historical volatility of our common stock and implied volatility. We chose

20

to use a combination of historical and implied volatility as we believe that this combination is more representative of future stock price trends than historical volatility alone. Changes in these assumptions can materially affect the estimate of the fair value of our share-based payments and the related amount recognized in our Consolidated Financial Statements.

Income Taxes. We calculate income taxes in accordance with ASC 740, Income Taxes ("ASC 740"), which requires the use of the asset and liability method. Under this method, deferred tax assets and liabilities are recognized based on the difference between the Consolidated Financial Statement carrying amounts of existing assets and liabilities and their respective tax bases as computed pursuant to ASC 740. Deferred tax assets and liabilities are measured using the tax rates, based on certain judgments regarding enacted tax laws and published guidance, in effect in the years when those temporary differences are expected to reverse. A valuation allowance is established against the deferred tax assets when it is more likely than not that some portion or all of the deferred taxes may not be realized. Changes in our level and composition of earnings, tax laws or the deferred tax valuation allowance, as well as the results of tax audits, may materially impact the effective income tax rate.

We evaluate our income tax positions in accordance with ASC 740 which prescribes a comprehensive model for recognizing, measuring, presenting and disclosing in the financial statements tax positions taken or expected to be taken on a tax return, including a decision whether to file or not to file in a particular jurisdiction. Under ASC 740, a tax benefit from an uncertain position may be recognized only if it is "more likely than not" that the position is sustainable based on its technical merits.

The calculation of the deferred tax assets and liabilities, as well as the decision to recognize a tax benefit from an uncertain position and to establish a valuation allowance require management to make estimates and assumptions. We believe that our assumptions and estimates are reasonable, although actual results may have a positive or negative material impact on the balances of deferred tax assets and liabilities, valuation allowances or net income.

Key Performance Indicators

Our management evaluates the following items, which are considered key performance indicators, in assessing our performance:

Comparable store sales - Comparable store sales provide a measure of sales growth for stores open at least one year over the comparable prior year period. In fiscal years following those with 53 weeks, including Fiscal 2007, the prior year period is shifted by one week to compare similar calendar weeks. A store is included in comparable store sales in the thirteenth month of operation. However, stores that have a gross square footage increase of 25% or greater due to a remodel are removed from the comparable store sales base, but are included in total sales. These stores are returned to the comparable store sales base in the thirteenth month following the remodel. Sales from American Eagle, aerie and 77kids stores are included in comparable store sales. Sales from AEO Direct and franchise stores are not included in comparable store sales.

Our management considers comparable store sales to be an important indicator of our current performance. Comparable store sales results are important to achieve leveraging of our costs, including store payroll, store supplies, rent, etc. Comparable store sales also have a direct impact on our total net sales, cash and working capital.

Gross profit - Gross profit measures whether we are optimizing the price and inventory levels of our merchandise and achieving an optimal level of sales. Gross profit is the difference between net sales and cost of sales. Cost of sales consists of: merchandise costs, including design, sourcing, importing and inbound freight costs, as well as markdowns, shrinkage, certain promotional costs and buying, occupancy and warehousing costs. Buying, occupancy and warehousing costs consist of: compensation, employee benefit expenses and travel for our buyers and certain senior merchandising executives; rent and utilities related to our stores, corporate headquarters, distribution centers and other office space; freight from our

21

distribution centers to the stores; compensation and supplies for our distribution centers, including purchasing, receiving and inspection costs; and shipping and handling costs related to our e-commerce operation. Merchandise profit is the difference between net sales and merchandise costs. The inability to obtain acceptable levels of sales, initial markups or any significant increase in our use of markdowns could have an adverse effect on our gross profit and results of operations.

Operating income - Our management views operating income as a key indicator of our success. The key drivers of operating income are comparable store sales, gross profit, our ability to control selling, general and administrative expenses and our level of capital expenditures.